Scott Pechstein – Why buying 3rd party is still the most efficient advertisement

38

Why buying 3rd party is still the most efficient advertisement Plus: How to engage the consumer in their preferred method of communication to increase engagement

-

Upload

sean-bradley -

Category

Automotive

-

view

132 -

download

0

Transcript of Scott Pechstein – Why buying 3rd party is still the most efficient advertisement

Why buying 3rd party is still the most efficient advertisement

Plus: How to engage the consumer in their preferred method of

communication to increase engagement

• How we gathered our results

• ROI of internet leads

• What is influencing buying behavior

• Best Practices (Phone, Email, Text, Chat)

• Mobile Opportunities

Topics

Copyright (c) 2014 Autobytel Inc.

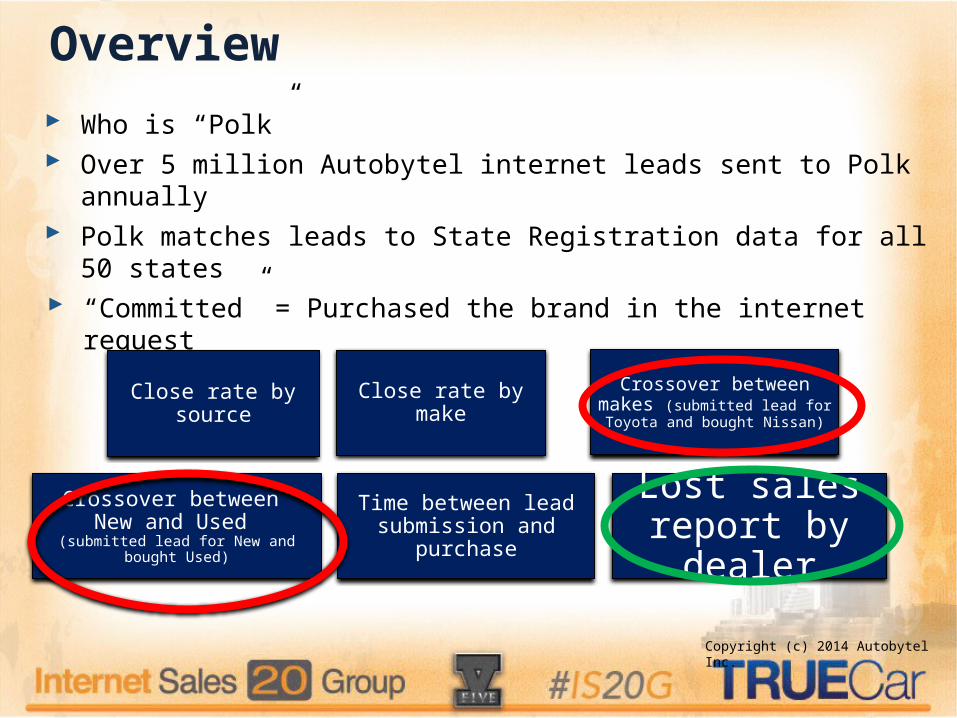

Overview Who is “Polk” Over 5 million Autobytel internet leads sent to Polk annually Polk matches leads to State Registration data for all 50 states “Committed” = Purchased the brand in the internet request

Close rate by source Close rate by makeCrossover between makes

(submitted lead for Toyota and bought Nissan)

Crossover between New and Used

(submitted lead for New and bought Used)

Time between lead submission and purchase

Lost sales report by dealer

Copyright (c) 2014 Autobytel Inc.

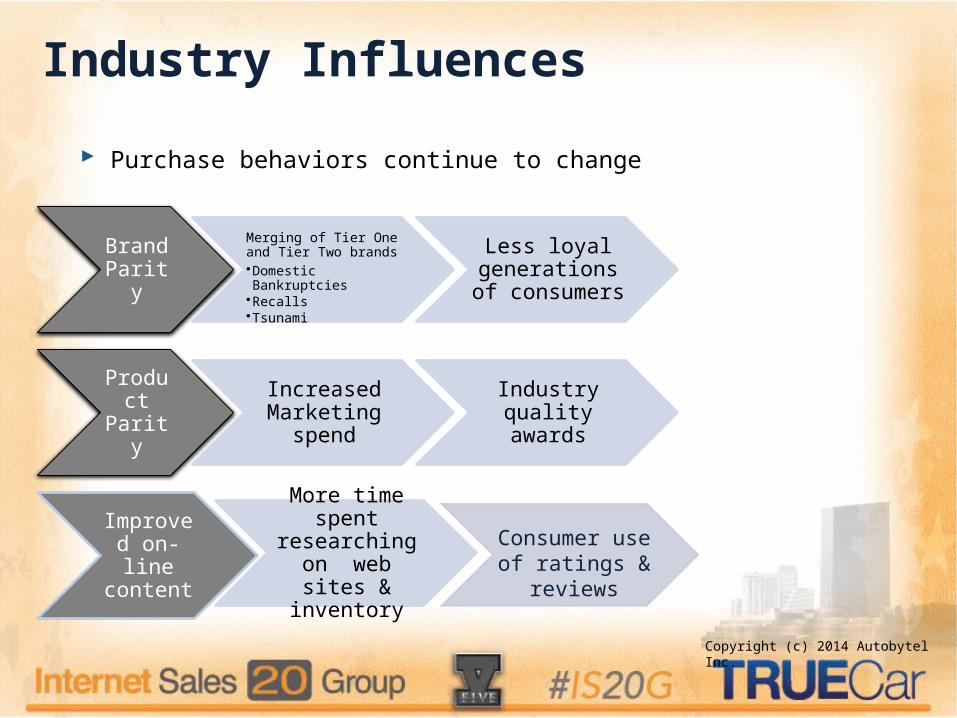

Industry Influences

Brand Parity

Merging of Tier One and Tier Two brands•Domestic Bankruptcies•Recalls•Tsunami

Less loyal generations of

consumers

Product Parity

Increased Marketing spend

Industry quality awards

More time spent researching on

web sites & inventory

Improved on-line content

Purchase behaviors continue to change

Consumer use of ratings & reviews

Copyright (c) 2014 Autobytel Inc.

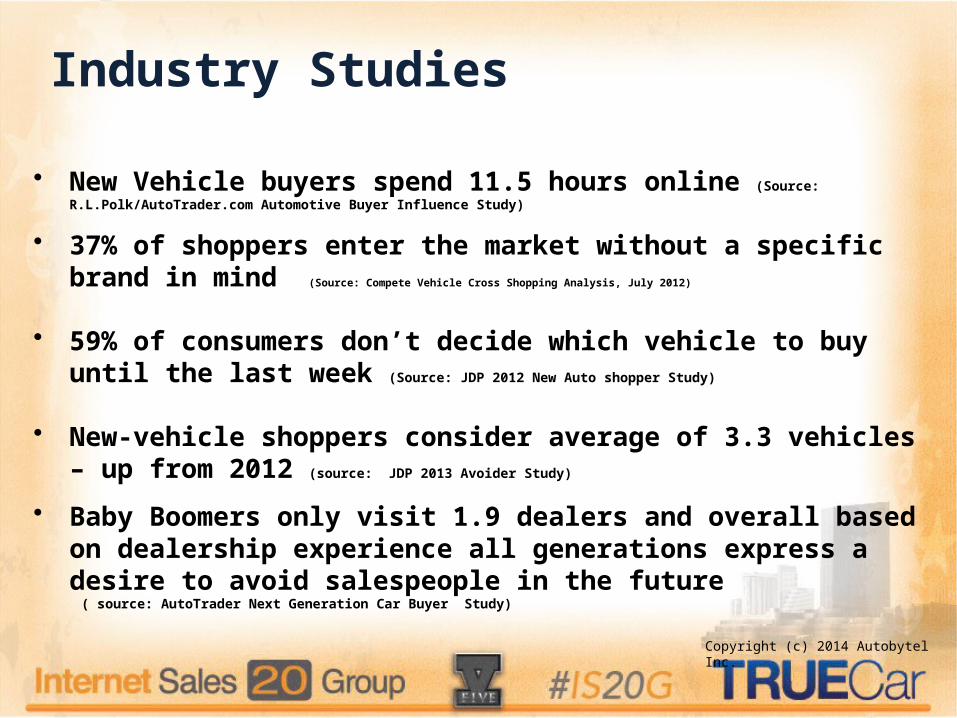

• New Vehicle buyers spend 11.5 hours online (Source: R.L.Polk/AutoTrader.com

Automotive Buyer Influence Study)

• 37% of shoppers enter the market without a specific brand in mind (Source: Compete Vehicle Cross Shopping Analysis, July 2012)

• 59% of consumers don’t decide which vehicle to buy until the last week (Source: JDP 2012 New Auto shopper Study)

• New-vehicle shoppers consider average of 3.3 vehicles – up from 2012 (source: JDP 2013 Avoider Study)

• Baby Boomers only visit 1.9 dealers and overall based on dealership experience all generations express a desire to avoid salespeople in the future

( source: AutoTrader Next Generation Car Buyer Study)

Industry Studies

Copyright (c) 2014 Autobytel Inc.

