SHANGHAI · shanghai office market report q1 2016 上海写字楼市场报告 2016 第一季度...

8

SHANGHAI OFFICE MARKET REPORT Q1 2016 上海写字楼市场报告 2016 第一季度 RESEARCH 研究报告

Transcript of SHANGHAI · shanghai office market report q1 2016 上海写字楼市场报告 2016 第一季度...

SHANGHAIOFFICE MARKET REPORT Q1 2016上海写字楼市场报告 2016 第一季度

RESEARCH 研究报告

2

In Q1, Shanghai’s Grade-A office rents remained on an upward trend (See Table 1).

Net absorptions in emerging business districts doubled to 150,000 sqm compared with the previous quarter.

In Q1, office space demand from financial and consultancy firms was vigorous.

Many multinational corporations (MNCs) have scheduled to relocate away from core CBD in 2016, which will drive up the vacancy rates in core CBD. Rental growth in core CBD is expected to slow down in the second half of 2016. Rents are set to increase 2% in the second quarter (Q2)

SHANGHAI GRADE-A OFFICE MARKET BUOYANT IN Q1 WITH VIGOROUS LEASING DEMANDIn the first quarter (Q1) of 2016, there was approximately 100,000 sqm of new supply in Shanghai’s Grade-A office market (see Table 1).

and 6% in the coming year.

In Q1, Shanghai’s investment market remained active with an en-bloc office transaction recorded in core CBD.

The Shanghai office market will witness over two million sqm of new supply in 2016. Rentals are expected to face pressure due to the huge supply.

Several office buildings are scheduled to complete in secondary and emerging business districts in Q2, providing approximately 400,000 sqm of new supply.

TABLE 1Shanghai Grade-A office market indicators

Indicator Q1 2016 figure Q-o-Q change Outlook(Q2 2016)

New supply 100,000 sqm ↓ 85.3% ↗

Rental RMB9.6 / sqm / day ↑ 2.3% ↗

Vacancy rate 4.2% ↓ 0.6 percentage point ↗

Price RMB60,330 / sqm ↑ 3.7% ↗

Yield 5.8% ↓ 0.1 percentage point ↔

Source: Knight Frank Research

3

RESEARCHSHANGHAI OFFICE MARKET REPORT Q1 2016

2007 20112009 20132008 20122010 2014 2015

TABLE 2Grade-A office market indicators, Q1 2016

Submarket Rent(RMB / sqm / day)

Rent % change (Q-o-Q)

Vacancy rate

Vacancy rate percentage point change (Q-o-Q)

