Necessity Drives Value - نادي خبراء المال...

35

REGIONAL FOOD | KFC June 21, 2010 Please Read Last Page For Contact Details and Important Disclaimer Kuwait Food Company (Americana) Necessity Drives Value jam

Transcript of Necessity Drives Value - نادي خبراء المال...

REGIONAL FOOD | KFC

June 21, 2010

Please Read Last Page For Contact Details and Important Disclaimer

Kuwait Food Company (Americana)

Necessity Drives Value

jam

REGIONAL FOOD | KFC

June 21, 2010

2

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Kuwait Food Co. (Americana) Necessity Drives Value Frenetic lifestyles, increasingly westernised habits and a large youth base are all helping to spur demand for both processed food and fast food outlets within the Middle East. The world-wide slowdown in economic growth and accompanying expatriate layoffs in GCC countries served to dampen the growth in demand for processed food yet, despite this, fast food restaurant turnover remained relatively unscathed. In this note we initiate coverage on Kuwait Food Company (KFC) [FOOD], one of the largest food conglomerates in the Middle East. The company operates 19 chains of restaurants with over 1000 restaurants in 79 cities, as well as running 21 industrial companies. KFC enjoys a strong market share in Egypt in the dairy and processed chicken segments whilst it has a similar influence in the GCC in regards to meat processing, frozen potatoes and canned beans. KFC is traded at 2010E EV/EBITDA of 6.5x vs. a composite peer average of 9.4x, and market average of 13.2x. We initiate coverage of the stock with an LTFV of KWD1.83/share and a target price of KWD1.64/share. Given the 18% upside potential vs. the target price we advocate a Hold rating.

Healthy business drivers: The food retail industry in the Middle East and North Africa (MENA) region enjoys strong growth potential mainly due to the high population growth and strong base of youth. Restaurants are a primary source of entertainment for families in the GCC market.

Robust business model: With 19 restaurant chains, KFC caters to a wide consumer base in the MENA region. The company has a strong portfolio of processed food ranging from meat and dairy to vegetables.

Valuation & Recommendation: KFC is valued using a sum-of-the-parts valuation method. We reached a fair value of KWD1.83/share and incorporated the book value of the available for sale investments into our valuation. KFC is traded at EV/EBITDA 2010E of 6.5x, a 31% discount vs. a composite peer average of 9.4x. Nevertheless, we are concerned with the negative technical view on the Kuwait Stock Exchange (KSE). Our target price is KWD1.64/share for KFC based on the estimated target EV/EBITDA of 7.5x. Given the 18% upside potential, we initiate coverage on the stock with a Hold rating.

KWD mn 2008 A 2009 A 2010 F 2011 F 2012 F

Revenues 557.45 616.43 691.21 754.83 824.94Growth rate 28.2% 10.6% 12.1% 9.2% 9.3%

EBITDA 103.82 86.78 101.61 114.70 124.15Growth rate 69.6% -16.4% 17.1% 12.9% 8.2%EBITDA margin 18.6% 14.1% 14.7% 15.2% 15.0%

Net income 35.22 36.28 39.61 46.69 50.28Growth rate -35.9% 3.0% 9.2% 17.9% 7.7%Net margin 6.3% 5.9% 5.7% 6.2% 6.1%

PER 15.3x 14.9x 13.6x 11.6x 10.7xP/BV 2.2x 1.9x 1.8x 1.8x 1.7xEV/EBITDA 6.6x 7.3x 6.5x 5.7x 5.2xNet debt/EBITDA 1.4x 1.1x 1.2x 1.0x 0.8xDividend yield 5.6% 4.3% 5.6% 6.6% 7.1% Source: Company reports & CICR analysis

INGY EL-DIWANY

HOLD LT FAIR VALUE | KWD1.83 TARGET PRICE | KWD1.64

COMPANY SYNOPSIS Kuwait food Company (Americana) was established in 1963 in Kuwait. KFC is one of the Middle East's largest group of companies operating in the following segments:

(i) Restaurants sector: KFC runs 19 chains of restaurants, in the fields of Fast Food, Casual Dining, cafés and Pastries.

(ii) Industries Sector: KFC manufactures frozen and processed meat, canned and frozen vegetables, tuna and canned fruits, confectionary items and cakes. Also, the company operates in the field of dairy products and runs one of the Middle East’s largest Poultry companies, Cairo Poultry.

(iii) Commercial and retail segment which runs agencies for distribution in Kuwait of Heinz for processed tomato and Ketchup, Cadbury chocolates, and others.

Also, KFC invests surplus funds in investment portfolios. These investments exceed KWD177mn.

SHAREHOLDER STRUCTURE

Al-Kharafi National Co. for Stocks & Real Estate 66.8%Kuwait food Company 2.70%Public 30.5% STOCK DATA Reuters; Bloomberg FOOD.KK Recent price as of 20-Jun-10 KWD1.38No. of outstanding shares 391 mnMarket cap KWD540 mn52-wk high / low KWD1.94 KWD1.18Avg. daily volume / turnover 0.14 mn / KWD229.5 mn

STOCK PERFORMANCE | 52 WEEKS

-

0.5

1.0

1.5

2.0

2.5

0.000.200.400.600.801.001.201.401.601.802.00

Jun-09 Sep-09 Jan-10 May-10

mn sharesKWD

Volume FOOD KWSE-rebased

Source: Bloomberg

REGIONAL FOOD | KFC

June 21, 2010

3

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Table of Contents Executive Summary _______________________________________________________________ 4 I. Investment Case ________________________________________________________________ 5 II. Valuation ______________________________________________________________________ 7 III. Industry Overview _____________________________________________________________ 14

A. Global Food Business _________________________________________________________ 14

B. Food Industry in the MENA Region _______________________________________________ 15 1. Main Characteristics ______________________________________________________________ 15

2. Dynamics of the Food Industry ______________________________________________________ 16

3. Key Regional Food Markets _________________________________________________________ 18

4. Future Outlook ___________________________________________________________________ 21

IV. Company Profile ______________________________________________________________ 23 A. Company Synopsis ___________________________________________________________ 23

B. Business segments ___________________________________________________________ 24

C. Recent Developments _________________________________________________________ 27

V. Operational and Financial Analysis _______________________________________________ 28 A. Operational Analysis __________________________________________________________ 28

B. Financial Analysis ____________________________________________________________ 29

i. Dec 2005–Dec 2009 _________________________________________________________ 29

ii. Interim Financial Summary (1Q10 vs. 1Q09) ______________________________________ 31

VI. Projection Assumptions ________________________________________________________ 32

REGIONAL FOOD | KFC

June 21, 2010

4

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Executive Summary

A shift in consumption patterns towards ready-to-eat food and out-of-home consumption is driving growth in the food market. Global food sales, estimated to be in the vicinity of USD6.7tn in 2009, consist of the retail food (fresh and processed food) and the food service establishment (restaurants and hotels) segments.

Kuwait Food Company (KFC) [FOOD] is one of the largest food players in the MENA region. And it really is a regional entity, operating in the GCC, Egypt and Africa, as well as the Levant.

The food market in the MENA region is sizable, with Egypt accounting for 51% of food sales with a total food retail value of USD44.8bn in 2009. In Egypt, the food industrial market is relatively underpenetrated as the vast majority of population lies within the mid-to-low income segments that prefer traditional fresh food products. The food service market is concentrated, with a few fast food outlets dominating the market.

Saudi Arabia is one of the most attractive consumer markets in the region in light of its large population base, a large tranche of foreign labour and the increasing average income in recent years. On top of this, demand from pilgrims for convenience foods such as pre-packed and ready-to-eat meals makes a major contribution to food retail sales and fast food chains.

Kuwait too provides a healthy potential for the food industry, driven in large by (i) a high GDP/Capita, and (ii) a young expat population (86% of the foreign population is between 15 and 64 years old).

KFC is a consumer-driven company and operates three business segments: a restaurants segment (51% of total revenues in 2009), industries segment (46% of revenues in 2009) and a commercial and retail segment (3% of revenues in 2009).

Through its restaurants and industries segments, KFC caters to a raft of different consumption patterns across the MENA region. Indeed, KFC operated international franchises across 79 cities in the MENA region through 1,157 restaurants under 19 restaurant chains at the end of 2009. Through its industries segment, KFC offers packaged food and enjoys a strong position in the manufacturing of meat, dairy products, and canned and frozen vegetables in its markets. The company’s packaged food business targets middle and high-end income classes who prefer buying ready-to-eat foods. The commercial & retail sector handles the distribution of Heinz ketchup and California Garden for canned foods in Kuwait.

KFC adopts a backward integration strategy by sourcing some of its basic requirements for chicken for its meat plants and restaurants from its subsidiary, Cairo Poultry Company [POUL]. Furthermore, KFC cultivates a number of crops used for production at its factories, including potatoes and vegetables for its subsidiaries Farm Frites and Egyptian Canning Company.

Though the prospects for KFC are promising, we believe rising food prices will remain the company’s main concern with prices expected to increase in light of the anticipated rebound in the global economy. To negotiate this, KFC is seeking to minimize its costs by diversifying purchase sources and rationalize its expenses along the value chain.

KFC is valued using a sum-of-the-parts valuation method. We reached a fair value of KWD1.83/share, providing a 33% upside potential over the recent market price. We incorporated the book value of the available for sale investments into our valuation. Despite the solid performance for the company being traded at EV/EBITDA 2010E of 6.5x, a 31% discount vs. peer composite average of 9.4x, we are mostly concerned with the negative technical view of the Kuwait Stock Exchange (KSE). Our target price for KFC is KWD1.64/share and, given the 18% upside potential, we assign the stock a Hold rating.

Global food sales estimated at USD6.7tn in 2009

Egypt accounted for 51% of the sizeable food market in the MENA region

Saudi Arabia is an attractive consumer market

Healthy potential in the Kuwaiti market

KFC operates in the food service and the food retail sectors

Part of KFC’s needs are supplied within the group

Rising food prices remain the company’s main concern

LTFV is KWD1.83/share Target price is KWD1.64/share; Recommendation: Hold

REGIONAL FOOD | KFC

June 21, 2010

5

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

I. Investment Case

Positives

Healthy business drivers: The food industry in the Middle East and North Africa (MENA) region enjoys strong growth potential mainly due to the high average population growth (2%), strong base of youth population, increasing per capita income, and high expenditure on food. Furthermore, increasing westernization and changing lifestyles are accelerating the region’s demand for fast food restaurants and ready-to-eat food. Also, restaurants are the major source of entertainment for families in the GCC markets. Consequently, the food franchise business has grown in the MENA region with countries such as Egypt, Saudi Arabia, Kuwait, and the UAE being considered the main markets. Against this backdrop, Kuwait Food Company (KFC) is well positioned to benefit with its strong brand name, wide geographic reach and diversified portfolio.

Robust business model: KFC has a robust business model, catering to the wide consumer preferences in the MENA region and overseas. The company maintains a strong market share in the food service and retail segments. The company caters in large part to the consumer segment (young, middle-income) that prefers fast food through its 19-strong chain of restaurants. These chains vary from international franchises (10 chains) for world famous brands such as Kentucky Fried Chicken, Hardee’s, Pizza Hut to the company’s own chains such as Tikka and Fish Market. Furthermore, KFC has a strong portfolio of packaged foods ranging from meat, chicken, and dairy products to canned and frozen vegetables and cakes and pastries. Such a product portfolio targets the daily food needs of consumers who prefer cooking food at home or buying ready-to-eat foods.

Successful growth strategy: KFC has been growing rapidly through a combination of organic and external growth. KFC managed to grow its restaurants segment by increasing the number of food outlets from 669 in 2004 to 1,157 in 2009 in 79 cities across the MENA region. The strong network of well-known international brand names under its franchise portfolio has enabled KFC to become a distinguished player in the region. Furthermore, on the industry front, its number of subsidiaries grew from 6 in 1998 to 21 in 2009. The company acquired a control stake in a number of leading players in Egypt, namely Greenland (which specialises in dairy products) in 2004, the Senyorita Group of Companies in 2006 and Cairo Poultry in 2007.

Backward integration enables cost efficiency: Through its own cultivation and land reclamation, the company secures basic raw materials for its industries sector (like potato and vegetables and other agricultural products that can be exported like strawberry). Furthermore, through the purchase of a 51% stake in Cairo Poultry in 2007, KFC obtained a partially reliable source of raw material for its restaurants. Its backward-integration strategy helps the company to reduce raw material costs, improve profitability and sell its products at reasonable prices in the MENA region.

Developing its supply chains: KFC maintains a strong relationship with its suppliers. This helps reduce storage time.

Demand for fast food spurred by:

i. High population growth,

ii. Strong youth base

iii. Increasing westernization

iv. Restaurants are a major sourceof entertainment in the GCC.

