Presentation to Shareholders - Bank South Pacific sales and service program integrated with our ......

36

Presentation to Shareholders 23 May 2014 Robin Fleming - Group CEO

Transcript of Presentation to Shareholders - Bank South Pacific sales and service program integrated with our ......

Presentation to Shareholders 23 May 2014 Robin Fleming - Group CEO

2

Vision “To be the Leading Bank in PNG and the South Pacific”.

Strategic Imperatives “To maintain, develop, and foster customers that will

deliver value to BSP; through customer care, best employees and innovation, and a continuing contribution to community development”.

3

Strategic Focus 2013

• In 2013 BSP moved from “transformation ” to “implementation”

• BSP has placed a sharper focus on strategically critical areas and cost control measures

• This focus has supported short term results in 2013 and is expected to positively impact future results

4

Strategic Imperatives 2014

• A key component of BSP’s strategy will be a whole of bank sales and service program integrated with our vision, our values, our culture

• Linkage of BSP’s values of integrity, professionalism, leadership, quality, people, and teamwork is intrinsic to embedding a true service and sales culture within BSP

5

Strategic Imperatives 2014

• BSP’s optimal sales and service culture is to place customer satisfaction at the forefront of planning processes and operational activities

• Customer satisfaction should then translate to improved returns for shareholders

• BSP is placing a renewed emphasis on training and career development of staff

• Financial inclusion remains a key objective of Retail bank’s strategy

6

Strategic Imperatives 2014

“Improved customer Sales & Service” will be delivered through market leadership in innovation, technological advances and the modernization of all our systems and procedures, and the continued simplification & automation of all our operational & support processes.

“Appropriately train, develop & reward our staff.”

“Continue our Social & Sporting commitment to people and communities in which we operate.”

7

Financial Performance 2013

8

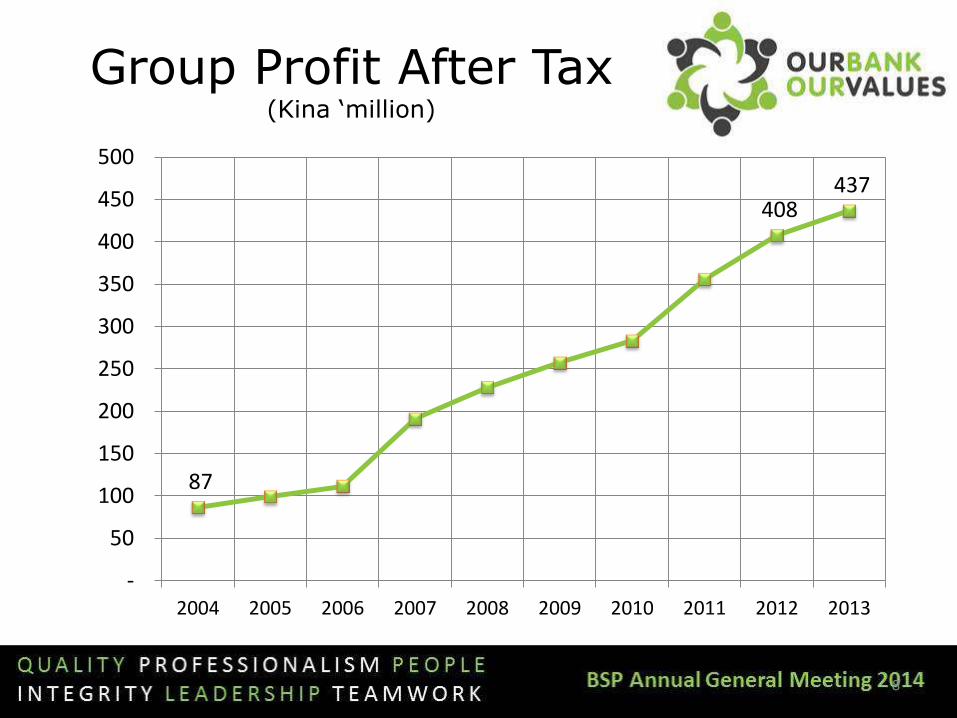

87

408 437

-

50

100

150

200

250

300

350

400

450

500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Group Profit After Tax (Kina ‘million)

