Torsten Hemme. Разработки доходов фермеров во всем мире....

23

18/10/2016 © IFCN 2016 | 1 Developments of farmers income all over the world Torsten Hemme, [email protected] IFCN Dairy Research Network, Germany

-

Upload

dairynews -

Category

Presentations & Public Speaking

-

view

269 -

download

0

Transcript of Torsten Hemme. Разработки доходов фермеров во всем мире....

18/10/2016 © IFCN 2016 | 1

Developments of farmers income all

over the world

Torsten Hemme,

IFCN Dairy Research Network, Germany

18/10/2016 © IFCN 2016 | 2

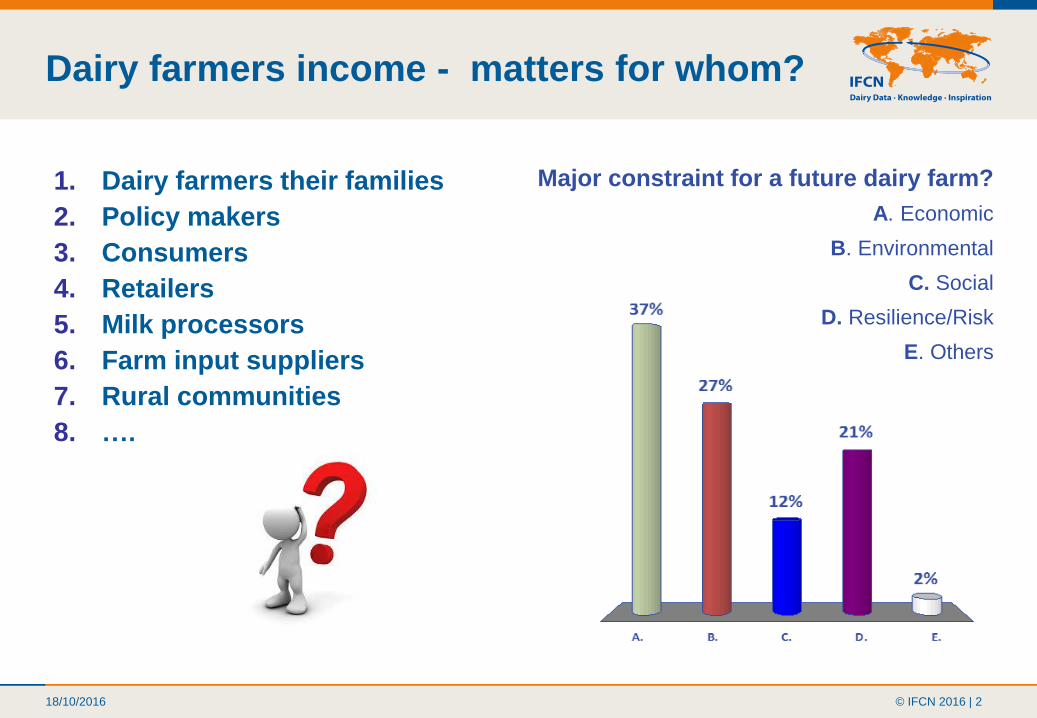

Dairy farmers income - matters for whom?

1. Dairy farmers their families

2. Policy makers

3. Consumers

4. Retailers

5. Milk processors

6. Farm input suppliers

7. Rural communities

8. ….

Major constraint for a future dairy farm?

A. Economic

B. Environmental

C. Social

D. Resilience/Risk

E. Others

18/10/2016 © IFCN 2016 | 3

Agenda

1. The IFCN Network Concept

2. Milk prices

3. Dairy farmers income 2015

4. Monthly income trends

5. Sum up

18/10/2016 © IFCN 2016 | 4

Mission:

We create a better understanding of the dairy world by providing

comparable data, knowledge and inspiration.

IFCN - The Dairy Research Network

The IFCN Network approach – consisting of three pillars

- the IFCN Research Network of researchers

- the IFCN Supporter Partner Network of companies/institutions

- the IFCN Research Center with > 15 dairy economists.