KFC has a strong market position in the food service sector and processed food sector

Organic and external growth strategies

Potato cultivation and the acquisition of Cairo Poultry partially help secure basic raw materials

REGIONAL FOOD | KFC

June 21, 2010

6

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Negatives

Volatility of food prices: The food industry is largely dependent on food prices which are sensitive to changes in economic conditions and subject to supply and demand forces. We believe prices will increase in the long-run given the expected global economic recovery. That said, the company’s vertical integration strategy and strong supplier base should partially offset rising food prices. In 2009, the EBITDA margin was pressured on the back of the company’s strategy to maintain market share, of only partially passing the higher costs of some of the raw materials, which came at the expense of lower margins.

Increasing competition: The food market in the MENA is concentrated, with a few large players dominating the market. Competition in the food industry has escalated recently on account of new players entering the lucrative market, both in the restaurants segment and the food manufacturing segment. This has made the industry sensitive to price and quality issues. However, KFC’s innovative products (more appealing to middle and high-end consumers) have helped the company maintain its market share.

Economic slowdown pressured growth: As a result of the global economic slowdown, consumers have become more price sensitive, preferring to purchase low-priced products and value meals. Moreover, some families cut their spending. We believe fast food restaurants like Hardee’s and other casual dining restaurants such as Pizza Hut and Tikka were relatively sheltered from the economic slowdown. Revenues from the restaurants segment recorded a 14% growth in 2009 vs. a 25% YoY growth in 2008. However, the industries segment reported lower relative YoY growth in revenues of 6% in 2009 vs. 35% YoY growth in 2008, leading us to believe that some consumers shifted to other fresh products.

In order to mitigate the negative impact of the crisis, the company started to rationalize its expenses in all levels, particularly raw materials and other décor packages through dealing in new markets. Furthermore, the company carefully selects the locations of its new restaurants to benefit from the decrease in prices in the real estate market, and additionally by negotiating to decrease rent.

A sizeable portion of investments in the stock exchanges: The company’s investment portfolio had reached nearly KWD177mn as of March 31st, 2010, and made up almost 27% of the company’s book value of total assets. The majority of these investments are listed on the Kuwait Stock Exchange (KSE). Previously, 43% of these investments were recorded using the designated as fair value through profit or loss method in which the historical income statements were exposed to the realised and unrealised gains resulting from fluctuations of the stock exchanges. Starting mid-2008, these investments were reclassified as available-for-sale investments. Given the drop in the stock market and based on management’s judgement, FY08 and FY09 income statements were charged with impairment losses of KWD36.9mn and KWD11.4mn, respectively. These impairment losses will not be reversed in the income statement. We believe the company’s decision to reclassify these investments as available-for-sale was intended to further prevent the volatility in earnings resulting from the unrealised losses from fluctuating fair values. In 1Q10, KFC revised upwards the fair value of its available for sale securities by KWD32.3mn which was included in the comprehensive income.

Strong supplier base and verticalintegration should partially offsetrising food prices somewhat

An attractive industry opens the door for competition

Consumers became price sensitive and prefer low-priced products and valuemeals

27% of the company’s assets are vulnerable to the stock exchanges’volatility

REGIONAL FOOD | KFC

June 21, 2010

7

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

II. Valuation

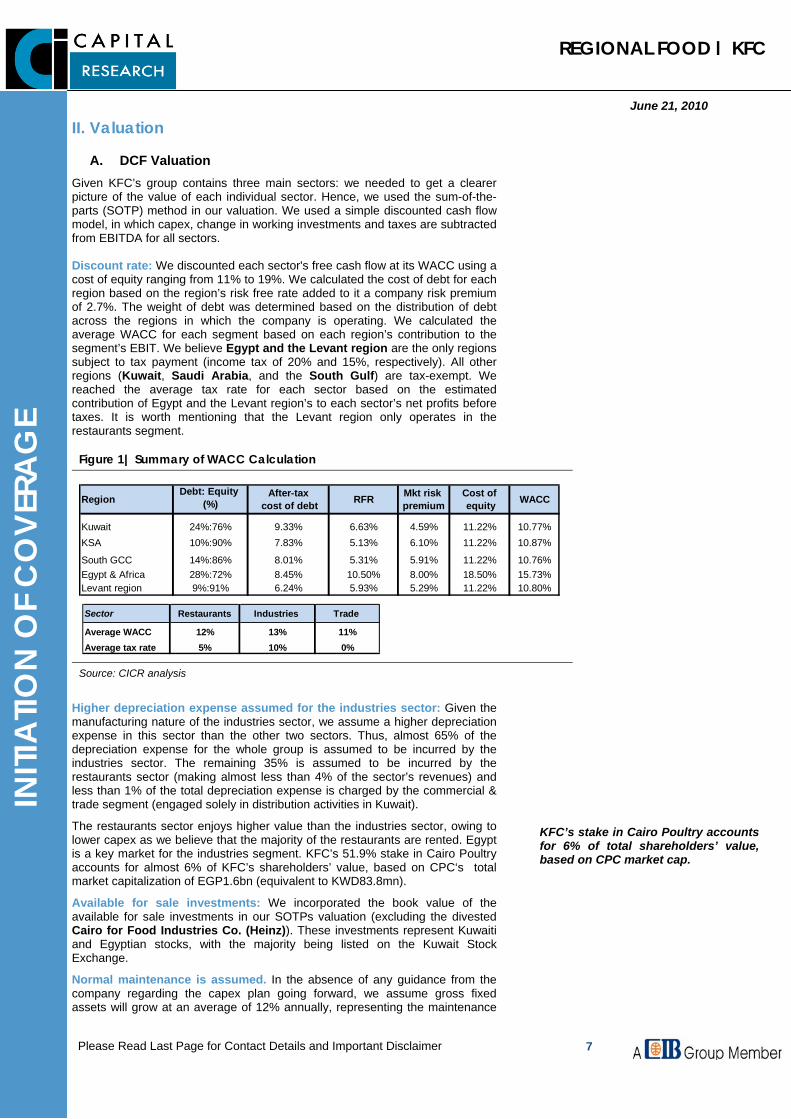

A. DCF Valuation Given KFC’s group contains three main sectors: we needed to get a clearer picture of the value of each individual sector. Hence, we used the sum-of-the-parts (SOTP) method in our valuation. We used a simple discounted cash flow model, in which capex, change in working investments and taxes are subtracted from EBITDA for all sectors. Discount rate: We discounted each sector's free cash flow at its WACC using a cost of equity ranging from 11% to 19%. We calculated the cost of debt for each region based on the region’s risk free rate added to it a company risk premium of 2.7%. The weight of debt was determined based on the distribution of debt across the regions in which the company is operating. We calculated the average WACC for each segment based on each region’s contribution to the segment’s EBIT. We believe Egypt and the Levant region are the only regions subject to tax payment (income tax of 20% and 15%, respectively). All other regions (Kuwait, Saudi Arabia, and the South Gulf) are tax-exempt. We reached the average tax rate for each sector based on the estimated contribution of Egypt and the Levant region’s to each sector’s net profits before taxes. It is worth mentioning that the Levant region only operates in the restaurants segment.

Figure 1| Summary of WACC Calculation

RegionDebt: Equity

(%)After-tax

cost of debt RFR Mkt risk premium

Cost of equity WACC

Kuwait 24%:76% 9.33% 6.63% 4.59% 11.22% 10.77%KSA 10%:90% 7.83% 5.13% 6.10% 11.22% 10.87%

South GCC 14%:86% 8.01% 5.31% 5.91% 11.22% 10.76%Egypt & Africa 28%:72% 8.45% 10.50% 8.00% 18.50% 15.73%Levant region 9%:91% 6.24% 5.93% 5.29% 11.22% 10.80%

Sector Restaurants Industries Trade

Average WACC 12% 13% 11%Average tax rate 5% 10% 0%

Source: CICR analysis

Higher depreciation expense assumed for the industries sector: Given the manufacturing nature of the industries sector, we assume a higher depreciation expense in this sector than the other two sectors. Thus, almost 65% of the depreciation expense for the whole group is assumed to be incurred by the industries sector. The remaining 35% is assumed to be incurred by the restaurants sector (making almost less than 4% of the sector’s revenues) and less than 1% of the total depreciation expense is charged by the commercial & trade segment (engaged solely in distribution activities in Kuwait). The restaurants sector enjoys higher value than the industries sector, owing to lower capex as we believe that the majority of the restaurants are rented. Egypt is a key market for the industries segment. KFC’s 51.9% stake in Cairo Poultry accounts for almost 6% of KFC’s shareholders’ value, based on CPC‘s total market capitalization of EGP1.6bn (equivalent to KWD83.8mn).

Available for sale investments: We incorporated the book value of the available for sale investments in our SOTPs valuation (excluding the divested Cairo for Food Industries Co. (Heinz)). These investments represent Kuwaiti and Egyptian stocks, with the majority being listed on the Kuwait Stock Exchange.

Normal maintenance is assumed. In the absence of any guidance from the company regarding the capex plan going forward, we assume gross fixed assets will grow at an average of 12% annually, representing the maintenance

KFC’s stake in Cairo Poultry accountsfor 6% of total shareholders’ value,based on CPC market cap.

REGIONAL FOOD | KFC

June 21, 2010

8

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

rate. We assume a greater portion of capex will be allocated to the industries sector and a minor portion allocated to the restaurants sector.

Net debt by sector: The absence of standalone financials for each sector led us to assume each sector's outstanding cash and short-term debt level as per its contribution to consolidated revenues. We assumed that the majority of the medium-term financing is withdrawn by the industries segment.

Figure 2 | Valuation of the Restaurants Sector

1. Restaurants (KWD000) Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Perpetual

Revenues 357,789 385,436 418,533 459,276 503,673 Revenues growth 10.9% 7.7% 8.6% 9.7% 9.7%EBITDA 45,106 51,368 55,312 60,435 65,817 EBITDA growth 11.2% 13.9% 7.7% 9.3% 8.9%EBITDA Margin 12.6% 13.3% 13.2% 13.2% 13.1%D&A as a %age of rev. 3.7% 3.8% 3.9% 4.0% 4.0%D&A 13,257 14,751 16,389 18,182 19,983 EBIT 31,849 36,616 38,924 42,253 45,834 Tax rate 5.2% 5.2% 5.2% 5.2% 5.2%Tax expense 1,640 1,886 2,005 2,176 2,360 EBITDA - Tax expense 43,466 49,482 53,308 58,259 63,457 CAPEX 15,570 17,202 18,345 20,549 22,016 CAPEX/Revenues 4% 4% 4% 4% 4%Change in Working Investments 13,680 2,861 3,080 3,570 3,779 FCFF 14,216 29,419 31,883 34,139 37,662 38,792

WACC 12.0%Perpetual Growth Rate 3.0%

PV of FCFF 14,998 27,704 26,791 25,607 25,215 287,586

Current Enterprise Value 407,902

Net debt 17,306 Equity value 390,595 Value/share (KWD) 1.00

Source: CICR analysis

Figure 3 | Valuation of the Industries Sector

2. Industries sector (KWD 000) Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Perpetual

Revenues 333,045 369,969 408,081 444,728 484,344 Revenues growth 14.0% 11.1% 10.3% 9.0% 8.9%EBITDA 55,259 62,028 67,480 72,858 78,902 EBITDA growth 26.3% 12.2% 8.8% 8.0% 8.3%EBITDA Margin 16.6% 16.8% 16.5% 16.4% 16.3%D&A as a %age of rev. 6.4% 6.4% 6.4% 6.4% 6.4%D&A 23,756 26,511 29,528 32,832 36,280 EBIT 31,503 35,517 37,952 40,026 42,622 Tax rate 9.8% 9.8% 9.8% 9.8% 9.8%Tax expense 3,087 3,480 3,718 3,922 4,176 EBITDA - Tax expense 52,173 58,548 63,762 68,936 74,726 CAPEX 28,806 32,500 35,003 38,936 41,456 CAPEX/Revenues 9% 9% 9% 9% 9%Change in Working Investments 12,734 2,746 3,003 3,457 3,634 FCFF 10,633 23,302 25,756 26,544 29,637 30,526

WACC 13.2%Perpetual Growth Rate 3.0%

PV of FCFF 11,275 21,820 21,292 19,378 19,108 192,301

Current Enterprise Value 285,173

Net debt 95,133 Equity value 190,040

Value/share 0.49 Source: CICR analysis

REGIONAL FOOD | KFC

June 21, 2010

9

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Figure 4 |Valuation of the Commercial & Retail Sector 3. Commercial & Retail sector (KWD000) Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Perpetual

Revenues 23,388 24,557 25,785 27,074 28,428 Revenues growth 5.0% 5.0% 5.0% 5.0% 5.0%EBITDA 1,248 1,304 1,357 1,413 1,470 EBITDA growth 5.1% 4.5% 4.1% 4.1% 4.1%EBITDA Margin 5.3% 5.3% 5.3% 5.2% 5.2%D&A as a %age of rev. 1.0% 1.0% 1.0% 1.0% 1.0%D&A 178 199 223 248 276 EBIT 1,070 1,105 1,135 1,164 1,194 Tax rate 0.0% 0.0% 0.0% 0.0% 0.0%Tax expense - - - - - EBITDA - Tax expense 1,248 1,304 1,357 1,413 1,470 CAPEX 25 26 27 28 29 CAPEX/Revenues 2% 2% 2% 2% 2%Change in Working Investments 894 182 190 210 213 FCFF 329 1,096 1,140 1,174 1,228 1,252

WACC 10.8%Perpetual Growth Rate 2.0%

PV of FCFF 345 1,038 975 906 855 9,947

Current Enterprise Value 14,067 Net debt 517

Equity value 13,550 Value/share 0.03

Source: CICR analysis

LTFV of 1.83/share: Consequently, we reached a fair value of KWD1.83/share, providing a 33% upside potential over the recent market price.

