The Role of the Chemical Tanker in Everyday Life 2011 CMA Chem Tank Presentation.pdf• Introduction...

41

The Role of the Chemical Tanker in Everyday Life CMA Luncheon Stamford, CT January 27, 2011 Jack Noonan Jack Noonan CEO CEO BLT Chembulk Group BLT Chembulk Group

Transcript of The Role of the Chemical Tanker in Everyday Life 2011 CMA Chem Tank Presentation.pdf• Introduction...

The Role of the Chemical Tanker in Everyday Life

CMA LuncheonStamford, CT

January 27, 2011

Jack NoonanJack NoonanCEOCEOBLT Chembulk GroupBLT Chembulk Group

• Introduction to BLT Chembulk Group

• Chemical Tanker Industry: An Overview

• 50 Years – A Brief History of Chemical Parcel Tanker Trade

• The Role of the Chemical Tanker in Everyday Life

• Chemical Tanker Trade

– Where it is today

– Where it is going

Today’s Agenda

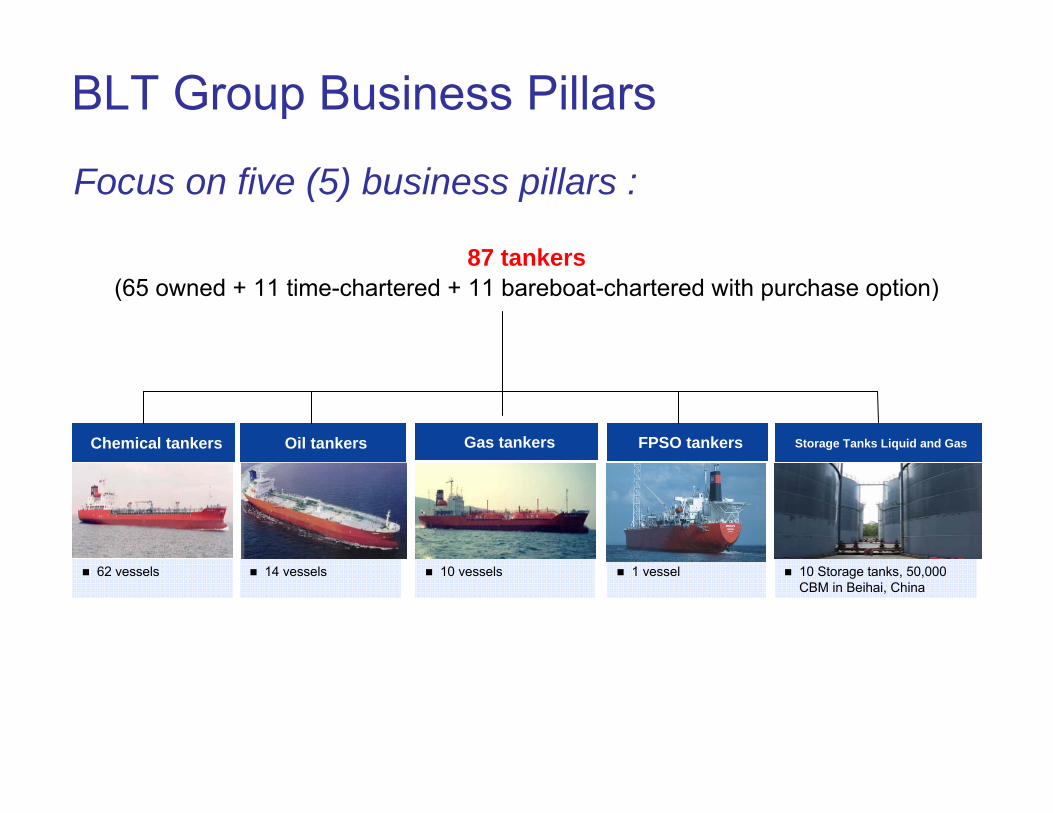

Focus on five (5) business pillars :

87 tankers(65 owned + 11 time-chartered + 11 bareboat-chartered with purchase option)

62 vessels 14 vessels 1 vessel

Chemical tankers Oil tankers FPSO tankersGas tankers

10 vessels

Storage Tanks Liquid and Gas

10 Storage tanks, 50,000 CBM in Beihai, China

BLT Group Business Pillars

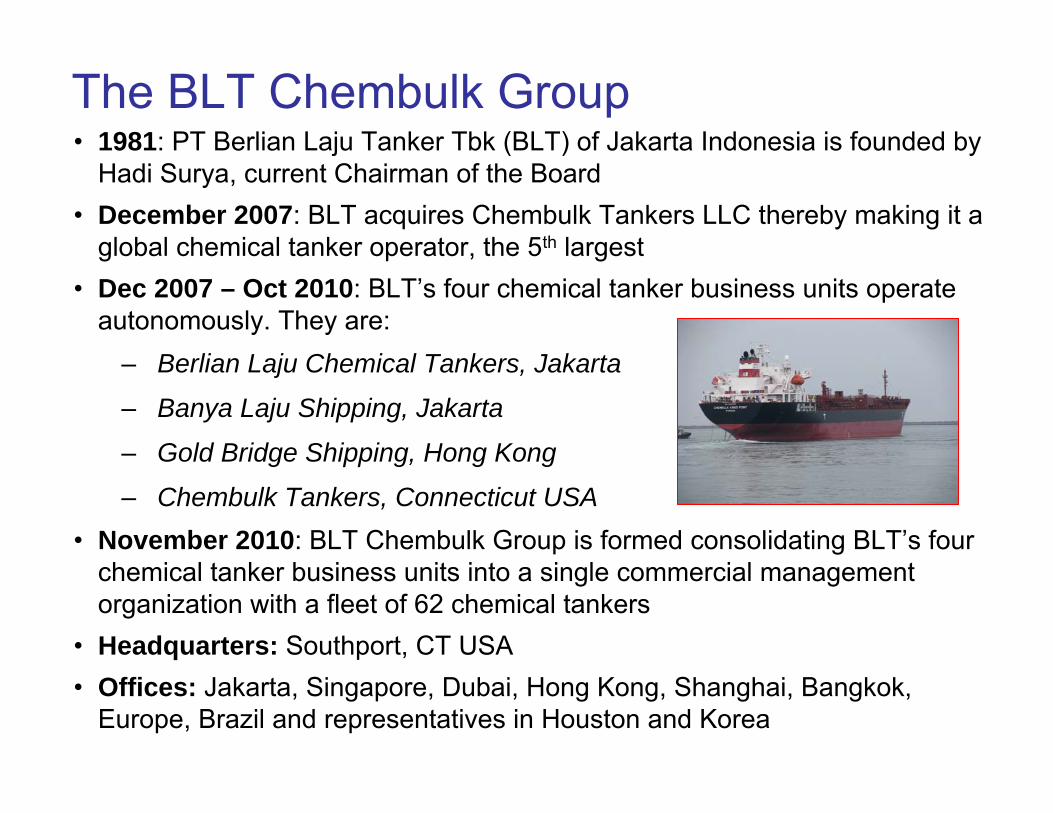

The BLT Chembulk Group • 1981: PT Berlian Laju Tanker Tbk (BLT) of Jakarta Indonesia is founded by

Hadi Surya, current Chairman of the Board • December 2007: BLT acquires Chembulk Tankers LLC thereby making it a

global chemical tanker operator, the 5th largest • Dec 2007 – Oct 2010: BLT’s four chemical tanker business units operate

autonomously. They are: – Berlian Laju Chemical Tankers, Jakarta

– Banya Laju Shipping, Jakarta

– Gold Bridge Shipping, Hong Kong

– Chembulk Tankers, Connecticut USA• November 2010: BLT Chembulk Group is formed consolidating BLT’s four

chemical tanker business units into a single commercial management organization with a fleet of 62 chemical tankers

• Headquarters: Southport, CT USA• Offices: Jakarta, Singapore, Dubai, Hong Kong, Shanghai, Bangkok,

