THE BLACK-SCHOLES-MERTON MODEL 指導老師:王詩韻老師 學生:曾雅琪 (69936017)...

57

THE BLACK-SCHOLES-MERTON THE BLACK-SCHOLES-MERTON MODEL MODEL 指指指指 指指指指指 : 指指 指指指 : (69936017) 指指指 , (69936011)

-

Upload

malcolm-butler -

Category

Documents

-

view

313 -

download

0

Transcript of THE BLACK-SCHOLES-MERTON MODEL 指導老師:王詩韻老師 學生:曾雅琪 (69936017)...

THE BLACK-SCHOLES-MERTON THE BLACK-SCHOLES-MERTON MODELMODEL

指導老師:王詩韻老師學生:曾雅琪 (69936017),藍婉綺 (69936011)

Contents

Lognormal property of stock prices The distribution of the rate of return The expected return Volatility Concept underlying the Black-Scholes-Merton differential

equation Derivation of the Black-Scholes-Merton differential equation Risk-neutral valuation Black-Scholes pricing formulas Cumulative normal distribution function Implied volatilities Dividends

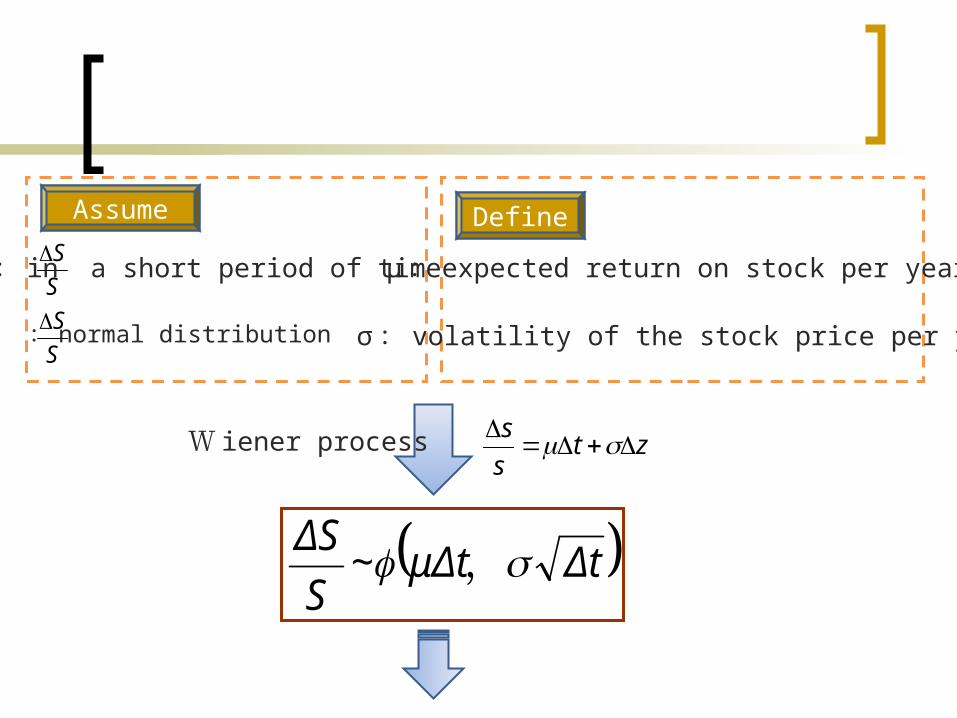

Assume

S

S

S

S

: in a short period of time(Δt)

: normal distribution

Define

μ: expected return on stock per year

σ: volatility of the stock price per year

W iener process zts

s

ΔtμΔt,~S

ΔS

TT

S

SSS T

T ,2

~lnlnln2

00

TTSST ,

2ln~ln

2

0

ΔtμΔt,~S

ΔS

dztxbdttxadx ),(),( dzSS

GdtS

S

G

t

GS

S

GdG

222

2

2

1

ItÔ’s Process ItÔ’s Lemma

0,1

,1

ln

2

2

t

G

SS

G

SS

G

SG

t

Example 13.1A stock with an initial price of $40An expected return of 16% per annumA volatility of 20% per annumAsk : the probability distribution of the stock price in 6 months?

TTSST ,

2ln~ln

2

0

56.5655.32

141.096.1759.3ln141.096.1759.3

141.0,759.3~ln

5.02.0,5.0)2

2.016.0(40ln~ln

141.096.1759.3141.096.1759.3

2

T

T

T

T

T

S

eSe

S

S

S

05.0

5.0

2.0

16.0

40

T

ST

Thus, there is a 95% probability that the stock price in 6 months will lie between $32.55~$56.56

Lognormal distribution

A variable that has s lognormal distribution can take any value between zero and infinity.