Figure 5 | Summary of the Sum-of-the-Parts Valuation

Segment WACC g EV Net Debt (Debt-Cash)

Equity [ EV-Net Debt]

%age of total value FV/share

KWD 000 except for per share values

1. Restaurants (000)Restaurants segment shareholders' value 12.0% 3% 407,902 17,306 390,595 51% 1.00

2. Industries Sector (000)Industries Sector shareholders' value 13.2% 3% 285,173 95,133 190,040 25% 0.49

3. Commercial and retails sector (000)Commercial and retail sector shareholders' value 10.8% 2% 14,067 517 13,550 2% 0.03

Total value of segments 594,185

Book value of available for sale investments 176,970 23% 0.45 Total EV (000) 771,155 100%Less value of minority interest* 55,669 SOTP valuation (000) 715,486 1.83 No. of outstanding shares (000) 391,154

* We incorporated the minority interest’s value for Cairo Poultry based on its market capitalization

Source: CICR analysis

REGIONAL FOOD | KFC

June 21, 2010

10

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

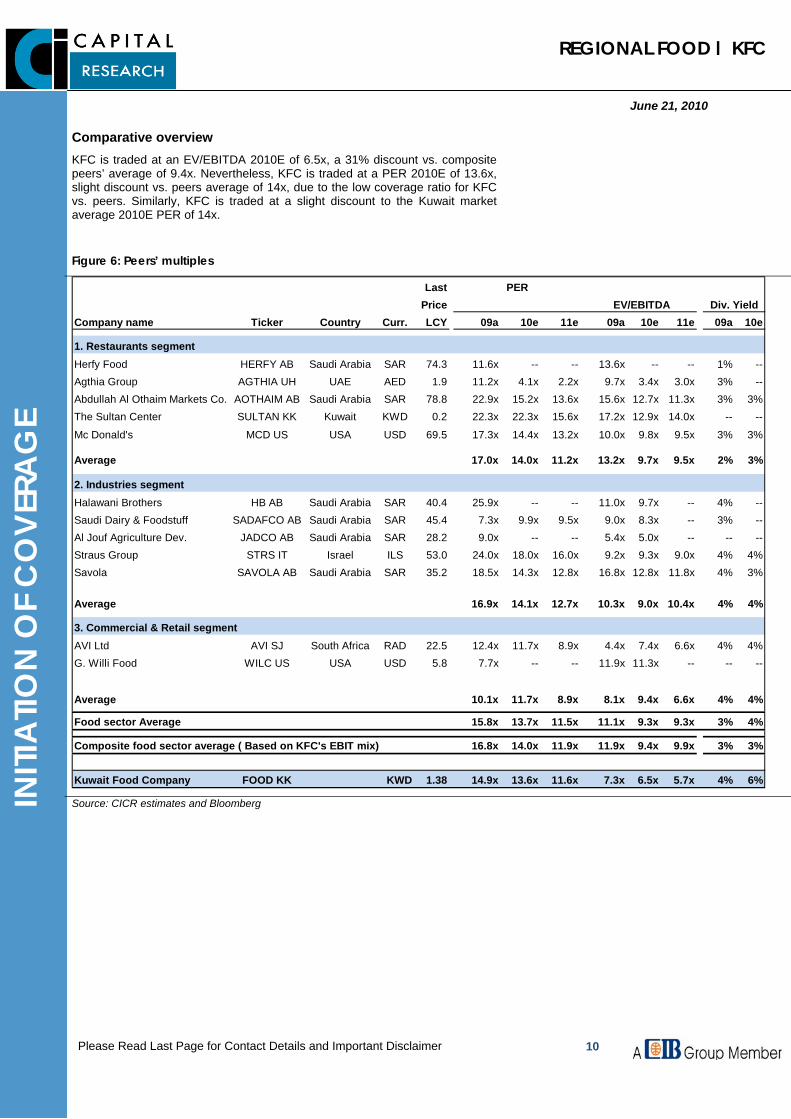

Comparative overview KFC is traded at an EV/EBITDA 2010E of 6.5x, a 31% discount vs. composite peers’ average of 9.4x. Nevertheless, KFC is traded at a PER 2010E of 13.6x, slight discount vs. peers average of 14x, due to the low coverage ratio for KFC vs. peers. Similarly, KFC is traded at a slight discount to the Kuwait market average 2010E PER of 14x.

Figure 6: Peers’ multiples

LastPrice

Company name Ticker Country Curr. LCY 09a 10e 11e 09a 10e 11e 09a 10e

1. Restaurants segmentHerfy Food HERFY AB Saudi Arabia SAR 74.3 11.6x -- -- 13.6x -- -- 1% --Agthia Group AGTHIA UH UAE AED 1.9 11.2x 4.1x 2.2x 9.7x 3.4x 3.0x 3% --Abdullah Al Othaim Markets Co. AOTHAIM AB Saudi Arabia SAR 78.8 22.9x 15.2x 13.6x 15.6x 12.7x 11.3x 3% 3%The Sultan Center SULTAN KK Kuwait KWD 0.2 22.3x 22.3x 15.6x 17.2x 12.9x 14.0x -- --

Mc Donald's MCD US USA USD 69.5 17.3x 14.4x 13.2x 10.0x 9.8x 9.5x 3% 3%

Average 17.0x 14.0x 11.2x 13.2x 9.7x 9.5x 2% 3%

2. Industries segment Halawani Brothers HB AB Saudi Arabia SAR 40.4 25.9x -- -- 11.0x 9.7x -- 4% --Saudi Dairy & Foodstuff SADAFCO AB Saudi Arabia SAR 45.4 7.3x 9.9x 9.5x 9.0x 8.3x -- 3% --Al Jouf Agriculture Dev. JADCO AB Saudi Arabia SAR 28.2 9.0x -- -- 5.4x 5.0x -- -- --Straus Group STRS IT Israel ILS 53.0 24.0x 18.0x 16.0x 9.2x 9.3x 9.0x 4% 4%Savola SAVOLA AB Saudi Arabia SAR 35.2 18.5x 14.3x 12.8x 16.8x 12.8x 11.8x 4% 3%

Average 16.9x 14.1x 12.7x 10.3x 9.0x 10.4x 4% 4%

3. Commercial & Retail segmentAVI Ltd AVI SJ South Africa RAD 22.5 12.4x 11.7x 8.9x 4.4x 7.4x 6.6x 4% 4%G. Willi Food WILC US USA USD 5.8 7.7x -- -- 11.9x 11.3x -- -- --

Average 10.1x 11.7x 8.9x 8.1x 9.4x 6.6x 4% 4%

Food sector Average 15.8x 13.7x 11.5x 11.1x 9.3x 9.3x 3% 4%

Composite food sector average ( Based on KFC's EBIT mix) 16.8x 14.0x 11.9x 11.9x 9.4x 9.9x 3% 3%

Kuwait Food Company FOOD KK KWD 1.38 14.9x 13.6x 11.6x 7.3x 6.5x 5.7x 4% 6%

Div. YieldEV/EBITDAPER

Source: CICR estimates and Bloomberg

REGIONAL FOOD | KFC

June 21, 2010

11

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

B. Target Price Determination We reached our target price of KWD1.64/share, which is the implied value based on a target EV/EBITDA of 7.5x (a slight premium to the historical average of 7.2x excluding outliers).

Given the 18% upside potential vs. our target price, we initiate coverage on the stock with a Hold recommendation.

Figure 7 |Target Price Calculation

Outstanding no. of shares 391,154 Market price (KWD/share) 1.38EBITDA 2010 (KWD 000) 101,613 Net Debt 2010 (KWD 000) 118,904

Target Price Calculation Implied valueTarget EV/EBITDA 7.5x 1.64

Target price

Source: CICR analysis

We believe that based on the target price of KWD1.64/share, KFC will be traded at 2011E P/E ratio of 13.8x and EV/EBITDA of 6.6x. We believe the target price is feasible based on KFC’s expected 5-year normalized earnings’ CAGR of 16%. Furthermore, based on 2011E EV/EBITDA, KFC will still be traded at a discount compared to composite peers’ average of 9.8x. Yet, our target price might not be reached in case the stock exchange remains unstable and lower-than-expected dividend is distributed by KFC in FY10.

Figure 8 |Implied P/E ratios and EV/EBITDA based on Target price

Current Price KWD1.38 2010E 2011E 2012EP/E 2010 13.6x 11.6x 10.7xEV/EBITDA 6.5x 5.7x 5.2x

Target Price KWD1.64 2010E 2011E 2012EP/E 2010 16.2x 13.8x 12.8xEV/EBITDA 7.5x 6.6x 6.0x Source: CICR analysis

REGIONAL FOOD | KFC

June 21, 2010

12

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Risks & Catalysts

Risks to our Recommendation

• Lower-than-expected payout ratio to finance expansions.

• Prolonged negative technical view on the stock market.

• Spread of disease may threaten demand for fast-food restaurants.

• Higher food prices and the inability to fully pass them to the end consumer.

• Scepticism about the merits of processed and fast-food in terms of health hygiene.

Catalysts for Future Growth

• Busy lifestyles, increased westernization and the growing number of working women.

• A growing population in the MENA region.

• The fact that a large tranche of the GCC market’s population is youthful is likely to boost fast-food demand.

• Food consumption is a key priority of consumers in the MENA region.

REGIONAL FOOD | KFC

June 21, 2010

13

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

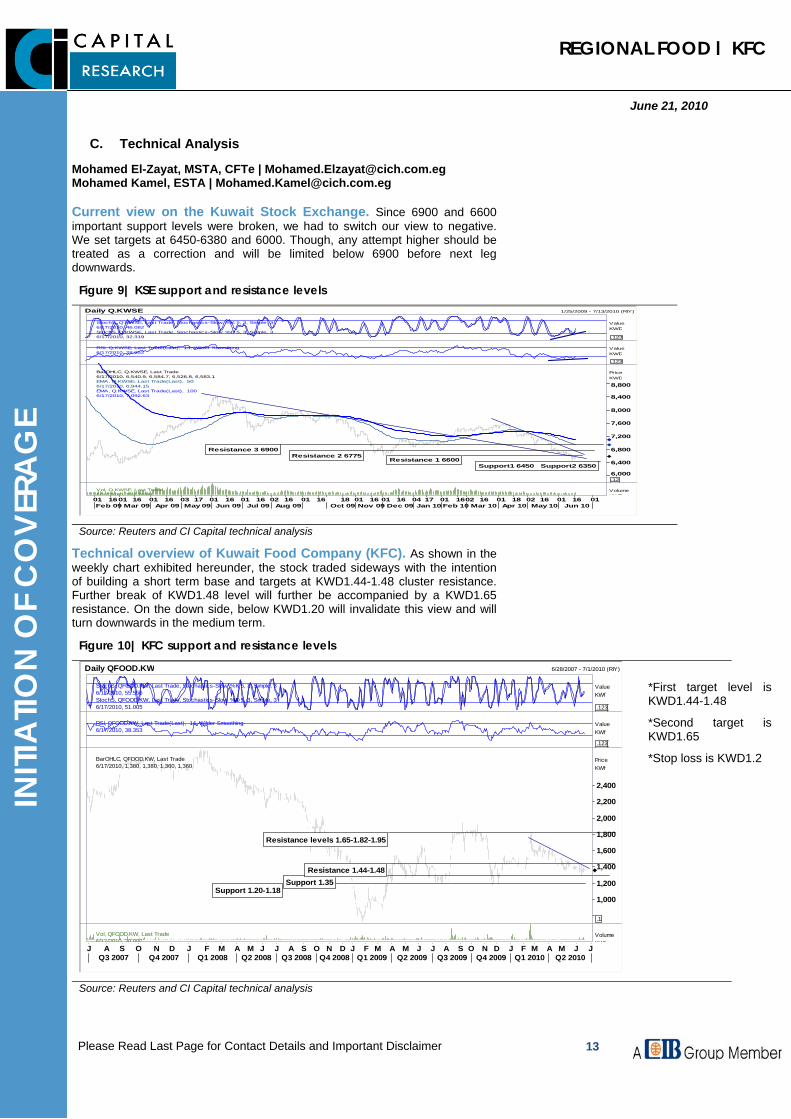

C. Technical Analysis

Mohamed El-Zayat, MSTA, CFTe | [email protected] Mohamed Kamel, ESTA | [email protected]

Current view on the Kuwait Stock Exchange. Since 6900 and 6600 important support levels were broken, we had to switch our view to negative. We set targets at 6450-6380 and 6000. Though, any attempt higher should be treated as a correction and will be limited below 6900 before next leg downwards.

