Centro PRISTEM – Università “Bocconi” Dipartimento di Matematica dell’Università di Padova

Upload

kylynn-torresCategory

view

41download

3description

Università Bocconi, A.A: 2005-2006 1Mec – Comparative public economics 1

Università Bocconi A.A. 2005-2006

Comparative public economics

Giampaolo Arachi

Università Bocconi, A.A: 2005-2006 2Mec – Comparative public economics 2

Alternative savings vehiclesAlternative savings vehicles

Intertemporally constant rates

Changes in tax rates over time

Assets with differentially taxed components

References:

M. Scholes, M. A. Wolfson, M. Erickson, E. L. Maydew, T. Shevlin (SWEMS), Taxes and business strategy: a planning approach, Pearson Prentice Hall, third edition, 2005, ch. 3

Università Bocconi, A.A: 2005-2006 3Mec – Comparative public economics 3

Alternative savings vehiclesAlternative savings vehicles

Intertemporally constant rates

Changes in tax rates over time

Assets with differentially taxed components

References:

M. Scholes, M. A. Wolfson, M. Erickson, E. L. Maydew, T. Shevlin (SWEMS), Taxes and business strategy: a planning approach, Pearson Prentice Hall, third edition, 2005, ch. 3

Università Bocconi, A.A: 2005-2006 4Mec – Comparative public economics 4

Different Legal Organizational FormsDifferent Legal Organizational Forms

There are different legal organizational forms (Alternative Savings Vehicles) through which individuals save for the future– Different needs: insurance policies v. bank deposits– Different regulations or policy aims: short and long period

Differences may be leveled out through new contractual arrangements or financial innovation

Università Bocconi, A.A: 2005-2006 5Mec – Comparative public economics 5

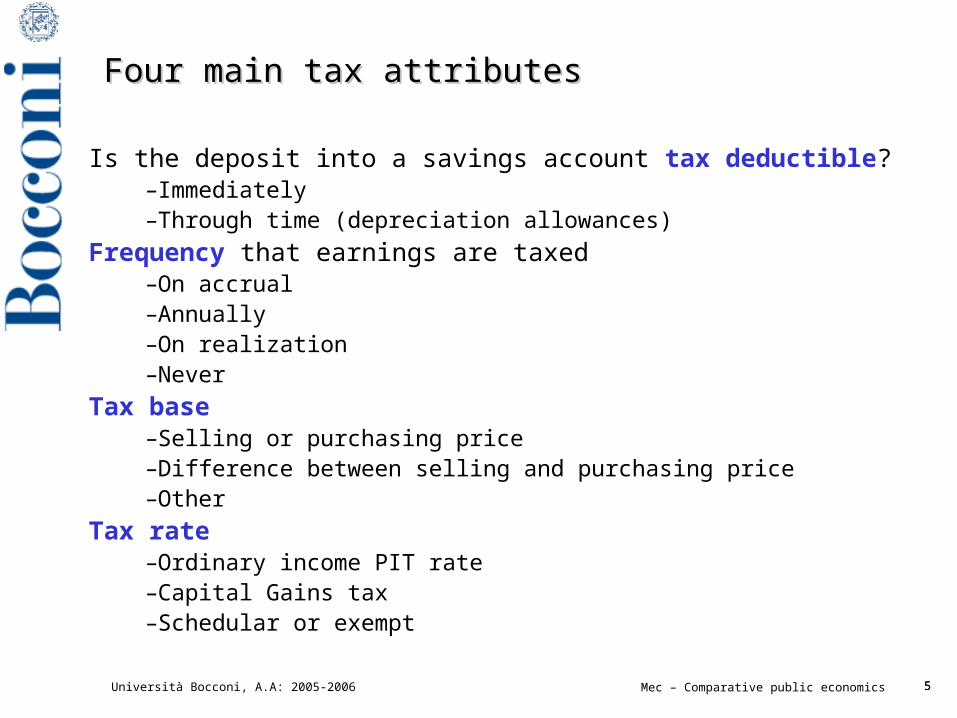

Four main tax attributesFour main tax attributes

Is the deposit into a savings account tax deductible?–Immediately–Through time (depreciation allowances)

Frequency that earnings are taxed–On accrual–Annually–On realization–Never

Tax base –Selling or purchasing price–Difference between selling and purchasing price–Other

Tax rate–Ordinary income PIT rate–Capital Gains tax–Schedular or exempt

Università Bocconi, A.A: 2005-2006 6Mec – Comparative public economics 6

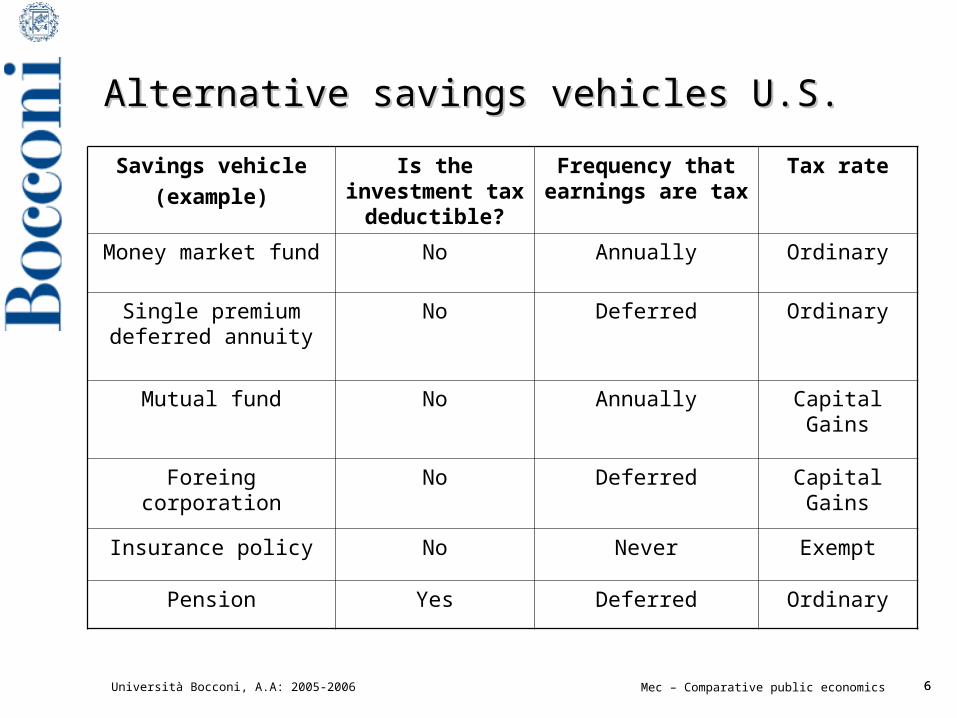

Alternative savings vehicles U.S.Alternative savings vehicles U.S.

Savings vehicle

(example)

Is the investment tax deductible?

