Which market? An overview of London, New York, - PwC · PDF fileWhich market? An overview of...

8

Which market? An overview of London, New York, Hong Kong and Singapore stock exchanges www.pwc.com

Transcript of Which market? An overview of London, New York, - PwC · PDF fileWhich market? An overview of...

Which market?An overview of London, New York, Hong Kong and Singapore stock exchanges

www.pwc.com

2 | Which market? | PwC

PwC | Which market? | 1

Which stock exchange is right for your company?

An overview of regulatory listing requirements in London, New York, Hong Kong and SingaporeHaving decided that a public offering is the next step in your company’s development, choosing ‘where’ to list is one of the next most important decisions to consider, whether you plan an initial public offering (IPO) or a secondary listing.

As the financial markets become increasingly global, companies have more options available to them. Most companies, typically have three options:

1. Listing on their domestic exchange

2. Listing on an overseas exchange

3. Dual listing on several exchanges

A variety of factors needs to be weighed up to help you get the best advantage for your company, during the listing process and once your company is trading as a publicly listed company. If key questions are considered early in the process it will help you understand what changes your company will need to go through before you start the process in earnest and also ensure you are aligned with all stakeholders’ expectations.

Choosing the most appropriate market may not be straightforward and will depend on a number of questions including:

• Stage in your company’s development

• Your overall growth strategy and objectives

• Regulatory requirements on each exchange (initial and ongoing)

• Speed and efficiency of listing

• Cost involved in the initial process and ongoing compliance

• The type of investors that may be interested in your company or sector

To help you determine which options are best for your company, we have developed this brochure working with our capital markets experts across the PwC global network. This brochure identifies the main regulatory requirements involved in a listing in some of the current leading global stock exchanges: London, New York, Hong Kong and Singapore.

We have compared the Main Markets of these exchanges, briefly highlighting the differences between them regarding certain key admission criteria and continuing obligations. We hope that you find our ‘Which market?’ brochure both informative and valuable.

2 | Which market? | PwC

MarketAdmittable securities Main indices

London Stock Exchange (LSE)

The LSE’s Main Market is the principal market for UK and international listed companies, from all industries and sectors.

The Main Market accommodates the admission of companies to trading on the Premium, High Growth Segment or Standard markets. A Premium Listing requires higher compliance and disclosure requirements than the EU minimum standards required for High Growth Segment and Standard Listings.

Main • Equities

• Depositary Receipts (DRs)

• FTSE series – open to international issuers

• FTSE 100

• FTSE 250

• FTSE All share

• FTSE techMark

• FTSE Russia IOB – top 15 Russian GDRs

AIM is the LSE's market for smaller high growth companies.

AIM • Equities • The FTSE AIM Index Series includes the FTSE AIM UK 50 Index, FTSE AIM 100 Index, FTSE AIM All-Share Index and FTSE AIM All-Share Supersector Indices

Hong Kong Stock Exchange (HKEx)

The HKEx Main Board is suitable for established companies that meet profit or other financial requirements.

Main • Equities

• DRs

• Hang Seng Index

The Growth Enterprise Market (GEM) is designed for growth companies.

GEM • Equities

New York Stock Exchange (NYSE)

The NYSE has several markets including NYSE and NYSE MKT. NYSE prescribes higher initial listing requirements, whereas the NYSE MKT is designed for younger, smaller and high-growth companies.

NYSE • Equities

• DRs

• Dow Jones Industrial

• NYSE composite

• NYSE U.S. 100

• S&P 500

NASDAQ There are three different markets within NASDAQ: NASDAQ Global Select Market, NASDAQ Global Market and NASDAQ Capital Market. NASDAQ Global Select Market prescribes the highest initial listing requirements.

NASDAQ • Equities

• DRs

• NASDAQ 100

• NASDAQ Global Select Market composite

• S&P 500

• Dow Jones Industrial

Singapore Exchange (SGX)

Main Board is suitable for large, established companies that meet financial entry requirements.

Main • Equities

• DRs

• FTSE Straits Times Index

Catalist is the market for smaller companies without a track record of profitability.

Catalist • Equities

Stock exchange overview

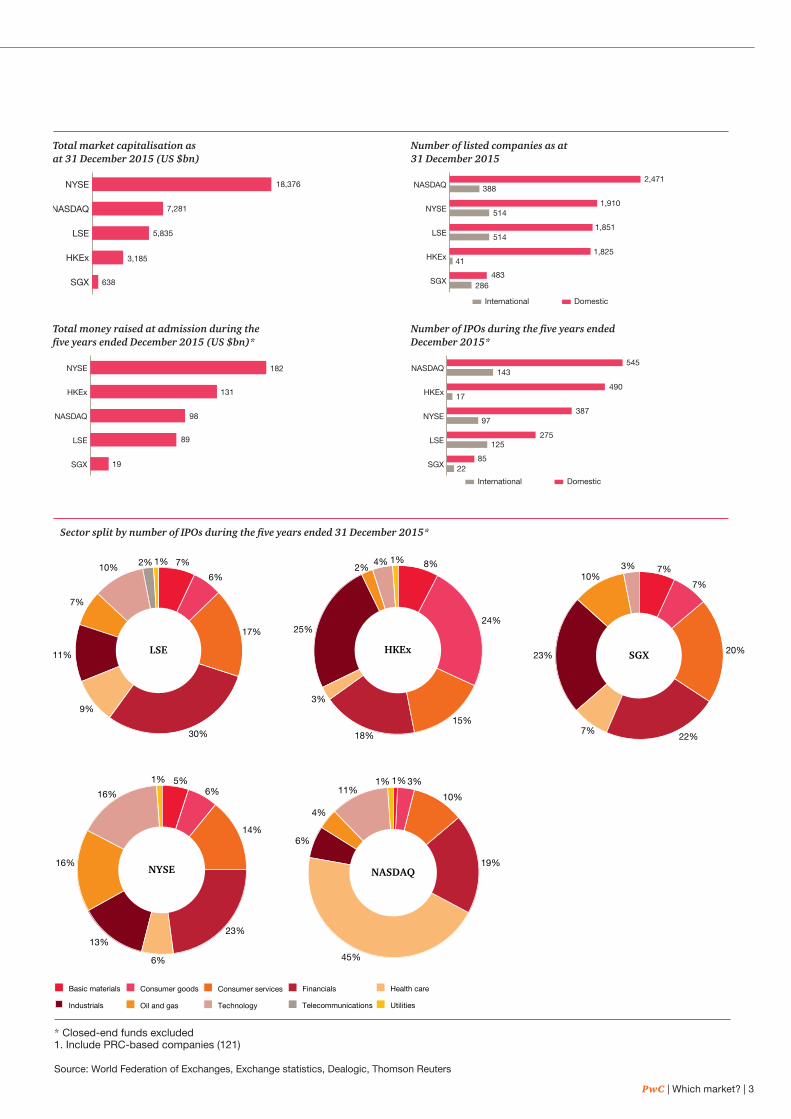

PwC | Which market? | 3

Total money raised at admission during the five years ended December 2015 (US $bn)*