Europe, Brazil and representatives in Houston and Korea

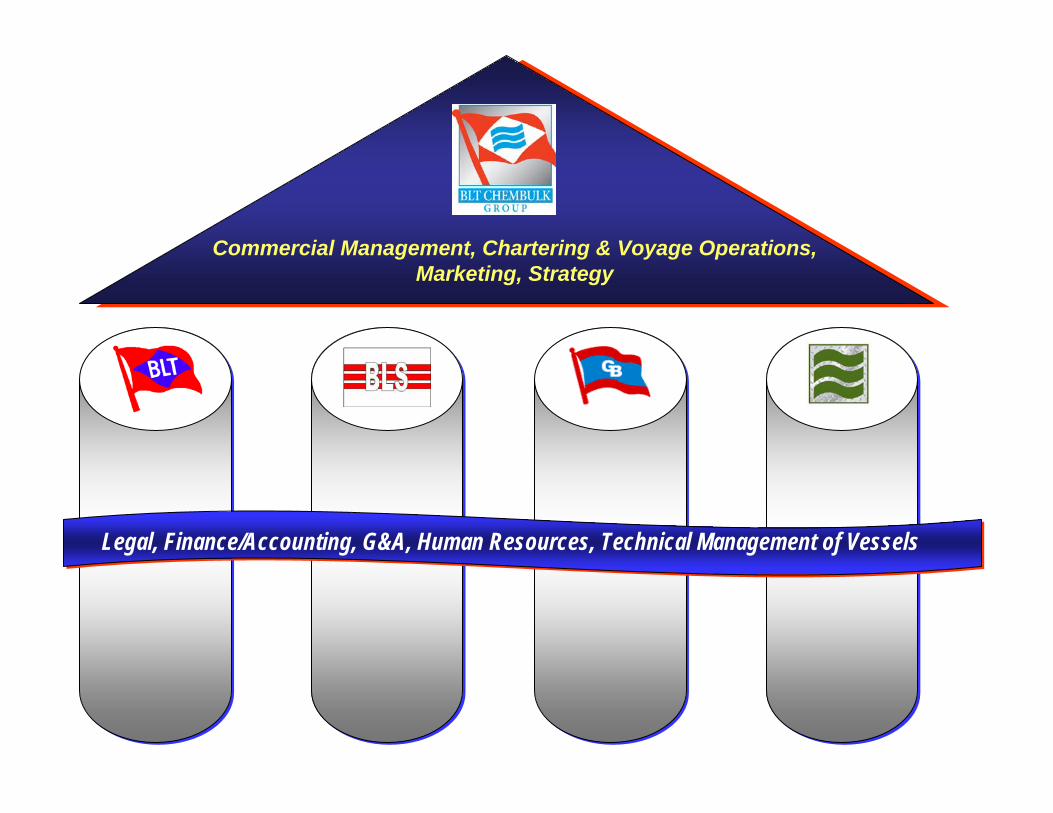

Commercial Management, Chartering & Voyage Operations, Marketing, Strategy

Legal, Finance/Accounting, G&A, Human Resources, Technical Management of Vessels

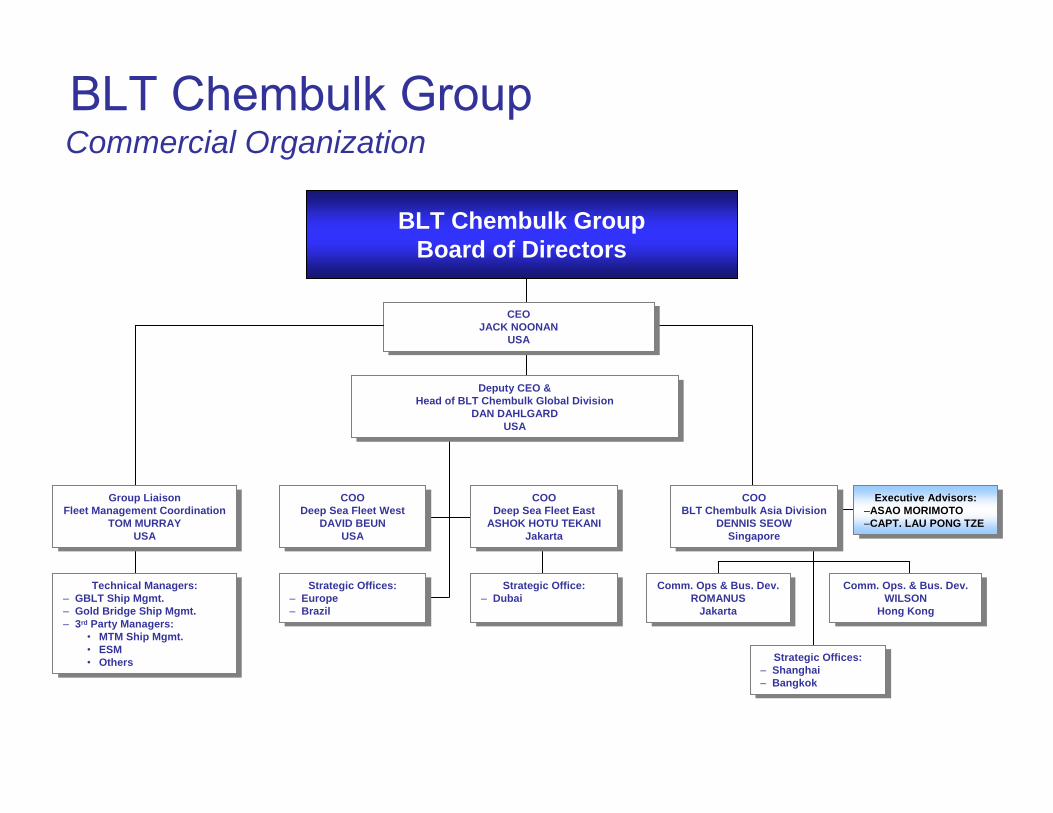

BLT Chembulk GroupCommercial Organization

BLT Chembulk GroupBoard of Directors

CEOJACK NOONAN

USA

CEOJACK NOONAN

USA

Deputy CEO &Head of BLT Chembulk Global Division

DAN DAHLGARDUSA

Deputy CEO &Head of BLT Chembulk Global Division

DAN DAHLGARDUSA

Group LiaisonFleet Management Coordination

TOM MURRAYUSA

Group LiaisonFleet Management Coordination

TOM MURRAYUSA

COODeep Sea Fleet West

DAVID BEUNUSA

COODeep Sea Fleet West

DAVID BEUNUSA

COODeep Sea Fleet East

ASHOK HOTU TEKANIJakarta

COODeep Sea Fleet East

ASHOK HOTU TEKANIJakarta

COOBLT Chembulk Asia Division

DENNIS SEOWSingapore

COOBLT Chembulk Asia Division

DENNIS SEOWSingapore

Executive Advisors:–ASAO MORIMOTO–CAPT. LAU PONG TZE

Executive Advisors:–ASAO MORIMOTO–CAPT. LAU PONG TZE

Technical Managers:– GBLT Ship Mgmt.– Gold Bridge Ship Mgmt.– 3rd Party Managers:

• MTM Ship Mgmt.• ESM• Others

Technical Managers:– GBLT Ship Mgmt.– Gold Bridge Ship Mgmt.– 3rd Party Managers:

• MTM Ship Mgmt.• ESM• Others

Strategic Offices:– Europe– Brazil

Strategic Offices:– Europe– Brazil

Strategic Office:– Dubai

Strategic Office:– Dubai

Comm. Ops & Bus. Dev.ROMANUS

Jakarta

Comm. Ops & Bus. Dev.ROMANUS

Jakarta

Comm. Ops. & Bus. Dev.WILSON

Hong Kong

Comm. Ops. & Bus. Dev.WILSON

Hong Kong

Strategic Offices:– Shanghai– Bangkok

Strategic Offices:– Shanghai– Bangkok

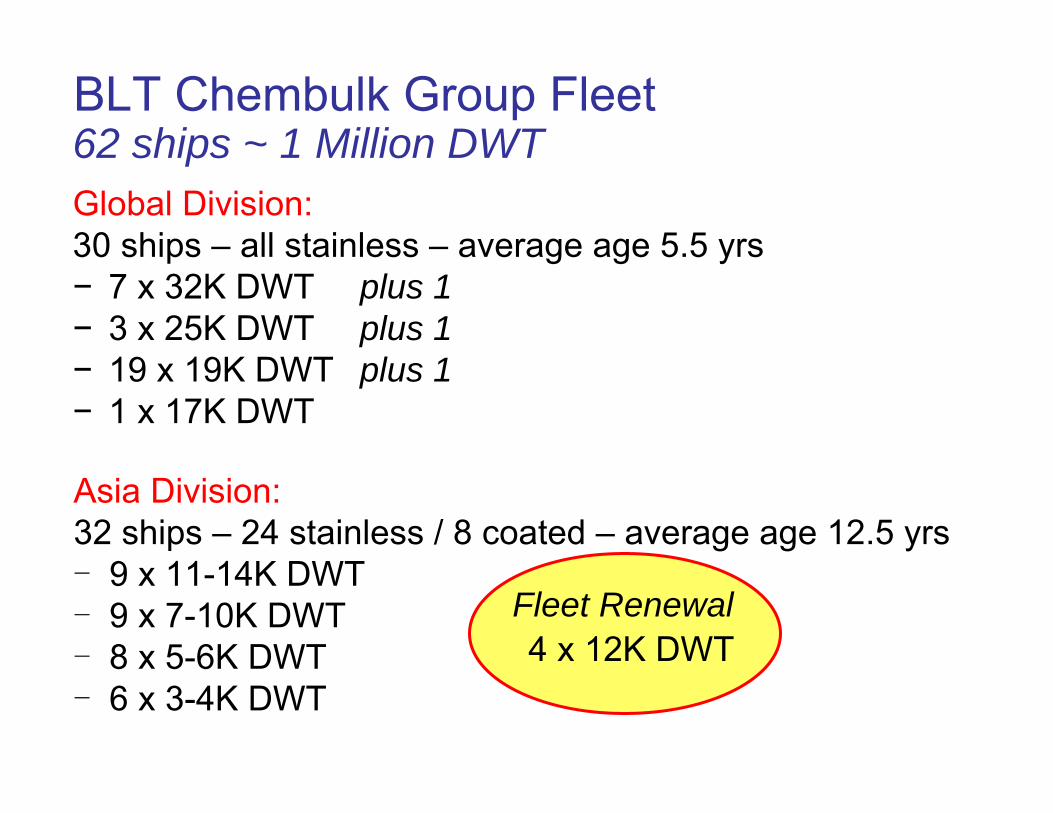

Asia Division:32 ships – 24 stainless / 8 coated – average age 12.5 yrs‒ 9 x 11-14K DWT‒ 9 x 7-10K DWT‒ 8 x 5-6K DWT‒ 6 x 3-4K DWT

BLT Chembulk Group Fleet

Global Division:30 ships – all stainless – average age 5.5 yrs− 7 x 32K DWT plus 1− 3 x 25K DWT plus 1− 19 x 19K DWT plus 1− 1 x 17K DWT

62 ships ~ 1 Million DWT

4 x 12K DWTFleet Renewal

88

Jakarta

Bangkok

Shanghai

Glasgow

Dubai

Global Division Trading

Asia Division Trading

Worldwide Trading Routes

Strategic Office

Regional Headquarters

BLT Chembulk Group HQ

Sao Paulo

Hong Kong

Southport,CT

Singapore

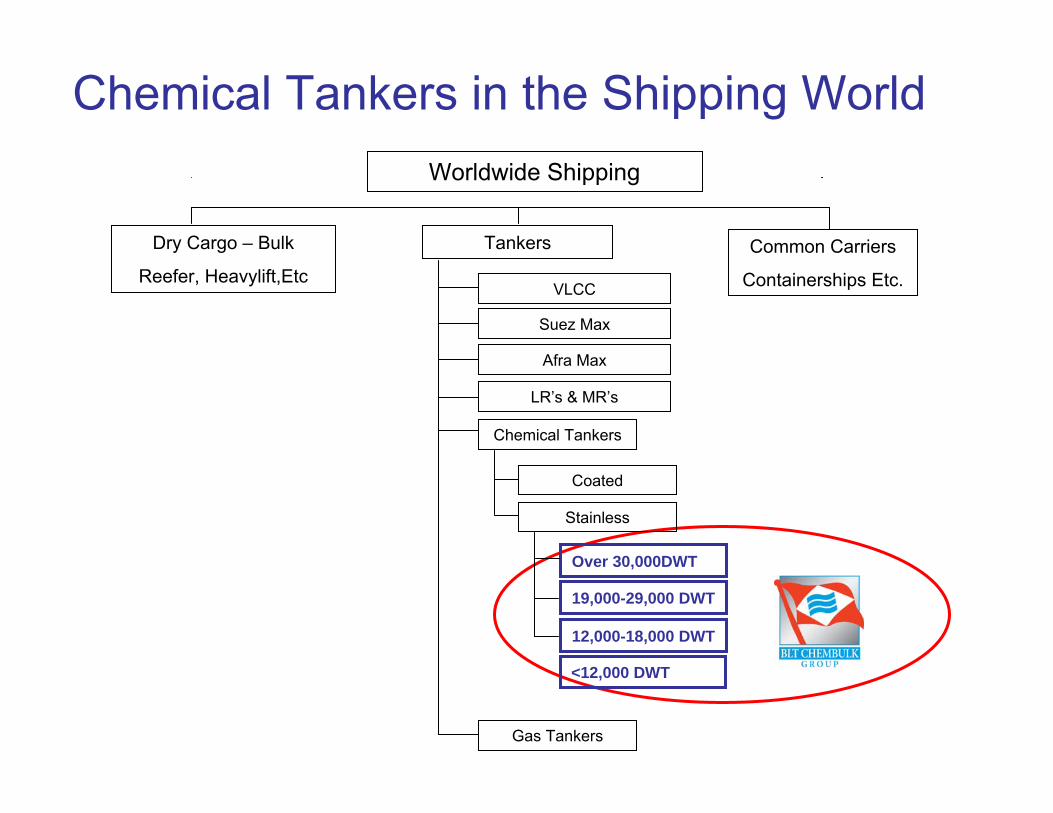

Chemical Tanker Trade: An Overview

Chemical Tankers in the Shipping WorldWorldwide Shipping

Dry Cargo – Bulk

Reefer, Heavylift,EtcCommon Carriers

Containerships Etc.

