Towers Watson of equity-based compensation programmes 3 A commonly used performance measure for long...

4

Towers Watson Valuation of equity-based compensation programmes

Transcript of Towers Watson of equity-based compensation programmes 3 A commonly used performance measure for long...

Towers Watson Valuation of equity-based compensation programmes

2 towerswatson.com

Introduction

Many listed companies in Europe operate an equity-based long term incentive plan for their board members / senior management. These plans include for example performance share plans, (performance) option plans and phantom cash plans.

According to the “IFRS 2 Share-based payments” rules, all these types of equity-based payment transactions should (at least) be valued at the moment of grant and subsequently recognised in the Profit & Loss statement during the vesting period.

Towers Watson is highly specialised in the valuation of complex equity-based compensation programmes, for clients of all sizes and operating in all types of businesses. Our clients use our valuation results not only for accounting purposes, but also for broader remuneration purposes – such as for the determination of grant levels or unwinding equity-based compensation programmes at termination.

Our approach

The valuation of equity-based compensation programmes requires a specialised understanding of the applicable regulations, financial instruments and derivatives, financial and actuarial modeling and executive compensation programmes strategy and design. Towers Watson has a team of highly qualified staff, who have an in-depth knowledge of the valuation of financial instruments and the mathematical and actuarial aspects of the underlying models and designs.

To execute reliable and robust valuations of equity-based long term incentive plans, it is induced by the IFRS 2 rules to follow the steps as described below:

• Discussion on valuation method and input parameters;

• Approval (by the external auditor) of the selected approach and input parameters;

• Executing the fair value calculations; • ‘Sign off’ by the external auditor.

Towers Watson can provide assistance on all of the steps described above and be a partner with the client during the whole valuation process. The main benefits of working with Towers Watson include:

• Knowledge Towers Watson is forged from decades of experience, innovation and a client-first philosophy. Over all these years of experience, Towers Watson has built extensive knowledge and edge-cutting tools for complex challenges (among others within the field of valuation of equity-based compensation programmes), based on an analytical approach. Towers Watson’s DNA to find answers to new challenges, gives us a kick-start at helping our clients on complex issues.

• Taking care of the full process Towers Watson is able to take care of the full process regarding the valuation of equity-based compensation programmes: Towers Watson helps clients to select the most appropriate approach for each valuation and helps to optimise valuation results by applying a tailored valuation model. Based on the valuation, Towers Watson is able to determine the final accounting charge, discuss the valuation with the auditor and is able to draft the section of the remuneration report on equity based compensation programmes (including disclosure tables).

• Local focus Towers Watson has a valuation team located in each country, which gives our clients the advantage of a local contact and local expertise and thus an efficient process. Although locally focused, the teams are able to profit from international deep expertise as Towers Watson has a truly global reach, helping our clients beyond their headquarters and throughout their global operations. This includes for example the valuation of equity-based compensation programmes of organisations running plans in multiple geographies.

Valuation of equity-based compensation programmes

Valuation of equity-based compensation programmes 3

A commonly used performance measure for long term incentive plans is relative Total Shareholder Return (TSR) – the measurement of stock price growth plus reinvested dividends over a specified time period, relative to an index or group of peer companies.

Towers Watson is able to provide assistance in monitoring performance of equity-based compensation programmes based on Total Shareholder Return. Towers Watson provides

An analysis to determine TSR performance and outcomes for compensation purposes, based on a cost-effective approach. The results of the analyses can be used to determine expected or final vesting and for communication purposes.

Monitoring performance plans Measuring Total Shareholder Return

• Our experience in the field of executive compensation Towers Watson is the world’s largest executive compensation consultant. Towers Watson is highly specialised in the design of equity-based long term incentive programmes in the context of each organisation’s business and reward strategy – including designing programme characteristics, identifying suitable performance metrics, setting performance targets and calibrating programmes.

Our Services

The valuation of equity-based compensation programmes requires sophisticated financial modeling. Essentially, Towers Watson determines the fair value by trying to estimate the price the market would give for the equity-based payment, given the specific terms and conditions upon which the instruments were granted. To estimate this market price, Towers Watson uses a broad range of well-established approaches. Towers Watson helps clients to select the most appropriate approach for each valuation and helps to optimise valuation results by assisting in determining the most optimal input parameters and applying a tailored valuation model. These valuation techniques include various approaches:

• Monte Carlo simulation; • Black Scholes / Binomial Option Pricing Model; • Scenario modelling (Monte Carlo Simulation).

Contact

To discuss the valuation of equity-based compensation programmes for your company, or in case of any questions, please do not hesitate to contact your executive compensation consultant.

towerswatson.com

About Towers WatsonTowers Watson is a leading global professional services company

that helps organisations improve performance through effective

people, financial and risk management. With 14,000 associates

around the world, we offer solutions in the areas of employee

benefit programmes, talent and reward programmes, and risk and

capital management.