Number of IPOs during the five years ended December 2015*

SGX

HKEx

LSE

NASDAQ

NYSE 18,376

7,281

5,835

3,185

638 SGX

HKEx

LSE

NYSE

NASDAQ

International Domestic

2,471388

514

514

41

483286

1,910

1,851

1,825

0 50 100 150 200

SGX

LSE

NASDAQ

HKEx

NYSE

131

182

98

89

19Non-domesticDomesticSGX

LSE

NYSE

HKEx

NASDAQ545

143

17

97

125

8522

490

387

275

International Domestic

Total market capitalisation as at 31 December 2015 (US $bn)

Number of listed companies as at 31 December 2015

7%10%6%

17%

30%

9%

11%

7%

1%2%

LSE

8%

24%

15%

25%

18%

3%

2%4% 1%

HKEx

5%6%

14%

23%

16%

16%

6%

13%

1%

NYSE

10%

19%

45%

6%

4%

11%1%1% 3%

NASDAQ

Sector split by number of IPOs during the five years ended 31 December 2015*

* Closed-end funds excluded 1. Include PRC-based companies (121)

Source: World Federation of Exchanges, Exchange statistics, Dealogic, Thomson Reuters

Basic materials Consumer goods Consumer services Financials Health care

Industrials Oil and gas Technology Telecommunications Utilities

7%

7%

20%23%

22%7%

10%3%

SGX

Ove

rvie

w o

f key

list

ing

regu

lato

ry r

equ

irem

ents

Th

is ta

ble i

s int

ende

d to

pro

vide

a h

igh

leve

l ove

rvie

w o

f key

list

ing

and

ongo

ing

regu

lato

r cri

teri

a fo

r com

pani

es lo

okin

g to

IPO

on

the m

arke

ts in

dica

ted.

Lond

on M

ain

Mar

ket (

Pre

miu

m

List

ing)

Hon

g K

ong

Mai

n B

oard

New

Yor

k S

tock

Exc

hang

eN

AS

DA

Q (G

loba

l Sel

ect)

Sin

gapo

re M

ain

Boa

rd

Init

ial l

isti

ng c

rite

ria

Spo

nsor

1R

equi

red

Req

uire

dN

ot re

quire

dN

ot re

quire

dR

equi

red

Aud

ited

trac

k re

cord

Thre

e ye

ars

audi

ted

acco

unts

, no

mor

e th

an

six

mon

ths

old

Thre

e ye

ars

audi

ted

acco

unts

, no

mor

e th

an

six

mon

ths

old

Thre

e ye

ars

audi

ted

acco

unts

. For

em

ergi

ng

grow

th c

ompa

nies

(EG

Cs)

und

er th

e JO

BS

A

ct, t

wo

year

s of

aud

ited

finan

cial

sta

tem

ents

ar

e pe

rmitt

ed

Thre

e ye

ars

audi

ted

acco

unts

. For

em

ergi

ng

grow

th c

ompa

nies

(EG

Cs)

und

er th

e JO

BS

Act

, tw

o ye

ars

of a

udite

d fin

anci

al s

tate

men

ts a

re

perm

itted

Thre

e ye

ars

audi

ted

acco

unts

, no

mor

e th

an s

ix

mon

ths

old

Acc

ount

ing

stan

dard

EU IF

RS

or I

FRS

equ

ival

ent f

or n

on-E

U is

suer

sH

K F

RS

, IFR

S, C

AS

BE

(for P

RC

issu

ers

only

) U

S G

AA

P o

r oth

er a

ccou

ntin

g st

anda

rds

may

be

acc

epte

d in

cer

tain

circ

umst

ance

s.

US

GA

AP

or I

FRS

U

S G

AA

P o

r IFR

SS

inga

pore

FR

S, I

FRS

or U

S G

AA

P

Fina

ncia

l crit

eria

At l

east

75%

of t

he e

ntity

’s b

usin

ess

mus

t be

supp

orte

d by

a re

venu

e ea

rnin

g tr

ack

reco

rd

for t

he th

ree

year

per

iod

(som

e di

spen

satio

n fo

r spe

cific

indu

strie

s e.

g. m

inin

g)M

inim

um m

arke

t cap

at a

dmis

sion

– £

700,

000

Com

pany

nee

ds to

mee

t one

of t

he fi

nanc

ial

crite

ria:

i) •

Pro

fit o

f at l

east

HK

$20

m fo

r th

e

mos

t rec

ent fi

nanc

ial y

ear,

•

Pro

fit in

agg

rega

te o

f at l

east

HK

$3

0m fo

r th

e tw

o pr

eced

ing

finan

cial

ye

ars,

and

•

Mar

ket c

ap o

f at l

east

HK

$20

0m a

t

tim

e of

list

ing.

ii) •

Mar

ket c

ap o

f at l

east

HK

$2b

n at

tim

e of

list

ing,

•

Rev

enue

of a

t lea

st H

K $

500m

for

th

e m

ost r

ecen

t fina

ncia

l yea

r, an

d

• Po

sitiv

e op

erat

ing

cash

flow

s of

at

leas

t HK

$10

0m in

agg

rega

te fo

r

the

thre

e pr

eced

ing

finan

cial

yea

rs.

iii)

• M

arke

t cap

of a

t lea

st H

K $

4bn

at ti

me

of

list

ing,

and

• R

even

ue o

f at l

east

HK

$50

0m fo

r

the

mos

t rec

ent fi

nanc

ial y

ear.

Com

pany

nee

ds to

mee

t one

of t

he fi

nanc

ial

crite

ria:

i) E

arni

ngs

Test

Inco

me

befo

re ta

x fr

om c

ontin

uing

op

erat

ions

and

afte

r m

inor

ity in

tere

st,

amor

tisat

ion

and

equi

ty in

the

earn

ings

or

loss

es o

f inv

este

es (s

ubje

ct to

ce

rtai

n ad

just

men

ts) m

ust t

otal

at l

east

•

US

$10

m in

the

aggr

egat

e fo

r th

e la

st

th

ree

fisca

l yea

rs, t

oget

her

with

a

min

imum

of U

S $

2m in

eac

h of

the

tw

o m

ost r

ecen

t fisc

al y

ears

, and

po

sitiv

e am

ount

s in

all

thre

e ye

ars

O

R

• U

S $

12m

in th

e ag

greg

ate

for

the

last

th

ree

fisca

l yea

rs, t

oget

her

with

a

min

imum

of U

S $

5m in

the

mos

t

re

cent

fisc

al y

ear

and

US

$2m

in th

e

next

mos

t rec

ent fi

scal

yea

r.

ii) E

arni

ngs

Test

fo

r E

GC

s In

com

e be

fore

tax

from

con

tinui

ngop

erat

ions

and

afte

r m

inor

ity in

tere

st,

amor

tisat

ion

and

equi

ty in

the

earn

ings

or lo

sses

of i

nves

tees

(sub

ject

to c

erta

in

adju

stm

ents

) mus

t tot

al a

t lea

st:

• U

S $

10m

in th

e ag

greg

ate

for

the

last

two

fisca

l yea

rs, t

oget

her

with

a

min

imum

of U

S $

2m in

bot

h ye

ars.

iii) G

loba

l Mar

ket C

apita

lisat

ion

Test

Issu

er m

ust h

ave

at le

ast:

•

US

$20

0m in

glo

bal m

arke

t cap

.

