Ian Palliser. Презентация в рамках Всемирного молочного...

15

-

Upload

dairynews -

Category

Presentations & Public Speaking

-

view

253 -

download

1

Transcript of Ian Palliser. Презентация в рамках Всемирного молочного...

Managing Volatility- Lessons from Oil?

Name Ian Palliser

Organisation PAZO Consulting

Event name World Dairy Summit, Rotterdam, October 2016

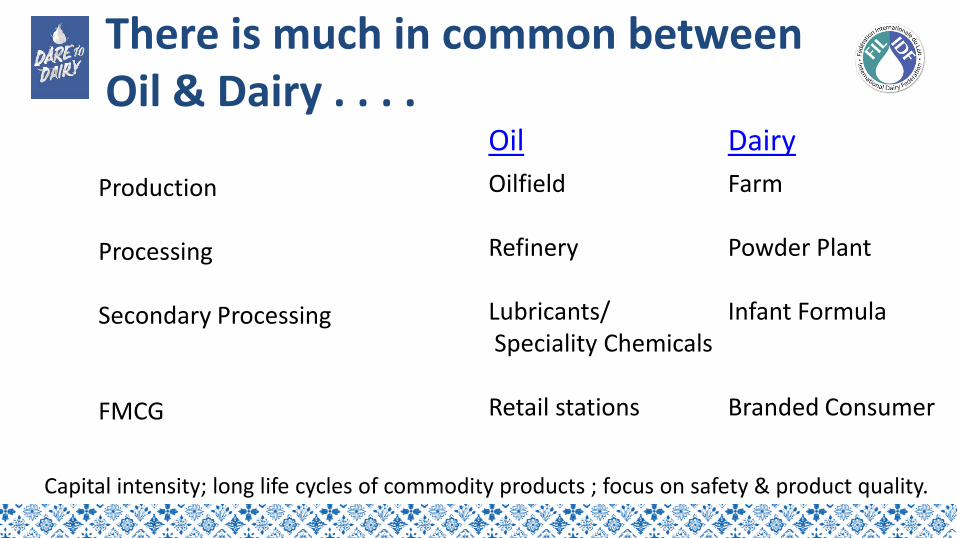

There is much in common betweenOil & Dairy . . . .

Production

Processing

Secondary Processing

FMCG

Oil Dairy

Oilfield Farm

Refinery Powder Plant

Lubricants/ Infant FormulaSpeciality Chemicals

Retail stations Branded Consumer

Capital intensity; long life cycles of commodity products ; focus on safety & product quality.

