The Use of Oligopoly Equilibrium for Economic and Policy Applications Jim Bushnell, UC Energy...

43

The Use of Oligopoly Equilibrium for Economic and Policy Applications Jim Bushnell, UC Energy Institute and Haas School of Business

-

date post

20-Dec-2015 -

Category

Documents

-

view

215 -

download

1

Transcript of The Use of Oligopoly Equilibrium for Economic and Policy Applications Jim Bushnell, UC Energy...

The Use of Oligopoly Equilibrium

for Economic and Policy Applications

Jim Bushnell, UC Energy Institute and Haas School of Business

A Dual Mission

• “Research Methods” - how oligopoly models can be used to tell us something useful about how markets work– Potentially very boring

• What makes electricity markets work (or not)?– Blackouts, Enron, “manipulation,” etc.– A new twist on how we think about vertical

relationships– Potentially very exciting

Oligopoly Models

– Large focus on theoretical results– Simple oligopoly models provide the

“structure” for structural estimation in IO

– Seldom applied to large data sets of complex markets• Some markets feature a wealth of detailed

data• Optimization packages make calculation of

even complex equilibria feasible

A Simple Oligopoly Model

• Concentration measures

where m is Cournot equilibrium margin.

HHI s i2

i

qi

Q

2

i

m p MC

p

1

n

HHI

Surprising Fact: Oligopoly models can tell us

something about reality• Requires careful consideration about the

institutional details of the market environment – Incentives of firms (Fringe vs. Oligopoly)– Physical aspects of production (transmission)– Vertical & contractual arrangements

• Recent research shows actual prices in several electricity markets reasonably consistent with Cournot prices

• Cournot models don’t have to be much more complicated than HHI calculations

b

nqap

bcn

bkaq i

i

,1

Empirical Applications

• Analysis of policy proposals– Prospective analysis of future market– Merger review, market liberalization, etc.

• Market-level empirical analysis– Retrospective analysis of historic market– Diagnose sources of competition problems– Simulate potential solutions

• Firm-level empirical analysis– Estimate costs or other parameters (contracts)– Evaluate optimality of firm’s “best” response– Potentially diagnose collusive outcomes

Oligopoly equilibrium models

• Cournot – firms set quantities– many variations

• Supply-function – firms bid p-q pairs– infinite number of functional forms– Range of potential outcomes is bounded by

Cournot and competitive– Capacity constraints, functional form

restrictions reduce the number of potential equilibria

• Differentiated products models (Bertrand)

Green and Newbery (1992)