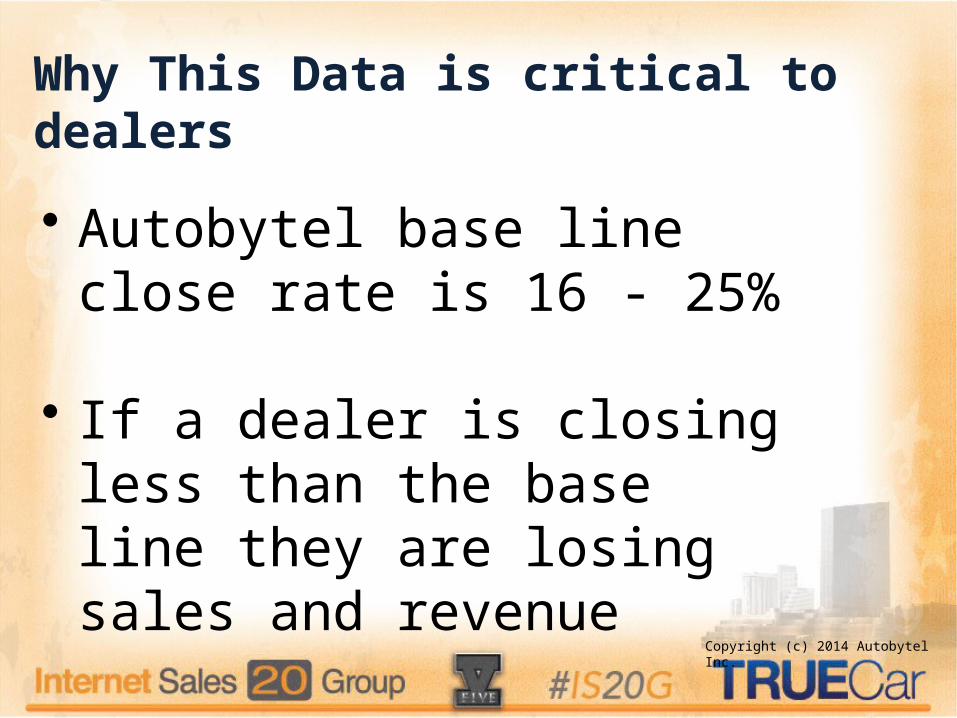

• Autobytel base line close rate is 16 - 25%

• If a dealer is closing less than the base line they are losing sales and revenue

Why This Data is critical to dealers

Copyright (c) 2014 Autobytel Inc.

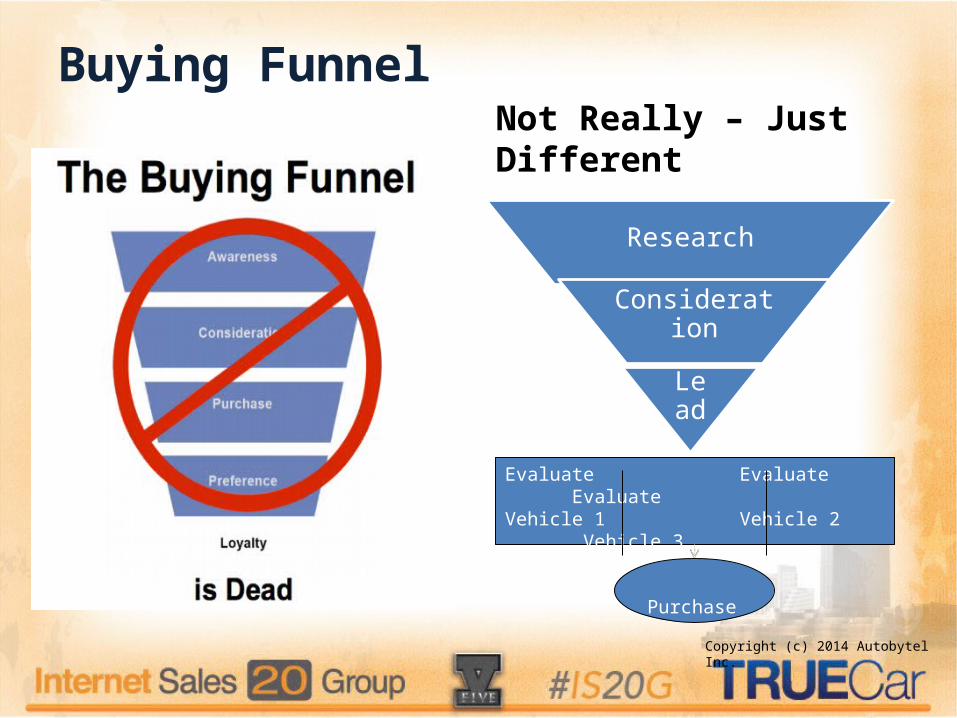

Buying Funnel

Not Really – Just Different

Research

Consideration

Lead

Evaluate Evaluate Evaluate Vehicle 1 Vehicle 2 Vehicle 3

Purchase

Copyright (c) 2014 Autobytel Inc.

What’s changed?

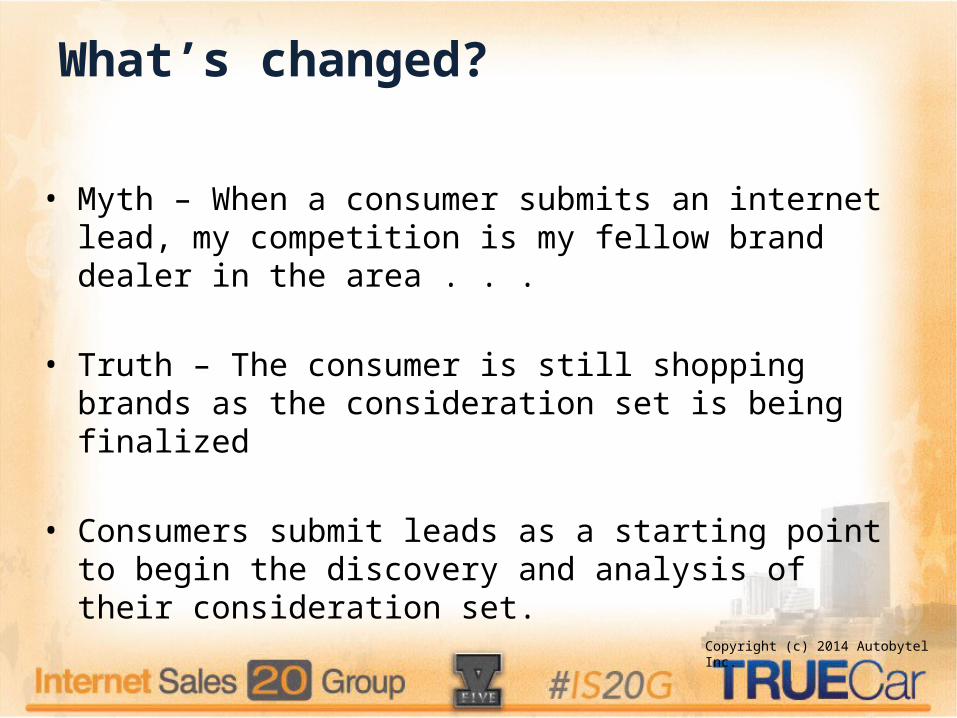

• Myth – When a consumer submits an internet lead, my competition is my fellow brand dealer in the area . . .

• Truth – The consumer is still shopping brands as the consideration set is being finalized

• Consumers submit leads as a starting point to begin the discovery and analysis of their consideration set.

Copyright (c) 2014 Autobytel Inc.

