What Role for the ECB during the Great Recession? · PDF fileWhat Role for the ECB during the...

29

What Role for the ECB during the Great Recession? Giuseppe De Arcangelis DiSSEc

Transcript of What Role for the ECB during the Great Recession? · PDF fileWhat Role for the ECB during the...

What Role for the ECB during the Great Recession?

Giuseppe De Arcangelis DiSSEc

Plan of the talk

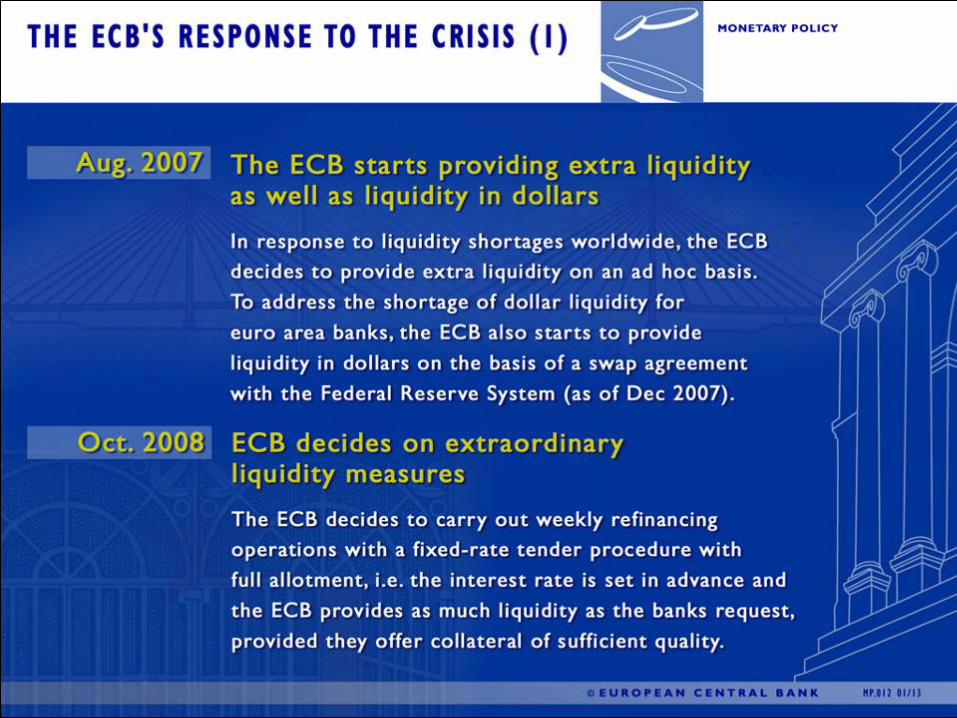

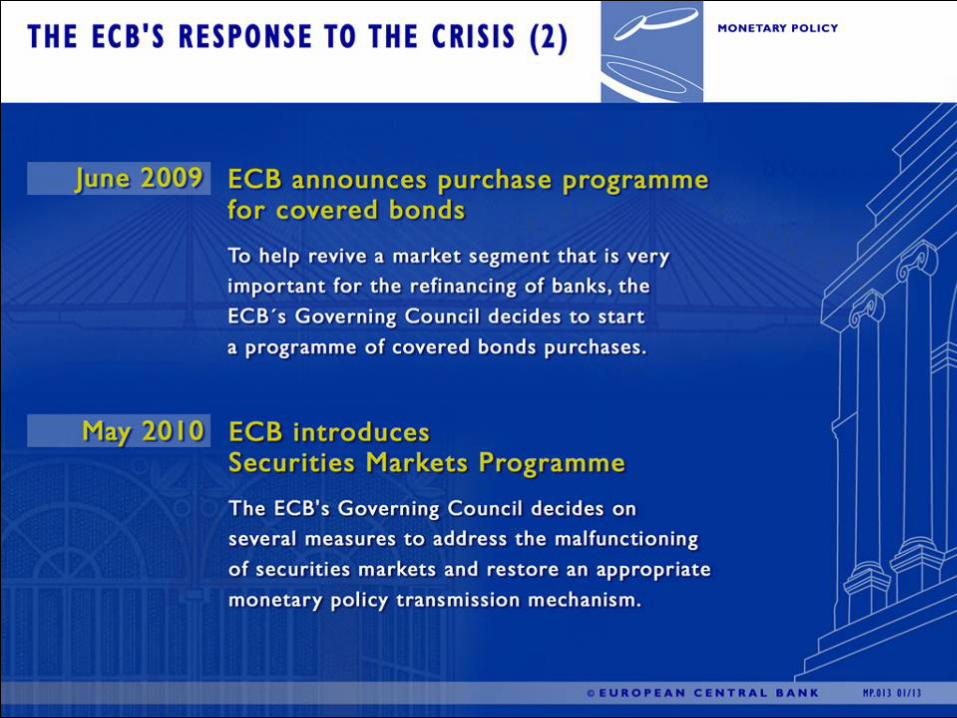

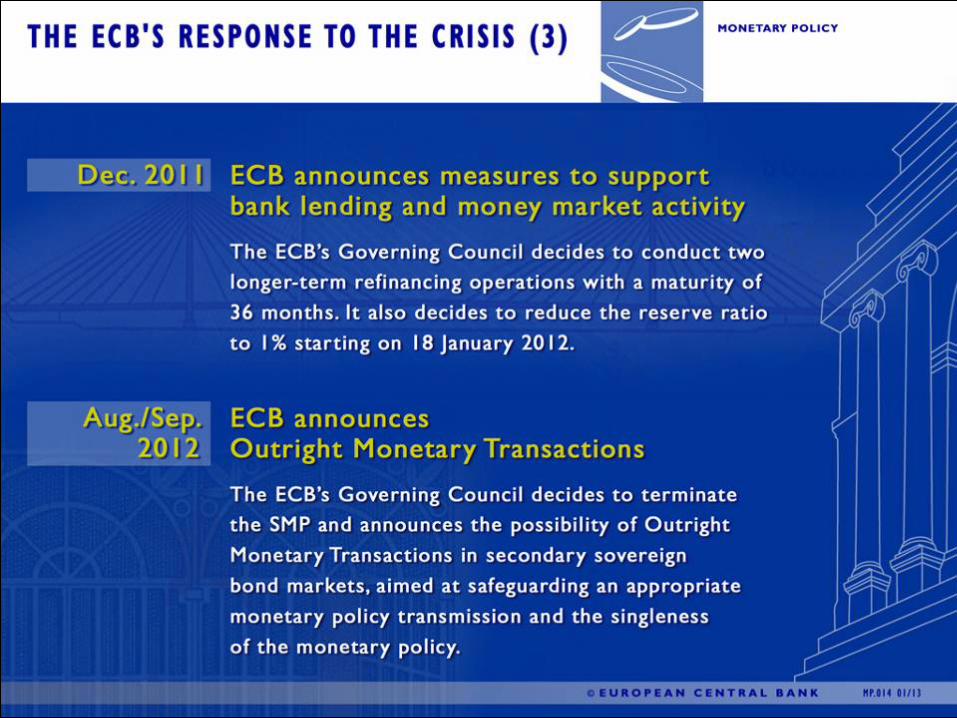

• Organization of the ECB • The decision making mechanism • Monetary Policy in the Eurozone • Changes in monetary policy making during