9

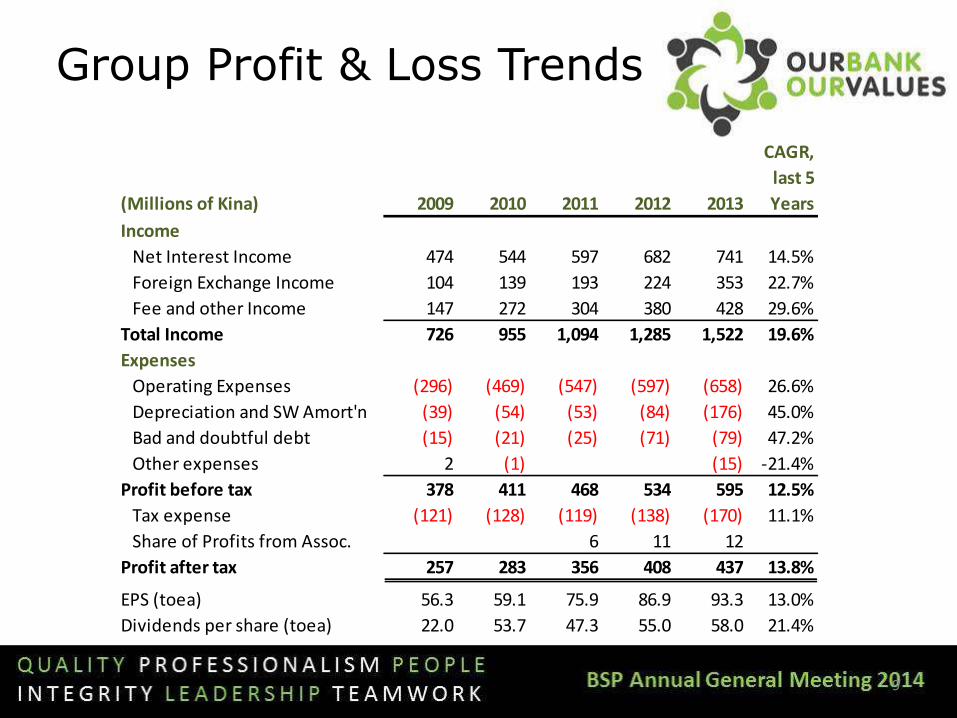

Group Profit & Loss Trends

(Millions of Kina) 2009 2010 2011 2012 2013

CAGR,

last 5

Years

Income

Net Interest Income 474 544 597 682 741 14.5%

Foreign Exchange Income 104 139 193 224 353 22.7%

Fee and other Income 147 272 304 380 428 29.6%

Total Income 726 955 1,094 1,285 1,522 19.6%

Expenses

Operating Expenses (296) (469) (547) (597) (658) 26.6%

Depreciation and SW Amort'n (39) (54) (53) (84) (176) 45.0%

Bad and doubtful debt (15) (21) (25) (71) (79) 47.2%

Other expenses 2 (1) (15) -21.4%

Profit before tax 378 411 468 534 595 12.5%

Tax expense (121) (128) (119) (138) (170) 11.1%

Share of Profits from Assoc. 6 11 12

Profit after tax 257 283 356 408 437 13.8%

EPS (toea) 56.3 59.1 75.9 86.9 93.3 13.0%

Dividends per share (toea) 22.0 53.7 47.3 55.0 58.0 21.4%

10

Group Balance Sheet Trends

(Millions of Kina) 2009 2010 2011 2012 2013

CAGR,

last 5

Years

Assets

Cash & Short Term Deposits 1,188 1,344 1,501 2,134 3,476 37.1%

Loans & Advances 3,639 4,091 4,301 4,805 5,306 17.8%

Investments 3,886 3,857 4,724 4,861 5,571 10.6%

Fixed Assets + Other Assets 685 735 1,155 1,533 1,455 30.8%

