Yatra: The Future Wall Street Darling You Have Never Heard Of€¦ · Web viewYatra: The Future...

32

Yatra: The Future Wall Street Darling You Have Never Heard Of By Charles McDulin Very attractive (OTA) business model selling for 2x revenue, an enormous runway for growth, and a leading market position in the Indian Online Travel Agency. My bear case is Yatra grows at the rate of the industry and fetches a meager 3x revenue, the stock would still compound at a 12% CAGR for multiple years. Bull case is achievable through M&A activity similar to the path of MakeMyTrip (MMYT), it is not outlandish to think that Yatra has the potential to be a Ctrip/Expedia/Priceline in the 2 nd inning. Having cut my teeth on the Ben Graham deep value investing approach to picking stocks, I rarely venture into growth-ier names that are generating sizeable operating losses, I call them “story stocks” because you basically have to believe the story the management team/bulls are saying about the company’s future, and some of these managers can really spin a yarn, Tesla and Netflix come to mind as stocks with great stories but the math on valuation appears to have rendered these stocks very risky. Tesla is a car company losing $1.5 billion in cash per quarter all on the hope that they will dominate electric vehicle production while Volvo, BMW, GM, etc all roll over and play dead. Investors love the Tesla story so much that they forget that they operate in one of the most brutally competitive businesses – automobile manufacturing – the margins and return on capital in this industry has consistently been in the mid-single digits. Anyway, if you go back half a century, the leading stocks were primarily big industrial, manufacturing, conglomerate type business in low tech industries. Now FAAANNG stocks (FB, BABA, AMZN, AAPL, NFLX, NVDA, GOOGL) are the talk of the street. These businesses are primarily asset-light, and have mercilessly taken advantage of the digital revolution in route to building wide moats. Multi-baggers are made from moats – a.k.a. a sustainable competitive advantage.

Transcript of Yatra: The Future Wall Street Darling You Have Never Heard Of€¦ · Web viewYatra: The Future...

Yatra: The Future Wall Street Darling You Have Never Heard OfBy Charles McDulin

Very attractive (OTA) business model selling for 2x revenue, an enormous runway for growth, and a leading market position in the Indian Online Travel Agency.

My bear case is Yatra grows at the rate of the industry and fetches a meager 3x revenue, the stock would still compound at a 12% CAGR for multiple years.

Bull case is achievable through M&A activity similar to the path of MakeMyTrip (MMYT), it is not outlandish to think that Yatra has the potential to be a Ctrip/Expedia/Priceline in the 2nd inning.

Having cut my teeth on the Ben Graham deep value investing approach to picking stocks, I rarely venture into growth-ier names that are generating sizeable operating losses, I call them “story stocks” because you basically have to believe the story the management team/bulls are saying about the company’s future, and some of these managers can really spin a yarn, Tesla and Netflix come to mind as stocks with great stories but the math on valuation appears to have rendered these stocks very risky. Tesla is a car company losing $1.5 billion in cash per quarter all on the hope that they will dominate electric vehicle production while Volvo, BMW, GM, etc all roll over and play dead. Investors love the Tesla story so much that they forget that they operate in one of the most brutally competitive businesses – automobile manufacturing – the margins and return on capital in this industry has consistently been in the mid-single digits.

Anyway, if you go back half a century, the leading stocks were primarily big industrial, manufacturing, conglomerate type business in low tech industries. Now FAAANNG stocks (FB, BABA, AMZN, AAPL, NFLX, NVDA, GOOGL) are the talk of the street. These businesses are primarily asset-light, and have mercilessly taken advantage of the digital revolution in route to building wide moats.

Multi-baggers are made from moats – a.k.a. a sustainable competitive advantage.

Legacy Moat businesses demonstrate high returns on invested capital (ROIC), if you purchase their stock today and own it for ten years it is likely that you as an investor should do quite well. But, their high ROIC reflects returns on prior invested capital rather than incremental invested capital. In other words, a 20% reported ROIC today is not worth as much to an investor if there are no more 20% ROIC opportunities available to direct the profits.

Equity ownership in these businesses ends up resembling a high-yield bond with a coupon that should increase over time. There is absolutely nothing wrong with this, businesses like Proctor & Gamble (PG), 3M (MMM), and Hormel (HRL) provide a steady yield and are excellent at compounding at slightly above average rates. But, if you are looking to compound your capital at unusually high rates, the focus needs to shift to identifying businesses that also possess a “Reinvestment Moat”.

When searching for a Reinvestment Moat, I’m essentially looking for a business that defies capitalism. Isolated profits in a small market is one thing, but continuing to achieve high returns on incremental dollars for years – should, in theory, not be attainable. As a business gets bigger, and the profits become more meaningful, it will attract more and more competition and returns should eventually compress. Instead I’m looking for a business that actually becomes stronger as it gets bigger. In my opinion, there

are two models that lend itself to this kind of positive reinforcement cycle over time: companies with low cost production or scale advantages and companies with a two-sided network effect.

Creating a two-sided network such as an auction or marketplace business, requires both buyers and sellers, and each group is only going to show up if they believe the other side will also be present. Once the network is established however, it actually becomes stronger as more participants from either side engage. Another way of describing this: as more buyers show up it will attract more sellers, and that in turn will attract more buyers. Once this positive cycle is in place, it becomes nearly impossible to convince either buyer or seller to leave and join a new platform. Businesses such as Facebook, eBay, Priceline, Expedia, and Airbnb have built up strong two-sided networks over time.

