Wealth management onboarding webinar jan262011

39

Wealth Management On-boarding: How to be More Responsive in the First 90 Days A Bank Systems & Technology Webcast Sponsored by

-

Upload

vinay-mummigatti -

Category

Technology

-

view

443 -

download

1

Transcript of Wealth management onboarding webinar jan262011

Wealth Management On-boarding:

How to be More Responsive

in the First 90 DaysA Bank Systems & Technology Webcast

Sponsored by

Webcast Logistics

Featured Speakers

Doug Dannemiller

Senior Analyst

Aite Group

Luis Sierra

Industry Vice President, Banking

Progress Software

Vinaykumar S Mummigatti

VP and Global Head of BPM Practice

Virtusa

Ranks of the Wealthy Are Growing

• The number of millionaires in the world grew 17% in 2009, to 10 million

• The number of ultra-high-net-worth people (with more than $30 million to invest) also grew, by 22% in 2009

• In North America, there were around 36,300 ultra-high-net-worth people at the end of 2009, up from 30,600 in 2008, yet down from 41,200 in 2007YOUR

PHOTO HERE

What Wealthy People Want

30% of wealthy investors don’t have a financial adviser:

•49% percent say the fees charged by financial advisers are too high

•40% percent say they can get better results on their own; 37% percent say they don’t think financial advisers have their clients’ best interests at heart

Talk to me, Harry Winston!

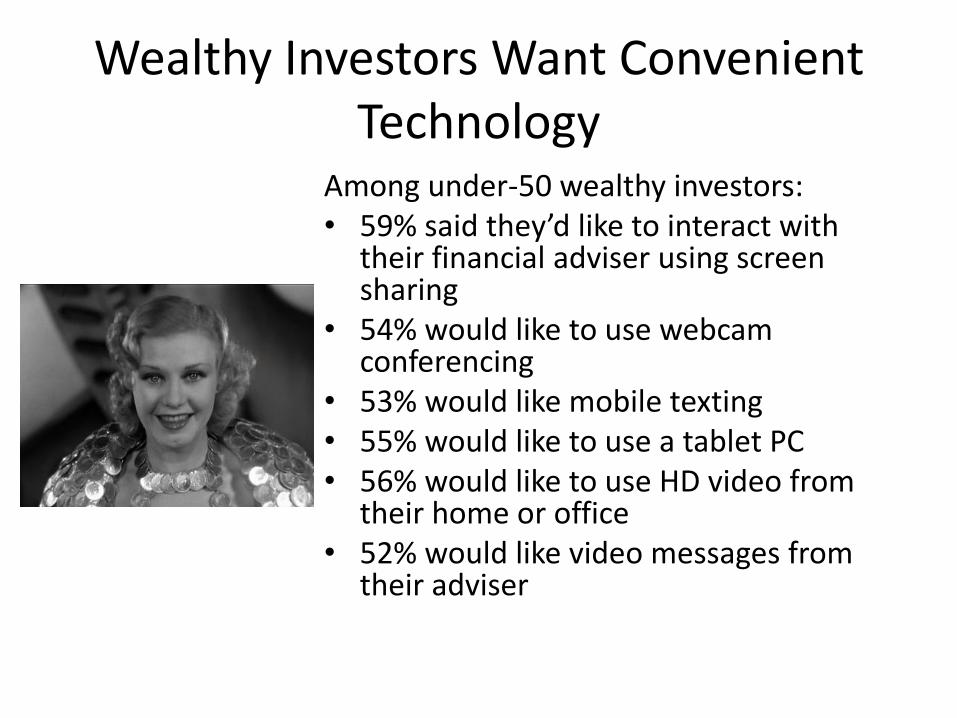

Wealthy Investors Want Convenient Technology

Among under-50 wealthy investors:• 59% said they’d like to interact with

their financial adviser using screen sharing

• 54% would like to use webcam conferencing

• 53% would like mobile texting• 55% would like to use a tablet PC• 56% would like to use HD video from

their home or office• 52% would like video messages from

their adviser

© 2010 Aite Group, LLC www.aitegroup.com Page 7

Actionable, strategic advice on IT, business, and regulatory issues in the financial services industry

Evolution of New Customer Processes in Wealth Management

WebinarJanuary, 2011

Doug Dannemiller

© 2010 Aite Group, LLC www.aitegroup.com

Wealth Management

There is a competitive battle under way for assets and advisers.

Assets are moving at double their historical pace.

Firms with efficient processes, backed by technology are winning the battle.

Page 8

© 2010 Aite Group, LLC www.aitegroup.com 9

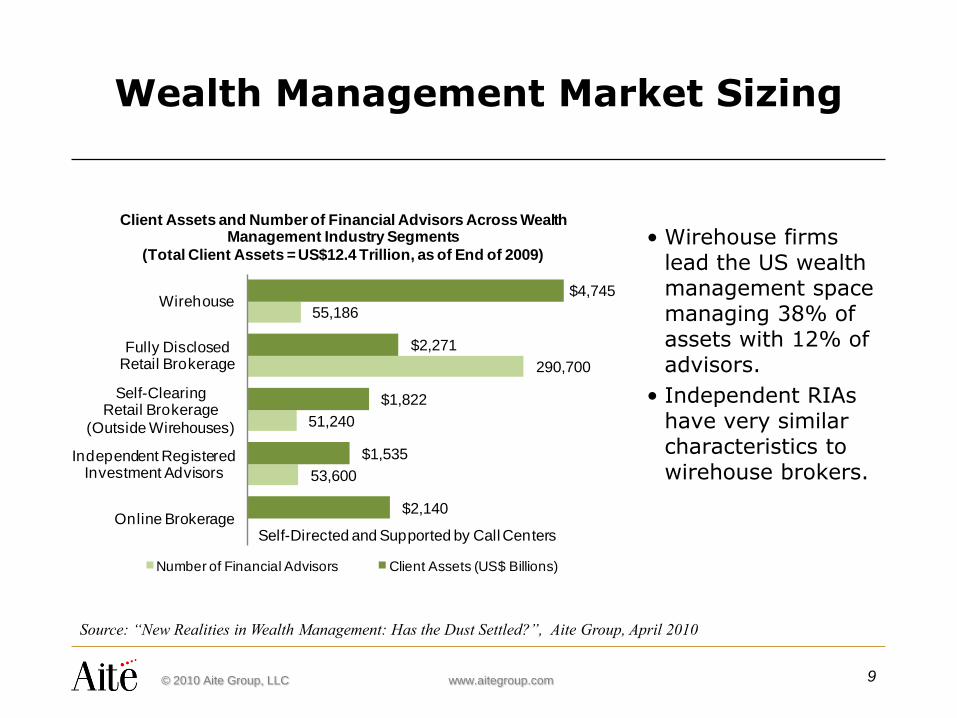

Wealth Management Market Sizing

• Wirehouse firms lead the US wealth management space managing 38% of assets with 12% of advisors.

• Independent RIAs have very similar characteristics to wirehouse brokers.