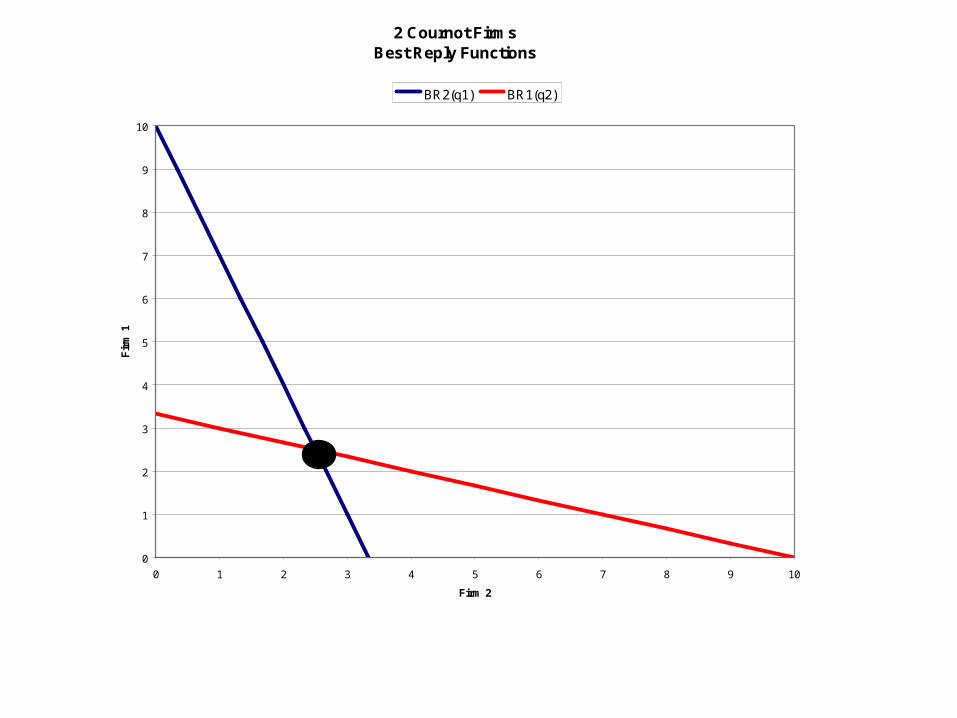

Simple Example

• 2 firms, c(q) = 1/2 qi 2, c = mc(q) = qi

• Market supply = Q = q1 + q2

• Linear demand Q = a-b*p = 10 – p• NO CAPACITY CONSTRAINTS

3

10

2)(

0)2(

5.)( 2

jjiji

iji

i

i

iiji

i

q

b

qaqqBR

qb

qqa

q

qqb

qqa

2 Cournot FirmsBest Reply Functions

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6 7 8 9 10

Firm 2

Fir

m 1

BR2(q1) BR1(q2)

Three Studies of Electricity

• Non-incremental regulatory and structural changes– Historic data not useful for predicting future behavior

• Large amounts of cost and market data available– High frequency data - legacy of regulation

• Borenstein and Bushnell (1999)– Simulation of prospective market structures

• Focus on import capacity constraints

• Bushnell (2005)– Simulation using actual market conditions

• Focus on import elasticities

• Bushnell, Saravia, and Mansur (2006)– Simulation of several markets

12

Western Regional Markets

• Path from NW to northern California rated at 4880 MW

• Path from NW to southern California rated at 2990 MW

• Path from SW to southern California rated at 9406 MW (W-O-R constraint)

• 408 MW path from northern Mexico and 1920 MW path from Utah

13

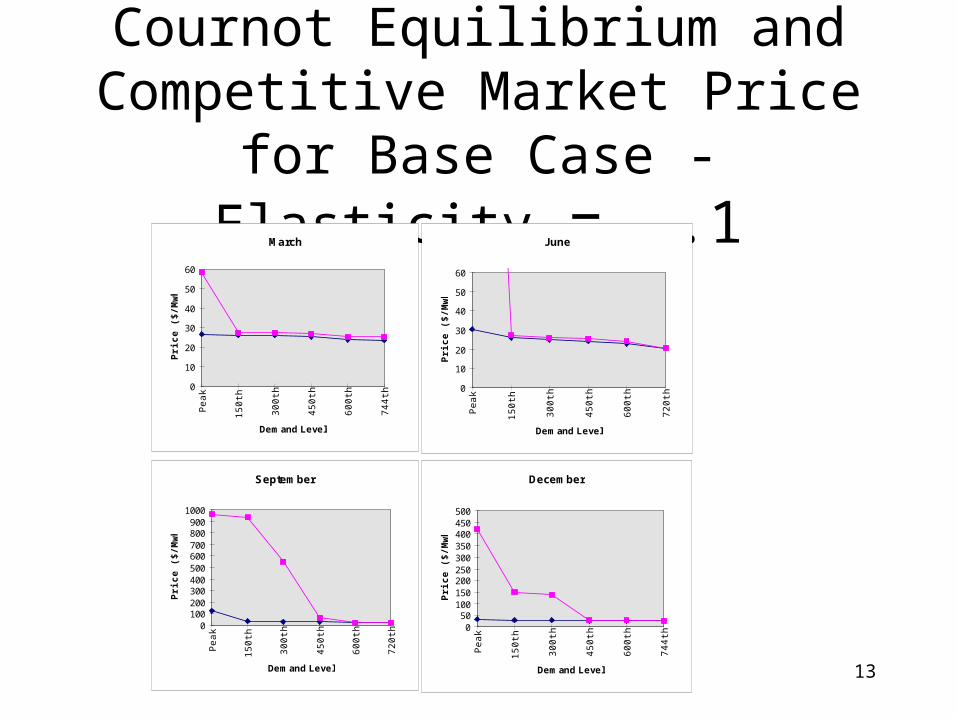

Cournot Equilibrium andCompetitive Market Price for Base Case - Elasticity = -.1

March

0

10

20

30

40

50

60

Pe

ak

15

0th

30

0th

45

0th

60

0th

74

4th

Demand Level

Pri

ce

($

/Mw

h)