Total Assets 9,398 10,027 11,681 13,333 15,809 18.4%

Liabilities

Customer Deposits 7,494 7,985 9,366 10,861 12,201 16.1%

Non-Lending Provisions 165 95 170 109 143 -0.6%

Other Liabilities 805 813 801 898 1,845 68.9%

Total Liabilities 8,464 8,893 10,337 11,867 14,190 18.5%

Shareholder Equity 934 1,134 1,344 1,466 1,619 16.8%

11

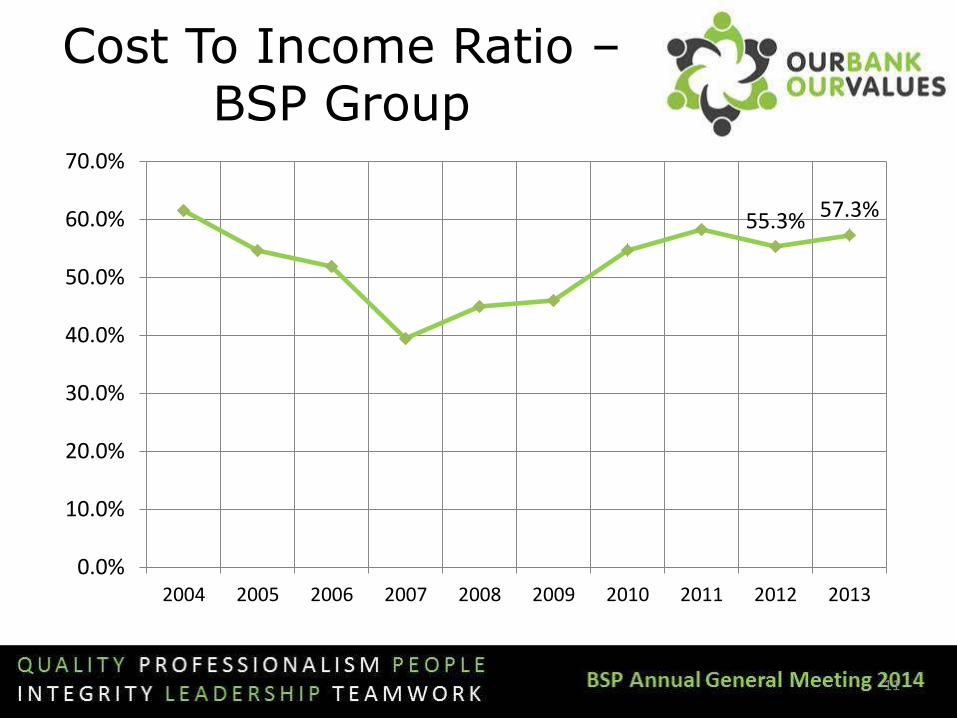

Cost To Income Ratio – BSP Group

55.3% 57.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

12

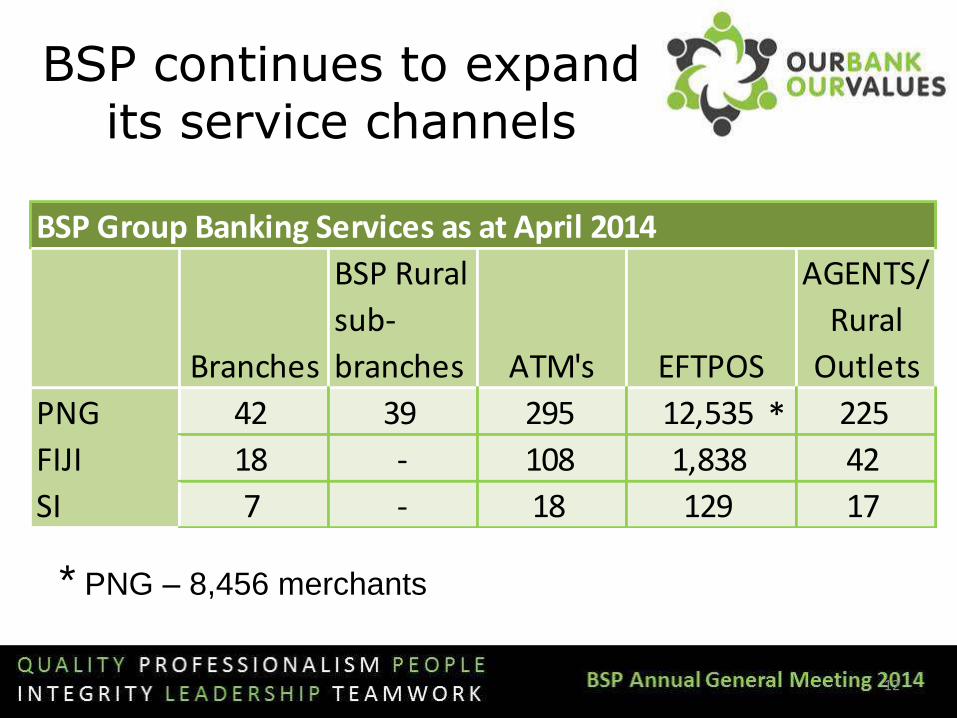

* PNG – 8,456 merchants

BSP continues to expand its service channels

BSP Group Banking Services as at April 2014

Branches

BSP Rural

sub-

branches ATM's EFTPOS

AGENTS/

Rural

Outlets

PNG 42 39 295 12,535 225

FIJI 18 - 108 1,838 42

SI 7 - 18 129 17

*

13

0

200

400

600

800

1,000

1,200

1,400

1,600

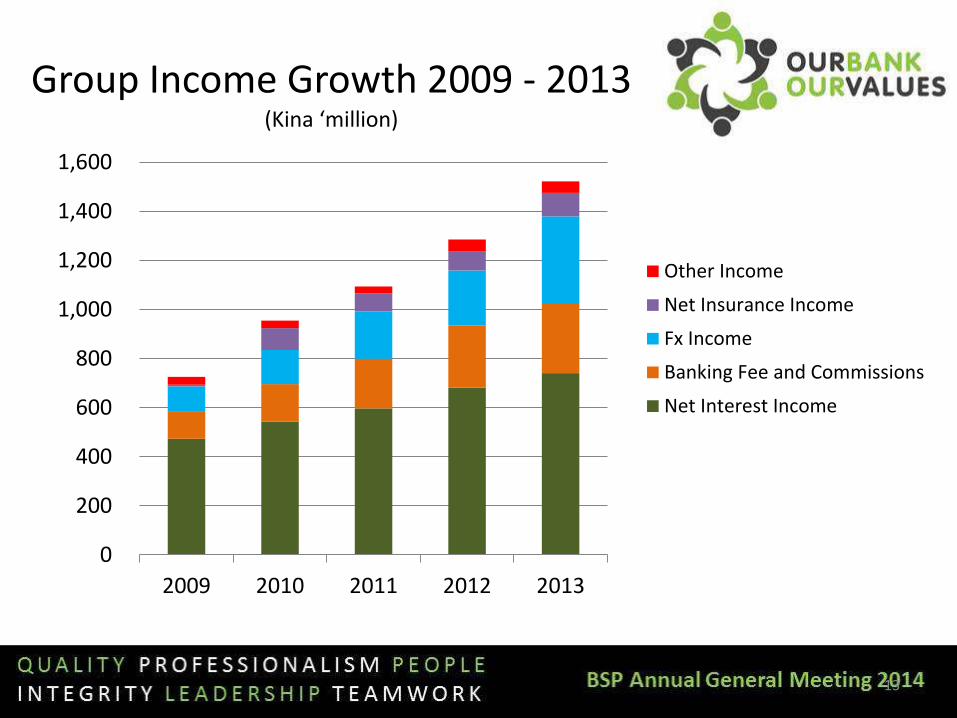

2009 2010 2011 2012 2013

Group Income Growth 2009 - 2013 (Kina ‘million)

Other Income

Net Insurance Income

Fx Income

Banking Fee and Commissions

Net Interest Income

14

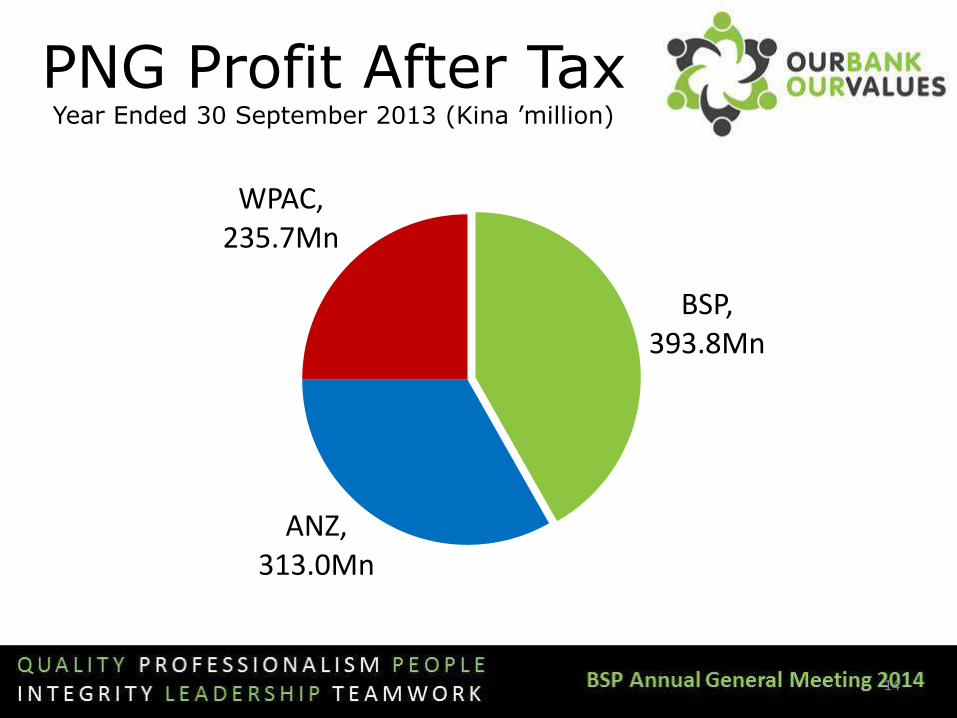

PNG Profit After Tax Year Ended 30 September 2013 (Kina ’million)