Source: “New Realities in Wealth Management: Has the Dust Settled?”, Aite Group, April 2010

53,600

51,240

290,700

55,186

$2,140

$1,535

$1,822

$2,271

$4,745

Online Brokerage

Independent Registered Investment Advisors

Self-Clearing Retail Brokerage

(Outside Wirehouses)

Fully Disclosed Retail Brokerage

Wirehouse

Client Assets and Number of Financial Advisors Across Wealth Management Industry Segments

(Total Client Assets = US$12.4 Trillion, as of End of 2009)

Number of Financial Advisors Client Assets (US$ Billions)

Self-Directed and Supported by Call Centers

© 2010 Aite Group, LLC www.aitegroup.com 10

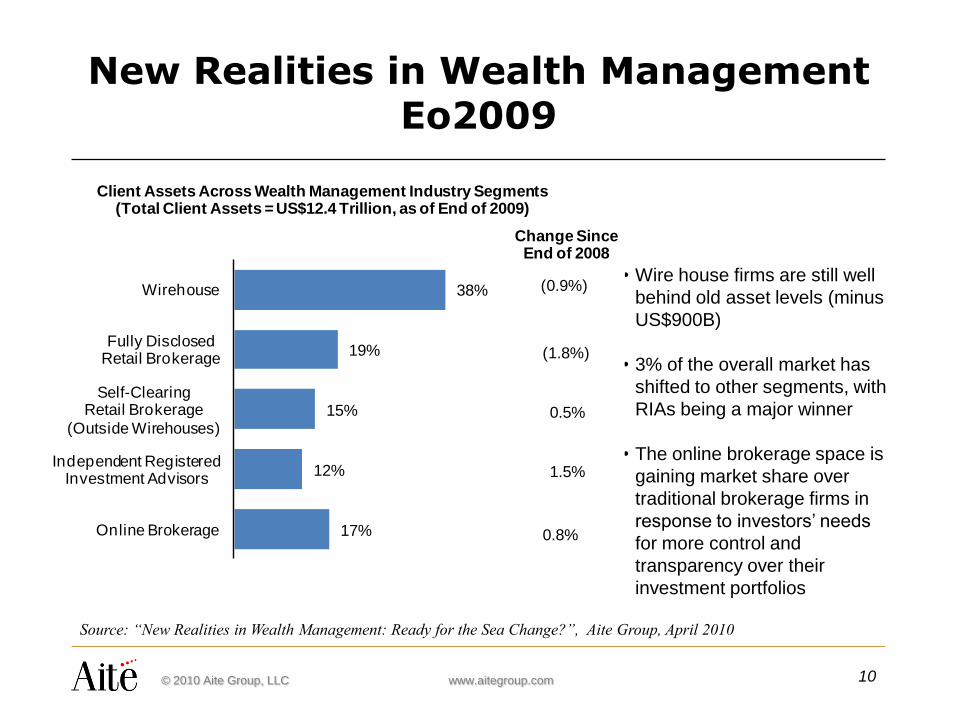

New Realities in Wealth Management Eo2009

• Wire house firms are still well

behind old asset levels (minus

US$900B)

• 3% of the overall market has

shifted to other segments, with

RIAs being a major winner

• The online brokerage space is

gaining market share over

traditional brokerage firms in

response to investors’ needs

for more control and

transparency over their

investment portfolios

Source: “New Realities in Wealth Management: Ready for the Sea Change?”, Aite Group, April 2010

38%

19%

15%

12%

17%

Wirehouse

Fully Disclosed Retail Brokerage

Self-Clearing Retail Brokerage

(Outside Wirehouses)

Independent Registered Investment Advisors

Online Brokerage

Client Assets Across Wealth Management Industry Segments(Total Client Assets = US$12.4 Trillion, as of End of 2009)

Change Since End of 2008

(0.9%)

(1.8%)

0.5%

1.5%

0.8%

© 2010 Aite Group, LLC www.aitegroup.com 11

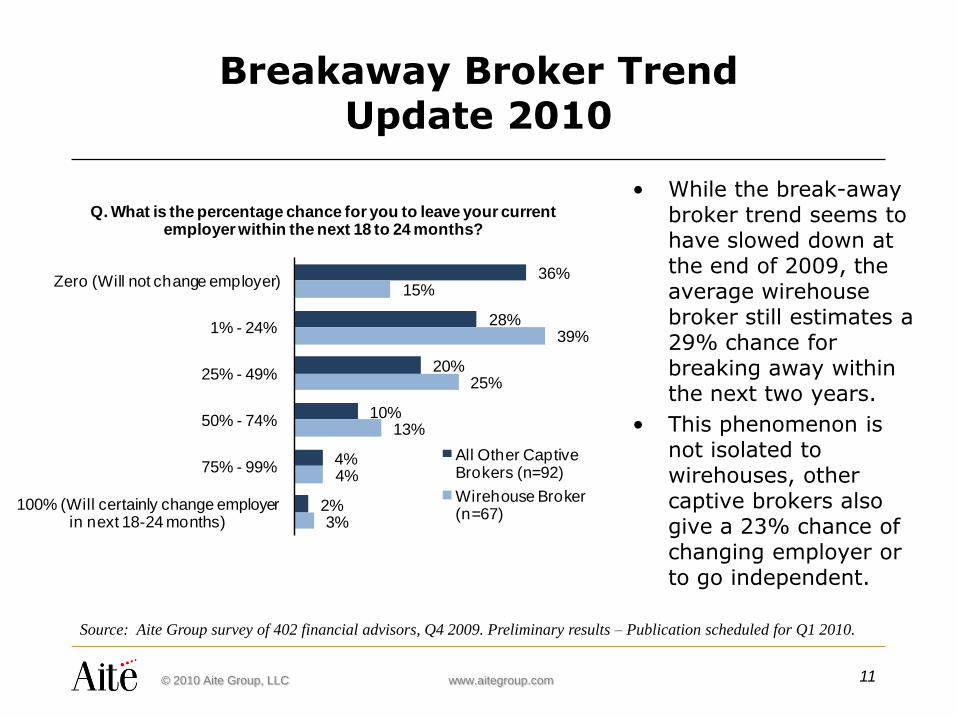

Breakaway Broker Trend Update 2010

• While the break-away broker trend seems to have slowed down at the end of 2009, the average wirehouse broker still estimates a 29% chance for breaking away within the next two years.

• This phenomenon is not isolated to wirehouses, other captive brokers also give a 23% chance of changing employer or to go independent.

36%

28%

20%

10%

4%

2%

15%

39%

25%

13%

4%

3%

Zero (Will not change employer)

1% - 24%

25% - 49%

50% - 74%

75% - 99%

100% (Will certainly change employer in next 18-24 months)

Q. What is the percentage chance for you to leave your current employer within the next 18 to 24 months?

All Other Captive Brokers (n=92)

Wirehouse Broker (n=67)

Source: Aite Group survey of 402 financial advisors, Q4 2009. Preliminary results – Publication scheduled for Q1 2010.

