The Future of Branding in the Food Industry - … Forum GIF/interventi/Casati.pdf · The Future of...

45

The Future of Branding in the Food Industry Gianfranco Casati September 16, 2011

Transcript of The Future of Branding in the Food Industry - … Forum GIF/interventi/Casati.pdf · The Future of...

The Future of Branding

in the Food Industry

Gianfranco Casati

September 16, 2011

2

Brand and Brand Value

Consumer

Trends

2 Case Examples

Agenda

3

A brand is a:

Promise, an expectation and

ultimately an experience

Declaration of the quality that

will be delivered

Marketplace differentiator

3

4

Strong brands

• Create lasting

impressions

• Reduce risk and

simplify decision

making

• Enable premium

pricing

5

Best Global Brands

• Investment and management of brand as a business asset with value

• Three brand value components:

− Financial performance

− Role of brand in decision making

− Brand strength

6

2010 Rank Company Brand Value ($m)

#1 Coca Cola 70,452

#23 Pepsi 14,061

#27 Nescafe 12,753

#35 Kellogg’s 11,041

#46 Heinz 7,534

#57 Nestle 6,548

#58 Danone 6,363

#61 Sprite 5,777

#97 Starbucks 3,339

#99 Campbell’s 3,241 6

Best Global Brands 2010

Brand Equity

7

Made in Italy who lived outside

The 221 high-quality Italian products protected by the EU recognition developed in 2010 a turnover of consumption over 9 billion of which approximately 1.5 billion realized on foreign markets through exports.

Made in Italy lived within

Almost half of Italians (47%) believe that a food made with products grown or reared entirely in Italy is worth at least 30% more. The superiority of Made in Italy food is given in the order:

to comply with tougher laws the goodness and freshness the guarantee of more controls.

Source: Coldiretti 2010.

8

Your tractor trailer pulls up once a week and delivers pizza dough and other food made somewhere else that only needs to be cooked or warmed up at your restaurant

Your menu is a never ending list of over-doing-it. Super sized,stuffed crust,meat lovers supreme,but buster specials that come in portions that could feed a large family…twice

You need to try way too hard to get approval from Italians because they would never eat in your restaurant and/or have never heard of the dishes you’re claiming are Italian

You use ingredients that can’t be pronounced in an effort to enhance taste and preserve “shelf-life”

Your recipes were developed in a laboratory by chefs with chemistry degrees

5 clues that your food is not authentic Italian:

1

2

4

5

3

Source: Italyville 2009.

FAKE ITALIAN

REAL

SIZE

TASTE

SAFETY

TRADITION

9

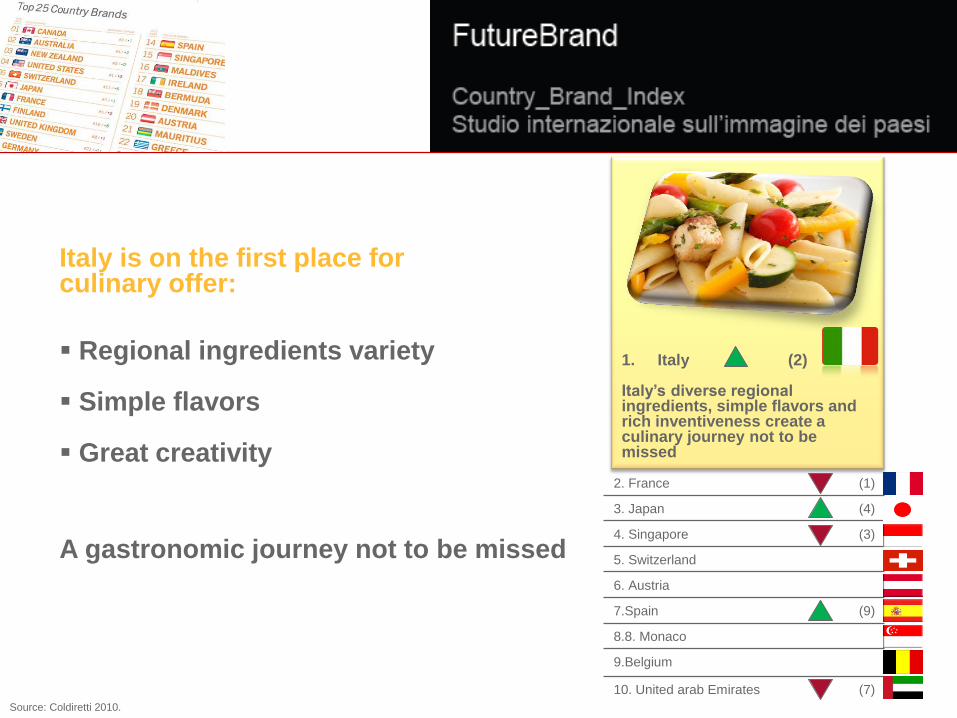

Italy is on the first place for culinary offer:

Regional ingredients variety Simple flavors Great creativity

A gastronomic journey not to be missed

1. Italy (2) Italy’s diverse regional ingredients, simple flavors and rich inventiveness create a culinary journey not to be missed

2. France (1)

3. Japan (4)

4. Singapore (3)

5. Switzerland

6. Austria

7.Spain (9)

8.8. Monaco

9.Belgium

10. United arab Emirates (7)

Source: Coldiretti 2010.

10

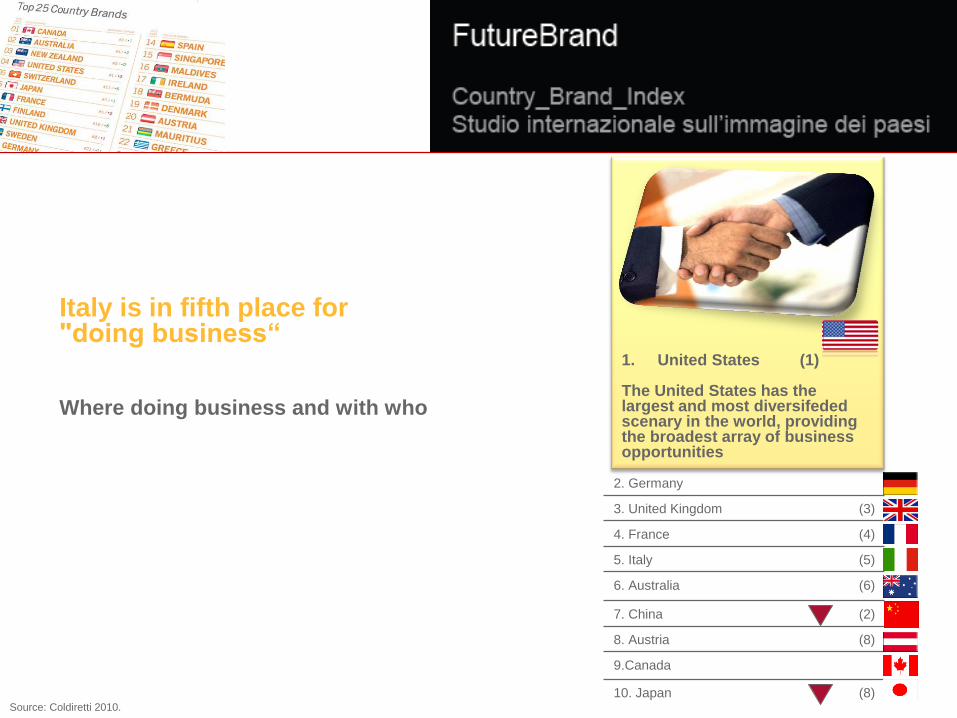

Italy is in fifth place for "doing business“ Where doing business and with who

1. United States (1) The United States has the largest and most diversifeded scenary in the world, providing the broadest array of business opportunities

2. Germany

3. United Kingdom (3)

4. France (4)

5. Italy (5)

6. Australia (6)

7. China (2)

8. Austria (8)

9.Canada

10. Japan (8) Source: Coldiretti 2010.

Copyright © 2011 Accenture All Rights Reserved.