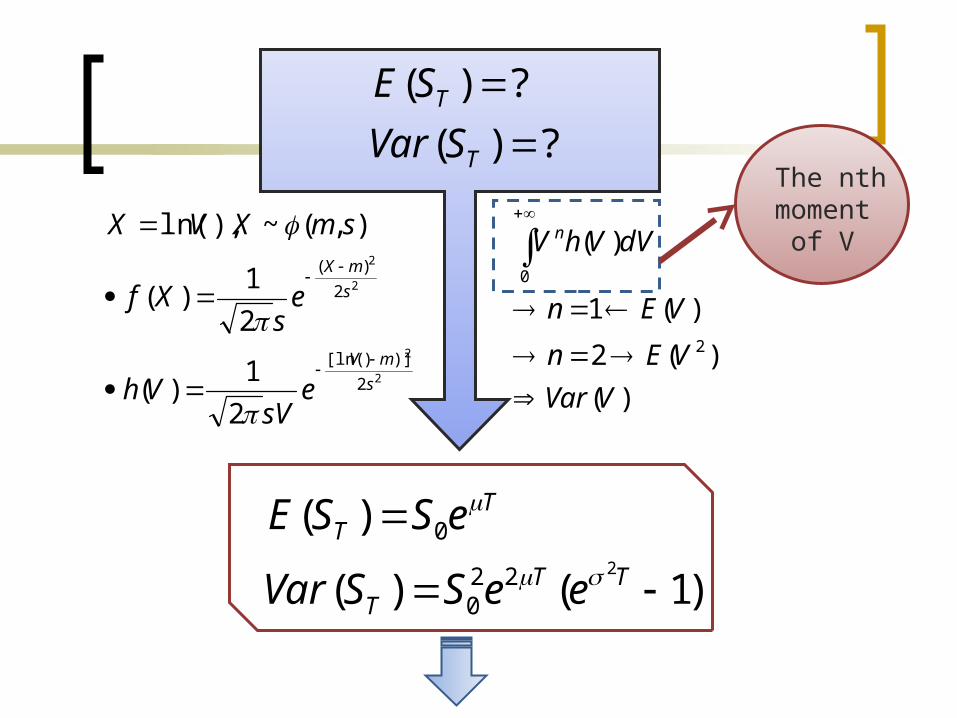

?)(

?)(

T

T

SVar

SE

)1()(

)(222

0

0

TT

T

TT

eeSSVar

eSSE

2

2

2

2

2

)])[ln(

2

)(

2

1)(

2

1)(

),(~),ln(

s

mV

s

mX

esV

Vh

es

Xf

smXVX

)(

)(2

)(1

)(

2

0

VVar

VEn

VEn

dVVhV n

The nth moment of V

2

2

)(

2

2

2

2

)(

2

2][

2

][

0

2

][

22

2

2222

2

422

2

22

2

22

2

2

2

2

)(

2

1

2

1

2

1

2

2

snnmn

s

nsmxsnnm

s

snmns

s

nsmx

s

nxsmx

s

mxnx

xs

mx

x

nx

edVVhV

dxes

e

dxees

dxes

dxes

e

deese

e

2

2

2

2

2

)])[ln(

2

)(

2

1)(

2

1)(

),(~),ln(

s

mV

s

mX

esV

Vh

es

Xf

smXVX

xeV

xedee

xxx

ln1

0

42222222

22222

222)(

222)(

snmnsnxsmmxxnsmx

nxsmmxxnxsmx

2

0

22

)(sn

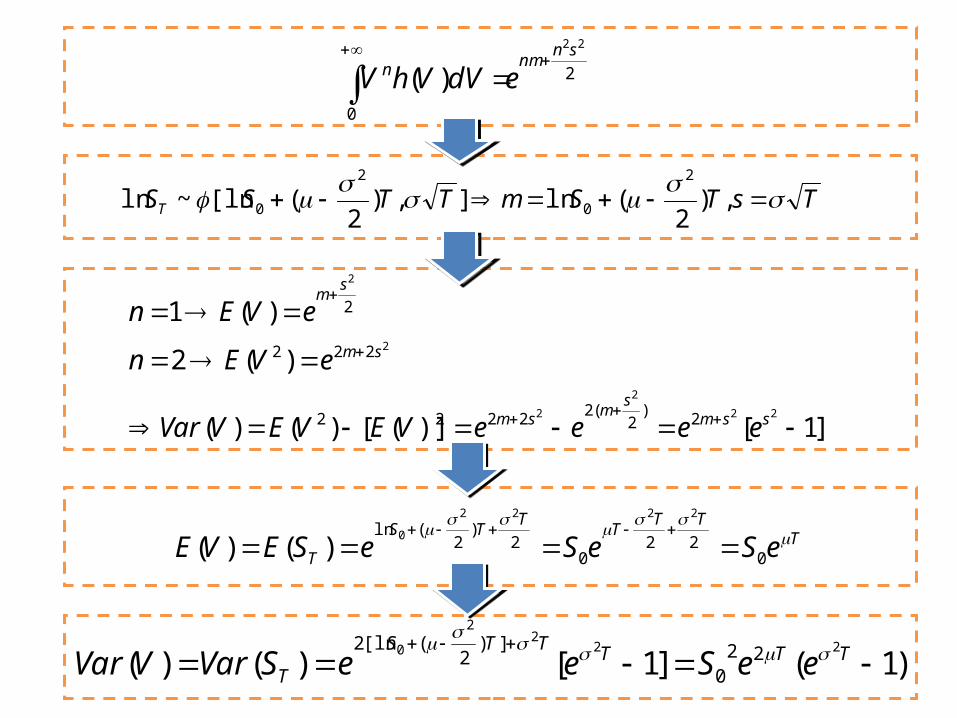

nmn edVVhV

TsTSmTTSST ,)2

(ln],)2

([ln~ln2

0

2

0

]1[)]([)()(

)(2

)(1

22

2

2

2

2

2)2

(22222

222

2

ssms

msm

sm

sm

eeeeVEVEVVar

eVEn

eVEn

TTT

TT

TS

T eSeSeSEVE

022

02

)2

(ln2222

0

)()(

)1(]1[)()(22

22

0 220

])2

([ln2

TTTTTS

T eeSeeSVarVVar

)1()(

)(222

0

0

TT

T

TT

eeSSVar

eSSE

Example 13.2A stock where the current price is $20An expected return of 20% per annumA volatility of 40% per annumAsk : the expected stock price, and the variance of the stock price, in 1year? 1

4.0

2.0

200

T

S

54.103)1(20)(

43.2420)(14.012.022

12.0

2

eeSVar

eSE

T

T

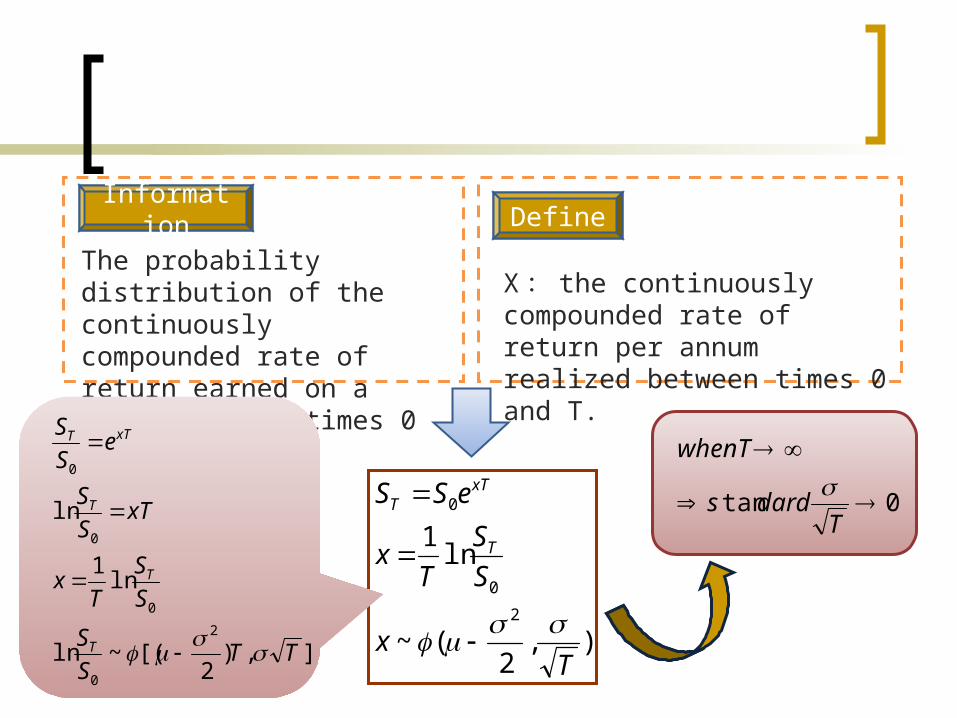

The distribution of the rate of return

Information Define

The probability distribution of the continuously compounded rate of return earned on a stock between times 0 and T.

X : the continuously compounded rate of return per annum realized between times 0 and T.