Frequency that earnings are tax

Tax rate

Money market fund No Annually Ordinary

Single premium deferred annuity

No Deferred Ordinary

Mutual fund No Annually Capital Gains

Foreing corporation No Deferred Capital Gains

Insurance policy No Never Exempt

Pension Yes Deferred Ordinary

Università Bocconi, A.A: 2005-2006 7Mec – Comparative public economics 7

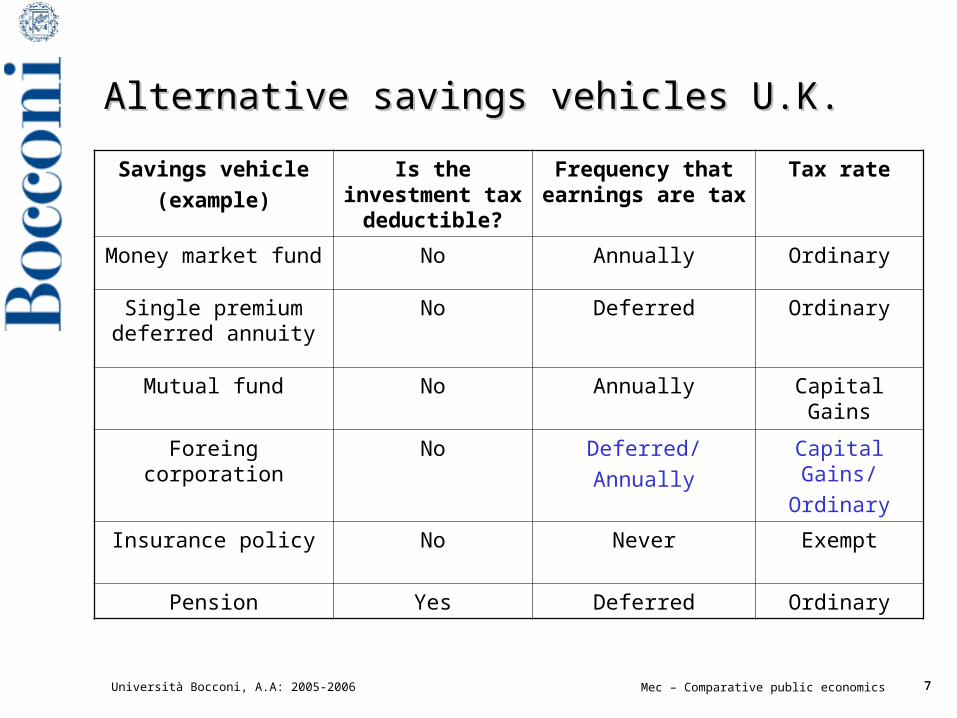

Alternative savings vehicles U.K.Alternative savings vehicles U.K.

Savings vehicle

(example)

Is the investment tax deductible?

Frequency that earnings are tax

Tax rate

Money market fund No Annually Ordinary

Single premium deferred annuity

No Deferred Ordinary

Mutual fund No Annually Capital Gains

Foreing corporation No Deferred/

Annually

Capital Gains/

Ordinary

Insurance policy No Never Exempt

Pension Yes Deferred Ordinary

Università Bocconi, A.A: 2005-2006 8Mec – Comparative public economics 8

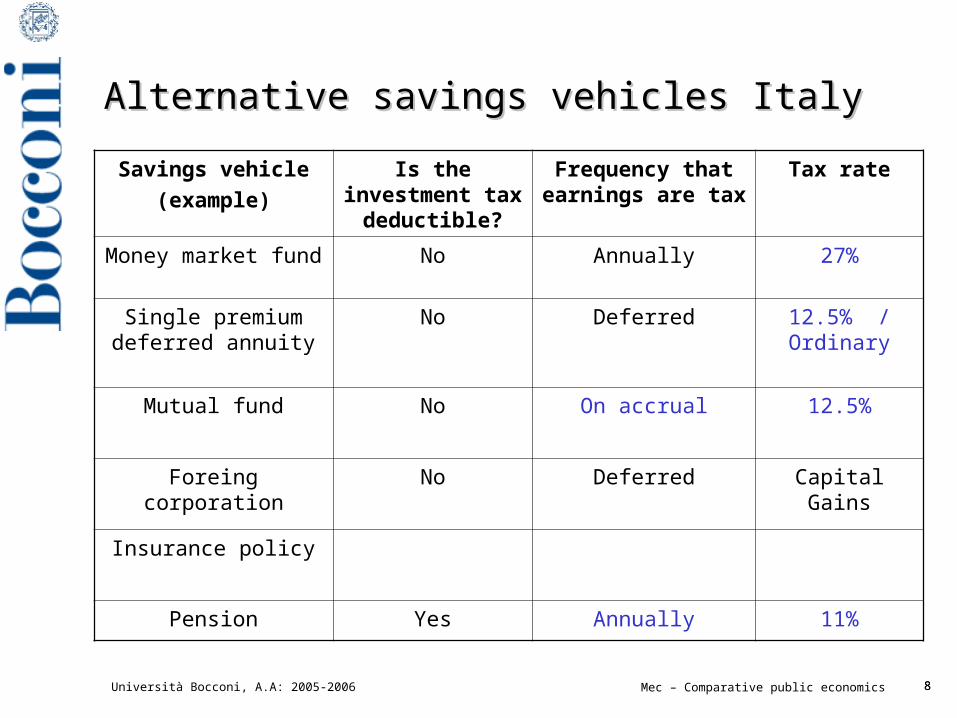

Alternative savings vehicles ItalyAlternative savings vehicles Italy

Savings vehicle

(example)

Is the investment tax deductible?

Frequency that earnings are tax

Tax rate

Money market fund No Annually 27%

Single premium deferred annuity

No Deferred 12.5% / Ordinary

Mutual fund No On accrual 12.5%

Foreing corporation No Deferred Capital Gains

Insurance policy

Pension Yes Annually 11%

Università Bocconi, A.A: 2005-2006 9Mec – Comparative public economics 9

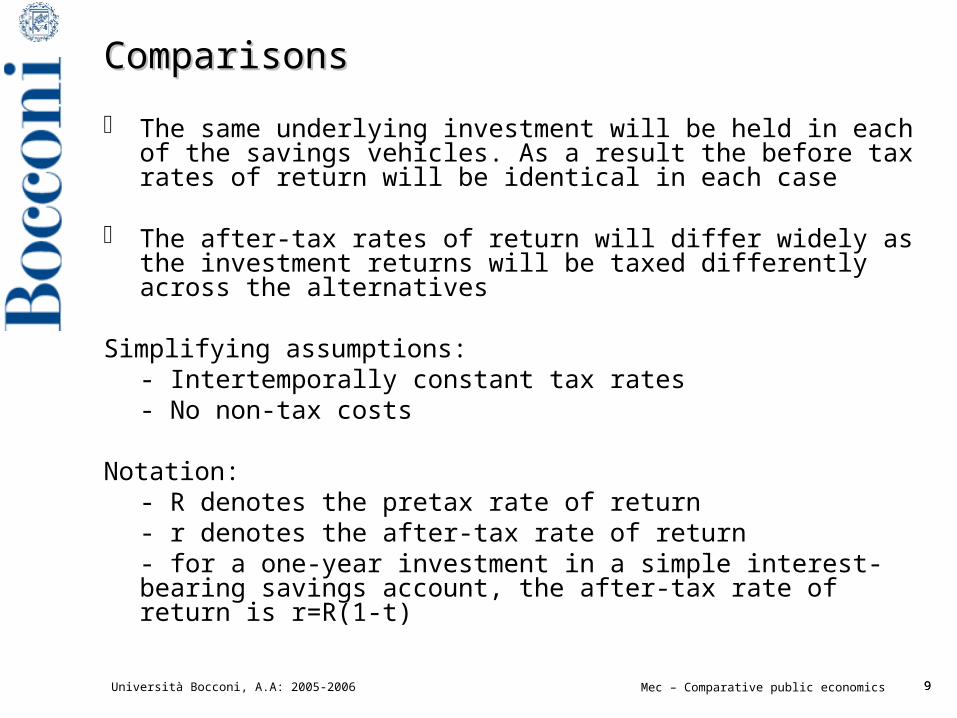

ComparisonsComparisons

The same underlying investment will be held in each of the savings vehicles. As a result the before tax rates of return will be identical in each case