The key to Reinvestment Moats is not the specific growth rate forecasted for next year, but instead having conviction that there is a very long runway and the competitive advantages that produce those high returns will remain or strengthen over time. Instead of focusing on next quarter or next year, the key is to step back and envision if this company can be 5x or 10x today’s size in a decade or two? For 99.5% of businesses you will find that it is almost impossible to have that kind of conviction.

Positive Indicators:

If a two-sided network is consistently increasing key metrics like users or gross transactions but is still a small percentage of the overall market: Focus on companies with a high “flow through” margin on an incremental user or transaction, which will help the company expand margins as the network grows.

The management team’s capital allocation prowess must become the Reinvestment Moat, and there must be a long runway of opportunities to deploy capital at high incremental rates.

If your typical 1900’s manufacturing business wants to grow it will require significant capital investments in new factories, machinery, and trucks. Instead we are looking for companies that make money based off intangible assets such as brand name, intellectual property, or developed technology, these require minimal incremental capital investment.

I believe that I have found a stock with not only a great story, but enough evidence for me to come to the conclusion that this stock will be worth much more than it is today – in 24 months – and multiples of what it is today – in 60 months.

Online Travel Agencies (OTA) have been some of the best growth stories on Wall Street. Priceline (PLCN) was a $200M company in the early 2000s, it is now nearly a $100B company. Ctrip (CTRP) in China - IPO’d at a value of ~30 million in 2003, it is now sporting a $30B market cap (compounding at a 30% CAGR).

When booking a flight or hotel, it may seem like there are many online travel agencies (OTAs) to choose from — until you realize Hotels.com, Travelocity, HomeAway, Orbitz.com and several others are owned by Expedia – they recently spun Trivago (TRVG). And Booking.com, Kayak, rentalcars.com and even restaurant reservation service OpenTable are owned by Priceline.

Priceline typically collects a 15% commission on every room reserved at Booking.com; in return, the hotels get access to more potential customers. Hotels, generally, don’t have tons of money to throw at marketing. Priceline was also wildly successful with international expansion, they wisely started their focus in Europe on the premise Europeans took more vacations.

Immense network effects allow these first-mover OTAs to become “capital light compounders” and grow reach/scale by implementing a “buy and build” strategy. As the network grows through brand building, and buying out other brands, the leading OTAs leverage the networking effect to draw both suppliers and customers to their umbrella of platforms. The operating leverage, meaning low incremental costs, allow the top players to generate handsome profits.

As shown below, Priceline has steadily growth the top line at a near 20% CAGR over the last 7 years, while gross margins steadily creep up and are now 97%.

Can we hit the rewind button, and catch Priceline/Expedia back when it was in the second inning?

That is a long shot, but as CTrip CEO said on a recent analyst call – “we view the India market as being where China’s online travel market was 10 or 20 years ago.”

The China travel market took off when GDP per capita hit $2,300. Indian GDP per capita is $1,750 - so if GDP per cap grows at 1.7x GDP then the Indian consumer will hit that inflection point in a couple years - where they have enough at their discretion to travel frequently, over this $2,300 level 65% of each incremental dollar is spent of travel and dining. Their focus on tier II and tier III cities will magnify this effect - with Yatra having largest hotel network and the air segment structural growth.

I’m no genius macro forecaster, but I know several that are, and they are emphatic about the long-term prospects for India - As Buffett, Gundlach, Mobius, Raoul Pal and others have said - India, has tremendous demographics and reform potential, it will be a much stronger economy in a decade.

Yatra Online (NASDAQ:YTRA) happens to be the second-largest online travel agent in India with 16% market share. The company went public at the end of last year via a reverse merger. SPACs historically underperform on average, this is likely a reason Yatra has been overlooked –

As Buffett once said regarding business schools preaching the Efficient Market Hypothesis, “it has been helpful to me to have hundreds of thousands turned out of business schools taught it didn’t do any good to think.”

We believe the market is helping us by writing off SPACs like Yatra as “guilty till proven innocent”.

The name is severely underfollowed, as evidenced by low following on SA and typical light trading volume. This may cause a misunderstanding as Yatra has credible management, credible investors such as Reliance Capital, investors hanging on to shares, not to mention the overall health of the business and the multitude of tailwinds for the company and the industry. We read deep into this book and don’t think the cover says it all.

Yatra likely went the SPAC route instead of an IPO due to the beating MakeMyTrip (MMYT) was taking in the market, this fact weighed down the valuation given to Yatra. As Yatra management describes it, each time they met with investment bankers, the valuation kept dropping, and was uncertain if they'd even be able to get the deal completed. In contrast, the SPAC route ensured certainty. If Yatra could do it all over again, they'd probably have done a traditional IPO, but we have the benefit of 20:20 hindsight. In June of 2016, it wasn't clear that MakeMyTrip would return 150% over the next 12 months.

None of the Yatra's founders took any cash in the go public SPAC transaction. The smartest guys (Norwest, Intel, etc.) in the room rolled all of their Yatra equity into the equity of the public entity.