),2

(~

ln1

2

0

0

Tx

S

S

Tx

eSS

T

xTT

],)2

[(~ln

ln1

ln

2

0

0

0

0

TTS

S

S

S

Tx

xTS

S

eS

S

T

T

T

xTT

0tan

Tdards

whenT

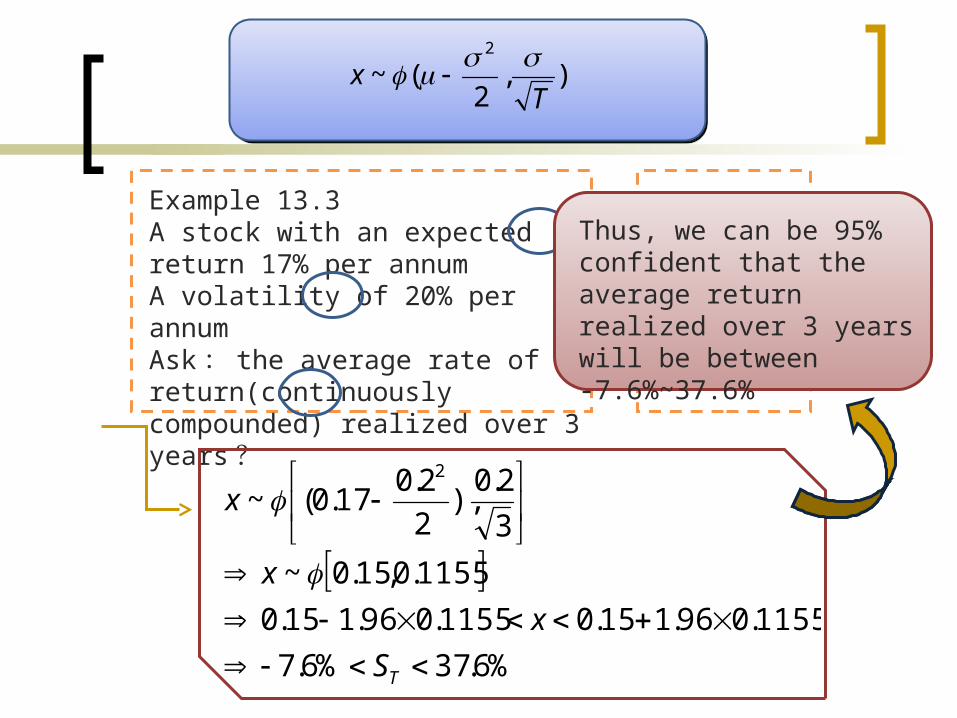

Example 13.3A stock with an expected return 17% per annumA volatility of 20% per annumAsk : the average rate of return(continuously compounded) realized over 3 years?

%6.37%6.7

1155.096.115.01155.096.115.0

1155.0,15.0~

3

2.0),

2

2.017.0(~

2

TS

x

x

x

05.0

3

2.0

17.0

T

Thus, we can be 95% confident that the average return realized over 3 years will be between-7.6%~37.6%

),2

(~2

Tx

The expected return

Expected return=E(R)= μ Expected return=E(x)=

ΔtμΔt,~S

ΔS ),2

(~2

Tx

2

2

TSSEeSSE TT

T 00 ln)](ln[)(

Assume In fact

)(

)][ln(

)ln()](ln[

)][ln()](ln[

0

0

RE

TS

SE

TSSE

SESE

T

T

TT

)2

)((

)(

)][ln(

)][ln()](ln[

2

0

xE

xE

TS

SE

SESE

T

TT

TSSEeSSE

TSSETS

S

TT

T

TT

00

2

0

2

0

ln)(ln)(

)2

(ln)][ln()2

()ln(

Arithmetic mean

Geometric mean

Example 13.4Initial investment of a mutual fund is $100The returns per annum report over the last five years:15%, 20%, 30%, -20%, 25%

Arithmetic mean>geometric meanArithmetic mean>geometric mean

%43.122

)1772.0(14.0)(

2)(

2

2

xE

xE

54.192)14.1(100 55 FV

Arithmetic mean

%145

%25%20%30%20%15

)(

RE

%4.12

1%)251%)(201(

%)301%)(201%)(151(

)(

5

xE

4.17925.18.0

3.12.115.11005

FV

Geometric mean

a. Estimating volatility from historical data

b. Trading days vs. calendar days

Volatility

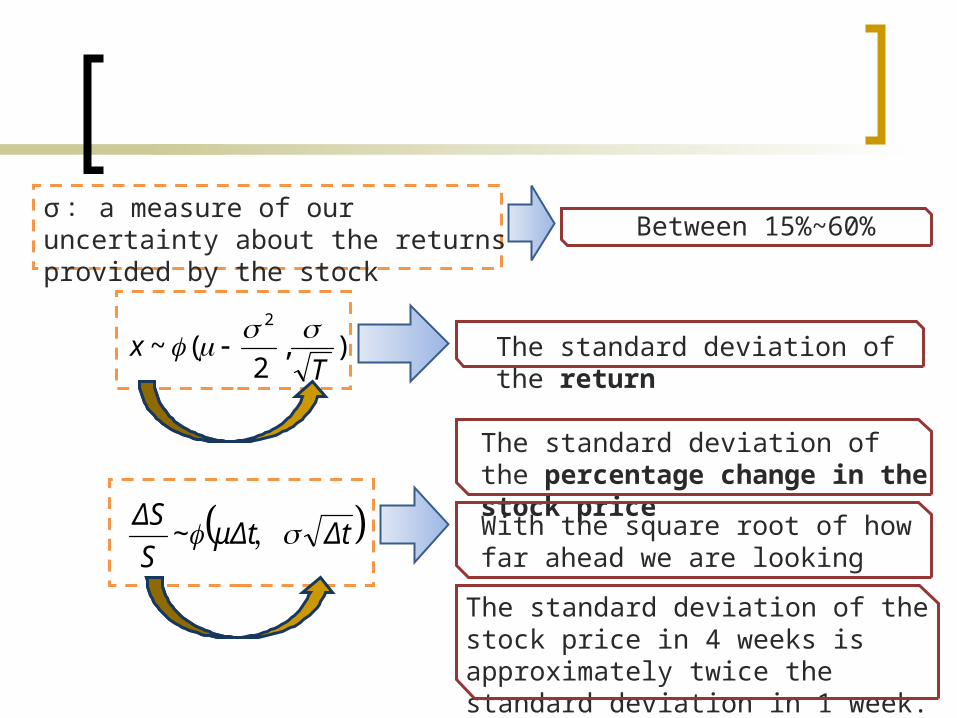

σ: a measure of our uncertainty about the returns provided by the stock

ΔtμΔt,~S

ΔS

),2

(~2

Tx

Between 15%~60%

The standard deviation of the return

The standard deviation of the percentage change in the stock price

With the square root of how far ahead we are looking

The standard deviation of the stock price in 4 weeks is approximately twice the standard deviation in 1 week.

Estimating volatility from historical data

Define

n+1 : number of observationsSi : stock price at end of ith interval, with i=0,1,2……,nτ: length of time interval in years

)ln(1

i

ii S

Su

2

11

2

1

2

)()1(

1

1

1

)(1

1

n

i i

n

i i

n

i i

unn

un

uun

s

s

s

),( iuVar

n2

Standard error( )

