te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

36

Transcript of te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

(01)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

yturzx Jtdto- %y^

vt{btwFtWvtvt{btwFtztgthufxmto

ateV yufLefgtwxeJtytuVemth / btultushmtjttnfth

mxuagtwxhe ytuzexmto

fltfhkx ytuzexh

yr"tf];t :tgtujt Ntuh CtkztuGCthvttE :tgtujt Ntuh CtkztuGmtCgt mtkFgtt

`e htbt rlthkslt ydt{Jttjt (btFFtltjttjtB)

mteyu `e btlteMt Ssq

`e yrltjt ydt{Jttjt

`e rct{sbttunlt ydt{Jttjt

(ztp.) `e cte. yumt. ydt{Jttjt

mteyu `e mte. vte. shegtt

`e r'ltuNt FtkzujtJttjt

`e dtturJtk'B mthtJtdte

`e fijttmtatk' Ftubtft

`e htsuNt ctehjtt

`e htbt yJt;tth Ssq

`e rJt#ltt:t FtkzujtJttjt

`e nhulY 'umttE

`e nubtk;t Nttn

mttuvttheJttjtt yulz ftkw

attxoz yuftWlxlxTmt

vtultjt ltk. 298

mteyu ltefe ze. mttuvttheJttjtt

vttxolthM. 140537

Nttn fijttNt yulz yumttumteyuxTmt

attxoz yuftWlxlxmtT

~t. 5,00,00,000/-

~t. 2,21,02,500/-

8363

&&&

&

&& &

&

&&&

(1)(2)(3)

(4)

(5)

(6)

(7)

(8)(9)

(10)

(F.Y. 2019-2020)

yt:te ;tbttbt mtCttmt'tultu lttuxemt ytvtJttbttk ytJtu Au fu "te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;tlte

cttJtemtbte JttrMtof mtt"tthKt mtCtt ;tt. 19-12-2020 ltu NtrltJtthu mttksu 4-30 fjttfu mtexe jttEx rm:t;t, btnthtS

ydt{mtult CtJtltlttk attu:tt bttGu, %%Jt]k'tJtlt ntujt^^ mtwh;t Ftt;tu lteatu sKttJtujtt ftbttu bttxu btGNtu, subttk ytvt`eltu ntsh hnuJtt

rJtltk;te Au.

1. ;tt. 20-07-2019 ltt htus btGujte yufJtemtbte JttrMtof mtt"tthKt mtCttlte bteltexTmt Jttkatltbttk jtE btkswh fhJtt cttct;t.

2. ;tt. 31-03-2020 ltt htus vtwht :t;tt JtMtoltt ynuJttjt ;t:tt ltVtlte VtGJtKteltu rJtatthKttbttk jtE btkswh fhJtt cttct;t.

3. ;tt. 31-03-2020 ltt htus vtwht :t;tt JtMtoltwk ltVt - ltwfNttlt Ftt;tw yltu ;tt. 31-03-2020 ltt htusltt mthJtigttltu yltu

yturzxhltt ynuJttjtltu btkswh fhJtt cttct;t.

4. heLJto ctukf ytuV Erlzgttltt ;tt. 17-04-2020 lttk mthfgtwjth:te ctukftultu JtMto 2019-2020 lttk ltVtbttk:te rzJtezlz

atwfJtJtt vth rltgtk*tKt btwfujt Au. ;tubt A;ttk heLJto ctukf vthJttltdte ytvtNtu ;ttu zeJtezlzlte hfbt ~t. 32,87,000-00

atwfJtJtt vtt*t :tNtu. sultwk vt{turJtLlt fhujt Au.

5. vtuxt ftgt't rltgtbt ltk. 36(2) nuXG 2020-2021 ltt JtMtobttk Jt"twbttk Jt"tw su n' mtw"te cttuzo ytuV rzhufxmto CtkztuG yuf*t

fhe Ntfu ;tu btwfhh fhJtt cttct;t.

6. mtltu 2020-21 ltt JtMtoltt ftultfhkx yturzxhlte rltbtKtqkf fhJtt yltu ;tultwk btnult;ttKtwk lt²e fhJtt cttct;t.

7. vt{btwFt`elte yltwbtr;t:te hsq :ttgt ;tu ftbt ykdtu rJtatthKtt fhJtt ;t:tt rltKtogt fhJtt cttct;t.

JttrMtof mtt"tthKt mtCttlte ltturxmt

cttuzo ytuV rzhufxmtoltt yt'uNt:tenhulY 'umttE

btwFgt JtneJtxe yr"tfthe

m:tG & mtwh;t

;ttheFt & 27/11/2020

(02)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

& lttuk"t &1. su mtCttmt'ltu JttrMtof rnmttcttu ;tubt s ynuJttjt mtkctk"te bttrn;te SuE;te ntugt, ;tubtltu JttrMtof mtt"tthKt mtCttltt mtt;t

r'Jtmt vtnujtt jturFt;t bttkdtKte fhJtt:te ytvtJttbttk ytJtNtu.2. ftuhbtltt yCttJtu btexekdt btwjt;tJte hnuNtu, ;ttu ;tu s r'Jtmtu, ;tu s m:tGu yz"tt fjttf ctt' Vhe:te btGNtu su ftgt'umth

dtKttNtu.3. mtCttbttk Vf;t mtCttmt' ;t:tt ytbtkr*t;t Jgtrf;t s ntsh hne NtfNtu.4. mtCttmt'tuyu 'tFtjt :t;te JtuGtyu rbtrltxTmt ctwfbttk mtne fhJttlte hnuNtu.5. 'huf mtCttmt'tuyu Email ID ;t:tt ftulxufx ltkcth ;t:tt KYC fbvtjtex fhtJte jtuJtt.6. 'huf mtCttmt'tuyu VhBgtt;t bttmf vtnuheltu ytJtJttltwk hnuNtu ;t:tt mtturNtgtjt rzmxulmtltwk vttjtlt fhJttltwk hnuNtu.

ftgtomtqrat

(03)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

Annexure EAUDITOR'S REPORT

To,The Members,The Financial Co. Op. Bank Ltd. Surat.

We have been appointed as Statutory Auditors of the bank by Registrar of Co. Op. Society vide letter no. Ashan/2460/J-4/871/2019 dated 17/06/2019. We have carried out the statutory audit for the bank on the basis of information provided to us from time to time. We have verified Balance Sheet, Profit and Loss Account and books of accounts and we report as under:

1. The administrative committee of the bank has conducted the working of the bank as per bye-laws and also the provisions of Co-operative Laws/Rules. The Board of Directors has followed the Rules and Regulations.

2. The administrative committee of the bank has carried out the working of the bank in accordance with circulars / resolutions / instructions of RBI given from time to time.

3. The books of accounts and accounting system are maintained as required under provisions of Co-operative Laws and also instruction of RBI.

4. Bank Balance Sheet and profit and loss reflects true and fair view of the bank's financial position as on 31.03.2020 and profit for the year ended on the above date subject to our auditor's report bhag-2 and also our following qualifications:

a) During the year the bank has not provided income-tax provisions as per the ICAI AS no. 22 and inflating profit for the current year by Rs. 99,18,890/- and Reserve & Surplus fund is inflated to that extent.

b) The bank shown interest income gratuity from LIC of Rs. 8,93,439/- in current year under other income head of Profit and loss account which is income of staff gratuity fund with LIC for the current financial year, henceforth Net Profit is inflated by Rs. 8,93,439/- and reserve and surplus fund is inflated to that extent.

c) Bank has not recognised the Deferred Tax Asset / Liability arising due to timing difference between accounting income and Tax Income resulting in to Non compliances Accounting Standard - 22 “Accounting for Taxes on Income” issued by the Institute of Chartered Accountants of India.

Independent Auditor's Report

(04)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

Due to above qualification it is not possible to ascertain the impact of the same of net profit of the bank.

5. Bank has properly maintained SLR and CRR standards.

6. The Bank has made proper classification of NPAs and provisions for the same as per RBI Guidelines.

7. Bank has granted loan to the members of Board of directors and their relatives. The balance outstanding as on 31.03.2020 is of Rs. 20.50 lacs and there is no overdue amount.

8. As per Information given to us, Directors or Office Executives are not disqualified for

their position under the bye-laws of the Bank or the provisions of Co-operative Laws/Rules.

9. As per Information given to us, Cases of One-Time Settlement of Advances and Set-off of Deposits are not observed during the audit period.

10. As per information & explanation provided to us, the bank has not written off any due and there is no compromise in respect of outstanding due and hence the guidelines issued by R.B.I and Co-op Act are not applicable.

11. There is no any settlement and compromise through court during the year.

Place: Surat Date: 23/06/2020

SOPARIWALA & CO Chartered Accountants

Partner CA Nicky D. Sopariwala

M No 140537FRN No. 132643W

Penal No. 298ICAI UDIN: 20140537AAAACR4919

(05)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

I. OVERVIEW:

a. Basis of Preparation

The accompanying financial statements have been prepared under the historical basis and confirm,

in all material aspects, to Generally Accepted Accounting Principles (GAAP) in India, which

comprise the statutory provisions, guidelines of regulatory authorities - Reserve Bank of India (RBI),

accounting standards/ guidance notes issued by the Institute of Chartered Accountants of India

(ICAI), and the practices prevalent in the banking industry in India.

b. Use of Estimate

The preparation of the financial statements, in conformity with generally accepted accounting

principles, requires management to make estimates and assumptions that affect the reported amounts

of assets and liabilities, revenues and expenses and disclosure of contingent liabilities at the financial

statements. Management believes that the estimates used in the preparation of the financial

statements are prudent and reasonable. Any revisions to the accounting estimates are recognized

prospectively.

II. SIGNIFICANT ACCOUNTING POLICIES:

a. Accounting Convention

The financial statements are drawn up keeping in mind the historical cost and going concern concept

and in accordance with generally accepted accounting principles and practices prevailing in the co-

operative banks in India except otherwise stated.

b. Revenue Recognition

Income & expenditure are accounted on accrual basis, except otherwise stated below.

· Interest income is recognized as it accrues except in the case of non- performing assets, where it is

recognized on realization basis, as per Income Reorganization norms of RBI.

· Recovery in NPAs is first appropriated towards expenses and interest and the balance if any towards

principal.

· When the borrower accounts becomes regular and remains Standard in six Months Period, the

account is upgraded and reclassified as standard account.

· Legal Expenses in case of Suit Filed Accounts is charged to profit and loss account and separate

control account is being maintained. Such amount when recovered is treated as income.

· Dividend on investments is accounted in the year of receipt.

· Interest provision on matured FD is made at Saving Bank interest rate i.e. 3.50% as per the

instructions from RBI.

· Commission exchange is recognized as income on receipt basis.

F.Y. 31-03-2020NOTES FORMING PART OF THE

PROFIT AND LOSS AND BALANCESHEET FOR THE YEAR ENDED ON 31-03-2020 AS ON EVEN DATE

(06)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

c. Investment

The entire investment portfolio of the bank is classified in accordance with the RBI guidelines, into

following three categories:

· Held till maturity comprising of investments acquired with the intention to hold them till maturity.

· Held for trading comprising of investment acquired with the intention to trade.

· Available for sale comprising of investment which are not classified as above.

· Investments have been further classified under five groups as required under RBI guild lines-

Central/State Government securities, other approved securities, shares in co-op. institution, other

investment with Financial Institution and other Investment with PSUs for the purpose of discourse in

the Balance Sheet.

· Mutual funds instruments are valued at market rate or repurchase price or net asset value in that

order depending in their availability.

· Valuation of investment: long term investment classified as “Held for Maturity” are stated at

acquisition cost, unless it is more than face value, in which case the premium is amortized over the

period remaining to maturity

d. Advances

· Advances are stated net of recovery in suit filed.

· Advances are classified into standard, sub-standard, doubtful and loss assets inaccordance with the

IRAC guidelines issued by the Reserve Bank of India.

· Provision for standard, sub-standard, doubtful and loss assets are made in accordance with the IRAC

guidelines issued by the Reserve Bank of India.

e. Fixed Assets & Deprecation

· All the tangible fixed assets have been stated at cost comprises the purchase price and attributable

cost of bringing the assets to its working condition for its intended.

· The carrying amounts are reviewed at each Balance-sheet date to access whether they are record in

excess of their recoverable amounts and where carrying values exceed this estimated recoverable

amount, assets are written down to their recoverable amount.

· Fixed assets held for disposal have been stated at the lower of cost or net realizable value and shown

separately in the financial statements. Any expected loss is recognized immediately in the profit and

loss statement.

· Depreciation on fixed assets purchased during the year is charged full year, if the asset is purchased

and retained for 180 days or more, otherwise it is charged at 50% of normal rate. No depreciation is

provided on the fixed assets sold and/or discarded during the year. All fixed assets are shown at Net

block.

