Roadshow Presentation - ГК "Ovostar Union" -...

35

June 2011 Roadshow Presentation Egg production and processing http://ovostar.ua/

Transcript of Roadshow Presentation - ГК "Ovostar Union" -...

June 2011

Roadshow Presentation

Egg production and processing

http://ovostar.ua/

Ovostar Union: Roadshow Presentation 2

Disclaimer

NOT FOR RELEASE, DIRECTLY OR INDIRECTLY, IN THE UNITED STATES OF AMERICA, AUSTRALIA, CANADA, JAPAN OR ANY OTHER JURISDICTION WHERE TO DO SO WOULD

BE UNLAWFUL.

IMPORTANT NOTICE

By attending the meeting where this presentation is made, you agree to be bound by the following limitations.

In the European Economic Area, with respect to any Member State that has implemented Directive 2003/71/EC (together with any applicable implementing measures in any Member

State, the "Prospectus Directive") this communication is only addressed to and is only directed at qualified investors in that Member State within the meaning of the Prospectus Directive.

The securities referred to herein have not been and will not be registered under the US Securities Act of 1933, as amended (the "Securities Act"), and may not be offered or sold in the United

States or to US persons (as such term is defined in Regulation S under the Securities Act) unless the securities are registered under the Securities Act, or an exemption from the registration

requirements of the Securities Act is available. The issuer of the securities has not registered, and does not intend to register, any portion of the offering in the United States, and does not

intend to conduct a public offering of securities in the United States.

This communication is directed solely at (i) persons outside Poland and the United Kingdom, or (ii) persons with professional experience in matters relating to investments and high net worth

entities, and other persons to whom it may lawfully be communicated, falling within respective provisions implementing article 3.2.a of the Prospectus Directive in Poland, (iii) persons with

professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 as amended (the

"Order"), (iv) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order, and (v) persons to whom an invitation or

inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000 ("FSMA")) in connection with the issue or sale of any securities

of the Company or any member of its group may otherwise lawfully be communicated or caused to be communicated (all such persons in (i)-(v) above being "relevant persons"). Any

investment activity to which this communication relates will only be available to and will only be engaged with relevant persons. Any person who is not a relevant person should not act or rely

on this communication.

This presentation and its contents are confidential and proprietary to Ovostar Union N.V. (the "Company") and no part of it or its subject matter may be reproduced, redistributed, passed

on, or the contents otherwise divulged, directly or indirectly, to any other person (excluding the relevant person's professional advisers) or published in whole or in part for any purpose without

the prior consent of the Company, BIC Securities SIA, BZ WBK S.A., DM BZ WBK S.A. and KBC Securities N.V. (Branch in Poland). If this presentation has been received in error then it

must be returned immediately. The recipients of this presentation should not base any behaviour in relation to investments or products which would amount to market abuse on the

information in this presentation until after the information has been made generally available. Nor should the recipient use the information in this presentation in any way which would

constitute market abuse.

These materials shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the securities referred to herein in any jurisdiction in which such

offer, solicitation or sale would be unlawful prior to registration, exemption from registration or qualification under the securities laws of any such jurisdiction.

The information contained in this presentation has not been independently verified. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the

correctness, completeness or accuracy of the information or opinions contained therein. Neither the Company nor any of its representatives will be liable for any damages arising from any

use of this presentation or otherwise arising in connection with this presentation.

Assumptions, opinions and views reflected in this presentation are solely opinions and forecasts of the Company. Opinions and forecasts are statements using expressions such as

"expects", "believes", "assumes", "is the opinion", "to the best of our knowledge" and similar phrases. They reflect the current view of the Company with regard to potential future

events, which, however, are uncertain and therefore subject to risk. A multitude of factors can cause actual events to differ significantly from an anticipated development, such as changes in

regulatory systems, increased or new competition in the market, risks arising from acquisitions, interest rate and currency risks or risks based on previous liabilities and litigation risks. Neither

the Company nor its management can answer for the future accuracy of the opinions expressed in this presentation or the actual occurrence of the developments forecast.

The information contained herein has been prepared using information available to the Company at the time of preparation of the presentation. External or other factors may have impacted

on the business of the Company and the content of this presentation, since its preparation. In addition all relevant information about the Company may not be included in this presentation.

A draft prospectus in connection with a proposed initial public offering (the “IPO”) of the Company has been filed with Autoriteit Financiële Markten (the "AFM") which is the competent capital

markets authority in the Netherlands. The Company may conduct the IPO once the AFM approves the prospectus, and provides Komisja Nadzoru Finansowego, the competent capital

markets authority in Poland with a certificate of approval of the Prospectus, and the Company publishes the approved prospectus. The Prospectus, if approved, will be published on the

website of the Issuer (www.ovostar.ua) and the website of the offering broker in Poland (www.dmbzwbk.pl).

This document is for promotional purposes only and under no circumstances shall constitute the basis for a decision to invest in securities of the Company. It does not constitute a

recommendation to invest in any securities. There is no assurance that the prospectus will be approved or that the Company will proceed with the IPO. The Prospectus will be the sole legally

binding document including information on the Company and the IPO.

