![[PPT]Slide 1 - Pendidikan Dokter Unand 2011 | Generation of ... · Web viewDari somit terbentuk jaringan penyambung muda ( mesenkim ), miotom, dan dermatom. Mesenkim selanjutnya berdifferensiasi](https://static.fdocument.pub/doc/165x107/5afcd5d07f8b9aa34d8ca815/pptslide-1-pendidikan-dokter-unand-2011-generation-of-viewdari-somit-terbentuk.jpg)

Poland’s Financial Market: Stability and Security Polski ... · miotom zarzàdzanie ich ryzykiem...

16

• Polish Financial System Stable Polska ma stabilny system finansowy • Polish Banks—T hen and Now Banki wczoraj i dziÊ • Improved Security for Polish Banknotes Nowe zabezpieczenia polskich banknotów Poland’s Financial Market: Stability and Security Polski rynek finansowy jest stabilny i bezpieczny The special section is beeing published in cooperation with Narodowy Bank Polski as part of an education initiative focusing on economic issues Projekt realizowany we wspó∏pracy z Narodowym Bankiem Polskim w ramach programu edukacji ekonomicznej

Transcript of Poland’s Financial Market: Stability and Security Polski ... · miotom zarzàdzanie ich ryzykiem...

• Polish Financial System StablePolska ma stabilny system finansowy

• Polish Banks—Then and NowBanki wczoraj i dziÊ

• Improved Security for Polish BanknotesNowe zabezpieczenia polskich banknotów

Poland’s Financial Market:Stability and Security

Polski rynek finansowy jest stabilny i bezpieczny

The special section is beeing published in cooperation with Narodowy Bank Polski as part of an education initiative focusing on economic issues

Projekt realizowany we wspó∏pracy z Narodowym Bankiem Polskim w ramach programu edukacji ekonomicznej

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

NBP’s latest Financial Stability Report, published inJuly, shows that the Polish financial system

remains stable and its outlook has improved over the last sixmonths. This is important because the stability of the financialsystem is a necessary condition for ensuring sustainable eco-nomic growth. Financial system stability is a situation whenthe system performs its functions in a continuous and efficientway, even when unexpected and adverse disturbances occuron a significant scale. The stability of the banking system is ofparticular importance for financial system stability.

According to the report, “Banks play a crucial role infinancing the economy and settling payments. They also per-form another important function by providing products thatallow other entities to manage their financial risk. Therefore,special emphasis is put on the analysis and assessment ofbanking system stability. Financial system stability is of par-ticular interest to NBP due to its statutory tasks to contributeto the stability of the domestic financial system and to estab-lish the necessary conditions for the development of thebanking system. Financial system stability is closely relatedto the primary task of the central bank, i.e. maintaining pricestability.”

The condition of banks, the largest segment of the finan-cial system, remains good and stable, the report says. Polishbanks have been resilient to significant deterioration in busi-ness conditions. Their average capital adequacy ratiosremained unchanged, and the high capacity to absorbpotential losses has been maintained. The high resilience ofPolish banks has been confirmed by stress tests carried outperiodically by NBP. The banks’ resilience to liquidity shockshas also improved. In the stress tests, a vast majority ofbanks proved to be resilient to even very strong liquidityshocks.

It is also important that the financial results of banks, whichare the primary source of growing capital, remain strong. Thequality of the loan portfolio has improved slightly. “The capitaladequacy ratio for the Polish banking sector is close to theaverage for EU countries, however the sector is characterizedby considerably more conservative risk weights and lowerleverage as well as high quality capital,” the report says.

Other components of the Polish financial system are also ingood shape. The situation of non-bank financial institutions-insurance companies, pension funds and investment funds—is also good and does not pose a risk to the stability of thefinancial system. In addition, interconnectedness betweenthese institutions and banks is insignificant so even if the sec-

tor experienced problems, the risk that these problems woulddirectly carry over to affect other institutions would be limited,the report says.

On the other hand, credit unions (SKOK) are having prob-lems. According to experts at the central bank, the capitalposition of credit unions is difficult and the value of their reg-ulatory capital, despite its growth in 2013, is not adequate totheir operations. Fortunately, the role of credit unions in thePolish financial system is limited. Their assets account foronly 1.4 percent of the banking sector’s total assets. “Due totheir minor share in the financial system and the low scale ofinterconnectedness with other financial institutions, in partic-ular with the banking sector, the condition of credit unionsshould not generate systemic risk,” the NBP report reads.

In addition to the results of financial system risk analysis,the Financial Stability Report contains recommendations onhow to reduce systemic risk and enhance the resilience ofthe Polish financial system. These recommendations applyto both financial system regulation and the financial safetynet, as well as to the condition of individual segments of thesystem.

According to NBP, the resilience of the Polish financial sys-tem could be strengthened further by measures including theestablishment of a Systemic Risk Council—which would workto ensure effective macroprudential supervision of thedomestic financial system—and the introduction to Polish lawof a special recovery and resolution mechanism for banks.

NBP also recommends that banks with a sensitive liquidityposition increase their liquid asset buffers and that banksincreasing lending as the economic situation improves main-tain stable financial leverage. Moreover, the central bank rec-ommends that banks take a cautious approach to the devel-opment of lending to the commercial real estate sector due tosigns of growing imbalances on that market. On the retail andoffice property market there is a growing supply with relative-ly high prices and rents. However, the situation on this marketposes no threat to domestic financial market stability, primar-ily due to the low exposure of domestic financial institutions tothe market, which is characterized by a significant share offoreign funding.

The NBP report also recommends closer integration of thecooperative banking sector and the transformation of associ-ations into institutional protection systems covering liquidityand bank equity. This reaction addresses the issue of lowcost-effectiveness stemming from the small scale of opera-tions of some banks. NBP also recommends that restructur-ing measures continue with a view to improving the opera-tional efficiency of credit unions and increasing their capital.This is to be done alongside the optimal utilization of theinternal resources of the credit unions system, while enhanc-ing the role of the model of strong common bonds amongmembers of each credit union.

The credit union problems identified in the report should notobscure the fact that the Polish financial system is stable andits outlook is improving every year. This is especially importantat a time when many European countries are still strugglingwith the fallout from the financial crisis. A.R.

This article uses content from the NBP website, www.nbp.pl

II

Polish FinancialSystem StablePolish banks are in excellent condition, as confirmedby the results of stress tests examining theirresilience to external negative shocks.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

III

Zopublikowanego w lipcu przez NBP cyklicznego„Raportu o stabilnoÊci systemu finansowego” wyni-ka, ˝e polski system finansowy pozostaje stabilny,

a perspektywy jego funkcjonowania poprawi∏y si´ w ciàguostatniego pó∏rocza. To wa˝ne, gdy˝ utrzymanie stabilno-Êci systemu finansowego jest warunkiem koniecznym dlazrównowa˝onego wzrostu gospodarczego. StabilnoÊçsystemu finansowego to stan, w którym pe∏ni on swojefunkcje w sposób ciàg∏y i efektywny, nawet w przypadkuwystàpienia nieoczekiwanych i niekorzystnych zaburzeƒo znacznej skali. Szczególne znaczenie dla zachowaniastabilnoÊci systemu finansowego ma utrzymanie stabilno-Êci sektora bankowego.

„Banki odgrywajà kluczowà rol´ w finansowaniu gospo-darki i w rozliczeniach pieni´˝nych. Wa˝nà funkcjà bankówjest te˝ tworzenie produktów umo˝liwiajàcych innym pod-miotom zarzàdzanie ich ryzykiem finansowym. Z tych po-wodów szczególnie du˝y nacisk k∏adzie si´ na analiz´i ocen´ stabilnoÊci banków. StabilnoÊç systemu finansowe-go jest przedmiotem szczególnego zainteresowania NBPze wzgl´du na powierzone tej instytucji ustawowe zadaniedzia∏ania na rzecz stabilnoÊci krajowego systemu finanso-wego oraz kszta∏towania warunków niezb´dnych do roz-woju systemu bankowego. StabilnoÊç systemu finansowe-go jest silnie zwiàzana z podstawowym zadaniem bankucentralnego – utrzymaniem stabilnoÊci cen”, czytamy w ko-munikacie NBP.

Wed∏ug autorów raportu, sytuacja banków – najwi´ksze-go segmentu systemu finansowego – pozostaje dobrai stabilna. Banki sà odporne nawet na istotne pogorszeniewarunków ich dzia∏alnoÊci. Ârednie wspó∏czynniki wyp∏a-calnoÊci pozosta∏y bez zmian, a wysoka zdolnoÊç do ab-sorbowania potencjalnych strat zosta∏a utrzymana. Wyso-kà odpornoÊç polskich banków potwierdzi∏y stress-testy,przeprowadzane cyklicznie przez NBP. Nastàpi∏a tak˝e po-prawa odpornoÊci banków na wystàpienie szoków p∏ynno-Êciowych. W testach zdecydowana wi´kszoÊç banków wy-kaza∏a odpornoÊç nawet w warunkach za∏o˝onego bardzosilnego szoku p∏ynnoÊciowego.

Istotne jest te˝ to, ˝e wyniki finansowe banków, b´dàcepodstawowym êród∏em rosnàcych kapita∏ów, wcià˝ pozo-stajà wysokie. Nieznacznie poprawi∏a si´ jakoÊç portfelakredytowego. „Wspó∏czynnik wyp∏acalnoÊci polskiegosektora bankowego jest zbli˝ony do Êredniej dla krajówUE, jednak sektor charakteryzuje si´ zdecydowanie bar-dziej konserwatywnymi wagami ryzyka i ni˝szà dêwignià fi-nansowà oraz wysokà jakoÊcià kapita∏ów”, czytamy w ra-porcie.

Nie tylko polskie banki sà w dobrej kondycji. „Sytuacjaniebankowych instytucji finansowych – zak∏adów ubezpie-czeƒ, funduszy emerytalnych i funduszy inwestycyjnych –

równie˝ jest dobra i nie stwarza ryzyka dla stabilnoÊci sys-temu finansowego. Ponadto zwiàzki mi´dzy tymi instytucja-mi i bankami sà niewielkie, wobec tego nawet gdyby w sek-torze tym wystàpi∏y jakiekolwiek problemy, ryzyko ich bez-poÊredniego przeniesienia na inne instytucje by∏oby ogra-niczone”, piszà autorzy raportu.

Problemy widaç za to w spó∏dzielczych kasach oszcz´d-noÊciowo-kredytowych (SKOK). Wed∏ug ekspertów bankucentralnego, sytuacja kapita∏owa SKOK jest trudna, a wy-sokoÊç funduszy w∏asnych, mimo ich wzrostu w 2013 r.,jest nieadekwatna do prowadzonej dzia∏alnoÊci. Na szcz´-Êcie, znaczenie SKOK w polskim systemie finansowym niejest zbyt du˝e. Ich aktywa odpowiadajà ok. 1,4 proc. akty-wów sektora bankowego. „Ze wzgl´du na ograniczonàskal´ dzia∏alnoÊci oraz niewielkie powiàzania z pozosta∏ymicz´Êciami sektorami finansowego, mimo trudnej sytuacjikapita∏owej SKOK nie generujà ryzyka systemowego”, czy-tamy w komunikacie NBP.

