Languages

Pages

Legal

LIFE INSURANCE:

THE CASE FOR CHANGE—

HOW DO WE MAKE LIFE INSURANCE SUSTAINABLE AND

FIT FOR PURPOSE IN A WORLD OF TECHNOLOGICAL

CHANGE AND EVOLVING RISKS?

WEALTH INSIGHTS

—

CONTENTS

CHAPTER ONE

Trust in insurance has been eroded

Page 2

—

CHAPTER TWO

Pricing pressure is increasing

Page 8

—

CHAPTER THREE

The sector is vulnerable to high-tech disruptors

Page 16

—

CHAPTER FOUR

Focusing on health and wellbeing

Page 22

—

CHAPTER FIVE

The Millennial challenge

Page 28

—

CHAPTER SIX

The data and analytics advantage

Page 34

—

CONCLUSION

Page 41

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 2 PAGE 3

Public controversies have undermined consumer confidence in life insurance, creating opportunity for insurers to respond positively with more transparent

products that fulfill the core purpose of insurance.

PUBLIC CONFIDENCE IN LIFE INSURANCE HAS DECLINED

Over the past few years a spate of highly publicised incidents of mis-selling and controversial claims decisions have led to a measurable decline in the public’s confidence in life insurance. Brought to light by media investigations and official inquiries, these incidents have fostered a perception of serious cultural problems across the sector.

An April 2016 survey by PwC found that, while 78 per cent of Australians viewed life insurance as important, only 42 per cent believed their life insurer would be there for them in their time of need.¹ This sentiment was echoed by Roy Morgan Research, which revealed a decline in satisfaction with life insurance products. In the 12 months

to December 2016, life and risk insurance recorded the lowest customer-satisfaction level of any insurance type, with only 23.9 per cent of policyholders saying they were “very satisfied”.²

Popular perceptions of the sector were encapsulated in a submission from consumer group CHOICE to the recently concluded inquiry into the life insurance industry by the Parliamentary Joint Committee on Corporations and Financial Services, which stated: “Recent scandals have demonstrated that when a consumer claims on life insurance there can be a big gap between the quality and coverage that is expected and what is actually delivered.” ³

It must be emphasised that these reported perceptions are not representative of the actual experiences of most insurance customers. According to a 2016 Australian Securities and Investments Commission report, 90 per cent of life insurance claims made between 2013 and 2015 were paid in the first instance, including 96 per cent of claims for life cover and 93 per cent of claims for income protection.⁴ Nevertheless, a public narrative of falling confidence has the potential to damage a sector whose products promise enduring peace of mind; it is also likely to exacerbate Australia’s chronic underinsurance problem.

CHAPTER ONE

TRUST IN INSURANCE HAS BEEN ERODED

KEY POINTS

1 PwC, ‘Future of life insurance in Australia’, 2017

2 Roy Morgan Single Source (Australia), 2017

3 CHOICE, Submission 49 to the Parliamentary Joint Committee on Corporations and Financial Services Inquiry into the Life Insurance Industry, 2016

4 ASIC, ‘Life insurance claims: An industry review’, Report 498, 2016

Media investigations and public inquiries have highlighted instances of poor service, eroding public confidence.

Regulatory activity is intensifying, requiring a greater commitment of resources from service providers.

Insurers who respond positively, with common sense, clear products, can help restore confidence and win a lasting competitive advantage.

Proportion “very satisfied” or “fairly satisfied”

42%

ONLY 42 PER CENT OF

AUSTRALIANS BELIEVE

THEIR LIFE INSURER WILL

BE THERE FOR THEM IN

THEIR TIME OF NEED

Figure 1.1 Customer satisfaction with insurance by type²

Base = Australians 14+

( ) = % point change from 2015

82.6% (-0.9%)

80.3% (-1.4%)

Comprehensive car

Household contents

Household building79.9% (-1.2%)

Third-party property car75.7% (-0.5%)

67.4% (-1.4%)

66.3% (-1.9%)

68.7% (-0.8%)

73.6% (-2.3%)

Private health

Life

Risk

Total risk and life

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

declined declined

declined declined

paid

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 4 PAGE 5

REGULATORY SCRUTINY IS SET TO INTENSIFY

These negative public perceptions have been accompanied by an upsurge in public scrutiny by regulators and industry bodies.

Recent initiatives include:

• Australian Prudential Regulation Authority (APRA) 2013 requirements on risk culture, implemented under Prudential Standard CPS 220 (Risk Management)

• ASIC’s 2014 review of life insurance advice and 2016 review of life insurance claims practices

• The 2015 Trowbridge review of retail life insurance advice, commissioned by the Association of Financial Advisers and the Financial Services Council (FSC)

• The release of the FSC’s Life Insurance Code of Practice, which became effective on July 1, 2017

• The life insurance industry inquiry by the Parliamentary Joint Committee on Corporations and Financial Services Inquiry, due to report by October 31, 2017.

This high level of regulatory activity is set to intensify. Recommendations made by ASIC, the Parliamentary Joint Committee and the recent Financial System Inquiry appear likely to result in further change and increased oversight. While many of these changes could lead to better outcomes for consumers and insurers, they will require greater organisational resources and energy from the sector.

At the same time as regulatory activity is increasing, there is growing need for insurers to invest in innovation amid rapid technological change and declining margins. In this scenario, heightened compliance requirements have the potential to absorb valuable resources that could otherwise be dedicated to product innovation.

Regulation may inhibit another important aspect of innovation in the sector: the ability to leverage alternative data sources for underwriting, allowing insurers to create personally tailored policies at more

affordable rates, and reduce the risk of declined claims due to non-disclosure.

The opportunity for insurers here is to accept not just the letter but the spirit of regulatory concerns, by creating transparent, core-purpose insurance products that are clearly communicated to the market.

Transparency in product design may become more important as insurers introduce innovative, technology-driven solutions for underwriting and product delivery. And such an approach will also go some way to re-establishing trust and positioning insurance and insurers in a more positive light to the market and authorities.

