Mouvements et natures de stock Stock physique Stock disponible Stock théorique Stock réservé.

Upload

vuongthienCategory

view

220download

0

Private and Confidential Orrick, Herrington & Sutcliffe LLP

Joseph Perkins

February 23, 2016

Understanding Investors and Preferred Stock Financings in Silicon Valley

AGENDA

• Choosing your Investor

• Setting the Stage for a Term Sheet

• Negotiating the Term Sheet

• Key Terms in a Preferred Stock Financing

• Process and Getting to Close

• Next Steps - What to do Now

Term Sheet Review – Venture Capital Preferred Stock Financing

2

Steps to Choosing your Investor:

• Know what you need

• Understand the Types of Investors and what they provide

• Investors – the Good, the Bad, and the Ugly

• Opening the Doors

Choosing Your Investor

3

Know What you Need:

All Companies need Capital to thrive, but there are different types of Capital:

• Human Capital (quantity and quality)

• Social Capital (breadth and depth)

• Financial Capital (current and access to additional)

Choosing Your Investor

4

Types of Investors: Incorporation and Seed-Stage Investors

• Friends & Family • Angels and Super Angels • Incubators and Accelerators • Government and Foundations

Early-Stage and Late-Stage Investors • Venture Capitalists • Strategic Investors • Commercial Banks (as lender) • Private Equity and Investment Banks • Government and Foundations

Choosing Your Investor

5

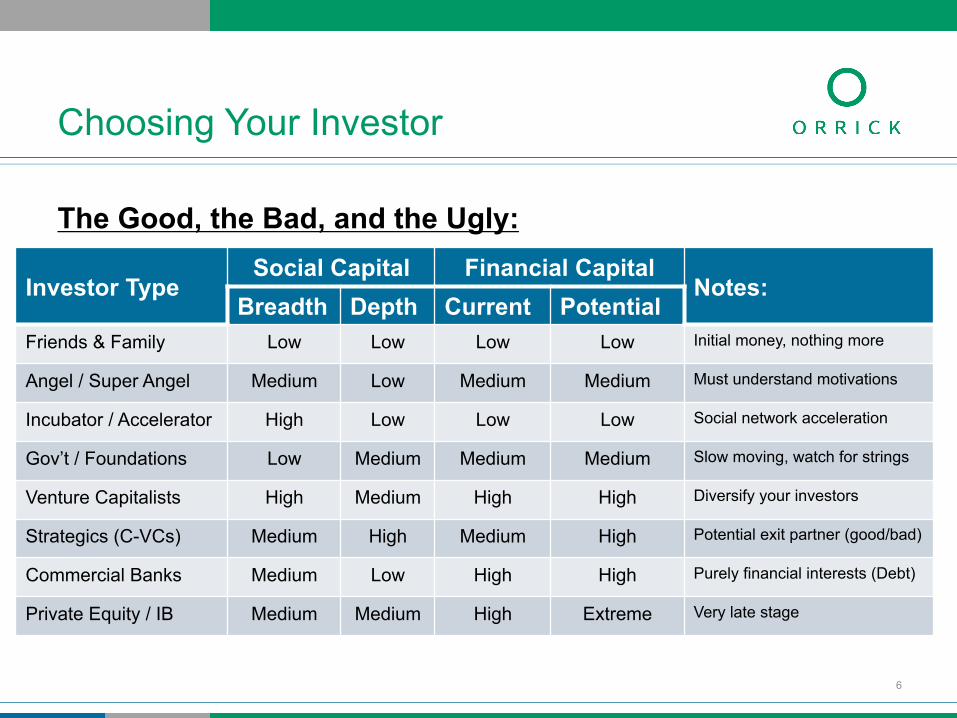

The Good, the Bad, and the Ugly:

Choosing Your Investor

6

Investor Type Social Capital Financial Capital

Notes: Breadth Depth Current Potential

Friends & Family Low Low Low Low Initial money, nothing more

Angel / Super Angel Medium Low Medium Medium Must understand motivations

Incubator / Accelerator High Low Low Low Social network acceleration

Gov’t / Foundations Low Medium Medium Medium Slow moving, watch for strings

Venture Capitalists High Medium High High Diversify your investors

Strategics (C-VCs) Medium High Medium High Potential exit partner (good/bad)

Commercial Banks Medium Low High High Purely financial interests (Debt)