© 2010 Aite Group, LLC www.aitegroup.com 12

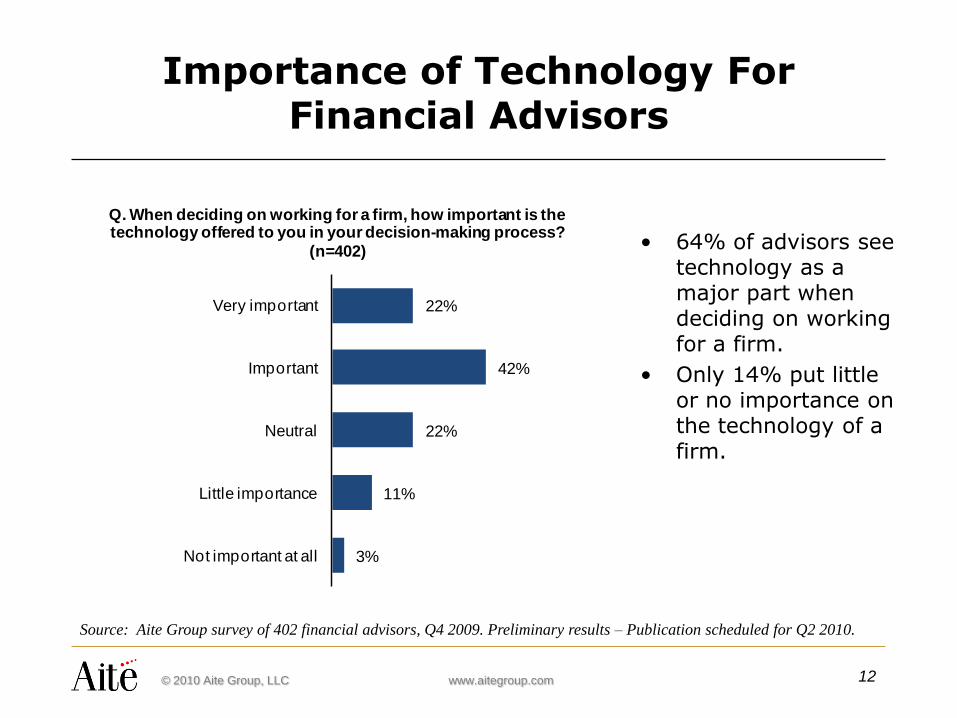

Importance of Technology For Financial Advisors

3%

11%

22%

42%

22%

Not important at all

Little importance

Neutral

Important

Very important

Q. When deciding on working for a firm, how important is the technology offered to you in your decision-making process?

(n=402) • 64% of advisors see technology as a major part when deciding on working for a firm.

• Only 14% put little or no importance on the technology of a firm.

Source: Aite Group survey of 402 financial advisors, Q4 2009. Preliminary results – Publication scheduled for Q2 2010.

© 2010 Aite Group, LLC www.aitegroup.com 13

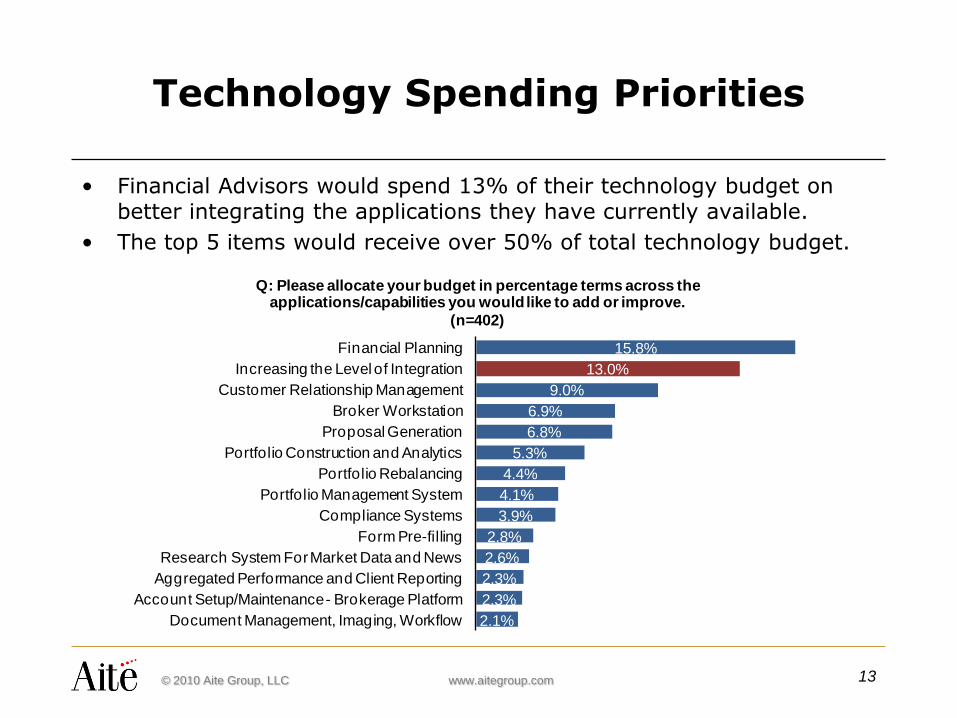

Technology Spending Priorities

• Financial Advisors would spend 13% of their technology budget on better integrating the applications they have currently available.

• The top 5 items would receive over 50% of total technology budget.

15.8%

13.0%

9.0%

6.9%

6.8%

5.3%

4.4%

4.1%

3.9%

2.8%

2.6%

2.3%

2.3%

2.1%

Financial Planning

Increasing the Level of Integration

Customer Relationship Management

Broker Workstation

Proposal Generation

Portfolio Construction and Analytics

Portfolio Rebalancing

Portfolio Management System

Compliance Systems

Form Pre-filling

Research System For Market Data and News

Aggregated Performance and Client Reporting

Account Setup/Maintenance - Brokerage Platform

Document Management, Imaging, Workflow

Q: Please allocate your budget in percentage terms across the applications/capabilities you would like to add or improve.

(n=402)

© 2010 Aite Group, LLC www.aitegroup.com

Account Opening - Key Process

New account processing is a critical and transparent tool for demonstrating to advisers

and customers that a firm’s technology infrastructure is up to date.

Consequently, it is an area under rapid development at many firms.