The after-tax rates of return will differ widely as the investment returns will be taxed differently across the alternatives

Simplifying assumptions: - Intertemporally constant tax rates- No non-tax costs

Notation:- R denotes the pretax rate of return- r denotes the after-tax rate of return- for a one-year investment in a simple interest-bearing savings account, the after-tax rate of return is r=R(1-t)

Università Bocconi, A.A: 2005-2006 10Mec – Comparative public economics 10

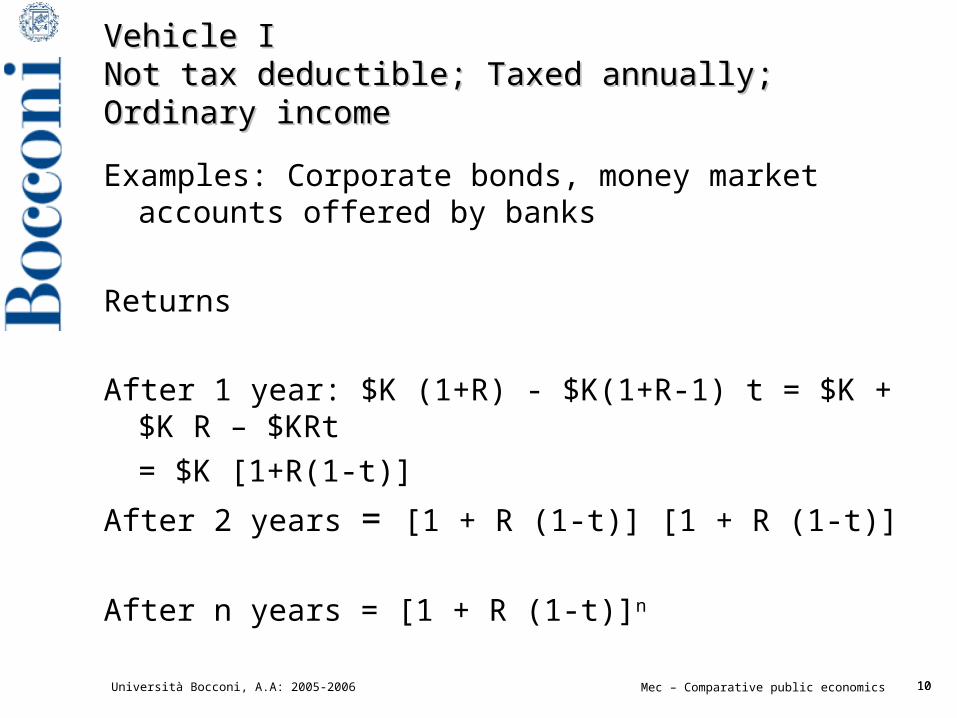

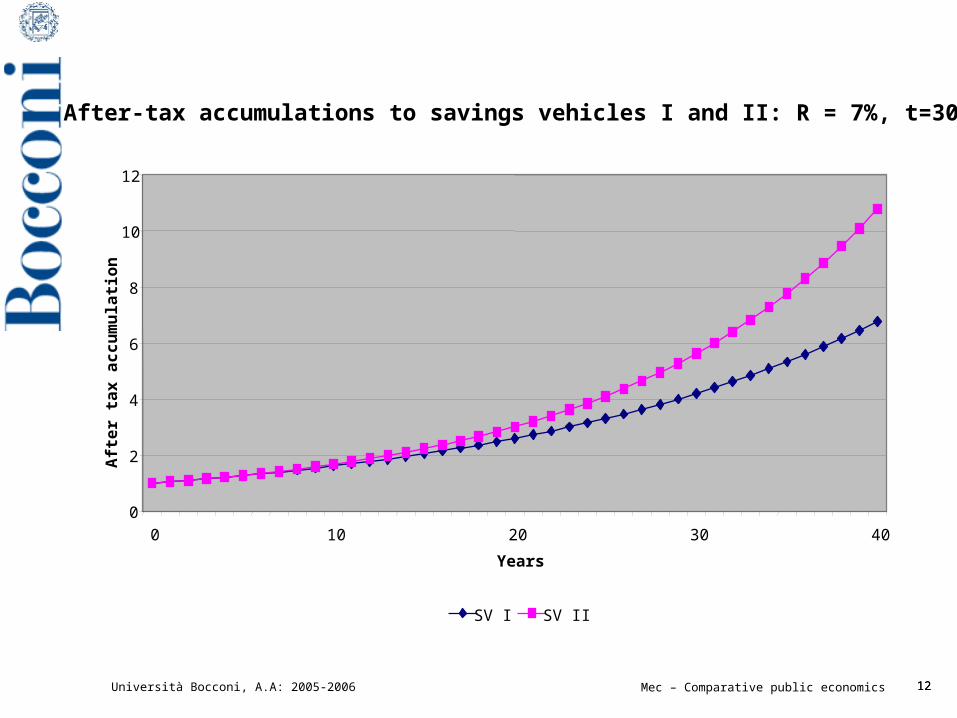

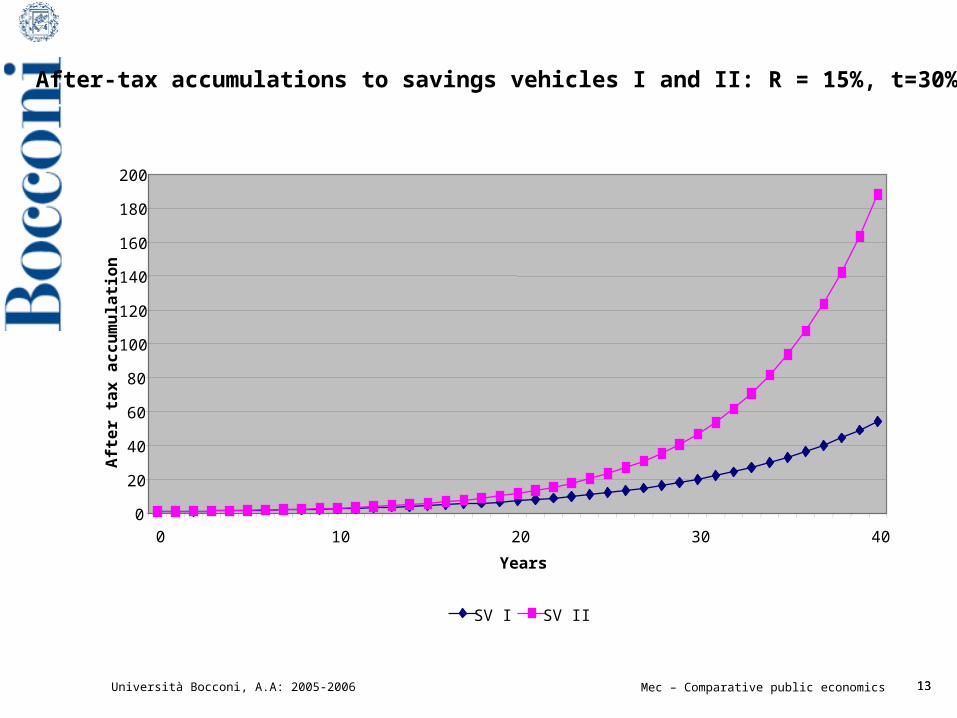

Vehicle IVehicle INot tax deductible; Taxed annually; Ordinary incomeNot tax deductible; Taxed annually; Ordinary income

Examples: Corporate bonds, money market accounts offered by banks

Returns

After 1 year: $K (1+R) - $K(1+R-1) t = $K + $K R – $KRt

= $K [1+R(1-t)]

After 2 years = [1 + R (1-t)] [1 + R (1-t)]