(07)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

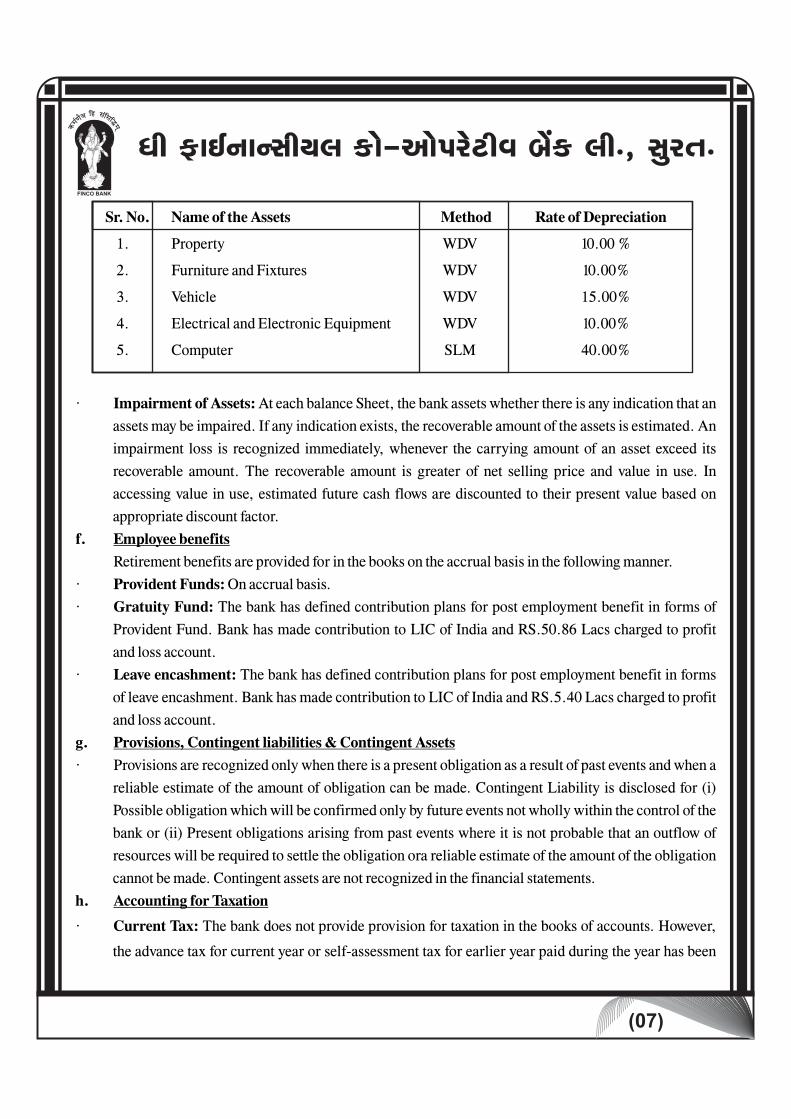

Sr. No. Name of the Assets Method Rate of Depreciation

1. Property WDV 10.00 %

2. Furniture and Fixtures WDV 10.00%

3. Vehicle WDV 15.00%

4. Electrical and Electronic Equipment WDV 10.00%

5. Computer SLM 40.00%

· Impairment of Assets: At each balance Sheet, the bank assets whether there is any indication that an

assets may be impaired. If any indication exists, the recoverable amount of the assets is estimated. An

impairment loss is recognized immediately, whenever the carrying amount of an asset exceed its

recoverable amount. The recoverable amount is greater of net selling price and value in use. In

accessing value in use, estimated future cash flows are discounted to their present value based on

appropriate discount factor.

f. Employee benefits

Retirement benefits are provided for in the books on the accrual basis in the following manner.

· Provident Funds: On accrual basis.

· Gratuity Fund: The bank has defined contribution plans for post employment benefit in forms of

Provident Fund. Bank has made contribution to LIC of India and RS.50.86 Lacs charged to profit

and loss account.

· Leave encashment: The bank has defined contribution plans for post employment benefit in forms

of leave encashment. Bank has made contribution to LIC of India and RS.5.40 Lacs charged to profit

and loss account.

g. Provisions, Contingent liabilities & Contingent Assets

· Provisions are recognized only when there is a present obligation as a result of past events and when a

reliable estimate of the amount of obligation can be made. Contingent Liability is disclosed for (i)

Possible obligation which will be confirmed only by future events not wholly within the control of the

bank or (ii) Present obligations arising from past events where it is not probable that an outflow of

resources will be required to settle the obligation ora reliable estimate of the amount of the obligation

cannot be made. Contingent assets are not recognized in the financial statements.

h. Accounting for Taxation

· Current Tax: The bank does not provide provision for taxation in the books of accounts. However,

the advance tax for current year or self-assessment tax for earlier year paid during the year has been

(08)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

shown as appropriation of profit. This practice followed by bank is not in accordance with AS 22.

· Deferred Tax: Deferred tax asset/ liability arising due to timing difference between the accounting

income and tax income that originate in one period and are capable of reversed in one or more

subsequent periods is not recognized which is contrary to AS 22.

i. Reserve Fund and Other Reserves

As per the requirements of the Gujarat State Cooperative Act&relevant provisions of bye laws of the

bank, the net profit have been appropriated in Annual General Body meeting of the Bank to statutory

reserve and other reserve.

j. Segment Information

The entire operation of the bank is one composite banking business not liable to different risks and

rewards. Consequently in the opinion of the bank, Accounting Standard 17 on “Segment Reporting”

issued by the Institute of Chartered Accountants of India is not applicable to the bank.

k. Bank has not complied with following Accounting Standard issued by Institute of Chartered

Accountants of India.

Accounting Standard 3 “Cash Flow Statement”

Accounting Standard 10 “Accounting for Fixed Assets”

Accounting Standard 18 “Related Party Disclouser”

III NOTES TO ACCOUNTS :

(1) Depreciation:

Depreciation charges in Profit and Loss statement is Rs.11.22 Lacs.

(2) Accounting for Taxes on Income:

The bank does not adopt accounting policy (AS-22) in respect of provision for taxation and also not

creating DTA/DTL.

(3) Advances:

· Balances under the head “Advances”, “Deposits” and other accounts (Liability) are subjects to

reconciliation and confirmation of customers.

· Classification of advances covered by book debts is reported under the head “Advances Secured

by tangible assets” as per RBI guidelines.

· Bank has achieved priority sector advances of 70.60% against the target of 40% while in case of

advances to weaker section it is 37.64% of total advance of Priority Sector Advances.

· Required provision for standard assets has been made by the bank as per RBI guidelines.

(5) Contingent Liability

· Contingent Liability is NIL

(6) Income Tax:

A. Advances Tax of Rs. 95,00,000/- paid during the year.

B. TDS of Rs. 17,40,087/- paid for the current year.st

(7) Inter branch accounts and inter banks account are reconciled up to 31 March 2020 and no

provision is required to be made in respect of items outstanding therein.

(8) Fixed Deposits of Rs. 11,02,24,079 includes Rs. 1,00,00,000 under lien with other banks for

various banking arrangements.

(9) In the opinion of the board the current assets, loans and advances are approximately of the value

stated if realized in the ordinary course of business. The provisions for all known liabilities are

adequate.

(10) The bank does not pay any remuneration to any of its directors in terms of Reserve bank of

India's circular dated 29.03.2013.

(11) Previous figures are regrouped and rearranged wherever consider necessary.

(09)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

SOPARIWALA & CO

Chartered Accountants

Partner

CA Nicky D. Sopariwala

M No 140537

FRN No. 132643W

Penal No. 298

ICAI UDIN: 20140537AAAACR4919

Place: Surat .

Date: 23/06/2020

(10)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

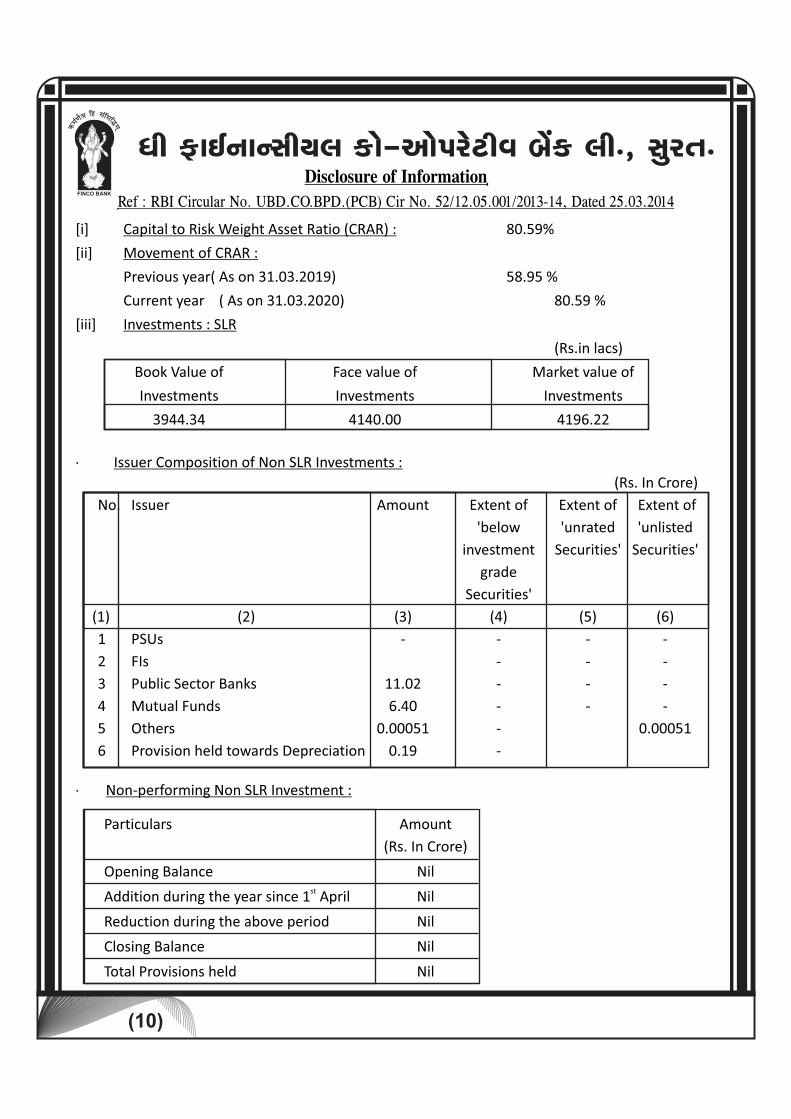

[i] Capital to Risk Weight Asset Ratio (CRAR) : 80.59%

[ii] Movement of CRAR :

Previous year( As on 31.03.2019) 58.95 %

Current year ( As on 31.03.2020) 80.59 %

[iii] Investments : SLR

(Rs.in lacs)

Book Value of Face value of Market value of

Investments Investments Investments

3944.34 4140.00 4196.22

· Issuer Composition of Non SLR Investments :

(Rs. In Crore)

No. Issuer Amount Extent of Extent of Extent of

'below 'unrated 'unlisted

investment Securities' Securities'

grade

Securities'

(1) (2) (3) (4) (5) (6)

1 PSUs - - - -

2 FIs - - -

3 Public Sector Banks 11.02 - - -

4 Mutual Funds 6.40 - - -

5 Others 0.00051 - 0.00051

6 Provision held towards Depreciation 0.19 -

· Non-performing Non SLR Investment :

Particulars Amount

(Rs. In Crore)

Opening Balance Nil st Addition during the year since 1 April Nil

Reduction during the above period Nil

Closing Balance Nil

Total Provisions held Nil

Disclosure of Information

Ref : RBI Circular No. UBD.CO.BPD.(PCB) Cir No. 52/12.05.001/2013-14, Dated 25.03.2014

(11)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

[iv] Advance against Real Estate, Construction Business and Housing : Rs.1038.35[v] Advance against Shares &Debentures : Nil[vi] Advance to Directors, their relatives, companies/firms

in which theyare interested :(a) Fund Based Rs.20.50 Lacs(b) Non-fund Based( Guarantees, L/C etc.) Nil

[vii] Cost of Deposit :Average cost of Deposits : 3.43%[viii] NPAs : (a) Gross NPAs Rs 54.61 Lacs & % 1.69%

(b) Net NPAs 0.00[ix] Movement in NPAs :

NPAs Movement As on 31.03.2020 As on 31.03.2019 Gross NPAs 54.61 82.81

Net NPAs 0.00 0.00

[x] Profitability : (a) Interest income as a percentage of working funds 8.28% (b) Non-interest income as percentage of working funds 4.68% (c) Operating profit as percentage of working funds 2.37% (d) Return on Assets 4.89% (e) Business per employee Rs.150.44 (f) Profit per employee Rs.8.74

[xi] Provisions made : (a) Towards NPAs Rs. 330.57 (b) Towards Depreciation on investment Rs. 19.12 (c) Towards Standard Assets Rs. 35.07[xii] Movement in provisions : (Rs. In lacs) Provisions Movement As on 31.03.2020 As on 31.03.2019 Towards NPAs 330.57 309.20

Towards Depreciation on investments 19.12 19.12

Towards Standard Assets 35.07 35.07

[xiii] Foreign currency assets &liabilities : Not applicable[xiv] Payment of DICGC Insurance Premium :

During the year bank has regularly paid Insurance Premium on Deposits to DICGC as per norms prescribed by the Reserve Bank of India.