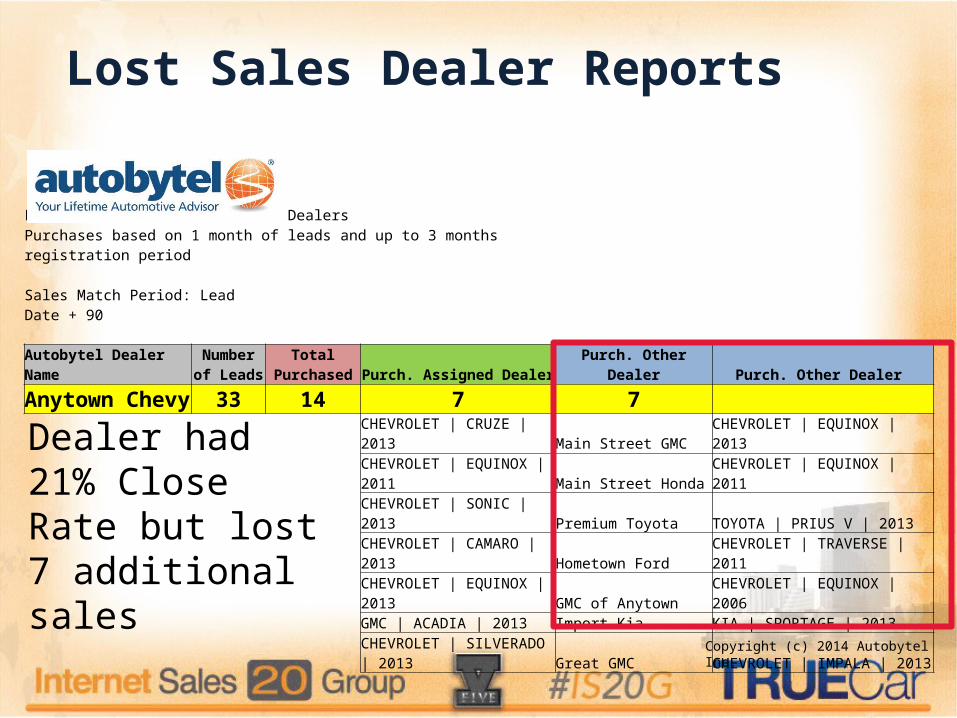

Lost Sales Dealer Reports

Leads Purchased from Detailed DealersPurchases based on 1 month of leads and up to 3 months registration period

Sales Match Period: Lead Date + 90

Autobytel Dealer NameNumber of

LeadsTotal

Purchased Purch. Assigned Dealer Purch. Other Dealer Purch. Other Dealer

Anytown Chevy 33 14 7 7 CHEVROLET | CRUZE | 2013 Main Street GMC CHEVROLET | EQUINOX | 2013CHEVROLET | EQUINOX | 2011 Main Street Honda CHEVROLET | EQUINOX | 2011

CHEVROLET | SONIC | 2013 Premium Toyota TOYOTA | PRIUS V | 2013CHEVROLET | CAMARO | 2013 Hometown Ford CHEVROLET | TRAVERSE | 2011CHEVROLET | EQUINOX | 2013 GMC of Anytown CHEVROLET | EQUINOX | 2006

GMC | ACADIA | 2013 Import Kia KIA | SPORTAGE | 2013CHEVROLET | SILVERADO | 2013 Great GMC CHEVROLET | IMPALA | 2013

Dealer had 21% Close Rate but lost 7 additional sales

Copyright (c) 2014 Autobytel Inc.

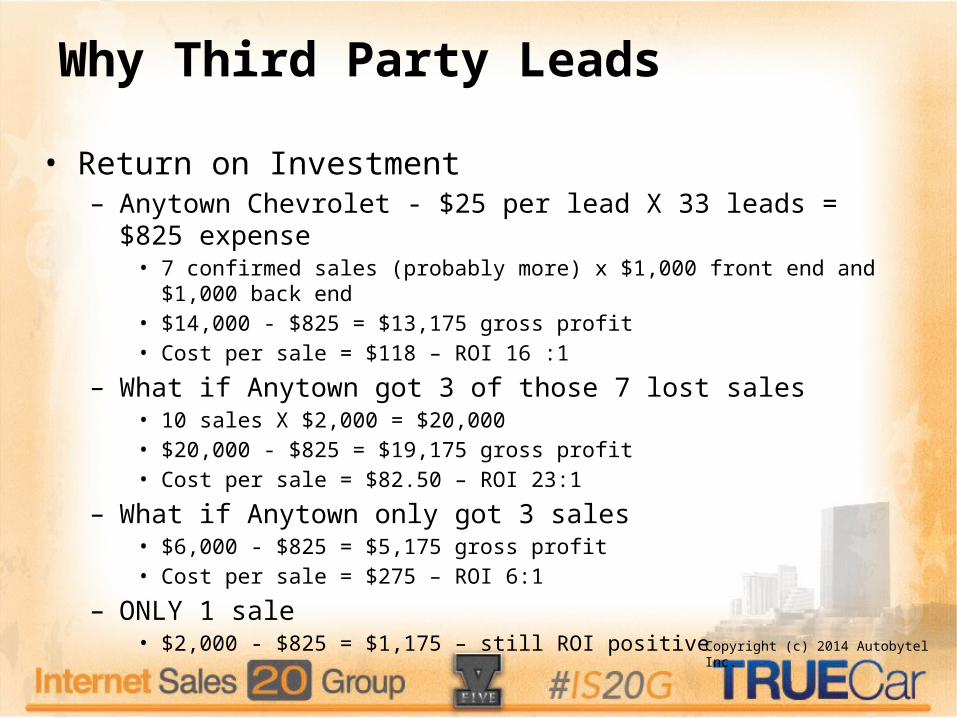

Why Third Party Leads

• Return on Investment– Anytown Chevrolet - $25 per lead X 33 leads = $825 expense

• 7 confirmed sales (probably more) x $1,000 front end and $1,000 back end• $14,000 - $825 = $13,175 gross profit• Cost per sale = $118 – ROI 16 :1

– What if Anytown got 3 of those 7 lost sales• 10 sales X $2,000 = $20,000• $20,000 - $825 = $19,175 gross profit• Cost per sale = $82.50 – ROI 23:1

– What if Anytown only got 3 sales• $6,000 - $825 = $5,175 gross profit• Cost per sale = $275 – ROI 6:1

– ONLY 1 sale• $2,000 - $825 = $1,175 – still ROI positive

Copyright (c) 2014 Autobytel Inc.

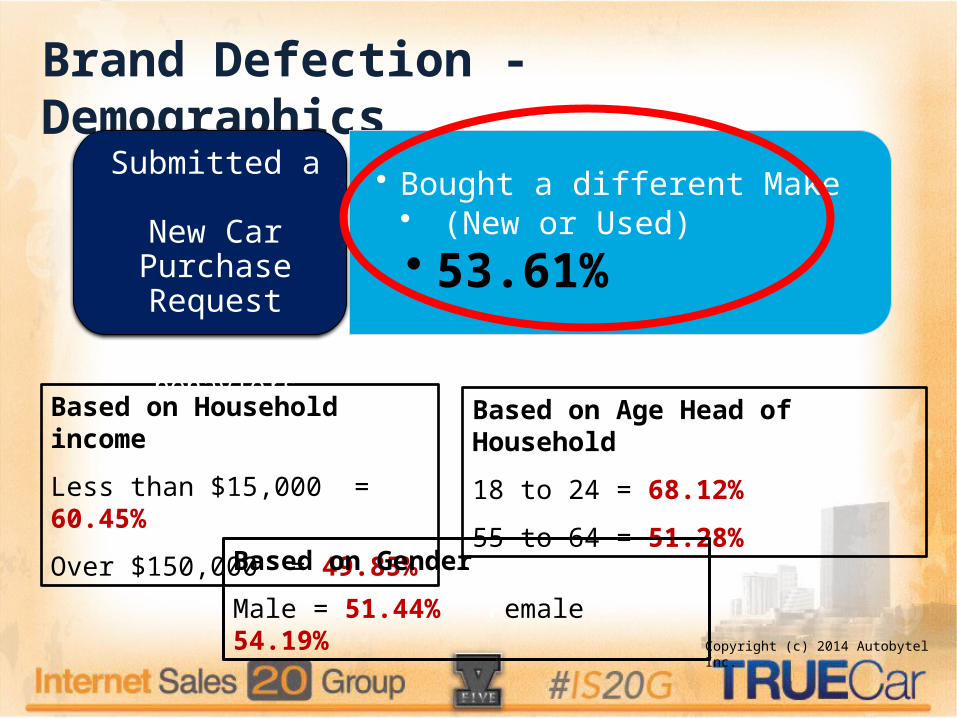

Brand Defection - Demographics

• Bought a different Make• (New or Used)• 53.61%

Submitted a New Car

Purchase Request

Based on Household income

Less than $15,000 = 60.45%

Over $150,000 = 49.85%

Based on Age Head of Household

18 to 24 = 68.12%

55 to 64 = 51.28%

Demographics show variance in buying behaviors

Based on Gender

Male = 51.44% Female = 54.19%Copyright (c) 2014 Autobytel Inc.

