Yu info 2015 final jg

42

Telecom and In ter net T r e n d s (and service provider challenges) Jož ek Gruš kovnjak Managing Director & Principal Consultant

-

Upload

jozek-gruskovnjak -

Category

Business

-

view

324 -

download

0

Transcript of Yu info 2015 final jg

Telecom and Internet Trends (and service provider challenges)

Jožek Gruškovnjak Managing Director & Principal Consultant

A Minute in the Life of the Internet

Source: GP Bullhorn

208,000 photos uploaded 30 hours of new video uploaded

2 million search queries $83,000 in revenue

100,000 tweets

100 new accounts

© Inluceo Consulting, Ltd., 2014 2

A Minute in the Life of the Internet

Source: GP Bullhorn

208,000 photos uploaded243,000 photos uploaded

30 hours of new video uploaded100 hours of new video uploaded

2 million search queries3.5 million search queries

$83,000 in revenue$118,000 in revenue

100,000 tweets350,000 tweets

100 new accounts120 new accounts

2012 2013

⬆1177%%

⬆2200%% ⬆7755%% ⬆4422%%

⬆223333%%⬆225500%%

© Inluceo Consulting, Ltd., 2014 3

All these new services and users are

51

62

76

91

110

132

0

20

40

60

80

100

120

140

2013 2014 2015 2016 2017 2018

Exab

ytes

per

Mon

th

Year

CAGR of 21%2.6 x increase

Source: Cisco VNI Global Forecast, 2013–2018© Inluceo Consulting, Ltd., 2014

§ Global IP traffic increased more than five-fold in the last five years.

§ Annual global traffic will surpass the zettabyte in 2016.

§ Content delivery networks (CDN) will carry more than 50% of internet traffic in 2018.

§ Over half of all IP traffic will originate with non-PC devices by 2018.

§ Globally, IP will be 79% of all consumer Internet traffic in 2018.

4

© Inluceo Consulting, Ltd., 2014 5

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013

GGrroo

wwtthh

IInnddee

xx ((22

000099==

110000))

SSPP PPrroo ttaabbiilliittyy vveerrssuuss IInntteerrnneett TTrraaff cc GGrroowwtthh22000099––22001133**

Total Internet traffic evolution Revenue EBITDA

Source: Cisco SPTG, Cisco Visual Networking Index, 2009-2014)

Growth – 38% CAGR

Revenue Growth – 6% CAGR

EBITDA Growth – 5% CAGR

Value Opportunity (?)