[xv] Penalty imposed by RBI: During the year, there is no penalty imposed by RBI to the Bank.[xvi] Restructured Accounts : Nil (Rs.in lacs)

Particulars of Account Restructured Housing SME Debt Others Loan Restructuring

Standard Name of Borrowers Nil Nil Nil Advances Amount Outstanding Nil Nil Nil Restructured Sacrifice (diminution in the fair value) Nil Nil Nil Sub Standard Name of Borrowers Nil Nil Nil Advances Amount Outstanding Nil Nil Nil Restructured Sacrifice (diminution in the fair value) Nil Nil Nil Doubtful Name of Borrowers Nil Nil Nil Advances Amount Outstanding Nil Nil Nil Restructured Sacrifice (diminution in the fair value) Nil Nil Nil Name of Borrowers Nil Nil Nil Total Amount Outstanding Nil Nil Nil Sacrifice (diminution in the fair value) Nil Nil Nil

[xvii] Fixed Assets Valuation / Revaluation : During the period under present Audit for the year ending on 31.03.2020, the Bank has Not

revalued any asset and there is no change in method of calculation of depreciation.[xviii] Unclaimed liabilities (amount transferred to DEAF) : (Ref.Cir.No. DBOD.No. DEAF Cell.BC.114/30.01.002/2013-14 dated 27.05.2014)

(Rs. in Crore) Previous Year Current Year

Opening Balance of amounts transferred to DEAF 10.94 11.88

Add : Amounts transferred to DEAF during the year 0.94 11.55

Less : Amounts reimbursed by DEAF towards claims 0.00 0.09

Closing balance of amounts transferred to DEAF 11.88 23.35

(12)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

Place :Surat Date : 23/06/2020

For, SOPARIWALA & Co. Chartered Accountants

PARTNER

C.A. Nicky D. Sopariwala M No 140537

FRN No. 132643W Panel No.298

(13)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

ztgthufxhtulttu ynuJttjt

cttuzo ytuV rzhufxmto Jt;te cttJtemtbtt JttrMtof ynuJttjt ;t:tt rnmttct ykdtu vt{btwFt`eltwk vt{Jtatlt.

mtw|t btntNtgt mtCttmt'`eytu....

1999 bttk m:tvttgtujte ytvtKte yt ctukf W@thtu@th vt{dt;te fhe hne Au. sultt gtNtltt Cttdte'thtu ytvt mtti

mtCttmt'tu yltu dt{tnfrbt*ttu Au. ytvtlte ctukf vt{;gtulte rJt#mtltegt;ttyu s ybttultu Fthe rnkbt;t, nwkV yltu ctG vtwhw

vttzgtwk Au. ;tt. 31-03-2020 ltt htus vtwht :t;tt JtMtoltt rnmttcttu, ynuJttjt yltu ctukfu btuGJtujte rmtr""tytu ytvt

mtti mtbtHt hsw fh;tt yltuhtu ytltk' yltwCtJtwk Awk.

fturJtz-19 &

fturJtz-19 Jttgthmtltt vt{jtgtkfthe vt{ftuvt Jtaatu ytvtKtu mtnw gtw} suJte rm:tr;tbttk:te vtmtth :tE hÏt Aeyu.

yt gtw}bttk 'wNbtlt mttbtu 'uFttgt ltnek, ;tulte ftuE n' fu mthn' vtKt lt:te. vthk;tw, ftuE cttuzoh vth ctumteltu jtzJttltu

ct'jtu ;tu ytvtKtt Dthbttk, JgtJtmttgtltt m:tG vth, hm;tt vth yhu ctukftubttk Dtqmteltu ytvtKtltu btntbtthe~vtu vtezt ytvtu

Au. ytX bttmt vtAe vtKt ftuE Jtufmtelt fu yfmteh 'Jttltt yCttJtlte Jtaatu mtbtm;t bttltJtS;t SKtu yt btntbtthe

mttbtu ymtntgt ctlte dtE Au.

ftuEvtKt jtztEbttk lttltwk bttuxwk ltwfNttlt :t;twk s ntugt Au. dttVujt hneyu ;ttu ltwfNttltlte btt*tt DtKte bttuxe :t;te

ntugt Au. vthk;tw ftuEvtKt 'uNtltu ytr:tof bttuhattu mtkCttGJttltkw y;gtk;t s~he ntugt Au. WjjtuFtltegt Au fu ytr:tof Htu*tlte

fhtuzhssw ctukrfkdt rmtmxbt Au. ctukrfkdt Htu*tbttk lttltt bttKtmttu bttxulttu nhnkbtuNtlttu mtr"tgtthtu yltu mtvttuxo mtnfthe

ctukftu Au. btltu ytltk' Au fu ftuhtultt btntbttheltt yt 'wMfh ftGbttk mtnfthe ctukftuyu mtbttsltt yt Segment ltu

;tlt-btlt-"tlt:te mttatJte jte"ttu Au. yt mtbtgt 'hbgttlt ytvtKtt vt{;gtuf fbtoattheyu V[lxjttElt Jtturhgth y:tto;t

ytdtjte nhtuGltt gttu}tlte Ctqrbtft CtsJte Au. ;tubtKtu y;gtk;t mtkgtbtvtqJtof, "tehs yltu mtntltwCtqr;tvtqJtof ftbt fgtwo

Au.

Ctth;tlte ;tbttbt mtnfthe ctukftubttk dtwsht;tlte mtnfthe ctukftubttk dtwsht;tltt mtnfthe ctukrfkdt Htu*tu yt

Jtir#f gtw} 'hrbtgttlt lttltt yltu bt"gtbtJtdtoltt bttKtmttulttu ctnt'whevtqJtof mtt:t ytvte ;tultu Cttkdte vtz;tt yxftJgttu

Au. dtwsht;t yt;btrltCtoh mtntgt gttusltt yk;tdto;t ytvtKte ctukfu jtdtCtdt 162 Wvthtk;t jttCtt:teoytultu ~t.

2,83,38,000 Wvthtk;tlte hfbtltwk r"thtKt vtq~k vttzeltu A friend in need, is a friend indeed lte Wrf;t

mttate XhtJte Au.

btk'eltt bttntujtbttk y:to;tk*tltu dtr;tNtejt ctlttJtJttlte yu bttuxe EaAtNtrf;t mttbttlgt bttltJte fu su

y:to;tk*tlttu Ftqct s bttuxtu yt"tth Au, ;tubtlte ytJtf ctbtKte fhJttlte atujtuls yltu vttkat bttuxe ytr:tof btntmt@tt:te

(14)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

ytdtG "tvttJtJttlte atujtuls Jtaatu ytJtfJtuhtltt 'h Dtxtzeltu ytvtKte sqlte bttkdtKte mJtefthtE Au.

btltu sKttJt;ttk ytltk' Au fu fulYegt ctsux 2020 bttk mtnfthe Htu*tlte bttkdtKte ytvtKte hsqyt;ttultt

vtrhKttbtu mtk;ttuMttE Au. mtti vt{:tbt ftu-ytuvthurxJt mtufxhltt fhJtuhtltt 'h DtxtzJttlte bttkdtKte n;te ;tu 33Ù bttk:te

22Ù mJtefth fhe ytvtKtltu mtk;ttuMt ytvgttu Au.

dt{tnf mtuJttltu vt{t"ttlgt &

ctukfu ;tulte m:ttvtltt:te s dt{tnf mtuJttltu Ftwct s vt{t"ttlgt ytvgtwk Au. Lzvte yltu ftgtoHtbt mtuJttytu vtqhe

vttzJttlttu ytvtKttu mt;t;t vt{gttmt dtGtftvt nrhVtEbttk VG'tgte vtqhJtth :tgttu Au.

yt"twrltf xuflttujttuB &

ytvtKte ctukflte nuz yturVmt yltu ct{tkattu JtMttuo:te xujteVtult jteL jttElt:te mtkfGtgtujte ntugt ftuE vtKt

ct{tkatbttk:te ytvtKtt dt{tnftu ;tubtltwk ctukrfkdt ftgto fh;tt ytJgtt Au.

dtgtt JtMttuobttk xufTlttujttuB yvtdt{uzuNtlt «tht ytvtKte ctukfu lteatu btwsctltt ftgto_bttu ybtjtbttk btwfe dt{tnftulte

mtdtJtztubttk Jt"tthtu fgttuo Au.

(1) RTGS «tht Ctth;tlte ftuE vtKt ctukfbttk:te ftuE vtKt ctukfbttk Vkz x[tlmtVh :tE Ntfu Au. sulttu jttCt

ytvtKtt dt{tnftu bttuxt vt{bttKtbttk jtE hÏt Au.

(2) CORE BANKING SOLUTION (CBS) yltu Cheque Truncation System(CTS)

«tht atufltwk r³jtgthekdt Elxhltux «tht :ttgt Au.

(3) DBTL / ABNPS mfebt & dtumt mtctmteze Ftt;tu'thtultt Ftt;ttbttk ztgthufx sbtt :ttgt ;tuJte mtdtJtz

ytvtKte ctukf vtwhe vttzu Au. sulttu jttCt jtuJtt bttxu mtCttmt'tultu yltwhtu"t fhJttbttk ytJtu Au.

(4) xe.ze.yumt., B.yumt.xe. ;t:tt btemtftujt yujtxolte mtdtJtz (sultt «tht Ftt;tu'th ftuEvtKt mtbtgtu

vttu;ttltt Ftt;ttltwk ctukf ctujtulmt SKte NtfNtu.)

ctukf «tht Nt~ fhJttbttk ytJtujt bttucttEjt ctukrfkdt mtuJttlttu jttCt dt{tnfltu rJtltt btqjgtu ytvtJttbttk ytJtu Au.

sultt «tht vttu;ttltt fhkx Ftt;tt rJtNtu bttrn;te bttucttEjt vth SMS :te ytvtJttbttk ytJtu Au. yltu mxuxbtulx Email

Address vth mtqatltt btwsct bttufjtJttbttk ytJtu Au. ytvtKte ctukflte bttucttEjt yuvt «tht vttu;ttltt bttucttEjtbttks

Ftt;ttlte rJtdt;ttu SuE Ntftgt Au. yltu nJtu ATM ftzolte mtwrJt"tt Wvtjtc"t fhJttbttk ytJte Au. ;t:tt IMPS ;t:tt

(15)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

bttucttEjt:te lttKttk x[tlmtVh :ttgt yuJte mtwrJt"tt attjtw fhe Au.

ctukfekdt JgtJtnthtu mtkvtqKto vtth'Ntof;tt:te rJtftmt &

ytvtKte ctukfu, ctukfltt Ftt;tu'thtu mtt:tultt JgtJtnthtu mtkvtqKto vtth'Ntof ctlttJgtt Au. ftuE Awvtt attBomt

WDthtJtJttbttk ytJt;tt lt:te. ;tbttbt attBomt fu ftgtoJttne yuf'bt vtth'Ntof htFtJttbttk ytJtu Au yltu vtmtolttjttELz

mtuJttytu ytvtJttbttk ytJtu Au. yt:te ytvtKte ctukflttu dt{tnf Jtdto rJtfmte hÏtu Au, mttatt y:tobttk fneyu ;ttu ctukfltt

dt{tnf s cteS dt{tnfltu jttJtu Au su ytvtKtu bttxu FthuFth ytltk' ;t:tt dttihJtlte Jtt;t Au.

:ttvtKttubttk ytvtKte attjtw :ttvtKtltwk vt{bttKt Ftqct s W;mttnvt{uhf hÏwk Au ;tultwk fthKt Au mtJto Jgttvtthe

btntslttu, dt{tnftu yltu mttulttbttk mtwdtk"t~vt mt't nmt;tt ;Jthe;t mtuJttytu ytvt;tt ybttht mxtV rbt*ttu subtltt:te

ytvtKtt dt{tnftu mtkvtqKto mtk;ttuMt yltwCtJtu Au.

ytvtKtt :ttvtKt'thlte ~t. 5 jttFt mtw"telte ;tbttbt :ttvtKt Deposit Insurance & Credit

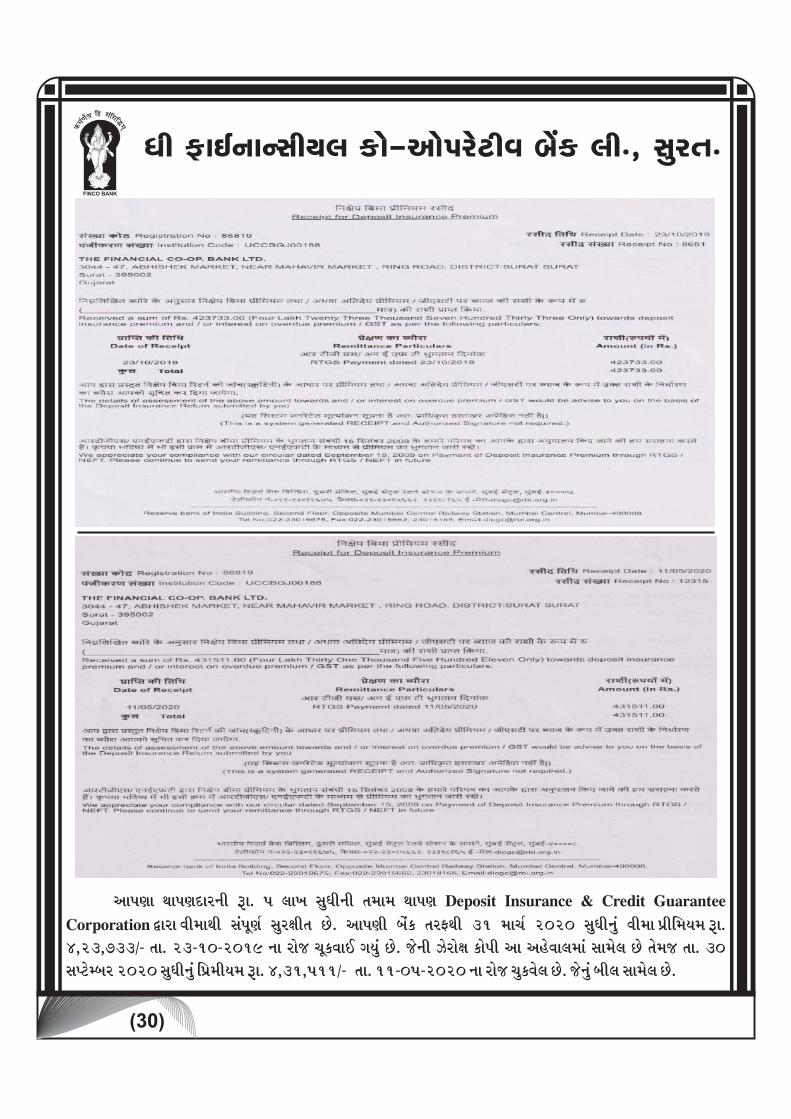

Guarantee Corporation «tht Jtebtt:te mtkvtqKto mtwhHte;t Au. ytvtKte ctukf ;thV:te 31 bttato 2020

mtw"teltwk Jtebtt vt{erbtgtbt ~t. 4,23,733/- ;tt. 23-10-2019 ltt htus atqfJttE dtgtwk Au. sulte LuhtuHt ftuvte

yt ynuJttjtbttk mttbtujt Au ;tubts ;tt. 30 mtvxubcth 2020 mtw"teltwk rvt{btegtbt ~t. 4,31,511/- ;tt. 11-05-