Huangpu 9.8 ↑ 2.1% 5.3% ↑ 0.6

Jing’an 11.0 ↑ 0.9% 4.4% ↑ 1.3

Pudong 10.7 ↑ 1.9% 2.4% ↑ 2.0

Xuhui 9.0 ↑ 1.1% 6.1% ↑ 3.3

Changning 7.7 ↔ 4.9% ↓ 0.5

Source: Knight Frank Research

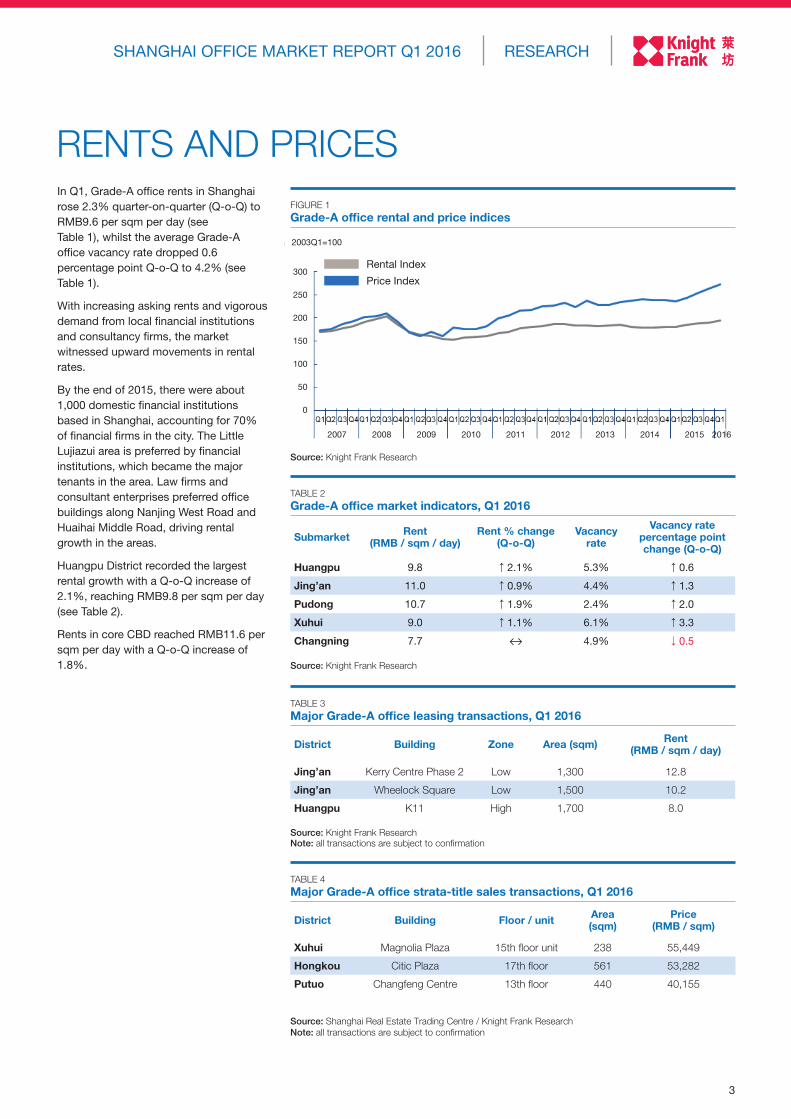

In Q1, Grade-A office rents in Shanghai rose 2.3% quarter-on-quarter (Q-o-Q) to RMB9.6 per sqm per day (see Table 1), whilst the average Grade-A office vacancy rate dropped 0.6 percentage point Q-o-Q to 4.2% (see Table 1).

With increasing asking rents and vigorous demand from local financial institutions and consultancy firms, the market witnessed upward movements in rental rates.

By the end of 2015, there were about 1,000 domestic financial institutions based in Shanghai, accounting for 70% of financial firms in the city. The Little Lujiazui area is preferred by financial institutions, which became the major tenants in the area. Law firms and consultant enterprises preferred office buildings along Nanjing West Road and Huaihai Middle Road, driving rental growth in the areas.

Huangpu District recorded the largest rental growth with a Q-o-Q increase of 2.1%, reaching RMB9.8 per sqm per day (see Table 2).

Rents in core CBD reached RMB11.6 per sqm per day with a Q-o-Q increase of 1.8%.

RENTS AND PRICES

Source: Knight Frank Research

TABLE 3Major Grade-A office leasing transactions, Q1 2016

District Building Zone Area (sqm) Rent(RMB / sqm / day)

Jing’an Kerry Centre Phase 2 Low 1,300 12.8

Jing’an Wheelock Square Low 1,500 10.2

Huangpu K11 High 1,700 8.0

Source: Knight Frank ResearchNote: all transactions are subject to confirmation

TABLE 4Major Grade-A office strata-title sales transactions, Q1 2016

District Building Floor / unit Area (sqm)

Price (RMB / sqm)

Xuhui Magnolia Plaza 15th floor unit 238 55,449

Hongkou Citic Plaza 17th floor 561 53,282

Putuo Changfeng Centre 13th floor 440 40,155

Source: Shanghai Real Estate Trading Centre / Knight Frank ResearchNote: all transactions are subject to confirmation

FIGURE 1Grade-A office rental and price indices

Rental Index

Price Index

2003Q1=100

300

200

100

250

150

50

0

2016

4

The new supply of Grade-A office space decreased 67.8% in Q1 year on year. Only two office buildings were completed, including UOB Building in the Little Lujiazui area, providing 30,000 sqm of office space, and Technology Innovation Tower Phase II in Caohejing, which brought approximately 70,000 sqm to the market.

The Grade-A office vacancy rate remained low due to strong rental demand in emerging business districts. In Q1, net absorptions in emerging business districts doubled to 150,000 sqm compared with the previous quarter.