the Great Recession • Some considerations on the current

monetary environment

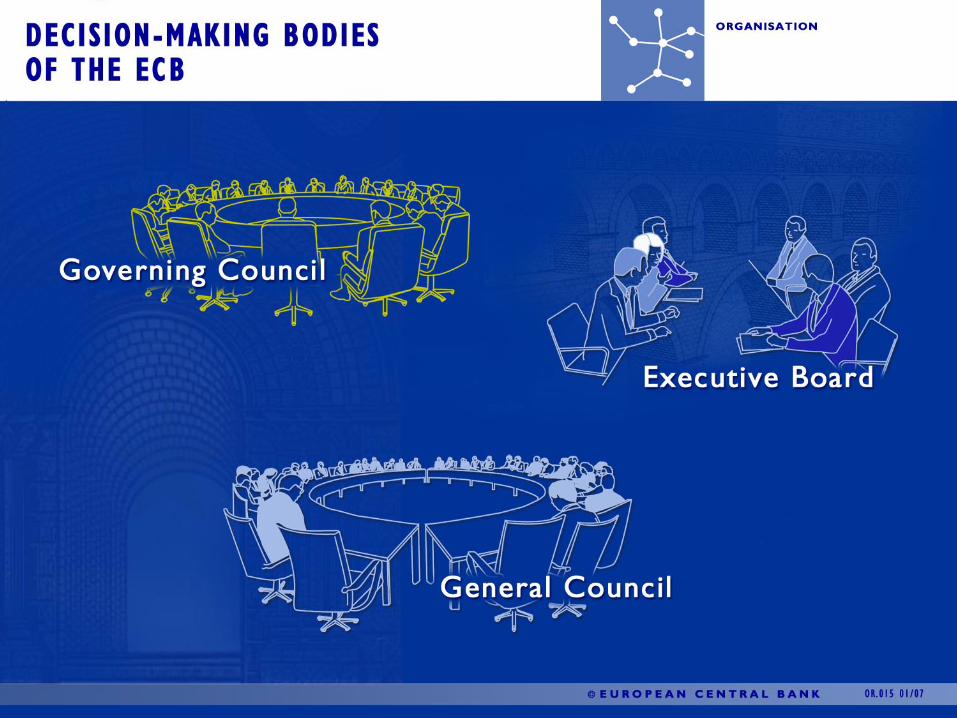

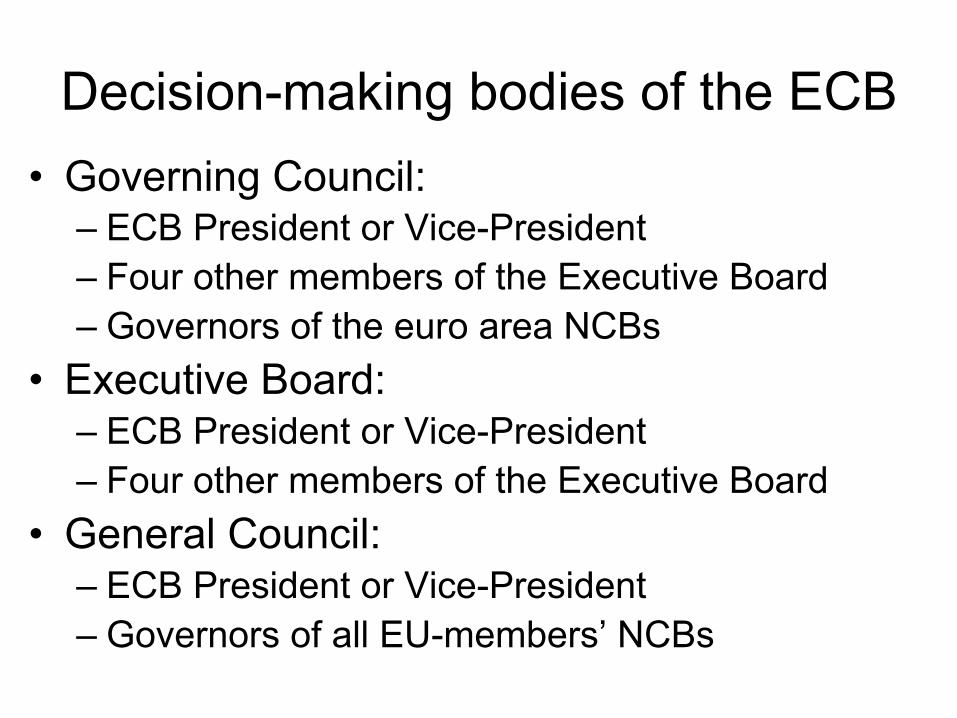

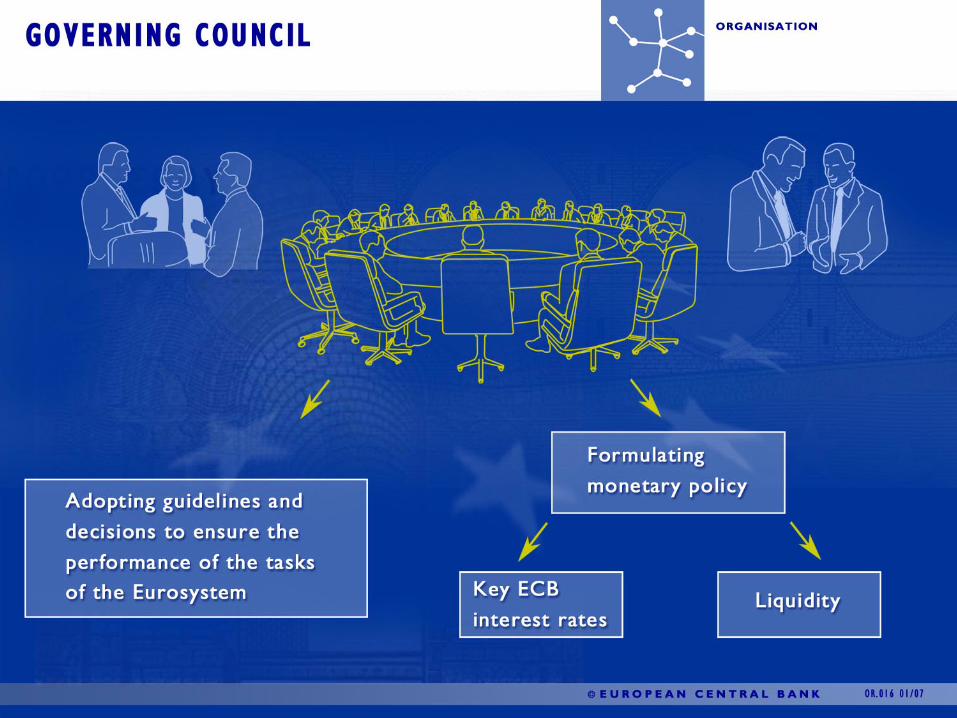

