Languages

Pages

Legal

Growing with Passion

Conference Call Interim Report as of March 31, 2015

Hans-Georg Frey, Chairman of the Board of Management Dr. Volker Hues, Member of the Board of Management, Finance Hamburg, May 8, 2015

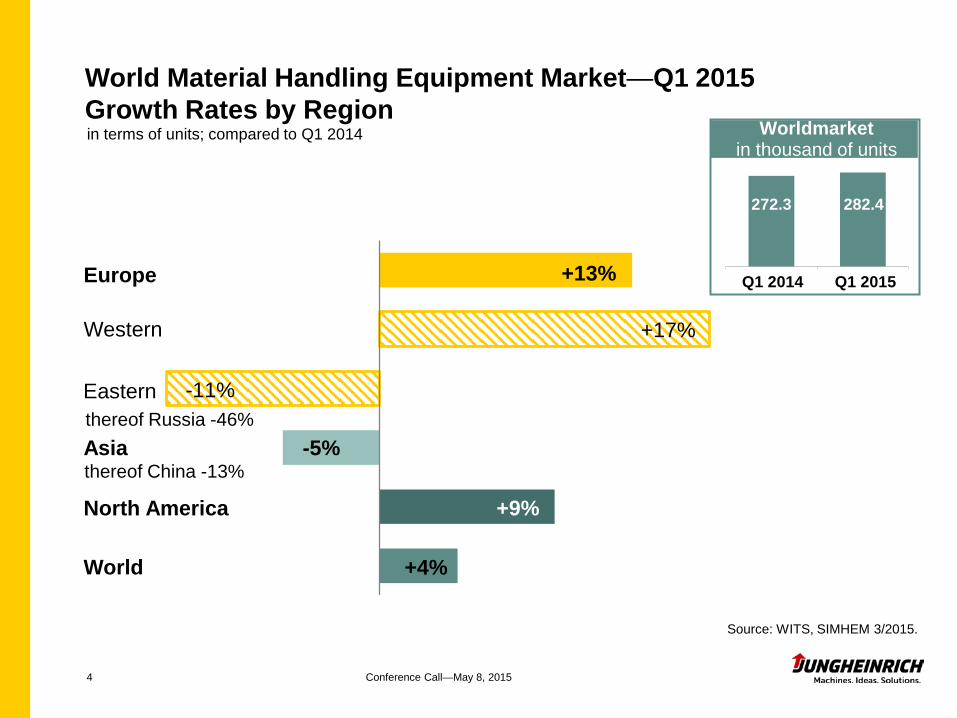

World material handling equipment market expands by 4%

Demand in Europe rises by 13%—despite the dramatic shrinkage of the Russian market

Market volume in Eastern Europe—excluding Russia—grows by 8%

The Asian market decreases in volume by 5% due to a drop in demand for IC engine-powered counterbalanced trucks in China (-18%)