Copyright © 2012 Towers Watson. All rights reserved.TW-NL-2012-27228

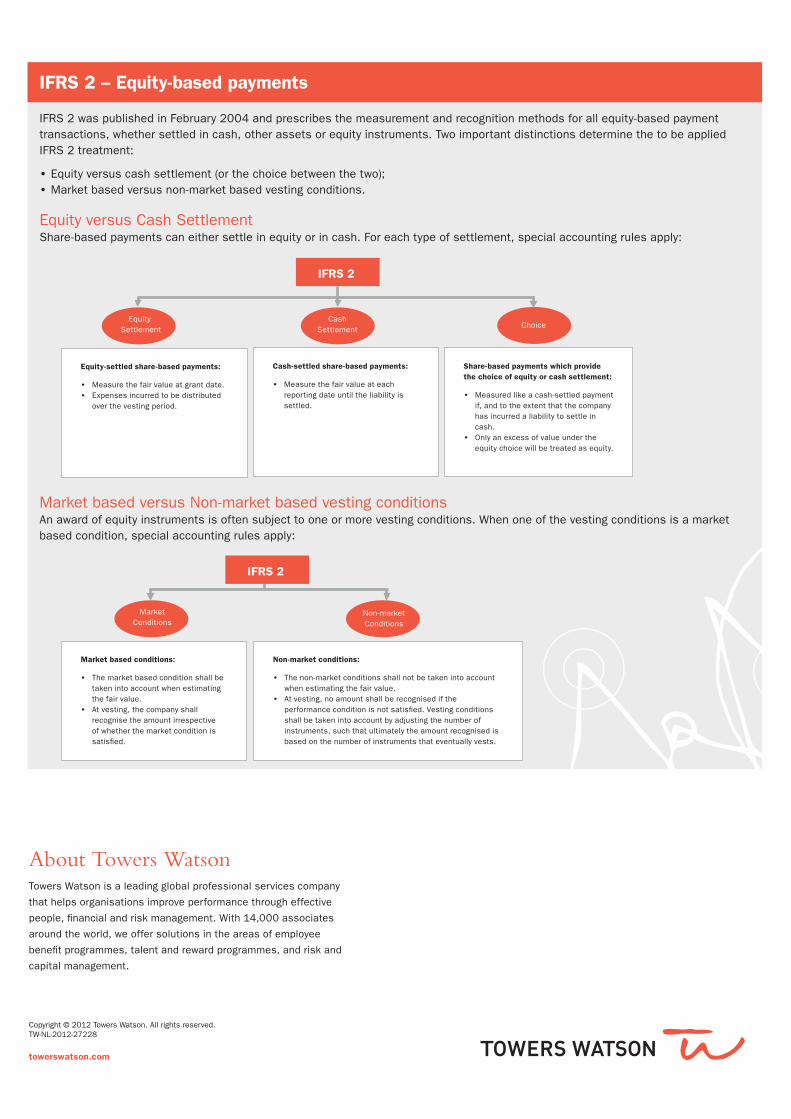

IFRS 2 was published in February 2004 and prescribes the measurement and recognition methods for all equity-based payment transactions, whether settled in cash, other assets or equity instruments. Two important distinctions determine the to be applied IFRS 2 treatment:

• Equity versus cash settlement (or the choice between the two); • Market based versus non-market based vesting conditions.

Equity versus Cash Settlement Share-based payments can either settle in equity or in cash. For each type of settlement, special accounting rules apply:

Market based versus Non-market based vesting conditions An award of equity instruments is often subject to one or more vesting conditions. When one of the vesting conditions is a market based condition, special accounting rules apply:

IFRS 2 – Equity-based payments

IFRS 2

Equity Settlement

Cash Settlement Choice

Cash-settled share-based payments:

• Measure the fair value at each reporting date until the liability is settled.

Share-based payments which provide the choice of equity or cash settlement:

• Measured like a cash-settled payment if, and to the extent that the company has incurred a liability to settle in cash.

• Only an excess of value under the equity choice will be treated as equity.

Equity-settled share-based payments:

• Measure the fair value at grant date. • Expenses incurred to be distributed

over the vesting period.

Market Conditions

Non-market Conditions

Non-market conditions:

• The non-market conditions shall not be taken into account when estimating the fair value.

• At vesting, no amount shall be recognised if the performance condition is not satisfied. Vesting conditions shall be taken into account by adjusting the number of instruments, such that ultimately the amount recognised is based on the number of instruments that eventually vests.

Market based conditions:

• The market based condition shall be taken into account when estimating the fair value.

• At vesting, the company shall recognise the amount irrespective of whether the market condition is satisfied.

IFRS 2