Consumer power

11

12

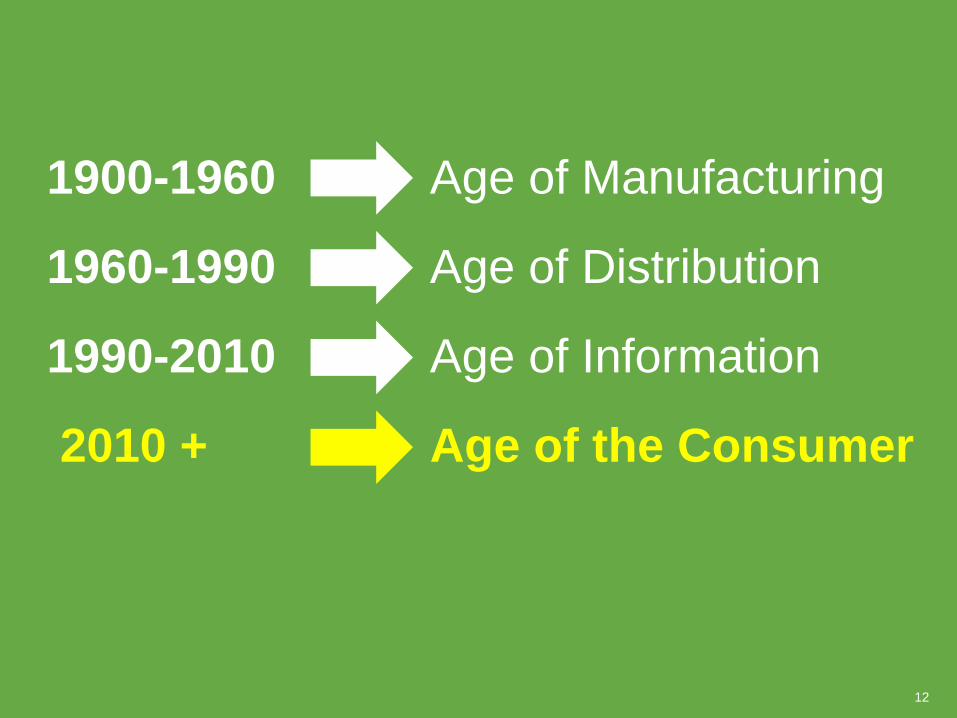

1900-1960 Age of Manufacturing

1960-1990 Age of Distribution

1990-2010 Age of Information

2010 + Age of the Consumer

13

The focus on the

consumer now matters

more than any other

strategic initiative

2011 Forrester Research,

Competitive Strategy In the

Age of the Consumer

14

Consumers want

things faster, better,

cheaper – with a

higher degree of

service

2011 Forrester Research,

Competitive Strategy In the

Age of the Consumer

15

New generation of consumers

• Aging population

• Prioritize convenience

• Inundated with options

• Have more tools to

research price, quality

and availability

15

16

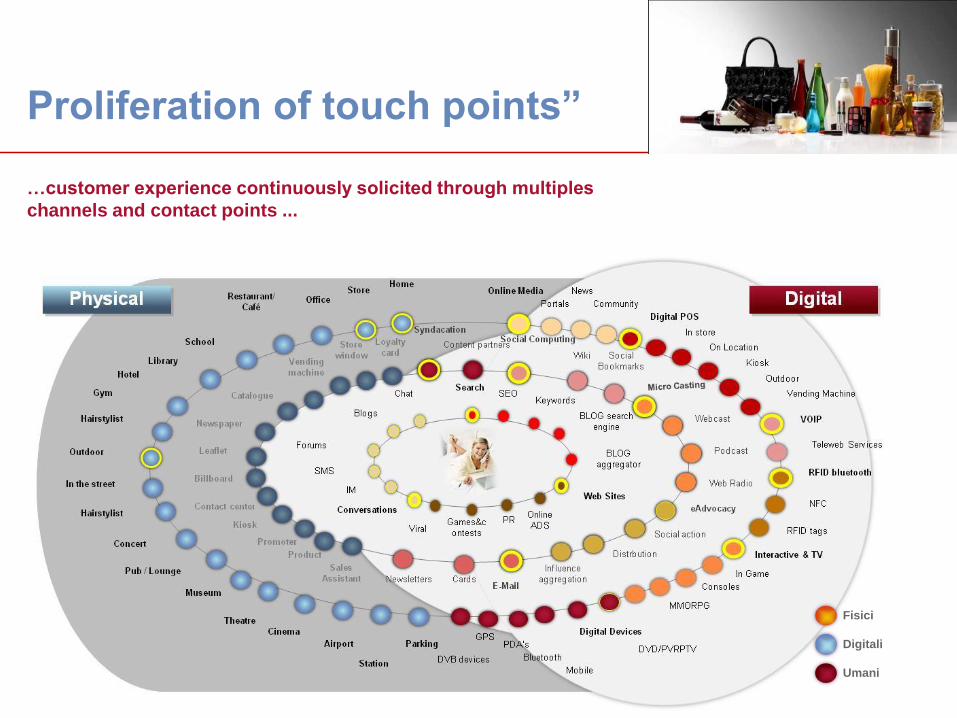

Proliferation of touch points”

…customer experience continuously solicited through multiples

channels and contact points ...

Umani

Digitali

Fisici

Copyright © 2011 Accenture All Rights Reserved.

Trends

17

18

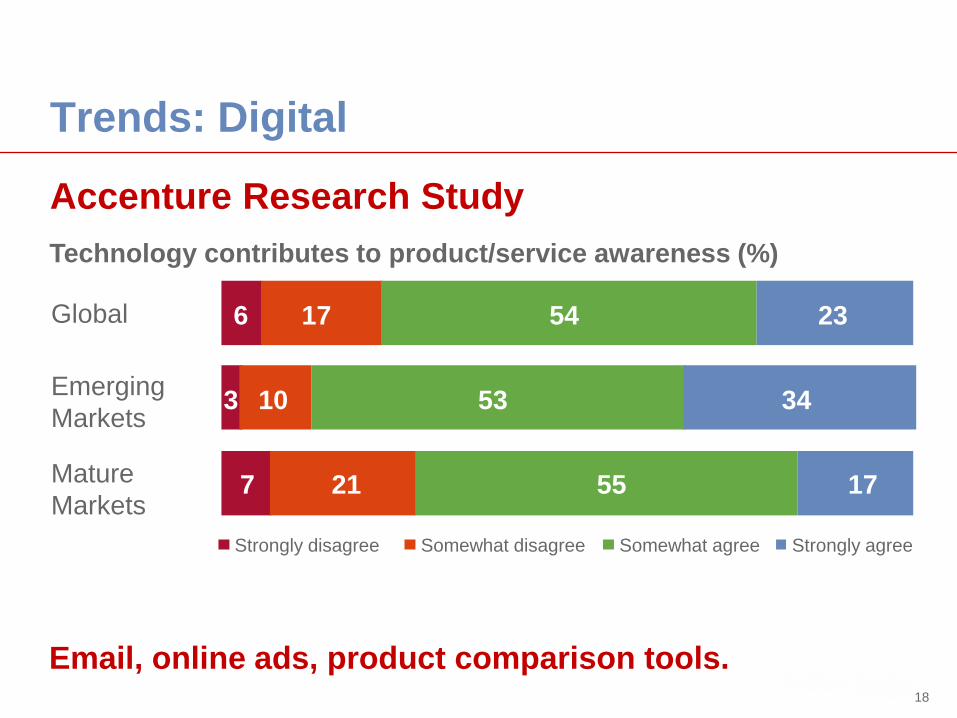

Trends: Digital

6 17 54 23 Global

Emerging

Markets

Mature

Markets

Technology contributes to product/service awareness (%)

Strongly disagree Somewhat disagree Somewhat agree Strongly agree

7 21 55 17

3 10 53 34

Accenture Research Study

Email, online ads, product comparison tools.