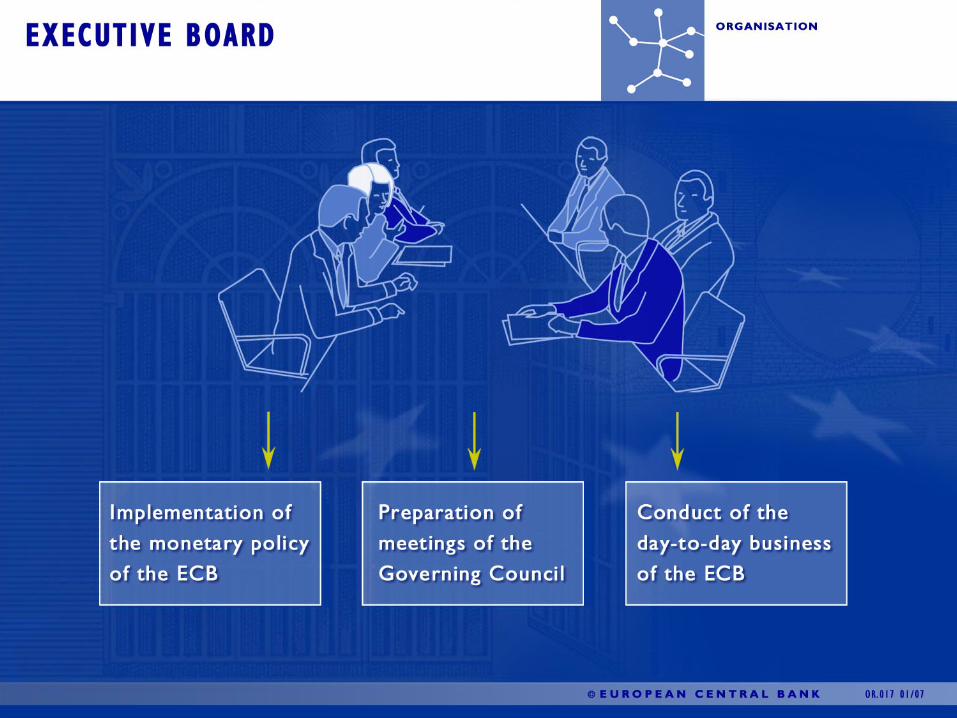

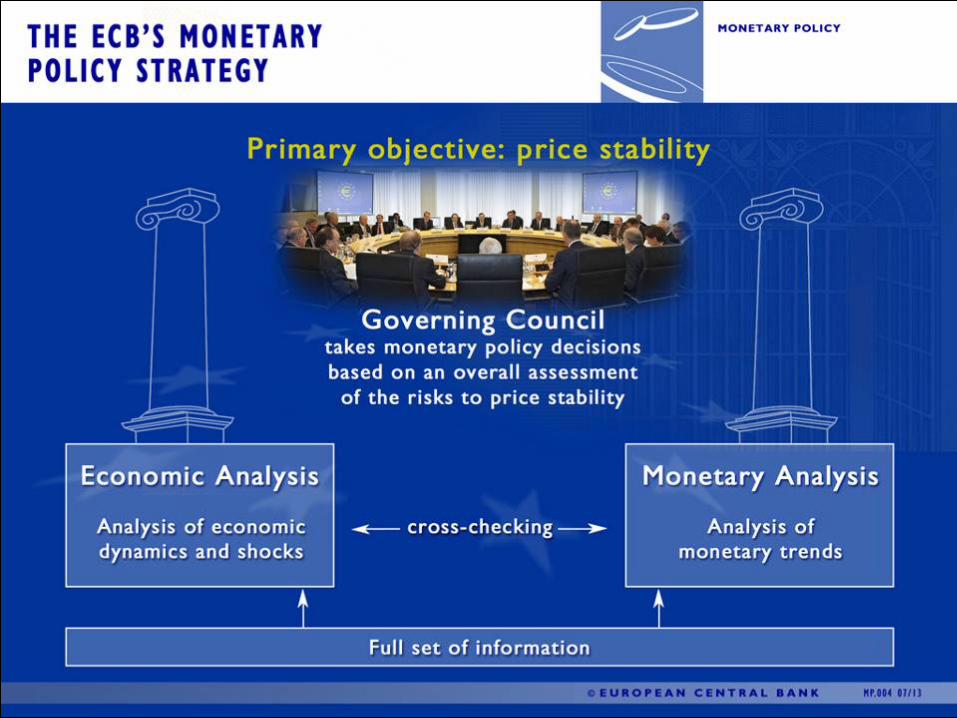

Decision-making bodies of the ECB • Governing Council:

– ECB President or Vice-President – Four other members of the Executive Board – Governors of the euro area NCBs

• Executive Board: – ECB President or Vice-President – Four other members of the Executive Board

• General Council: – ECB President or Vice-President – Governors of all EU-members’ NCBs

