Languages

Pages

Legal

The Ups and Downs, Ins and Outs of Transportation

10th Annual Rocky Mountain Commercial Real Estate Expo

November 12, 2004

Current State of The Airline Industry

Who’s in Charge of the Airlines?

“The industry doesn’t attract the most able minds in the business world…Who in their right mind would work for an airline?”

Sam Addoms, Chairman – Frontier Airlines

Denver Post (September 19, 2004)

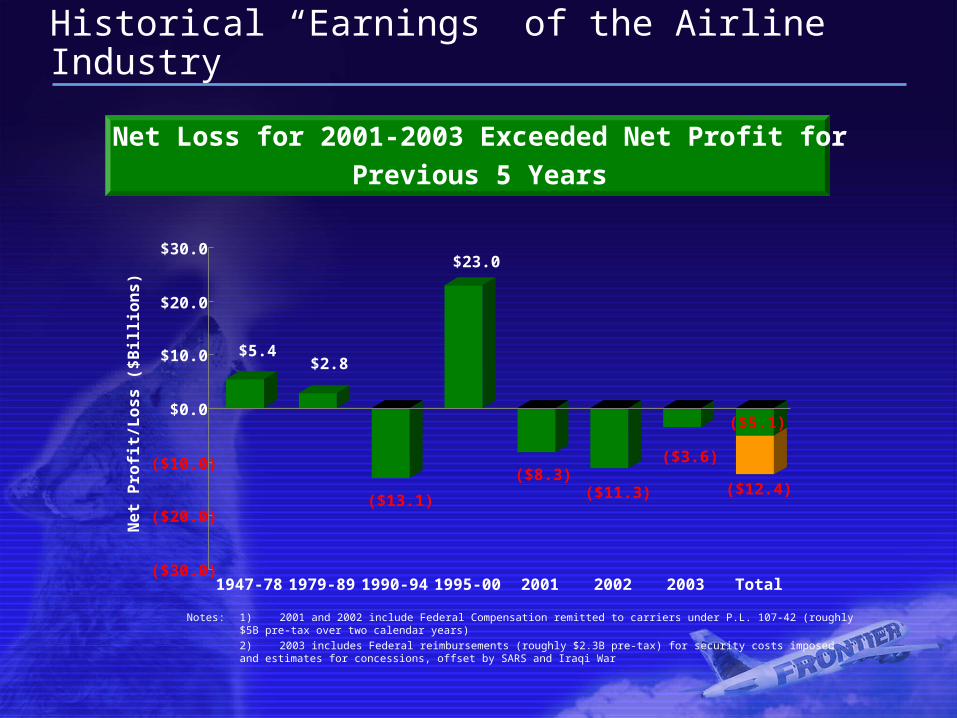

Historical “Earnings” of the Airline Industry

Net Loss for 2001-2003 Exceeded Net Profit for

Previous 5 Years

Notes: 1) 2001 and 2002 include Federal Compensation remitted to carriers under P.L. 107-42 (roughly $5B pre-tax over two calendar years)

2) 2003 includes Federal reimbursements (roughly $2.3B pre-tax) for security costs imposed and estimates for concessions, offset by SARS and Iraqi War

$5.4$2.8

($13.1)

$23.0

($8.3)($11.3)

($3.6)

($5.1)

($12.4)

($30.0)

($20.0)

($10.0)

$0.0

$10.0

$20.0

$30.0

Ne

t P

rofi

t/L

os

s (

$B

illi

on

s)

1947-78 1979-89 1990-94 1995-00 2001 2002 2003 Total

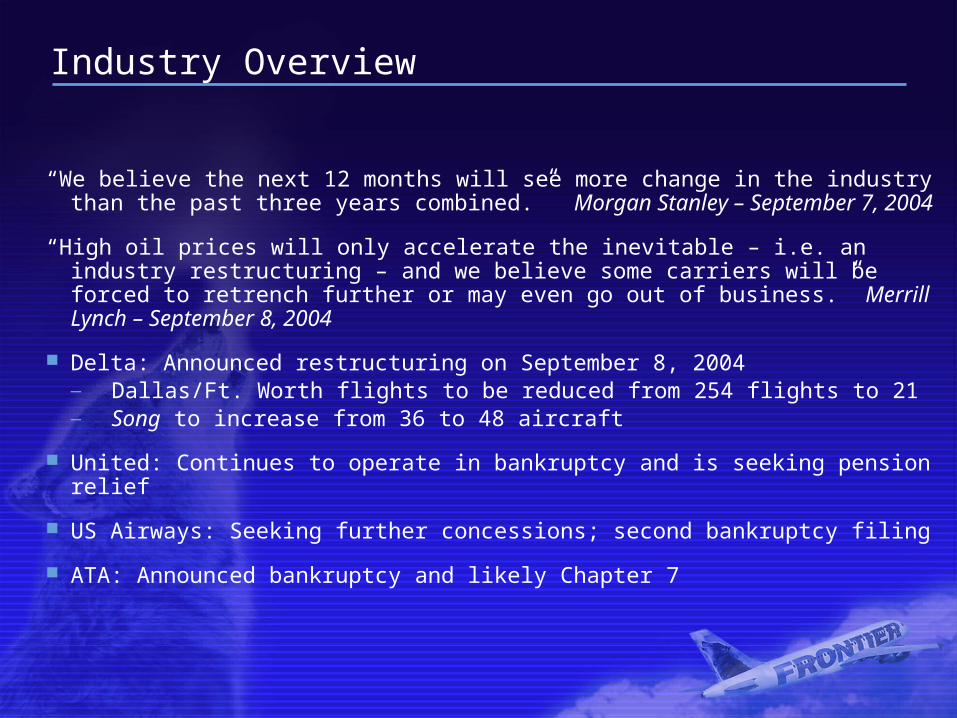

Industry Overview

“We believe the next 12 months will see more change in the industry than the past three years combined.” Morgan Stanley – September 7, 2004

“High oil prices will only accelerate the inevitable – i.e. an industry restructuring – and we believe some carriers will be forced to retrench further or may even go out of business.” Merrill Lynch – September 8, 2004

Delta: Announced restructuring on September 8, 2004— Dallas/Ft. Worth flights to be reduced from 254 flights to 21— Song to increase from 36 to 48 aircraft