„Raport o stabilnoÊci systemu finansowego” zawiera –obok wyników analiz ryzyka wyst´pujàcego w systemie fi-nansowym – równie˝ rekomendacje, których realizacjaprzyczyni∏aby si´ do ograniczenia ryzyka systemowegoi wzmocnienia odpornoÊci polskiego systemu finansowe-go. Rekomendacje dotyczà zarówno regulacji systemu fi-nansowego i sieci bezpieczeƒstwa finansowego, jak i sytu-acji poszczególnych segmentów tego systemu.

W ocenie NBP do dalszego umocnienia odpornoÊci pol-skiego systemu finansowego przyczyni∏oby si´ m.in. powo-∏anie Rady ds. Ryzyka Systemowego, której uprawnieniazapewnia∏yby skuteczne prowadzenie nadzoru makro-ostro˝noÊciowego nad krajowym systemem finansowym,a tak˝e wprowadzenie do polskiego prawa mechanizmudzia∏aƒ naprawczych oraz restrukturyzacji i uporzàdkowa-nej likwidacji (recovery and resolution) dla banków.

WÊród zaleceƒ NBP znalaz∏o si´ te˝ zwi´kszanie buforówaktywów p∏ynnych przez banki o wra˝liwej pozycji p∏ynno-Êciowej oraz utrzymanie stabilnej dêwigni finansowej przezbanki zwi´kszajàce skal´ akcji kredytowej wraz z poprawàkoniunktury. Zaleca si´ te˝ ostro˝ne podejÊcie banków dorozwoju kredytowania sektora nieruchomoÊci komercyj-nych ze wzgl´du na oznaki narastajàcej nierównowagi natym rynku. Na rynku nieruchomoÊci handlowo-us∏ugowychi biurowych roÊnie poda˝ przy relatywnie wysokim pozio-mie cen i czynszów. Nie stwarza to zagro˝enia dla stabilno-Êci z powodu niskiej ekspozycji krajowych instytucji finan-sowych na rynek, który jest zdominowany przez inwesto-rów zagranicznych.

W raporcie NBP rekomenduje te˝ ÊciÊlejszà integracj´sektora bankowoÊci spó∏dzielczej i przekszta∏cenie zrze-

Polska ma stabilny system finansowyPolskie banki sà w bardzo dobrej kondycji, co potwierdzajà wyniki stress-testów, w których badanajest wra˝liwoÊç banków na wystàpienie skrajnie niekorzystnych warunków.

dokoƒczenie na stronie XVI

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

Of course, the banking sector existed in Polandbefore the country’s transition from commu-nism to a market economy, but it functioned

along completely different lines than today. There wereno private banks on the market and individual state-runfinancial institutions focused on different types of activity.Bank PKO BP provided retail banking services, BankHandlowy handled financial settlements related to foreigntrade and the servicing of Poland’s foreign debt, andBank Pekao SA provided services to Polish citizens livingoutside the country and ran foreign currency accounts forclients at home. Bank Gospodarki ˚ywnoÊciowej, towhich cooperative banks were affiliated, specialized inproviding services to state-owned farms (PGRs) andagri-food processing enterprises such as Hortex. In addi-tion, in 1986, Bank Rozwoju Eksportu was established asa specialized “export development bank.” The customerservice standards and banking procedures at the timehad little in common with banking in developed marketeconomies.

Fully-fledged banking did not begin in Poland until 1989,though reforms of the country’s banking sector had start-ed a few years earlier. In 1986-1987, work began on areform of the Polish central bank—Narodowy BankPolski—and the entire banking system, and measureswere taken to restore the credibility of the national curren-cy, the zloty. As a result of the reforms, Narodowy BankPolski (NBP) was given the role of the central bank,responsible for the value of the Polish currency.

The work of building the Polish banking system was noteasy, and the models included the American and Frenchsystems. The first step was the formation of nine regionalbanks from the central bank to subsequently become thebackbone of commercial banking in Poland. These nineregional banks were the following: Bank Gdaƒski, BankÂlàski in Katowice, Bank Przemys∏owo-Handlowy inCracow, Powszechny Bank Gospodarczy in ¸ódê, BankDepozytowo-Kredytowy in Lublin, Wielkopolski BankKredytowy in Poznaƒ, Pomorski Bank Kredytowy inSzczecin, Paƒstwowy Bank Kredytowy in Warsaw, andBank Zachodni in Wroc∏aw. Each was provided with a net-work of branches inherited from NBP. The banks werelocated in Poland’s biggest cities. In 1993, a 10th univer-sal bank emerged, Polski Bank Inwestycyjny, which was

later taken over by Kredyt Bank. In an especially importantmove, Poland’s largest bank, PKO BP, as well as BankHandlowy and Bank Pekao were given a certain degree ofautonomy. The emergence of a modern banking systemin the form it has in Poland today would not have beenpossible without passing laws enabling the establishmentand launch of private commercial banks.

A watershed event was the entry of foreign banks ontothe Polish market, which resulted in increased competitionin the banking sector. As a result of numerous transfor-mations, Poland’s key banks today—with the exception ofBank PKO BP, the largest in the country in terms of rev-enue—are tied to Europe’s largest banks in terms of cap-ital, while Bank Handlowy is owned by Citibank of theUnited States.

Reform of the central bank

Narodowy Bank Polski has played a major role in forgingthe current shape of the Polish banking sector. In the com-munist era, NBP had a monopoly not only on the issuanceof money (as is still the case), but also on granting loansand collecting people’s savings (through PowszechnaKasa Oszcz´dnoÊci /“universal savings bank”/ that it con-trolled). NBP’s activity was dependent on external politicaland administrative decisions, as a result of which intereston loans and deposits, for example, was determined bythe finance minister. However, even under these systemicconditions, NBP performed tasks that helped rationalizethe economy. Examples included the organization of non-cash settlements, servicing the budget and drawing upthe balance of payments.

One of NBP’s greatest achievements in the last quarterof a century was that it restored the Polish currency to itsdue position. In the early 1990s, people in Poland did nothave confidence in the Polish zloty. They kept 75 percentof their assets in dollars, and only 25 percent in zlotys –either in cash or on bank accounts. However, this washardly surprising in a situation when inflation was spiralingout of control. In 1990, prices of consumer goods and ser-vices increased almost sevenfold in Poland (specificallyby 685.8 percent). Combating inflation became a priorityfor NBP. In 1991, price growth decelerated to 170 percent,and by the mid-1990s the authorities had managed to

IV

25 years of change in Poland’s banking sector

Polish Banks—Then and NowIn few areas has the Polish economy changed so immensely in the last quarter of a century as in banking. Almost everything has changed over the past 25 years: the banking system, the banking products, the technologies, and even the appearanceof bank branches.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

V

reduce inflation to 30 percent, which was quite a successby the standards of the time.

With measures taken by institutions, including by thecentral bank, the public’s confidence in both the zloty andthe Polish banking sector grew with each year. The num-ber of bank branches also increased rapidly. According toNBP data, in 1993 there were a total of 1,740 bank outletsthroughout the country, with cooperative banks account-ing for a significant portion of the total number (1,653). Tocompare, today there are around 630 bank outlets inPoland. Thanks to the activities of NBP as well as bankingsupervision authorities and the government, smaller andweaker banks were combined together to form strongerentities. A huge success was that the consolidationprocess was carried out in such a way that it did not neg-atively affect banks’ clients.

Confidence in the zloty on the domestic market wasstrengthened by a redenomination operation carried outin 1995. The value of the new zloty was equal to 10,000old zlotys, as a result of which prices again began to becounted in tens and hundreds rather than millions. Frommid-May 1995 onward, the exchange rate of the zlotybegan to be determined on the foreign exchange market.In June 1995 the zloty became a freely convertible curren-cy according to International Monetary Fund standards.

The position of the Polish central bank within the systemof public institutions was strengthened by the law onNarodowy Bank Polski enacted in 1997 and by the newconstitution, which ensured NBP statutory independenceand created a new body called the Monetary PolicyCouncil, responsible for monetary policy. Banking supervi-sion was put in the hands of the Banking SupervisionCommission, and the General Inspectorate of BankingSupervision, a separate department within NBP, was taskedwith providing this supervision on a day-to-day basis. In thisway the main objectives of NBP became watching over thezloty and working to ensure the stability of the financial sys-tem. “Of all the institutions created since 1989, NBP defi-nitely comes across the best. It has retained its credibilityand operates according to the best standards,” saysMiros∏aw Gronicki, a former finance minister.

In the new system, commercial banks became fullyautonomous institutions operating in a competitive envi-ronment. They gained the freedom to offer various kindsof banking services and to independently set interestrates on deposits and loans. However, they have beenobligated under law to maintain payment liquidity andensure the security of the money entrusted to them byclients. Another important element of the new bankingsystem was the building of institutions to enhance thesecurity of bank clients, such as the Credit InformationBureau (Biuro Informacji Kredytowej) and the BankGuarantee Fund (Bankowy Fundusz Gwarancyjny). Thelatter is tasked with protecting client deposits in the eventof any problems experienced by banks.

According to Krzysztof Pietraszkiewicz, head of thePolish Bank Association (ZBP), today the Polish bankingsector is one of the most modern and safe in the world.

“We have provided the central bank with autonomy, builta solid banking supervision system, and also focused onequity building. In addition, we have launched an efficientinterbank settlement system and a system of financialinformation about clients. We have managed to diversifythis sector. We do not have a sector that would have onlyone owner, whether state or private, or coming from onlyone country. Instead of banking behemoths, we havebanks whose size is optimal, and even potential problemsexperienced by one of them cannot destabilize either thePolish economy or the budget,” Pietraszkiewicz said.

The Polish banking system is regarded as stable andmodern. This is evidenced by the fact that, after a periodof political and economic transition following the end ofcommunism, there was no structural crisis in the bankingsector in Poland. However, it was necessary to restructurestate-owned banks, an operation that was carried out in1993-1996 at the relatively low cost of around 2.5 percentof GDP. Six commercial banks have gone under in Polandsince 1989. Most bank bankruptcies and liquidationsoccurred in the 1990s. The bankruptcy of BankStaropolski was the highest-profile one. Bank KomercyjnyPosnania, Bank Promocji Eksportu Animex, AgrobankS.A., Bydgoski Bank Budownictwa S.A., and Savim Bankalso declared bankruptcy. However, no bank has gonebankrupt in Poland since 2000. A good management sys-tem in banks, a system for exchanging information aboutclients, a conservative approach to business, and well-educated bank staff—all this has made it possible to neu-tralize the fallout of the global financial crisis in recentyears. Polish taxpayers did not have to contribute a singlezloty to rescue banks.

Modern and innovative

State-of-the-art technology has been used extensively inthe process of modernizing Poland’s banking system. Asa result Poland is a pioneer in many banking servicestoday, for example in the field of online payments, espe-cially mobile payments. Huge progress has been made inpayment systems. In the early 1990s just a handful ofPolish banks offered payment cards. Also missing was aninfrastructure for accepting card payments. In 1993, therewere fewer than 50,000 payment cards in circulation inPoland, around 6,800 acceptance devices and fewer than100 ATMs. By the end of last year that had grown to about35 million cards and the annual value of transactionsmade with them was more than PLN 400 billion.