Private Equity / IB Medium Medium High Extreme Very late stage

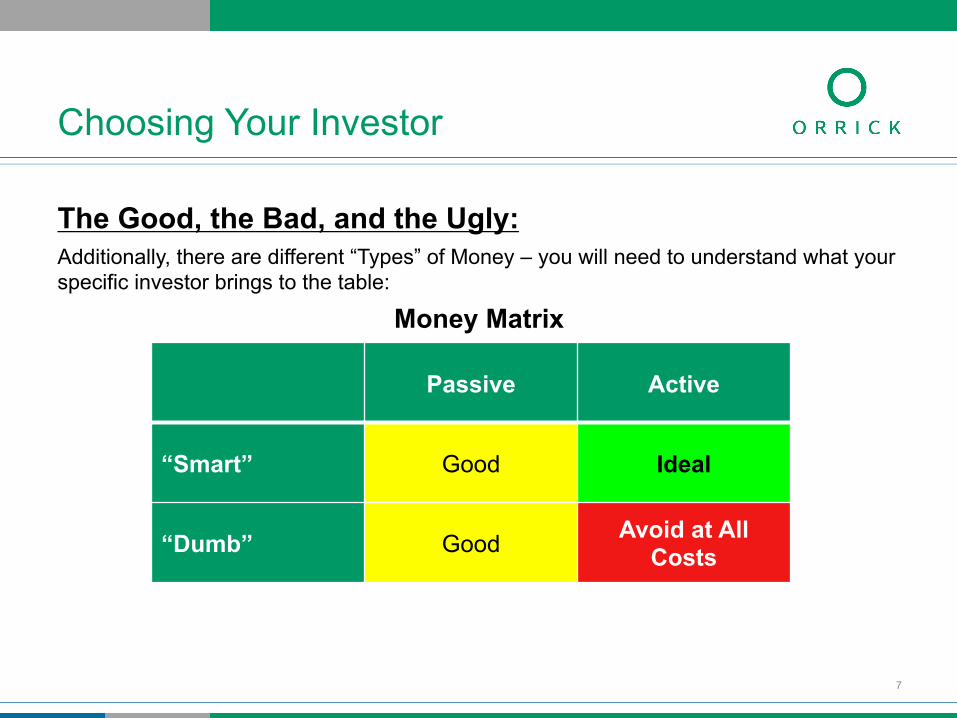

The Good, the Bad, and the Ugly: Additionally, there are different “Types” of Money – you will need to understand what your specific investor brings to the table:

Money Matrix

Choosing Your Investor

7

Passive Active

“Smart” Good Ideal

“Dumb” Good Avoid at All Costs

Opening the Doors:

• Find investors through your current network (other founders, service providers, prior co-workers, etc.)

• Reach out 3-6 months before you actually need the investment (build relationships, set expectations, get advice)

• After meeting, determine who is likely to be most helpful to you (analyze their financial and social capital, personality, and strategic fit)

• Keep investors updated on key developments and trajectory (but avoid disclosing too much)

Choosing Your Investor

8

What do you need to do before you get a term sheet?

• Build your product!

• Define your metrics and deliver (differs by industry and stage).

• Get documentation in order (minimize red flags):

» Organizational documents

» IP Assignment

» Capitalization Table clean up as needed

» Former founder/employee releases

Setting the Stage for a Term Sheet

9

What do Investors Look For?

• Market (threshold question – must swing for the fences)

• Product (innovative, simple, scalable within the market)

• Team

» Human Capital (depth of experience individually and as a team, diverse backgrounds, likability)

» Social Capital (what is the network you already have established)

• Ultimately, it is about whether they think they can get a big return on investing in your Company.*

* may not hold true for Strategic Investors / Corporate VCs, who may invest for reasons that are not directly related to return on investment.

Setting the Stage for a Term Sheet

10

Process

• Initial Pitch – you and one investor

• Full Pitch – you and the investor team

• VC will put together the initial term sheet (don’t negotiate against yourself)

• Get quality advice (advisors, attorneys, other founders)

• 2 term sheets are 5x better than 1

Negotiating the Term Sheet

11

Common Mistakes • Not understanding valuation (how it is calculated)

• Overplaying/underplaying your hand (not knowing your position)

• Getting caught in the weeds (missing the big picture)

• Getting star-struck by a big name

• Single Issue fixation

• Not looking down the road (Series A as a precedent for future rounds)

• Not respecting the process (relationship with potential investors)

• Pay attention to the no-shop (this matters)

Negotiating the Term Sheet

12

Key Terms • Valuation

• Control

• Exit Mechanics

• Everything Else (see Appendix)

Key Documents • Certificate of Incorporation

• Preferred Stock Purchase Agreement

• Investors’ Rights Agreement

• Voting Agreement

• Right of First Refusal and Co-Sale Agreement

Key Terms in Preferred Stock Financings

13

Where does the valuation come from?

• How much capital can the Company effectively use over 12-18 months?

• Target equity ownership.

• Similar companies (if any) as a comparison point.

• Fundraise / Target ownership = Pre-Money Valuation (shorthand).

