The crisis & building an ethical financial system Steve Keen University of Western Sydney .

16

The crisis & building an ethical financial system Steve Keen University of Western Sydney www.debtdeflation.com/blogs www.debunkingeconomics.com

-

Upload

bryce-atkinson -

Category

Documents

-

view

214 -

download

0

Transcript of The crisis & building an ethical financial system Steve Keen University of Western Sydney .

The crisis & building an ethical financial system

Steve KeenUniversity of Western Sydneywww.debtdeflation.com/blogs

www.debunkingeconomics.com

Overview• Crisis caused by growth & collapse of biggest private debt

bubble ever• Banks succumbed to inherent temptation to create

excessive debt• Ethical system must break debt-asset price feedback

– Break temptation of “unearned income” to borrowers• Relate debt to income of asset, not borrower• Reorient finance to support productive investment,

innovation• “Modern Jubilee” needed to overcome current crisis

• Conventional economics misunderstands debt & banking

– New economics needed as well as new financial architecture

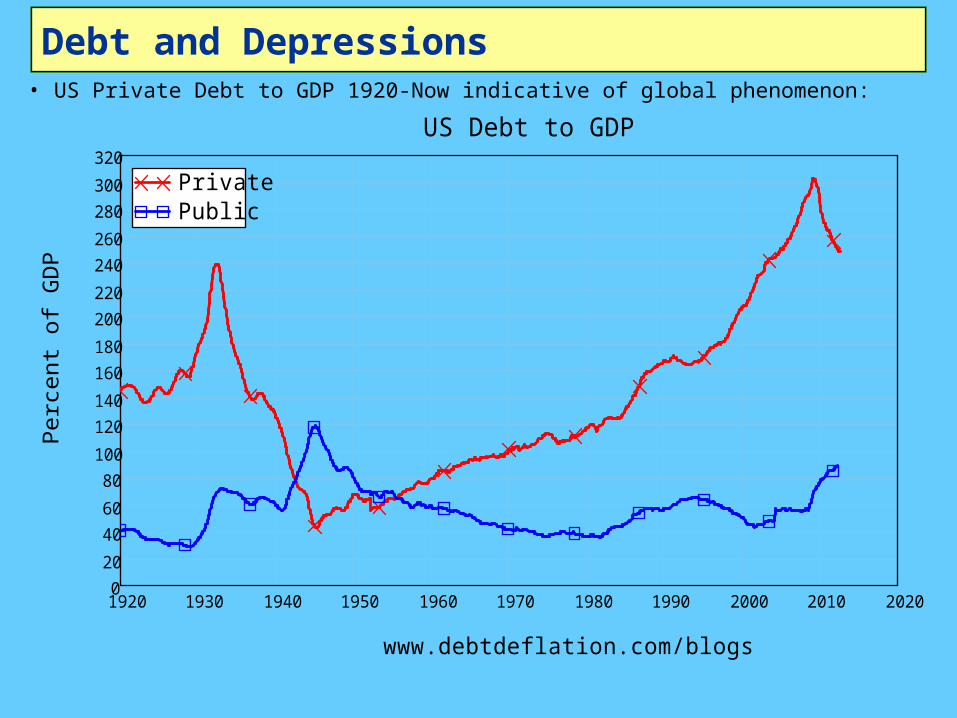

Debt and Depressions• US Private Debt to GDP 1920-Now indicative of global phenomenon:

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 20200

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

320

PrivatePublic

US Debt to GDP

www.debtdeflation.com/blogs

Perc

ent o

f GD

P

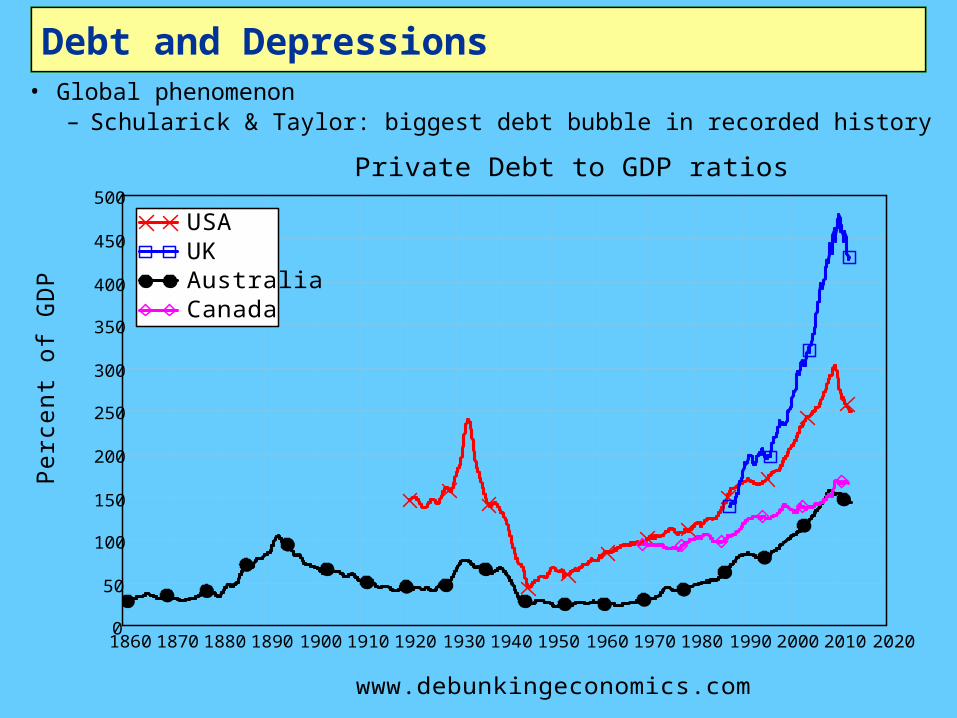

Debt and Depressions• Global phenomenon

– Schularick & Taylor: biggest debt bubble in recorded history

1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 20200

50

100

150

200

250

300

350

400

450

500

USAUKAustraliaCanada

Private Debt to GDP ratios

www.debunkingeconomics.com

Per

cent

of

GD

P

Debt Dynamics & The Crisis• Crisis caused by reversal from rising to falling debt