Ovostar Union: Roadshow Presentation 3

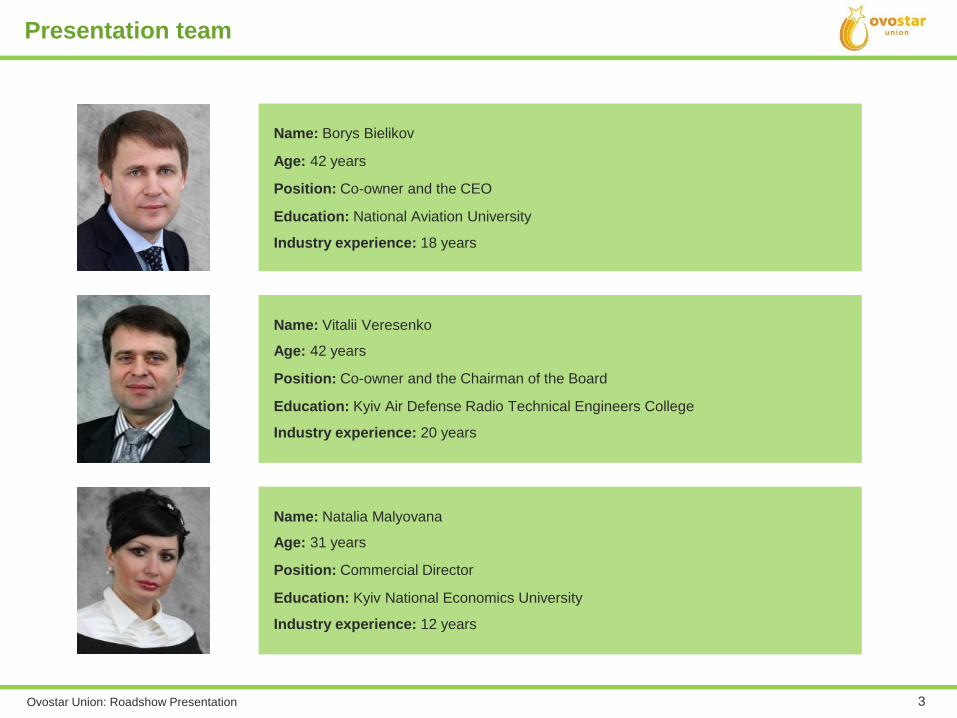

Presentation team

Name: Borys Bielikov

Age: 42 years

Position: Co-owner and the CEO

Education: National Aviation University

Industry experience: 18 years

Name: Vitalii Veresenko

Age: 42 years

Position: Co-owner and the Chairman of the Board

Education: Kyiv Air Defense Radio Technical Engineers College

Industry experience: 20 years

Name: Natalia Malyovana

Age: 31 years

Position: Commercial Director

Education: Kyiv National Economics University

Industry experience: 12 years

Ovostar Union: Roadshow Presentation 4

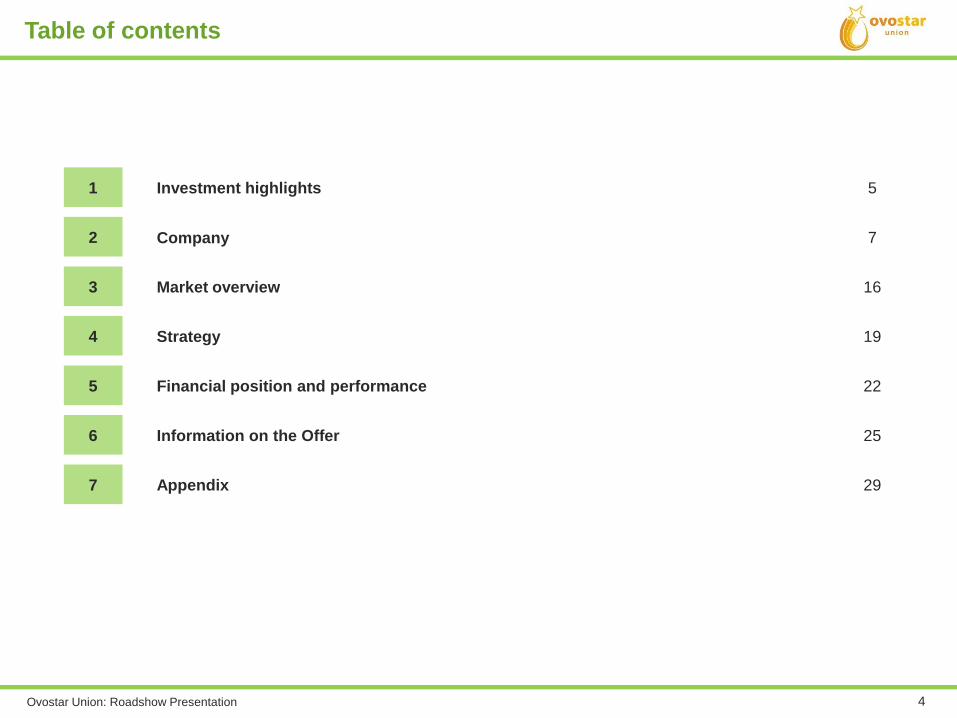

1 Investment highlights 5

2 Company 7

3 Market overview 16

4 Strategy 19

5 Financial position and performance 22

6 Information on the Offer 25

7 Appendix 29

Table of contents

Ovostar Union: Roadshow Presentation 5

Investment highlights

Section 1

Ovostar Union: Roadshow Presentation 6

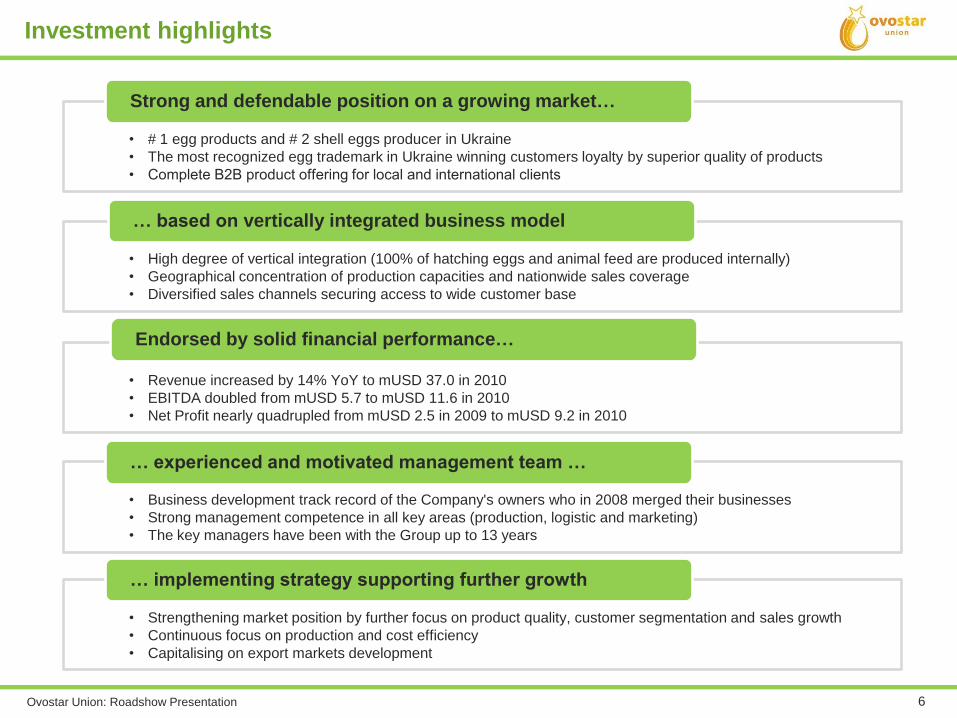

Investment highlights

• # 1 egg products and # 2 shell eggs producer in Ukraine

• The most recognized egg trademark in Ukraine winning customers loyalty by superior quality of products

• Complete В2В product offering for local and international clients

Strong and defendable position on a growing market…

• High degree of vertical integration (100% of hatching eggs and animal feed are produced internally)

• Geographical concentration of production capacities and nationwide sales coverage

• Diversified sales channels securing access to wide customer base

… based on vertically integrated business model

• Revenue increased by 14% YoY to mUSD 37.0 in 2010

• EBITDA doubled from mUSD 5.7 to mUSD 11.6 in 2010

• Net Profit nearly quadrupled from mUSD 2.5 in 2009 to mUSD 9.2 in 2010

Endorsed by solid financial performance…

• Business development track record of the Company's owners who in 2008 merged their businesses

• Strong management competence in all key areas (production, logistic and marketing)

• The key managers have been with the Group up to 13 years

… experienced and motivated management team …

• Strengthening market position by further focus on product quality, customer segmentation and sales growth

