學科補習、成績表現與升學結果── 以學測成績與上公立大學為例黃毅志、陳俊瑋 學科補習、成績表現與升學結果──以學測成績與上公立大學為例

科技部TSSCI期刊

期貨與選擇權學刊 Journal of Futures and Options

第九卷第一期 二○一六年四月 Volume 9, Number 1, April 2016

臺灣期貨交易所 2015年4月榮獲「The Asian Banker 2015年度

金融衍生性商品交易所」 2015年9月榮獲「FOW 2015年亞洲區股權類

商品創新契約」 2015年11月榮獲「The Asian Banker 2015年

最佳區域性人民幣期貨交易所」

臺灣期貨交易所繼2004及2009年獲選為Asia Risk雜誌年度風雲

交易所(Derivatives Exchange of the Year)獎項之肯定後,國際財經專

業雜誌亞洲銀行家(The Asian Banker)於2015年4月宣布期交所榮獲

「年度金融衍生性商品交易所」(Financial Derivatives Exchange of the

Year);繼而於9月,因與歐洲期貨交易所跨國合作商品「歐臺期與

歐臺選」(Eurex/TAIFEX Link),榮獲Futures and Options World(FOW)

評選為「2015年亞洲區股權類商品創新契約獎」;11月再獲亞洲銀

行家雜誌肯定,宣布期交所為「2015年最佳區域性人民幣期貨交易

所」(Best Exchange for Offshore RMB FX Futures by Region)。

在主管機關鼎力支持及期貨業界與期交所共同努力下,近年臺

灣期貨市場表現亮眼,2014年交易量首度突破2億口大關,2015年

交易量更成長至2.5億口,為期交所成立以來年度最高量,推動市

場大幅成長原因主要為推出符合交易人多元化需求之商品、交易結

算制度的調整、辦理國內外宣導推廣活動,以及陸續推出多項國際

合作商品所致。

展望未來,期交所將持續以「避險增益、價格發現」為商品及

制度研發之主軸,加快國際合作腳步,達成「活絡期貨交易、服務

實質經濟」目標,並滿足市場參與者各項需求,以不斷強化核心競

爭優勢,為臺灣期貨市場開創新局,注入源源不絕的活力與動能。

期貨與選擇權學刊 Journal of Futures and Options

第九卷 第一期 (中華民國九十七年五月創刊)

發 行 人:劉連煜

總 監:邱文昌

總 編 輯:李存修

編輯委員:王耀輝 古永嘉 朱浩民 李賢源 周行一 俞明德

馬秀如 張森林 張傳章 郭維裕 郭震坤 陳春山

游啟璋 馮震宇 黃金澤 楊光華 葉銀華 廖四郎

薛富井 謝明華

執行編輯:蔡蒔銓

助理編輯:許維敏、矯恒杰、陶富美、蔡季婷

出版者:臺灣期貨交易所股份有限公司

地 址:台北市羅斯福路二段100號14樓 電 話:(02)2369-5678 傳 真:(02)2369-3689 網 址:http://www.taifex.com.tw

編印者:元照出版公司

地 址:台北市館前路18號5樓 電 話:(02)2375-6688 網 址:http://www.angle.com.tw

本刊著作權所有,未經臺灣期貨交易所股份有限公司同意,

不得轉載全部或部分內容。

「期貨與選擇權學刊」 出版政策

臺灣期貨交易所為鼓勵期貨與選擇權領域之學術研究風氣、提

供相關領域學術論文發表管道,以建立與學界之溝通交流平台、吸

引學界關注期貨市場,為臺灣期貨市場之人才培育與制度健全發展

奠定基石,特發行「期貨與選擇權學刊」。

本學刊廣徵有關期貨、選擇權或衍生性商品(含法律規範與制

度)之理論、實證或應用之中、英文學術論文,歡迎海內外學者、

專家及關心期貨市場發展之人士踴躍投稿。

本學刊固定於每年4月、8月及12月出刊,採匿名審稿程序,設

置編輯委員會處理審稿及編輯業務,每篇文稿至少由兩位學者專家

評審,稿件採隨到隨審方式,經刊登之文稿每篇致贈稿酬新台幣1萬元。

本學刊自2013年起榮獲科技部收錄為臺灣社會科學引文索引核

心期刊(TSSCI),並追溯至2010年起算,未來亦將積極申請收錄

於SSCI資料庫,並期望成為期貨與選擇權相關領域之標竿期刊。

欲知更多詳情,請上

期貨與選擇權學刊網站!

編輯手札

本刊發行迄今已逾八個年頭,今年正式邁入第九年,前四年

2008~2011 年的平均每年投稿數僅 13 篇,接下來的四年中

(2012~2015),平均每年投稿數已倍增至26篇,2016年第一季投稿數

7篇,亦能維持高度的投稿能量,而進入TSSCI(2013年)之後,平均

的接受率為32.95%,亦能有效地提昇本刊的質量。

本刊的另一特色是審稿速度極快,2013~2015年的初審平均天數

僅22.18天,2016年第一季更降到僅14.16天。若計算從投稿到審稿定

案的天數,2013~2015年之平均為37.53天,2016年第一季則降為26

天。審稿快速對投稿者相當有利,節省了許多等待的時間,也降低

了投稿的焦慮情緒。2016年底前,本刊將全面採用線上投稿、審

稿,省去了稿件郵寄的時間,相信審稿時間會再進一步縮短。

本期(第九卷第一期)收錄了三篇頗具實務應用價值的文章,包

括王佳真、王尹柔與李君屏探討股價指數之波動性偏態指標與指數

變動之關係;蘇亭丰評估槓桿型與反向型之長短期追蹤績效;以及

洪瑞成與王偉權所分析投機性交易對臺灣期貨市場之影響等,相信

讀者能從中獲得不少啟發。

總編輯 李存修 謹識

於國立臺灣大學

二○一六年四月

Editor’s Notes

At the end of the eighth year since JFO’s inception, we are pleased to

find that the annual number of submissions in the last four years doubled that

in the first four years, 26 vs. 13. The acceptance rate, on the other hand, head-

ed down to 32.95% since TSSCI enlisting in 2013.

Another favorable feature of JFO is high speed of review process. For

the last three years (2013~2015), first review on average took only 22.18

days and shortened to 14.16 days in the first quarter of 2016. If we look at the

length of the full review process until a final decision is made on a submis-

sion, the average in 2013~2015 was 37.53 days and down to 26 days in the

first quarter of 2016. JFO will adopt a new one-line submission and review

system by the end of 2016, hoping to see an even speedier review process.

Three practical papers are included in this first issue of volume nine.

Wang, Wang and Lee document the connections between volatility skew

measures and TAIEX return. Su evaluates the tracking performance of sever-

al newly introduced leveraged and inverse ETF’s. Finally, Hung and Wang

investigate how return and volatility are affected by speculative trading ac-

tivities. I believe that the readers wull gain lots of insights through these arti-

cals.

Editor in Chief

Tsun-siou Lee, Ph.D. At National Taiwan University

April, 2016

期貨與選擇權學刊 第九卷 第一期 2016. 4

目 錄

波動性偏態指標與臺灣

加權股價指數變動率間的關聯 .. 王佳真、王尹柔、李君屏 1

槓桿型與反向型ETF長短期追蹤績效之研究 ........... 蘇亭丰 61

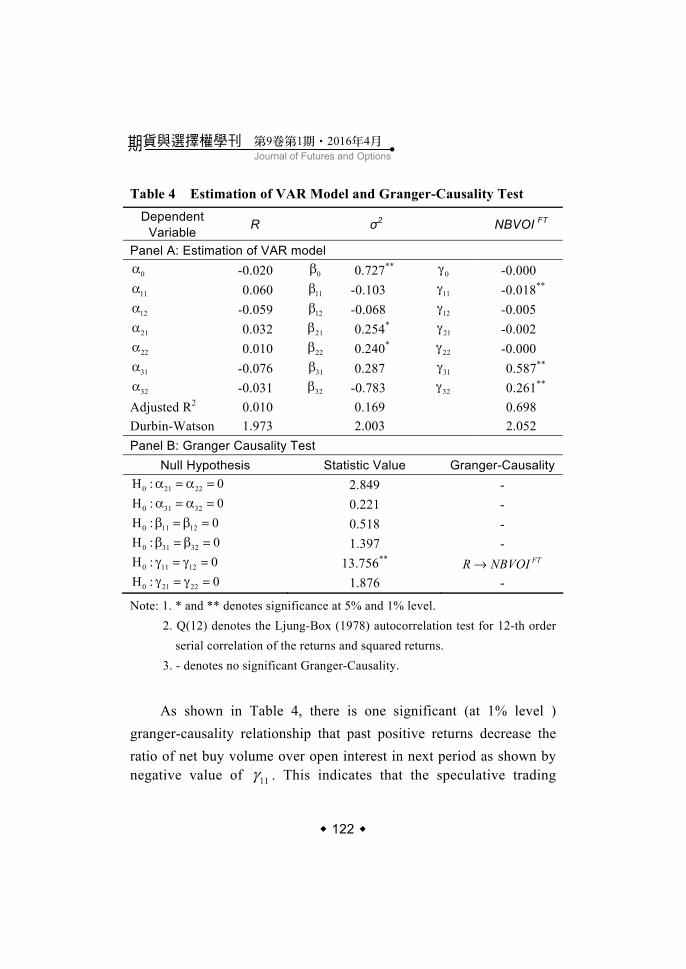

投機交易活動對臺灣期貨市場

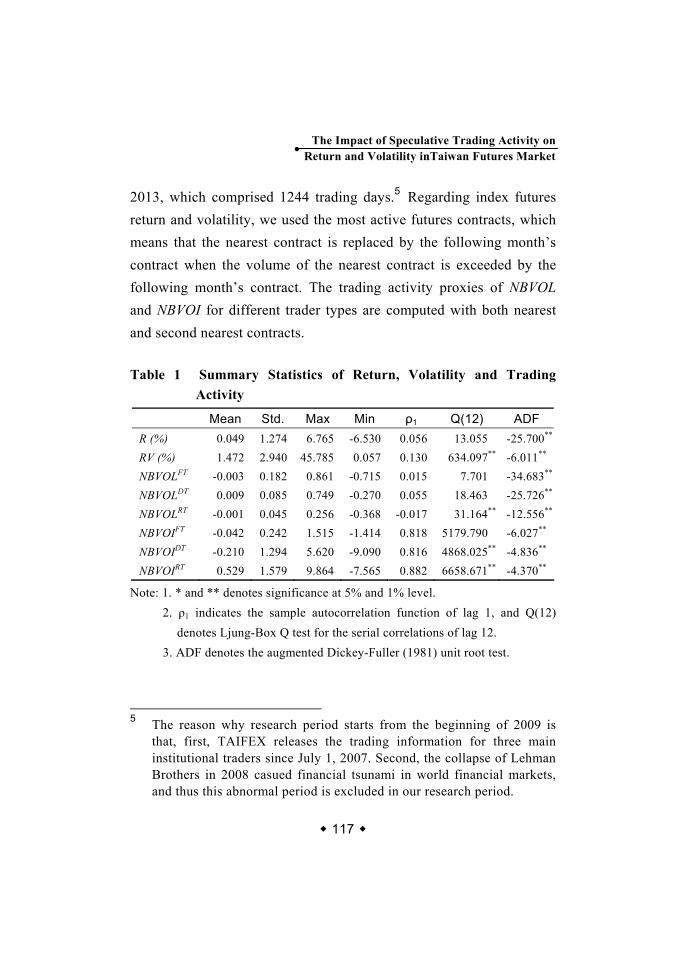

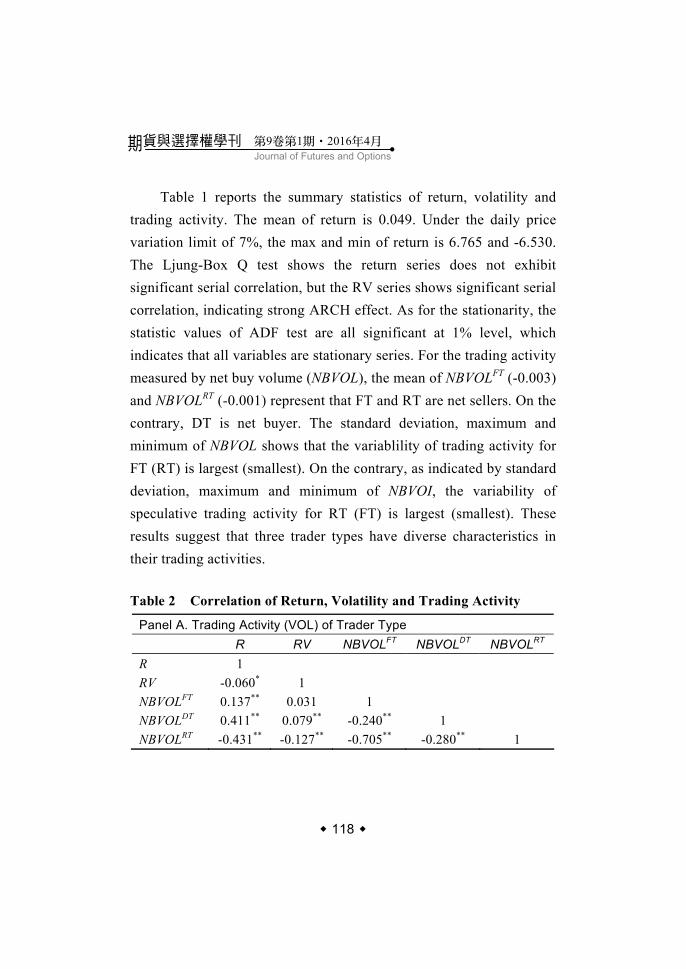

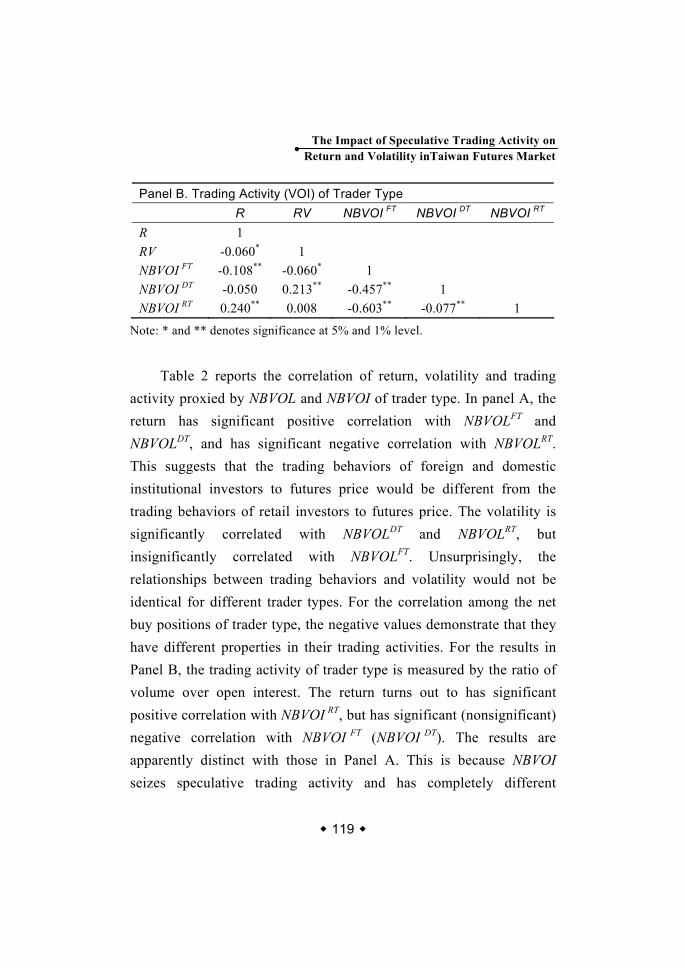

報酬與波動的衝擊 ..................................... 洪瑞成、王偉權 103

Journal of Futures and Options

Vol. 9 No. 1 April 2016

CONTENTS

Connections between Volatility Skew Measures and TAIEX Return

Jai-Jen Wang, Yin-Rou Wang, Jin-Ping Lee ................................ 1 An Investigation of Short- and Long-term Tracking Performance of Leveraged and Inverse ETFs