Highlights of the Material Handing Equipment Market —Q1 2015

2 Conference Call—May 8, 2015

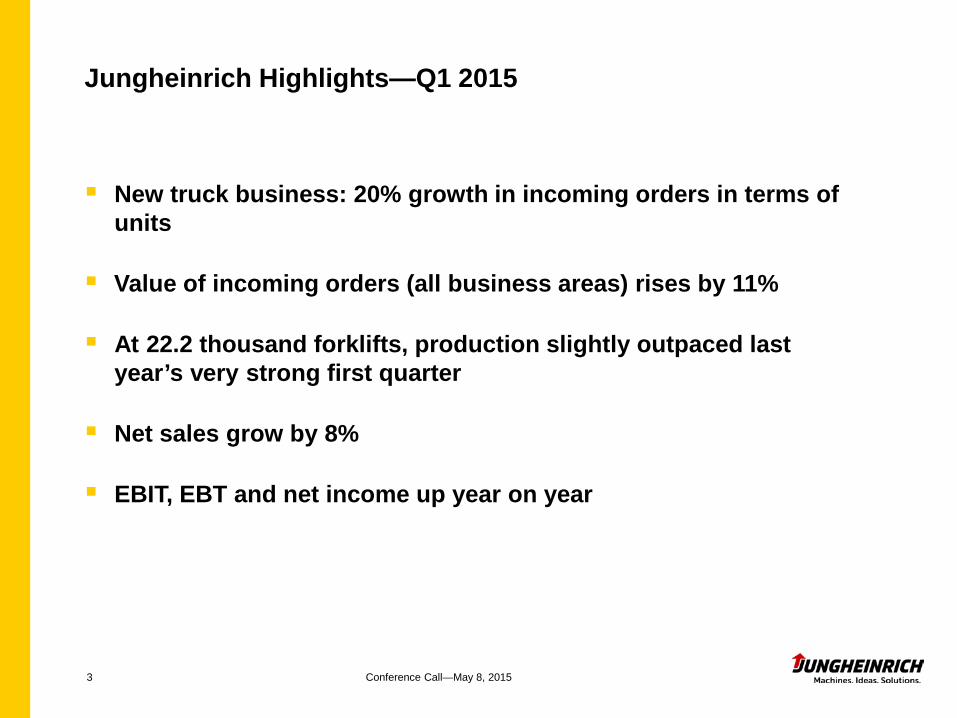

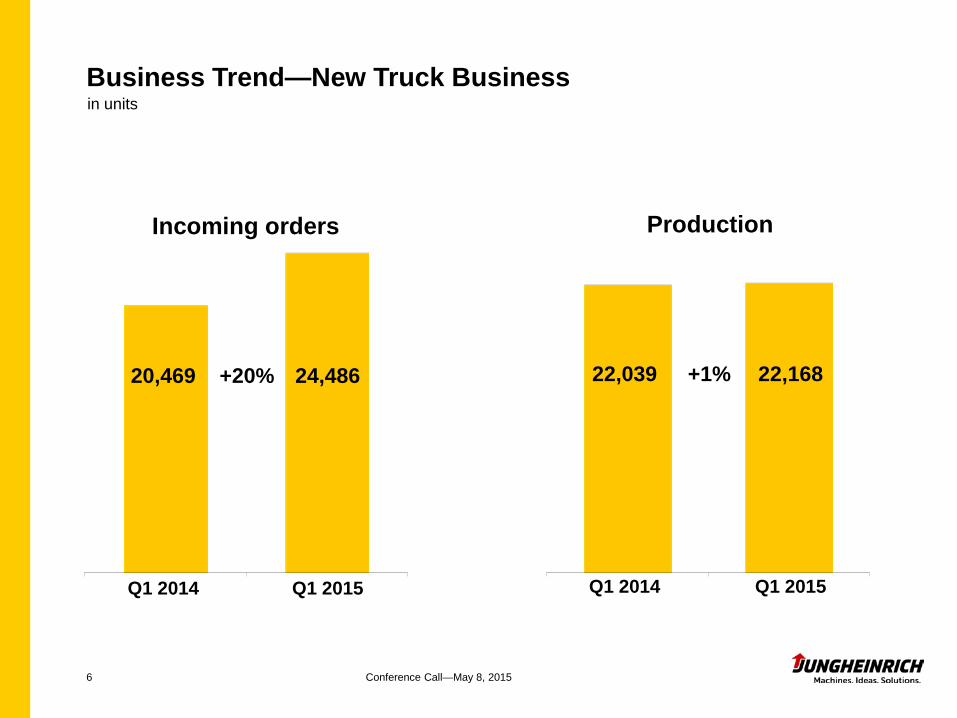

New truck business: 20% growth in incoming orders in terms of units

Value of incoming orders (all business areas) rises by 11%

At 22.2 thousand forklifts, production slightly outpaced last year’s very strong first quarter