Life Income protection

Trauma Total permanent disability

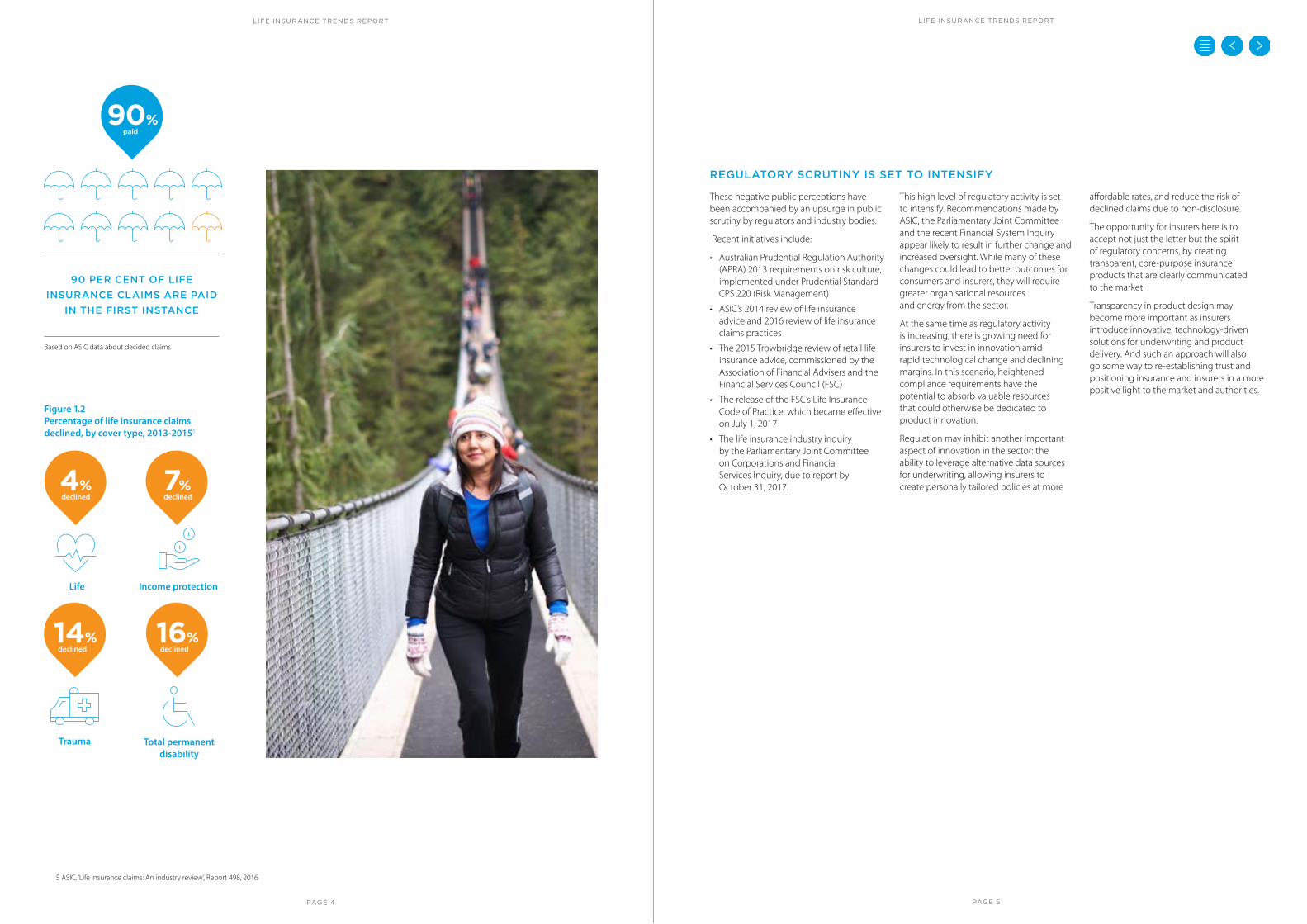

Figure 1.2 Percentage of life insurance claims declined, by cover type, 2013-20155

4% 7%

14% 16%

90%

Based on ASIC data about decided claims

90 PER CENT OF LIFE

INSURANCE CLAIMS ARE PAID

IN THE FIRST INSTANCE

5 ASIC, ‘Life insurance claims: An industry review’, Report 498, 2016

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 6 PAGE 7

COMPLEX PRODUCTS ADD TO CONFUSION AND UNDERINSURANCE

Underinsurance remains a significant issue in Australia, as has been widely observed. PwC research shows that, while Australians generally believe they have adequate cover, Australian life insurance premiums represent a significantly smaller proportion of gross domestic product than in comparable developed countries –Sweden is 50 per cent higher than Australia, and Japan doubles our rate.6 Similarly, Rice Warner has found, based on the most recent available data, that the median level of life cover meets only 61 per cent of a family’s basic needs and 37 per cent of the income replacement level required to maintain current living standards until 65.7

A recurring theme of both media investigations and regulatory reviews has been that life insurance products are often complex, poorly understood by consumers, and largely undifferentiated – and that this complexity has contributed to consumers’ reluctance to take out adequate levels of cover. For example, in its submission to the Parliamentary Joint Committee, CHOICE commented that: “Central to restoring confidence in this sector will be giving assurance to consumers that products

reflect their expectations and that they won’t be denied claims on the basis of fine-print technicalities.” 8

The Financial Services Council has acted to address the issue of complexity by developing minimum medical definitions for some of the most common causes of claim, including heart attack, stroke and cancer. Among others, Australia and New Zealand Banking Group (ANZ) has supported the implementation of standard, minimum medical definitions for life insurance cover to allow for greater consistency and to enable customers to more easily compare policies.9

The sector can do more to help consumers by introducing simpler, clearer product documentation. An important first step would be the development of a concise key fact statement for life insurance products, helping to explain risks, inclusions and fees without consumers needing to search lengthy product disclosure statements, which are often more than 100 pages long.9

It should be noted that financial advisers already play an important role here. They are a very significant partnership channel for

life insurers and act as a relatable interface between what are sometimes necessarily complex products and customers in need.

The packaging of advice with an insurance product is already an effective solution for addressing customer confusion. But room remains for insurers to expand the range of products advisers can offer clients, especially those who may struggle with cost and are looking for straight forward cover.

The final piece of the puzzle is likely to be the introduction of more targeted and clearly differentiated products that leverage new technologies for seamless, personalised underwriting and tailored communications, which this paper will explore. Importantly, introducing clearer products does not necessarily mean restricting or reducing the depth of cover, simply a return to the core purpose of insurance: helping to restore claimants to the state of health and prosperity they enjoyed before they became sick or injured, so they can resume their place in the workforce and continue to enjoy full and satisfying lives.

Insurers who choose a progressive response to regulation, media scrutiny and public criticism, and who accept the implicit challenge to become more transparent, can help restore consumer confidence and gain a lasting competitive advantage.