Ting-Feng Su ............................................................................. 61 The Impact of Speculative Trading Activity on Return and Volatility in Taiwan Futures Market

Jui-Cheng Hung, Wei-Chuan Wang ......................................... 103

1

Connections between Volatility Skew Measures and TAIEX Return ‧

波動性偏態指標與臺灣 加權股價指數變動率間的關聯

* Connections between Volatility Skew

Measures and TAIEX Return

王佳真** Jai-Jen Wang

王尹柔*** Yin-Rou Wang

李君屏**** Jin-Ping Lee

* 2015中部財金學術聯盟研討會_期貨與選擇權學刊推薦,完成本刊審稿

程序。 ** 逢甲大學財務金融系。

Department of Finance, Feng-Chia University *** 財團法人中華民國私立學校教職員退休撫卹離職資遣儲金管理委員

會。 The ROC Private School Staff Retirement and Compensation Fund Management Committee

**** 通訊作者︰逢甲大學財務金融系,臺中市西屯區文華路100號。電話:

+886-4-24517250轉4160;傳真:+886-4-24513796;Email: jplee@fcu. edu.tw。 Department of Finance, Feng-Chia University

投稿日期:2015年9月7日;第一次修訂:2015年11月29日;接受刊登日

期:2015年12月9日 Received: Sep. 7, 2015; First Revision: Nov. 29, 2015; Accepted: Dec. 9, 2015

2

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

Contents

I. Introduction 1. Motivation 2. Literature Review

II. Methodology 1. Dataset 2. Volatility Skew Measures

2.1 Volatility Skew Measure of Out-of-the-Money Put and At-the-Money Call Options ( OTMPSKEW )

2.2 Volatility Skew Measures of the Realized and Implied Volatilities of Spot Asset and At-the-Money Call Options (RVIV 1 and RVIV 2)

2.3 Volatility Skew Measures of At-the-Money Put and At-the-Money Call Options ( ATMSKEW and

ATMSKEW∆ )

2.4 Volatility Skew Measure of Out-of-the-Money Call and At-the-Money Put Options ( OTMPSKEW )

3. Methodology III. Empirical Results

1. Descriptive Statistics 1.1 Trading Statistics of

Option Contracts 1.2 Descriptive Statistics of

Volatility Skew Measures 2. Empirical Results of

Regression Analyses 2.1 Single Regressions 2.2 Correlations among

Volatility Skew Measures 2.3 Multivariate

Regressions 3. The Effect of Liquidity 4. The Impact of the 2008

Financial Tsunamis IV. Conclusion

3

Connections between Volatility Skew Measures and TAIEX Return ‧

摘 要

本文使用2002年1月至2013年12月的臺灣市場相關數據,透

過歷史波動率與隱含波動率的組合,計算出六種波動性偏態指

標;並觀察不同價性、不同成交量篩選門檻,以及金融風暴期

間、現貨與選擇權市場間的關聯。結果顯示,臺灣證券交易所

加權股價指數的變動率與波動性偏態指標具有和過去文獻一致

的關聯性。亦即當市場偏向牛市氣氛時,由歷史與隱含波動率

算出的賣權波動性偏態指標,會有縮小的統計特徵,而且其後

的現貨市場也會有偏悲觀的趨勢,或是績效變差的轉移特徵。

而當市場偏向熊市氣氛時,買權波動性偏態指標,會有放大的

統計特徵,而且其後的現貨市場也會有偏樂觀的趨勢,或是績

效轉佳的特徵。投資人可以參考本研究結果,納入波動性偏態

指標的資訊來制訂投資決策。

關鍵詞:隱含波動率、歷史波動率、價性、波動性偏態指標、

臺灣證券交易所總加權股價指數(TAIEX) JEL碼:G11, G12.

4

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

Abstract

With the considerations of moneyness, liquidity filters, sampling periods, realized and implied volatilities, this paper applies six volatility skew measures to examine the information contents between the spot and option markets in Taiwan from January 2002 to December 2013. We find that these measures significantly correlate with the TAIEX return series, and their relationships are consistent with the expected directions as explained in the literatures. Specifically, when bearish/bullish perception arises, the skew measures of implied volatilities of puts and calls become higher/lower, and the skew measures turn smaller/larger. Moreover, the spot market becomes more pessimistic/optimistic and performs poorly/well. This suggests that investors can exploit the information from volatility skew measures for various investment demands in dealing with their equity positions.

Keywords: Implied Volatility, Realized Volatility, Moneyness, Volatility Skew Measure, Taiwan Stock Exchange Capitalization Weighted Stock Index (TAIEX)

JEL: G11, G12.

5

Connections between Volatility Skew Measures and TAIEX Return ‧

I. Introduction

1. Motivation The Taiwan Futures Exchange (TAIFEX) launched TAIEX

options in 2002. The debut of these options offers more vehicles to meet the alternative needs of investors in Taiwan. The introduction of TAIEX options also provides investors more flexible channels to simultaneously trade instruments in the stock market and the option market for speculative, hedging or arbitrage motives.

The presumptions of frictionless and complete-market in the typical option pricing model, such as the well-known Black-Scholes model, imply that an option contract can be seen as a redundant security. The payoffs from the option contract can be duplicated by an arbitrage portfolio consisting of the underlying asset and a riskless asset. It implies that there is no additional information content that can be extracted from option trading. However, the contradiction of a frictionless assumption and the properties of lower transaction cost, higher leverage, and less restricted short-selling constraint for option trading lead to informed investors tending to trade and release their private information in the option market instead of or prior to their corresponding trading in the spot market. It indicates that option trading provides the function of price discovery in the capital market. A series of studies examine the interaction between the option market and spot market. For example, under the setting of two groups of boundedly rational agents, newswatchers and momentum traders, Hong and Stein (1999) theoretically demonstrate that attempts at

6

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

arbitrage may inevitably lead to overreaction over long horizons, and information generated from the option market may lead the stock market in an unstable way due to traders’ different levels of rationality and their different investing styles.

Chakravarty, Guien and Mayhew (2004) address the role of price discovery played by the option market as well. They empirically estimate an option market’s contribution to price discovery to be about 17% on average based on five years of stock and option data for 60 U.S. firms, further finding that the contribution level is affected by trading volume and spreads in both markets. Hong, Torous and Valkanov (2007) investigate whether the returns of industry portfolios are able to predict the movements of stock markets through spot and option positions. Their empirical results of the nine largest equity markets in the world, including the U.S., reveal remarkably similar patterns and suggest that stock markets react with a delay to information not only contained in industry about their fundamentals, but also contained in the option markets. Lien and Shrestha (2009, 2014) generalize an information share measure developed by Hasbrouck (1995) to examine the price discovery process among the interrelated securities markets. They apply the measure to investigate the information content released in the credit default swap (CDS) market and the bond market. The result indicates that the price discovery mostly takes place in the CDS market. Xie and Mo (2014) use the panel data of Chinese stock market to examine the impact of the introduction of CSI 300 index futures on stock market volatility. They find that the spot price experiences a long-term trend of diminishing volatility after the commencing of CSI 300 index futures.

7

Connections between Volatility Skew Measures and TAIEX Return ‧

In the field of the empirical connection between an option and its underlying asset, the literature seems to pay more attention to the leading-lagging relationship between the return or price series of the two markets. Some studies have recently begun to highlight the junction of volatility and return series between the two markets. For example, Banerjee et al. (2007) find that both the levels and innovations in implied volatility have significant predictive power for future returns on the market portfolio. Bali and Hovakimian (2009) test the significance of the information spillover effect between option and stock markets, noting empirical evidence that the volatility spillover effect takes place from the option market to the stock market, which implies that informed traders tend to first take actions in the option market with their private information.

Goyal and Saretto (2009) construct decile portfolios by sorting stocks on the difference between historical realized volatility and at-the-money implied volatility. A zero-cost trading strategy can be formulated by taking a long (short) position in the decile with a large positive (negative) difference. They find that the strategy produces an economically and statistically significant average monthly return. The profitability result is robust to different market conditions, various industry groupings, diverse levels of option liquidity, and cannot be explained by the usual risk factor models.

Xing, Zhang and Zhao (2010) study the shape of the volatility smirk and find significant cross-sectional predictive power from the smirk for future equity returns. Stocks exhibiting the steepest smirks in their traded options underperform stocks with the least pronounced volatility smirks in their options by around 10.9% per year on a risk-

8

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

adjusted basis. This predictability persists for at least six months, and firms with the steepest volatility smirks are those experiencing the worst earnings shocks in the following quarter.

Cremers and Weinbraum (2010) observe the influence of deviations from the put-call parity on future stock returns. They use the difference in implied volatility between pairs of call and put options to measure these deviations and find that stocks with relatively expensive calls outperform stocks with relatively expensive puts by at least 45 basis points per week. Baltussen et al. (2012) assert that the option market contains exploitable information for equity investors for an investable universe of liquid large-cap stocks. Strategies based on several option volatility skew measures can predict returns on the underlying stock. These findings unanimously suggest that information diffuses gradually from the option market into the underlying stock market.

While studies on the leading-lagging relationship between the option and spot markets thrive in the literature, most of them focus on the return or price series of the two markets. It seems that less empirical studies target the junction of the volatility skew measures in the option market and the return or price series in the underlying market, in particular for Taiwan markets. This study thus follows Bali and Hovakimian (2009), Goyal and Saretto (2009), Xing, Zhang and Zhao (2010), Cremers and Weinbraum (2010), and Baltussen et al. (2012) and tries to observe effects from the option market to the stock market in Taiwan through different volatility skew measures developed in the literature. Our empirical results may help investors extend their information contents and improve their investing

9

Connections between Volatility Skew Measures and TAIEX Return ‧

performance by exploiting these volatility skew measures.

2. Literature Review The S-shaped value function of the prospect theory developed by

Kahneman and Tversky (1979) demonstrates that traders hold different risk attitudes when coping with different expectation scenarios according to reference points in their mental accounts. They might be risk averse or risk loving while managing their uncertain investing opportunity sets. The call and put contracts in the option market are able to help satisfy their asymmetric investing demands, and it is the asymmetry of risk attitude or demand that results in a smile-shaped relationship between volatility and moneyness. For example, according to the net buying pressure hypothesis proposed by Bollen and Whaley (2004), the volatility smile is directly related to net buying pressure from public order flow dominated by call option demand. If institutional demand tends to be focused in a particular option series, such as out-of-the-money puts, then the volatility function will be downward sloping.

Trading activities in the option market specifically not only reveal the price expectations of participants on the underlying asset, but also unveil their different facets of risk attitude or behavioral tendency. Thus, practical indicators such as return or volatility measures from option positions may help us comprehend the information contents participants hold in an advanced or earlier sense before what the underlying market shows.

As the traditional literature has noted, the price discovery function of derivative markets comes from the favorable frictions that

10

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

spot markets do not have. For example, Black (1975) and Duffie (1996) present that lower transaction cost, higher leverage, and less restricted short-selling constraints in derivative markets make informed traders more active in derivative markets. Fleming, Ostdiek and Whaley (1996) argue that the prices of securities and their derivatives must simultaneously reflect new information in perfectly frictionless and rational markets; otherwise, costless arbitrage profits would be possible. Their empirical results show that the S&P500 index futures market leads the S&P500 stock index and that the S&P100 index option market leads the S&P100 stock index.

The no-arbitrage condition seems to be a reasonable basis of linkage between derivative and underlying markets, and it is an usual behavior assumption in the literature of asset pricing models. However, Hong and Stein (1999) demonstrate that owing to different information-processing capabilities and different investing styles of traders, the linkage between derivative and underlying markets may not be perfect and simultaneous. Thus, the no-arbitrage pricing equilibrium might be dampened by the rationality friction of an over- or under-reaction.

Buraschi and Jackwerth (2001) do not take the viewpoint that an option is a redundant position, because additional priced risk factors such as stochastic interest rates or jumps result in a time-varying or stochastic diffusion term in the spot return process. Using daily S&P500 index options data from 1986-1995, their empirical findings are inconsistent with deterministic volatility models, but are consistent with stochastic models that incorporate these additional priced risk factors. It is stochasticity that makes the information generated by

11

Connections between Volatility Skew Measures and TAIEX Return ‧

implied volatility measures in the option market more valuable in an earlier-step sense in contrast to the spot market.

Chakravarty, Guien and Mayhew (2004) find evidence of significant price discovery in the option market. While the results suggest that both leverage and liquidity play important roles in promoting price discovery, the option market tends to be more informative on average when option trading volume is high, when stock volume is low, when option effective spreads are narrow, and when stock spreads are wide. They also investigate whether the estimates of price discovery in the option market differ across options of different strike prices. On average, the information share tends to be slightly higher for out-of-the-money options than at-the-money options, but this result varies cross-sectionally as a function of trading volume and spreads.

Chan and Shih (2005) investigate empirical relationships among time series of futures, spot, and option positions in the Taiwan markets. They find that these series are significantly interrelated to each other in irregular directions. While derivative positions, including both futures and option positions, significantly lead their spot counterparts, the leading-lagging relationship between the futures and option series is not monotonic. Hong, Torous and Valkanov (2007) develop the hypothesis that the gradual diffusion of information across markets leads to cross-asset return predictability. They test the cross-predictability relationship among industry portfolios and market indices using data from stock markets around the world, finding remarkably similar patterns supporting the gradual-information-diffusion hypothesis among the nine largest stock markets. They assert

12

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

that the pervasive empirical results suggest much more work remains to be done, in particular looking at stocks and the options listed on them. Moreover, the gradual information diffusion effect or the price discovery function can be detected or proxied by volatility measures in the spot and option markets.

Traditional volatility measures, such as the historical volatility in the underlying market, represent the realized uncertain degree of the past spot price or return series, while the implied volatility in the option market can proxy the current expectations that traders hold for the future spot price or return series. For example, Frijns, Tallau and Tourani-Rad (2010) develop an implied volatility index for the Australian stock market and assess the information content of the index. They find that the index contains more information than the traditional volatility measures and significantly improves the forecasting power for the future stock market.

Xing, Zhang and Zhao (2010) suggest the combination of realized and implied volatilities with the considerations of different features of option contracts can be more informative. They develop an out-of-the-money volatility skew measure by the difference between the implied volatilities estimated by the out-of-the money put options and the at-the-money call options to examine the relationship between the volatility skew and the future stock returns. They assert that the volatility skew contains the information of the possibility of a negative price jump, the expected magnitude of the price jump, and the premium to compensate the investors for bearing price jump risk.

