1 April 2017 v.4 - Unilever Global · Unilever SAC Scheme Rules v4.5 1 April 2017 Page 3 of 39 2)...

39

Unilever SAC Scheme Rules v4.5 1 April 2017 Page 1 of 39 1 April 2017 v.4.5

Transcript of 1 April 2017 v.4 - Unilever Global · Unilever SAC Scheme Rules v4.5 1 April 2017 Page 3 of 39 2)...

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 1 of 39

1 April 2017 v.4.5

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 2 of 39

BACKGROUND

By 2020 Unilever intends to buy all its agricultural raw materials from farms applying

sustainable agricultural practices, so that:

Farmers and farm workers can obtain a liveable income and improve living conditions

Soil fertility of agricultural land is maintained and improved

Water availability and quality are protected and enhanced

Nature, biodiversity and climate are protected and enhanced.

This ambition has been the inspiration for the Unilever Sustainable Agriculture programme,

which started in 1998. In 2010, this programme, in wide consultation with farmers, NGOs and

academics, resulted in the publication of the Unilever Sustainable Agriculture Code. This, in

turn, became the basis for the Unilever Sustainable Sourcing programme, one of the pillars

of the Unilever Sustainable Living Plan, which was launched in November 2010.

PURPOSE OF THE SCHEME RULES

In order for Unilever to be able to report on progress in Sustainable Sourcing, the following

scheme rules have been developed to determine whether a certain volume of raw material

A, purchased from supplier X, qualifies to be included in the Unilever Sustainable Sourcing

Metric, i.e. whether this material will classify as having been ‘sustainably sourced’.

These scheme rules will be reviewed annually.

THE SUPPLIER AND THE UNILEVER SUPPLIER CODE

The concept of Sustainable Sourcing of agricultural raw materials revolves around farming.

However, Unilever does not generally buy fresh produce from farmers directly. Unilever

buys from ‘suppliers’ (usually processors or traders). The supplier has to have acknowledged

the Unilever Supplier Code and ensure their activities are conducted in accordance with it, in

order for any volume that Unilever buys from this supplier, to qualify as ‘sustainably

sourced’.

It is Unilever’s policy to formally request that all our suppliers respect the principles of our

Supplier Code and adopt practices that are consistent with it. Unilever's direct suppliers will

take responsibility to require adherence to the principals of this Supplier Code from their

direct suppliers and exercise diligence in verifying that these principles are being adhered to

in their supply chains.

Unilever will develop mechanisms to ensure suppliers are informed about the Supplier

Code, informed about any updates, and to ensure that the commitment is reviewed on a

regular basis.

STANDARDS AND VERIFICATION

Sustainable Sourcing refers to the way raw materials have been produced, i.e. the term

‘sustainable’ can be attached to materials produced by farmers who adhere to a certain set

of farming practices, or a certain production code. There are two mechanisms through

which adherence to such production codes can be verified:

1) Certification of farms against an external standard, formally recognised by Unilever

as compliant with the principles and practices of sustainable agriculture

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 3 of 39

2) Active farmer engagement in, and commitment to, a sustainability improvement

programme based on the Unilever Sustainable Agriculture Code 1.0 (SAC). The SAC

contains mandatory requirements for performance reporting to demonstrate

tangible continuous improvement in the sustainability of the raw materials.

1. Certified Practices

Any material from farms that have been certified against standards and codes recognised by

Unilever as compliant with the principles and practices of sustainable agriculture, qualifies

as being ‘sustainably sourced’. The current list of recognised external standards and codes

is given in Annex IA.

2. Self-Assessed Practices of Farmers Engaged in Sustainability Programmes

Any material from farmers supplying our suppliers recognised by Unilever as compliant with

the Unilever Sustainable Agriculture Code 1.0 as defined by the rules relating to the SAC

(pages 5-8), qualifies as being ‘sustainably sourced’. Unilever has partnered with the

software company ‘Muddy Boots’ to develop a system (Greenlight Assessments1) to collect

information from suppliers on compliance, calculate scores and track metrics for

continuous improvement.

Annex II contains external standards which have been benchmarked against the SAC, which

are not considered fully equivalent, but cover certain chapters that Unilever will accept as

equivalent. If suppliers are compliant with the standards or codes in Annex II, they will need

to self-assess against the SAC for any chapters not covered by the standard or code, e.g.

through Greenlight Assessments. If a supplier is using a standard or code that is not listed in

Annex II they can request, via their Unilever contact, for a benchmark to be carried out.

In addition to publicly-available external standards and codes, Unilever will also consider

any current in-house or industry-level sustainability programmes that suppliers use. In

these cases suppliers are required to benchmark their system or programme against the UL

SAC, and inform Unilever of the result. Unilever will make the final decision on which areas,

if any, of a supplier or industry-level system are equivalent to the SAC. Any chapters of the

SAC not covered will need to be checked through self-assessment. The current list of

accepted industry-level schemes can be seen in Annex IB.

If a supplier or farmer has any doubt or grievance with respect to our benchmarking of

either an external standard or in-house or industry-level programme, please contact

Vanessa King on email: [email protected].

WILD-HARVESTED MATERIALS

Assessment of the sustainability of wild-harvested materials requires a different approach,

since the issues are different from those related to cultivated products and using SAC is not

appropriate. For such situations a risk assessment approach is taken, using the template in

Annex V. Rules relating the use of this approach are described in paragraphs 8-11 (page 9).

1 Previously called “Quickfire”

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 4 of 39

Different Supply Chain Options

Several certification schemes, for example RSPO and RTRS, offer the possibility of buying

certificates (e.g. Greenpalm certificates in the case of RSPO). These indicate that even if the

actual raw material you have bought is not produced in a sustainable way, an equivalent

amount of raw material has. Some schemes, which would also include FSC, offer different

ways of allowing certified and non-certified material to be mixed (e.g. FSC Mixed Sources,

RSPO Mass Balance).

The important point about these supply chain systems is that there has to be a strict

administrative system in place to ensure there is no double counting of sustainable raw

material, i.e. the equivalent amount of sustainable raw material could not be sold to more

than one purchaser, either as the physical raw material, or as certificates.

Material produced under such systems will be counted by Unilever as ‘sustainably sourced’.

However, in order to be credible and acceptable to Unilever, systems or operators that use

mass balance and related systems need to:

1. have stated an intention to develop a segregated supply chain over time

2. have shown that segregated supply is not feasible in the short term

3. have an independently verified administrative system that ensures no double counting

can take place

The use of mass balance will be restricted to either single processing units or a group of

processing units that operate under a single Internal Control System and with one

homogenous supply base of farmers.

In the absence of these elements, a segregated supply is required to ensure that the raw

material bought is counted as sustainable.

A detailed description of how mass balance can be used in self-assessment against the SAC

can be seen in Annex IV of this document.

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 5 of 39

RULES RELATING TO THE USE OF THE UNILEVER SUSTAINABLE AGRICULTURE

CODE (SAC)

1. General Conditions

a) The scope and responsibilities as per sections 0.3 and 0.4 of the SAC2 are adhered to.

b) The units that need to do the farm assessments are the primary processing plants

from which Unilever (or Unilever suppliers) buy raw material.

c) A random sample of farms for self-assessment will be taken for each new

assessment round from the full list of farmers supplying that processing plant with

raw materials that are supplied to Unilever. The selection will be made automatically

through the Greenlight Assessments software system, or, if the software is not being

used, by a Unilever representative, but not by the supplier themselves. Point 6. in this

document describes what is meant by a random sample.

d) The number of farms to be sampled per processing plant is determined by the

following rules:

i. If there are fewer than 30 farms, all the farmers are assessed.

ii. When the number of farms is >30 the sampling rule is the square root of N

(where N = the number of farms) or 30, whichever is the higher. This means that

>30 farms must be sampled only if there are more than 900 farmers for the

processing plant.

iii. Suppliers may choose to sample >30 farms per processing plant, even if this is

not required in ii.

e) Where more than one processing plant, more than one crop, and/or more than one

farmer group is involved, the sampling rules apply to every farmer group who fall

under a separate management scheme or Internal Control System3. For example:

2 0.3 Scope

Unless otherwise stated in the text, the scope of this document is as below:

Practices referring to Scope

Soils, soil management Field on which Unilever crops are grown, including fields in

rotation with other crops.

Crop husbandry Unilever crops

Animal husbandry Unilever animals. Animal slaughter and transport of animals

off-farm is currently out of scope.

People, working conditions, health & safety, training Whole farm

Activities stretching beyond the farm, such as some

aspects of Biodiversity, Water or Value chain

Whole farm

0.4 Responsibilities

This Code of Conduct is applicable to all Unilever suppliers of agricultural goods, the farmers producing them and

contractors working on farm. We hold our suppliers responsible for implementing this Code. However, many good

practices must be applied by farmers, not suppliers.

3 A Management Scheme or Internal Control System is a documented and tested step-by-step method

aimed at smooth functioning through standard practices. They generally include detailed information

on topics such as (1) organising a programme, (2) setting and implementing corporate policies and

targets, (3) establishing accounting, monitoring, and control procedures, (4) choosing and training

employees, (5) evaluation procedures.

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 6 of 39

i Where one processing plant supplies more than one raw material to Unilever

(e.g. different dried vegetables) the number of farms producing all the raw

materials supplied to Unilever will be added together, and the total number used

to determine how many farms need to be sampled, according to the rules under

d). At least 2 farms must be sampled for each raw material. If a farm in the

sample of 30 produces more than one raw material for Unilever, it may be asked

to answer the metrics-related questions for each raw material separately.

ii If a supplier has 3 plants in 3 locations (e.g. 1 plant per country), purchasing

from different groups of farmers, each will be assessed separately. However, if

different processing plants buy raw materials from the same group of farmers,

or different groups of farmers under the same management system, the group

need only be assessed once.

f) When groups of farmers are located in different regions but are managed under the

same management scheme or Internal Control System (i.e. are counted as one group

for sampling purposes) documentary evidence of the common management system

must be provided to Unilever.

g) Assessments are carried out at the level of a particular raw material (farmer

requirements) or product sold to Unilever (supplier requirements).

h) The volume of material counted as ‘sustainably sourced’ is the volume of product

purchased by Unilever, or produced in a Unilever primary processing plant, not the

volume of the harvested product. For example, soybean oil not soy beans, black leaf

tea, not fresh leaf, tomato paste, not tomatoes.