TT

S

ST ,2

~ln2

0

)(deviation standard iu

2

11

2

2

11

2

1

2

1

2

1

2

1 1 1

2112

1

22

1

2

)()1(

1

1

1

])(1

[1

1

])(1

)(2

[1

1

])()(2[1

1

)2(1

1

)(1

1

n

i i

n

i i

n

i i

n

i i

n

i

n

i i

n

i ii

n

i

n

i

n

i

n

i i

n

i iii

n

i ii

n

i i

unn

un

un

un

un

un

un

n

u

n

uuu

n

uuuun

uun

s

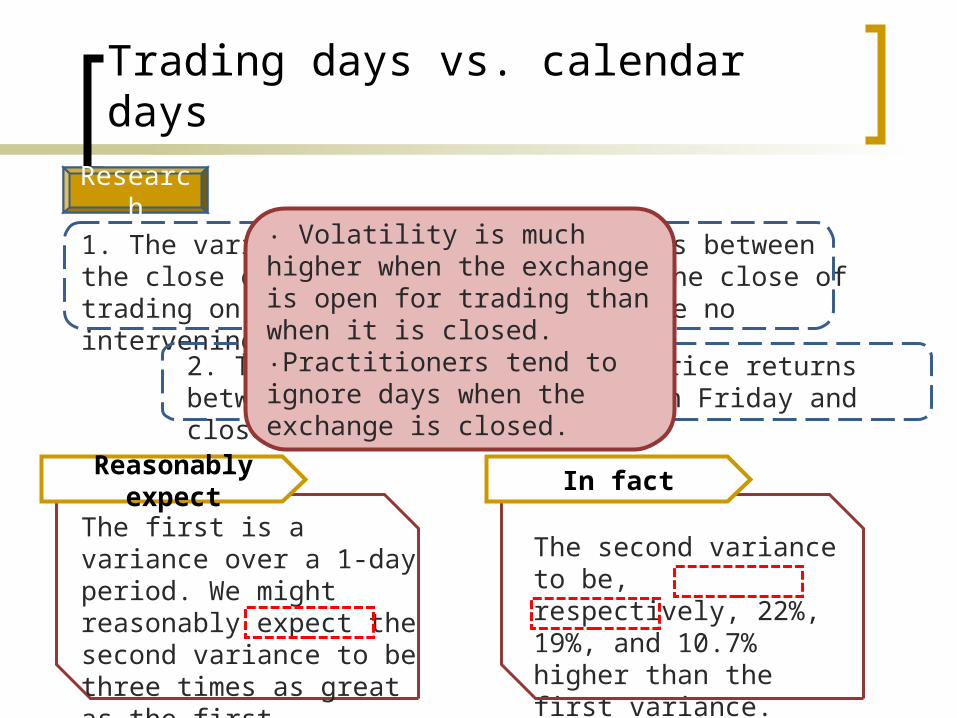

Trading days vs. calendar days

1. The variance of stock price returns between the close of trading on one day and the close of trading on the next day when there are no intervening nontrading days.

2. The variance of the stock price returns between the close of trading on Friday and close of trading on Monday.

Research

Reasonably expect

The first is a variance over a 1-day period. We might reasonably expect the second variance to be three times as great as the first variance.

The second variance to be, respectively, 22%, 19%, and 10.7% higher than the first variance.

In fact

‧ Volatility is much higher when the exchange is open for trading than when it is closed.‧Practitioners tend to ignore days when the exchange is closed.

annumper days

tradingofNumber

day trading

per Volatility

annumper

Volatility

252

matutityoption until days tradingofNumber T

The number of trading days in a years is usually assumed to be 252 for stocks.

00326.0

09531.0220

1

20

1

i i

i i

u

u

01216.0)120(20

09531.0

120

00326.0

)()1(

1

1

1

2

2

11

2

n

i i

n

i i unn

un

s

(year)193.0

2521

01216.0

s

031.0202

193.0

2

n

Standard error( )

00.20

10.20

90.20

75.20

90.20

90.20

00500.1ln

99282.0ln

00000.1ln

Concepts

derivationstock

A riskless portfolio

Return(portfolio)=risk-free interest rate(r)

No arbitrage opportunities

Example p.290△ c=0.4 S△→1. a long position in 0.4 shares 2. a short position in 1 call option

△ c=o.5△ S→1. an extra 0.1 share be purchased 2. for each call option sold

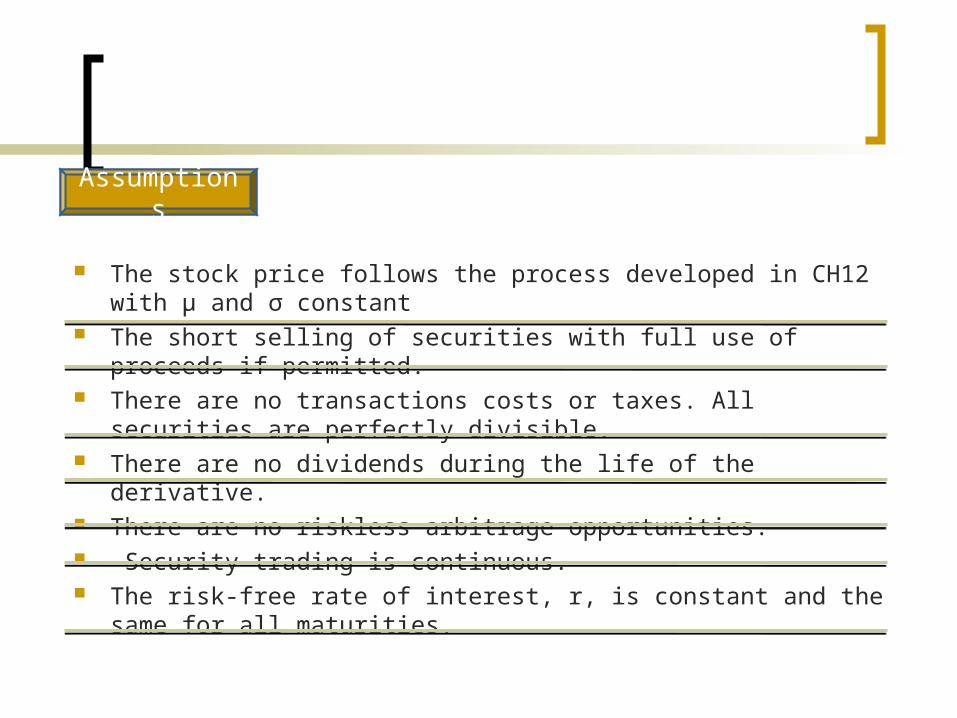

The stock price follows the process developed in CH12 with μ and σ constant

The short selling of securities with full use of proceeds if permitted. There are no transactions costs or taxes. All securities are perfectly

divisible. There are no dividends during the life of the derivative. There are no riskless arbitrage opportunities. Security trading is continuous. The risk-free rate of interest, r, is constant and the same for all

maturities.

Assumptions

Define

f : the price of the call option or other derivative contingent on S→f must be come function of S and t.π: the value of the portfolio

zStSS

zSS

ftS

S

f

t

fS

S

ff

222

2

2

1

equation

portfolio

S

f

-1 : derivative

: shares

process

tSS

f

t

f

zSS

ftS

S

fzS

S

ftS

S

ft

t

ftS

S

f

zStSS

fzS

S

ftS

S

f

t

fS

S

f

SS

ff

SS

ff

222

2

222

2

222

2

2

1

2

1

2

1

zStSS

zSS

ftS

S

f

t

fS

S

ff

222

2

2

1

This equation does not involve z△

222

2

222

2

222

2

2

1

2

1

2

1

SS

frS

S

f

t

frf

rSS

frfS

S

f

t

f

tSS

ffrtS

S

f

t

f

tr

△π=rπ t△The portfolio must instantaneously earn the same rate of return as other short-term risk-free securities.