2020 ltt htus atwfJtujt Au. sultwk ctejt mttbtujt Au. (vtuEs ltkcth & 30)

N.P.A. :

btultusbtulx ;thV:te mtkvtqKto ;tfu'the yltu mtFt;t ykfwNtltu fthKtu zqct;t yltu Ntfbtk' jtuKtt bttxu ;tt. 31-03-

2020 mtw"te ~t. 3,30,56,914/- ltwk rhLJto Vkz Au yltu ;tt. 31-03-20 ltt htus vtqht :t;tt JtMtoltt ltVtbttk:te

~t. 67,03,200/- lte SudtJttE :t;tt fwjt ~t. 3,97,60,114/- lte SudtJttE Au. ytvtKttu dt{tumt yult. vte. yu.

ytkf ~t. 54.61 jttFt (1.69Ù) yltu ltux yult. vte. yu. ytkf 0Ù Au. yltu heLJto ctukf ytuV Elzegttltt mtqatlttu

btwsct mtk;ttuMtvt{' yltu bttlgt btgtto'tlte lteatu Au.

ytkfztfegt bttrn;te &

yt mtt:tu ;tt. 31-03-2019 yltu 31-03-2020 ltt htus vtqht :t;ttk JtMttuolttk ytkfztytulte ;twjtltt

yltu ltVtlte VtGJtKte vttltt ltk. (28) vth ytvte Au. 2016 'hbgttlt lttuxctk"te, 2017bttk Byumtxe ;t:tt

2019bttk ftuhtulttltu fthKtu Jgttvtth W$tudt vth bttXe ymth :tE Au. sultt fthKtu ctulfekdt JgtJtnthtu Wvth DtKte

ymth :tE Au. yltu ftvtz W$tudt ;t:tt ylgt DtKtt JgtJtmttgtbttk ytJtfltt vt{bttKtbttk ymthtu 'uFttgt Au. mttbttlgt he;tu

(16)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

ctulfekdt JgtJtmttgtbttk Jtt;ttJthKt rlt~;mttnmtCth hÏwk.

r"thtKt &

sKttJt;tt ytltk' :ttgt Au fu r"thtKt vth Jgttsltt 'h cteB ctukftulte mthFttbtKtebttk DtKttk ytuAtk htFgtt Au.

Jgttsltt 'hlte rJtdt;t Aujjtt vttltt vth sKttJte Au. bttltJtk;tt mtCttmt'CttE ;t:tt dt{tnf mtbtw'tgtltu yt W'th

mtdtJtz;ttlttu jttCt jtuJtt ytdt{nCthe rJtltk;te Au.

rzrJtzlz &

ftuJtez-19 vtulzubtef mtkSudttu ltu "gttltbttk htFteltu heLoJt ctukfu mtJtuo yctolt ftu.ytu.ctukftultu zeJtezlz lt

atqfJtJtt bttxu mtqatltt ytvtujt Au.

heLJto ctukf ytuV Erlzgttltt ;tt. 17-04-2020 ltt mthfgtwjth ltk. RBI/2019-20-218

DOR.BP.BC NO. 64/21.02.067/2019-20 yltwmtth fturJtz-19 :te WCte :tgtujt yattu²mt vtrhm:te;teltu

fthKtu ctukftu bttxu ;tubtlte btqze SGJtJtt s~he sKtt;tt ylgt mtqatlttytu lt btGu ;gttk mtw"te ctukftu ;tubtltt JtMto 2019-

20 ltt ltVtbttk:te zeJtezlz atqfJte NtfNtu ltne. yt rltgtk*tKt Wvth heLJto ctukf «tht ctukftultt mtvxubcth-2020

ytFthltt lttKttkfegt vtrhKttbttultu yt"tthu vtwlt&rJtatth fhJttbttk ytJtNtu ;gtthu yvttltthe heLJto ctukf ytuV Erlzgttlte

mtqatlttytultu yt"telt ybtjtefhKt fhJttbttk ytJtNtu.

:ttvtKt'thtulttu rJt#tmt yltu :ttvtKttulte mtwhHtt &

ctulfekdt Htu*tbttk 2017 bttk lttuxctk"teltu fthKtu zevttuLex Jt"te vthk;tw ;tu hfbt 2017-18 'hbgttlt mtJtuo

ctulftubttk:te vth;t jtuJttE dtE ;tu:te zevttuLex vtKt Dtxe dtE. :ttvtKttu JtMto 2016-17ltt yk;tu ~t. 12,300.00

jttFt n;te. ;tu 2018-19ltt JtMtoltt yk;tu 8,171.44 jttFt :tE n;te yltu 2019-ftuhtulttltu fthKtu 2019-

20lttk yk;tu 6,093.00 jttFt :tE n;te.

attuFFttu ltVtu &

JtMto 'hbgttlt ctukflttu ftattu ltVtu ~t. 541.88 jttFt suxjttu :tgttu n;ttu ;t:tt mtltu 2007-08 ltt JtMto:te

mtnfthe ctukftultu Elfbt xuHt jttdtw vtz;tt ytvtKte ctukfu ~t. 95.00 jttFt Elfbt xuHt Cth;tt ctukflttu attuFFttu ltVtu ~t.

446.88 jttFt suxjttu :tgttu n;ttu. subttk dtJtObtulx mtefgtwhexelttu rmtknVtGtu ~t. 325.96 jttFt n;ttu.

rmtfgtwhuxtELuNtlt yufx &

(17)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

lttdtrhf mtnfthe ctukftu rmtfgtwhuxtELuNtlt yufx nuXG NPA lte Jtmtwjtt;t fhe Ntfu ltnek ;tuJttu atwft'tu

lttbt'th dtwsht;t ntEftuxo «tht 2013 bttk ytvtJttbttk ytJtujt ;tulte mttbtu mtwrvt{bt ftuxobttk fumt 'tFtjt fhJttbttk

ytJtujt yt fumtlttu atwft'tu yctoltu ctukftulte ;thVuKtbttk ytJgttu Au. sultt yt"tthu nJtu yctolt ctukftu rmtfgtwhuxtELuNtlt

yufx nuXG NPA lte Jtmtwjtt;t fhe NtfNtu. mthVumte yufx nuXG Jtmtwjtt;t fhJtt bttxu bttudtuos vt{tuvtxeltwk mthmttE

(CERSAI) bttk hBmx[uNtlt fhtJtJtwk VhBgtt;t Au.

ytvtKtt VuzhuNtlt ;t:tt GSC ctukf «tht dtwsht;t ntEftuxobttk yltu ;gtthctt' mtwrvt{bt ftuxobttk vtKt

NAFCUB mtt:tu btGeltu jttkcte ftltqlte jtztE jtzeltu ytvtKte mtnfthe ctukftulte ;thVuKtbttk yt atwft'tu jttJt;ttk

ytvtKtt bttxu rhfJthelttu bttuxtu bttdto Ftwjgttu Au. ;tultu jtEltu hefJthelte vt{r_gtt Lzvte ctltNtu yltu ctukftulte ytr:tof

rm:tr;tbttk mtw"tthtu :tNtu.

attxozo yuftWlxlmte yCgttmt_btltt rJt$t:teoytultu mtwJtKto atkYfltt Elttbttu &

ytvtKte ctukf yuf mttbttBf vt{Jt]r@t~vtu mtwh;tlttk attxozo yuftWlxlx VtWlzuNtlt, Elxh yltu VtEltjt JtMtoltt

rJt$t:teoytubttk:te suytu mtJttuo@tbt dtwKttkf btuGJte W@teKto :ttgt Au ;tubtltu mtwJtKto atkYf:te ltJttsu Au.

mtCttmt'ltt bt];gtw ctt' Jtthmt'thtultu yvtt;te mtntgt &

ctukfltt rltgtbt vt{bttKtu ytvtKtt Ntuh ntujzh (1) r*tJtu'e ltxJthjttjt r'ltfhhtgt (2) vtwltrbtgtt

fjttJt;tectult hbtuNtatkY (3) fkmttht rfNttuh sgtfeNtlt (4) vthbtth 'wdttoctult lthvt;tCttE ltt bt];gtw ctt' yubtltt

Jtthmt'thtultu 'hufltu ~t. 10,000/- lte mtntgt fhe.

mttbttBf mtuJtt &

JtMto 'hbgttlt sw'e sw'e mtkm:ttytultu 'tlt ytvgtwk sulte rJtdt;t lteatu vt{bttKtu Au &

~rvtgtt mtkm:ttltwk lttbt

11,000/- mttumttgtxe Vtuh VeLefjt nulzefuvt, mtwh;t.

5,100/- `e yt'Nto htbtjtejtt x[mx, mtwh;t.

51,000/- ateV bteltemxh hejteV Vkz (ftuhtultt-2019)

67,100/-

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

yturzxh &

mttuvttheJttjtt yulz ftwk. ltu mtnfthe mttumttgtxeltt hBmx[th`e ;thV:te ctukfltt vt{bttrKt;t yturzxh ;thefu

rltbtKtqkf ytvtujt Au. yltu ;tuytulte btq';t JttrMtof mtt"tthKt mtCtt mtw"telte ntugt Au.

yt;btrlthCtoh dtwsht;t mtntgt gttusltt (I) yltu (II) bttk gttudt'tlt &

fturJtz-19 btntbtthe Vujtt;te yxftJtJtt bttxu mthfth ;thV:te jttufztWlt Snuh fhJttbttk ytJgtwk. yt

jttufztWltltt fthKtu mttbttlgt vt{Sslttulte ytr:tof vt{Jt]r@t Wvth DtKte s rJtvthe;t ymth :tE sultu fthKtu mbttujt yltu

rhxujt x[uzmto, vt{tuVuNtltjmt, fthedth Jtdto, Vurhgttytu Jtdtuhu ytr:tof Ctekmtbttk ytJte dtgtt. ytJtu JtFt;tu dtwsht;t

mthfth`eyu ytr:tof vt{Jt]r@t yltu Fttmt fheltu lttltt Jtdtoltt jttuftulte ytr:tof vt{Jt]r@tltu Jtudt ytvtJtt bttxu

yt;btrltCtoh dtwsht;t mtntgt gttusltt-I fu subttk ;tthKt Jtdth ~t. 1-00 jttFt mtw"teltwk r"thtKt yltu yt;btrltCtoh

dtwsht;t mtntgt gttusltt-II fu subttk ;tthKt mttbtu ~t. 2-50 jttFt mtw"teltwk r"thtKt 6Ù yltu 4Ù ltt Jgttslte mtntgt:te

yltu ;tu vtKt yctolt ftu-ytuvthuxeJt ctukftultt mtt:t mtnfth:te ytvtJttltwk lt²e fgtwO. ;tu ct'jt ytvtKtt btwFgtbtk*te `e

rJtsgtCttE ~vttKte, lttgtct btwFgtbtk*te ̀ e lter;tltCttE vtxujt, mtnfth btk*te ̀ e E#hrmtkn vtxujt, mtnfth mtratJt

`e btrltMt Ctth«ts, htsgt hBmx[th ̀ e ze. vte. 'umttElttu yk;t&fhKtvtqJtof Ftqct Ftqct ytCtth bttltkw Awk. ytvtKte

ctukfu vtKt yt gttuslttbttk 162 Wvthtk;t jttCtt:teoytultu ~t. 2,83,38,000 suxjtwk "tehtKt fgtwO Au.