2. Scoring system

A farmer starts to count as compliant if their assessment (farmer and supplier questions

combined) achieves:

100 % of Mandatory requirements

80 % of Applicable Musts in total4

50 % of Applicable Musts per SAC Chapter

The volume counted as ‘sustainably sourced’ from a supplier is calculated as follows:

a) If all farmers sampled and assessed (as defined in 1c.-e. above) are compliant then

the total volume of product sold to Unilever is counted.

b) If x/y farmers sampled are compliant then (x/y) * 100% of the total volume of product

sold to Unilever can count. BUT all mandatory requirements must be achieved by all

farmers sampled for any of the volume to count, i.e. if ANY of the sampled farmers

fail ANY of the mandatory requirements, NONE of the volume of product sold to

Unilever counts as sustainably sourced. Note: it is the number of farmers that is used

in the calculation, regardless of the volume of material those farmers supply. This should

be presented to Unilever as ‘sustainably sourced (controlled mixing)’.

c) If the conditions required for mass balance have been agreed with Unilever (see box

‘Different Supply Chain Options’), the volume is calculated as (x/y)*100% (as in b), but

the volume should be presented to Unilever as ‘sustainably sourced (mass balance)’.

4 This percentage is calculated by dividing the number of ‘musts’ complied with by the total number of

applicable ‘musts’ in the assessment multiplied by 100.

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 7 of 39

The calculation as under a), b) and c) above will apply to the volume purchased by

Unilever after all assessments for a supplier have been submitted and closed in the

software system and compliance confirmed (‘compliant date’).

3. Timing of Subsequent Assessments (Re-assessments)

Re-assessment of a supplier must take place in accordance with the following rules:

a) For ‘compliant dates’ between 1 January and 30 June, all re-assessments must be

submitted and closed before 30 June of the following year.

b) For ‘compliant dates’ between 1 July and 31 December, all re-assessments must be

submitted and closed before 31 December of the following year.

A new random sample will be used for each round of assessments.

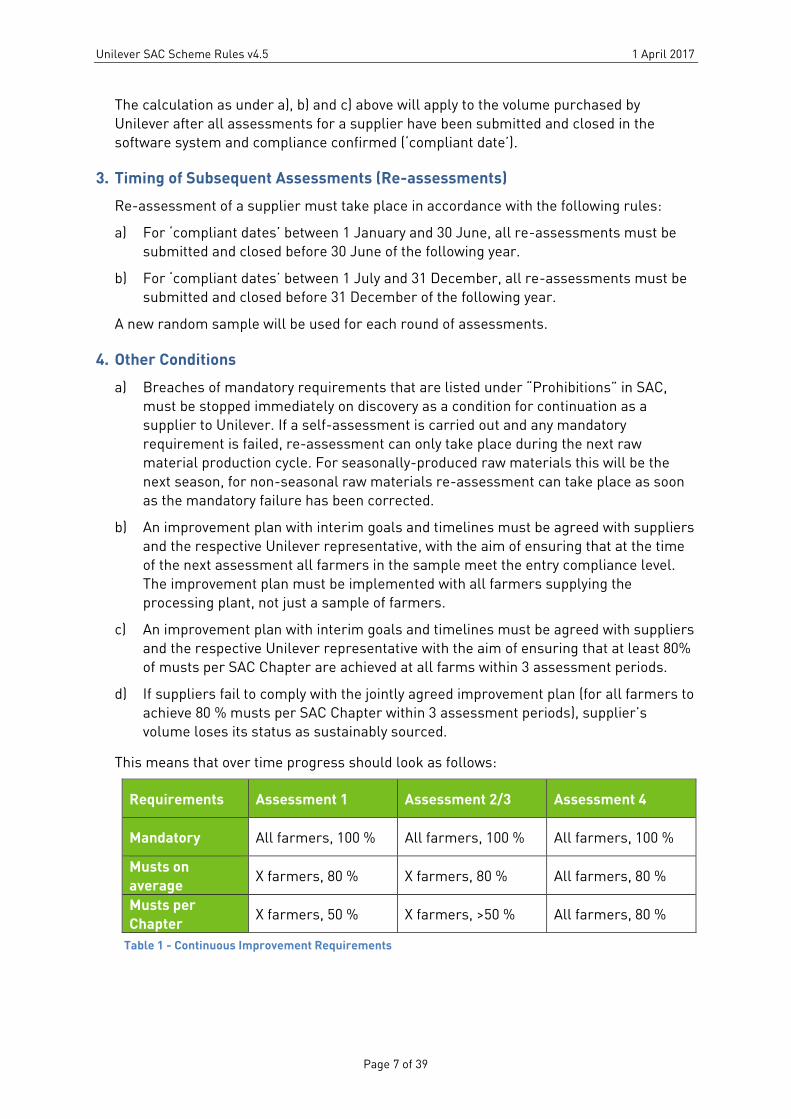

4. Other Conditions

a) Breaches of mandatory requirements that are listed under “Prohibitions” in SAC,

must be stopped immediately on discovery as a condition for continuation as a

supplier to Unilever. If a self-assessment is carried out and any mandatory

requirement is failed, re-assessment can only take place during the next raw

material production cycle. For seasonally-produced raw materials this will be the

next season, for non-seasonal raw materials re-assessment can take place as soon

as the mandatory failure has been corrected.

b) An improvement plan with interim goals and timelines must be agreed with suppliers

and the respective Unilever representative, with the aim of ensuring that at the time

of the next assessment all farmers in the sample meet the entry compliance level.

The improvement plan must be implemented with all farmers supplying the

processing plant, not just a sample of farmers.

c) An improvement plan with interim goals and timelines must be agreed with suppliers

and the respective Unilever representative with the aim of ensuring that at least 80%

of musts per SAC Chapter are achieved at all farms within 3 assessment periods.

d) If suppliers fail to comply with the jointly agreed improvement plan (for all farmers to

achieve 80 % musts per SAC Chapter within 3 assessment periods), supplier’s

volume loses its status as sustainably sourced.

This means that over time progress should look as follows:

Requirements Assessment 1 Assessment 2/3 Assessment 4

Mandatory All farmers, 100 % All farmers, 100 % All farmers, 100 %

Musts on

average X farmers, 80 % X farmers, 80 % All farmers, 80 %

Musts per

Chapter X farmers, 50 % X farmers, >50 % All farmers, 80 %

Table 1 - Continuous Improvement Requirements

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 8 of 39

5. Self-Assessment Verification

Unilever will commission an independent verification body to spot-audit a random sample

of Unilever suppliers who use self-assessment, weighted by a sustainability risk

assessment of the raw material origin. Based on a combination of sustainability risk

indicators (e.g. risk of corruption, human rights abuses, child labour, illegal land clearing)

countries are assigned a High Risk or Low Risk category. Sample size for verification in

Low Risk countries is “square root of the number of suppliers who have done a self-

assessment”, sample size in High Risk countries is twice that. Samples are random. For

each supplier in the sample, three farmers are selected at random. The verification

process checks whether the self-assessment, both at supplier and farmer level, were

done correctly. If negative deviations are found, a pro-rata discount factor is calculated

and applied to the total self-assessed volume for the year.

6. Random Sampling

In random sampling each farmer included in the sample is chosen entirely by chance and

each member of the farmer group has an equal chance of being included in the sample.

Every possible sample of a given size has the same chance of selection; i.e. each member

of the farmer group is equally likely to be chosen at any stage in the sampling process.

This reduces the chance of bias in the sample.

The random sample of farms for self-assessment is an automated part of the

assessment set creation process in the Greenlight Assessments self-assessment

software. Prior to assessment set creation the full list of farmers supplying that

processing plant with raw materials supplied to Unilever must be imported into

Greenlight Assessments and the raw material assigned to each site.

In exceptional circumstances, where Greenlight Assessments cannot be used to generate

the random sample, suppliers must provide a database of their farmers, with numbers

allocated to each farmer e.g. 1-100. Random numbers are then generated to select the

sample. Random numbers can be generated using a calculator, spreadsheet or printed

tables of random numbers. The generation of the random sample must be made by a

Unilever representative, not by the supplier themselves.

7. Transition Period

When new revisions of the Sustainable Agriculture Code or these scheme rules are

published, suppliers and their farmers will have a transition period of 12 months from the

date of publication, within which to comply with any changes.