After n years = [1 + R (1-t)]n

Università Bocconi, A.A: 2005-2006 11Mec – Comparative public economics 11

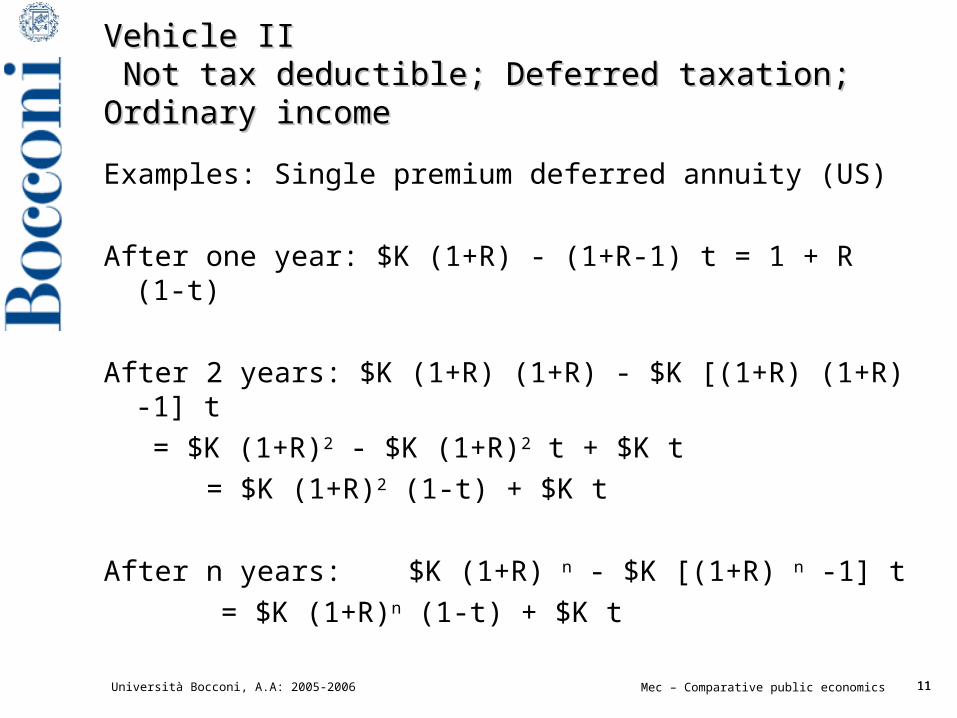

Vehicle IIVehicle II Not tax deductible; Deferred taxation; Ordinary incomeNot tax deductible; Deferred taxation; Ordinary income

Examples: Single premium deferred annuity (US)

After one year: $K (1+R) - (1+R-1) t = 1 + R (1-t)

After 2 years: $K (1+R) (1+R) - $K [(1+R) (1+R) -1] t

= $K (1+R)2 - $K (1+R)2 t + $K t

= $K (1+R)2 (1-t) + $K t

After n years: $K (1+R) n - $K [(1+R) n -1] t

= $K (1+R)n (1-t) + $K t

Università Bocconi, A.A: 2005-2006 12Mec – Comparative public economics 12

After-tax accumulations to savings vehicles I and II: R = 7%, t=30%

0

2

4

6

8

10

12

0 10 20 30 40

Years

Aft

er

tax

ac

cu

mu

lati

on

SV I SV II

Università Bocconi, A.A: 2005-2006 13Mec – Comparative public economics 13

After-tax accumulations to savings vehicles I and II: R = 15%, t=30%

0

20

40

60

80

100

120

140

160

180

200

0 10 20 30 40

Years

MMA

Aft

er

tax

ac

cu

mu

lati

on

SV I SV II

Università Bocconi, A.A: 2005-2006 14Mec – Comparative public economics 14

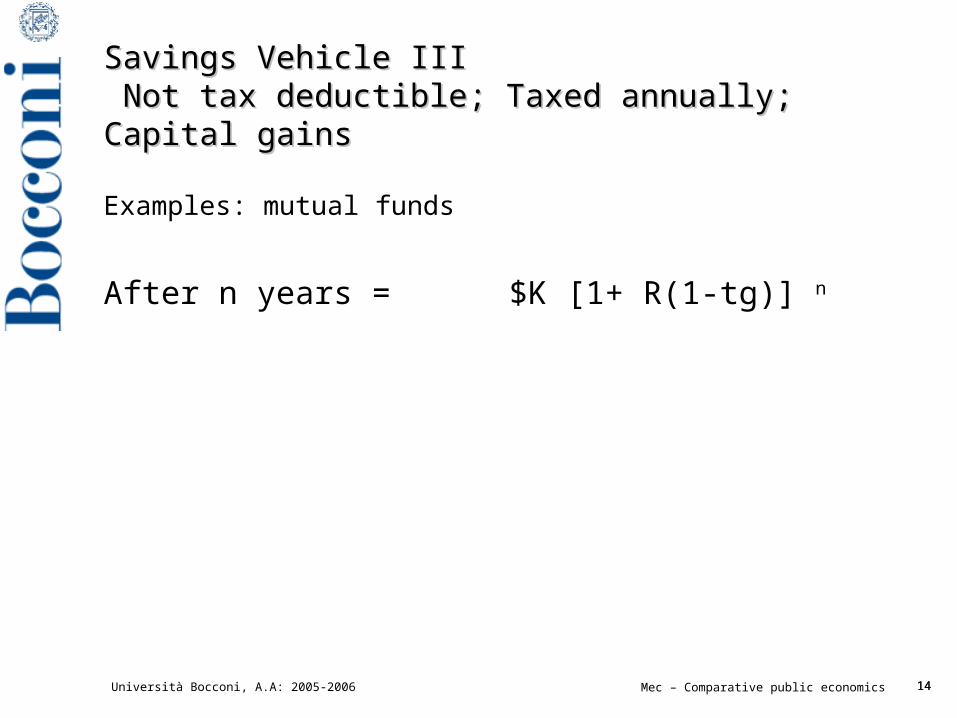

Savings Vehicle IIISavings Vehicle III Not tax deductible; Taxed annually; Capital gainsNot tax deductible; Taxed annually; Capital gains

Examples: mutual funds

After n years = $K [1+ R(1-tg)] n

Università Bocconi, A.A: 2005-2006 15Mec – Comparative public economics 15

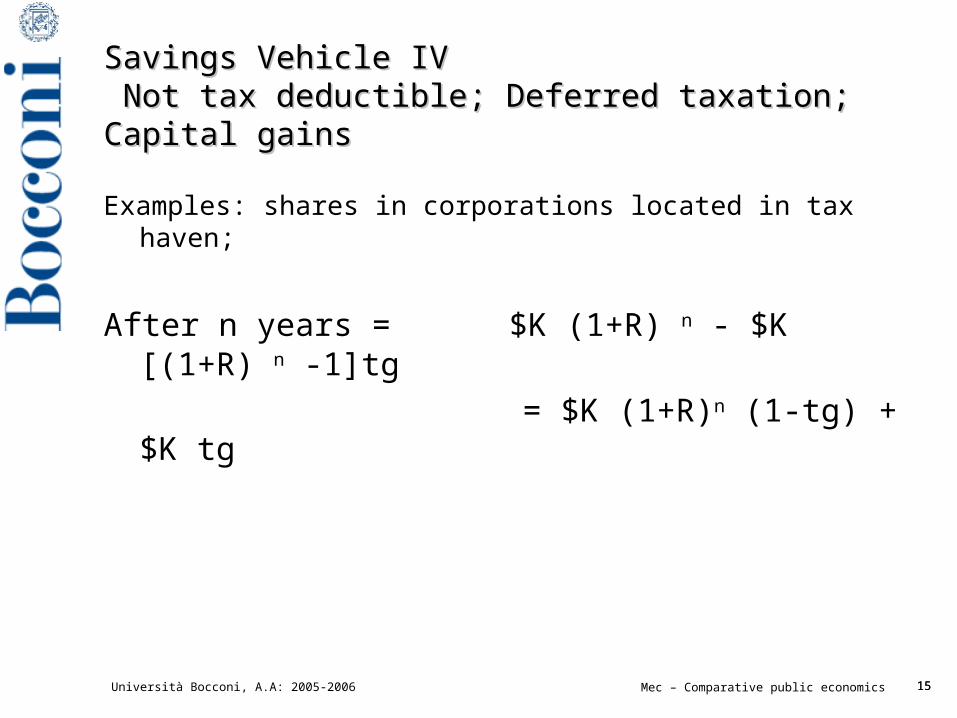

Savings Vehicle IVSavings Vehicle IV Not tax deductible; Deferred taxation; Capital gainsNot tax deductible; Deferred taxation; Capital gains