Basic Calculation of Price Per Share

• Pre-money Valuation / Pre-money capitalization = Price Per Share

Key Terms - Valuation

14

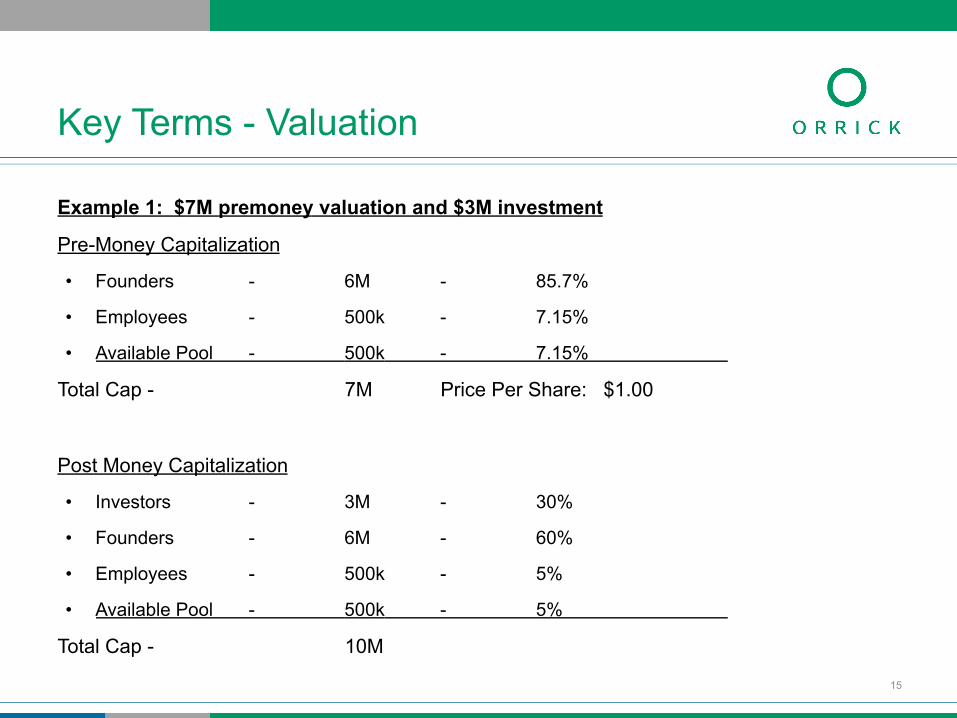

Example 1: $7M premoney valuation and $3M investment

Pre-Money Capitalization

• Founders - 6M - 85.7%

• Employees - 500k - 7.15%

• Available Pool - 500k - 7.15%

Total Cap - 7M Price Per Share: $1.00

Post Money Capitalization

• Investors - 3M - 30%

• Founders - 6M - 60%

• Employees - 500k - 5%

• Available Pool - 500k - 5%

Total Cap - 10M

Key Terms - Valuation

15

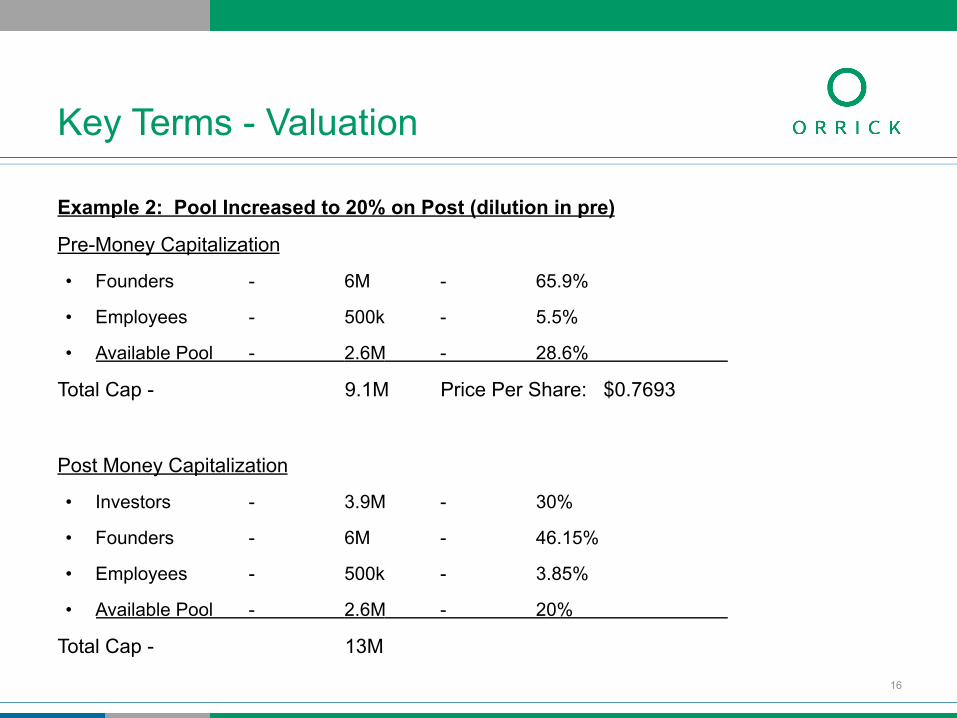

Example 2: Pool Increased to 20% on Post (dilution in pre)

Pre-Money Capitalization

• Founders - 6M - 65.9%

• Employees - 500k - 5.5%

• Available Pool - 2.6M - 28.6%

Total Cap - 9.1M Price Per Share: $0.7693

Post Money Capitalization

• Investors - 3.9M - 30%

• Founders - 6M - 46.15%

• Employees - 500k - 3.85%

• Available Pool - 2.6M - 20%

Total Cap - 13M

Key Terms - Valuation

16

Price Per Share Levers

• Pre-Money Valuation

• Pre-Money Capitalization – what goes into the denominator when calculating price per share in addition to outstanding shares (warrants, convertible notes, etc.)

• Option Plan Size

Key Terms - Valuation

17

Remember what you are selling.

• Common Stock v. Preferred Stock – What’s the difference?

• Separate Classes/Series have separate protections

How the Company is Controlled

• Board of Directors

• Voting Agreement

• Protective Provisions

Key Terms - Control

18

Board of Directors

• Board Composition (how many and who designates)

• Limitations on rights to designate board members:

» Minimum share holding

» Employment with the Company

• Voting Agreement – obligates all stockholders to vote for the designees of specific stockholders

• Board Observer Rights

Key Terms - Control

19

Protective Provisions • Company must receive consent of Preferred holders (majority or super majority)

for the following actions (differs from Company to Company): » Authorize/Issue new Preferred Stock » Amending the terms of the existing Preferred Stock » Grant options beyond a certain limit » Amend the certificate of incorporation » Sell the Company – exit events » Additional Debt » Change in the Business » Key Hires » Acquisitions of other Companies

Key Terms - Control

20

Protective Provisions

• Focus on the voting threshold (whose consent do you need).

• Watch out for Veto Power held by multiple stockholders.

• Consider Board Carve-Outs (i.e. if unanimous board approves, separate stockholder consent not required).

• Protective Provisions can slow the management of the Company.