United: Continues to operate in bankruptcy and is seeking pension relief

US Airways: Seeking further concessions; second bankruptcy filing

ATA: Announced bankruptcy and likely Chapter 7

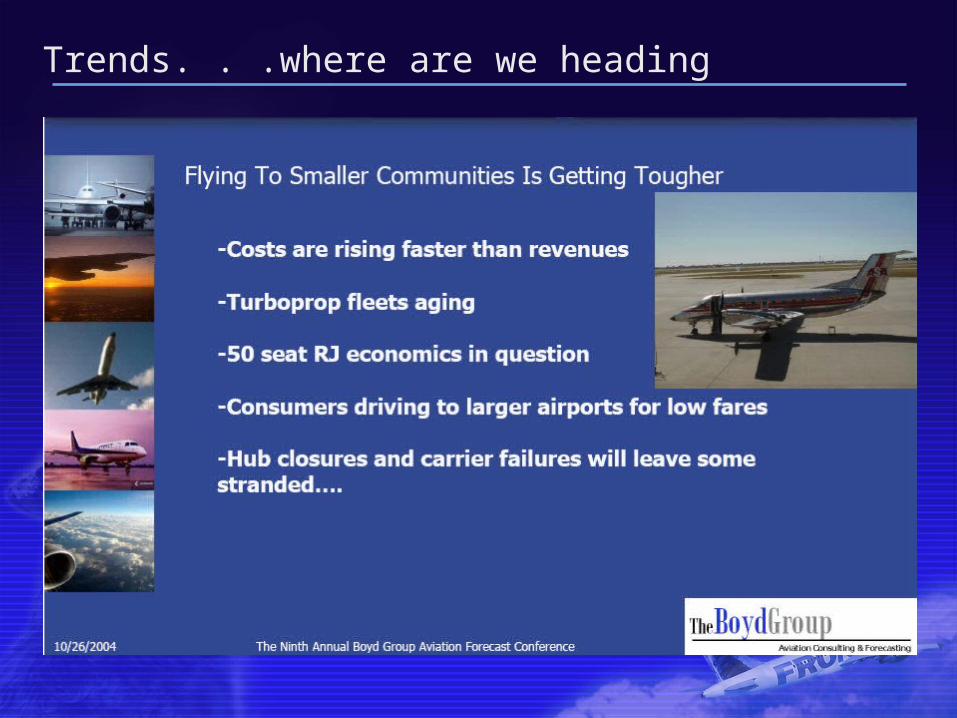

Trends. . .where are we heading

Trends. . .where are we heading

Trends. . .where are we heading

Trends. . .where are we heading

Distribution

Trends. . .where are we heading

Trends. . .where are we heading

Trends. . .where are we heading

As Colorado Grows. . .

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

2005 2010 2015 2020 2025 2030

Po

pu

latio

n (M

illio

ns

)

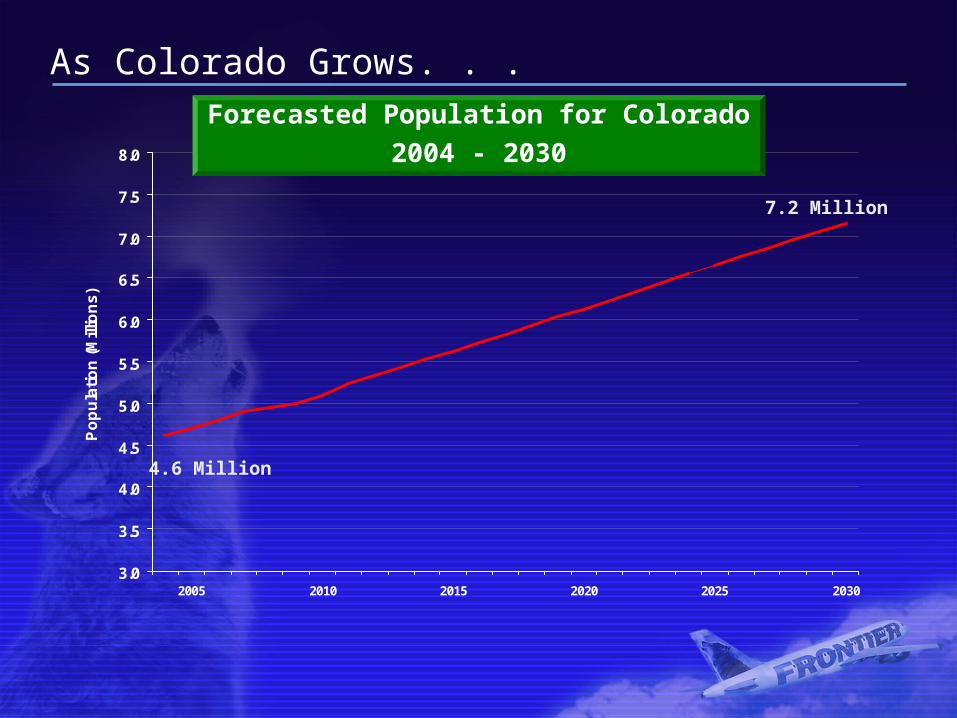

Forecasted Population for Colorado

2004 - 2030

4.6 Million

7.2 Million

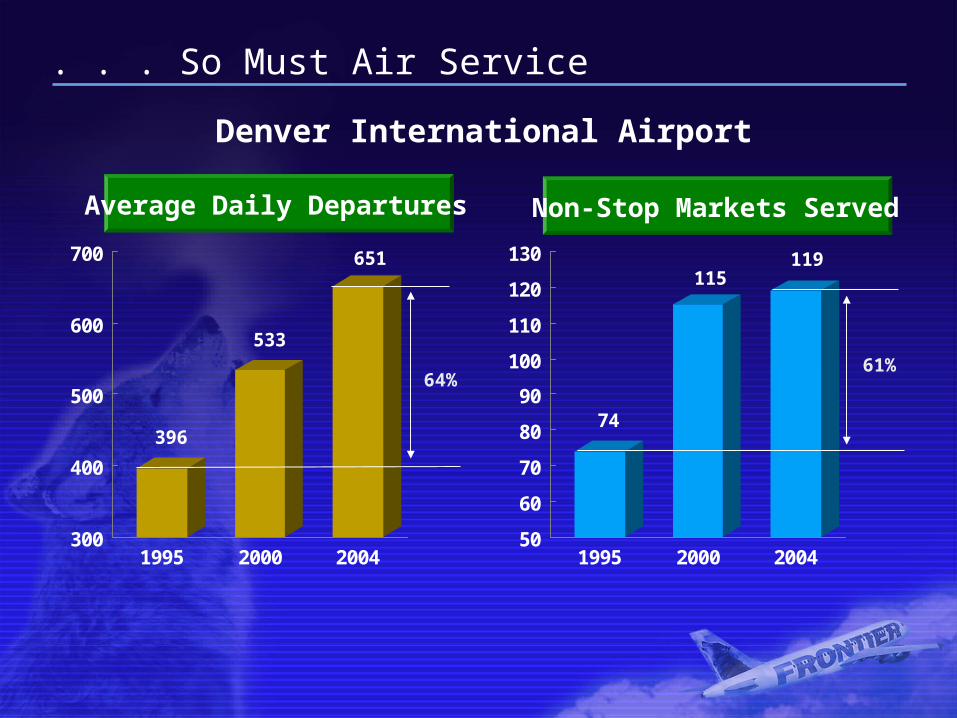

. . . So Must Air Service

396

533

651

300

400

500

600

700

1995 2000 2004

74

115119

50

60

70

80

90

100

110

120

130

1995 2000 2004

61%64%

Average Daily Departures Non-Stop Markets Served

Denver International Airport

13.7

16.5

10

15

20

2003 2004

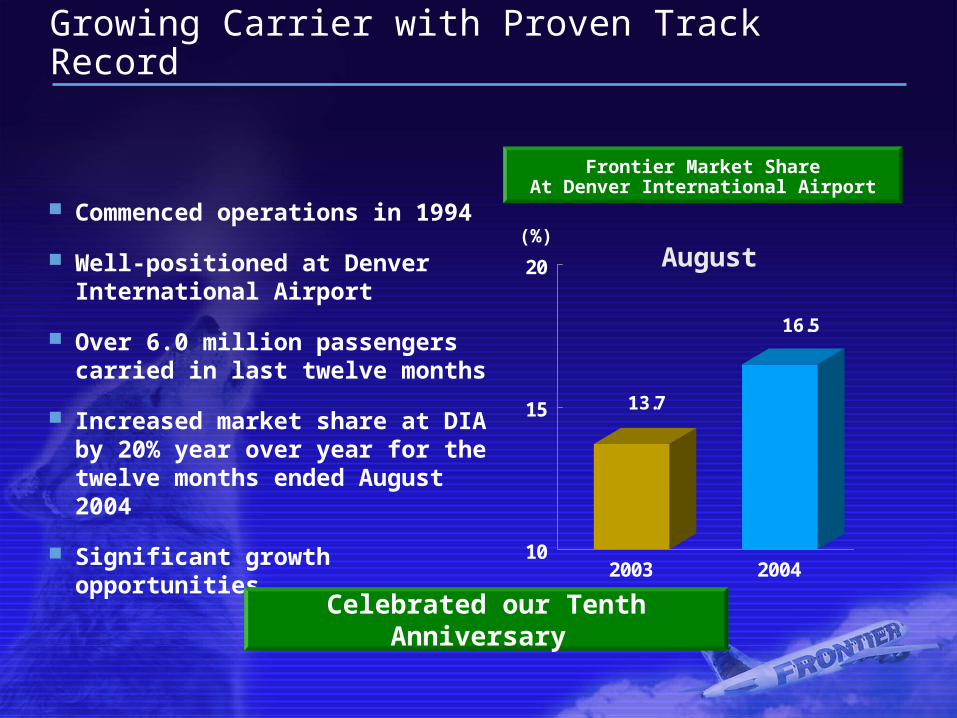

Growing Carrier with Proven Track Record

Commenced operations in 1994

Well-positioned at Denver International Airport

Over 6.0 million passengers carried in last twelve months

Increased market share at DIA by 20% year over year for the twelve months ended August 2004