Figure 9| KSE support and resistance levels Daily Q.KWSE 1/25/2009 - 7/13/2010 (RIY)

StochS, Q.KWSE, Last Trade, Stochastics-Slow %K 5, 3, Simple, 36/17/2010, 46.082StochS, Q.KWSE, Last Trade, Stochastics-Slow %D 5, 3, Simple, 36/17/2010, 32.319

ValueKWD

.123

RSI, Q.KWSE, Last Trade(Last), 14, Wilder Smoothing6/17/2010, 28.952

ValueKWD

.123

Resistance 1 6600Resistance 2 6775

Resistance 3 6900

Support1 6450 Support2 6350

BarOHLC, Q.KWSE, Last Trade6/17/2010, 6,540.9, 6,584.7, 6,526.8, 6,583.1EMA, Q.KWSE, Last Trade(Last), 506/17/2010, 6,944.15EMA, Q.KWSE, Last Trade(Last), 1006/17/2010, 7,092.63

PriceKWD

.126,000

6,400

6,800

7,200

7,600

8,000

8,400

8,800

Vol, Q.KWSE, Last Trade6/17/2010 234 255M

VolumeKWD

01 16 01 16 01 16 03 17 01 16 01 16 02 16 01 16 18 01 16 01 16 04 17 01 16 02 16 01 18 02 16 01 16 01Feb 09 Mar 09 Apr 09 May 09 Jun 09 Jul 09 Aug 09 Oct 09 Nov 09 Dec 09 Jan 10 Feb 10 Mar 10 Apr 10 May 10 Jun 10

Source: Reuters and CI Capital technical analysis

Technical overview of Kuwait Food Company (KFC). As shown in the weekly chart exhibited hereunder, the stock traded sideways with the intention of building a short term base and targets at KWD1.44-1.48 cluster resistance. Further break of KWD1.48 level will further be accompanied by a KWD1.65 resistance. On the down side, below KWD1.20 will invalidate this view and will turn downwards in the medium term.

Figure 10| KFC support and resistance levels

Daily QFOOD.KW 6/28/2007 - 7/1/2010 (RIY)

StochS, QFOOD.KW, Last Trade, Stochastics-Slow %K 5, 3, Simple, 36/17/2010, 55.556StochS, QFOOD.KW, Last Trade, Stochastics-Slow %D 5, 3, Simple, 36/17/2010, 51.005

ValueKWf

.123

RSI, QFOOD.KW, Last Trade(Last), 14, Wilder Smoothing6/17/2010, 38.353

ValueKWf

.123

Support 1.20-1.18Support 1.35

Resistance 1.44-1.48

Resistance levels 1.65-1.82-1.95

BarOHLC, QFOOD.KW, Last Trade6/17/2010, 1,380, 1,380, 1,360, 1,360

PriceKWf

.1

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

Vol, QFOOD.KW, Last Trade6/17/2010, 30,000

VolumeKWf

J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J JQ3 2007 Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010

Source: Reuters and CI Capital technical analysis

*First target level is KWD1.44-1.48

*Second target is KWD1.65

*Stop loss is KWD1.2

REGIONAL FOOD | KFC

June 21, 2010

14

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

III. Industry Overview

A. Global Food Business

Global food sales reached USD6.7tn in 2009. Global food sales (estimated to be in the vicinity of USD6.7tn in 2009) are comprised of the retail food (fresh and processed food) and food service establishment (restaurants and hotels) segments. Food retail sales reached an estimated value of USD5.2tn in 2009, exhibiting a four-year CAGR growth of 7% over the period 2005–09. The food service market—which includes restaurants, fast food establishments, and all other outdoor eating establishments—was valued at about USD1.5tn in 20091, accounting for almost 22% of global food sales. A shift in consumption patterns towards ready-to-eat food and out-of-home consumption is driving growth in the food market. The US led the global food market with expenditure on food, beverage and tobacco reaching USD890bn in 2009. Now, emerging economies in Asia and the MENA region are witnessing strong growth in the food retail and service businesses due to economic expansions, busy lifestyles and increasing urbanization. Figure 11| Structure of the Food Market

Food market

Retail

Fresh Processed

Packaged Food Beverages

Food service establishment

Hotels Restaurants

1 Source: Yum Brand Presentation

Source: Economic Research Service/ USDA

POTENTIALS

Food consumption accounts for a large portion of total spending in the MENA region.

Strong population base of over 300mn capita in the MENA region.

Wide tranche of youth population and foreign expats in GCC markets.

Increasing demand for dining and food. Changing lifestyles, increasing

westernization and growing numbers of working women.

RISKS

A large portion of Egypt’s population - a major food market in MENA - falls into the lower income bracket and consumes a higher portion of traditional food products.

Scepticism about the merits of processed and fast food in terms of health hygiene.

Fluctuating international food prices. Shortage of arable area and limited water

supply in the MENA. Vulnerability to food product spoilage in the

event of malfunctioning freezing systems or lower demand.

The spread of diseases such as the swine flu, Avian flu and the foot-and-mouth disease virus.

REGIONAL FOOD | KFC

June 21, 2010

15

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

B. Food Industry in the MENA Region

The food industry in the MENA region has a diverse structure due to varying rates of economic development across the region. Several countries in the Middle East and a few countries in North Africa (such as Egypt) have witnessed strong growth in the food market.

1. Main Characteristics

a) Size of the food market

The retail food market in the Middle East and North African region is estimated to be in the vicinity of USD87.6bn in 20092. This constitutes 53% of the growing USD165bn retail sales in the region. Egypt, the largest food market, accounted for 51% of the food sales in the MENA region with a total food retail value of USD44.8bn in 2009.

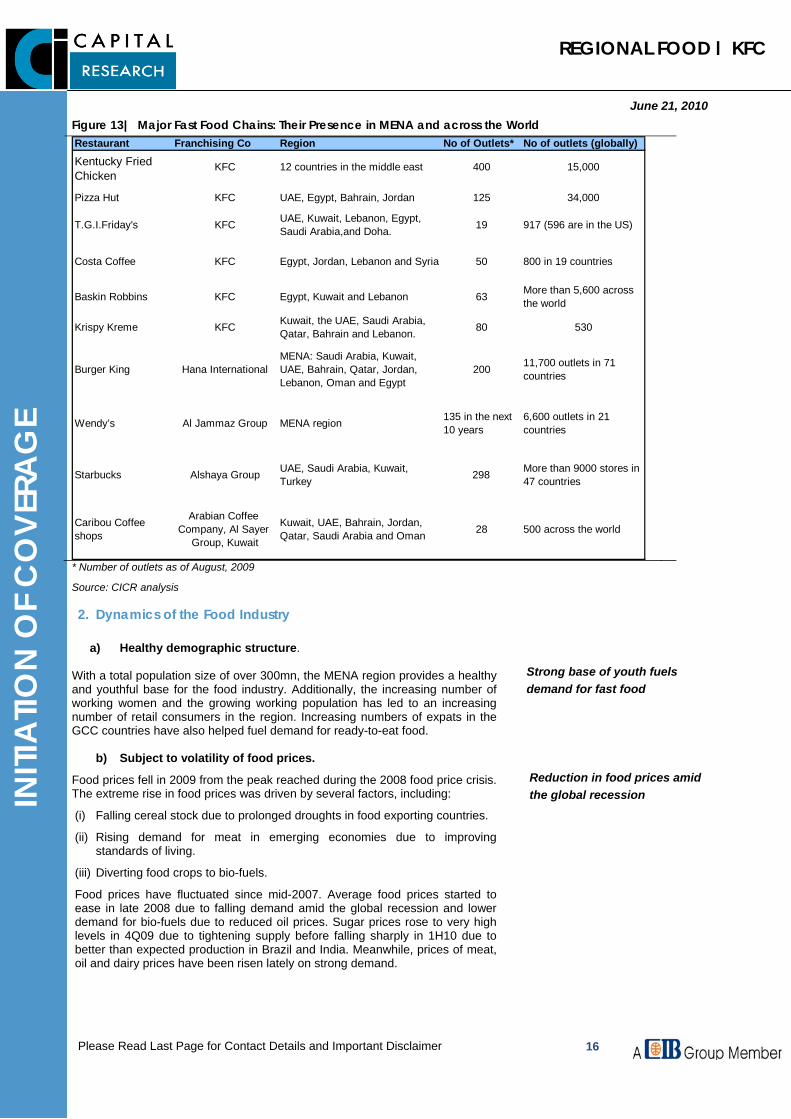

On the food service establishment front, fast-food franchise business have grown steadily in the MENA region, with several well-known brands (such as Kentucky Fried Chicken, Pizza Hut and McDonalds) penetrating the market during the last twenty years. The franchise industry in the MENA region was valued at over USD14bn in 2008.

Source: EIU

b) Market structure

The food manufacturing sector in the MENA region is still underpenetrated though and relies heavily on imports due to a shortage of arable land and water supply. A few large local players dominate the market such as Almarai, Savola, Halwani Brothers and Kuwait Food Company. These companies specialise in meat production, dairy products and frozen and canned vegetables.

Given the high priority of dining in the MENA region (in light of the new trend in the industry towards fast-food restaurants), the food service industry has exhibited strong growth. Although many restaurants and street-side stalls are available throughout the market, it is dominated by a limited number of fast food companies.

2 Source: EIU

Retail food sales in MENA accounted for 53% of total retail sales

Figure 12 | Retail Sales in MENA (2009)

Non food sales47%

Egypt 27%

Saudi 17%

others9%

Food sales53%

A limited number of players dominates the market

REGIONAL FOOD | KFC

June 21, 2010

16

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

* Number of outlets as of August, 2009

Source: CICR analysis

2. Dynamics of the Food Industry

a) Healthy demographic structure. With a total population size of over 300mn, the MENA region provides a healthy and youthful base for the food industry. Additionally, the increasing number of working women and the growing working population has led to an increasing number of retail consumers in the region. Increasing numbers of expats in the GCC countries have also helped fuel demand for ready-to-eat food.

b) Subject to volatility of food prices.

Food prices fell in 2009 from the peak reached during the 2008 food price crisis. The extreme rise in food prices was driven by several factors, including:

(i) Falling cereal stock due to prolonged droughts in food exporting countries.

(ii) Rising demand for meat in emerging economies due to improving standards of living.

(iii) Diverting food crops to bio-fuels.

Food prices have fluctuated since mid-2007. Average food prices started to ease in late 2008 due to falling demand amid the global recession and lower demand for bio-fuels due to reduced oil prices. Sugar prices rose to very high levels in 4Q09 due to tightening supply before falling sharply in 1H10 due to better than expected production in Brazil and India. Meanwhile, prices of meat, oil and dairy prices have been risen lately on strong demand.

Figure 13| Major Fast Food Chains: Their Presence in MENA and across the World Restaurant Franchising Co Region No of Outlets* No of outlets (globally)

Kentucky Fried Chicken

KFC 12 countries in the middle east 400 15,000

Pizza Hut KFC UAE, Egypt, Bahrain, Jordan 125 34,000

T.G.I.Friday's KFC UAE, Kuwait, Lebanon, Egypt, Saudi Arabia,and Doha. 19 917 (596 are in the US)

Costa Coffee KFC Egypt, Jordan, Lebanon and Syria 50 800 in 19 countries

Baskin Robbins KFC Egypt, Kuwait and Lebanon 63 More than 5,600 across the world

Krispy Kreme KFC Kuwait, the UAE, Saudi Arabia, Qatar, Bahrain and Lebanon. 80 530

Burger King Hana International MENA: Saudi Arabia, Kuwait, UAE, Bahrain, Qatar, Jordan, Lebanon, Oman and Egypt

200 11,700 outlets in 71 countries

Wendy’s Al Jammaz Group MENA region 135 in the next 10 years

6,600 outlets in 21 countries

Starbucks Alshaya Group UAE, Saudi Arabia, Kuwait, Turkey 298 More than 9000 stores in

47 countries

Caribou Coffee shops

Arabian Coffee Company, Al Sayer

Group, Kuwait

Kuwait, UAE, Bahrain, Jordan, Qatar, Saudi Arabia and Oman 28 500 across the world

Strong base of youth fuels demand for fast food

Reduction in food prices amid the global recession

REGIONAL FOOD | KFC

June 21, 2010

17

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Source: FAO

c) High per capita consumption.

Given that food is a major priority in the MENA region, per capita food consumption as a percentage of household consumption is high in the MENA region (particularly in UAE, Saudi Arabia (KSA) and Kuwait).