19

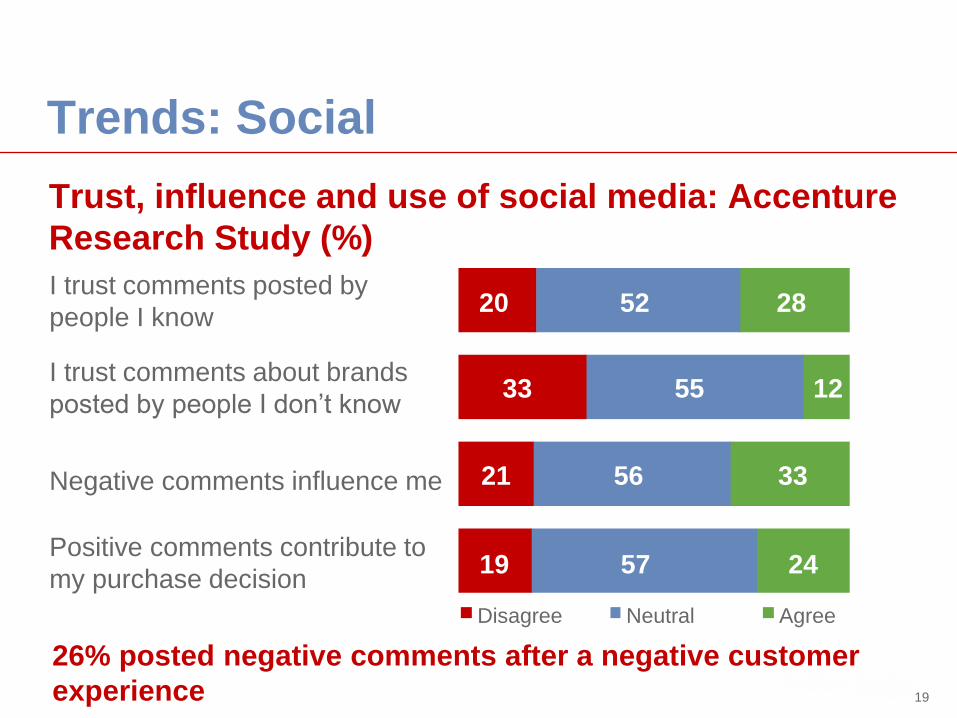

Trends: Social

Trust, influence and use of social media: Accenture

Research Study (%)

I trust comments posted by

people I know

I trust comments about brands

posted by people I don’t know

Negative comments influence me

Positive comments contribute to

my purchase decision

Disagree Neutral Agree

26% posted negative comments after a negative customer

experience

20

33

21

19

52

55

56

57

28

12

33

24

20

Trends: Social

• Purchasing habits driven by tapping into

networks of friends, fans and followers

• Dramatically accelerates exchange of

customer opinion

• Four areas influence behavior:

- Discovery

- Ratings

- Feedback

- Together

21

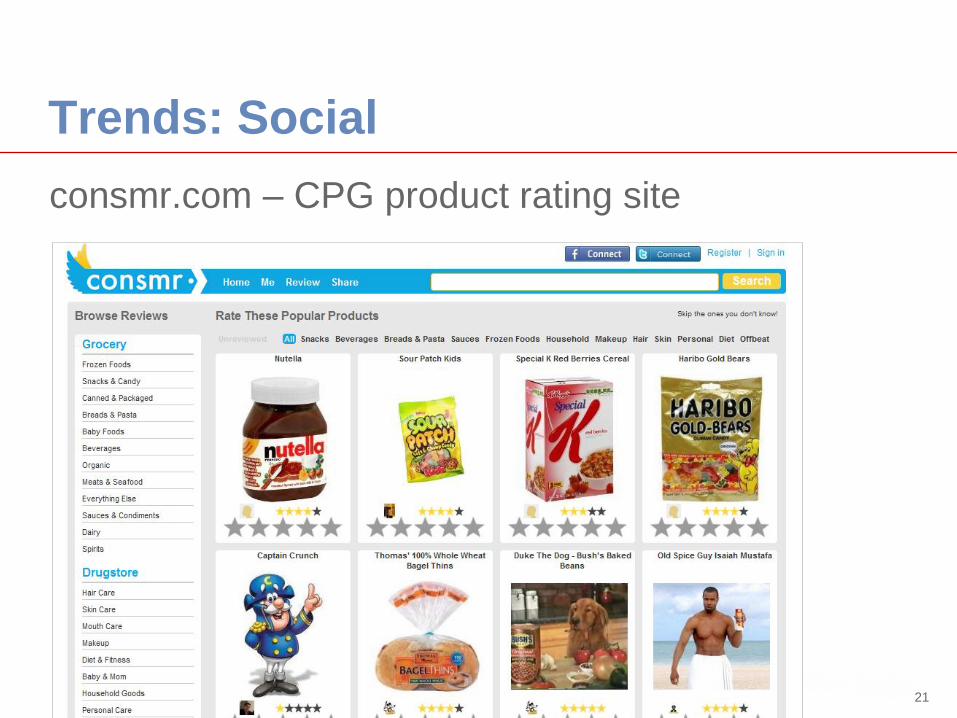

Trends: Social

consmr.com – CPG product rating site

22

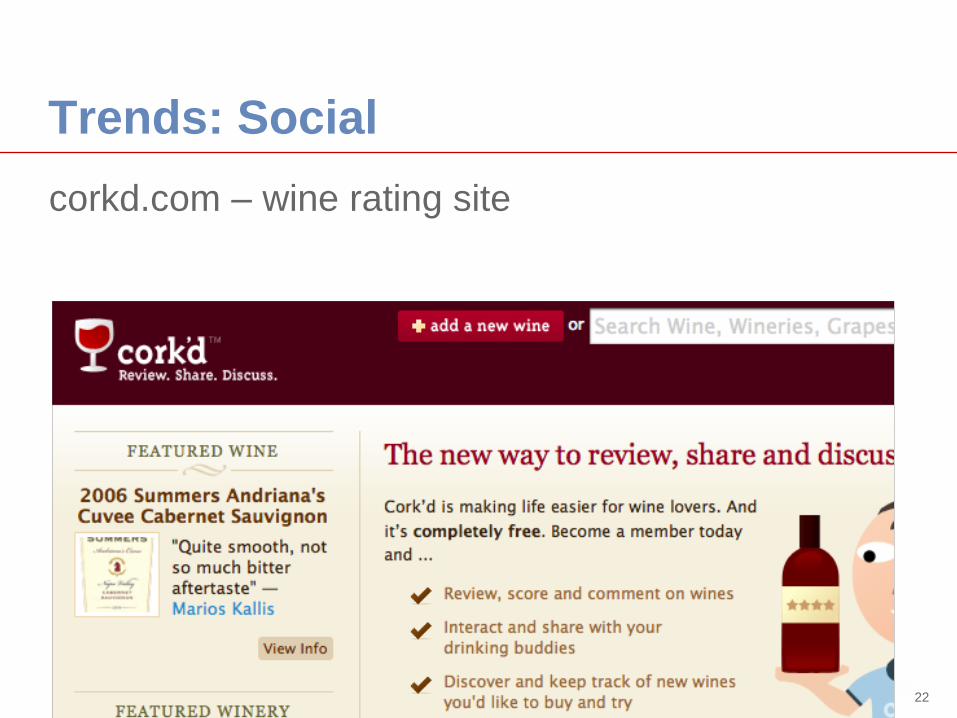

Trends: Social

corkd.com – wine rating site

23

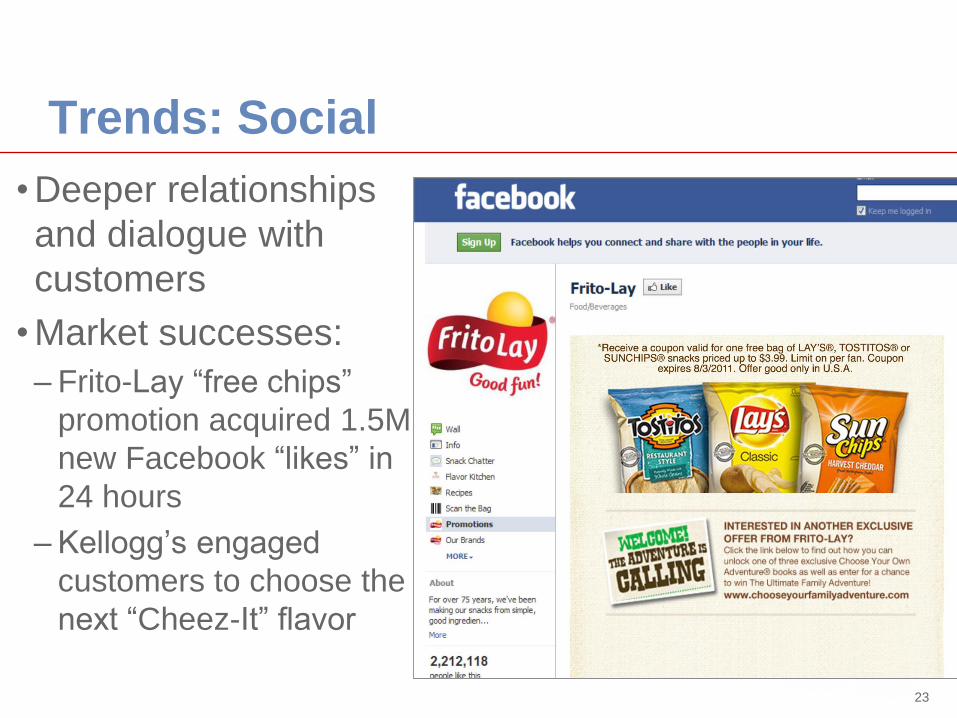

Trends: Social

• Deeper relationships

and dialogue with

customers

• Market successes:

– Frito-Lay “free chips”

promotion acquired 1.5M

new Facebook “likes” in

24 hours

– Kellogg’s engaged

customers to choose the

next “Cheez-It” flavor

24

Trends: Mobile

• Delivers convenient price comparison in-store vs. online

• Provides retailers new order opportunities for mobile consumers

• Ocado app in UK generated: – 2% of retailer’s sales in

Feb. 2010

– 6% in May 2010

– Presently > 10%

25

Trends: Cross-boarder e-commerce

• Pent-up demand in markets where products are

not available

• Consumers want latest trends − from internet,

magazines, movies

• Increasingly willing to buy items from websites

outside their home country

• Retailers launch online in new markets to test

waters before opening stores

26

Trends: Now-or-never commerce

Flash sale sites like Groupon

- General Mills was the first CPG company to run a daily deal

in April 2011 – to encourage trial and sampling

- "Groupon Now” allows

customers to view

real-time deals in their

current vicinity.

- Could supermarkets

be next to offer deals

on major branded

foods and beverages?

26

2 Case Examples

27

The world’s most extensive study on

brands

•Over 750,000 respondents

•50,000 brands across 200 categories

•18 years of data

•72 brand metrics

•51 countries

BrandAsset® Valuator (Y&R)

28

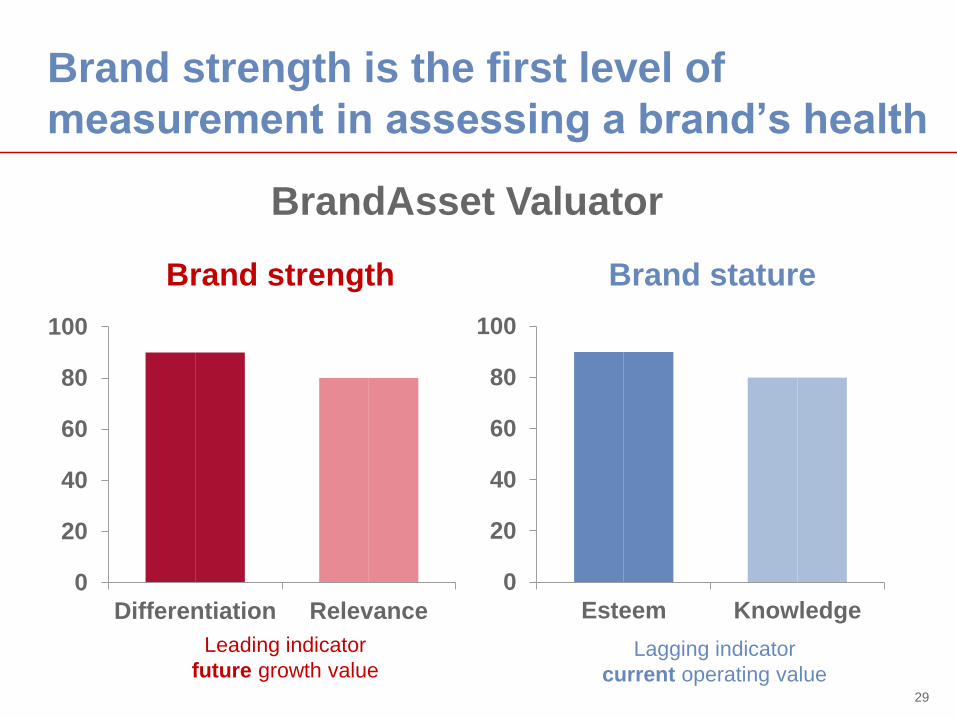

0

20

40

60

80

100

Differentiation Relevance

0

20

40

60

80

100

Esteem Knowledge

Brand strength is the first level of

measurement in assessing a brand’s health

29

BrandAsset Valuator

Brand strength Brand stature

Leading indicator

future growth value Lagging indicator

current operating value

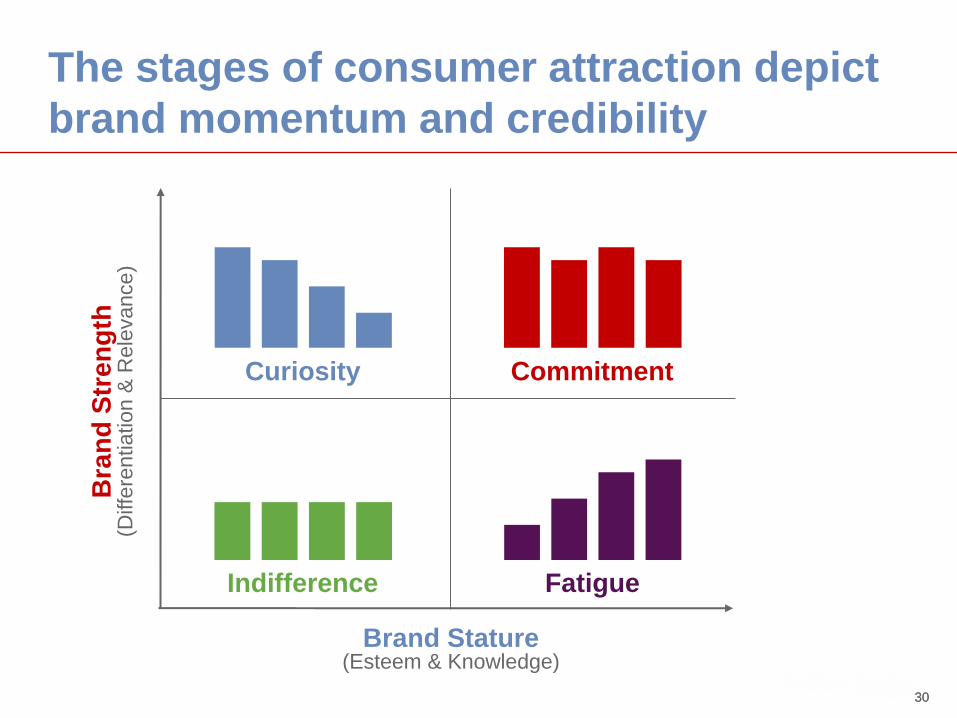

30

The stages of consumer attraction depict

brand momentum and credibility

30

Bra

nd

Str

en

gth

(D

iffe

rentia

tion &

Rele

vance)