Several studies have proposed similar volatility skew measures combined with other features of option contracts. For example, Bali

13

Connections between Volatility Skew Measures and TAIEX Return ‧

and Hovakimian (2009) find a negative and significant relationship between expected stock returns and their volatility measures, which are the spreads of realized or implied volatility between call and put contracts. They take their measures as proxies for volatility risk and take the correlations of expected stock return and the volatility measures as proxies for jump risk. Their empirical results indicate significant information flows from individual equity options to individual stocks. Goyal and Saretto (2009) find that information contained in their volatility skew measures produces an economically and statistically significant average monthly return, which is robust to different market conditions, to stock risks-characteristics, to various industry groupings, to option liquidity characteristics, and cannot be explained by the typical risk factor models.

Cremers and Weinbraum (2010) use the difference in implied volatility between pairs of call and put options as their volatility skew measure. They find that both levels and changes in the measure matter for future stock returns and suggest that the option market can affect its underlying market for information-based rather than friction-based reasons only. Baltussen et al. (2012) find that their volatility skew measures can be applied to formulate an effective portfolio, which is substantially different from other well-known stock selection strategies. Their portfolio produces an even stronger profitability result with an annualized performance of around 10%, thereby strengthening the relevance of the publicly available information contained in the option market for equity investors.

14

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

II. Methodology

1. Dataset Our sample period is from January 2002 to December 2013.

Stock and option data are from Taiwan Economic Journal Data Bank (TEJ), which provides time series data on the spot price, the Taiwan stock exchange capitalization weighted stock index (TAIEX), and the time series associated with the option contracts such as open interest, volume, and number of days to maturity. It also computes realized and implied volatilities for all listed options with different contract specifications.1 To calculate realized and implied volatilities for each trading day, TEJ first computes the standard deviation of daily TAIEX return, S, within the window of its previous 260 trading days. And an annualized percentage version of realized volatility can be produced by the formula, 260 /100S × , which is the base to be utilized for

different contracts. The implied volatilities are estimated with observed market data in the theoretical Black-Scholes formula with the Newton-Rahpson iteration methodology. The threshold to stop iteration is set to be less than 0.5 between observed and theoretical premiums.2

1 There is a series of TAIEX option contracts with different maturity dates in

the market and the options are traded 15 minutes longer than the spot market. It is worthy to note that the empirical results may be masked by the potential nonsynchronous problem. However, due to the cost of data collection, the daily data instead of intraday data is applied for the empirical analysis in this study.

2 For the complete specification and methodology, please refer to the Taiwan

15

Connections between Volatility Skew Measures and TAIEX Return ‧

On the other hand, in order to obtain the most informative dataset, we employ three criteria as filters to refine the empirical results: (1) liquidity, (2) nearness, and (3) moneyness. As Baltussen et al. (2012) note, the liquidity and nearness requirements make option contracts investable for many traders. The sample of option contracts with zero trading volume is also excluded. Because most activity in options is concentrated in the short end, we select nearby options with the remaining maturity of 10-40 trading days, or approximately a calendar length of one month.

The third criterion, moneyness, is another important dimension of option information content. For example, Xing, Zhang and Zhao (2010) claim that an out-of-the-money put is a natural place for informed traders with negative news to place their trades. If there is an overwhelming pessimistic perception of the stock, investors would tend to buy put options either for protection against future stock price drops (hedge purpose) or for a high potential return on the long put positions (speculation purpose). Thus, we follow Xing, Zhang and Zhao (2010) and Baltussen et al. (2012) to categorize option contracts by the moneyness types and calculate various volatility skew measures thereafter.

We specifically use different ratio ranges of the strike price (K) to the stock index (S) to define the moneyness types. For instance, a call option in our empirical study is defined as at-the-money (ATM) when the ratio of K to S (K/S) is between 0.95 and 1.05, and is abbreviated as ATMC. A put option is defined as out-of-the-money (OTM) when

Economic Journal Data Bank and Benninga (1989).

16

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

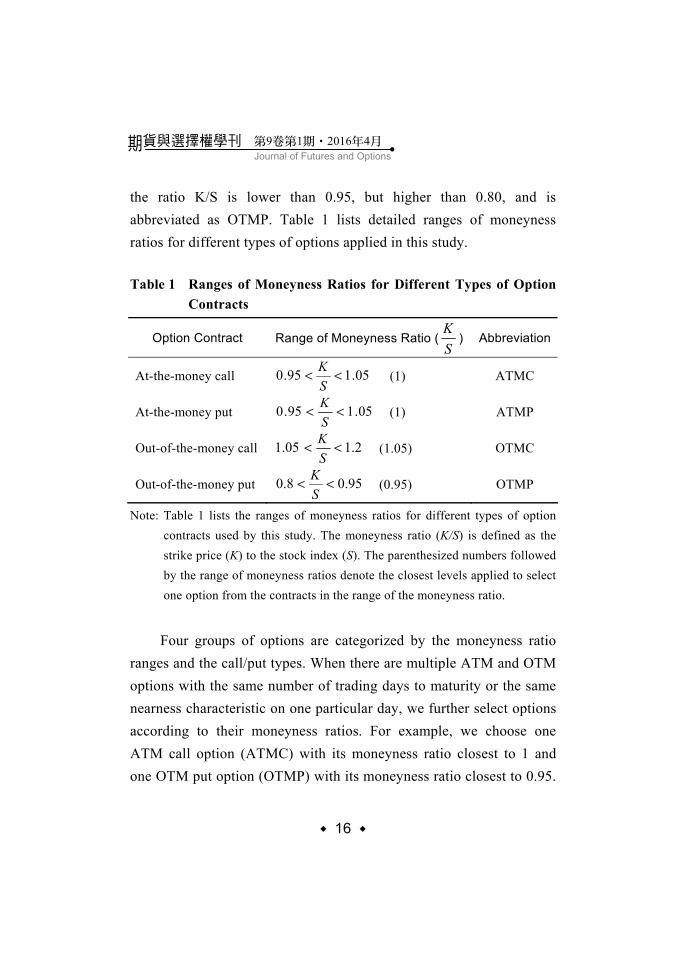

the ratio K/S is lower than 0.95, but higher than 0.80, and is abbreviated as OTMP. Table 1 lists detailed ranges of moneyness ratios for different types of options applied in this study.

Table 1 Ranges of Moneyness Ratios for Different Types of Option

Contracts

Option Contract Range of Moneyness Ratio (KS

) Abbreviation

At-the-money call 05.195.0 <<SK

(1)

ATMC

At-the-money put 05.195.0 <<SK

(1)

ATMP

Out-of-the-money call 1.21.05 <<SK

(1.05)

OTMC

Out-of-the-money put 0.950.8 <<SK

(0.95)

OTMP

Note: Table 1 lists the ranges of moneyness ratios for different types of option contracts used by this study. The moneyness ratio (K/S) is defined as the strike price (K) to the stock index (S). The parenthesized numbers followed by the range of moneyness ratios denote the closest levels applied to select one option from the contracts in the range of the moneyness ratio.

Four groups of options are categorized by the moneyness ratio

ranges and the call/put types. When there are multiple ATM and OTM options with the same number of trading days to maturity or the same nearness characteristic on one particular day, we further select options according to their moneyness ratios. For example, we choose one ATM call option (ATMC) with its moneyness ratio closest to 1 and one OTM put option (OTMP) with its moneyness ratio closest to 0.95.

17

Connections between Volatility Skew Measures and TAIEX Return ‧

These closest levels, applied to deal with contracts of the same nearness characteristic and call/put type, are adopted by Xing, Zhang and Zhao (2010) and Baltussen et al. (2012) and are denoted by the parenthesized numbers followed by the moneyness ratio ranges in Table 1.

2. Volatility Skew Measures Following the methodologies adopted by Bali and Hovakimian

(2009), Goyal and Saretto (2009), Xing, Zhang and Zhao (2010), Cremers and Weinbraum (2010), and Baltussen et al. (2012), we apply liquidity, nearness, and moneyness filters to refine our dataset. We also develop some volatility skew measures here to exert information contents in the Taiwan option and stock markets.

2.1 Volatility Skew Measure of Out-of-the-Money Put and At-the-Money Call Options ( OTMPSKEW )

Gârleanu, Pedersen and Poteshman (2009) and Xing, Zhang and Zhao (2010) assert that a pessimistic informed trader tends to buy a put either for hedge or for speculation purpose. As more and more informed traders come out with a pessimistic perception of the underlying asset, the buying pressure on the out-of-the-money put and its premium will increase, which associates the implied volatility of the put contract with bad news about the future spot price. Thus, the first volatility skew measure at time t, OTMP

tSKEW , is defined as the

difference between the implied volatility of the out-of-the-money put ( OTMP

tIV ) and the implied volatility of the at-the-money call ( ATMC

tIV ):

18

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

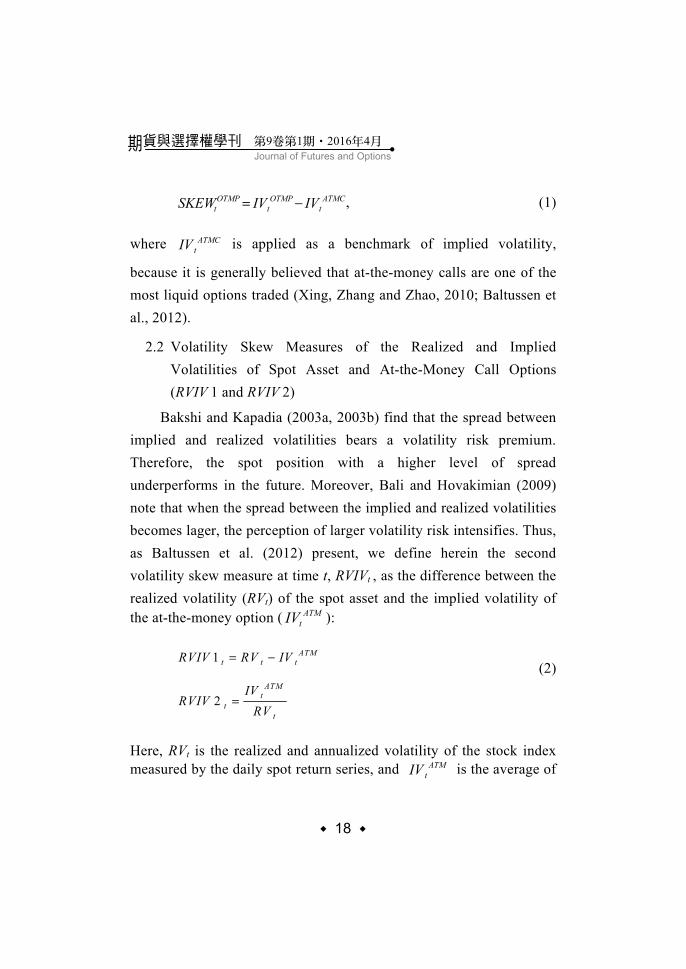

ATMCt

OTMPt

OTMPt IVIVSKEW −= , (1)

where ATMCtIV is applied as a benchmark of implied volatility,

because it is generally believed that at-the-money calls are one of the most liquid options traded (Xing, Zhang and Zhao, 2010; Baltussen et al., 2012).

2.2 Volatility Skew Measures of the Realized and Implied Volatilities of Spot Asset and At-the-Money Call Options (RVIV 1 and RVIV 2)

Bakshi and Kapadia (2003a, 2003b) find that the spread between implied and realized volatilities bears a volatility risk premium. Therefore, the spot position with a higher level of spread underperforms in the future. Moreover, Bali and Hovakimian (2009) note that when the spread between the implied and realized volatilities becomes lager, the perception of larger volatility risk intensifies. Thus, as Baltussen et al. (2012) present, we define herein the second volatility skew measure at time t, RVIVt , as the difference between the realized volatility (RVt) of the spot asset and the implied volatility of the at-the-money option ( ATM

tIV ):

1

2

ATMt t t

ATMt

tt

RVIV RV IV

IVRVIV

RV

= −

=

(2)

Here, RVt is the realized and annualized volatility of the stock index measured by the daily spot return series, and ATM

tIV is the average of

19

Connections between Volatility Skew Measures and TAIEX Return ‧

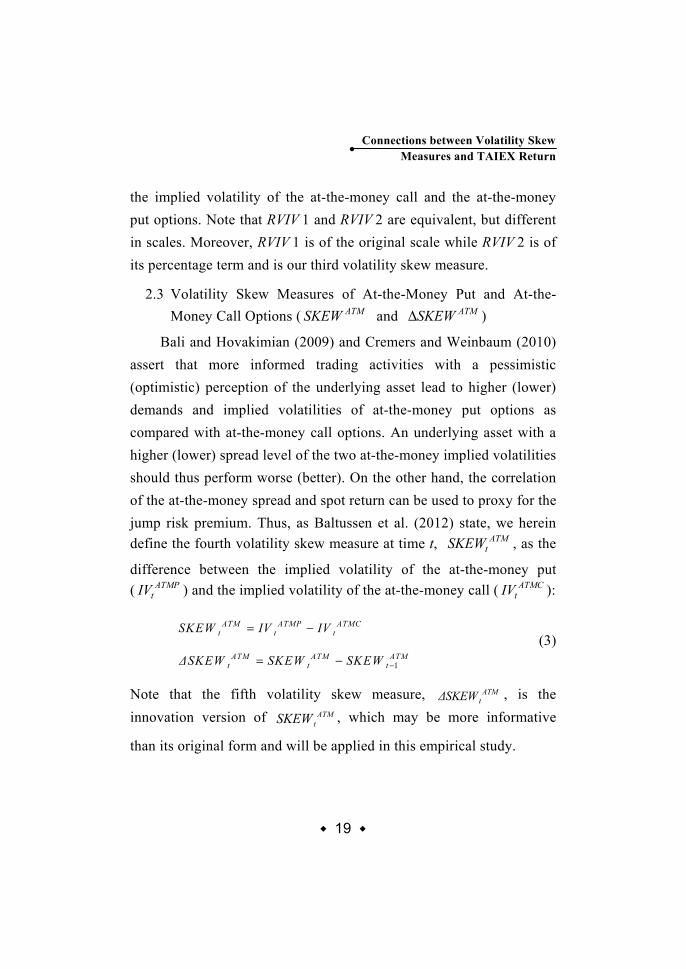

the implied volatility of the at-the-money call and the at-the-money put options. Note that RVIV 1 and RVIV 2 are equivalent, but different in scales. Moreover, RVIV 1 is of the original scale while RVIV 2 is of its percentage term and is our third volatility skew measure.

2.3 Volatility Skew Measures of At-the-Money Put and At-the-Money Call Options ( ATMSKEW and ATMSKEW∆ )

Bali and Hovakimian (2009) and Cremers and Weinbaum (2010) assert that more informed trading activities with a pessimistic (optimistic) perception of the underlying asset lead to higher (lower) demands and implied volatilities of at-the-money put options as compared with at-the-money call options. An underlying asset with a higher (lower) spread level of the two at-the-money implied volatilities should thus perform worse (better). On the other hand, the correlation of the at-the-money spread and spot return can be used to proxy for the jump risk premium. Thus, as Baltussen et al. (2012) state, we herein define the fourth volatility skew measure at time t, ATM

tSKEW , as the

difference between the implied volatility of the at-the-money put ( ATMP

tIV ) and the implied volatility of the at-the-money call ( ATMCtIV ):

1

ATM ATMP ATMCt t t

ATM ATM ATMt t t

SKEW IV IV

∆SKEW SKEW SKEW −

= −

= − (3)

Note that the fifth volatility skew measure, ATMt∆SKEW , is the

innovation version of ATMtSKEW , which may be more informative

than its original form and will be applied in this empirical study.