Significant growth opportunities

Frontier Market ShareAt Denver International Airport

(%)August

Celebrated our Tenth Anniversary

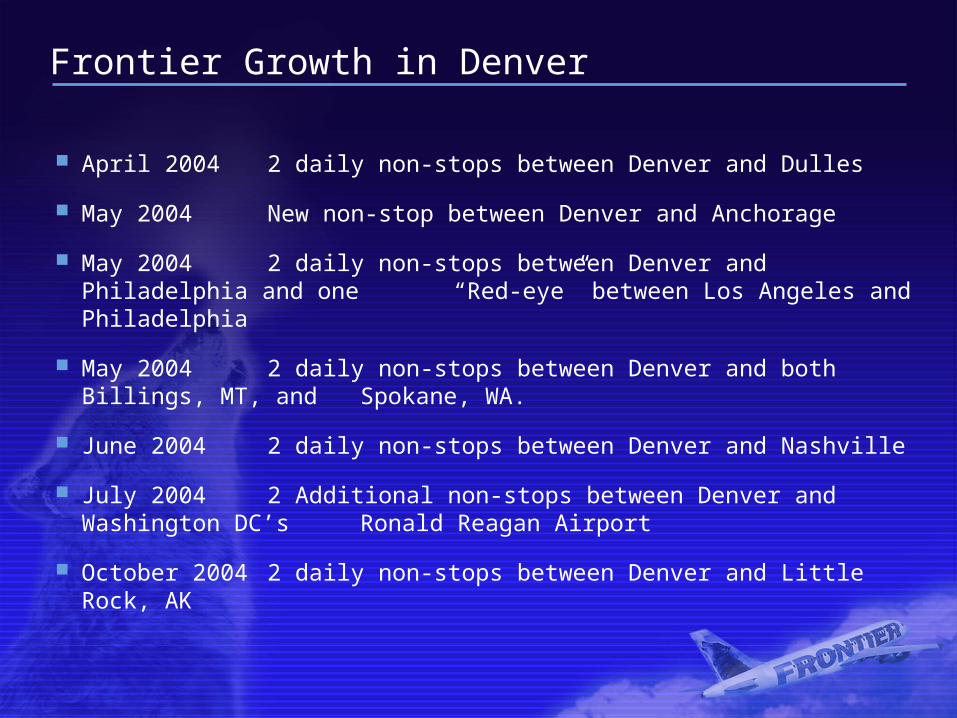

Frontier Growth in Denver Markets

Albuquerque Atlanta Austin Chicago Dallas/Ft.

Worth El Paso Ft. Meyers Kansas City Las Vegas Minneapolis

New Orleans Oklahoma City Phoenix San Diego San Francisco San Jose Seattle St. Louis Tucson

Increased Frontier Frequencies Since January 2004

Frontier Growth in Denver

April 2004 2 daily non-stops between Denver and Dulles

May 2004 New non-stop between Denver and Anchorage

May 2004 2 daily non-stops between Denver and Philadelphia and one “Red-eye” between Los Angeles and Philadelphia

May 2004 2 daily non-stops between Denver and both Billings, MT, and Spokane, WA.

June 2004 2 daily non-stops between Denver and Nashville

July 2004 2 Additional non-stops between Denver and Washington DC’s Ronald Reagan Airport