– Decline in income relatively mild…

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20149 10

6

1 107

1.1 107

1.2 107

1.3 107

1.4 107

1.5 107

1.6 107

1.7 107

1.8 107

1.9 107

2 107

GDP

USA GDP

www.debunkingeconomics.com

US

$ M

illi

on

BNP

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20149 10

6

1 107

1.1 107

1.2 107

1.3 107

1.4 107

1.5 107

1.6 107

1.7 107

1.8 107

1.9 107

2 107

GDPGDP + Debt Change

USA GDP

www.debunkingeconomics.com

US

$ M

illi

on

BNP

– But decline in debt change huge…

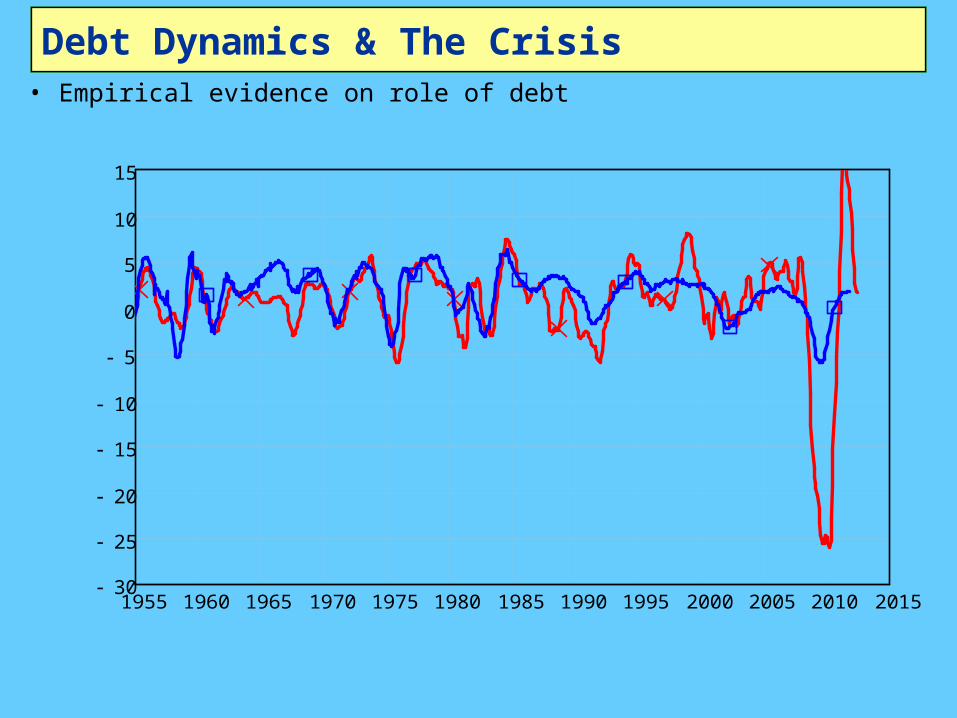

Debt Dynamics & The Crisis• Empirical evidence on role of debt (theoretical analysis later)

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

0

11

10

9

8

7

6

5

4

3

2

1

0

30

25

20

15

10

5

0

5

10

15

20

25

30

UnemploymentDebt Change

Change in Private Debt & Unemployment

www.debtdeflation.com/blogs

Per

cent

of

Wor

kfor

ce U

nem

ploy

ed

Per

cent

of

GD

P p.

a.

0

BNP

Debt Dynamics & The Crisis• Empirical evidence on role of debt

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 201530

25

20

15

10

5

0

5

10

15

Acceleration of private debtChange in Private Employment

Acceleration of private debt & change in employment, USA

Year

Per

cent

p.a

. 0

Debt Dynamics & The Crisis• Empirical evidence on role of debt

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 20146

5

4

3

2

1

0

1

2

3

4

5

6

18

15

12

9

6

3

0

3

6

9

12

15

18

Mortgage AcceleratorHouse Price Change

Mortgage Acceleration & House Price Change: USA

Per

cent

of

GD

P p.

a.

Rea

l Per

cent

p.a

.

0

Margin Acceleration & Change in Australian Shares

• Acceleration of margin debt & change in Australian ASX

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20133

2.5

2

1.5

1

0.5

0

0.5

1

1.5

2

60

50

40

30

20

10

0

10

20

30

40

Margin AccelerationShare Index Change

Margin Debt Acceleration & Share Price Change (Corr = 0.81)

www.debunkingeconomics.com

Per

cent

of

GD

P p.

a.

Per

cent

rea

l cha

nge

p.a.

0

Why was this allowed to happen?• Conventional economics ignores banks, debt & money

– E.g., Paul Krugman on my analysis of the crisis• “Keen … asserts that putting banks in the story is

essential.• Now, I’m all for including the banking sector in stories

where it’s relevant;– but why is it so crucial to a story about debt

and leverage?...”• Neoclassical “Loanable Funds” model ignores banks

– “If I decide to cut back on my spending and stash the funds in a bank, which lends them out to someone else, this doesn’t have to represent a net increase in demand.”