tSS

f

t

f

22

2

2

2

1

SS

ff

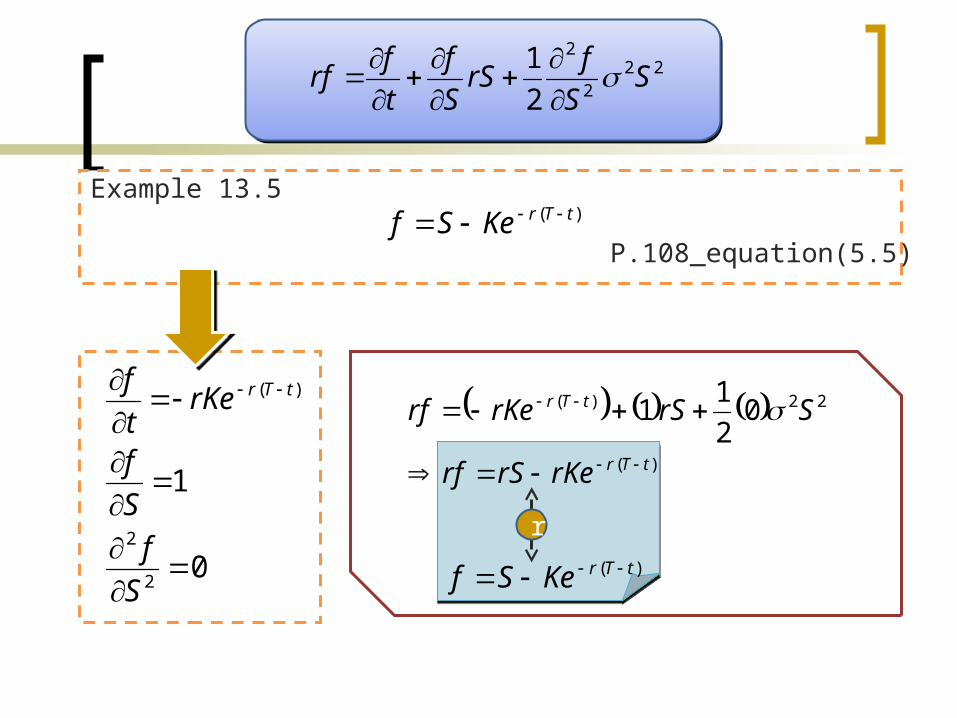

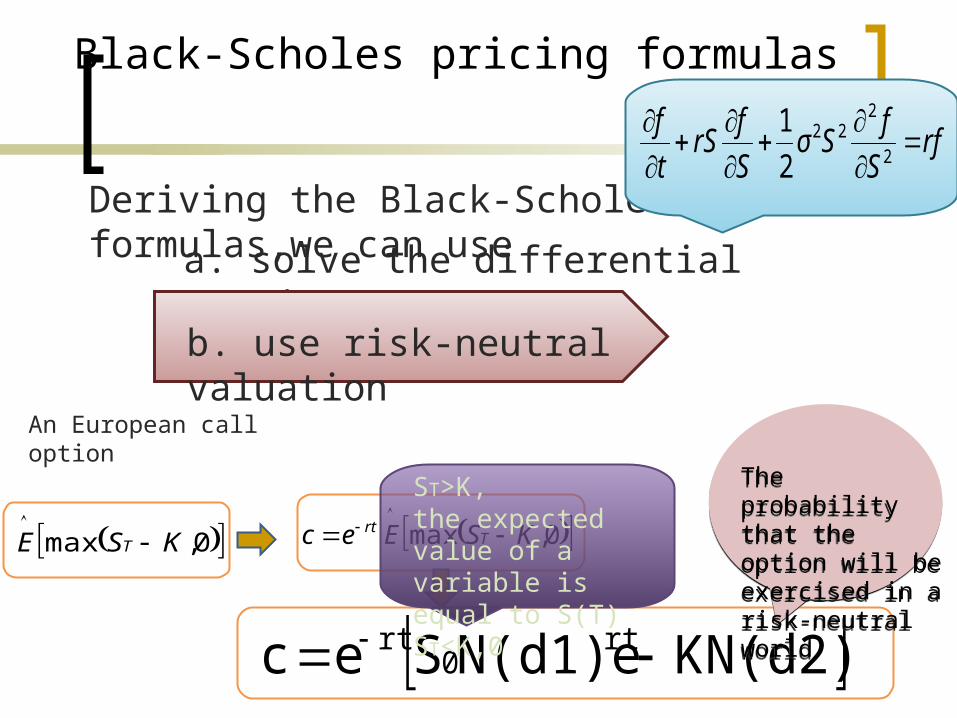

(Black-Schiles-Merton differential equation)

)( tTrKeSf

r

)( tTrKeSf Example 13.5

P.108_equation(5.5)

222

2

2

1S

S

frS

S

f

t

frf

0

1

2

2

)(

S

f

S

f

rKet

f tTr )(

22)( 02

11

tTr

tTr

rKerSrf

SrSrKerf

Application to Forward Contracts on a Stock

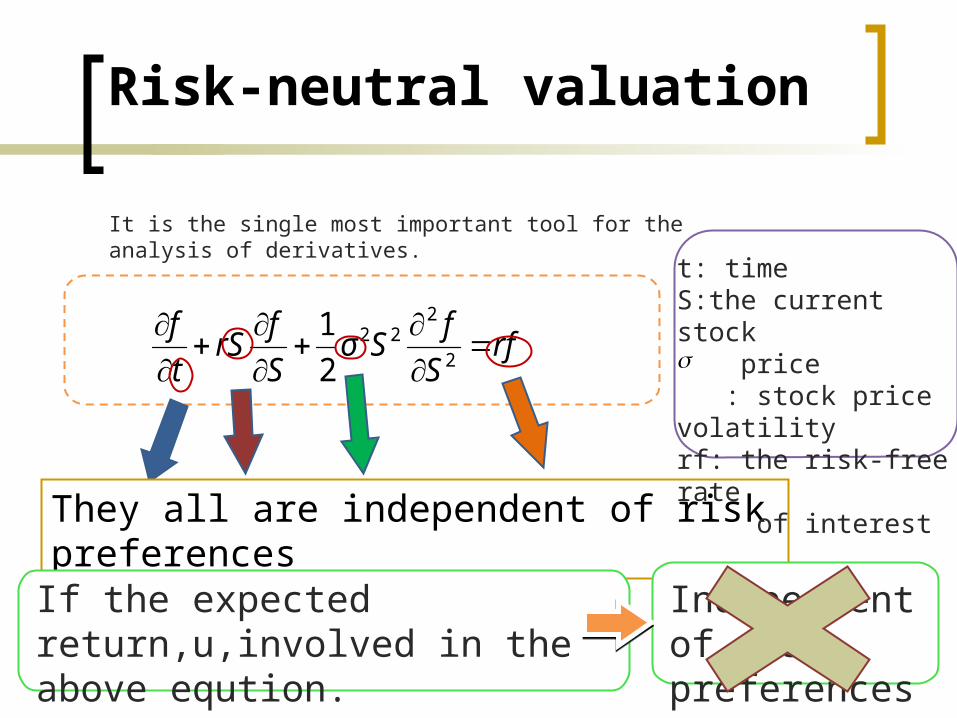

Risk-neutral valuation

rfS

fSσ

S

frS

t

f

2

222

2

1

It is the single most important tool for the analysis of derivatives.

Risk-neutral valuation

They all are independent of risk preferences

t: timeS:the current stock price : stock price volatilityrf: the risk-free rate of interest

If the expected return,u,involved in the above eqution.

Independent of risk preferences

Risk-neutral valuation

All investors are risk neutralAssumption:

The expected return of all investment asset is the risk-free rate of interest, r .

the expected return = rWhy

?Why

?

The risk-neutral investors do not require a premium to induce them to take risks.

1.

r=rf + s

Risk-neutral valuation

Reason:

present value expected value

Discount by r

2.

Any cash flow

How to use risk-neutral valuation

A derivative provides a payoff at one particular time.

step1

the expected return from the underlying asset is the risk-free interest rate, r.