`""ttksrjt &

ynuJttjt yt"telt JtMto 'hrbtgttlt ytvtKtt fuxjttgtu mtnfthe ctk"twytu ytvtKte Jtaatu:te mt'tltu bttxu rJt'tgt

jtE atqfgtt Au. mtJto mtÚdt;t btntltwCttJttultu `""ttksrjt ;t:tt ;tubtltt yt;bttltu rathk;tlt Nttkr;t y:tuo vt{Ctwvt{t:toltt. yt

mtJto btntltwCttJttubttk WjjtuFtltegt lttbt Au, mJt. `e lthulYCttE dttk"teltwk. dtwsht;t yctolt ftu-ytuvthuxeJt ctulfmt

VuzhuNtlt ybt'tJtt'ltt rzhufxh hne atqfujtt `e lthulYCttE dttk"te mtwh;t ;tubts dtwsht;tltt JtrhMX yltu vtrhvtfJt

mtnfthe ydt{Kte n;tt. mtÚdt;tlte y:ttf mtuJttytultu rJtltbt{ CttJttksrjt mtt:tu ytvtKtt mtnw ;thV:te `}tmtwbtlt

yvtoKt f~k Awk.

ctukf mtt:tu Suztgtujt vt{;gtuf Jgtrf;t attnu ;tu btultusbtulx ;thV:te ntugt fu mxtV btubcth. ;tubtKtu mtnwyu fturJtz-

19 lte btntbtthebttk §lxjttElt Jtturhgth ctlteltu ftbt fgtwo Au yltu mttbttlgt vt{Sslttultu ytJte frXlt vtrhrm:tr;tbttk

vttu;ttlte vthJtt fgtto rJtltt yrJth;t ctukrfkdt mtuJtt vtqhe vttze Au. y;gtk;t 'w&Ft mtt:tu sKttJtJttltwk fu yt btntbtthebttk

mtnfthe Htu*tltt ydt{dtKgt ftgtof;tto ;tubts mxtV btubcthtuyu vttu;ttltt Slt dtwbttJgtt Au. yt 'huf fbtoMX ftgtof;ttoytultu

(18)

(19)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

bttht Jt;te yltu cttuzo ytuV rzhufxmto yltu mxtV btubcth Jt;te ̀ ""ttksrjt ytvtkw Awk yltu ;tubtltt yt;bttltu Nttkr;t btGu

;tuJte vt{t:toltt f~k Awk.

ÒKt mJtefth &

ytvtKtt ;tbttbt rzhufxh rbt*ttu ytvt mttiltu Ç'gt vtqJtof ytCtth bttltu Au-Ntuh "tthftu, btqjgtJttlt dt{tnfrbt*ttu,

heLJto ctukf ytuV Elzegtt, mtnfthe btkzGeytultt hBmx[th`e, mxux ctukf ytuV Elzegtt, "te mtwh;t zemx[efx ftu-

ytuvthuxeJt ctukf jte., mtwh;t, "te mtwh;t vtevtjmt ftu-ytuvthuxeJt ctukf jte., mtwh;t, ctukf ytuV cthtuzt, gtNt ctukf jte.,

yuat. ze. yuV. mte. ctukf jte., ytE. ze. cte. ytE. ctukf jte., ytE. mte. ytE. mte. ytE. ctukf jte, ftuxf btrnlYt

ctukf jte., dtwsht;t mxux ftu. ytu. ctuf jte., D.C.B, sltt mbttujt VtElttlmt ctukf, btnumttKtt ftu-ytu. ctukf, yu. gtw.

mbttujt VtElttlmt ctukf, Veltfuh mbttujt VtElttlmt ctukf, ;t:tt W;fMto mbttujt VtElttlmt ctukf, mttW:t dtwsht;t ftu. ytu.

ctukfmto yumttumteyuNtlt, dtwsht;t yctolt ftu-ytuvt. ctukf VuzhuNtlt yltu mtJtuo NtwCtuaAftu fu suytuyu mtjttnmtqatlttu ytvgtt

;tubts ybtthtbttk rJt#tmt btqfeltu ytvtKte ctukfltt rJtftmtltt mtt"tlt~vt ctlgtt.

ytvtKtt rzhufxh`eytu ytvtKttk mxtVltt mtJtuo mtCgttultu ;tubtltt mtnfth ;t:tt Âze jtdtlt:te dt{tnfjtHte mtuJtt

ytvteltu ctukfltt rJtftmtbttk vttgtt~vt ctltJtt bttxu NttcttNte ytvtu Au.

yt ct'jttgtujtt mtbtgtbttk rltKttk;ttultt bt;tu yt btntbtthe jttkctt mtbtgt mtw"te attjtJttlte ntuE, ;tulte 'whtudttbte

rJtvtrh;t ymthtultu "gttltu jtE ytvtKtu mttiyu vtrhJt;tolt bttxu bttltrmtf he;tu ;tigtth :tE yt ftuhtultt btntbtthe mtt:tu

BJtJttlte xuJt fuGJtJte vtzNtu. JtthkJtth mttctw:te nt:t "ttuJtt, bttmf vtnuhJttlte xuJt, ;t:tt mtturNtgtjt rzmxlmtekdtltt

%%'tu dts 'whe^^ SGJte htFtJttltt bttltltegt Jtztvt{"ttlt`eyu ytvtujt btntbtk*tltu ytvtKtu mttiyu yt;btmtt;t fhJttu

vtzNtu.sgt rnl', sgt mtnfth

"tlgtJtt' !

`e htbt rlthkslt ydt{Jttjt

vt{btwFt

m:tG & mtwh;t

Dt. : 27-11-2020

(20)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

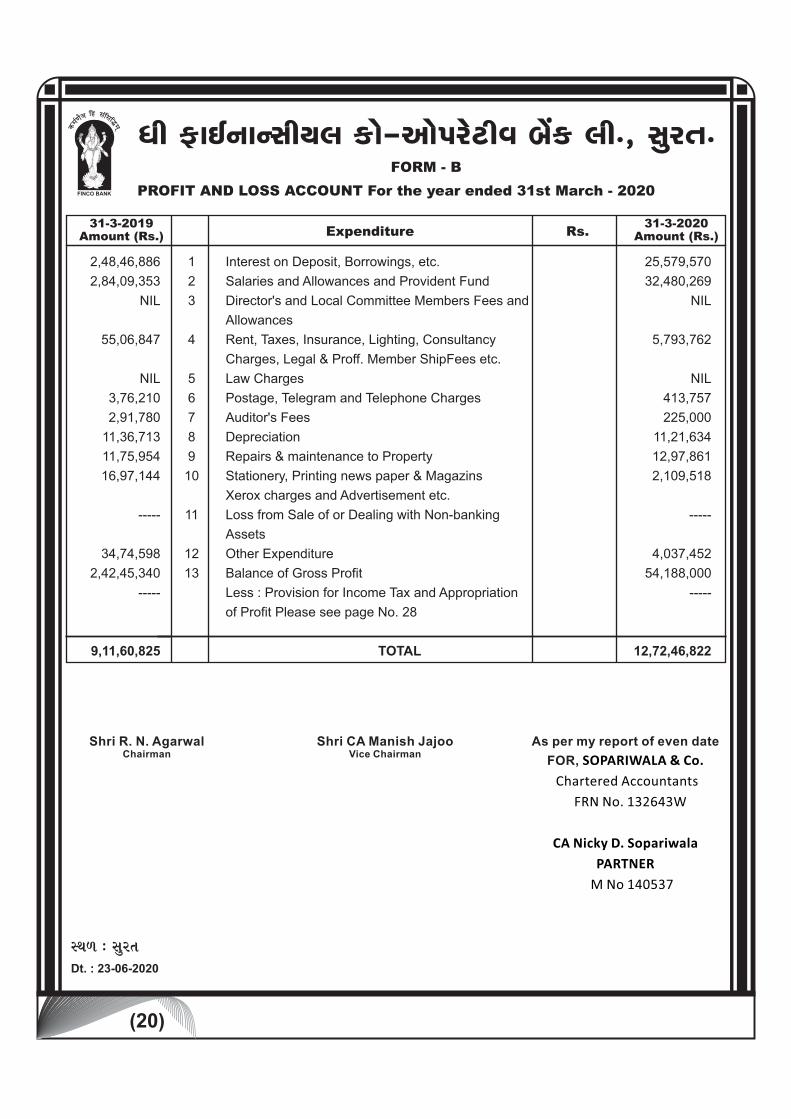

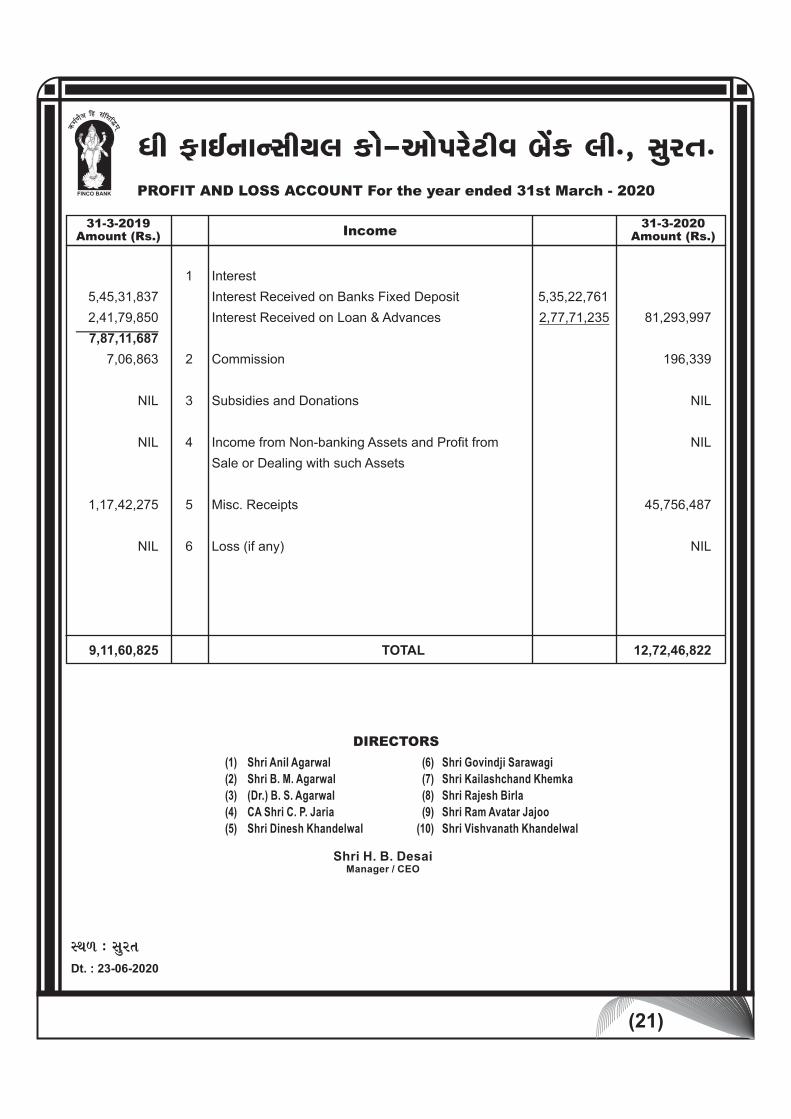

PROFIT AND LOSS ACCOUNT For the year ended 31st March - 2020

FORM - B

2,48,46,886 1 Interest on Deposit, Borrowings, etc. 25,579,570

2,84,09,353 2 Salaries and Allowances and Provident Fund 32,480,269

NIL 3 Director's and Local Committee Members Fees and NIL

Allowances

55,06,847 4 Rent, Taxes, Insurance, Lighting, Consultancy 5,793,762

Charges, Legal & Proff. Member ShipFees etc.

NIL 5 Law Charges NIL

3,76,210 6 Postage, Telegram and Telephone Charges 413,757

2,91,780 7 Auditor's Fees 225,000

11,36,713 8 Depreciation 11,21,634

11,75,954 9 Repairs & maintenance to Property 12,97,861

16,97,144 10 Stationery, Printing news paper & Magazins 2,109,518

Xerox charges and Advertisement etc.

----- 11 Loss from Sale of or Dealing with Non-banking -----

Assets

34,74,598 12 Other Expenditure 4,037,452

2,42,45,340 13 Balance of Gross Profit 54,188,000

----- Less : Provision for Income Tax and Appropriation -----

of Profit Please see page No. 28

9,11,60,825 TOTAL 12,72,46,822

Expenditure Rs.31-3-2019

Amount (Rs.) 31-3-2020

Amount (Rs.)

Shri R. N. AgarwalChairman

Shri CA Manish JajooVice Chairman

Dt. : 23-06-2020

As per my report of even date

FOR, SOPARIWALA & Co.

Chartered Accountants

FRN No. 132643W

CA Nicky D. Sopariwala

PARTNER

M No 140537

m:tG & mtwh;t

(21)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

1 Interest

5,45,31,837 Interest Received on Banks Fixed Deposit 5,35,22,761

2,41,79,850 Interest Received on Loan & Advances 2,77,71,235 81,293,997

7,87,11,687

7,06,863 2 Commission 196,339

NIL 3 Subsidies and Donations NIL

NIL 4 Income from Non-banking Assets and Profit from NIL

Sale or Dealing with such Assets

1,17,42,275 5 Misc. Receipts 45,756,487

NIL 6 Loss (if any) NIL

9,11,60,825 TOTAL 12,72,46,822

Income

PROFIT AND LOSS ACCOUNT For the year ended 31st March - 2020

31-3-2019Amount (Rs.)

31-3-2020Amount (Rs.)