Page 14

© 2010 Aite Group, LLC www.aitegroup.com

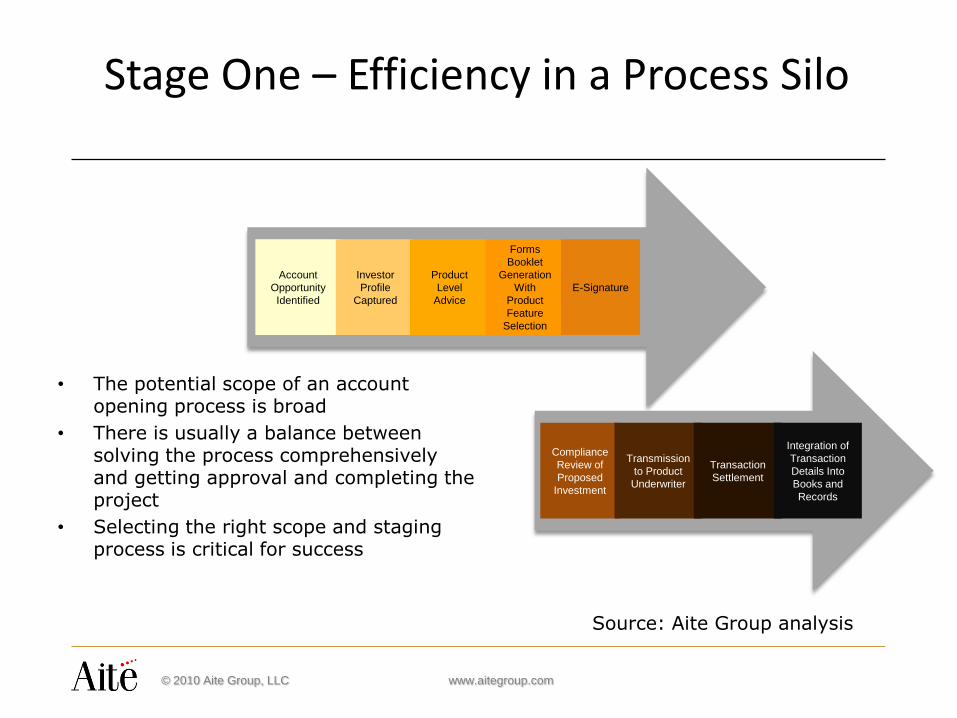

Stage One – Efficiency in a Process Silo

Source: Aite Group analysis

Account

Opportunity

Identified

Investor

Profile

Captured

Product

Level

Advice

Forms

Booklet

Generation

With

Product

Feature

Selection

E-Signature

Compliance

Review of

Proposed

Investment

Transmission

to Product

Underwriter

Transaction

Settlement

Integration of

Transaction

Details Into

Books and

Records

• The potential scope of an account opening process is broad

• There is usually a balance between solving the process comprehensively and getting approval and completing the project

• Selecting the right scope and staging process is critical for success

© 2010 Aite Group, LLC www.aitegroup.comPage 16

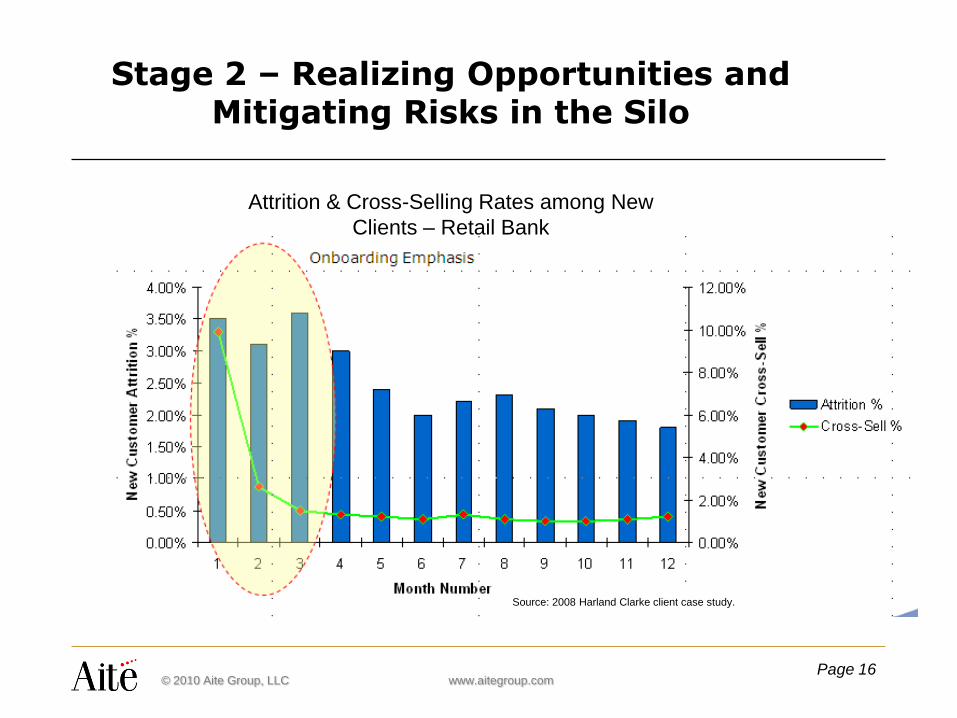

Stage 2 – Realizing Opportunities and Mitigating Risks in the Silo

Attrition & Cross-Selling Rates among New

Clients – Retail Bank

Source: 2008 Harland Clarke client case study.

© 2010 Aite Group, LLC www.aitegroup.com

Stage 2 - Execution: Many Firms Have Rolled-out Detailed Processes

Page 17

Stage 2 is business unit centric – cross-selling is narrowly defined as another product offered by the initiating business unit

© 2010 Aite Group, LLC www.aitegroup.com

The Next Stage

Stage 3 is an environment where the Stage 2 processes are in place – from account opening through customer on-boarding

And…

The information created or gathered in the process is captured, stored, and utilized throughout the organization

Page 18

© 2010 Aite Group, LLC www.aitegroup.com

Enabling Stage 3

Stage 3 is about creating an optimal enterprise customer relationship.

Viewing customer interactions and data as events in a complex system can enable stage 3.

In plain terms, this approach means systematically saving data that may be temporal in nature, and not necessarily viewed as “of further value” to personnel operating in a process silo.

In order to fully enable Stage 3, patterns as well as data elements need to be recognized for example:

– Multiple addresses for a single client (pattern)

– Large cash flow – passed AML screening (data)

– Very strong credit score (data)

– Direct deposit level has changed significantly (pattern)

– Source of direct deposit change (pattern)

– Beneficiaries reach age thresholds (18, 21)

Page 19

© 2010 Aite Group, LLC www.aitegroup.com

Benefits of Stage 3

Operators within a silo focus on the result they are seeking – in this case a successfully opened account.

• Landing beneficiary accounts

• Finding neighborhoods (other segments) to target market – based on successful customer relationships

• Enterprise cross-selling

• Enterprise risk mitigation

• Resource allocation at process, business unit, and enterprise level through tracking of KPI at individual, unit, and region levels.

Stage 3 allows for enterprise opportunities to be realized - across business unit, and even cross-customer.

Page 20

© 2011 Progress Software Corporation. All rights reserved.21

Poll Question

Of what stage of automation are your onboarding

processes?