18/10/2016 © IFCN 2016 | 5

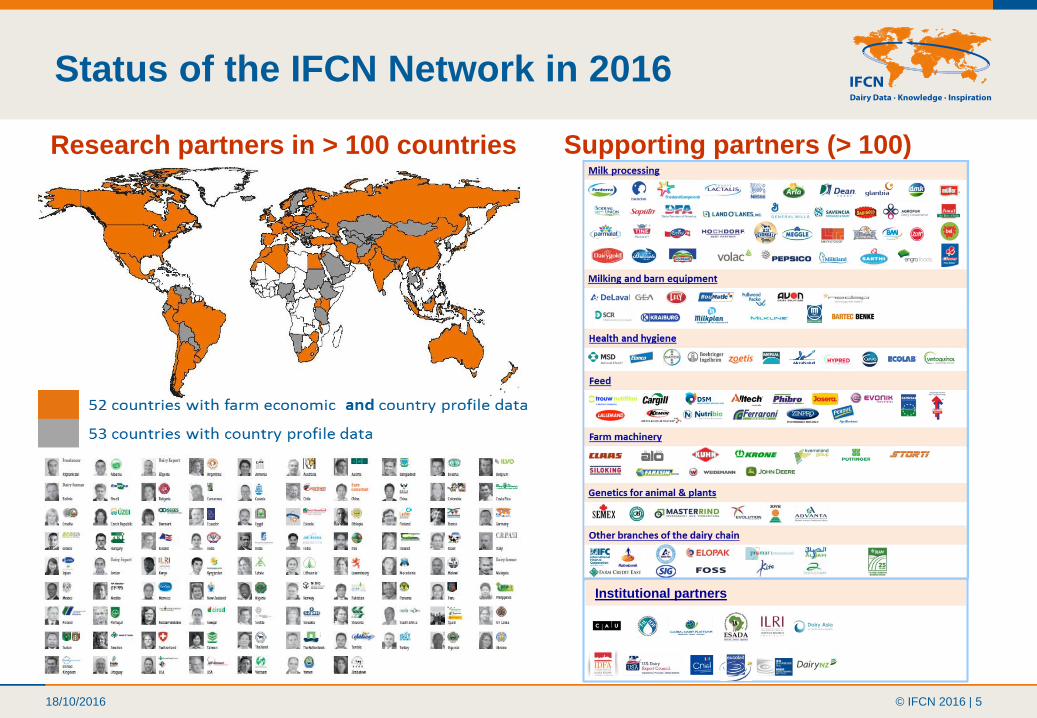

Research partners in > 100 countries

Status of the IFCN Network in 2016

Supporting partners (> 100)

Institutional partners

18/10/2016 © IFCN 2016 | 6

Agenda

1. The IFCN Network Concept

2. Milk prices

3. Dairy farmers income 2015

4. Monthly income trends

5. Sum up

18/10/2016 © IFCN 2016 | 7

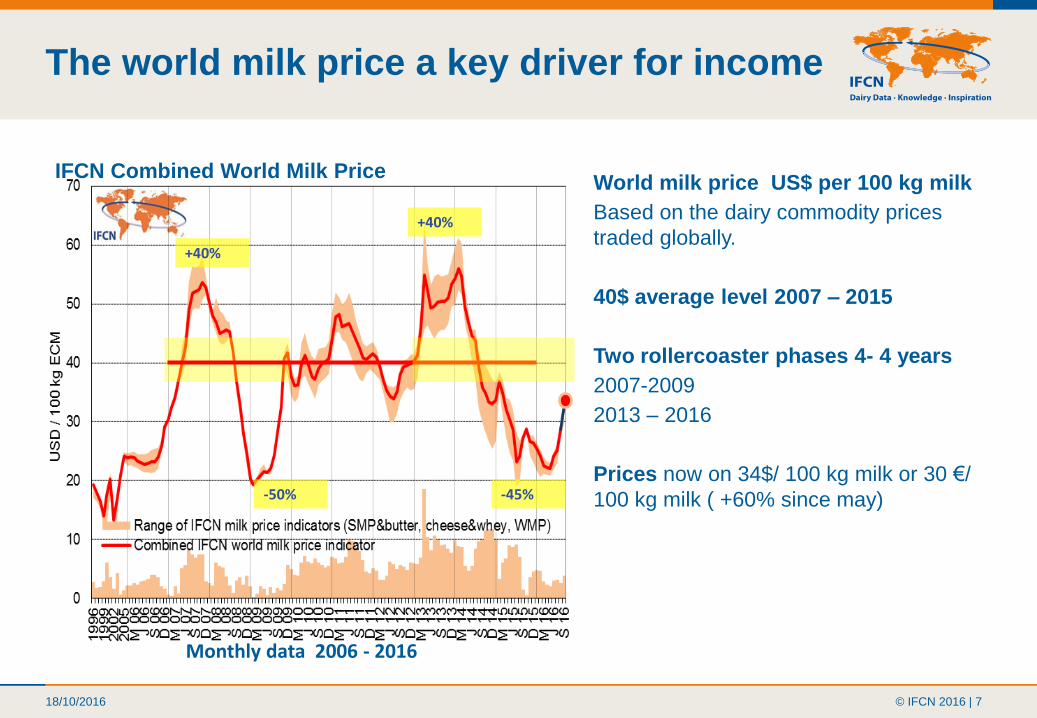

The world milk price a key driver for income

Monthly data 2006 - 2016

World milk price US$ per 100 kg milk

Based on the dairy commodity prices

traded globally.