Assume: Step2 Calculate the expected payoff from the derivative

Step3Discount the expected payoff at the risk-free interest rate.

Step3

Application to Forward Contracts on a Stock

Verify

Equation(5.5)

f = S 0 – Ke-rt A long forward contract

Maturity: time T Delivery price: K

A long forward contract

Maturity: time T Delivery price: K

step1Calculate:the value at maturity

ST - KST - K

ST : stock price at time T

Step2Calculate: the value at time 0

f = e-rT E(ST – K) = e-rTE(ST) –Ke-rT

(13.17)

Equation13.4

E(ST) = S0erT

E(ST) = S0erT

(13.18)

Substitute equation(13.18

) into (13.17)f = S0 – Ke-rt

step3

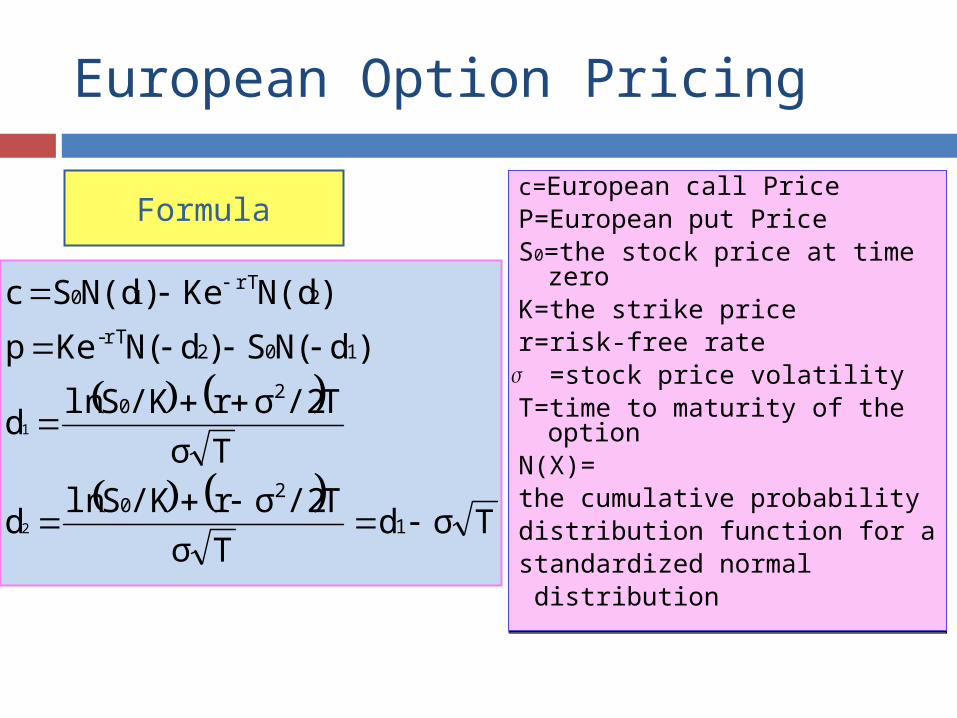

European Option Pricing

c=European call PriceP=European put PriceS0=the stock price at time zeroK=the strike pricer=risk-free rate =stock price volatilityT=time to maturity of the optionN(X)=the cumulative probability distribution function for a standardized normal distribution

c=European call PriceP=European put PriceS0=the stock price at time zeroK=the strike pricer=risk-free rate =stock price volatilityT=time to maturity of the optionN(X)=the cumulative probability distribution function for a standardized normal distribution

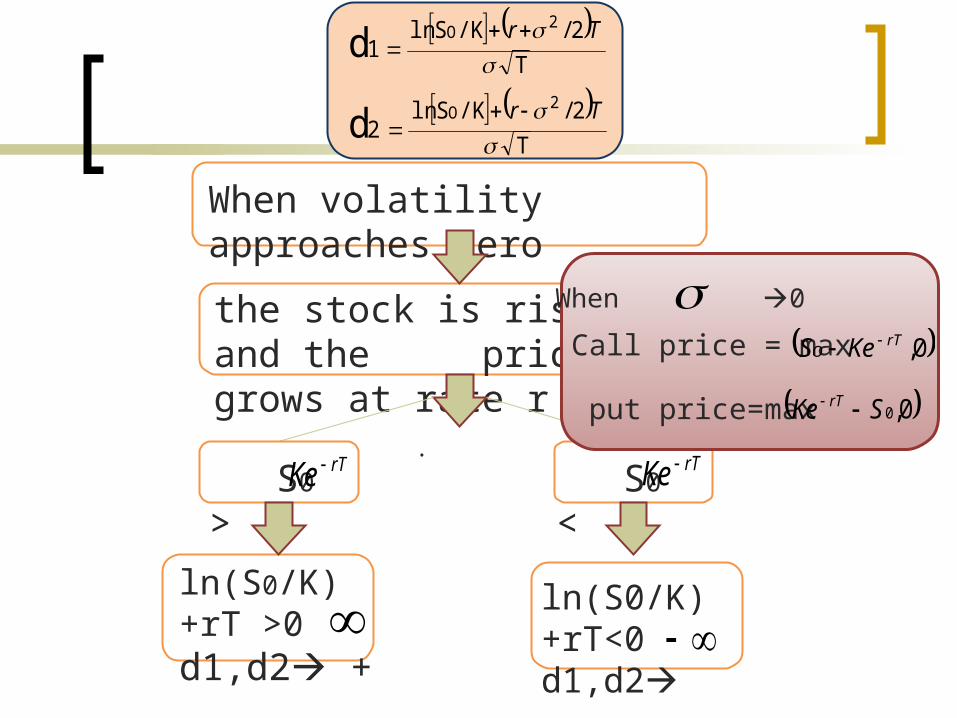

Tσd

Tσ

T/2σr/KSlnd

Tσ

T/2σr/KSlnd

)dN(S)dN(Kep

)N(dKe)N(dSc

1

20

20

102rT-

2rT

10

2

1

Formula

Black-Scholes pricing formulas

0,max KSE T 0,max KSEec T

rt

KN(d2)N(d1)eSec rt0

rt

ST>K,the expected value of a variable is equal to S(T)ST<K,0

The probability that the option will be exercised in a risk-neutral world

The probability that the option will be exercised in a risk-neutral world

a. solve the differential equation(13.16)