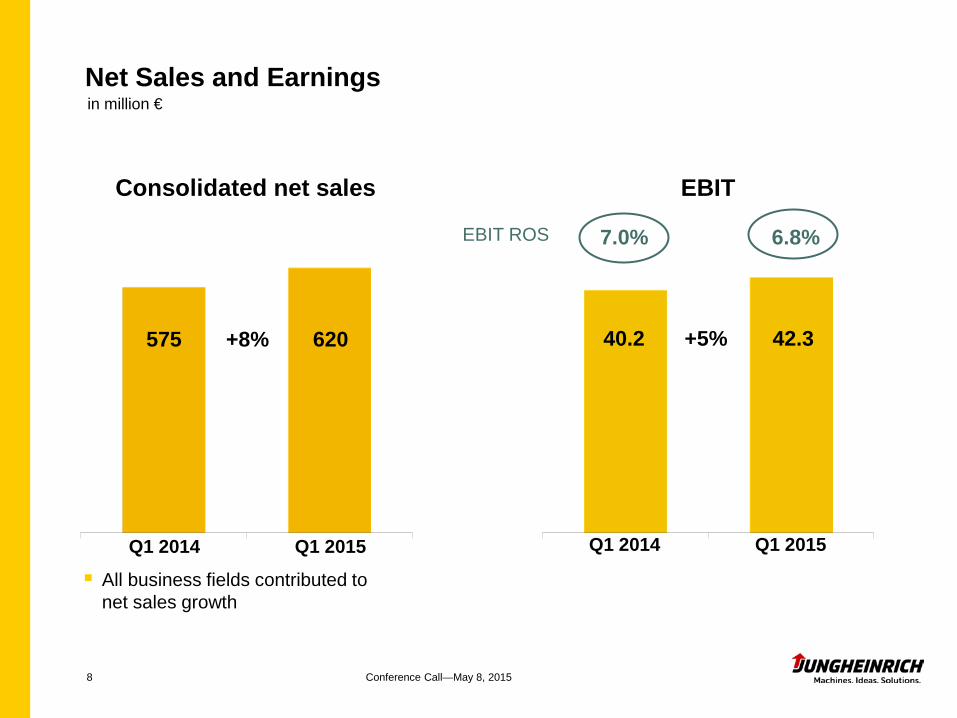

Net sales grow by 8%

EBIT, EBT and net income up year on year

Jungheinrich Highlights—Q1 2015

3 Conference Call—May 8, 2015

4

+13%

+17%

-11%

-5%

+4%

272.3

Q1 2014

282.4

Q1 2015

+9%

thereof China -13%

thereof Russia -46%

Source: WITS, SIMHEM 3/2015.

World Material Handling Equipment Market—Q1 2015 Growth Rates by Region in terms of units; compared to Q1 2014 Worldmarket