There is a perfect storm in the making

© Inluceo Consulting, Ltd., 2014 6

Voice

Messaging

Video

Conferencing

Music

© Inluceo Consulting, Ltd., 2014 7

© Inluceo Consulting, Ltd., 2014 8

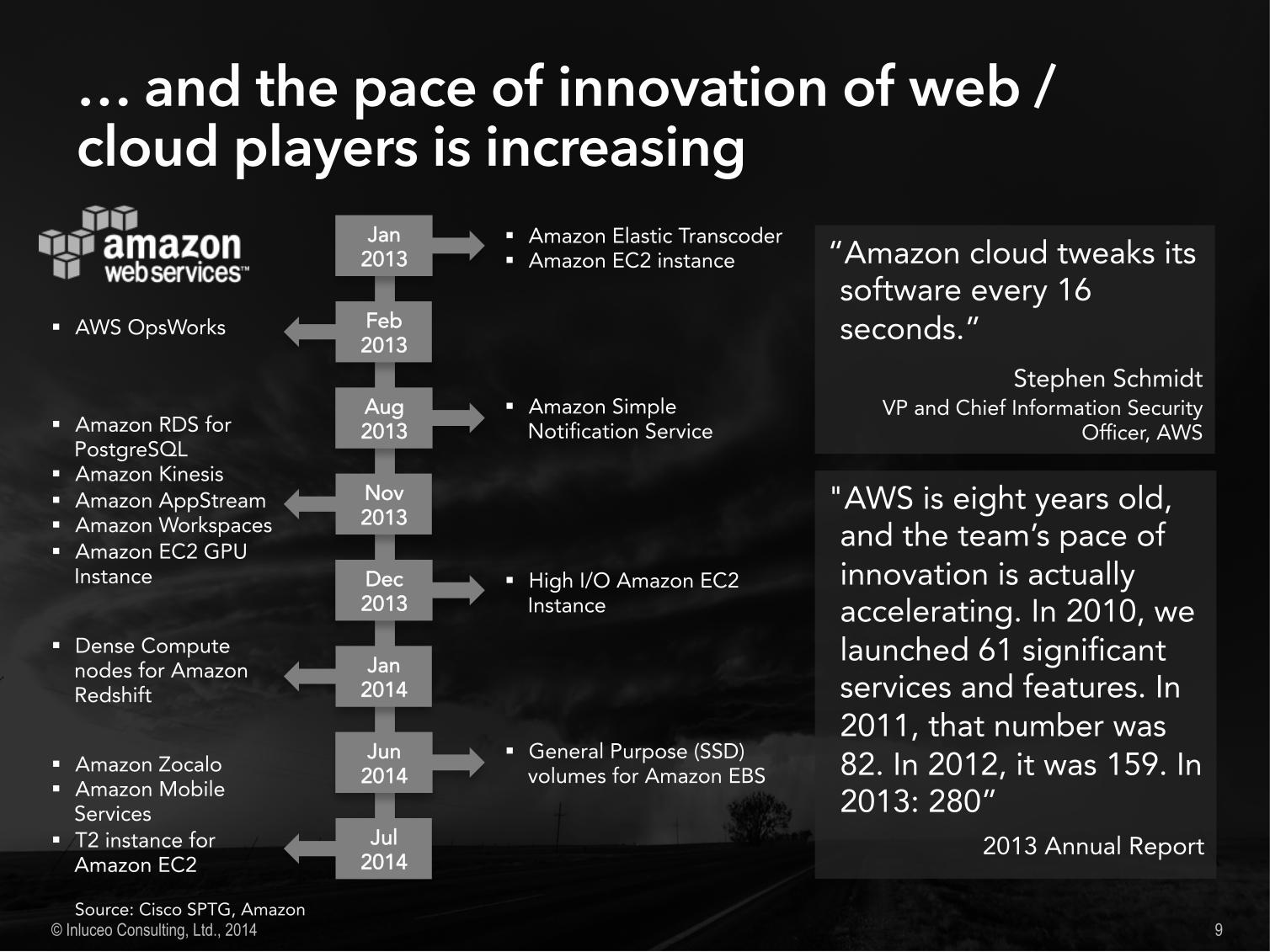

$11BB qquuaarrtteerrllyy AAWWSS rreevveennuueess220000MM++ ccuussttoommeerr aaccccoouunnttss

880000MM iiOOSS ddeevviicceess sshhiippppeedd11..22BB mmoonntthhllyy aaccttiivvee

uusseerrss ((7777%% mmoobbiillee))

1B Android 1B YouTube 750M Chrome 1B Web 425M Gmail users

Over 1.25B Windows 750M Office 70M Xbox 41M Skype 900M Web users

FFiigghhtt ttoo OOwwnn//

CCoonnttrrooll

CCuussttoommeerr

CClloouudd

PPllaattffoorrmm

EEccoossyysstteemm

DDaattaa

DDoollllaarrss

Source: Cisco SPTG, Source: Web Operation Quarterly Update, Patrick Morrissey

© Inluceo Consulting, Ltd., 2014

JJaann22001133

FFeebb22001133

AAuugg22001133

NNoovv22001133

DDeecc22001133

JJaann22001144

JJuunn22001144

JJuull22001144

§ Amazon Zocalo§ Amazon Mobile

Services § T2 instance for

Amazon EC2

§ Dense Compute nodes for Amazon Redshift

§ General Purpose (SSD) volumes for Amazon EBS

§ High I/O Amazon EC2 Instance

§ Amazon RDS for PostgreSQL

§ Amazon Kinesis§ Amazon AppStream§ Amazon Workspaces§ Amazon EC2 GPU

Instance

§ Amazon Simple Notification Service

§ AWS OpsWorks

§ Amazon Elastic Transcoder§ Amazon EC2 instance “Amazon cloud tweaks its

software every 16 seconds.”