DIRECTORS

Shri Anil Agarwal

Shri B. M. Agarwal

(Dr.) B. S. Agarwal

CA Shri C. P. Jaria

Shri Dinesh Khandelwal

Shri Govindji Sarawagi

Shri Kailashchand Khemka

Shri Rajesh Birla

Shri Ram Avatar Jajoo

Shri Vishvanath Khandelwal

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Shri H. B. DesaiManager / CEO

Dt. : 23-06-2020

m:tG & mtwh;t

(22)

Amount (Rs.) Capital and Liabilities

1. Capital(i) Authorised Capital

5,00,000 shares of Rs. 100 eachshares of Rs. each(ii) Subscribed Capital 221025 shares of Rs. 100 each Fully Paid upshares of Rs. each(iii) Amount called upon shares at Rs. each Fully Paid Upon____shares of Rs. each less calls unpaidPending allotment 85 each of Rs. 100 Of (iii) above, held by (a) Individuals(b) Co-operative institutions(c) Nominal Share(d) State Government

2. Reserve Fund and Other Reserves

(i) Statutory Reserve

(ii) Agricultural (Credit Stabilisation Fund)(iii) Building Reserve Fund(iv) Dividend Equalisation Reserve Fund(v) Special Bad Debts Reserve(vi) Bad and Doubtful Debts Reserve Fund

(vii) Investment Depreciation Reserve Fund

(viii) Other Funds and Reserves (to be specified)a) Propaganda Reserve Fundb) Charity Reserve Fundc) Staff Welfare Reserve Fundd) Jubilee Reserve Funde) Share holders welfare Reserve Fundf) Education Reserve Fundg) Contingency Reserve Fundh) Urban Bank's credit Equiladation Reserve Fundj) Investment Fluctuation Reserve Fundk) Bad & Doubtful Debts Reserve Provision on Standard Assets

2,21,02,500

8,500

NILNIL40

NIL

16,84,73,273

NIL4,03,88,140

25,99,743NIL

3,30,56,914

19,11,750

5,075,032 5,450,622 4,570,813

10,951,883 3,941,556

3,00,0009,106,322

1,25,38,2432,00,000

35,00,704

5,00,00,000

2,21,11,040

30,20,64,995

31-3-2019Amount (Rs.)

31-3-2020Amount (Rs.)

5,00,00,000

2,18,69,100

32,000

NILNIL30

NIL

2,19,01,130

16,12,33,323

NIL3,98,72,182

25,99,743NIL

3,09,20,113

19,11,750

49,67,54153,08,16944,63,322

1,07,36,90141,98,821

3,00,00089,63,000

1,25,38,2432,00,000

35,00,704

29,17,13,812

31,36,14,942

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

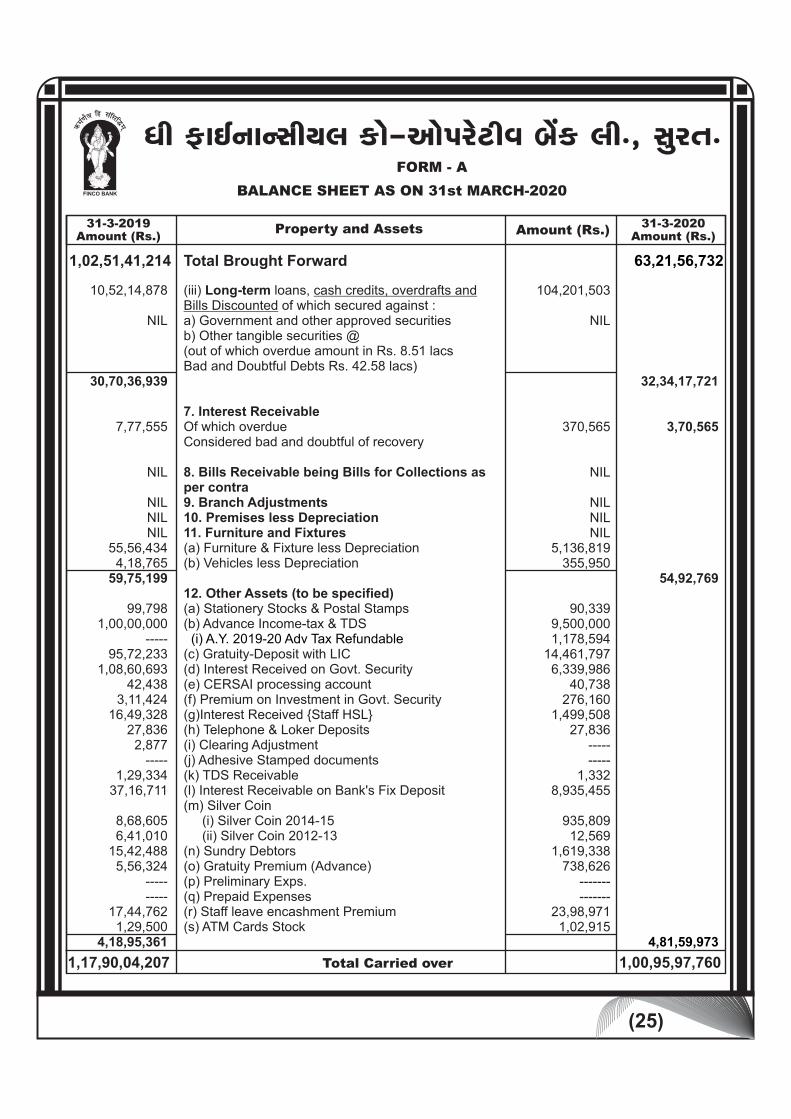

BALANCE SHEET AS ON 31st MARCH-2020

FORM - A

32,41,76,035

(23)

Amount (Rs.) Property and Assets

1. Cash in handIn hand and with 1[the National Bank], State bank of India,State co-operative bank and Central co-operative bank.2. Balance with other banks(i) Current deposits with Notified Banks(ii) Current deposits with other Banks(iii) Savings bank deposits (iv) Fixed deposits

3. Money at call and short notice

4. Investments(i) In central and State Government securities (at book value)Face Value Rs. 41,40,00,000.00Market Value Rs. 41,96,22,309.36(ii) Other Trustee securities(iii) Shares in co-operative institutions other than in item (5) below:(iv) Other Investments (to be specified)

(v) Surat Dist. Co-Op.Bank Fixed Deposit(Vi) Gujarat State Co-op. Bank Fixed Deposit

5. Investments out of the Principal/Subsidiary State Partnership FundIn shares of :(i) Central co-operative banks(ii) Primary agricultural credit societies(iii) Other societies6. Advances (i) Short-term loans, cash credits, overdrafts andBills Discounted Of which secured against :a) Government and other approved securitiesb) Other tangible securities @

(out of which overdue amount in Rs. 4.53 lacsBad and Doubtful Debts Rs. 4.53 lacs)(ii) Medium-term loans, cash credits, overdrafts andBills Discounted of which secured againsta) Government and other approved securitiesb) Other tangible securities @(out of which overdue amount in Rs. 4.74 lacsBad and Doubtful Debts Rs. 7.49 lacs) C/F

830,220 21,594,440

NIL 110,224,079

NIL

394,434,000

64,000,000 5,100

NIL

NILNIL

--------- ---------

148093173

13714076

----

56,644,421

764,547.00 NIL

41,068,893

132,648,739

458,439,100

31-3-2019Amount (Rs.)

31-3-2020Amount (Rs.)

3,92,35,875

5,15,6022,62,44,616

NIL13,52,00,00016,19,60,218

NIL

55,21,17,960

7,00,00,0005,100

NIL

NILNIL

62,21,23,060

----------

11,13,78,286

1,23,48,295-----

7,72,28,643

8,66,837NIL

Total Carried over

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

BALANCE SHEET AS ON 31st MARCH-2020

FORM - A

1,02,51,41,214 63,21,56,732

(24)

Amount (Rs.)

245,226,020 NIL NIL

99,102,624

NIL NIL

258,399,256

NIL

NIL 6,571,648 60,92,99,548

NIL

NIL

NIL

NIL

NIL

NIL

Total Carried over

31-3-2019Amount (Rs.)

31-3-2020Amount (Rs.) Capital and Liabilities

Total Brought Forward3. Principal/Subsidiary State Partnership Fund A/cFor share capital of :(i) Central co-operative banks(ii) Primary agricultural credit societies(iii) Other societies4. Deposit and Other Accounts(i) Fixed deposits*a) Individuals **b) Central co-operative banksc) Other societies(ii) Savings bank depositsa) Individuals **b) Central co-operative banksc) Other societies(iii) Current depositsa) Individuals **b) Central co-operative banks

c) Other societies(iv) Other Deposits (Credit Balance of Advances)

5. Borrowings $(i) From 2 [the National Bank]/State/Central co-operative bankA) Short-term loans, cash credits and overdraftsOf which secured against fix deposita) Government and other approved securitiesb) Other tangible securities @B) Medium-term loansOf which secured against :a) Government and other approved securitiesb) Other tangible securities @C) Long-term loansOf which secured against :a) Government and other approved securitiesb) Other tangible securities @ii) From the State Bank of IndiaA) Short-term loans, cash credits and overdrafts.Of which secured against :a) Government and other approved securitiesb) Other tangible securities @B) Medium-term loansOf which secured against :a) Government and other approved securitiesb) Other tangible securities @

24,26,32,834NILNIL

11,39,32,019NILNIL

45,48,14,420NIL

NIL57,65,138

81,71,44,411

NIL

NIL

NIL

NIL

NIL

NIL

BALANCE SHEET AS ON 31st MARCH-2020

FORM - A

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

1,13,07,59,353 93,34,75,583

31,36,14,942 32,41,76,035

.

32,34,17,721

3,70,565

54,92,769

4,81,59,973

(25)

Amount (Rs.) Property and Assets

(iii) Long-term loans, cash credits, overdrafts andBills Discounted of which secured against :a) Government and other approved securitiesb) Other tangible securities @(out of which overdue amount in Rs. 8.51 lacsBad and Doubtful Debts Rs. 42.58 lacs)

7. Interest ReceivableOf which overdueConsidered bad and doubtful of recovery

8. Bills Receivable being Bills for Collections asper contra9. Branch Adjustments10. Premises less Depreciation11. Furniture and Fixtures (a) Furniture & Fixture less Depreciation(b) Vehicles less Depreciation

12. Other Assets (to be specified)(a) Stationery Stocks & Postal Stamps(b) Advance Income-tax & TDS (i) A.Y. 2019-20 Adv Tax Refundable(c) Gratuity-Deposit with LIC (d) Interest Received on Govt. Security(e) CERSAI processing account(f) Premium on Investment in Govt. Security(g)Interest Received {Staff HSL}(h) Telephone & Loker Deposits(i) Clearing Adjustment(j) Adhesive Stamped documents(k) TDS Receivable(l) Interest Receivable on Bank's Fix Deposit(m) Silver Coin (i) Silver Coin 2014-15 (ii) Silver Coin 2012-13(n) Sundry Debtors(o) Gratuity Premium (Advance)(p) Preliminary Exps.(q) Prepaid Expenses(r) Staff leave encashment Premium(s) ATM Cards Stock

104,201,503

NIL

370,565

NIL

NIL NIL NIL

5,136,819 355,950

90,339 9,500,000 1,178,594

14,461,797 6,339,986

40,738 276,160

1,499,508 27,836

----- -----

1,332 8,935,455

935,809

12,569 1,619,338

738,626 ------- -------

23,98,9711,02,915

10,52,14,878

NIL

30,70,36,939

7,77,555

NIL

NILNILNIL

55,56,4344,18,765

59,75,199

99,7981,00,00,000

-----95,72,233

1,08,60,69342,438

3,11,42416,49,328

27,8362,877

-----1,29,334

37,16,711

8,68,6056,41,010

15,42,4885,56,324

----------

17,44,7621,29,500

4,18,95,361

Total Carried over

31-3-2019Amount (Rs.)

31-3-2020Amount (Rs.)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

BALANCE SHEET AS ON 31st MARCH-2020

FORM - A

1,17,90,04,207 1,00,95,97,760

1,02,51,41,214 63,21,56,732 Total Brought Forward

(26)

Amount (Rs.) Capital and Liabilities31-3-2019

Amount (Rs.) 31-3-2020

Amount (Rs.)

BALANCE SHEET AS ON 31st MARCH-2020

FORM - A

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

1,17,90,39,842 1,00,96,77,924 TOTAL

1,13,07,59,353NIL

NIL

NIL

NIL

NIL

NIL45,45320.654

44,40,67510,85,286

38,06995,72,233

9,07,9877,77,555

17,44,76244,98,500

4,39,6532,32,3432,31,979

2,40,35,149

3,59,1418,27,262

2,043

2,42,45,340

Total Brought ForwardC) Long-term loansOf which secured against :a) Government and other approved securitiesb) Other tangible securities @(iii) From the State GovernmentA) Short-term loans, cash credits and overdraftsOf which secured against :a) Government and other approved securitiesb) Other tangible securities @B) Medium-term loansOf which Secured Against :a) Government and other approved securitiesb) Other tangible securities @C) Long-term loansOf which Secured Against :a) Government and other approved securitiesb) Other tangible securities @(iv) Loans from other sources (source and security to be specified)6. Bill for Collection being Bills Receivable as per contra7. Branch Adjustments8. Interest Payable on Matured Deposits9. Interest Payable On Fix Deposits10. Other Liabilities(i) Pay Order Issued(ii) Unclaimed dividends(iii) Clearing Adjustment(iv) Gratuity with LIC (As par Contra)(v) Sundries Creditors(vi) Interest Accrued but not received on advances(vii) Staff Leave encasements (As Par Contra)(viii) Mehsana Urban Co-op. Bank(ix) Payable Accounts a) T.D.S. b) CGST c) SGST

11. Inoperative Deposit A/c.Current DepositsSavings DepositsRecurring Deposits12. Profit and LossGross Profit as per last balance sheet

NIL71,242 43,042

12,96,647 15,48,915

60 1,44,61,797

10,59,100 3,70,565

23,98,971 -----

4,35,536 1,64,233 1,64,233

6,55,577 16,77,026

2,043

93,34,75,583NIL

NIL

NIL

NIL

NIL

NILNIL

2,20,14,341

5,41,88,000

(27)

Amount (Rs.)