Consumers want more targeted and clearly differentiated insurance products, presented in an easy-to-understand way, supported by clear, engaging communications.

Increased adviser transparency (including transparency on fee structures) as well as product choice, will provide much-needed clarity and reassure consumers their best interests are being recognised.

As the market evolves and products become more differentiated, a life insurer’s identity (i.e. what its brand stands for) and consumer focus will be critical factors in re-establishing trust and winning new customers.

More affordable, common sense products can help restore trust and address underinsurance, by bringing insurance back to its core purpose and making it more affordable and transparent.

OPPORTUNITIES FOR CHANGE

6 PwC, ‘Future of life insurance in Australia’, 2017

7 Rice Warner, ‘Underinsurance in Australia 2015’, 2016

8 CHOICE, Submission 49 to the Parliamentary Joint Committee on Corporations and Financial Services Inquiry into the Life Insurance Industry, 2016

9 ANZ, Submission 44 to the Parliamentary Joint Committee on Corporations and Financial Services Inquiry into the Life Insurance Industry, 2016

61%

ONLY 61 PER CENT OF A

FAMILY'S BASIC NEEDS ARE

COVERED BY THE MEDIAN

LEVEL OF LIFE COVER

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 8 PAGE 9

Loss-making disability policies highlight the need for a broader range of products to create a stronger, more sustainable sector for the future.

RISING COSTS HAVE PUT SUSTAINABILITY AT RISK

Contrary to public perceptions, not all life insurance products are highly profitable – especially at a time when insurers are investing in innovation and product design to keep pace with a rapidly evolving market and relentless technological change. And while many (but not all) insurers are subsidiaries of financial institutions that generate healthy returns, they rarely cross-subsidise life-insurance divisions. This bigger issue is insurers' subsidising unprofitable products with profitlable ones, which is not in the best interests of consumers, investors or the financial system.

According to the Australian Prudential Regulation Authority (APRA), net profit after tax across the Australian life insurance sector declined by 20 per cent in the year to March 2017, with the overall return-on-net-assets figure falling to 10 per cent.

More importantly, insurers continue to make losses on disability products, particularly individual disability cover, as claim costs rise rapidly. Over the past three years the sector has lost more than $1 billion on individual disability policies, including $427 million in the year to March 2017.10

Figure 2.1 Life insurers’ return on net assets11

CHAPTER TWO

PRICING PRESSURE IS INCREASING

10 APRA, Submission 50 to the Parliamentary Joint Committee on Corporations and Financial Services Inquiry into the Life Insurance Industry, 2016

11 APRA, ‘Quarterly life insurance performance statistics’, March 2017

KEY POINTS

$1 BILLION ON INDIVIDUAL

DISABILITY POLICIES HAS

BEEN LOST OVER THE PAST

THREE YEARS

Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015 Mar 2016 Mar 2017

Rolling 12 months

Rising claim costs have put the sustainability of some life insurance products at risk.

Affordability for consumers remains an important issue, impacting levels of cover.

Targeted products and lower-cost, technologically enabled channels have the potential to overcome pricing problems and create a more sustainable and responsive sector.

1billion

20

15

10

5

% pa

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 10 PAGE 11

Figure 2.2 Net profit after tax from insurance risk products ($bn)12

Year ended March

Group lump sum

Group disability income insurance

Individual lump-sum risk

Individual disability income insurance

These figures suggest that while mortality risk products (paying a lump sum after an insurance event) remain financially sustainable, many morbidity policies (with regular payments over time to an ill or disabled claimant) are not, at least as they are currently formulated.

Insurers have been able to cross-subsidise these loss-making products, but this is not a sustainable approach. Cross-subsidisation leads to:

• inequitable outcomes for:

– consumers (who are forced to pay more for other products to help cover rising costs)

– shareholders (who earn a lower return on equity)

• risk for the long-term financial sustainability of the institutions (as investors seek out more profitable alternatives).

None of these outcomes is in the interests of consumers or of regulators, who rely on insurers remaining stable and well funded by generating consistently healthy returns over the long term. As APRA commented in its submission to the Parliamentary Joint Committee Inquiry into the Life Insurance

Industry: “Consumers of long-term products such as life insurance are ultimately best served if insurers are financially sustainable, thereby enabling firms to deliver on their long-term promises.”13

That means it is in no one’s interest for returns to become volatile or uncertain, especially as changing trends in disability (such as a rise in mental health claims) make the need for reliable cover even more important. Above all, policyholders want to be confident that their insurer is here for the long term – which means that every product and policy needs to be financially sustainable.

This is not to say there is anything actually wrong with existing products in the market. They perform their function and are perfectly suitable for particular segments. It's the cost to insurers that is problematic.

A broader choice of life insurance products with different price points will create a more sustainable sector by appealing to a broader market, giving financial advisers more to offer, with a net effect of more people taking out cover, and therefore helping insurers balance some of the risk they face in this area, particularly through morbidity policies.

-1

0

1

2

$bn

2010 2011 2012 2013 2014 2015 2016 2017

12 APRA, ‘Quarterly life insurance performance statistics’, March 2017

13 APRA, Submission 50 to the Parliamentary Joint Committee on Corporations and Financial Services Inquiry into the Life Insurance Industry, 2016

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 12 PAGE 13

WHY ARE PRICING PRESSURES RISING?

Pricing life insurance products can be uniquely challenging, given the need to accurately forecast long-tail risks which could extend for decades. Today’s pricing pressures are driven by an upsurge in claims on disability policies originally designed in the early 2000s when the world was a very different place. Since then we have experienced an almost unprecedented level of change in technology, the workplace environment and the economy.

The following five key factors have contributed to a deteriorating claims experience.

14 Financial Services Council, Submission 26 (Supplementary) to the Parliamentary Joint Committee on Corporations and Financial Services Inquiry into the Life Insurance Industry, 2016

Changed claimant behaviour

There are some indications that claimants are, in some instances, adjusting their lifestyles to take advantage of their policy benefits in ways that weren’t envisaged when those policies were designed. For example, a clause intended to help self-employed individuals work a minimum number of hours to keep their businesses operating, facilitating an early return to work, could potentially be used to help a claimant earn a full-time salary while working part time.

While these behaviours are legitimate, they do suggest the need for better-designed products that more accurately target the original objective of disability insurance: to help an injured person recover and re-enter the workforce without financial stress.