October 2004 2 daily non-stops between Denver and Little Rock, AK

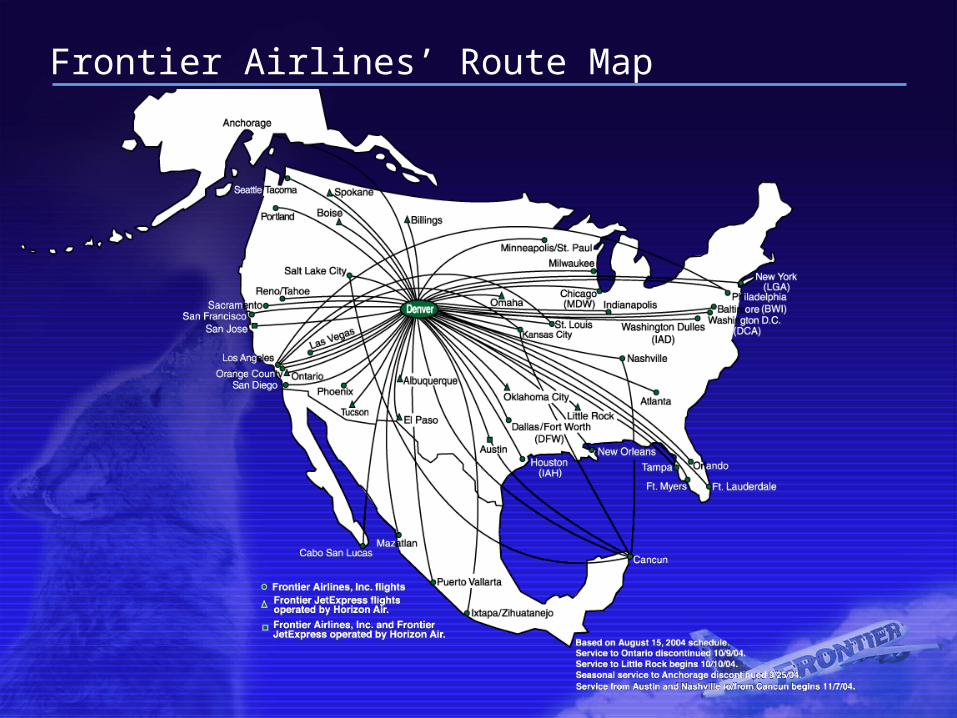

Frontier Airlines’ Route Map

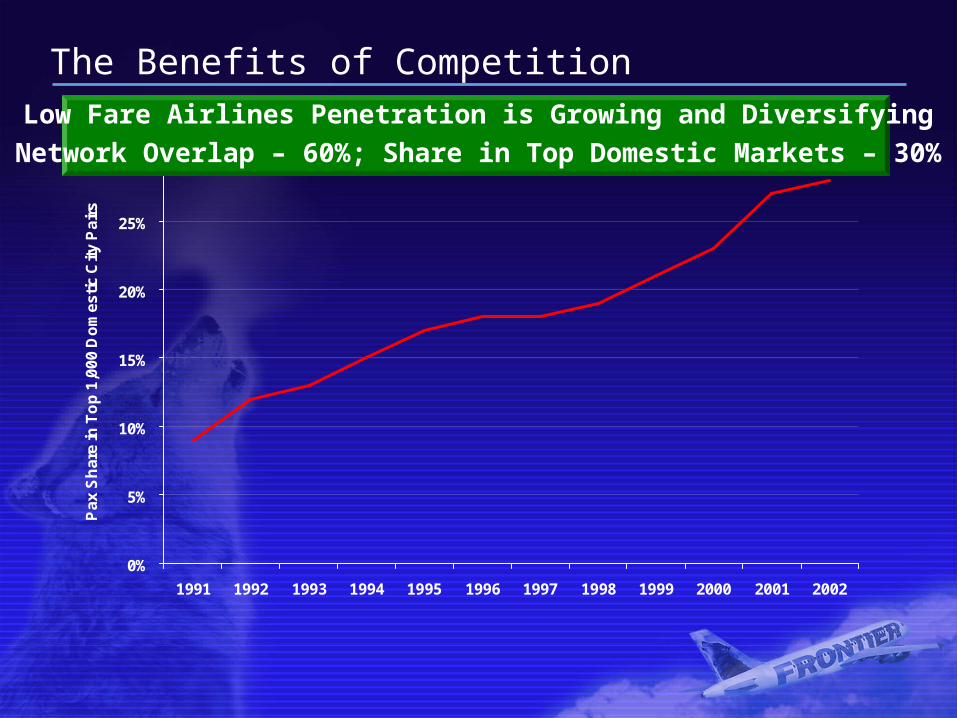

The Benefits of Competition

0%

5%

10%

15%

20%

25%

30%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Pax

Sh

are

in T

op

1,0

00 D

om

estic

City

Pai

rs

Low Fare Airlines Penetration is Growing and Diversifying

Network Overlap – 60%; Share in Top Domestic Markets – 30%

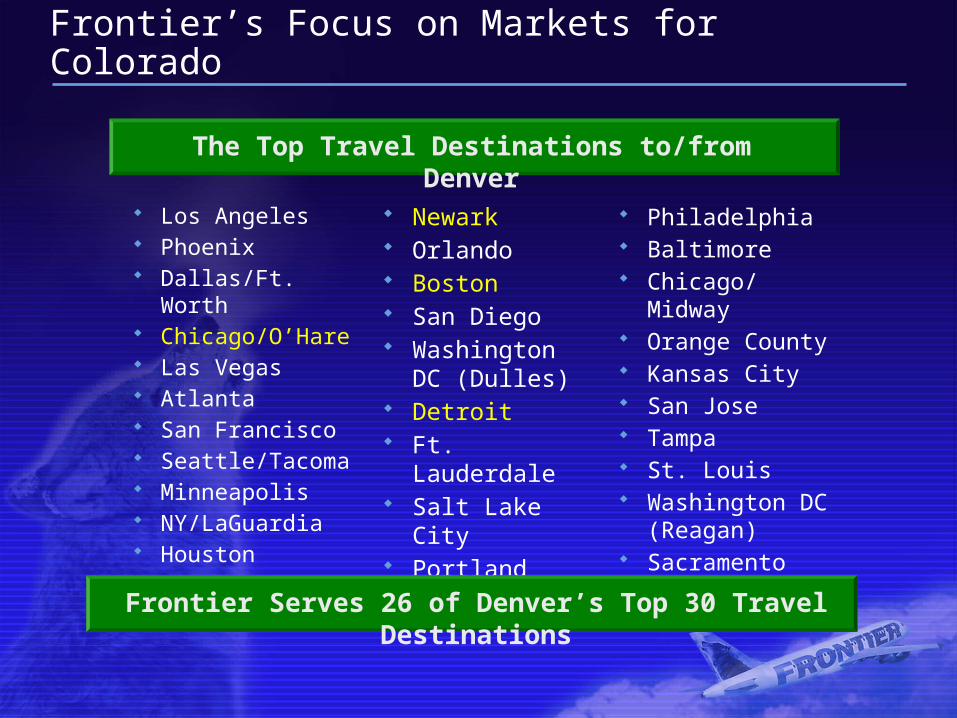

Frontier’s Focus on Markets for Colorado

Los Angeles Phoenix Dallas/Ft. Worth Chicago/O’Hare Las Vegas Atlanta San Francisco Seattle/Tacoma Minneapolis NY/LaGuardia Houston

Newark Orlando Boston San Diego Washington DC

(Dulles) Detroit Ft. Lauderdale Salt Lake City Portland

The Top Travel Destinations to/from Denver

Philadelphia Baltimore Chicago/Midway Orange County Kansas City San Jose Tampa St. Louis Washington DC

(Reagan) Sacramento

Frontier Serves 26 of Denver’s Top 30 Travel Destinations

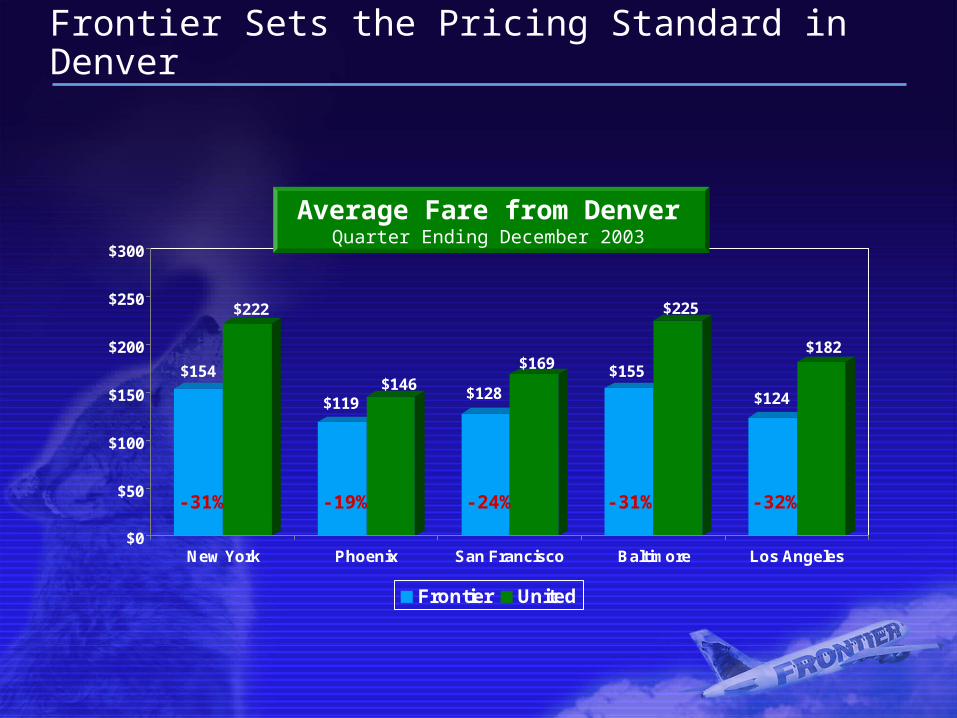

Frontier Sets the Pricing Standard in Denver

$154

$222

$119$146

$128

$169 $155

$225

$124

$182

$0

$50

$100

$150

$200

$250

$300

New York Phoenix San Francisco Baltimore Los Angeles

Frontier United

Average Fare from DenverQuarter Ending December 2003

-31% -19% -24% -31% -32%

Impact of Increased Competition…Lower Fares

LCC Growth at Denver International Airport

And Effect on Fares

Departures

Seats

Average Fares:

Top 50 Markets

Other Markets

Total

2001

10.5%

12.4%

$188

$192

$189

2002

15.0%

16.8%

$163

$168

$164

2003

17.5%

19.8%

$144

$153

$145

03 v 01

65.3%

51.7%

-23.5%

-20.1%

-22.9%

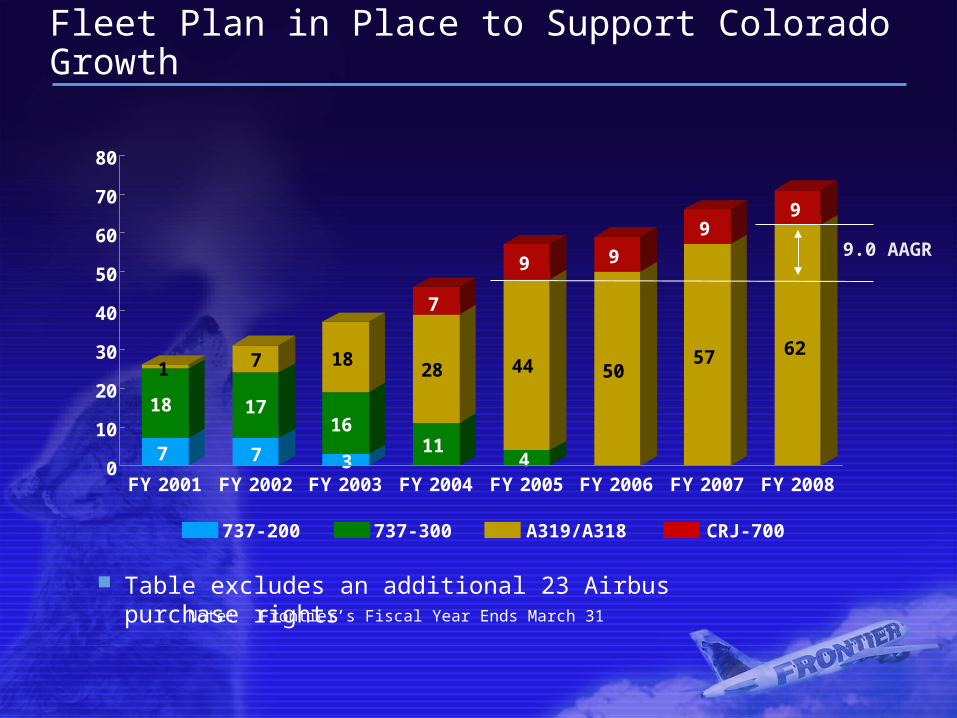

7

18

1

7

17

7

3

16

18

11

28

7

4

44

9

50

9

57

9

62

9

0

10

20

30

40

50

60

70

80

FY 2001 FY 2002 FY 2003 FY 2004 FY 2005 FY 2006 FY 2007 FY 2008

Fleet Plan in Place to Support Colorado Growth

Note: Frontier’s Fiscal Year Ends March 31

Table excludes an additional 23 Airbus purchase rights