Curiosity Commitment

Indifference Fatigue

Brand Stature (Esteem & Knowledge)

Key consumer and business metrics

•Pricing power

•Usage and preference

•Loyalty

•Social currency

• Intangible value

creation

BrandAsset Valuator metrics

relate to marketplace performance

31

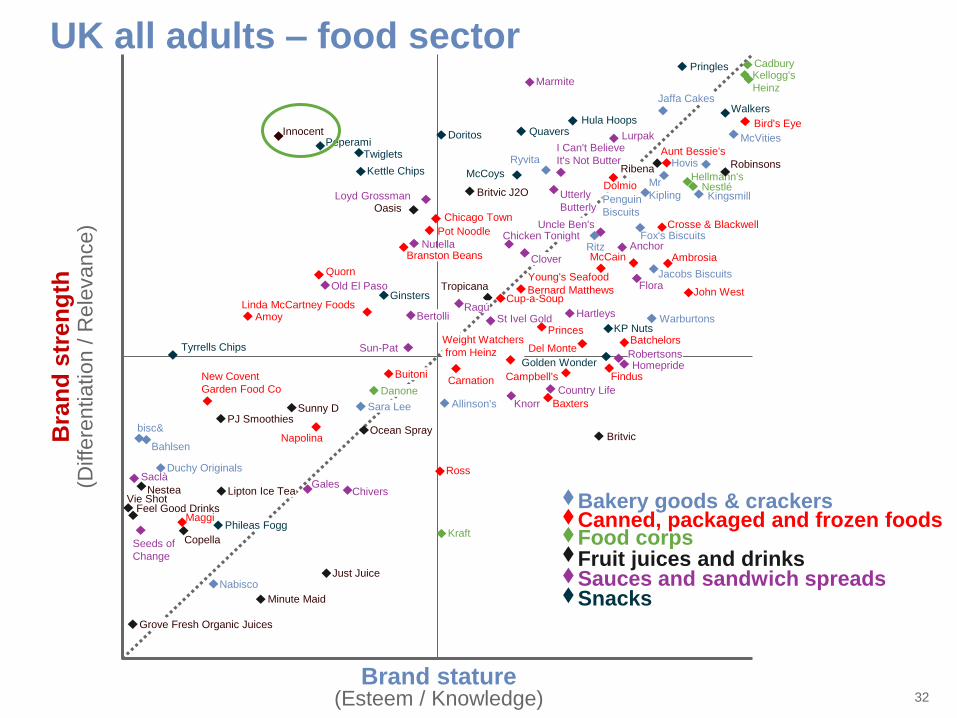

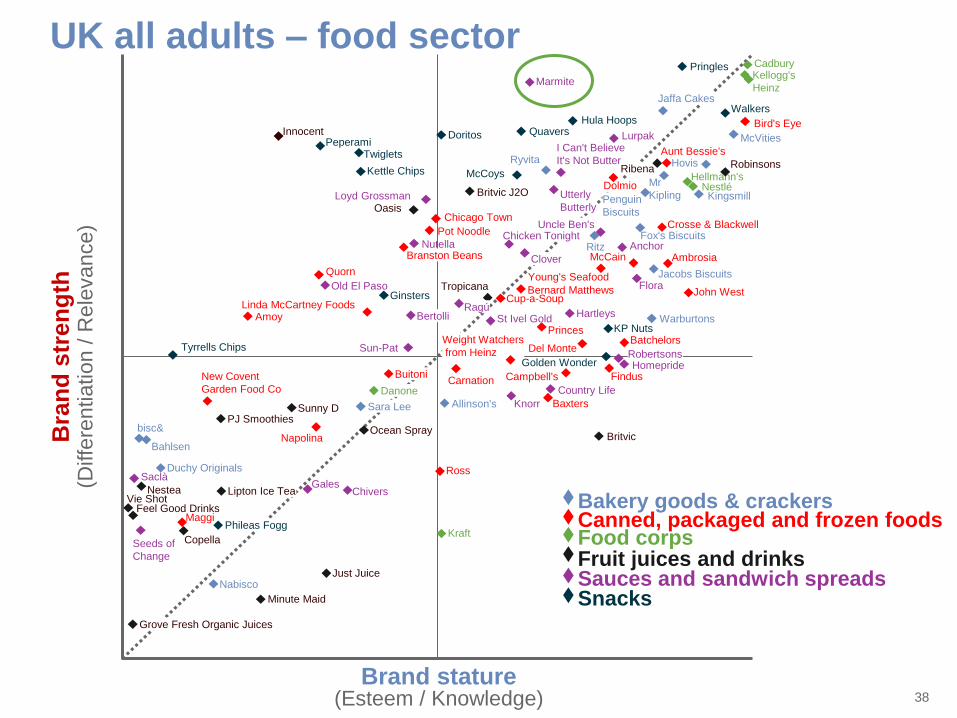

UK all adults – food sector

Food corps

Bakery goods & crackers

Fruit juices and drinks

Canned, packaged and frozen foods

Sauces and sandwich spreads Snacks

Bra

nd

str

en

gth

(D

iffe

ren

tiation

/ R

ele

van

ce)

Brand stature (Esteem / Knowledge)

Cadbury

Danone

Heinz

Hellmann's

Kellogg's

Kraft

Nestlé

Allinson's

Bahlsen

bisc&

Duchy Originals

Fox's Biscuits

Hovis

Jacobs Biscuits

Jaffa Cakes

Kingsmill

McVities

Nabisco

Penguin

Biscuits

Ritz

Ryvita

Sara Lee

Warburtons

Mr

Kipling

Britvic

Britvic J2O

Copella

Feel Good Drinks

Grove Fresh Organic Juices

Innocent

Just Juice

Lipton Ice Tea

Minute Maid

Nestea

Oasis

Ocean Spray PJ Smoothies

Ribena Robinsons

Sunny D

Tropicana

Vie Shot

Anchor

Bertolli

Chicken Tonight

Chivers

Clover

Country Life

Flora

Gales

Hartleys

Homepride

I Can't Believe

It's Not Butter

Knorr

Loyd Grossman

Lurpak

Marmite

Nutella

Old El Paso

Ragú

Robertsons

Seeds of

Change

St Ivel Gold

Sun-Pat

Uncle Ben's

Utterly

Butterly

Saclà

Ambrosia

Amoy

Aunt Bessie's

Batchelors

Baxters

Bernard Matthews

Bird's Eye

Branston Beans

Campbell's Carnation

Chicago Town Crosse & Blackwell

Cup-a-Soup

Findus

John West

Linda McCartney Foods

Maggi

McCain

Napolina

New Covent

Garden Food Co

Pot Noodle

Princes

Quorn

Ross

Weight Watchers

from Heinz

Young's Seafood

Buitoni

Dolmio

Del Monte

Doritos

Ginsters

Golden Wonder

Hula Hoops

Kettle Chips

KP Nuts

McCoys

Peperami

Phileas Fogg

Pringles

Quavers

Twiglets

Tyrrells Chips

Walkers

32

•Created its own category

of smoothies

•Fun and different brand

•Unique marketing efforts

and social events

− New packaging and flavors

− The Big Knit, Village Fete,

Hungry Grassy Van

− Recipe books

33 33

Bra

nd

str

en

gth

(D

iffe

rentia

tion /

Rele

vance

)