Com

pany

nee

ds to

mee

t one

of t

he fi

nanc

ial

crite

ria:

i) •

Min

imum

inco

me

from

con

tinui

ng

oper

atio

ns b

efor

e in

com

e ta

xes

of:

– U

S $

11m

ove

r th

e pr

ior

thre

e fis

cal

ye

ars

in a

ggre

gate

, and

– U

S $

2.2m

in e

ach

of th

e tw

o m

ost

re

cent

fisc

al y

ears

, and

•

Posi

tive

inco

me

from

con

tinui

ng

oper

atio

ns b

efor

e in

com

e ta

xes

in

each

of t

he p

rior

thre

e fis

cal y

ears

.

ii) •

Min

imum

tota

l rev

enue

in th

e pr

evio

us

fisca

l yea

r –

US

$11

0m,

•

Min

imum

ave

rage

mar

ket c

ap o

ver

th

e pr

ior

12 m

onth

s –

US

$55

0m,

•

Min

imum

cas

h flo

ws

of U

S $

27.5

m

over

the

prio

r th

ree

fisca

l yea

rs in

ag

greg

ate,

and

•

Posi

tive

cash

flow

s in

eac

h of

the

pr

ior

thre

e fis

cal y

ears

.

iii) •

Min

imum

tota

l rev

enue

in th

e pr

evio

us

fisca

l yea

r –

US

$90

m, a

nd

• M

inim

um a

vera

ge m

arke

t cap

ove

r

the

prio

r 12

mon

ths

– U

S $

850m

.

iv) •

Min

imum

ave

rage

mar

ket c

ap a

t the

tim

e of

list

ing

– U

S $

160m

, and

•

US

$80

m o

f tot

al a

sset

s an

d U

S

$55m

of s

tock

hold

ers’

equ

ity in

the

m

ost r

ecen

t pub

licly

repo

rted

fina

ncia

l

st

atem

ents

.

Com

pany

nee

ds to

mee

t one

of t

he fi

nanc

ial

crite

ria:

i) •

Min

imum

con

solid

ated

pre

-tax

pro

fit

of a

t lea

st S

$30m

for

the

late

st

finan

cial

yea

r,

• O

pera

ting

trac

k re

cord

of a

t lea

st

thre

e ye

ars.

ii) •

Pro

fitab

le in

the

late

st fi

nanc

ial y

ear,

•

Mar

ket c

ap o

f not

less

than

S$1

50m

ba

sed

on th

e is

sue

pric

e an

d po

st-

invi

tatio

n is

sued

sha

re c

apita

l, an

d

• O

pera

ting

trac

k re

cord

of a

t lea

st

thre

e ye

ars.

iii) •

Ope

ratin

g re

venu

e in

the

late

st

co

mpl

eted

fina

ncia

l yea

r, an

d

• M

arke

t cap

of n

ot le

ss th

an S

$300

m

base

d on

the

issu

e pr

ice

and

post

-

in

vita

tion

issu

ed s

hare

cap

ital.

Rea

l

E

stat

e In

vest

men

t Tru

sts

and

Bus

ines

s Tr

usts

who

hav

e m

et th

e

S$3

00m

mar

ket c

ap te

st b

ut d

o no

t

ha

ve h

isto

rical

fina

ncia

l inf

orm

atio

n

may

app

ly u

nder

this

rul

e if

they

ar

e ab

le to

dem

onst

rate

that

they

will

ge

nera

te o

pera

ting

reve

nue

imm

edia

tely

upo

n lis

ting.

Ope

ratin

g

trac

k re

cord

requ

ired

is a

t lea

st o

ne

year

.

Pro

fit fo

reca

stO

ptio

nal4

Opt

iona

l 4

Priv

ate

profi

t for

ecas

t mem

oran

dum

for t

he

rem

aind

er o

f the

fina

ncia

l yea

r req

uire

d to

be

subm

itted

to H

KE

x

for r

evie

w.

No

requ

irem

ents

No

requ

irem

ents

• Fo

r co

mpa

nies

, pro

fit a

nd c

ash

flo

w fo

reca

st m

emor

andu

m fo

r th

e

cu

rren

t yea

r an

d en

suin

g ye

ar

mus

t be

subm

itted

upo

n re

ques

t

by

the

Exc

hang

e.•

For

busi

ness

trus

ts a

nd R

EIT

s, p

rofit

and

cash

flow

fore

cast

and

proj

ectio

ns a

re re

quire

d to

be

incl

uded

in th

e pr

ospe

ctus

.W

orki

ng c

apita

l st

atem

ents

Cov

erin

g 12

mon

ths

Cov

erin

g 12

mon

ths

Not

requ

ired

Not

requ

ired

Cov

erin

g 12

mon

ths

Com

pany

his

tory

2Th

ree

year

s, s

ubje

ct to

exe

mpt

ions

Thre

e ye

ars,

sub

ject

to e

xem

ptio

nsTh

ree

year

s fo

r com

pani

es li

stin

g un

der

Earn

ings

Tes

t and

Glo

bal M

arke

t Cap

italis

atio

n Te

st, t

wo

year

s fo

r com

pani

es li

stin

g un

der

Earn

ings

Tes

t for

EG

Cs

Thre

e ye

ars,

sub

ject

to e

xem

ptio

ns, t

wo

year

s re

quire

d in

cer

tain

inst

ance

sTh

ree

year

s

Ow

ners

hip

of a

sset

sC

ontr

ol o

ver t

he m

ajor

ity o

f ass

ets

for t

he th

ree

year

per

iod

Ow

ners

hip

cont

inui

ty a

nd c

ontr

ol fo

r at l

east

th

e m

ost r

ecen

t aud

ited

finan

cial

yea

rN

o re

quire

men

tsN

o re

quire

men

tsN

o re

quire

men

ts

Min

imum

num

ber o

f sh

areh

olde

rsN

o re

quire

men

ts30

040

0 ro

und

lot5 s

hare

hold

ers

450

roun

d lo

t5 sha

reho

lder

s or

2,2

00 to

tal

shar

ehol

ders

or 5

50 to

tal s

hare

hold

ers

and

aver

age

mon

thly

trad

ing

volu

me

over

the

past

12

mon

ths

of a

t lea

st 1

.1m

sha

res

per m

onth

.

500

Min

imum

free

floa

t (o

r pub

lic fl

oat)3

25%

of c

lass

of s

hare

s lis

ted

25%

or a

t lea

st H

K$

50m

– If

mar

kt c

ap. >

HK

$ 10

bn,

can

be

redu

ced

to 1

5%U

S $

40m

for I

PO

s, U

S $

100m

for a

ll ot

her

listin

gs1,

250

thou

sand

sha

res,

US

$45

m m

arke

t val

ue

of p

ublic

ly h

eld

shar

es o

r mar

ket v

alue

of

publ

icly

hel

d sh

ared

and

sto

ckho

lder

s’ e

quity

.

25%

or i

f mar

ket c

ap >

S$3

00 m

n, fr

ee fl

oat

varie

s be

twee

n 12

% to

20%

Inte

rnal

con

trol

s/fin

anci

al re

port

ing

proc

edur

es

Spo

nsor

’s d

ecla

ratio

n on

ade

quac

y of

fina

ncia

l re

port

ing

proc

edur

es, w

ith th

e pr

ivat

e re

port

ing

acco

unta

nt’s

repo

rt.

Spo

nsor

’s d

ecla

ratio

n on

ade

quac

y of

fina

ncia

l re

port

ing

proc

edur

es, s

upor

ted

by p

rivat

e in

tern

al c

ontr

ols

cons

ulta

nt’s

repo

rt.