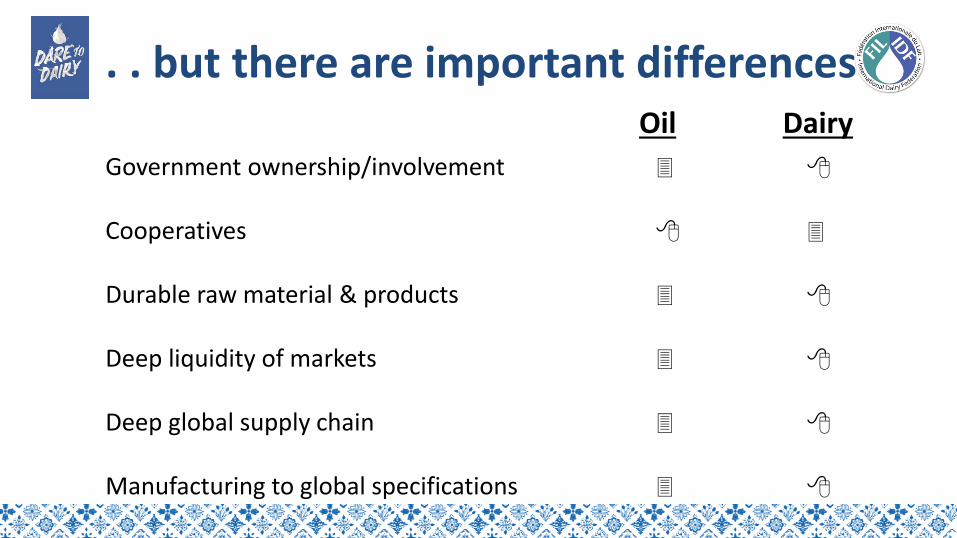

. . but there are important differencesOil Dairy

Government ownership/involvement

Cooperatives

Durable raw material & products

Deep liquidity of markets

Deep global supply chain

Manufacturing to global specifications

3

8

3

3

3

3

8

3

8

8

8