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 9 of 39

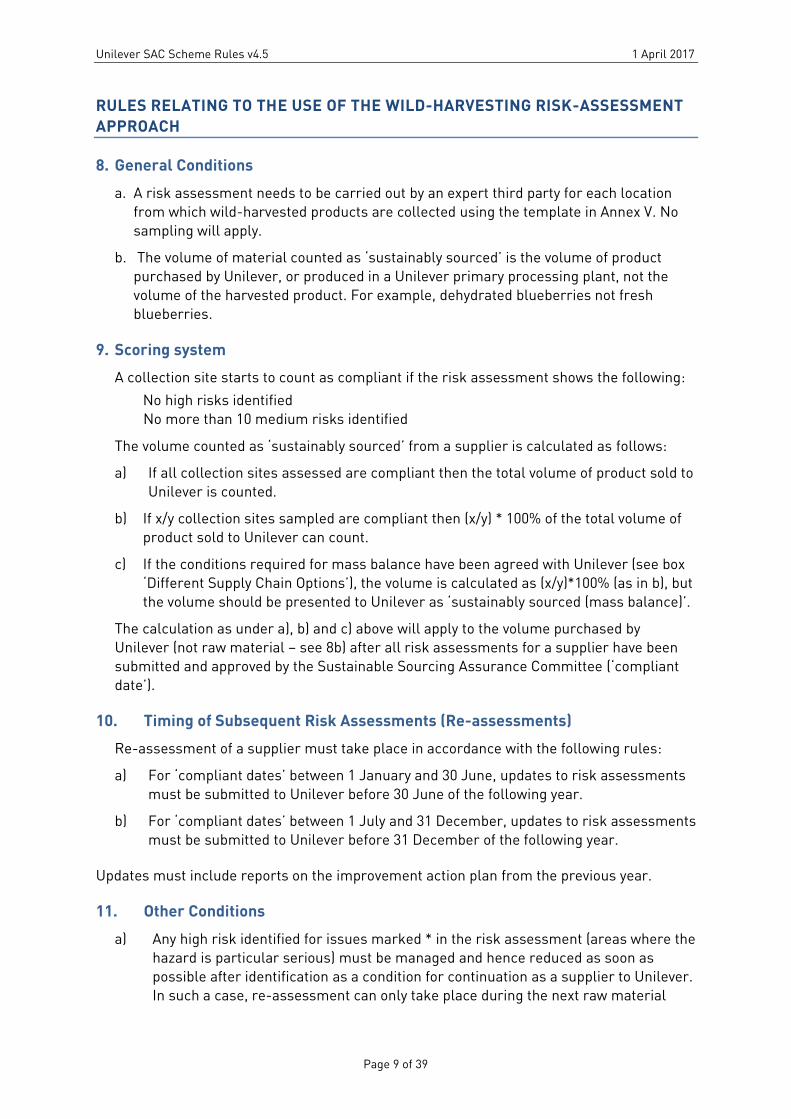

RULES RELATING TO THE USE OF THE WILD-HARVESTING RISK-ASSESSMENT

APPROACH

8. General Conditions

a. A risk assessment needs to be carried out by an expert third party for each location

from which wild-harvested products are collected using the template in Annex V. No

sampling will apply.

b. The volume of material counted as ‘sustainably sourced’ is the volume of product

purchased by Unilever, or produced in a Unilever primary processing plant, not the

volume of the harvested product. For example, dehydrated blueberries not fresh

blueberries.

9. Scoring system

A collection site starts to count as compliant if the risk assessment shows the following:

No high risks identified

No more than 10 medium risks identified

The volume counted as ‘sustainably sourced’ from a supplier is calculated as follows:

a) If all collection sites assessed are compliant then the total volume of product sold to

Unilever is counted.

b) If x/y collection sites sampled are compliant then (x/y) * 100% of the total volume of

product sold to Unilever can count.

c) If the conditions required for mass balance have been agreed with Unilever (see box

‘Different Supply Chain Options’), the volume is calculated as (x/y)*100% (as in b), but

the volume should be presented to Unilever as ‘sustainably sourced (mass balance)’.

The calculation as under a), b) and c) above will apply to the volume purchased by

Unilever (not raw material – see 8b) after all risk assessments for a supplier have been

submitted and approved by the Sustainable Sourcing Assurance Committee (‘compliant

date’).

10. Timing of Subsequent Risk Assessments (Re-assessments)

Re-assessment of a supplier must take place in accordance with the following rules:

a) For ‘compliant dates’ between 1 January and 30 June, updates to risk assessments

must be submitted to Unilever before 30 June of the following year.

b) For ‘compliant dates’ between 1 July and 31 December, updates to risk assessments

must be submitted to Unilever before 31 December of the following year.

Updates must include reports on the improvement action plan from the previous year.

11. Other Conditions

a) Any high risk identified for issues marked * in the risk assessment (areas where the

hazard is particular serious) must be managed and hence reduced as soon as

possible after identification as a condition for continuation as a supplier to Unilever.

In such a case, re-assessment can only take place during the next raw material

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 10 of 39

production cycle. For seasonal raw materials this will be the next season, for non-

seasonal raw materials re-assessment can take place as soon as the risk

management process has been put in place.

b) Any risks identified must be managed via the action plan on the final page of the

risk-assessment template in Annex V.

c) Self-Assessment verification as outlined in Rule 5. (Page 8) will apply to suppliers of

wild-harvested products using the risk-assessment approach.

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 11 of 39

ANNEX IA: EXTERNAL STANDARDS RECOGNISED BY UNILEVER AS FULLY

COMPLIANT WITH THE PRINCIPLES OF SUSTAINABLE AGRICULTURE

ANNEX IA UPDATED 01/04/2017

Standard

[Version #]

Comments Applicable to Logos

1. SAN standard

[Rainforest

Alliance, July

2010]

Sustainable Agriculture

Network standard, basis

for Rainforest Alliance

certification

Crops as per

the SAN

standard.

2. SAN Cattle

Standard

[Rainforest

Alliance, July

2010

Sustainable Agriculture

Network standard, basis

for Rainforest Alliance

certification

Cattle (South

America)

3. RSPO [Principles

and Criteria

(2007)/

Certification

Systems (2008)]

Roundtable for

Sustainable Palm Oil.

Either physical volumes of

oil that are RSPO

certified, or equivalent

volumes of Greenpalm

certificates, can be

included.

Palm oil and

all palm oil

based

products,

including fatty

acid, fatty

alcohol, fatty

amine.

4. FSC Principles

and Criteria for

Forest

Stewardship –

FSC-STD-01-001

(Version 4-0)

FSC Standard for

Chain of Custody

Certification –

FSC-STD-40-004

(Version 1-1)

Forestry Stewardship

Council

Paper and

board

5. FLO [Version

15.08.2009]

Fair Trade Labelling

Organisation

Crops as per

the FLO

standards.

6. MSC [Principles

and Criteria

(2002)/Chain of

Custody (2005)]

Marine Stewardship

Council

Any seafood

from fisheries

certified by

MSC

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 12 of 39

7. IFOAM [Soil

Association

Revision 16.3,

November

2010/National

Programme for

Organic

Production, India,

2005]

International Federation

of Organic Agriculture

Movements. Any organic

standard recognised by

IFOAM

Any raw

material

8. RTRS [Version

1.0, 10.06.2010]

Roundtable for

Responsible Soy

Soybeans

9. Utz Certified

[Version

2009/2010]

Utz Certified Good Inside Coffee, Tea,

Cocoa

10. Proterra (Version

2.0)

Proterra standard

developed by CERT ID

All crops

11. Bonsucro

Production

Standard

Including

Bonsucro EU

Production

Standard

(Version 3.0

March 2011)

Accompanying

documents:

Bonsucro Certification

Protocol Including

Bonsucro EU Certification

Protocol (2011)

Bonsucro Audit Guidance

for Production Standard

Including EU Audit

Guidance for the

Production Standard

(2011)

Sugar (from

sugarcane)

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 13 of 39

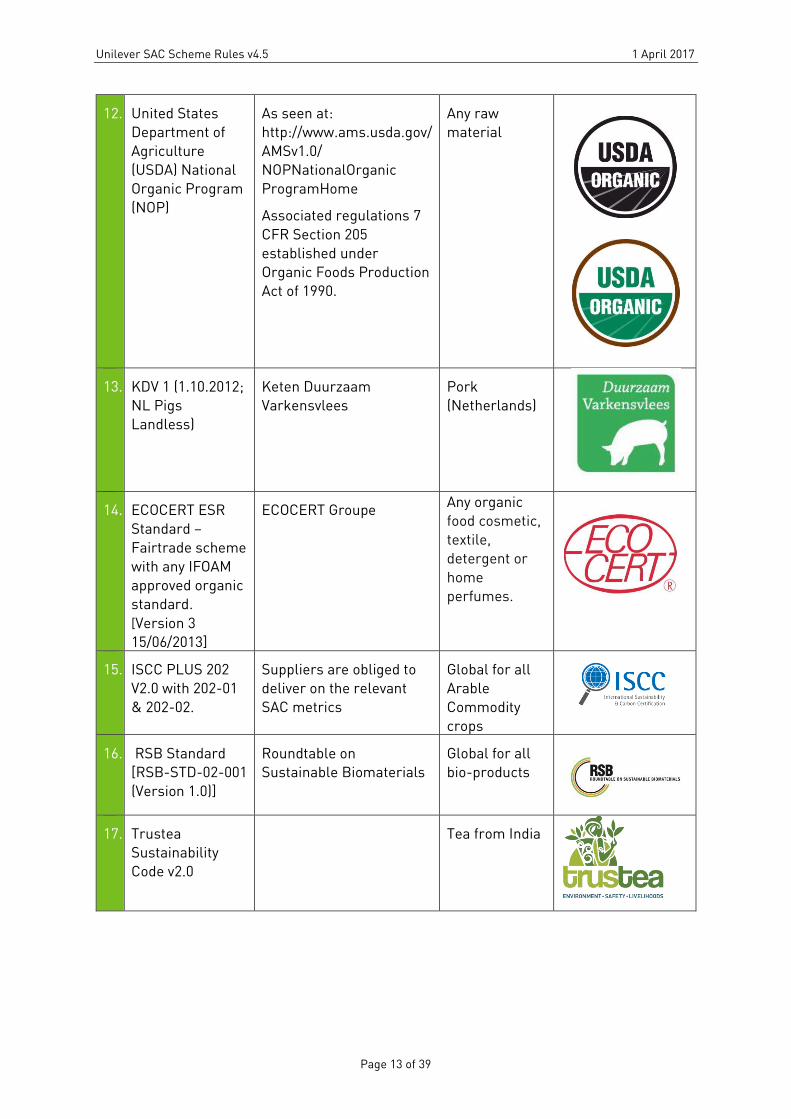

12. United States

Department of

Agriculture

(USDA) National

Organic Program

(NOP)

As seen at:

http://www.ams.usda.gov/

AMSv1.0/

NOPNationalOrganic

ProgramHome

Associated regulations 7

CFR Section 205

established under

Organic Foods Production

Act of 1990.