in thousand of units

Western

Eastern

Europe

Asia

North America

World

Conference Call—May 8, 2015

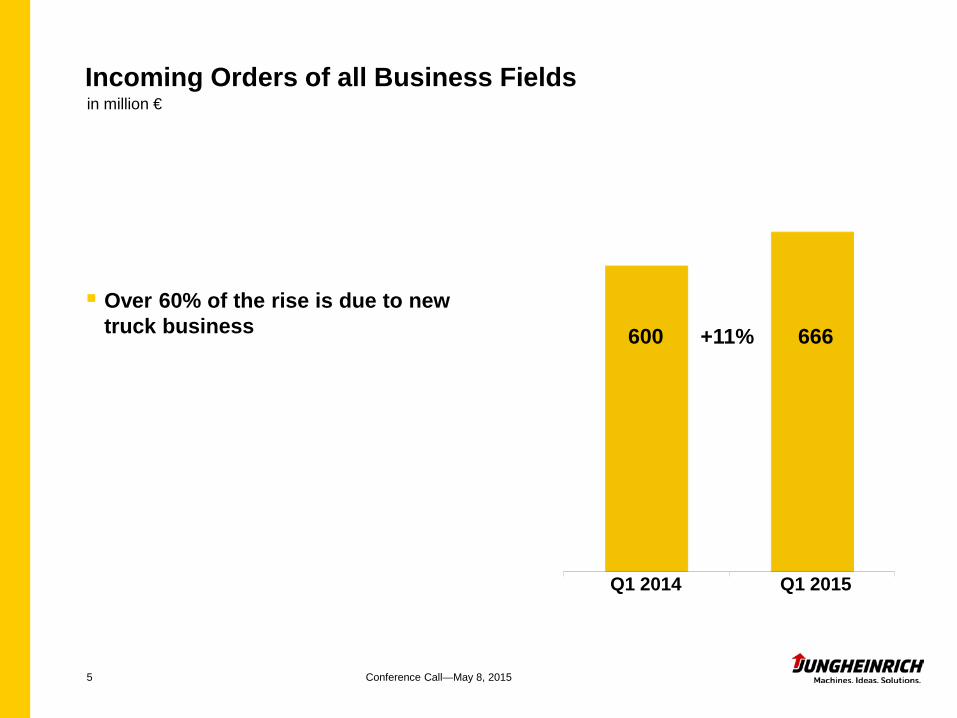

Incoming Orders of all Business Fields

5 Conference Call—May 8, 2015

in million €

Q1 2014 Q1 2015

+11% 600 666 Over 60% of the rise is due to new

truck business

22,168 24,486

Business Trend—New Truck Business

6 Conference Call—May 8, 2015

in units

Incoming orders Production

20,469 22,039

Q1 2014 Q1 2015

+1% +20%

Q1 2014 Q1 2015

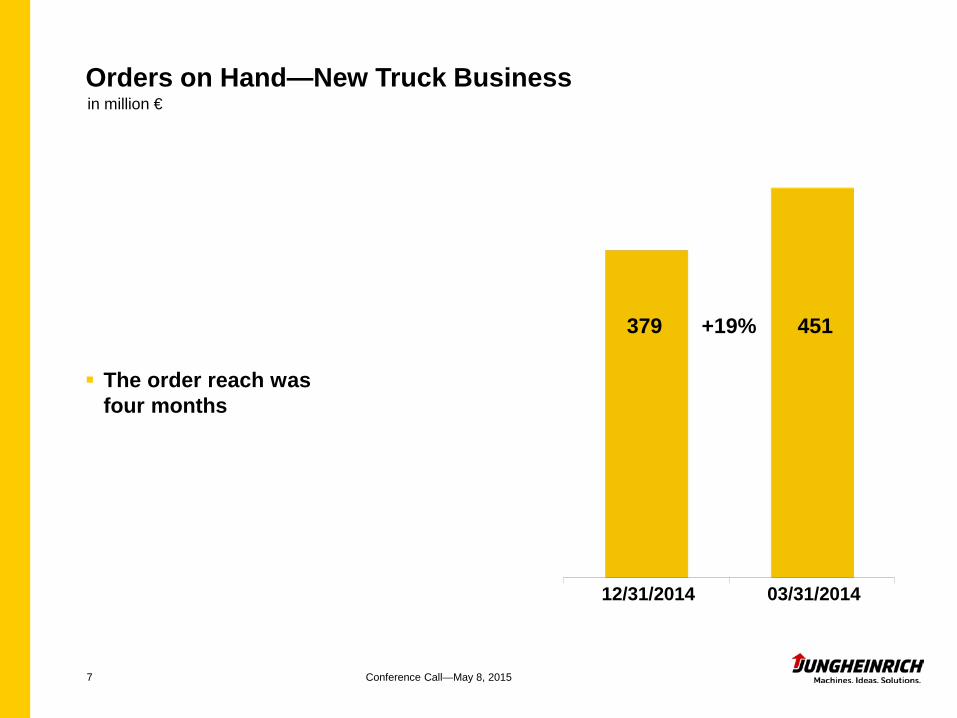

451 379 +19%

7

12/31/2014 03/31/2014

Orders on Hand—New Truck Business

Conference Call—May 8, 2015

The order reach was four months

in million €

Conference Call—May 8, 2015 8

Net Sales and Earnings in million €

7.0% EBIT ROS 6.8%

Consolidated net sales EBIT

40.2 42.3 +5% 575 620 +8%

Q1 2014 Q1 2015 Q1 2014 Q1 2015

