TAB 5 Bassett, Desai, Gill, Malik

65

1 TAX IMPLICATIONS OF DOING BUSINESS IN INDIA NOVEMBER 6, 2006 22nd ANNUAL SJSU/TEI HIGH TECHNOLOGY INSTITUTE Nishith Desai NISHITH DESAI ASSOCIATES David Gill Gagan Malik ERNST & YOUNG LLP Barton Bassett FENWICK & WEST LLP

-

Upload

mikunpanda30 -

Category

Documents

-

view

220 -

download

0

Transcript of TAB 5 Bassett, Desai, Gill, Malik

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 1/65

1

TAX IMPLICATIONS OF

DOING BUSINESS IN INDIANOVEMBER 6, 2006

22nd ANNUAL SJSU/TEI HIGH TECHNOLOGY INSTITUTE

Nishith DesaiNISHITH DESAI ASSOCIATES

David GillGagan MalikERNST & YOUNG LLP

Barton BassettFENWICK & WEST LLP

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 2/65

2

Overview of Economy and Key Regulations

Legal Entity Comparison

Indian Tax Regime

Refreshment Break

Structuring Issues and Opportunities

Agenda

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 3/65

3

Overview of Economy and

Key Regulations

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 4/65

4

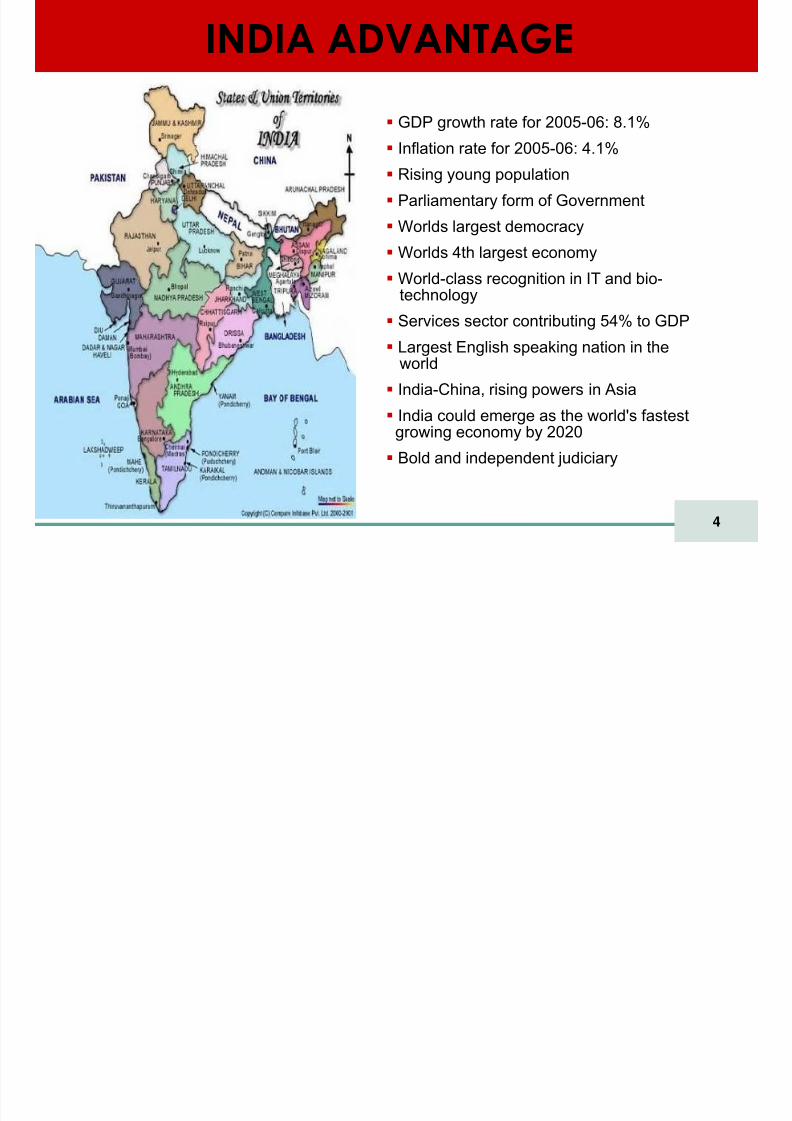

INDIA ADVANTAGE

GDP growth rate for 2005-06: 8.1%Inflation rate for 2005-06: 4.1%

Rising young population

Parliamentary form of Government

Worlds largest democracy

Worlds 4th largest economyWorld-class recognition in IT and bio-technology

Services sector contributing 54% to GDP

Largest English speaking nation in theworld

India-China, rising powers in Asia

India could emerge as the world's fastestgrowing economy by 2020

Bold and independent judiciary

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 5/65

5

KEY CONSIDERATIONS

Tax Corporate

Exchange Control

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 6/65

6

ExchangeControl

laws

Income taxAct

Investments

KEY REGULATIONS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 7/657

FOREIGN INVESTMENT REGULATIONS

Foreign Institutional Investment (FII)

Foreign Venture Capital Investment (FVCI)

Foreign Direct Investment (FDI)

Non-Resident Indian Investment (NRI)

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 8/658

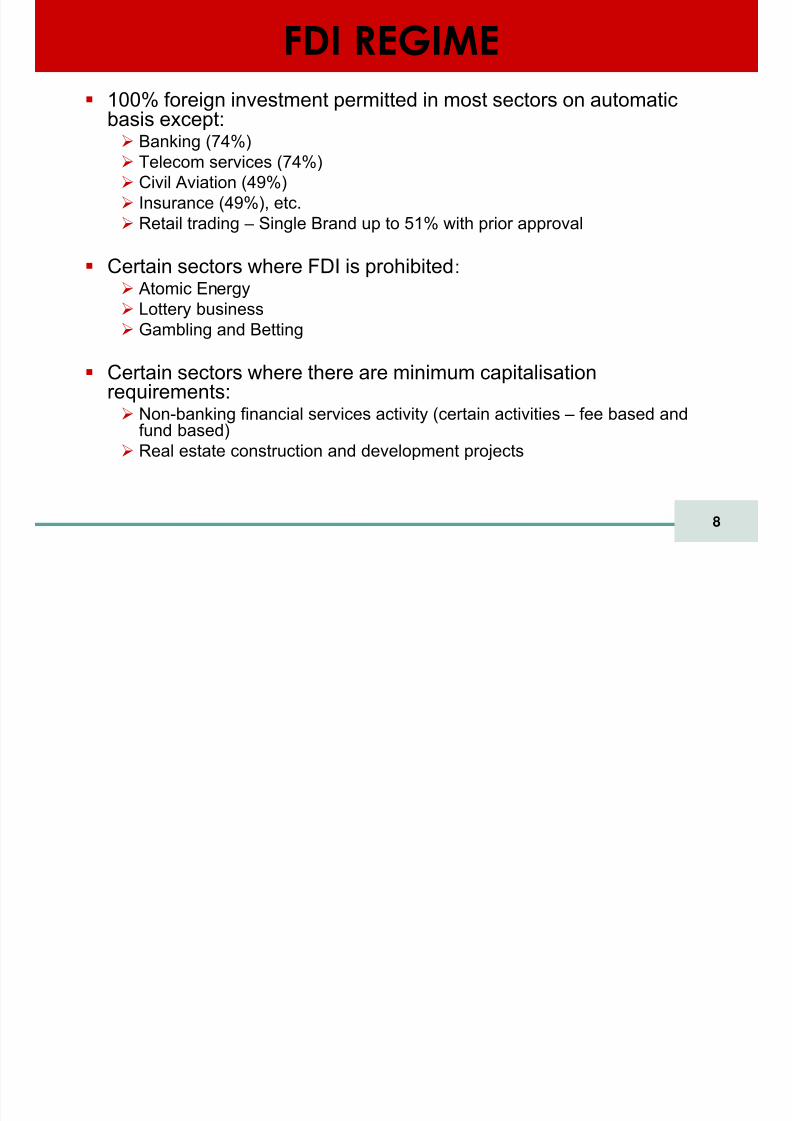

100% foreign investment permitted in most sectors on automatic

basis except:Banking (74%)Telecom services (74%)Civil Aviation (49%)Insurance (49%), etc.Retail trading – Single Brand up to 51% with prior approval

Certain sectors where FDI is prohibited : Atomic EnergyLottery businessGambling and Betting

Certain sectors where there are minimum capitalisationrequirements:Non-banking financial services activity (certain activities – fee based andfund based)Real estate construction and development projects

FDI REGIME

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 9/659

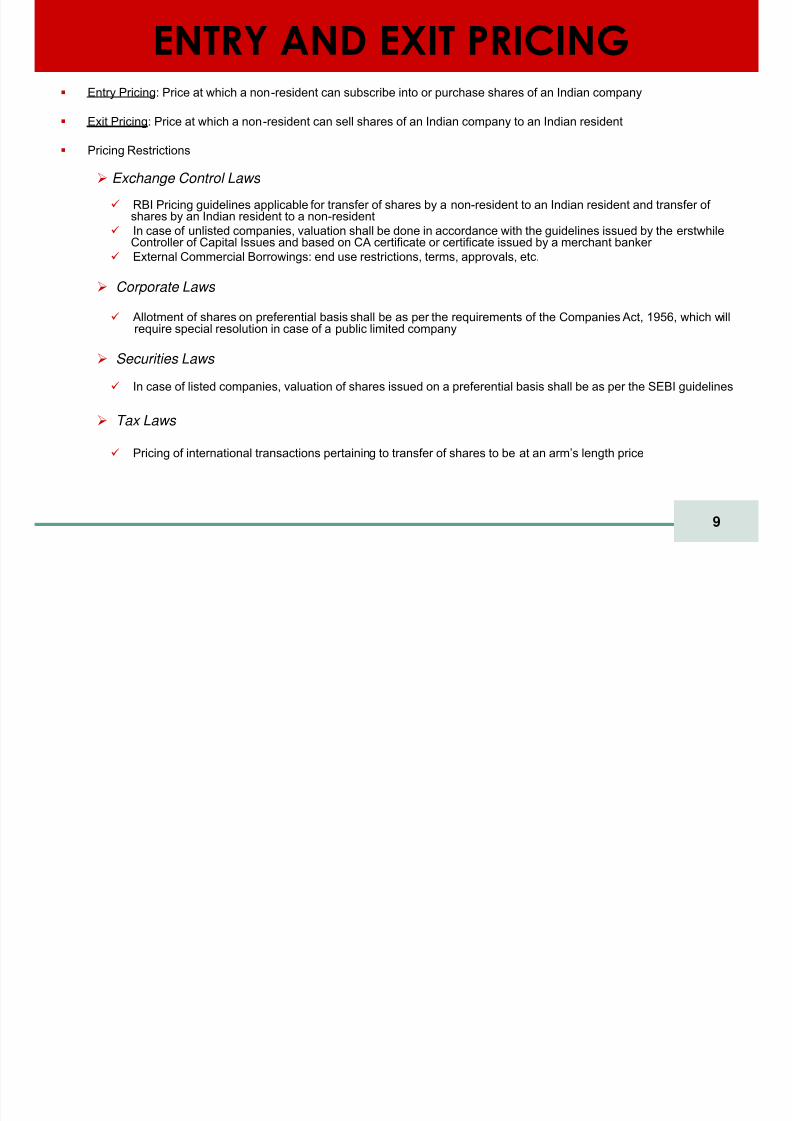

Entry Pricing: Price at which a non-resident can subscribe into or purchase shares of an Indian company

Exit Pricing: Price at which a non-resident can sell shares of an Indian company to an Indian residentPricing Restrictions

Exchange Control Laws

RBI Pricing guidelines applicable for transfer of shares by a non-resident to an Indian resident and transfer of shares by an Indian resident to a non-residentIn case of unlisted companies, valuation shall be done in accordance with the guidelines issued by the erstwhileController of Capital Issues and based on CA certificate or certificate issued by a merchant banker External Commercial Borrowings: end use restrictions, terms, approvals, etc.

Corporate Laws

Allotment of shares on preferential basis shall be as per the requirements of the Companies Act, 1956, which willrequire special resolution in case of a public limited company

Securities Laws

In case of listed companies, valuation of shares issued on a preferential basis shall be as per the SEBI guidelines

Tax Laws

Pricing of international transactions pertaining to transfer of shares to be at an arm‟s length price

ENTRY AND EXIT PRICING

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 10/65

10

FLOW OF INVESTMENT INTO INDIA

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 11/65

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 12/65

12

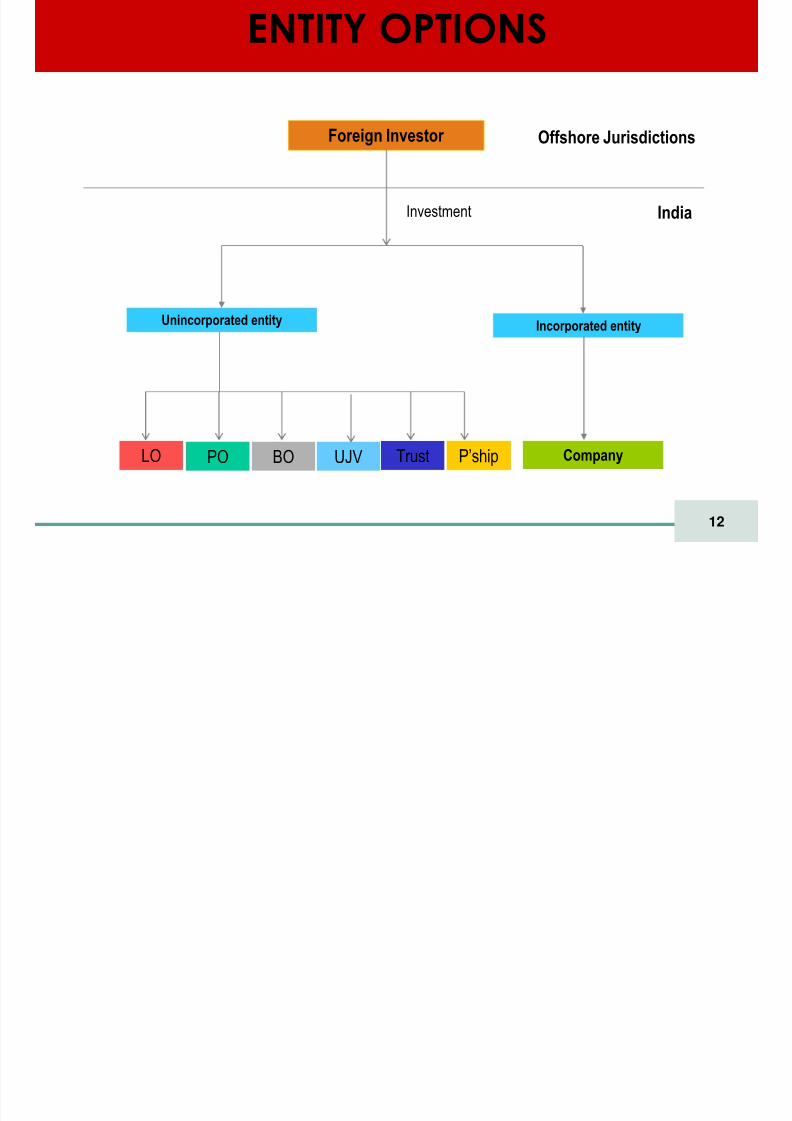

ENTITY OPTIONS

Foreign Investor

Investment

Unincorporated entity Incorporated entity

Company

India

PO BO

Offshore Jurisdictions

TrustUJV P’ship LO

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 13/65

13

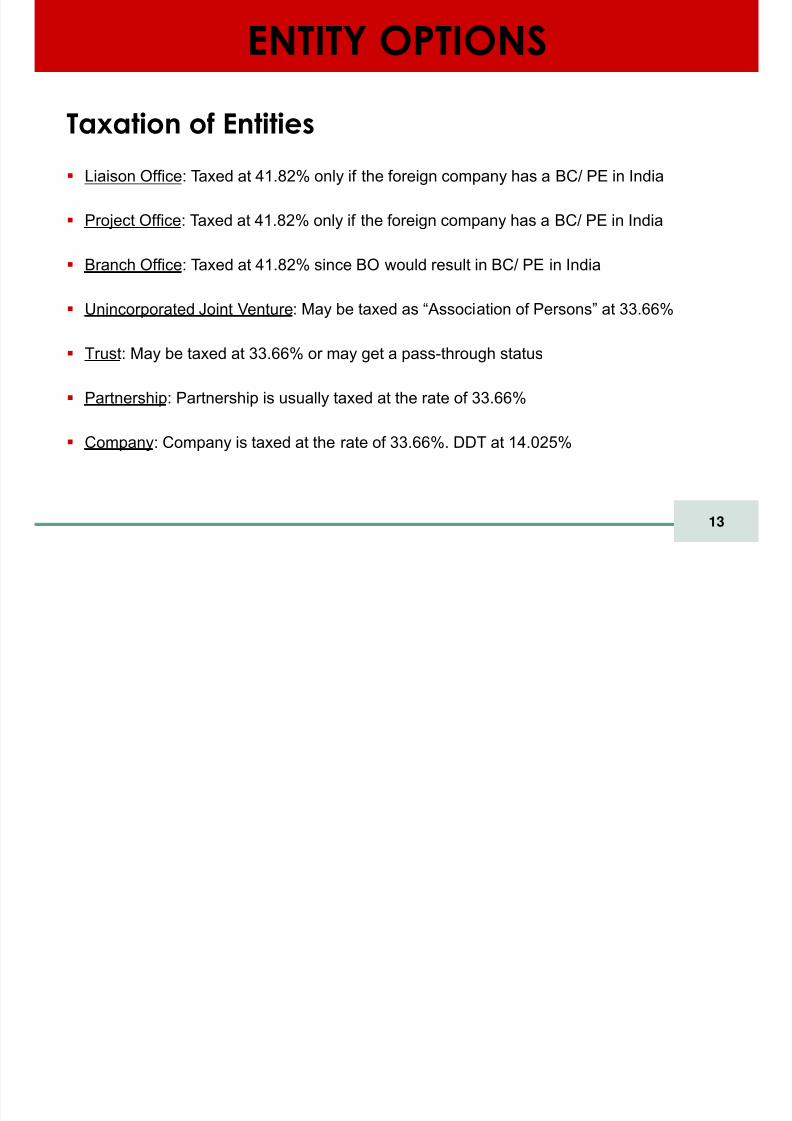

ENTITY OPTIONS

Taxation of EntitiesLiaison Office: Taxed at 41.82% only if the foreign company has a BC/ PE in India