Huge changes have occurred in services for clients.Twenty-five years ago, clients sometimes had to wait sev-eral hours in long lines to get business done at a bank,and transactions were carried out with a considerabledelay. The range of products was modest. Virtually allretail banking was limited to a few kinds of deposits andloans. Today every bank offers dozens of products,including sophisticated investment products. Banks now

continued on page XVI

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

Sektor bankowy w Polsce istnia∏ oczywiÊcie przedtransformacjà ustrojowà, ale funkcjonowa∏ on zu-pe∏nie inaczej ni˝ obecnie. Na rynku nie by∏o ban-

ków prywatnych, a poszczególne paƒstwowe instytucjefinansowe by∏y skoncentrowane na wybranych rodzajachdzia∏alnoÊci. I tak PKO BP prowadzi∏ us∏ugi detaliczne,Bank Handlowy zajmowa∏ si´ rozliczeniami z tytu∏u obro-tów z zagranicà oraz obs∏ugà polskiego d∏ugu zagranicz-nego, a Pekao SA Êwiadczy∏ m.in. us∏ugi dla polskichobywateli zamieszka∏ych poza granicami kraju i prowadzi∏rachunki walutowe Polaków. Z kolei Bank Gospodarki˚ywnoÊciowej, z którym by∏y powiàzane banki spó∏dziel-cze, specjalizowa∏ si´ w obs∏udze przede wszystkim Paƒ-stwowych Gospodarstw Rolnych (PGR) oraz przedsi´-biorstw przetwórstwa rolno-spo˝ywczego, takich jak np.Hortex. Od 1986 r. dzia∏a∏ jeszcze specjalistyczny BankRozwoju Eksportu. OczywiÊcie, ówczesne standardy ob-s∏ugi klientów czy procedury bankowe nie mia∏y wielewspólnego z bankowoÊcià krajów wysoko rozwini´tych.

BankowoÊç z prawdziwego zdarzenia narodzi∏a si´w Polsce po 1989 r., ale sektor bankowy zaczà∏ byç re-formowany ju˝ kilka lat wczeÊniej. W latach 1986-87 roz-pocz´∏y si´ prace nad reformà NBP i ca∏ego systemubankowego, a tak˝e podj´to dzia∏ania majàce na celuprzywrócenie z∏otemu zdolnoÊci pe∏nienia funkcji naro-dowego pieniàdza. Efektem reform by∏o nadanie Naro-dowemu Bankowi Polskiemu roli banku centralnego, od-powiedzialnego za wartoÊç polskiego pieniàdza.

Budowa polskiego systemu bankowego nie by∏a ∏atwa,a wzorce czerpano m.in. z systemów amerykaƒskichi francuskich. Pierwszym krokiem by∏o wydzielenie dzie-wi´ciu banków regionalnych z banku centralnego, któremia∏y stanowiç trzon bankowoÊci komercyjnej w Polsce.By∏y to: Bank Gdaƒski w Gdaƒsku, Bank Âlàski w Katowi-cach, Bank Przemys∏owo-Handlowy w Krakowie, Po-wszechny Bank Gospodarczy w ¸odzi, Bank Depozyto-wo-Kredytowy w Lublinie, Wielkopolski Bank Kredytowyw Poznaniu, Pomorski Bank Kredytowy w Szczecinie,Paƒstwowy Bank Kredytowy w Warszawie, Bank Zachod-ni we Wroc∏awiu. Ka˝dy z nich otrzyma∏ sieç oddzia∏ówstanowiàcych spuÊcizn´ po NBP. Banki by∏y zlokalizowa-ne w najwi´kszych aglomeracjach miejskich Polski.W 1993 roku do ̋ ycia powo∏ano dziesiàty bank uniwersal-ny – Polski Bank Inwestycyjny, który w póêniejszym okre-sie zosta∏ przej´ty przez Kredyt Bank. Bardzo istotne by-

∏o te˝ nadanie pewnej samodzielnoÊci najwi´kszemu pol-skiemu bankowi, czyli PKO BP, a tak˝e Bankowi Handlo-wemu i Pekao. Stworzenie nowoczesnego systemu ban-kowego funkcjonujàcego obecnie w Polsce, nie by∏obymo˝liwe bez przyj´cia ustaw pozwalajàcych na tworzeniei powstawanie prywatnych banków komercyjnych.

Bardzo wa˝nym wydarzeniem by∏o wejÊcie na polskirynek banków zagranicznych, co spowodowa∏o wzrostkonkurencji w sektorze bankowym. W efekcie licznychprzekszta∏ceƒ, obecnie g∏ówne banki w Polsce – oprócznajwi´kszego pod wzgl´dem przychodów PKO BP – sàzale˝ne kapita∏owo od najwi´kszych banków europej-skich. Wyjàtkiem jest Bank Handlowy, którego w∏aÊcicie-lem zosta∏ amerykaƒski Citibank.

Reforma banku centralnego

W tworzeniu obecnego kszta∏tu polskiego sektora ban-kowego du˝à rol´ odegra∏ Narodowy Bank Polski. W go-spodarce socjalistycznej NBP dzia∏a∏ jako monobank.By∏ monopolistà nie tylko w dziedzinie emisji pieniàdza(tak jak jest to obecnie), ale tak˝e udzielania kredytówi gromadzenia oszcz´dnoÊci ludnoÊci (za poÊrednic-twem kontrolowanej Powszechnej Kasy Oszcz´dnoÊci).Jego dzia∏alnoÊç by∏a zale˝na od zewn´trznych decyzjipolitycznych i administracyjnych, czego przejawem by∏onp. to, ˝e oprocentowanie kredytów i depozytów ustala∏minister finansów. Jednak nawet w tych warunkachustrojowych NBP wykonywa∏ zadania, które przyczynia∏ysi´ do racjonalizacji procesu gospodarowania. Przyk∏a-dem takich dzia∏aƒ by∏o organizowanie rozliczeƒ bezgo-tówkowych, a tak˝e obs∏uga bud˝etu czy opracowywa-nie bilansu p∏atniczego.

Jednym z najwi´kszych osiàgni´ç NBP w ostatnimçwierçwieczu by∏o przywrócenie nale˝nej pozycji polskiejwalucie. Na poczàtku lat 90. Polacy nie mieli zaufania doz∏otego. A˝ 75 proc. zasobów trzymali w dolarach, a tyl-ko 25 proc. w gotówce w z∏otych i na rachunkach banko-wych. Trudno jednak by∏o si´ temu dziwiç w sytuacji sza-lejàcej inflacji. W 1990 r. ceny towarów i us∏ug wzros∏yw Polsce prawie siedmiokrotnie (a dok∏adnie o 685,8proc.). Walka z inflacjà sta∏a si´ priorytetem NBP. W 1991roku tempo wzrostu cen spad∏o do 170 proc., a do po∏o-wy lat 90. uda∏o si´ obni˝yç inflacj´ do poziomu 30 proc.,co by∏o wtedy sporym sukcesem.

VI

25 lat transformacji polskiej bankowoÊci

Banki wczoraj i dziÊW niewielu obszarach polska gospodarka przesz∏a w minionym çwierçwieczu tak gwa∏towne zmiany, jak w bankowoÊci. Przez 25 lat zmieni∏o si´ niemal wszystko: system bankowy, produkty, technologie, a nawet wyglàd placówek bankowych.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

VII

Podejmowane m.in. przez bank centralny dzia∏aniasprawi∏y, ˝e z roku na rok w Polsce ros∏o zaufanie obywa-teli zarówno do pieniàdza, jak i do polskiego sektorabankowego. Bardzo szybko ros∏a te˝ liczba placówekbankowych. Wed∏ug danych NBP, w 1993 r. by∏o ich ju˝1740, przy czym znaczna cz´Êç z nich (1653) to by∏y pla-cówki banków spó∏dzielczych. Dla porównania, obecniew Polsce funkcjonuje ok. 630 placówek bankowych.Dzi´ki dzia∏aniom NBP, a tak˝e nadzoru bankowego orazrzàdu mniejsze i s∏absze banki ∏àczy∏y si´ ze sobà, two-rzàc silniejsze organizmy. Ogromnym sukcesem by∏oprzeprowadzenie procesu konsolidacji w sposób, którynie odbi∏ si´ negatywnie na klientach banków.

Zaufanie do z∏otego na rynku wewn´trznym wzmocni-∏a przeprowadzona w 1995 r. operacja denominacji. No-wy z∏oty zyska∏ wartoÊç 10 000 starych, dzi´ki czemu ce-ny zacz´∏y byç liczone znowu w dziesiàtkach i setkach,a nie w milionach. Od po∏owy maja 1995 roku kurs z∏ote-go zaczà∏ kszta∏towaç si´ na rynku walutowym.A w czerwcu 1995 roku z∏oty sta∏ si´ walutà wymienialnàwed∏ug standardu Mi´dzynarodowego Funduszu Walu-towego.

Pozycj´ polskiego banku centralnego w systemie in-stytucji publicznych wzmocni∏y uchwalona w 1997 r.ustawa o NBP i nowa konstytucja, która zapewni∏a muustawowà niezale˝noÊç i zwiàza∏a polityk´ pieni´˝nàz nowym organem – Radà Polityki Pieni´˝nej. Sprawo-wanie nadzoru nad bankami powierzono Komisji Nadzo-ru Bankowego, a jego realizacj´ – Generalnemu Inspek-toratowi Nadzoru Bankowego, wydzielonemu departa-mentowi w strukturze NBP. W ten sposób g∏ównymi cela-mi dzia∏alnoÊci NBP sta∏y si´ dba∏oÊç o z∏otego i czuwa-nie nad stabilnoÊcià systemu finansowego. „Ze wszyst-kich instytucji, które powsta∏y po 1989 r., NBP wypadazdecydowanie najlepiej. Uda∏o si´ stworzyç instytucj´,która zachowa∏a wiarygodnoÊç i dzia∏a wed∏ug najlep-szych standardów”, uwa˝a Miros∏aw Gronicki, by∏y mini-ster finansów.

W nowym systemie banki komercyjne sta∏y si´ instytu-cjami w pe∏ni samodzielnymi, dzia∏ajàcymi na zasadziekonkurencji. Zyska∏y swobod´ w zakresie oferowaniaró˝nego rodzaju us∏ug bankowych, samodzielnego usta-lania wysokoÊci oprocentowania lokat i kredytów itd.Jednak ustawowo zosta∏y zobowiàzane do utrzymywa-nia p∏ynnoÊci p∏atniczej i zapewnienia bezpieczeƒstwapowierzonych im przez klientów pieni´dzy. Wa˝nym ele-mentem nowego systemu bankowego sta∏o si´ te˝ zbu-dowanie instytucji, podnoszàcych poziom bezpieczeƒ-stwa klientów banków, takich jak Biuro Informacji Kredy-towej czy Bankowy Fundusz Gwarancyjny, którego zada-niem jest zabezpieczanie depozytów klientów na wypa-dek ewentualnych problemów banków.