Figure 15 | 2009 GDP per Capita (PPP) (USD based on 2005 prices)

1,580 2,494

12,161

30,622 32,168

37,19841,646

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Egypt China KSA Kuwait UAE UK USA

USD

/ Cap

ita

Source: ERS International macroeconomic data

Figure 14 | International Food Price Indices: 2006-1H10

0

50

100

150

200

250

300

350

400

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10

Food Price Index Meat Price Index Dairy Price IndexOils Price Index Sugar Price Index

Meat

Food

Oil

Sugar

Dairy

Food is a major priority in MENA

REGIONAL FOOD | KFC

June 21, 2010

18

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

3. Key Regional Food Markets

KFC operates in various MENA food markets, with its major markets being Egypt, Kuwait, Saudi Arabia, and the southern Gulf countries such as the UAE, Qatar and Bahrain. The business dynamics of these markets are discussed below. a) Egypt: Backed by a populous market

Due to its robust economic development in recent years, Egypt represents one of the major retail food markets in the MENA region. With 76mn inhabitants in June 2009, Egypt has one of the largest populations in the MENA region, and almost 50% of the population lies within the ages of 15 and 45. The country’s GDP grew at a four-year average rate of 6.5%, reaching almost EGP796.8bn in June 2009.

Figure 16 | Egypt Consumer Expenditure: Food, Beverages & Tobacco (USDbn)

A= Actual E=Estimated

27.8 31.838.1

52.3

61.0

397 445

524

703 805

-

100

200

300

400

500

600

700

800

900

0

10

20

30

40

50

60

70

2005A 2006E 2007E 2008E 2009E

USD

/cap

ita

USD

bn

Consumption of food (LHS) Annual per capita food consumption (RHS)

A=Actual E=Estimate

Source: EIU

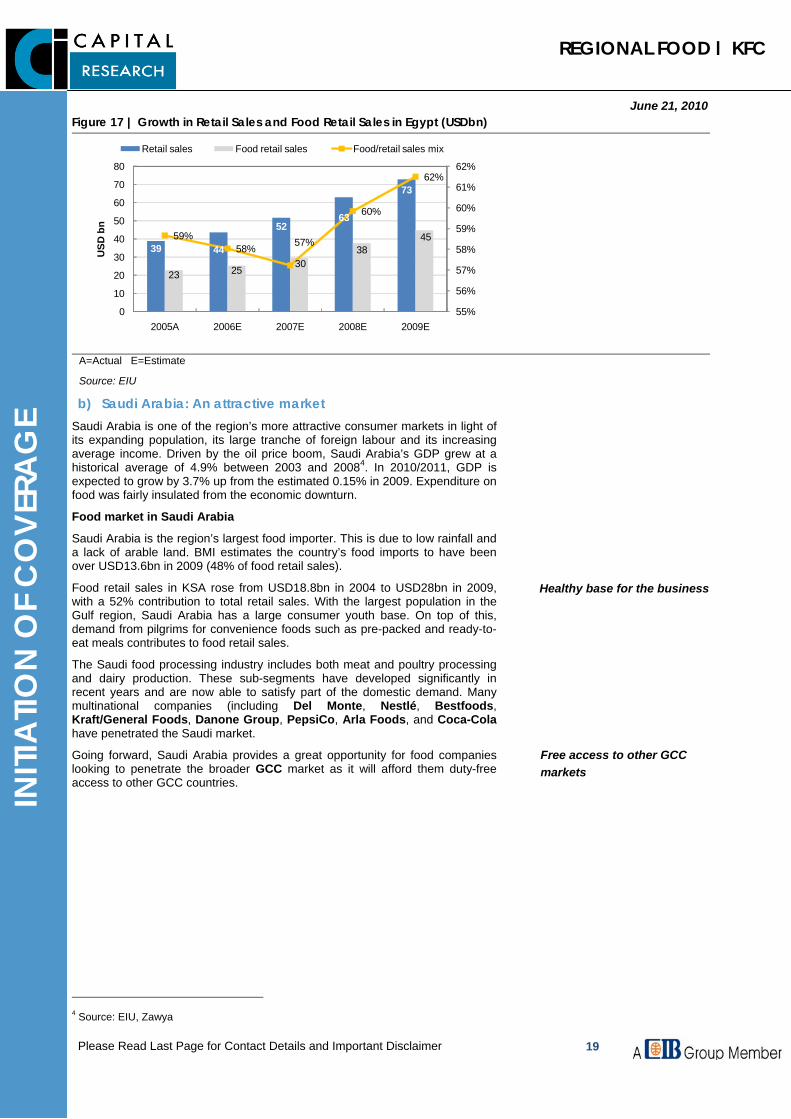

(1) Food market in Egypt

Food retail sales in Egypt reached a size of USD44.8bn3 in 2009, contributing 62% of Egypt’s retail sector sales. The fast-food business has emerged as one of the quickest growing segments in the country’s food service sector, with KFC recording turnover in Egypt of almost EGP1.25bn in 2009.

(a) Retail food market

The food manufacturing sector is underpenetrated given that the vast majority of the population lies within mid-to-low income segments preferring traditional, fresh products purchased from independent grocery outlets. Demand for processed food is primarily generated by middle to higher income consumers.

Due to rising demand for processed food, investment from regional companies such as Saudi Arabia's Halwani Brothers and a number of multinationals such as Nestlé and Kraft (attracted by the size of the Egyptian market) has penetrated the Egyptian market.

(b) Food service segment

Egypt has a wide range of chains operating in food service segments, including chains of Kuwait Food Company, Amer Group, McDonald’s, Mo’men and many others. In the fast food service segment, the Egyptian market is concentrated, with the top three chains controlling an estimated market share of 65%. McDonald’s has a market share of 24%, Kentucky Fried Chicken (KFC) a market share of 21% and Mo’men a share ranging from 18%-20%.

3 Source: EIU

Demand for processed food is generated by middle to high income consumers

Top three fast food restaurants have a market share of 65%

REGIONAL FOOD | KFC

June 21, 2010

19

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Figure 17 | Growth in Retail Sales and Food Retail Sales in Egypt (USDbn)

39 44

5263

73

23 2530

384559%

58% 57%

60%

62%

55%

56%

57%

58%

59%

60%

61%

62%

0

10

20

30

40

50

60

70

80

2005A 2006E 2007E 2008E 2009E

USD

bn

Retail sales Food retail sales Food/retail sales mix

A=Actual E=Estimate

Source: EIU

b) Saudi Arabia: An attractive market Saudi Arabia is one of the region’s more attractive consumer markets in light of its expanding population, its large tranche of foreign labour and its increasing average income. Driven by the oil price boom, Saudi Arabia’s GDP grew at a historical average of 4.9% between 2003 and 20084. In 2010/2011, GDP is expected to grow by 3.7% up from the estimated 0.15% in 2009. Expenditure on food was fairly insulated from the economic downturn.

Food market in Saudi Arabia

Saudi Arabia is the region’s largest food importer. This is due to low rainfall and a lack of arable land. BMI estimates the country’s food imports to have been over USD13.6bn in 2009 (48% of food retail sales).

Food retail sales in KSA rose from USD18.8bn in 2004 to USD28bn in 2009, with a 52% contribution to total retail sales. With the largest population in the Gulf region, Saudi Arabia has a large consumer youth base. On top of this, demand from pilgrims for convenience foods such as pre-packed and ready-to-eat meals contributes to food retail sales.

The Saudi food processing industry includes both meat and poultry processing and dairy production. These sub-segments have developed significantly in recent years and are now able to satisfy part of the domestic demand. Many multinational companies (including Del Monte, Nestlé, Bestfoods, Kraft/General Foods, Danone Group, PepsiCo, Arla Foods, and Coca-Cola have penetrated the Saudi market.

Going forward, Saudi Arabia provides a great opportunity for food companies looking to penetrate the broader GCC market as it will afford them duty-free access to other GCC countries.

4 Source: EIU, Zawya

Healthy base for the business

Free access to other GCC markets

REGIONAL FOOD | KFC

June 21, 2010

20

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

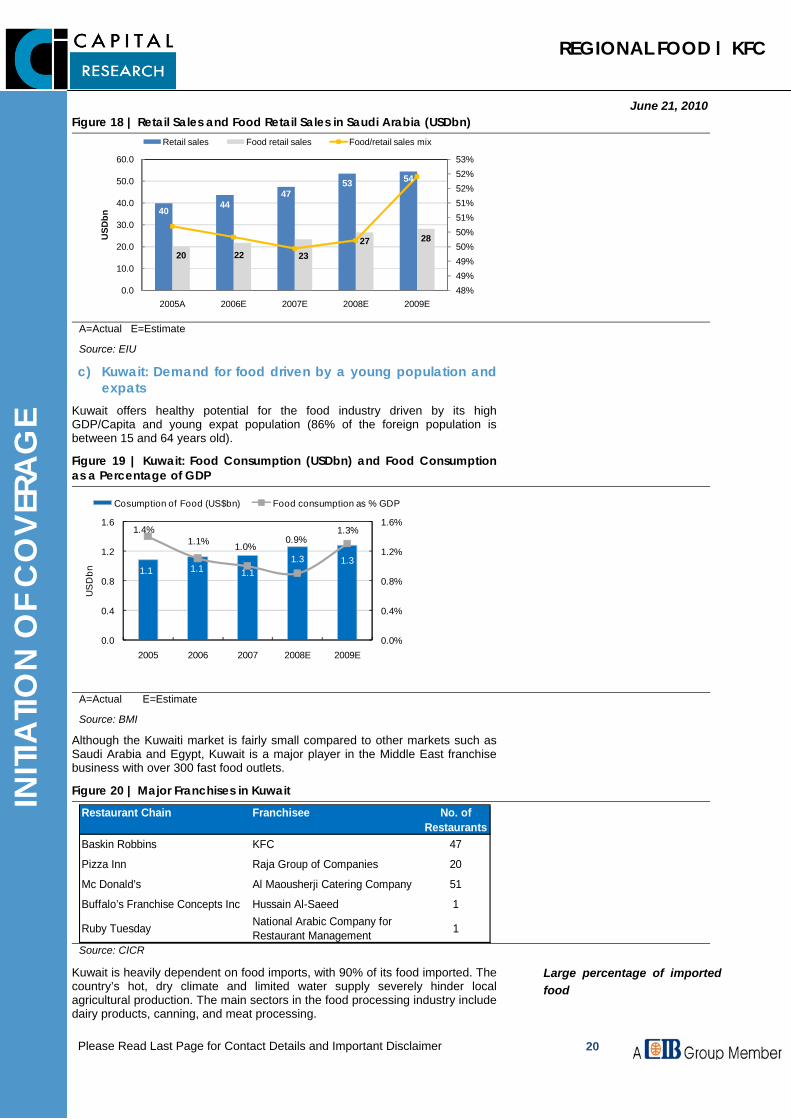

Figure 18 | Retail Sales and Food Retail Sales in Saudi Arabia (USDbn)

A= Actual E=Expected F=ForecastSource: EIU

4044

4753 54

20 22 2327 28

48%49%49%50%50%51%51%52%52%53%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2005A 2006E 2007E 2008E 2009E

USD

bn

Retail sales Food retail sales Food/retail sales mix

A=Actual E=Estimate

Source: EIU

c) Kuwait: Demand for food driven by a young population and expats

Kuwait offers healthy potential for the food industry driven by its high GDP/Capita and young expat population (86% of the foreign population is between 15 and 64 years old).

Figure 19 | Kuwait: Food Consumption (USDbn) and Food Consumption as a Percentage of GDP

1.1 1.1 1.11.3 1.3

1.4%1.1% 1.0%

0.9%1.3%

0.0%

0.4%

0.8%

1.2%

1.6%

0.0

0.4

0.8

1.2

1.6

2005 2006 2007 2008E 2009E

US

Dbn

Cosumption of Food (US$bn) Food consumption as % GDP

A=Actual E=Estimate

Source: BMI

Although the Kuwaiti market is fairly small compared to other markets such as Saudi Arabia and Egypt, Kuwait is a major player in the Middle East franchise business with over 300 fast food outlets.

Figure 20 | Major Franchises in Kuwait Restaurant Chain Franchisee No. of

RestaurantsBaskin Robbins KFC 47

Pizza Inn Raja Group of Companies 20

Mc Donald’s Al Maousherji Catering Company 51

Buffalo’s Franchise Concepts Inc Hussain Al-Saeed 1

Ruby Tuesday National Arabic Company for Restaurant Management 1

Source: CICR

Kuwait is heavily dependent on food imports, with 90% of its food imported. The country’s hot, dry climate and limited water supply severely hinder local agricultural production. The main sectors in the food processing industry include dairy products, canning, and meat processing.

Large percentage of imported food

REGIONAL FOOD | KFC

June 21, 2010

21

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

d) Other GCC markets Bahrain and the UAE are the major markets in the southern Gulf region for KFC.

(1) Bahrain

The food retail market in Bahrain is relatively underdeveloped, mainly due to its small population (approximately 1mn) and lower percentage of food expenditure. Bahrain’s GDP growth is estimated to reach 4.1%5 in 2010/2011 (up from 3.1% in 2009). According to BMI, food consumption in Bahrain is estimated to rise to USD0.39bn in 2013 up from USD0.35bn in 2008.