Examples: shares in corporations located in tax haven;

After n years = $K (1+R) n - $K [(1+R) n -1]tg

= $K (1+R)n (1-tg) + $K tg

Università Bocconi, A.A: 2005-2006 16Mec – Comparative public economics 16

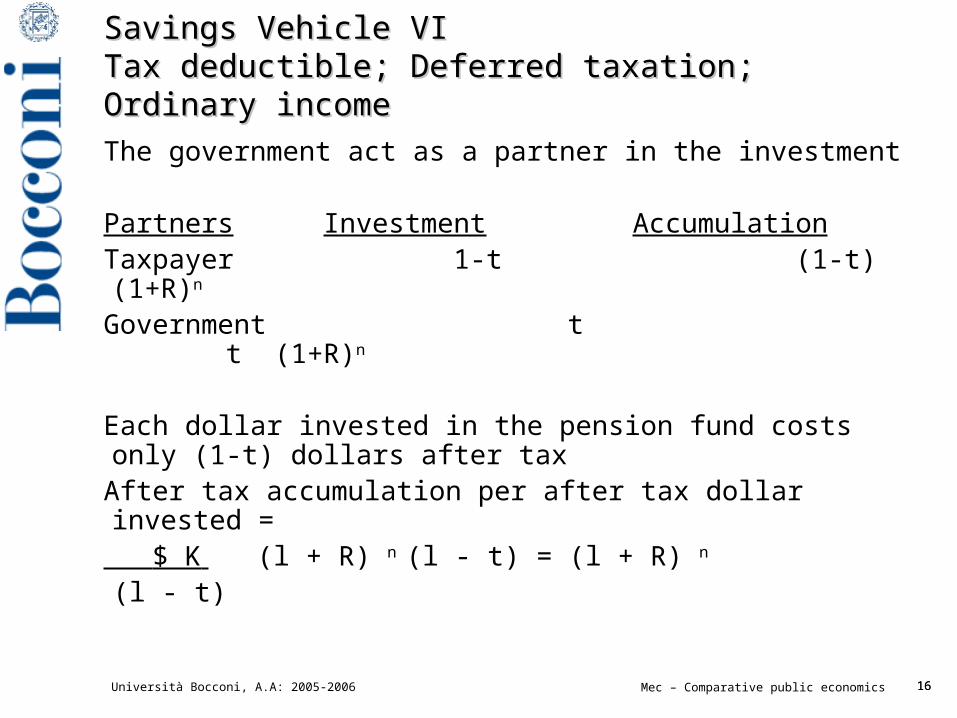

Savings Vehicle VISavings Vehicle VITTax deductible; Deferred taxation; Ordinary incomeax deductible; Deferred taxation; Ordinary income

The government act as a partner in the investment

Partners Investment AccumulationTaxpayer 1-t (1-t) (1+R)n

Government t t (1+R)n

Each dollar invested in the pension fund costs only (1-t) dollars after tax

After tax accumulation per after tax dollar invested = $ K (l + R) n (l - t) = (l + R) n

(l - t)

Università Bocconi, A.A: 2005-2006 17Mec – Comparative public economics 17

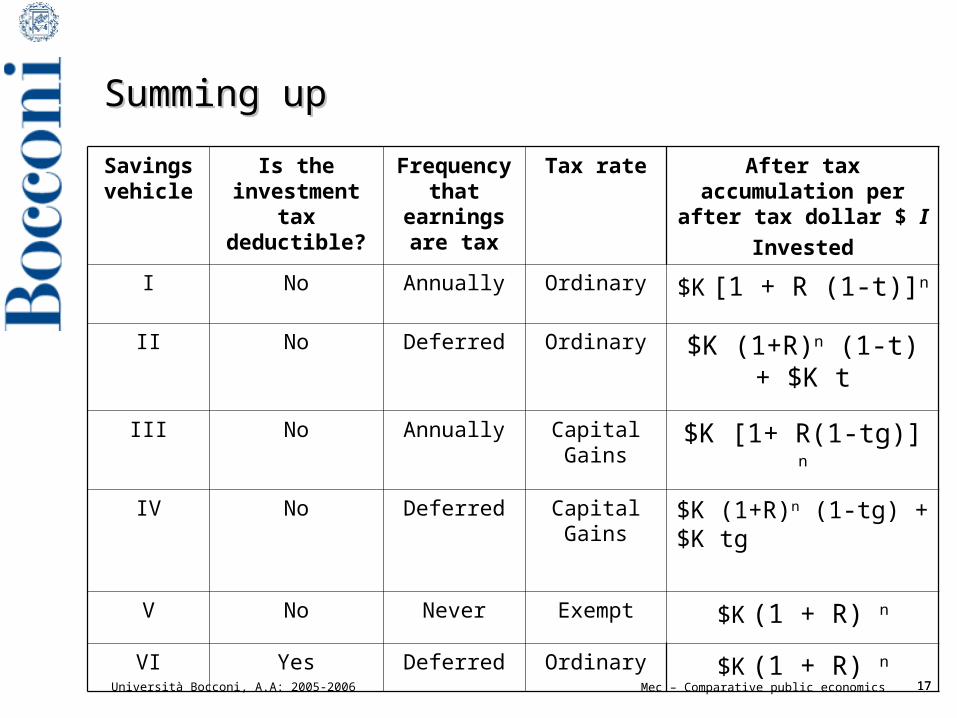

Summing upSumming up

Savings vehicle

Is the investment tax

deductible?