Key Terms - Control

21

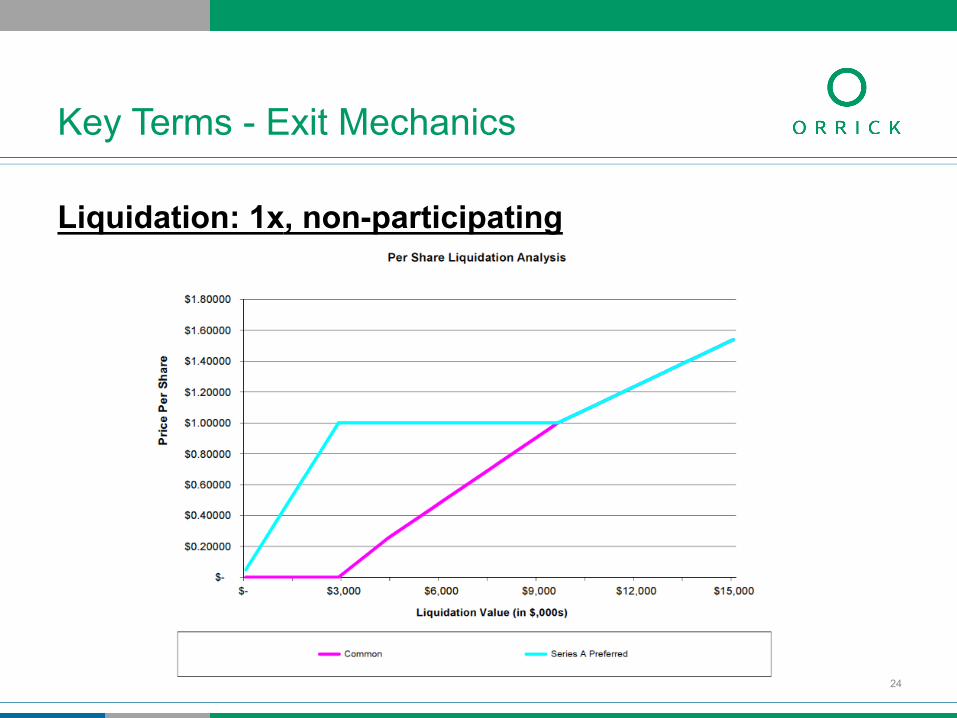

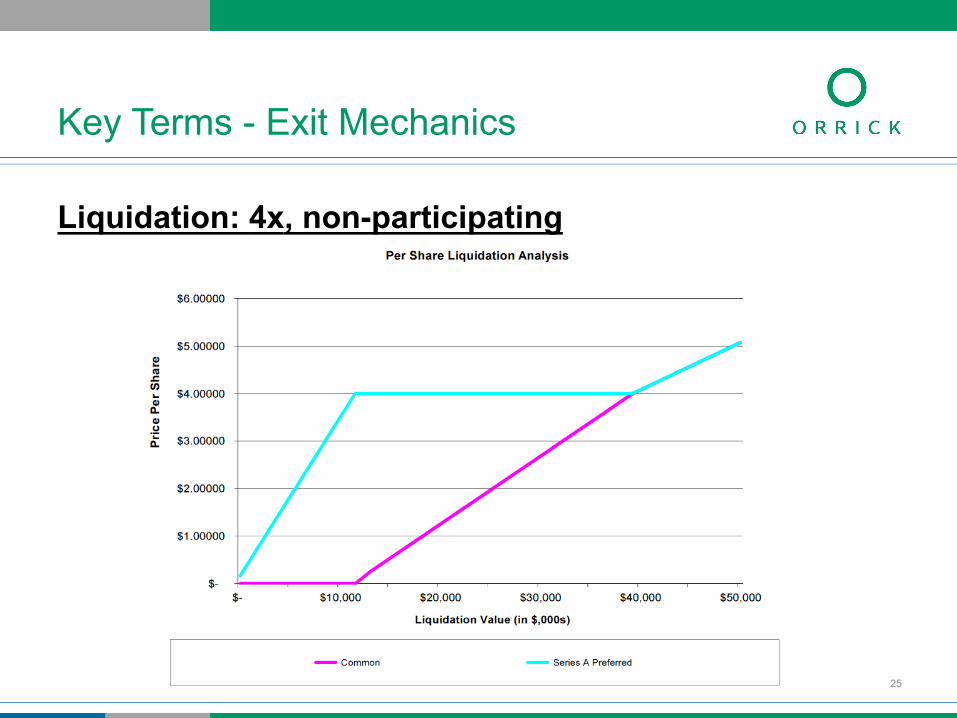

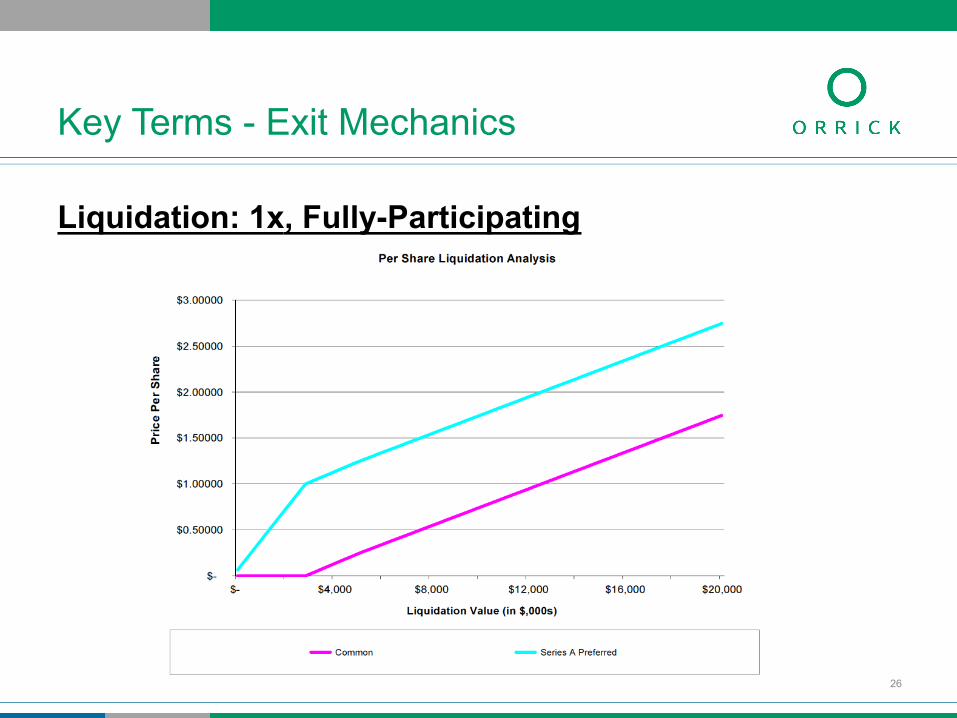

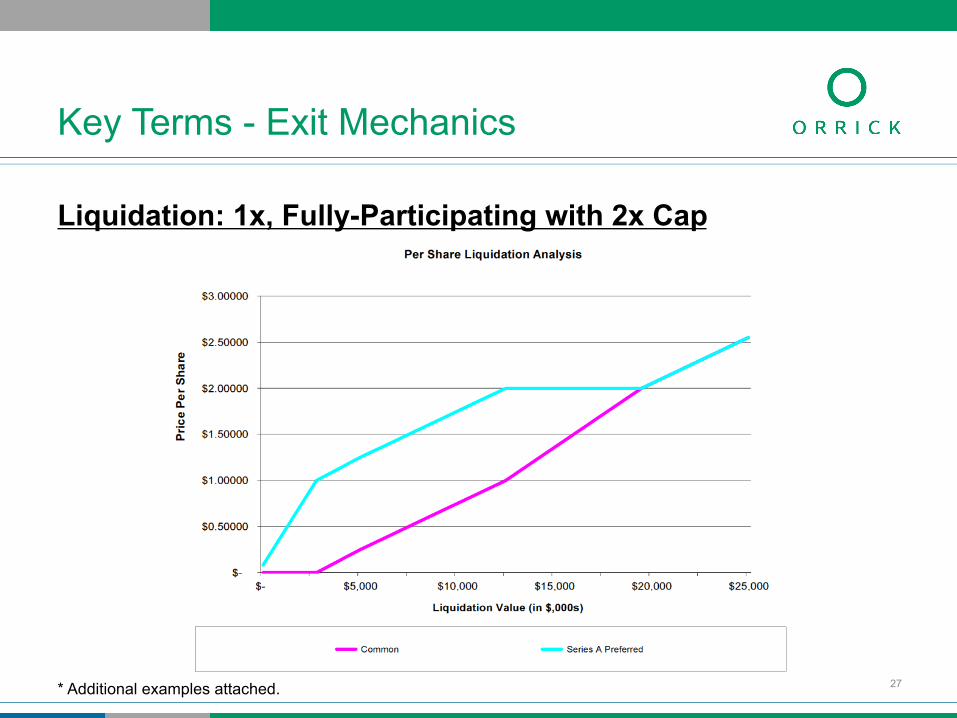

Liquidation Preference

• Paid on a Change of Control (merger, asset sale or other liquidation).

• “Preference” – they get paid first (down-side protection).

• “Participation” – Having your cake and eating it too.

• Cap on Participation – limiting the damage.

• Think through the potential exit scenarios and try to get incentives to line up as much as possible (minimize the “Zone of Indifference”)

Key Terms - Exit Mechanics

22