Zdaniem Krzysztofa Pietraszkiewicza, prezesa Zwiàz-ku Banków Polskich (ZBP), obecnie polski sektor banko-wy nale˝y do jednego z najnowoczeÊniejszych i najbez-pieczniejszych na Êwiecie. „ZapewniliÊmy autonomi´bankowi centralnemu, zbudowaliÊmy solidny nadzórbankowy, postawiliÊmy te˝ na budow´ funduszy w∏a-

snych. Ponadto uruchomiliÊmy sprawny system rozli-czeƒ mi´dzybankowych oraz system informacji gospo-darczej o klientach. Uda∏o si´ nam zdywersyfikowaç tensektor. Nie mamy sektora, który mia∏by jednego w∏aÊci-ciela czy to paƒstwowego czy prywatnego lub pocho-dzàcego wy∏àcznie z jednego kraju. Nie mamy molo-chów bankowych, ale banki których wielkoÊç jest opty-malna i nawet ewentualne k∏opoty jednego z nich nie sàw stanie zdestabilizowaç polskiej gospodarki ani bud˝e-tu”, napisa∏ Krzysztof Pietraszkiewicz na portalu ZBP.

Polski system bankowy uchodzi za stabilny i nowocze-sny. Dowodem tego jest to, ˝e po okresie transformacjiustrojowej w Polsce nie by∏o strukturalnego kryzysu ban-kowego. Ale konieczna by∏a restrukturyzacja bankówpaƒstwowych, przeprowadzona w latach 1993-1996,której koszty by∏y relatywnie bardzo niskie i wynios∏y ok.2,5% PKB. W historii Polski upad∏o jak dotàd szeÊç ban-ków komercyjnych. Przy czym do wi´kszoÊci upad∏oÊcii likwidacji banków dosz∏o w latach 90. ubieg∏ego wieku.Za najwi´ksze uchodzi bankructwo Banku Staropolskie-go. Upad∏oÊç og∏osi∏y te˝ Bank Komercyjny Posnania,Bank Promocji Eksportu Animex, Agrobank S.A., Bydgo-ski Bank Budownictwa S.A., Savim Bank. Jednak po ro-ku 2000 na polskim rynku nie odnotowano ju˝ jakiego-kolwiek bankructwa. Dobry system zarzàdzania w ban-kach, system wymiany informacji o klientach, konserwa-tywne podejÊcie do biznesu oraz dobrze przygotowanekadry bankowe pozwoli∏y na zniwelowanie skutków Êwia-towego kryzysu finansowego ostatnich lat. Polski podat-nik nie musia∏ do∏o˝yç ani z∏otego do ratowania banków.

Nowoczesne i innowacyjne

W procesie modernizacji polskiej bankowoÊci wdro˝onobardzo wiele najnowszych technologii. Dlatego obecniePolska jest pionierem w zakresie wielu us∏ug bankowych,chocia˝by w dziedzinie p∏atnoÊci internetowych,a przede wszystkim mobilnych. Ogromny post´p zano-towano te˝ w dziedzinie p∏atnoÊci. Na poczàtku lat 90.tylko kilka polskich banków oferowa∏o karty p∏atnicze.Brakowa∏o tak˝e odpowiedniej infrastruktury technicznejakceptujàcej p∏atnoÊci kartami. W 1993 r. w Polsce by∏oniespe∏na 50 tys. wydanych kart p∏atniczych, ok. 6,8 tys.urzàdzeƒ akceptujàcych oraz mniej ni˝ 100 bankoma-tów. Pod koniec ubieg∏ego roku by∏o ju˝ ok. 35 mln kartp∏atniczych, a roczna wartoÊç dokonywanych nimi trans-akcji przekracza 400 mld z∏.

Olbrzymie zmiany nastàpi∏y w sferze obs∏ugi klientów.25 lat temu, ˝eby za∏atwiç jakàÊ spraw´ w banku trzebaby∏o odczekaç nieraz kilka godzin w d∏ugiej kolejce,a transakcje by∏y przeprowadzane z du˝ym opóênie-niem. Bardzo skromna by∏a te˝ oferta produktowa. Prak-tycznie ca∏a bankowoÊç detaliczna ogranicza∏a si´ dokilku rodzajów lokat i kredytów. Dzisiaj ka˝dy bank oferu-je dziesiàtki produktów, w tym wyrafinowane produkty in-westycyjne. Banki dysponujà zintegrowanymi systemami

dokoƒczenie na stronie XVI

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

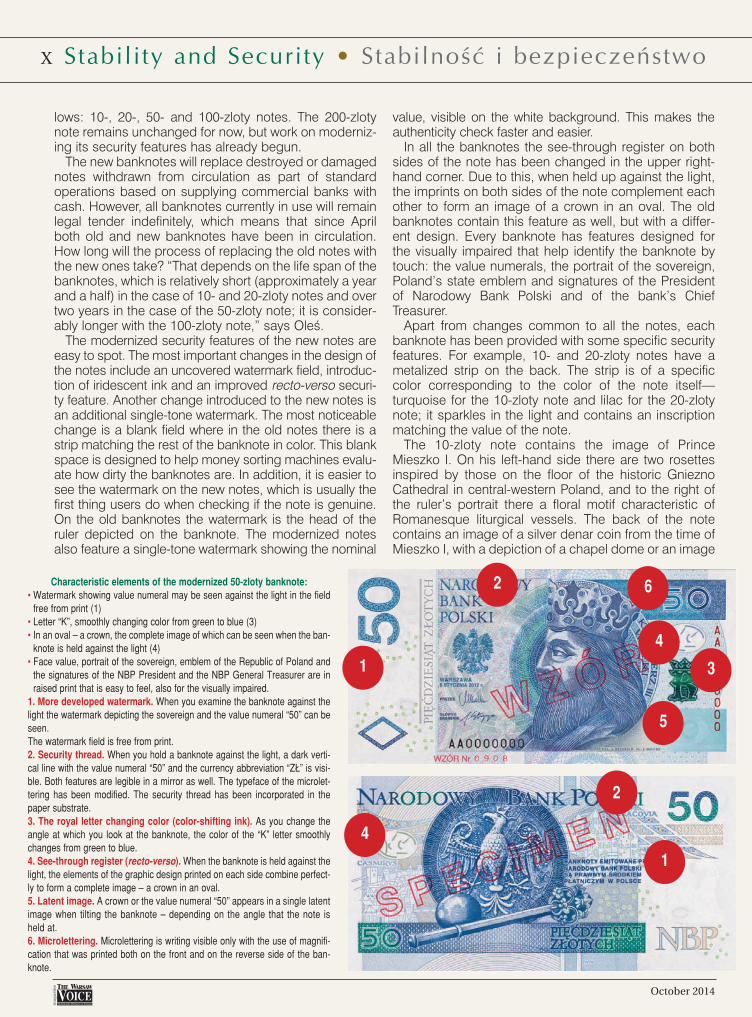

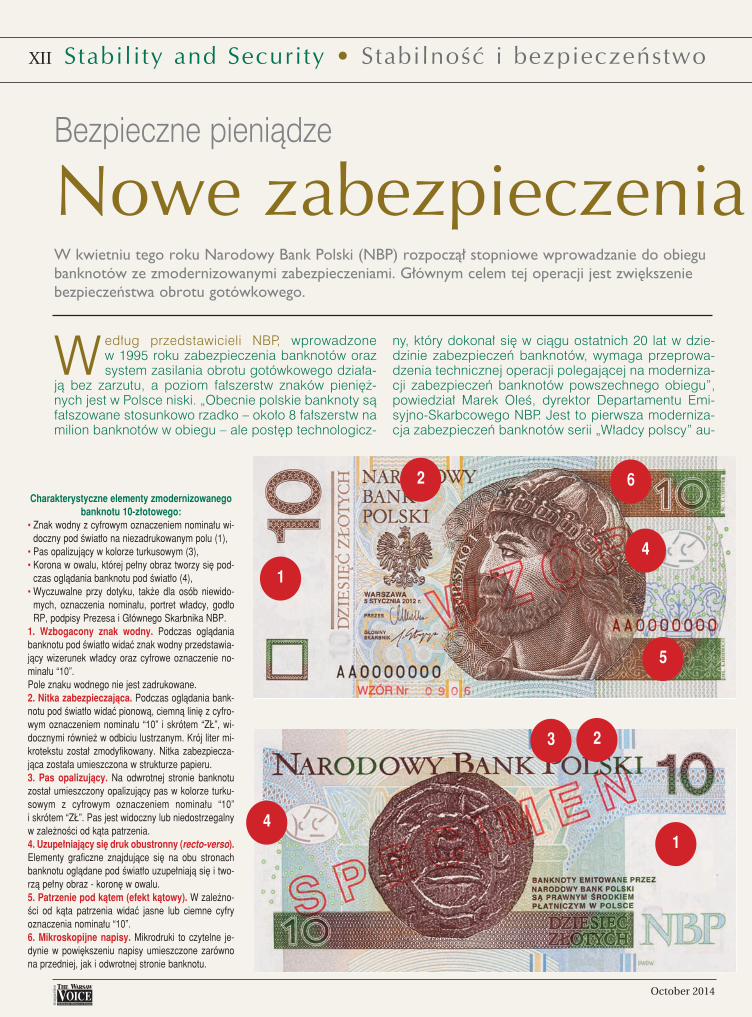

According to NBP, the banknote security features intro-duced in 1995 and the cash circulation system areworking well and the level of forgery is low.

“Counterfeiting is relatively rare in the case of Polish notes—around eight counterfeits per 1 million notes in circulation—but the technological change that has occurred in banknotesecurity over the past 20 years requires modernized securi-

ty measures for notes in general circulation,” said MarekOleÊ, director of NBP’s Cash and Issue Department. This isthe first modernization of the security features of the “PolishRulers” series of banknotes that was designed by AndrzejHeidrich and put into circulation in 1995.

Such measures are nothing unusual. They are carriedout on a regular basis by central banks all over the world.

VIII

Safe Cash

Improved Security for In April this year, Narodowy Bank Polski started the process of gradually replacing old notes with new ones boasting improved security features. The aim is to increasethe security of cash transactions.

1

1

2

23

6

4

4

5

Characteristic elements of the modernized 10-zloty banknote:

• Watermark showing value numeral may be seenagainst the light in the field free from print (1)

• Turquoise-colored iridescent strip (3)• In an oval – a crown, the complete image of which can

be seen when the banknote is held against the light (4)• Face value, portrait of the sovereign, emblem of the

Republic of Poland and the signatures of the NBPPresident and the NBP General Treasurer are inraised print, which is easy to feel, also for the visuallyimpaired.