40$ average level 2007 – 2015

Two rollercoaster phases 4- 4 years

2007-2009

2013 – 2016

Prices now on 34$/ 100 kg milk or 30 €/

100 kg milk ( +60% since may)

IFCN Combined World Milk Price

+40%

-50%

+40%

-45%

18/10/2016 © IFCN 2016 | 8Source: IFCN Monthly Real Time Data

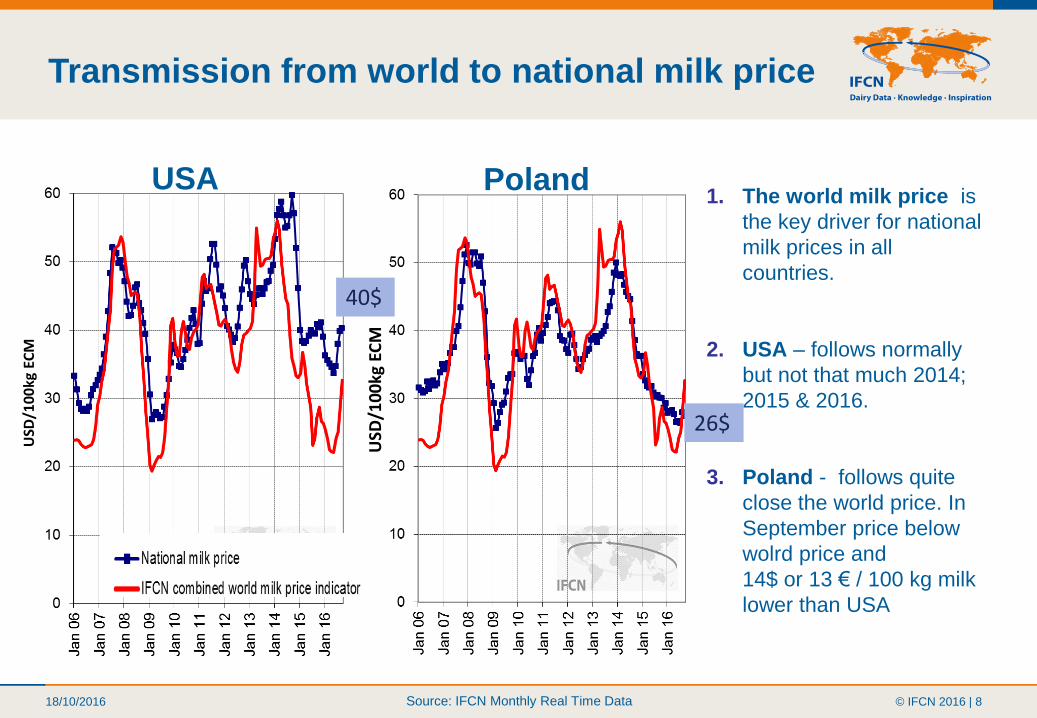

USA Poland1. The world milk price is

the key driver for national

milk prices in all

countries.

2. USA – follows normally

but not that much 2014;

2015 & 2016.

3. Poland - follows quite

close the world price. In

September price below

wolrd price and

14$ or 13 € / 100 kg milk

lower than USA

40$

26$

USD

/10

0kg

EC

M

USD

/10

0kg

EC

M

Transmission from world to national milk price

18/10/2016 © IFCN 2016 | 9

Deviation of national milk price from world milk price

September 2016 (real time estimation)