737-200 737-300 A319/A318 CRJ-700

9.0 AAGR

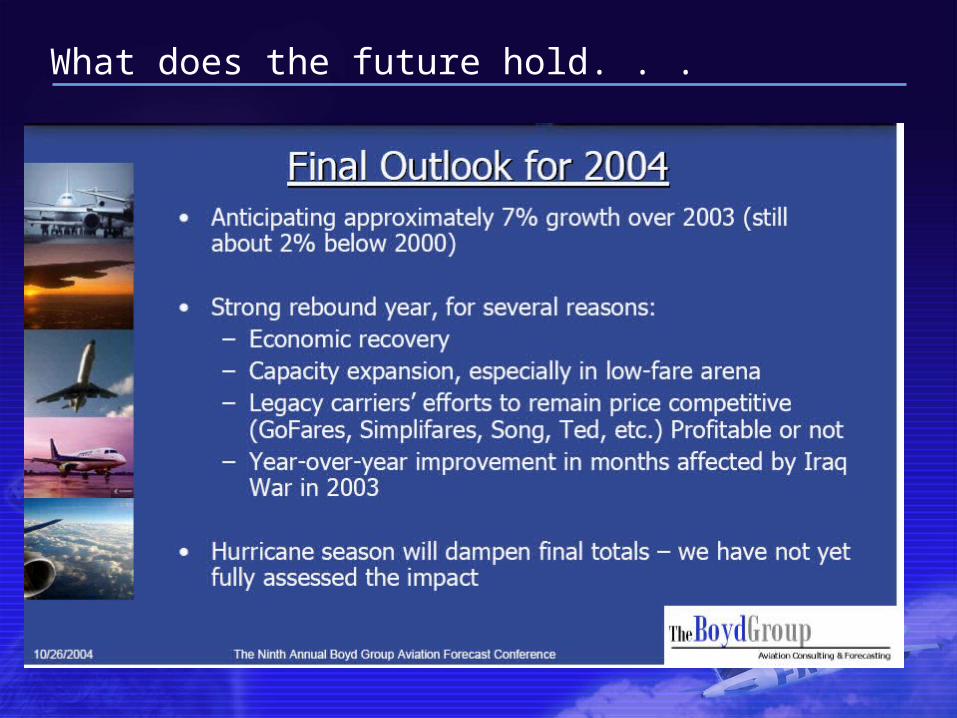

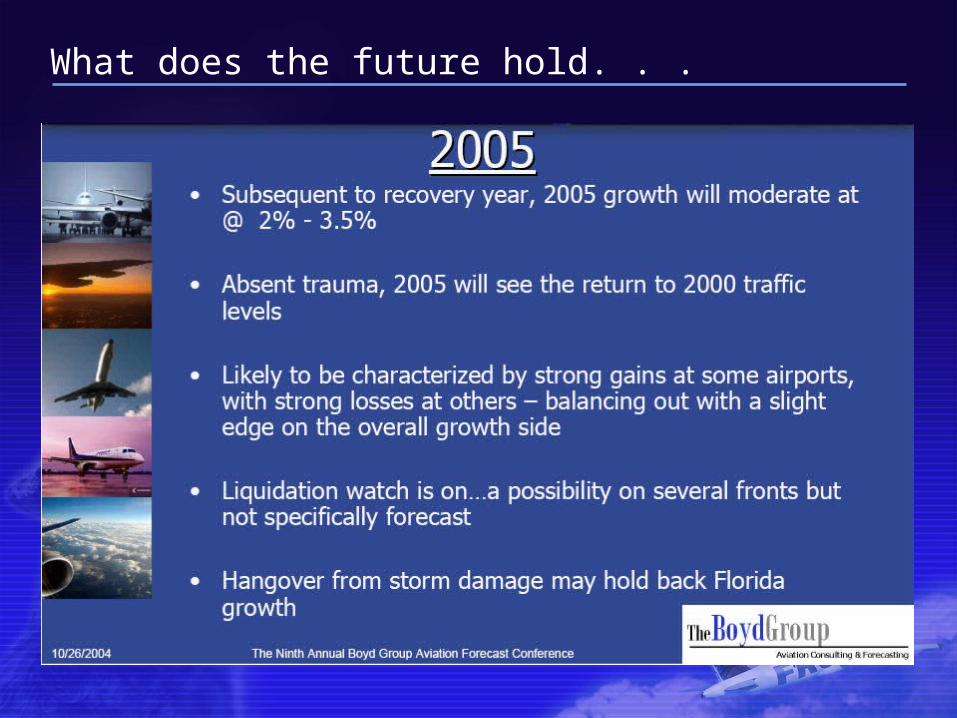

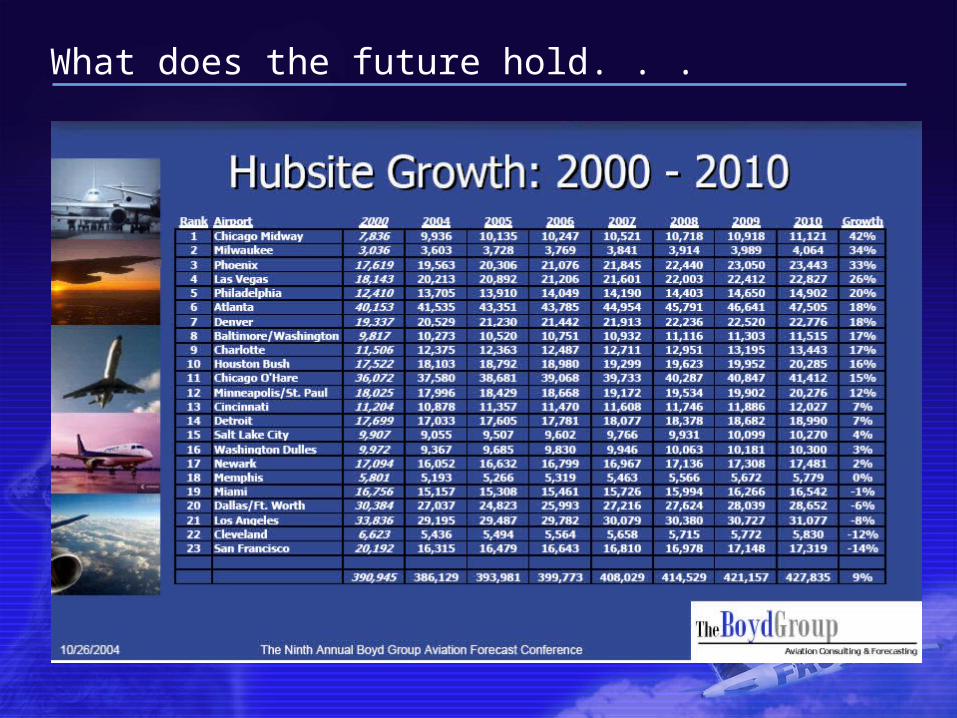

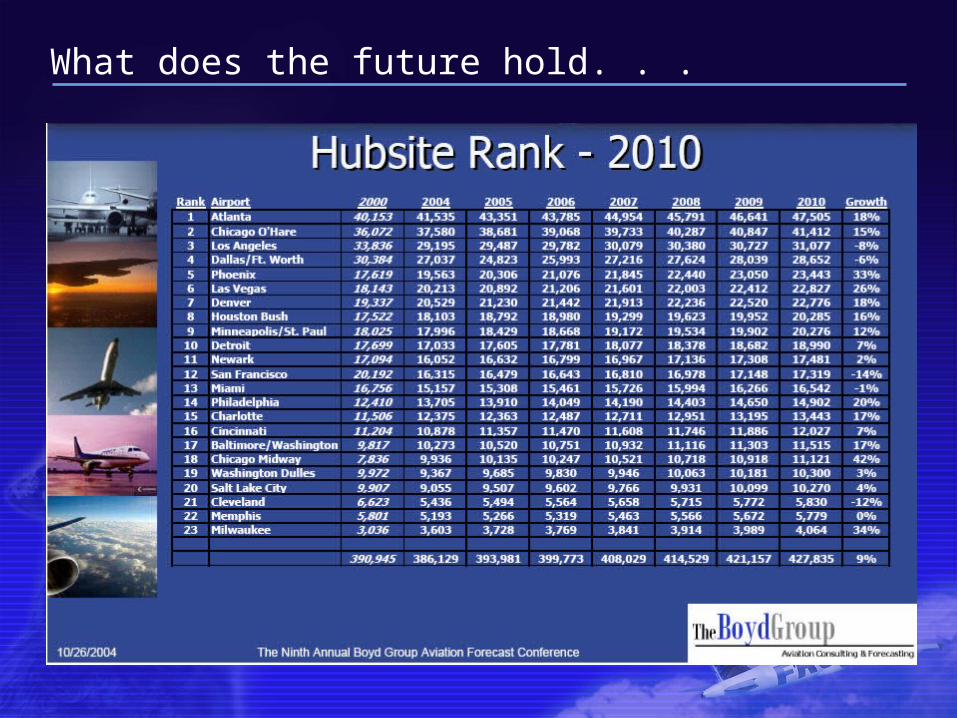

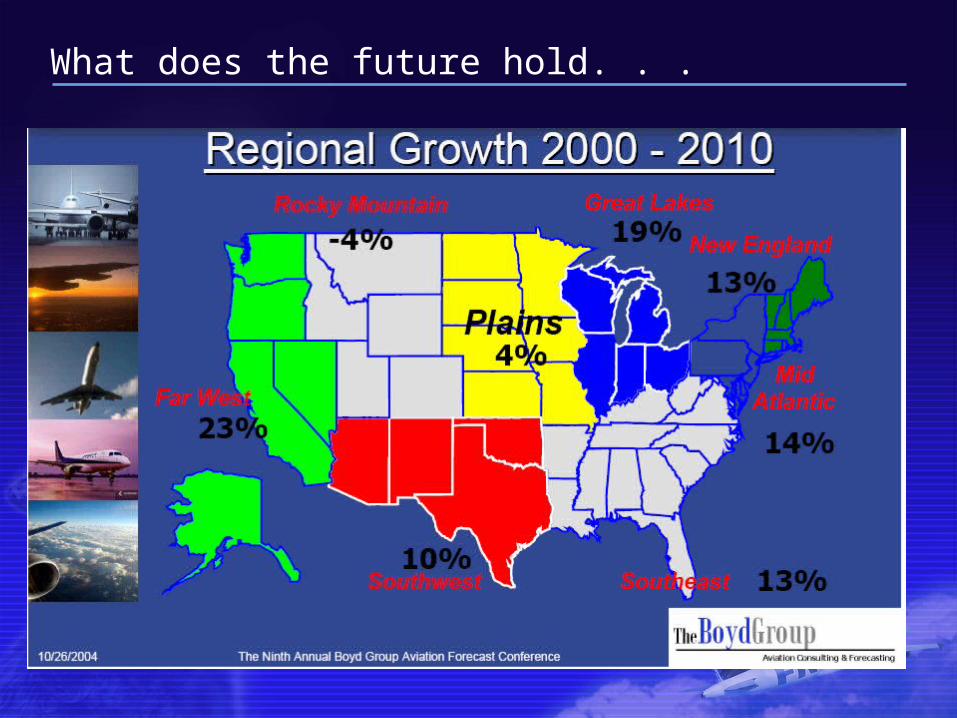

What does the future hold. . .

What does the future hold. . .

What does the future hold. . .

What does the future hold. . .

What does the future hold. . .

What does the future hold. . .

What does the future hold. . .

What does the future hold. . .