• Stage 1 – Some processes automated

• Stage 2 – Most onboarding processes are automated

• Stage 3 - Intelligent onboarding operations

Wealth Management

On-boarding Transformation

Luis Sierra

Industry Vice President

Progress Software

Vinaykumar Mummigatti

VP and Global Head of BPM Practice

Virtusa

January 26, 2011

© 2011 Progress Software Corporation. All rights reserved.23

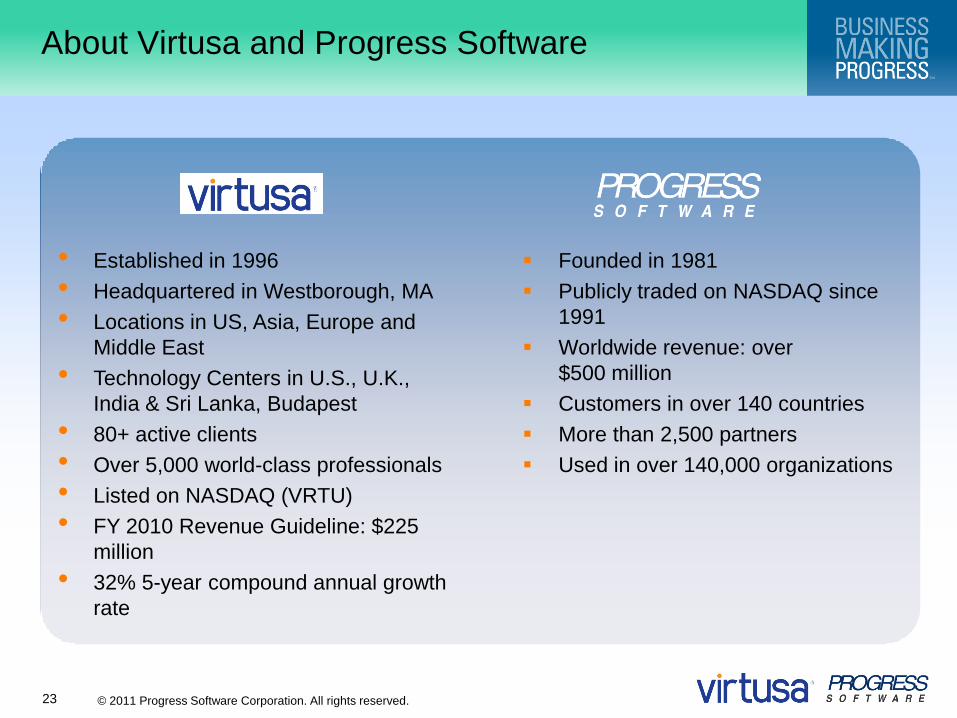

About Virtusa and Progress Software

• Established in 1996

• Headquartered in Westborough, MA

• Locations in US, Asia, Europe and

Middle East

• Technology Centers in U.S., U.K.,

India & Sri Lanka, Budapest

• 80+ active clients

• Over 5,000 world-class professionals

• Listed on NASDAQ (VRTU)

• FY 2010 Revenue Guideline: $225

million

• 32% 5-year compound annual growth

rate

Founded in 1981

Publicly traded on NASDAQ since

1991

Worldwide revenue: over

$500 million

Customers in over 140 countries

More than 2,500 partners

Used in over 140,000 organizations

© 2011 Progress Software Corporation. All rights reserved.24

Account-related

data is captured

through interview

and regulatory

forms

Information

captured on the

application is

verified

The account goes

through the

organizational

workflow for setup

and approval,

having multiple

institutional and

regulatory rules

applied

Customer can

now fund the

account to

begin the

transactions

The account is

operational

Client application

process begins

Capture

Customer Data

Identify

Verification

Account Setup

& Approval

Account

Funding

Application /

InitiationFulfillment

Core Phases of the On-boarding Process

MailDirect: Broker /

Branch / Advisor Mobile Call Center Online

© 2011 Progress Software Corporation. All rights reserved.25

Business Challenges for Wealth ManagementClient On-boarding

On-boarding The process of taking a customer from “application” to “active,”

i.e., providing a customer (retail or corporate) with access to the

product and services of a firm

Requirements vary greatly by type of financial services product

within a firm

Complex decision-making around the application process, or

Complexity around gaining access to the firm’s systems

For Financial Services firms, products typically are offered either

direct to a client (i.e. web channel) or require an intermediary

(i.e. financial advisor)

© 2011 Progress Software Corporation. All rights reserved.26

Business Challenges for Wealth ManagementClient On-boarding (cont.)

On-boarding For more complex retail products and for majority of corporate

products, there are multi step processes and approvals

frequently before you can finalize onboarding:

These typically can be very manually intensive and paper based

and lack automation and workflow control

Duplication of effort and systems across multiple product lines and

multiple channels due to lack of an enterprise-wide account

opening platform/workflow

Errors and delays in the process have high negative customer

impact

Time delays can also frustrate the Bank’s financial advisors as well

as lead to loss of fees for the bank

© 2011 Progress Software Corporation. All rights reserved.27

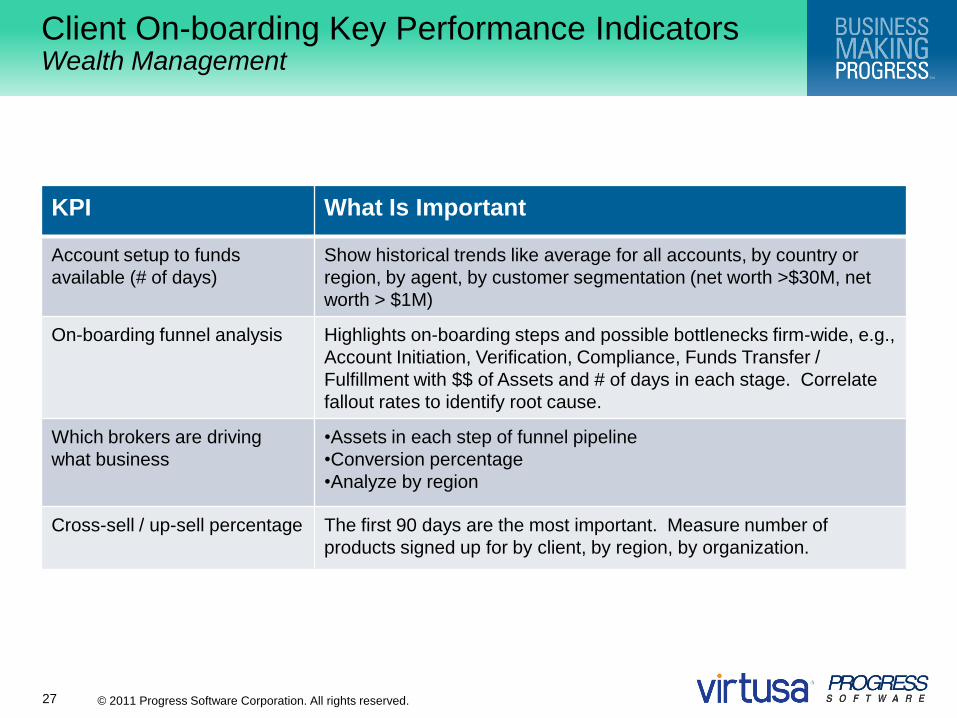

Client On-boarding Key Performance IndicatorsWealth Management

KPI What Is Important

Account setup to funds

available (# of days)

Show historical trends like average for all accounts, by country or

region, by agent, by customer segmentation (net worth >$30M, net

worth > $1M)

On-boarding funnel analysis Highlights on-boarding steps and possible bottlenecks firm-wide, e.g.,

Account Initiation, Verification, Compliance, Funds Transfer /

Fulfillment with $$ of Assets and # of days in each stage. Correlate

fallout rates to identify root cause.

Which brokers are driving

what business

•Assets in each step of funnel pipeline

•Conversion percentage

•Analyze by region

Cross-sell / up-sell percentage The first 90 days are the most important. Measure number of

products signed up for by client, by region, by organization.