The Grade-A office market in core CBD is expected to face challenges brought about by the increasing vacant space left by relocated companies. Vacant offices at good locations with lower rents were absorbed more easily. For example, a law firm rented two floors in The Centre in Q1 previously occupied by WPP. Premium Grade-A office vacancies with high rents in core CBD took longer time to be absorbed amid an uncertain economic climate. Architecture consultant AECOM is scheduled to relocate from Wheelock Square in Nanjing West Road to Knowledge and Innovation Community in Wujiaochang in

In Q1, Shanghai’s investment market recorded two en-bloc transactions, with one of them located in core CBD, namely Evergo Tower in Huaihai Middle Road sold for RMB1.3 billion to Real Power Capital. Office buildings in core CBD became an appealing asset class to funds and developers, owing to their sustainable rental growth and low vacancy rates.

SUPPLY, TAKE-UP AND VACANCY

INVESTMENT MARKET

FIGURE 2Grade-A office supply, take-up and vacancy rate

Grade-A office supply (Left)

Grade-A office net absorption (Left)

Vacancy rate (Right)

Q2, Merck Sharp and Dohme China also relocated from Park Place to Caohejing Business Park as evidence of continuing trend to decentralise among foreign firms.

With the government increasing support to small and start-up businesses, co-working pattern from abroad has become increasingly popular in China, with its low rents and flexible lease terms attracting start-up companies. A buoyant local co-working market has attracted

many mature international brands to enter the China market. WeWork, the first co-working operator in the U.S, made its debut in China in Jing’an District, renting two floors covering 3,000 sqm in WE Creative Park. In the coming years, WeWork plans to set up two more offices in Shanghai to meet increasing leasing demand from start-ups. Meanwhile, 36Kr, another well-known local co-working operator, also rented 1,000 sqm of office space in Yangpu District.

Meanwhile, Sunac China acquired two residential projects totaling 53,756 sqm in the southern suburb of Pudong for RMB4.03 billion.

The new taxation policy, replacing business tax with a value added tax (VAT) for real estate, is expected to have a positive impact on the office sales market

by encouraging owner-occupation of office space, as enterprises are allowed to have a VAT deduction with taxes they pay for property purchase.

Source: Knight Frank Research

‘000 sqm

5

研究报告上海写字楼市场报告 2016年第一季度

第一季度,上海甲级写字楼租金继续上

涨(见表一)。

新兴商务区写字楼净吸纳面积达到15万

平方米,较上一季度增长一倍。

第一季度,来自于金融及咨询服务行业

的租赁需求旺盛。

多家跨国企业计划在年内搬离现有的

核心商务区写字楼,核心商务区空置

率将上升,导致市场租金在未来半年

升势放缓。第二季度写字楼租金涨幅

预计在2%左右,未来一年租金涨幅大

约为6%。

第一季度,投资市场持续活跃,核心商

务区录得一宗写字楼交易。

展望未来,2016年写字楼市场上将有

200多万平方米的新增供应面积,巨大

的新增供应将对租金上涨造成压力。

展望第二季度,预计次级以及新兴商务

区将有多栋写字楼竣工交付,新增供应

预计达到400,000平方米。

第一季度租赁需求旺盛带动上海甲级写字楼市场表现积极2016年第一季度,上海甲级写字楼市场仅有约10万平方米的新增写字楼供应(见表一)。

表一

上海甲级写字楼市场参考指标

指标 2016年第一季度数字 按季变幅预测

(2016年第二季)

新增供应 100,00平方米 ↓85.3% ↗

租金 人民币9.6元/平方米/天 ↑2.3% ↗

空置率 4.2% ↓0.6 个百分点 ↗

价格 人民币60,330元/平方米/天 ↑3.7% ↗

回报率 5.8% ↓0.1 个百分点 ↔

资料来源:莱坊研究部

6

2007 20112009 20132008 20122010 2014 2015

300

200

100

250

150

50

0

2016

表二

甲级写字楼租金及空置率,2016年第一季度

区域租金

(人民币/平方米/天)租金

环比变幅空置率

空置率环比变幅(百分点)