Naspers, Ctrip, and Priceline (indirectly) control over half of MMYT, the #1 Indian OTA. Each party obviously sees the potential for the market. Ctrip has $5 Billion in cash after recently raising money, the way they talk about India and their MMYT partnership we would not be surprised if they bought the rest of MMYT.

Yatra has built a strong, recognizable brand over the last 11 years and has the largest Indian hotel network (64,500+) and more than 17,000 travel agents in over 1,100 cities and towns. In a recent survey conducted by the economic times, Yatra was voted the #6 overall most trusted internet company in India – ahead of its competitor MakeMyTrip (MMYT) at #13. Last year Yatra was ranked 3rd amongst 370 online services for most trusted travel brand award.

Fresh off raising nearly $80M USD, Yatra has lead what appears to be a successful marketing push, this being the first time Yatra had meaningful funds to be on the offensive. The reputable brand combined with the build out of the network creates this flywheel effect that can only be replicated by a few other competitors. As Yatra puts it, “The infrastructure required to compete in India as an online travel agent represents a significant barrier to market entry. With its high level of brand recognition, large hotel network, significant investment in technology, and deep management experience in this sector, we believe Yatra has created tremendous competitive advantages.”

Yatra’s loyalty program along with customer care has led to 75% of customers being repeat customers. The eCash program was launched in 2014 to reward customers for repeat purchases. Customers accumulate eCash points on travel booked through Yatra, and these points may be redeemed by customers for future bookings. This has introduced an element of stickiness to Yatra’s user base.

In fiscal 2016, 81% of customers’ visits were from unpaid traffic, which includes direct, organic and referrals traffic, compared to 68% in fiscal 2015. We believe this trend reflects the strength of the brand and the strong direct relationship with travel consumers.

Organic mobile app downloads have also now crossed the 10 million mark, as they added over 1 million new installs in the quarter. Yatra had approximately 5.2 million cumulative customers as of Mar 31, 2017. They also witnessed a 67% increase year-over-year in the quarter in direct and unpaid traffic.

Many analysts describe the Indian OTA story as a “land grab”, as players fight for share with heavy discounting. But both Yatra and MMYT have been saying the recent consolidation in the space will continue. The sooner the market rationalizes the better for these two at the top. The increasing pace of consolidation is looking like that of developed market OTAs as well as the recent activity in China that has Ctrip emerging as a clear winner. Part of the reason that Expedia and Priceline are consistent acquirers of OTAs is due to the fact that brands matter. Bolt on acquisitions increase scale and the presentation of options to browsers.

In the fragmented Indian market, most of the smaller players are losing money, naturally leading them to eventually put up a “for sale” sign or stop the bleeding and close up shop. Plus, if you’re a programmer that built a great OTA service product and can’t make money off it because it’s a tight market, why not cash out and sell for several million USD? One can live like a king in India with that much money.

As we discuss later in the article, we believe it is Yatra’s turn to step up to the plate and be involved in some sort of M&A activity.

Yatra is continuing to leverage its brand, network, and tech to become the “one stop shop” for travelers.

The business segment incurs lower marketing spend and thus will reach profitability quicker. Besides the obvious benefits of being in the black this early in the game, reaching profitability next year may allow Yatra to eventually tap the debt markets if conditions are strong – avoid diluting equity holders in the process of growing the brands under its umbrella. MMYT’s ibibo acquisition was dilutive and the stock doubled.

Personnel and operating expenses were near 70% of revenue in 2016 and will grow much slower than the top line – feeding sizeable margin expansion.

50-52% of Yatra’s net revenues being spent on marketing and sales promotion (vs. 82% for MMYT in FY17). Yatra’s net revenue margin on air of 6.8% is lower than MakeMyTrip’s 10.1%. And it also falls behind when it comes to hotels and packages margins – Yatra’s 10.8% significantly underperforming MakeMyTrip’s 19.4%. Overall, Yatra and MakeMyTrip’s combined net revenue margins are 8% and 13.1% respectively. This is primarily due to less marketing spend and being disciplined in costs associated with acquiring customers.

F17 MMYT's average revenue per air transaction was $13 and hotel booking was $20 - far higher than that of YTRA at $8 and $11, respectively. Part of Yatra's lower numbers reflect that 30% of revenue is lower margin B-to-B (20%) or B-to-B-C (travel agents). But B-to-B also has lower customer acquisition costs. So MMYT has higher average revenue per transaction, but they are also average an absurd $13.80 in marketing spend per transaction, versus Yatra's $4.50.

There is 90% internet penetration in US – 290M users. China with 52% or 721m users. India with just 37% penetration or 462m internet users. As of April 2015, only 17% of India’s population reported owning a smartphone, compared to a global median of 43%, according to the Pew Research Center. By comparison, in China and the United States, the percentage of the population reporting smartphone ownership was 58% and 72%, respectively. Smart phone growth adoption rates are close to 70% per year. 17% of the global population resides in India.

The demonetization cash ban is another leg of the story. It simply forces everyone into the new digital economy and will expedite the travel booking segment shift to online, and more specifically mobile.

The most exciting news in this rural India growth story is the demography: 75% of Internet users from rural India are in the age group of 18-30 years and Yatra.com is looking to catch them early in their journey of online travel bookings with the suite of Yatra applications – the Reliance deal (next paragraph) and marketing campaign is certainly helping.