BSP, 393.8Mn

ANZ, 313.0Mn

WPAC, 235.7Mn

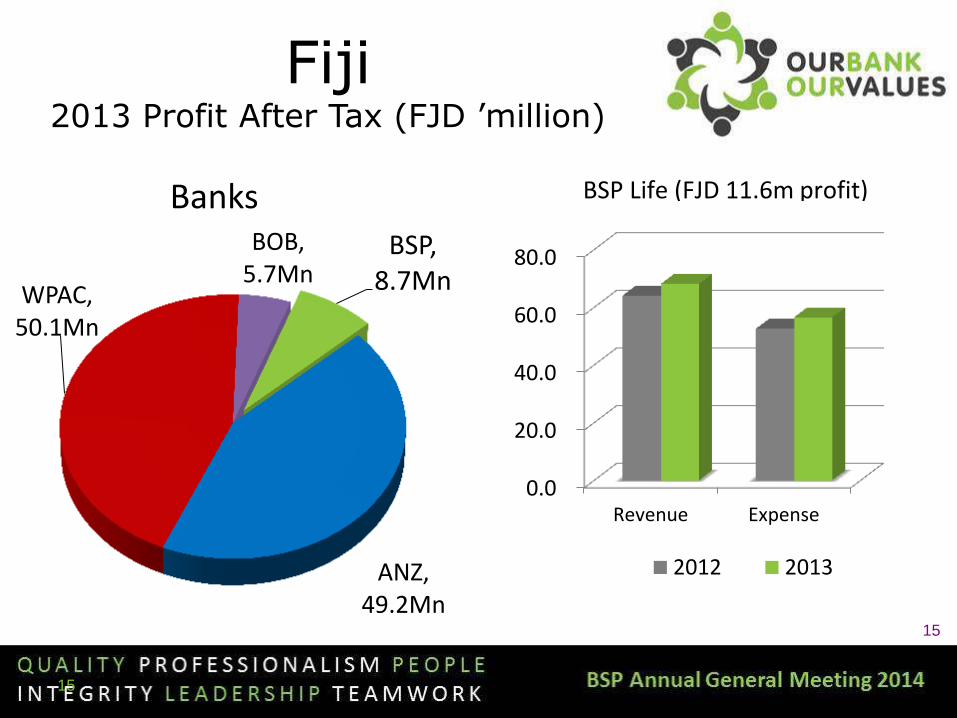

Fiji 2013 Profit After Tax (FJD ’million)

15

15

Banks BSP,

8.7Mn

ANZ, 49.2Mn

WPAC, 50.1Mn

BOB, 5.7Mn

0.0

20.0

40.0

60.0

80.0

Revenue Expense

2012 2013

BSP Life (FJD 11.6m profit)

16

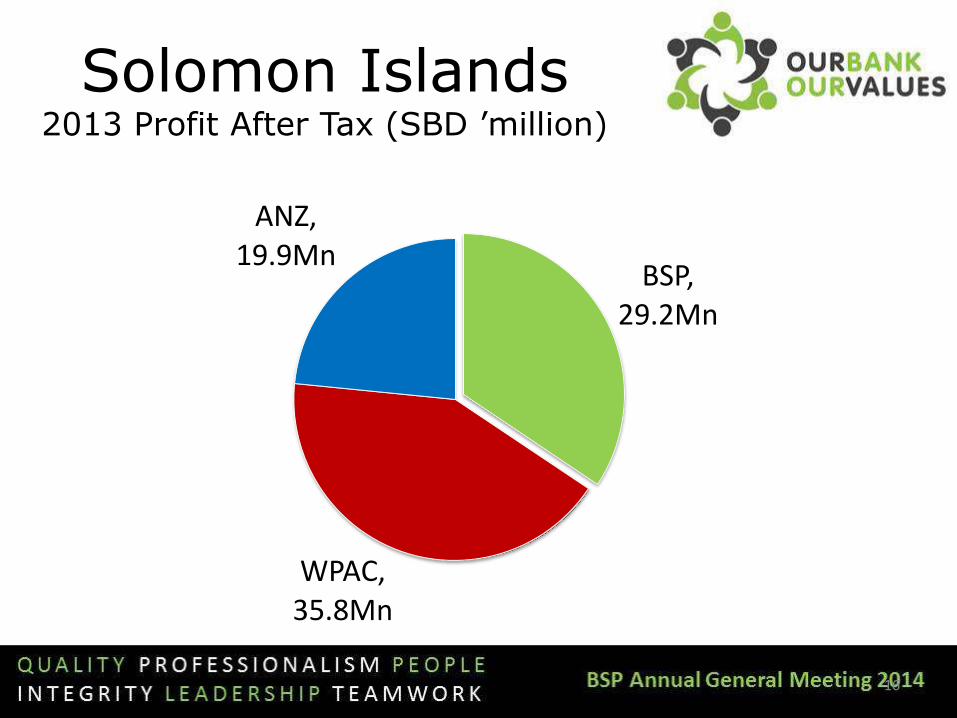

Solomon Islands 2013 Profit After Tax (SBD ’million)

BSP, 29.2Mn

WPAC, 35.8Mn

ANZ, 19.9Mn

17

Group Objectives – Four Themes 1. Financial:

Income growth through serving all segments (whole of

bank proposition) across all market segments, higher

yielding products; revenue leakage mitigation through

diversification of BSP’s customer base

2. Customer:

Brand preservation, effectively servicing the “unbanked”,

and ensuring retention. Intensifying the Group wide effort

to develop profitable products and channels that our

current and future customers need and want.

18

Group Objectives – Four Themes (cont’d)