CEO

/CFO

cer

tifica

tion

of e

ffect

iven

ess

of

inte

rnal

con

trol

s ov

er fi

nanc

ial r

epor

ting,

with

th

e ex

tern

al a

udito

r’s a

ttes

tatio

n re

port

in th

e se

cond

ann

ual fi

ling.

Em

ergi

ng g

row

th

com

pani

es m

ay e

lect

to fo

llow

an

exte

nded

ph

ase

– in

per

iod

of u

p to

five

yea

rs o

n th

e re

quire

men

t of a

n au

dito

r’s a

ttes

tatio

n re

port

on

inte

rnal

con

trol

s.

CEO

/CFO

cer

tifica

tion

of e

ffect

iven

ess

of

inte

rnal

con

trol

s ov

er fi

nanc

ial r

epor

ting,

with

th

e ex

tern

al a

udito

r’s a

ttes

tatio

n re

port

in th

e se

cond

ann

ual fi

ling.

Em

ergi

ng g

row

th

com

pani

es m

ay e

lect

to fo

llow

an

exte

nded

ph

ase

– in

per

iod

of u

p to

five

yea

rs o

n th

e re

quire

men

t of a

n au

dito

r’s a

ttes

tatio

n re

port

on

inte

rnal

con

trol

s.

Dire

ctor

s’ o

pini

on o

n ad

equa

cy o

f int

erna

l co

ntro

ls in

the

pros

pect

us. A

udito

r’s re

port

to

man

agem

ent o

n in

tern

al c

ontr

ols

and

acco

untin

g sy

stem

s re

quire

d as

par

t of l

istin

g ap

plic

atio

n.

Reg

ulat

ory

and

ong

oing

ob

ligat

ion

req

uire

men

tsS

peci

al c

riter

ia fo

r in

tern

atio

nal i

ssue

rs

• N

on-U

K in

corp

orat

ed c

ompa

nies

mus

t ha

ve m

ore

than

50%

free

floa

t for

FTS

E U

K

serie

s in

dex

incl

usio

n.

• M

ust b

e in

corp

orat

ed in

an

‘acc

epta

ble

juris

dict

ion’

ass

esse

d on

a c

ase-

by-c

ase

basi

s.•

Mus

t app

oint

a p

roce

ss a

gent

in H

K to

ac

cept

ser

vice

and

not

ices

.•

Mus

t app

oint

at l

east

one

aut

horis

ed

repr

esen

tativ

e as

the

prin

cipa

l cha

nnel

of

com

mun

icat

ion

betw

een

fore

ign

issu

er a

nd

HK

Ex.

• M

ust k

eep

a re

gist

er o

f hol

ders

in H

K fo

r tr

ansf

ers

to b

e re

gist

ered

loca

lly (n

ot

requ

ired

for l

istin

g of

dep

osito

ry re

ceip

ts).

• M

ust b

e re

gist

ered

as

a no

n-H

K c

ompa

ny

unde

r the

HK

Com

pani

es O

rdin

ance

.

A F

orei

gn P

rivat

e Is

suer

mus

t be:

•

a fo

reig

n (n

on-U

S),

non-

gove

rnm

enta

l is

suer

• 50

% o

f out

stan

ding

vot

ing

secu

ritie

s or

le

ss h

eld

by U

S r

esid

ents

– if

mor

e th

an

50%

, mus

t not

–H

ave

a m

ajor

ity o

f its

dire

ctor

s or

ex

ecut

ive

office

rs w

ho a

re U

S re

side

nts

–H

ave

mor

e th

an 5

0% o

f its

ass

ets

loca

ted

in th

e U

S –

Adm

inis

ter i

ts b

usin

ess

prin

cipa

lly in

the

US

• D

iffer

ent m

inim

um d

istr

ibut

ion

requ

irem

ents

, mar

ket v

alue

requ

irem

ent

and

finan

cial

sta

ndar

ds a

re a

pplie

d (5

,000

ro

und

lot s

hare

hold

ers,

at l

east

2.5

m

publ

icly

hel

d sh

ares

wor

ldw

ide

with

mar

ket

valu

e at

leas

t US

$10

0m. (

only

app

licab

le if

co

mpa

ny li

sts

unde

r spe

cial

inte

rnat

iona

l lis

ting

stan

dard

s, d

omes

tic d

istr

ibut

ion

requ

irem

ents

app

ly to

FP

Is th

at li

st u

nder

th

e do

mes

tic li

stin

g st

anda

rds)

.).•

Mus

t reg

iste

r the

cla

ss o

f sec

uriti

es it

in

tend

s to

list

with

SEC

by

filin

g a

regi

stra

tion

stat

emen

t (Fo

rm 2

0-F)

6 .

A F

orei

gn P

rivat

e Is

suer

mus

t be:

• A

fore

ign

(non

-US

), no

n-go

vern

men

t iss

uer

• 50

% o

f out

stan

ding

vot

ing

secu

ritie

s or

less

he

ld b

y U

S re

side

nts

– if

mor

e th

an 5

0%,

mus

t not

–H

ave

a m

ajor

ity o

f its

dire

ctor

s or

ex

ecut

ive

office

rs w

ho a

re U

S re

side

nts

–H

ave

mor

e th

an 5

0% o

f its

ass

ets

loca

ted

in th

e U

S –

Adm

inis

ter i

ts b

usin

ess

prin

cipa

lly in

the

US

• M

ust r

egis

ter t

he c

lass

of s

ecur

ities

it

inte

nds

to li

st w

ith S

EC b

y fil

ing

a re

gist

ratio

n st

atem

ent (

Form

20-

F).

• A

fore

ign

com

pany

mus

t hav

e at

leas

t tw

o in

depe

nden

t dire

ctor

s w

ho re

side

in

Sin

gapo

re.

• C

onfir

mat

ion

that

an

anno

unce

men

t will

be

mad

e as

soo

n as

ther

e is

any

cha

nge

in th

e la

w o

f its

pla

ce o

f inc

orpo

ratio

n w

hich

may

aff

ect o

r cha

nge

shar

ehol

ders

’ rig

hts

or

oblig

atio

ns o

ver i

ts s

ecur

ities

.•

Wai

ver f

rom

hav

ing

to c

ompl

y w

ith

cont

inui

ng li

stin

g ob

ligat

ions

if li

sted

on

anot

her r

ecog

nise

d fo

reig

n st

ock

exch

ange

.

Fina

ncia

l rep

ortin

g re

quire

men

ts

Hal

f yea

rlyA

nnua

lH

alf y

early

Ann

ual

Qua

rter

ly6

Ann

ual

FPIs

: Sem

i-Ann

ual

Qua

rter

ly6

Ann

ual

Qua

rter

lyA

nnua

l

Reg

ulat

ory

auth

ority

FCA

/UK

LAH

KE

x, S

ecur

ities

and

Fut

ures

Com

mis

sion

(S

FC)

SEC

SEC

SG

X, M

onet

ary

Aut

horit

y of

Sin

gapo

re (M

AS

)

Maj

or tr

ansa

ctio

n pr

e-ap

prov

al b

y th

e sh

areh

olde

rs

App

rova

l is

requ

ired

for s

igni

fican

t (>2

5%)

acqu

isiti

ons

and

disp

osal

s an

d m

ater

ial (

>5%

) re

late

d pa

rty

tran

sact

ions

.