黄浦 9.8 ↑ 2.1% 5.3% ↑ 0.6

静安 11.0 ↑ 0.9% 4.4% ↑ 1.3

浦东 10.7 ↑ 1.9% 2.4% ↑ 2.0

徐汇 9.0 ↑ 1.1% 6.1% ↑ 3.3

长宁 7.7 ↔ 4.9% ↓ 0.5

资料来源:莱坊研究部

上海甲级写字楼租金环比上涨2.3%至

每天每平方米人民币9.6元(见表一),

甲级写字楼平均空置率第一季度环比

下降0.6个百分点至4.2%(见表一)。

写字楼租金上涨的主要原因是业主方调

高租金,同时来自国内金融机构和咨询

服务行业的旺盛租赁需求也进一步推

高租金。

截至2015年末,在沪国内金融机构的

数量约有1,000多家,占总体在沪金融

机构数量的70%。金融机构尤其青睐

小陆家嘴区域,其成为小陆家嘴的主力

租户类型。律师事务所以及咨询企业则

偏好租赁南京西路及淮海中路沿线的写

字楼,活跃的租赁活动为租金上涨的原

因之一。

黄浦区写字楼市场依然是租金上涨幅度

最大的区域,平均租金环比上涨2.1%

至每天每平方米人民币9.8元(见表

二)。

核心商圈甲级写字楼第一季度租金环比

上涨1.8%至每天每平方米人民币11.6

元。

资料来源:莱坊研究部

表三

甲级写字楼主要租赁成交,2016年第一季度

区域 项目 楼层/单元面积

(平方米)租金

(人民币/平方米/天)

静安 嘉里中心二期 低区 1,300 12.8

静安 会德丰广场 低区 1,500 10.2

黄浦 香港新世界K11大厦 高区 1,700 8.0

资料来源:莱坊研究部注:所有成交均有待落实

表四

甲级写字楼主要散售成交,2016年第一季度

区域 项目 楼层/单元面积

(平方米)成交单价

(人民币/平方米)

徐汇 汇京国际广场 第15层单元 238 55,449

虹口 中信广场 第17层 561 53,282

普陀 浙铁绿城长风中心 第13层 440 40,155

资料来源:上海房地产交易中心 / 莱坊研究部注:所有成交均有待落实

租金及价格

图一

甲级写字楼租金及价格指数

租金指数

价格指数

2003Q1=100

7

研究报告上海写字楼市场报告 2016年第一季度

第一季度,上海房地产投资市场录得两

宗整栋交易,其中核心商务区录得一宗

成交。位于淮海中路的爱美高大厦以人

民币13亿元售予瑞力投资基金,核心

商务区的写字楼由于其较低的市场空

第一季度上海写字楼新增供应同比减少

67.8%,仅有两栋写字楼交付。其中,

位于小陆家嘴区域的大华银行大厦竣工

交付,为市场带来30,000平方米的新增

供应;位于漕河泾的科创动力二期竣

工交付,为市场带来约7万平方米的办

公面积。

来自新兴商务区的旺盛租赁需求使整体市

场空置率持续保持在较低水平。第一季

度,新兴商务区写字楼净吸纳面积达到15

万平方米,较上一季度增长一倍。

公司搬离核心商务区产生的空置面积预计

将给甲级写字楼的租赁业务带来挑战。位

置好、租金相对较低的写字楼空置面积比

较容易被吸纳。例如,第一季度世纪商贸

广场在WPP搬离之后,有两个楼面被某

律师事务所租用。然而,在经济环境并不

明朗的背景下,租金高企的超甲级写字楼

空置面积或将需要更长时间被吸纳。外企

向次级商务区搬迁的趋势仍在持续,建筑

咨询公司艾奕康已计划在第二季度从目前

的会德丰广场搬离至五角场的创智天地,

而默沙东制药已从越洋广场迁至漕河泾

园区。

供应量、吸纳量及空置率

投资市场

图二

甲级写字楼供应量、吸纳量及空置率

甲级写字楼供应量(左轴)

甲级写字楼吸纳量(左轴)

空置率(右轴)

千平方米

资料来源:莱坊研究部

政府扶持小微企业的力度不断加大,来

自国外的联合办公模式也在国内掀起热

潮。联合办公模式的低租金和弹性租赁

方式可以满足初创企业对于办公租赁的

需求。国内联合办公市场的活跃也吸引

了国外成熟品牌的入驻。美国联合办公

鼻祖WeWork在静安区开设了第一家联

合办公门店,租用了WE创意园的两个

楼面,共约3,000平方米的办公面积,

未来几年其还将在上海开设两家门店,

以满足大量创业者对于办公空间的需

求。与此同时,国内较有影响力的众创

空间氪空间也在杨浦区租用了1,000平

方米的办公面积。

置率以及持续增长的租金收入,成为基

金公司以及开发商青睐的资产类别。此

外,融创中国则以人民币40.3亿元的价

格购得浦东南郊的两个住宅项目,共计

53,756平方米。

新政“营业税改征增值税”允许企业将

购置的商办物业所交的税款用于抵扣增

值税,预期将增加商办自用物业的需

求,对于写字楼销售将产生积极影响。

Knight Frank Research provides strategic advice, consultancy services and forecasting to a wide range of clients worldwide, including developers and investors, as well as financial and corporate institutions. All recognise the need for the provision of expert independent advice, customised to their specific needs.