1. More developed watermark. When you examinethe banknote against the light the watermark depictingthe sovereign and the value numeral “10” can be seen.The watermark field is free from print.2. Security thread. When you hold a banknote againstthe light, a dark vertical line with the value numeral “10”and the currency abbreviation “Z¸” is visible. Both fea-tures are legible in a mirror as well. The typeface of themicrolettering has been modified. The security threadhas been incorporated in the paper substrate.3. Iridescent strip. On the reverse side of the ban-knote there is a turquoise-colored strip with the valuenumeral “10” and “Z¸” symbol. The strip becomes visi-ble depending on the angle at which the banknote isviewed.4. See-through register (recto-verso). When the ban-knote is held against the light, the elements of thegraphic design printed on each side combine perfectlyto form a complete image – a crown in an oval.5. Latent image. A light or dark value numeral “10”appears in a single latent image when tilting the ban-knote – depending on the angle that the note is held at.6. Microlettering. Microlettering is writing visible onlywith the use of magnification that was printed both onthe front and on the reverse side of the banknote.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

IX

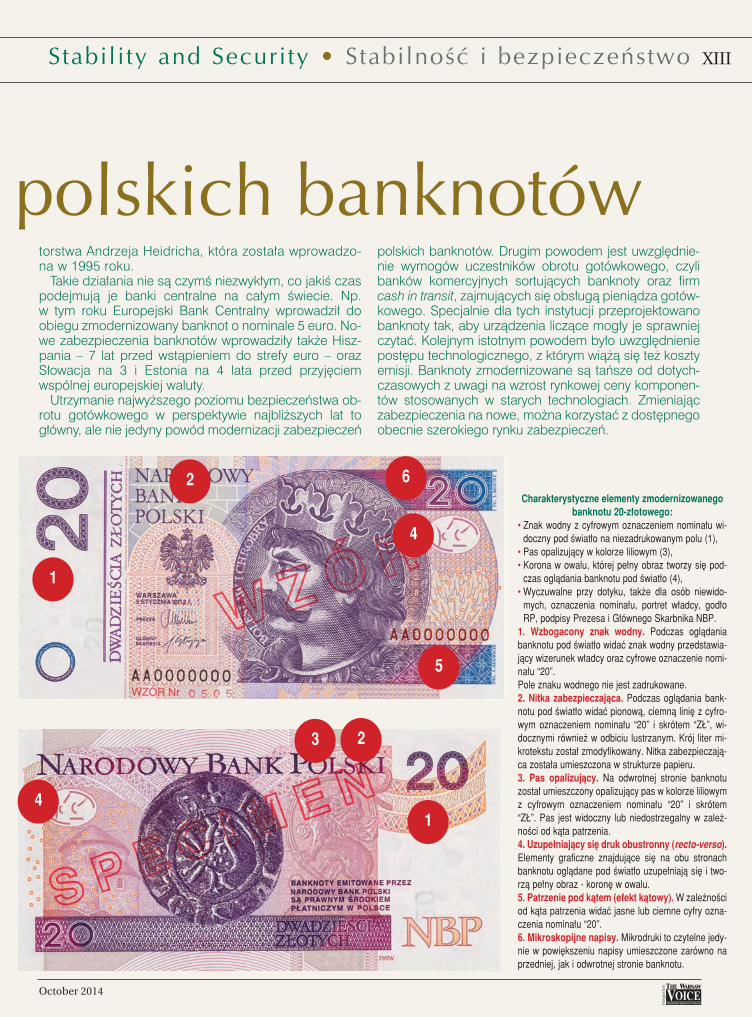

For instance, the European Central Bank issued a mod-ernized 5-euro banknote this year. New banknote securi-ty measures were also introduced by Spain (seven yearsbefore joining the eurozone) as well as Slovakia andEstonia—three and four years prior to adopting the sin-gle European currency respectively.

The maintenance of the highest level of security forcash transactions in the years to come is the main, butnot the only, reason for modernizing security features ofPolish banknotes. Another reason relates to the needs ofcommercial banks and cash-in-transit companies, whichare entrusted with the physical transfer of banknotes andcoins.

Banknotes have been redesigned especially for theseorganizations so that counting machines can work morequickly. Yet another reason is technological change andmoney issuance costs. The modernized notes arecheaper than the old ones owing to higher prices of thematerials used in the old technology. By introducing newsecurity features, NBP may rely on an ample array ofsolutions available on the market.

Changing the security features of banknotes is a pure-ly technical process. The graphic design has remainedunchanged, but the use of new security features explainswhy the differences between the new and old notes arevisible. The notes that have been modernized are as fol-

Polish Banknotes

1

2 6

4

1

23

4

5

Characteristic elements of the modernized 20-zloty banknote:

• Watermark showing value numeral may be seenagainst the light in the field free from print (1)

• Lilac-colored iridescent strip (3)• In an oval – a crown, the complete image of which

can be seen when the banknote is held against thelight (4)

• Face value, portrait of the sovereign, emblem of theRepublic of Poland and the signatures of the NBPPresident and the NBP General Treasurer are inraised print that is easy to feel, also for the visuallyimpaired.

1. More developed watermark. When you examinethe banknote against the light the watermark depictingthe sovereign and the value numeral “20” can beseen.The watermark field is free from print.2. Security thread. When you hold a banknoteagainst the light, a dark vertical line with the valuenumeral “20” and the currency abbreviation “Z¸” is vis-ible. Both features are legible in a mirror as well. Thetypeface of the microlettering has been modified. Thesecurity thread has been incorporated in the papersubstrate.3. Iridescent strip. On the reverse side of the ban-knote there is a lilac strip with the value numeral “20”and “Z¸” symbol. The strip becomes visible dependingon the angle at which the banknote is viewed.4. See-through register (recto-verso). When thebanknote is held against the light, the elements of thegraphic design printed on each side combine perfect-ly to form a complete image – a crown in an oval.5. Latent image. A light or dark value numeral “20”appears in a single latent image when tilting the ban-knote– depending on the angle that the note is held at.6. Microlettering. Microlettering is writing visible onlywith the use of magnification that was printed both onthe front and on the reverse side of the banknote.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

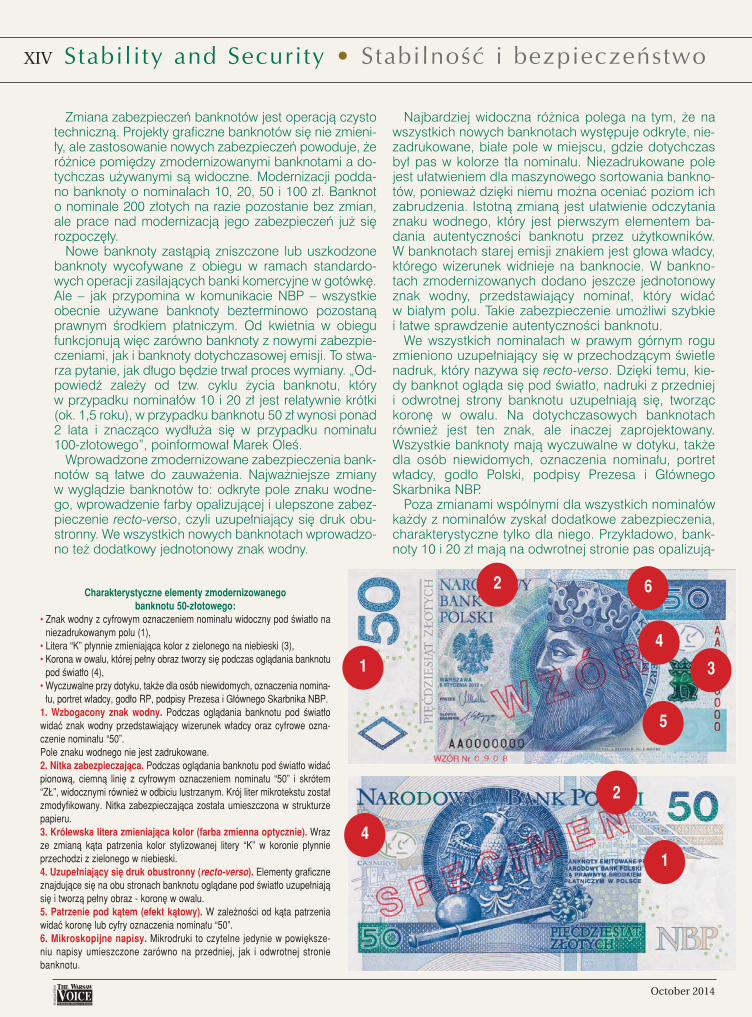

lows: 10-, 20-, 50- and 100-zloty notes. The 200-zlotynote remains unchanged for now, but work on moderniz-ing its security features has already begun.

The new banknotes will replace destroyed or damagednotes withdrawn from circulation as part of standardoperations based on supplying commercial banks withcash. However, all banknotes currently in use will remainlegal tender indefinitely, which means that since Aprilboth old and new banknotes have been in circulation.How long will the process of replacing the old notes withthe new ones take? “That depends on the life span of thebanknotes, which is relatively short (approximately a yearand a half) in the case of 10- and 20-zloty notes and overtwo years in the case of the 50-zloty note; it is consider-ably longer with the 100-zloty note,” says OleÊ.

The modernized security features of the new notes areeasy to spot. The most important changes in the design ofthe notes include an uncovered watermark field, introduc-tion of iridescent ink and an improved recto-verso securi-ty feature. Another change introduced to the new notes isan additional single-tone watermark. The most noticeablechange is a blank field where in the old notes there is astrip matching the rest of the banknote in color. This blankspace is designed to help money sorting machines evalu-ate how dirty the banknotes are. In addition, it is easier tosee the watermark on the new notes, which is usually thefirst thing users do when checking if the note is genuine.On the old banknotes the watermark is the head of theruler depicted on the banknote. The modernized notesalso feature a single-tone watermark showing the nominal

value, visible on the white background. This makes theauthenticity check faster and easier.

In all the banknotes the see-through register on bothsides of the note has been changed in the upper right-hand corner. Due to this, when held up against the light,the imprints on both sides of the note complement eachother to form an image of a crown in an oval. The oldbanknotes contain this feature as well, but with a differ-ent design. Every banknote has features designed forthe visually impaired that help identify the banknote bytouch: the value numerals, the portrait of the sovereign,Poland’s state emblem and signatures of the Presidentof Narodowy Bank Polski and of the bank’s ChiefTreasurer.

Apart from changes common to all the notes, eachbanknote has been provided with some specific securityfeatures. For example, 10- and 20-zloty notes have ametalized strip on the back. The strip is of a specificcolor corresponding to the color of the note itself—turquoise for the 10-zloty note and lilac for the 20-zlotynote; it sparkles in the light and contains an inscriptionmatching the value of the note.

The 10-zloty note contains the image of PrinceMieszko I. On his left-hand side there are two rosettesinspired by those on the floor of the historic GnieznoCathedral in central-western Poland, and to the right ofthe ruler’s portrait there a floral motif characteristic ofRomanesque liturgical vessels. The back of the notecontains an image of a silver denar coin from the time ofMieszko I, with a depiction of a chapel dome or an image

X

1

2

4

1

2 6

4

3

5

Characteristic elements of the modernized 50-zloty banknote:• Watermark showing value numeral may be seen against the light in the field

free from print (1)• Letter “K”, smoothly changing color from green to blue (3)• In an oval – a crown, the complete image of which can be seen when the ban-

knote is held against the light (4)• Face value, portrait of the sovereign, emblem of the Republic of Poland and

the signatures of the NBP President and the NBP General Treasurer are inraised print that is easy to feel, also for the visually impaired.