All business fields contributed to net sales growth

R&D and Capital Expenditures

Conference Call—May 8, 2015 9

Capital Expenditures R&D Expenditures Capex ratio as a percentage of net sales

in million €

Capitalization ratio

25% 19% 2% 3 %

12.1 13.1 14 16

Capital expenditures characterized by large-scale construction projects

Q1 2014 Q1 2015 Q1 2014 Q1 2015

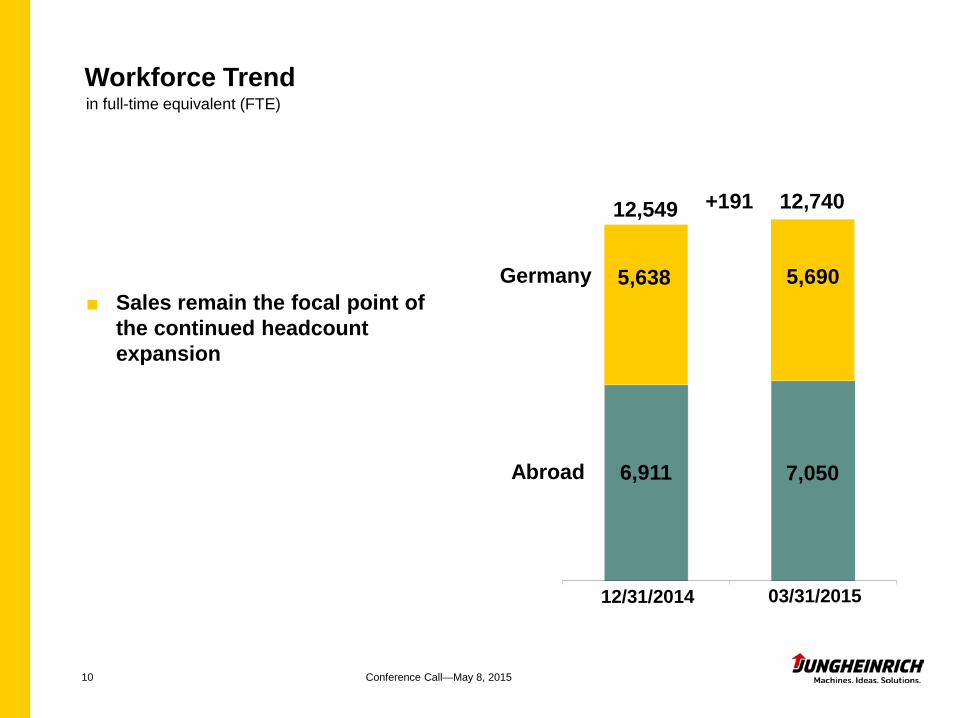

Workforce Trend

12/31/2014 03/31/2015

Germany

Abroad

Conference Call—May 8, 2015 10

in full-time equivalent (FTE)

■ Sales remain the focal point of the continued headcount expansion

6,911 7,050

5,638 5,690

12,740 +191 12,549

201

401

316

219

444

345

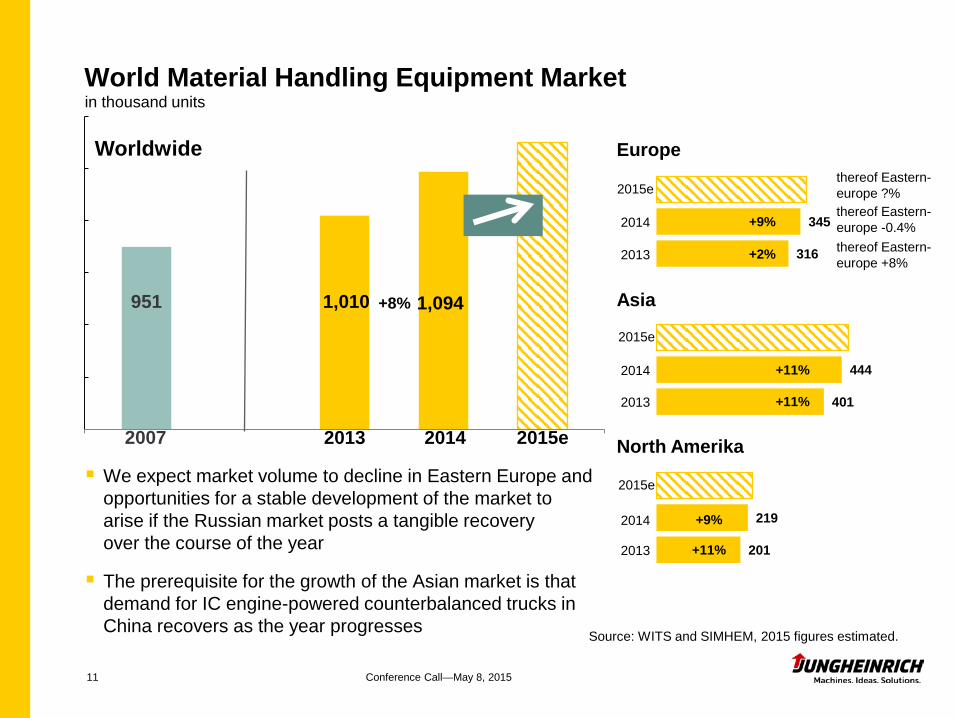

Worldwide

2013 2014

Europe

Asia

North Amerika

11

951

2007

1,010 1,094

+9%

Source: WITS and SIMHEM, 2015 figures estimated.