• Continuous focus on production and cost efficiency

• Capitalising on export markets development

… implementing strategy supporting further growth

Ovostar Union: Roadshow Presentation 7

Company

Section 2

Ovostar Union: Roadshow Presentation 8

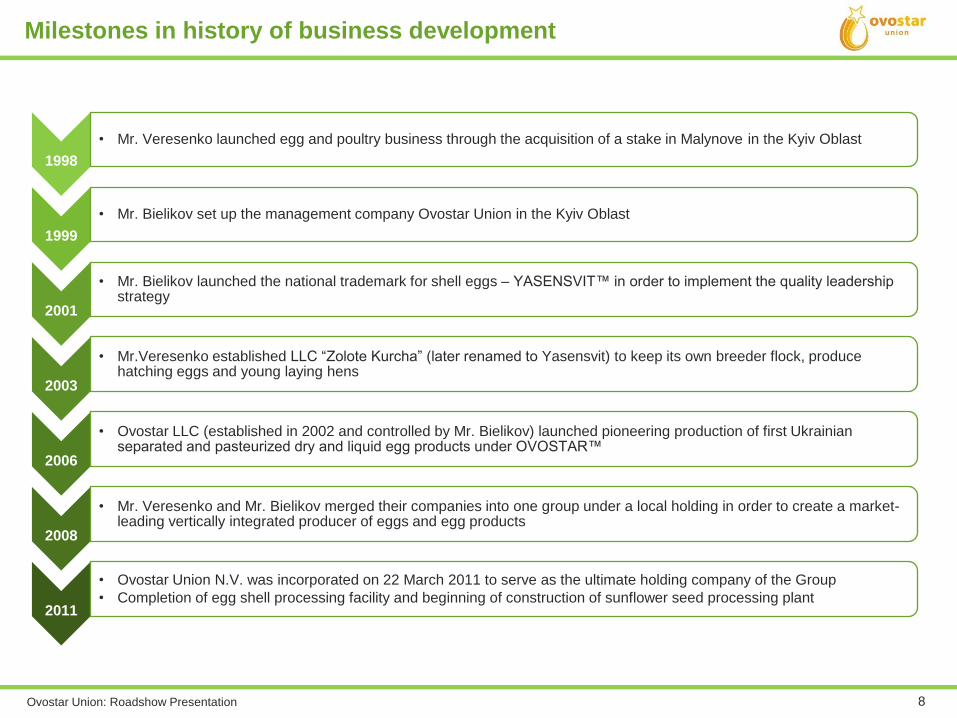

Milestones in history of business development

1998

• Mr. Veresenko launched egg and poultry business through the acquisition of a stake in Malynove in the Kyiv Oblast

1999

• Mr. Bielikov set up the management company Ovostar Union in the Kyiv Oblast

2001

• Mr. Bielikov launched the national trademark for shell eggs – YASENSVIT™ in order to implement the quality leadership strategy

2003

• Mr.Veresenko established LLC “Zolote Kurcha” (later renamed to Yasensvit) to keep its own breeder flock, produce hatching eggs and young laying hens

2006

• Ovostar LLC (established in 2002 and controlled by Mr. Bielikov) launched pioneering production of first Ukrainian separated and pasteurized dry and liquid egg products under OVOSTAR™

2008

• Mr. Veresenko and Mr. Bielikov merged their companies into one group under a local holding in order to create a market-leading vertically integrated producer of eggs and egg products

2011

• Ovostar Union N.V. was incorporated on 22 March 2011 to serve as the ultimate holding company of the Group

• Completion of egg shell processing facility and beginning of construction of sunflower seed processing plant

Ovostar Union: Roadshow Presentation 9

3 177 3 497

4 706

2008 2009 2010

One of the largest player in shell eggs and egg products market specializing in the production of high-quality branded

products:

546.1 million shell eggs and 4.7 ths tons of egg products produced in 2010 – product mix shifted towards liquid egg products

two modern poultry farms with a total of 2.1 million productive laying hens as at 31.12.2010

independently producing all 100% of hatching eggs for its in-house needs and 100% of animal feed required for its poultry

the second largest egg exporter in Ukraine (with 13.9% share of Ukrainian export in terms of volume in 2010)

One of the leaders on the Ukrainian egg market

Net Sales dynamics by products, mUSD

Source: Ovostar Union

Production of Shell Eggs, mln pieces Production of Egg Products, tons

527.5540.1 546.1

2008 2009 2010

6.8%

2.5%

1.1%

39.3%

10.1%

34.6%

25.020.1

24.2

10.8

11.010.0

1.01.3

2.8

2008 2009 2010

Shell eggs Egg products Poultry and other

36.7 32.3 37.0

27%

65%

8%

Ovostar Union: Roadshow Presentation 10

64% 64%

85%

36% 36%

15%

2008 2009 2010

Branded eggs Unbranded eggs

24.220.125.0

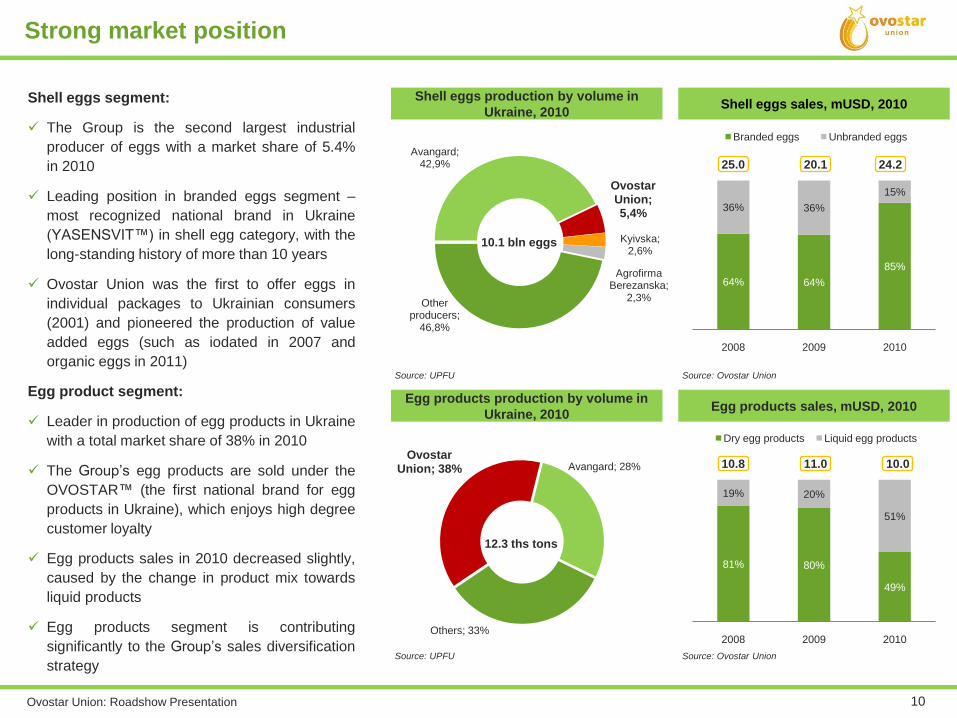

Strong market position

Shell eggs production by volume in

Ukraine, 2010

Egg products production by volume in

Ukraine, 2010

Avangard; 42,9%

Ovostar Union; 5,4%

Kyivska; 2,6%

Agrofirma Berezanska;

2,3%Other

producers; 46,8%

Ovostar Union; 38% Avangard; 28%

Others; 33%

10.1 bln eggs

12.3 ths tons

Source: UPFU

Source: UPFU

Shell eggs segment:

The Group is the second largest industrial

producer of eggs with a market share of 5.4%

in 2010

Leading position in branded eggs segment –

most recognized national brand in Ukraine

(YASENSVIT™) in shell egg category, with the

long-standing history of more than 10 years

Ovostar Union was the first to offer eggs in

individual packages to Ukrainian consumers

(2001) and pioneered the production of value

added eggs (such as iodated in 2007 and

organic eggs in 2011)

Egg product segment:

Leader in production of egg products in Ukraine

with a total market share of 38% in 2010

The Group’s egg products are sold under the

OVOSTAR™ (the first national brand for egg

products in Ukraine), which enjoys high degree

customer loyalty

Egg products sales in 2010 decreased slightly,

caused by the change in product mix towards

liquid products

Egg products segment is contributing

significantly to the Group’s sales diversification

strategy

Shell eggs sales, mUSD, 2010

Egg products sales, mUSD, 2010

Source: Ovostar Union

Source: Ovostar Union

81% 80%

49%

19% 20%

51%

2008 2009 2010

Dry egg products Liquid egg products

10.011.010.8

Ovostar Union: Roadshow Presentation 11

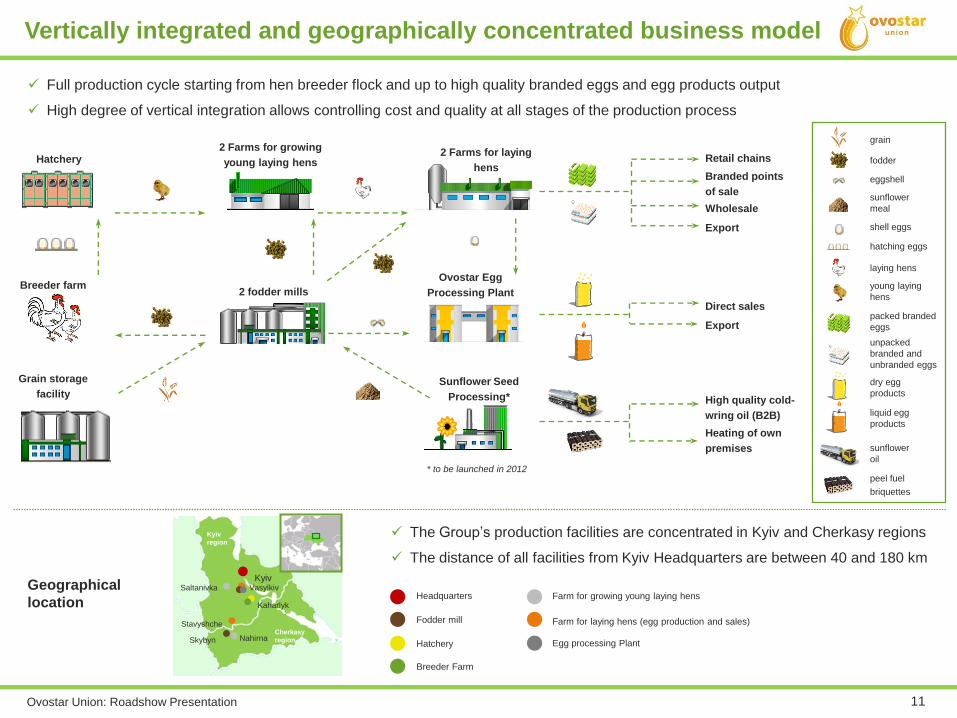

Cherkasy

region

Kyiv

region

KyivVasylkiv

NahirnaSkybyn

Saltanivka

Kaharlyk

Stavyshche

Full production cycle starting from hen breeder flock and up to high quality branded eggs and egg products output

High degree of vertical integration allows controlling cost and quality at all stages of the production process

Vertically integrated and geographically concentrated business model

grain

fodder

eggshell

dry egg

products

packed branded

eggs

unpacked

branded and

unbranded eggs

liquid egg

products

sunflower

meal

sunflower

oil

peel fuel

briquettes

* to be launched in 2012

Retail chains

Branded points

of sale

Wholesale

Export

Hatchery

Breeder farm

2 Farms for growing

young laying hens

2 fodder mills

2 Farms for laying

hens

Ovostar Egg

Processing Plant

Sunflower Seed

Processing*

Grain storage

facility

Direct sales

Export

High quality cold-

wring oil (B2B)

Heating of own

premises

Fodder mill

Hatchery

Farm for laying hens (egg production and sales)

Headquarters

Egg processing Plant

Farm for growing young laying hens

Breeder Farm

The Group’s production facilities are concentrated in Kyiv and Cherkasy regions

The distance of all facilities from Kyiv Headquarters are between 40 and 180 km

Geographical

location

shell eggs

hatching eggs

laying hens

young laying

hens

Ovostar Union: Roadshow Presentation 12

To

p-3

eg

gs b

y g

ross

ma

rgin

in 2

01

0

To

p-3

eg

gs b

y c

on

trib

uti

on

to

sh

ell

eg

gs s

ale

s in

201

0 Widest range of packed chicken eggs in Ukraine aimed at different clients’ segments

YASENSVIT™ is the most recognized umbrella egg brand in Ukraine with more than 10 years history

YASENSVIT™ brand contributed 50% of the Group’s revenue supported by a portfolio of sub-brands

* Gross Margin ** contribution to Total shell eggs sales / Packed eggs sales

Name: Ukraina (Ukraine)

GM: 24%

Sales (T/P): 8.3% / 21.4%

Segment: Economy

Name: Zolote Yayechko (Golden Egg)

GM: 26%

Sales (T/P): 2.2% / 5.5%

Segment: Standard

Name: Svizhi Yaitsya (Fresh eggs)

GM: 24%

Sales (T/P): 5.6% / 14.1%

Segment: Standard

Name: Super

GM*: 38%

Sales** (T/P): 0.8% / 2.1%

Segment: Premium

Name: Molodylni (Rejuvenating)

GM: 34%

Sales (T/P): 2.4% / 6.1%

Segment: Premium

Name: Rankovi (Morning eggs)

GM: 34%

Sales (T/P): 1.7% / 4.5%

Segment: Premium

Products: highly recognized egg trademark in Ukraine

Source: Ovostar Union

Ovostar Union: Roadshow Presentation 13

Price per kg:

USD 3.95

End-use:

confectionary

and mayonnaise

production

Market share

Egg powder

60%

Price per kg:

USD 5.41

End-use:

mayonnaise

production

Market share

Dry egg yolk

80%

Price per kg:

USD 3.68

End-use:

confectionary

production

Market share

Liquid egg yolk

100%

Price per kg:

USD 5.92

End-use:

mayonnaise

production

Market share

Dry fermented

yolk

80%

Price per kg:

USD 8.48

End-use :

confectionary

production

Market share

Dry egg albumen

11%

Price per kg:

USD 1.55

End-use:

confectionary

production

Market share

Liquid whole egg

90%

Price per kg:

USD 1.09

End-use:

confectionary

and crab sticks

production

Market share*

Liquid egg white

100%

Source: Ovostar Union

Note: Prices are farm gate as at March 2011. Liquid fermented thermostable and pasteurized egg yolks are combined under Liquid egg yolk. Treated shell eggs, supplied to McDonald’s, are not shown

* Ukrainian market (including import) share by value in 2010

Ovostar has the most complete В2В product offering and significant market share in all egg product categories in Ukraine