3. Operational Excellence:

Continually challenge and improve internal

processes, and realise efficiencies through

technology and other significant investments to

materially reduce cost

4. People:

Foster a culture committed to teamwork and

accountability. Focus on basic skills proficiency,

professionalism, sales culture, outstanding

employment practices

19

BSP’s Core Values Theme of 2014 Managers Conference

BSP’s Core Values are shared by and serve to underpin, guide,

and shape everything we do as we work toward realising the

vision of being the leading bank of the South Pacific

1. Integrity

2. Professionalism

3. Leadership

4. Quality

5. People

6. Teamwork

20

Capital Management

The Capital Base of the

BSP Group exceeds

regulatory standards for an

adequately capitalised bank

• The decrease in the

overall ratio is reflected

in the build up of

capitalised fixed assets,

and in larger holdings of

FC deposits

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2010 2011 2012 2013

Tier 2 Tier 1 Bank PNG requirement

Capital Adequacy

21

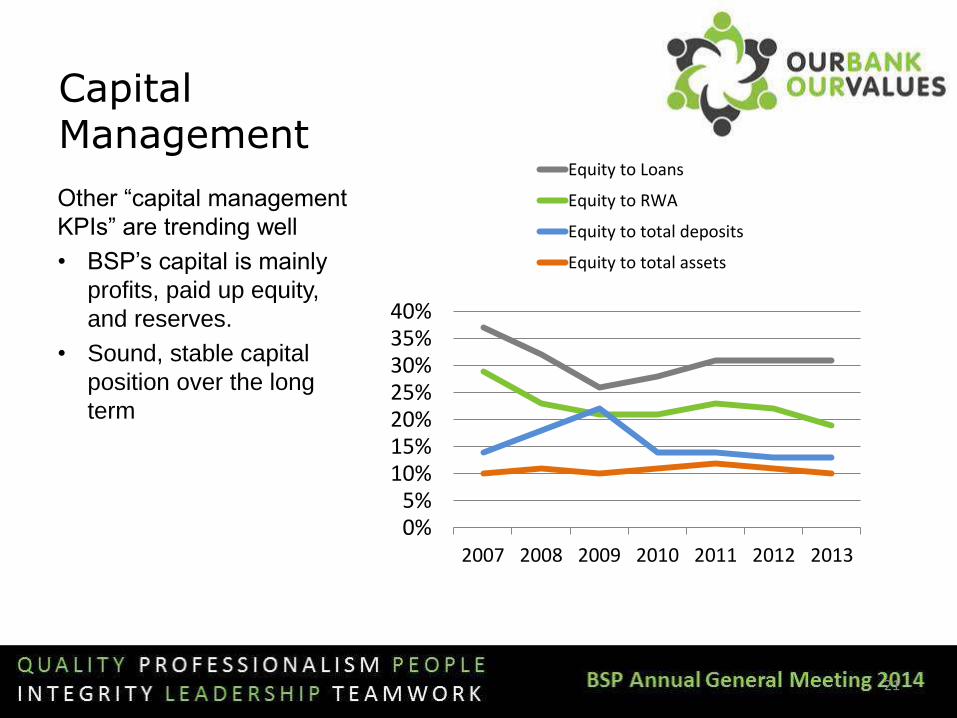

Capital Management

Other “capital management

KPIs” are trending well

• BSP’s capital is mainly

profits, paid up equity,

and reserves.

• Sound, stable capital

position over the long

term

0%5%

10%15%20%25%30%35%40%

2007 2008 2009 2010 2011 2012 2013

Equity to Loans

Equity to RWA

Equity to total deposits

Equity to total assets

22

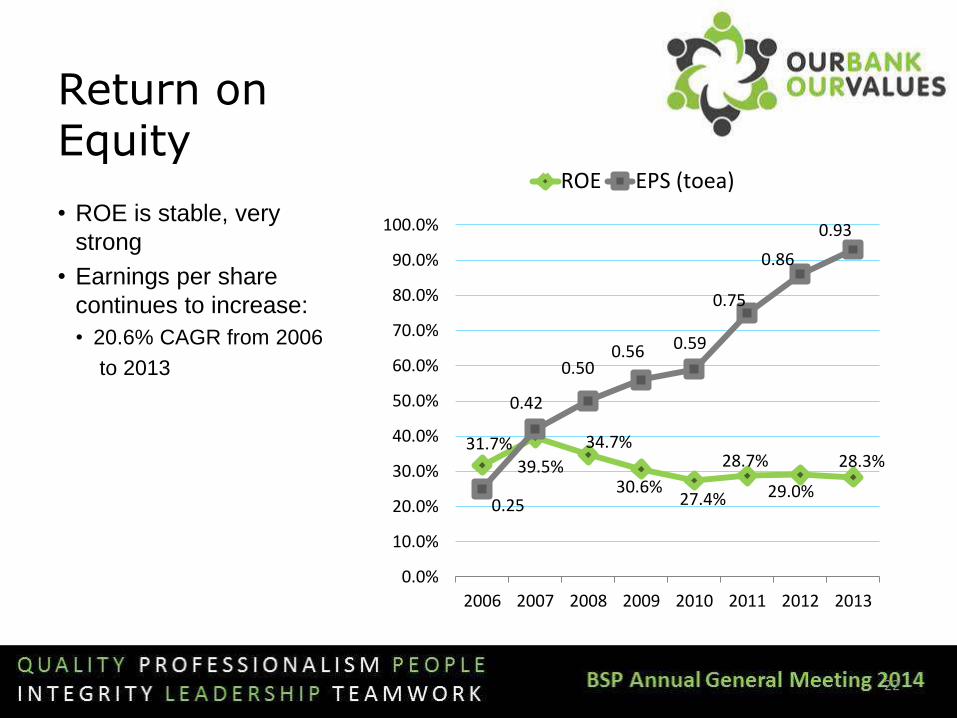

Return on Equity • ROE is stable, very

strong

• Earnings per share

continues to increase:

• 20.6% CAGR from 2006

to 2013

31.7% 39.5%

34.7%

30.6% 27.4%

28.7%

29.0%

28.3%

0.25

0.42

0.50 0.56 0.59

0.75

0.86

0.93

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2006 2007 2008 2009 2010 2011 2012 2013

ROE EPS (toea)