Project Office: Taxed at 41.82% only if the foreign company has a BC/ PE in India

Branch Office: Taxed at 41.82% since BO would result in BC/ PE in India

Unincorporated Joint Venture : May be taxed as “Association of Persons” at 33.66%

Trust: May be taxed at 33.66% or may get a pass-through status

Partnership: Partnership is usually taxed at the rate of 33.66%

Company: Company is taxed at the rate of 33.66%. DDT at 14.025%

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 14/65

14

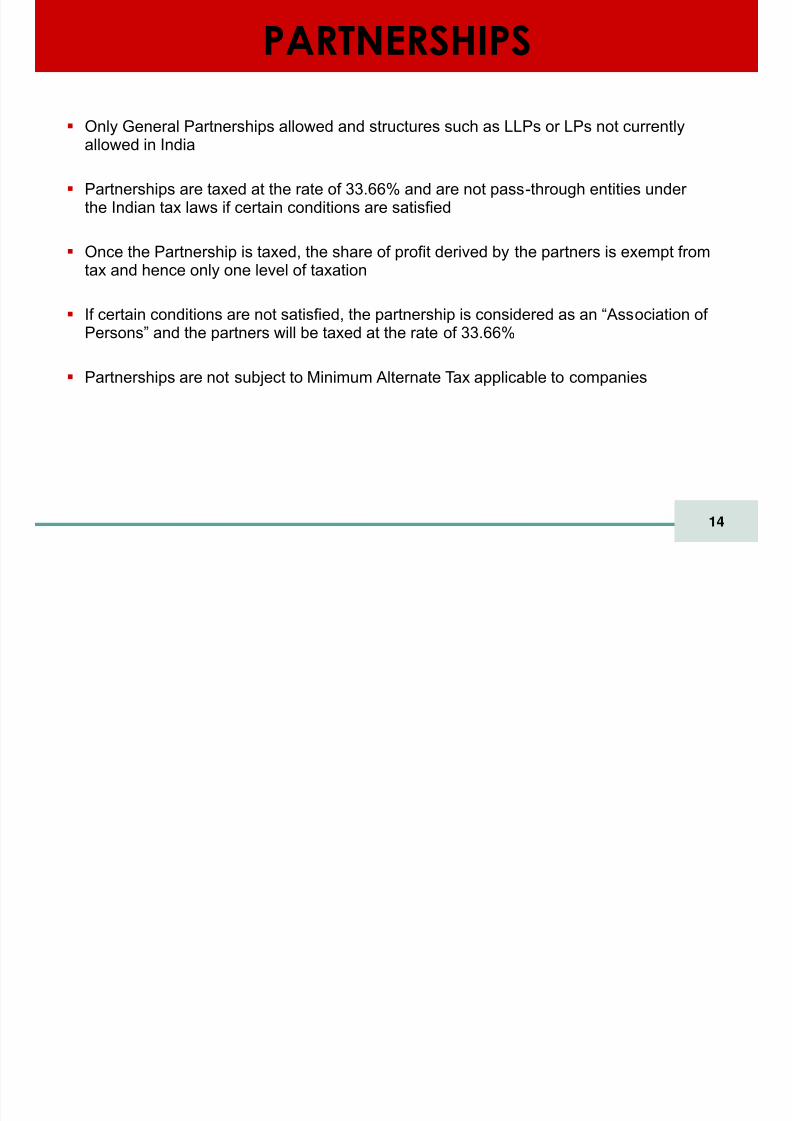

PARTNERSHIPS

Only General Partnerships allowed and structures such as LLPs or LPs not currentlyallowed in India

Partnerships are taxed at the rate of 33.66% and are not pass-through entities under the Indian tax laws if certain conditions are satisfied

Once the Partnership is taxed, the share of profit derived by the partners is exempt fromtax and hence only one level of taxation

If certain conditions are not satisfied, the partnership is considered as an “Association of Persons” and the partners will be taxed at the rate of 33.66%

Partnerships are not subject to Minimum Alternate Tax applicable to companies

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 15/65

15

TRUSTS

Typically used for making Venture Capital / Private Equity investments

Trusts may be taxed at the rate of 33.66% or could be pass-through entities under theIndian tax laws if certain conditions are satisfied

Registered trusts (i.e. Venture Capital Funds registered with SEBI) are accorded pass-through status for tax purposes and the investors are taxed when the income isdistributed by the registered trusts

Unregistered trusts are usually taxed at the rate of 33.66% if the share of thebeneficiaries are indeterminate or if the trust is irrevocable

Unregistered trusts may also be accorded pass-through status if the share of thebeneficiaries are determinate or if the trust is revocable

Trusts are not subject to Minimum Alternate Tax applicable to companies

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 16/65

16

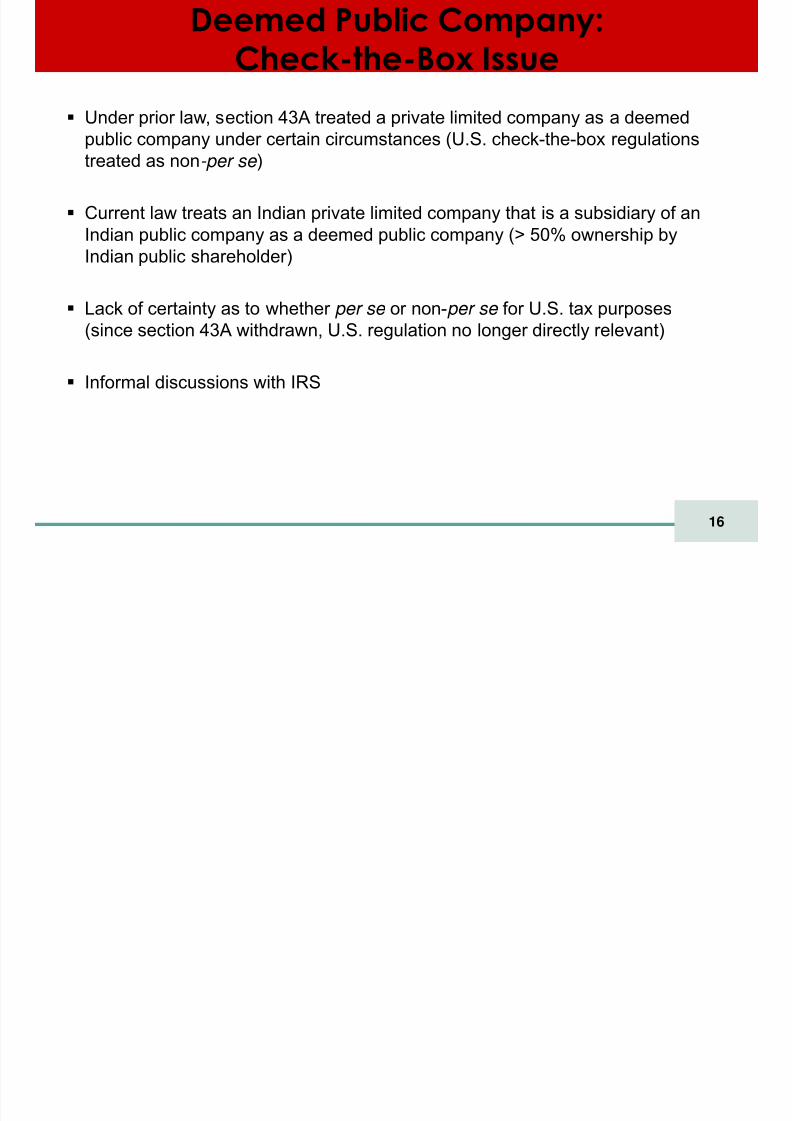

Deemed Public Company:Check-the-Box Issue

Under prior law, section 43A treated a private limited company as a deemedpublic company under certain circumstances (U.S. check-the-box regulationstreated as non -per se )

Current law treats an Indian private limited company that is a subsidiary of anIndian public company as a deemed public company (> 50% ownership by

Indian public shareholder)

Lack of certainty as to whether per se or non- per se for U.S. tax purposes(since section 43A withdrawn, U.S. regulation no longer directly relevant)

Informal discussions with IRS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 17/65

17

Indian Tax Regime

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 18/65

18

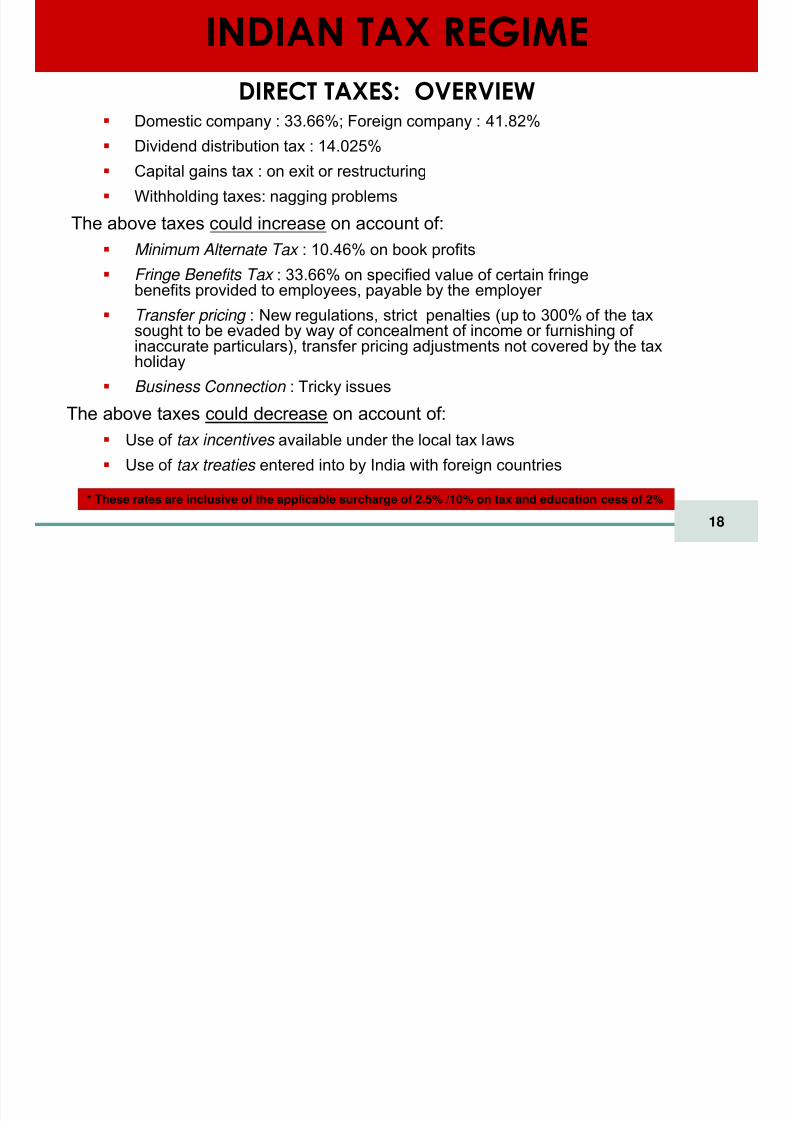

INDIAN TAX REGIME DIRECT TAXES: OVERVIEW

Domestic company : 33.66%; Foreign company : 41.82%Dividend distribution tax : 14.025%Capital gains tax : on exit or restructuringWithholding taxes: nagging problems

The above taxes could increase on account of:

Minimum Alternate Tax : 10.46% on book profits Fringe Benefits Tax : 33.66% on specified value of certain fringe

benefits provided to employees, payable by the employer Transfer pricing : New regulations, strict penalties (up to 300% of the tax

sought to be evaded by way of concealment of income or furnishing of inaccurate particulars), transfer pricing adjustments not covered by the taxholiday

Business Connection : Tricky issuesThe above taxes could decrease on account of:

Use of tax incentives available under the local tax lawsUse of tax treaties entered into by India with foreign countries

* These rates are inclusive of the applicable surcharge of 2.5% /10% on tax and education cess of 2%

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 19/65

19

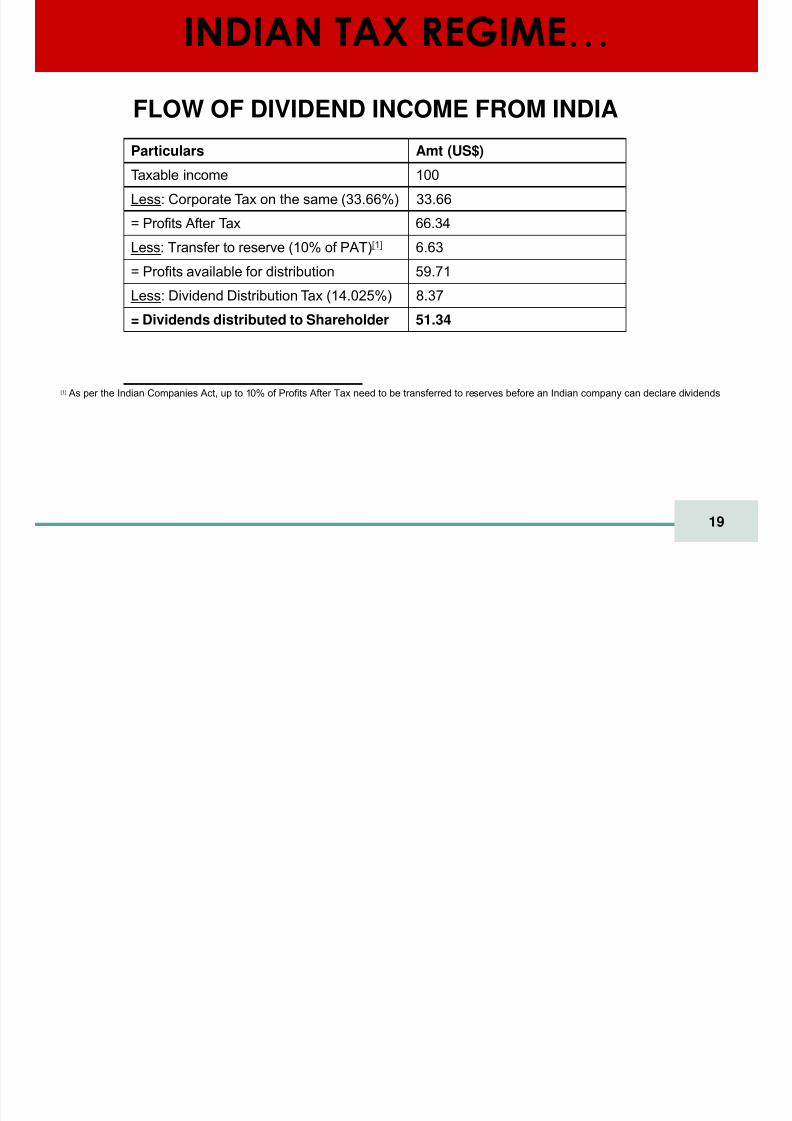

INDIAN TAX REGIME…

Particulars Amt (US$)

Taxable income 100

Less: Corporate Tax on the same (33.66%) 33.66

= Profits After Tax 66.34

Less: Transfer to reserve (10% of PAT) [1] 6.63

= Profits available for distribution 59.71

Less: Dividend Distribution Tax (14.025%) 8.37

= Dividends distributed to Shareholder 51.34

[1] As per the Indian Companies Act, up to 10% of Profits After Tax need to be transferred to reserves before an Indian company can declare dividends

FLOW OF DIVIDEND INCOME FROM INDIA

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 20/65

20

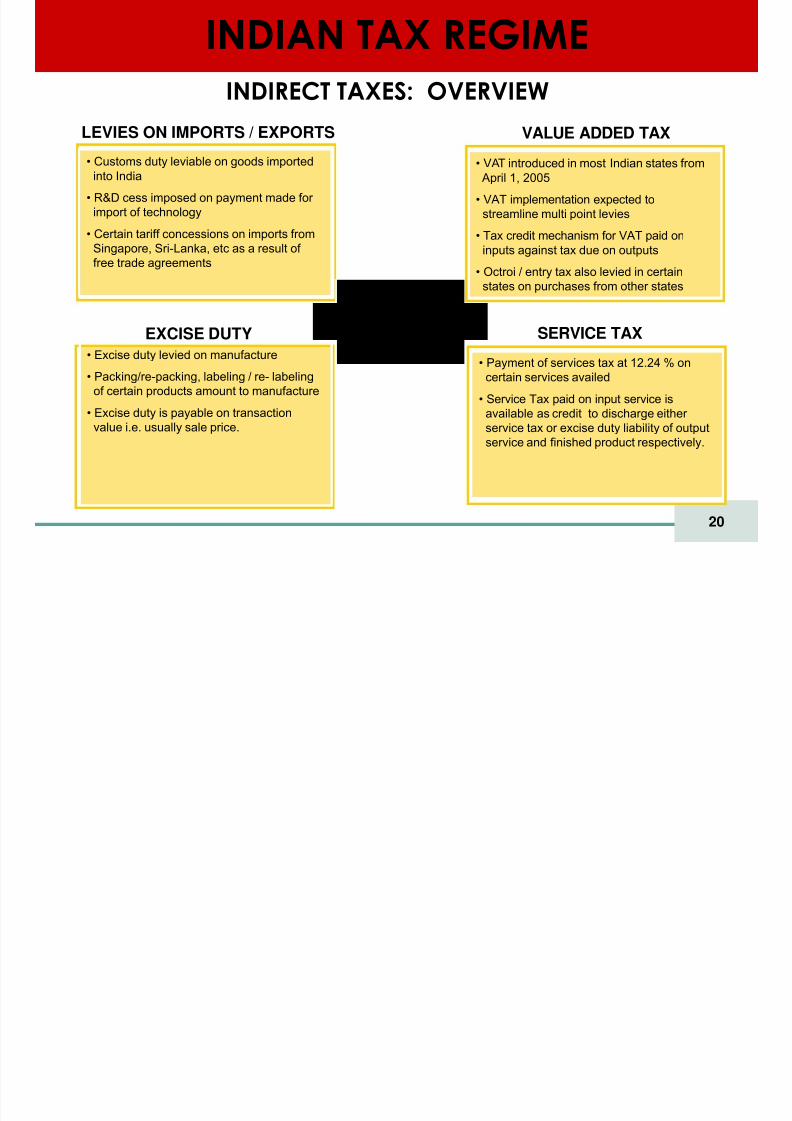

Indirect taxes• Payment of services tax at 12.24 % on

certain services availed• Service Tax paid on input service is

available as credit to discharge either service tax or excise duty liability of outputservice and finished product respectively.