20

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

2.4 Volatility Skew Measure of Out-of-the-Money Call and At-the-Money Put Options ( OTMPSKEW )

With more optimistic informed traders active in the option market, the buying pressure on the out-of-the-money call becomes larger and its premium will increase, which associates the implied volatility of the call contract with good news about the future spot price. Here, the sixth volatility skew measure, OTMPSKEW , is defined as the difference between the implied volatility of the out-of-the-money call ( OTMC

tIV ) and the implied volatility of the at-the-money put ( ATMP

tIV ):

OTM C OTM C ATM Pt t tSKEW IV IV= − , (4)

where ATMPtIV is applied as a benchmark of implied volatility in

contrast to the out-of-the-money calls, because at-the-money options are the most liquid positions for traders.

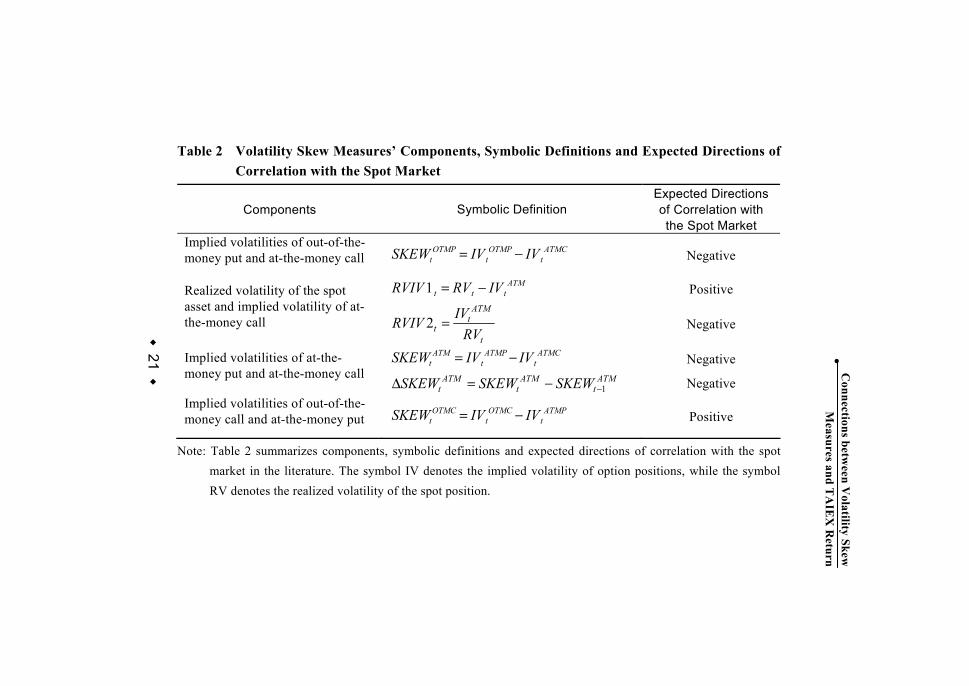

We apply the six volatility skew measures to investigate empirical connections between the option and spot markets in Taiwan. Table 2 summarizes their components, symbolic definitions, and expected directions of correlation with the spot market in the literature.

Table 2 Volatility Skew Measures’ Components, Symbolic Definitions and Expected Directions of Correlation with the Spot Market

Components Symbolic Definition Expected Directions of Correlation with the Spot Market

Implied volatilities of out-of-the-money put and at-the-money call

ATMCt

OTMPt

OTMPt IVIVSKEW −= Negative

ATMttt IVRVRVIV −=1 Positive Realized volatility of the spot

asset and implied volatility of at-the-money call 2

ATMt

tt

IVRVIVRV

= Negative

ATMCt

ATMPt

ATMt IVIVSKEW −= Negative Implied volatilities of at-the-

money put and at-the-money call 1

ATM ATM ATMt t tSKEW SKEW SKEW −∆ = − Negative

Implied volatilities of out-of-the-money call and at-the-money put

ATMPt

OTMCt

OTMCt IVIVSKEW −= Positive

Note: Table 2 summarizes components, symbolic definitions and expected directions of correlation with the spot market in the literature. The symbol IV denotes the implied volatility of option positions, while the symbol RV denotes the realized volatility of the spot position.

21 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

22

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

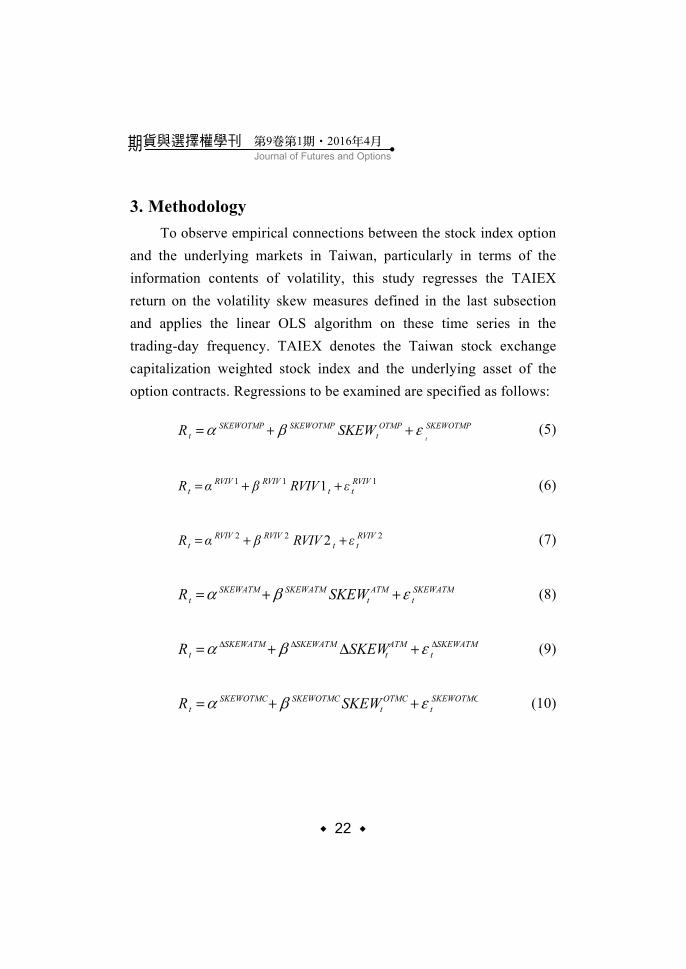

3. Methodology To observe empirical connections between the stock index option

and the underlying markets in Taiwan, particularly in terms of the information contents of volatility, this study regresses the TAIEX return on the volatility skew measures defined in the last subsection and applies the linear OLS algorithm on these time series in the trading-day frequency. TAIEX denotes the Taiwan stock exchange capitalization weighted stock index and the underlying asset of the option contracts. Regressions to be examined are specified as follows:

SKEWOTMPOTMPt

SKEWOTMPSKEWOTMPt t

SKEWR εβα ++= (5)

1 1 11RVIV RVIV RVIVt t tR α β RVIV ε= + + (6)

2 2 22RVIV RVIV RVIVt t tR α β RVIV ε= + + (7)

SKEWATMt

ATMt

SKEWATMSKEWATMt SKEWR εβα ++= (8)

SKEWATMt

ATMt

SKEWATMSKEWATMt SKEWR ∆∆∆ +∆+= εβα (9)

SKEWOTMCt

OTMCt

SKEWOTMCSKEWOTMCt SKEWR εβα ++= (10)

23

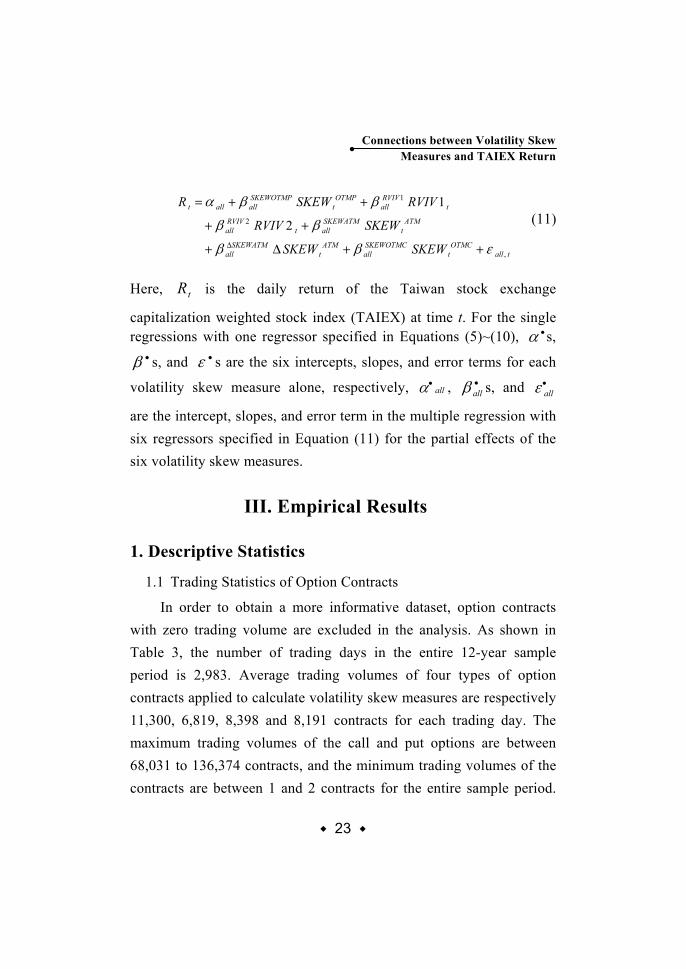

Connections between Volatility Skew Measures and TAIEX Return ‧

tallOTMC

tSKEWOTMCall

ATMt

SKEWATMall

ATMt

SKEWATMallt

RVIVall

tRVIVall

OTMPt

SKEWOTMPallallt

SKEWSKEW

SKEWRVIV

RVIVSKEWR

,

2

1

2

1

εββ

ββ

ββα

++∆+

++

++=

∆

(11)

Here, tR is the daily return of the Taiwan stock exchange

capitalization weighted stock index (TAIEX) at time t. For the single regressions with one regressor specified in Equations (5)~(10), •α s,

•β s, and •ε s are the six intercepts, slopes, and error terms for each

volatility skew measure alone, respectively, all•α , •

allβ s, and •allε

are the intercept, slopes, and error term in the multiple regression with six regressors specified in Equation (11) for the partial effects of the six volatility skew measures.

III. Empirical Results

1. Descriptive Statistics

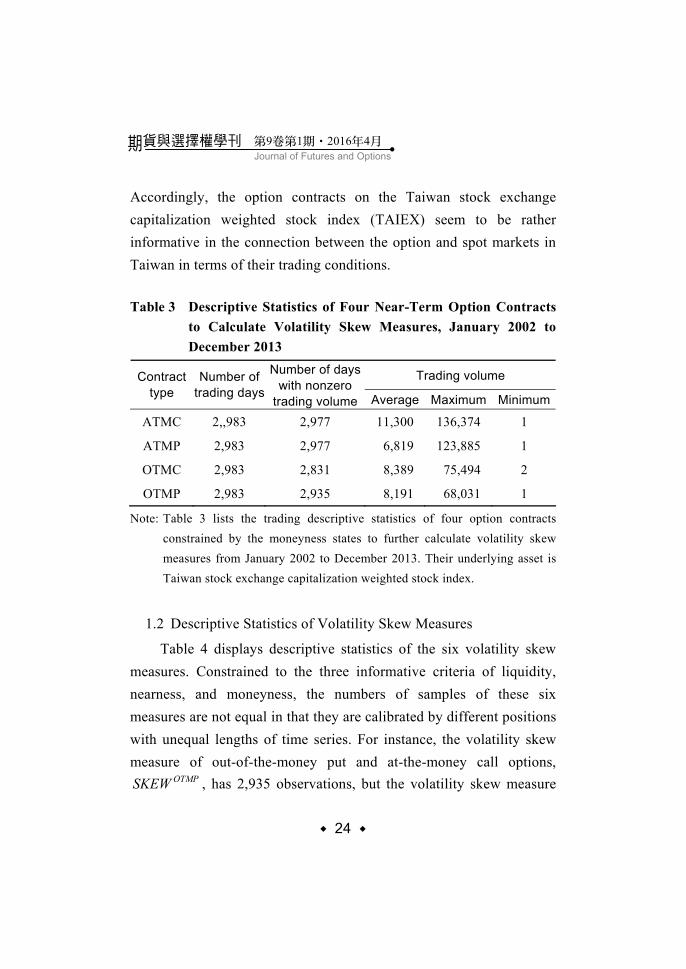

1.1 Trading Statistics of Option Contracts

In order to obtain a more informative dataset, option contracts with zero trading volume are excluded in the analysis. As shown in Table 3, the number of trading days in the entire 12-year sample period is 2,983. Average trading volumes of four types of option contracts applied to calculate volatility skew measures are respectively 11,300, 6,819, 8,398 and 8,191 contracts for each trading day. The maximum trading volumes of the call and put options are between 68,031 to 136,374 contracts, and the minimum trading volumes of the contracts are between 1 and 2 contracts for the entire sample period.

24

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

Accordingly, the option contracts on the Taiwan stock exchange capitalization weighted stock index (TAIEX) seem to be rather informative in the connection between the option and spot markets in Taiwan in terms of their trading conditions.

Table 3 Descriptive Statistics of Four Near-Term Option Contracts

to Calculate Volatility Skew Measures, January 2002 to December 2013

Trading volume Contracttype

Number of trading days

Number of days with nonzero

trading volume Average Maximum Minimum

ATMC 2,,983 2,977 11,300 136,374 1

ATMP 2,983 2,977 6,819 123,885 1

OTMC 2,983 2,831 8,389 75,494 2

OTMP 2,983 2,935 8,191 68,031 1

Note: Table 3 lists the trading descriptive statistics of four option contracts constrained by the moneyness states to further calculate volatility skew measures from January 2002 to December 2013. Their underlying asset is Taiwan stock exchange capitalization weighted stock index.