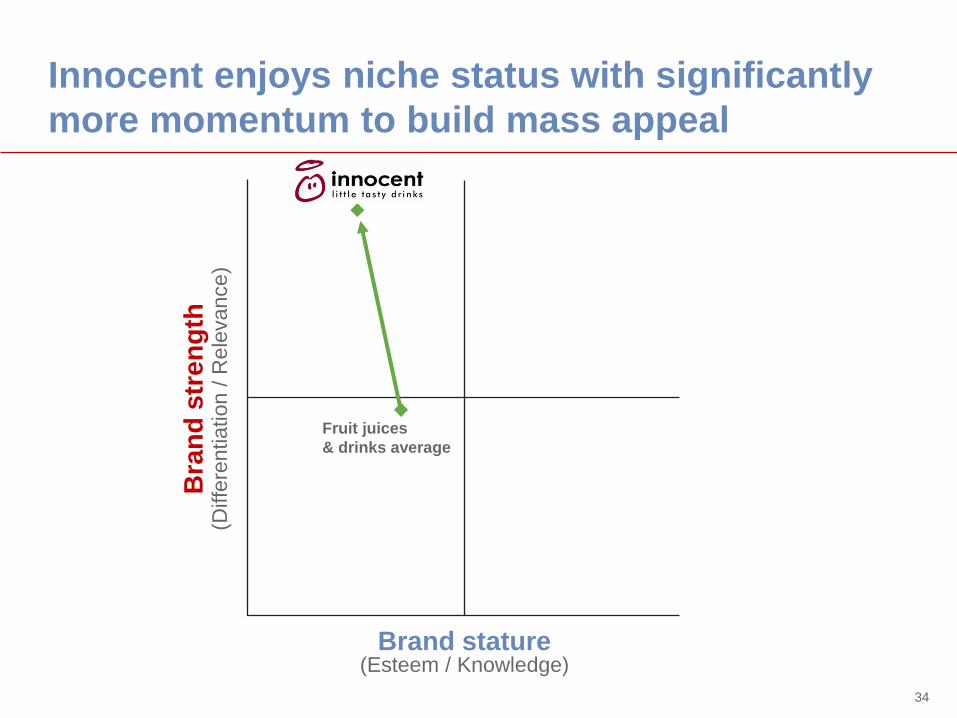

Innocent enjoys niche status with significantly

more momentum to build mass appeal

34

Fruit juices

& drinks average

Brand stature (Esteem / Knowledge)

35

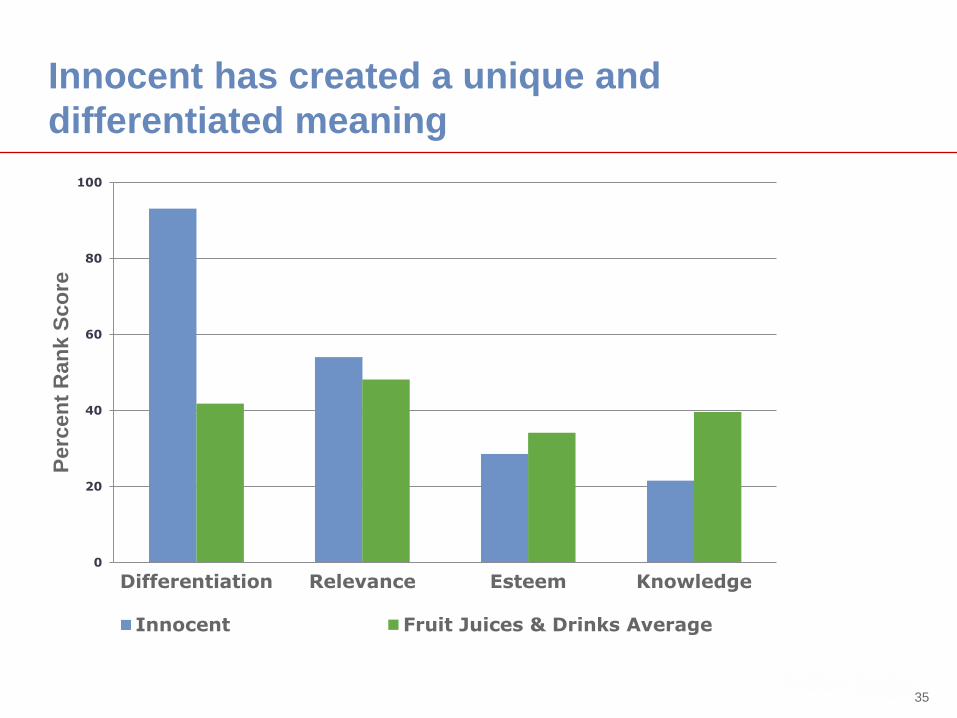

Innocent has created a unique and

differentiated meaning

0

20

40

60

80

100

Differentiation Relevance Esteem Knowledge

Perc

en

t R

an

k S

co

re

Innocent (drinks) Fruit Juices & Drinks Average

36

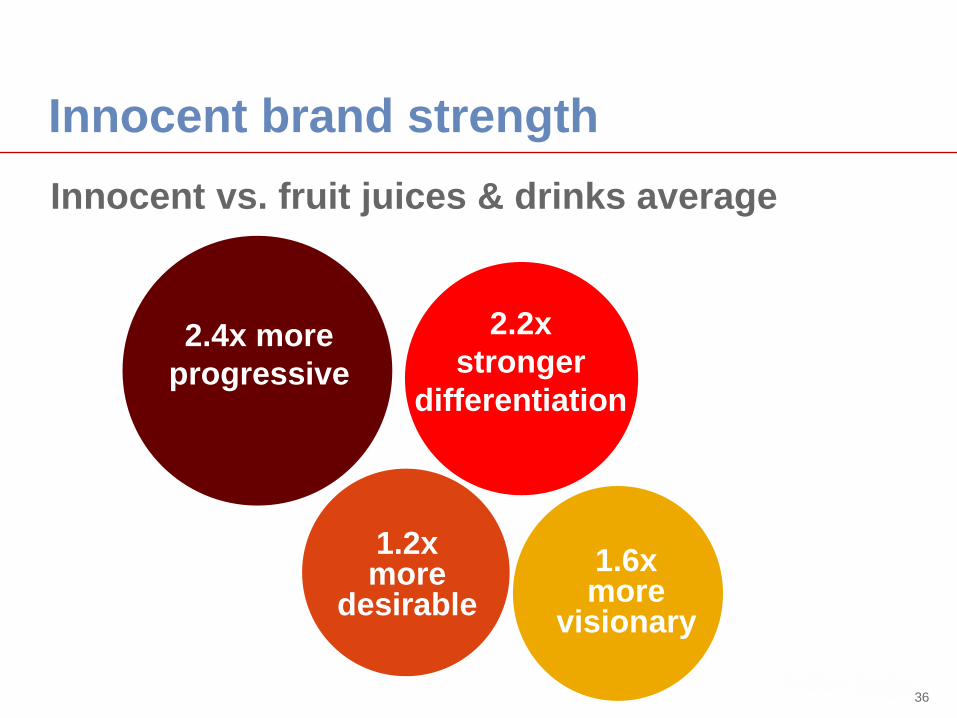

Innocent brand strength

Innocent vs. fruit juices & drinks average

2.4x more

progressive

2.2x

stronger

differentiation

1.6x more

visionary

1.2x more

desirable

Fruit Juices & Drinks Category Average

Innocent

indexed t

o c

ate

gory

avera

ge

Ind

ex

vs. C

ate

go

ry

Category average (%)