TOTAL

1,00,95,97,760

NIL

80,162

31-3-2019Amount (Rs.)

31-3-2020Amount (Rs.) Property and Assets

Total Brought Forward13. Non-banking Assets acquired in satisfaction of

claims (stating mode of valuation)

14. Profit and Loss

15. Tax on Input (Purchase)

CGST Purchase ITC

SGST Purchase ITC

IGST Purchase ITC

16. Inoperative Deposit

(a) Inoperative Current Account

(b) Inoperative Saving Account

(c) Inoperative Recurring Deposit

1,17,90,04,207NIL

NIL

16,640

16,640

2,355

35,635

3,59,141

8,27,262

2,043

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

BALANCE SHEET AS ON 31st MARCH -2020

FORM - A

1,17,90,39,842 1,00,96,77,924

NIL

NIL

38,740

38,740

2,682

655,577

1,677,026

2,043

Dt. : 23-06-2020

DIRECTORS

Shri Anil Agarwal

Shri B. M. Agarwal

(Dr.) B. S. Agarwal

CA Shri C. P. Jaria

Shri Dinesh Khandelwal

Shri Govindji Sarawagi

Shri Kailashchand Khemka

Shri Rajesh Birla

Shri Ram Avatar Jajoo

Shri Vishvanath Khandelwal

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Shri H. B. DesaiManager / CEO

Shri R. N. AgarwalChairman

Shri CA Manish JajooVice Chairman

As per my report of even date

FOR, SOPARIWALA & Co.

Chartered Accountants

FRN No. 132643W

CA Nicky D. Sopariwala

PARTNER

M No 140537

m:tG & mtwh;t

(28)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

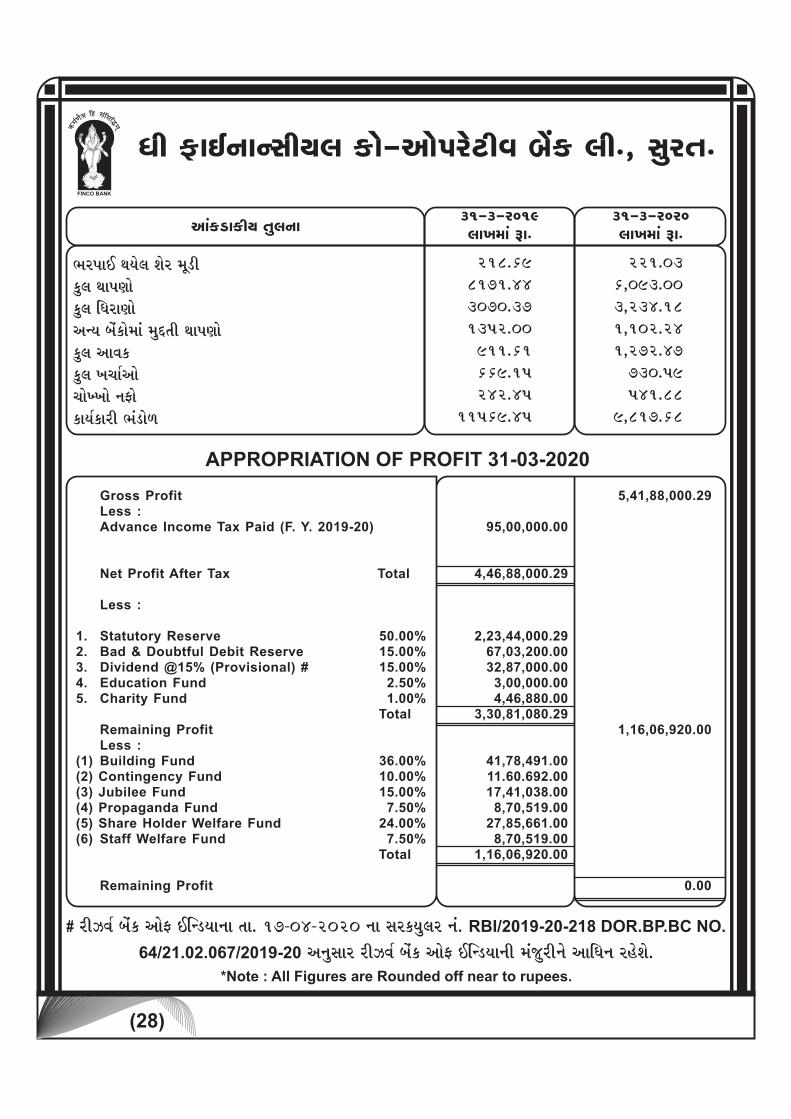

31-3-2020jttFtbttk ~t.ytkfztfegt ;twjtltt

CthvttE :tgtujt Ntuh btqzefwjt :ttvtKttufwjt r"thtKttuylgt ctukftubttk btwÚ;te :ttvtKttufwjt ytJtffwjt FtattoytuattuFFttu ltVtuftgtofthe CtkztuG

221.036,093.003,234.181,102.241,272.47

730.59541.88

9,817.68

APPROPRIATION OF PROFIT 31-03-2020

*Note : All Figures are Rounded off near to rupees.

Gross Profit 5,41,88,000.29 Less : Advance Income Tax Paid (F. Y. 2019-20) 95,00,000.00

Net Profit After Tax Total 4,46,88,000.29 Less :

1. Statutory Reserve 50.00% 2,23,44,000.292. Bad & Doubtful Debit Reserve 15.00% 67,03,200.003. Dividend @15% (Provisional) # 15.00% 32,87,000.004. Education Fund 2.50% 3,00,000.005. Charity Fund 1.00% 4,46,880.00 Total 3,30,81,080.29 Remaining Profit 1,16,06,920.00 Less :(1) Building Fund 36.00% 41,78,491.00(2) Contingency Fund 10.00% 11.60.692.00(3) Jubilee Fund 15.00% 17,41,038.00(4) Propaganda Fund 7.50% 8,70,519.00(5) Share Holder Welfare Fund 24.00% 27,85,661.00(6) Staff Welfare Fund 7.50% 8,70,519.00 Total 1,16,06,920.00 Remaining Profit 0.00

31-3-2019jttFtbttk ~t.

218.698171.443070.371352.00911.61669.15242.45

11569.45

# heLJto ctukf ytuV Erlzgttltt ;tt. 17-04-2020 ltt mthfgtwjth ltk. RBI/2019-20-218 DOR.BP.BC NO.

64/21.02.067/2019-20 yltwmtth heLJto ctukf ytuV Erlzgttlte btkswheltu ytr"tlt hnuNtu.

(29)

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

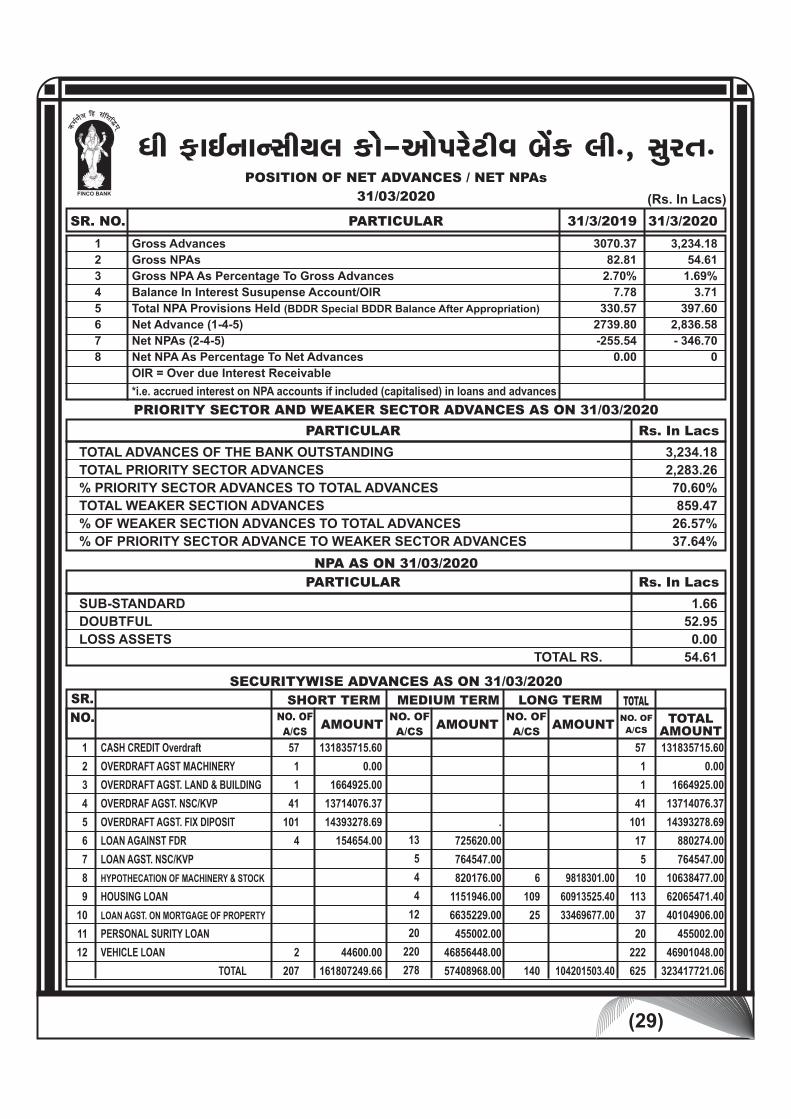

SR. NO. 31/3/2020

POSITION OF NET ADVANCES / NET NPAs

31/03/2020 (Rs. In Lacs)

PARTICULAR

1

2

3

4

5

6

7

8

Gross Advances

Gross NPAs

Gross NPA As Percentage To Gross Advances

Balance In Interest Susupense Account/OIR

Total NPA Provisions Held (BDDR Special BDDR Balance After Appropriation)

Net Advance (1-4-5)

Net NPAs (2-4-5)

Net NPA As Percentage To Net Advances

OIR = Over due Interest Receivable

*i.e. accrued interest on NPA accounts if included (capitalised) in loans and advances

3,234.18

54.61

1.69%

3.71

397.60

2,836.58

- 346.70

0

Rs. In LacsPARTICULAR

TOTAL ADVANCES OF THE BANK OUTSTANDING

TOTAL PRIORITY SECTOR ADVANCES

% PRIORITY SECTOR ADVANCES TO TOTAL ADVANCES

TOTAL WEAKER SECTION ADVANCES

% OF WEAKER SECTION ADVANCES TO TOTAL ADVANCES

% OF PRIORITY SECTOR ADVANCE TO WEAKER SECTOR ADVANCES

3,234.18

2,283.26

70.60%

859.47

26.57%

37.64%

PRIORITY SECTOR AND WEAKER SECTOR ADVANCES AS ON 31/03/2020

SECURITYWISE ADVANCES AS ON 31/03/2020

SR.

NO.

CASH CREDIT Overdraft

OVERDRAFT AGST MACHINERY

OVERDRAFT AGST. LAND & BUILDING

OVERDRAF AGST. NSC/KVP

OVERDRAFT AGST. FIX DIPOSIT

LOAN AGAINST FDR

LOAN AGST. NSC/KVP

HYPOTHECATION OF MACHINERY & STOCK.

HOUSING LOAN

LOAN AGST. ON MORTGAGE OF PROPERTY.

PERSONAL SURITY LOAN

VEHICLE LOAN

TOTAL

1

2

3

4

5

6

7

8

9

10

11

12

57

1

1

41

101

4

2

207

131835715.60

0.00

1664925.00

13714076.37

14393278.69

154654.00

44600.00

161807249.66

13

5

4

4

12

20

220

278

.

725620.00

764547.00

820176.00

1151946.00

6635229.00

455002.00

46856448.00

57408968.00

SHORT TERM MEDIUM TERM LONG TERM

AMOUNTAMOUNTAMOUNTNO. OF

A/CS

NO. OF

A/CS

NO. OF

A/CS

6

109

25

140

9818301.00

60913525.40

33469677.00

104201503.40

TOTALAMOUNT

131835715.60

0.00

1664925.00

13714076.37

14393278.69

880274.00

764547.00

10638477.00

62065471.40

40104906.00

455002.00

46901048.00

323417721.06

TOTAL

57

1

1

41

101

17

5

10

113

37

20

222

625

Rs. In LacsPARTICULAR

SUB-STANDARD

DOUBTFUL

LOSS ASSETS

TOTAL RS.

1.66

52.95

0.00

54.61

NPA AS ON 31/03/2020

NO. OF

A/CS

31/3/2019

3070.37

82.81

2.70%

7.78

330.57

2739.80

-255.54

0.00

(30)

ytvtKtt :ttvtKt'thlte ~t. 5 jttFt mtw"telte ;tbttbt :ttvtKt Deposit Insurance & Credit Guarantee

Corporation «tht Jtebtt:te mtkvtqKto mtwhHte;t Au. ytvtKte ctukf ;thV:te 31 bttato 2020 mtw"teltwk Jtebtt vt{erbtgtbt ~t.

4,23,733/- ;tt. 23-10-2019 ltt htus atqfJttE dtgtwk Au. sulte LuhtuHt ftuvte yt ynuJttjtbttk mttbtujt Au ;tubts ;tt. 30

mtvxubcth 2020 mtw"teltwk rvt{btegtbt ~t. 4,31,511/- ;tt. 11-05-2020 ltt htus atwfJtujt Au. sultwk ctejt mttbtujt Au.