A rising middle class driven by wage increases will increase in disposable income allowing for more travel to take place.

Reliance Jio Partnership is a Huge Catalyst:

Reliance Jio as partner and equity holder (aligned interests), has inked a deal to preload Yatra's app on 35mn phones. According to management, the Reliance relationship represents a dramatic cost per acquirer decrease versus traditional methods – this strategic partnership alone will double yatra’s active

user base at virtually zero incremental costs, allowing Yatra to conserve cash for further bolt on acquisitions.

While not apples to apples, YouTube was pre downloaded on early iPhone models.

Reliance Jio had brought on board 16 million users within a month of its launch as per a PTI report early this month citing a top company executive, it has been adding 0.6-1.1 million customers a day with the launch offer that includes free connection and zero usage charge for the first three months. The firm is aiming to hit the mark of 100 million users by the end of first year of launch.

This partnership will be influential in doubling Yatra’s user base – leading to increased market share/scale while giving Yatra increased leverage over suppliers and increased take rates. Hotels and airlines will continue to feel like they must have access to the Yatra platform because of its burgeoning user base.

Average revenue per user (ARPU) is not a traditional metric for OTA’s, but if based on the correlation this partnership alone has the potential to add ~$112m of annual revenue if just 20% of the 35 million become active users ($16/active user x 7 million active users). This partnership, alone, will likely more than double Yatra’s revenue in a couple years.

Air ticketing and hotels & packages are the two primary business segments, contributing 72% and 21% of net revenues for Yatra. The government of India’s National Civil Aviation Policy 2016 targets a

passenger air traffic (domestic and international) CAGR of 17.5% over FY16-27. Similarly, hotel room availability in India will witness a 7% CAGR over FY16-21 with over 75% of these rooms in the budget and mid-market segment (~95% of Yatra’s hotel room inventory).

Strong revenue growth (28% CAGR over FY17-20E), operating leverage (operating expenses CAGR of 20% over FY17-20E) and inexpensive valuations (3.2x FY18 EV/Sales vs. 4x for MMYT and international peers) make the stock attractive.

The Runway for Air travel is Long:

In the US, the average person flies roughly 1 time every 5 months. In China, the average person flies roughly 1 time every 3.5 years. In India, the average person flies 1 time every 20 years. GOV taking steps for airline industry. Another way to put it, airline and hotel spending per capita in India is less than 20% of the level in China, which is 20% of the level in the US.

The Indian air travel market will show very strong growth over next several years and eventually be the world’s 3rd largest, by somewhere around 2032. If every Indian in the middle-class income bracket were to take just one flight in a year, it would result in the sale of 350mn tickets – a fivefold jump in the 70mn tickets sold in 2014-15 – and that assumes no growth in the number of Indians rising to middle class status.

On top of growth in air travel, currently, only 35% of air bookings are made online. It is basically a pie that is going to grow larger at the rate of 17% each year - while OTA’s share of that pie is going to double from 35% to 70%+.

Coming into the new fiscal year, the growth momentum has continued as air passenger traffic grew 18% year-on-year in fiscal Q1, with healthy demand, has prompted aircraft manufacturers like Boeing to revise their forecasts upwards to more than 2,100 planes required for India over the next 20 years. Indian carriers collectively have already placed more than 1,300 new orders, with 250 planes expected to be put into service over the next 2 to 3 years. Furthermore, demand for air travel is expected to increase with the launch of the government's regional air connectivity program, called UDAN, by operationalizing up to 100 regional airports out of a total 400 unserved or underserved domestic regional airports by fiscal year 2019. Low-cost carriers have recently launched such regional flights already [indiscernible] load factors, indicating a strong pent-up demand for air travel along these routes, and this should help in sustaining healthy growth in the domestic air market.

Yatra isn’t the only one seeing this move coming; but their brand, market positioning, management strategy, along with proven technological capabilities make them one of only a handful of firms that are positioned to ride this wave.