• VAT introduced in most Indian states from April 1, 2005

• VAT implementation expected tostreamline multi point levies

• Tax credit mechanism for VAT paid on

inputs against tax due on outputs• Octroi / entry tax also levied in certain

states on purchases from other states

• Customs duty leviable on goods importedinto India

• R&D cess imposed on payment made for import of technology

• Certain tariff concessions on imports fromSingapore, Sri-Lanka, etc as a result of free trade agreements

EXCISE DUTY SERVICE TAX• Excise duty levied on manufacture

• Packing/re-packing, labeling / re- labelingof certain products amount to manufacture

• Excise duty is payable on transactionvalue i.e. usually sale price.

LEVIES ON IMPORTS / EXPORTS VALUE ADDED TAX

INDIAN TAX REGIMEINDIRECT TAXES: OVERVIEW

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 21/65

21

INDIAN TAX REGIME…

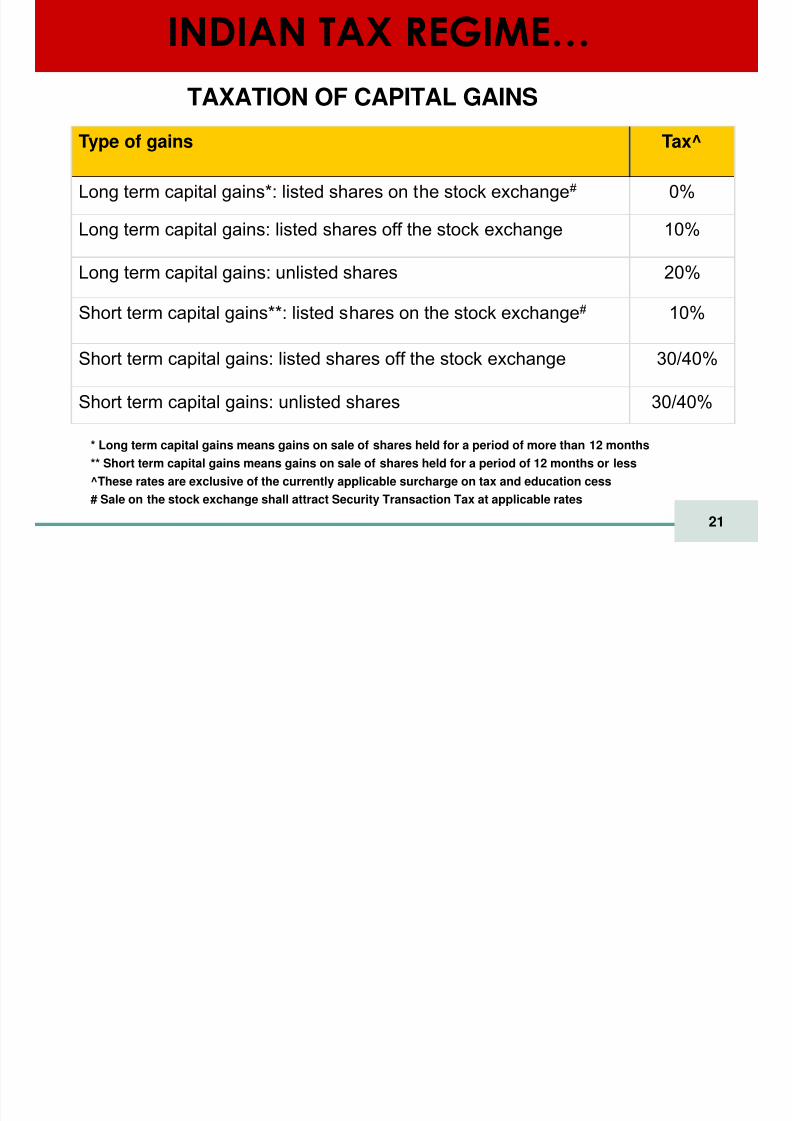

Type of gains Tax^

Long term capital gains*: listed shares on the stock exchange # 0%

Long term capital gains: listed shares off the stock exchange 10%

Long term capital gains: unlisted shares 20%

Short term capital gains**: listed shares on the stock exchange # 10%

Short term capital gains: listed shares off the stock exchange 30/40%

Short term capital gains: unlisted shares 30/40%

TAXATION OF CAPITAL GAINS

* Long term capital gains means gains on sale of shares held for a period of more than 12 months** Short term capital gains means gains on sale of shares held for a period of 12 months or less^These rates are exclusive of the currently applicable surcharge on tax and education cess# Sale on the stock exchange shall attract Security Transaction Tax at applicable rates

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 22/65

22

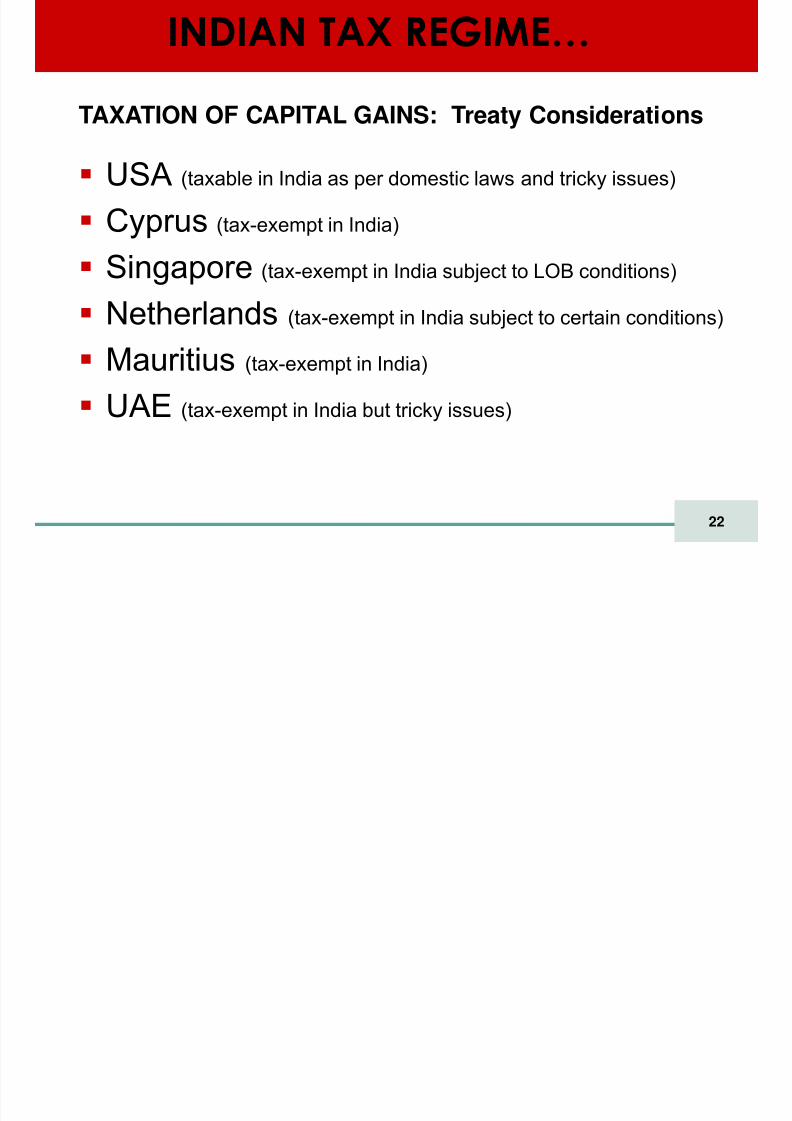

INDIAN TAX REGIME…

TAXATION OF CAPITAL GAINS: Treaty Considerations

USA (taxable in India as per domestic laws and tricky issues)

Cyprus (tax-exempt in India)

Singapore (tax-exempt in India subject to LOB conditions)

Netherlands (tax-exempt in India subject to certain conditions)

Mauritius (tax-exempt in India)

UAE (tax-exempt in India but tricky issues)

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 23/65

23

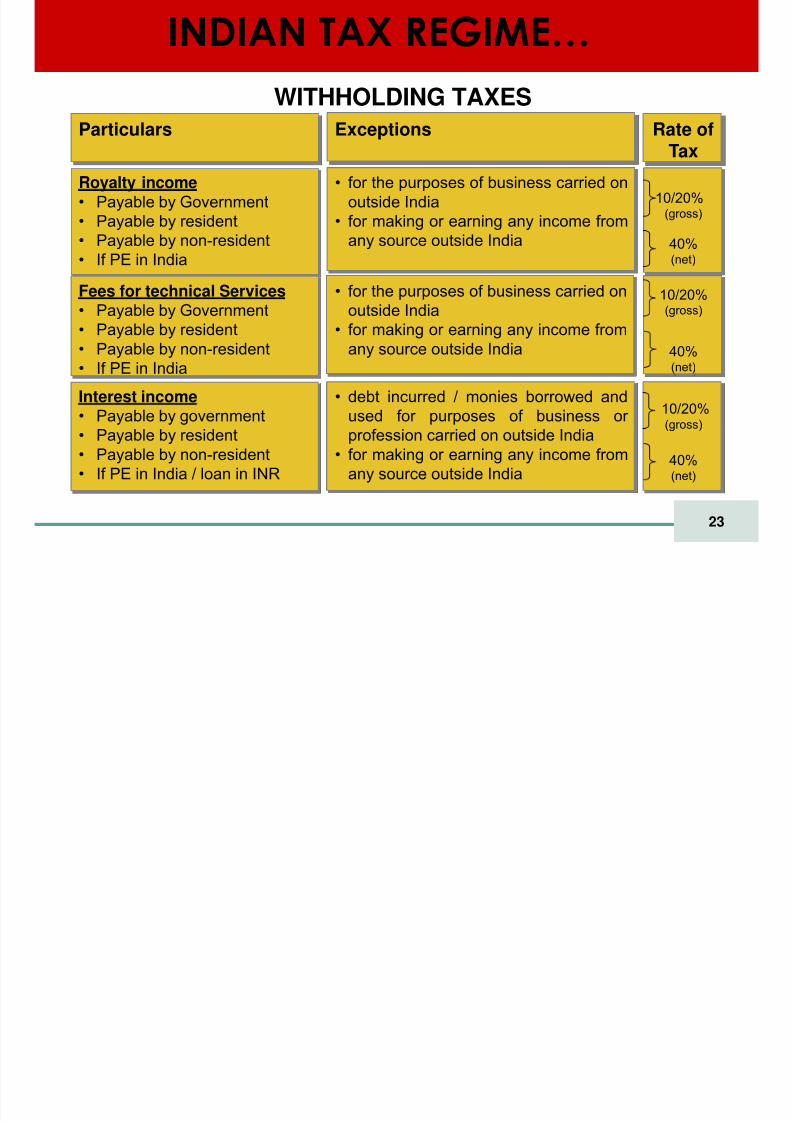

Royalty income• Payable by Government• Payable by resident• Payable by non-resident• If PE in India

• for the purposes of business carried onoutside India

• for making or earning any income fromany source outside India

10/20%(gross)

40%(net)

10/20%(gross)

40%(net)

Particulars Exceptions Rate ofTax

Interest income• Payable by government• Payable by resident• Payable by non-resident• If PE in India / loan in INR

• debt incurred / monies borrowed andused for purposes of business or profession carried on outside India

• for making or earning any income fromany source outside India

Fees for technical Services• Payable by Government• Payable by resident• Payable by non-resident• If PE in India

• for the purposes of business carried onoutside India

• for making or earning any income fromany source outside India

10/20%(gross)

40%(net)

INDIAN TAX REGIME… WITHHOLDING TAXES

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 24/65

24

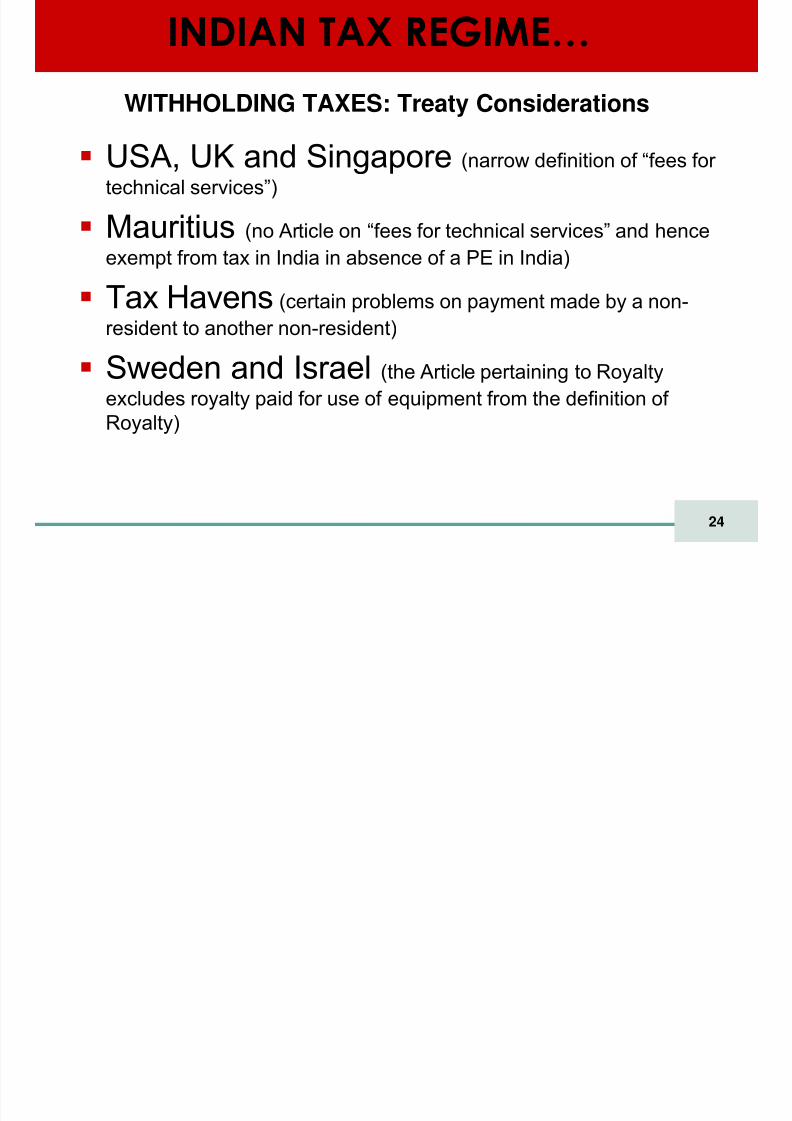

INDIAN TAX REGIME… WITHHOLDING TAXES: Treaty Considerations

USA, UK and Singapore (narrow definition of “fees for technical services”)

Mauritius (no Article on “fees for technical services” and hence

exempt from tax in India in absence of a PE in India)

Tax Havens (certain problems on payment made by a non-resident to another non-resident)

Sweden and Israel(the Article pertaining to Royalty

excludes royalty paid for use of equipment from the definition of Royalty)