Ovostar is the only producer of liquid egg white and liquid egg yolk in Ukraine

Products: egg product offering

Ovostar Union: Roadshow Presentation 14

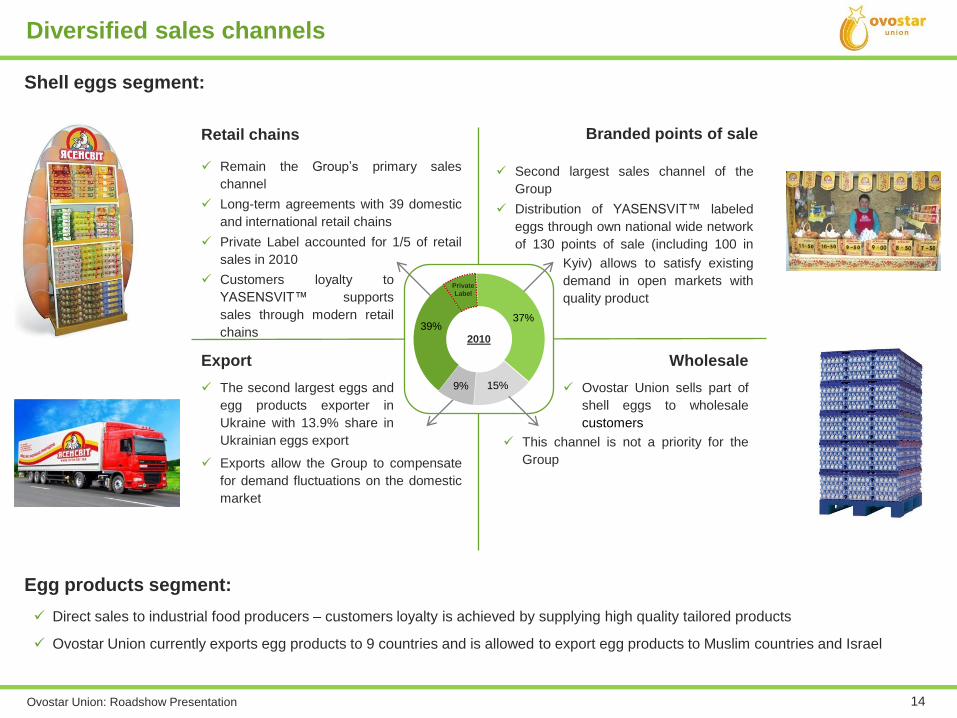

Ovostar Union sells part of

shell eggs to wholesale

customers

Second largest sales channel of the

Group

Distribution of YASENSVIT™ labeled

eggs through own national wide network

of 130 points of sale (including 100 in

Kyiv

Diversified sales channels

Retail chains Branded points of sale

Export Wholesale

Remain the Group’s primary sales

channel

Long-term agreements with 39 domestic

and international retail chains

Private Label accounted for 1/5 of retail

sales in 2010

Customers loyalty to

YASENSVIT™ supports

sales through modern retail

chains

Exports allow the Group to compensate

for demand fluctuations on the domestic

market

Direct sales to industrial food producers – customers loyalty is achieved by supplying high quality tailored products

Ovostar Union currently exports egg products to 9 countries and is allowed to export egg products to Muslim countries and Israel

Shell eggs segment:

The second largest eggs and

egg products exporter in

Ukraine with 13.9% share in

Ukrainian eggs export

Egg products segment:

2010

Kyiv) allows to satisfy existing

demand in open markets with

quality product

This channel is not a priority for the

Group

39%37%

15%9%

Private

Label

Ovostar Union: Roadshow Presentation 15

Client name Client descriptionShare in

procurement

HoReCa

McDonald’s Ukraine has 70 restaurants (24 in Kyiv) in 21 cities

in Ukraine100%

Mayonnaise and sauces

Volynholding is #1 sauces producer in Ukraine, acquired by

Nestle in 200350%

Lviv Zhyrokombinat is large Ukrainian sauces producer 100%

JV South Food (Chumak TM) is the largest ketchup and sauces

producer in Ukraine 100%

Confectionary

Roshen is #1 Ukrainian confectionary producer 50%

Konti is #2 Ukrainian confectionary producer 42%

AVK is #3 Ukrainian confectionary producer 20%

Zhytomiski Lasoschi is #5 Ukrainian confectionary producer 30%

Zhako is #1 Ukrainian zephyr producer 100%

Foods processing

Technokom is #1 producer of instant noodles and fast-cooking

noodles acquired by Nestle in 201050%

Hercules is one of the leading producer of frozen food and ice-

cream in Ukraine50%

Donetsk frozen food factory is one of the leading producer of

frozen food in Ukraine100%

Acquafrost is large producer of crab sticks 42%

Source: Public data, State Statistics Committee of Ukraine, Ovostar Union

Clients: proven quality leadership

Client name Client descriptionShare in

procurement

Multinational retailer, operating 26

classical stores (4 in Kyiv) in 18 cities

in Ukraine

30%

Multinational retailer, operating 8

supermarkets (4 in Kyiv) in 5 cities in

Ukraine

77%

Part of REWE Group, operating 20

supermarkets (5 in Kyiv) in 14 cities

in Ukraine

50%

Top 5 local retail company (25%

owned by Auchan) operating 115

multi-format stores in Ukraine

60%

Top 10 local retail company ,

operating 46 multi-format stores in

Ukraine

60%

Key customers include multinational food companies

such as Nestle and McDonalds and largest

international retailers such as Metro, Auchan and Billa

(REWE Group). Domestic customers include flagship

companies in food industry (Roshen, AVK etc.)

Ovostar Union produces Private Label products for

leading international and local retailers and enjoys 83%

share in Private Label segment by volume

Source: Public data, State Statistics Committee of Ukraine, Ovostar Union

Ovostar Union: Roadshow Presentation 16

Market overview

Section 3

Ovostar Union: Roadshow Presentation 17

6,5 7,6 7,5 8,4 9,1 10,1 11,2 12,3

6,66,6 6,5 6,5 6,6

6,86,6

6,8

50%53% 54%

56% 58% 60%63% 65%

2005 2006 2007 2008 2009 2010 2011F 2012F

Industrial producers

Household producers

% of industrial producers in total production

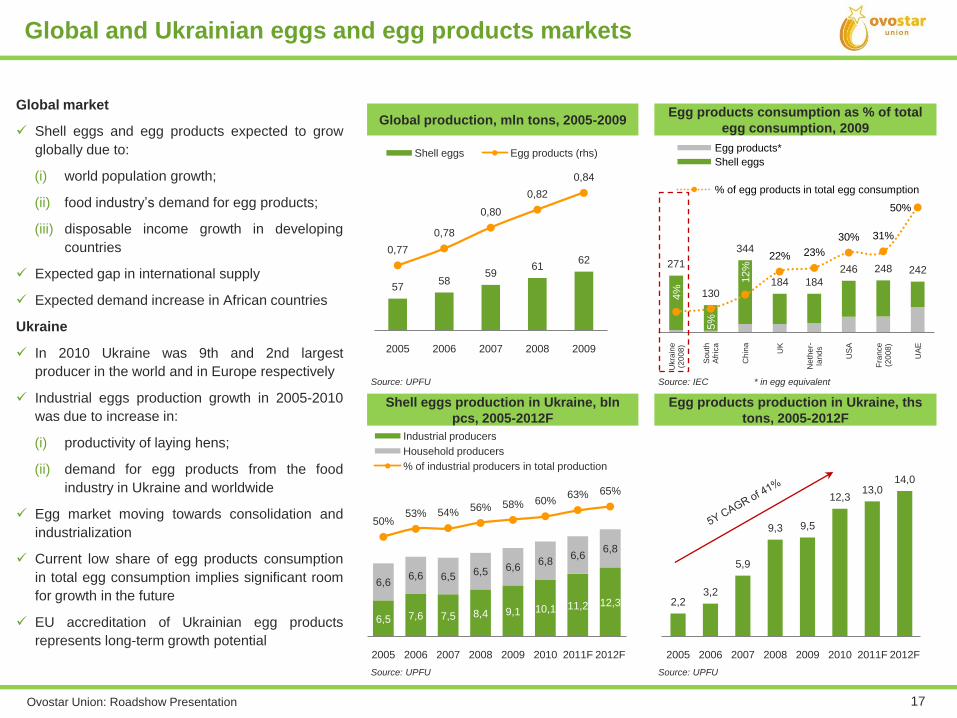

Global market

Shell eggs and egg products expected to grow

globally due to:

(i) world population growth;

(ii) food industry’s demand for egg products;

(iii) disposable income growth in developing

countries

Expected gap in international supply

Expected demand increase in African countries

Ukraine

In 2010 Ukraine was 9th and 2nd largest

producer in the world and in Europe respectively

Industrial eggs production growth in 2005-2010

was due to increase in:

(i) productivity of laying hens;

(ii) demand for egg products from the food

industry in Ukraine and worldwide

Egg market moving towards consolidation and

industrialization

Current low share of egg products consumption

in total egg consumption implies significant room

for growth in the future

EU accreditation of Ukrainian egg products

represents long-term growth potential

Source: UPFU

5758

5961

620,77

0,78

0,80

0,82

0,84

2005 2006 2007 2008 2009

Shell eggs Egg products (rhs)