The growing complexity of work

Technological change and a more complex work environment have made it more difficult for temporarily disabled claimants to return to work, as they lose touch with rapid workplace changes. This issue has been exacerbated by Australia’s economic transition in the wake of the global financial crisis, with cost-cutting increasing pressure on employees, and the recent decline in mining investment leaving some sectors of blue-collar workers with an uncertain future.

Rise in mental health claims

According to the Financial Services Council, the life insurance sector has been paying a large and growing proportion of benefits for claims relating to mental-health conditions, accounting for up to 30 per cent of income-protection claims for some providers.14

In part, this is the result of a positive social change, with people now more willing to recognise and address mental health issues. However, it also reflects the challenges of re-entering the workforce at a time of increasing complexity, and the effects of social isolation on those unexpectedly left unable to work. Many claimants cease work due to a physical condition, then remain out of the workforce as a result of consequential mental-health impacts.

Broad policy terms

In the early 2000s, competitive pressures led Australian insurers to introduce some of the world’s broadest disability policy terms. For example, many policies allow claimants to:

• qualify as disabled if they are unable to perform just one of the key duties of their own occupation, instead of all or most of them

• continue to receive a benefit while working a limited number of hours each week or earning a proportion of their pre-existing income (a measure originally intended to help self-employed people keep their businesses operating, and facilitate a faster return to work, this benefit has become increasingly relevant with the rise of the gig economy).

1 3

2

4

Lower investment returns

At the same time, insurers have been affected by a low-return environment that has reduced investment returns on the premium pool, further impacting their financial position.

5

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 14 PAGE 15

15 Australian Bureau of Statistics, Wage price index, Australia, March 2017 (Release 6345)

16 Reserve Bank of Australia, Household sector chart pack, July 2017

17 ME, Household financial comfort report, 2017

18 Australian Bureau of Statistics, Population projections, Australia, 2012 (base) to 2101, Australia, November 2013 (Release 3222.0)

By providing more targeted products, that focus on the core purpose of returning disabled claimants to health, insurers can create a clear point of difference while providing a critical service at an affordable price, to the benefit of consumers and advisers.

Insurers can also reduce costs and create better outcomes for policyholders by collaborating with health providers to accelerate their return to work, using rapid triage to refer clients to personalised programs tailored to their needs.

Insurers are likely to increase their focus on products targeted to the specific needs of people at different life stages, including over-65s, with individualised pricing linked to health and wellbeing incentives.

OPPORTUNITIES FOR CHANGE

THERE IS LITTLE RELIEF IN SIGHT

While insurers have responded to pricing pressures by lifting premiums, this will only provide short-term relief and will not address the longer-term issues for these products. Meanwhile, the affordability of cover has become an important issue, and is likely to remain so for the foreseeable future.

At a time when wage growth is at record lows15 and household debt is at record highs,16 many Australian households are becoming worried about the rising costs of necessities such as energy, fuel and groceries, with one in two saying they have no cash left over at the end of each month.17

As a result, many are cutting back on recurring expenses – something that could

lead them to reduce their levels of cover or remain underinsured.

Meanwhile, an ageing population is likely to lead to increasing claims, with predictions that one in five Australians will be aged over 65 by 2046.18

The only real choice is for insurers to create a more sustainable life insurance sector, by broadening their product offering, particularly with those that focus on the core purpose of keeping people financially afloat as they seek to return to work.

Such commonsense, more affordable products will be more sustainable for consumers, help create more sustainable businesses for advisers, as well as insurers themselves.

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 16 PAGE 17

Insurers need to adapt rapidly to thrive in the emerging FinTech ecosystem, or risk declining market share.

DIGITAL DISRUPTION IS RESHAPING THE ECONOMIC LANDSCAPE

The past 10 years have demonstrated the potential for high-tech disruptors to reshape industries and displace iconic companies. To cite one familiar example, while traditional news mastheads have seen subscriptions slump, rival digital start-ups such as BuzzFeed have become the news sources of choice for millions of consumers, made particularly accessible through social media.

Importantly, these disruptors do not owe their success to providing a higher-quality product than the incumbents. They simply deliver a low-cost (or no-cost) offering that is ‘good enough’, through a channel better geared to changing consumer preferences. This approach gives new entrants time to build market share and improve quality while keeping costs down – a tactic likely to be paralleled by insurtech innovators looking to build a presence among the uninsured and underinsured.19

And investment in insurtech has been surging over the past few years, with 496 venture-capital-backed deals globally

worth around $US8 billion in the first half of 2017 alone, according to CBInsights.20 While much of that activity has centred on general insurance, it is indicative of the growing potential for change across the life insurance sector. As a result, three in four insurance companies around the globe believe that some part of their business is at risk of disruption, according to PwC.21

Tech disruptors are also infiltrating the medical device community in ways likely to impact insurance markets in the very near future. Verily Life Sciences, formerly known as Google Life Sciences, has created a joint venture with healthcare giant Sanofi to develop “comprehensive solutions that combine devices, software, medicine and professional care to enable simple and intelligent disease management”.22 Verily projects include the Google Contact Lens, which measures the blood-glucose levels of people with diabetes “in the blink of an eye” – data likely to prove invaluable to the high-tech insurers of the future.

Figure 3.1 Disruptors threaten incumbents with low-cost products offering ‘good enough’ quality20

CHAPTER THREE

THE SECTOR IS VULNERABLE TO HIGH-TECH

DISRUPTORS

KEY POINTS

Partnerships between trusted brands and tech-savvy start-ups have the potential to disrupt established businesses and reshape the insurance sector.

Emerging data and analytics capabilities are set to change insurance from a business focused on risk processes to a business powered by insights.