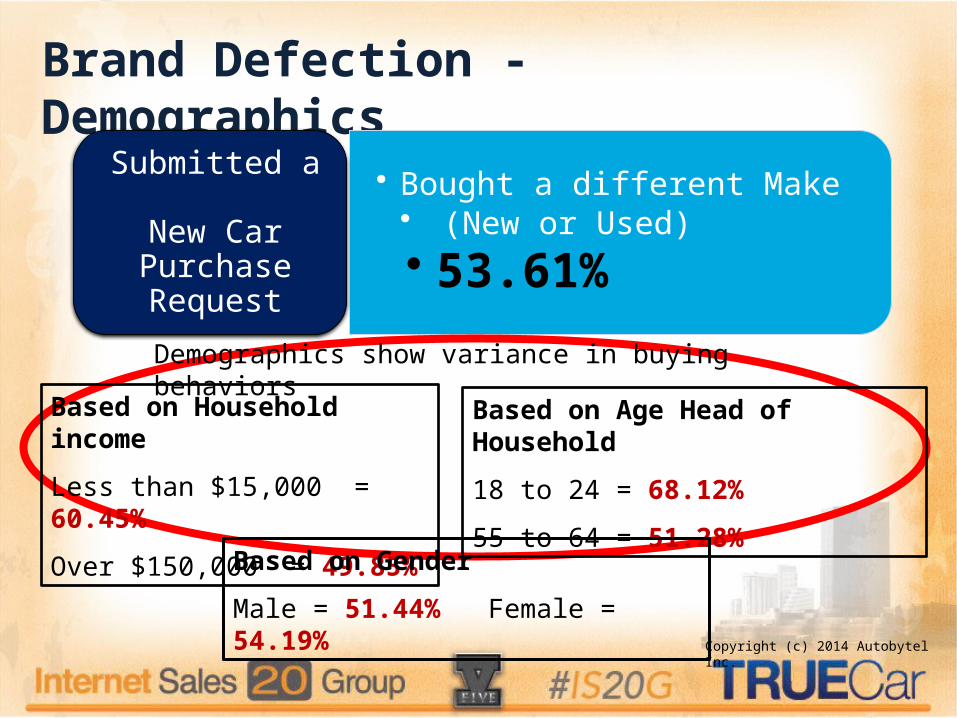

Brand Defection - Demographics

• Bought a different Make• (New or Used)• 53.61%

Submitted a New Car

Purchase Request

Based on Household income

Less than $15,000 = 60.45%

Over $150,000 = 49.85%

Based on Age Head of Household

18 to 24 = 68.12%

55 to 64 = 51.28%

Demographics show variance in buying behaviors

Based on Gender

Male = 51.44% Female = 54.19%Copyright (c) 2014 Autobytel Inc.

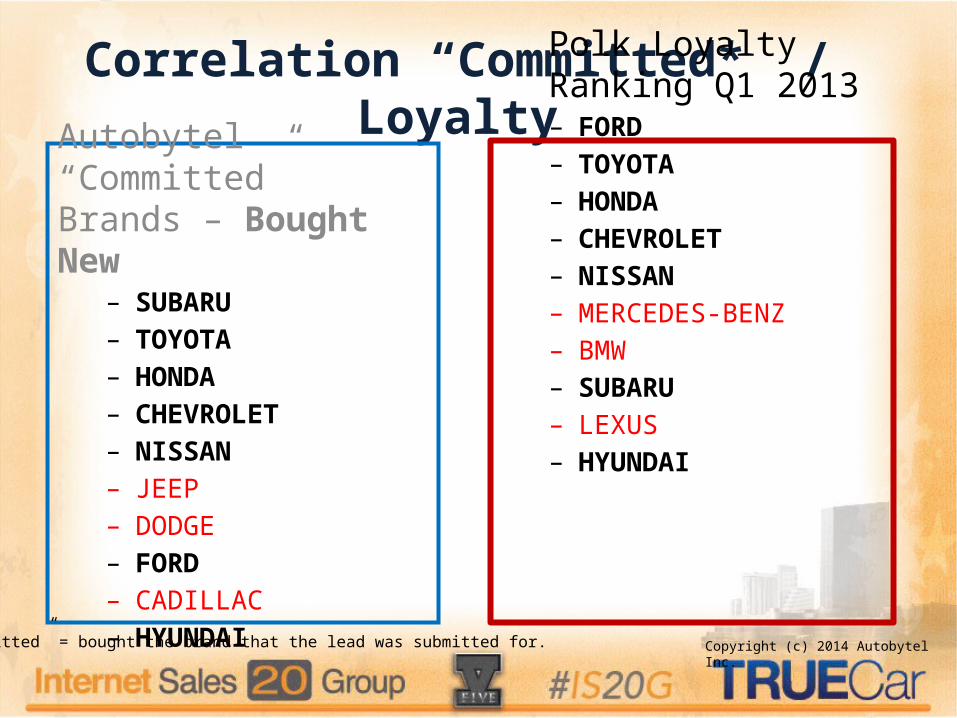

Correlation “Committed*” / Loyalty

Autobytel “Committed” Brands – Bought New

– SUBARU– TOYOTA– HONDA– CHEVROLET– NISSAN– JEEP– DODGE– FORD– CADILLAC– HYUNDAI

“Committed” = bought the brand that the lead was submitted for. Copyright (c) 2014 Autobytel Inc.

Correlation “Committed*” / Loyalty

Autobytel “Committed” Brands – Bought New

– SUBARU– TOYOTA– HONDA– CHEVROLET– NISSAN– JEEP– DODGE– FORD– CADILLAC– HYUNDAI

Polk Loyalty Ranking Q1 2013– FORD– TOYOTA– HONDA– CHEVROLET– NISSAN– MERCEDES-BENZ– BMW– SUBARU– LEXUS– HYUNDAI

“Committed” = bought the brand that the lead was submitted for. Copyright (c) 2014 Autobytel Inc.