June

0

10

20

30

40

50

60

Pe

ak

15

0th

30

0th

45

0th

60

0th

72

0th

Demand Level

Pri

ce

($

/Mw

h)

September

0100200300400500600700800900

1000

Pe

ak

15

0th

30

0th

45

0th

60

0th

72

0th

Demand Level

Pri

ce

($

/Mw

h)

December

050

100150200250300350400450500

Pe

ak

15

0th

30

0th

45

0th

60

0th

74

4th

Demand Level

Pri

ce

($

/Mw

h)

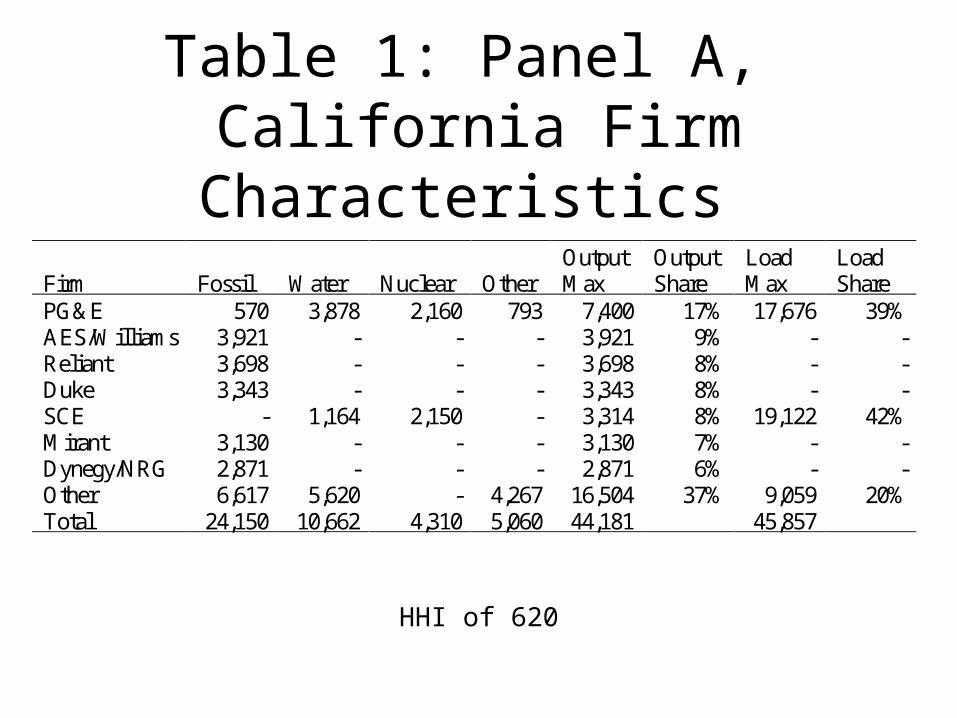

Table 1: Panel A, California Firm Characteristics

HHI of 620

Output Output Load Load Firm Fossil Water Nuclear Other Max Share Max Share PG&E 570 3,878 2,160 793 7,400 17% 17,676 39% AES/Williams 3,921 - - - 3,921 9% - - Reliant 3,698 - - - 3,698 8% - - Duke 3,343 - - - 3,343 8% - - SCE - 1,164 2,150 - 3,314 8% 19,122 42% Mirant 3,130 - - - 3,130 7% - - Dynegy/NRG 2,871 - - - 2,871 6% - - Other 6,617 5,620 - 4,267 16,504 37% 9,059 20% Total 24,150 10,662 4,310 5,060 44,181 45,857