8

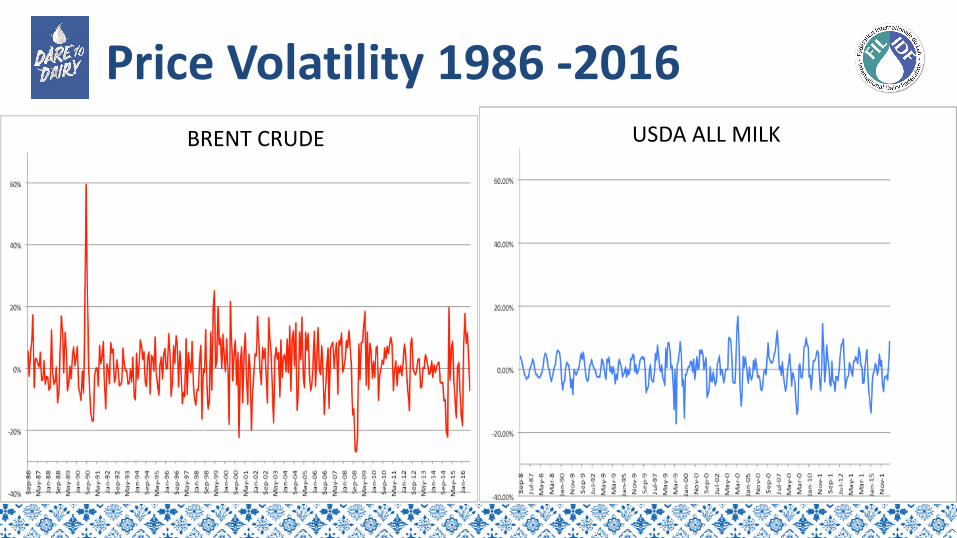

Price Volatility 1986 -2016USDA ALL MILKBRENT CRUDE

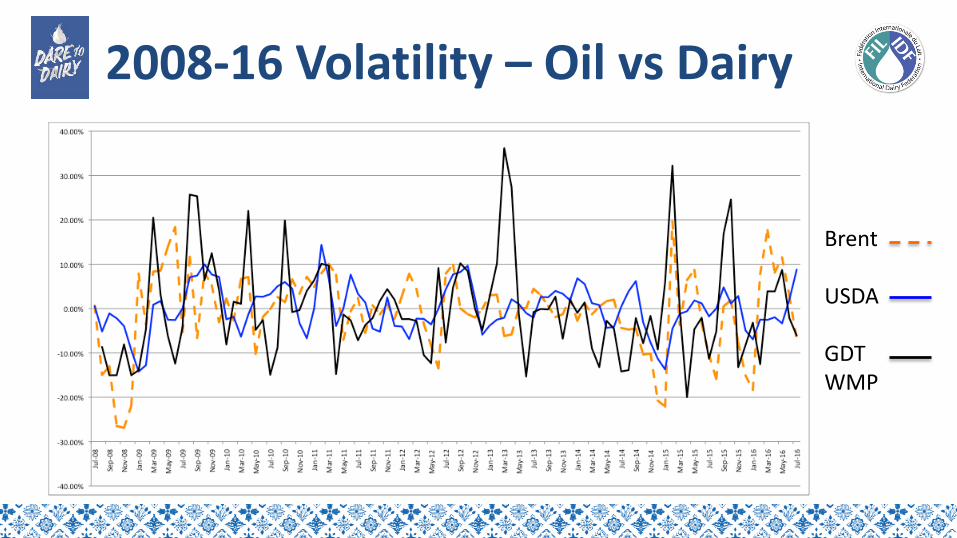

2008-16 Volatility – Oil vs Dairy

Brent

USDA

GDTWMP

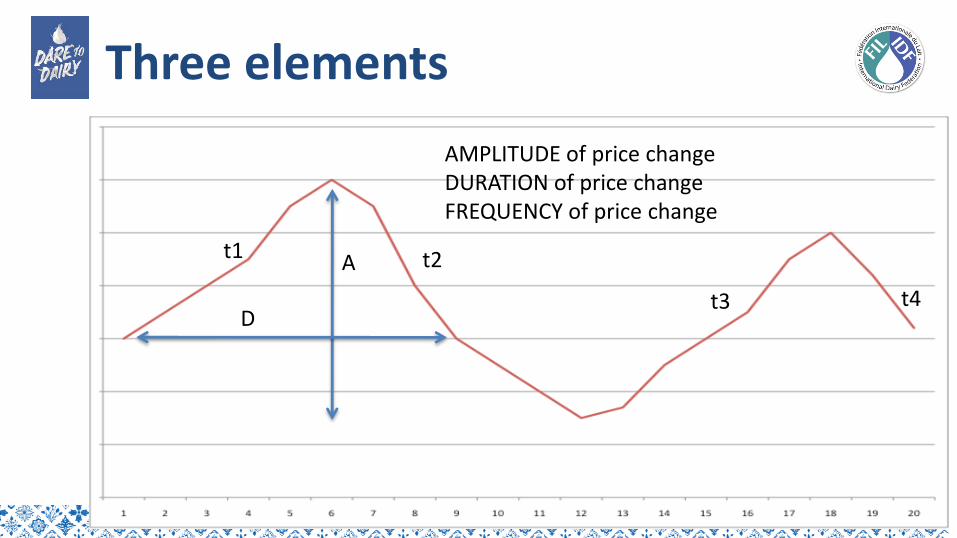

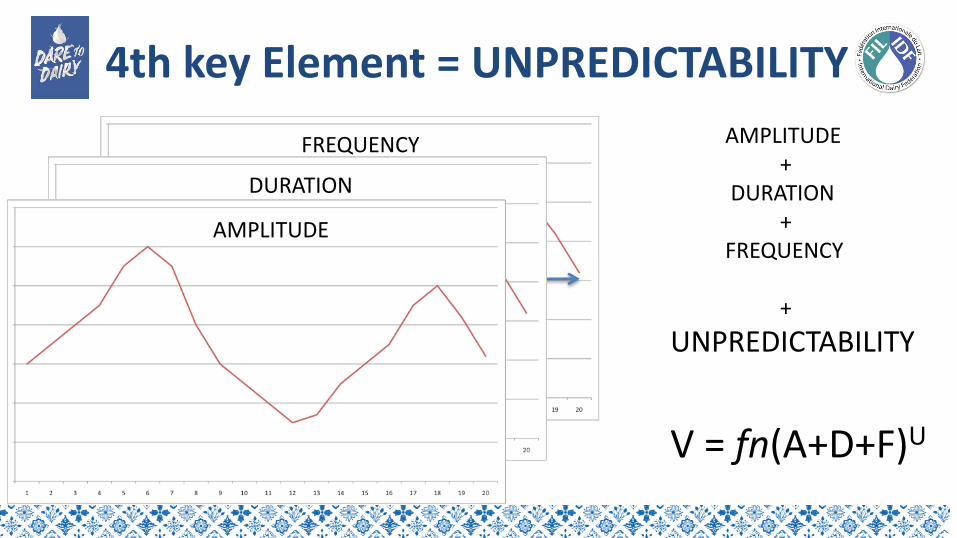

What is Volatility?