© 2011 Progress Software Corporation. All rights reserved.28

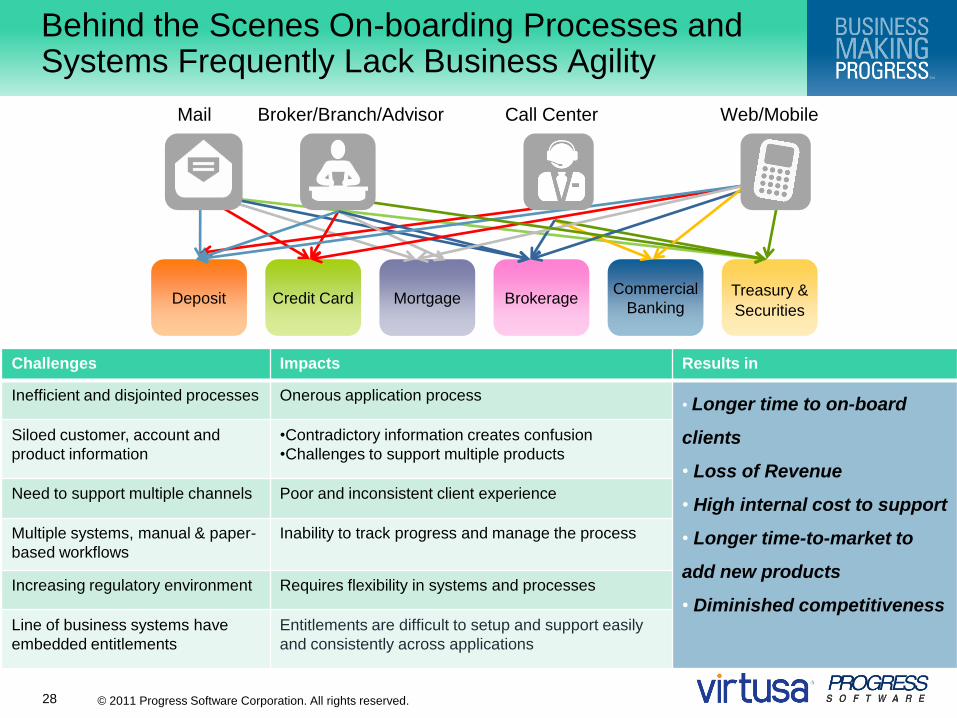

Mail Broker/Branch/Advisor Call Center Web/Mobile

Deposit Credit Card Mortgage BrokerageCommercial

BankingTreasury &

Securities

Behind the Scenes On-boarding Processes and Systems Frequently Lack Business Agility

Challenges Impacts Results in

Inefficient and disjointed processes Onerous application process• Longer time to on-board

clients

• Loss of Revenue

• High internal cost to support

• Longer time-to-market to

add new products

• Diminished competitiveness

Siloed customer, account and

product information

•Contradictory information creates confusion

•Challenges to support multiple products

Need to support multiple channels Poor and inconsistent client experience

Multiple systems, manual & paper-

based workflows

Inability to track progress and manage the process

Increasing regulatory environment Requires flexibility in systems and processes

Line of business systems have

embedded entitlements

Entitlements are difficult to setup and support easily

and consistently across applications

© 2011 Progress Software Corporation. All rights reserved.29

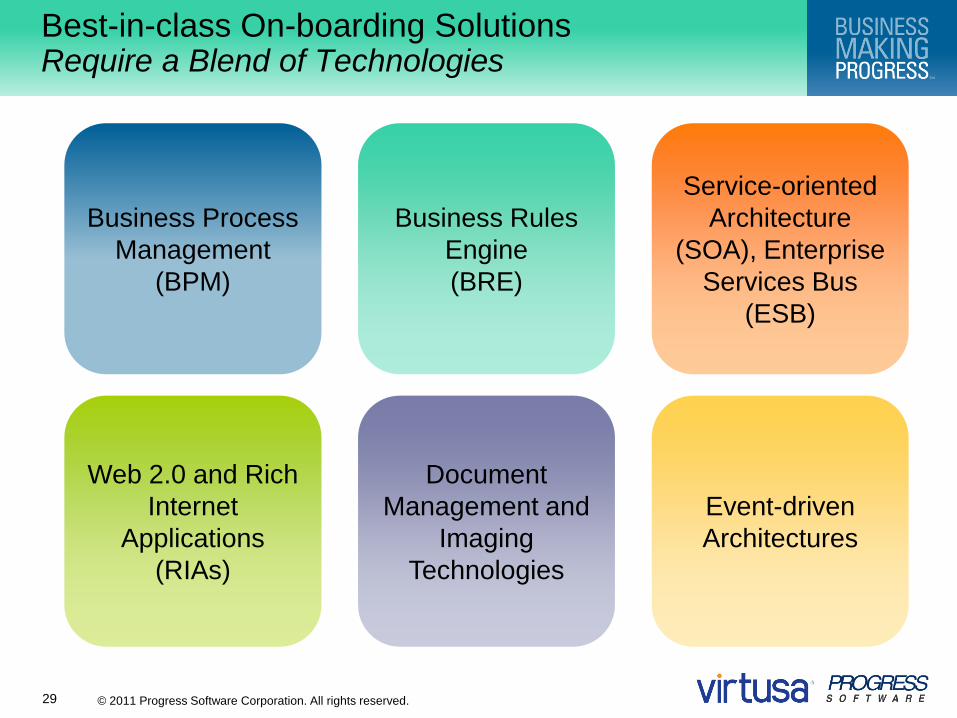

Business Process

Management

(BPM)

Business Rules

Engine

(BRE)

Service-oriented

Architecture

(SOA), Enterprise

Services Bus

(ESB)

Web 2.0 and Rich

Internet

Applications

(RIAs)

Document

Management and

Imaging

Technologies

Event-driven

Architectures

Best-in-class On-boarding Solutions Require a Blend of Technologies

© 2011 Progress Software Corporation. All rights reserved.30

Delivering Operational Responsiveness

Continuous

Business Process

Improvement

Immediate Sense-

and-Respond

Real-time

Business Visibility

Further automate to capture

opportunities (cross-sell)

and minimize threats (non-

compliance, attrition)