To remain sustainable, insurers must meet customer expectations for rich and responsive digital experiences.

s

Prod

uct q

ualit

y

Time

THREE IN FOUR INSURANCE

COMPANIES AROUND THE

GLOBE BELIEVE THAT SOME

PART OF THEIR BUSINESS IS

AT RISK OF DISRUPTION

19 Gen Re, ‘Disruption innovation – Coming to life insurance near you’, 2016

20 CBInsights, ‘The global fintech report’, Quarter 2, 2017

21 PwC, ‘Opportunities await: How insurtech is reshaping insurance’, Global FinTech Survey, 2016

22 Verily Life Sciences, verily.com, 2017

‘Good enough’ for many customers

Disruptor

Incumbent

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 18 PAGE 19

23 Verily Life Sciences, verily.com, 2017

24 Capgemini and Efma, ‘World insurance report 2016’

25 Capgemini, ‘Top 10 trends in insurance in 2016’

26 Australian Treasury, ‘Backing Australian FinTech’, fintech.treasury.gov.au/australias-fintech-priorities

Figure 3.2 Global, venture-capital-backed FinTech investment ($USbn)23

These new entrants could pose a significant competitive threat to established insurers – especially among the next generation of digitally savvy customers, who are less likely to be satisfied with the status quo. Research shows that while 47 per cent of insurance (all categories) customers around the world say they have positive experiences with their insurer, only 34 per cent of Millennial customers say they do, and that these young consumers have a high level of trust in technology companies and social media.24 As a result, they are the generation most likely to buy new insurance offerings from high-tech companies entering the industry through partnerships, alliances, joint ventures and acquisitions.25

THE POWER OF PARTNERSHIPS

Until now, the life insurance sector has been largely sheltered from disruption due to the substantial regulatory requirements insurance providers must meet, posing a significant barrier to new entrants. But while a focus on rigorous risk processes has enabled insurers to succeed in the past, it has also made them relatively slow to adopt new technologies.

One likely way forward is for insurers to partner with high-tech innovators, combining their risk-management expertise with the agility and technological expertise

of a start-up. In general insurance, the recent partnership between Suncorp’s AAI and on-demand insurance app developer Trōv is a case in point (page 19). But the window of opportunity for incumbents may be closing.

At the end of 2016, the Australian government legislated a regulatory sandbox designed to allow “FinTech start-ups and innovators to develop, test and globally launch their innovative financial products and services” with the aim of “making

Australia the leading market for FinTech innovation and investment in Asia”. 26

The government noted: “Better information through big data can transform daily interactions by consumers with financial products and services, especially insurance.... The FinTech industry would like the Government to support increased flexibility to support emerging micro-insurance and quasi insurance models (e.g. self-funded excess and peer-to-peer insurance) which are not readily facilitated by current models”.26

CASE STUDY: TROV AND SUNCORP

Described as the world’s first on-demand insurance service, Trōv provides instant insurance cover for possessions through a mobile app. Launched in Australia in May 2016, the company secured $45 million in funding for its global expansion less than a year later.

Trōv operates in partnership with AAI, which underwrites Suncorp-branded policies and processes claims. Trōv’s business strategy is based on three key ingredients: on-demand, single-item and micro-duration policies.

Trōv addresses a number of pain points for insurance customers. By providing a mobile interface through which customers can upload sales receipts and photos of their contents, Trōv can sell more accurate policies with easier claims processes. Young consumers find its functionality familiar and easy to use: swipe right to start an insurance policy, then swipe left to end it as little as a day later.27

Q1 2015

Q2 2015

Q3 2015

Q4 2015

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Q1 2017

Q2 2017

27 Jonathan Shieber, ‘Trōv adds $45 million for the global expansion of its on-demand insurance’, TechCrunch, 2017; Rachel Botsman, ‘Scott Walchek, founder of on-demand insurance app Trōv’, The Australian Financial Review, 2016; Trōv, trov.com

1

2

3

4

5

6

0

250

300

200

Deals$bn

Deals

Funding volume

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 20 PAGE 21

Insurers can get ahead of the curve by disrupting themselves first, with a focus on their own strategic strengths. Creating a lasting point of difference will help life insurers to compete more effectively in a changing market.

Clearer and more engaging product design and communications will help to crowd out competitors, leaving less room for disruption.

Technology creates an opportunity for the insurance sector to evolve from ‘life protection’ to ‘life enrichment’, using personal data to create truly consumer-centric offerings.

In the longer term, insurance decisions are likely to be driven by timely communications designed to guide policyholders at critical points in their lives, underpinned by digital innovation focused on the customer experience.

OPPORTUNITIES FOR CHANGE

CREATING RICHER DIGITAL EXPERIENCES

To avoid being left behind by the pace of innovation, insurers need to take charge of the digital conversation before it passes them by. Right now, established insurers have a powerful legacy on their side, but they need to exercise that power before new entrants catch up.

The good news is that there is plenty of low-hanging fruit ready for the sector to grasp. To take one example: ANZ internal

data suggest that around 35 per cent of all advised life-insurance applications started electronically currently go through to completion without requiring further information from the customer. An improved digital experience has the potential to significantly improve that conversion rate, reducing costs while delivering on the promise of easier and more accessible products.

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 22 PAGE 23

A renewed focus on wellness across the developed world, supported by new technologies, is a valuable opportunity for insurers to create deeper and more

lasting relationships with customers.

THE CHANGING FACE OF WELLBEING

New technologies and social trends are redefining approaches to healthy living and inspiring an upsurge of interest in personal wellbeing.

Medical diagnosis and treatment continue to improve, bringing benefits to patients but creating challenges for underwriters and insurance product designers. Developments in analytics, wearable devices, connected health and artificial intelligence are increasing the range and

depth of insights for insurers in assessing and supporting clients. The challenge for insurers is in determining how to access this wealth of data and use it most effectively.

A growing awareness of mental health has also brought challenges of a different kind. Recent years have seen a significant rise in recorded mental illnesses across the developed world.

In the US, mental illness has become the second most common cause of disability,28

while in Australia, mental illness claims have played a significant part in the rising cost of disability insurance. This suggests insurers need to proactively cater for mental health issues with targeted support programs and clear and accurate definitions, avoiding what advocacy group Beyond Blue has described as a one-size-fits all approach that “conflates mental health symptoms with mental health conditions and lumps all mental health conditions together as a homogenous group”.29

Figure 4.1 The US experience: mental illness claims have increased30

CHAPTER FOUR

FOCUSING ON HEALTH AND WELLBEING

28 US Social Security Administration, ‘Annual statistical report on the Social Security Disability Insurance Program’, 2014

29 Beyond Blue, Submission 18 to the Parliamentary Joint Committee on Corporations and Financial Services Inquiry into the Life Insurance Industry, 2016

30 Australian Bureau of Statistics, Population projections, Australia, 2012 (base) to 2101, Australia, November 2013 (Release 3222.0)

31 Australian Institute of Health and Welfare (AIHW), ‘Healthy life expectancy in Australia: Patterns and trends 1998 to 2012’, AIHW Bulletin 126, 2014

32 AIHW, ‘Australia’s health’, 2016

KEY POINTS

1981 1985 1989 1993 1997 20092001 20132005

Num

ber o

f disa

bilit

y pa

ymen

ts (t

hous

ands

)

300

200

100

0

Year of disability payments

Musculoskeletal

Mental

Cardiovascular

Supporting customers’ mental and physical wellbeing can help insurers reduce costs and create stronger client relationships.