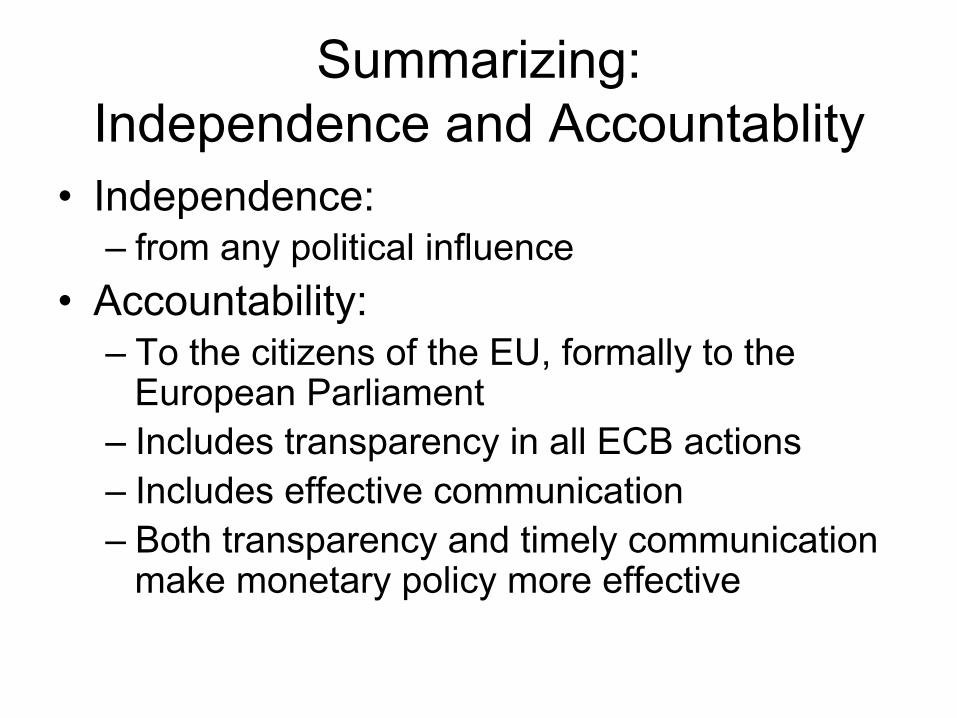

Summarizing: Independence and Accountablity

• Independence: – from any political influence

• Accountability: – To the citizens of the EU, formally to the

European Parliament – Includes transparency in all ECB actions – Includes effective communication – Both transparency and timely communication

make monetary policy more effective

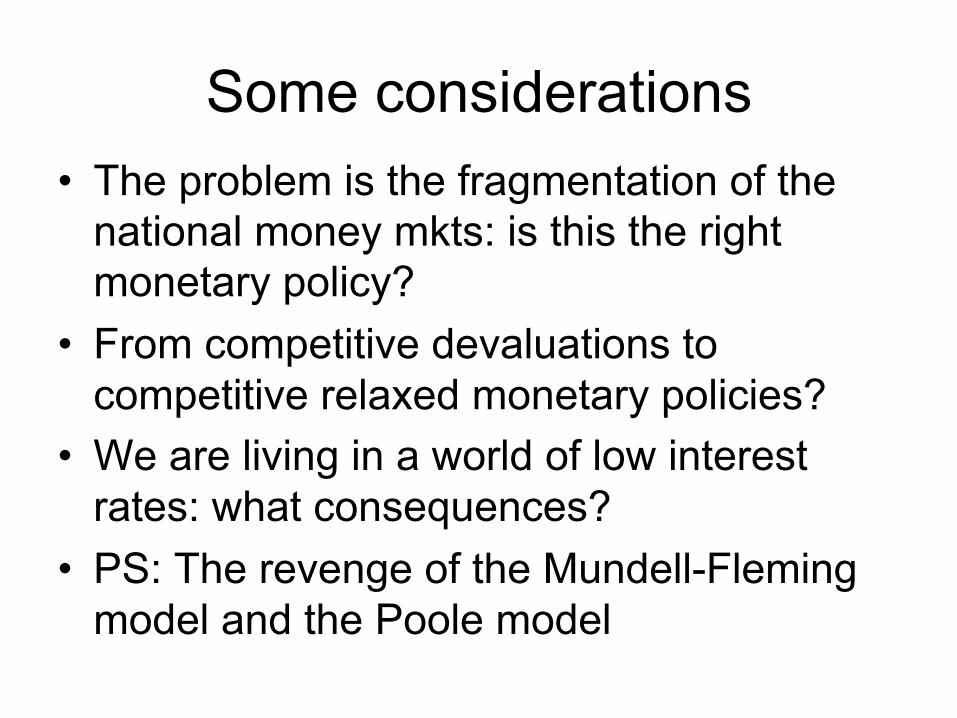

Some considerations • The problem is the fragmentation of the

national money mkts: is this the right monetary policy?