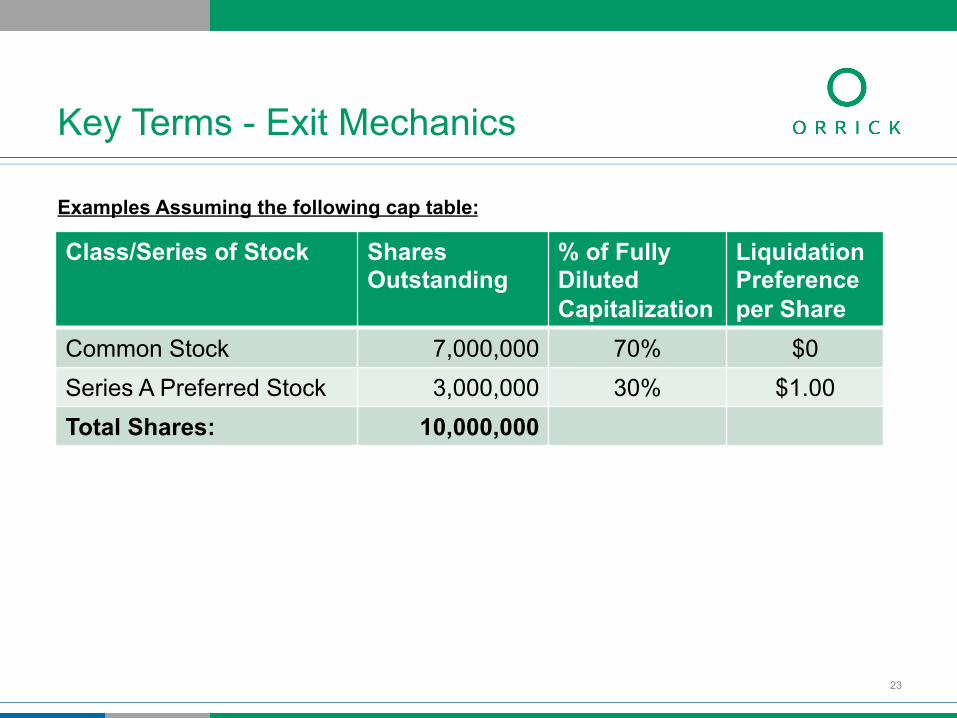

Examples Assuming the following cap table:

Key Terms - Exit Mechanics

23

Class/Series of Stock Shares Outstanding

% of Fully Diluted Capitalization

Liquidation Preference per Share

Common Stock 7,000,000 70% $0 Series A Preferred Stock 3,000,000 30% $1.00 Total Shares: 10,000,000

Key Terms - Exit Mechanics

Liquidation: 1x, non-participating

24

Key Terms - Exit Mechanics

Liquidation: 4x, non-participating

25

Key Terms - Exit Mechanics

Liquidation: 1x, Fully-Participating

26

Key Terms - Exit Mechanics

Liquidation: 1x, Fully-Participating with 2x Cap

27 * Additional examples attached.