Technology provides a rich source of data that can be used to encourage healthy behaviours and provide a truly personalised offering.

However, customers are only likely to share personal data if they believe they will receive real benefit in return.

Australian insurers and healthcare providers will also be increasingly confronted with the impacts of an ageing population. By the end of the century, one in four Australians are projected to be aged 65 or over, up from just 14 per cent in 2012.30 Along with declining birth rates, a key driver of this trend is a welcome rise in life expectancies, accompanied by improved healthcare that has helped to deliver Australians a higher quality of life in old age, including a significant rise in disability-free years.31

Nonetheless, an ageing population will inevitably bring an increased prevalence of people living with multiple chronic and potentially disabling conditions.32 This underscores the need for insurers to actively support ageing customers with wellness initiatives designed to extend healthy lives and reduce the ongoing impacts of disability.Neoplasm

Respiratory

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 24 PAGE 25

LEVERAGING PERSONAL HEALTH DATA FOR PRODUCT DESIGN

Lifestyle-based, reward-for-fitness insurance programs are increasing in popularity, powered by wearables such as smart watches.33 This approach uses technology to establish an ongoing dialogue between insurers and customers, with benefits for both.

CASE STUDY: WELLMO

Founded in 2012 by two veterans of Nokia’s discontinued wellness division, Wellmo is one of a new wave of cloud-based platforms helping insurance companies leverage wearables and wellness apps to reduce health risks and encourage positive behaviours.

As at December 2016, Wellmo had partnered with 20 international insurers servicing more than 7 million customers, allowing it to draw on data from a widening ecosystem of wearable products, coaching services and content providers.

By combining insurance cover with health tracking and coaching, then rewarding healthy lifestyle behaviours, Wellmo’s insurance partners help to drive positive change and create stronger relationships with their customers. This can result in a measurable improvement in customers’ wellbeing. For example, Finnish insurer LocalTapiola has harnessed Wellmo to power its Smart Life Insurance product, with 80 per cent of users saying they have achieved a positive lifestyle change.

33 Shifting Gears, ‘The future of insurance’ survey report, 2016

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 26 PAGE 27

CUSTOMERS CAN BE PERSUADED TO SHARE DATA – IF THEY ARE REWARDED

The success of existing wellness programs is proof that certain customer segments are willing to share their health-related data in return for reduced premiums. This insight can be translated into a compelling customer proposition; for example, “Let us help you lower your blood pressure to lower your premium”.

This concept empowers customers to reduce risk and engage positively with their insurers. Insurers who run these types of programs build loyalty by visibly supporting customers’ healthy goals, while learning

more about their customers. This allows them to better design products and claims processes that prioritise the right benefits while minimising costs.

As the number of people who track their own health data increases, so too will the demand for insurers to use that data in developing policies. However, research also suggests these offerings need to be carefully positioned to persuade customers to provide access to personal data. When global market researcher GfK asked Australians whether they would be willing

to share their data in exchange for a reward, only 17 per cent responded positively, while another 56 per cent were neutral.

European economic think-tank Bruegel has called personal data the “oil of the twenty-first century” 34 – the fuel that powers richer and more meaningful customer interactions. By using that data to focus on wellness, both physical and mental, insurers can add value for customers, help them to avoid injury, and create better return-to-work outcomes for claimants.

Figure 4.2 Willingness to share personal data in exchange for rewards, by country35

Australia

UK

Spain

France

Japan

Canada

Germany

Netherlands

South Korea

Agrentina

USA

Brazil

Italy

Russia

Mexico

China

Belgium

12% 30%

18% 28%

29% 21%

20% 13%

8% 22%

17% 27%

38% 8%

12% 40%

16% 27%

16% 26%

15% 37%

14% 31%

24% 26%

26% 34%

28% 19%25% 23%

30% 23%

Agreement Total = 27%

DisagreementTotal = 19%

34 Bruegel, ‘The economic value of personal data for online platforms, firms and consumers’, 2016

35 GfK Market Research, 2017

By focusing on wellness (mental and physical), insurers can add value for consumers and lead claimants back to work, thereby lowering costs and bringing insurance back to its core purpose – providing a pathway to health, rather than funding disability.

Insurers can use technology to simplify transactions and participate more meaningfully in the lives of customers – both when they are well and when they are injured.

Insurers can offer discounted premiums and other incentives based on customers’ health activities, encouraging engagement and loyalty and supporting customers’ health goals.

OPPORTUNITIES FOR CHANGE

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 28 PAGE 29

Tech-savvy Millennials are both a challenge and an opportunity for insurers, demanding a high-quality

digital experience from them underpinned by a deep understanding of their needs.

CHAPTER FIVE

THE MILLENNIAL CHALLENGE

KEY POINTS

MILLENNIALS ARE NOW THE

NUMBER-ONE SOURCE OF

GLOBAL INCOME, SPENDING

AND WEALTH CREATION

36 Telstra Research, ‘Millennials, mobiles and money: The forces reinventing financial services’, 2016

THE OPPORTUNITY

Australia’s ageing population and marked disparity in wealth between the old and the young make it all too easy to focus on Generation X and the Baby Boomers, ignoring the potential of Millennials as an influential customer segment.

But that would be a mistake. Millennials are a large and growing market that presents unique challenges to insurers seeking to adapt to the evolving market.

And Millennials have numbers on their side. In 2014 they overtook Baby Boomers as the largest global demographic group and emerged as the number-one source of global income, spending and wealth creation.36

Millennials value high-quality digital experiences over human interactions.

Financial adviser roles should be focused on where they can add the most value.

Insurers need to re-engineer their processes to meet evolving customer demand.

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 30 PAGE 31

Figure 5.1 Consumer satisfaction with online experience, by industry 40

5 KEY CONSIDERATIONS IN DESIGNING PRODUCTS FOR MILLENNIALS

Recognise that there is valuable, untapped potential within the 18–24-year-old segment.

Learn to engage with these younger customers through modern, digital channels – it’s your future as well as theirs.

Use new types of data to create personalised offerings that are relevant and helpful throughout life.

Address the knowledge gap by educating young adults about insurance, but avoid puncturing their optimism.

Overcome traditional stereotypes and operational barriers.