Stephen SchmidtVP and Chief Information Security

Officer, AWS

"AWS is eight years old, and the team’s pace of innovation is actually accelerating. In 2010, we launched 61 significant services and features. In 2011, that number was 82. In 2012, it was 159. In 2013: 280”

2013 Annual Report

9 Source: Cisco SPTG, Amazon

Telecommunications services providers are feeling the

aaiinn

© Inluceo Consulting, Ltd., 2014 10

Traditional telecommunications services are

© Inluceo Consulting, Ltd., 2014 11

648 608 533

468 532 574

1,296 1,216 1,189

720 912 1,189

468 532 615 3,600

3,800 4,100

-

1,000

2,000

3,000

4,000

5,000

Past Now Future

RReevvee

nnuueess

((UUSSDD

BB$$))

Fixed Voice Fixed Data Mobile Voice Mobile Data Video

2012 & 2013 2014 & 2015 2016 & 2017

2.8%Y/Y growth

3.4%Y/Y growth

2.7%Y/Y growth

Mobile Datakey growth driver

Source: Cisco SPTG, Ovum Knowledge Centre

Overall CAGR 2012 – 2017: 3.1%

11 16 21 20 33 52 27

77

139

-

50

100

150

200

250

Past Now Future

RReevvee

nnuueess

((UUSSDD

BB$$))

OOTTTT && AAddvveerrttiissiinngg

Social Media Ads OTT Mobile Internet Ads

2012 & 2013 2014 & 2015 2016 & 2017

691 1,141

1,681

231 363 580 18 28

48

-

1,000

2,000

RReevvee

nnuueess

((UUSSDD

BB$$))

MMaacchhiinnee--ttoo--MMaacchhiinnee

M2M Revenue MNO Addressable MNO Expected

© Inluceo Consulting, Ltd., 2014 12

Past Now Future2012 & 2013 2014 & 2015 2016 & 2017

11 12 11 6 17 23 80

142 198

2

5

10

-

50

100

150

200

250

300

Past Now Future

RReevvee

nnuueess

((UUSSDD

BB$$))

CClloouudd

IaaS PaaS SaaS BPaaS

CAGR: 26%

CAGR: 40% CAGR: 25%

2012 & 2013 2014 & 2015 2016 & 2017

…

Sources: Cisco SPTG, ABI Research, eMarketer, BIA/Kelsey, Machina Research

The trend is improving as service providers enter new markets deploy new pricing strategies. Examples: § Industry focus (Singtel,

SK Telecom – gaming, …)

§ Tiered data plans (Comcast, Airtel, Telstra, …)

§ Shared data plans (Vodafone, …)

§ App-centric data plans (MTN, NTT Docomo, …)

© Inluceo Consulting, Ltd., 2014 13

-‐10% -‐5% 0% 5%

La�n America

E. Europe, MEA

Europe

North America

Asia (Developed)

Asia (Emerging)