Tankers

19,000-29,000 DWT

Suez Max

Afra Max

LR’s & MR’s

Chemical Tankers

Stainless

Coated

VLCC

12,000-18,000 DWT

Over 30,000DWT

Gas Tankers

<12,000 DWT

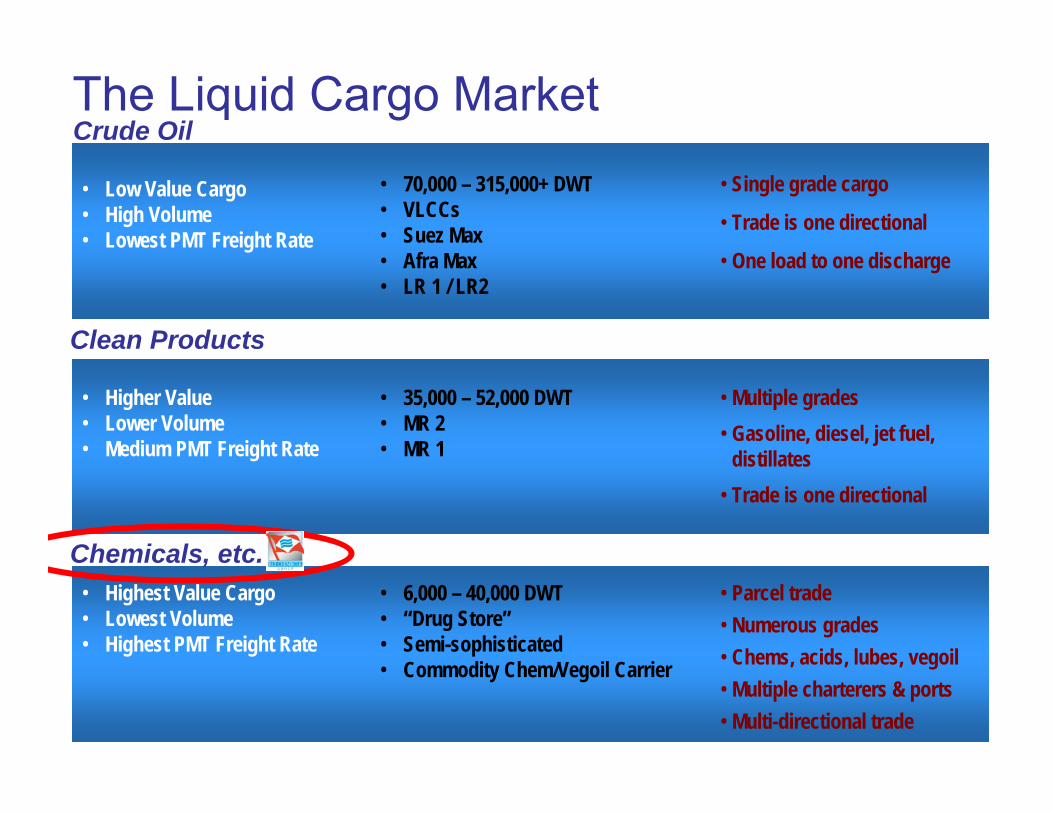

The Liquid Cargo Market

• 70,000 – 315,000+ DWT• VLCCs• Suez Max• Afra Max• LR 1 / LR2

• 35,000 – 52,000 DWT• MR 2• MR 1

• 6,000 – 40,000 DWT• “Drug Store”• Semi-sophisticated• Commodity Chem/Vegoil Carrier

• Single grade cargo

• Trade is one directional

• One load to one discharge

• Multiple grades• Gasoline, diesel, jet fuel,

distillates• Trade is one directional

• Parcel trade• Numerous grades• Chems, acids, lubes, vegoil• Multiple charterers & ports• Multi-directional trade

• Higher Value• Lower Volume• Medium PMT Freight Rate

• Low Value Cargo• High Volume• Lowest PMT Freight Rate

• Highest Value Cargo• Lowest Volume• Highest PMT Freight Rate

Crude Oil

Clean Products

Chemicals, etc.

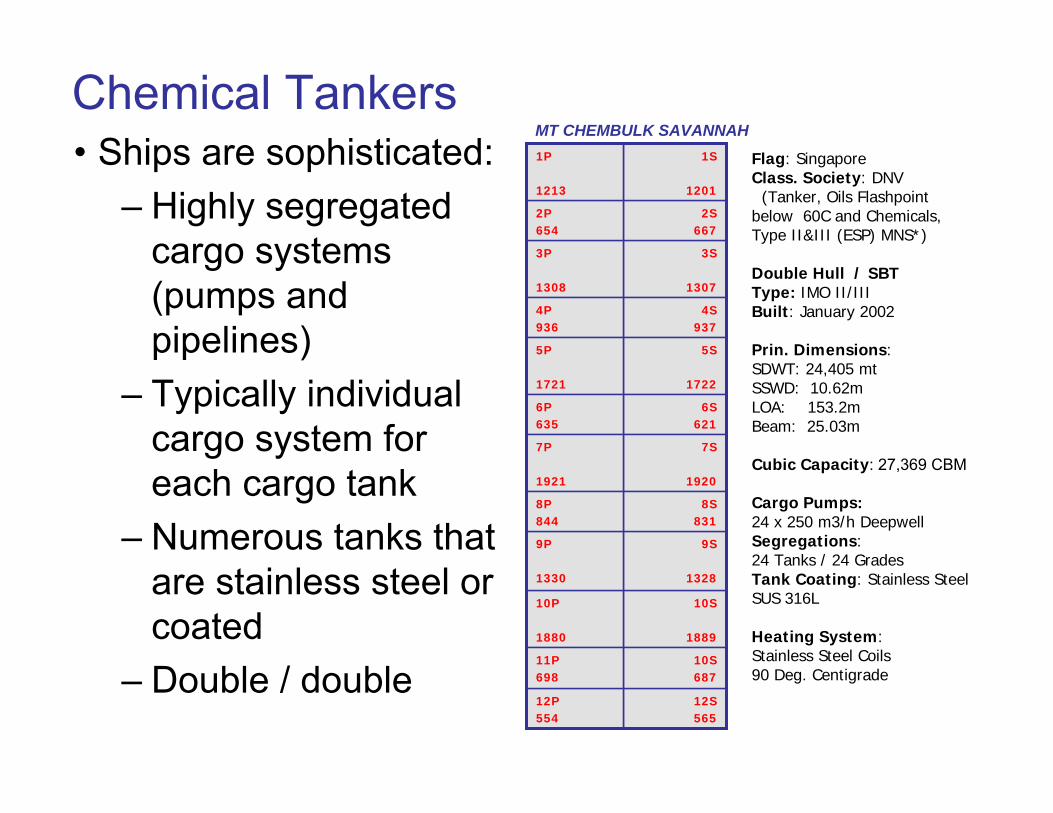

Chemical Tankers• Ships are sophisticated:

– Highly segregated cargo systems (pumps and pipelines)

– Typically individual cargo system for each cargo tank

– Numerous tanks that are stainless steel or coated

– Double / double

10S

1889

10P

1880

3S

1307

3P

1308

4S937

4P936

5S

1722

5P

1721

6S621

6P635

7S

1920

7P

1921

12S565

12P554

10S687

11P698

9S

1328

9P

1330

8S831

8P844

2S667

2P654

1S

1201

1P

1213

MT CHEMBULK SAVANNAH

Flag: SingaporeClass. Society: DNV

(Tanker, Oils Flashpoint below 60C and Chemicals, Type II&III (ESP) MNS*)

Double Hull / SBTType: IMO II/IIIBuilt: January 2002

Prin. Dimensions:SDWT: 24,405 mt SSWD: 10.62m LOA: 153.2mBeam: 25.03m

Cubic Capacity: 27,369 CBM

Cargo Pumps: 24 x 250 m3/h DeepwellSegregations: 24 Tanks / 24 GradesTank Coating: Stainless Steel SUS 316L

Heating System: Stainless Steel Coils90 Deg. Centigrade

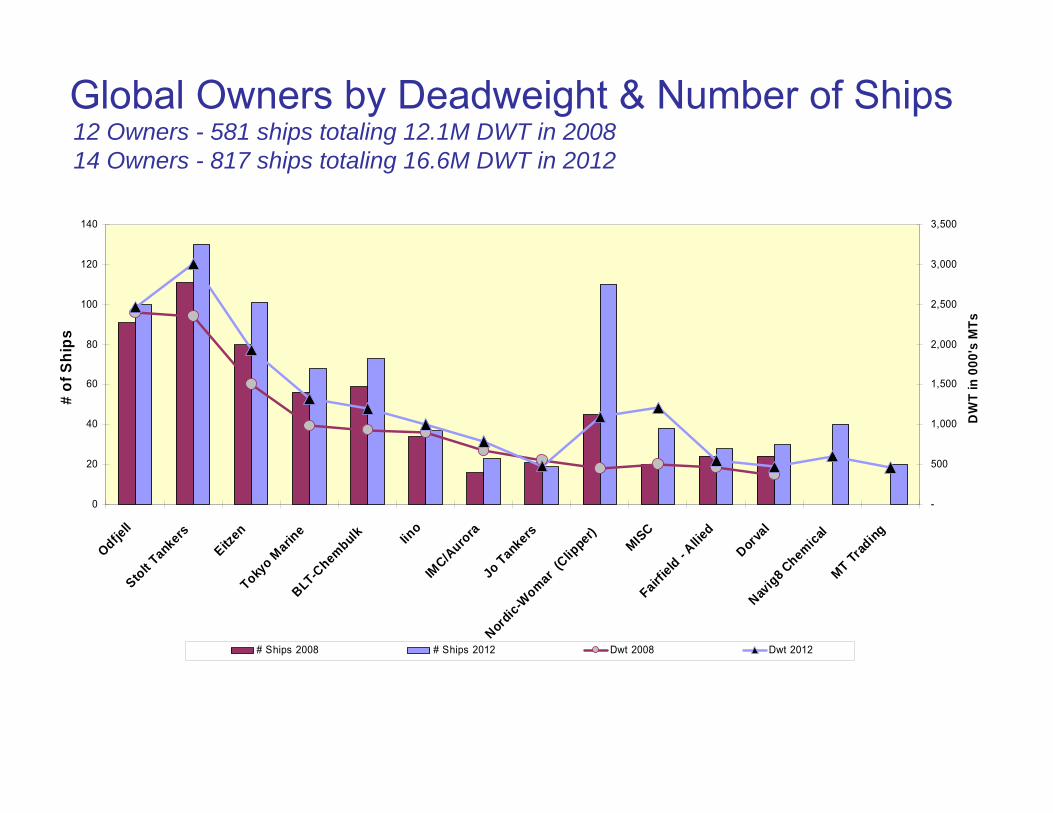

The global owning sector is an oligopoly.