The Government’s initiative to transform Bahrain into the region’s financial hub is expected to benefit the country’s retail food industry.

(2) UAE

UAE’s fast food market has been growing largely due to increasing consumer preference for ready-to-eat fast food. The UAE is heavily reliant on food and drink imports to meet domestic demand. Amid the current economic downturn, consumers are shifting more towards cooking at home low-cost fast food. Yet, KFC’s restaurant’s turnover in the UAE exceeded AED1bn in 2009.

4. Future Outlook

Stable demand for the food industry in MENA: While the food industry in developed economies is bearing the brunt of the economic downturn, the relatively strong economic position of most Middle East countries is enabling MENA’s food sector to make it through relatively unscathed. Furthermore, fast-food is doing well, owing to its low priced products. This is exemplified by the strong performance of fast-food restaurants in the MENA region (an 11% YoY increase in net sales of both Herfy in Saudi Arabia and Kuwait Food Company in 2009). Going forward, MENA countries’ 2010 real GDP growth is expected to remain higher (4.5%) than that of developed economies (3.1% in the US and 1.3% in the UK). Given that food spending accounts for the largest expenditure in MENA, the region offers a stable market for companies operating in this sector.

Rising food prices: In light of the expected rebound in the global economy, food prices are expected to increase. Although currently prices of some of the major food staples have eased (such as wheat and sugar) from their high levels, other food products such as meat, dairy products and oil have escalated, spurred on by growing demand.

5 Source: EIU

Strong economic position in MENA sheltered the food sector

Food prices will rise on the back of the rebound in the economy

REGIONAL FOOD | KFC

June 21, 2010

22

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Figure 21 | SWOT Analysis for the Food Industry in the MENA Region

High per capita food consumption in MENA

A large portion of Egypt’s population - amajor food market in MENA - falls intolower income bracket and consumes ahigher portion of traditional food products

Strong population base of over 300mn in MENA

Scepticism about the merit of processed and fast food in terms of health hygiene

Wide tranche of youth population andforeign expats in GCC markets

Vulnerability to spoilage of food products in case of mal frozen system or in case oflower demand

Restaurants are a main source ofentertainment for families in the GCCcountries

Shortage of arable area and limited watersupply in the MENA

Frenetic lifestyles, increasinglywesternised habits

Spreading of diseases such as the swine flue, Avian flue and foot-and-mouth disease virus

Growing number of working women Limited ability of passing on the increasing food prices to the end user

Free access between arab countries

The gap between demand and importsis of potential for local manufacturers

Opportunities Threats

Strengths Weakness

Source: CI Capital

REGIONAL FOOD | KFC

June 21, 2010

23

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

IV. Company Profile

A. Company Synopsis

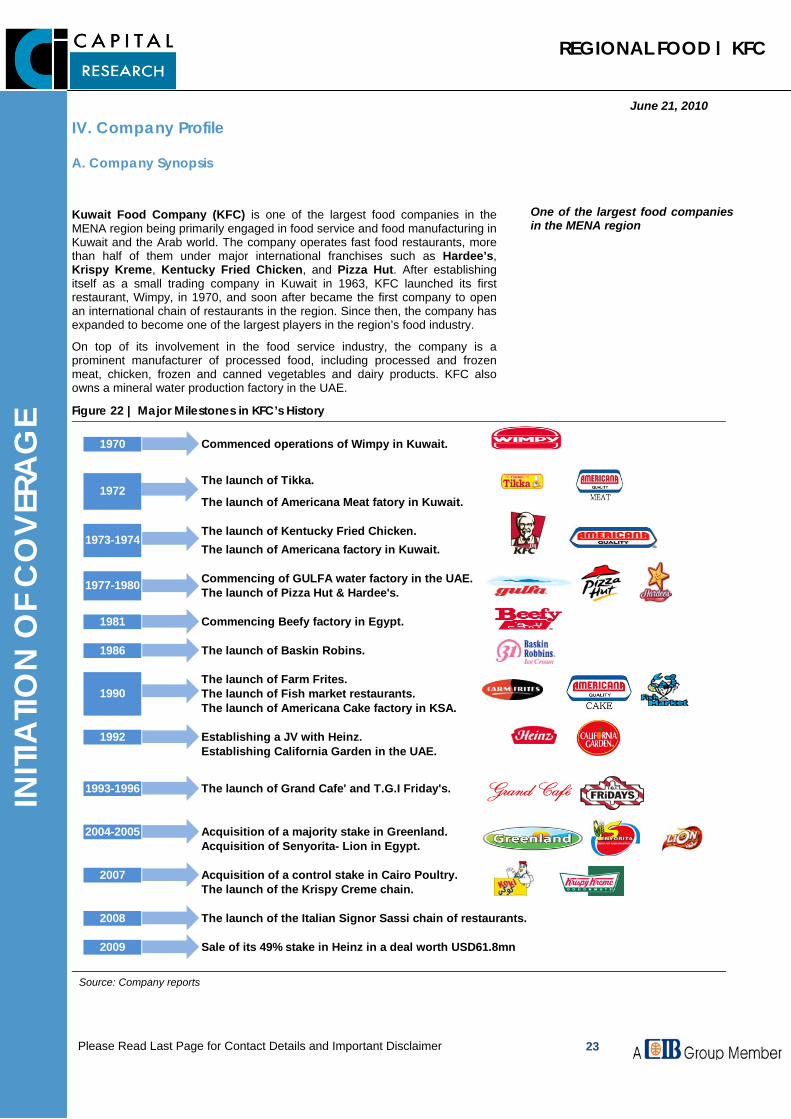

Kuwait Food Company (KFC) is one of the largest food companies in the MENA region being primarily engaged in food service and food manufacturing in Kuwait and the Arab world. The company operates fast food restaurants, more than half of them under major international franchises such as Hardee’s, Krispy Kreme, Kentucky Fried Chicken, and Pizza Hut. After establishing itself as a small trading company in Kuwait in 1963, KFC launched its first restaurant, Wimpy, in 1970, and soon after became the first company to open an international chain of restaurants in the region. Since then, the company has expanded to become one of the largest players in the region’s food industry.

On top of its involvement in the food service industry, the company is a prominent manufacturer of processed food, including processed and frozen meat, chicken, frozen and canned vegetables and dairy products. KFC also owns a mineral water production factory in the UAE.

Figure 22 | Major Milestones in KFC’s History

1970

1981

1986

The launch of Fish market restaurants.The launch of Americana Cake factory in KSA.

1992Establishing California Garden in the UAE.

1993-1996

2004-2005

2007

2008 The launch of the Italian Signor Sassi chain of restaurants.

2009 Sale of its 49% stake in Heinz in a deal worth USD61.8mn

The launch of Grand Cafe' and T.G.I Friday's.

Commencing of GULFA water factory in the UAE.

Acquisition of a majority stake in Greenland.Acquisition of Senyorita- Lion in Egypt.

The launch of the Krispy Creme chain.Acquisition of a control stake in Cairo Poultry.

The launch of Pizza Hut & Hardee's.

Commencing Beefy factory in Egypt.

The launch of Baskin Robins.

The launch of Farm Frites.1990

Establishing a JV with Heinz.

1972

1973-1974

1977-1980

Commenced operations of Wimpy in Kuwait.

The launch of Tikka.

The launch of Americana Meat fatory in Kuwait.

The launch of Kentucky Fried Chicken.The launch of Americana factory in Kuwait.

Source: Company reports

One of the largest food companies in the MENA region

REGIONAL FOOD | KFC

June 21, 2010

24

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

B. Business segments

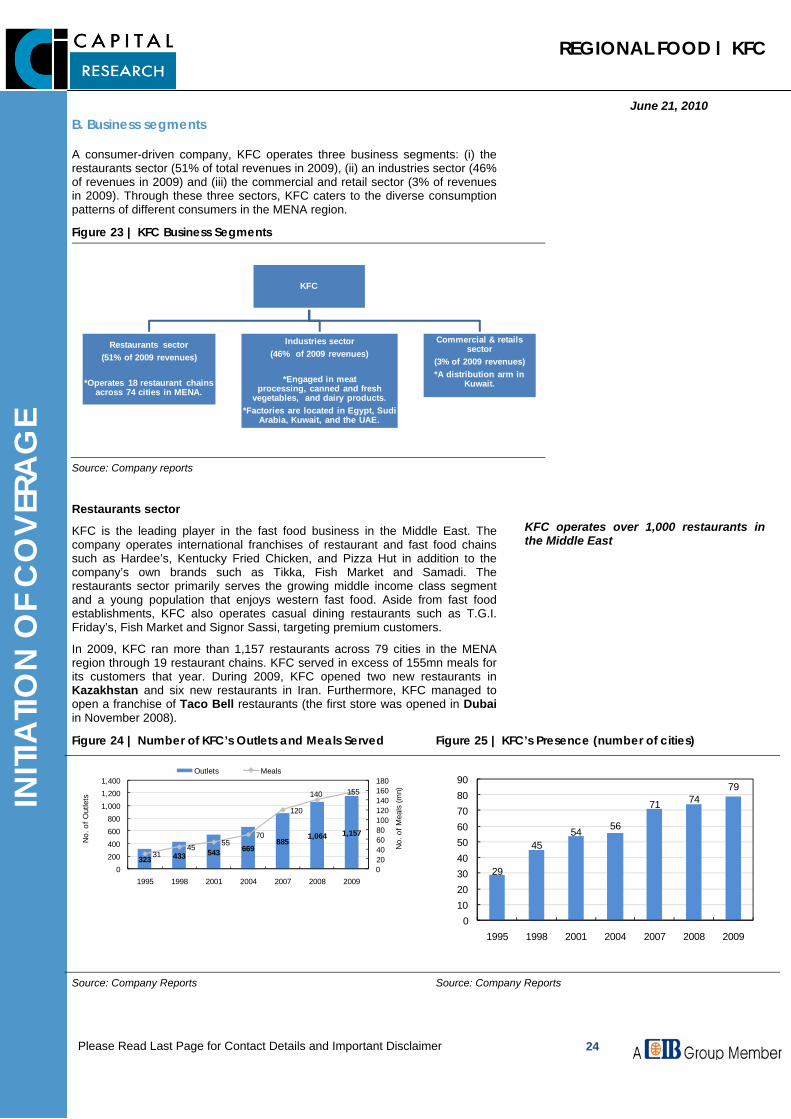

A consumer-driven company, KFC operates three business segments: (i) the restaurants sector (51% of total revenues in 2009), (ii) an industries sector (46% of revenues in 2009) and (iii) the commercial and retail sector (3% of revenues in 2009). Through these three sectors, KFC caters to the diverse consumption patterns of different consumers in the MENA region.

Figure 23 | KFC Business Segments

KFC

Restaurants sector(51% of 2009 revenues)

*Operates 18 restaurant chains across 74 cities in MENA.

Industries sector(46% of 2009 revenues)

*Engaged in meat processing, canned and fresh

vegetables, and dairy products. *Factories are located in Egypt, Sudi

Arabia, Kuwait, and the UAE.

Commercial & retails sector

(3% of 2009 revenues)*A distribution arm in

Kuwait.

Source: Company reports

Restaurants sector

KFC is the leading player in the fast food business in the Middle East. The company operates international franchises of restaurant and fast food chains such as Hardee’s, Kentucky Fried Chicken, and Pizza Hut in addition to the company’s own brands such as Tikka, Fish Market and Samadi. The restaurants sector primarily serves the growing middle income class segment and a young population that enjoys western fast food. Aside from fast food establishments, KFC also operates casual dining restaurants such as T.G.I. Friday’s, Fish Market and Signor Sassi, targeting premium customers.

In 2009, KFC ran more than 1,157 restaurants across 79 cities in the MENA region through 19 restaurant chains. KFC served in excess of 155mn meals for its customers that year. During 2009, KFC opened two new restaurants in Kazakhstan and six new restaurants in Iran. Furthermore, KFC managed to open a franchise of Taco Bell restaurants (the first store was opened in Dubai in November 2008).

Figure 24 | Number of KFC’s Outlets and Meals Served Figure 25 | KFC’s Presence (number of cities)

323 433 543 669885

1,064 1,157

3145 55

70

120

140 155

020406080100120140160180

0200400600800

1,0001,2001,400

1995 1998 2001 2004 2007 2008 2009

No.

of M

eals

(mn)

No.

of O

utle

ts

Outlets Meals

29

4554 56

71 7479

0102030405060708090

1995 1998 2001 2004 2007 2008 2009

Source: Company Reports Source: Company Reports

KFC operates over 1,000 restaurants in the Middle East

REGIONAL FOOD | KFC

June 21, 2010

25

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Figure 26 |KFC’s Restaurants and Stores across MENA Figure 27 | Geographic Revenues Breakdown of the Restaurants Sector (2009)

Restaurants & Stores Year of Launch Description Outlets

Chicken Tikka 1972KFC’s first owned restaurant. This chain is spread across Egypt, Kuwait, Oman, Saudi Arabia, and the UAE .