Average

2015

2014

2013

2012

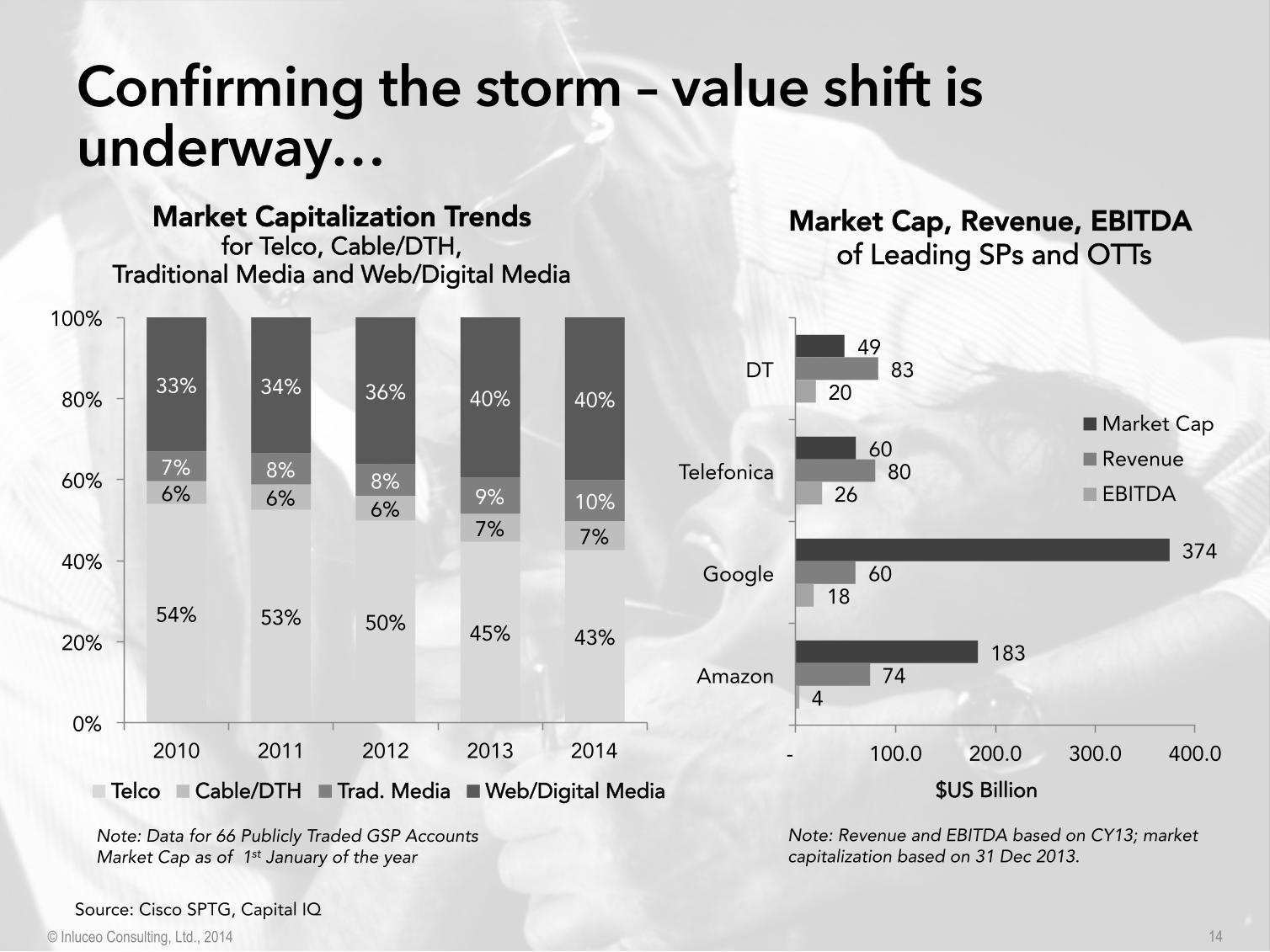

54% 53% 50% 45% 43%

6% 6% 6%7% 7%

7% 8% 8%9% 10%

33% 34% 36% 40% 40%

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014

TTeellccoo CCaabbllee//DDTTHH TTrraadd.. MMeeddiiaa WWeebb//DDiiggiittaall MMeeddiiaa

© Inluceo Consulting, Ltd., 2014 14

MMaarrkkeett CCaappiittaalliizzaattiioonn TTrreennddssffoorr TTeellccoo,, CCaabbllee//DDTTHH,,

TTrraaddiittiioonnaall MMeeddiiaa aanndd WWeebb//DDiiggiittaall MMeeddiiaa

49

60

374

183

83

80

60

74

20

26

18

4

- 100.0 200.0 300.0 400.0

DT

Telefonica

Amazon

$$UUSS BBiilllliioonn

Market CapRevenueEBITDA

Note: Revenue and EBITDA based on CY13; market capitalization based on 31 Dec 2013.

MMaarrkkeett CCaapp,, RReevveennuuee,, EEBBIITTDDAA ooff LLeeaaddiinngg SSPPss aanndd OOTTTTss

Note: Data for 66 Publicly Traded GSP AccountsMarket Cap as of 1st January of the year

Source: Cisco SPTG, Capital IQ

CONNECTIVITY SERVICES Entry Barriers High Lower

Investment Long-term, high volume, lower risk

Short-term, lower volume, higher risk

Metrics Unit cost Time-to-market, agility

Market Velocity Years / decades Weeks / months

SP Role Incumbency, few players Just one of competitors

Key Success Factors

§ Ubiquitous, seamless connectivity

§ Lean, utility-type production§ Build scale§ Differentiate via speed/QoS,

price, service§ Smart service enablement§ Manage disruption (FTTX,

WiFi/small cells)

§ All-in service ecosystems§ Time-to-market and agility § Highly scalable cost

structures (new services at ≈ zero incremental cost)

§ Customer ownership§ Information & data

ownership/management

© Inluceo Consulting, Ltd., 2014 15

So what should telecommunications service providers focus on?