莱坊研究团队向众多商业和住宅物业客户,包括发展商、投资者、金融机构和企业机构提供策略性建

议、市场预测和顾问服务。客户均认为我们按其特定需要提供的专业和独立意见能切合他们的需要。

RECENT MARKET-LEADING RESEARCH PUBLICATIONS 近期市场研究报告

RESEARCH & CONSULTANCY 研究及咨询部

David Ji 纪言迅 Director, Head of Research & Consultancy, Greater China 董事及大中华区研究及咨询部主管 +852 2846 9552 [email protected]

Regina Yang 杨悦晨 Director, Head of Research & Consultancy, Shanghai 董事及上海研究及咨询部主管

+86 21 6032 1728 [email protected]

Vincent Li 李想 Assistant Manager, Research & Consultancy, Beijing 北京研究及咨询部助理经理

+86 10 6113 8017 [email protected]

Ocean Ruan 阮洋 Manager, Research & Valuation, Guangzhou 广州研究及估价部经理 +86 20 3839 6408 [email protected]

Pamela Tsui 崔佩贤 Senior Manager, Research & Consultancy, Greater China 大中华区研究及咨询部高级经理 +852 2846 4843 [email protected]

Cliff So 苏锐强 Executive Director, Agency & Professional Advisory Services, REPro Knight Frank, Taipei 台北瑞普莱坊 物业代理及咨询部副总经理 +886 2 8729 8770 [email protected]

SHANGHAI OFFICE LEASING 上海写字楼租赁

Peter Zhang 张延军 Director, Head of TenantServices, Representation, Commercial Services 董事及商业物业代理部主管 +86 21 6032 1713 [email protected]

For the latest news, views and analysison the world of prime property, visit

KnightFrankblog.com/global-briefing

GLOBAL BRIEFING

Prime Cities Forecast Report 2016

Follow us on Wechat关注莱坊微信帐号Scan the QR code and tune in to the latest property insights and research from Knight Frank.扫描二维码,即时了解更多房产资讯及莱坊研究报告。

Knight Frank Research Reports are available at 浏览莱坊的全球研究报告,请登入 KnightFrank.com/Research

© Knight Frank 莱坊 2016This document and the material contained in it is general information only and is subject to change without notice. All images are for illustration only. No representations or warranties of any nature whatsoever are given, intended or implied. Knight Frank will not be liable for negligence, or for any direct or indirect consequential losses or damages arising from the use of this information. You should satisfy yourself about the completeness or accuracy of any information or materials.This document and the material contained in it is the property of Knight Frank and is given to you on the understanding that such mate-rial and the ideas, concepts and proposals expressed in it are the intellectual property of Knight Frank and protected by copyright. It is understood that you may not use this material or any part of it for any reason other than the evaluation of the document unless we have entered into a further agreement for its use. This document is provided to you in confidence on the understanding it is not disclosed to anyone other than to your employees who need to evaluate it.本文件及其内容只提供一般资料,可能随时变更而不作另行通知。所有图片只供展示用途。本文件并不表示、意图或暗示任何性质的代表或担

保。因使用此资料而直接或间接引致的损失或损毁,莱坊恕不负责。客户应自行确保数据或内容的完整和准确性。

本文件及其内容属莱坊所有,使用者知悉其中的观点,概念及建议均属莱坊的知识产权所有,并受版权保护。除了对上述文件作出评估外,若

非已与莱坊达成协议,任何人不得以任何原因使用这些内容或其部分。 本文件在保密的情况下提供予使用者,除参与评估此文件的人员外,

恕不得向任何人透露。

Global House Price Index Q4 2015

Wealth Report 2016 The Global Cities Report

![信用评级报告 - shxsj.com file[此处键入本期债券名称全称] 信用评级报告 上海新世纪资信评估投资服务有限公司 Shanghai Brilliance Credit Rating &](https://static.fdocument.pub/doc/165x107/5e1acd3fa6a53055dd604751/cec-shxsj-eoeoecc-cec.jpg)