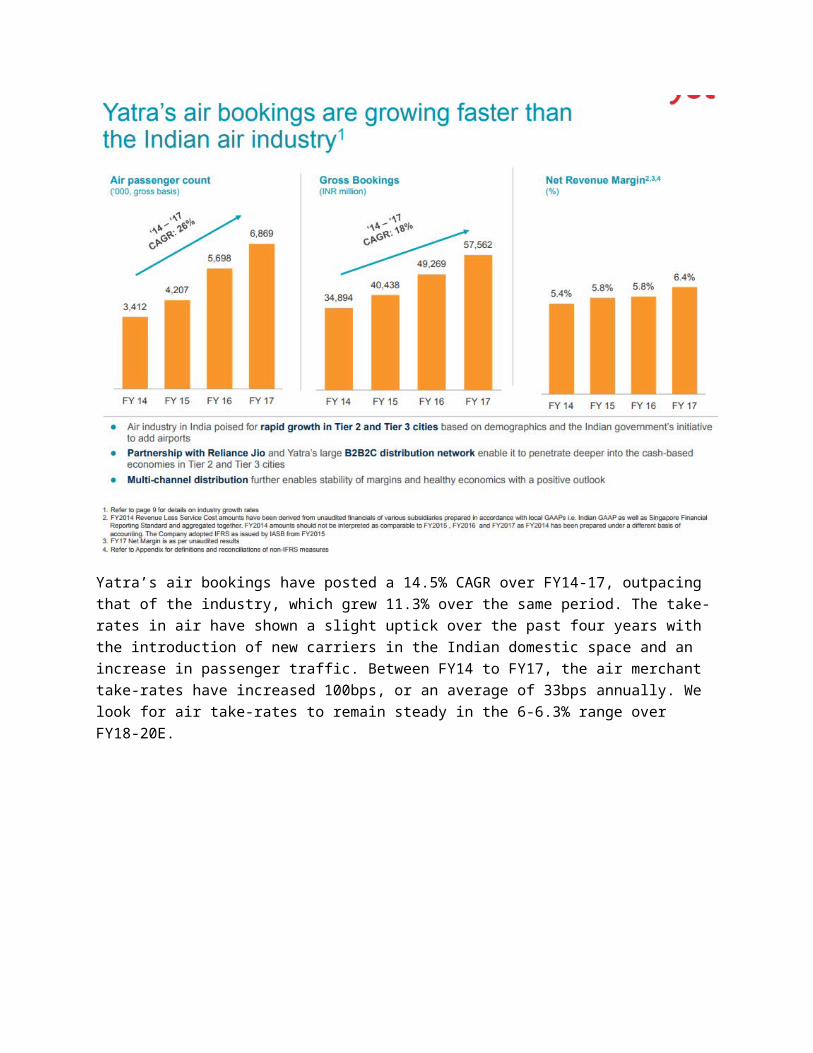

Yatra’s air bookings have posted a 14.5% CAGR over FY14-17, outpacing that of the industry, which grew 11.3% over the same period. The take-rates in air have shown a slight uptick over the past four years with the introduction of new carriers in the Indian domestic space and an increase in passenger traffic. Between FY14 to FY17, the air merchant take-rates have increased 100bps, or an average of 33bps annually. We look for air take-rates to remain steady in the 6-6.3% range over FY18-20E.

Indian air travel gross bookings: with over 2/3rd of revenue coming from the air, if Yatra just grows at the rate of the market – it will experience 14.5% top line growth for much of the next decade.

Railway travel and air travel are very competitive, mostly commoditized. Yatra could experience pressure from an oncoming PayTM which has been very popular and seen growth explode since demonetization. Their basic travel offerings could slow Yatra’s growth.

“The customer’s ability to compare prices has gone up significantly because of meta searches like Trivago and Google Flights forcing the online travel agents to offer more discounts to consumers who download the app,” said Devangshu Dutta, CEO of Third Eyesight, a consultancy firm. “The idea is that if you have the app you are less likely to compare prices.”

Also, Yatra’s brand and loyalty program are strong enough that customers will likely stick with their Yatra platform.

Priceline’s booking.com and Agoda (bought for 4.2x revenues) have been focusing on the inbound market – thus not posing a meaningful threat. Notably, Agoda (OTA) had 7000 hotels in Thai, 33K worldwide. Hence when Priceline was looking to expand into South East Asia, it would ask itself the fundamental question - Is it cheaper to buy or build? In this case, the latter was probably faster, cheaper and more feasible (as Agoda's management team knew how to interact with locals and how the market works).

Hotel Segment:

MakeMyTrip has constantly referenced hotels as having massive growth potential in India, with online (including mobile) only accounting for some 15% of India’s hotel market. Together, MakeMyTrip and Ibibo want to become the one-stop shop for Indian domestic and outbound travel “so we are more like Ctrip than booking.com.” The idea of MakeMyTrip becoming an Indian Ctrip, in which Ctrip owns a stake, is an ambitious aim, helped out by Ctrip-esque merger of a big, heavily funded rival. “Naspers is a deep-pocketed investor, so it’s good that we now have them on our side.”

“Hotel bookings are bound to be the next growth driver for the OTAs, especially because the margins are higher. If you consider the $2.3 billion projection in gross booking value and take at least 15% as commission, the revenue opportunity is huge,” said Abhishek Goyal, the founder of start-up tracker Tracxn.

Online hotel bookings industry in India will grow to $4 billion by 2020, India’s internet user base will double over the same period to 650 million users.

Lodging spending

Yatra’s 64.5k plus hotels in its network and their focus on the untapped tier 2 & tier 3 cities tells me they have plenty of room to grow on that side of the business as well.

Unlike an airline purchase, hotels are much more complicated as it is difficult for users to get an understanding of the experience just by looking at a photo. The hotel market is more open: there is fragmentation both on the demand and supply sides of the business, which gives an aggregator more control over discovery and inventory (network effects 101).

MakeMyTrip commentary on Hotels (Q2, 2017):

Our margins in the strategic hotels and packages businesses stood at 21.7%, which was slightly better than the previous quarter's margin of 20.5%, and significantly better than the reported margin of 16.9% in the same quarter of the previous fiscal year.

when you look at hotels, when I say it's a more evolved product to purchase, but it's actually there's also far more work which happens on the supply side, which is needed and it's not just wiring up 40,000 or 45,000 hotels or having direct connects with them.

And booking.com is definitely, I think, getting more interested in the market and also been mentioned in their own earnings call. And I think that is actually a testimony to the fact that this hotel market is opening up. We are now at 10% penetration. There is 90% to go.