App

rova

l is

requ

ired

for m

ajor

and

ver

y su

bsta

ntia

l (>2

5%) a

cqui

sitio

ns a

nd d

ispo

sals

an

d la

rge

(>5%

) con

nect

ed p

arty

tran

sact

ions

, su

bjec

t to

cert

ain

exem

ptio

ns.

• Is

suan

ces

resu

lting

in a

cha

nge

of c

ontr

ol.

• Eq

uity

com

pens

atio

n pl

ans.

• P

rior t

o th

e is

suan

ce o

f sec

uriti

es in

any

tr

ansa

ctio

n to

a d

irect

or o

f the

com

pany

, su

bsid

iary

, affi

liate

or o

ther

clo

sely

rela

ted

pers

on o

f a R

elat

ed P

arty

, or a

ny c

ompa

ny

or e

ntity

in w

hich

Rel

ated

Par

ty h

as

subs

tant

ial i

nter

est.

• P

rior t

o th

e is

suan

ce o

f sec

uriti

es in

any

tr

ansa

ctio

n if

the

votin

g po

wer

equ

als

to o

r in

exc

ess

of 2

0% o

f the

vot

ing

pow

er

outs

tand

ing

befo

re th

e is

suan

ce (t

here

are

ce

rtai

n co

nditi

ons

whe

n ap

prov

al is

not

re

quire

d fo

r som

e ab

ove-

men

tione

d is

suan

ces)

.•

Not

app

licab

le to

FP

Is

• A

cqui

sitio

ns w

here

the

issu

ance

equ

als

20%

or m

ore

of th

e pr

e-tr

ansa

ctio

n ou

tsta

ndin

g sh

ares

, or 5

% o

r mor

e of

the

pre-

tran

sact

ion

outs

tand

ing

shar

es w

hen

a re

late

d pa

rty

has

a 5%

or g

reat

er in

tere

st in

th

e ac

quis

ition

targ

et.

• Is

suan

ces

resu

lting

in a

cha

nge

of c

ontr

ol

• Eq

uity

com

pens

atio

n.

• P

rivat

e pl

acem

ents

whe

re th

e is

suan

ce

(toge

ther

with

sa

les

by o

ffice

rs, d

irect

ors,

or s

ubst

antia

l sh

areh

olde

rs,

if an

y), e

qual

s 20

% o

r mor

e of

the

pre-

tran

sact

ion

outs

tand

ing

shar

es a

t a

pric

e le

ss th

an th

e gr

eate

r of b

ook

or

mar

ket v

alue

.

• S

hare

hold

er a

ppro

val f

or in

tere

sted

per

son

tran

sact

ions

(>5%

), m

ajor

tran

sact

ions

(>

20%

), a

reve

rse

take

over

and

a d

elis

ting

of it

s se

curit

ies

from

the

SG

X-S

T.

5 | W

hich

mar

ket?

| P

wC

1.

Spon

sor (

or e

quiv

alen

t) is

an

inve

stm

ent b

ank

appo

inte

d to

man

age

the

IPO

pro

cess

, wit

h re

spon

sibi

litie

s to

bot

h th

e re

gula

tor a

nd th

e is

suer

.2.

C

ompa

ny h

isto

ry re

fers

to th

e le

ngth

of t

ime

the

com

pany

has

bee

n in

exi

sten

ce.

3.

Free

floa

t is

the

num

ber o

f out

stan

ding

sha

res

in th

e ha

nds

of p

ublic

inve

stor

s.4.

If

the

com

pany

cho

oses

to in

clud

e a

prof

it fo

reca

st, t

he li

stin

g re

gist

rati

on d

ocum

ent m

ust c

onta

in p

rinc

ipal

ass

umpt

ions

upo

n w

hich

the

com

pany

has

bas

ed it

s fo

reca

st a

nd b

e pu

blic

ly re

port

ed u

pon

by th

e in

depe

nden

t acc

ount

ant.

5.

Rou

nd lo

t is

the

term

use

d fo

r a n

orm

al u

nit o

f tra

ding

, whi

ch is

100

sha

res.

6.

Fore

ign

priv

ate

issu

ers

are

not r

equi

red

to fi

le q

uart

erly

repo

rts.

Not

e: T

he li

stin

g re

quir

emen

ts in

the

tabl

e ab

ove

are

subj

ect t

o ex

empt

ions

and

dif

fere

nt s

tand

ards

app

ly to

issu

ers

in s

peci

alis

t sec

tors

| F

or re

cent

upd

ates

on

the

listi

ng r

ules

ple

ase

refe

r to

the

stoc

k ex

chan

ge w

ebsi

te.

Lond

on M

ain

Mar

ket (

Pre

miu

m

List

ing)

Hon

g K

ong

Mai

n B

oard

New

Yor

k S

tock

Exc

hang

eN

AS

DA

Q (G

loba

l Sel

ect)

Sin

gapo

re M

ain

Boa

rd

Init

ial l

isti

ng c

rite

ria

Spo

nsor

1R

equi

red

Req

uire

dN

ot re

quire

dN

ot re

quire

dR

equi

red

Aud

ited

trac

k re

cord

Thre

e ye

ars

audi

ted

acco

unts

, no

mor

e th

an

six

mon

ths

old

Thre

e ye

ars

audi

ted

acco

unts

, no

mor

e th

an

six

mon

ths

old

Thre

e ye

ars

audi

ted

acco

unts

. For

em

ergi

ng

grow

th c

ompa

nies

(EG

Cs)

und

er th

e JO

BS

A

ct, t

wo

year

s of

aud

ited

finan

cial

sta

tem

ents

ar

e pe

rmitt

ed

Thre

e ye

ars

audi

ted

acco

unts

. For

em

ergi

ng

grow

th c

ompa

nies

(EG

Cs)

und

er th

e JO

BS

Act

, tw

o ye

ars

of a

udite

d fin

anci

al s

tate

men

ts a

re

perm

itted

Thre

e ye

ars

audi

ted

acco

unts

, no

mor

e th

an s

ix

mon

ths

old

Acc

ount

ing

stan

dard

EU IF

RS

or I

FRS

equ

ival

ent f

or n

on-E

U is

suer

sH

K F

RS

, IFR

S, C

AS

BE

(for P

RC

issu

ers

only

) U

S G

AA

P o

r oth

er a

ccou

ntin

g st

anda

rds

may

be

acc

epte

d in

cer

tain

circ

umst

ance

s.