A = AMPLITUDE

D = DURATION

F = FREQUENCY

U =

FREQUENCY

Three elements

AMPLITUDE of price changeDURATION of price changeFREQUENCY of price change

A

D

t1 t2

t4t3

FREQUENCY

4th key Element = UNPREDICTABILITY

DURATION

AMPLITUDE

AMPLITUDE+

DURATION+

FREQUENCY

+

UNPREDICTABILITY

V = fn(A+D+F)U

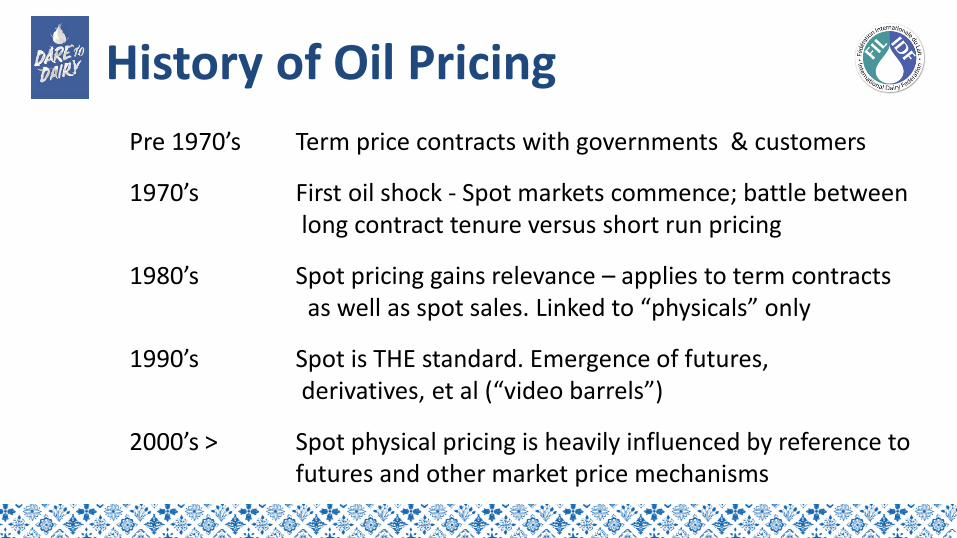

History of Oil Pricing

Pre 1970’s

1970’s

1980’s

1990’s

2000’s >

Term price contracts with governments & customers

First oil shock - Spot markets commence; battle betweenlong contract tenure versus short run pricing

Spot pricing gains relevance – applies to term contractsas well as spot sales. Linked to “physicals” only

Spot is THE standard. Emergence of futures,derivatives, et al (“video barrels”)

Spot physical pricing is heavily influenced by reference to futures and other market price mechanisms