Chemical Tanker Ownership

As depicted on the following graph:

• In 2008 the three largest owners operate ~52% of the total deadweight (~45% in 2012)

• ~85% of the total global deadweight is operated by just twelve companies (14 companies in 2012)

• The balance is mostly comprised of numerous smaller owners operating regionally; many in Asia

0

20

40

60

80

100

120

140

Odfjell

Stolt Tankers

Eitzen

Tokyo M

arine

BLT-Chembulk Iin

oIM

C/Auro

raJo Tankers

Nordic-W

omar (Clip

per)

MISCFairf

ield - Allie

d

Dorval

Navig8 C

hemicalMT Trad

ing

# of

Shi

ps

-

500

1,000

1,500

2,000

2,500

3,000

3,500

DW

T in

000

's M

Ts

# Ships 2008 # Ships 2012 Dwt 2008 Dwt 2012

Global Owners by Deadweight & Number of Ships12 Owners - 581 ships totaling 12.1M DWT in 200814 Owners - 817 ships totaling 16.6M DWT in 2012

Chemical Tanker IndustryA Brief History: 1959-2010

• Young industry – born in 1959 – approximately 50 years

• First chemical tankers were modified product tankers– Additional tanks, pumprooms & pipelines– Providing for more grades, smaller quantities

• Earliest trade – vegoils and tallow from Great Lakes to Europe

• Alternative to drums and deep-tanks of general cargo ships– Improved economies of scale

• Stolt-Nielsen and Odfjell in the vanguard

• Transatlantic eastbound (USG to NWE) is benchmark tradelane– Chemical producer, commodity chemical focused

The Beginning: 1959 - 1970

First “purpose built” chemical tankers delivered:The 1970’s: Development Decade

• Significantly increased cargo segregation and integrity

− Individual “per tank” cargo systems

− Cofferdams and double-bottoms

− Improved tank coatings and stainless steel

− Beginning of true “drug store” trade

• Proto-typical size: 20-30K DWT

• Rise of commodity trader business (Phillip Bothers, Sogo Shosha)

• Transpacific westbound (USG to North Asia) becomes benchmark trade

• Significant newbuilding programs by majors – Stolt, Odfjell, JOT

• Volatile decade for chemical tanker owners

– Market boom 1973-74 due to inelastic supply

– Market collapse in 1975 following first oil price shock

– 2nd oil price shock in 1979 brings about major recovery

The 1980’s: Transition • Late 70’s strong market spurs new owner entry – primarily Japanese

• Further fleet expansion by majors

• 30-40K DWT becomes proto-typical size for deep-sea chemical tanker

• Emergence of smaller (6-9,000 DWT) ships for short-sea trade – “A lot of them!”

• Significant vessel deliveries in early 80’s coupled with cyclical chemical downturn severely dampens market.

• Numerous bankruptcies among newcomers – and resulting rationalization

− 2nd hand ownership and rise of the time-charter operator

• Cyclical upswing, owner rationalization in 2nd half of 80’s stabilizes market

• Legislative and regulatory requirements have commercial impact

− Last-cargo (FOSFA, NIOP) and environmental (MARPOL) restrictions

The 1990’s: Maturity• Gulf War 1990-91 market spike and subsequent trough• OPA 90 – increased regulatory compliance and quality control• Asian Tigers: Industrial growth in Thailand, Taiwan, So. Korea, etc.

− New chemical production creates new intra-regional trade routes− Impacts established deep-sea markets, reduces ton-mile demand

• Mergers and consolidation trend begins – reducing market participants− BPAmoco, ExxonMobil, Dow-UCC, Odfjell & Seachem Tankers

• Mid 90’s majors’ fleet renewal− Fully stainless steel − Double/double construction

• Depressed market as decade ends− Surplus tonnage− Change in trading patterns− Asian currency crisis

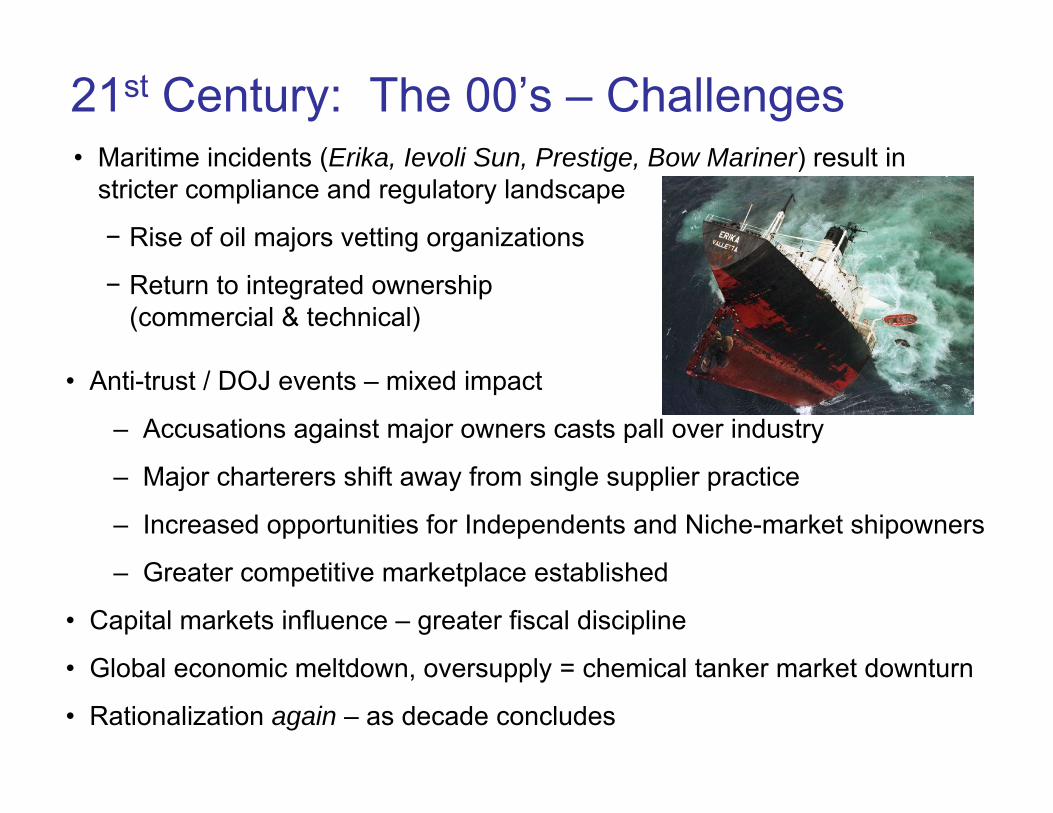

21st Century: The 00’s – Challenges • Maritime incidents (Erika, Ievoli Sun, Prestige, Bow Mariner) result in

stricter compliance and regulatory landscape

• Anti-trust / DOJ events – mixed impact

– Accusations against major owners casts pall over industry

– Major charterers shift away from single supplier practice

– Increased opportunities for Independents and Niche-market shipowners

– Greater competitive marketplace established

• Capital markets influence – greater fiscal discipline

• Global economic meltdown, oversupply = chemical tanker market downturn

• Rationalization again – as decade concludes

− Rise of oil majors vetting organizations

− Return to integrated ownership (commercial & technical)

The Role of the Chemical Tanker in Everyday Life

Tallow Chemicals

MolassesCPPVegOils

Lube Oils

Chemical Tanker Cargoes

Chemical Tankers Clientele

Commodity Traders, Grain Houses & Agricultural Concerns:

PETROBRAS

Multinational Chemical Producers:

International Oil Majors & National Oil Companies:

Chemicals: What WE remember, maybe?