Global production, mln tons, 2005-2009Egg products consumption as % of total

egg consumption, 2009

Source: IEC * in egg equivalent

Source: UPFU

Global and Ukrainian eggs and egg products markets

Shell eggs production in Ukraine, bln

pcs, 2005-2012F

Egg products production in Ukraine, ths

tons, 2005-2012F

2,23,2

5,9

9,3 9,5

12,313,0

14,0

2005 2006 2007 2008 2009 2010 2011F 2012F

Source: UPFU

271

130

344

184 184

246 248 242

4%

5%

12%

22% 23%

30% 31%

50%

Ukra

ine

(20

08

)

So

uth

Afr

ica

Chin

a

UK

Neth

er-

lan

ds

US

A

Fra

nce

(20

08

)

UA

E

Egg products*

Shell eggs

% of egg products in total egg consumption

Ovostar Union: Roadshow Presentation 18

Source: GfK GeoMarketing, State Statistics Committee of Ukraine, Central Statistical Office of Poland

* based on CEE countries on the graph, includes Russia ** based on developed countries on the graph

Retail sales per capita, USD, 2009

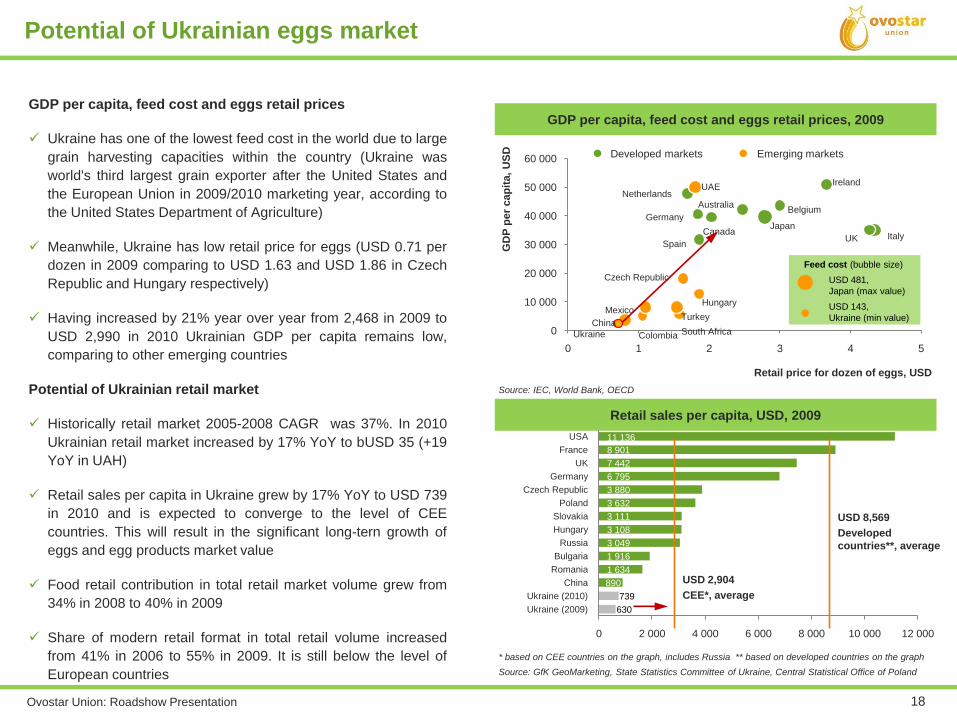

GDP per capita, feed cost and eggs retail prices

Ukraine has one of the lowest feed cost in the world due to large

grain harvesting capacities within the country (Ukraine was

world's third largest grain exporter after the United States and

the European Union in 2009/2010 marketing year, according to

the United States Department of Agriculture)

Meanwhile, Ukraine has low retail price for eggs (USD 0.71 per

dozen in 2009 comparing to USD 1.63 and USD 1.86 in Czech

Republic and Hungary respectively)

Having increased by 21% year over year from 2,468 in 2009 to

USD 2,990 in 2010 Ukrainian GDP per capita remains low,

comparing to other emerging countries

Potential of Ukrainian retail market

Historically retail market 2005-2008 CAGR was 37%. In 2010

Ukrainian retail market increased by 17% YoY to bUSD 35 (+19

YoY in UAH)

Retail sales per capita in Ukraine grew by 17% YoY to USD 739

in 2010 and is expected to converge to the level of CEE

countries. This will result in the significant long-tern growth of

eggs and egg products market value

Food retail contribution in total retail market volume grew from

34% in 2008 to 40% in 2009

Share of modern retail format in total retail volume increased

from 41% in 2006 to 55% in 2009. It is still below the level of

European countries

Potential of Ukrainian eggs market

0

10 000

20 000

30 000

40 000

50 000

60 000

0 1 2 3 4 5

China

Mexico

Colombia

Spain

Ukraine South Africa

Turkey

Hungary

Czech Republic

UAENetherlands

Germany

Canada

Belgium

Ireland

Japan

Australia

UK Italy

GD

P p

er

cap

ita,

US

D

USD 481,

Japan (max value)

Feed cost (bubble size)

USD 143,

Ukraine (min value)

Retail price for dozen of eggs, USD

Developed markets Emerging markets

Source: IEC, World Bank, OECD

GDP per capita, feed cost and eggs retail prices, 2009

630

739

890

1 634

1 916

3 049

3 108

3 111

3 632

3 880

6 795

7 442

8 901

11 136

0 2 000 4 000 6 000 8 000 10 000 12 000

Ukraine (2009)

Ukraine (2010)

China

Romania

Bulgaria

Russia

Hungary

Slovakia

Poland

Czech Republic

Germany

UK

France

USA

USD 2,904

CEE*, average

USD 8,569

Developed

countries**, average

Ovostar Union: Roadshow Presentation 19

Strategy

Section 4

Ovostar Union: Roadshow Presentation 20

Our main goal is to further strengthen position of the leading producer of high quality branded eggs and egg products in Ukraine

Further

development of

the “Yasensvit”

national egg brand

Further expansion

of production

capacities

Strengthening

position as a

leader in product

quality with

“Ovostar”TM egg

products

Focus on vertical

integration

Further export

markets

development

Development of the

“Yasensvit” national

brand and

successful launching

new sub-brands

Concentrate

marketing efforts on

strengthening brand

loyalty among

emerging middle

class consumers

Reconstruction of

existing laying

hens houses and

purchase of new

cage equipment

Expansion of

production

capacity of the

Egg Processing

Plant

Always offer high

quality products to

strengthen position

as a leader in a B2B

market

Continue to secure

long-terms contracts

with the biggest local

and multinational

food companies in

Ukraine

Maximize the production

process efficiency

New initiatives to

sustain profitability and

competitive advantages

(i.e. Sunflower Seed

Processing Plant)