US

GA

AP

or I

FRS

U

S G

AA

P o

r IFR

SS

inga

pore

FR

S, I

FRS

or U

S G

AA

P

Fina

ncia

l crit

eria

At l

east

75%

of t

he e

ntity

’s b

usin

ess

mus

t be

supp

orte

d by

a re

venu

e ea

rnin

g tr

ack

reco

rd

for t

he th

ree

year

per

iod

(som

e di

spen

satio

n fo

r spe

cific

indu

strie

s e.

g. m

inin

g)M

inim

um m

arke

t cap

at a

dmis

sion

– £

700,

000

Com

pany

nee

ds to

mee

t one

of t

he fi

nanc

ial

crite

ria:

i) •

Pro

fit o

f at l

east

HK

$20

m fo

r th

e

mos

t rec

ent fi

nanc

ial y

ear,

•

Pro

fit in

agg

rega

te o

f at l

east

HK

$3

0m fo

r th

e tw

o pr

eced

ing

finan

cial

ye

ars,

and

•

Mar

ket c

ap o

f at l

east

HK

$20

0m a

t

tim

e of

list

ing.

ii) •

Mar

ket c

ap o

f at l

east

HK

$2b

n at

tim

e of

list

ing,

•

Rev

enue

of a

t lea

st H

K $

500m

for

th

e m

ost r

ecen

t fina

ncia

l yea

r, an

d

• Po

sitiv

e op

erat

ing

cash

flow

s of

at

leas

t HK

$10

0m in

agg

rega

te fo

r

the

thre

e pr

eced

ing

finan

cial

yea

rs.

iii)

• M

arke

t cap

of a

t lea

st H

K $

4bn

at ti

me

of

list

ing,

and

• R

even

ue o

f at l

east

HK

$50

0m fo

r

the

mos

t rec

ent fi

nanc

ial y

ear.

Com

pany

nee

ds to

mee

t one

of t

he fi

nanc

ial

crite

ria:

i) E

arni

ngs

Test

Inco

me

befo

re ta

x fr

om c

ontin

uing

op

erat

ions

and

afte

r m

inor

ity in

tere

st,

amor

tisat

ion

and

equi

ty in

the

earn

ings

or

loss

es o

f inv

este

es (s

ubje

ct to

ce

rtai

n ad

just

men

ts) m

ust t

otal

at l

east

•

US

$10

m in

the

aggr

egat

e fo

r th

e la

st

th

ree

fisca

l yea

rs, t

oget

her

with

a

min

imum

of U

S $

2m in

eac

h of

the

tw

o m

ost r

ecen

t fisc

al y

ears

, and

po

sitiv

e am

ount

s in

all

thre

e ye

ars

O

R

• U

S $

12m

in th

e ag

greg

ate

for

the

last

th

ree

fisca

l yea

rs, t

oget

her

with

a

min

imum

of U

S $

5m in

the

mos

t

re

cent

fisc

al y

ear

and

US

$2m

in th

e

next

mos

t rec

ent fi

scal

yea

r.

ii) E

arni

ngs

Test

fo

r E

GC

s In

com

e be

fore

tax

from

con

tinui

ngop

erat

ions

and

afte

r m

inor

ity in

tere

st,

amor

tisat

ion

and

equi

ty in

the

earn

ings

or lo

sses

of i

nves

tees

(sub

ject

to c

erta

in

adju

stm

ents

) mus

t tot

al a

t lea

st:

• U

S $

10m

in th

e ag

greg

ate

for

the

last

two

fisca

l yea

rs, t

oget

her

with

a

min

imum

of U

S $

2m in

bot

h ye

ars.

iii) G

loba

l Mar

ket C

apita

lisat

ion

Test

Issu

er m

ust h

ave

at le

ast:

•

US

$20

0m in

glo

bal m

arke

t cap

.

Com

pany

nee

ds to

mee

t one

of t

he fi

nanc

ial

crite

ria:

i) •

Min

imum

inco

me

from

con

tinui

ng

oper

atio

ns b

efor

e in

com

e ta

xes

of:

– U

S $

11m

ove

r th

e pr

ior

thre

e fis

cal

ye

ars

in a

ggre

gate

, and

– U

S $

2.2m

in e

ach

of th

e tw

o m

ost

re

cent

fisc

al y

ears

, and

•

Posi

tive

inco

me

from

con

tinui

ng

oper

atio

ns b

efor

e in

com

e ta

xes

in

each

of t

he p

rior

thre

e fis

cal y

ears

.

ii) •

Min

imum

tota

l rev

enue

in th

e pr

evio

us

fisca

l yea

r –

US

$11

0m,

•

Min

imum

ave

rage

mar

ket c

ap o

ver

th

e pr

ior

12 m

onth

s –

US

$55

0m,

•

Min

imum

cas

h flo

ws

of U

S $

27.5

m

over

the

prio

r th

ree

fisca

l yea

rs in

ag

greg

ate,

and

•

Posi

tive

cash

flow

s in

eac

h of

the

pr

ior

thre

e fis

cal y

ears

.

iii) •

Min

imum

tota

l rev

enue

in th

e pr

evio

us

fisca

l yea

r –

US

$90

m, a

nd

• M

inim

um a

vera

ge m

arke

t cap

ove

r

the

prio

r 12

mon

ths

– U

S $

850m

.

iv) •

Min

imum

ave

rage

mar

ket c

ap a

t the

tim

e of

list

ing

– U

S $

160m

, and

•

US

$80

m o

f tot

al a

sset

s an

d U

S

$55m

of s

tock

hold

ers’

equ

ity in

the

m

ost r

ecen

t pub

licly

repo

rted

fina

ncia

l

st

atem

ents

.

Com

pany

nee

ds to

mee

t one

of t

he fi

nanc

ial

crite

ria:

i) •

Min

imum

con

solid

ated

pre

-tax

pro

fit

of a

t lea

st S

$30m

for

the

late

st

finan

cial

yea

r,

• O

pera

ting

trac

k re

cord

of a

t lea

st

thre

e ye

ars.

ii) •

Pro

fitab

le in

the

late

st fi

nanc

ial y

ear,

•

Mar

ket c

ap o

f not

less

than

S$1

50m

ba

sed

on th

e is

sue

pric

e an

d po

st-

invi

tatio

n is

sued

sha

re c

apita

l, an

d

• O

pera

ting

trac

k re

cord

of a

t lea

st

thre

e ye

ars.

iii) •

Ope

ratin

g re

venu

e in

the

late

st

co

mpl

eted

fina

ncia

l yea

r, an

d

• M

arke

t cap

of n

ot le

ss th

an S

$300

m

base

d on

the

issu

e pr

ice

and

post

-

in

vita

tion

issu

ed s

hare

cap

ital.

Rea

l

E

stat

e In

vest

men

t Tru

sts

and

Bus

ines

s Tr

usts

who

hav

e m

et th

e

S$3

00m

mar

ket c

ap te

st b

ut d

o no

t

ha

ve h

isto

rical

fina

ncia

l inf

orm

atio

n

may

app

ly u

nder

this

rul

e if

they

ar

e ab

le to

dem

onst

rate

that

they

will

ge

nera

te o

pera

ting

reve

nue

imm

edia

tely

upo

n lis

ting.

Ope

ratin

g

trac

k re

cord

requ

ired

is a

t lea

st o

ne

year

.

Pro

fit fo

reca

stO

ptio

nal4

Opt

iona

l 4

Priv

ate

profi

t for

ecas

t mem

oran

dum

for t

he

rem

aind

er o

f the

fina

ncia

l yea

r req

uire

d to

be

subm

itted

to H

KE

x

for r

evie

w.