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 25/65

25

INDIAN TAX REGIME…

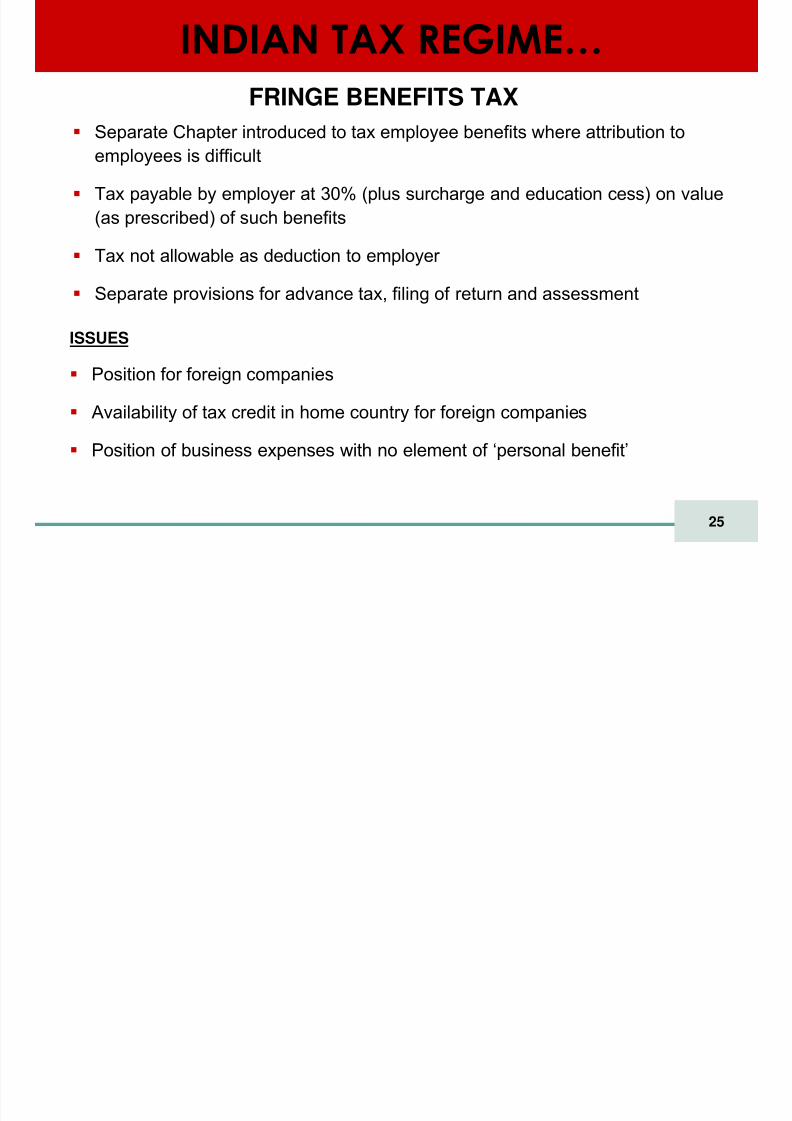

Separate Chapter introduced to tax employee benefits where attribution toemployees is difficult

Tax payable by employer at 30% (plus surcharge and education cess) on value(as prescribed) of such benefits

Tax not allowable as deduction to employer Separate provisions for advance tax, filing of return and assessment

ISSUES

Position for foreign companies

Availability of tax credit in home country for foreign companies

Position of business expenses with no element of „personal benefit‟

FRINGE BENEFITS TAX

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 26/65

26

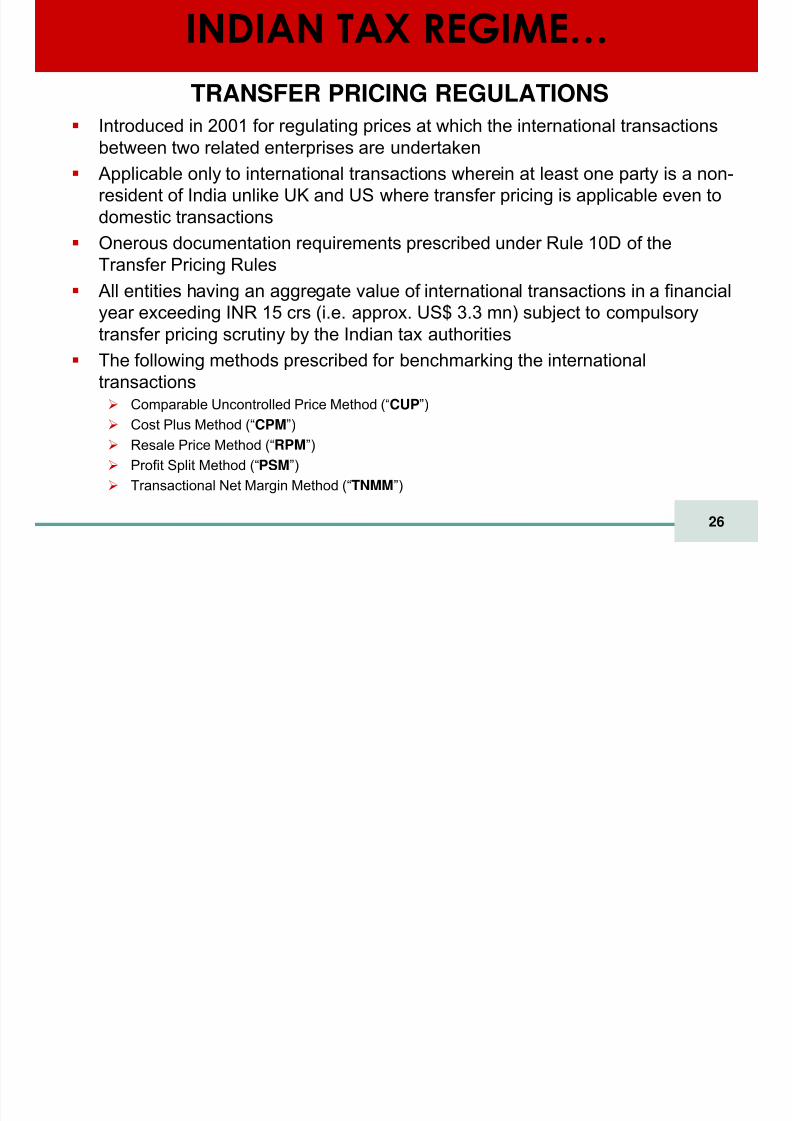

INDIAN TAX REGIME… TRANSFER PRICING REGULATIONS

Introduced in 2001 for regulating prices at which the international transactionsbetween two related enterprises are undertaken Applicable only to international transactions wherein at least one party is a non-resident of India unlike UK and US where transfer pricing is applicable even todomestic transactionsOnerous documentation requirements prescribed under Rule 10D of theTransfer Pricing Rules

All entities having an aggregate value of international transactions in a financialyear exceeding INR 15 crs (i.e. approx. US$ 3.3 mn) subject to compulsorytransfer pricing scrutiny by the Indian tax authoritiesThe following methods prescribed for benchmarking the international

transactions Comparable Uncontrolled Price Method (“ CUP ”) Cost Plus Method (“ CPM ”) Resale Price Method (“ RPM ”) Profit Split Method (“ PSM ”) Transactional Net Margin Method (“ TNMM”)

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 27/65

27

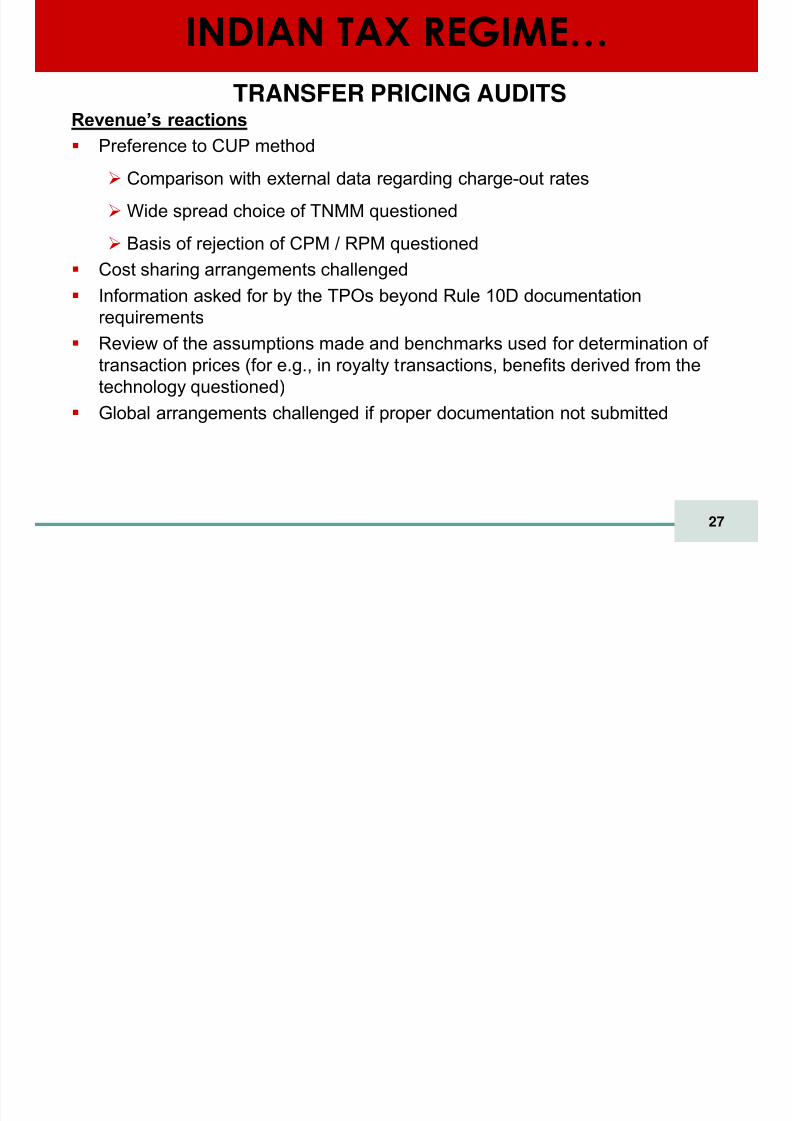

INDIAN TAX REGIME… TRANSFER PRICING AUDITS

Revenue’s reactions Preference to CUP method

Comparison with external data regarding charge-out rates

Wide spread choice of TNMM questioned

Basis of rejection of CPM / RPM questionedCost sharing arrangements challengedInformation asked for by the TPOs beyond Rule 10D documentationrequirementsReview of the assumptions made and benchmarks used for determination of transaction prices (for e.g., in royalty transactions, benefits derived from thetechnology questioned)Global arrangements challenged if proper documentation not submitted

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 28/65

28

INDIAN TAX REGIME…

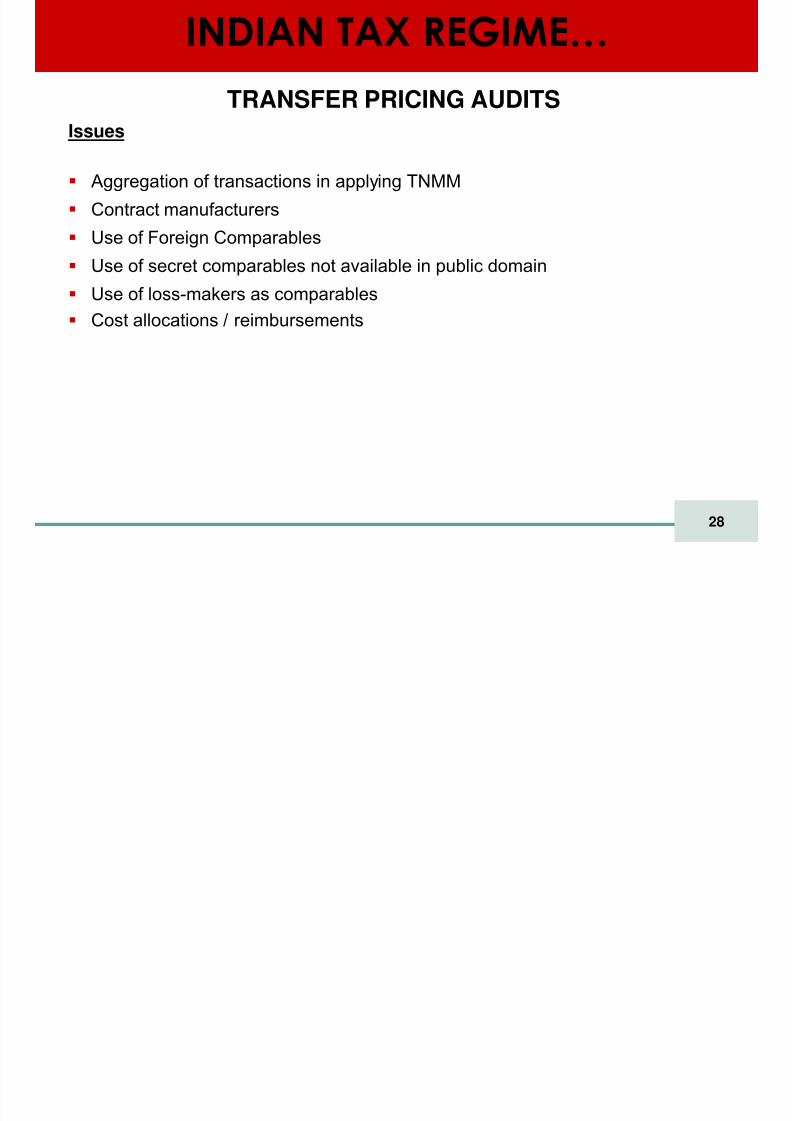

Issues

Aggregation of transactions in applying TNMMContract manufacturersUse of Foreign ComparablesUse of secret comparables not available in public domainUse of loss-makers as comparablesCost allocations / reimbursements

TRANSFER PRICING AUDITS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 29/65

29

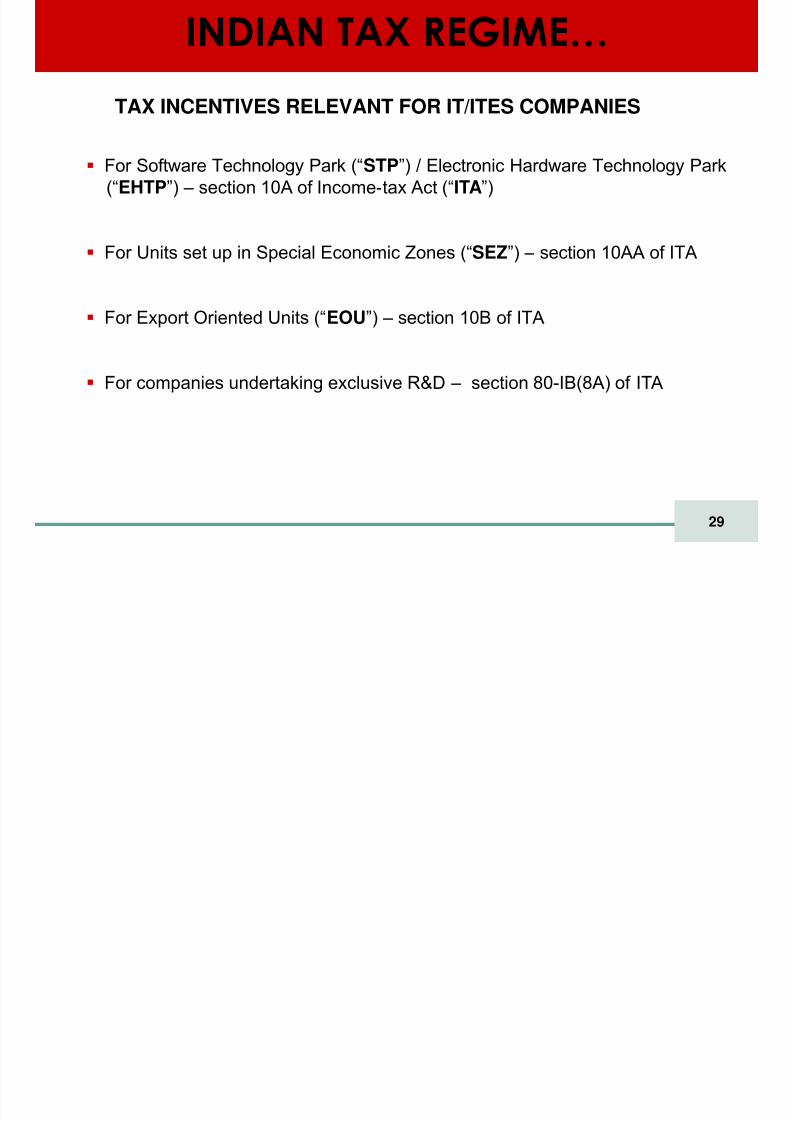

For Software Technology Park (“ STP ”) / Electronic Hardware Technology Park(“EHTP ”) – section 10A of Income- tax Act (“ ITA”)