Different

Distinctive

Unique

Dynamic

Innovative

Leader

Reliable

High quality Arrogant

Authentic Best Brand

Carefree

Cares Customers

Charming

Daring Down to Earth

Energetic

Friendly Fun

Gaining In Popularity

Glamorous

Good Value

Healthy

Helpful

High Performance

Independent

Intelligent

Kind

Obliging

Original

Prestigious

Progressive

Restrained

Rugged

Sensuous

Simple Social

Straightforward

Stylish

Traditional

Trendy

Trustworthy

Unapproachable

Up To Date

Upper Class

Visionary

Worth More

20

40

60

80

100

120

140

160

180

200

220

240

260

280

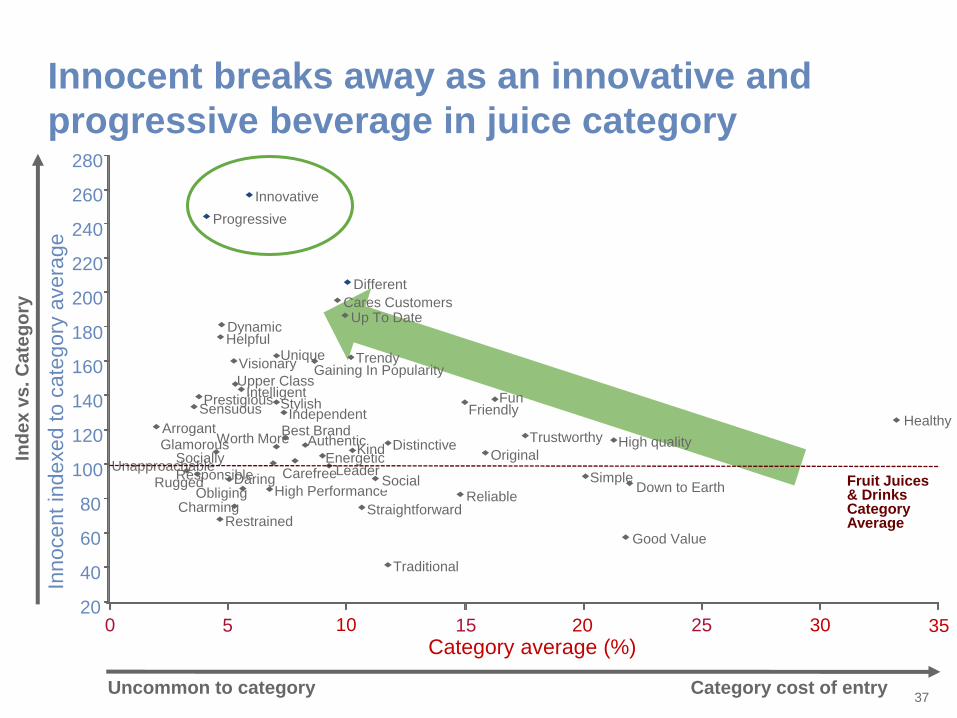

0 5 10 15 20 25 30

Socially

Responsible

Innocent breaks away as an innovative and

progressive beverage in juice category

37

35

Category cost of entry Uncommon to category

UK all adults – food sector

Food corps

Bakery goods & crackers

Fruit juices and drinks

Canned, packaged and frozen foods

Sauces and sandwich spreads Snacks

Bra

nd

str

en

gth

(D

iffe

ren

tiation

/ R

ele

van

ce)

Brand stature (Esteem / Knowledge)

Cadbury

Danone

Heinz

Hellmann's

Kellogg's

Kraft

Nestlé

Allinson's

Bahlsen

bisc&

Duchy Originals

Fox's Biscuits

Hovis

Jacobs Biscuits

Jaffa Cakes

Kingsmill

McVities

Nabisco

Penguin

Biscuits

Ritz

Ryvita

Sara Lee

Warburtons

Mr

Kipling

Britvic

Britvic J2O

Copella

Feel Good Drinks

Grove Fresh Organic Juices

Innocent

Just Juice

Lipton Ice Tea

Minute Maid

Nestea

Oasis

Ocean Spray PJ Smoothies

Ribena Robinsons

Sunny D

Tropicana

Vie Shot

Anchor

Bertolli

Chicken Tonight

Chivers

Clover

Country Life

Flora

Gales

Hartleys

Homepride

I Can't Believe

It's Not Butter

Knorr

Loyd Grossman

Lurpak

Marmite

Nutella

Old El Paso

Ragú

Robertsons

Seeds of

Change

St Ivel Gold

Sun-Pat

Uncle Ben's

Utterly

Butterly

Saclà

Ambrosia

Amoy

Aunt Bessie's

Batchelors

Baxters

Bernard Matthews

Bird's Eye

Branston Beans

Campbell's Carnation

Chicago Town Crosse & Blackwell

Cup-a-Soup

Findus

John West

Linda McCartney Foods

Maggi

McCain

Napolina

New Covent

Garden Food Co

Pot Noodle

Princes

Quorn

Ross

Weight Watchers

from Heinz

Young's Seafood

Buitoni

Dolmio

Del Monte

Doritos

Ginsters

Golden Wonder

Hula Hoops

Kettle Chips

KP Nuts

McCoys

Peperami

Phileas Fogg

Pringles

Quavers

Twiglets

Tyrrells Chips

Walkers

38

•Savory spread invented in the late 1800s

• “The growing up

spread you never

grow out of”

•Quirky communications

– Love It or Hate It

Campaign

– Marmarati Campaign:

Portrays Marmite fans as

an exclusive, desirable

segment to belong to

39

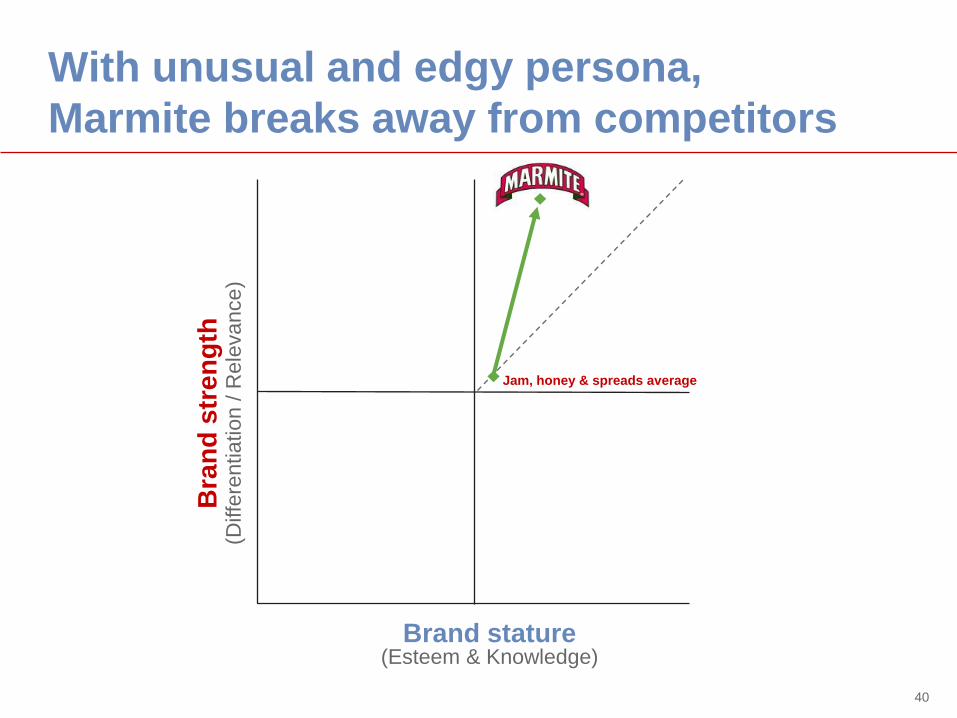

With unusual and edgy persona,

Marmite breaks away from competitors

40

Jam, honey & spreads average

Bra

nd

str

en

gth

(D

iffe

rentia

tion /

Rele

vance

)

Brand stature (Esteem & Knowledge)