0 5 10 15 20

Personal banking

Online merchants

Media retail

Electricity, gas, water

Automobiles

Electronics retail

Apparel retail

Airlines

Investments

Hotels

Supermarkets

Government services

Healthcare providers

Insurance

Real estate

Telco and cable

15.2

11.8

11.1

10.0

8.9

8.5

8.5

8.0

5.8

5.0

4.3

4.2

4.1

4.0

3.8

3.5

1

2

3

4

5

37 Boston Consulting Group (BCG), ‘The connected world: Delivering digital satisfaction – US consumers raise the ante’, 2013

38 Capgemini and Efma, ‘World insurance report’, 2016

39 Capgemini, ‘Top 10 trends in insurance in 2016’

40 BCG, ‘Delivering digital satisfaction’, 2013

Relative satisfaction utility score

MILLENNIALS EXPECT HIGH-QUALITY DIGITAL EXPERIENCES

Born between 1980 and the mid-2000s, Millennials are digital natives and the first generation to grow up with the internet. Their willingness to engage online provides insurers with a highly efficient, cost-effective channel for creating greater engagement and capturing new business. But while Millennials are open to the use of their data by product providers, they also have an expectation that brands will adapt to their preferred ways of communicating and provide a high-quality online experience.

That’s something insurers across all categories have sometimes struggled to provide. Research from Boston Consulting Group found US insurers lagging behind most other industries for online customer satisfaction, with negative scores for both research and post-transaction activities.37

That creates a particular challenge for insurers seeking to reach out to the next generation of Millennial consumers, while fending off the competitive threat of insurtech innovators.

Millennials are least likely to say they have had positive experiences with their current insurer (for life and other insurance),38 and most likely to buy new insurance offerings from high-tech companies entering the industry through partnerships, alliances, joint ventures and acquisitions.39

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 32 PAGE 33

Insurers can increase their appeal to Millennials by leading with high-quality online interactions and refocusing the role of advisers where they can provide most value. That means the advice proposition needs to evolve.

Modern customers’ demands for products are geared around their preferences and how they live – which means insurers need to build products around those lifestyles, not around risk processes.

As a result, business strategies need to be more customer-centric, promoting ongoing engagement across the entire customer journey – before and after transactions.

That means using sophisticated technology to deliver a simple and seamless customer experience, with transparent products focused on the core promise of insurance – helping consumers return to wellness and prosperity in times of need.

TURNING COMPLEX CONVERSATIONS INTO SIMPLE ONLINE PROCESSES

This isn’t to underestimate the extent of the challenge. Life insurance underwriting can be a complex process, with risks to both consumer and product provider if information gathering is incomplete or inaccurate.

The good news is that Millennials are accustomed to making complicated transactions online and are willing to exchange personal data for better-designed products. They’re also keen to access financial services information, but aren’t sure who to trust or where to find it.41

In fact, recent research from Telstra found that 67 per cent of all Millennials and 70 per cent of affluent Millennials prefer to receive financial advice on digital platforms.42

This could be a clear opening for financial advisers, who can address the lack of certainty among Millennials by offering services through the channels that appeal to them.

By meeting Millennials on their terms, digitally savvy financial advisers can expand their market and be an effective intermediary for insurers to this generation.

This suggests that product providers can best appeal to Millennials by leading with a tailored online experience, supported by personal interactions in instances where an adviser can add extra value. The resulting step change in digital capabilities has the potential to benefit all insurance customers, no matter which generation they belong to.

41 Accenture, ‘The challenge of making life insurance ageless: Selling the prospect of death to invincible 18–24-year-olds’, 2016

42 Telstra Research, ‘Millennials, mobiles and money: The forces reinventing financial services’, 2016

OPPORTUNITIES FOR CHANGE

TraditionalDigital

All

HNW

33%

30%

All

HNW

67%

70%

Figure 5.2 Preferred delivery platform for financial advice on products and services 41

HNWs = high net worth ($500k-$1m+)

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 34 PAGE 35

Data-driven underwriting offers significant benefits to insurers and customers alike – simplifying processes,

improving accuracy and lowering costs.

CHAPTER SIX

THE DATA AND ANALYTICS ADVANTAGE

KEY POINTS

Disruptive medical technologies have the potential to transform underwriting by providing a rich stream of data to power faster, more accurate decisions.

To realise that potential, insurers need to invest in analytically minded staff and data-driven systems, while actively engaging customers and regulators.

Those who succeed will create more personalised products and pricing, delivering an enhanced customer experience, while ensuring the ongoing sustainability of their business.

ACCESSING RICHER DATA SOURCES

High-quality, personalised underwriting relies on accurate data. Yet traditional data-gathering methods are cumbersome for insurers, and invasive and time-consuming for customers. Currently, it can take up to six weeks for an underwriting decision to be made – a common pain point highlighting a clear opportunity for a better customer experience and efficiency for the life-insurance sector.

Disruptive medical technologies have the potential to overcome these problems. E-health innovations such as mobile apps, m-health devices, wearables and rapid

genetic testing can all generate an ongoing stream of data that insurers can use to reach underwriting decision more rapidly and confidently, delivering a better customer experience.

By combining big data with predictive analytic models, insurers can also better understand insurance risks and personalise their products, with individualised pricing based on a confident assessment of the risk each individual represents.

FOUR POTENTIAL USES OF PREDICTIVE ANALYTICS IN INSURANCE UNDERWRITING

Segmentation of insurance risks by identifying new relationships between variables

Improved and more consistent underwriting and pricing decisions

Improved results from marketing efforts

Enhanced claims management and fraud detection

Figure 6.1Underwriting decisions can be made using unstructured data from multiple sources43

Pricing granularityAccess to richer, more accurate medical information has enabled a better understanding of risk. By developing sharper pricing capabilities, life insurers can now compete more effectively for share.

Product designWith access to more granular, faster information about customers, it is now possible not just to customise insurance products but also to develop holistic income solutions catering to individuals’ specific needs.

SimplicityAutomation of core processes has started to reduce cycle time, making it possible to improve customer abandon rates through the quoting process and allowing for greater market capture.

43 PwC, ‘Life insurance 2020: Competing for a future’, 2012

Network

Doctor’s consideration

Immediate emergency attention

File for future reference

Telephone

Mobile device

Wireless

Hearing

EEG

Vision

Positioning Glucose

ECG

DNA proteinImplants Blood

pressure

Toxins

1

2

3

4

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 36 PAGE 37

In 2015, South African insurer Absa Life offered 700,000 qualifying Absa Bank clients automatic life insurance without filling in a lengthy questionnaire or undergoing a medical examination.