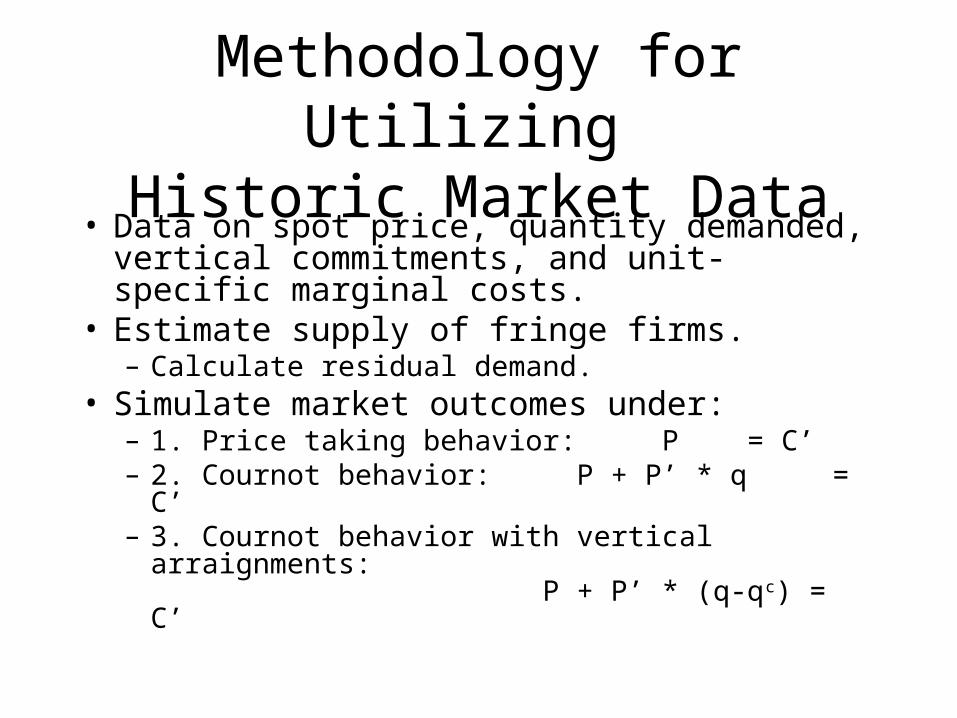

Methodology for Utilizing Historic Market Data

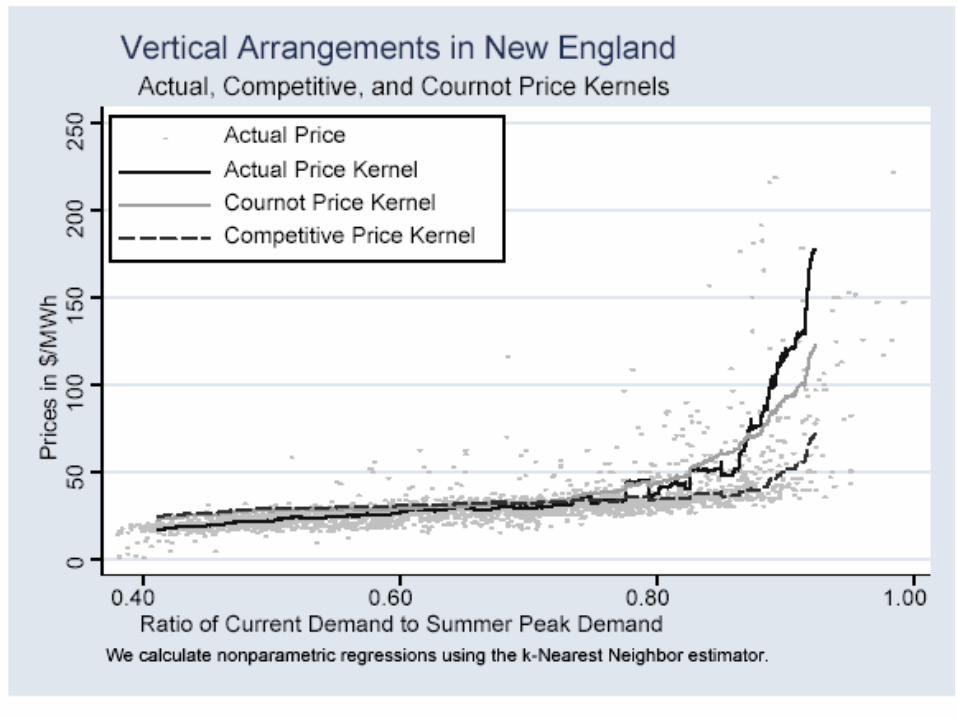

• Data on spot price, quantity demanded, vertical commitments, and unit-specific marginal costs.

• Estimate supply of fringe firms.– Calculate residual demand.