41

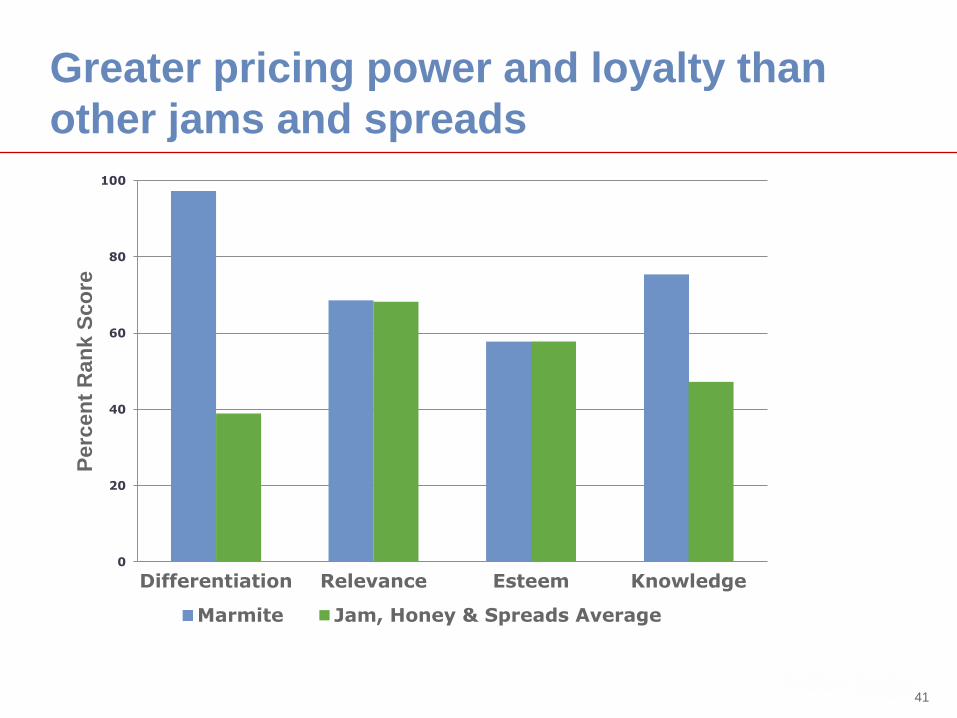

Greater pricing power and loyalty than

other jams and spreads

0

20

40

60

80

100

Differentiation Relevance Esteem Knowledge

Perc

en

t R

an

k S

co

re

Marmite Jam, Honey & Spreads Average

42

Marmite brand strength

Marmite vs. spreads average

1.5x greater

emotional

commitment

1.2x greater

pricing power

1.5x greater

behavioral

commitment

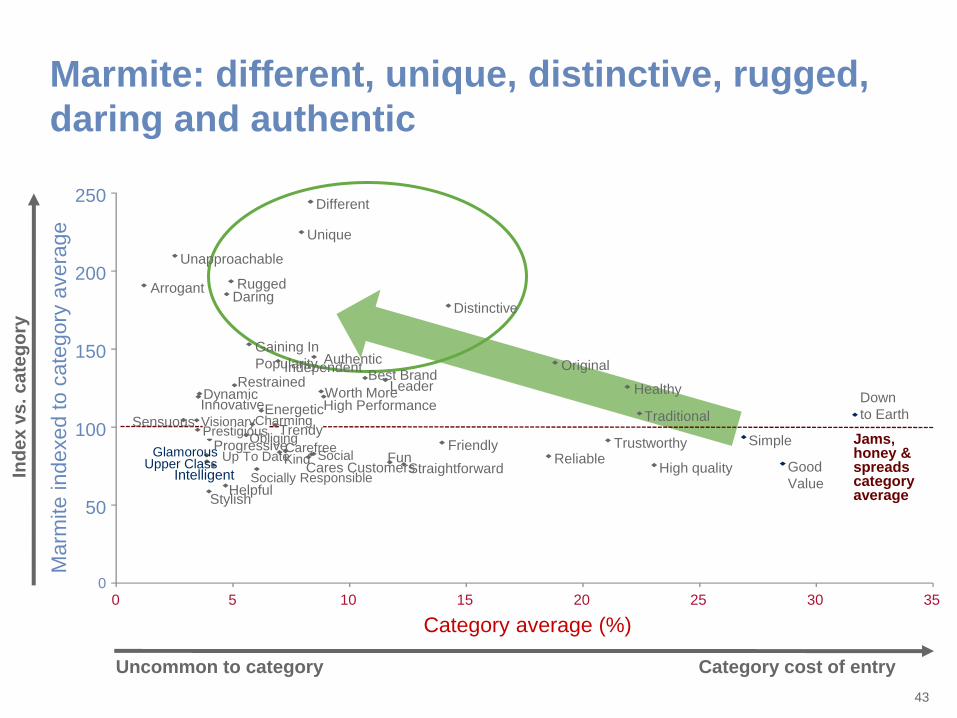

Marmite: different, unique, distinctive, rugged,

daring and authentic

Jams, honey & spreads category average

Marm

ite indexed t

o c

ate

gory

avera

ge

Ind

ex

vs. c

ate

go

ry

Category cost of entry Uncommon to category

Category average (%)

Different

Distinctive

Unique

Dynamic Innovative

Leader

Reliable High quality

Arrogant

Best Brand

Carefree

Cares Customers

Daring

Down

to Earth Energetic

Friendly Fun

Gaining In

Popularity

Glamorous Good

Value

Healthy

Helpful

High Performance

Independent

Intelligent Kind

Original

Prestigious Progressive

Restrained

Rugged

Sensuous

Simple Social

Socially Responsible Straightforward

Stylish

Traditional Trendy

Trustworthy

Unapproachable

Up To Date Upper Class

Visionary

Worth More

0

50

100

150

200

250

0 5 10 15 20 25 30 35

Authentic

Charming

Obliging

43

Habits, behaviuors

and values

44

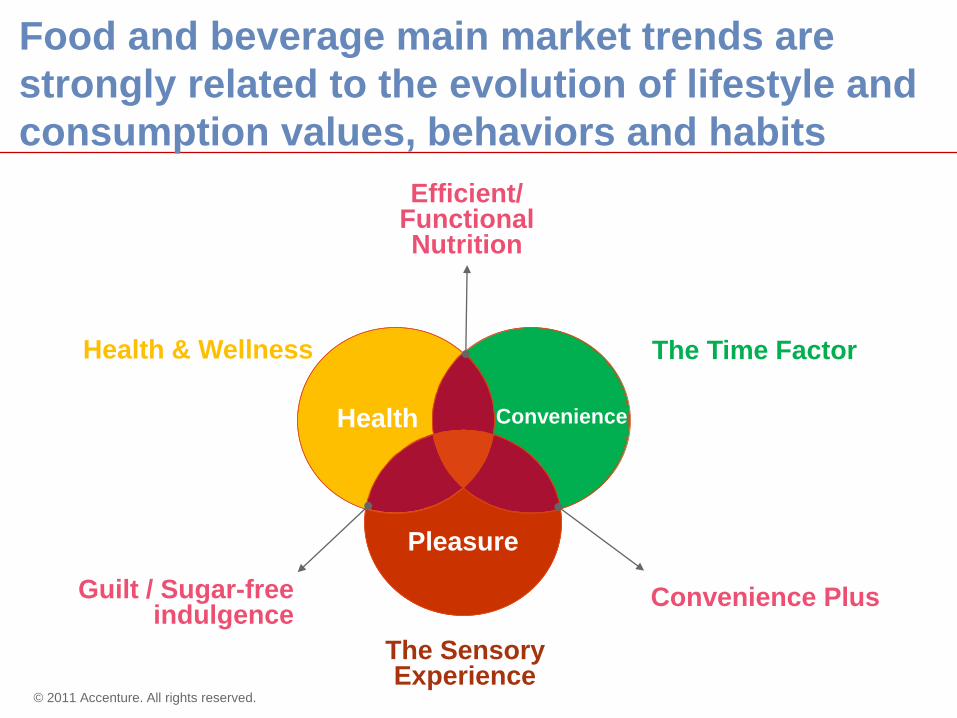

Food and beverage main market trends are

strongly related to the evolution of lifestyle and

consumption values, behaviors and habits

Pleasure

Health . Convenience

Efficient/ Functional Nutrition

The Sensory Experience

The Time Factor

Convenience Plus

Health & Wellness

Guilt / Sugar-free indulgence

© 2011 Accenture. All rights reserved.