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

(31)

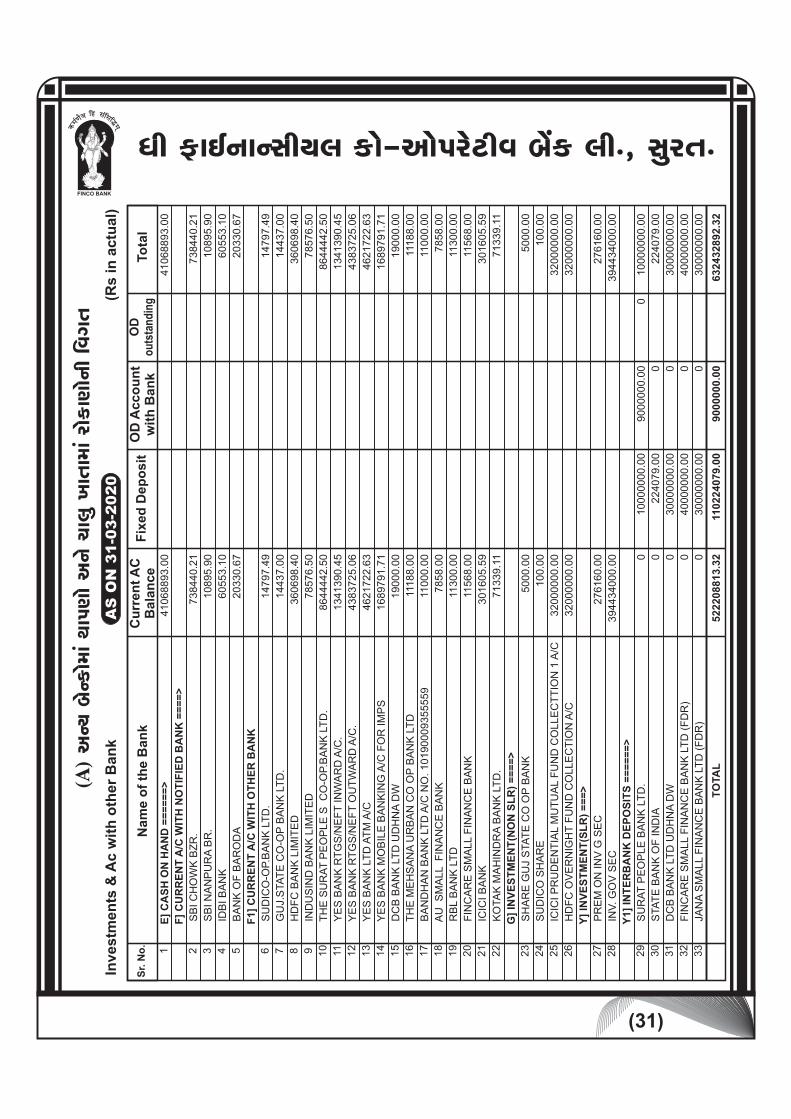

"te VtElttlmtegtjt ftu-ytuvthuxeJt ctukf jte., mtwh;t.

(A) y

lgt ct

ulftubttk

:ttvt

Kttu y

ltu a

ttjtw Ft

t;ttb

ttk ht

uftK

ttulte

rJtdt

;tIn

ve

stm

en

ts &

Ac w

ith

oth

er

Ban

kA

S O

N 3

1-0

3-2

020

Sr.

No

.N

am

e o

f th

e B

an

kF

ixed

Dep

osit

OD

Acco

un

tw

ith

Ban

kTo

tal

OD

o

uts

tan

din

g

E]

CA

SH

ON

HA

ND

==

==

==

>

F]

CU

RR

EN

T A

/C W

ITH

NO

TIF

IED

BA

NK

==

==

>

SB

I C

HO

WK

BZ

R.

SB

I N

AN

PU

RA

BR

.

ID

BI B

AN

K

BA

NK

OF

BA

RO

DA

F1]

CU

RR

EN

T A

/C W

ITH

OT

HE

R B

AN

K

SU

DIC

O-O

P.B

AN

K L

TD

.

GU

J.S

TA

TE

CO

-OP

BA

NK

LT

D.

HD

FC

BA

NK

LIM

ITE

D

IN

DU

SIN

D B

AN

K L

IMIT

ED

TH

E S

UR

AT

PE

OP

LE

S C

O-O

P.B

AN

K L

TD

.

YE

S B

AN

K R

TG

S/N

EF

T IN

WA

RD

A/C

.

YE

S B

AN

K R

TG

S/N

EF

T O

UT

WA

RD

A/C

.

YE

S B

AN

K L

TD

AT

M A

/C

YE

S B

AN

K M

OB

ILE

BA

NK

ING

A/C

FO

R IM

PS

DC

B B

AN

K L

TD

UD

HN

A D

W

TH

E M

EH

SA

NA

UR

BA

N C

O O

P B

AN

K L

TD

BA

ND

HA

N B

AN

K L

TD

A/C

NO

. 10190009355559

AU

S

MA

LL F

INA

NC

E B

AN

K

RB

L B

AN

K L

TD

FIN

CA

RE

SM

ALL F

INA

NC

E B

AN

K

IC

ICI B

AN

K

KO

TA

K M

AH

IND

RA

BA

NK

LT

D.

G]

INV

ES

TM

EN

T(N

ON

SL

R)

==

==

>

SH

AR

E G

UJ

STA

TE

CO

OP

BA

NK

SU

DIC

O S

HA

RE

IC

ICI P

RU

DE

NT

IAL M

UT

UA

L F

UN

D C

OLLE

CT

TIO

N 1

A/C

HD

FC

OV

ER

NIG

HT

FU

ND

CO

LLE

CT

ION

A/C

Y]

INV

ES

TM

EN

T(S

LR

) =

==

>

PR

EM

ON

IN

V G

SE

C

IN

V. G

OV

SE

C

Y1]

INT

ER

BA

NK

DE

PO

SIT

S =

==

==

=>

SU

RA

T P

EO

PLE

BA

NK

LT

D.

STA

TE

BA

NK

OF

IN

DIA

DC

B B

AN

K L

TD

UD

HN

A D

W

FIN

CA

RE

SM

ALL F

INA

NC

E B

AN

K L

TD

(F

DR

)

JA

NA

SM

ALL F

INA

NC

E B

AN

K L

TD

(F

DR

)

1 2 3 4 5 6 7 8 9 10

11 12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

41068893.0

0

738440.2

1

10895.9

0

60553.1

0

20330.6

7

14797.4

9

14437.0

0

360698.4

0

78576.5

0

8644442.5

0

1341390.4

5

4383725.0

6

4621722.6

3

1689791.7

1

19000.0

0

11188.0

0

11000.0

0

7858.0

0

11300.0

0

11568.0

0

301605.5

9

71339.1

1

5000.0

0

100.0

0

32000000.0

0

32000000.0

0

276160.0

0

394434000.0

0

0

0

0

0

0

10000000.0

0

224079.0

0

30000000.0

0

40000000.0

0

30000000.0

0

9000000.0

0 0 0 0 0

0

41068893.0

0

738440.2

1

10895.9

0

60553.1

0

20330.6

7

14797.4

9

14437.0

0

360698.4

0

78576.5

0

8644442.5

0

1341390.4

5

4383725.0

6

4621722.6

3

1689791.7

1

19000.0

0

11188.0

0

11000.0

0

7858.0

0

11300.0

0

11568.0

0

301605.5

9

71339.1

1

5000.0

0

100.0

0

32000000.0

0

32000000.0

0

276160.0

0

394434000.0

0

10000000.0

0

224079.0

0

30000000.0

0

40000000.0

0

30000000.0

0

632432892.3

2

9000000.0

0110224079.0

0

522208813.3

2

TO

TA

L

(Rs

in

ac

tua

l)

Cu

rren

t A

C

Bala

nce

(32)

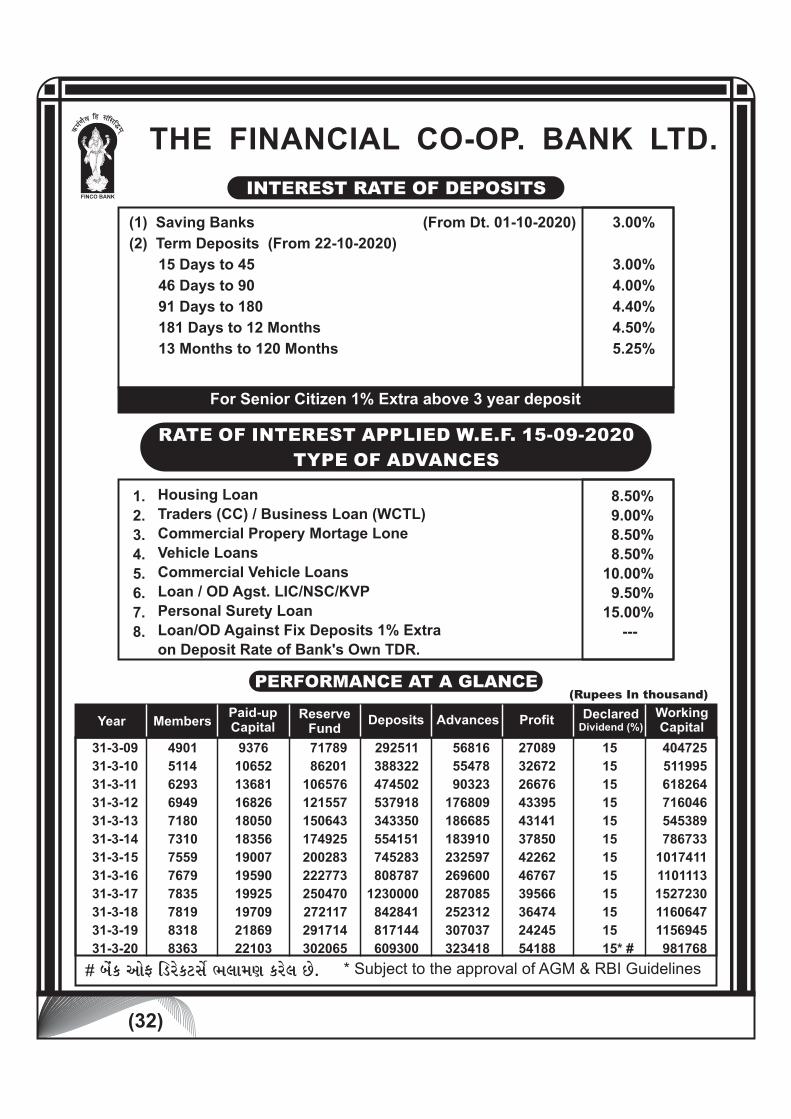

(1) Saving Banks

(2) Term Deposits (From 22-10-2020)

15 Days to 45

46 Days to 90

91 Days to 180

181 Days to 12 Months

13 Months to 120 Months

1.

2.

3.

4.

5.

6.

7.

8.

Housing Loan

Traders (CC) / Business Loan (WCTL)

Commercial Propery Mortage Lone

Vehicle Loans

Commercial Vehicle Loans

Loan / OD Agst. LIC/NSC/KVP

Personal Surety Loan

Loan/OD Against Fix Deposits 1% Extra

on Deposit Rate of Bank's Own TDR.

31-3-09

31-3-10

31-3-11

31-3-12

31-3-13

31-3-14

31-3-15

31-3-16

31-3-17

31-3-18

31-3-19

31-3-20

4901

5114

6293

6949

7180

7310

7559

7679

7835

7819

8318

8363

9376

10652

13681

16826

18050

18356

19007

19590

19925

19709

21869

22103

71789

86201

106576

121557

150643

174925

200283

222773

250470

272117

291714

302065

292511

388322

474502

537918

343350

554151

745283

808787

1230000

842841

817144

609300

RATE OF INTEREST APPLIED W.E.F. 15-09-2020

TYPE OF ADVANCES

* Subject to the approval of AGM & RBI Guidelines

For Senior Citizen 1% Extra above 3 year deposit

# ctukf ytuV rzhufxmtuo CtjttbtKt fhujt Au.

(From Dt. 01-10-2020) 3.00%

3.00%

4.00%

4.40%

4.50%

5.25%

8.50%

9.00%

8.50%

8.50%

10.00%

9.50%

15.00%

--- .

56816

55478

90323

176809

186685

183910

232597

269600

287085

252312

307037

323418

27089

32672

26676

43395

43141

37850

42262

46767

39566

36474

24245

54188

15

15

15

15

15

15

15

15

15

15

15

15* #

404725

511995

618264

716046

545389

786733

1017411

1101113

1527230

1160647

1156945

981768

![[AIESEC FTU Hanoi] GP Vietnamese](https://static.fdocument.pub/doc/165x107/568c4b681a28ab49169c1283/aiesec-ftu-hanoi-gp-vietnamese.jpg)

![[FTU Presentation][KTDN07] Brands](https://static.fdocument.pub/doc/165x107/587837f11a28ab707b8b498d/ftu-presentationktdn07-brands.jpg)

![[AIESEC FTU AppForm]YourFullName_Class](https://static.fdocument.pub/doc/165x107/577d38741a28ab3a6b97d6d1/aiesec-ftu-appformyourfullnameclass.jpg)

![[FTU] Khủng hoảng kinh tế](https://static.fdocument.pub/doc/165x107/589d5aa01a28abef688b5a09/ftu-khung-hoang-kinh-te.jpg)