© Inluceo Consulting, Ltd., 2014 Photo: HBR

16

© Inluceo Consulting, Ltd., 2014

Revenue

OOppeerraattiioonnaall CCoommppeettiittiivveenneessss:: OOPPEEXX RReedduuccttiioonn,, NNeettwwoorrkk SShhaarriinngg,,

CCoo--ooppeettiittiioonn

CCaattcchhiinngg tthhee NNeexxtt WWaavvee ooff

CClloouudd

UUnnlloocckkiinngg TThhee VVaalluuee ooff SSMMBB

NNeettwwoorrkk VViirrttuuaalliizzaattiioonn &&

PPrrooggrraammmmaabbiilliittyy

IInntteerrnneett--ooff--TThhiinnggss

PPrrooffiittaabbiilliittyy aanndd GGrroowwtthh ooff DDiiggiittaall

MMeeddiiaa

PPeerrvvaassiivvee MMoobbiilliittyy

BBiigg DDaattaa aanndd AAnnaallyyttiiccss

SSPP SSeerrvviicceess EEvvoolluuttiioonn

17

Photo: Tauno Tõhk, Creative Commons, http:// /photos/toehk/

The world has gone

18

The world has gone

© Inluceo Consulting, Ltd., 2014 19

-

25

50

75

100

125

-

2,500

5,000

7,500

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14*

PPeerr 110000 IInnhhaabbiittaannttss

MMoobb

iillee--CC

eelllluu

llaarr SS

uubbsscc

rriippttiioo

nnss ((MM

iilllliioo

nnss))

GGlloobbaall MMoobbiillee SSuubbssccrriibbeerrss ((22000011--22001144))

Subscriptions

Source: ITU World Telecommunication/ICT Indicators database

-

500

1,000

1,500

2,000

2,500

'05 '06 '07 '08 '09 '10 '11 '12* '13*

MMoobb

iillee--CC

eelllluu

llaarr SS

uubbsscc

rriippttiioo

nnss

((MMiillll

iioonnss

))

BBrrooaaddbbaanndd SSuubbssccrriibbeerrss -- FFiixxeedd vvss.. MMoobbiillee

((22000055--22001111))

Fixed BBMobile BB

* estimates

Converging forces§ 3rd Generation Applications – video,

social networks, music, books, etc.§ Devices – bigger, powerful§ New, faster cellular technologies –

LTE, LTEA, 5G, …§ Rise of Wi-Fi – availability, ease of

use§ Nomadic Use – versus mobile… drive staggering mobile data traffic growth – 66% CAGR beween 2012 and 2017

© Inluceo Consulting, Ltd., 2014 20

-

200

400

600

800

1,000

1,200

2012 2013 2014 2015 2016 2017 2018 2019

Mobile Services Revenues(2012 – 2019, billions USD)

Americas Asia & Oceania Europe MEA

-

5

10

15

20

25

2012 2013 2014 2015 2016 2017 2018 2019

Mobile Services ARPU(2012 – 2019, USD)

Americas Asia & Oceania Europe MEA

Questions that needs to be answered:How can MNOs make money in new mobile world? What is the next generation of mobile monetization?

Subscriber Penetration

Net

Reve

nue

Revenue Growth Curves

Voice

Messaging

Access Next Generation Mobile Monetization

Sources: Cisco IBSG, Ovum, revenue growth curves adopted from Chetan Sharma Consulting

CAGR: 2.3% L

can use to create additional value

© Inluceo Consulting, Ltd., 2014 21

How to make enough money from mobile to

justify infrastructure investments?