• From competitive devaluations to competitive relaxed monetary policies?

• We are living in a world of low interest rates: what consequences?

• PS: The revenge of the Mundell-Fleming model and the Poole model

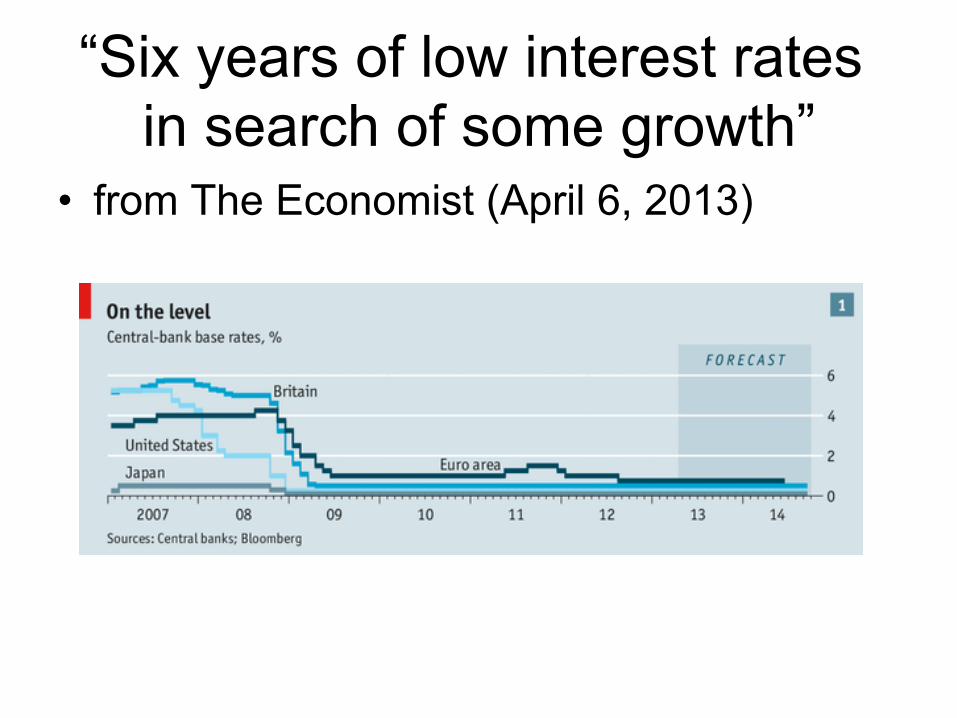

“Six years of low interest rates in search of some growth”

• from The Economist (April 6, 2013)

This is great! • Mortgages more affordable to more people à more «liquid» housing mkt à more people mobility

• Easier consumption credit, however positive signs only from the US (automobile mkt)

• Big bonanza for all debtors – including (some) sovereign debtors «instead of offering risk-free return they offer return-free risk» (Jim Grant)

Are we sure? • Cheap credit has consequences also on

other financial mkts • Savers dislike low rates of return (hate

negative real RoR) and new derivatives are (re)created and moving to more riskier investment