– Sees level of debt as having no macroeconomic consequence…

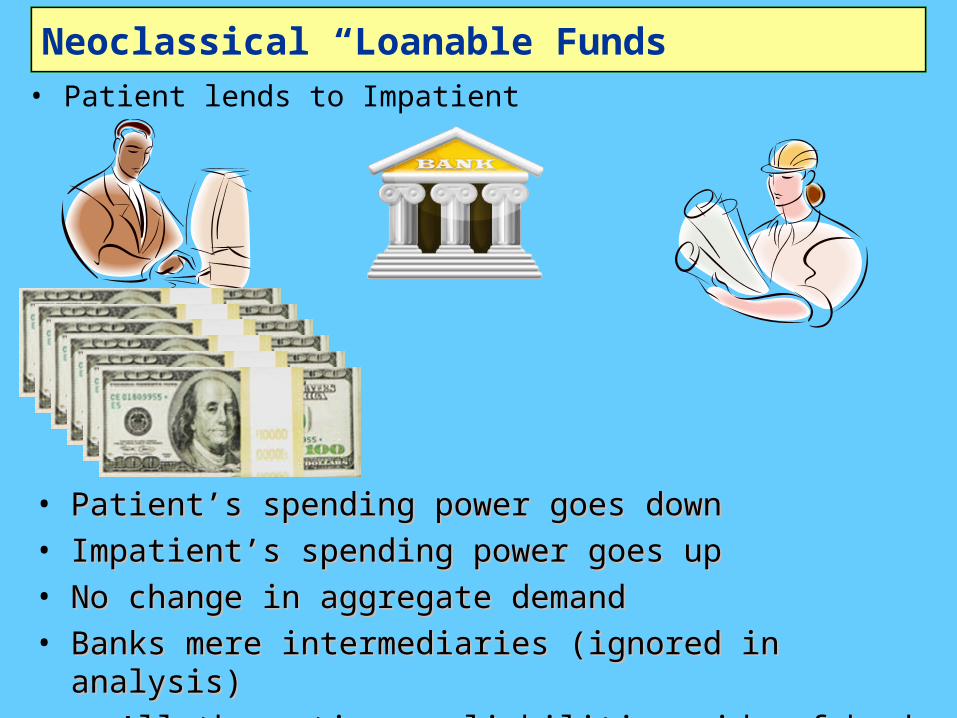

Neoclassical “Loanable Funds”• Patient lends to Impatient

• Patient’s spending power goes downPatient’s spending power goes down• Impatient’s spending power goes upImpatient’s spending power goes up• No change in aggregate demandNo change in aggregate demand• Banks mere intermediaries (ignored in analysis)Banks mere intermediaries (ignored in analysis)

• All the action on liabilities side of bank ledgersAll the action on liabilities side of bank ledgers

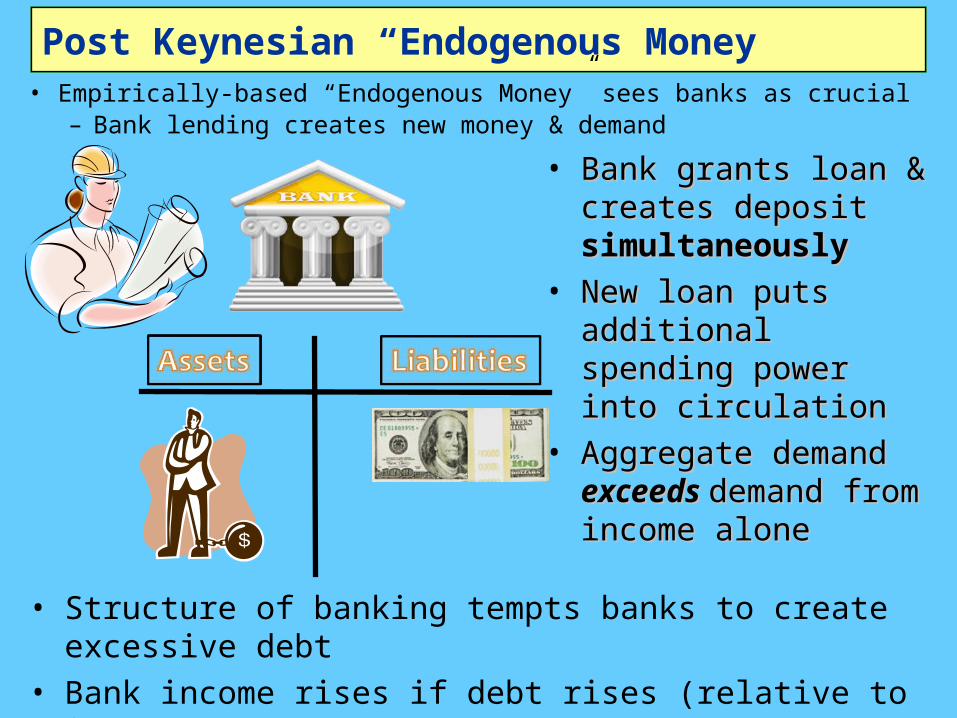

Post Keynesian “Endogenous Money”• Empirically-based “Endogenous Money” sees banks as crucial

– Bank lending creates new money & demand

• Bank grants loan & Bank grants loan & creates deposit creates deposit simultaneouslysimultaneously

• New loan puts New loan puts additional spending additional spending power into circulationpower into circulation

• Aggregate demand Aggregate demand exceeds exceeds demand demand from income alonefrom income alone

• Structure of banking tempts banks to create excessive debt

• Bank income rises if debt rises (relative to income)