Chemicals: Or maybe YOU remember this?

• Bunsen burners

• Multi-syllabic, difficult to pronounce nomenclature

• Di-Chloro blah blah

• Tri-Flouro blah blah blah

• Ethyl-Hexyl-Phenyl stuff

• Antidisestablishmentarianism

1978 Rutgers University Bumper Sticker: Honk if you passed Organic Chemistry!

1978 Rutgers University Bumper Sticker: 1978 Rutgers University Bumper Sticker: Honk if you passed Organic Chemistry!Honk if you passed Organic Chemistry!

Hydrocarbons

Chemicals – What THEY Think Now

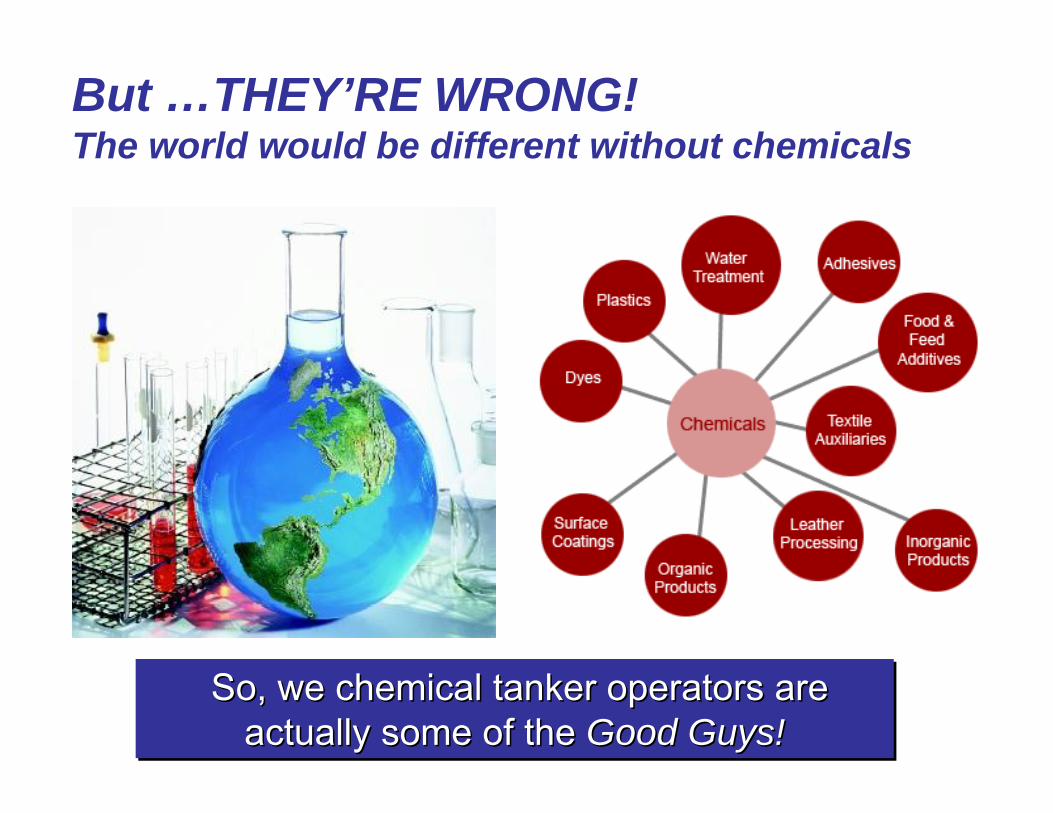

So, we chemical tanker operators are perceived to be some of the Bad Guys!So, we chemical tanker operators are So, we chemical tanker operators are

perceived to be some of the perceived to be some of the Bad Guys!Bad Guys!

But …THEY’RE WRONG!The world would be different without chemicals

So, we chemical tanker operators are actually some of the Good Guys!

So, we chemical tanker operators are So, we chemical tanker operators are actually some of the actually some of the Good Guys!Good Guys!