Correlate events: e.g.,

compliance, regional

operations

Have real-time visibility of all

wealth management on-

boarding operations

© 2011 Progress Software Corporation. All rights reserved.31

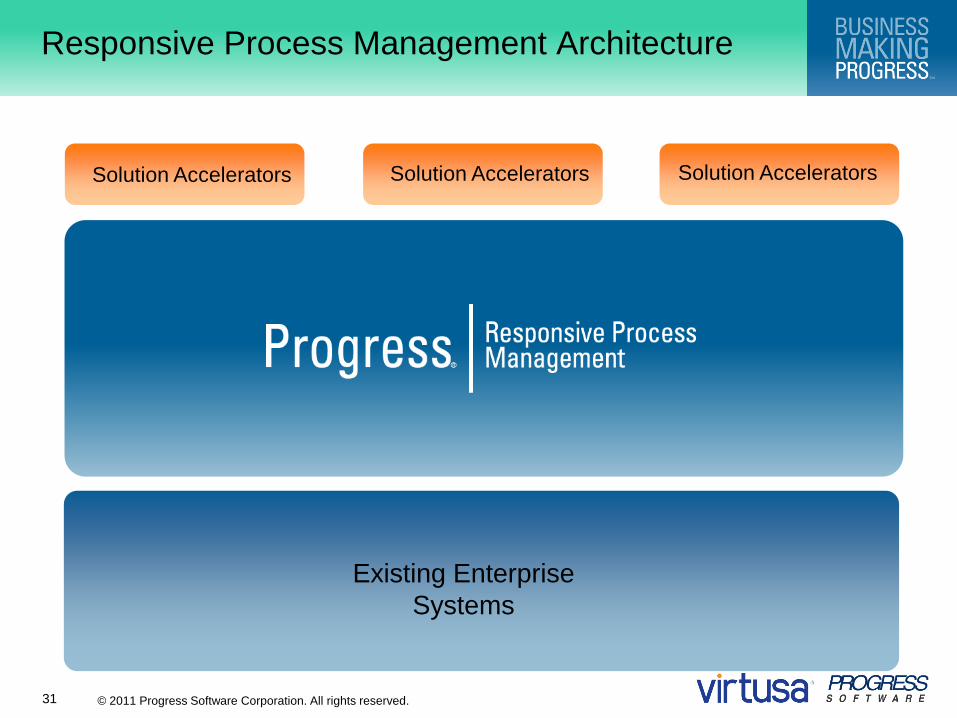

Responsive Process Management Architecture

Solution Accelerators Solution Accelerators Solution Accelerators

Existing Enterprise

Systems

© 2011 Progress Software Corporation. All rights reserved.32

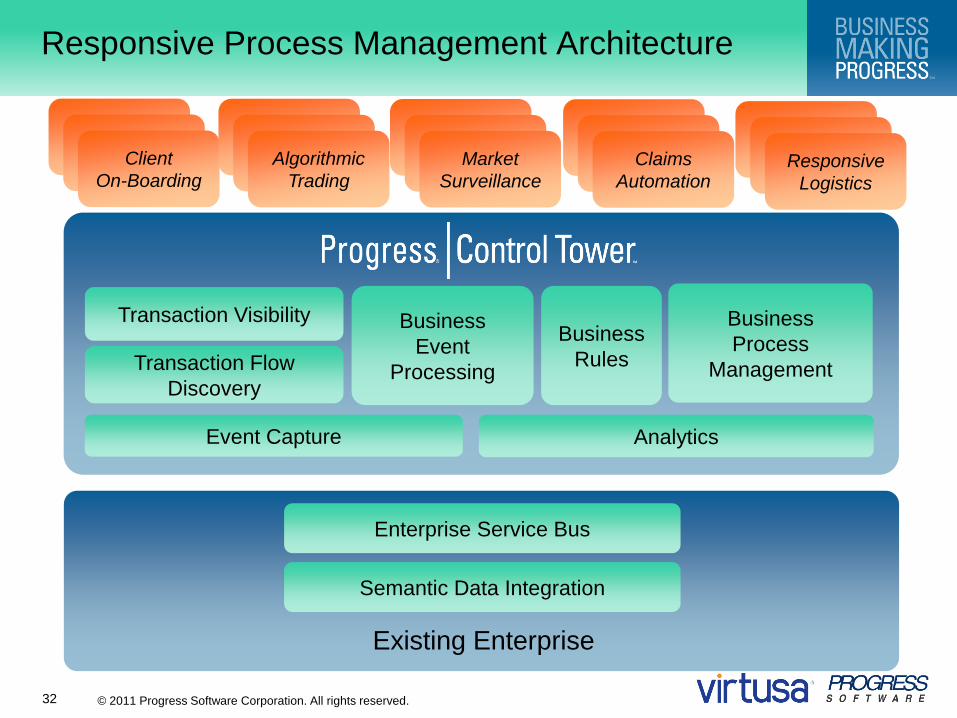

Responsive Process Management Architecture

Enterprise Service Bus

Semantic Data Integration

Event Capture

Transaction Flow

Discovery

Transaction Visibility Business

Event

Processing

Business

Process

Management

Business

Rules

Analytics

Existing Enterprise

Market

SurveillanceMarket

SurveillanceClient

On-Boarding

Algorithmic

TradingAlgorithmic

TradingAlgorithmic

Trading

Market

Surveillance

Smart

AirlinesSmart

AirlinesClaims

Automation

Smart

AirlinesSmart

AirlinesResponsive

Logistics

© 2011 Progress Software Corporation. All rights reserved.33

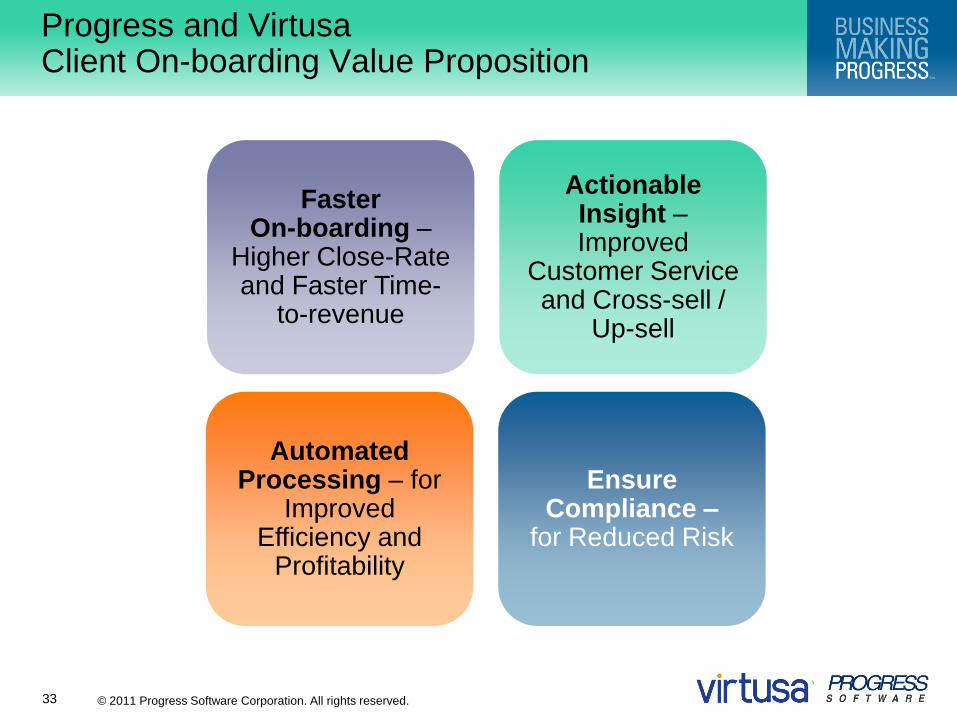

Progress and Virtusa Client On-boarding Value Proposition

Faster On-boarding –

Higher Close-Rate and Faster Time-

to-revenue

Actionable Insight –Improved

Customer Service and Cross-sell /

Up-sell

Automated Processing – for

Improved Efficiency and

Profitability

Ensure Compliance –

for Reduced Risk

© 2011 Progress Software Corporation. All rights reserved.34

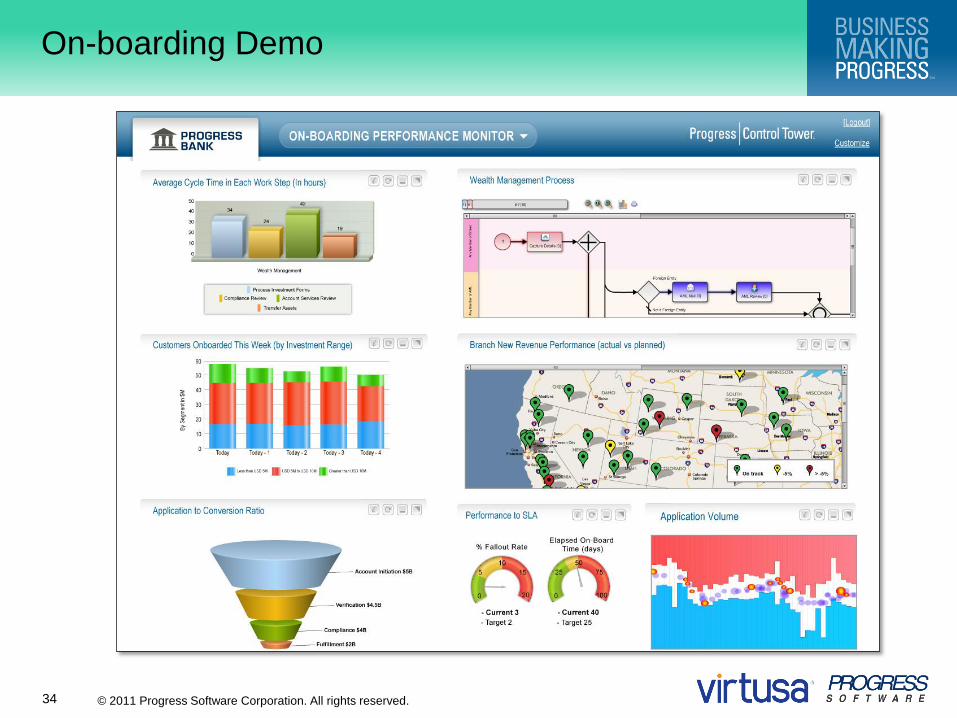

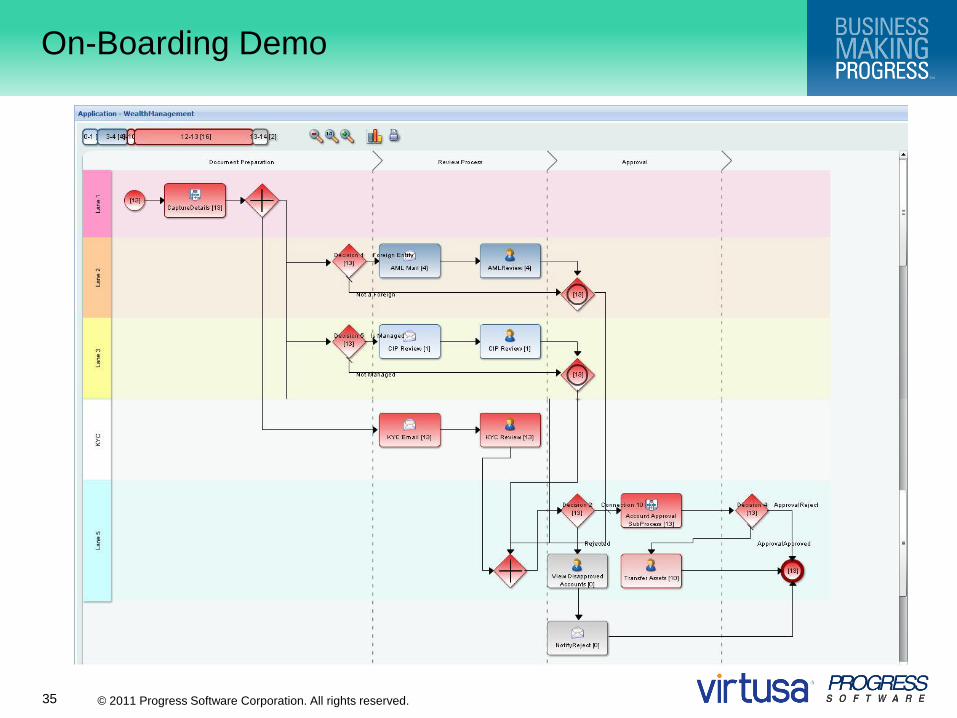

On-boarding Demo

© 2011 Progress Software Corporation. All rights reserved.35