Any raw

material

13. KDV 1 (1.10.2012;

NL Pigs

Landless)

Keten Duurzaam

Varkensvlees

Pork

(Netherlands)

14. ECOCERT ESR

Standard –

Fairtrade scheme

with any IFOAM

approved organic

standard.

[Version 3

15/06/2013]

ECOCERT Groupe Any organic

food cosmetic,

textile,

detergent or

home

perfumes.

15. ISCC PLUS 202

V2.0 with 202-01

& 202-02.

Suppliers are obliged to

deliver on the relevant

SAC metrics

Global for all

Arable

Commodity

crops

16. RSB Standard

[RSB-STD-02-001

(Version 1.0)]

Roundtable on

Sustainable Biomaterials

Global for all

bio-products

17. Trustea

Sustainability

Code v2.0

Tea from India

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 14 of 39

18. VVAK+DAB

V.2013-14

The DAB is a voluntary

add on to the VVAK

standard meant as a

‘licence to produce’, but

must be added for this

Annex 1 status to apply.

Arable and

Industrial

Vegetable

Crops in The

Netherlands

(NL) and

Belgium (BE)

19. ASC Shrimp

Standard Version

1.0 (March 2014)

Aquaculture

Stewardship Council Global for all

shrimp

products

produced by

Aquaculture

20. Fair for Life

Social and Fair

Trade

Certification

Programme

(December 2013)

Institute for

Marketecology (IMO)

Global, any raw

material

21. SCS Sustainably

Grown v2.1 (July

2016)

SCS Global Services Global, any

food or fibre

crop

22. SAI Platform

Farm

Sustainability

Assessment

(FSA) v2.0

Equivalent at Silver level All crops,

globally

23. Utz Certified

Hazelnut Module

(v1.0 November

2015)

Utz Certified Good

Inside

Hazelnuts

globally

24. Vegaplan (2014) Benchmarked by SAI as

FSA Silver-equivalent

Arable crops

and vegetables

25. Fieldprint®

Platform (FPP)

plus

supplemental

questionnaire

Memorandum of

Understanding between

FTM and FSA – users

must complete

supplemental questions

and score Silver to be

equivalent.

Commodity

crops in the

USA

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 15 of 39

ANNEX IB: INDUSTRY-LEVEL PROGRAMMES RECOGNISED BY UNILEVER AS

FULLY COMPLIANT WITH THE PRINCIPLES OF SUSTAINABLE AGRICULTURE

ANNEX IB updated 01/03/2016

Programme Comments Applicable to Logos

1. Dairy Australia

Approach

Industry-level

standard plus action

plans

Dairy Products

supplied by

Australian

suppliers

2. Sustainable

Dairy Assurance

Scheme (SDAS)

Rev 01

(December 2013)

Use conditional upon

extra data provided by

Bord Bia showing

compliance with

environmental

requirements

Dairy Products

from Eire

(Republic of

Ireland)

3. US Soybean

Sustainability

Assurance

Protocol + Field

to Market

“Fieldprint

Calculator”

Farmers must

complete the full Field

to Market “Fieldprint

Calculator”), including

the Habitat Protection

Index module

Soybeans from

Iowa, Illinois

and Kansas,

USA

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 16 of 39

ANNEX II - EXTERNAL STANDARDS RECOGNISED BY UNILEVER AS PARTIALLY

COMPLIANT WITH THE PRINCIPLES OF SUSTAINABLE AGRICULTURE

ANNEX II UPDATED 12/07/2016

Standard Equivalence Areas not covered

Applicable to Logo

1. PEFC

(Programme

for the

Endorsement

of Forest

Certification)

Equivalence is

PEFC certification

with full Chain of

Custody in

compliance with

“Non-

controversial

Sources”

requirements

(see Annex III)

Additional

requirements

(see Annex III)

Paper and

Board

2. GLOBALG.A.

P. Integrated

Farm

Assurance

Standard

(Crops Base)

[Version 4.0,

March 2011]

Equivalence with

SAC chapters on

Agrochemicals

and Fuels, Value

Chain, Training

Continuous

Improvement,

Soils, Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital

All crops

3. GLOBALG.A.

P. Integrated

Farm

Assurance

Standard

(Livestock

Base)

[Version 4.0,

March 2011]

Equivalence with

SAC chapters on

Agrochemicals

and Fuels, Animal

Welfare, Value

Chain, Training

Continuous

Improvement,

Soils, Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital

Livestock

4. Food Alliance

[Version

08.21.08]

Equivalence with

SAC chapters on

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity

Continuous

Improvement,

Energy, Waste,

Social and

Human Capital,

Value Chain,

Training

Crops and

livestock

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 17 of 39

5. LEAF Marque

Global

Standard

[Version 11.1

08/10/13]

Equivalence with

SAC chapters on

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity,

Energy, Waste,

Social and Human

Capital, Training

Animal Welfare,

Value Chain

Crops and

livestock

6. Red Tractor

Combinable

Crops and

Sugar Beet

Standards

Version 2.0

(October

2011

Agrochemicals

and Fuels, Soils,

Water, Energy

(Risk

Assessment),

Waste, Value

Chain, Training

Continuous

Improvement,

Biodiversity,

Energy

(efficiency),

Social and

Human Capital

Crops

7. Red Tractor

Dairy Farm

Standards

Version 2.0

(October

2011)

Agrochemicals

and Fuels, Water,

Waste, Value

Chain Training,

Animal Welfare

Continuous

Improvement,

Soils,

Biodiversity,

Energy, Social

and Human

Capital

Dairy

Production

8. SQF (Safe

Quality Food)

1000 Level 3

[Version

January

2010]

Equivalence with

SAC chapters on

Animal Welfare,

Value Chain,

Training

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital

Crops and

livestock

9. QS (Guideline

Agriculture)

[Version:

01.01.2011]

Equivalence with

SAC chapters on

Animal Welfare,

Value Chain

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital,

Training

Livestock

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 18 of 39

10. DANISH

Product

Standard

[Version

December

2010]

Equivalence with

SAC chapters on

Animal Welfare,

Value Chain

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital,

Training

Pig production

11. RSPCA

Freedom

Food [RSPCA

Welfare

Standards for

dairy cattle

(January

2010), beef

cattle (March

2010),

chickens

(February

2008), pigs

(January

2010)]

Equivalence with

SAC chapters on

Animal Welfare

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital,

Value Chain,

Training

Livestock

(specific

standards for

individual

products)

12. IKB Pork v

9.0 [January

2012]

Equivalence with

SAC chapters on

Continuous

Improvement,

Agrochemicals

and Fuels5, Water

(quality), Waste,

Social and Human

Capital, Animal

Welfare, Value

Chain, Training

Soils, Water

(irrigation

management),

Biodiversity,

Energy

5 IKB Pork is recognised by GlobalG.A.P. as equivalent to their standard (for details of benchmarking process see

http://www2.globalgap.org/full_app_stand.html). We have therefore assumed equivalence for the Agrochemicals

and Fuels chapter. Other chapters have been benchmarked according to our own procedures.

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 19 of 39

13. ISCC [V1.15

2010]

Equivalence with

SAC chapters on

Agrochemicals

and Fuels, Soils,

Social & Human

Capital and

Training

Continuous

Improvement,

Water (quality

and irrigation

management),

Biodiversity,

Energy, Waste,

Value Chain

Oil seed rape

within

Germany (with

additional

requirements)

14. Sedex

[Version 4.0

2012]

Equivalence with

SAC Criteria

within Social and

Human Capital

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity,

Energy, Waste,

Animal Welfare,

Value Chain,

Training

All raw

materials

15. IKM v5.1/

Vegaplan

(2014)

Equivalence with

SAC chapters on

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water, Waste,

Social and Human

Capital, Animal

Welfare, Value

Chain, Training

Biodiversity,

Energy

Dairy/Livestoc

k and mixed

farming

including

fodder

16. MgSzH (now

NEBIH) +

ISCC Plus

202

Equivalence with

SAC chapters on

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water, Waste,

Energy, Social

and Human

Capital, Value

Chain, Training

Biodiversity Sunflower

within Hungary

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 20 of 39

17. FairWild

Standard

v.2.0

Equivalence with

SAC chapters on:

Biodiversity and

Social and Human

Capital

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water, Waste,

Energy, Value

Chain, Training

Wild Harvested

crops

18. Agro 2.1 and

2.2 version 2

Equivalence with

SAC chapters on

Agrochemicals

and Fuels, Value

Chain, Training

Continuous

Improvement,

Soils, Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital

All crops

19. Teh Lestari

v1.0

Equivalence with

SAC chapters on

Continuous

Improvement,

Agrochemicals &

Fuels, Soils,

Water,

Biodiversity,

Social & Human

Capital, Value

Chain and

Training.