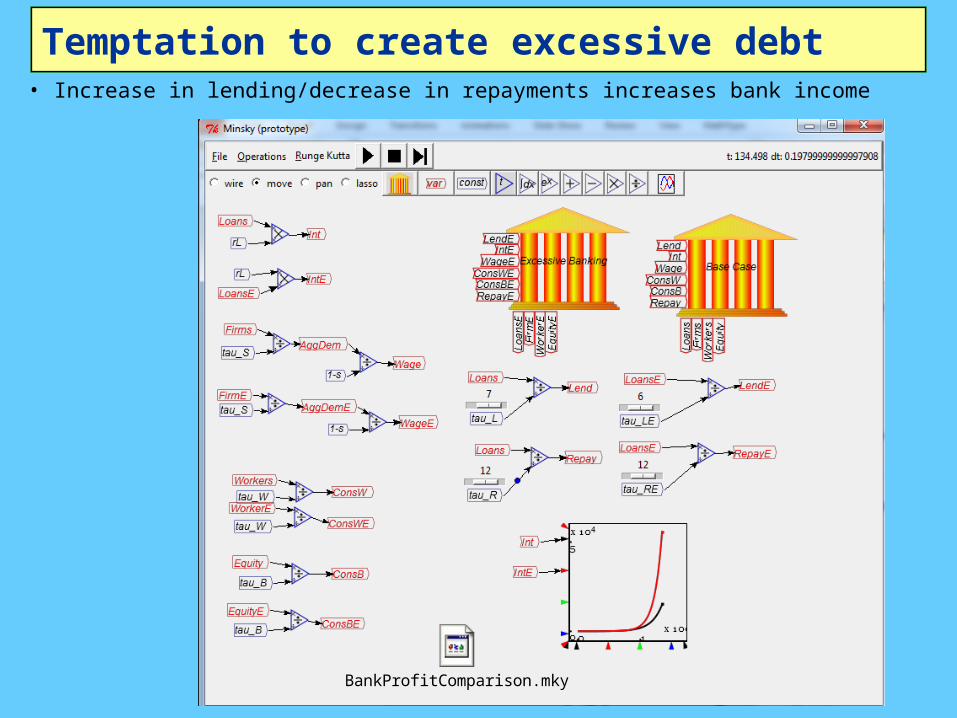

Temptation to create excessive debt• Increase in lending/decrease in repayments increases bank income

BankProfitComparison.mky

Ethical Finance?• Primary role of finance should be supporting industry &

community– Working capital for firms– Debt-financed purchase of long-lived consumption items– Developing infrastructure

• But limited profits entice lending for asset speculation instead– Difficult to remove temptation for banks– Possible to remove temptation to debt for borrowers

• In asset purchases, base lending limits on income of asset, not buyer– Now, if 2 people compete for the same house– The one with higher leverage wins– Proposal: “Property Income Limited Leverage”

• Maximum loan 10 times imputed rental income of property• No possibility of higher leverage advantage for buyers• Buyer with higher savings wins

– Proposal: Maximum borrowing for share purchase based on prospective dividend yield of shares

Escaping the crisis• Fundamental cause of crisis excessive lending for asset speculation

– Responsibility overwhelmingly lies with lenders, not borrowers• Far greater resources to analyze viability of loan• Lending based on trust: abuse of trust & fiduciary duty

• Best way out of crisis to reduce debts– “Debts that can’t be repaid, won’t be repaid” (Hudson)

• Best means a “Modern Jubilee”– Can’t just abolish debt as in Biblical Jubilee

• Securitized debt means non-bank savers would suffer– Central Bank fund injection directly to public via bank accounts

• Those in debt must repay debt• Those without debt keep cash injection

– Bank debt reduced—bank income falls– Securitized debt holders lose: fall in value of & income from

bonds• But compensated by debt injection

– Deleveraging drag on aggregate demand eliminated

Without deliberate action?• Deleveraging could dominate economy for 20 years…

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 20300

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

320

Debt to GDP ratio12.5% p.a. decline9% p.a. decline7.3% p.a.Extrapolated

USA Private Debt to GDP

www.debtdeflation.com/blogs

Perc

ent o

f G

DP

80

2027