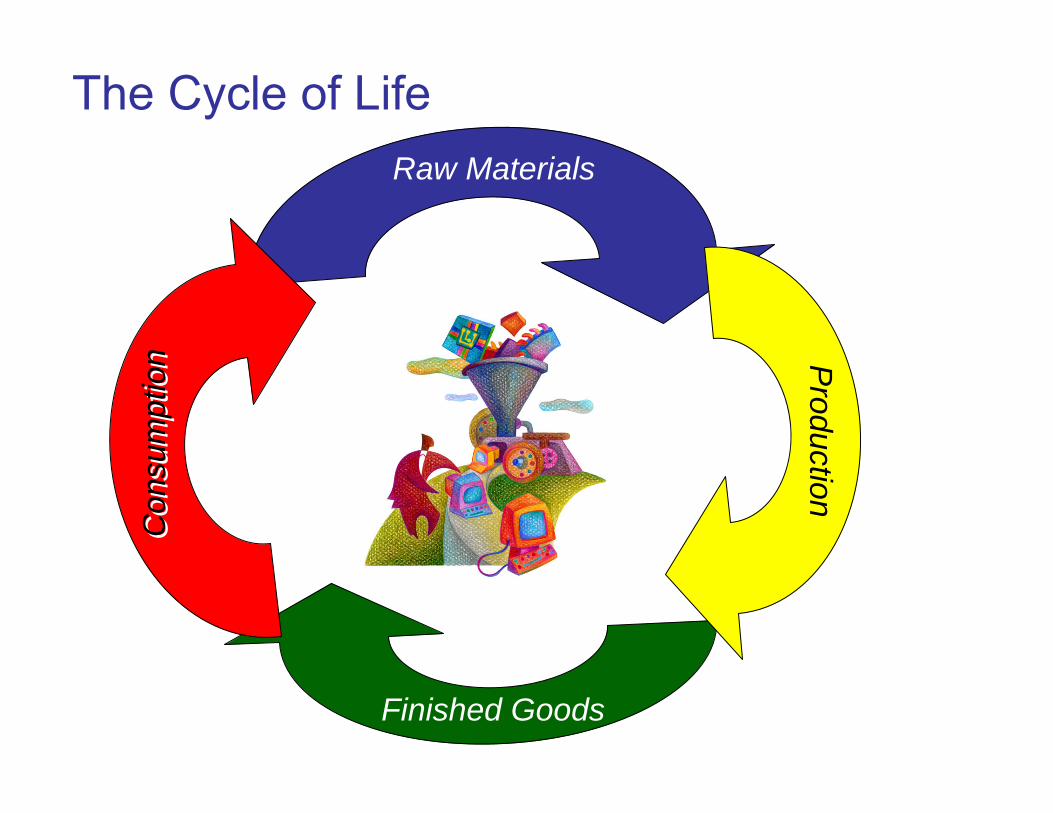

The Cycle of Life

Finished Goods

Raw Materials

Production

Con

sum

ptio

nC

onsu

mpt

ion

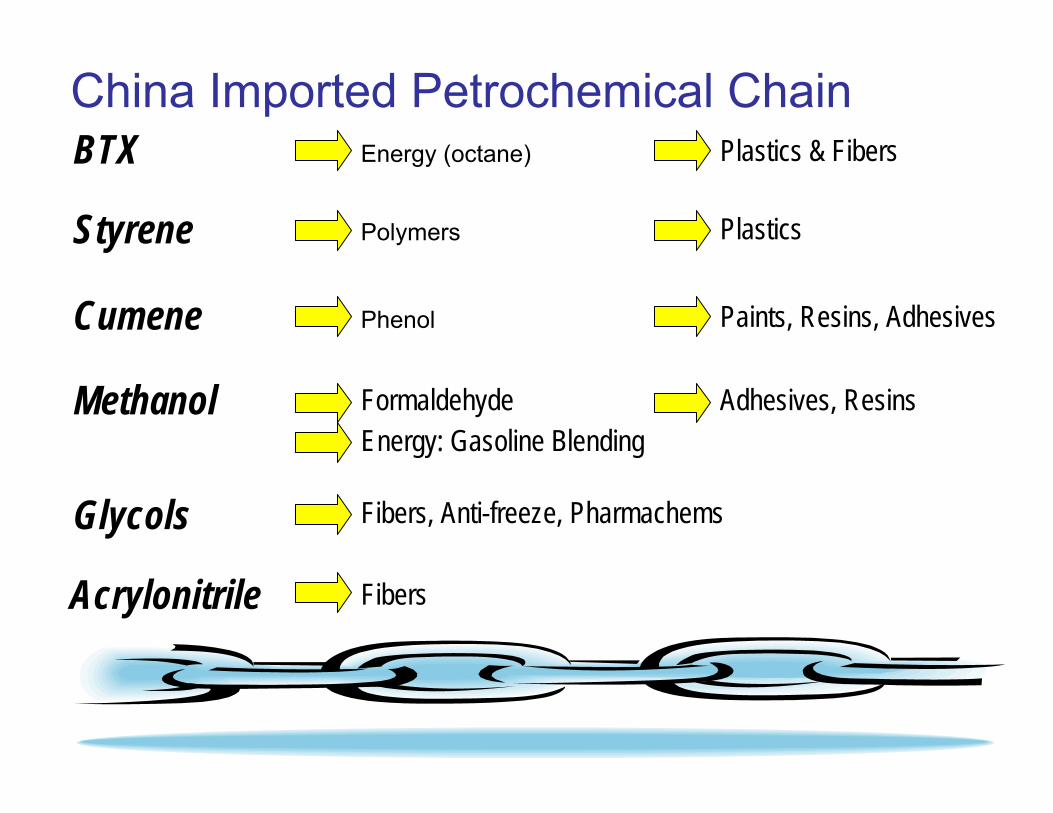

China Imported Petrochemical Chain

Glycols Fibers, Anti-freeze, Pharmachems

Acrylonitrile Fibers

Methanol Formaldehyde Adhesives, ResinsEnergy: Gasoline Blending

BTX Plastics & FibersEnergy (octane)

Styrene PlasticsPolymers

Cumene Paints, Resins, AdhesivesPhenol

China Chemical Production & Export Chain Plastics & Fibers Automotive production

Everyday consumer goodsFurnitureClothing

Resins & Adhesives Housing materialsManufacture of PlywoodPaints

Pharmachems PharmaceuticalsHealth & Beauty Aids

Caustic Soda AluminumPaper

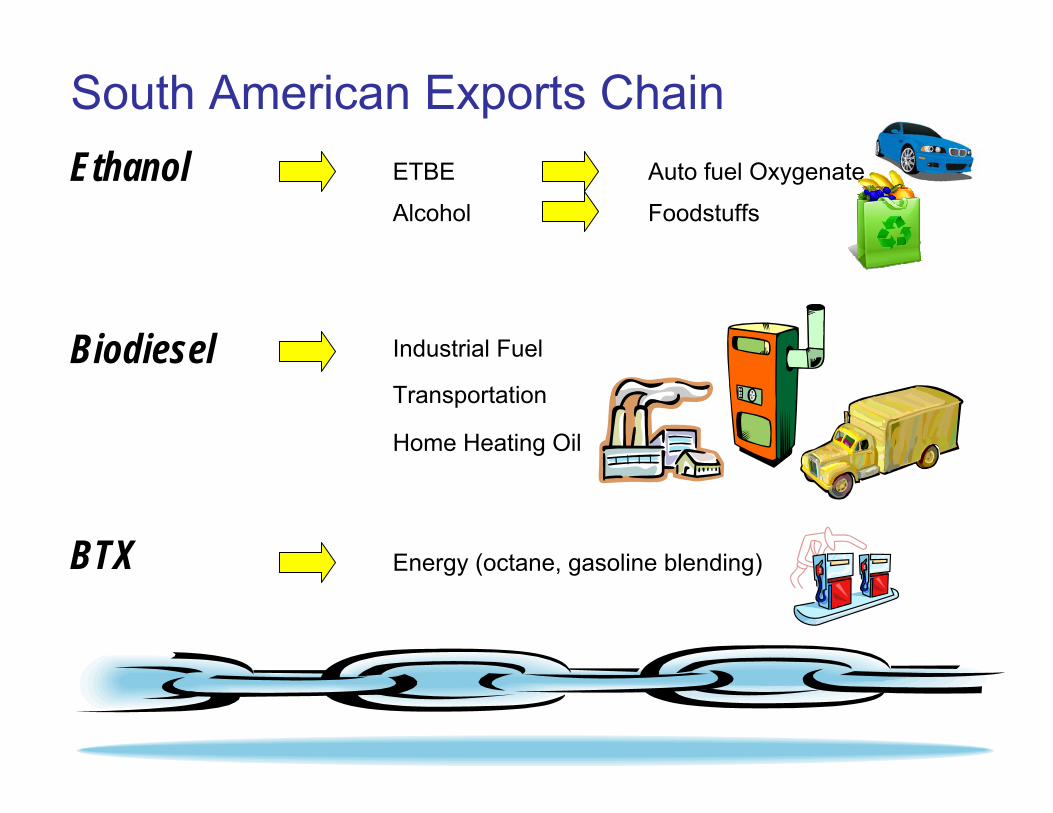

South American Import Chain

Lubricating Oils Industrial & Automotive

Inorganic Acid Fertilizer

Acetyls

Acrylates

Styrene Plastics

GlycolsFibers

South American Exports Chain Ethanol ETBE

Alcohol

Auto fuel Oxygenate

Foodstuffs

Biodiesel Industrial Fuel

Transportation

Home Heating Oil

BTX Energy (octane, gasoline blending)

The Chemical Tanker TradeWhere are we today ?Where are we going ?

Supply vs. Demand Paradigm • Tonnage Supply vs. Demand for Freight:

−Supply:

IMO II classification of vegoils

Vessel and operator quality control

Significant new order book

−Demand: The World is Flat – Thomas L. Friedman

World-flattening events create a global market place

Going Green – ethanol and biodiesel

Economic volatility in developed economies

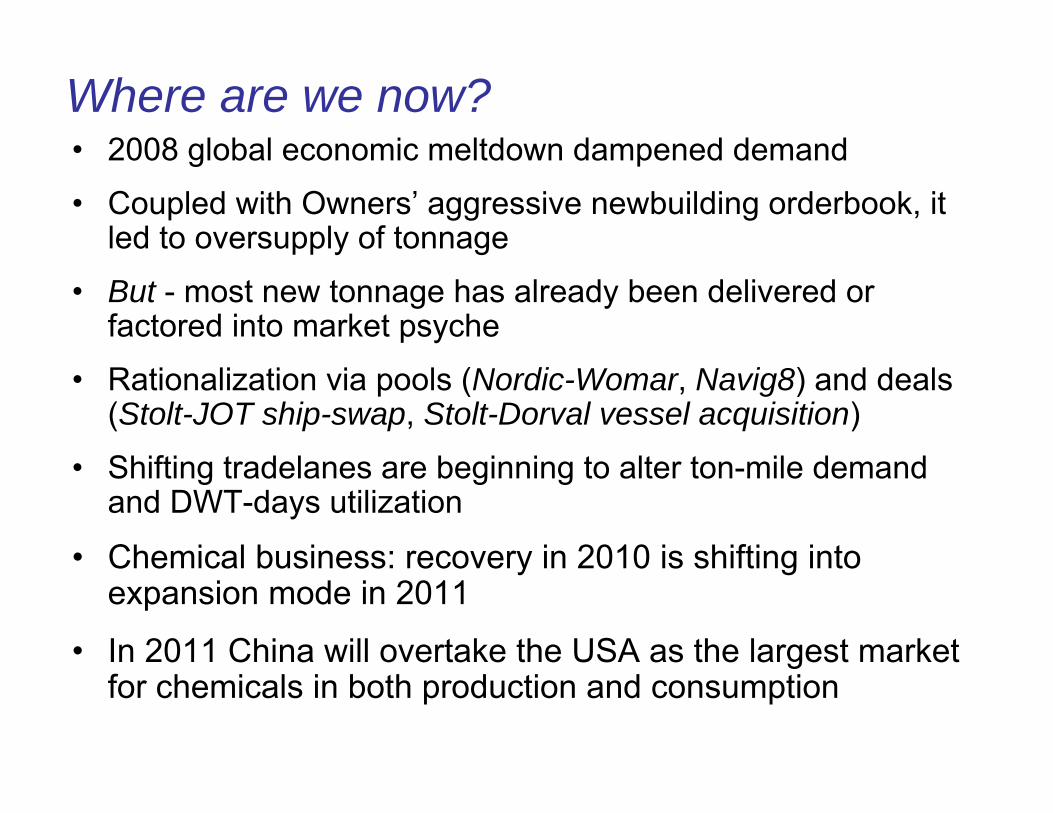

Where are we now? • 2008 global economic meltdown dampened demand

• Coupled with Owners’ aggressive newbuilding orderbook, it led to oversupply of tonnage