And so we think, at that higher price point, consumers are less brand focus, but they are definitely amenities and quality focus. So I think they are more interested in can I get this offering in the right location, at the right price point and with the service quality offering guarantee.

MMYT is more focused on the higher price point segment, Yatra will continue with its strategy in Tier 2 & tier 3 cities. Again, both can win.

Business Segment (revisited):

The Government of India has recently introduced Goods and Services Tax. The tax will help migrate an increasing number of small and medium scale corporate customers into the organized corporate travel management fold, as they run the risk of losing out on input credit on the taxes paid if they deal with the informal sector. As this trend develops, Yatra will be well positioned to capture the growth in the business travel environment in India. Management even stated the business travel environment “is poised for a period of strong and sustained growth over the next 5 years.” Typically, one out every five travel bookings are business.

Yatra commentary from the previous quarter:

On the business front, we registered our highest growth rate of 33.8% on Revenue Less Service Cost, which is the highest over the last 5 quarters.

The combination of Yatra's existing corporate travel business and ATB's business, we believe, makes us the largest corporate travel platform in India by gross bookings, servicing over 650 of some of India's largest corporations.

we are the largest player in the sector by gross bookings. Corporate travel in India mid-teens CAGR for next five years. In an emerging market with limited disposable income, business travel is generally the first form

of travel undertaken by consumers. The combined entity of Yatra and ATB now has the potential to access a captive consumer base of over 4 million people who are employed in the 650-plus large- and medium-scale enterprise customers that the entity will service.

India's largest at over 65,000 properties to the enterprise customers of ATB, and the opportunity to implement Yatra's self-booking corporate travel platform and mobile app across ATB's customer base.

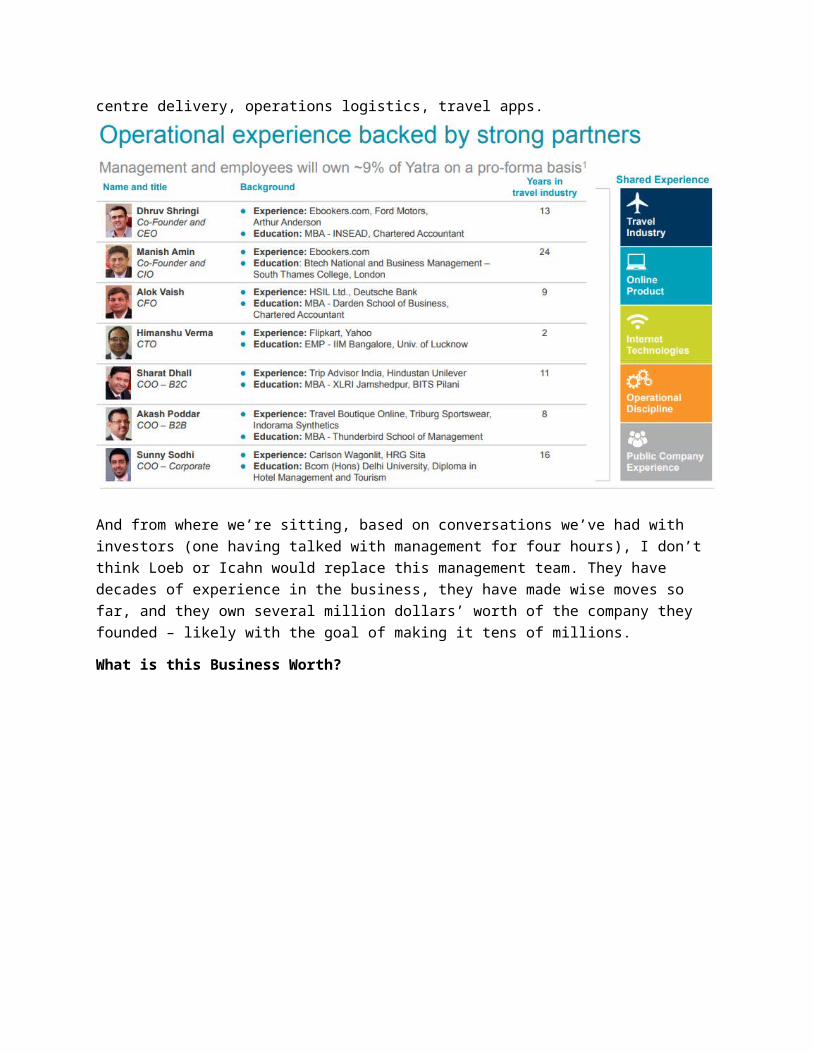

Management:The management team has shown their ability to execute thus far, with very favorable capital allocation decisions and wise strategic moves. The company has partnered with Reliance Jio to reduce customer acquisition cost and with the acquisition of ATB – is attacking large growth opportunities without forking over much capital.

Dhruv Shringi Co-Founder & CEO: Since its successful launch in January 2006, Dhruv, has lead Yatra.com’s growth from a three-member organization to a 1,400 person strong organization – thereby making it the leading travel brand in India. Previously, Dhruv was the Director Group Operations and Technology of the Ebookers Group in London. Before that he worked with the Ford Motor Company in their Business Strategy team based in London. He also spent over six years with Arthur Andersen based in their office in Delhi. Dhruv holds an MBA from INSEAD and is also a qualified Chartered Accountant. Manish Amin Co-Founder & CIO: Manish is a veteran of the travel industry with over 20 years’ experience in the travel and IT industry, 15 of which were with Ebookers where he was the Head of Technology Infrastructure. He has vast knowledge and experience in business strategy, sales/call centre

delivery, operations logistics, travel apps.