Deriving the Black-Scholes formulas,we can use

b. use risk-neutral valuation

rfS

fSσ

S

frS

t

f

2

222

2

1

An European call option

Derivation

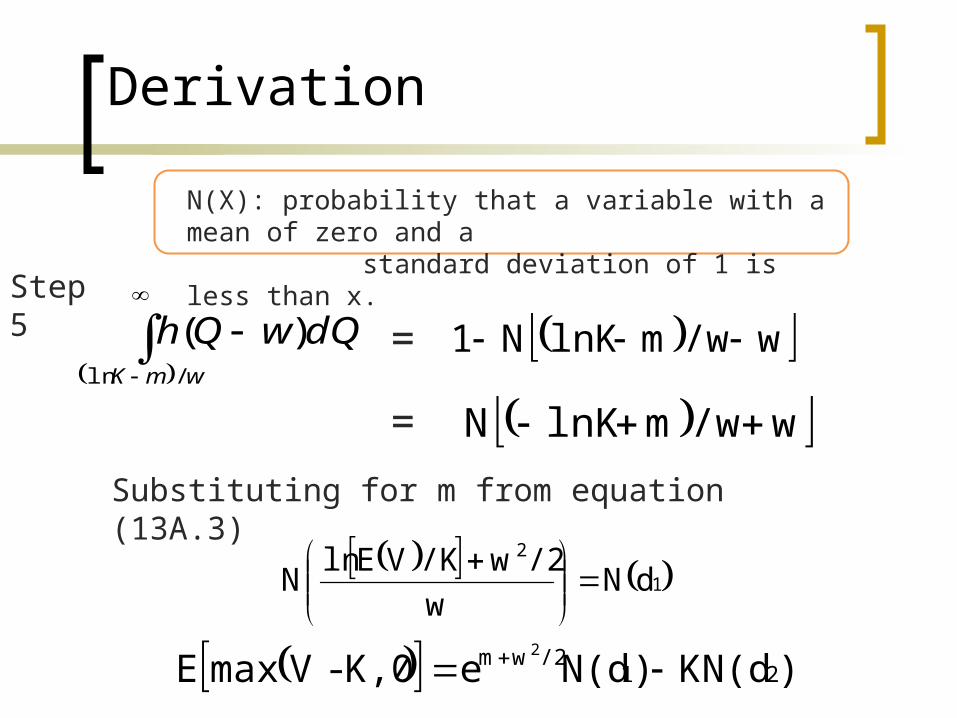

If ln V~ N(m, w)E [max(V − K, 0)] = E(V )N(d1) − KN(d2)where

W

2/2W- ln[E(V)/K]d2

W

2/2Wln[E(V)/K]d1

E : expected value

Key result

Derivation

Define g(V) as the probability density function of V . It follows that

K

K)g(V)dV-(V K,0-VmaxE

• ln V ~ N(m, w) m=ln[E(V)] - w2/2 (13A.3)

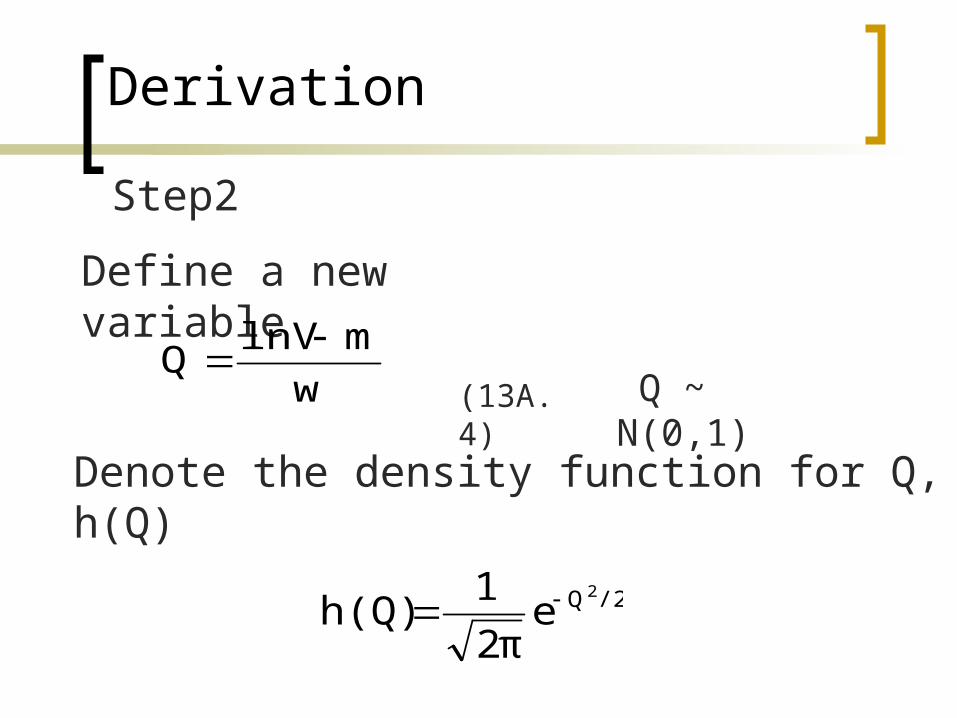

Step1

(13A.2)

Derivation

Define a new variable

(13A.4) Q ~ N(0,1)

Denote the density function for Q, h(Q)

/2Q2

e2π

1h(Q)

w

mlnVQ

Step2

Derivation

Step3Using equation(13A.4) to convert the expression on the right-hand side of equation(13A.2)from an integral over V to an integral over Q

QdQhK)(eK,0VmaxEm)/w(lnK

mQw

m)/w(lnKm)/w(lnK

mQw QdQhKQdQheK,0VmaxE

(13A.5)

Derivation

/22m2QwQmQw 2

e2π

1Qhe

/2w2mwQ 22

e2π

1

/2wQ/2wm

2

2

e2π

e

w)h(Qe /2wm 2

QdQhKe wm

m)/w(lnKm)/w(lnK

2/ w)dQ-h(QK,0 - VmaxE2

step4

(13A.6)

Derivation

w/wmlnKN1

w/wmlnKN

12

dNw

/2w/KVElnN

)KN(d)N(deK,0 - VmaxE 21/2wm 2

N(X): probability that a variable with a mean of zero and a standard deviation of 1 is less than x.

wmK

dQwQh/ln

)( =

=

Substituting for m from equation (13A.3)

Step5

T

2//KSln2

T

2//KSln1

2O

2O

d

d

Tr

Tr

Properties of the Black-Scholes Formulas

When stock price becomes very large

N(d1)1N(d2)1

N(-d1)0N(-d2)0

d1.d2 become very largeN(-d1)=1-N(d1)N(-d2)=1-N(d2)

)N(dKe)N(dSc 2rT

10 d1)N(Sd2)N(Kep 0

rT

price p approaches zero

So- Ke-rt

very similar to a forward contract with delivery price K.

When volatility approaches zero

rTeS 0

the stock is riskless and the price grows at rate r to .

S0 > rTKe S0 < rTKe

ln(S0/K)+rT >0d1,d2 + ln(S0/K)+rT<0

d1,d2

T

2//KSln2

T

2//KSln1

2O

2O

d

d

Tr

Tr

Call price = max put price=max

When 0 0,rTO KeS

0,0SKe rT

Cumulative normal distribution function

2 3 4 51 2 3 4 51 ( )( ) 0

( )1 ( ) 0

N x a k a k a k a k a k if xN x

N x if x

1

, 0.23164191

kx

1 0.319381530a 2 0.356563782a 3 1.781477937a

4 1.821255978a 5 1.330274429a

2 21( )

2xN x e

Example

Example 13.6The stock price 6months from the expiration of an option is $ 42The exercise price of the option is $40The risk-free interest rate is 10%The volatility of 20% per annum

5.0

2.0

1.0

40

420

T

r

K

S

6278.0

0.50.2

5.02/2.00.142/40ln2

2

d

Ke-rt =40e-0.1*0.5 = 38.049

7693.0

0.50.2

5.02/2.00.142/40ln1

2

d

c=42N(0.7693)-38.049N(0.6278) p= 38.049 N(-0.6278)-38.049N(-0.7693)

N(0.7693)=0.7791 N(-0.7693)=0.2209N(0.6278)=0.7349N(0.-6278)=0.2651

Implied volatilities

In the Black-Scholes pricing formulas

the volatility of the stock price.