21

8

3

-6

0

0

-5

25

-7

-6-4

-12 -7EU weighted average is -4 USDabove world milk price

1

5

19

18/10/2016 © IFCN 2016 | 10

Agenda

1. The IFCN Network Concept

2. Milk prices

3. Dairy farmers income 2015

4. Monthly income trends

5. Sum up

18/10/2016 © IFCN 2016 | 11

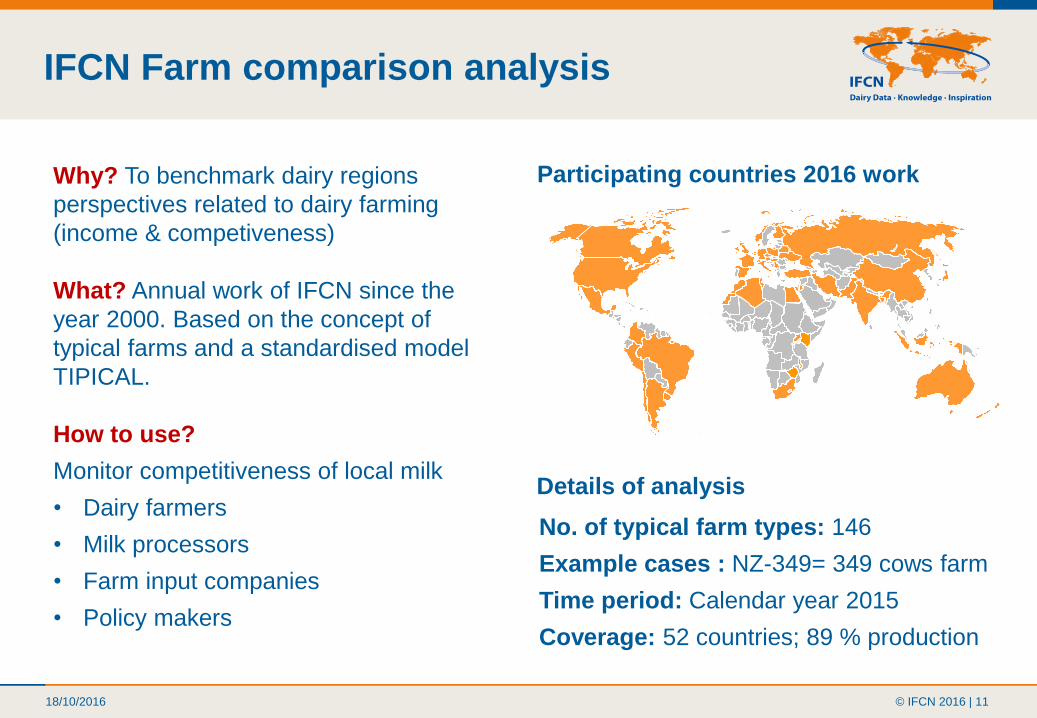

IFCN Farm comparison analysis

Participating countries 2016 work

No. of typical farm types: 146

Example cases : NZ-349= 349 cows farm

Time period: Calendar year 2015

Coverage: 52 countries; 89 % production

ID

Why? To benchmark dairy regions

perspectives related to dairy farming

(income & competiveness)

What? Annual work of IFCN since the

year 2000. Based on the concept of

typical farms and a standardised model

TIPICAL.

How to use?

Monitor competitiveness of local milk

• Dairy farmers

• Milk processors

• Farm input companies

• Policy makers

Details of analysis

18/10/2016 © IFCN 2016 | 12

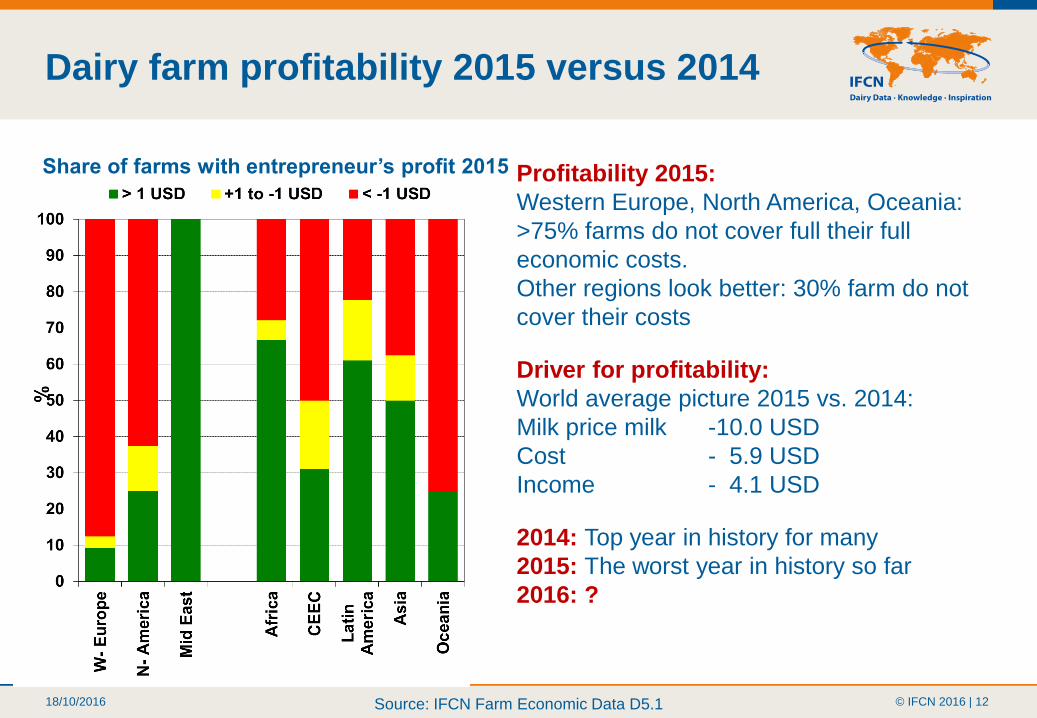

Dairy farm profitability 2015 versus 2014

Share of farms with entrepreneur’s profit 2015

Source: IFCN Farm Economic Data D5.1

Profitability 2015:

Western Europe, North America, Oceania:

>75% farms do not cover full their full

economic costs.

Other regions look better: 30% farm do not

cover their costs

Driver for profitability:

World average picture 2015 vs. 2014:

Milk price milk -10.0 USD

Cost - 5.9 USD

Income - 4.1 USD

2014: Top year in history for many

2015: The worst year in history so far

2016: ?