For Units set up in Special Economic Zones (“ SEZ ”) – section 10AA of ITA

For Export Oriented Units (“ EOU ”) – section 10B of ITA

For companies undertaking exclusive R&D – section 80-IB(8A) of ITA

INDIAN TAX REGIME…

TAX INCENTIVES RELEVANT FOR IT/ITES COMPANIES

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 30/65

30

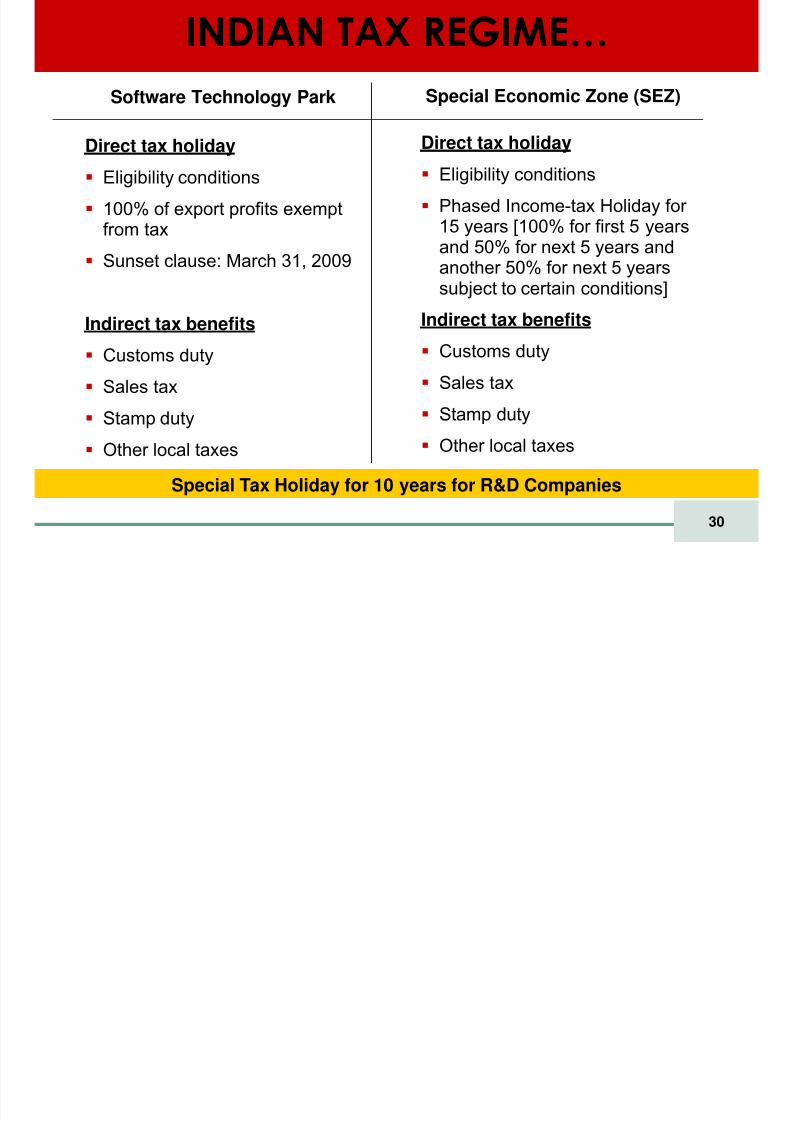

INDIAN TAX REGIME… Software Technology Park Special Economic Zone (SEZ)

Direct tax holiday

Eligibility conditions

100% of export profits exemptfrom tax

Sunset clause: March 31, 2009

Indirect tax benefits

Customs duty

Sales taxStamp duty

Other local taxes

Direct tax holiday

Eligibility conditions

Phased Income-tax Holiday for 15 years [100% for first 5 yearsand 50% for next 5 years andanother 50% for next 5 yearssubject to certain conditions]

Indirect tax benefits

Customs duty

Sales taxStamp duty

Other local taxes

Special Tax Holiday for 10 years for R&D Companies

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 31/65

31

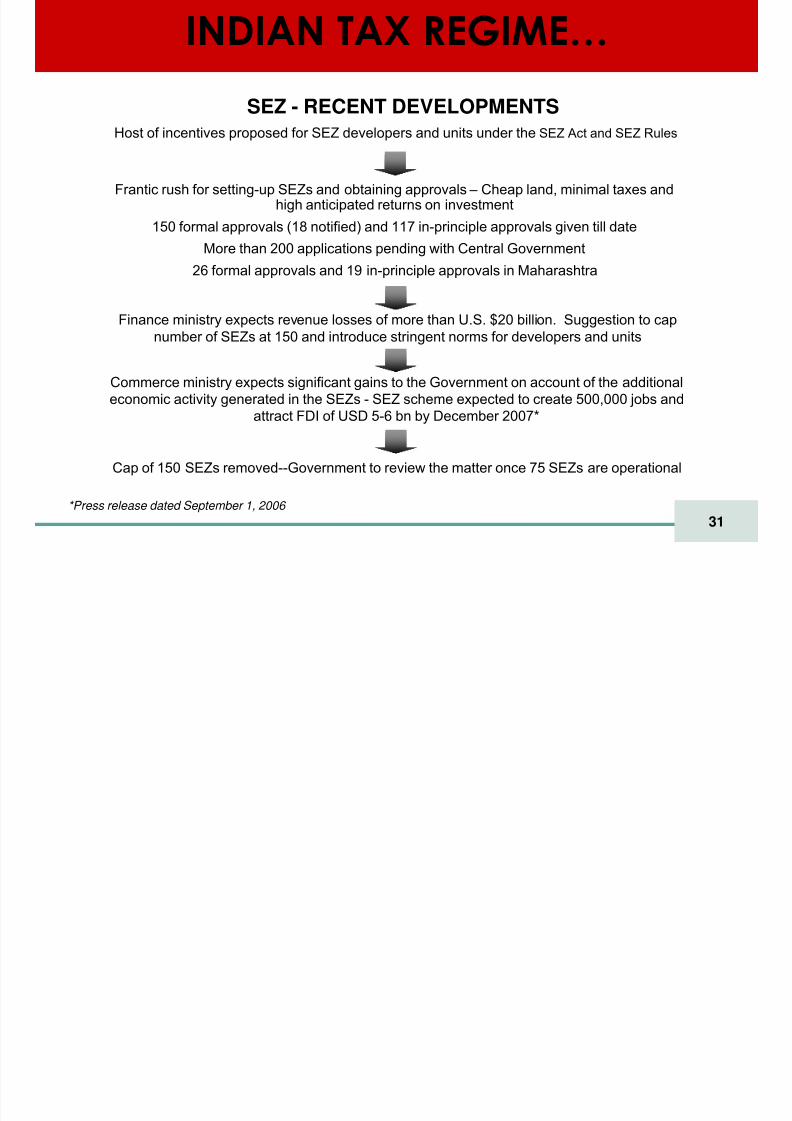

Host of incentives proposed for SEZ developers and units under the SEZ Act and SEZ Rules

Frantic rush for setting-up SEZs and obtaining approvals – Cheap land, minimal taxes andhigh anticipated returns on investment

150 formal approvals (18 notified) and 117 in-principle approvals given till dateMore than 200 applications pending with Central Government

26 formal approvals and 19 in-principle approvals in Maharashtra

*Press release dated September 1, 2006

Commerce ministry expects significant gains to the Government on account of the additionaleconomic activity generated in the SEZs - SEZ scheme expected to create 500,000 jobs andattract FDI of USD 5-6 bn by December 2007*

Finance ministry expects revenue losses of more than U.S. $20 billion. Suggestion to capnumber of SEZs at 150 and introduce stringent norms for developers and units

Cap of 150 SEZs removed--Government to review the matter once 75 SEZs are operational

INDIAN TAX REGIME…

SEZ - RECENT DEVELOPMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 32/65

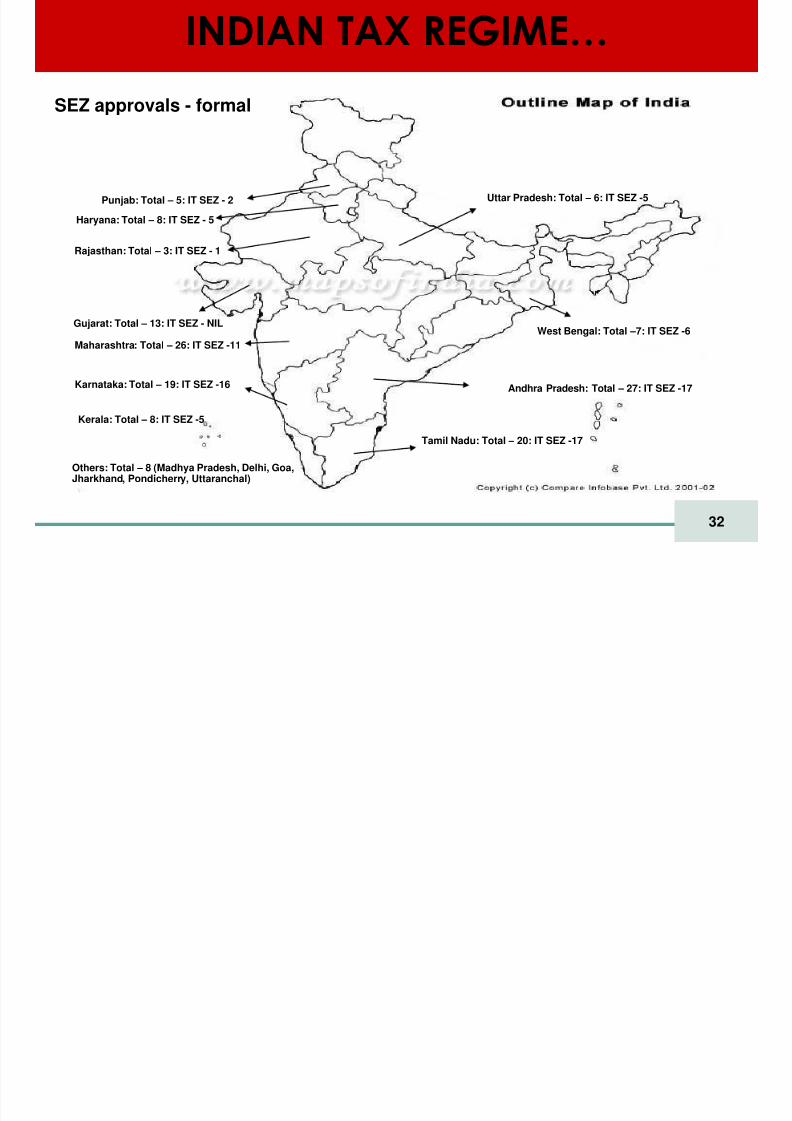

32

Andhra Pradesh: Total – 27: IT SEZ -17

Maharashtra: Total – 26: IT SEZ -11

Tamil Nadu: Total – 20: IT SEZ -17

Karnataka: Total – 19: IT SEZ -16

Gujarat: Total – 13: IT SEZ - NIL

Haryana: Total – 8: IT SEZ - 5

West Bengal: Total – 7: IT SEZ -6

Uttar Pradesh: Total – 6: IT SEZ -5Punjab: Total – 5: IT SEZ - 2

Rajasthan: Total – 3: IT SEZ - 1

Kerala: Total – 8: IT SEZ -5

Others: Total – 8 (Madhya Pradesh, Delhi, Goa,Jharkhand, Pondicherry, Uttaranchal)

INDIAN TAX REGIME…

SEZ approvals - formal

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 33/65

33

HOT ISSUES

Characterization of income

Royalties and fees for technical services

Capital gains

Permanent Establishment / Business Connection

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 34/65

34

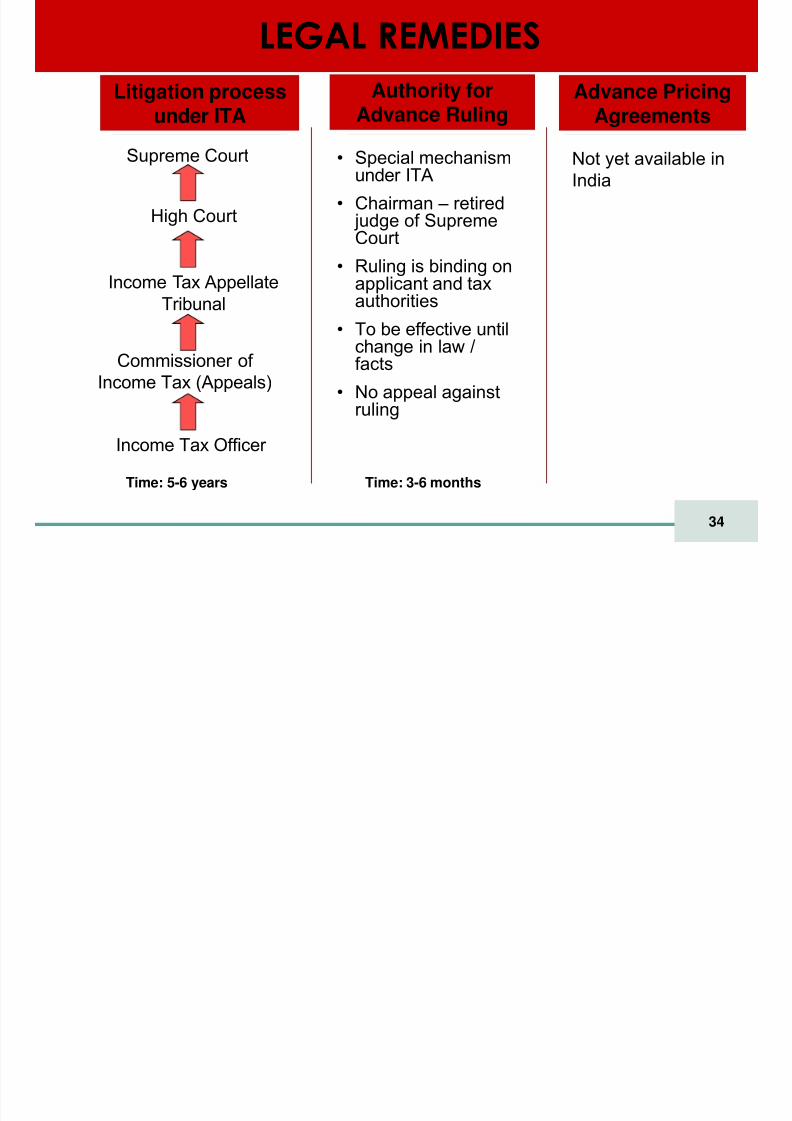

LEGAL REMEDIESLitigation process

under ITAAuthority for

Advance RulingAdvance Pricing

Agreements

Not yet available inIndia

Income Tax Officer

Commissioner of

Income Tax (Appeals)

Income Tax AppellateTribunal

Time: 5-6 years

• Special mechanismunder ITA

• Chairman – retired judge of SupremeCourt

• Ruling is binding onapplicant and taxauthorities

• To be effective untilchange in law /facts

• No appeal againstruling

Time: 3-6 months

High Court

Supreme Court

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 35/65

35

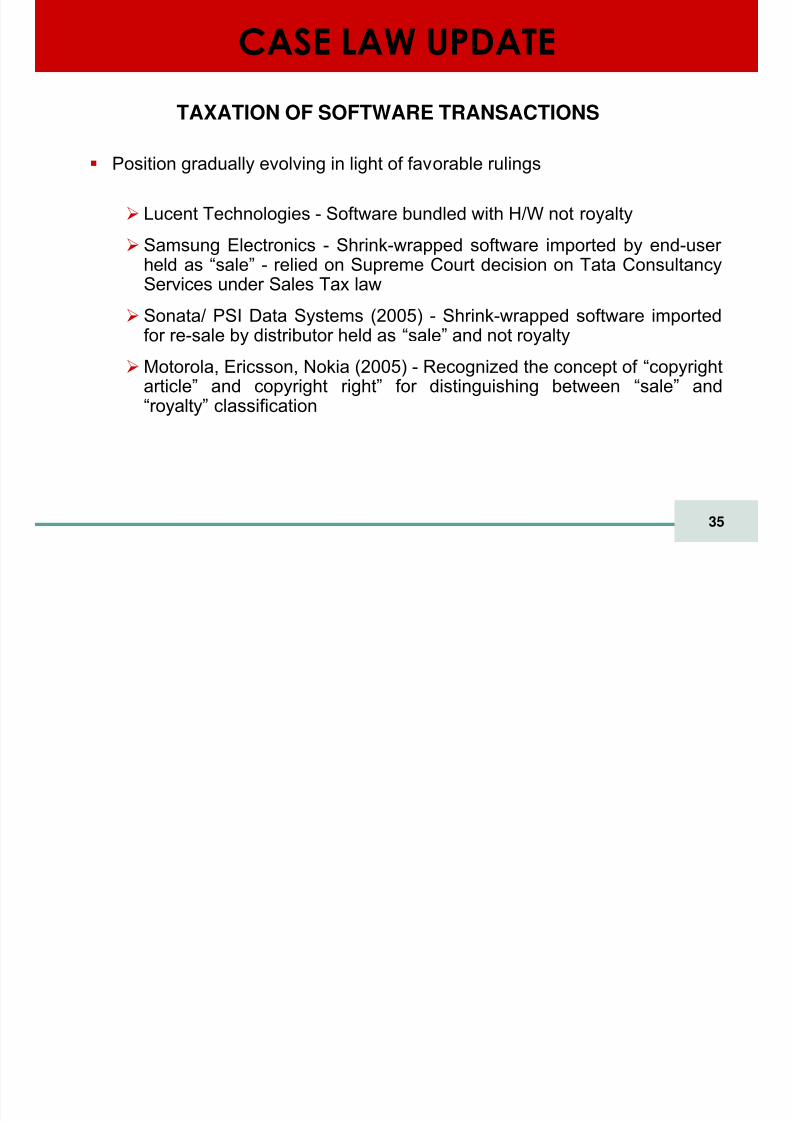

CASE LAW UPDATE

TAXATION OF SOFTWARE TRANSACTIONS

Position gradually evolving in light of favorable rulings

Lucent Technologies - Software bundled with H/W not royalty

Samsung Electronics - Shrink-wrapped software imported by end-user held as “sale” - relied on Supreme Court decision on Tata ConsultancyServices under Sales Tax law