1. More developed watermark. When you examine the banknote against thelight the watermark depicting the sovereign and the value numeral “50” can beseen.The watermark field is free from print.2. Security thread. When you hold a banknote against the light, a dark verti-cal line with the value numeral “50” and the currency abbreviation “Z¸” is visi-ble. Both features are legible in a mirror as well. The typeface of the microlet-tering has been modified. The security thread has been incorporated in thepaper substrate.3. The royal letter changing color (color-shifting ink). As you change theangle at which you look at the banknote, the color of the “K” letter smoothlychanges from green to blue.4. See-through register (recto-verso). When the banknote is held against thelight, the elements of the graphic design printed on each side combine perfect-ly to form a complete image – a crown in an oval.5. Latent image. A crown or the value numeral “50” appears in a single latentimage when tilting the banknote – depending on the angle that the note isheld at.6. Microlettering. Microlettering is writing visible only with the use of magnifi-cation that was printed both on the front and on the reverse side of the ban-knote.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

XI

of a crown with a small cross. On both sides of the denarthere are images of stylized Romanesque columns fromthe Benedictine abbey in Tyniec, a historic village inPoland and now part of the city of Cracow.

The 20-zloty note contains a portrait of King Boles∏aw Ithe Brave. To the left of the portrait there is an outline ofa Romanesque portal, and to the right—a depiction ofthe crown of an oak tree from the Gniezno Doors—a pairof bronze doors at the entrance to Gniezno Cathedralthat are one of the most significant works ofRomanesque art in Poland. Gniezno is a former capital ofthe Polish state.

The back of the 20-zloty note is adorned with an imageof the silver denar of King Boles∏aw I the Brave with anoutline of a bird and the inscription “Princes Poloniae.”On the left there is an image of the Rotunda of St.Nicholas in Cieszyn, in southern Poland, and to the rightof the portrait is the image of a lion set against the back-ground of a floral ornament from the frame of theGniezno Doors.

The 50-zloty note is ornamented with a portrait of KingKazimierz III the Great. On his right there is a crownedletter “K” from the king’s monogram on the doors ofWawel Cathedral in Cracow, with Gothic ornamentationin the background. The back of the note contains adepiction of the White Eagle from King Kazimierz III theGreat’s royal seal, with the royal insignia—the orb andthe scepter—underneath. In the background, there is apanorama of Cracow and its historical Kazimierz districtfrom a woodcut by Hartmann Schedel, a German travel-

er from the end of the 15th century. The letter “K” is print-ed in a new color. Looking at the banknote from differentangles, it is possible to see how the color of the letterchanges smoothly from green to blue.

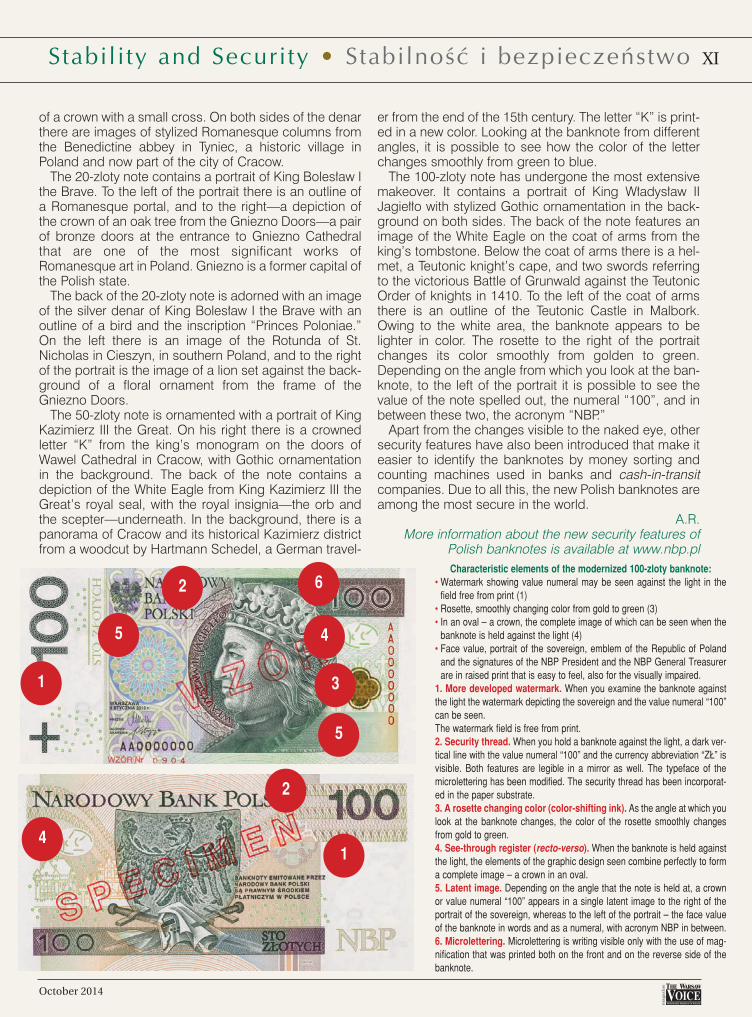

The 100-zloty note has undergone the most extensivemakeover. It contains a portrait of King W∏adys∏aw IIJagie∏∏o with stylized Gothic ornamentation in the back-ground on both sides. The back of the note features animage of the White Eagle on the coat of arms from theking’s tombstone. Below the coat of arms there is a hel-met, a Teutonic knight’s cape, and two swords referringto the victorious Battle of Grunwald against the TeutonicOrder of knights in 1410. To the left of the coat of armsthere is an outline of the Teutonic Castle in Malbork.Owing to the white area, the banknote appears to belighter in color. The rosette to the right of the portraitchanges its color smoothly from golden to green.Depending on the angle from which you look at the ban-knote, to the left of the portrait it is possible to see thevalue of the note spelled out, the numeral “100”, and inbetween these two, the acronym “NBP.”

Apart from the changes visible to the naked eye, othersecurity features have also been introduced that make iteasier to identify the banknotes by money sorting andcounting machines used in banks and cash-in-transitcompanies. Due to all this, the new Polish banknotes areamong the most secure in the world.

A.R.More information about the new security features of

Polish banknotes is available at www.nbp.pl

1

2

4

1

2 6

4

3

5

5

Characteristic elements of the modernized 100-zloty banknote:• Watermark showing value numeral may be seen against the light in the

field free from print (1)• Rosette, smoothly changing color from gold to green (3)• In an oval – a crown, the complete image of which can be seen when the

banknote is held against the light (4)• Face value, portrait of the sovereign, emblem of the Republic of Poland

and the signatures of the NBP President and the NBP General Treasurerare in raised print that is easy to feel, also for the visually impaired.

1. More developed watermark. When you examine the banknote againstthe light the watermark depicting the sovereign and the value numeral “100”can be seen.The watermark field is free from print.2. Security thread. When you hold a banknote against the light, a dark ver-tical line with the value numeral “100” and the currency abbreviation “Z¸” isvisible. Both features are legible in a mirror as well. The typeface of themicrolettering has been modified. The security thread has been incorporat-ed in the paper substrate.3. A rosette changing color (color-shifting ink). As the angle at which youlook at the banknote changes, the color of the rosette smoothly changesfrom gold to green.4. See-through register (recto-verso). When the banknote is held againstthe light, the elements of the graphic design seen combine perfectly to forma complete image – a crown in an oval.5. Latent image. Depending on the angle that the note is held at, a crownor value numeral “100” appears in a single latent image to the right of theportrait of the sovereign, whereas to the left of the portrait – the face valueof the banknote in words and as a numeral, with acronym NBP in between.6. Microlettering. Microlettering is writing visible only with the use of mag-nification that was printed both on the front and on the reverse side of thebanknote.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

Wed∏ug przedstawicieli NBP, wprowadzonew 1995 roku zabezpieczenia banknotów orazsystem zasilania obrotu gotówkowego dzia∏a-

jà bez zarzutu, a poziom fa∏szerstw znaków pieni´˝-nych jest w Polsce niski. „Obecnie polskie banknoty sàfa∏szowane stosunkowo rzadko – oko∏o 8 fa∏szerstw namilion banknotów w obiegu – ale post´p technologicz-

ny, który dokona∏ si´ w ciàgu ostatnich 20 lat w dzie-dzinie zabezpieczeƒ banknotów, wymaga przeprowa-dzenia technicznej operacji polegajàcej na moderniza-cji zabezpieczeƒ banknotów powszechnego obiegu”,powiedzia∏ Marek OleÊ, dyrektor Departamentu Emi-syjno-Skarbcowego NBP. Jest to pierwsza moderniza-cja zabezpieczeƒ banknotów serii „W∏adcy polscy” au-

XII

Bezpieczne pieniàdze

Nowe zabezpieczenia W kwietniu tego roku Narodowy Bank Polski (NBP) rozpoczà∏ stopniowe wprowadzanie do obiegubanknotów ze zmodernizowanymi zabezpieczeniami. G∏ównym celem tej operacji jest zwi´kszeniebezpieczeƒstwa obrotu gotówkowego.

1

1

2

23

6

4

4

5

Charakterystyczne elementy zmodernizowanegobanknotu 10-z∏otowego:

• Znak wodny z cyfrowym oznaczeniem nomina∏u wi-doczny pod Êwiat∏o na niezadrukowanym polu (1),

• Pas opalizujàcy w kolorze turkusowym (3),• Korona w owalu, której pe∏ny obraz tworzy si´ pod-

czas oglàdania banknotu pod Êwiat∏o (4),• Wyczuwalne przy dotyku, tak˝e dla osób niewido-

mych, oznaczenia nomina∏u, portret w∏adcy, god∏oRP, podpisy Prezesa i G∏ównego Skarbnika NBP.

1. Wzbogacony znak wodny. Podczas oglàdaniabanknotu pod Êwiat∏o widaç znak wodny przedstawia-jàcy wizerunek w∏adcy oraz cyfrowe oznaczenie no-mina∏u “10”. Pole znaku wodnego nie jest zadrukowane.2. Nitka zabezpieczajàca. Podczas oglàdania bank-notu pod Êwiat∏o widaç pionowà, ciemnà lini´ z cyfro-wym oznaczeniem nomina∏u “10” i skrótem “Z¸”, wi-docznymi równie˝ w odbiciu lustrzanym. Krój liter mi-krotekstu zosta∏ zmodyfikowany. Nitka zabezpiecza-jàca zosta∏a umieszczona w strukturze papieru.3. Pas opalizujàcy. Na odwrotnej stronie banknotuzosta∏ umieszczony opalizujàcy pas w kolorze turku-sowym z cyfrowym oznaczeniem nomina∏u “10”i skrótem “Z¸”. Pas jest widoczny lub niedostrzegalnyw zale˝noÊci od kàta patrzenia.4. Uzupe∏niajàcy si´ druk obustronny (recto-verso).Elementy graficzne znajdujàce si´ na obu stronachbanknotu oglàdane pod Êwiat∏o uzupe∏niajà si´ i two-rzà pe∏ny obraz - koron´ w owalu.5. Patrzenie pod kàtem (efekt kàtowy). W zale˝no-Êci od kàta patrzenia widaç jasne lub ciemne cyfryoznaczenia nomina∏u “10”.6. Mikroskopijne napisy. Mikrodruki to czytelne je-dynie w powi´kszeniu napisy umieszczone zarównona przedniej, jak i odwrotnej stronie banknotu.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

XIII

torstwa Andrzeja Heidricha, która zosta∏a wprowadzo-na w 1995 roku.