No

requ

irem

ents

No

requ

irem

ents

• Fo

r co

mpa

nies

, pro

fit a

nd c

ash

flo

w fo

reca

st m

emor

andu

m fo

r th

e

cu

rren

t yea

r an

d en

suin

g ye

ar

mus

t be

subm

itted

upo

n re

ques

t

by

the

Exc

hang

e.•

For

busi

ness

trus

ts a

nd R

EIT

s, p

rofit

and

cash

flow

fore

cast

and

proj

ectio

ns a

re re

quire

d to

be

incl

uded

in th

e pr

ospe

ctus

.W

orki

ng c

apita

l st

atem

ents

Cov

erin

g 12

mon

ths

Cov

erin

g 12

mon

ths

Not

requ

ired

Not

requ

ired

Cov

erin

g 12

mon

ths

Com

pany

his

tory

2Th

ree

year

s, s

ubje

ct to

exe

mpt

ions

Thre

e ye

ars,

sub

ject

to e

xem

ptio

nsTh

ree

year

s fo

r com

pani

es li

stin

g un

der

Earn

ings

Tes

t and

Glo

bal M

arke

t Cap

italis

atio

n Te

st, t

wo

year

s fo

r com

pani

es li

stin

g un

der

Earn

ings

Tes

t for

EG

Cs

Thre

e ye

ars,

sub

ject

to e

xem

ptio

ns, t

wo

year

s re

quire

d in

cer

tain

inst

ance

sTh

ree

year

s

Ow

ners

hip

of a

sset

sC

ontr

ol o

ver t

he m

ajor

ity o

f ass

ets

for t

he th

ree

year

per

iod

Ow

ners

hip

cont

inui

ty a

nd c

ontr

ol fo

r at l

east

th

e m

ost r

ecen

t aud

ited

finan

cial

yea

rN

o re

quire

men

tsN

o re

quire

men

tsN

o re

quire

men

ts

Min

imum

num

ber o

f sh

areh

olde

rsN

o re

quire

men

ts30

040

0 ro

und

lot5 s

hare

hold

ers

450

roun

d lo

t5 sha

reho

lder

s or

2,2

00 to

tal

shar

ehol

ders

or 5

50 to

tal s

hare

hold

ers

and

aver

age

mon

thly

trad

ing

volu

me

over

the

past

12

mon

ths

of a

t lea

st 1

.1m

sha

res

per m

onth

.

500

Min

imum

free

floa

t (o

r pub

lic fl

oat)3

25%

of c

lass

of s

hare

s lis

ted

25%

or a

t lea

st H

K$

50m

– If

mar

kt c

ap. >

HK

$ 10

bn,

can

be

redu

ced

to 1

5%U

S $

40m

for I

PO

s, U

S $

100m

for a

ll ot

her

listin

gs1,

250

thou

sand

sha

res,

US

$45

m m

arke

t val

ue

of p

ublic

ly h

eld

shar

es o

r mar

ket v

alue

of

publ

icly

hel

d sh

ared

and

sto

ckho

lder

s’ e

quity

.

25%

or i

f mar

ket c

ap >

S$3

00 m

n, fr

ee fl

oat

varie

s be

twee

n 12

% to

20%

Inte

rnal

con

trol

s/fin

anci

al re

port

ing

proc

edur

es

Spo

nsor

’s d

ecla

ratio

n on

ade

quac

y of

fina

ncia

l re

port

ing

proc

edur

es, w

ith th

e pr

ivat

e re

port

ing

acco

unta

nt’s

repo

rt.

Spo

nsor

’s d

ecla

ratio

n on

ade

quac

y of

fina

ncia

l re

port

ing

proc

edur

es, s

upor

ted

by p

rivat

e in

tern

al c

ontr

ols

cons

ulta

nt’s

repo

rt.

CEO

/CFO

cer

tifica

tion

of e

ffect

iven

ess

of

inte

rnal

con

trol

s ov

er fi

nanc

ial r

epor

ting,

with

th

e ex

tern

al a

udito

r’s a

ttes

tatio

n re

port

in th

e se

cond

ann

ual fi

ling.

Em

ergi

ng g

row

th

com

pani

es m

ay e

lect

to fo

llow

an

exte

nded

ph

ase

– in

per

iod

of u

p to

five

yea

rs o

n th

e re

quire

men

t of a

n au

dito

r’s a

ttes

tatio

n re

port

on

inte

rnal

con

trol

s.

CEO

/CFO

cer

tifica

tion

of e

ffect

iven

ess

of

inte

rnal

con

trol

s ov

er fi

nanc

ial r

epor

ting,

with

th

e ex

tern

al a

udito

r’s a

ttes

tatio

n re

port

in th

e se

cond

ann

ual fi

ling.

Em

ergi

ng g

row

th

com

pani

es m

ay e

lect

to fo

llow

an

exte

nded

ph

ase

– in

per

iod

of u

p to

five

yea

rs o

n th

e re

quire

men

t of a

n au

dito

r’s a

ttes

tatio

n re

port

on

inte

rnal

con

trol

s.

Dire

ctor

s’ o

pini

on o

n ad

equa

cy o

f int

erna

l co

ntro

ls in

the

pros

pect

us. A

udito

r’s re

port

to

man

agem

ent o

n in

tern

al c

ontr

ols

and

acco

untin

g sy

stem

s re

quire

d as

par

t of l

istin

g ap

plic

atio

n.

Reg

ulat

ory

and

ong

oing

ob

ligat

ion

req

uire

men

tsS

peci

al c

riter

ia fo

r in

tern

atio

nal i

ssue

rs

• N

on-U

K in

corp

orat

ed c

ompa

nies

mus

t ha

ve m

ore

than

50%

free

floa

t for

FTS

E U

K

serie

s in

dex

incl

usio

n.

• M

ust b

e in

corp

orat

ed in

an

‘acc

epta

ble

juris

dict

ion’

ass

esse

d on

a c

ase-

by-c

ase

basi

s.•

Mus

t app

oint

a p

roce

ss a

gent

in H

K to

ac

cept

ser

vice

and

not

ices

.•

Mus

t app

oint

at l

east

one

aut

horis

ed

repr

esen

tativ

e as

the

prin

cipa

l cha

nnel

of

com

mun

icat

ion

betw

een

fore

ign

issu

er a

nd

HK

Ex.

• M

ust k

eep

a re

gist

er o

f hol

ders

in H

K fo

r tr

ansf

ers

to b

e re

gist

ered

loca

lly (n

ot

requ

ired

for l

istin

g of

dep

osito

ry re

ceip

ts).

• M

ust b

e re

gist

ered

as

a no

n-H

K c

ompa

ny

unde

r the

HK

Com

pani

es O

rdin

ance

.

A F

orei

gn P

rivat

e Is

suer

mus

t be:

•

a fo

reig

n (n

on-U

S),

non-

gove

rnm

enta

l is

suer

• 50

% o

f out

stan

ding

vot

ing

secu

ritie

s or

le

ss h

eld

by U

S r

esid

ents

– if

mor

e th

an

50%

, mus

t not

–H

ave

a m

ajor

ity o

f its

dire

ctor

s or

ex

ecut

ive

office

rs w

ho a

re U

S re

side

nts

–H

ave

mor

e th

an 5

0% o

f its

ass

ets

loca

ted

in th

e U

S –

Adm

inis

ter i

ts b

usin

ess

prin

cipa

lly in

the

US

• D

iffer

ent m

inim

um d

istr

ibut

ion

requ

irem

ents

, mar

ket v

alue

requ

irem

ent

and

finan

cial

sta

ndar

ds a

re a

pplie

d (5

,000

ro

und

lot s

hare

hold

ers,

at l

east

2.5

m

publ

icly

hel

d sh

ares

wor

ldw

ide

with

mar

ket

valu

e at

leas

t US

$10

0m. (

only

app

licab

le if

co

mpa

ny li

sts

unde

r spe

cial

inte

rnat

iona

l lis

ting

stan

dard

s, d

omes

tic d

istr

ibut

ion

requ

irem

ents

app

ly to

FP

Is th

at li

st u

nder

th

e do

mes

tic li

stin

g st

anda

rds)

.).•

Mus

t reg

iste

r the

cla

ss o

f sec

uriti

es it

in

tend

s to

list

with

SEC

by

filin

g a

regi

stra

tion

stat

emen

t (Fo

rm 2

0-F)

6 .