Sonata/ PSI Data Systems (2005) - Shrink-wrapped software importedfor re-sale by distributor held as “sale” and not royalty

Motorola, Ericsson, Nokia (2005) - Recognized the concept of “copyright article” and copyright right” for distinguishing between “sale” and“royalty” classification

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 36/65

36

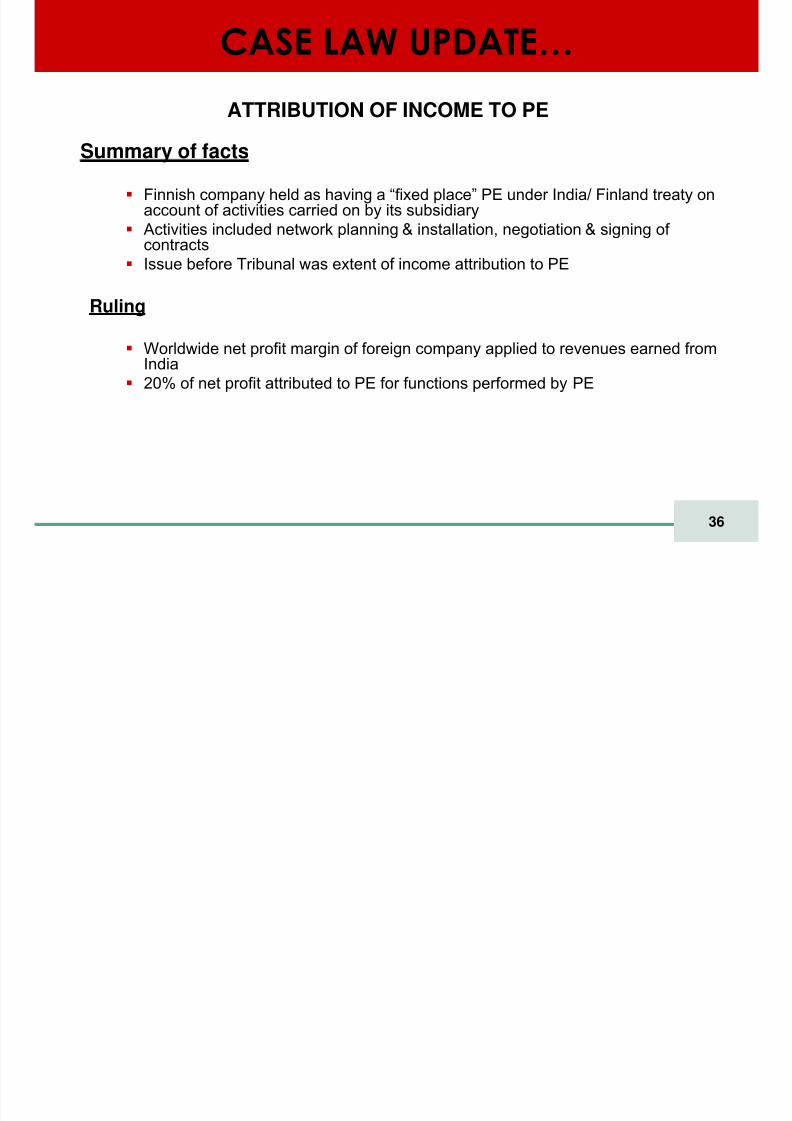

CASE LAW UPDATE…

ATTRIBUTION OF INCOME TO PE

Summary of facts

Finnish company held as having a “fixed place” PE under India/ Finland treaty onaccount of activities carried on by its subsidiary

Activities included network planning & installation, negotiation & signing of contractsIssue before Tribunal was extent of income attribution to PE

Ruling

Worldwide net profit margin of foreign company applied to revenues earned fromIndia

20% of net profit attributed to PE for functions performed by PE

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 37/65

37

CASE LAW UPDATE…

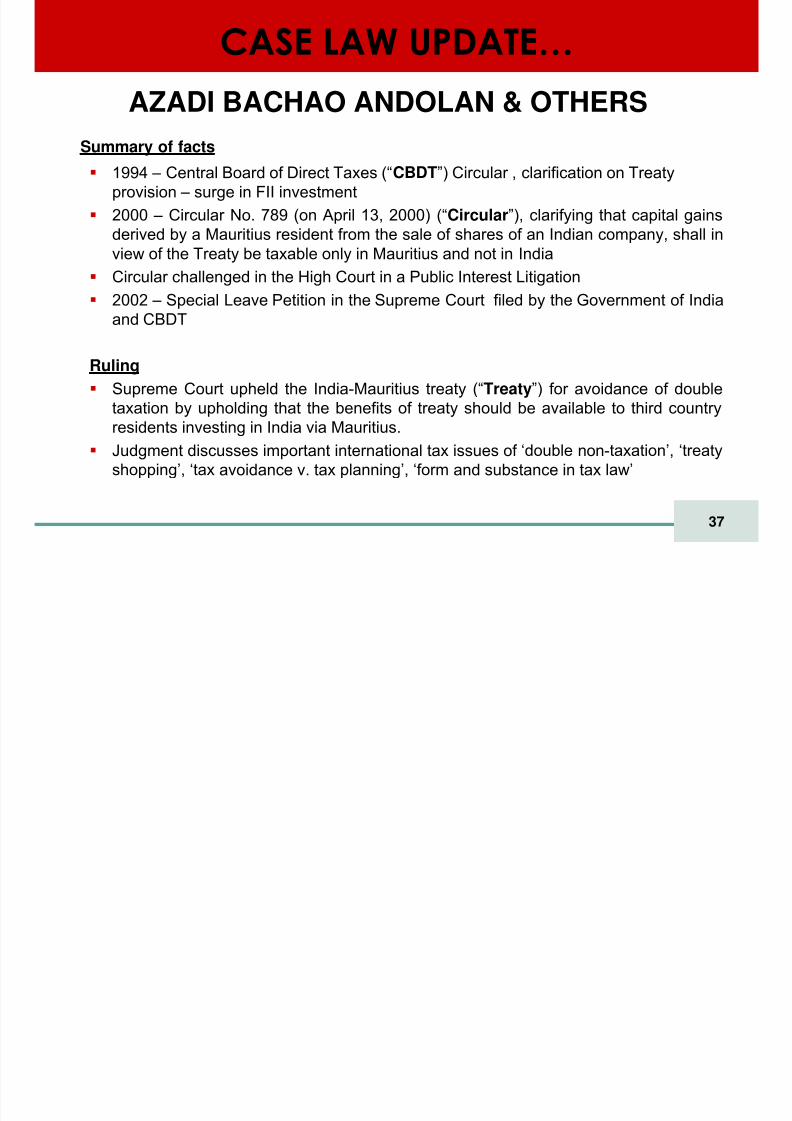

AZADI BACHAO ANDOLAN & OTHERSSummary of facts

1994 – Central Board of Direct Taxes (“ CBDT ”) Circular , clarification on Treatyprovision – surge in FII investment2000 – Circular No. 789 (on April 13, 2000) (“Circular ”), clarifying that capital gainsderived by a Mauritius resident from the sale of shares of an Indian company, shall in

view of the Treaty be taxable only in Mauritius and not in IndiaCircular challenged in the High Court in a Public Interest Litigation2002 – Special Leave Petition in the Supreme Court filed by the Government of Indiaand CBDT

Ruling

Supreme Court upheld the India-Mauritius treaty (“Treaty ”) for avoidance of doubletaxation by upholding that the benefits of treaty should be available to third countryresidents investing in India via Mauritius.Judgment discusses important international tax issues of „double non- taxation‟, „treaty shopping‟, „tax avoidance v. tax planning‟, „form and substance in tax law‟

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 38/65

38

RECENT ADVANCE TAX RULINGS

MORGAN STANLEY & CO INTERNATIONAL LTD

Summary of facts

USCo had outsourced certain services to an affiliate “captive” BPO Co in India USCo was to send personnel to provide “stewardship” services to BPO Co as

well as to work under direction of BPO CoQuestion before Authority for Advance Ruling (AAR) on whether USCo had aPE in India

Ruling

USCo does not have a “fixed place of business” PE as business of USCo is notcarried out through premises of BPO CoUSCo would have a PE under “Service PE” rule on account of deputationarrangement

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 39/65

39

RECENT ADVANCE TAX RULINGS…

DUN & BRADSTREET ESPANA S.A.

Summary of facts

Dun & Bradstreet (“ DB”)- a business information database which providesproducts including Business Information Reports (“ BIR”s) to businessesworldwideDB India, a subsidiary of DB SAME which is a tax resident of Spain,electronically purchased BIRs from DB SAME for sale in the Indian marketQuestions raised as to the characterization of income of DB SAME from India

Ruling

BIRs were copyright protected

Transaction involved sale of copyrighted good and not transfer of copyrightTherefore, income of DB SAME from electronic sale of BIRs to be treated as thebusiness profits of DB SAME in India, and not taxable in the absence of a PESeparately, it was held that DB India could not be said to be a PE of DB SAMEin India.

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 40/65

40

RECENT ADVANCE TAX RULINGS… AGENCY PE

Summary of facts

USCo engaged in business of international transportation servicesTransportation agreement between USCo and JVCo (India) for movement of packages within and outside IndiaJVCo to provide services to USCo for delivery of packages within India (inboundconsignment) and USCo to provide services to JVCo for delivery of packagesoutside India (outbound consignment)Question before AAR was if USCo would have a PE in India under the agencyrule

Ruling

JVCo would be regarded as an agent of USCo as it is acting for and on behalf of USCoDescription of the relationship as independent contractors in agreement notconclusiveJVCo “secures orders” for USCo both with regard to outbound consignments andinbound consignmentsUSCo would therefore have an agency PE on account of its relationship withJVCo

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 41/65

41

RECENT ADVANCE TAX RULINGS… Fidelity Advisors Series VIII

General Electric Pension Trust

Key Outcomes of the Rulings

Gains from trading in shares by FIIs may be regarded as business income which is nottaxable in India in the absence of a PE in IndiaDeterminative tests:

If seller holds security as stock-in-trade & not as capital investmentSubstantial nature of transactions, manner of maintaining books of accounts, magnitude of purchases & sales, purchases & sales ratiomotive of earning a profit versus objective to derive income by way of dividend, etc

Treaty benefits not available to a tax exempt US pension trust since it is not subject to

tax in US

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 42/65

42

Refreshment

Break

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 43/65

43

Structuring Issues and

Opportunities

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 44/65

44

STRUCTURING OF INVESTMENTSGeneral Structuring Considerations

Deferral vs. U.S. tax deductions?Is U.S. investor interested in maximizing deferral planning?

Is U.S. investor more interested in obtaining U.S. tax deductions – arelosses expected?

Management of contributions to IndCoWhat assets/cash? Consider § 367 issues.

Which entities in the group will make contributions?

Management of IP

Will IndCo own any IP?License/royalty issues with respect IndCo

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 45/65

45

STRUCTURING OF INVESTMENTSGeneral Structuring Considerations

What are the U.S. investor‟s cash needs? Is there a need to maximize flexibility in terms of the movement of funds?

Can the U.S. investor tolerate a cash build-up in India from a businessstandpoint?

Influences type of investment

Debt/ Equity/Hybrids

What functions will IndCo perform with respect to the U.S. investor‟sbusiness operations?

R&DServices – direct/outsourced/combination

Sales

Manufacturing/production

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 46/65

46

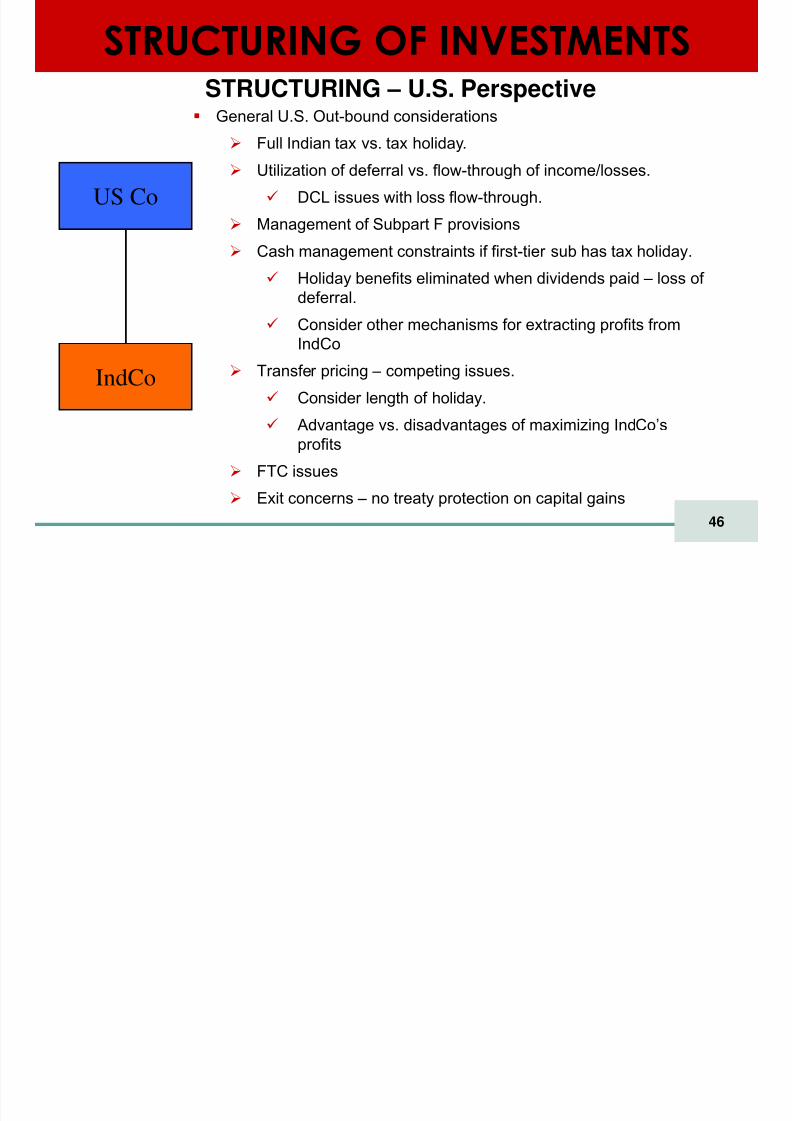

STRUCTURING OF INVESTMENTSSTRUCTURING – U.S. Perspective

General U.S. Out-bound considerations

Full Indian tax vs. tax holiday.

Utilization of deferral vs. flow-through of income/losses.

DCL issues with loss flow-through.

Management of Subpart F provisions

Cash management constraints if first-tier sub has tax holiday.

Holiday benefits eliminated when dividends paid – loss of deferral.

Consider other mechanisms for extracting profits fromIndCo

Transfer pricing – competing issues.

Consider length of holiday.

Advantage vs. disadvantages of maximizing IndCo‟sprofits

FTC issues

Exit concerns – no treaty protection on capital gains

US Co

IndCo

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 47/65

47

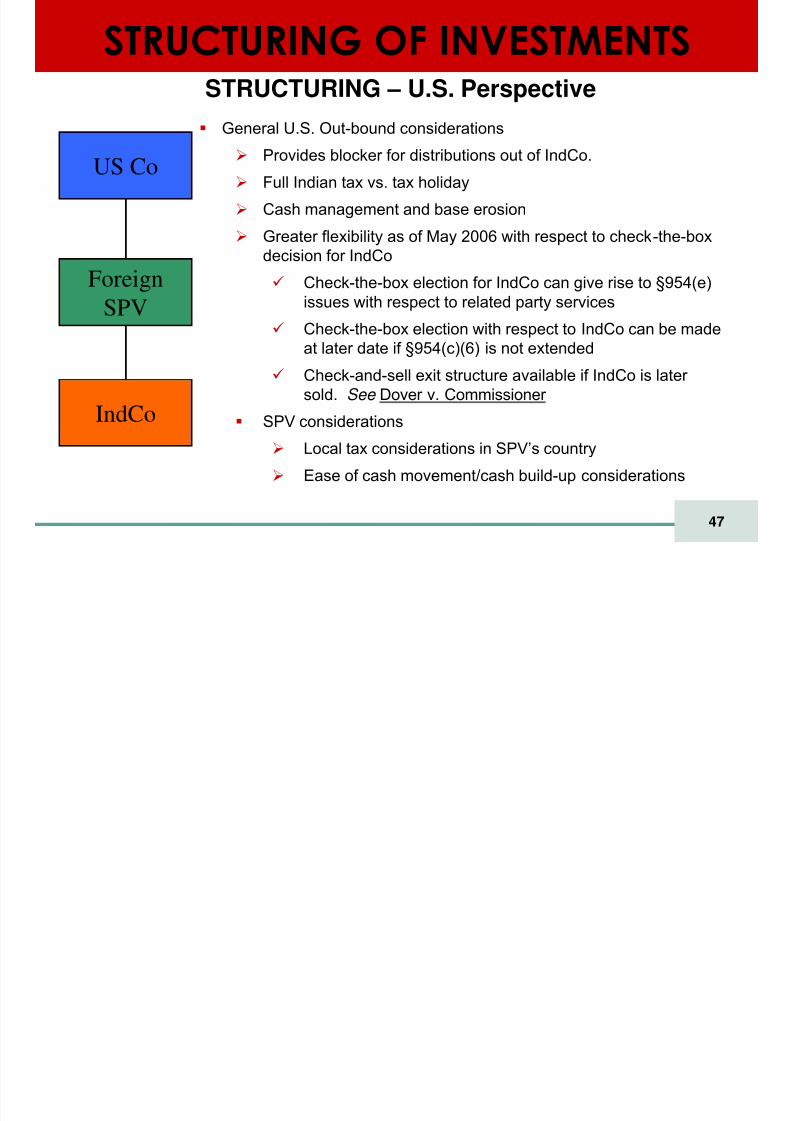

STRUCTURING OF INVESTMENTSSTRUCTURING – U.S. Perspective

General U.S. Out-bound considerationsProvides blocker for distributions out of IndCo.