Takie dzia∏ania nie sà czymÊ niezwyk∏ym, co jakiÊ czaspodejmujà je banki centralne na ca∏ym Êwiecie. Np.w tym roku Europejski Bank Centralny wprowadzi∏ doobiegu zmodernizowany banknot o nominale 5 euro. No-we zabezpieczenia banknotów wprowadzi∏y tak˝e Hisz-pania – 7 lat przed wstàpieniem do strefy euro – orazS∏owacja na 3 i Estonia na 4 lata przed przyj´ciemwspólnej europejskiej waluty.

Utrzymanie najwy˝szego poziomu bezpieczeƒstwa ob-rotu gotówkowego w perspektywie najbli˝szych lat tog∏ówny, ale nie jedyny powód modernizacji zabezpieczeƒ

polskich banknotów. Drugim powodem jest uwzgl´dnie-nie wymogów uczestników obrotu gotówkowego, czylibanków komercyjnych sortujàcych banknoty oraz firmcash in transit, zajmujàcych si´ obs∏ugà pieniàdza gotów-kowego. Specjalnie dla tych instytucji przeprojektowanobanknoty tak, aby urzàdzenia liczàce mog∏y je sprawniejczytaç. Kolejnym istotnym powodem by∏o uwzgl´dnieniepost´pu technologicznego, z którym wià˝à si´ te˝ kosztyemisji. Banknoty zmodernizowane sà taƒsze od dotych-czasowych z uwagi na wzrost rynkowej ceny komponen-tów stosowanych w starych technologiach. Zmieniajàczabezpieczenia na nowe, mo˝na korzystaç z dost´pnegoobecnie szerokiego rynku zabezpieczeƒ.

polskich banknotów

1

2 6

4

1

23

4

5

Charakterystyczne elementy zmodernizowanegobanknotu 20-z∏otowego:

• Znak wodny z cyfrowym oznaczeniem nomina∏u wi-doczny pod Êwiat∏o na niezadrukowanym polu (1),

• Pas opalizujàcy w kolorze liliowym (3),• Korona w owalu, której pe∏ny obraz tworzy si´ pod-

czas oglàdania banknotu pod Êwiat∏o (4),• Wyczuwalne przy dotyku, tak˝e dla osób niewido-

mych, oznaczenia nomina∏u, portret w∏adcy, god∏oRP, podpisy Prezesa i G∏ównego Skarbnika NBP.

1. Wzbogacony znak wodny. Podczas oglàdaniabanknotu pod Êwiat∏o widaç znak wodny przedstawia-jàcy wizerunek w∏adcy oraz cyfrowe oznaczenie nomi-na∏u “20”. Pole znaku wodnego nie jest zadrukowane.2. Nitka zabezpieczajàca. Podczas oglàdania bank-notu pod Êwiat∏o widaç pionowà, ciemnà lini´ z cyfro-wym oznaczeniem nomina∏u “20” i skrótem “Z¸”, wi-docznymi równie˝ w odbiciu lustrzanym. Krój liter mi-krotekstu zosta∏ zmodyfikowany. Nitka zabezpieczajà-ca zosta∏a umieszczona w strukturze papieru.3. Pas opalizujàcy. Na odwrotnej stronie banknotuzosta∏ umieszczony opalizujàcy pas w kolorze liliowymz cyfrowym oznaczeniem nomina∏u “20” i skrótem“Z¸”. Pas jest widoczny lub niedostrzegalny w zale˝-noÊci od kàta patrzenia.4. Uzupe∏niajàcy si´ druk obustronny (recto-verso).Elementy graficzne znajdujàce si´ na obu stronachbanknotu oglàdane pod Êwiat∏o uzupe∏niajà si´ i two-rzà pe∏ny obraz - koron´ w owalu.5. Patrzenie pod kàtem (efekt kàtowy). W zale˝noÊciod kàta patrzenia widaç jasne lub ciemne cyfry ozna-czenia nomina∏u “20”.6. Mikroskopijne napisy. Mikrodruki to czytelne jedy-nie w powi´kszeniu napisy umieszczone zarówno naprzedniej, jak i odwrotnej stronie banknotu.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

Zmiana zabezpieczeƒ banknotów jest operacjà czystotechnicznà. Projekty graficzne banknotów si´ nie zmieni-∏y, ale zastosowanie nowych zabezpieczeƒ powoduje, ˝eró˝nice pomi´dzy zmodernizowanymi banknotami a do-tychczas u˝ywanymi sà widoczne. Modernizacji podda-no banknoty o nomina∏ach 10, 20, 50 i 100 z∏. Banknoto nominale 200 z∏otych na razie pozostanie bez zmian,ale prace nad modernizacjà jego zabezpieczeƒ ju˝ si´rozpocz´∏y.

Nowe banknoty zastàpià zniszczone lub uszkodzonebanknoty wycofywane z obiegu w ramach standardo-wych operacji zasilajàcych banki komercyjne w gotówk´.Ale – jak przypomina w komunikacie NBP – wszystkieobecnie u˝ywane banknoty bezterminowo pozostanàprawnym Êrodkiem p∏atniczym. Od kwietnia w obiegufunkcjonujà wi´c zarówno banknoty z nowymi zabezpie-czeniami, jak i banknoty dotychczasowej emisji. To stwa-rza pytanie, jak d∏ugo b´dzie trwa∏ proces wymiany. „Od-powiedê zale˝y od tzw. cyklu ˝ycia banknotu, któryw przypadku nomina∏ów 10 i 20 z∏ jest relatywnie krótki(ok. 1,5 roku), w przypadku banknotu 50 z∏ wynosi ponad2 lata i znaczàco wyd∏u˝a si´ w przypadku nomina∏u100-z∏otowego”, poinformowa∏ Marek OleÊ.

Wprowadzone zmodernizowane zabezpieczenia bank-notów sà ∏atwe do zauwa˝enia. Najwa˝niejsze zmianyw wyglàdzie banknotów to: odkryte pole znaku wodne-go, wprowadzenie farby opalizujàcej i ulepszone zabez-pieczenie recto-verso, czyli uzupe∏niajàcy si´ druk obu-stronny. We wszystkich nowych banknotach wprowadzo-no te˝ dodatkowy jednotonowy znak wodny.

Najbardziej widoczna ró˝nica polega na tym, ˝e nawszystkich nowych banknotach wyst´puje odkryte, nie-zadrukowane, bia∏e pole w miejscu, gdzie dotychczasby∏ pas w kolorze t∏a nomina∏u. Niezadrukowane polejest u∏atwieniem dla maszynowego sortowania bankno-tów, poniewa˝ dzi´ki niemu mo˝na oceniaç poziom ichzabrudzenia. Istotnà zmianà jest u∏atwienie odczytaniaznaku wodnego, który jest pierwszym elementem ba-dania autentycznoÊci banknotu przez u˝ytkowników.W banknotach starej emisji znakiem jest g∏owa w∏adcy,którego wizerunek widnieje na banknocie. W bankno-tach zmodernizowanych dodano jeszcze jednotonowyznak wodny, przedstawiajàcy nomina∏, który widaçw bia∏ym polu. Takie zabezpieczenie umo˝liwi szybkiei ∏atwe sprawdzenie autentycznoÊci banknotu.

We wszystkich nomina∏ach w prawym górnym roguzmieniono uzupe∏niajàcy si´ w przechodzàcym Êwietlenadruk, który nazywa si´ recto-verso. Dzi´ki temu, kie-dy banknot oglàda si´ pod Êwiat∏o, nadruki z przednieji odwrotnej strony banknotu uzupe∏niajà si´, tworzàckoron´ w owalu. Na dotychczasowych banknotachrównie˝ jest ten znak, ale inaczej zaprojektowany.Wszystkie banknoty majà wyczuwalne w dotyku, tak˝edla osób niewidomych, oznaczenia nomina∏u, portretw∏adcy, god∏o Polski, podpisy Prezesa i G∏ównegoSkarbnika NBP.

Poza zmianami wspólnymi dla wszystkich nomina∏ówka˝dy z nomina∏ów zyska∏ dodatkowe zabezpieczenia,charakterystyczne tylko dla niego. Przyk∏adowo, bank-noty 10 i 20 z∏ majà na odwrotnej stronie pas opalizujà-

XIV

1

2

4

1

2 6

4

3

5

Charakterystyczne elementy zmodernizowanego banknotu 50-z∏otowego:

• Znak wodny z cyfrowym oznaczeniem nomina∏u widoczny pod Êwiat∏o naniezadrukowanym polu (1),

• Litera “K” p∏ynnie zmieniajàca kolor z zielonego na niebieski (3),• Korona w owalu, której pe∏ny obraz tworzy si´ podczas oglàdania banknotu

pod Êwiat∏o (4),• Wyczuwalne przy dotyku, tak˝e dla osób niewidomych, oznaczenia nomina-

∏u, portret w∏adcy, god∏o RP, podpisy Prezesa i G∏ównego Skarbnika NBP.1. Wzbogacony znak wodny. Podczas oglàdania banknotu pod Êwiat∏o widaç znak wodny przedstawiajàcy wizerunek w∏adcy oraz cyfrowe ozna-czenie nomina∏u “50”. Pole znaku wodnego nie jest zadrukowane.2. Nitka zabezpieczajàca. Podczas oglàdania banknotu pod Êwiat∏o widaçpionowà, ciemnà lini´ z cyfrowym oznaczeniem nomina∏u “50” i skrótem“Z¸”, widocznymi równie˝ w odbiciu lustrzanym. Krój liter mikrotekstu zosta∏zmodyfikowany. Nitka zabezpieczajàca zosta∏a umieszczona w strukturzepapieru.3. Królewska litera zmieniajàca kolor (farba zmienna optycznie). Wrazze zmianà kàta patrzenia kolor stylizowanej litery “K” w koronie p∏ynnieprzechodzi z zielonego w niebieski.4. Uzupe∏niajàcy si´ druk obustronny (recto-verso). Elementy graficzneznajdujàce si´ na obu stronach banknotu oglàdane pod Êwiat∏o uzupe∏niajàsi´ i tworzà pe∏ny obraz - koron´ w owalu.5. Patrzenie pod kàtem (efekt kàtowy). W zale˝noÊci od kàta patrzenia widaç koron´ lub cyfry oznaczenia nomina∏u “50”.6. Mikroskopijne napisy. Mikrodruki to czytelne jedynie w powi´ksze-niu napisy umieszczone zarówno na przedniej, jak i odwrotnej stroniebanknotu.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

XV

cy. Jest to mieniàcy si´ w Êwietle pas odpowiadajàcykolorowi nomina∏u – turkusowy na banknocie 10-z∏oto-wym i liliowy na 20-z∏otowym – z napisem odpowiada-jàcym danemu nomina∏owi: 10 z∏ i 20 z∏. Banknot o no-minale 10 z∏otych zdobi portret ksi´cia Mieszka I. Z je-go lewej strony przedstawiono dwie rozety inspirowanewzorem z posadzki katedry gnieênieƒskiej, z prawej –roÊlinny motyw spotykany na romaƒskich naczyniach li-turgicznych. Na odwrotnej stronie umieszczono srebrnydenar z wizerunkiem kopu∏y kaplicy lub wyobra˝eniemkorony z krzy˝ykiem. Po obu stronach denara znajdujàsi´ stylizowane kolumny romaƒskie z opactwa bene-dyktynów w Tyƒcu.