20

Kentucky Fried Chicken 1973

Kentucky Fried Chicken is KFC's fastest growing chain in Bahrain, Egypt, Jordan, Kuwait, Lebanon, Morocco, Oman, Qatar, Saudi Arabia, Syria, and the UAE.

400

Samadi 1975 KFC introduced Samadi sweets in Egypt and Kuwait. 50

Pizza Hut 1979Pizza Hut was first launched in the UAE followed by Egypt; it subsequently reached Bahrain and Jordan.

125

Hardee’s 1980Hardee’s, the US sandwich chain, is located in Bahrain, Egypt, Kuwait, Jordan, Lebanon, Oman, Qatar, Saudi Arabia, and the UAE.

170

Baskin Robbins 1986 This ice cream chain is present in Egypt, Kuwait, and Lebanon. 63

Fish Market 1990 Fish Market restaurants offer seafood cuisine in Egypt and recently in Kuwait. 7

Grand Café 1993 The first Grand Café was opened in Alexandria, Egypt. 8

TGIF’s 1996

With TGIF’s, KFC became the first company to open an international casual dining restaurant chain in the Middle East; and is spread across Egypt, Kuwait, Lebanon, Qatar, Saudi Arabia, and the UAE.

15

Costa Coffee 2004

KFC engaged in the branded coffee shop service by launching Costa Coffee in Egypt followed by Jordan, Lebanon, Syria, and Turkey.

NA

Krispy Kreme 2006Krispy Kreme is a leading branded retailer of doughnuts in Kuwait, the UAE, Saudi Arabia, Qatar, Bahrain, and Lebanon.

80

South Gulf37%

Egypt and Africa20%

Saudi Arabia18%

Kuwait17%

Sham and others

8%

* Number of outlets as of August, 2009

Source: Company’s website

Source: Company reports

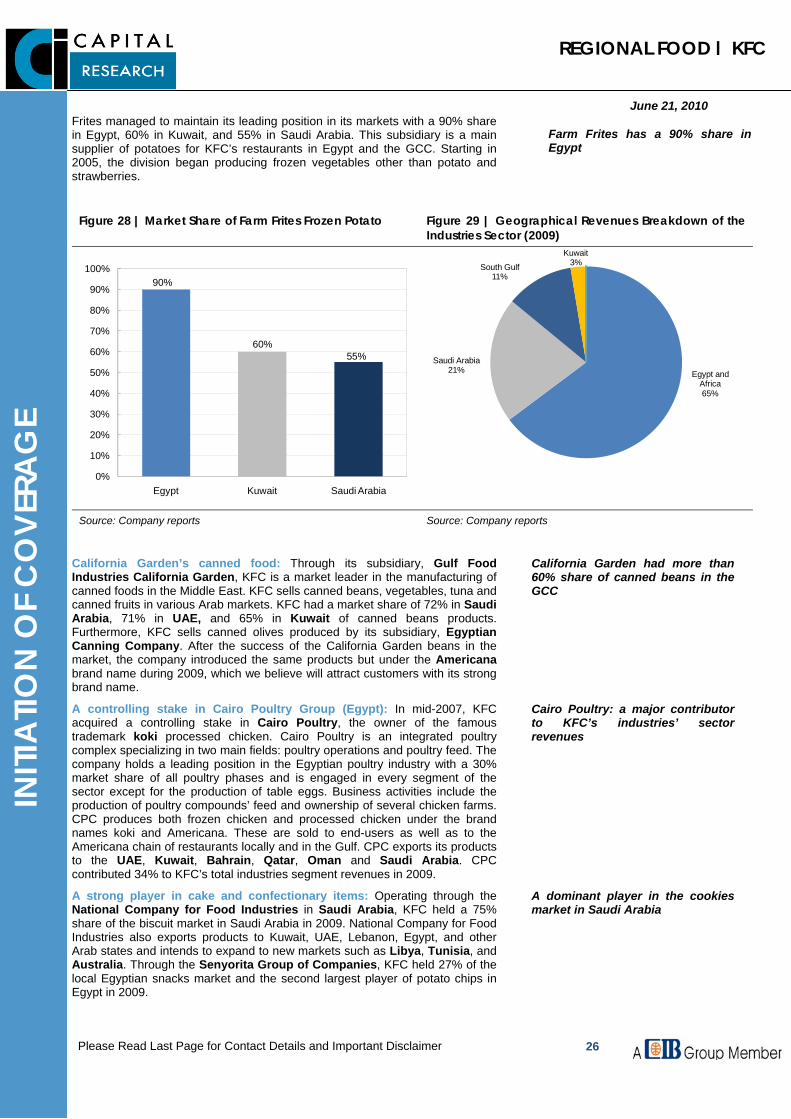

Industries Sector

Through its Industries sector, KFC maintains a strong market share in the fields of meat processing, dairy production, and canned and frozen vegetables. The company’s processed food retail business targets the middle and high-end income classes that prefer buying ready-to-eat foods for daily consumption.

Meat processing: Through the National Company for Food Industries, KFC has an important position in the meat processing market in the Middle East. Despite the challenges faced in terms of high costs, scarcity and increasing competition, through developing its relationship with suppliers, KFC has managed to combat these challenges and provide products at reasonable prices without reducing their quality. In 2009, the company held a 38% share of the frozen meat market in KSA and 29% in Qatar. Also, KFC had a 36% and 61% share of frozen meat and cooked meat in Kuwait. In 2007, KFC had a 12% share in Bahrain, and 11% in UAE.

Strong share in the Egyptian dairy sector: In Egypt, Greenland Company (a 75% subsidiary of KFC) maintained an estimated market share of 40% in the Egyptian dairy sector in 2009. Greenland exports its products to more than 10 Arab countries and 4 European Countries.

Frozen vegetables: KFC engages in agricultural production and processing through its Egyptian subsidiary, International Company for Agricultural Development (Farm Frites), which is the leading company in the Arab world for producing frozen potato. The company adopts a backward integration strategy in the cultivation of potato necessary for the production process. Farm

A considerable market share in the GCC meat markets

Greenland had a 40% share of the Egyptian dairy market in 2009

REGIONAL FOOD | KFC

June 21, 2010

26

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Frites managed to maintain its leading position in its markets with a 90% share in Egypt, 60% in Kuwait, and 55% in Saudi Arabia. This subsidiary is a main supplier of potatoes for KFC’s restaurants in Egypt and the GCC. Starting in 2005, the division began producing frozen vegetables other than potato and strawberries.

Figure 28 | Market Share of Farm Frites Frozen Potato Figure 29 | Geographical Revenues Breakdown of the Industries Sector (2009)

90%

60%55%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Egypt Kuwait Saudi Arabia

Egypt and Africa65%

Saudi Arabia21%

South Gulf11%

Kuwait3%

Source: Company reports Source: Company reports

California Garden’s canned food: Through its subsidiary, Gulf Food Industries California Garden, KFC is a market leader in the manufacturing of canned foods in the Middle East. KFC sells canned beans, vegetables, tuna and canned fruits in various Arab markets. KFC had a market share of 72% in Saudi Arabia, 71% in UAE, and 65% in Kuwait of canned beans products. Furthermore, KFC sells canned olives produced by its subsidiary, Egyptian Canning Company. After the success of the California Garden beans in the market, the company introduced the same products but under the Americana brand name during 2009, which we believe will attract customers with its strong brand name.

A controlling stake in Cairo Poultry Group (Egypt): In mid-2007, KFC acquired a controlling stake in Cairo Poultry, the owner of the famous trademark koki processed chicken. Cairo Poultry is an integrated poultry complex specializing in two main fields: poultry operations and poultry feed. The company holds a leading position in the Egyptian poultry industry with a 30% market share of all poultry phases and is engaged in every segment of the sector except for the production of table eggs. Business activities include the production of poultry compounds’ feed and ownership of several chicken farms. CPC produces both frozen chicken and processed chicken under the brand names koki and Americana. These are sold to end-users as well as to the Americana chain of restaurants locally and in the Gulf. CPC exports its products to the UAE, Kuwait, Bahrain, Qatar, Oman and Saudi Arabia. CPC contributed 34% to KFC’s total industries segment revenues in 2009.

A strong player in cake and confectionary items: Operating through the National Company for Food Industries in Saudi Arabia, KFC held a 75% share of the biscuit market in Saudi Arabia in 2009. National Company for Food Industries also exports products to Kuwait, UAE, Lebanon, Egypt, and other Arab states and intends to expand to new markets such as Libya, Tunisia, and Australia. Through the Senyorita Group of Companies, KFC held 27% of the local Egyptian snacks market and the second largest player of potato chips in Egypt in 2009.

Farm Frites has a 90% share in Egypt

California Garden had more than 60% share of canned beans in the GCC

Cairo Poultry: a major contributor to KFC’s industries’ sector revenues

A dominant player in the cookies market in Saudi Arabia

REGIONAL FOOD | KFC

June 21, 2010

27

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

Water bottling in the UAE: KFC also has presence in UAE’s water bottling sector through its subsidiary Gulfa Mineral Water and Processing Industries.

Commercial and Retail Sectors

Heinz for Processed Tomato and Cadbury chocolates: This segment handles distribution agencies in Kuwait. These agencies distribute Heinz ketchup, Cadbury chocolates, California Garden for canned foods, and Americana-branded products such as tuna, canned foods, and cheese. In 2009, the sector covered 35% of the croissant market in Kuwait.

C. Recent Developments

In December 2009, it was announced that Kuwait Food Company and its two subsidiaries had sold their 49% combined stake in Cairo for Food Industrial Company (Heinz) in a deal worth USD61.8mn. KFC recorded a capital gain of KWD16.8mn (equivalent to USD56mn) from the transaction.

KFC distributed a DPS of 60% of par value (equivalent to KWD0.06/share) on March 21st, 2010.

Distributes Heinz, Cadbury, and California Garden canned food in Kuwait

Divesting its stake in Heinz in a deal worth USD61.8mn

REGIONAL FOOD | KFC

June 21, 2010

28

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

V. Operational and Financial Analysis

A. Operational Analysis

i. A partial backward integration business model

KFC adopts partially a backward integration strategy in its production process in order to control raw material costs and provide a cushion against supply shocks by reducing the company’s dependence on external suppliers.

Figure 30 | KFC’s Business Model

Source: CICR analysis

Cultivation and land reclamation initiatives: The company strives to ensure the supply of basic raw materials and agricultural crops for its production process by reclaiming and cultivating around 2000 acres of land (half of it being olive trees) through its two subsidiaries, Americana Company for Reclaiming and Cultivating Land and Americana Company for Agricultural Development.

Furthermore, KFC’s subsidiary Farm Frites Company also enjoys the advantage of backward integration through the International Company for Agricultural Processing and Production, which cultivates potatoes and strawberries necessary for the production process. KFC plans to cultivate around 30k acres during the next few years. Cairo poultry enhances the backward integration strategy: CPC products are sold to end-users as well as to Americana chain of restaurants locally and in the Gulf.

ii. Penetrating new markets

In addition to maintaining its presence in 14 countries in MENA, KFC plans to penetrate new markets, such as Korea, Thailand, and parts of northern and southern Africa. The company also seeks to expand in a greater number of cities in the countries in which it operates. In 2009, KFC opened two new restaurants in Kazakhstan and six new restaurants in Iran. Moreover, KFC seeks to open 150 new restaurants in 2010.

Penetrating the Far East

Backward Integration (cultivating crops and

poultry business) Industries sector

Restaurants sector

REGIONAL FOOD | KFC

June 21, 2010

29

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

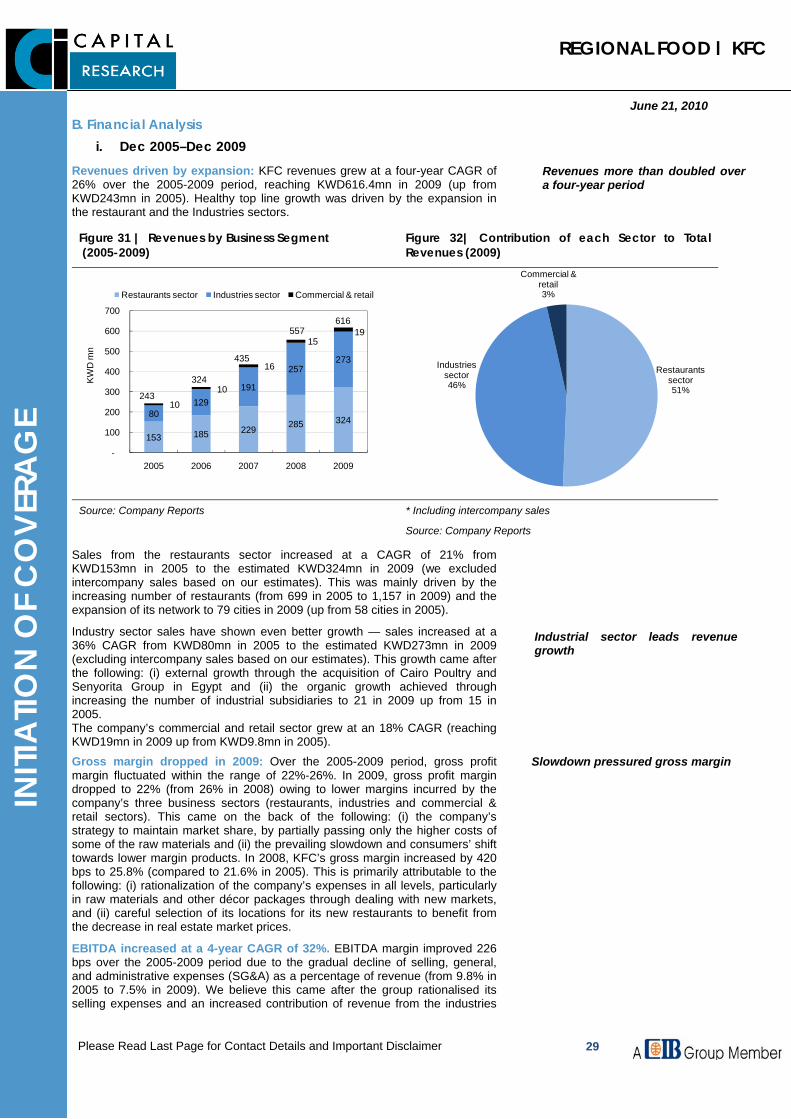

B. Financial Analysis i. Dec 2005–Dec 2009

Revenues driven by expansion: KFC revenues grew at a four-year CAGR of 26% over the 2005-2009 period, reaching KWD616.4mn in 2009 (up from KWD243mn in 2005). Healthy top line growth was driven by the expansion in the restaurant and the Industries sectors.