Energy and

Waste

Tea from

Indonesia

2BSvs v1.7

(May

2011)/Conditi

onalité 2013-

13 French Oil

Seed and

Wheat

Production

Equivalence with

SAC chapters on

Continuous

Improvement,

Agrochemicals &

Fuels, Soils,

Water, Energy

Social & Human

Capital

Biodiversity,

Waste, Value

Chain and

Training

Oil seed crops,

wheat,

starches and

sweeteners

from France

20. CanadaGAP

[Version 6.2

2013]

Equivalence with

SAC chapters on

Value Chain

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital,

Training

Canadian fresh

fruits,

vegetables and

herbs

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 21 of 39

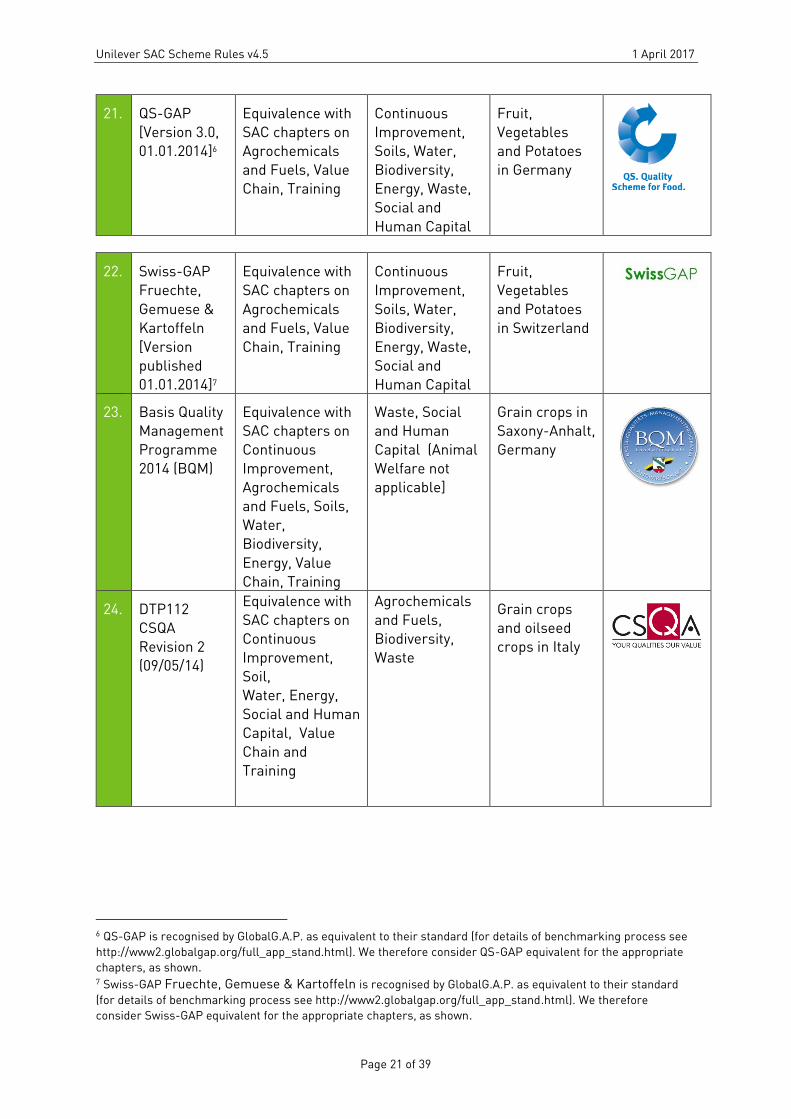

21. QS-GAP

[Version 3.0,

01.01.2014]6

Equivalence with

SAC chapters on

Agrochemicals

and Fuels, Value

Chain, Training

Continuous

Improvement,

Soils, Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital

Fruit,

Vegetables

and Potatoes

in Germany

22. Swiss-GAP

Fruechte,

Gemuese &

Kartoffeln

[Version

published

01.01.2014]7

Equivalence with

SAC chapters on

Agrochemicals

and Fuels, Value

Chain, Training

Continuous

Improvement,

Soils, Water,

Biodiversity,

Energy, Waste,

Social and

Human Capital

Fruit,

Vegetables

and Potatoes

in Switzerland

23. Basis Quality

Management

Programme

2014 (BQM)

Equivalence with

SAC chapters on

Continuous

Improvement,

Agrochemicals

and Fuels, Soils,

Water,

Biodiversity,

Energy, Value

Chain, Training

Waste, Social

and Human

Capital (Animal

Welfare not

applicable]

Grain crops in

Saxony-Anhalt,

Germany

24. DTP112

CSQA

Revision 2

(09/05/14)

Equivalence with

SAC chapters on

Continuous

Improvement, Soil,

Water, Energy,

Social and Human

Capital, Value

Chain and

Training

Agrochemicals

and Fuels,

Biodiversity,

Waste

Grain crops

and oilseed

crops in Italy

6 QS-GAP is recognised by GlobalG.A.P. as equivalent to their standard (for details of benchmarking process see

http://www2.globalgap.org/full_app_stand.html). We therefore consider QS-GAP equivalent for the appropriate

chapters, as shown. 7 Swiss-GAP Fruechte, Gemuese & Kartoffeln is recognised by GlobalG.A.P. as equivalent to their standard

(for details of benchmarking process see http://www2.globalgap.org/full_app_stand.html). We therefore

consider Swiss-GAP equivalent for the appropriate chapters, as shown.

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 22 of 39

ANNEX III - IMPLEMENTATION GUIDELINES TO THE

UNILEVER SUSTAINABLE PAPER AND BOARD PACKAGING SOURCING POLICY

Acceptable Forest Management Certification Schemes

Unilever accept the following Forest Management Certification Schemes: Forest

Stewardship Council (FSC) or Programme for the Endorsement of Forest Certifications

(PEFC) with full Chain of Custody in compliance with “Non-controversial Sources”

requirements.

Legal Origin

Virgin fibre used in the paper packaging product is from a traceable source down to the

forest where the legal origin can be verified, by either a Legality Certification (a) or by

Credible Evidence (b).

Note: Virgin fibre from a forest based in a country according to the Country Exception List

must have a Legality Certification

a) Legality Certification according to any of the below verification schemes* 8

- SW VLC/SW VLO: http://www.rainforest-alliance.org/

- SGS TLTV: http://www.forestry.sgs.com/timber-legality-traceability-verification-

tltv.htm

- Certisource: http://www.certisource.co.uk/

b) Credible Evidence proving legal origin. All following criteria must be met:

- The fibre comes from a “Known” source: Reliable documentation from the

supplier/s is provided that identifies the source location, the source entity, and each

intermediary in the supply chain.

- Suppliers have mechanisms in place to ensure that the timber has been harvested

and traded in compliance with the applicable legislation

- There is evidence of compliance with applicable CITES requirements, if applicable.

Non-controversial Sources

Paper Packaging Product is from legal origin and complies with one of the below criteria, a)

or b)

a) Virgin fibre from a forest not based in a country according to the Country Exception List:

Suppliers conduct their own risk assessment to ensure compliance with the following

requirements:

- Wood is not harvested in violation of traditional and civil rights.

- Wood is not harvested in forests where high conservation values are threatened.

- Wood is not harvested in forests being converted to plantations or non-forest use.

b) The virgin fibre comes from a forest based in a country according to the Country

Exception List:

- FSC Controlled Wood or

8 Schemes will be reviewed on a regular basis

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 23 of 39

- Regarded as equivalent to FSC Controlled Wood by a 3rd party audit initiated by

Unilever or

- Engaged in a phased approach to FSC Certification program, such as Rainforest

Alliance's SmartStep, TFT or WWF’s GFTN producer group.

Certified Paper Packaging Products

Certified Paper Packaging Products are Packaging Products that are supplied to Unilever

under the following conditions:

- They are in compliance with “Non-controversial Sources” requirements and

- The supplying company holds a valid COC certificate of one of the Forest

Management Certification Schemes and the certified paper packaging products

supplied are included in the supplier’s certificate scope.

- The certified paper packaging products used are clearly identifiable as such. e.g.

product carries the certification label, products are identified by a barcode or batch

number clearly linked to the transport documentation and invoices, and are

accompanied by documentation sufficient to link the invoice to the products supplied.

- The certified paper products’ transport documentation and invoices contain clear

indication of the certification claim of the products and the supplying company’s

COC certificate code.

Country Exception List9

Countries listed below have been identified by various scientific institutions and

environmental NGOs as requiring special attention for one or more of the following activities

related to wood product harvesting:

- Illegal Logging

- Forest Conversion

- Civil and Traditional Rights Violations

- Threatened High Conservation Values

9This list will be reviewed on a regular basis

Asia

Indonesia

Vietnam

Malaysia

China

Myanmar (Burma)

Cambodia

Philippines

Thailand

Papua New Guinea

Solomon Islands

South Korea

Taiwan

Laos

Africa

Democratic

Republic of Congo

Gabon

Ivory Coast

Equatorial Guinea

Liberia

Cameron

Ghana

Sierra Leone

Guinea

Central Africa

Republic

Nigeria

Latin America

Honduras

Peru

Brazil

Ecuador

Europe

Romania

Russia

Lithuania

Bulgaria

Ukraine

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 24 of 39

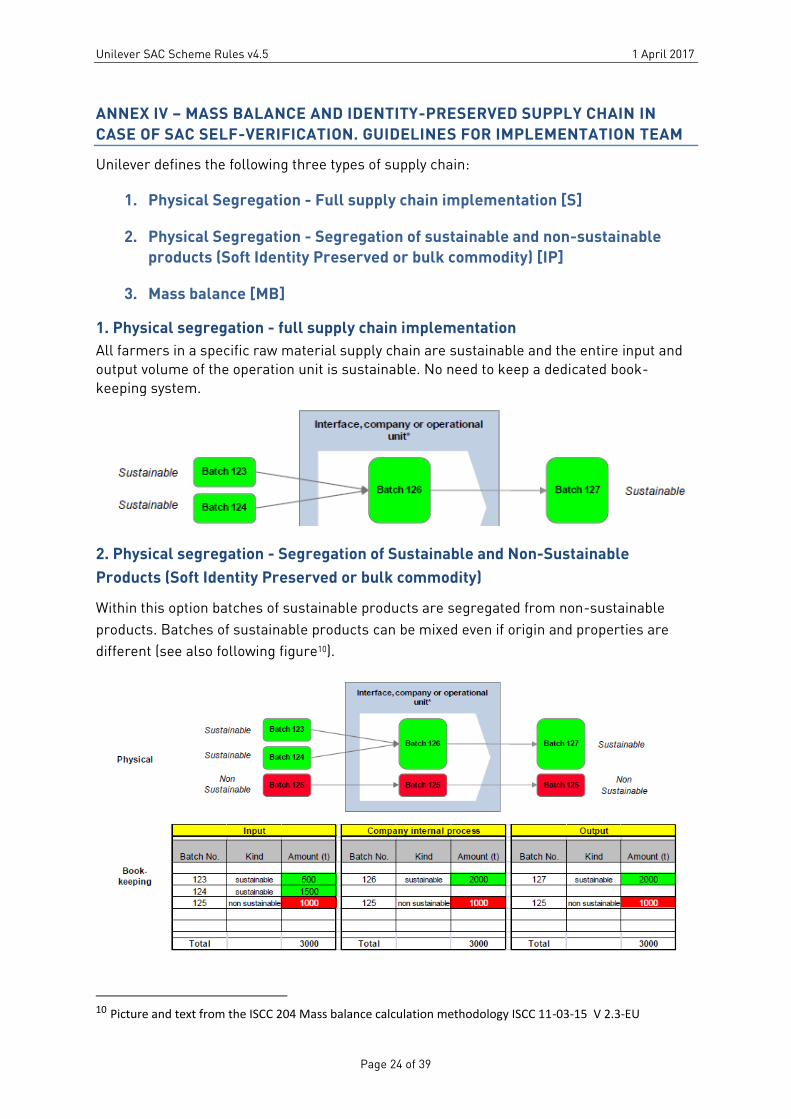

ANNEX IV – MASS BALANCE AND IDENTITY-PRESERVED SUPPLY CHAIN IN

CASE OF SAC SELF-VERIFICATION. GUIDELINES FOR IMPLEMENTATION TEAM

Unilever defines the following three types of supply chain:

1. Physical Segregation - Full supply chain implementation [S]

2. Physical Segregation - Segregation of sustainable and non-sustainable

products (Soft Identity Preserved or bulk commodity) [IP]

3. Mass balance [MB]

1. Physical segregation - full supply chain implementation

All farmers in a specific raw material supply chain are sustainable and the entire input and

output volume of the operation unit is sustainable. No need to keep a dedicated book-

keeping system.

2. Physical segregation - Segregation of Sustainable and Non-Sustainable

Products (Soft Identity Preserved or bulk commodity)

Within this option batches of sustainable products are segregated from non-sustainable

products. Batches of sustainable products can be mixed even if origin and properties are

different (see also following figure10).

10 Picture and text from the ISCC 204 Mass balance calculation methodology ISCC 11-03-15 V 2.3-EU

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 25 of 39

What does the consultant need to ask the supplier to do?

1. The supplier must create and maintain a book-keeping system able to record volumes of

sustainably sourced volumes together with the non-sustainable as in the diagram above.

2. The supplier must provide on request the evidence that each batch of material delivered

to Unilever come exclusively from the sustainable sources.

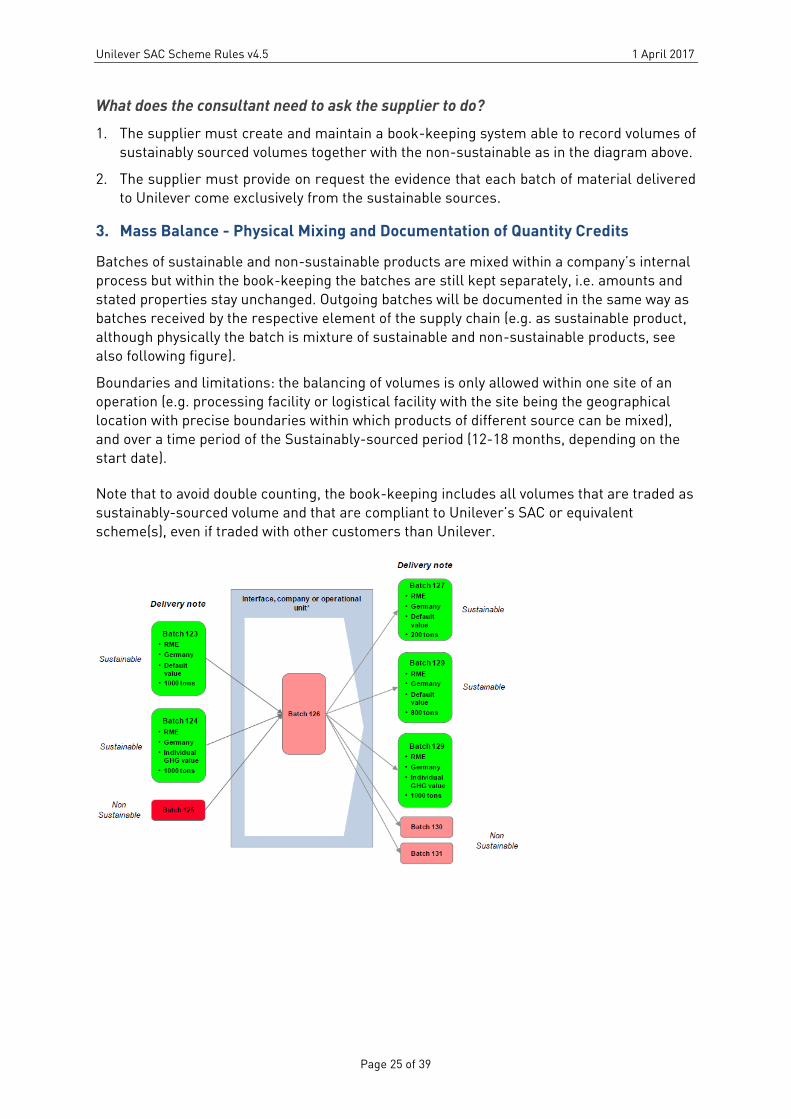

3. Mass Balance - Physical Mixing and Documentation of Quantity Credits

Batches of sustainable and non-sustainable products are mixed within a company’s internal

process but within the book-keeping the batches are still kept separately, i.e. amounts and

stated properties stay unchanged. Outgoing batches will be documented in the same way as

batches received by the respective element of the supply chain (e.g. as sustainable product,

although physically the batch is mixture of sustainable and non-sustainable products, see

also following figure).

Boundaries and limitations: the balancing of volumes is only allowed within one site of an

operation (e.g. processing facility or logistical facility with the site being the geographical

location with precise boundaries within which products of different source can be mixed),

and over a time period of the Sustainably-sourced period (12-18 months, depending on the

start date).

Note that to avoid double counting, the book-keeping includes all volumes that are traded as

sustainably-sourced volume and that are compliant to Unilever’s SAC or equivalent

scheme(s), even if traded with other customers than Unilever.

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 26 of 39

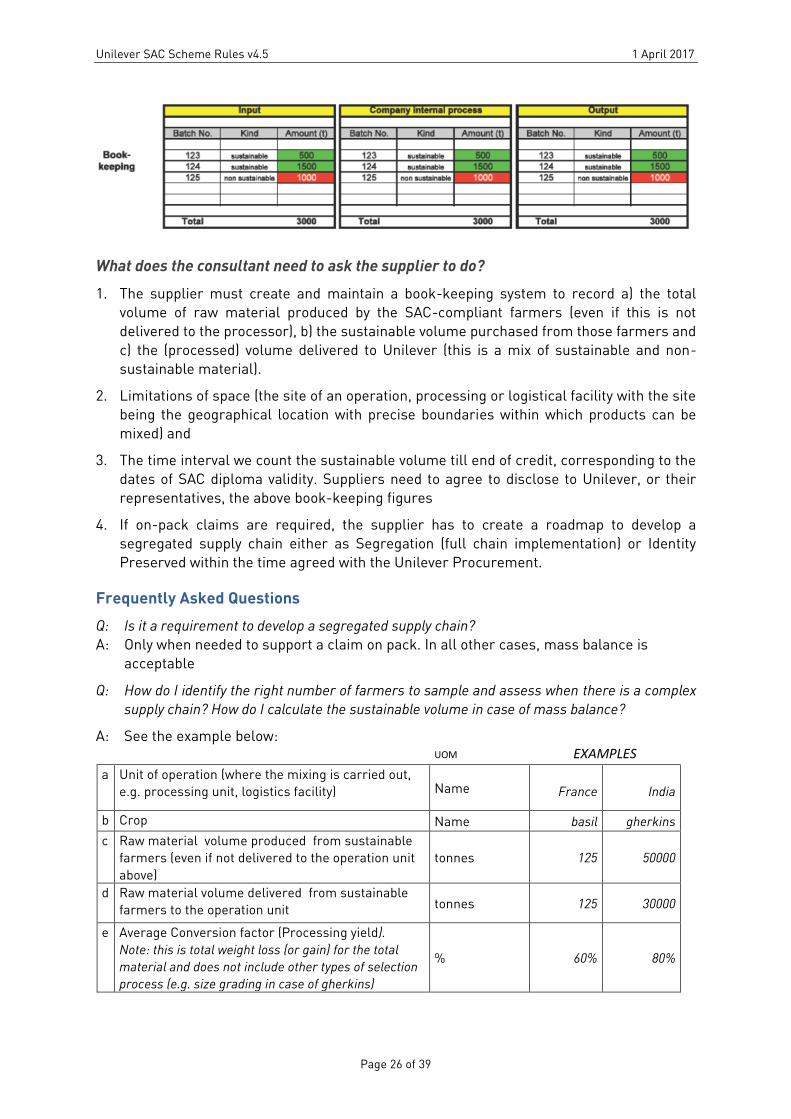

What does the consultant need to ask the supplier to do?

1. The supplier must create and maintain a book-keeping system to record a) the total

volume of raw material produced by the SAC-compliant farmers (even if this is not

delivered to the processor), b) the sustainable volume purchased from those farmers and

c) the (processed) volume delivered to Unilever (this is a mix of sustainable and non-

sustainable material).

2. Limitations of space (the site of an operation, processing or logistical facility with the site

being the geographical location with precise boundaries within which products can be

mixed) and

3. The time interval we count the sustainable volume till end of credit, corresponding to the

dates of SAC diploma validity. Suppliers need to agree to disclose to Unilever, or their

representatives, the above book-keeping figures

4. If on-pack claims are required, the supplier has to create a roadmap to develop a

segregated supply chain either as Segregation (full chain implementation) or Identity

Preserved within the time agreed with the Unilever Procurement.