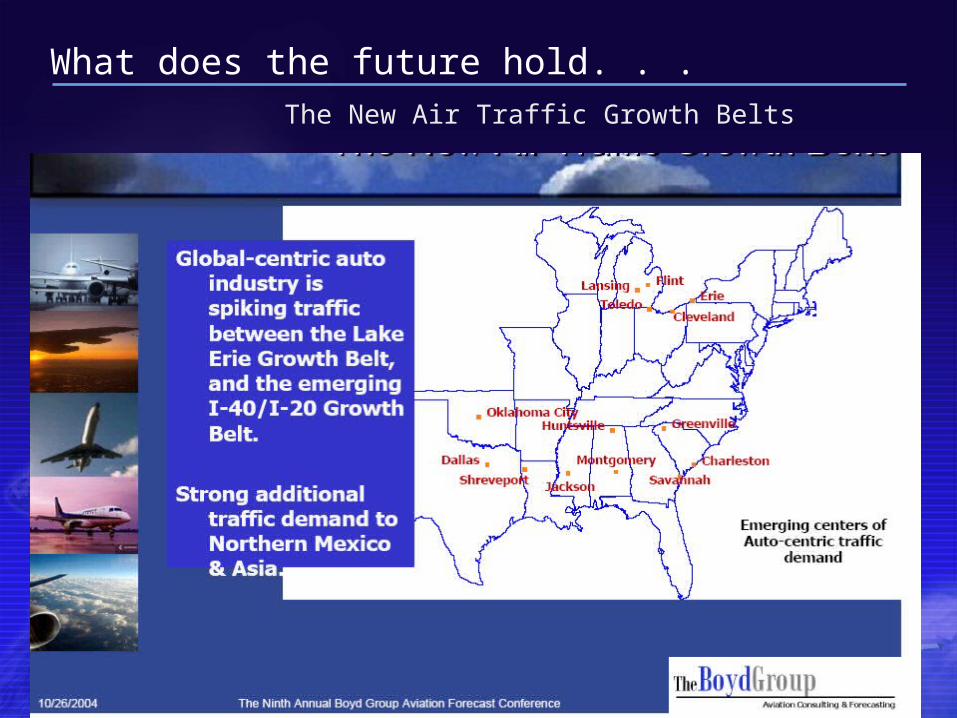

What does the future hold. . . The New Air Traffic Growth Belts

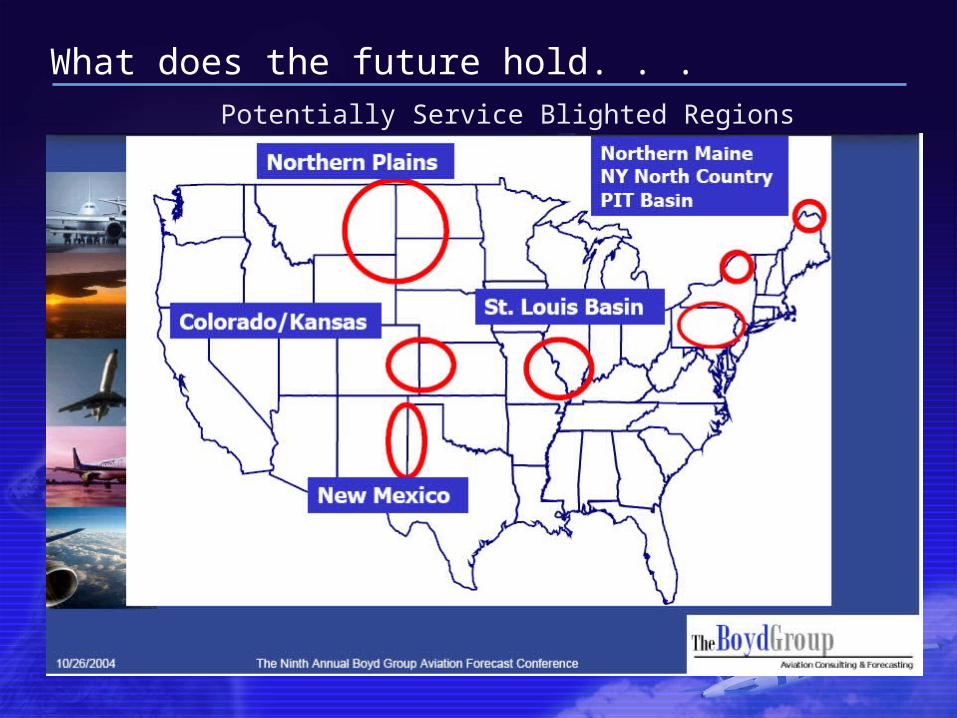

What does the future hold. . . Potentially Service Blighted Regions

Why are Airports, Airlines and Frontier Important to Real Estate?

National Economic Impact

Aviation Facilitates Economic Growth

— 2000 GDP Contribution: $900B or 9% of GDP

Employment

— Job Contribution: 11MM or 7% of US Employment

— Half of Post-9/11 U.S. Job Loss is Aviation and Travel Related

Investments

— From 2000 to 2012: Investments in Airports could mean and additional $31B for the US Economy

Why are Airports, Airlines and Frontier Important to Real Estate?

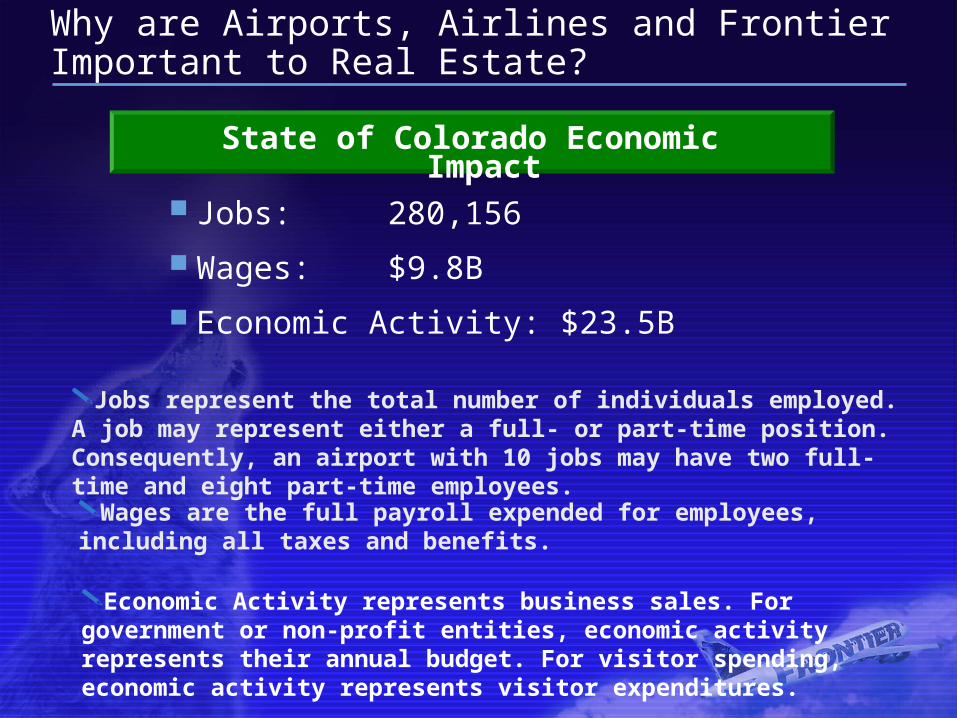

Jobs represent the total number of individuals employed. A job may represent either a full- or part-time position. Consequently, an airport with 10 jobs may have two full-time and eight part-time employees.

Wages are the full payroll expended for employees, including all taxes and benefits.

Economic Activity represents business sales. For government or non-profit entities, economic activity represents their annual budget. For visitor spending, economic activity represents visitor expenditures.

Jobs: 280,156

Wages: $9.8B

Economic Activity: $23.5B

State of Colorado Economic Impact

Why are Airports, Airlines and Frontier Important to Real Estate?