23

Share Price

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

7.00

7.20

7.40

7.60

7.80

8.00

8.20

Dec-11 Apr-12 Aug-12 Dec-12 Apr-13 Aug-13 Dec-13 Apr-14

Share b’back

ceased March

2013

Dec’2011

K7.53

Volume

Traded

in

millions

K3.6bn market

Cap

Share Price K7.78

30th Apr

Share Price

in Kina

24

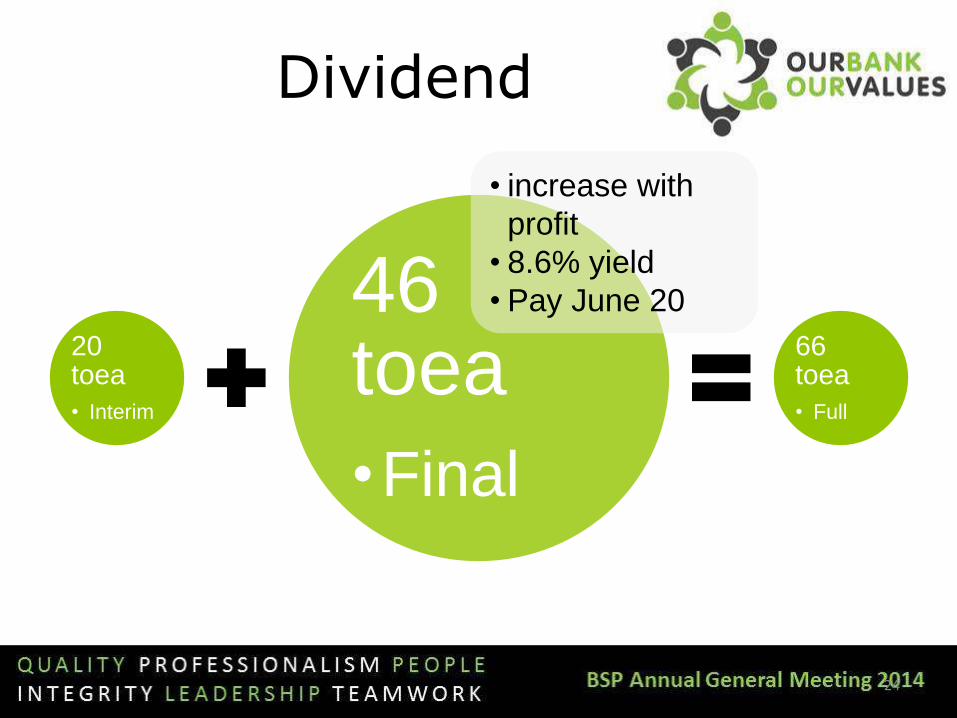

Dividend

20 toea

• Interim

46 toea

•Final

66 toea

• Full

• increase with

profit

• 8.6% yield

• Pay June 20

25

BSP Qtr.1/2014 Results Summary

Johnson Kalo, Group Deputy CEO / Group CFO

Annual General Meeting, May 2014

26

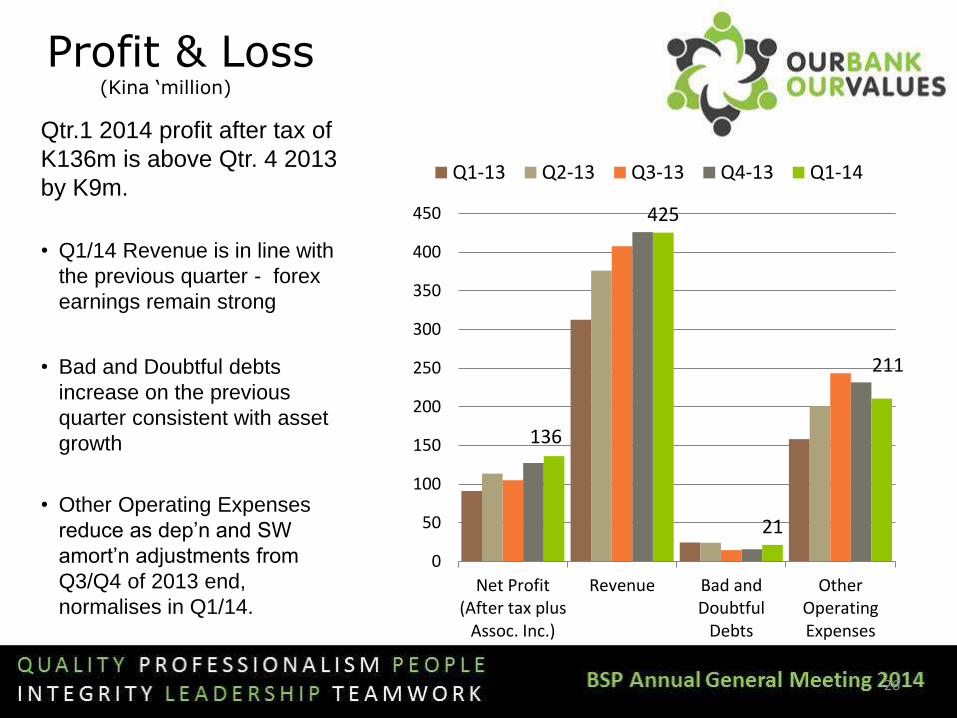

Profit & Loss (Kina ‘million)

Qtr.1 2014 profit after tax of

K136m is above Qtr. 4 2013

by K9m.

• Q1/14 Revenue is in line with

the previous quarter - forex

earnings remain strong

• Bad and Doubtful debts

increase on the previous

quarter consistent with asset

growth

• Other Operating Expenses

reduce as dep’n and SW

amort’n adjustments from

Q3/Q4 of 2013 end,

normalises in Q1/14.

136

425

21

211

0

50

100

150

200

250

300

350

400

450

Net Profit(After tax plus

Assoc. Inc.)

Revenue Bad andDoubtful

Debts

OtherOperatingExpenses

Q1-13 Q2-13 Q3-13 Q4-13 Q1-14

27

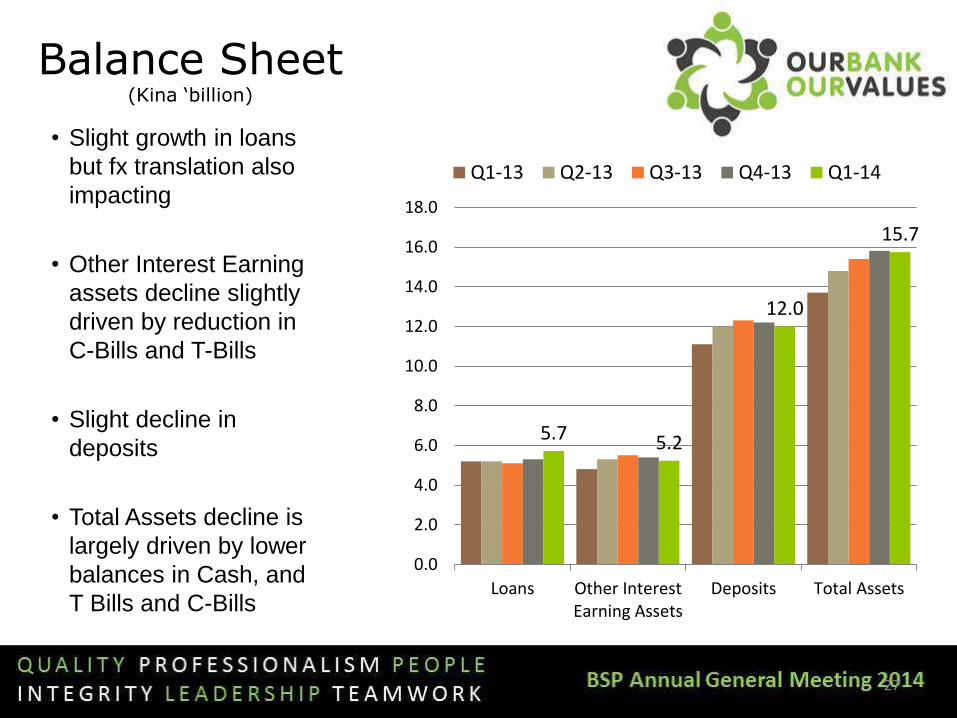

Balance Sheet (Kina ‘billion)

• Slight growth in loans

but fx translation also

impacting

• Other Interest Earning

assets decline slightly

driven by reduction in

C-Bills and T-Bills

• Slight decline in

deposits

• Total Assets decline is

largely driven by lower

balances in Cash, and

T Bills and C-Bills

5.7 5.2

12.0

15.7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Loans Other InterestEarning Assets