Liquidation Control

• Board Control (Board must approve all exits)

• Protective Provisions

• Drag-Along Right. Forcing other stockholders to consent to a sale of the Company

» Who is dragging? (Triggers for activating the drag along)

» Who is being dragged?

» Conditions for enforcing the drag along (restrictions)

• Unwritten control of the Founders – IF the founder is still at the Company

Key Terms - Exit Mechanics

28

Timing of a Deal • Getting to know the investors: 3-6 months

• Investor diligence and investigation period: 2-4 weeks

• Term Sheet negotiation: 1-2 weeks

• Definitive Document Negotiation and Drafting: 2-4 weeks

• Closing and Funding: 2-5 days

The Process – Getting to Close

29

How to Close a Deal Fast • Prepare Now

» Organize your documents

» Flag issues that will need to be discussed / disclosed

• Focus on the Right Things » Key business terms

» Relationships (Social Capital)

• Respond to questions/inquiries promptly

• Prepare your Board / Stockholders / Noteholders for what is coming

• Coordinate schedules ahead of time

• Use a checklist.

The Process – Getting to Close

30

Action Items to Take Today • Take Inventory – figure out where your weak spots are

• Increase Human and Social Capital » Get the right co-founders (diversity of skill sets and backgrounds)

» Networking (investors, partners, service providers)

• Develop your product

• Put together your timeline (business plan – this is meant to by dynamic)

• Create an Executive Summary (1 page summary of the Company)

• Get corporate documents in order

Next Steps – What to do Now

31

Joseph Z. Perkins, a partner in Orrick's Silicon Valley office, is a member of the Technology Companies Group, which advises emerging companies and venture capital firms. Mr. Perkins focuses his practice on providing private venture financing and merger and acquisition services to Internet, high tech, and clean technology companies in the United States and Japan.

Some of Mr. Perkins's current and former clients include the following.

• Bleacher Report (Sports media; acquired by Turner Broadcasting) • Doki Doki (Stealth) • FOVE (Virtual Reality Hardware) • Getaround (Car sharing community) • Instagram (Photo social media; acquired by Facebook) • iSpace (Robotics) • Life360 (Family connectivity and safety) • Orchestra - aka Mailbox (e-mail management; acquired by Dropbox) • Ooma (VoiP hardware) • Pinterest (Social Media) • PowerSet (Search; acquired by Microsoft) • Social Finance (Social Lending) • UniversityNow (Online education) • WHILL (Personal Mobility) • Xobni Corporation (e-mail and contact management; acquired by Yahoo)

Joseph Z. Perkins

33

Education • J.D., Harvard Law School • B.S., summa cum laude,

Philosophy, University of Utah

• B.A., summa cum laude, Japanese, University of Utah

Admitted In

• California

Honors

• Phi Beta Kappa

Technology Companies Group

Silicon Valley

Contact

+1 (650) 289-7188 [email protected]

34

Appendix

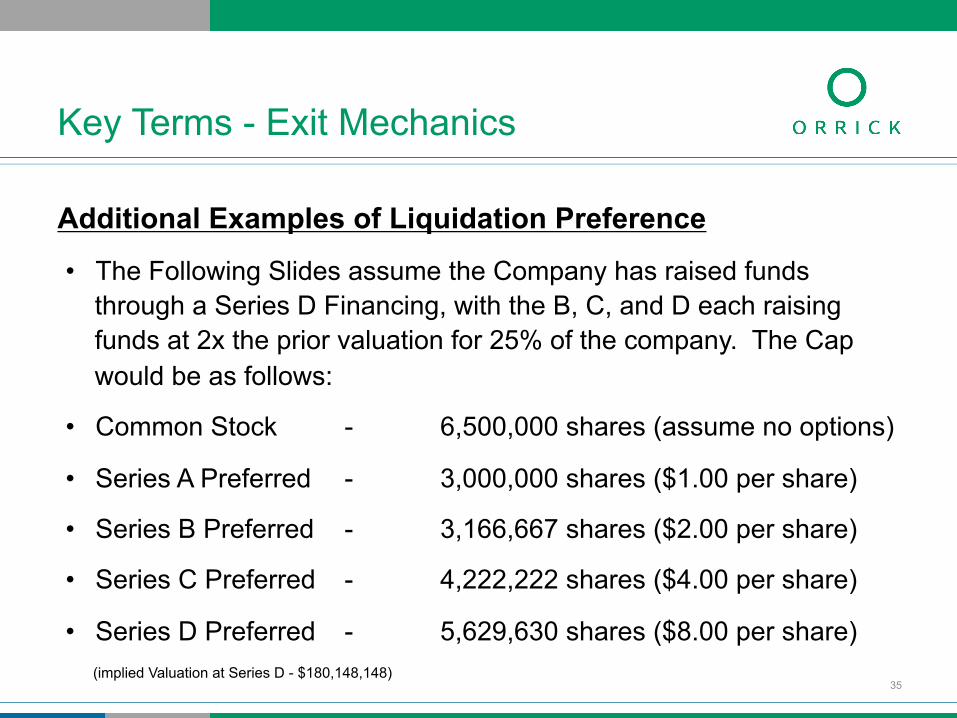

Additional Examples of Liquidation Preference

• The Following Slides assume the Company has raised funds through a Series D Financing, with the B, C, and D each raising funds at 2x the prior valuation for 25% of the company. The Cap would be as follows:

• Common Stock - 6,500,000 shares (assume no options)

• Series A Preferred - 3,000,000 shares ($1.00 per share)

• Series B Preferred - 3,166,667 shares ($2.00 per share)

• Series C Preferred - 4,222,222 shares ($4.00 per share)

• Series D Preferred - 5,629,630 shares ($8.00 per share) (implied Valuation at Series D - $180,148,148)

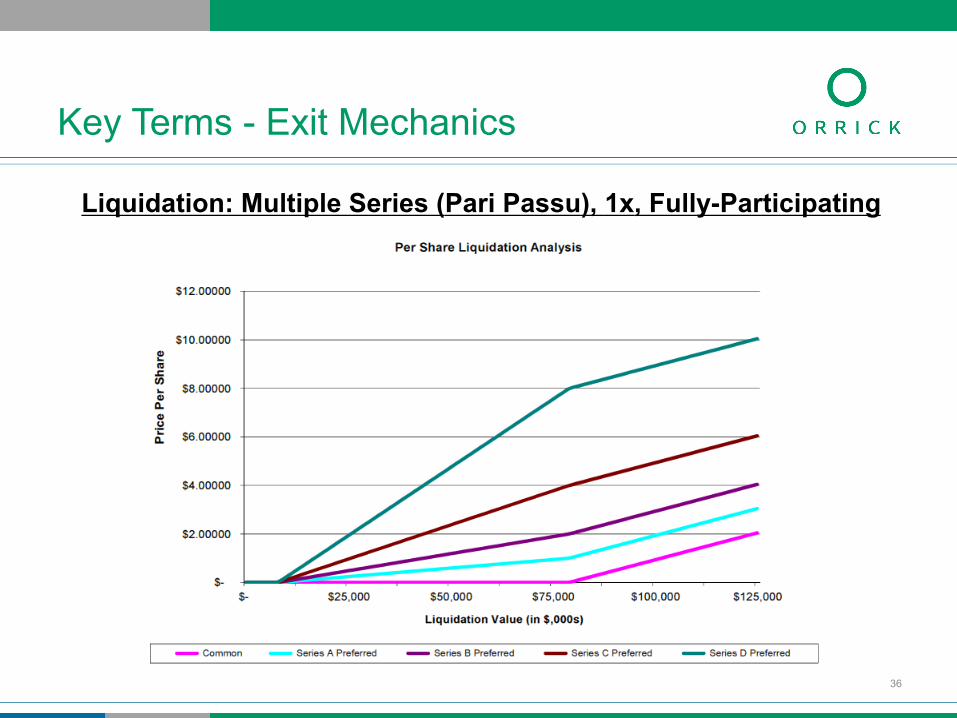

Key Terms - Exit Mechanics

35

Key Terms - Exit Mechanics

Liquidation: Multiple Series (Pari Passu), 1x, Fully-Participating

36

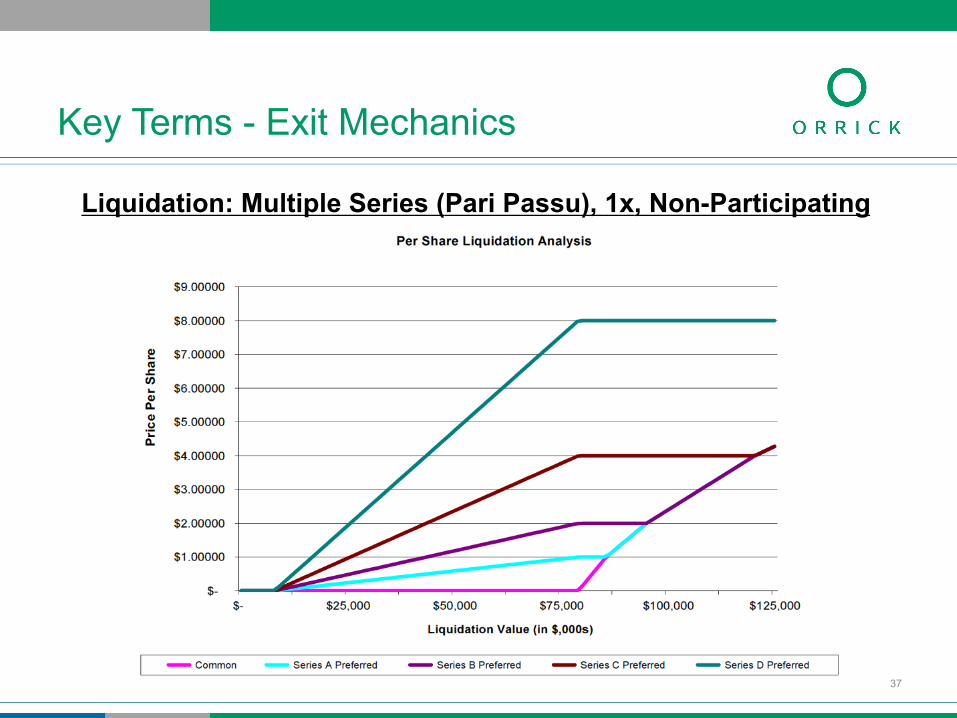

Key Terms - Exit Mechanics

Liquidation: Multiple Series (Pari Passu), 1x, Non-Participating

37

Key Terms - Exit Mechanics

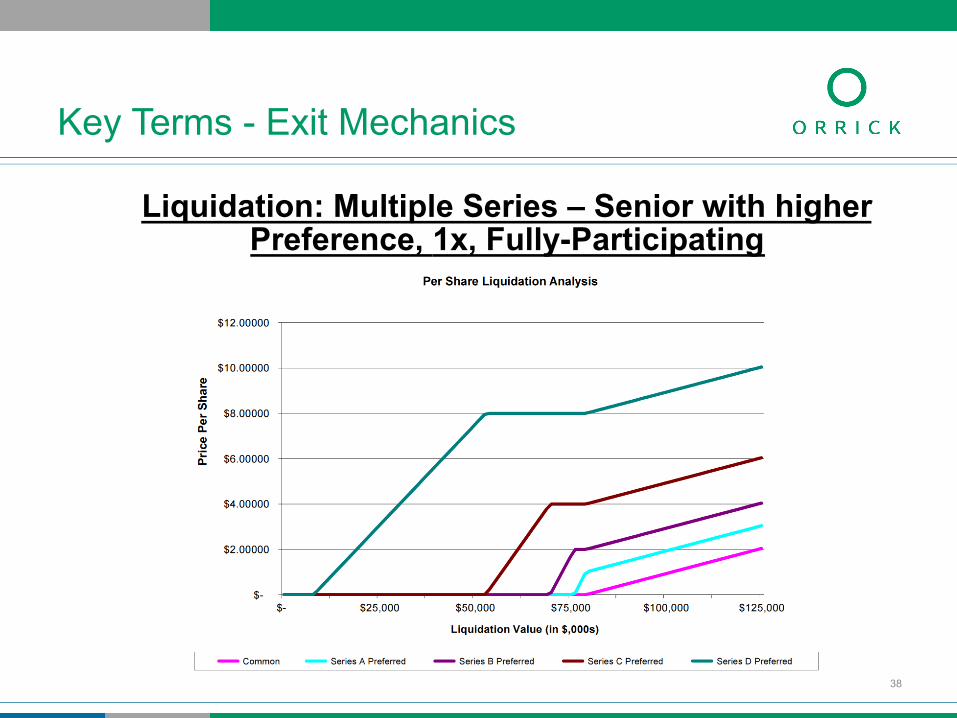

Liquidation: Multiple Series – Senior with higher Preference, 1x, Fully-Participating

38

Dividend

• Cumulative vs. non-cumulative dividends

• Generally, non-cumulative dividends are never paid as they are payable only “when and if declared by the Board of Directors”

• Generally set around 6.0%-8.0% per annum – can be used in redemption provisions

• Cumulative may be treated as debt for accounting

Key Terms - Everything Else

39

Redemption Rights (not common)

• Force the Company to repurchase the Preferred Stock

• Return is often similar to liquidation preference or original purchase price but with a hurdle

» Timing for redemption – the further out the better (5-7 years)

» Triggers for calling a redemption – the more difficult the better

» Installments – the more the merrier

» May Trigger Debt Treatment for Accounting

Key Terms - Everything Else

40

Conversion

• Optional Conversion

» Preferred stock is convertible into common stock at any time at the option of the holder.

• Mandatory Conversion

» Triggers for mandatory conversion – IPO or vote by the preferred stock

» Percent preferred vote necessary to trigger conversion

» Watch out for series block

Key Terms - Everything Else

41

Anti-dilution Provisions If you sell stock at a lower price in the future

• Full ratchet vs. weighted average anti-dilution adjustment

• Broad based vs. narrow based weighted average anti-dilution adjustment

• Exceptions for Non-Financing Offerings

» Stock Options (watch for caps)

» JV and Commercial Agreement

» Stock issued in connection with Bank Debt

» Waivable by % of Preferred

Key Terms - Everything Else

42

Voting