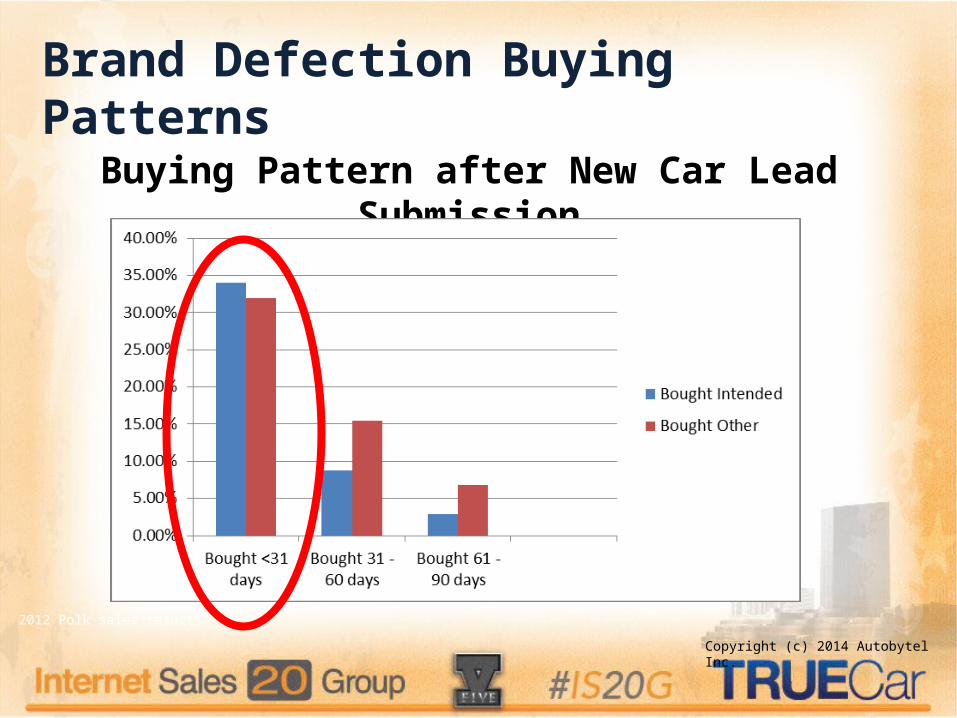

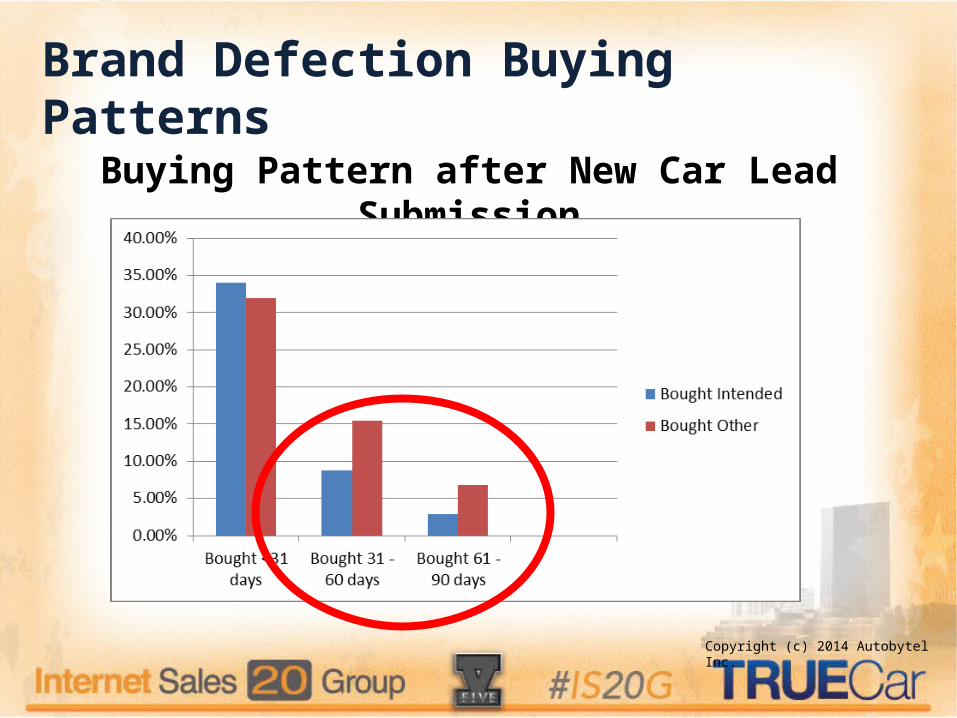

Brand Defection Buying Patterns

Buying Pattern after New Car Lead Submission

2012 Polk sales results

Copyright (c) 2014 Autobytel Inc.

Brand Defection Buying Patterns

Buying Pattern after New Car Lead Submission

Copyright (c) 2014 Autobytel Inc.

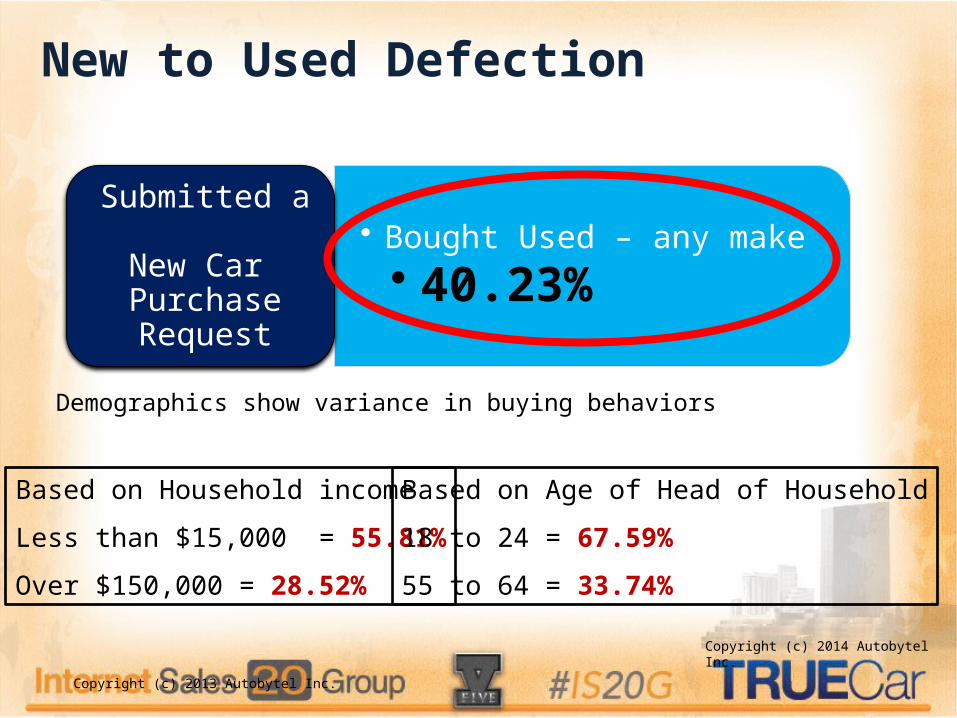

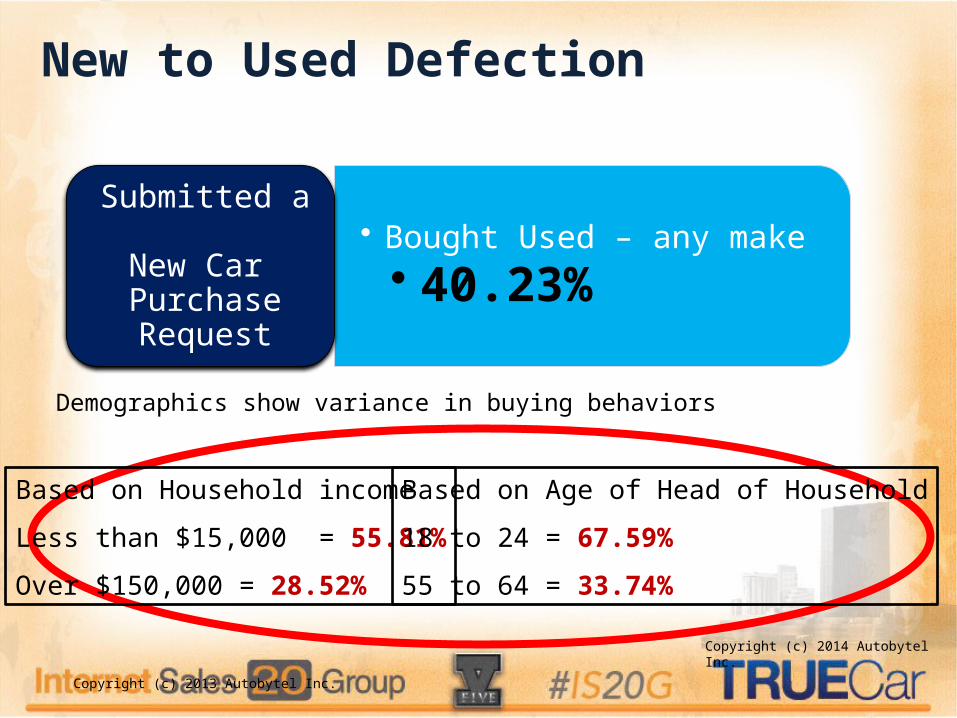

New to Used Defection

• Bought Used – any make• 40.23%

Submitted a New Car Purchase Request

Based on Household income

Less than $15,000 = 55.81%

Over $150,000 = 28.52%

Copyright (c) 2013 Autobytel Inc.

Based on Age of Head of Household

18 to 24 = 67.59%

55 to 64 = 33.74%

Demographics show variance in buying behaviors

Copyright (c) 2014 Autobytel Inc.

New to Used Defection

• Bought Used – any make• 40.23%

Submitted a New Car Purchase Request

Based on Household income

Less than $15,000 = 55.81%

Over $150,000 = 28.52%

Copyright (c) 2013 Autobytel Inc.

Based on Age of Head of Household

18 to 24 = 67.59%

55 to 64 = 33.74%

Demographics show variance in buying behaviors

Copyright (c) 2014 Autobytel Inc.