Cost Optimization11

Pricing22

Network Enabled Features

33

New Solutions and Services

44

§ Virtualized production architectures § Next generation mobile access § Improving business agility § New business models

§ Tiered pricing & usage caps § Valued-based pricing § Shared plans Internet of Everything

readiness § Plan rationalization & simplification § Bundling

§ Quality of Service § Policy § APIs § Data & analytics § Security

§ Mobile cloud § Internet of Things “IoT” § Connected vehicles § Enterprise/SMB solutions § OTT collaboration § Wi-Fi/small cell solutions

© Inluceo Consulting, Ltd., 2014 22

0

100

200

300

400

500

600

700

800

900

n Portable Media Players

n Connected TVs

n Desktop PCs

— Traditional TVs

Video Enabled Devices Connected-Fixed; Connected-Portable; Traditional

BRIC Countries

n Notebook

n Netbook

n Tablet

n Wi-Fi Cell Phone

n Portable Game Console

Tablets expands mobile video§ 11% of online users own / planning

to buy a tablet§ 439 installed base by 2015

Mobile TV and Video Service revenue§ $4.5 billion (2013) è $9.5 billion

(2017)§ By 2017, 2 B mobile and tablet users

will watch TV and video on their devices

Online video§ 70% of online users watch online

video

§ In 2020 viewing of internet / online video will surpass live broadcast

2010 2011 2012 2013 2014 2015F

Sources: Cisco IBSG, Screen Digest 2011, Strategy Analytics, 2011, eMarketer, The Diffusion Group

now

© Inluceo Consulting, Ltd., 2014 23

Multi-screen TV

experience

Online Content on TV /STB

Intuitive Unified Navigation for All Content

Social and Interactive Experiences on TV/STB

Cloud-enabled ‘Hassle free’ features

Sources: Cisco IBSG

Objective: Provide high-quality user experience.Services examples:§ Usage Based Tiers and Video§ New Video Experiences (e.g., Web

Video on TV)§ Replay/Catch-up TV§ N-Screen services§ Ad-supported content§ Application and Content Store

Objective: Enable IP distribution to spread content.Services examples:§ Media vault/storage§ Content repurposing§ CDN service§ User profiling§ Targeted advertising§ Billing and payment

exist

© Inluceo Consulting, Ltd., 2014 24

Business to Consumer (B2C)

Source: Cisco WWSP and IBSG

Broadcasters

Advertisers

Content Aggregators

Application Developers

Business to Business (B2B)

$

Service Provider

- massive growth

© Inluceo Consulting, Ltd., 2014 26 Source: Business Insider

Analytics and business intelligence tools empower decision makers as never before by extracting and presenting meaningful information in real-time, helping us be more predictive than reactive.

AAnn tt ccss

Ubiquitous networks and device proliferation enable access to a massive and growing amount of traditionally siloed Information.

BB DD tt

Where is the ?

© Inluceo Consulting, Ltd., 2014 27

The Internet of Things connects all manner of end-points, unraveling a treasure trove of data.

Valu

e fo

r bus

ines

s

IIooTT

Source: Frost & Sullivan

l SSeeaarrcchhl BBrroowwssiinngg

l FFrriieennddss && FFaammiillyyl LLiikkeess && HHoobbbbiieess

l CCoonntteenntt CCoonnssuummeeddl AApppplliiccaattiioonnss

the

© Inluceo Consulting, Ltd., 2014 28

Public Internet

Corporate / Private Internet

Internet of Things

CCoonntteexxtt ccaann bbee sseeeenn by the network(Location, Identity, Presence, X-Platform, etc.)

AAccttiioonn ccaann bbee ttaakkeenn through network control points

(Policy, Security, QoS, Fog, Routing, etc.)

u RReettaaiillu BBaannkkiinngg

u OOiill && GGaassu MMaannuuffaaccttuurriinngg

u HHeeaalltthhccaarree

u CCoommppaannyy--SSppeecciiffiicc AAnnaallyyttiiccssu BBuussiinneessss AApppplliiccaattiioonnss

n MMeetteerrssn MMeeddiiccaall

n CCaarrss // FFlleeeettssn TToollllss

n CCoonnssuummeerr DDeevviicceess

n CCiittyy CCaammeerraassu PPuubblliicc SSeeccttoorr

NNeett

wwoorr

kk DD

aattaa

EExxcchh

aannggee

NNeettww

oorrkk DDaattaa EExxcchhaannggee

Data is being collected everywhere, but the network is always in the middle, able to see, correlate patterns and take action

© Inluceo Consulting, Ltd., 2014 29

-

20

40

60

80

100

120

140

160

180

2011201220132014201520162017201820192020

TToottaa

ll PPuubb

lliicc CC

lloouudd

MMaarr

kkeettss

((BB$$))