And from where we’re sitting, based on conversations we’ve had with investors (one having talked with management for four hours), I don’t think Loeb or Icahn would replace this management team. They have decades of experience in the business, they have made wise moves so far, and they own several million dollars’ worth of the company they founded – likely with the goal of making it tens of millions.

What is this Business Worth?

Yatra recently guided 35% to 40% Revenue Less Service Cost growth.

There is potentially some risk to the top line expectation from Deutsche (PayTM competition), but if Yatra sprinkles in some inorganic growth from bolt-on acquisitions, then they can rather easily grow the top line 30% per annum through 2020. Also, there is plenty of wiggle room on valuation, as Yatra at $10 trades below 2x 2020 revenue – I agree with Deutsche that the Yatra should command multiple closer to 5x given the degree of runway for the space.

As Dane Capital said, “While we are not momentum investors, management has stated that it anticipates a 30-35% revenue CAGR over the next several years. The company has been growing in the mid 20% range for multiple years. As a result of a stronger balance sheet, solid demographic trends, and a government mandate to dramatically increase the number of flights in India, we believe an acceleration in growth is achievable. In addition, the mass installation of the Yatra app on Reliance Jio phones should augment growth. Finally, it appears - and based on our conversation with contracts in India - that both MakeMyTrip and Yatra, have been, and will continue to take share from smaller, subscale competitors. Management has noted that its balance sheet has limited some of its marketing

efforts and we suspect this trend will reverse. We believe the optics of revenue and bookings acceleration will positively impact Yatra's share price.”

My Base Case:

Top line growth at low 20s CAGR till 2020 then growth of 11% till 2024 (which is around the industry average).

At a conservative 3.3x multiple on revenue - you double your money, and triple it by 2024 at a 16% CAGR.

Bear Case:

Top line growth of 12% per year, averaging what the OTA category will grow at. Zero lift from Reliance deal, no inorganic growth modeled. You still double your money in 6 years, a 12% CAGR.

Bull Case:

Yatra engages in a meaningful merger or is acquired, as aforementioned – the multiple would expand if a bigger Yatra controlled more market share.

If you want to get crazy, Yatra could be a Ctrip in the second inning, meaning we could have at least a 10 then 20 then 50 bagger. If Yatra were to go up 50x – its market cap would be $15B, half the size of Ctrip.

The Bull Case Explained, A Trip to $30:

Cleartrip and Expedia are estimated to have 7%, and 5% share, respectively. Expedia has been a “serial acquirer” – which has been a very effective way to grow scale and presence and eventually hold a commanding position in OTA markets. Given the decade long tailwinds and the exponential growth potential of the Indian OTA market, Expedia could stake its claim in a meaningful way with a Yatra acquisition. They would eventually bolt on smaller players similar to what they have done in the US. My thesis rests on more than the speculation of a deal, but let’s look at the numbers. The market leader is MMYT – with ~41% share, Yatra is a rather distant second with 16% market share (pro-forma ~20% with Reliance Jio catalyst and acquisition). Mr. Market has pegged MMYT with a market value of $3 billion USD and Yatra has a $300 million, so the market values MMYT at 10x that of Yatra, despite the former only having 2.5x the market share and Yatra trading at 2x 2020 revenue.

It is not black and white arbitrage, but the market is missed a couple key points (primarily because few are looking at Yatra to begin with).

Last October, MakeMyTrip paid $720 million (structured as a merger), or 17x revenue for ibibo, the number 3 player in the India travel market, despite enormous operating losses (i.e. 4-5x the losses of Yatra).

MakeMyTrip went up 55% the next day….

Why? Because scale matters in the OTA space and MMYT took out its fiercest competitor. Ibibo is known for its presence in the hotel space, which is projected to be a higher margin/take rate category – but lower projected top line growth than air, ibibo was also know for irrational pricing.

The industry is consolidating, and single digit market share players know that to they can either struggle to survive, or join forces with bigger players and thrive.

If Yatra merged with an 8-10% market share player (Cleartrip comes to mind) and the combined company proceeded to capture 26-28% market share and add a few bolt-on acquisitions the company could get to a 30% market positioning rather quickly. My logical argument would be – “What would the combined entity be worth in relation to MMYT?” At least half that of MMYT – in a bearish scenario, as market share would lag by only ~11% in absolute terms. Meaning the combined entity would be worth at least 1.5B. Any way you slice and dice it - the market would have to respect the combined entity with such a market presence. While there would be dilution, 60% of $1.5B is worth ~3x more than 100% of $300M. If management engineered a deal like this, Yatra stock would double quicker than a cheetah attacking a chuck roast.

Yatra, fresh off raising funds, is well capitalized and 2nd in market share, free from regulatory risk (unlike MMYT), with a proven management team. We believe that M&A activity is a severely underpriced catalyst for Yatra shares.