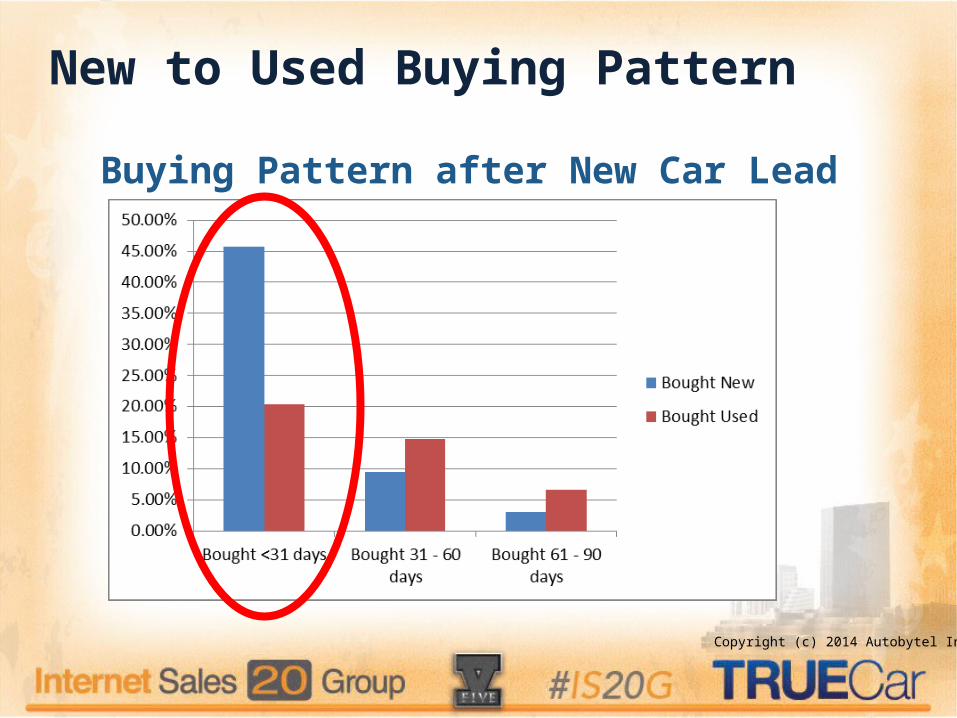

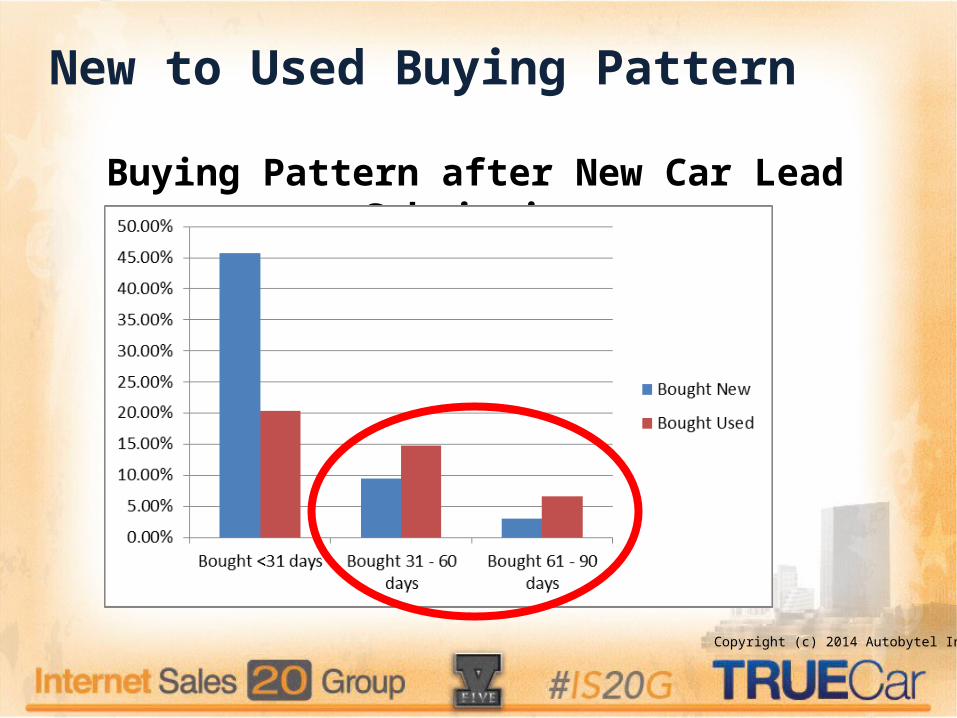

New to Used Buying Pattern

Buying Pattern after New Car Lead Submission

Copyright (c) 2014 Autobytel Inc.

New to Used Buying Pattern

Buying Pattern after New Car Lead Submission

Copyright (c) 2014 Autobytel Inc.

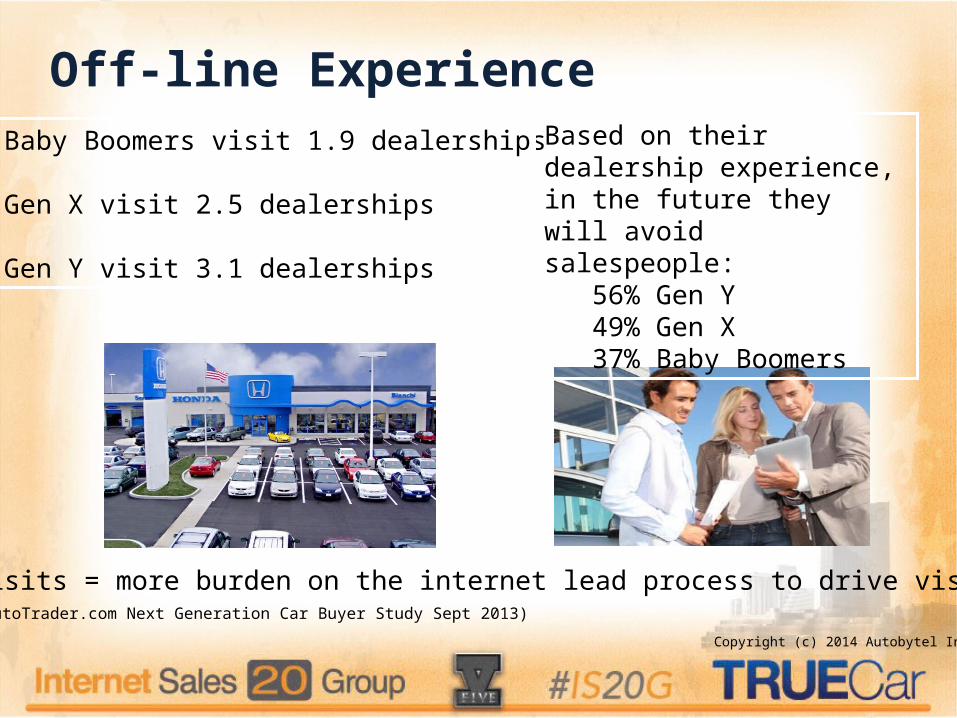

Off-line Experience

Copyright (c) 2014 Autobytel Inc.

Less visits = more burden on the internet lead process to drive visits

Baby Boomers visit 1.9 dealerships

Gen X visit 2.5 dealerships

Gen Y visit 3.1 dealerships

Based on their dealership experience, in the future they will avoid salespeople:

56% Gen Y49% Gen X37% Baby Boomers

(AutoTrader.com Next Generation Car Buyer Study Sept 2013)

Off-line Advantages

Dealership Brand is featured

• Ability to test drive and explore vehicle features and benefits

• Ability for a professional walk around of the vehicle

Sales Consultant can be a vehicle consultant:

• Who will be driving the car?

• How will the car be used?

• What features are important in a vehicle?

Ability to profile the consumer to lead them down a personalized vehicle presentation

• New/Used/CPO – Model – Trim – Colors – Optional Equipment

Copyright (c) 2014 Autobytel Inc.

On-line Experience

What demographics and buying behavior trends do we know about this consumer?

How committed are they to my brand?

Do we stop at price or do we start asking questions?

Copyright (c) 2014 Autobytel Inc.

On-line Challenge

How can we give them the off-line dealership visit experience?

How do we create a need for them to visit my dealership?

This applies to responding to leads plus website strategies to drive showroom traffic

Copyright (c) 2014 Autobytel Inc.

On-line lead responses (phone and form)

Internet Sales Consultant can be pigeon holed into being an information provider:

1) Do you have the car I want?2) What is the price?

When a consumer submits a lead WE MAKE THEM PICK A YEAR/MAKE/MODEL.

Is that the vehicle that really meets their needs?

Copyright (c) 2014 Autobytel Inc.