Deposits Total Assets

Q1-13 Q2-13 Q3-13 Q4-13 Q1-14

28

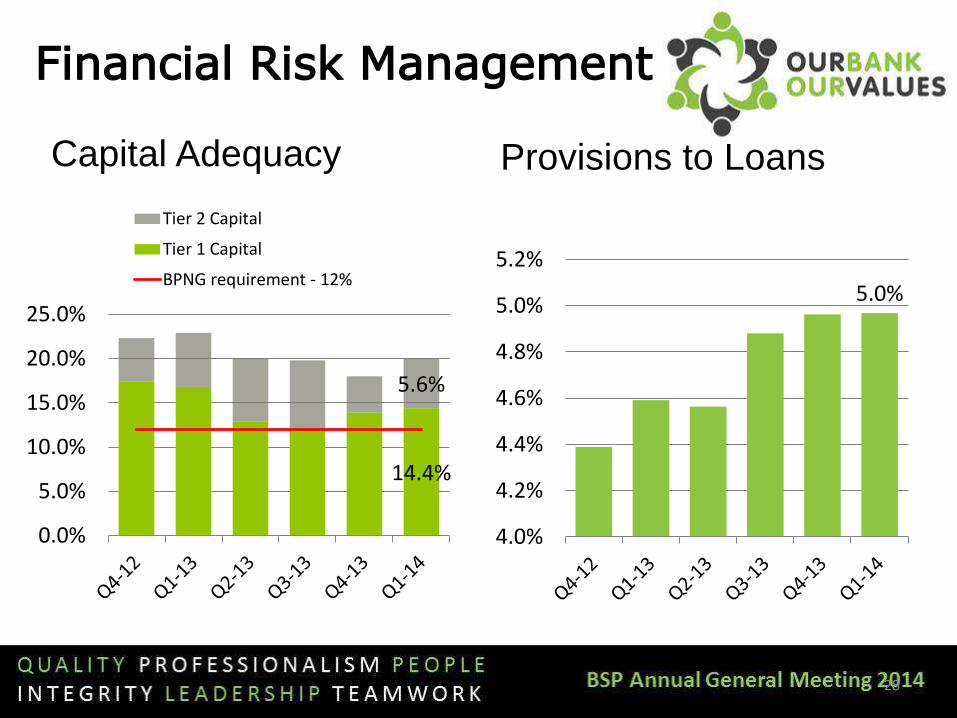

Financial Risk Management

Capital Adequacy Provisions to Loans

5.0%

4.0%

4.2%

4.4%

4.6%

4.8%

5.0%

5.2%

14.4%

5.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Tier 2 Capital

Tier 1 Capital

BPNG requirement - 12%

29

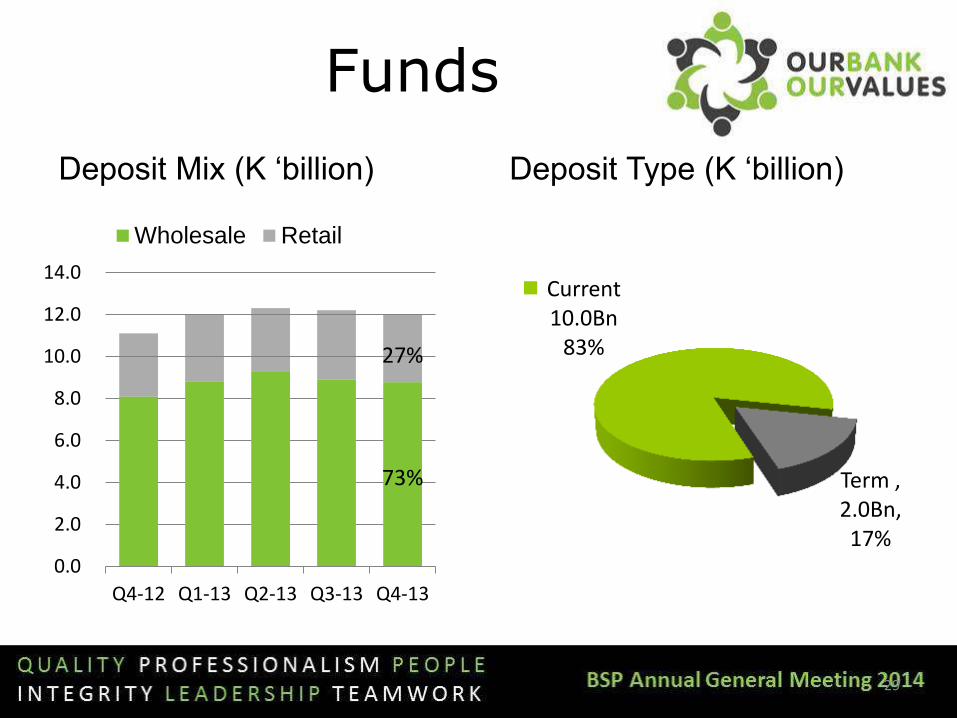

Funds

73%

27%

0%

20%

40%

60%

80%

100%

120%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Q4-12 Q1-13 Q2-13 Q3-13 Q4-13

Wholesale Retail

Current 10.0Bn

83%

Term , 2.0Bn, 17%

Deposit Type (K ‘billion) Deposit Mix (K ‘billion)

30

Qtr.1-2014 Performance Summary

• Revenues – Q1/14 Revenue is in line with the previous quarter -

forex earnings remain strong

– Channel growth continuing with more eftPOS devices

in market

• Balance Sheet – Stable lending market share in PNG

• Capital Adequacy – Improvement in Q1 of 2014 to 20.0%

31

Summary

32

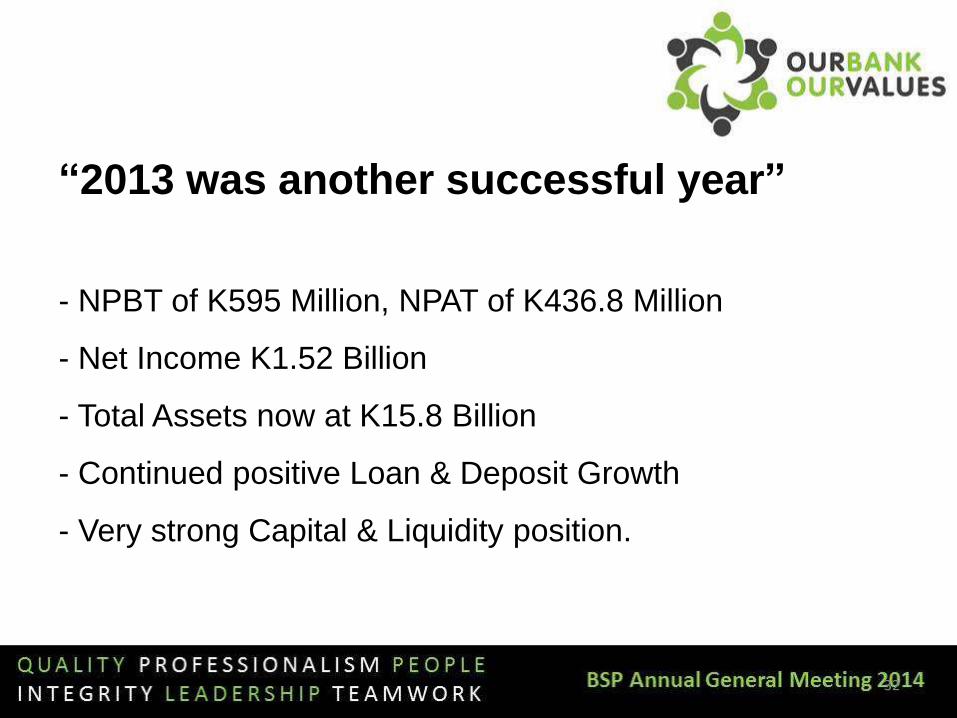

“2013 was another successful year”