Frequency that

earnings are tax

Tax rate After tax accumulation per after tax dollar $ I

Invested

I No Annually Ordinary $K [1 + R (1-t)]n

II No Deferred Ordinary $K (1+R)n (1-t) + $K t

III No Annually Capital Gains

$K [1+ R(1-tg)] n

IV No Deferred Capital Gains

$K (1+R)n (1-tg) + $K tg

V No Never Exempt $K (1 + R) n

VI Yes Deferred Ordinary $K (1 + R) n

Università Bocconi, A.A: 2005-2006 18Mec – Comparative public economics 18

OutlineOutline

Intertemporally constant rates

Changes in tax rates over time

Assets with differentially taxed components

Università Bocconi, A.A: 2005-2006 19Mec – Comparative public economics 19

Changes in tax rates over timeChanges in tax rates over time

Simplifying assumption: future tax rates are known

• Returns depends on realization strategy: realize profit when taxes are low and losses when taxes are high

• Simple dominance relations no longer hold

Università Bocconi, A.A: 2005-2006 20Mec – Comparative public economics 20

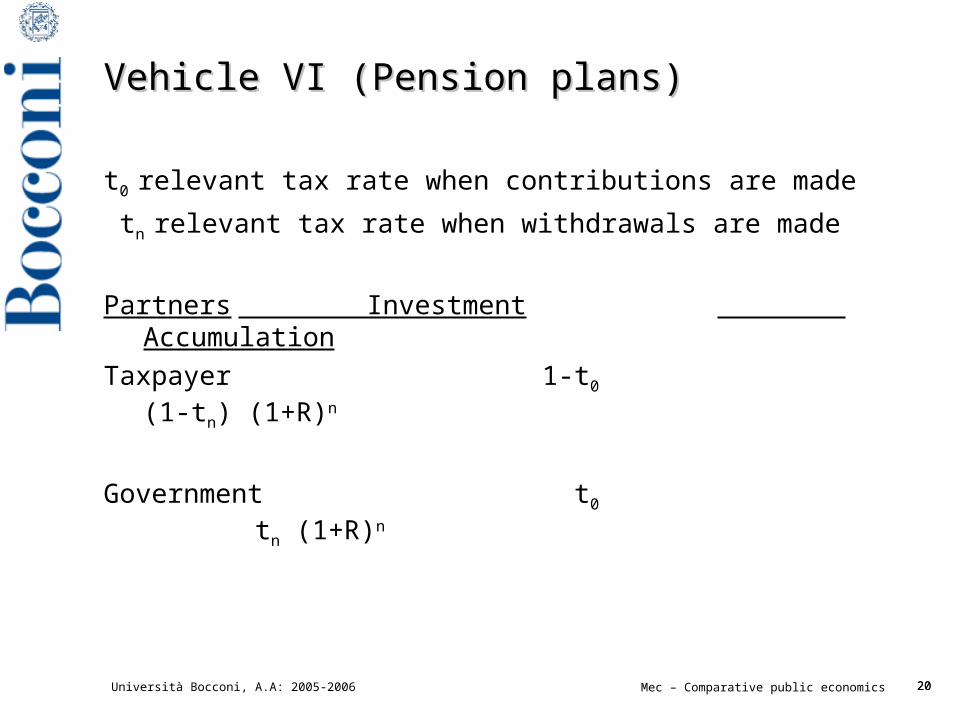

Vehicle VI (Pension plans)Vehicle VI (Pension plans)

t0 relevant tax rate when contributions are made

tn relevant tax rate when withdrawals are made

Partners Investment Accumulation

Taxpayer 1-t0 (1-tn) (1+R)n

Government t0 tn (1+R)n

Università Bocconi, A.A: 2005-2006 21Mec – Comparative public economics 21

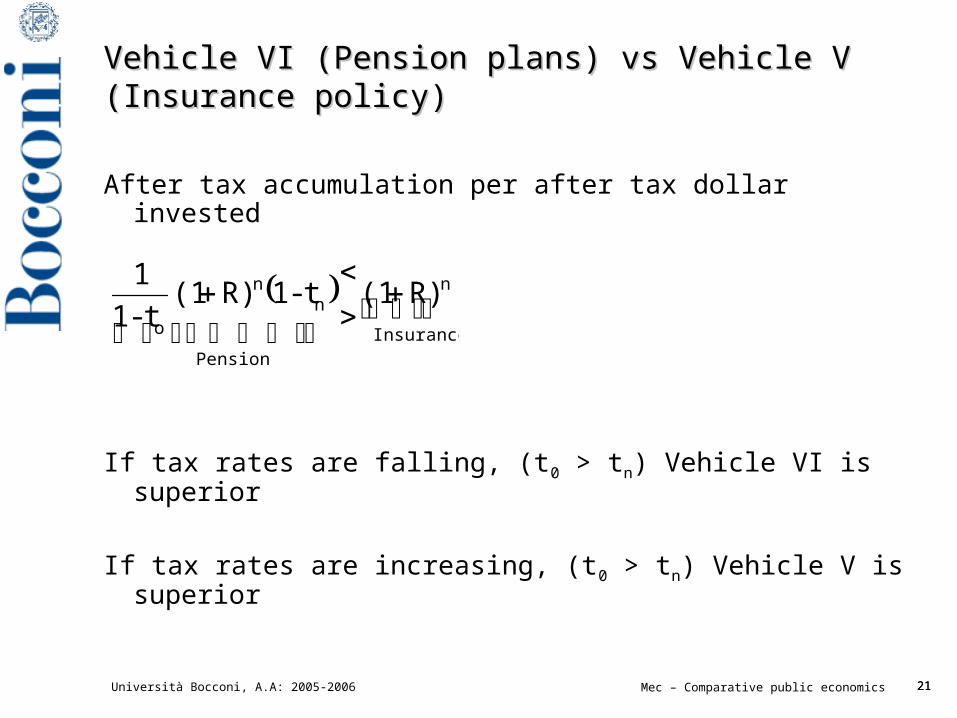

Vehicle VI (Pension plans) vs Vehicle V (Insurance Vehicle VI (Pension plans) vs Vehicle V (Insurance policy)policy)

After tax accumulation per after tax dollar invested

If tax rates are falling, (t0 > tn) Vehicle VI is superior

If tax rates are increasing, (t0 > tn) Vehicle V is superior

Insurance

n

Pension

nn

o

R)(1t-1R)(1t-1

1

Università Bocconi, A.A: 2005-2006 22Mec – Comparative public economics 22

Rollover into a different vehicleRollover into a different vehicle

Traditional deductible IRA

An eligible taxpayer may contribute up to $2000 per year. Contributions are tax deductible and earnings in the pension account are tax deferred until the taxpayer makes withdrawals in retirement.

Savings Vehicle VI

Università Bocconi, A.A: 2005-2006 23Mec – Comparative public economics 23

Rollover into a different vehicleRollover into a different vehicle

Roth IRA

An eligible taxpayer may contribute up to $2000 per year. Contributions are NOT tax deductible and withdrawals are tax free.

Savings Vehicle V

Università Bocconi, A.A: 2005-2006 24Mec – Comparative public economics 24

Rollover into a different vehicleRollover into a different vehicle

Since 1998 taxpayers with balances in deductible IRAs can rollover the balance into a Roth IRA.

The amount rolled over is included in the taxapayer taxable income in the year of the rollover

Is it the rollover profitable?

Deductible IRA accumulation = V (1+R)n (1-tn)

Rollover Roth accumulation = V (1+R)n - taxes paid at rollover - returns lost on taxes paid