Frequently Asked Questions

Q: Is it a requirement to develop a segregated supply chain?

A: Only when needed to support a claim on pack. In all other cases, mass balance is

acceptable

Q: How do I identify the right number of farmers to sample and assess when there is a complex

supply chain? How do I calculate the sustainable volume in case of mass balance?

A: See the example below:

UOM EXAMPLES

a Unit of operation (where the mixing is carried out,

e.g. processing unit, logistics facility) Name

France

India

b Crop Name basil gherkins

c Raw material volume produced from sustainable

farmers (even if not delivered to the operation unit

above)

tonnes 125 50000

d Raw material volume delivered from sustainable

farmers to the operation unit tonnes 125 30000

e Average Conversion factor (Processing yield).

Note: this is total weight loss (or gain) for the total

material and does not include other types of selection

process (e.g. size grading in case of gherkins)

% 60% 80%

Unilever SAC Scheme Rules v4.5 1 April 2017

Page 27 of 39

f Semi-processed saleable sustainable material

available for Unilever (credits) [c*e] tonnes 75 24000

g Start of the last cropping cycle as reference time to

start counting the volume credit (dd/mm/yyyy) 01/07/2014 01/03/2014

i SAC diploma validity ‘from date’ (the date from

which we start counting the credit as Sustainably

Sourced)

(dd/mm/yyyy) 30/11/2014 30/05/2014

j SAC diploma validity ‘to date’ (the date on which we

stop counting the credit as Sustainably Sourced) (dd/mm/yyyy) 31/12/2015 30/06/2015

Q: Would suppliers be willing to disclose their sensitive information such as the UL volume

purchased versus their total volume?

A: Suppliers need to agree to disclose only the minimum information needed to ensure

transparency of the mass balance calculation to external auditors.

Q: What if we have a trading organisations selling product to Unilever coming from separate

sustainable and ‘not-sustainable’ sources (i.e. just an invoicing activity)?

A: In this case mass balance can be applied only to each single source.

Q: Who advises the supplier about the elements of the mass balance approach (i.e: format of the

book-keeping system, volume of raw material sustainably sourced, roadmap to segregated

supply, time intervals etc).

A: Unilever or their representative (e.g.: Control Union within their role of supplier

consultant.

Version December 2014

Page 28 of 39

ANNEX V – WILD HARVESTING RISK ASSESSMENT TEMPLATE

Template for Risk Assessment on Wild Collection

Name supplier: Country: Province: Crop: Primary Processor: Address: Assessor: Accompanied by:

Assessment date: Executed by:

[Insert general photo if available]

Version December 2014

Page 29 of 39

Index;

1. Summary of findings

2. Region description

3. Region mapping - Sourcing / wild collection area

4. Harvest and Crop description

5. Collectors profile

6. Supply Chain information and structure

7. Laws and legislation

8. Scope assessment

9. Risk assessment

10. Improvement Action Plan

Version December 2014

Page 30 of 39

1. SUMMARY OF FINDINGS Insert text to indicate that this should summarise findings including main risks and improvements

recommended.

2. REGION DESCRIPTION

Insert text to indicate geography, size and ownership of the land.

3. REGION MAPPING - SOURCING / WILD COLLECTION AREA

[Insert appropriate maps to show the sourcing area]

4. HARVEST AND CROP DESCRIPTION

Insert relevant information about the crop (including its IUCN status) and the cropping cycle should

be included here. Add any appropriate photos.

5. COLLECTORS PROFILE

Insert information on the number of collectors in the area, gender and age profile and further relevant information e.g. whether local, indigenous or immigrant workers etc. Add any relevant

photos.

6. SUPPLY CHAIN INFORMATION AND STRUCTURE

Version December 2014

Page 31 of 39

Include information on the chain from field to consumers, harvesting rate, number of traders,

processors etc. involved. And any certifications held etc.

7. LAWS AND LEGISLATION

Include information on relevant legislation and enforcement activities, requirements for permits, licenses and/or other restrictions.

8. FUNDAMENTAL REQUIREMENTS11

Compliance

Yes No NA

If required by legislation, an authorisation or license to harvest from local responsible department (State forestry, management of the wild areas) is presented. Date of issue cannot be older than 1 year if expiration is not stated.

* Laws, regulations and permits relating to harvesting are understood and respected by supplier, processors and collectors

Conservation status of the area and wild harvest material has been assessed

Remarks: [Insert any relevant comments on the above requirements, particularly if any are marked N/A.

Comments should describe what form the assessment of conservation status takes.]

9. RISK ASSESSMENT1

Users of this template need to consider both the SEVERITY of the hazard and the

LIKELIHOOD of it taking place when coming to a conclusion on the final level of risk. Those risks marked with an * indicate a hazard of highest severity.

Risk exists

11 Requirements marked with an * and in bold text show areas that are mandatory in the Unilever SAC

Version December 2014

Page 32 of 39

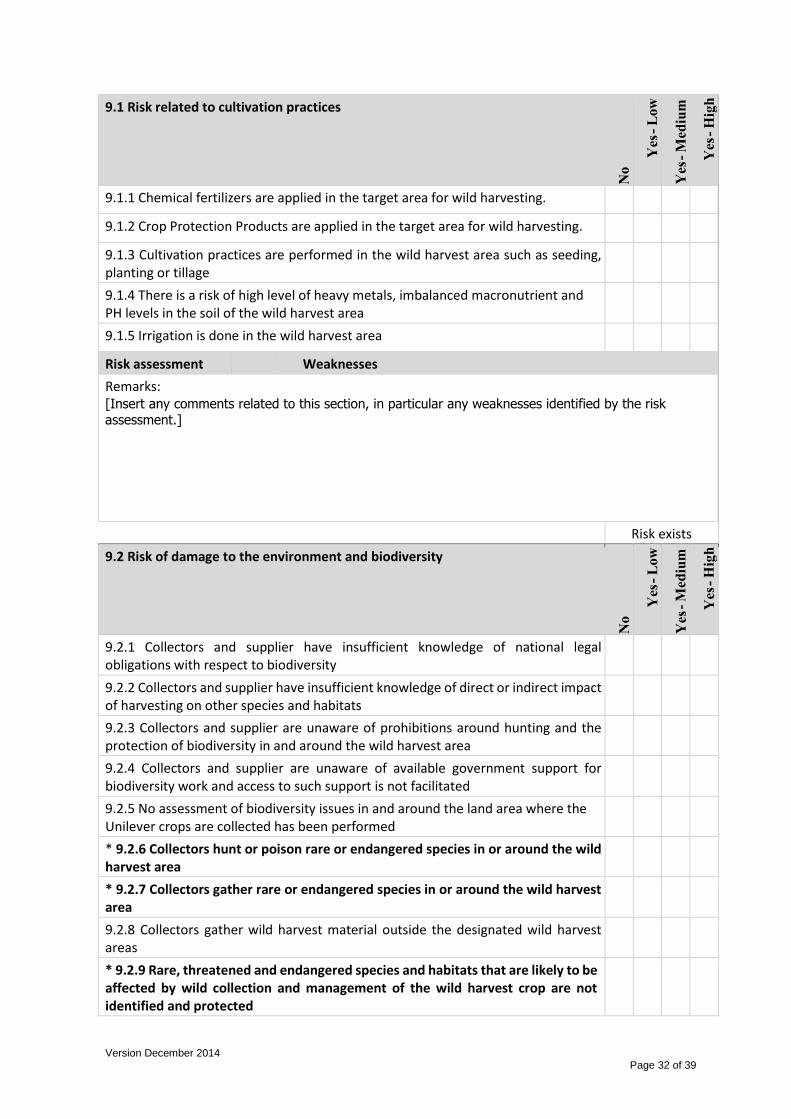

9.1 Risk related to cultivation practices

9.1.1 Chemical fertilizers are applied in the target area for wild harvesting.

9.1.2 Crop Protection Products are applied in the target area for wild harvesting.

9.1.3 Cultivation practices are performed in the wild harvest area such as seeding, planting or tillage

9.1.4 There is a risk of high level of heavy metals, imbalanced macronutrient and PH levels in the soil of the wild harvest area

9.1.5 Irrigation is done in the wild harvest area

Risk assessment Weaknesses

Remarks: [Insert any comments related to this section, in particular any weaknesses identified by the risk

assessment.]

Risk exists

9.2 Risk of damage to the environment and biodiversity

9.2.1 Collectors and supplier have insufficient knowledge of national legal obligations with respect to biodiversity

9.2.2 Collectors and supplier have insufficient knowledge of direct or indirect impact of harvesting on other species and habitats

9.2.3 Collectors and supplier are unaware of prohibitions around hunting and the protection of biodiversity in and around the wild harvest area

9.2.4 Collectors and supplier are unaware of available government support for biodiversity work and access to such support is not facilitated

9.2.5 No assessment of biodiversity issues in and around the land area where the Unilever crops are collected has been performed

* 9.2.6 Collectors hunt or poison rare or endangered species in or around the wild harvest area

* 9.2.7 Collectors gather rare or endangered species in or around the wild harvest area

9.2.8 Collectors gather wild harvest material outside the designated wild harvest areas

* 9.2.9 Rare, threatened and endangered species and habitats that are likely to be affected by wild collection and management of the wild harvest crop are not identified and protected