Full Indian tax vs. tax holiday

Cash management and base erosion

Greater flexibility as of May 2006 with respect to check-the-box

decision for IndCoCheck-the-box election for IndCo can give rise to §954(e)issues with respect to related party services

Check-the-box election with respect to IndCo can be madeat later date if §954(c)(6) is not extended

Check-and-sell exit structure available if IndCo is later sold. See Dover v. Commissioner

SPV considerations

Local tax considerations in SPV‟s country

Ease of cash movement/cash build-up considerations

US Co

IndCo

ForeignSPV

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 48/65

48

STRUCTURING OF INVESTMENTS… COMMONLY CONSIDERED JURISDICTIONS FOR SPVS

Singapore

No tax on incoming or outgoing dividends. CECA with India

Netherlands

Participation exemption - no tax on incoming dividends and on sale of shares of the subsidiary

Cyprus

International Business Company regime. No tax on dividends and capital gainsreceived and no withholding tax on dividends and interest distributed

UK

Substantial shareholding (based on % of holding and length of ownership) – underlying tax credit is available

Mauritius

GBC 1 regime, effective 3% tax. Tax credit available in India for underlying taxesin respect of dividends. Credit in India for taxes “payable”

S C G O S S

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 49/65

49

STRUCTURING OF INVESTMENTS… COMPARISON OF COMMONLY USED TREATIESSingapore

LOB issuesBuy-Back could raise §301(c) type concerns in Singapore

Netherlands

Can provide repatriation benefitsComplexity on capital gainsRemoval of capital duty makes more attractive

Cyprus

Benefits for debt push-down in India Access to EU directivesU.S. business concerns can ariseMauritius

Continues to be preferred from a U.S. perspectiveChina-Mauritius developmentsIndian Supreme Court validated use of Mauritius

Amendment/withdrawal of India-Mauritius Treaty?

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 50/65

50

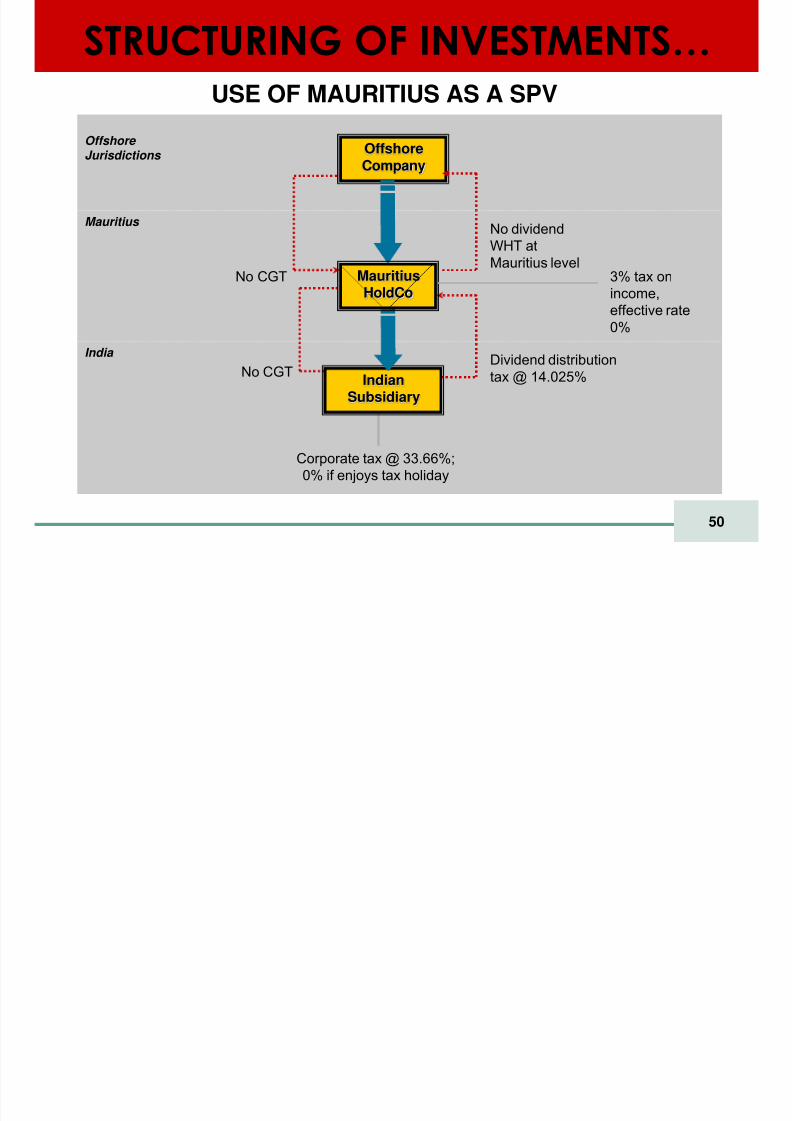

STRUCTURING OF INVESTMENTS… USE OF MAURITIUS AS A SPV

OffshoreCompany

No dividendWHT atMauritius level

Corporate tax @ 33.66%;0% if enjoys tax holiday

Dividend distributiontax @ 14.025%

3% tax onincome,effective rate0%

IndianSubsidiary

No CGT

No CGT

Offshore Jurisdictions

Mauritius

India

MauritiusHoldCo

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 51/65

51

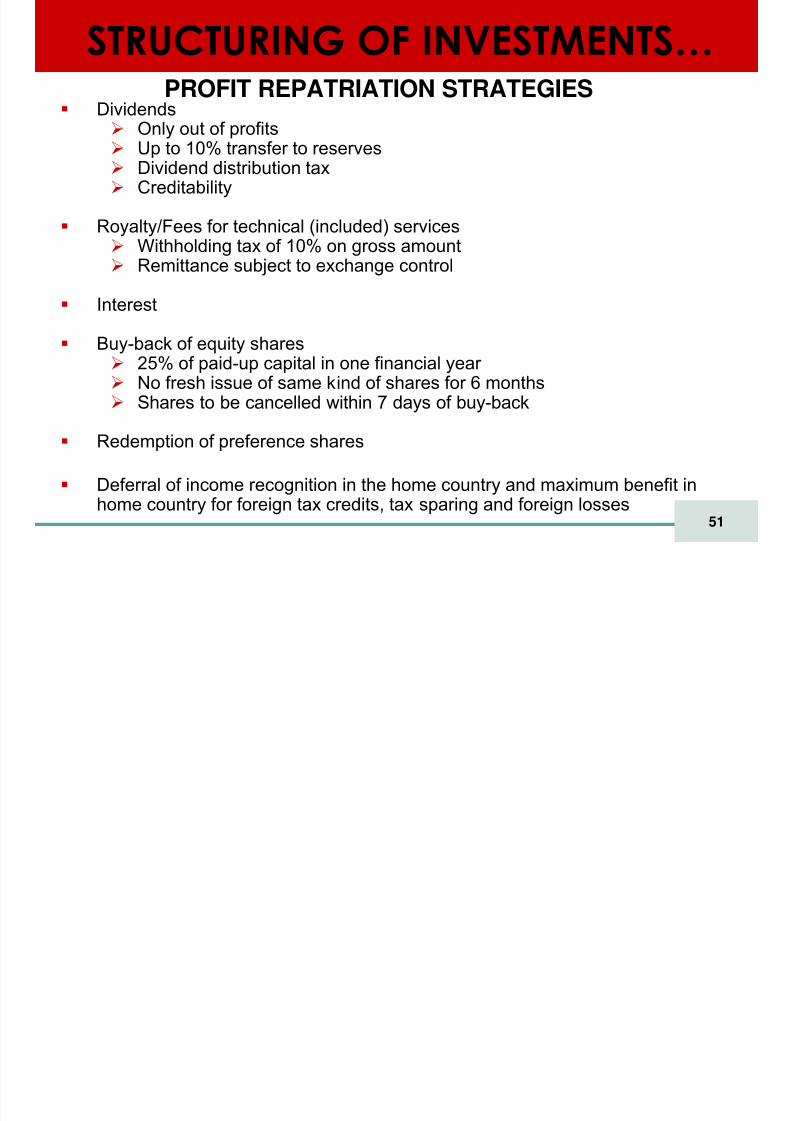

STRUCTURING OF INVESTMENTS… PROFIT REPATRIATION STRATEGIES

Dividends

Only out of profitsUp to 10% transfer to reservesDividend distribution taxCreditability

Royalty/Fees for technical (included) servicesWithholding tax of 10% on gross amountRemittance subject to exchange control

Interest

Buy-back of equity shares25% of paid-up capital in one financial year

No fresh issue of same kind of shares for 6 monthsShares to be cancelled within 7 days of buy-back

Redemption of preference shares

Deferral of income recognition in the home country and maximum benefit inhome country for foreign tax credits, tax sparing and foreign losses

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 52/65

52

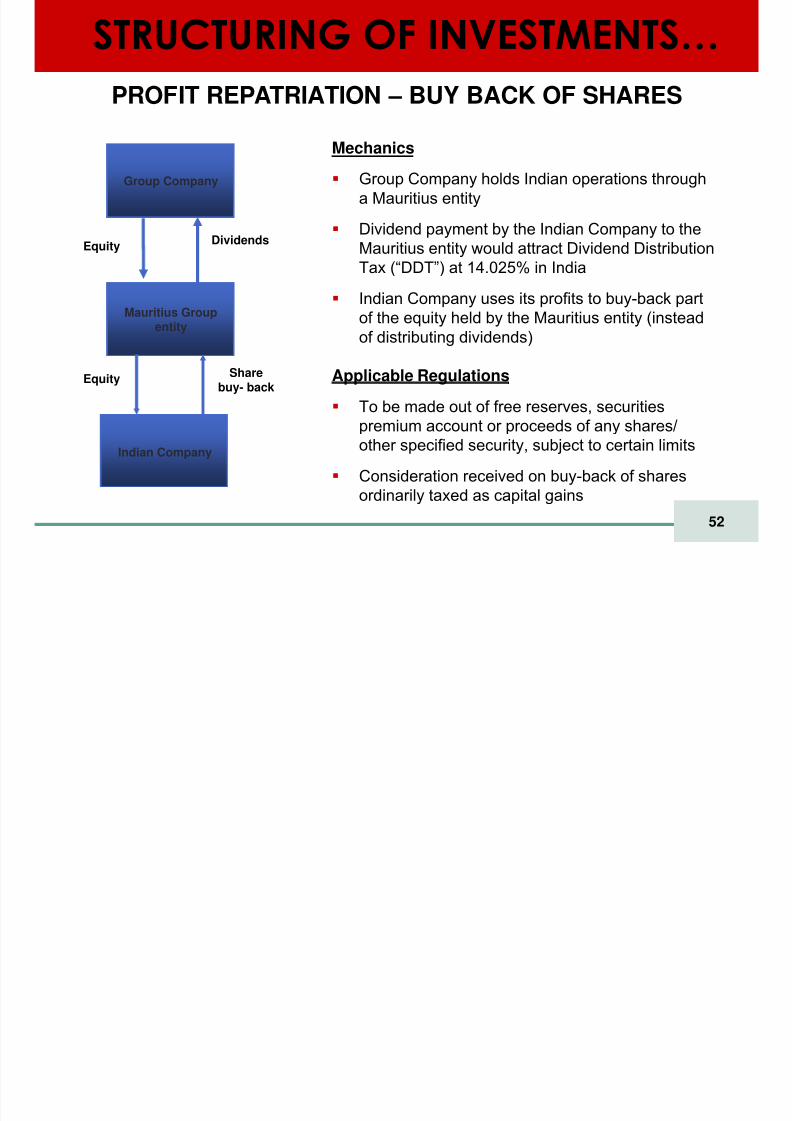

Group Company

Mauritius Groupentity

Share

buy- backEquity

Equity Dividends

Mechanics

Group Company holds Indian operations througha Mauritius entity

Dividend payment by the Indian Company to theMauritius entity would attract Dividend DistributionTax (“DDT”) at 14.025% in India

Indian Company uses its profits to buy-back partof the equity held by the Mauritius entity (insteadof distributing dividends)

Applicable Regulations

To be made out of free reserves, securitiespremium account or proceeds of any shares/other specified security, subject to certain limits

Consideration received on buy-back of sharesordinarily taxed as capital gains

Indian Company

PROFIT REPATRIATION – BUY BACK OF SHARES

STRUCTURING OF INVESTMENTS…

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 53/65

53

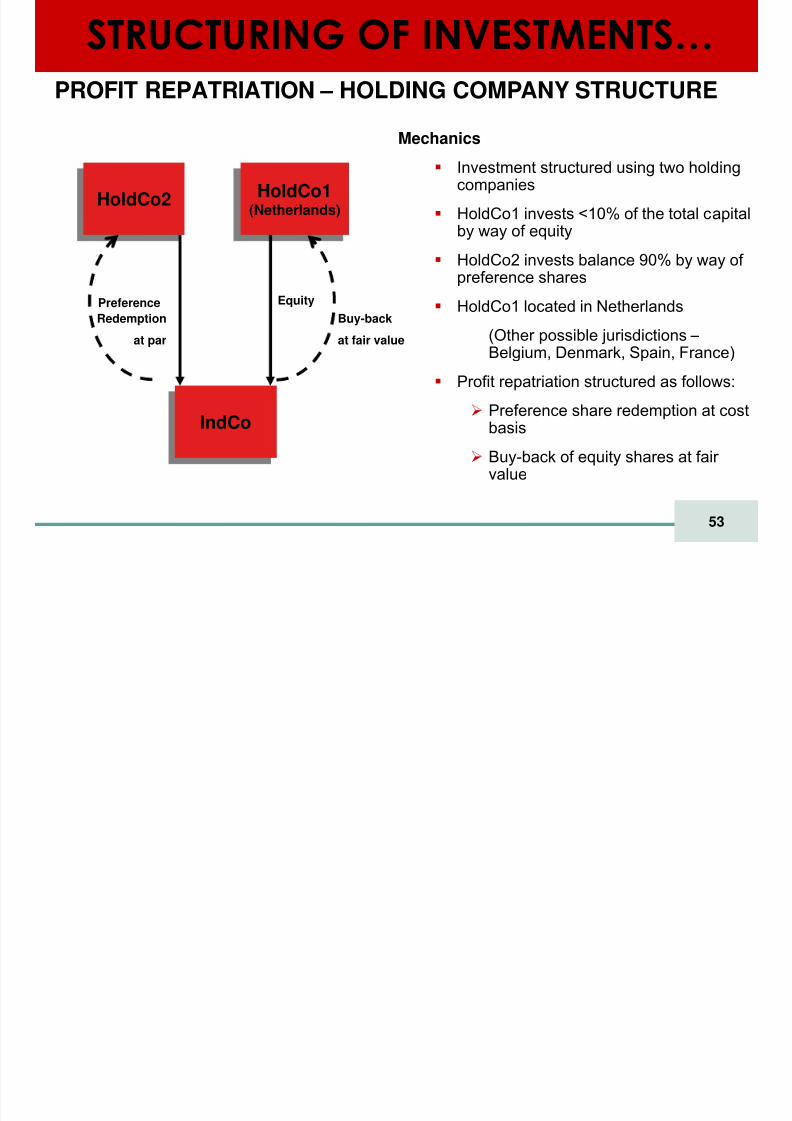

MechanicsInvestment structured using two holdingcompanies

HoldCo1 invests <10% of the total capitalby way of equity

HoldCo2 invests balance 90% by way of preference shares

HoldCo1 located in Netherlands

(Other possible jurisdictions – Belgium, Denmark, Spain, France)

Profit repatriation structured as follows:Preference share redemption at costbasis

Buy-back of equity shares at fair value

IndCo

HoldCo2 HoldCo1(Netherlands)