Università Bocconi, A.A: 2005-2006 25Mec – Comparative public economics 25

Rollover into a different vehicleRollover into a different vehicle

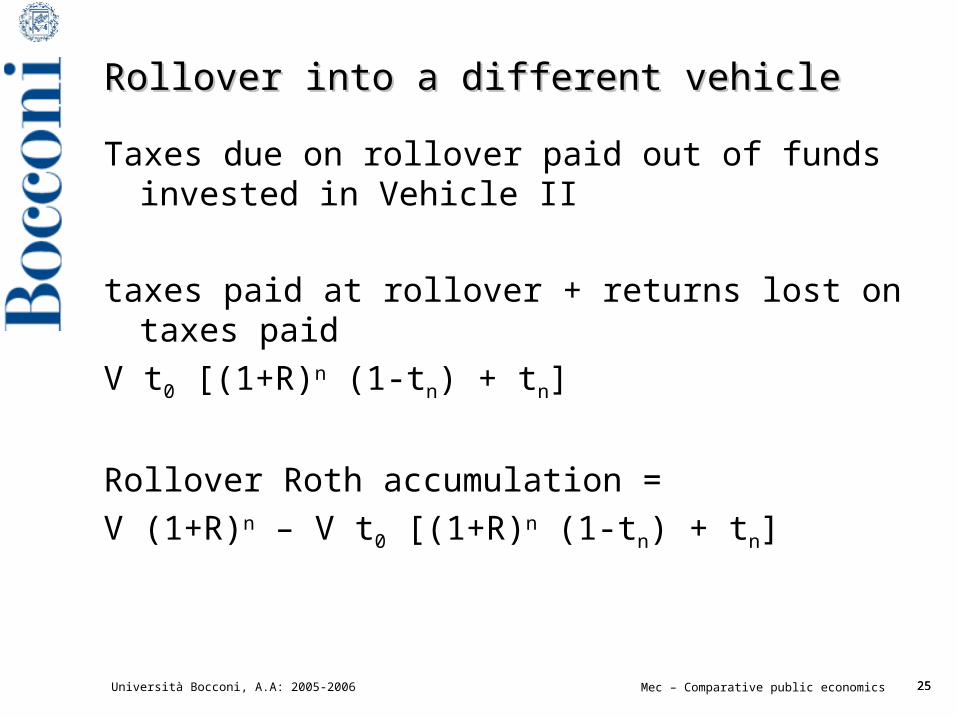

Taxes due on rollover paid out of funds invested in Vehicle II

taxes paid at rollover + returns lost on taxes paid

V t0 [(1+R)n (1-tn) + tn]

Rollover Roth accumulation =

V (1+R)n – V t0 [(1+R)n (1-tn) + tn]

Università Bocconi, A.A: 2005-2006 26Mec – Comparative public economics 26

Rollover into a different vehicleRollover into a different vehicle

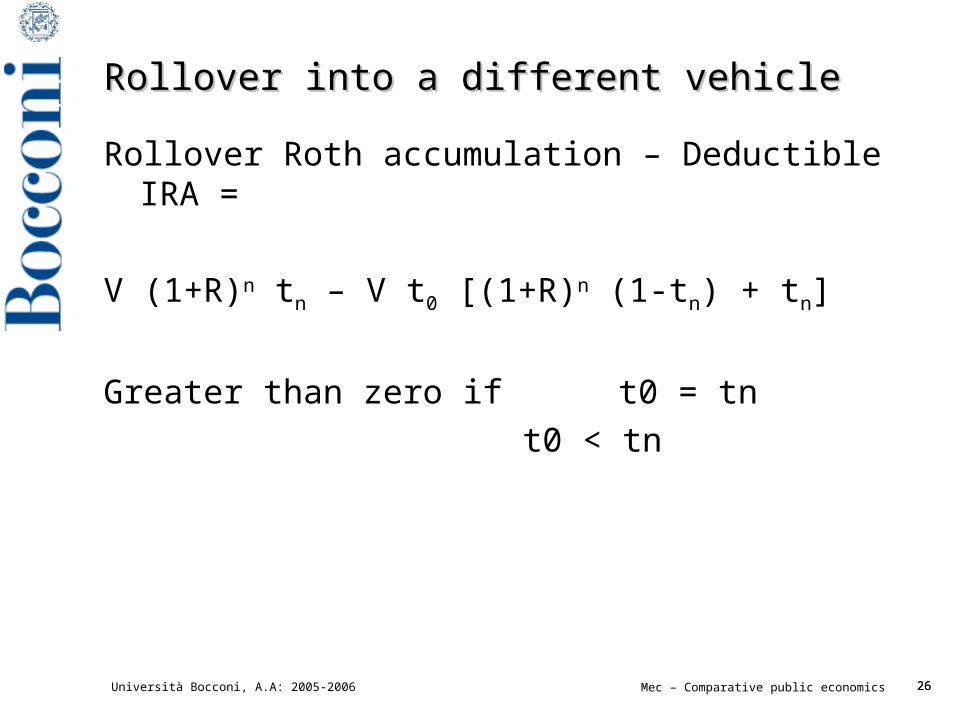

Rollover Roth accumulation – Deductible IRA =

V (1+R)n tn – V t0 [(1+R)n (1-tn) + tn]

Greater than zero if t0 = tn

t0 < tn

Università Bocconi, A.A: 2005-2006 27Mec – Comparative public economics 27

OutlineOutline

Intertemporally constant rates

Changes in tax rates over time

Assets with differentially taxed components

Università Bocconi, A.A: 2005-2006 28Mec – Comparative public economics 28

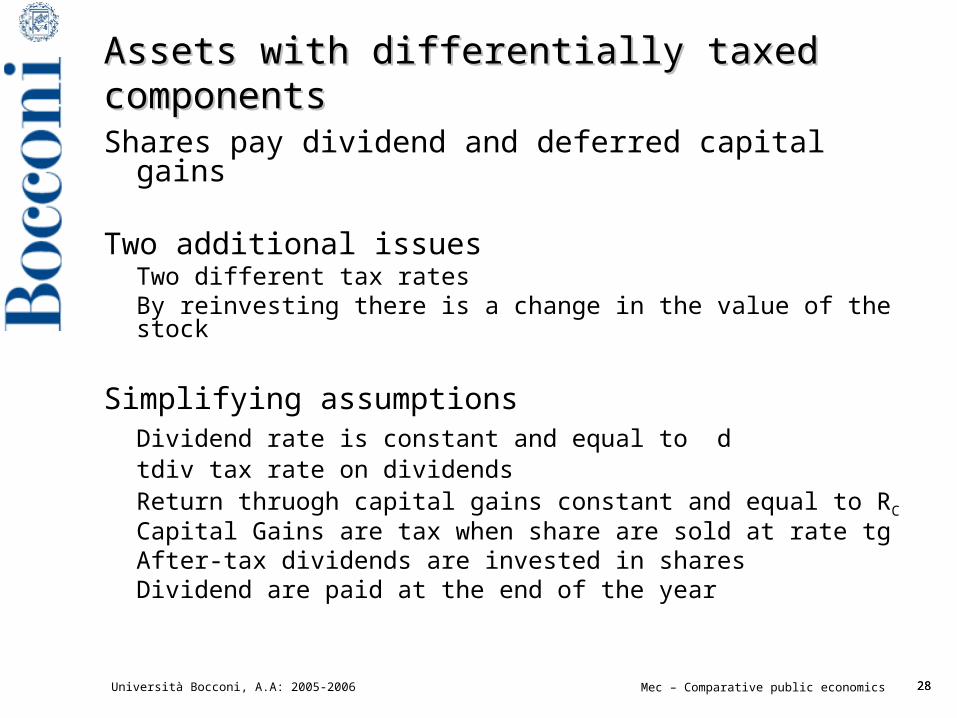

Assets with differentially taxed componentsAssets with differentially taxed components

Shares pay dividend and deferred capital gains

Two additional issuesTwo different tax ratesBy reinvesting there is a change in the value of the stock

Simplifying assumptionsDividend rate is constant and equal to dtdiv tax rate on dividendsReturn thruogh capital gains constant and equal to RC

Capital Gains are tax when share are sold at rate tgAfter-tax dividends are invested in sharesDividend are paid at the end of the year