Figure 31 | Revenues by Business Segment (2005-2009)

Figure 32| Contribution of each Sector to Total Revenues (2009)

153 185 229 285 32480

129191

257273

10

10

16

1519

243

324

435

557 616

-

100

200

300

400

500

600

700

2005 2006 2007 2008 2009

KW

D m

n

Restaurants sector Industries sector Commercial & retail

Restaurants sector51%

Industries sector46%

Commercial & retail3%

Source: Company Reports * Including intercompany sales

Source: Company Reports

Sales from the restaurants sector increased at a CAGR of 21% from KWD153mn in 2005 to the estimated KWD324mn in 2009 (we excluded intercompany sales based on our estimates). This was mainly driven by the increasing number of restaurants (from 699 in 2005 to 1,157 in 2009) and the expansion of its network to 79 cities in 2009 (up from 58 cities in 2005).

Industry sector sales have shown even better growth — sales increased at a 36% CAGR from KWD80mn in 2005 to the estimated KWD273mn in 2009 (excluding intercompany sales based on our estimates). This growth came after the following: (i) external growth through the acquisition of Cairo Poultry and Senyorita Group in Egypt and (ii) the organic growth achieved through increasing the number of industrial subsidiaries to 21 in 2009 up from 15 in 2005. The company’s commercial and retail sector grew at an 18% CAGR (reaching KWD19mn in 2009 up from KWD9.8mn in 2005).

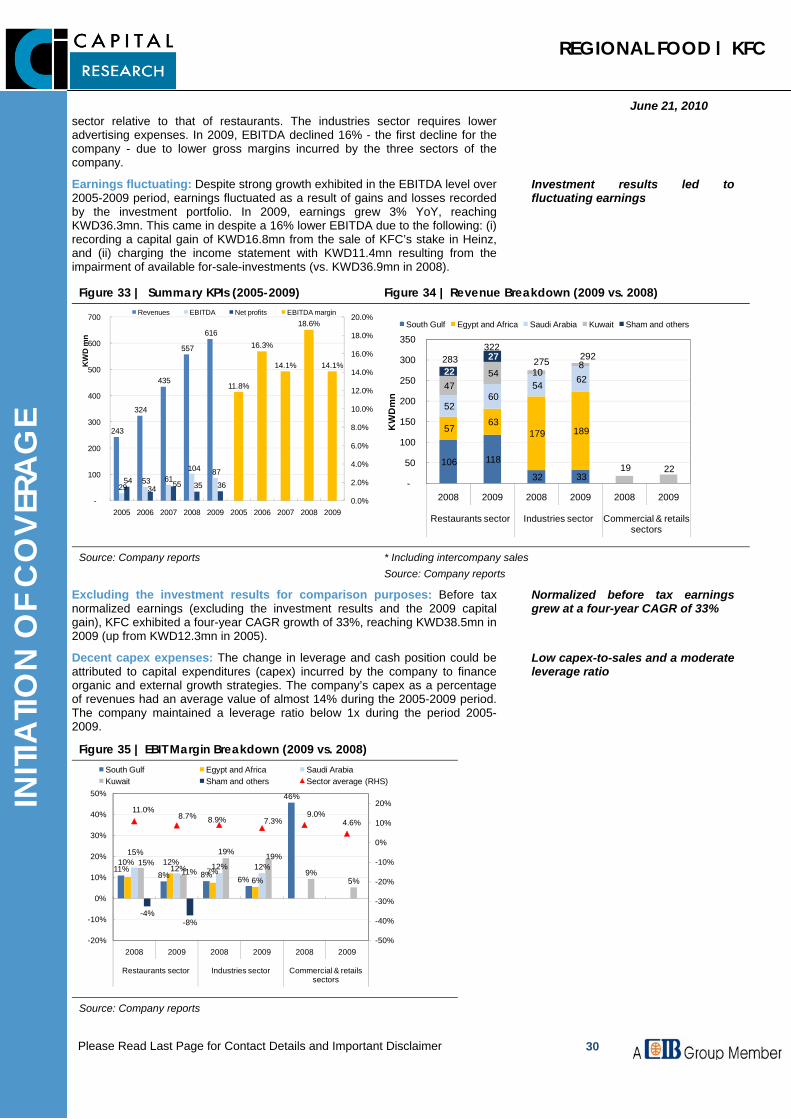

Gross margin dropped in 2009: Over the 2005-2009 period, gross profit margin fluctuated within the range of 22%-26%. In 2009, gross profit margin dropped to 22% (from 26% in 2008) owing to lower margins incurred by the company’s three business sectors (restaurants, industries and commercial & retail sectors). This came on the back of the following: (i) the company’s strategy to maintain market share, by partially passing only the higher costs of some of the raw materials and (ii) the prevailing slowdown and consumers’ shift towards lower margin products. In 2008, KFC’s gross margin increased by 420 bps to 25.8% (compared to 21.6% in 2005). This is primarily attributable to the following: (i) rationalization of the company’s expenses in all levels, particularly in raw materials and other décor packages through dealing with new markets, and (ii) careful selection of its locations for its new restaurants to benefit from the decrease in real estate market prices.

EBITDA increased at a 4-year CAGR of 32%. EBITDA margin improved 226 bps over the 2005-2009 period due to the gradual decline of selling, general, and administrative expenses (SG&A) as a percentage of revenue (from 9.8% in 2005 to 7.5% in 2009). We believe this came after the group rationalised its selling expenses and an increased contribution of revenue from the industries

Revenues more than doubled over a four-year period

Industrial sector leads revenue growth

Slowdown pressured gross margin

REGIONAL FOOD | KFC

June 21, 2010

30

INITI

ATIO

N O

F C

OVE

RAG

E

Please Read Last Page for Contact Details and Important Disclaimer

sector relative to that of restaurants. The industries sector requires lower advertising expenses. In 2009, EBITDA declined 16% - the first decline for the company - due to lower gross margins incurred by the three sectors of the company.

Earnings fluctuating: Despite strong growth exhibited in the EBITDA level over 2005-2009 period, earnings fluctuated as a result of gains and losses recorded by the investment portfolio. In 2009, earnings grew 3% YoY, reaching KWD36.3mn. This came in despite a 16% lower EBITDA due to the following: (i) recording a capital gain of KWD16.8mn from the sale of KFC’s stake in Heinz, and (ii) charging the income statement with KWD11.4mn resulting from the impairment of available for-sale-investments (vs. KWD36.9mn in 2008).

Figure 33 | Summary KPIs (2005-2009) Figure 34 | Revenue Breakdown (2009 vs. 2008)

243

324

435

557

616

29 53 61

104 87 54

34 55 35 36

11.8%

16.3%

14.1%

18.6%

14.1%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

-

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2005 2006 2007 2008 2009

KW

D m

n

Revenues EBITDA Net profits EBITDA margin

106 118

32 33

57 63

179 189

52 60

54 62 47

54 10 8

19 22

22 27 283

322 275 292

-

50

100

150

200

250

300

350

2008 2009 2008 2009 2008 2009

Restaurants sector Industries sector Commercial & retails sectors

KW

Dm

n

South Gulf Egypt and Africa Saudi Arabia Kuwait Sham and others

Source: Company reports * Including intercompany sales Source: Company reports

Excluding the investment results for comparison purposes: Before tax normalized earnings (excluding the investment results and the 2009 capital gain), KFC exhibited a four-year CAGR growth of 33%, reaching KWD38.5mn in 2009 (up from KWD12.3mn in 2005).

Decent capex expenses: The change in leverage and cash position could be attributed to capital expenditures (capex) incurred by the company to finance organic and external growth strategies. The company’s capex as a percentage of revenues had an average value of almost 14% during the 2005-2009 period. The company maintained a leverage ratio below 1x during the period 2005-2009.

Figure 35 | EBIT Margin Breakdown (2009 vs. 2008)

11%8% 8% 6%

46%

10% 12%7%

6%

15%

12% 12% 12%15%11%

19% 19%

9%5%

-4%-8%

11.0%8.7% 8.9% 7.3%

9.0%4.6%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

-20%

-10%

0%

10%

20%

30%

40%

50%

2008 2009 2008 2009 2008 2009

Restaurants sector Industries sector Commercial & retails sectors

South Gulf Egypt and Africa Saudi ArabiaKuwait Sham and others Sector average (RHS)

Source: Company reports

Investment results led to fluctuating earnings

Normalized before tax earnings grew at a four-year CAGR of 33%

Low capex-to-sales and a moderate leverage ratio

REGIONAL FOOD | KFC

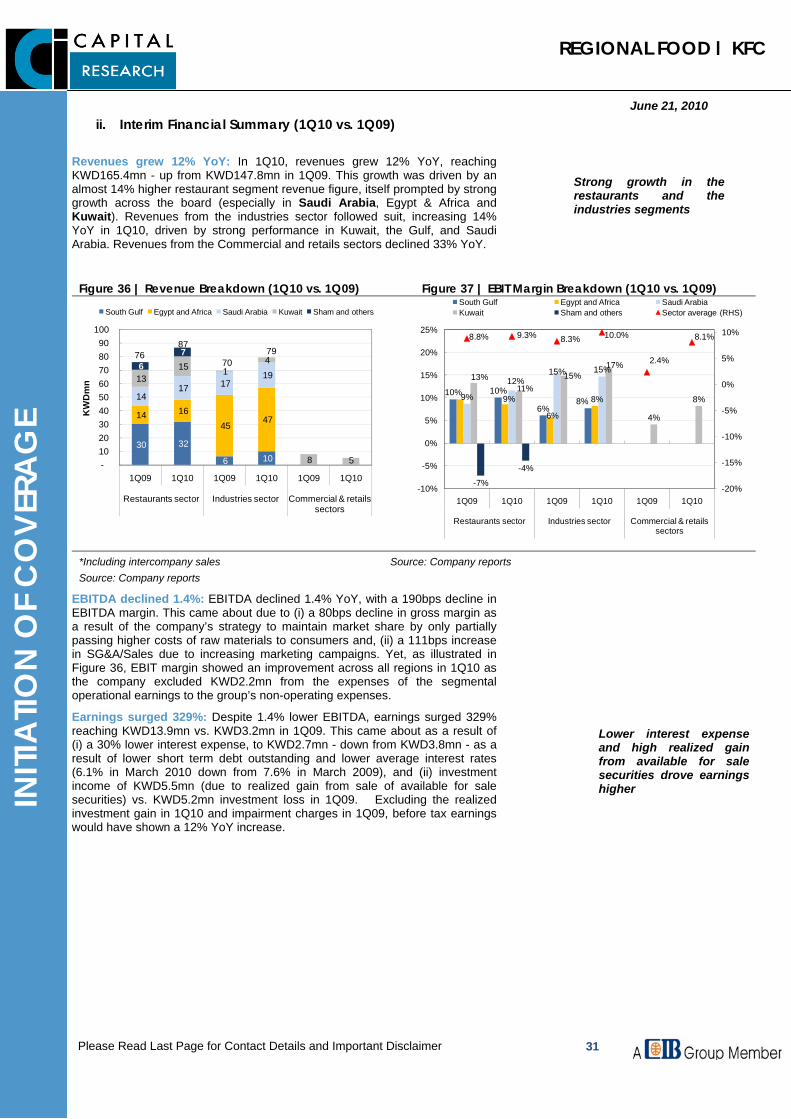

June 21, 2010

31