18/10/2016 © IFCN 2016 | 13

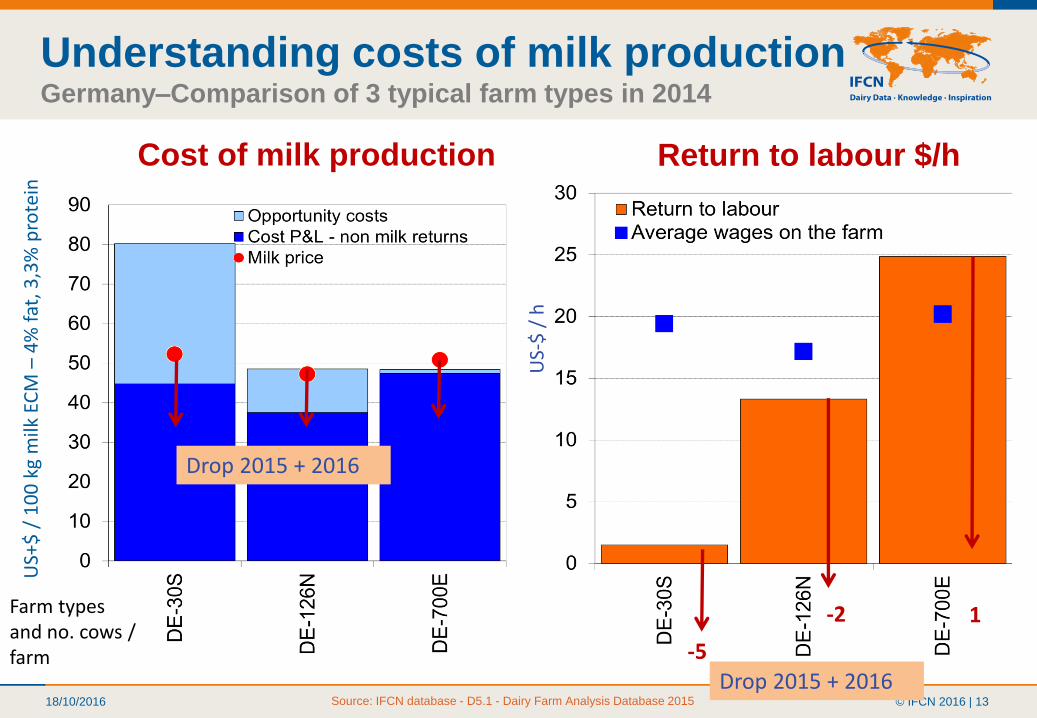

Understanding costs of milk production Germany–Comparison of 3 typical farm types in 2014