Università Bocconi, A.A: 2005-2006 29Mec – Comparative public economics 29

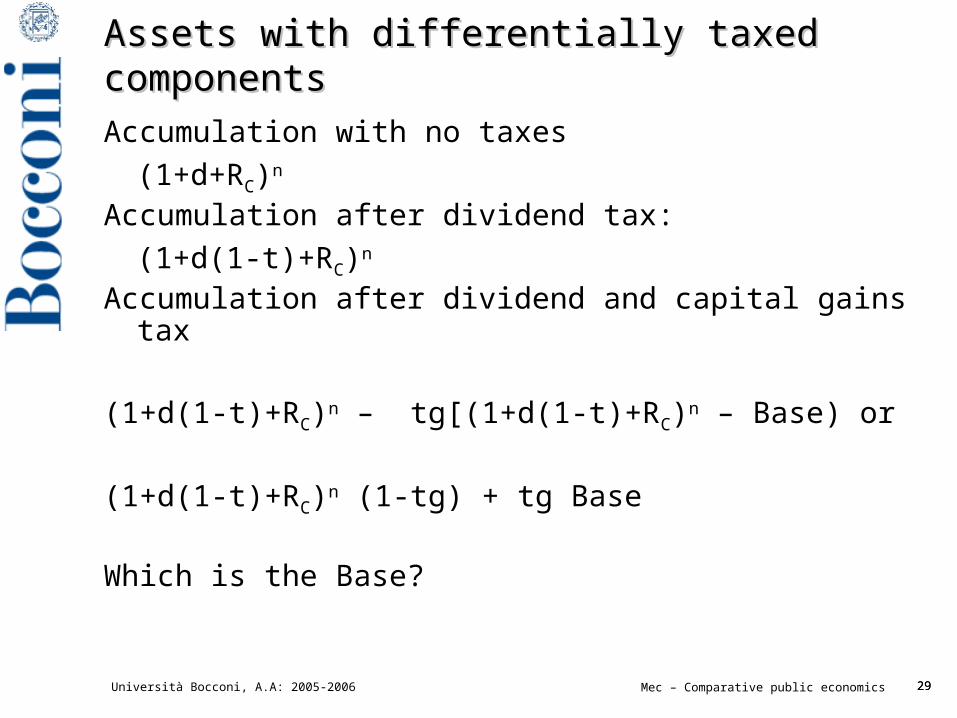

Assets with differentially taxed componentsAssets with differentially taxed components

Accumulation with no taxes

(1+d+RC)n

Accumulation after dividend tax:

(1+d(1-t)+RC)n

Accumulation after dividend and capital gains tax

(1+d(1-t)+RC)n – tg[(1+d(1-t)+RC)n – Base) or

(1+d(1-t)+RC)n (1-tg) + tg Base

Which is the Base?

Università Bocconi, A.A: 2005-2006 30Mec – Comparative public economics 30

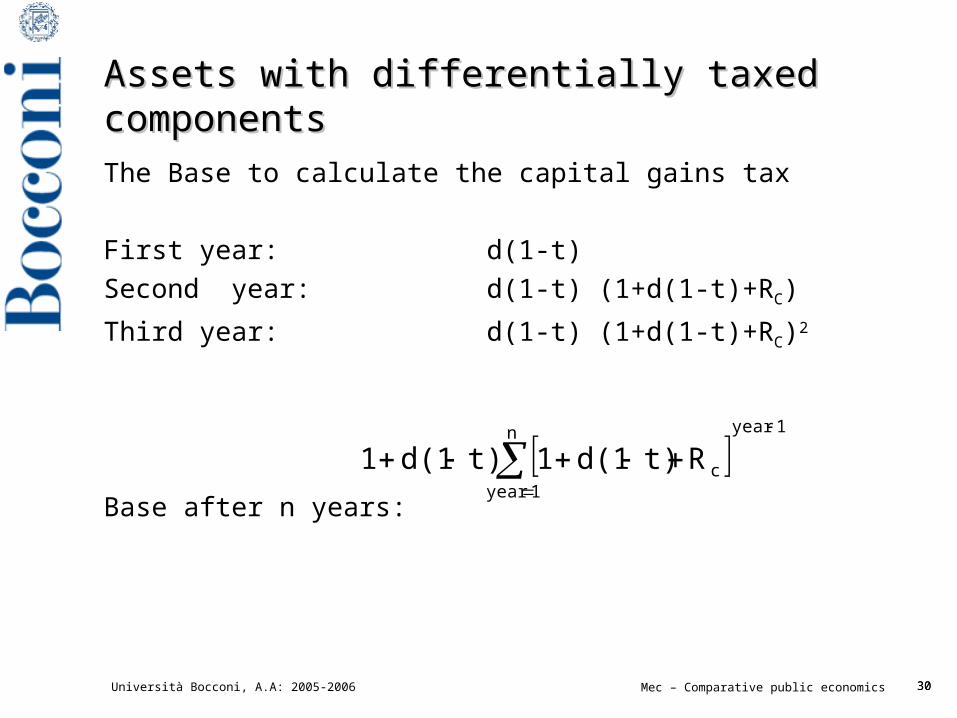

Assets with differentially taxed componentsAssets with differentially taxed components

The Base to calculate the capital gains tax

First year: d(1-t)

Second year: d(1-t) (1+d(1-t)+RC)

Third year: d(1-t) (1+d(1-t)+RC)2

Base after n years:

1yearn

1yearcRt)d(11t)d(11

Università Bocconi, A.A: 2005-2006 31Mec – Comparative public economics 31

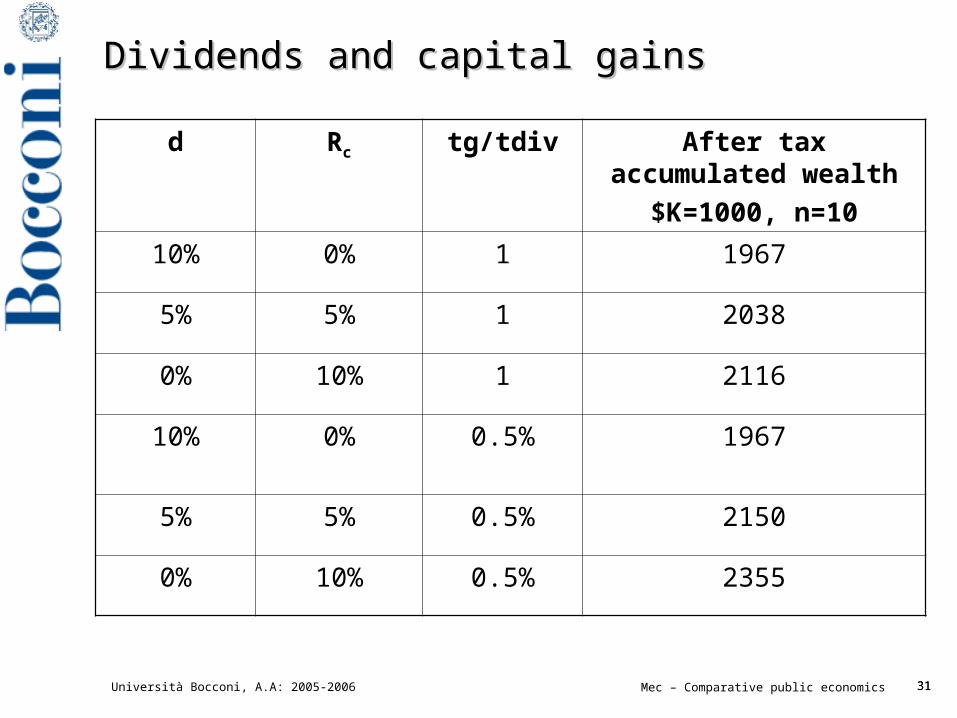

Dividends and capital gainsDividends and capital gains

d Rc tg/tdiv After tax accumulated wealth

$K=1000, n=10

10% 0% 1 1967

5% 5% 1 2038

0% 10% 1 2116

10% 0% 0.5% 1967

5% 5% 0.5% 2150

0% 10% 0.5% 2355