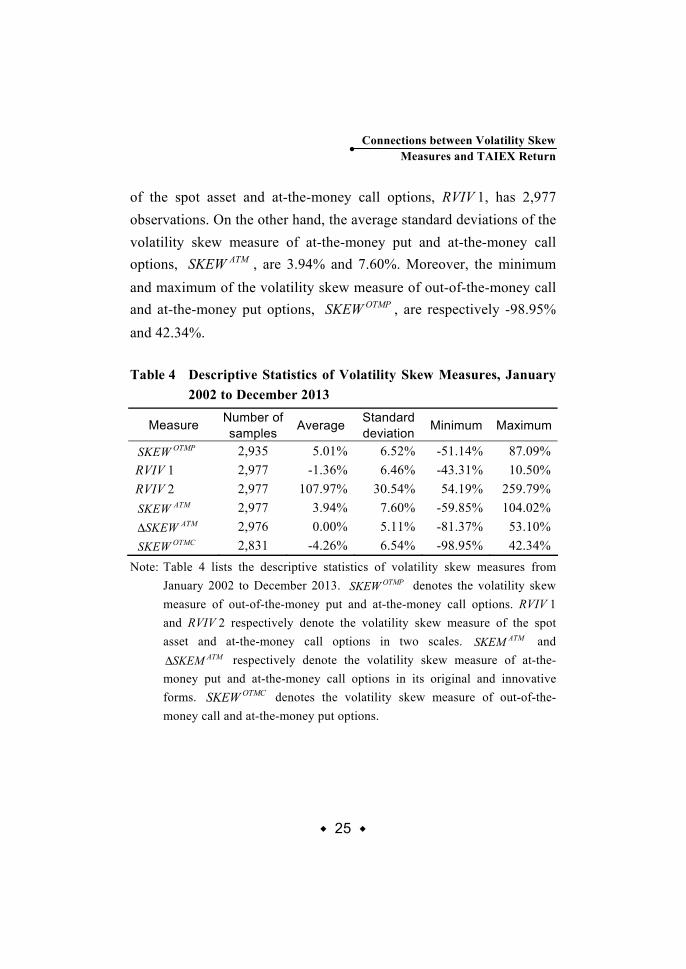

1.2 Descriptive Statistics of Volatility Skew Measures

Table 4 displays descriptive statistics of the six volatility skew measures. Constrained to the three informative criteria of liquidity, nearness, and moneyness, the numbers of samples of these six measures are not equal in that they are calibrated by different positions with unequal lengths of time series. For instance, the volatility skew measure of out-of-the-money put and at-the-money call options,

OTMPSKEW , has 2,935 observations, but the volatility skew measure

25

Connections between Volatility Skew Measures and TAIEX Return ‧

of the spot asset and at-the-money call options, RVIV 1, has 2,977 observations. On the other hand, the average standard deviations of the volatility skew measure of at-the-money put and at-the-money call options, ATMSKEW , are 3.94% and 7.60%. Moreover, the minimum and maximum of the volatility skew measure of out-of-the-money call and at-the-money put options, OTMPSKEW , are respectively -98.95% and 42.34%.

Table 4 Descriptive Statistics of Volatility Skew Measures, January

2002 to December 2013

Measure Number of samples Average Standard

deviation Minimum Maximum OTMPSKEW 2,935 5.01% 6.52% -51.14% 87.09%

RVIV 1 2,977 -1.36% 6.46% -43.31% 10.50% RVIV 2 2,977 107.97% 30.54% 54.19% 259.79%

ATMSKEW 2,977 3.94% 7.60% -59.85% 104.02% ATMSKEW∆ 2,976 0.00% 5.11% -81.37% 53.10%

OTMCSKEW 2,831 -4.26% 6.54% -98.95% 42.34% Note: Table 4 lists the descriptive statistics of volatility skew measures from

January 2002 to December 2013. OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of the spot asset and at-the-money call options in two scales. ATMSKEM and

ATMSKEM∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options.

26

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

2. Empirical Results of Regression Analyses

2.1 Single Regressions

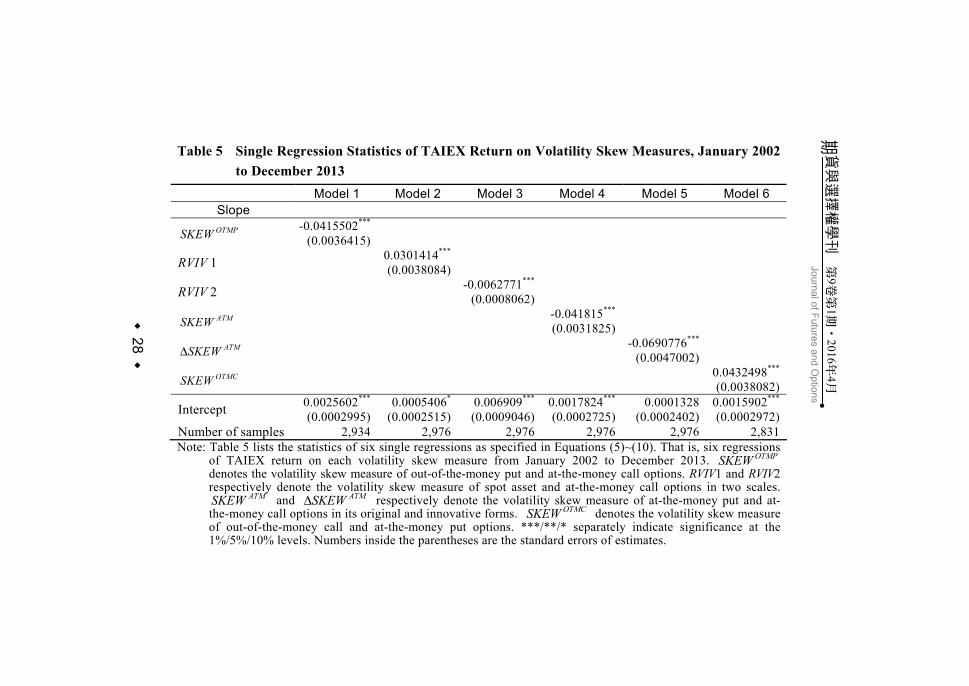

Table 5 lists the statistics of single regressions as specified in Equations (5)~(10). That is, regressions of TAIEX return on each volatility skew measure are conducted separately from January 2002 to December 2013. In terms of the slope estimates in Models 1~6, each volatility skew measure correlates with TAIEX return at the 1% significance level, which means all of the measures are full of information contents about the spot market. In particular, their slope estimates are all consistent with the expected directions of correlation with the spot market in the literature as noted in Table 2.

For instance, OTMPSKEW , the volatility skew measure of out-of-the-money put and at-the-money call options, significantly and negatively correlates with TAIEX return. Its estimated slope is -0.0415502, which is consistent with the reasoning in the literature that as informed pessimistic traders become more active than other ones in option and spot markets, OTMPSKEW will get larger and spot return will get smaller (Gârleanu, Pedersen and Poteshman, 2009; Xing, Zhang and Zhao, 2010).

RVIV 1, the volatility skew measure of the spot asset and at-the-money call options, significantly and positively correlates with TAIEX return This is consistent with the argument in the literature that as the perception of volatility or jump risk in the spot market escalates, the implied volatility or the price of option positions increases faster or to a larger degree than the realized volatility does, and hence RVIV 1 will get smaller and the spot asset tends to underperform in the future. The

27

Connections between Volatility Skew Measures and TAIEX Return ‧

same reasoning applies on RVIV 2 as well, except that the definition of RVIV 2 differs from RVIV 1 at scale and has an inverse +/- direction (Bakshi and Kapadia, 2003a, 2003b; Bali and Hovakimian, 2009). Their estimated slopes are respectively 0.0301414 and -0.0062771.

ATMSKEW , the volatility skew measure of at-the-money put and at-the-money call options, significantly and negatively correlates with TAIEX return. This is consistent with the similar reasoning in the literature as OTMPSKEW , but it is specified in terms of the at-the-money put position rather than the out-of-the-money one. In other words, a larger ATMSKEW or a positive ATMSKEW∆ usually comes when the spot market underperforms (Bali and Hovakimian, 2009; Cremers and Weinbaum, 2010; Baltussen et al., 2012). Their estimated slopes are respectively -0.041815 and -0.0690776.

In contrast to the pessimistic perception that comes with put contracts, OTMPSKEW reveals its information contents through an optimistic perception with the call contracts. As informed optimistic traders become more active than other ones in option and spot markets, implied volatility or the premium of the out-of-the-money call contracts will get higher and the spot return will tend to outperform. As shown in Table 5, OTMPSKEW , the volatility skew measure of out-of-the-money call and at-the-money put options, significantly and positively correlates with TAIEX return, and its estimated slope is 0.0432498.

28

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Table 5 Single Regression Statistics of TAIEX Return on Volatility Skew Measures, January 2002 to December 2013 Model 1 Model 2 Model 3 Model 4 Model 5 Model 6

Slope OTMPSKEW -0.0415502***

(0.0036415)

RVIV 1 0.0301414***

(0.0038084)

RVIV 2 -0.0062771***

(0.0008062)

ATMSKEW -0.041815***

(0.0031825) ATMSKEW∆ -0.0690776***

(0.0047002)OTMCSKEW 0.0432498***

(0.0038082)

Intercept 0.0025602***

(0.0002995)0.0005406*

(0.0002515)0.006909***

(0.0009046)0.0017824***

(0.0002725) 0.0001328

(0.0002402)0.0015902***

(0.0002972)Number of samples 2,934 2,976 2,976 2,976 2,976 2,831Note: Table 5 lists the statistics of six single regressions as specified in Equations (5)~(10). That is, six regressions

of TAIEX return on each volatility skew measure from January 2002 to December 2013. OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV1 and RVIV2 respectively denote the volatility skew measure of spot asset and at-the-money call options in two scales.

ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicate significance at the 1%/5%/10% levels. Numbers inside the parentheses are the standard errors of estimates.

29

Connections between Volatility Skew Measures and TAIEX Return ‧

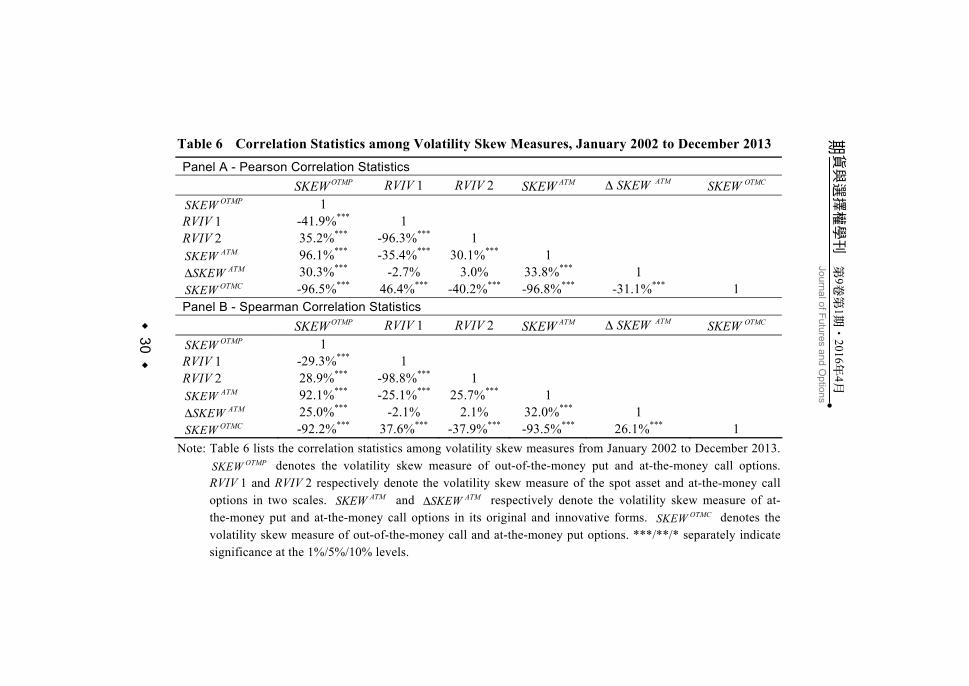

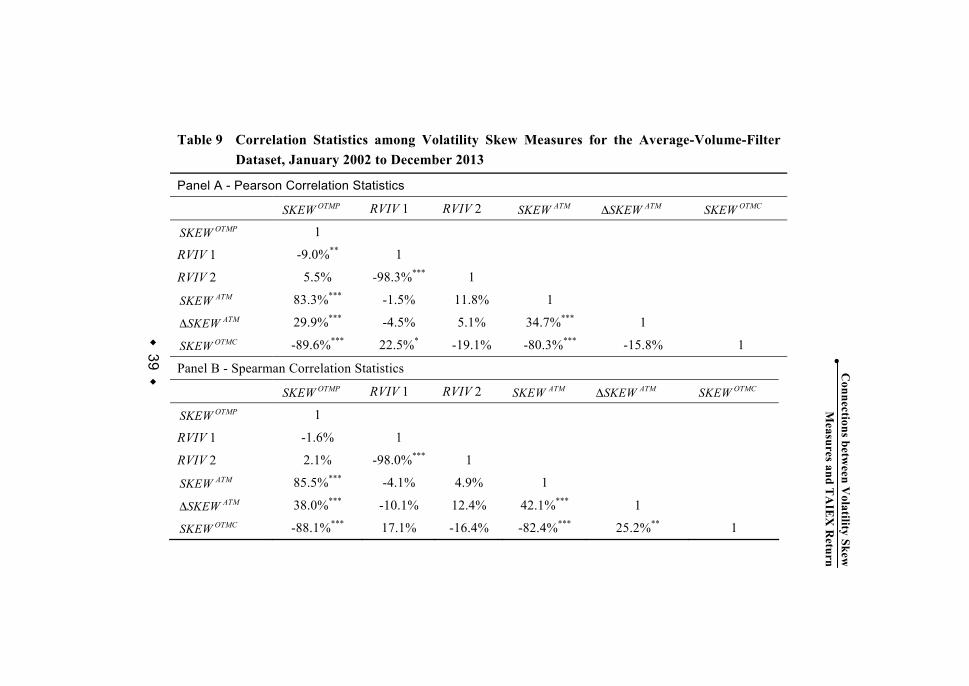

2.2 Correlations among Volatility Skew Measures

This subsection calculates correlations among the six volatility skew measures in order to supplement the analyses of multivariate OLS regressions in the later subsection. There are two types of bivariate correlation coefficients common in the literature. The first one is the Pearson correlation coefficient calculated in terms of variables’ original scales, which can help detect the collinearity problem in econometrics. The second one is the Spearman correlation coefficient calculated in terms of variables’ ranking scales, which is the non-parametric version of the Pearson correlation.

As shown in Panel A and Panel B of Table 6, both Pearson and Spearman statistics display very similar estimated results. Except for ( ATMSKEW∆ , RVIV 1) and ( ATMSKEW∆ , RVIV 2), the correlation coefficients of other pairs are all different from zero at the 1% significance level. In particular, the absolute values of the correlation coefficients of four pairs are extremely high or in excess of 90%. They are ( ATMSKEW , OTMPSKEW ), ( OTMCSKEW , OTMPSKEW ), (RVIV 1, RVIV 2), and ( OTMCSKEW , ATMSKEW ), which means that the collinearity problem cannot be ignored. This problem will be further examined and dealt with in a later subsection of multivariate regression analyses.

30

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Table 6 Correlation Statistics among Volatility Skew Measures, January 2002 to December 2013 Panel A - Pearson Correlation Statistics OTMPSKEW RVIV 1 RVIV 2 ATMSKEW

ATMSKEW∆ OTMCSKEW OTMPSKEW 1

RVIV 1 -41.9%*** 1 RVIV 2 35.2%*** -96.3%*** 1

ATMSKEW 96.1%*** -35.4%*** 30.1%*** 1 ATMSKEW∆ 30.3%*** -2.7% 3.0% 33.8%*** 1

OTMCSKEW -96.5%*** 46.4%*** -40.2%*** -96.8%*** -31.1%*** 1 Panel B - Spearman Correlation Statistics OTMPSKEW RVIV 1 RVIV 2 ATMSKEW

ATMSKEW∆ OTMCSKEW OTMPSKEW 1

RVIV 1 -29.3%*** 1 RVIV 2 28.9%*** -98.8%*** 1

ATMSKEW 92.1%*** -25.1%*** 25.7%*** 1 ATMSKEW∆ 25.0%*** -2.1% 2.1% 32.0%*** 1

OTMCSKEW -92.2%*** 37.6%*** -37.9%*** -93.5%*** 26.1%*** 1 Note: Table 6 lists the correlation statistics among volatility skew measures from January 2002 to December 2013.

OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of the spot asset and at-the-money call options in two scales. ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicate significance at the 1%/5%/10% levels.

31

Connections between Volatility Skew Measures and TAIEX Return ‧

2.3 Multivariate Regressions

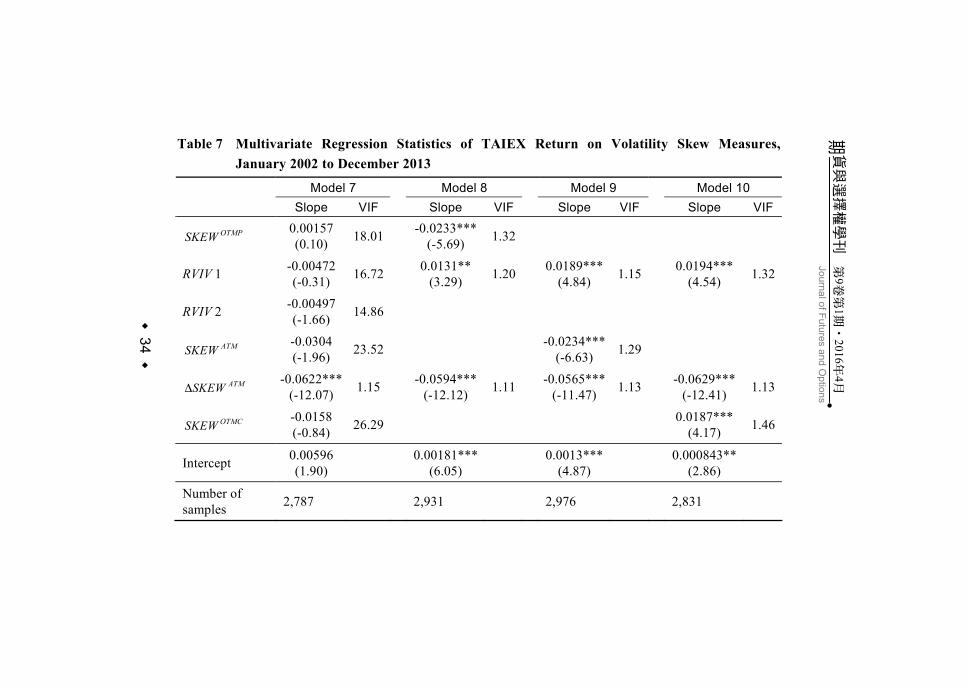

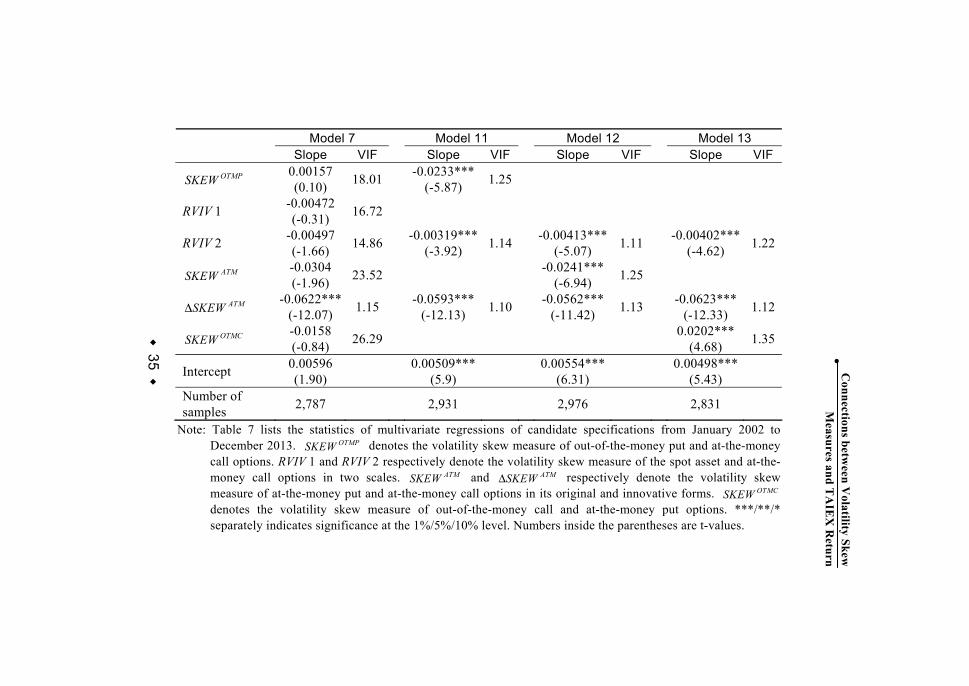

As shown in Table 5, each volatility skew measure significantly correlates with TAIEX return according to the single regression analyses, and they are all consistent with the expected correlation directions in the literature. This subsection presents the collective effects of these measures on spot return by multivariate regression specifications. The collinearity problem among these measures cannot be ignored in that the correlation coefficients of some pairs are extremely high as shown in Table 6, which may result in spurious statistics of the multivariate regressions. Here, the variance inflation faction (VIF) is employed to help detect the collinearity degrees of regressors in candidate multivariate specifications.

Table 7 lists the statistics of multivariate regressions. For instance, Model 7 specified in Equation (11) contains all six volatility skew measures as the regressors. However, the slope estimates are not unanimously consistent with their corresponding empirical results under the single regression framework, and they do not have the same expected directions of correlation with the spot market in the literature. Specifically, RVIV 1 and OTMCSKEW should be positively correlated with the spot market, while OTMPSKEW , RVIV 2,

ATMSKEW , and ATMSKEW∆ should be negatively correlated with the spot market, as explained in the subsection of single regressions. However, the regressors OTMPSKEW and RVIV 1 of Model 7 correlate with the spot market in opposite directions.

Only ATMSKEW∆ in Model 7 significantly correlates with TAIEX return. The other five measures are insignificant regressors

32

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

under the multivariate regression specification, which contradicts the empirical results of 1% significant slope estimates presented in the subsection of single regressions. We also note that only ATMSKEW∆ is endowed with a small VIF statistic, 1.15. The VIFs of the other five measures are pretty large, ranging from 14.86 to 26.09, which indicate that the collinearity is an issue.

Thus, it is consequently reasonable to discard some regressors of Model 7 to cope with the collinearity problem. ATMSKEW∆ is definitely the first one to be kept in the regression. We then consider the pairs in which the absolute values of correlation coefficients are extremely high or in excess of 90%. They are ( ATMSKEW , OTMPSKEW ), ( OTMCSKEW , OTMPSKEW ), (RVIV 1, RVIV 2), and ( OTMCSKEW , ATMSKEW ). RVIV 1 and RVIV 2 are the same except in different scales. Only one of them should be kept in a regression. It also can be found that two among OTMPSKEW ,

ATMSKEW , and OTMCSKEW can be discarded owing to their high correlations with each other.

Model 8~13 listed in Table 7 demonstrate all possible combinations of regressors after allowing for the above considerations. They are ( OTMPSKEW , RVIV 1, ATMSKEW∆ ), (RVIV 1, ATMSKEW ,

ATMSKEW∆ ), (RVIV 1, ATMSKEW∆ , OTMCSKEW ), ( OTMPSKEW , RVIV 2, ATMSKEW∆ ), (RVIV 2, ATMSKEW , ATMSKEW∆ ), and (RVIV 2, ATMSKEW∆ , OTMCSKEW ), for a total of six multivariate regressions. Note that the VIFs of their regressors range from 1.10 to 1.46, which are pretty small, implying that the collinearity problem may not be an issue for the six multivariate regressions.

In contrast to Model 7, the slope estimates in Models 8~13 are

33

Connections between Volatility Skew Measures and TAIEX Return ‧

overall significant at the 5% or 1% level. In fact, only regressor RVIV 1 in Model 8 is significant at the 5% level, as the other slope estimates in Models 8~13 are significant at the 1% level, which means that all of the measures are full of information contents about the spot market in the collective sense. In particular, the slope estimates are all consistent with the expected directions in the literature as noted in Table 2. The slope estimates are also all consistent with their corresponding empirical results under the single regression framework.

34

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Table 7 Multivariate Regression Statistics of TAIEX Return on Volatility Skew Measures, January 2002 to December 2013

Model 7 Model 8 Model 9 Model 10

Slope VIF Slope VIF Slope VIF Slope VIF

OTMPSKEW 0.00157 (0.10) 18.01 -0.0233***

(-5.69) 1.32

RVIV 1 -0.00472(-0.31) 16.72 0.0131**

(3.29) 1.20 0.0189*** (4.84) 1.15 0.0194***

(4.54) 1.32

RVIV 2 -0.00497(-1.66) 14.86

ATMSKEW -0.0304 (-1.96) 23.52 -0.0234***

(-6.63) 1.29

ATMSKEW∆ -0.0622***(-12.07) 1.15 -0.0594***

(-12.12) 1.11 -0.0565*** (-11.47) 1.13 -0.0629***

(-12.41) 1.13

OTMCSKEW -0.0158 (-0.84) 26.29 0.0187***

(4.17) 1.46

Intercept 0.00596 (1.90) 0.00181***

(6.05) 0.0013*** (4.87) 0.000843**

(2.86)

Number of samples 2,787 2,931 2,976 2,831

35 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

Model 7 Model 11 Model 12 Model 13 Slope VIF Slope VIF Slope VIF Slope VIF

OTMPSKEW 0.00157 (0.10) 18.01 -0.0233***

(-5.87) 1.25

RVIV 1 -0.00472(-0.31) 16.72

RVIV 2 -0.00497(-1.66) 14.86 -0.00319***

(-3.92) 1.14 -0.00413*** (-5.07) 1.11 -0.00402***

(-4.62) 1.22

ATMSKEW -0.0304 (-1.96) 23.52 -0.0241***

(-6.94) 1.25

ATMSKEW∆ -0.0622***(-12.07) 1.15 -0.0593***

(-12.13) 1.10 -0.0562*** (-11.42) 1.13 -0.0623***

(-12.33) 1.12

OTMCSKEW -0.0158 (-0.84) 26.29 0.0202***

(4.68) 1.35

Intercept 0.00596 (1.90) 0.00509***

(5.9) 0.00554*** (6.31) 0.00498***

(5.43)

Number of samples 2,787 2,931 2,976 2,831

Note: Table 7 lists the statistics of multivariate regressions of candidate specifications from January 2002 to December 2013. OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of the spot asset and at-the-money call options in two scales. ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicates significance at the 1%/5%/10% level. Numbers inside the parentheses are t-values.

36

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

3. The Effect of Liquidity In order to take into account the effect of liquidity on the relation

between the volatility skews and TAIEX return, we develop a liquidity filter to extract the trades with relative high liquidity. In contrast to considering the trades with nonzero trading volume (denoted as the zero-volume-filter dataset, hereafter), we set the liquidity filter to equal the average trading volume of the previous year. The dataset organized by the trades with relative high liquidity is denoted as the average-volume-filter dataset. The test applying the average-volume-filter dataset can examine the effect of liquidity on the relations between alternative skews/skew combinations and TAIEX return.

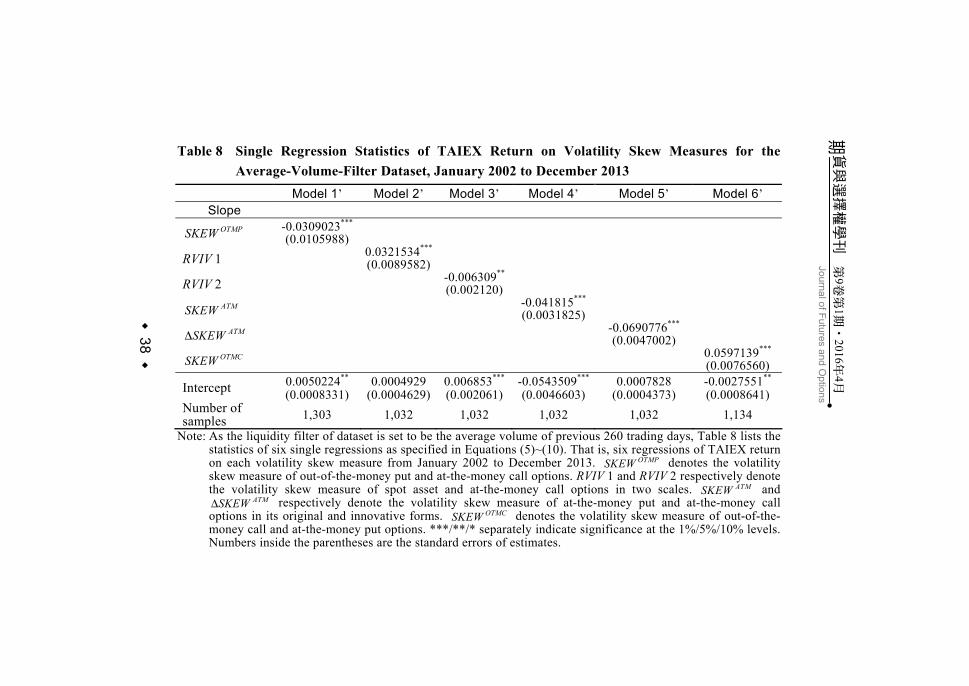

Table 8 shows the results of single regressions for the average-volume-filter dataset. We observe that all of the volatility skews are significantly related with TAIEX return at the expected directions illuminated by the literature.

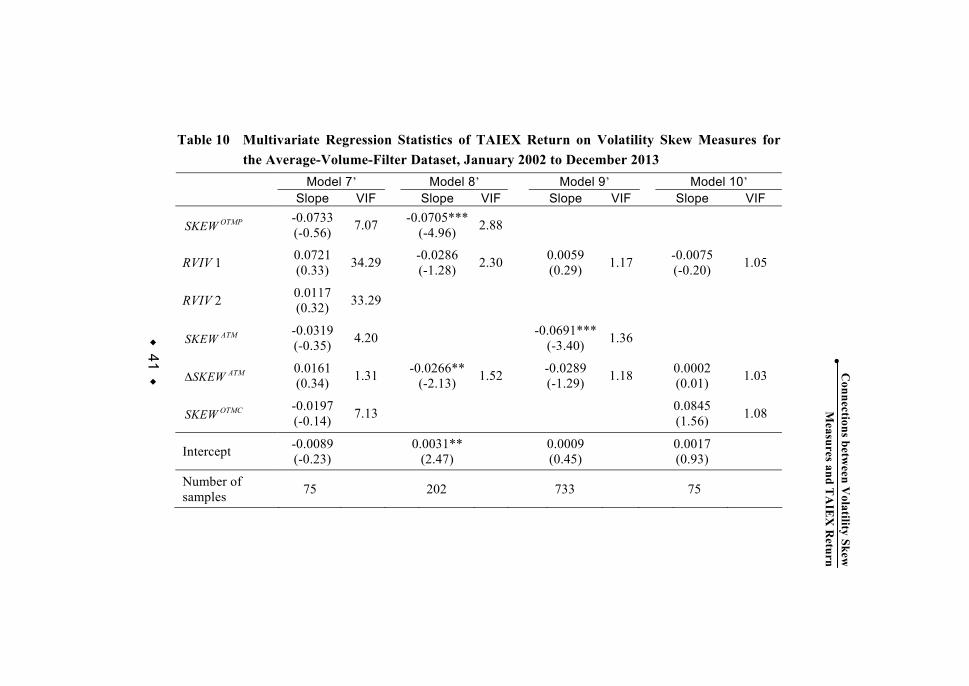

The single regression result shows that each of the six volatility skew measures is significantly correlated with TAIEX return for the zero-volume-filter dataset as well as the average-volume-filter dataset. In this subsection, we examine the collective effects of skew measures on TAIEX return by the alternative multivariate regression specifications. We follow the same criteria developed in 3.2.3 to deal with the potential collinearity problem. The alternative multivariate regression models are developed while the average-volume-filter dataset is applied. The results are summarized in Table 10. Model 7’ specified by Equation (11) in which simultaneously incorporates all six volatility skew measures. It shows that all of the six slope

37

Connections between Volatility Skew Measures and TAIEX Return ‧

estimates are not related with TAIEX return at 10% significant level even they are not unanimously consistent with their corresponding empirical results of single regression frameworks. Therefore, it is reasonable to discard some regressors of Model 7’ to cope with the collinearity problem. Model 8’~13’ demonstrate the possible combinations of skews after allowing for the previous considerations as those specified in Table 7 in which the zero-volume-filter dataset is applied. Note that the VIFs of regressors range from 1.02 to 2.88, which are smaller than the values of VIFs in Model 7’. It indicates that the collinearity problem can be lessened in these multivariate regression models. Comparing the results of multivariate regressions where the average-volume-filter dataset is applied with the corresponding results where the zero-volume-filter dataset is applied, we observe that most of the skew measures are still significantly correlated with the spot return at the expected directions. However, we also observe that some volatility skew measures such as RVIV 1, RVIV 2, and ATMSKEW∆ impose less connection on the spot return while the average-volume-filter dataset being applied.