Part of the Barclays Group, Absa used the Group’s bancassurance model and big-data technology to create a predictive underwriting solution, eliminating the need for traditional underwriting processes. By correlating claims data and banking transaction records, Absa was able to pre-qualify selected customers using just three questions and no medical tests.

While available only to selected customers, the successful pilot and in-market launch means the company can make more accurate long-term decisions without prejudicing policyholders.

DEVELOPING IMPROVED ANALYTIC CAPABILITIES

Traditionally, many insurers have had relatively limited data quality and analytic capabilities, making it difficult to achieve meaningful back-end efficiencies. When KPMG asked global insurers about the challenges preventing them from making more effective use of data analytics, they were most likely to cite problems capturing reliable data, then analysing and interpreting it.44

As large volumes of customer data become more freely available, problems of analysis and interpretation are likely to come into sharper focus. Faced with a constant stream of unstructured and undifferentiated information, insurers will need to develop significant analytic skills to identify the data points that matter most, then use them to generate actionable insights. They will also need to be transparent in explaining the methods they use to access, analyse and harness data, respecting individuals’ legitimate privacy concerns while offering them access to the tailored products and enhanced support data-driven underwriting can bring.

Figure 6.2Challenges faced by companies using data analytics⁴⁴

Capturing reliable data

Implementing the right solutions to analyse and interpret the data

Balancing human judgement with data-driven decision making

Identifying the right risk indicators/parameters

Reacting in a timely fashion as insights are identified

Keeping data secure

44 KPMG International, ‘Digital technology’s effect on insurance’, 2014

2% 8%12%

18%

29%

31%

CASE STUDY: CREATING A PREDICTIVE LIFE INSURANCE POLICY BASED ON BIG DATA

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 38 PAGE 39

CREATING TAILORED PRODUCTS AND SERVICES

Big data offers the potential for insurers to develop a more granular understanding of customers, so they can create genuinely personalised products and services.

Predictive modelling can help shape processes that are easier for customers to navigate, with opportunities to improve customers’ digital experiences across every step of the value chain – from product design and underwriting to interactions with intermediaries, treatment service providers and claims processing.

Developments in data, devices and artificial intelligence all represent opportunities

to engage with customers. Advances in interface and user-experience design represent new ways to build trust by giving customers seamless, intuitive ways to interact and be rewarded for ongoing engagement and data provision.

Just as importantly, improved pricing capabilities offer the potential for insurers to create a genuinely sustainable product offering – ensuring that they will continue to be there to support customers, now and in the future.

Rich customer data can speed up the underwriting process, delivering pre-approval in minutes.

Technology and superior digital experiences can capture data that can be used to simplify underwriting, reduce premiums and manage risks efficiently. This enables insurers to provide affordable and transparent insurance products through a seamless customer experience that makes it easier for consumers to secure the protection they need.

The key for insurers is to develop effective analytics offering a consistent view of customer, operational and financial data from a range of sources – including third parties, transactions, personal interactions and wearables.

The insurers of the future will recruit and nurture analytically minded staff who are able to collaborate with data teams and confidently leverage insights and predictive models to make sound business decisions.

OPPORTUNITIES FOR CHANGE

LIFE INSURANCE TRENDS REPORT LIFE INSURANCE TRENDS REPORT

PAGE 40 PAGE 41

It’s time for insurers to focus on their core purpose: helping customers in times of need.

CONCLUSION

There is enormous promise and challenge for life insurers in the years ahead.

In the short term the pain points of a damaged reputation and loss-making insurance products must be addressed. Both of these factors continue to erode the ability of businesses to operate well in the marketplace.

Fortunately, the solution is straightforward: clear, core-purpose products that provide genuine protection against the financial impacts of disability at an affordable price.

For consumers, this will meet their demand for simplicity and affordability in life insurance, helping to restore the sector’s credibility in their eyes and encouraging take-up, which will go some way to addressing the problem of underinsurance. For financial advisers, it gives them more choice in what they can offer, expanding the markets they can reach.

For the sector, such products will support what should be insurers’ overall objective: to restore the individual to the position they enjoyed before they had need to claim, and particularly to support their return to work, while not overpaying for minor events or inadvertently discouraging claimants from re-entering the workforce after they have recovered their capacity to work.

If the sector continues on its current path, the risk is that some products will become unsustainable. This will force up premiums, making cover unaffordable for customers and depriving them of the opportunity to protect themselves and their families.

Even worse, the continuation of loss-making policies could threaten the ongoing financial health of the insurance providers that consumers rely on to cover them for years into the future.

By creating a more sustainable sector, this approach leads directly to the medium- to long-term objectives of insurers – wholesale adaptation to technological developments and changing customer expectations to produce more personalised products, improve customer experience and efficiency of operations.

Using the many sources of customer data becoming available will revolutionise how insurance policies are underwritten, making premiums more manageable where appropriate and making policies more precise, reducing risk and drastically improving the speed and efficiency of the underwriting process.

This will directly feed through to consumers’ front-end experience of a simpler, seamless (usually digital) interaction with their

insurer – of particular appeal to Millennials. More data and better understanding of policyholders means insurers can be much more customer-centric, at a personal level, with policies built around customers’ lifestyles. This will also flow through to improve the services that advisers offer.

Life insurers have already started on this journey with their increased focus on health and wellbeing. Using customers’ health data enables them to offer rewards for fitness, which increases customer engagement and therefore their ongoing relationship with their insurer, manages risk and pricing of premiums, and enriches the data available to insurers so they can get personal with their customers.

By meeting the challenges posed by emerging technologies, changing consumer sentiments and the evolving economics of the sector by proactively making the changes these challenges demand, insurers will reap tremendous rewards, principal among them being a strong and sustainable future.

Important information:

© Australia and New Zealand Banking Group Limited ABN 11 005 357 522 (ANZ).

This paper is current as at September 2017 but may be subject to change. It is of a general nature only and does not contain any securities advice or recommendations on any particular matter. While ANZ has taken care to ensure that this information is from sources considered reliable, it cannot warrant its accuracy, completeness or suitability for your intended use. To the extent permitted by law, ANZ does not accept any responsibility or liability arising from the use of this information, or any loss or damage from it, to any person. As such you should seek qualified advice before making any decision based on this information or any of it.

Top Related