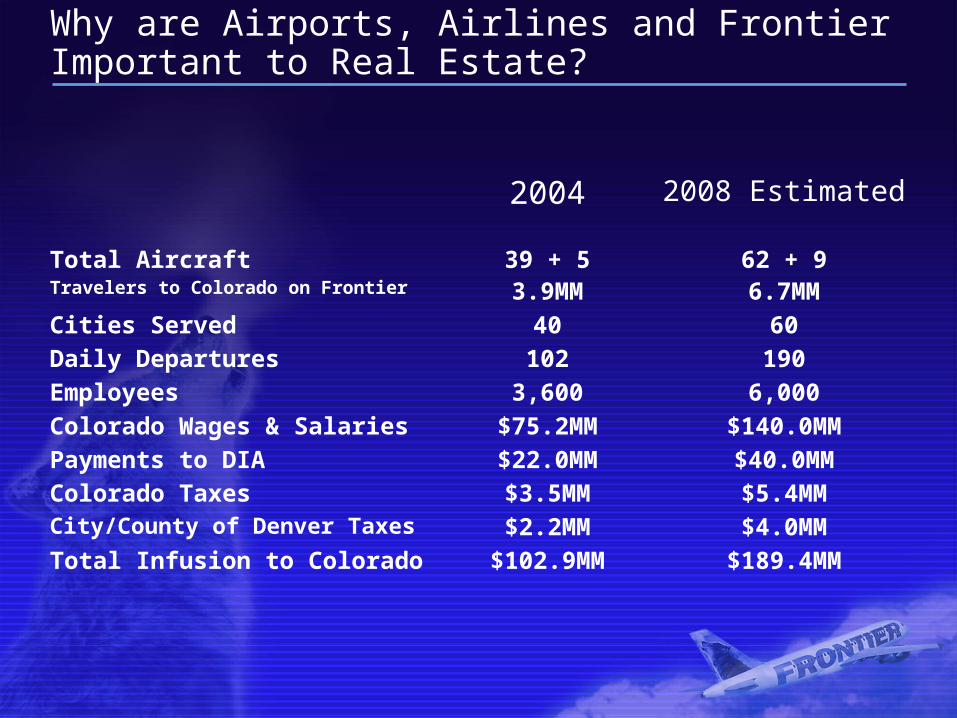

190102Daily Departures

2008 Estimated2004

62 + 939 + 5Total Aircraft6.7MM3.9MMTravelers to Colorado on Frontier

6040Cities Served

6,0003,600Employees

$140.0MM$75.2MMColorado Wages & Salaries

$40.0MM$22.0MMPayments to DIA

$5.4MM$3.5MMColorado Taxes

$4.0MM$2.2MMCity/County of Denver Taxes

$189.4MM$102.9MMTotal Infusion to Colorado

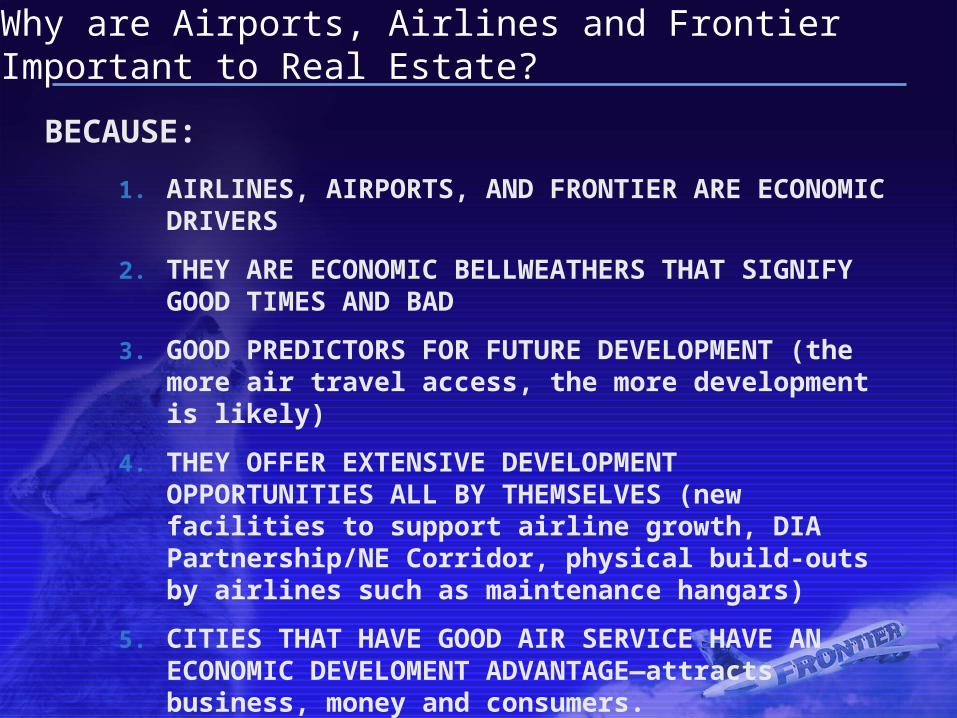

1. AIRLINES, AIRPORTS, AND FRONTIER ARE ECONOMIC DRIVERS

2. THEY ARE ECONOMIC BELLWEATHERS THAT SIGNIFY GOOD TIMES AND BAD

3. GOOD PREDICTORS FOR FUTURE DEVELOPMENT (the more air travel access, the more development is likely)

4. THEY OFFER EXTENSIVE DEVELOPMENT OPPORTUNITIES ALL BY THEMSELVES (new facilities to support airline growth, DIA Partnership/NE Corridor, physical build-outs by airlines such as maintenance hangars)

5. CITIES THAT HAVE GOOD AIR SERVICE HAVE AN ECONOMIC DEVELOMENT ADVANTAGE—attracts business, money and consumers.

Why are Airports, Airlines and Frontier Important to Real Estate?

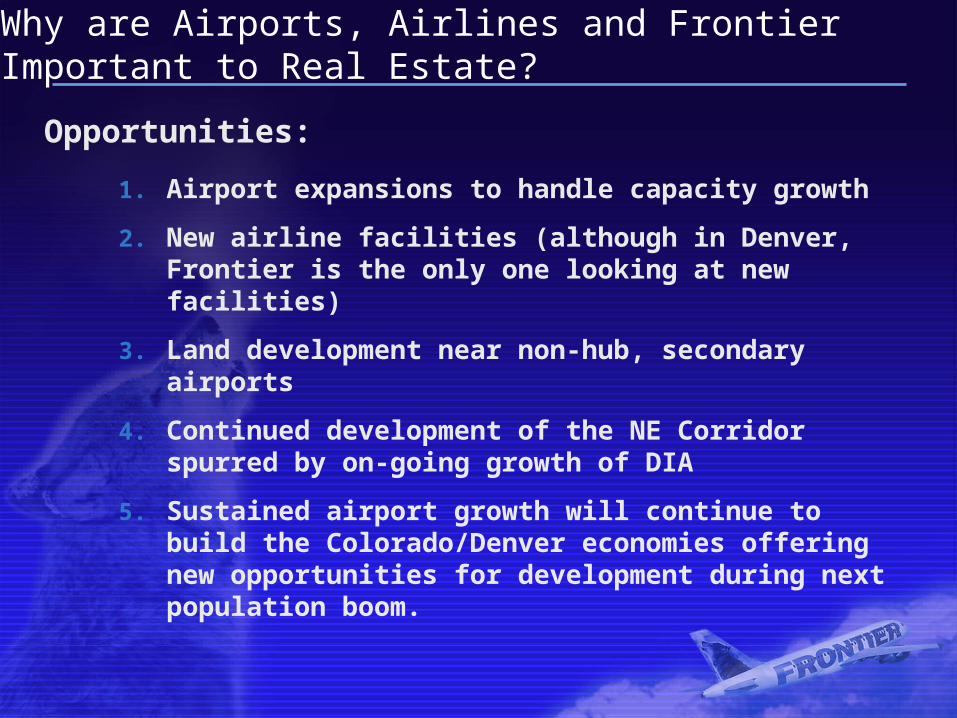

BECAUSE:

1. Airport expansions to handle capacity growth

2. New airline facilities (although in Denver, Frontier is the only one looking at new facilities)

3. Land development near non-hub, secondary airports

4. Continued development of the NE Corridor spurred by on-going growth of DIA

5. Sustained airport growth will continue to build the Colorado/Denver economies offering new opportunities for development during next population boom.

Why are Airports, Airlines and Frontier Important to Real Estate?

Opportunities:

Just for Fun

American Cuisine

Binoculars

Just for Fun

EarlyReturns

Mexico

Just for Fun

Snow

Underwear