- NPBT of K595 Million, NPAT of K436.8 Million

- Net Income K1.52 Billion

- Total Assets now at K15.8 Billion

- Continued positive Loan & Deposit Growth

- Very strong Capital & Liquidity position.

33

• Papua New Guinea continues to be the predominant driver of BSP’s performance

• Strong growth in international services product lines

• Continued growth in net interest income from increased loan assets off-setting margin compression in a more competitive lending market

• Income contribution emerging from BSP’s Mobile Banking suite of products

34

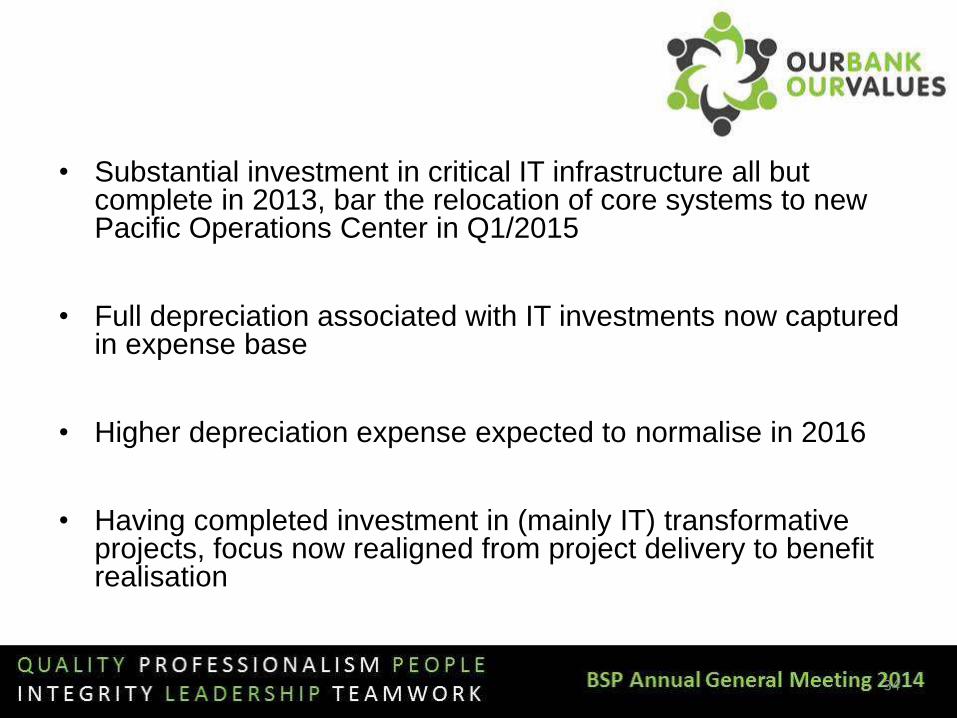

• Substantial investment in critical IT infrastructure all but complete in 2013, bar the relocation of core systems to new Pacific Operations Center in Q1/2015

• Full depreciation associated with IT investments now captured in expense base

• Higher depreciation expense expected to normalise in 2016

• Having completed investment in (mainly IT) transformative projects, focus now realigned from project delivery to benefit realisation

35

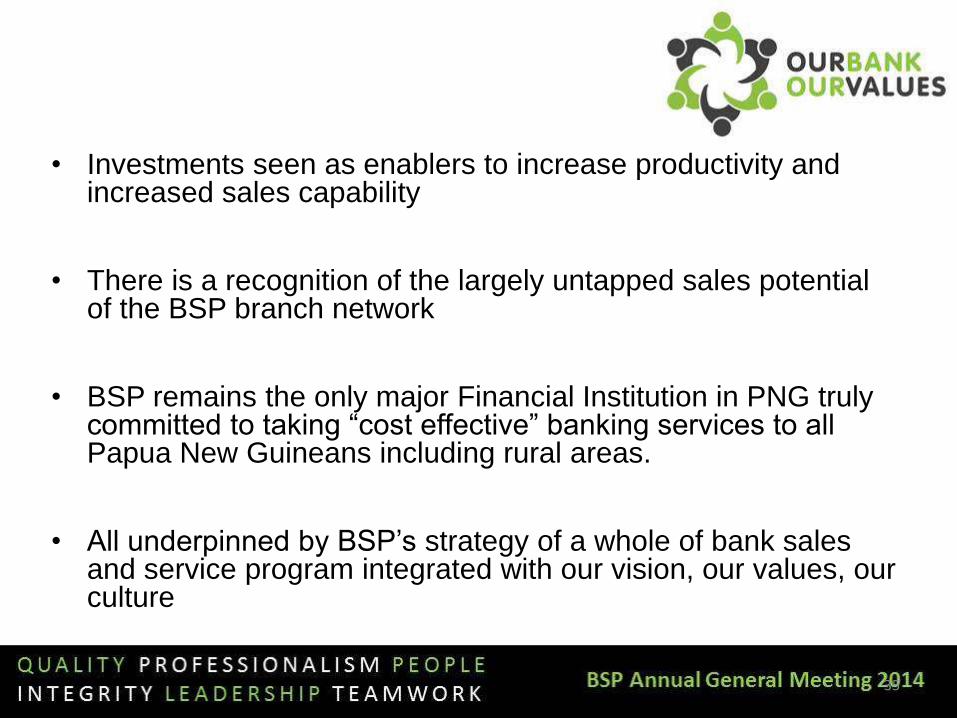

• Investments seen as enablers to increase productivity and increased sales capability

• There is a recognition of the largely untapped sales potential of the BSP branch network

• BSP remains the only major Financial Institution in PNG truly committed to taking “cost effective” banking services to all Papua New Guineans including rural areas.

• All underpinned by BSP’s strategy of a whole of bank sales and service program integrated with our vision, our values, our culture

36

Thank You