• Preferred Votes with Common Stock on all matters on an as-converted to Common Stock basis. (Note the 242.b.2 waiver on authorized Common Stock changes)

Pay to Play

• Triggers for activating the pay to play

• Consequences for failure to pay

Key Terms - Everything Else

43

Registration Rights

• Common Rights – Don’t spend too much time on this

• Demand registration = forcing function for your company to go public

• S-3 registration = short form registration for eligible issuers

• Piggyback registration = investors tagging along company registration

• Lock-up = absolutely necessary for company to retain underwriters

Key Terms - Everything Else

44

Information Rights

• Common Rights – Don’t spend too much time on this

• Reserved for “Major Investors”

• Financial statements –

» annual, quarterly, monthly; audited vs. unaudited

» budget

» cap table

• Visitation rights – conditions for exclusion

Key Terms - Everything Else

45

Pre-emptive Rights (Participation Rights)

• Right of investors to maintain ownership %

• Standard Right for “Major Investors”

• Calculation of pro rata share (what to include in denominator)

• Excluded issuances (Carve-outs)

• Accredited Investor Requirement

• Lose if they don’t exercise?

Key Terms - Everything Else

46

Negative Covenants

• Ordinary course of business items vs. extraordinary events

• Dollar threshold

Affirmative Covenants

• Non-compete, non-solicit, non-disclosure and inventions assignment

• Board matters (frequency of meetings, reimbursement, etc.)

• Option vesting

• Key person and D&O insurance

Key Terms - Everything Else

47

Founder Restrictions (ROFR and Co-Sale)

• Right of First Refusal and Co-Sale on Sale of Stock of Founders and Existing Stockholders

» Restricted parties

» Participants

» Excluded transfers (carve-outs)

• “Reverse vesting”

• Customary Terms for Founders - best to have in place prior to deal

» 4 year vesting with credit for time served with double trigger acceleration on change of control and termination without cause

Key Terms - Everything Else

48

Other Terms • No Shop

» Restriction period and relationship to anticipated closing date

» Restricted activities

• Closing Conditions » All Consultants/Employees Sign CIIAA

» Employment/Vesting Agreements with Founders (structures exit of Founder)

» Legal Opinion

» Key Common Holders all signing Voting and ROFR Agreement

» Amendment of Charter

» Representations True and Correct

Key Terms - Everything Else

49