• Simulate market outcomes under:– 1. Price taking behavior: P =

C’– 2. Cournot behavior: P + P’ * q = C’– 3. Cournot behavior with vertical

arraignments: P + P’ * (q-qc) = C’

Modeling Imports and Fringe

• Source of elasticity in model• We observe import quantities, market price, and weather

conditions in neighboring states• Estimate the following regression using 2SLS (load as

instrument)

9

6 1

7 24

2 2

ln( )S

fringet i it t s st

i s

j jt h ht tj h

q Month p Temp

Day Hour

• Estimates of price responsiveness are greatest in California (>5000) relative to New England (1250) and PJM (850)

Residual Demand function

ttt

actualt

actualtt

Qp

pQ

exp

)ln(

• The demand curve is fit through the observed price and quantity outcomes.

mean mean meanobservations Cournot PX Competitive

price ($/MWh) price ($/MWh) price ($/MWh)June 699 127.93 122.29 52.67July 704 131.84 108.60 60.27August 724 185.02 169.16 79.14September 696 116.26 116.64 75.12

Table 1: Cournot Simulation and Actual PX Prices - Summer 2000

Simulation ResultsCalifornia 2000

01

00

20

03

00

40

0co

urn

ot/

PX

_p

rice

/co

mp

etit

ive

0 5000 10000 15000dem_cal

cournot PX_price

competitive

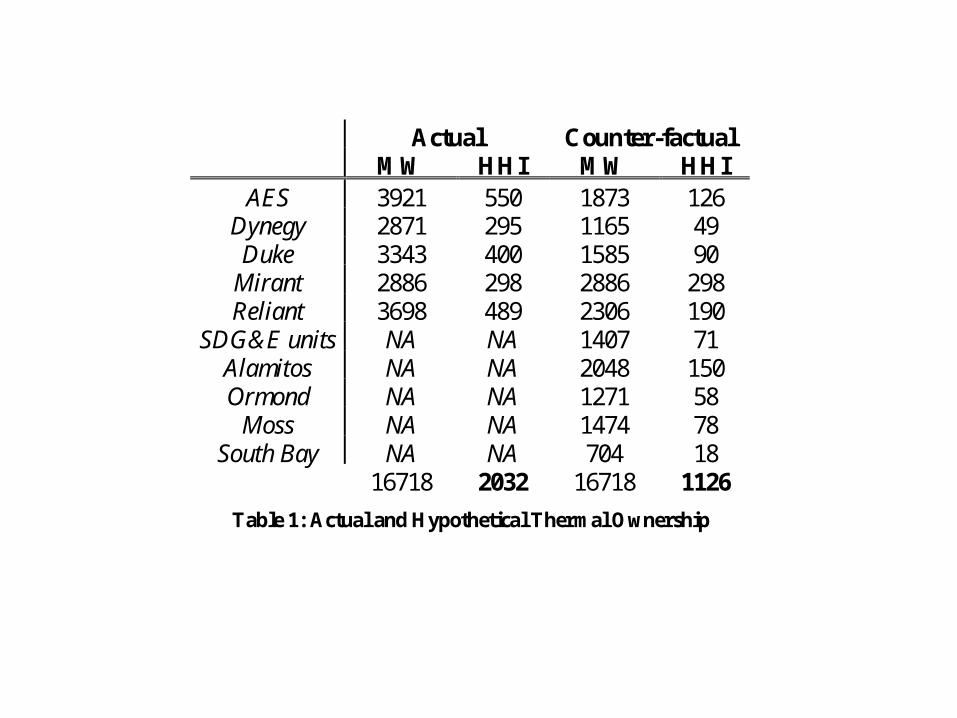

Actual Counter-factualMW HHI MW HHI

AES 3921 550 1873 126Dynegy 2871 295 1165 49Duke 3343 400 1585 90

Mirant 2886 298 2886 298Reliant 3698 489 2306 190

SDG&E units NA NA 1407 71Alamitos NA NA 2048 150Ormond NA NA 1271 58

Moss NA NA 1474 78South Bay NA NA 704 18

16718 2032 16718 1126

Table 1: Actual and Hypothetical Thermal Ownership

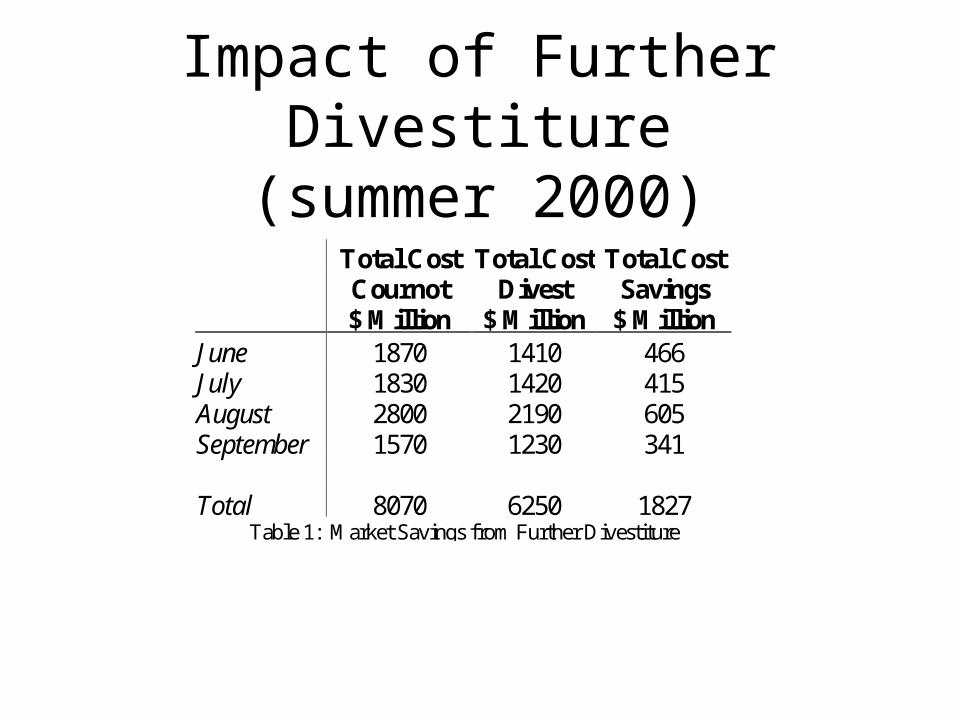

Total Cost Total Cost Total CostCournot Divest Savings$ Million $ Million $ Million

June 1870 1410 466July 1830 1420 415August 2800 2190 605September 1570 1230 341

Total 8070 6250 1827Table 1: Market Savings from Further Divestiture

Impact of Further Divestiture

(summer 2000)

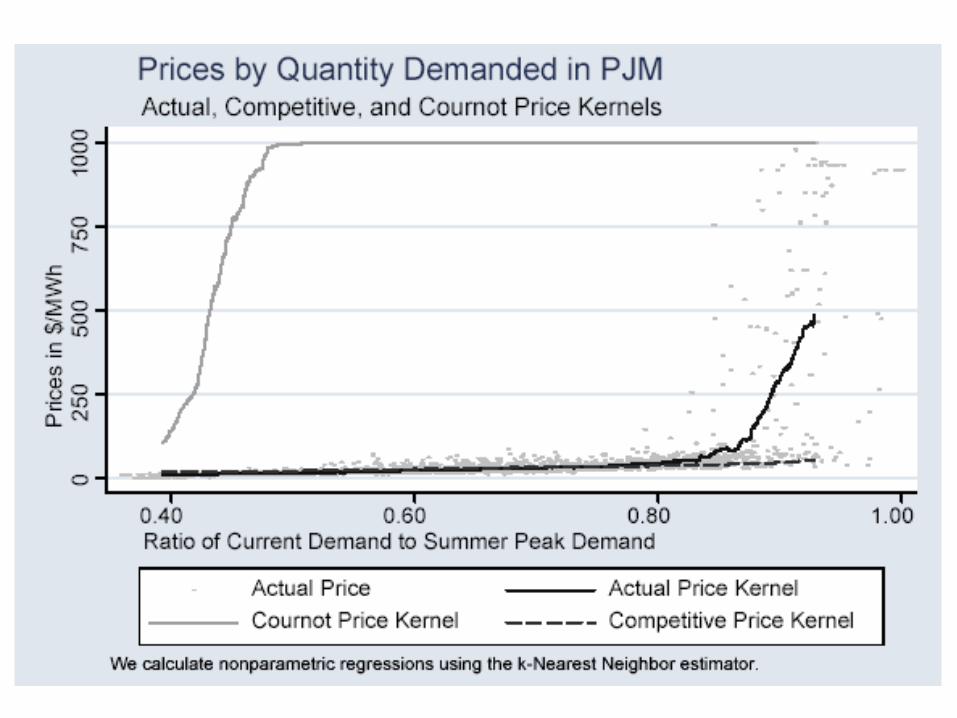

September 2000 Cournot Prices

0.00

50.00

100.00

150.00

200.00

250.00

300.00

0 2000 4000 6000 8000 10000 12000 14000 16000 18000

Residual Demand

Pri

ce (

$/M

Wh

)