Expand export sales to

Middle East, African and

CIS countries as well as

Muslim countries and

Israel

Consider export markets

as an opportunity to gain

on favorable prices

Strategy

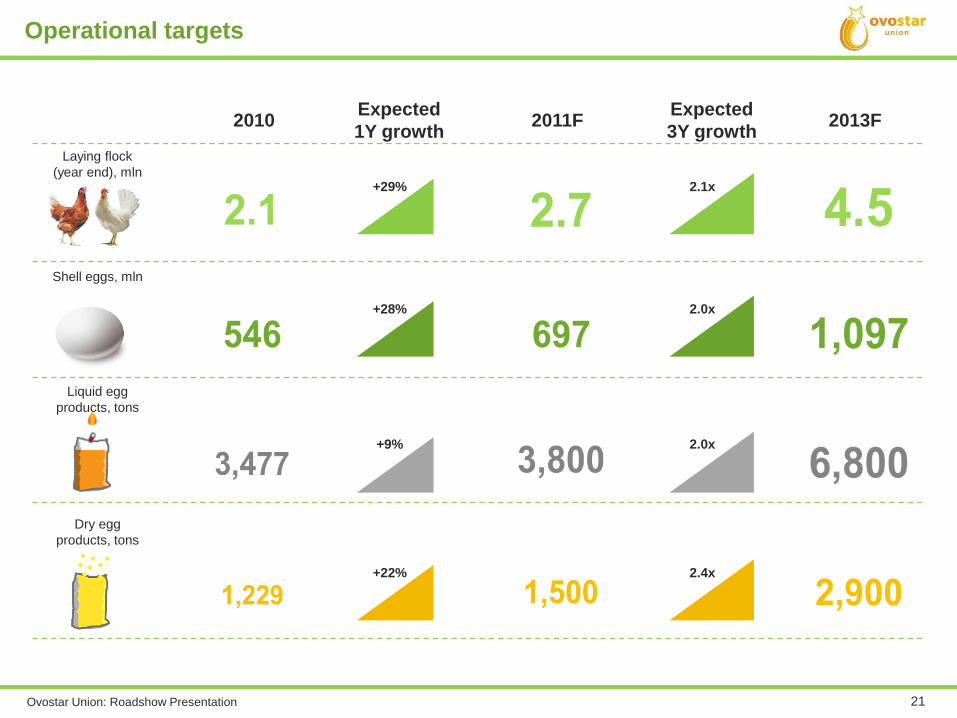

Ovostar Union: Roadshow Presentation 21

Operational targets

2010 2013FExpected

1Y growth

Laying flock

(year end), mln

Shell eggs, mln

Liquid egg

products, tons

Dry egg

products, tons

+29%

+28%

+9%

+22%

2011FExpected

3Y growth

2.1x

2.0x

2.0x

2.4x

Ovostar Union: Roadshow Presentation 22

Financial position and

performance

Section 5

Ovostar Union: Roadshow Presentation 23

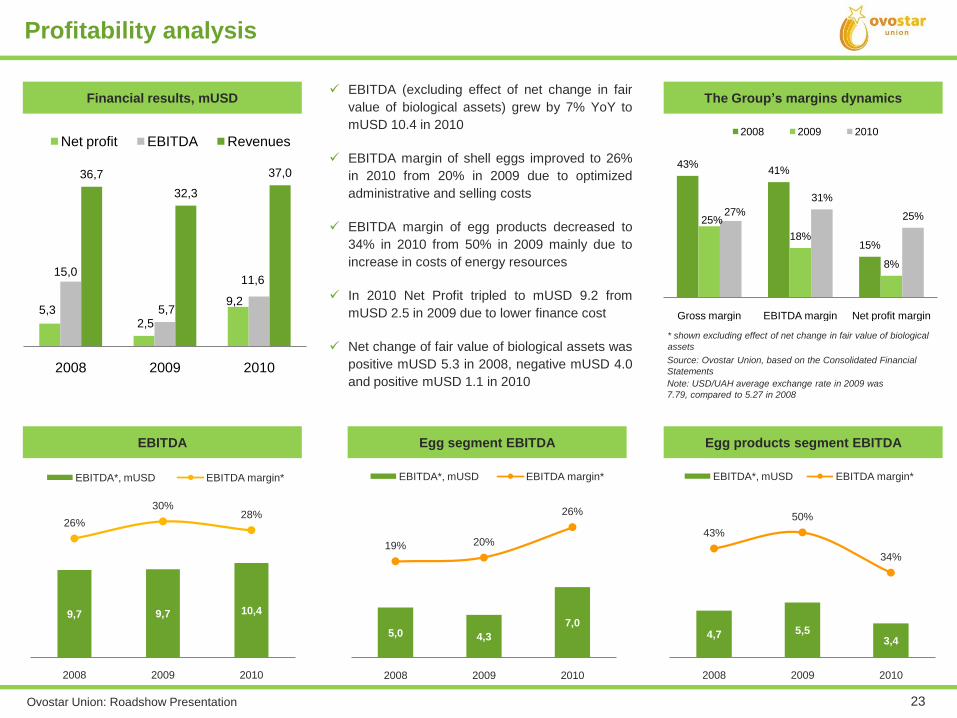

Egg segment EBITDA Egg products segment EBITDA

5,0 4,3

7,0

19% 20%

26%

2008 2009 2010

EBITDA*, mUSD EBITDA margin*

Profitability analysis

4,7 5,53,4

43%

50%

34%

2008 2009 2010

EBITDA*, mUSD EBITDA margin*

EBITDA

9,7 9,7 10,4

26%

30%28%

2008 2009 2010

EBITDA*, mUSD EBITDA margin*

* shown excluding effect of net change in fair value of biological

assets

Source: Ovostar Union, based on the Consolidated Financial

Statements

Note: USD/UAH average exchange rate in 2009 was

7.79, compared to 5.27 in 2008

The Group’s margins dynamics EBITDA (excluding effect of net change in fair

value of biological assets) grew by 7% YoY to

mUSD 10.4 in 2010

EBITDA margin of shell eggs improved to 26%

in 2010 from 20% in 2009 due to optimized

administrative and selling costs

EBITDA margin of egg products decreased to

34% in 2010 from 50% in 2009 mainly due to

increase in costs of energy resources

In 2010 Net Profit tripled to mUSD 9.2 from

mUSD 2.5 in 2009 due to lower finance cost

Net change of fair value of biological assets was

positive mUSD 5.3 in 2008, negative mUSD 4.0

and positive mUSD 1.1 in 2010

43%41%

15%

25%

18%

8%

27%

31%

25%

Gross margin EBITDA margin Net profit margin

2008 2009 2010

5,3 2,5

9,2

15,0

5,7

11,6

36,7

32,3

37,0

2008 2009 2010

Net profit EBITDA Revenues

Financial results, mUSD

Ovostar Union: Roadshow Presentation 24

Income Statement

kUSD 2008 2009 2010

Net Sales 36,703 32,345 37,033

Net change in fair value of biological assets 5,318 -4,043 1,137

Cost of sales -26,241 -20,136 -28,133

Gross profit 15,780 8,166 10,037

SG&A -8,246 -5,881 -5,054

Other operating income, net 4,637 1,328 4,521

Operating profit 12,171 3,613 9,504

Depreciation 2,802 2,083 2,056

EBITDA 14,973 5,696 11,560

Finance costs, net -6,570 -1,193 -234

Income tax expense -275 118 -107

Profit for the year 5,326 2,538 9,163

Exchange differences -9,259 -696 -159

Total comprehensive income / (loss) -3,933 1,842 9,004

USD/UAH, average 5.27 7.79 7.94

Source: Ovostar Union, based on the Consolidated Financial Statements

Summary Financial Data

Balance Sheet

kUSD 31/12/2008 31/12/2009 31/12/2010

Non-current assets 18,273 18,473 18,930

Fixed assets 13,873 12,210 11,629

Non-current biological assets 894 1,468 6,121

Other long-term assets 3,506 4,795 1,180

Current assets 24,843 23,333 21,874

Current biological assets 7,946 5,950 5,026

Other current assets 16,897 17,383 16,848

Total assets 43,116 41,806 40,804

Owners’ equity 28,539 30,009 31,425

Non-current loans and borrowings 3,560 2,194 230

Current loans and borrowings 6,453 5,894 4,150

Trade and other payables 4,198 3,508 4,972

Other liabilities 366 201 27

Total liabilities 14,577 11,797 9,379

Total liabilities and equity 43,116 41,806 40,804

USD/UAH, end of period 7.70 7.99 7.96

kUSD 31/12/2008 31/12/2009 31/12/2010

Net cash flows received from (used in)