Cost of milk production Return to labour $/h

Farm typesand no. cows / farm

Source: IFCN database - D5.1 - Dairy Farm Analysis Database 2015

US+

$ /

10

0 k

g m

ilk E

CM

–4

% f

at, 3

,3%

pro

tein

US-

$ /

h

-5

-2 1

Drop 2015 + 2016

Drop 2015 + 2016

18/10/2016 © IFCN 2016 | 14

Agenda

1. The IFCN Network Concept

2. Milk prices

3. Dairy farmers income 2015

4. Monthly income trends

5. Sum up

18/10/2016 © IFCN 2016 | 15

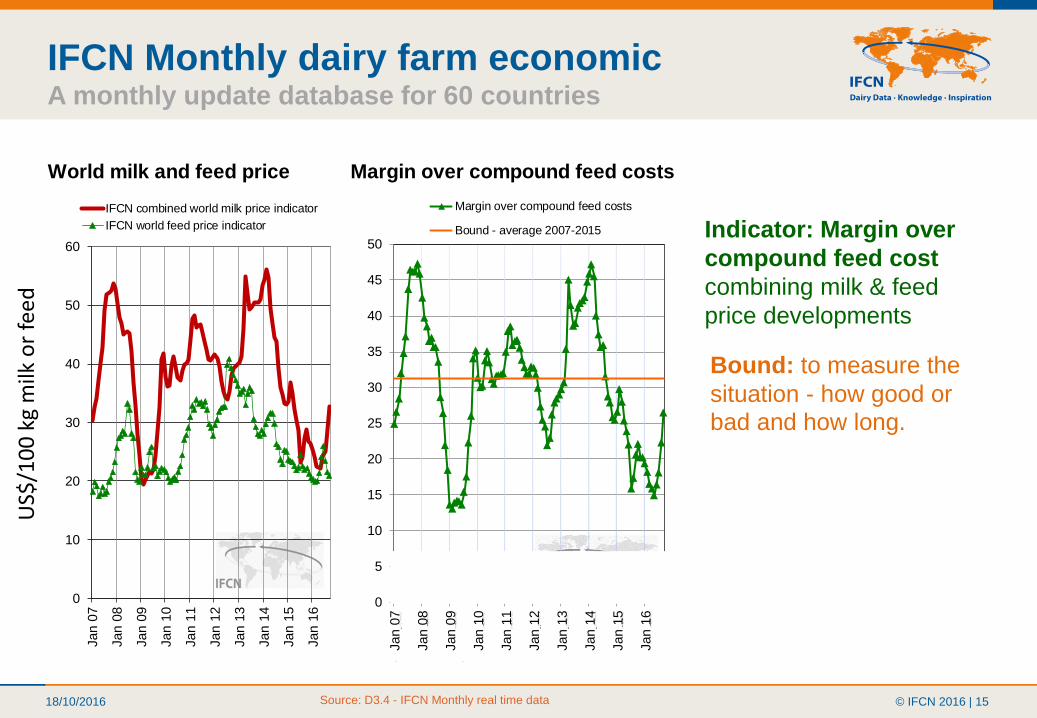

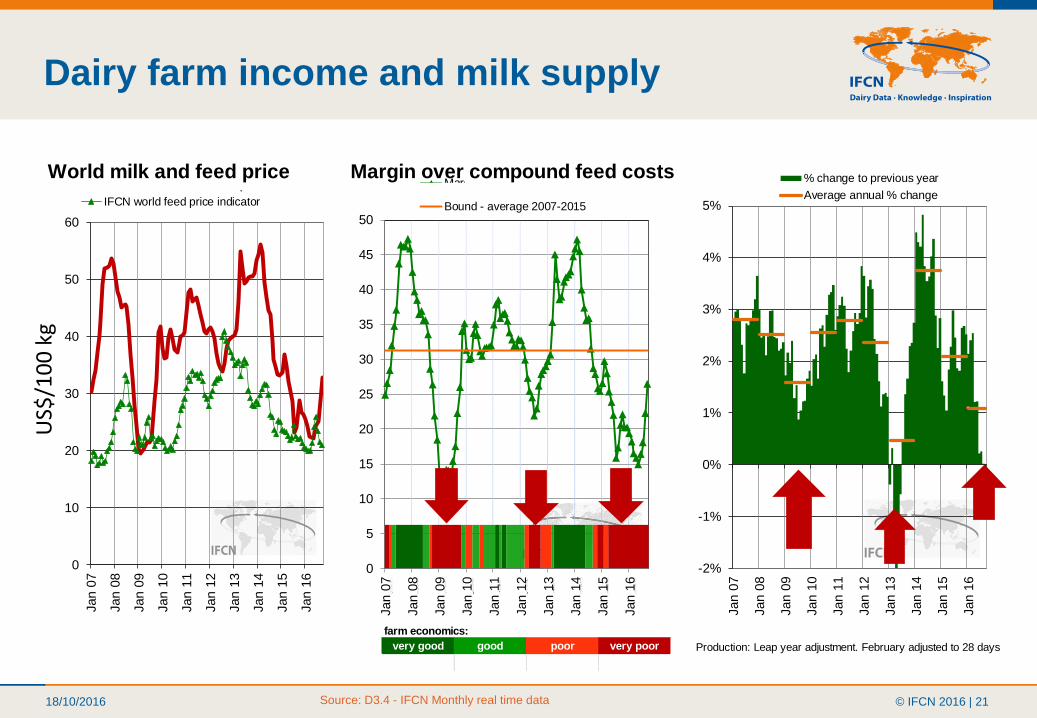

World milk and feed price Margin over compound feed costs

farm economics:

very good good poor very poor

0

5

10

15

20

25

30

35

40

45

50

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

Margin over compound feed costs

Bound - average 2007-2015

0

10

20

30

40

50

60

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

IFCN combined world milk price indicator

IFCN world feed price indicator

Source: D3.4 - IFCN Monthly real time data

IFCN Monthly dairy farm economicA monthly update database for 60 countries

Indicator: Margin over

compound feed cost

combining milk & feed

price developments

Bound: to measure the

situation - how good or

bad and how long.

US$

/10

0 k

g m

ilk o

rfe

ed

18/10/2016 © IFCN 2016 | 16

World milk and feed price Margin over compound feed costs

farm economics:

very good good poor very poor

0

5

10

15

20

25

30

35

40

45

50

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

Margin over compound feed costs

Bound - average 2007-2015

0

10

20

30

40

50

60

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

IFCN combined world milk price indicator

IFCN world feed price indicator

Source: D3.4 - IFCN Monthly real time data

IFCN Monthly dairy farm economicA monthly update database for 60 countries

Indicator: Margin over

compound feed cost

combining milk & feed

price developments

Bound: to measure the

situation - how good or

bad and how long.

US$

/10

0 k

g m

ilk o

rfe

ed

18/10/2016 © IFCN 2016 | 17

World milk and feed price Margin over compound feed costs

farm economics:

very good good poor very poor

0

5

10

15

20

25

30

35

40

45

50

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

Margin over compound feed costs

Bound - average 2007-2015

0

10

20

30

40

50

60

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

IFCN combined world milk price indicator

IFCN world feed price indicator

Source: D3.4 - IFCN Monthly real time data

IFCN Monthly dairy farm economicA monthly update database for 60 countries

Indicator: Margin over

compound feed cost

combining milk & feed

price developments

Bound: to measure the

situation - how good or

bad and how long.