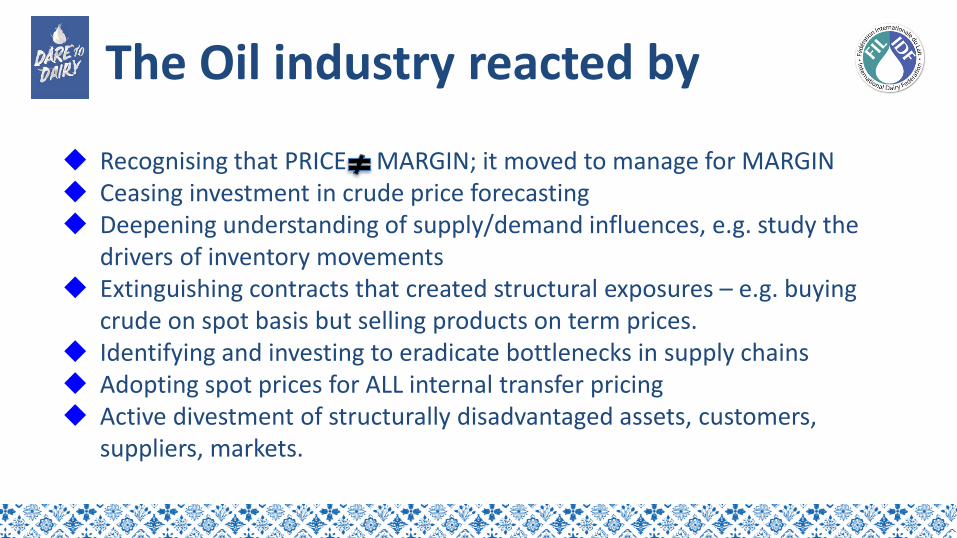

The Oil industry reacted by

Recognising that PRICE MARGIN; it moved to manage for MARGIN Ceasing investment in crude price forecasting Deepening understanding of supply/demand influences, e.g. study the

drivers of inventory movements Extinguishing contracts that created structural exposures – e.g. buying

crude on spot basis but selling products on term prices. Identifying and investing to eradicate bottlenecks in supply chains Adopting spot prices for ALL internal transfer pricing Active divestment of structurally disadvantaged assets, customers,

suppliers, markets.

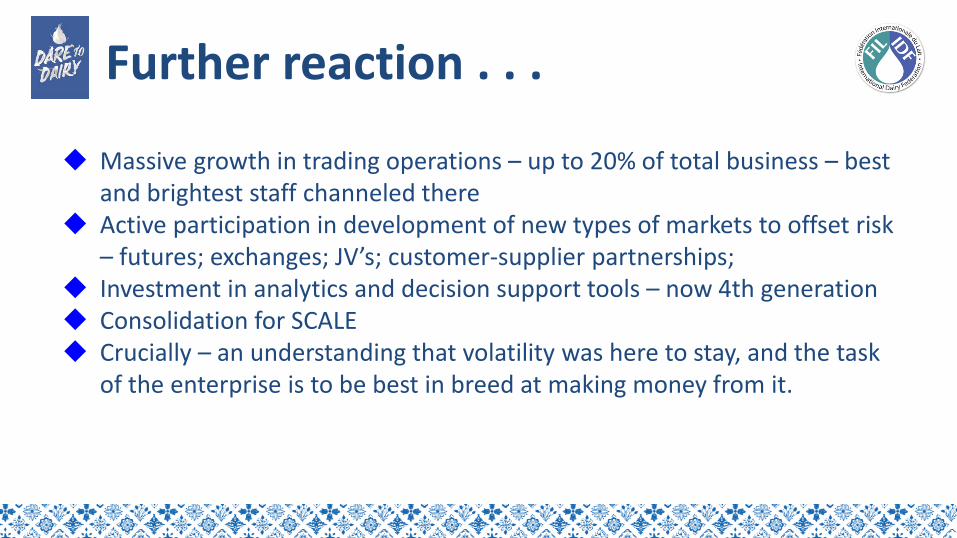

Further reaction . . .

Massive growth in trading operations – up to 20% of total business – best and brightest staff channeled there

Active participation in development of new types of markets to offset risk – futures; exchanges; JV’s; customer-supplier partnerships;

Investment in analytics and decision support tools – now 4th generation Consolidation for SCALE Crucially – an understanding that volatility was here to stay, and the task

of the enterprise is to be best in breed at making money from it.