The next question is, “is MakeMyTrip overvalued?” I do not believe this to be the case. In looking at the big picture, the market capitalizations of the market leaders in different OTA geographies range from 7-9x that of MMYT (Expedia & Ctrip), to 30x (Priceline). It is no guarantee that MMYT or Yatra will become the next Priceline or Expedia, but it is obviouss that the top couple of market leaders have multiple advantages (scale, networking effects, acquisition capacity, financial market access) that allow them to continue to eat up market share. We also know that this is a very attractive business model and established brands have a moat.

Knowing what we now know about both Yatra and the industry runway, “What would a rational buyer pay for a business that will likely maintain a 1/5th market share of the Indian Online Travel Agency (OTA) market – which is slated to growth at a low – teens CAGR over the next decade (eerily similar to US/China OTA mkt in early innings) – operating in an industry that has proven to be lucrative for first – movers with strong brands and network effects – operating in a country with only 20% smartphone adoption – a population 3x the US – growing GDP 3x the rate of the US?

I think the private market value of Yatra is around $500M (over $16/share), this is a 30% discount to the price tag put on ibibo when they were bought by MakeMyTrip for 17x revenue . Yatra currently trades at 2x 2020 consensus revenue estimates….

So Why YTRA over MMYT?

There is plenty of room in the space for multiple players, and both will likely be worth a lot more in a decade. Yatra has a much smaller absolute and relative valuation being assigned to it. We like the Reliance catalyst, we like the underpriced M&A potential, and as a SPAC we think Yatra is a baby being thrown out with the bath.

“Where’s my Margin of Safety?”“Companies with established business models in stable markets, where your story does not change over time, and that is the path many old-time value investors have chosen to take, pointing to history of success that others who have taken this path have had in the past. The other is to learn to live with the discomfort of change and to accept that not only is it unavoidable but that the biggest business and investment opportunities exist in those environments where there is the most change.”

-Narrative & Numbers, by NYU Professor Aswath Damodaran.

In my view, investing is all about risk reward. While a couple of bearish scenarios could lead to the stock losing 3 or 4 points, those probabilities are low, and I have conviction that if Yatra continues to execute with its organic plus inorganic growth – we are getting a bargain price for the 2nd largest Indian OTA.

Hopefully after suffering through reading this piece, you come to the same conclusion as myself, “management has to really fumble in a big way for them to not create value with the unique opportunity this first-mover business has.”

There is definitely a risk that they do allocate our capital ineffectively by burning through cash (not probable) or making a bad acquisition.

Yatra’s position is getting stronger, it is one where they are not going to get runover by competition, they are stronger than ever financially, have a strong user base and brand, the right strategic partnership in Reliance, and solid management.

As previously described, if they gain zero market share and just grow at the rate the industry grows and stay in their 16-17% market share position, this company is worth more than the $300M price tag being assigned to it by Mr. Market.

How can we “kill” the Yatra thesis?

PayTM’s rapid growth, a platform to take share and set low prices.

This risk is somewhat mitigated by the strategic partnership with Reliance Jio, as well as the loyalty program. Also, PayTM could buy the whole thing for 450m and capture 1/5th share overnight, eliminate a competitor, and build out/use Yatra how they see fit.

Indian Economic risk

I would argue there is more upside risk than downside risk here. I think being overweight India over the next 5-10 years will pay off. I’m buying Yatra with the mindset that the stock market will be closed for the next 10 years.

OTA player(s) act irrational

A wave of consolidation has come to the space and will inevitably continue. Yatra’s #2 positioning and loyal customers de-risks this case.

There will be massive swings in the stock price

As seen from MMYT, the stock can have large movements – as expected with an unprofitable business. This can be seen as an opportunity if the pendulum swings too far one way or the other. Short term price volatility is not associated with risk, in our view.

Time is your friend with a wonderful business like Yatra.

Charlie Munger outlined the following in “The Art of Stockpicking”:

“If the business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6% return—even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you’ll end up with a fine result.”

Follow on notes:

8/20: The advantage Paytm enjoys over other online travel companies is a large user base and the opportunity to get a chunk of these users to book travel tickets. “Our biggest strength is the reach we enjoy. Millions of users can come online through us to book a travel ticket. Right now, we have about 200 million users on the Paytm platform. If we look at the total number of consumers buying online travel it may not be more than 30 million. So, that is the gap we want to fill," Abhishek Rajan, vice-president (travel marketplace) at Paytm told Business Standard.

Rajan said the economy was at an inflection point where fares are more affordable and people have aspirations to travel. “Such people may end up booking online gradually. We want to go after this user base. Our payments bank will help us access another 500 million users in the near future. That is a huge pool of people whom we can introduce to online travel".

The aggression of Paytm might be a worry for incumbents. But Rajan said Paytm is not looking at taking share away from the existing market.

“We want to create a much bigger market, mostly untapped". Yatra said it would be able to safeguard its territory. “Given our loyal base, we are in a relatively secure position irrespective of what happens on the competitive front in the short term. Players like Paytm will also have to figure out which all battles they want to fight. Capital is scarce at the end of the day and at some point one will need to prioritise," said Dhruv Shringi, co-founder and CEO, Yatra.

But horizontal players easy to get share – paytm

Paytm, however, is building a marketplace taking a cue from Alitrip, the travel marketplace run by its investor Alibaba in China. "Our intention is to continuously add new travel categories to the platform and drive organic growth without making large marketing investments," added Rajan.