Z kolei na banknocie o nominale 20 z∏otych widniejeportret króla Boles∏awa I Chrobrego. Z jego lewej stro-ny znajduje si´ portal romaƒski, zaÊ z prawej – koronam∏odego d´bu z Drzwi Gnieênieƒskich ze sceny wysta-wienia zw∏ok Êw. Wojciecha. Stron´ odwrotnà zdobisrebrny denar Boles∏awa I Chrobrego z sylwetkà ptakai napisem Princes Poloniae. Z lewej strony umieszczo-no wizerunek rotundy Êw. Miko∏aja w Cieszynie, a z pra-wej – lwa rozpi´tego na wici roÊlinnej z obramowaniaDrzwi Gnieênieƒskich.

Banknot o nominale 50 z∏otych zdobi portret króla Ka-zimierza III Wielkiego. Z jego prawej strony widniejeukoronowana litera „K” z monogramu królewskiegoz drzwi katedry na Wawelu, a w tle ornament gotycki.Odwrotnà stron´ zdobi Orze∏ Bia∏y z piecz´ci króla Ka-zimierza III Wielkiego, a poni˝ej widaç ber∏o i jab∏ko –insygnia królewskie. W tle widnieje panorama Krakowa

i Kazimierza z drzeworytu Hartmanna Schedla, podró˝-nika niemieckiego z koƒca XV wieku. Na banknocie 50z∏ nowoÊcià jest zmiana farby, którà wydrukowano kró-lewskà liter´ „K”. Wraz ze zmianà kàta patrzenia jej ko-lor p∏ynnie przechodzi z zielonego w niebieski.

Najwi´cej zmian widocznych jest na banknocie 100z∏. Na tym banknocie umieszczono portret króla W∏ady-s∏awa II Jagie∏∏y. W tle po jego obu stronach znajdujàsi´ stylizowane elementy ornamentyki gotyckiej. Stron´odwrotnà zdobi Orze∏ Bia∏y na tarczy herbowej z na-grobka króla. Poni˝ej tarczy umieszczono he∏m,p∏aszcz krzy˝acki oraz dwa miecze nawiàzujàce dozwyci´skiej bitwy pod Grunwaldem w 1410 roku. Z le-wej strony tarczy widnieje zarys zamku krzy˝ackiegow Malborku. Dzi´ki polu bieli banknot wydaje si´ ja-Êniejszy. Rozeta z prawej strony portretu p∏ynnie zmie-nia kolor ze z∏otego na zielony. W zale˝noÊci od kàtapatrzenia z lewej strony portretu w∏adcy widaç s∏ownei cyfrowe oznaczenia nomina∏u, a pomi´dzy nimi skrót„NBP”.

Poza zmianami widocznymi go∏ym okiem wprowa-dzono tak˝e wiele innych zabezpieczeƒ, które sà od-czytywane przez urzàdzenia sortujàce i liczàce, co jestu∏atwieniem dla banków i firm obs∏ugujàcych obrót go-tówki. Wszystko to sprawia, ˝e nowe polskie banknotysà jednymi z najlepiej zabezpieczonych znaków pie-ni´˝nych na Êwiecie.

A.R.Wi´cej informacji na temat nowych zabezpieczeƒ

banknotów mo˝na znaleêç na stronach www.nbp.pl

1

2

4

1

2 6

4

3

5

5

Charakterystyczne elementy zmodernizowanego banknotu 100-z∏otowego:

• Znak wodny z cyfrowym oznaczeniem nomina∏u widoczny pod Êwiat∏o naniezadrukowanym polu (1),

• Rozeta p∏ynnie zmieniajàca kolor ze z∏otego na zielony (3),• Korona w owalu, której pe∏ny obraz tworzy si´ podczas oglàdania bankno-

tu pod Êwiat∏o (4),• Wyczuwalne przy dotyku, tak˝e dla osób niewidomych, oznaczenia nomina-

∏u, portret w∏adcy, god∏o RP, podpisy Prezesa i G∏ównego Skarbnika NBP.1. Wzbogacony znak wodny. Podczas oglàdania banknotu pod Êwiat∏o widaç znak wodny przedstawiajàcy wizerunek w∏adcy oraz cyfrowe oznacze-nie nomina∏u “100”. Pole znaku wodnego nie jest zadrukowane.2. Nitka zabezpieczajàca. Podczas oglàdania banknotu pod Êwiat∏o widaçpionowà, ciemnà lini´ z cyfrowym oznaczeniem nomina∏u “100” i skrótem“Z¸”, widocznymi równie˝ w odbiciu lustrzanym. Krój liter mikrotekstu zosta∏zmodyfikowany. Nitka zabezpieczajàca zosta∏a umieszczona w strukturzepapieru.3. Rozeta zmieniajàca kolor (farba zmienna optycznie). Wraz ze zmianàkàta patrzenia kolor rozety p∏ynnie przechodzi ze z∏otego w zielony.4. Uzupe∏niajàcy sie druk obustronny (recto-verso). Elementy graficzneznajdujàce si´ na obu stronach banknotu oglàdane pod Êwiat∏o uzupe∏niajàsi´ i tworzà pe∏ny obraz - koron´ w owalu.5. Patrzenie pod kàtem (efekt kàtowy). W zale˝noÊci od kàta patrzeniaz prawej strony portretu w∏adcy widaç koron´ lub cyfry oznaczenia nomina-∏u “100”, z lewej zaÊ s∏owne i cyfrowe oznaczenia nomina∏u, a pomi´dzy nimi skrót “NBP”.6. Mikroskopijne napisy. Mikrodruki to czytelne jedynie w powi´kszeniu napisy umieszczone zarówno na przedniej, jak i odwrotnej stronie banknotu.

Stability and Security • StabilnoÊç i bezpieczeƒstwo

October 2014

XVI

The Poland’s Financial Market: Stability and Security special section has been published by WV Marketing sp. z o. o. in association with Warsaw Voice SA in cooperation with Narodowy Bank Polski as part of an education initiative focusing on economic issues. NBP Head Office, 11/21 Âwi´tokrzyska St., 00-919 Warsaw. More information on financial issues at wwwwww..nnbbpp..ppll and wwwwww..nnbbppoorrttaall..ppllSekcja specjalna „Polski rynek finansowy jest stabilny i bezpieczny” wydana przez WV Marketing Sp. z o. o. we wspó∏pracy z Warsaw Voice S.A. to projekt realizowany we wspó∏pracy z Narodowym Bankiem Polskim w ramach programu edukacji ekonomicznej. Centrala NBP, ul. Âwi´tokrzyska 11/21, 00-919 Warszawa. Wi´cej informacji na tematy finansowe na stronach wwwwww..nnbbpp..ppll i wwwwww..nnbbppoorrttaall..ppll

have integrated information systems and access to bankaccounts via the Internet has become commonplace.

Twenty-five years ago several specialized banks operat-ed on the Polish market. In practice, they did not competewith one another. Today the banking market is highly com-petitive and banks are bending over backwards to enlistclients. Especially stiff competition can be seen in termsof the range of products offered and the quality of service,but in this battle for clients banks must also take into

account many other factors. The image of a typical bankwith marble counters and tellers behind windows isalready a thing of the past. Wanting to be seen as mod-ern, banks have begun to use elegant open-plan spacesin their branches. The interior design colors and logoshave also changed. Although conservative blue andnavy—designed to communicate solidity and predictabil-ity—still dominate, many banks today use bright, some-times garish, colors in order to stand out.

The appearance of bank head offices and branchestoday is testament to the changes that have taken placein the Polish banking sector in the last quarter-century. Butfar more important are the system changes, thanks towhich Polish banks are doing well and generating sub-stantial profits, and the banking system as a whole is oneof the most modern and one of the safest in Europe.

A.R.

informatycznymi, a dost´p do rachunków bankowychprzez Internet sta∏ si´ powszechny.

25 lat temu na polskim rynku dzia∏a∏o kilka wyspecjali-zowanych banków, które praktycznie ze sobà nie konku-rowa∏y. Obecnie rynek bankowy jest bardzo konkurencyj-ny i o klienta trzeba zabiegaç. G∏ównym polem konku-rencji jest oferta produktowa i jakoÊç serwisu, ale w wal-ce o klienta trzeba braç pod uwag´ równie˝ wiele innychczynników. Produkty bankowe nie ró˝nià si´ wiele od sie-bie, dlatego ˝eby si´ wyró˝niç trzeba zadbaç o identyfi-kacj´ wizualnà. Jedne banki w swojej identyfikacji piel´-

gnujà tradycj´, drugie nowoczesnoÊç. Ale obraz bankuz marmurowymi kontuarami, kasjerami za szybami nale-˝y ju˝ do przesz∏oÊci. Banki – chcàc byç postrzegane ja-ko nowoczesne – zacz´∏y w swoich oddzia∏ach stoso-waç otwartà, eleganckà przestrzeƒ. Zmieni∏a si´ te˝ ko-lorystyka wystroju wn´trz i logotypów. Chocia˝ na pol-skim rynku bankowym nadal dominujà kolory niebieskii granatowy, majàce wzbudzaç zaufanie, to wiele ban-ków w swojej identyfikacji wizualnej u˝ywa dzisiaj ja-snych, czasami nawet krzykliwych kolorów.

Obecny wyglàd siedzib i oddzia∏ów banków jest Êwia-dectwem przemian, jakie dokona∏y si´ w polskim sekto-rze bankowym w ostatnim çwierçwieczu. Ale du˝o istot-niejsze sà zmiany systemowe, dzi´ki którym banki w Pol-sce majà si´ dobrze, przynoszàc pokaêne zyski, a ca∏ysystem bankowy nale˝y do jednego z najbardziej nowo-czesnych i bezpiecznych w Europie. A.R.

Polish Banks—Thenand Now

Banki wczoraj i dziÊdokoƒczenie ze strony VII

szeƒ w systemy ochrony instytucjonalnej obejmujàce p∏yn-noÊç i kapita∏ banków. To odpowiedê na niskà efektywnoÊçkosztowà zwiàzanà z ma∏à skalà dzia∏alnoÊci cz´Êci ban-ków. Zalecane jest te˝ kontynuowanie dzia∏aƒ restruktury-zacyjnych zmierzajàcych do wzrostu efektywnoÊci dzia∏a-

nia spó∏dzielczych kas oszcz´dnoÊciowo-kredytowychi zwi´kszenia ich kapita∏ów. Odbywaç si´ to ma przy opty-malnym wykorzystaniu wewn´trznych zasobów systemuSKOK oraz zwi´kszeniu roli modelu silnych wi´zi mi´dzycz∏onkami indywidualnych SKOK.

Wskazane w raporcie problemy spó∏dzielczych kasoszcz´dnoÊciowo-kredytowych nie przes∏aniajà faktu, ˝epolski system finansowy jest stabilny, a perspektywy jegofunkcjonowania z roku na rok poprawiajà si´. To wa˝ne,szczególnie w czasie, kiedy wiele europejskich krajów bo-ryka si´ jeszcze ze skutkami kryzysu finansowego.

A.R.W tekÊcie wykorzystano informacje ze strony www.nbp.pl

continued from page V

dokoƒczenie ze strony III

Polska ma stabilnysystem finansowy