GGlloobbaall PPuubblliicc CClloouudd MMaarrkkeett SSiizzee

IaaS PaaS SaaS BPaaS

Total CAGR of 23%

CAGR

39%

23%

35%6%

Telecommunications Service Providers

Systems Integrators & Server Vendors

Advanced SI capabilities, enterprise trust, SMB channels

Internet Companies

Global footprint and scale, large scale apps experience,

low cost

Deciding is critical

© Inluceo Consulting, Ltd., 2014 30

Variable Business ProcessSystem Legacy /

Heterogeneity

Real-time QoS Dynamic Bandwidth

Security / Privacy

Decoupled Best Effort Network

IT ComplexitySimple IT

IITTplus

SSII SSeerrvviicceess

IInntteerrnneett plus

LLaarrggee--SSccaallee DDaattaa CCeenntteerr

IInntteeggrraatteedd NNeettwwoorrkk aanndd IITTIInntteeggrraatteedd NNWW--IITT

plusSSII SSeerrvviicceess

CClloouudd PPllaayyss

(Gaming / HCS / TPaaS / VDI / APM / Hybrid Cloud / CDN / …)

Source: Cisco IBSG SP

(ERP, BPO, …)

(AWS, Gmail, …) (Desktop Outsourcing)

Network - IT Interdependency

Probably the best bet for network service providers

© Inluceo Consulting, Ltd., 2014 31

$11,739

$1,599

$934

$1,211

$1,764

$3,387

$966

$18,225

$12,509 $15,772

$7,855

$1,220

$100

$1,000

$10,000

-10% -5% 0% 5% 10% 15% 20% 25% 30% 35% 40%

Aver

age

Annu

al S

pend

(201

2 –

2017

, log

arith

mic

scal

e)

CAGR 2012 - 2017

SSMMBB SSeerrvviicceess iinn LLAATTAAMM:: SSiizzee aanndd GGrroowwtthh(2012 – 2017)

Source: AMI Partners, 2012, Cisco IBSG Analysis

Wireline Voice

Wireless Communications

Wireless Data

Network

IT Support

Web Hosting

Managed Network

Managed Communications

SaaS Collaboration

IaaS

RMITS SaaS

LLAATTAAMM 22001133 SSppeenndd

SB (1- 99 empl.) 52.8 B$

MB (100-999 empl.) 14.0 B$

Consumers are getting addicted to

© Inluceo Consulting, Ltd., 2014 32

18% 33% 39% 43%67%

66%42% 38% 36%

18%

Mobile Data Pay TV Mobile Voice Landline Phone Broadband

Respondents dropping last or second to lastRespondents dropping first or second

Source: Cisco IBSG, 2011, base: 6 Country Average

reduce expenses?

Some Canadians would give up essentials in order to have access to the Internet, 34% would give up liquor and beer, 31% would give up chocolate, 27% would give up coffee,

6% would give up sex, and 4% would give up daily bathing or showering.

– Rogers Innovation Report 2012

the factors that consumers value ?

© Inluceo Consulting, Ltd., 2014 33

€0.26 / liter €1.10 / liter €4.44 / liter

VALUE BASED PRICING

§ New value criteria – and thus pricing levers – can be created even in mature commodity products

§ The key is to identify & develop new value levers for broadband access

§ Potential levers:

² Broadband access: speed, consumption, quality

² Services portfolio: new SP services, 3rd party services

² Bundling

to

© Inluceo Consulting, Ltd., 2014 34

Evolution of cable operations and infrastructure

User experience

New device ecosystem

IP video end-to-end

Cloud computing

§ New interactive experiences§ Easy to change § Embrace the web§ Aggregation of info, entertainment & communication

§ Lower cost, commoditized devices§ Flexible storage architecture§ Managed configuration

§ Serve any device, source any content§ Leverage personal media§ Off-footprint reach

§ Faster product cycles with web development process

§ Apps store§ Easier to support more devices at scale

§ Ingest content, serve user interfaces§ Billing and entitlement§ Support service with customers

Example: Comcast Strategy / Vision

in this direction

© Inluceo Consulting, Ltd., 2014 35

UUnnlliimmiitteedd PPllaannssCCaappppeedd//TTiieerreeddPPllaannss

SShhaarreedd DDaattaa PPllaannss

AApppp--CCeennttrriicc PPllaannss

0% 20% 40% 60% 80% 100%

UUnnlliimmiitteedd

SShhaarreedd

AApppp--CCeennttrriicc

VVaalluuee--bbaasseedd

%% ooff OOppeerraattoorrss OOffffeerriinngg SSppeeccii eedd DDaattaa PPllaannss

2014

2012

Statistics from a Study conducted by Allot Communications based on data collected from ~180 mobile operators worldwide