Version December 2014

Page 33 of 39

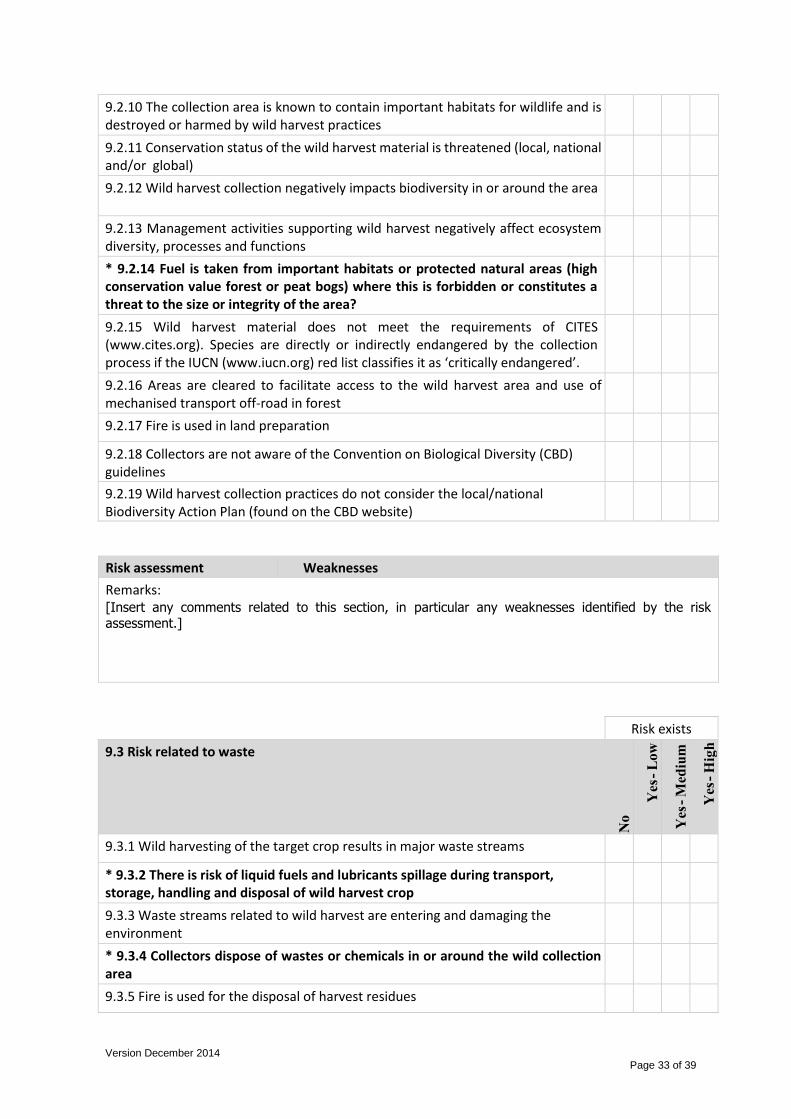

9.2.10 The collection area is known to contain important habitats for wildlife and is destroyed or harmed by wild harvest practices

9.2.11 Conservation status of the wild harvest material is threatened (local, national and/or global)

9.2.12 Wild harvest collection negatively impacts biodiversity in or around the area

9.2.13 Management activities supporting wild harvest negatively affect ecosystem diversity, processes and functions

* 9.2.14 Fuel is taken from important habitats or protected natural areas (high conservation value forest or peat bogs) where this is forbidden or constitutes a threat to the size or integrity of the area?

9.2.15 Wild harvest material does not meet the requirements of CITES (www.cites.org). Species are directly or indirectly endangered by the collection process if the IUCN (www.iucn.org) red list classifies it as ‘critically endangered’.

9.2.16 Areas are cleared to facilitate access to the wild harvest area and use of mechanised transport off-road in forest

9.2.17 Fire is used in land preparation

9.2.18 Collectors are not aware of the Convention on Biological Diversity (CBD) guidelines

9.2.19 Wild harvest collection practices do not consider the local/national Biodiversity Action Plan (found on the CBD website)

Risk assessment Weaknesses

Remarks: [Insert any comments related to this section, in particular any weaknesses identified by the risk assessment.]

Risk exists

9.3 Risk related to waste

9.3.1 Wild harvesting of the target crop results in major waste streams

* 9.3.2 There is risk of liquid fuels and lubricants spillage during transport, storage, handling and disposal of wild harvest crop

9.3.3 Waste streams related to wild harvest are entering and damaging the environment

* 9.3.4 Collectors dispose of wastes or chemicals in or around the wild collection area

9.3.5 Fire is used for the disposal of harvest residues

Version December 2014

Page 34 of 39

* 9.3.6 Hazardous waste is stored in areas where unauthorised people have access

Risk assessment Weaknesses

Remarks: [Insert any comments related to this section, in particular any weaknesses identified by the risk

assessment.]

Risk exists

9.4 Risk of natural resource depletion

9.4.1 The collection rate exceeds the species’ ability to regenerate over the long term

9.4.2 The target material is harvested at inappropriate times (just before pollinating, breeding, etc.)

9.4.3 Scale and trend of use and trade in the wild harvest material is high or increasing

9.4.4 Crop or plant is damaged or destroyed by collection practice

9.4.5 Harvesting and removing crop from the area leads to severe nutrient loss in the soil

Other:

Risk assessment Weaknesses

Remarks: [Insert any comments related to this section, in particular any weaknesses identified by the risk assessment. Add any relevant photos.]

Version December 2014

Page 35 of 39

Risk exists

9.5 Risk of non-compliance with local or international legislation and regulations

* 9.5.1 Children are hired or contracted as collectors

9.5.2 Young collectors perform hazardous work

9.5.3 Children helping with collecting are not well supervised; the amount of work they do is unclear

* 9.5.4 Collectors or workers are forced or perform compulsory labour related to the wild harvest material

9.5.5 Terms and conditions, and payment for contracted collectors are not well defined

* 9.5.6 Payments for harvested materials do not comply with national regulations

* 9.5.7 There is lack of clarity on legal situation for collectors and workers

9.5.8 Collectors do not comply with rules and regulations in relation to the wild harvest area or the wild harvest crop

Other:

Risk assessment Weaknesses

[Insert any comments related to this section, in particular any weaknesses identified by the risk

assessment.]

Risk exists

9.6 Risk of social inequity

* 9.6.1 Land tenure, ownership, use rights and management authority of crops or wild harvest area are not well defined

9.6.2 Local communities traditional use and practice, access rights and cultural heritage of land and material is disturbed or threatened

9.6.3 Benefit-sharing with local communities has not been arranged with appropriate agreements according to the Nagoya Protocol

9.6.4 Particular social groups, tribes, castes etc. are excluded from participation in harvest practice

9.6.5 Age, gender, sexual orientation, religion etc. exclude people from participation in harvest practice

Version December 2014

Page 36 of 39

9.6.6 There is potential for conflicts between collectors or groups and lack of local agreements to avoid conflict

9.6.7 Grievance procedures are unavailable or people are not confident to use them

9.6.8 Evaluation has shown there to be a case for benefit sharing (as related to the Nagoya Protocol)

* 9.6.9 There is no individual responsible for ensuring workers' rights and fair pay

Other:

Risk assessment Weaknesses

[Insert any comments related to this section, in particular any weaknesses identified by the risk assessment.]

Risk exists

9.7 Risks to/from the local economy

9.7.1 There is no fair system of payment for collectors or workers

9.7.2 There is lack of transparency in terms of payment for collectors or workers

9.7.3 There is no timely announcement of prices for the harvested material

9.7.4 Untimely payment for collectors or workers

9.7.5 Harvesting makes other local businesses lose viability

9.7.6 Harvesting is becoming unsustainable because more lucrative opportunities are opening up locally

9.7.7 There are potential conflicts between harvesting and other seasonal activities.

9.7.8 There is lack of transparency in pricing

Risk assessment Weaknesses

Remarks: [Insert any comments related to this section, in particular any weaknesses identified by the risk

assessment.]

Version December 2014

Page 37 of 39

Risk exists

9.8 Supply chain and traceability

9.8.1 No traceability or uncertainty on where the material is harvested from

9.8.2 Supplier has no direct contact with or influence on harvesters

9.8.3 Size of the collection area is too big to be effectively checked and controlled

9.8.4 Number of collectors is too high to be effectively checked and controlled

9.8.5 Wild harvest material under scope of this assessment is mixed with conventional material

9.8.6 Traceability of material is lost during transport

9.8.7 Record keeping of volumes harvested per collector or collector group is none existent or unreliable

Risk assessment Weaknesses

Remarks:

[Insert any comments related to this section, in particular any weaknesses identified by the risk assessment. Include any relevant photos.]

Risk exists

9.9 Health and Safety

9.9.1 Dangerous practices involved in harvesting (tree climbing, working on steep slopes)

9.9.2 Harvesting is done with tools or sharp implements

9.9.3 Harvesting is done by using ladders and working at heights

9.9.4 Appropriate safety equipment either not provided, not used or collectors did not receive training on how to use

* 9.9.5 Agro-chemical application is done by untrained personnel

9.9.6 Road worthiness of vehicles in poor condition or not checked

9.9.7 Spraying or fumigation (DDT, Synthetic pyrethroids) by the local agency for the for the management of contagious disease like malaria, cholera etc.

Risk assessment Weaknesses

Version December 2014

Page 38 of 39

Remarks [Insert any comments related to this section, in particular any weaknesses identified by the risk

assessment. Include any relevant photos.]

Risk exists

9.10 Food Safety and Quality

9.10.1 There is risk of contamination in the field from nearby areas under agricultural cultivation

9.10.2 Personal hygiene of harvesters to ensure cleanliness of products is insufficient

9.10.3 There is risk of poor quality or degradation of harvested crop entering the supply chain

9.10.4 There is risk of contamination of product during storage

9.10.5 There is risk of contamination during harvest season because wild harvest and cultivated materials are harvested simultaneously

9.10.6 There is risk of contamination because collection points for wild harvest and cultivated materials are the same

9.10.7 There is risk of contamination during transport

Risk assessment Weaknesses

Remarks: [Insert any comments related to this section, in particular any weaknesses identified by the risk

assessment.]

Version December 2014

Page 39 of 39

10. IMPROVEMENT ACTION PLAN

Weakness Improvement action Deadline

Risks related to cultivation practices

Risk of damage to the environment and biodiversity

Risk related to waste

Risk of natural resource depletion

Risk of non-compliance with local or international legislation and regulations

Risk of social inequity

Risks to/from the local economy

Supply chain and traceability

Health and Safety

Food Safety and Quality