+2%

+9%

+11%

+11%

+11%

2015e

+8%

2014

2013

2015e

2014

2013

2015e

2014

2013

2015e

World Material Handling Equipment Market in thousand units

Conference Call—May 8, 2015

We expect market volume to decline in Eastern Europe and opportunities for a stable development of the market to arise if the Russian market posts a tangible recovery over the course of the year

The prerequisite for the growth of the Asian market is that demand for IC engine-powered counterbalanced trucks in China recovers as the year progresses

thereof Eastern-europe -0.4% thereof Eastern-europe +8%

thereof Eastern-europe ?%

12

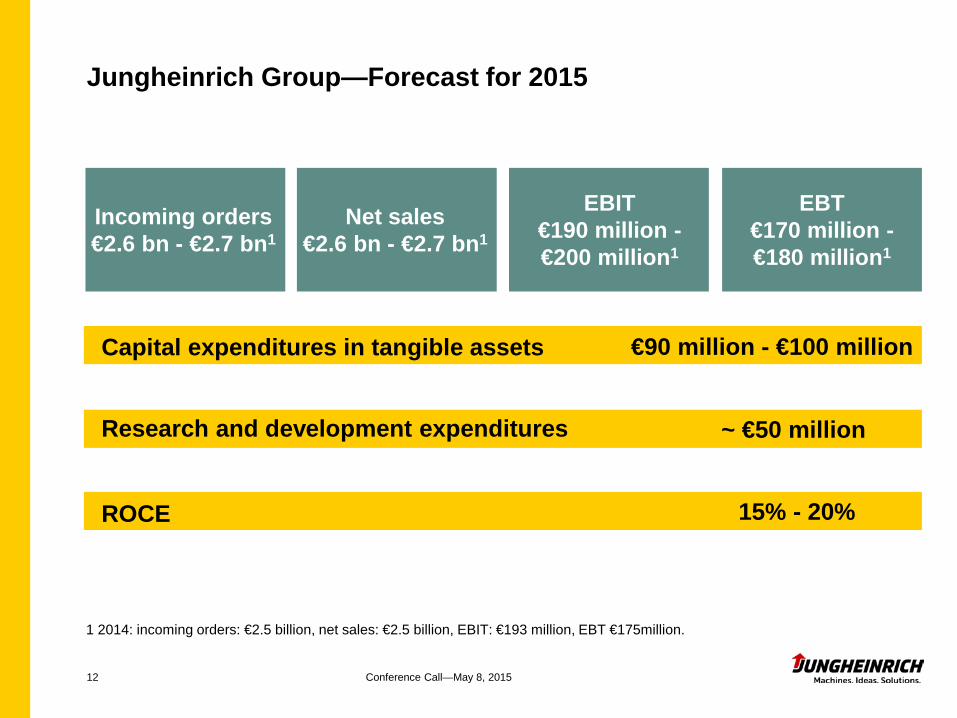

Jungheinrich Group—Forecast for 2015

Incoming orders €2.6 bn - €2.7 bn1

Net sales €2.6 bn - €2.7 bn1

EBIT €190 million - €200 million1

~ €50 million

Capital expenditures in tangible assets

Research and development expenditures

€90 million - €100 million

15% - 20% ROCE

1 2014: incoming orders: €2.5 billion, net sales: €2.5 billion, EBIT: €193 million, EBT €175million.

EBT €170 million - €180 million1

Conference Call—May 8, 2015

Conference Call—May 8, 2015 13

Disclaimer

Since developments cannot be foreseen, the actual business trend may deviate from the expectations presented here based on assumptions and estimates made by Jungheinrich company management. Factors that may lead to such deviations include changes in the economic environment, changes in the political and legal environment and within the material handling equipment sector as well as exchange and interest rate fluctuations. Therefore, no responsibility is taken for forward-looking statements made in this presentation and no ensuing liability is assumed.

Top Related