Simple Cournot actual non-linear cournot

The Effect of Forward Contracts

• Contract revenue is sunk by the time the spot market is run– no point in withholding output to drive up a price

that is not relevant to you• More contracts by 1 firm lead to more spot

production from that firm, less from others• More contracts increase total production

– lower prices• Firms would like to be the only one signing

contracts, are in trouble if they are the only ones not signing contracts– prisoner’s dilemma

Simple Example

– 2 firms, c(q) = 1/2 qi 2, c = mc(q) = qi

– Market supply = Q = q1 + q2

– Linear demand Q = a-b*p = 10 – p– NO CAPACITY CONSTRAINTS

– Firm 2 has contracts for quantity qc2

3

10

2)(

0)2(

5.)(

2121212

2212

2

2

2222

122

cc

c

c

b

qqaqqBR

qb

qqqa

q

qqqb

qqa

2 Cournot FirmsBest Reply Functions

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6 7 8 9 10

Firm 2

Fir

m 1

BR2(q1) BR1(q2)

2 Cournot FirmsBest Reply Functions

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6 7 8 9 10

Firm 2

Fir

m 1

BR2(q1) BR1(q2)

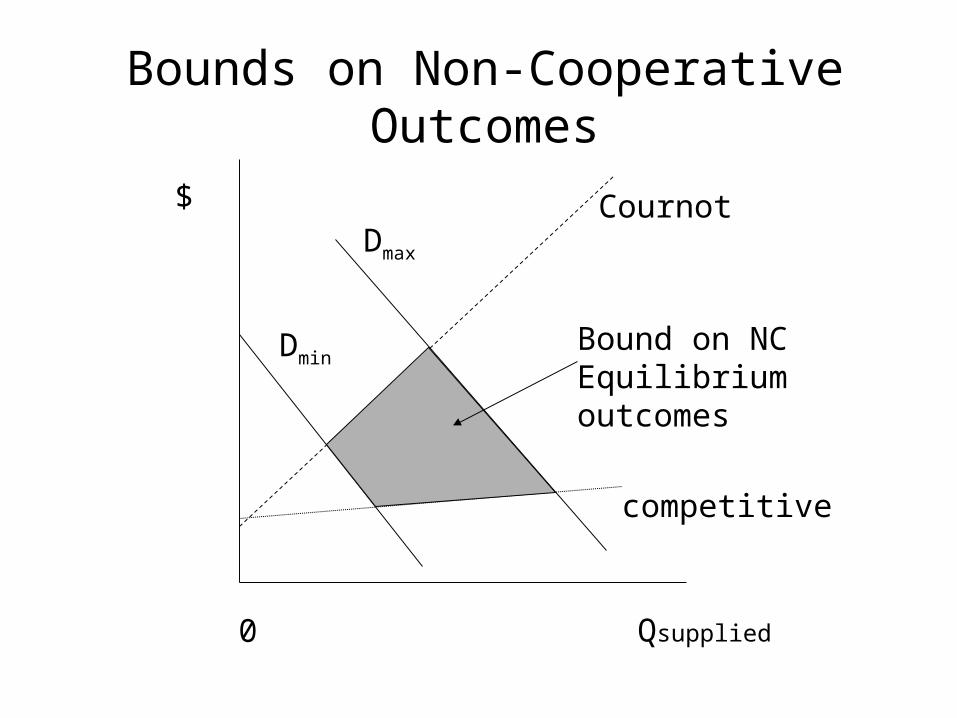

Green and Newbery (1992)