© Inluceo Consulting, Ltd., 2014 36

© Inluceo Consulting, Ltd., 2014 37

Differentiated User Experience, Service Velocity, and Monetization

SP Platform Use Network and Data Assets

$ Content Aggregators

Broadcasters

Application Developers

Utilities

Advertisers

$$

$$

$$

$$

$ $$

$

review of is needed

© Inluceo Consulting, Ltd., 2014 38

59

53

47

45

64

47

59

75

81

average

Outsourcing capabilities

Capability to international

Capability to operate lean

Partnership development

Merger and acquisition

Deeper analytics for competitive insights

Deeper analytics for customer insights

Agility (capability to change)

CCaappaabbiilliittiieess aass mmuusstt hhaavvee ttoo ccoommppeettee iinn tthhee ffuuttuurreePercent of respondents

Source: McKinsey TMT, “Fast-forward: An inside view of the TMT sector’s future” Oct. 2012

Business agility is becoming a critical “must have”.

Business Architecture

Technology Architecture

Agile Service Provider

need to evolve their

© Inluceo Consulting, Ltd., 2014 39

Architectural Blueprint

= Standardized Interface

Consumer Business …WholesaleCustomer-centric Business Units

11

Service Supplier Orchestration E2EServiceManagement

22

ServiceSupplier…Access &

TransportMedia& Apps

ThirdParty

IPNetwork

33

44 44 44 44

Source: Cisco IBSG

Guiding Principles

11 Customer segment-centric, market-facing business units

22 Technology-agnostic , end-to-end service fulfillment and assurance

33 Self-contained, component-level service 'factories’ with standardized interfaces to orchestration layer

44 Modular operations governed by SLAs and with minimum inter-dependencies

Interdependent operational processes become modularized into a logical hierarchy that is easily managed and modified

© Inluceo Consulting, Ltd., 2014

Revenue

OOppeerraattiioonnaall CCoommppeettiittiivveenneessss:: OOPPEEXX RReedduuccttiioonn,, NNeettwwoorrkk SShhaarriinngg,,

CCoo--ooppeettiittiioonn

CCaattcchhiinngg tthhee NNeexxtt WWaavvee ooff CClloouudd

UUnnlloocckkiinngg TThhee VVaalluuee ooff SSMMBB

NNeettwwoorrkk VViirrttuuaalliizzaattiioonn &&

PPrrooggrraammmmaabbiilliittyy

IInntteerrnneett--ooff--TThhiinnggss

PPrrooffiittaabbiilliittyy aanndd GGrroowwtthh ooff DDiiggiittaall

MMeeddiiaa

PPeerrvvaassiivvee MMoobbiilliittyy

BBiigg DDaattaa aanndd AAnnaallyyttiiccss

SSPP SSeerrvviicceess EEvvoolluuttiioonn

40

The times are changing for services providers and they need to evolve their service portfolios and business and technology architectures…

© Inluceo Consulting, Ltd., 2014 41

““IIff yyoouu ddiisslliikkee cchhaannggee,, yyoouu wwiillll ddiisslliikkee iirrrreelleevvaannccee eevveenn mmoorree..””

General Eric Shineski

CChhaannggee is not optional.

PPaanneell DDiissccuussssiioonn Telecom and Internet Trends

© Inluceo Consulting, Ltd., 2014 42

PROCESS PLAN CREATIVE

COM

MUN

ICAT

E MOTIVATE INNOVATE CREATE

STRATEGY GO WORK

BRAIN

MEDIA

BOX OUT OF THE

WRI

TE

RESEARCH

SKET

CH

MEE

TIN

G

SUCC

ESS

!

! OK

THINK IDEA

SE

LL PO

SITI

VE

BRAINSTORM POWER

TEAM GOAL

MAR

KET

MOTIVATE

TARGET GROUP

TALK

W

ORD

S iinnlluucceeoo consulting

Thank You!

[email protected] © Inluceo Consulting, Ltd., 2014 43