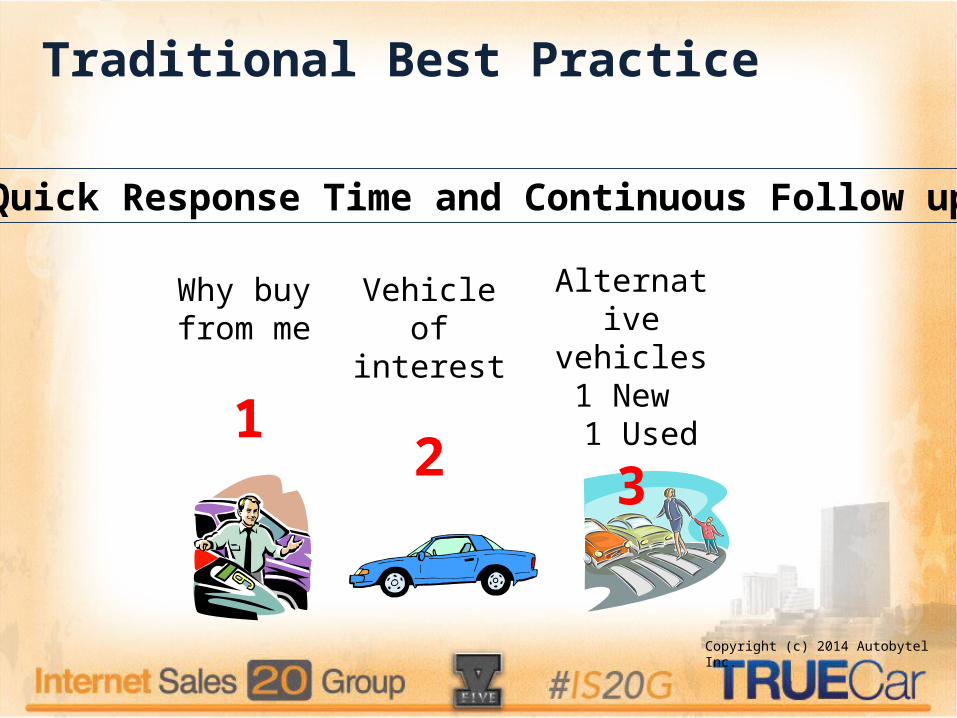

Traditional Best Practice

Why buy from me

1

Vehicle of interest

2

Alternative vehicles 1 New 1 Used

3

Quick Response Time and Continuous Follow up

Copyright (c) 2014 Autobytel Inc.

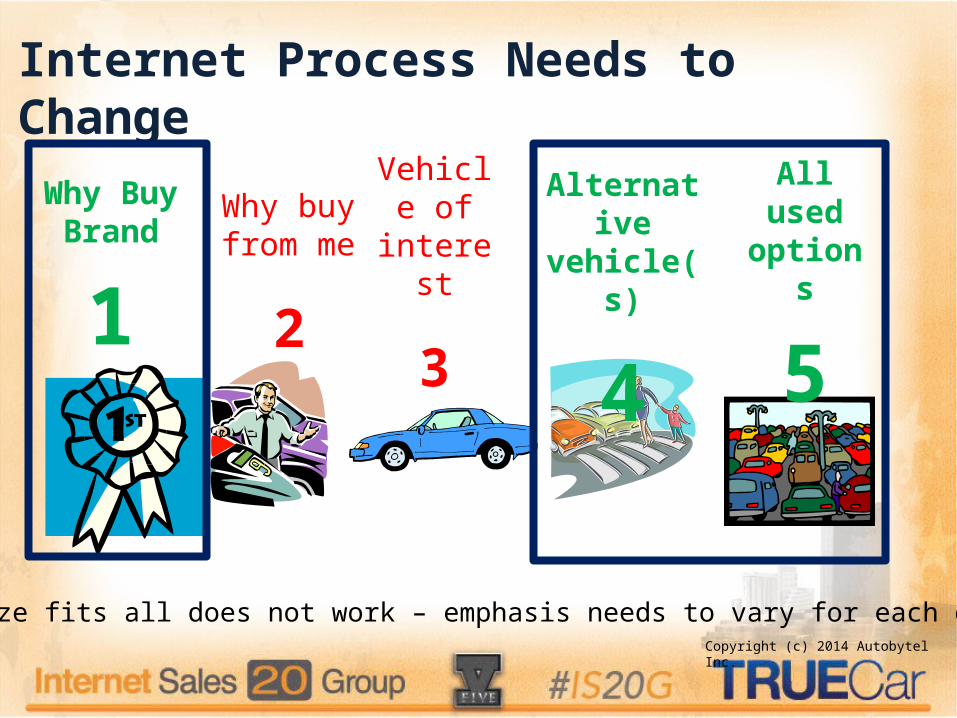

Internet Process Needs to Change

Why Buy Brand

1

Why buy from me

2

Vehicle of

interest

3

Alternative vehicle(s)

4

All used

options

5

One size fits all does not work – emphasis needs to vary for each dealCopyright (c) 2014 Autobytel Inc.

Recap/Communicate Differently

• Email responses and talk tracks need to:– Reinforce the brand – why BLANK is a great brand with a great

lineup– Mention the various trim levels and other similar models– Briefly explain CPO and your used inventory (all models)

• But the real opportunity lies in communicating differently– Texteo and Audio interaction– Video and Audio interaction PLUS co-browsing

April 18, 2023

Copyright (c) 2014 Autobytel Inc.

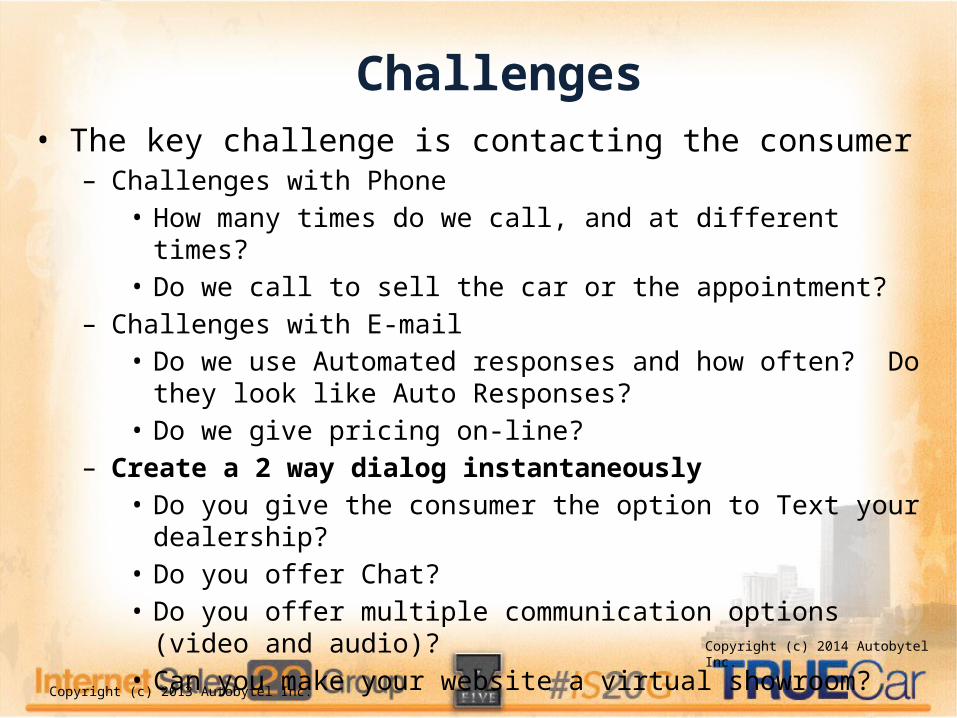

Challenges• The key challenge is contacting the consumer

– Challenges with Phone • How many times do we call, and at different times?• Do we call to sell the car or the appointment?

– Challenges with E-mail• Do we use Automated responses and how often? Do they look like

Auto Responses?• Do we give pricing on-line?

– Create a 2 way dialog instantaneously• Do you give the consumer the option to Text your dealership?• Do you offer Chat?• Do you offer multiple communication options (video and audio)?• Can you make your website a virtual showroom?

Copyright (c) 2013 Autobytel Inc.

Copyright (c) 2014 Autobytel Inc.

Why Mobile?

Copyright (c) 2014 Autobytel Inc.