38

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Table 8 Single Regression Statistics of TAIEX Return on Volatility Skew Measures for the Average-Volume-Filter Dataset, January 2002 to December 2013

Model 1’ Model 2’ Model 3’ Model 4’ Model 5’ Model 6’ Slope

OTMPSKEW -0.0309023***

(0.0105988)

RVIV 1 0.0321534***

(0.0089582)

RVIV 2 -0.006309** (0.002120)

ATMSKEW -0.041815***

(0.0031825)

ATMSKEW∆ -0.0690776***

(0.0047002)

OTMCSKEW 0.0597139***

(0.0076560)

Intercept 0.0050224**

(0.0008331)0.0004929

(0.0004629)0.006853*** (0.002061)

-0.0543509***

(0.0046603) 0.0007828

(0.0004373) -0.0027551**

(0.0008641) Number of samples 1,303 1,032 1,032 1,032 1,032 1,134

Note: As the liquidity filter of dataset is set to be the average volume of previous 260 trading days, Table 8 lists the statistics of six single regressions as specified in Equations (5)~(10). That is, six regressions of TAIEX return on each volatility skew measure from January 2002 to December 2013. OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of spot asset and at-the-money call options in two scales. ATMSKEW and

ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicate significance at the 1%/5%/10% levels. Numbers inside the parentheses are the standard errors of estimates.

39 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

Table 9 Correlation Statistics among Volatility Skew Measures for the Average-Volume-Filter Dataset, January 2002 to December 2013

Panel A - Pearson Correlation Statistics

OTMPSKEW RVIV 1 RVIV 2 ATMSKEW ATMSKEW∆ OTMCSKEW OTMPSKEW 1

RVIV 1 -9.0%** 1

RVIV 2 5.5% -98.3%*** 1 ATMSKEW 83.3%*** -1.5% 11.8% 1

ATMSKEW∆ 29.9%*** -4.5% 5.1% 34.7%*** 1 OTMCSKEW -89.6%*** 22.5%* -19.1% -80.3%*** -15.8% 1

Panel B - Spearman Correlation Statistics

OTMPSKEW RVIV 1 RVIV 2 ATMSKEW ATMSKEW∆ OTMCSKEW OTMPSKEW 1

RVIV 1 -1.6% 1

RVIV 2 2.1% -98.0%*** 1 ATMSKEW 85.5%*** -4.1% 4.9% 1

ATMSKEW∆ 38.0%*** -10.1% 12.4% 42.1%*** 1 OTMCSKEW -88.1%*** 17.1% -16.4% -82.4%*** 25.2%** 1

40

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Note: As the liquidity filter of dataset is set to be the average volume of previous 260 trading days, Table 9 lists the correlation statistics among volatility skew measures from January 2002 to December 2013. OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of the spot asset and at-the-money call options in two scales. ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicate significance at the 1%/5%/10% levels.

41 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

Table 10 Multivariate Regression Statistics of TAIEX Return on Volatility Skew Measures for the Average-Volume-Filter Dataset, January 2002 to December 2013

Model 7’ Model 8’ Model 9’ Model 10’ Slope VIF Slope VIF Slope VIF Slope VIF

OTMPSKEW -0.0733 (-0.56) 7.07 -0.0705***

(-4.96) 2.88

RVIV 1 0.0721 (0.33) 34.29 -0.0286

(-1.28) 2.30 0.0059 (0.29) 1.17 -0.0075

(-0.20) 1.05

RVIV 2 0.0117 (0.32) 33.29

ATMSKEW -0.0319 (-0.35) 4.20 -0.0691***

(-3.40) 1.36

ATMSKEW∆ 0.0161 (0.34) 1.31 -0.0266**

(-2.13) 1.52 -0.0289 (-1.29) 1.18 0.0002

(0.01) 1.03

OTMCSKEW -0.0197 (-0.14) 7.13 0.0845

(1.56) 1.08

Intercept -0.0089 (-0.23) 0.0031**

(2.47) 0.0009 (0.45) 0.0017

(0.93)

Number of samples 75 202 733 75

42

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Model 7’ Model 11’ Model 12’ Model 13’ Slope VIF Slope VIF Slope VIF Slope VIF

OTMPSKEW -0.0733(-0.56) 7.07 -0.0884***

(-3.46) 1.09

RVIV 1 0.0721 (0.33) 34.29

RVIV 2 0.0117 (0.32) 33.29 -0.0009

(-0.27) 1.02 0.0010 (0.49) 1.11 0.0045

(0.90) 1.68

ATMSKEW -0.0319(-0.35) 4.20 -0.0477***

(-8.87) 1.25

ATMSKEW∆ 0.0161 (0.34) 1.31 -0.0306

(-1.38) 1.09 -0.0310*** (-4.03) 1.13 -0.0338***

(-2.86) 1.34

OTMCSKEW -0.0197(-0.14) 7.13 0.0564***

(4.96) 2.05

Intercept -0.0089(-0.23) 0.0060

(1.65) 0.00554*** (6.31) -0.0032

(-0.63)

Number of samples 75 206 733 203

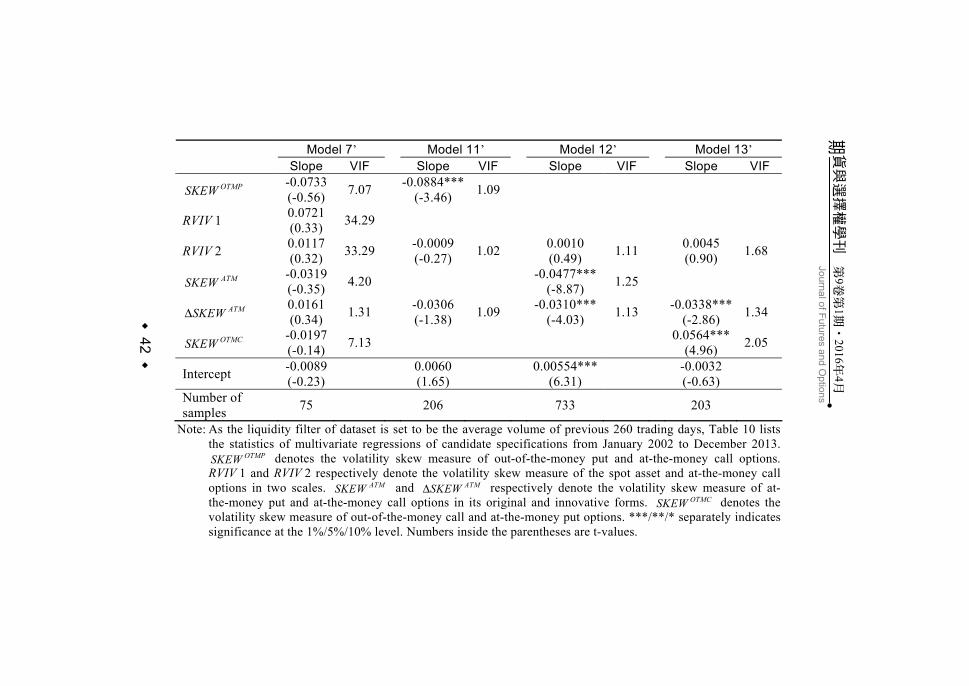

Note: As the liquidity filter of dataset is set to be the average volume of previous 260 trading days, Table 10 lists the statistics of multivariate regressions of candidate specifications from January 2002 to December 2013.

OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of the spot asset and at-the-money call options in two scales. ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicates significance at the 1%/5%/10% level. Numbers inside the parentheses are t-values.

43

Connections between Volatility Skew Measures and TAIEX Return ‧

4. The Impact of the 2008 Financial Tsunamis In order to consider the impact of the 2008 financial tsunamis on

the relation between the skew measures and TAIEX return, we apply the single regression models and multivariate regression models developed in the previous section to examine the relation between the volatility skew measures and TAIEX return after the financial tsunamis (2008/1-2013/12).

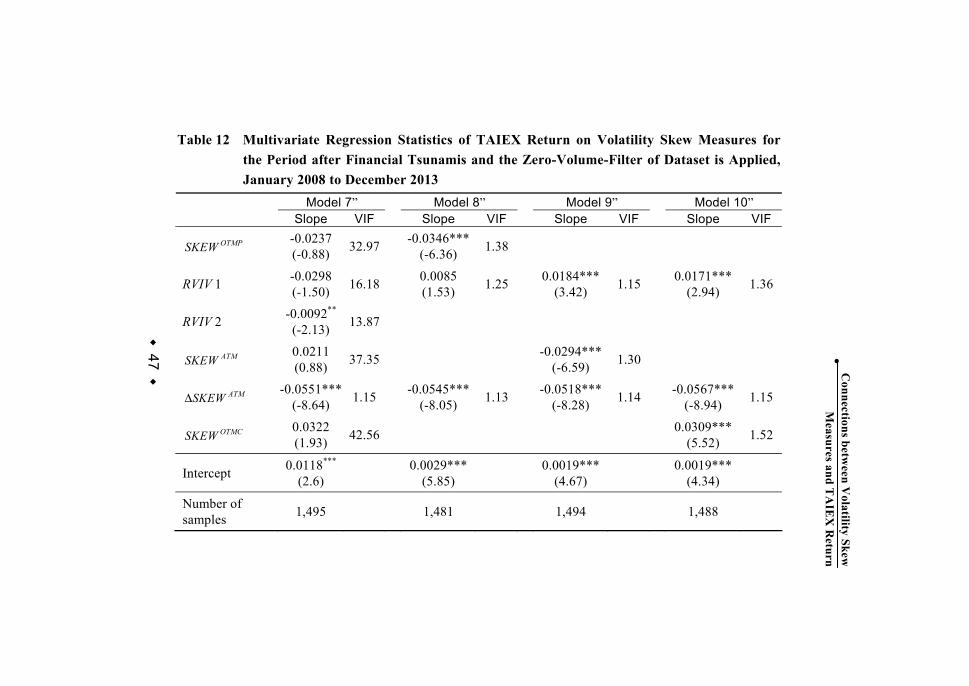

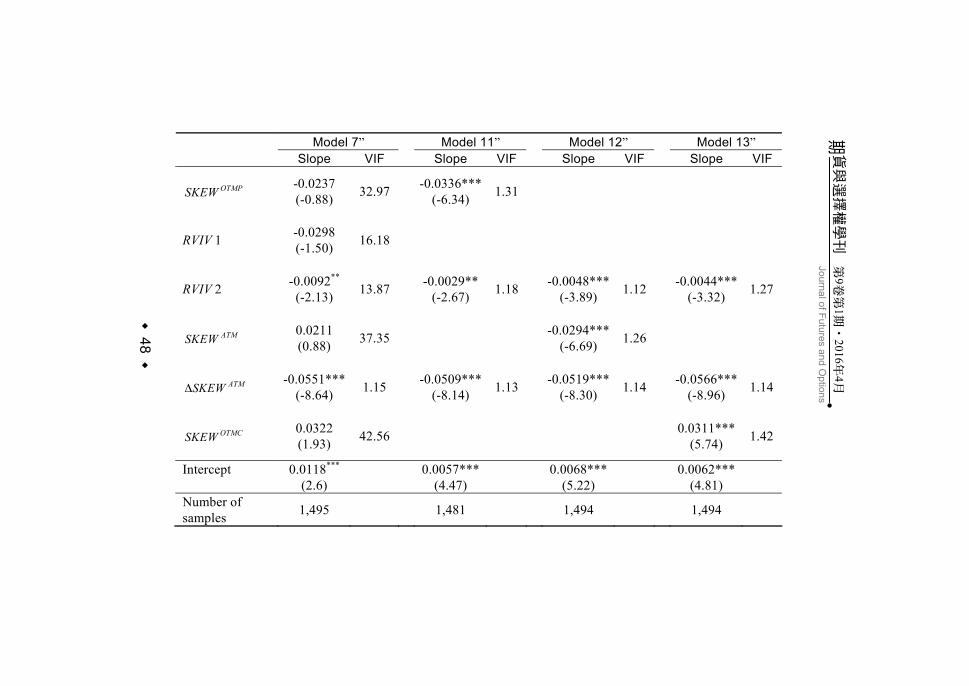

Tables 11 shows the results of single regressions after the financial tsunamis in the case of the zero-volume-filter dataset being applied. We observe that all the six skew measures are still related with spot return at 1% significant level after the financial tsunamis. The results of multivariate regressions for the period after the financial tsunamis are presented in Table 12. Model 7’’ specified in Equation (11) contains all six volatility skew measures. Model 8’’~13’’ demonstrate corresponding specifications as those specified in the former subsections. We observe that only the RVIV 1 in Model 8’’ is not statistically related with TAIEX return, the other combinations of skew measures are all correlated with TAIEX return at 1% significantly level during the period after the financial tsunamis.