• But - most new tonnage has already been delivered or factored into market psyche

• Rationalization via pools (Nordic-Womar, Navig8) and deals (Stolt-JOT ship-swap, Stolt-Dorval vessel acquisition)

• Shifting tradelanes are beginning to alter ton-mile demand and DWT-days utilization

• Chemical business: recovery in 2010 is shifting into expansion mode in 2011

• In 2011 China will overtake the USA as the largest market for chemicals in both production and consumption

Chemical Tanker Demand by Tradelane(In millions of metric tons)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

N Am

erica

to N

Asia

N Asia

to th

e Am

erica

sSE

Asia

to U

SA

Asia to

Eur

ope (

Chem

s)

Asia to

Eur

ope (

Veg)

Amer

icas

to E

urop

e

Euro

pe to

the A

mer

icas

Intra

-Amer

icas

USA to

Afri

ca &

Indi

an O

ean

Euro

pe to

Nor

th A

siaME G

ulf t

o USA

ME Gul

f to

Europ

e

ME Gul

f to

North

Asia

ME Gul

f to

Indi

an S

ubco

ntME G

ulf t

o SE

Asia

Major Trade Route

Mill

ions

MTs 2008

2012

Source: Richardson Lawrie Associates

Total worldwide demand 2008 – 87.7MTotal worldwide demand 2008 – 87.7M

Total worldwide demand 2012 – 105.2MTotal worldwide demand 2012 – 105.2M

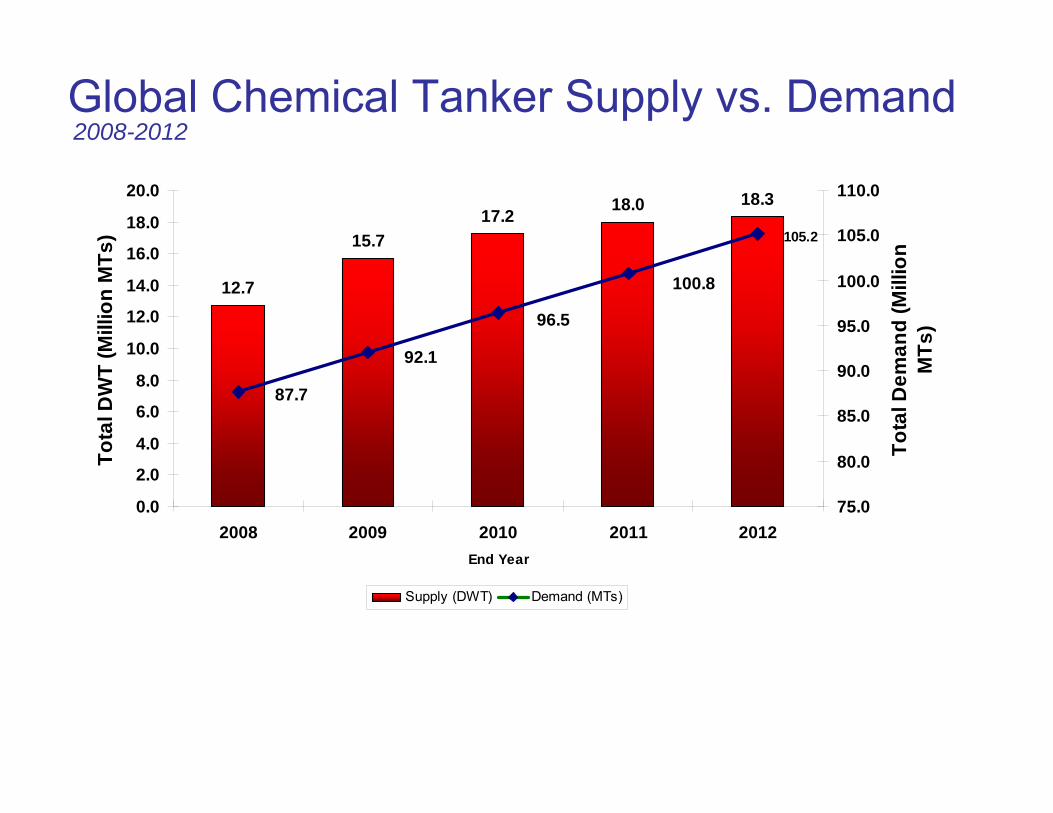

12.7

15.717.2 18.0 18.3

87.7

92.1

96.5

100.8

105.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2008 2009 2010 2011 2012End Year

Tota

l DW

T (M

illio

n M

Ts)

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

Tota

l Dem

and

(Mill

ion

MTs

)

Supply (DWT) Demand (MTs)

Global Chemical Tanker Supply vs. Demand2008-2012

Year on Year Percentage Change

-3.3%

+5.1%

+5.4%

+8.8%

+7.7%

+8.4%

+12.2%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2008 2009 2010 2011 2012

Cum

ulat

ive

Perc

enta

ge C

hang

e vs

200

8 (G

loba

l) or

200

9 (E

mer

ging

Mar

kets

)

Global Chemical Production Emerging Markets Chemical Production

Where are we going ?Chemical Production Growth 2008-2012

• Middle East chemical production expansion projects

• Chemical sector is a cyclical business – ACC sees a potential “supercycle” in certain products and regions

• Economic recovery, driven by emerging markets and tight chemical supply/demand balances, will boost profitability

• The BRIC factor – Brazil, Russia, India & China – are the primary growth economies

• Korea, Taiwan & Singapore also show promise

• 2012 tonnage supply steady – or- declining due to age related vessel removal

Where are we going?

Outlook for the global chemical sector is positive.Are we headed for a longer and stronger peak?

Outlook for the global chemical sector is positive.Outlook for the global chemical sector is positive.Are we headed for a longer and stronger peak?Are we headed for a longer and stronger peak?

Sources for the data presented herein include:

• American Chemistry Council

• Clarksons

• Eastport Maritime

• Quincannon Associates

• Richardson Lawrie Associates

• Simpson, Spence & Young

• Sound Tanker Chartering

Acknowledgements

Thank you for your time today!Thank you for your time today!Thank you for your time today!

![[BLT] 특허권의내용과명세서의이해_김성현_20160824_v2](https://static.fdocument.pub/doc/165x107/58735df41a28abe7648b4f7b/blt-20160824v2-58bd808549376.jpg)

![[Blt] 2014년 정부지원사업12월](https://static.fdocument.pub/doc/165x107/559cebdc1a28ab2b708b4788/blt-2014-12.jpg)

![[BLT] 창업과 지식재산](https://static.fdocument.pub/doc/165x107/5592e7321a28ab1f698b4701/blt-5592e7321a28ab1f698b4701.jpg)

![[BLT] 브랜드 네이밍 사례 - BLT 브랜드 네이밍 연구소 (엄정한 변리사)](https://static.fdocument.pub/doc/165x107/58a3fc3b1a28ab64528b57fd/blt-blt-.jpg)

![[BLT] 지식재산권 기초강의](https://static.fdocument.pub/doc/165x107/557ef825d8b42ad17d8b5064/blt-557ef825d8b42ad17d8b5064.jpg)