EquityPreferenceRedemption

at par

Buy-back

at fair value

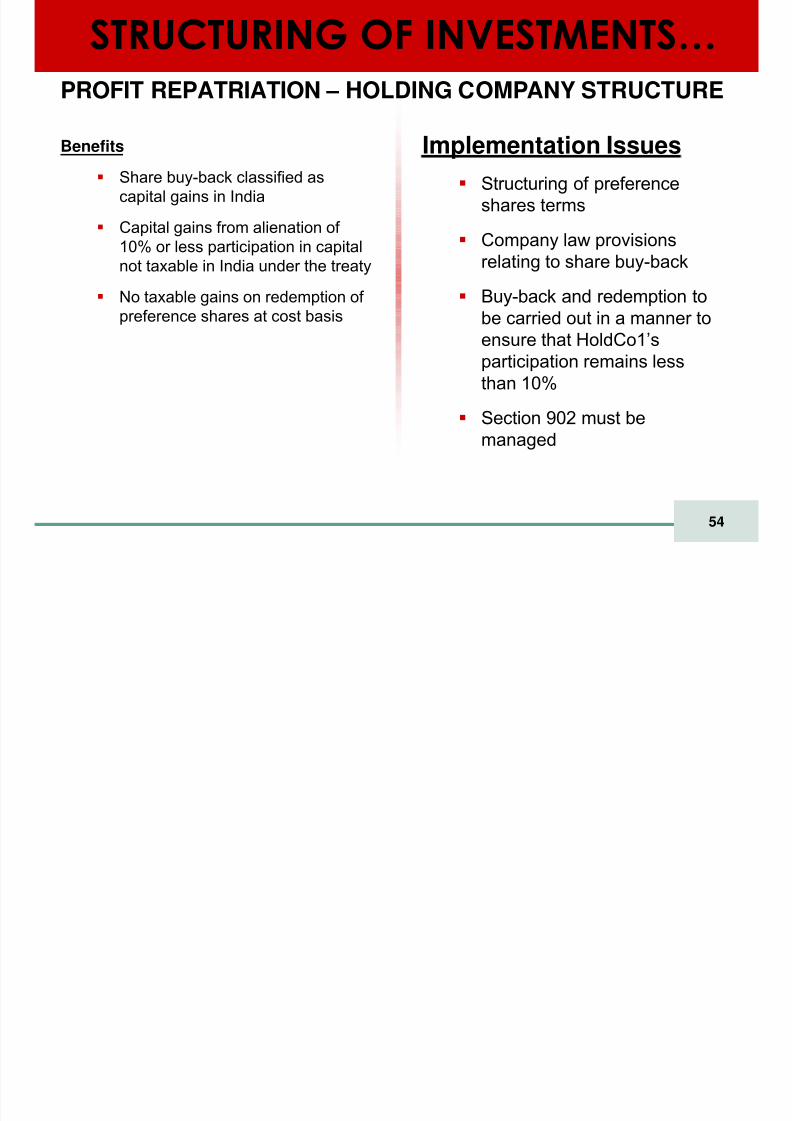

STRUCTURING OF INVESTMENTS… PROFIT REPATRIATION – HOLDING COMPANY STRUCTURE

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 54/65

54

Benefits

Share buy-back classified ascapital gains in India

Capital gains from alienation of 10% or less participation in capitalnot taxable in India under the treaty

No taxable gains on redemption of preference shares at cost basis

Implementation IssuesStructuring of preferenceshares terms

Company law provisions

relating to share buy-backBuy-back and redemption tobe carried out in a manner toensure that HoldCo1‟sparticipation remains less

than 10%Section 902 must bemanaged

STRUCTURING OF INVESTMENTS… PROFIT REPATRIATION – HOLDING COMPANY STRUCTURE

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 55/65

55

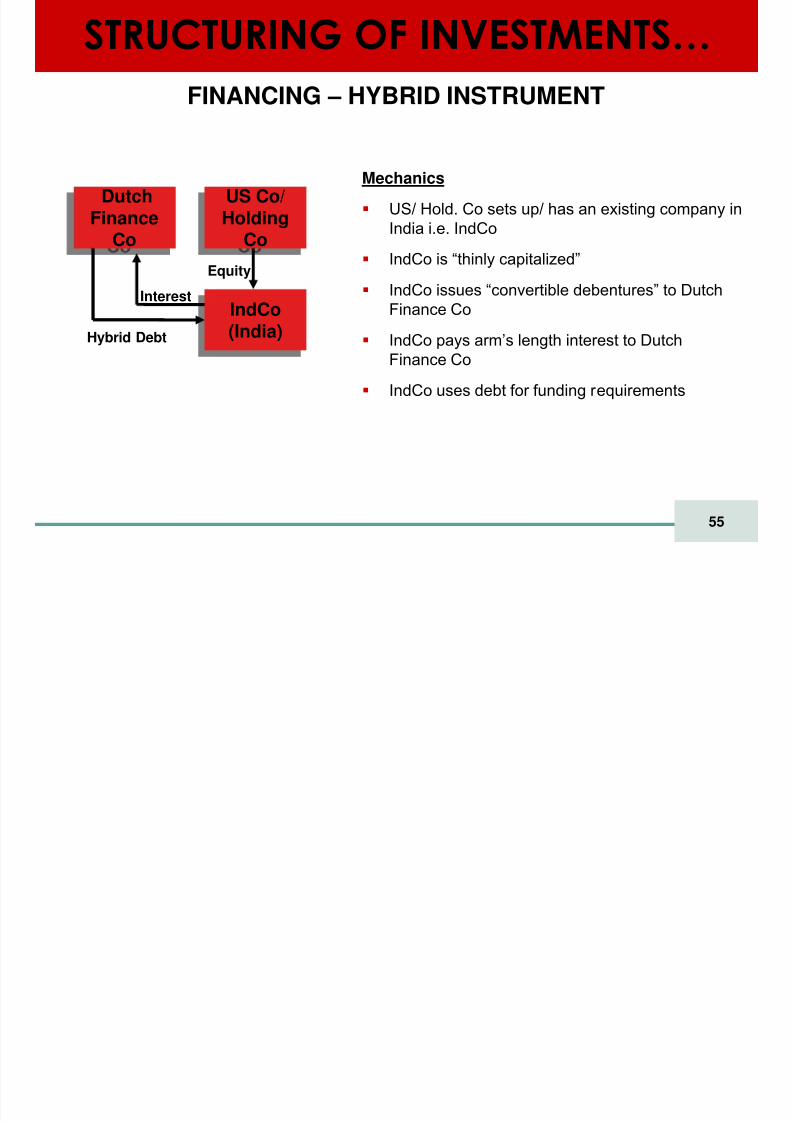

FINANCING – HYBRID INSTRUMENT

IndCo(India)

DutchFinance

Co

US Co/Holding

Co

Hybrid Debt

Interest

Equity

STRUCTURING OF INVESTMENTS…

Mechanics

US/ Hold. Co sets up/ has an existing company inIndia i.e. IndCo

IndCo is “thinly capitalized” IndCo issues “convertible debentures” to DutchFinance Co

IndCo pays arm‟s length interest to DutchFinance Co

IndCo uses debt for funding requirements

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 56/65

56

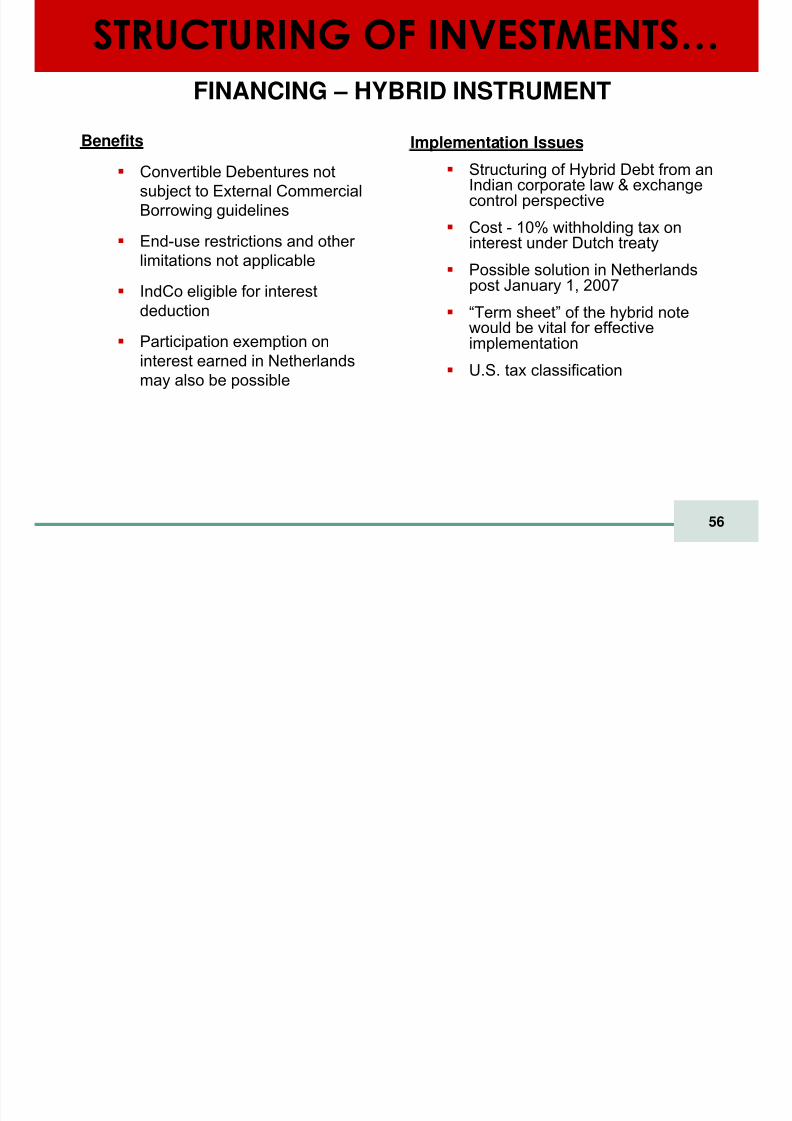

Implementation Issues

Structuring of Hybrid Debt from anIndian corporate law & exchangecontrol perspective

Cost - 10% withholding tax oninterest under Dutch treaty

Possible solution in Netherlandspost January 1, 2007

“Term sheet” of the hybrid notewould be vital for effectiveimplementation

U.S. tax classification

Benefits

Convertible Debentures notsubject to External CommercialBorrowing guidelines

End-use restrictions and other

limitations not applicableIndCo eligible for interestdeduction

Participation exemption oninterest earned in Netherlandsmay also be possible

STRUCTURING OF INVESTMENTS… FINANCING – HYBRID INSTRUMENT

US STRUCTURING CONSIDERATIONS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 57/65

57

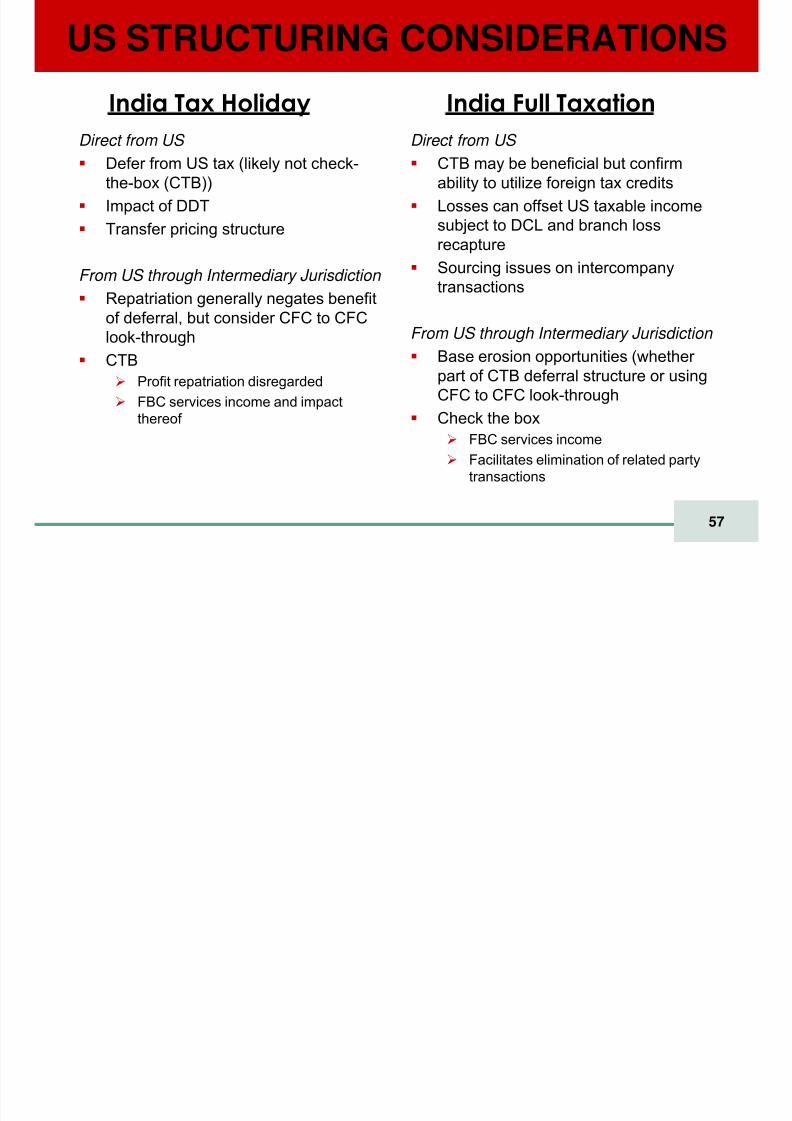

US STRUCTURING CONSIDERATIONS

Direct from US Defer from US tax (likely not check-the-box (CTB))Impact of DDTTransfer pricing structure

From US through Intermediary Jurisdiction Repatriation generally negates benefitof deferral, but consider CFC to CFClook-throughCTB

Profit repatriation disregardedFBC services income and impactthereof

Direct from US CTB may be beneficial but confirmability to utilize foreign tax creditsLosses can offset US taxable incomesubject to DCL and branch lossrecaptureSourcing issues on intercompanytransactions

From US through Intermediary Jurisdiction Base erosion opportunities (whether part of CTB deferral structure or usingCFC to CFC look-throughCheck the box

FBC services incomeFacilitates elimination of related partytransactions

India Tax Holiday India Full Taxation

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 58/65

58

STRUCTURING OF INVESTMENTSManaging U.S. Deferral

A popular planning option for managing Subpart F has been to makea disregarded entity election for IndCo in SPV structure

Enables taxpayer to maintain deferral with respect to dividenddistributions from IndCo to SPV

This planning technique can give rise to issues with respect to theapplication and management of §954(e) with respect to related partyservice activities

Potentially problematic with respect to the application of the Branchrule of §954(d)(2)

Also applicable to “Super Holdco” structures

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 59/65

59

STRUCTURING OF INVESTMENTSManaging U.S. Deferral

Significantly greater flexibility following the introduction of §954(c)(6)in May of 2006

Exception to FPHCI provisions – provides look-through treatment withrespect to dividends, interest, rents, and royalties received fromrelated party CFCs

Impacts check-the-box decisions with respect to SPV structures

Now consider delay of check-the-box elections until §954(c)(6) sunsets.

Consider restructuring out of prior check-the-box elections to the extentthere is an exposure to §954(e)

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 60/65

60

STRUCTURING OF INVESTMENTS

U.S. Issues with Respect to Managing IP Ownership

IP ownership with respect to R&D functions performed by IndCo canpresent issues from both a business and U.S. tax standpoint

Will IndCo own any IP rights?

What entities within the corporate group will contract with IndCo for theperformance of contract R&D functions

Issues can arise under proposed §482 service/intellectual propertyregulations

Services can be transmuted into deemed IP transfers

Consider the use of cost-sharing structuresProposed cost-sharing regulations are problematic, even with respect toforeign-to-foreign cost-sharing structures

STRUCTURING OF INVESTMENTS

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 61/65

61

STRUCTURING OF INVESTMENTSTAX EFFICIENT EXIT

Sale of shares of the Indian entityConsider “check -and- sell” option in SPV structure if IndCo notcharacterized as a disregarded entity for U.S. purposes

Sale of assets of the Indian entity

Sale of shares of the immediate Parent company in case of globalrestructuring

Buy-back of equity shares by the Indian entity

Redemption of preference shares

Liquidation of the Indian entity

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 62/65

Acquisition Planning

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 63/65

63

Acquisition Planning… INDIAN CONSIDERATIONS

Regulatory IssuesCarryover of incentives/holidays and other tax attributes

Special rulesMergersDemergersSlump sales

Legal integration into global structureSale of assets followed by liquidationMerger / amalgamation

Acquisition Planning

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 64/65

64

Acquisition Planning… Growing Interest in Inversion Transactions

Recent trend of private U.S. companies seeking access to Indian capitalmarket, which applies lower-thresholds for public offerings

U.S. tax issues under §§ 367 and 7874 need to be managed

US Private

Co

IndCo

Shareholders

RestructuringUS Private

Co

IndCo

Shareholders

New IndCo

7/31/2019 TAB 5 Bassett, Desai, Gill, Malik

http://slidepdf.com/reader/full/tab-5-bassett-desai-gill-malik 65/65

THANK YOUNishith DesaiNishith Desai & AssociatesMumbai, [email protected]

Barton BassettFenwick & West LLPMountain [email protected]

David GillErnst & Young LLPSan [email protected]

Gagan MalikErnst & Young LLPSan [email protected]