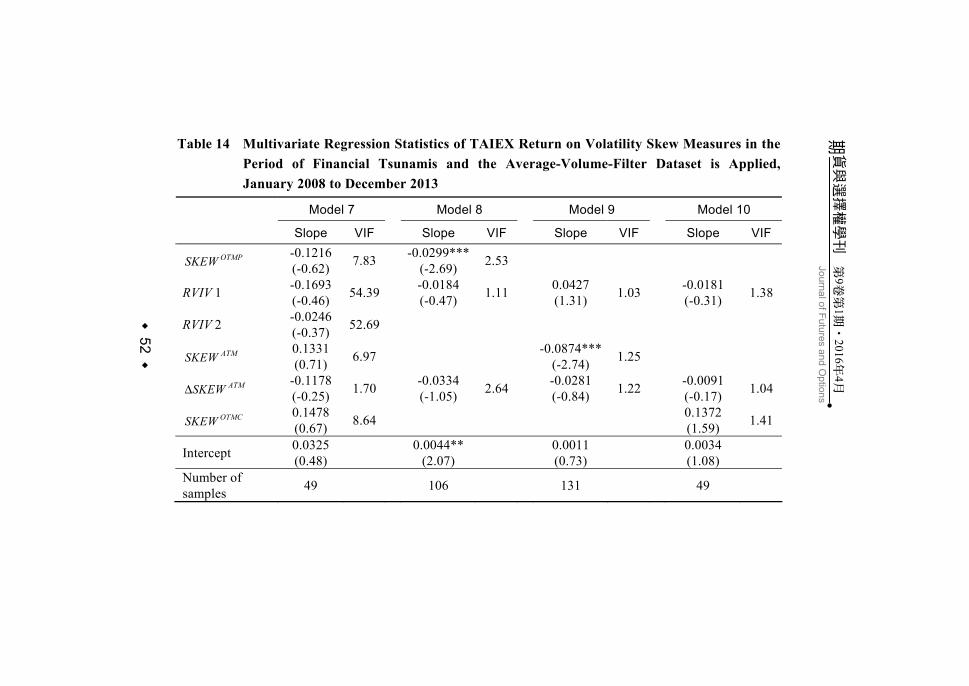

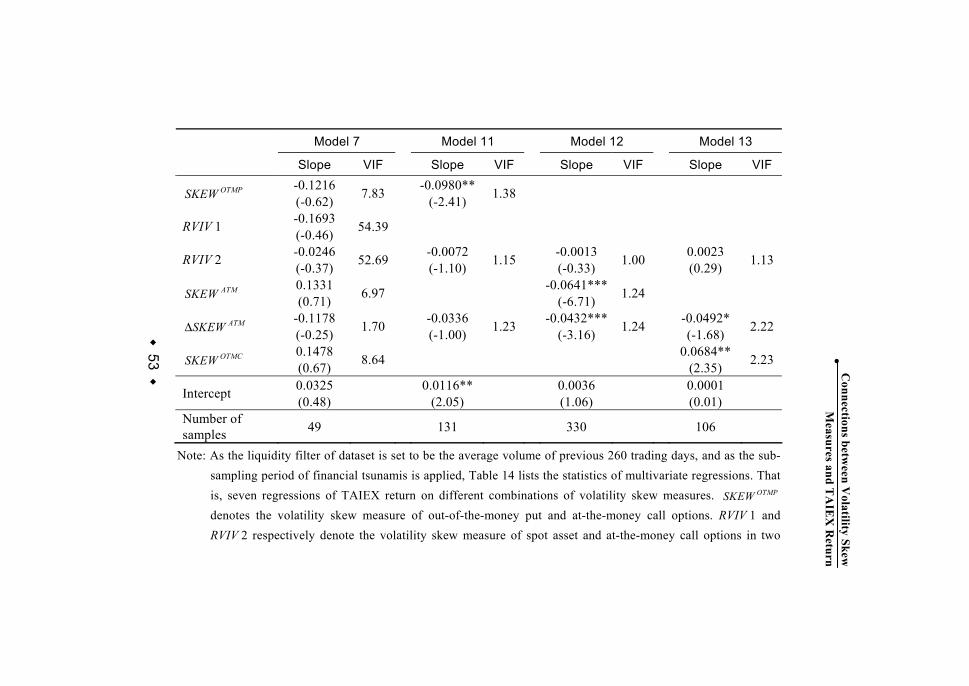

The results of single regressions and multivariate regressions during the period after the financial tsunamis while the average-volume-filter dataset being applied are presented in Tables 13 and 14, respectively. We observe that only three of the six skew measures,

ATMSKEW , ATMSKEW∆ , and OTMCSKEW , are correlated with TAIEX return at 1% significant level after the financial tsunamis. The result of multivariate regression shows that the correlation between the skew measures and TAIEX return become weaker after the financial

44

Journal of Futures and Options期貨與選擇權學刊 第9卷第1期 201‧ 6年4月

‧

tsunamis when the average-volume-filter dataset is applied. The phenomenon may be attributed to the interaction effect of volatility skews, liquidity and time-varying systematic risk on the capital markets. The issue is worth of exploring in the future.

45 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

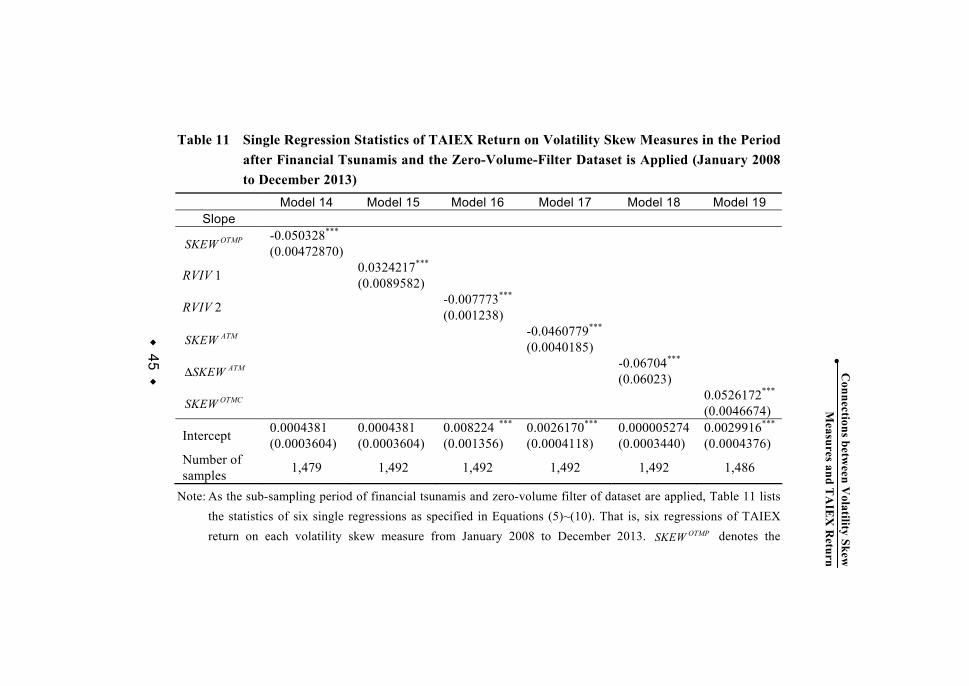

Table 11 Single Regression Statistics of TAIEX Return on Volatility Skew Measures in the Period after Financial Tsunamis and the Zero-Volume-Filter Dataset is Applied (January 2008 to December 2013)

Model 14 Model 15 Model 16 Model 17 Model 18 Model 19 Slope

OTMPSKEW -0.050328***

(0.00472870)

RVIV 1 0.0324217*** (0.0089582)

RVIV 2 -0.007773*** (0.001238)

ATMSKEW -0.0460779***

(0.0040185)

ATMSKEW∆ -0.06704***

(0.06023)

OTMCSKEW 0.0526172***

(0.0046674)

Intercept 0.0004381

(0.0003604) 0.0004381 (0.0003604)

0.008224 *** (0.001356)

0.0026170***

(0.0004118) 0.000005274(0.0003440)

0.0029916***

(0.0004376)Number of samples 1,479 1,492 1,492 1,492 1,492 1,486

Note: As the sub-sampling period of financial tsunamis and zero-volume filter of dataset are applied, Table 11 lists the statistics of six single regressions as specified in Equations (5)~(10). That is, six regressions of TAIEX return on each volatility skew measure from January 2008 to December 2013. OTMPSKEW denotes the

46

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of spot asset and at-the-money call options in two scales.

ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicate significance at the 1%/5%/10% levels. Numbers inside the parentheses are the standard errors of estimates.

47 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

Table 12 Multivariate Regression Statistics of TAIEX Return on Volatility Skew Measures for the Period after Financial Tsunamis and the Zero-Volume-Filter of Dataset is Applied, January 2008 to December 2013

Model 7” Model 8” Model 9” Model 10” Slope VIF Slope VIF Slope VIF Slope VIF

OTMPSKEW -0.0237(-0.88) 32.97 -0.0346***

(-6.36) 1.38

RVIV 1 -0.0298(-1.50) 16.18 0.0085

(1.53) 1.25 0.0184*** (3.42) 1.15 0.0171***

(2.94) 1.36

RVIV 2 -0.0092**

(-2.13) 13.87

ATMSKEW 0.0211 (0.88) 37.35 -0.0294***

(-6.59) 1.30

ATMSKEW∆ -0.0551***(-8.64) 1.15 -0.0545***

(-8.05) 1.13 -0.0518*** (-8.28) 1.14 -0.0567***

(-8.94) 1.15

OTMCSKEW 0.0322 (1.93) 42.56 0.0309***

(5.52) 1.52

Intercept 0.0118***

(2.6) 0.0029***(5.85) 0.0019***

(4.67) 0.0019***(4.34)

Number of samples 1,495 1,481 1,494 1,488

48

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Model 7” Model 11” Model 12” Model 13” Slope VIF Slope VIF Slope VIF Slope VIF

OTMPSKEW -0.0237 (-0.88) 32.97 -0.0336***

(-6.34) 1.31

RVIV 1 -0.0298 (-1.50) 16.18

RVIV 2 -0.0092**

(-2.13) 13.87 -0.0029**(-2.67) 1.18 -0.0048***

(-3.89) 1.12 -0.0044***(-3.32) 1.27

ATMSKEW 0.0211 (0.88) 37.35 -0.0294***

(-6.69) 1.26

ATMSKEW∆ -0.0551***(-8.64) 1.15 -0.0509***

(-8.14) 1.13 -0.0519*** (-8.30) 1.14 -0.0566***

(-8.96) 1.14

OTMCSKEW 0.0322 (1.93) 42.56 0.0311***

(5.74) 1.42

Intercept 0.0118***

(2.6) 0.0057***(4.47) 0.0068***

(5.22) 0.0062***(4.81)

Number of samples 1,495 1,481 1,494 1,494

49 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

Note: As the sub-sampling period of financial tsunamis and zero-volume filter of dataset are applied, Table 12 lists the statistics of multivariate regressions. That is, seven regressions of TAIEX return on different combinations of volatility skew measures. OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of spot asset and at-the-money call options in two scales. ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicate significance at the 1%/5%/10% levels. Numbers inside the parentheses are the standard errors of estimates.

50

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Table 13 Single Regression Statistics of TAIEX Return on Volatility Skew Measures in the Period after the Financial Tsunamis and the Average-Volume-Filter Dataset is Applied, January 2008 to December 2013

Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Slope

OTMPSKEW -0.024989

(0. 015486)

RVIV 1 -0.0181572 (0.0189681)

RVIV 2 -0.0006053 (0.0042665)

ATMSKEW -0.077330***

(0.008693)

ATMSKEW∆ -0.0835129***

(0.0130656)

OTMCSKEW 0.101494*** (0.018296)

Intercept 0. 003637

(0. 001399)0.0016210* (0.0007356)

0.0019108 (0.0040261)

0.003119***

(0.000641) 0.0009854

(0.0006427) -0.001209

(0.001182) Number of samples 215 330 330 330 330 177

Note: As the liquidity filter of dataset is set to be the average volume of previous 260 trading days, and as the sub-sampling period of financial tsunamis is applied, Table 13 lists the statistics of six single regressions as specified in Equations (5)~(10). That is, six regressions of TAIEX return on each volatility skew measure

51 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

from January 2008 to December 2013. OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of spot asset and at-the-money call options in two scales. ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicate significance at the 1%/5%/10% levels. Numbers inside the parentheses are the standard errors of estimates.

52

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

Table 14 Multivariate Regression Statistics of TAIEX Return on Volatility Skew Measures in the Period of Financial Tsunamis and the Average-Volume-Filter Dataset is Applied, January 2008 to December 2013

Model 7 Model 8 Model 9 Model 10

Slope VIF Slope VIF Slope VIF Slope VIF

OTMPSKEW -0.1216(-0.62) 7.83 -0.0299***

(-2.69) 2.53

RVIV 1 -0.1693(-0.46) 54.39 -0.0184

(-0.47) 1.11 0.0427 (1.31) 1.03 -0.0181

(-0.31) 1.38

RVIV 2 -0.0246

(-0.37) 52.69

ATMSKEW 0.1331 (0.71) 6.97 -0.0874***

(-2.74) 1.25

ATMSKEW∆ -0.1178(-0.25) 1.70 -0.0334

(-1.05) 2.64 -0.0281 (-0.84) 1.22 -0.0091

(-0.17) 1.04

OTMCSKEW 0.1478 (0.67) 8.64 0.1372

(1.59) 1.41

Intercept 0.0325

(0.48) 0.0044**(2.07) 0.0011

(0.73) 0.0034 (1.08)

Number of samples 49 106 131 49

53 ‧Connections betw

een Volatility Skew

M

easures and TA

IEX

Return

Model 7 Model 11 Model 12 Model 13

Slope VIF Slope VIF Slope VIF Slope VIF

OTMPSKEW -0.1216 (-0.62) 7.83 -0.0980**

(-2.41) 1.38

RVIV 1 -0.1693 (-0.46) 54.39

RVIV 2 -0.0246

(-0.37) 52.69 -0.0072 (-1.10) 1.15 -0.0013

(-0.33) 1.00 0.0023 (0.29) 1.13

ATMSKEW 0.1331 (0.71) 6.97 -0.0641***

(-6.71) 1.24

ATMSKEW∆ -0.1178 (-0.25) 1.70 -0.0336

(-1.00) 1.23 -0.0432*** (-3.16) 1.24 -0.0492*

(-1.68) 2.22

OTMCSKEW 0.1478 (0.67) 8.64 0.0684**

(2.35) 2.23

Intercept 0.0325

(0.48) 0.0116**(2.05) 0.0036

(1.06) 0.0001 (0.01)

Number of samples 49 131 330 106

Note: As the liquidity filter of dataset is set to be the average volume of previous 260 trading days, and as the sub-sampling period of financial tsunamis is applied, Table 14 lists the statistics of multivariate regressions. That is, seven regressions of TAIEX return on different combinations of volatility skew measures. OTMPSKEW denotes the volatility skew measure of out-of-the-money put and at-the-money call options. RVIV 1 and RVIV 2 respectively denote the volatility skew measure of spot asset and at-the-money call options in two

54

期貨與選擇權學刊

第

9卷

第1期

201‧

6年

4月

Journal of Futures and O

ptions

‧

scales. ATMSKEW and ATMSKEW∆ respectively denote the volatility skew measure of at-the-money put and at-the-money call options in its original and innovative forms. OTMCSKEW denotes the volatility skew measure of out-of-the-money call and at-the-money put options. ***/**/* separately indicate significance at the 1%/5%/10% levels. Numbers inside the parentheses are the standard errors of estimates.

55

Connections between Volatility Skew Measures and TAIEX Return ‧

IV. Conclusion

Call and put contracts can satisfy traders’ investing demands when coping with different expectation scenarios conditional on their asymmetric risk attitudes. On the other hand, the no-arbitrage argument connects option and spot markets in a natural way. However, some favorable frictions make investors tend to trade and reveal their private information in the option market instead of or prior to their corresponding operation in the spot market. All these merits endow the option market with a price discovery function relative to the spot market. Consequently, it is interesting to probe into the connection between the two markets.

Information contents of such a connection can be detected or proxied not only by price or return series, but also by volatility measures. This study is one of the few to examine the Taiwan markets in terms of volatility measures. Six skew measures consisting of realized and implied volatilities with the moneyness consideration are applied to address this issue. The TAIEX return is regressed on these measures under the frameworks of single and multivariate regressions allowing for the collinearity problem.