A F

orei

gn P

rivat

e Is

suer

mus

t be:

• A

fore

ign

(non

-US

), no

n-go

vern

men

t iss

uer

• 50

% o

f out

stan

ding

vot

ing

secu

ritie

s or

less

he

ld b

y U

S re

side

nts

– if

mor

e th

an 5

0%,

mus

t not

–H

ave

a m

ajor

ity o

f its

dire

ctor

s or

ex

ecut

ive

office

rs w

ho a

re U

S re

side

nts

–H

ave

mor

e th

an 5

0% o

f its

ass

ets

loca

ted

in th

e U

S –

Adm

inis

ter i

ts b

usin

ess

prin

cipa

lly in

the

US

• M

ust r

egis

ter t

he c

lass

of s

ecur

ities

it

inte

nds

to li

st w

ith S

EC b

y fil

ing

a re

gist

ratio

n st

atem

ent (

Form

20-

F).

• A

fore

ign

com

pany

mus

t hav

e at

leas

t tw

o in

depe

nden

t dire

ctor

s w

ho re

side

in

Sin

gapo

re.

• C

onfir

mat

ion

that

an

anno

unce

men

t will

be

mad

e as

soo

n as

ther

e is

any

cha

nge

in th

e la

w o

f its

pla

ce o

f inc

orpo

ratio

n w

hich

may

aff

ect o

r cha

nge

shar

ehol

ders

’ rig

hts

or

oblig

atio

ns o

ver i

ts s

ecur

ities

.•

Wai

ver f

rom

hav

ing

to c

ompl

y w

ith

cont

inui

ng li

stin

g ob

ligat

ions

if li

sted

on

anot

her r

ecog

nise

d fo

reig

n st

ock

exch

ange

.

Fina

ncia

l rep

ortin

g re

quire

men

ts

Hal

f yea

rlyA

nnua

lH

alf y

early

Ann

ual

Qua

rter

ly6

Ann

ual

FPIs

: Sem

i-Ann

ual

Qua

rter

ly6

Ann

ual

Qua

rter

lyA

nnua

l

Reg

ulat

ory

auth

ority

FCA

/UK

LAH

KE

x, S

ecur

ities

and

Fut

ures

Com

mis

sion

(S

FC)

SEC

SEC

SG

X, M

onet

ary

Aut

horit

y of

Sin

gapo

re (M

AS

)

Maj

or tr

ansa

ctio

n pr

e-ap

prov

al b

y th

e sh

areh

olde

rs

App

rova

l is

requ

ired

for s

igni

fican

t (>2

5%)

acqu

isiti

ons

and

disp

osal

s an

d m

ater

ial (

>5%

) re

late

d pa

rty

tran

sact

ions

.

App

rova

l is

requ

ired

for m

ajor

and

ver

y su

bsta

ntia

l (>2

5%) a

cqui

sitio

ns a

nd d

ispo

sals

an

d la

rge

(>5%

) con

nect

ed p

arty

tran

sact

ions

, su

bjec

t to

cert

ain

exem

ptio

ns.

• Is

suan

ces

resu

lting

in a

cha

nge

of c

ontr

ol.

• Eq

uity

com

pens

atio

n pl

ans.

• P

rior t

o th

e is

suan

ce o

f sec

uriti

es in

any

tr

ansa

ctio

n to

a d

irect

or o

f the

com

pany

, su

bsid

iary

, affi

liate

or o

ther

clo

sely

rela

ted

pers

on o

f a R

elat

ed P

arty

, or a

ny c

ompa

ny

or e

ntity

in w

hich

Rel

ated

Par

ty h

as

subs

tant

ial i

nter

est.

• P

rior t

o th

e is

suan

ce o

f sec

uriti

es in

any

tr

ansa

ctio

n if

the

votin

g po

wer

equ

als

to o

r in

exc

ess

of 2

0% o

f the

vot

ing

pow

er

outs

tand

ing

befo

re th

e is

suan

ce (t

here

are

ce

rtai

n co

nditi

ons

whe

n ap

prov

al is

not

re

quire

d fo

r som

e ab

ove-

men

tione

d is

suan

ces)

.•

Not

app

licab

le to

FP

Is

• A

cqui

sitio

ns w

here

the

issu

ance

equ

als

20%

or m

ore

of th

e pr

e-tr

ansa

ctio

n ou

tsta

ndin

g sh

ares

, or 5

% o

r mor

e of

the

pre-

tran

sact

ion

outs

tand

ing

shar

es w

hen

a re

late

d pa

rty

has

a 5%

or g

reat

er in

tere

st in

th

e ac

quis

ition

targ

et.

• Is

suan

ces

resu

lting

in a

cha

nge

of c

ontr

ol

• Eq

uity

com

pens

atio

n.

• P

rivat

e pl

acem

ents

whe

re th

e is

suan

ce

(toge

ther

with

sa

les

by o

ffice

rs, d

irect

ors,

or s

ubst

antia

l sh

areh

olde

rs,

if an

y), e

qual

s 20

% o

r mor

e of

the

pre-

tran

sact

ion

outs

tand

ing

shar

es a

t a

pric

e le

ss th

an th

e gr

eate

r of b

ook

or

mar

ket v

alue

.

• S

hare

hold

er a

ppro

val f

or in

tere

sted

per

son

tran

sact

ions

(>5%

), m

ajor

tran

sact

ions

(>

20%

), a

reve

rse

take

over

and

a d

elis

ting

of it

s se

curit

ies

from

the

SG

X-S

T.

About PwC

Contact us

We have experience of a wide range of IPOs, international and domestic – we can help you evaluate the pros and cons upfront. Our philosophy is simply – we demystify the process, take you through it and prepare you for life as a public company.

For more information about listing on any global exchange contact our IPO Centre:

Whether a company is an emerging business seeking venture capital, or an established company seeking to expand through an IPO, PwC can provide a full range of audit, reporting accountant, advisory and support services. PwC brings experience in a broad range of functional areas to help management anticipate business risks and develop programs for managing such risks early in the IPO planning process. Our experienced teams work with clients to provide guidance through the complex life cycle of a capital market transaction, from helping to determine the right entry strategy and assessing IPO-readiness, to assisting with the public registration process, to preparing for the ongoing obligations as a public company.

PwC’s global presence, extensive knowledge of capital markets, and network of financing relationships provide the expertise and insight needed at every stage.

• We provide experienced and integrated insight into multiple elements of the transaction process

• We advise on the technical accounting and financial reporting complexities associated with the Going Public process

• We undertake due diligence on behalf of sponsors, investment banks and boards of directors

• We evaluate and advise on company controls and processes

• We advise on the breadth of the change organisations experience as they prepare to migrate into a public company across multiple functional areas