• Companies may engage in more riskier project and banks may be willing to lend

• Bubbles again

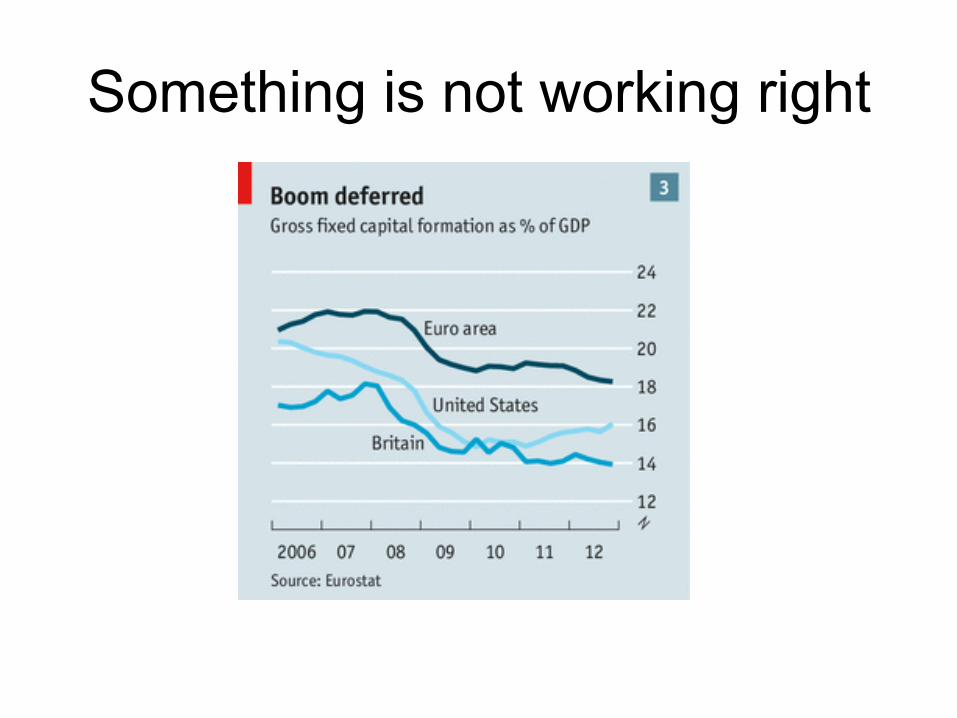

Something is not working right

Conclusions

• Cheap credit from central banks may not help

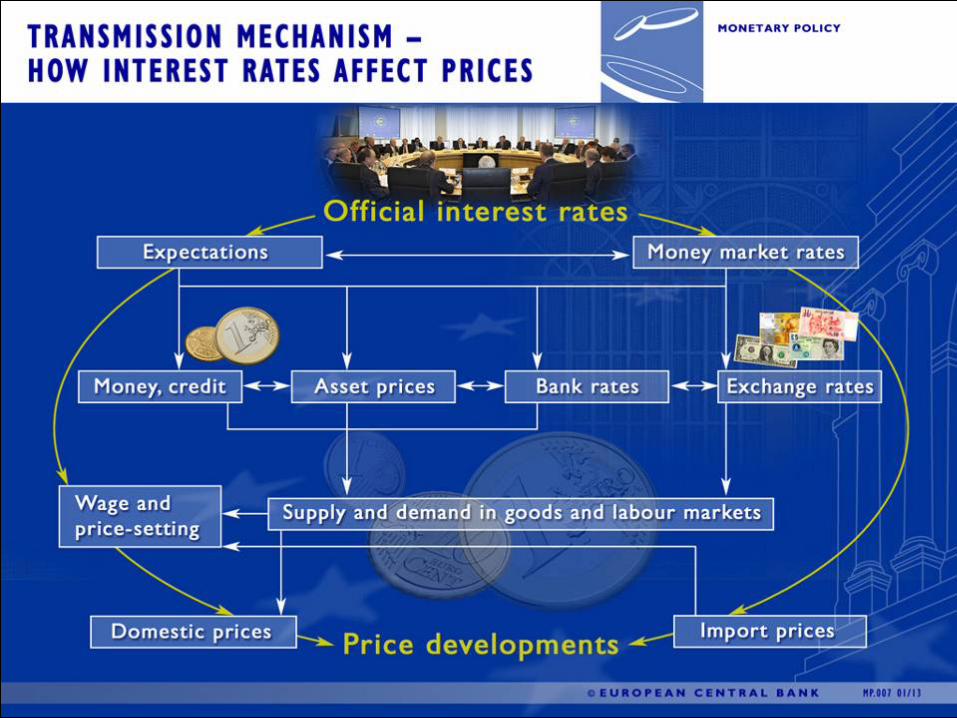

• The transmission mechanism may be broken

• Large amounts of liquidity are not igniting growth

• Careful not to ignite a new bubble! • Back to the inital point?