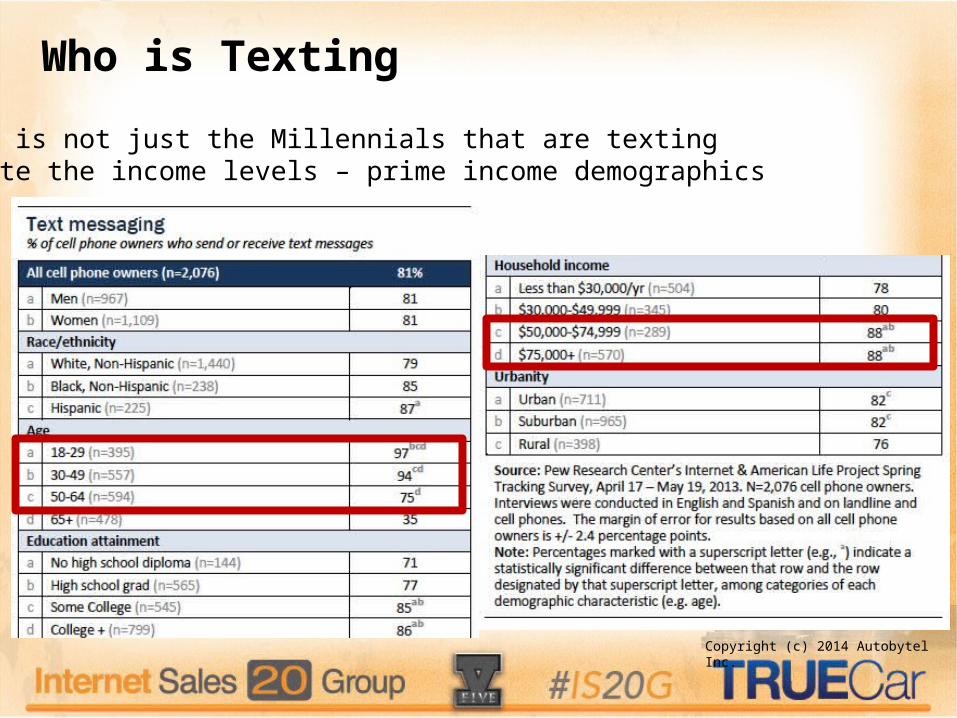

Who is Texting

• It is not just the Millennials that are texting• Note the income levels – prime income demographics

Copyright (c) 2014 Autobytel Inc.

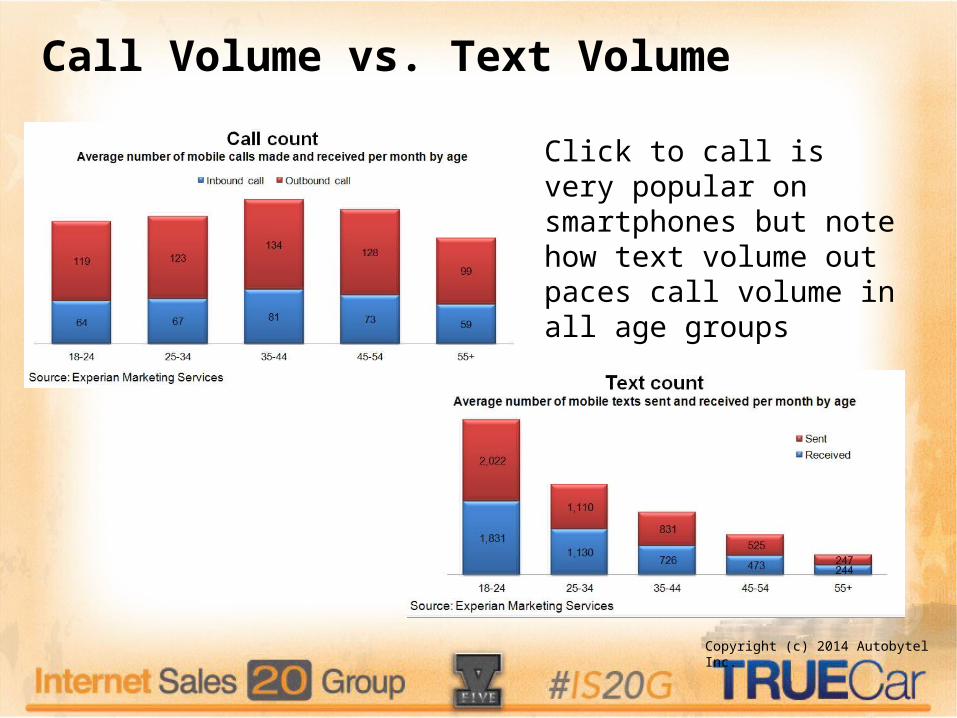

Call Volume vs. Text Volume

Click to call is very popular on smartphones but note how text volume out paces call volume in all age groups

Copyright (c) 2014 Autobytel Inc.

Text Leads • Consumer adoption of Texting is growing

– 98% of text messages are read, compared to 22% of emails, 29% of tweets and 12% of Facebook posts. (Frost & Sullivan 2010, Slick Text)

• Limitation on characters leads to more of a conversation than trying to cover every detail in one e-mail or phone script

• Ability to be consultative– Two way conversation

• Ability to respond to consumers on the lot – Your lot and others

• 49% of automotive smartphone users made a purchase related to that interaction (The xAd/Telmetrics Mobile Path to Purchase Study)

Copyright (c) 2014 Autobytel Inc.

Concerns Government compliance (TCPA)

Several recent text message cases have resulted in multi-million dollar settlements. For instance: • Lithia Motors - $2.5 million class-action settlement (between

$175 and $500/phone number)• Twentieth Century Fox - $16 million class-action settlement

($200/ phone number)• Simon & Schuster - $10 million class-action settlement

($175/ phone number)• Timberland Company - $7 million class-action settlement

($150/ phone number)

Copyright (c) 2012 Autobytel Inc.35

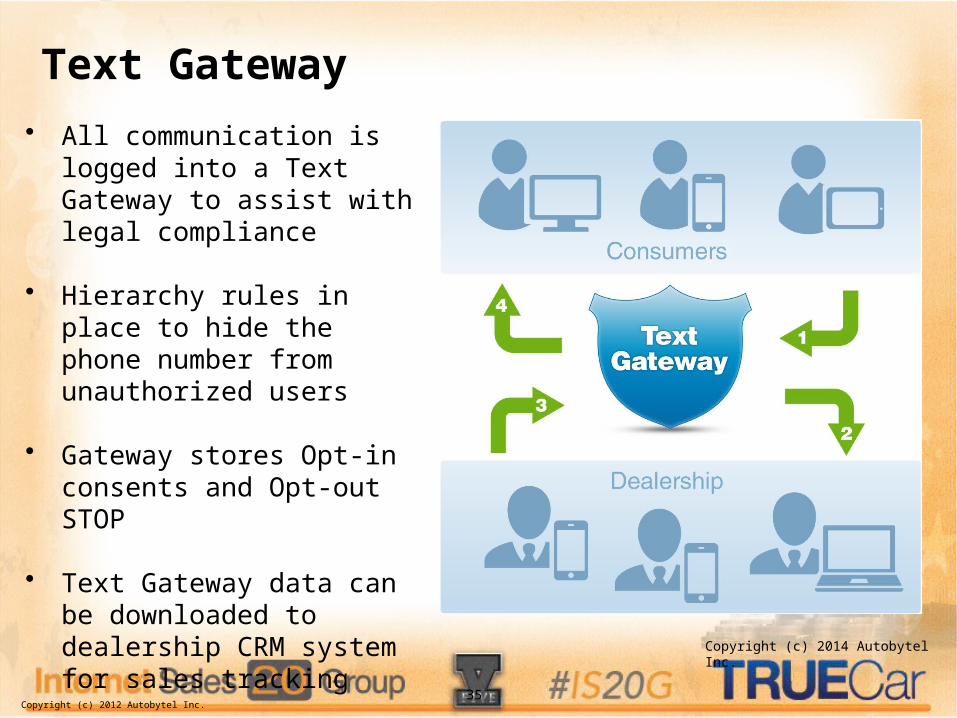

Text Gateway• All communication is logged

into a Text Gateway to assist with legal compliance

• Hierarchy rules in place to hide the phone number from unauthorized users

• Gateway stores Opt-in consents and Opt-out STOP

• Text Gateway data can be downloaded to dealership CRM system for sales tracking

Copyright (c) 2014 Autobytel Inc.

Interactive Engagement Platform

• A true “virtual up” to create a high-touch interaction with consumers

• Video, voice, chat and dual-cursor guided browsing with any visitor

• Explain incentives and offers to visitors in real-time

• Traffic is viewed real time on the website

With in-person visits to dealerships declining, consumers are now walking around “virtual showrooms” (automotive websites) to make their purchase

Conclusion• The traditional buying funnel has changed

– More vehicles are being considered and the funnel is fluid– Majority of consumers do not buy what they think they are going to buy

• Form leads are not dead but there are more options available today to communicate beyond phone and e-mail

• It is not hard to have a positive ROI with Third Party Leads• Text Communications is growing

– Actionable & Customer initiated

• Recent technology allows for bringing the showroom experience into desktop and mobile devices

– Audio and Video Chat & Co-browsing

• Bottom line – allow consumers to communicate with you in their preferred communication method– Higher Engagement with More Efficient Communication– Capture the high % that leave without filling out a lead form

Copyright (c) 2014 Autobytel Inc.

Thank you

• Scott Pechstein• Vice President, Sales• Direct: (949) 862-3001• Mobile (949) 278-8618• [email protected]• Nasdaq ABTL

Copyright (c) 2014 Autobytel Inc.