Traffic lights: judgment

on farm economics

US$

/10

0 k

g m

ilk o

rfe

ed

Distance to bound

• ≥15% dark green

• +15% light green

farm economics:

very good good poor very poor

18/10/2016 © IFCN 2016 | 18

“Farmers income”- 5 countries since 2006

• -15% light red

• ≤-15% dark red

Distance to bound

• ≥15% dark green

• +15% light greenfarm economics:

very good good poor very poor

Source: D3.4 - IFCN Monthly real time data

Dairy farm economics based on margin over compound feed in national currency Country comparison

J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F M A M J J A S O N D J F # A # J J A S

World market 0 0 1 3 3 2 2 2 2 2 2 2 2 2 2 2 2 3 3 3 1 0 0 0 0 0 0 0 0 0 0 0 0 0 3 3 1 1 1 3 3 3 1 1 3 3 3 3 3 2 2 3 2 2 3 3 3 3 3 3 3 3 1 1 0 0 0 0 0 1 1 1 1 1 3 2 2 2 2 2 2 2 2 2 2 2 2 2 2 3 3 3 1 1 0 0 0 1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Poland 1 1 1 1 3 3 3 3 3 2 2 2 2 3 3 3 3 1 1 1 1 1 1 0 0 0 0 0 0 0 0 1 1 1 1 1 1 1 1 1 1 1 1 3 1 1 3 1 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 3 3 3 2 2 2 2 2 2 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 0 0 0 0 0 0

United States of

America 0 0 1 1 3 2 2 2 2 2 2 2 3 3 1 1 3 3 3 3 1 1 1 1 0 0 0 0 0 0 0 0 0 0 0 1 1 1 0 0 0 1 1 1 1 1 1 0 0 1 3 3 3 2 2 2 2 3 3 3 1 1 1 1 0 0 0 1 1 3 3 3 1 1 1 1 3 1 1 3 3 3 3 2 2 2 2 2 2 2 2 2 2 2 2 3 1 1 1 1 1 1 1 1 1 1 1 1 1 0 0 0 0 0 1 1 1

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

farm economics:

very good good poor very poor

J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F # A # J J A S O N D J F M A M J J A S O N D J F # A # J J A S

Brazil 0 0 1 1 1 3 2 2 2 2 2 3 3 3 3 3 3 3 3 3 1 1 1 0 0 0 0 0 0 1 3 3 3 3 1 0 0 0 1 3 3 3 1 1 1 1 1 1 1 1 1 1 1 3 3 3 3 3 3 3 1 3 3 1 1 1 1 1 1 1 1 1 1 1 1 3 1 3 3 2 2 2 2 3 1 1 3 3 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 3 1 1 1 1 1 1 3 3 3 3 2 2 2

South Africa 0 0 0 1 1 3 3 3 2 2 2 2 2 2 2 2 2 2 2 3 3 3 3 3 3 3 3 3 3 3 2 2 2 3 3 3 3 3 2 2 3 3 3 3 1 1 1 1 1 0 1 0 0 1 1 1 0 1 1 1 1 1 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 0 1 1 1 1 1 1 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 1 1 0 1 1 1 1 1 3 1 1 3 3 3

China 0 0 0 0 0 0 0 0 1 2 2 2 2 2 2 2 2 3 3 3 3 2 2 2 3 3 1 1 0 0 0 0 0 1 1 1 1 1 3 3 3 3 3 3 3 1 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 3 3 3 2 2 2 2 2 2 3 3 3 3 3 3 3 3 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 0 0 0 0 0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

18/10/2016 © IFCN 2016 | 19

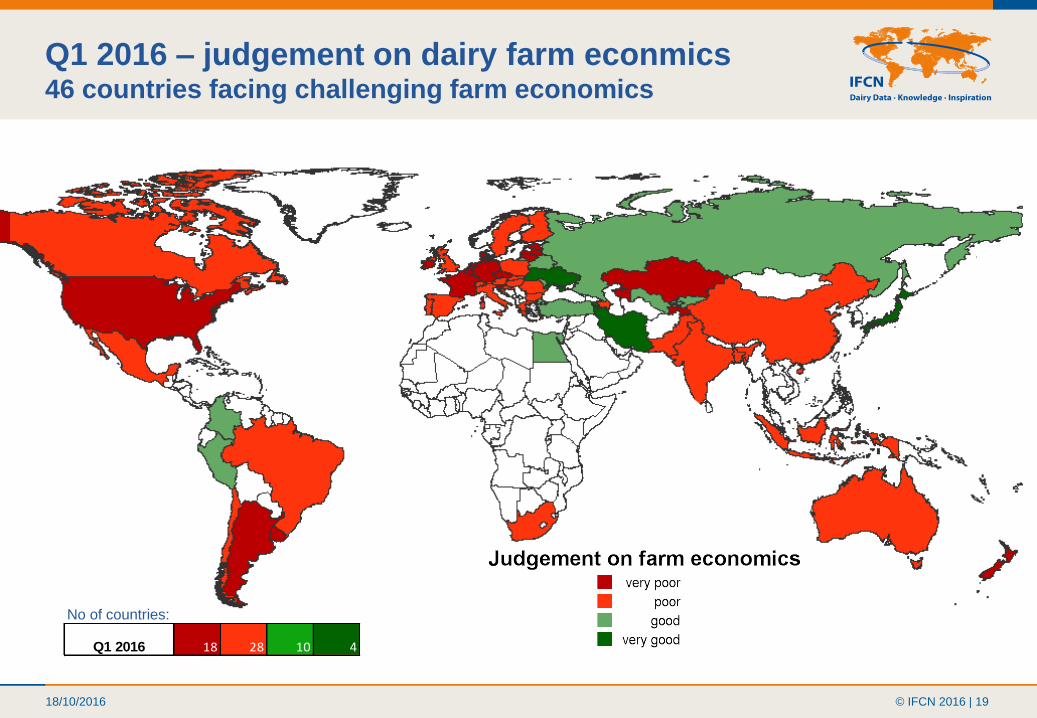

Q1 2016 – judgement on dairy farm econmics46 countries facing challenging farm economics