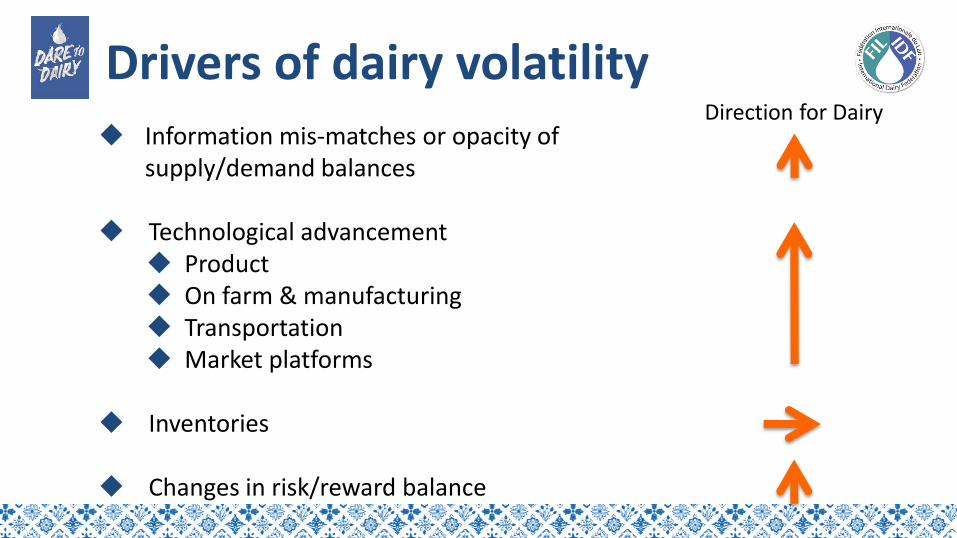

Drivers of dairy volatility Information mis-matches or opacity of

supply/demand balances

Technological advancement Product On farm & manufacturing Transportation Market platforms

Inventories

Changes in risk/reward balance

Direction for Dairy

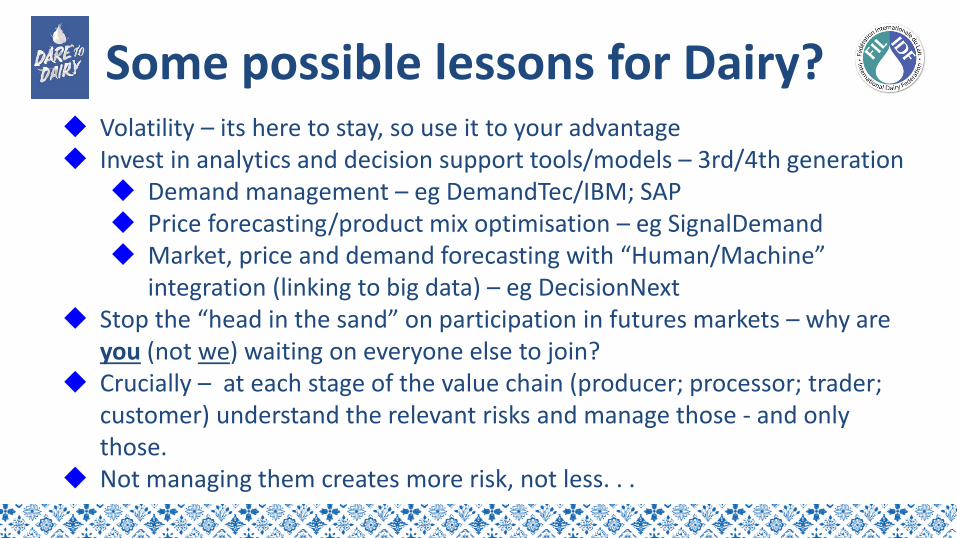

Some possible lessons for Dairy? Volatility – its here to stay, so use it to your advantage Invest in analytics and decision support tools/models – 3rd/4th generation

Demand management – eg DemandTec/IBM; SAP Price forecasting/product mix optimisation – eg SignalDemand Market, price and demand forecasting with “Human/Machine”

integration (linking to big data) – eg DecisionNext Stop the “head in the sand” on participation in futures markets – why are

you (not we) waiting on everyone else to join? Crucially – at each stage of the value chain (producer; processor; trader;

customer) understand the relevant risks and manage those - and onlythose.

Not managing them creates more risk, not less. . .