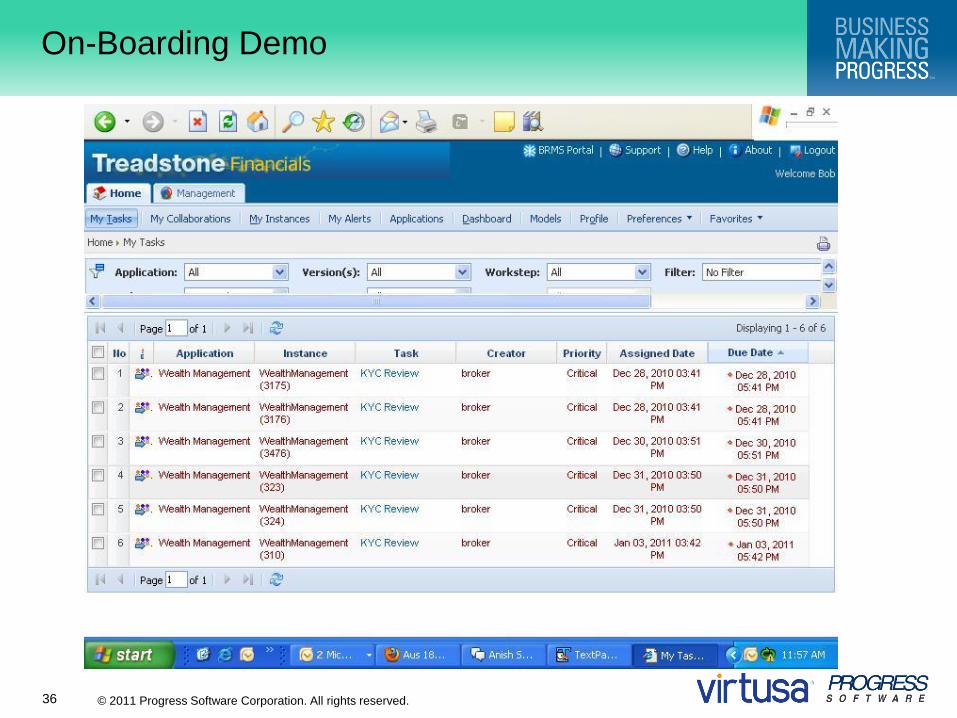

On-Boarding Demo

© 2011 Progress Software Corporation. All rights reserved.36

On-Boarding Demo

© 2011 Progress Software Corporation. All rights reserved.37

RPM Test Drive for Client On-boarding

RPM Test Drive for on-boarding

can accelerate time to market and

eliminate risks

Intensive 3-week engagement built on

Virtusa’s Understand-Evaluate-

Demonstrate (UED) framework

BPM education and RPM concepts

overview

Align Stakeholders around business

goals and KPI’s

Evaluation of on-boarding business

challenges and business case

preparation

Solution architecture/product

architecture approach for on-boarding

Solution prototype for on-boarding

Assets Offered

RPM training material

On-boarding business

case templates & ROI

calculations tool

Product evaluation

framework

Customizable On-

boarding demo

Reference architecture

for On-boarding

mapped to Progress

RPM software

© 2011 Progress Software Corporation. All rights reserved.38

RPM Test Drive for Client On-boarding (cont.)

Target audience for RPM Test Drive

Clients who have identified Customer on-

boarding as one of the key transformation areas

Business and IT stakeholders have a different

view of process and transformation goals

Largely manual processes today with little

transparency and control

Evaluating Technology options

Defining overall Program roadmap for on-

boarding

© 2011 Progress Software Corporation. All rights reserved.39

Question and Answers

Please Submit Your Questions

For more information, go to

http://www.progress.com/bankinginfo

or contact us at

or 781.280.4700

Luis Sierra

Vinaykumar Mummigatti