Q1 2016 18 28 10 4

No of countries:

18/10/2016 © IFCN 2016 | 20

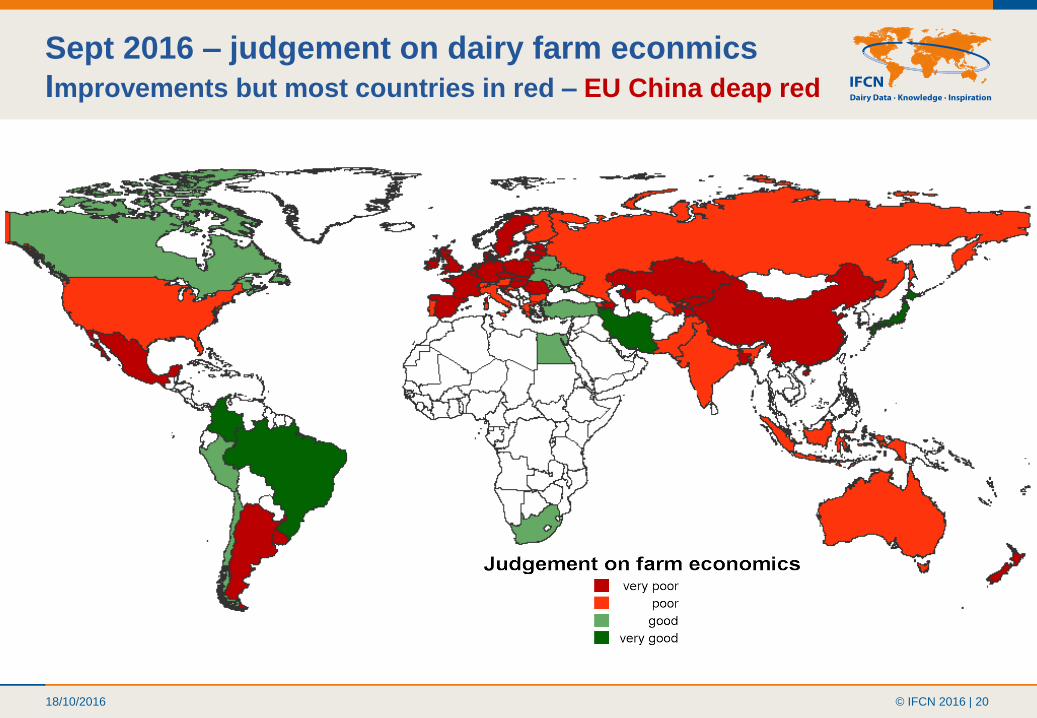

Sept 2016 – judgement on dairy farm econmics

Improvements but most countries in red – EU China deap red

18/10/2016 © IFCN 2016 | 21

farm economics:

very good good poor very poor Production: Leap year adjustment. February adjusted to 28 days

How to use this sheet:

For selecting countries for the charts, please type in the

numbers (country codes) into the yellow boxes below.

0

5

10

15

20

25

30

35

40

45

50

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

Margin over compound feed costs

Bound - average 2007-2015

0

10

20

30

40

50

60

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

IFCN combined world milk price indicator

IFCN world feed price indicator

-2%

-1%

0%

1%

2%

3%

4%

5%

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

% change to previous year

Average annual % change

Source: D3.4 - IFCN Monthly real time data

Dairy farm income and milk supplyU

S$/1

00

kg

World milk and feed price Margin over compound feed costs

farm economics:

very good good poor very poor

0

5

10

15

20

25

30

35

40

45

50

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

Margin over compound feed costs

Bound - average 2007-2015

0

10

20

30

40

50

60

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

Jan 1

5

Jan 1

6

IFCN combined world milk price indicator

IFCN world feed price indicator

18/10/2016 © IFCN 2016 | 22

Summing up

1. We are in the third world dairy farm crisis since 2007: World milk price is

in a rollercoaster mode which means +/- 40% around the mean level

2. Monthly milk price transmission

World milk price drives farmers milk prices in countries with a delay

3. Farm income 2015; 2016

two years with really bad / partly no incomes especially in EU

4. Monthly farm income developments

Despite world milk price recovery most countries income in red

5. Milk supply is responding to dairy farm economics but with delay!!!

Milk production decline globally this now drives prices up

18/10/2016 © IFCN 2016 | 23

Thank you for your attention

IFCN Dairy Research CenterNetwork of IFCN Researchers Network of IFCN Supporters

This presentation is the result of a large number of people

working together since 2000.