Functions:a.Monitor the market’s opinion about the volatility of particular stock.b. From actively traded option on a certain asset,Traders use to calculate the appropriate volatility for pricing a less actively traded option on the same stock.

calculated by option price observed in the market.

We can’t find

We can’t find

σ=0.2 c=1.76 too low

σ=0.3 c=2.1 too high

σ=0.25 too high

European call option (No dividend)C=1.875So= 21K= 20r=10% (per annum)T=0.25Ask: σ =??Implied volatility

)N(dKe)N(dSc 2rT

10

How to do?? Iterative search

C is an increasing function of σ

σ lies between 0.2 and 0.25.In this example, the implied volatilities is 0.235

Dividends

Assumption:

a.The amount and timing of the dividends during the life of an option can be predicted with certainty.

b.The date on which the dividend is paid should be assumed to be the ex-dividend date.

c.On this date the stock price declines by the amount of the dividend.

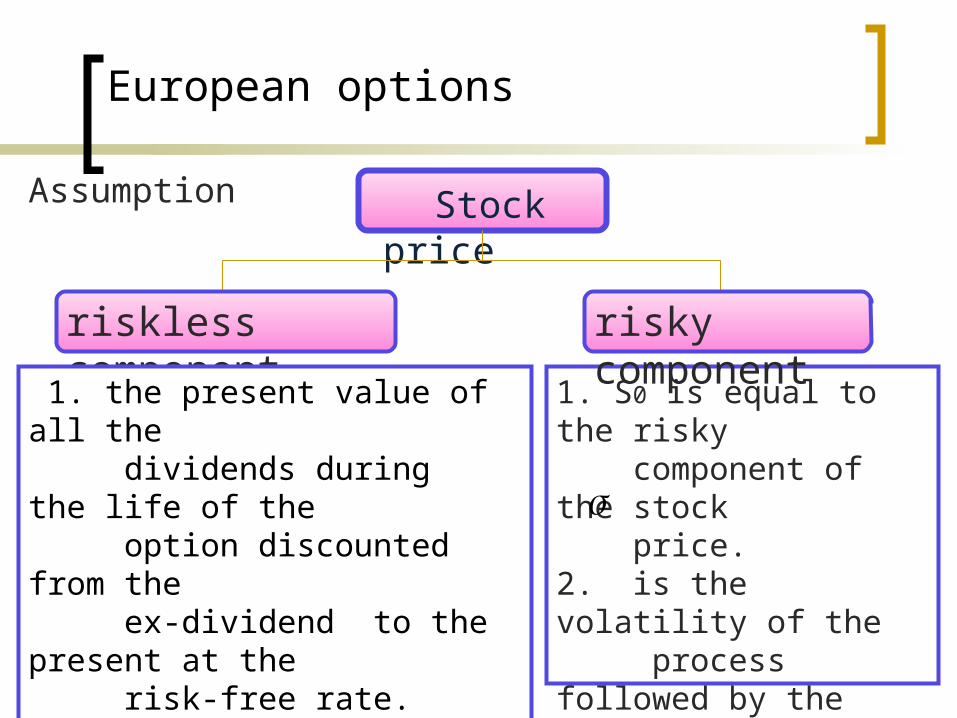

European options

Assumption Stock price

riskless component risky component

1. the present value of all the dividends during the life of the option discounted from the ex-dividend to the present at the risk-free rate. 2.By the time the option matures, the dividends will have been paid and the this part will no longer exist.

1. S0 is equal to the risky component of the stock price.2. is the volatility of the process followed by the risky component

Example 13.8European call option on a stockEx-dividend dates in two months and five monthsThe dividend is expected to be $0.5The current share price is$40The exercise price is $40The risk-free interest rate is 9%The volatility of 30% per annumTime maturity is six monthsASK:European call option price??

9.0

5.0

3.0

40

5.0

400

r

T

K

D

S

Calculate the present value of the dividends 0.5e-0.1667*0.09 + 0.5e-0.4167*0.09 = 0.9741

2/122/12 5/12

5/12

So minus the present value of the dividends 40 - 0.9741=39.0259

Use Black-Scholes pricing formulas d1=0.2017 N(d1)=0.58 d2=-0.0104 N(d2)=0.4959

Call price: 39.0259 × 0.58 - 40e-0.5*0.09 ×0.4959 =3.67

T

2//KSln2

T

2//KSln1

2O

2O

d

d

Tr

Tr

)N(dKe)N(dSC 21rT

0

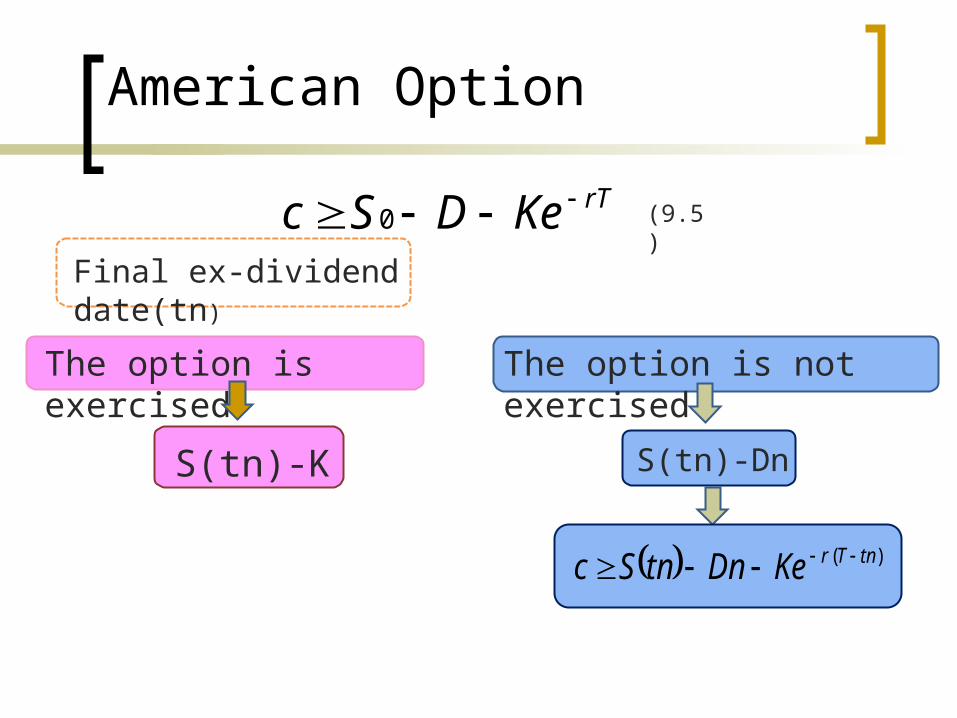

American Option

The dividends corresponding to these times will be denoted by D1,D2 …,Dn,respectively.

Assumption

When there are dividends, it is optimal to exercise only at a time immediately before the stock goes ex-dividend.

n ex-dividend dates are anticipated and they are at times t1,t2 …tn, with(t1<t2< …<tn)

American Option

rTKeDSc 0 (9.5)

Final ex-dividend date(tn)

The option is exercised

S(tn)-K

The option is not exercised

S(tn)-Dn

)( tnTrKeDntnSc

American Option

If )()( KtnSKeDntnS tnTr

)1( )( tnTreKDn then

It cannot be optimal to exercise at time tn

)( 11 titr ieKDi

It is not optimal to exercise immediately prior to time ti

It can be optimal to exercise at time tn)1( )( tnTreKDn

If

Very large

T-tn is small