0

$Dmax

DminBound on NCEquilibriumoutcomes

Cournot

competitive

Bounds on Non-Cooperative Outcomes

Qsupplied

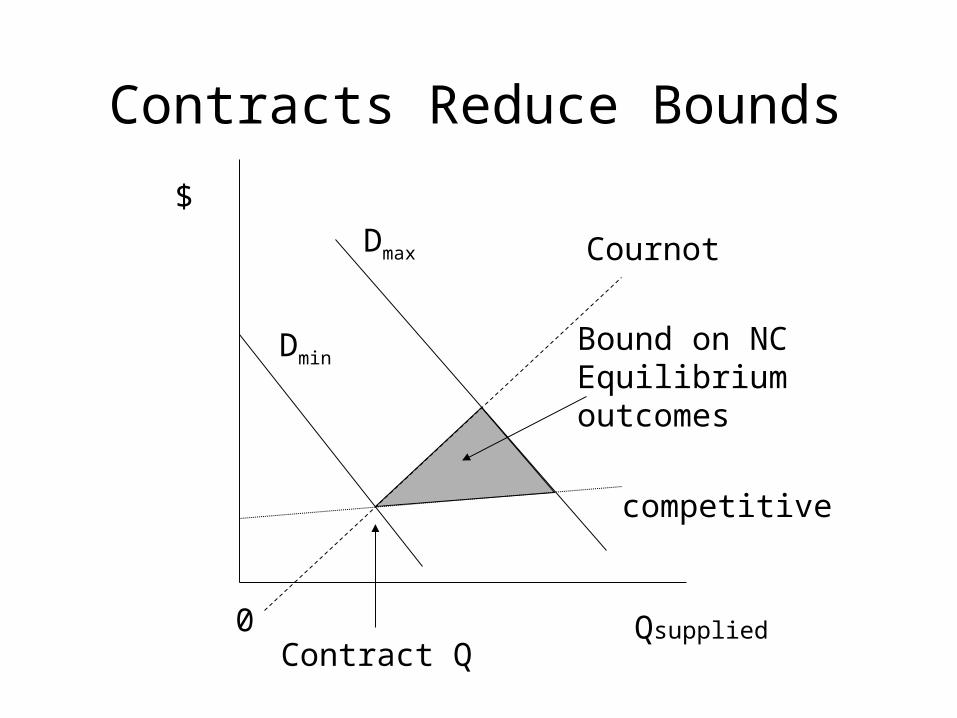

0

$

Qsupplied

Dmax

DminBound on NCEquilibriumoutcomes

Cournot

competitive

Contracts Reduce Bounds

Contract Q

0

Dmax

Dmin Bound on NCEquilibriumoutcomes

Cournot

competitive

Contract QQsupplied

$

“Over-Contracting’ can drive prices below competitive

levels

Vertical structure and forward commitments

• Vertical integration makes a firm a player in two serially related markets

• Usually we think of wholesale (upstream) price determining the (downstream) retail price– Gilbert and Hastings– Hendricks and McAfee (simultaneous)

• In some markets, retailers make forward commitments to customers– utilities – telecom services – construction

• In these markets a vertical arrangement plays the same role as a forward contract– a pro-competitive effect

Retail and Generation in PJM, 1999

GPU Inc.GPU Inc.

Public Service Electric & Gas

Public Service Electric & Gas

PECO Energy

PECO EnergyPP&L Inc.

PP&L Inc.

Potomac Electric Power

Potomac Electric Power

Baltimore Gas & Electric

Baltimore Gas & ElectricOther

Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Retail Generation

Retail and Generation in New England 1999

Northeast Util.Northeast Util.

PG&E N.E.G.

PG&E N.E.G.

Mirant

Sithe

FP&L Energy

Wisvest

Other

Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Retail Generation

Retail and Generation in California 1999

PG&E

PG&E

SCE

SCE

AES/Williams

Reliant

Mirant

Duke

Dynegy/NRG

Other

Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Retail Generation

Methodology

• Simulate prices under:– Price taking behavior– Cournot behavior– Cournot with vertical arraignments (integration or

contracts)

, c tt i,t -i,t i,t i,t i,t i,t

, i,t

p=p (q ,q )+[q -q ]· -C (q ) 0

qi t

i tq

ci,tq

• Use market data on spot price, market demand and production costs.

• The first order condition is:

Methodology

• Data on spot price, quantity demanded, vertical commitments, and unit-specific marginal costs.

• Estimate supply of fringe firms.– Calculate residual demand.

• Simulate market outcomes under:– 1. Price taking behavior: P = C’– 2. Cournot behavior: P + P’ * q = C’– 3. Cournot behavior with vertical arraignments:

P + P’ * (q-qc) = C’

Summary

• Oligopoly models married with careful empirical methods are a useful tool for both prospective and retrospective analysis of markets

• Careful consideration of the institutional details of the market is necessary

• In electricity, vertical arrangements (or contracts) appear to be a key driver of market performance– The form and extent of these arrangements going

forward will determine whether the “success” of the markets that are working well can be sustained