operating activities23,450 5,152 5,250

Net cash flow received from (used in) in

investment activities-7,222 -808 -687

Net cash flow received from (used in)

financing activities-7,218 -3,406 -4,656

Net foreign exchange difference -8,956 -696 -126

Net cash flow for the period 54 242 -219

Cash Flow

mUSD 2008 2009 2010 Total

Eggs 3.9 1.2 2.1 7.2

Egg products 2.5 0.3 0.1 2.9

Sunflower processing - - 0.4 0.4

Total 6.4 1.5 2.6 10.5

Historical CAPEX overview

Ovostar Union: Roadshow Presentation 25

Information on the Offer

Section 6

Ovostar Union: Roadshow Presentation 26

2.1 mln

546 mln/year

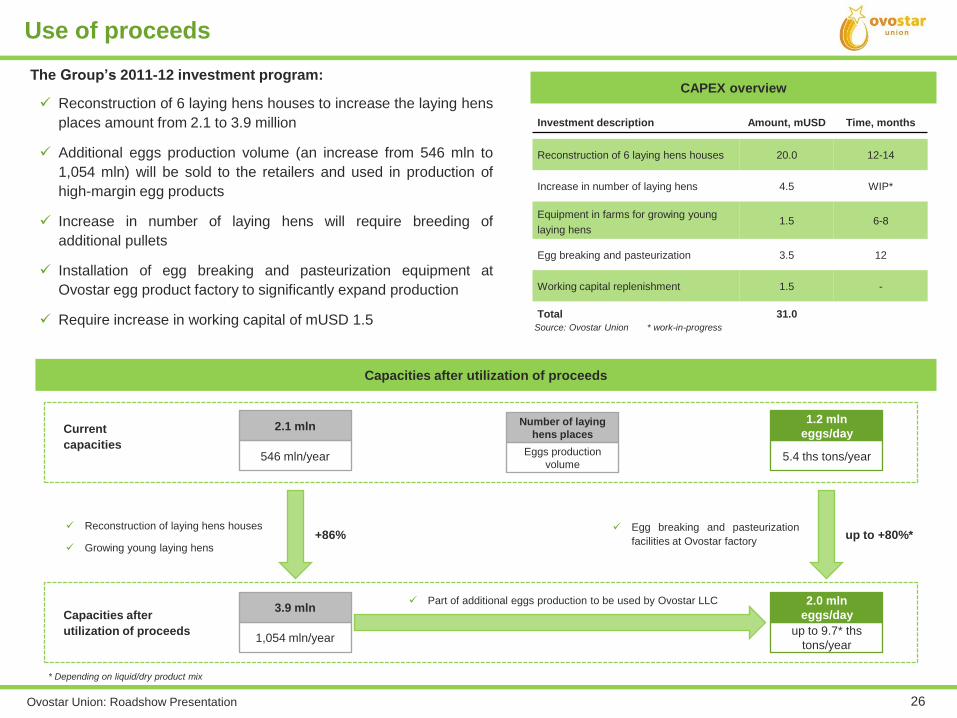

The Group’s 2011-12 investment program:

Reconstruction of 6 laying hens houses to increase the laying hens

places amount from 2.1 to 3.9 million

Additional eggs production volume (an increase from 546 mln to

1,054 mln) will be sold to the retailers and used in production of

high-margin egg products

Increase in number of laying hens will require breeding of

additional pullets

Installation of egg breaking and pasteurization equipment at

Ovostar egg product factory to significantly expand production

Require increase in working capital of mUSD 1.5

3.9 mln

1,054 mln/year

1.2 mln

eggs/day

5.4 ths tons/year

2.0 mln

eggs/day

up to 9.7* ths

tons/year

Reconstruction of laying hens houses

Growing young laying hens

Egg breaking and pasteurization

facilities at Ovostar factory

Part of additional eggs production to be used by Ovostar LLC

Current

capacities

Capacities after

utilization of proceeds

Number of laying

hens places

Eggs production

volume

Source: Ovostar Union * work-in-progress

CAPEX overview

Capacities after utilization of proceeds

* Depending on liquid/dry product mix

Use of proceeds

Investment description Amount, mUSD Time, months

Reconstruction of 6 laying hens houses 20.0 12-14

Increase in number of laying hens 4.5 WIP*

Equipment in farms for growing young

laying hens1.5 6-8

Egg breaking and pasteurization 3.5 12

Working capital replenishment 1.5 -

Total 31.0

+86% up to +80%*

Ovostar Union: Roadshow Presentation 27

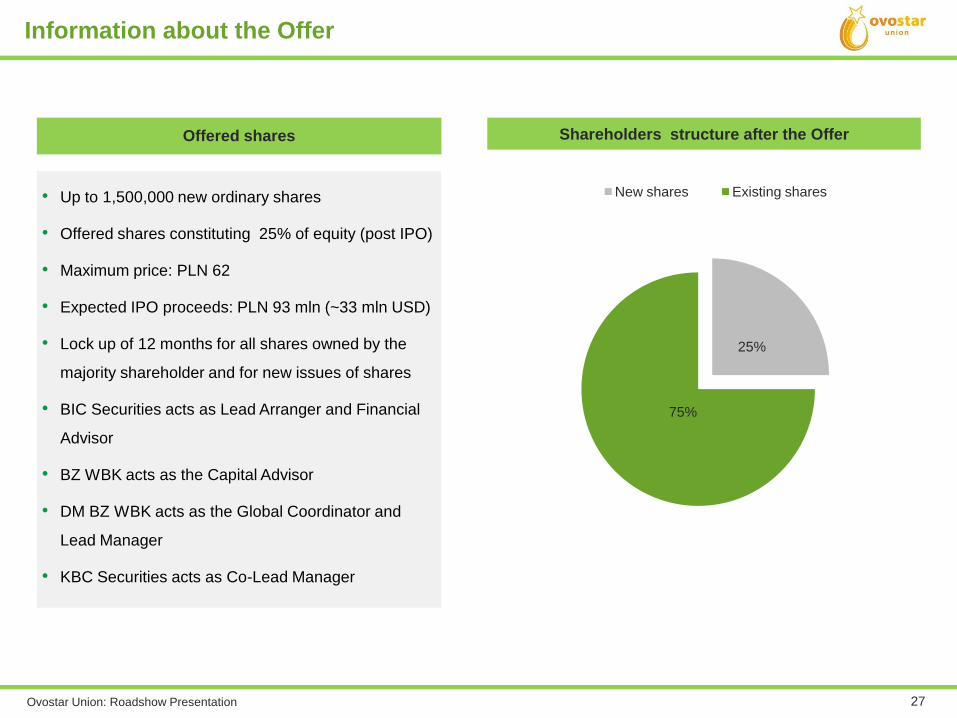

Offered shares

• Up to 1,500,000 new ordinary shares

• Offered shares constituting 25% of equity (post IPO)

• Maximum price: PLN 62

• Expected IPO proceeds: PLN 93 mln (~33 mln USD)

• Lock up of 12 months for all shares owned by the

majority shareholder and for new issues of shares

• BIC Securities acts as Lead Arranger and Financial

Advisor

• BZ WBK acts as the Capital Advisor

• DM BZ WBK acts as the Global Coordinator and

Lead Manager

• KBC Securities acts as Co-Lead Manager

Shareholders structure after the Offer

25%

75%

New shares Existing shares

Information about the Offer

Ovostar Union: Roadshow Presentation 28

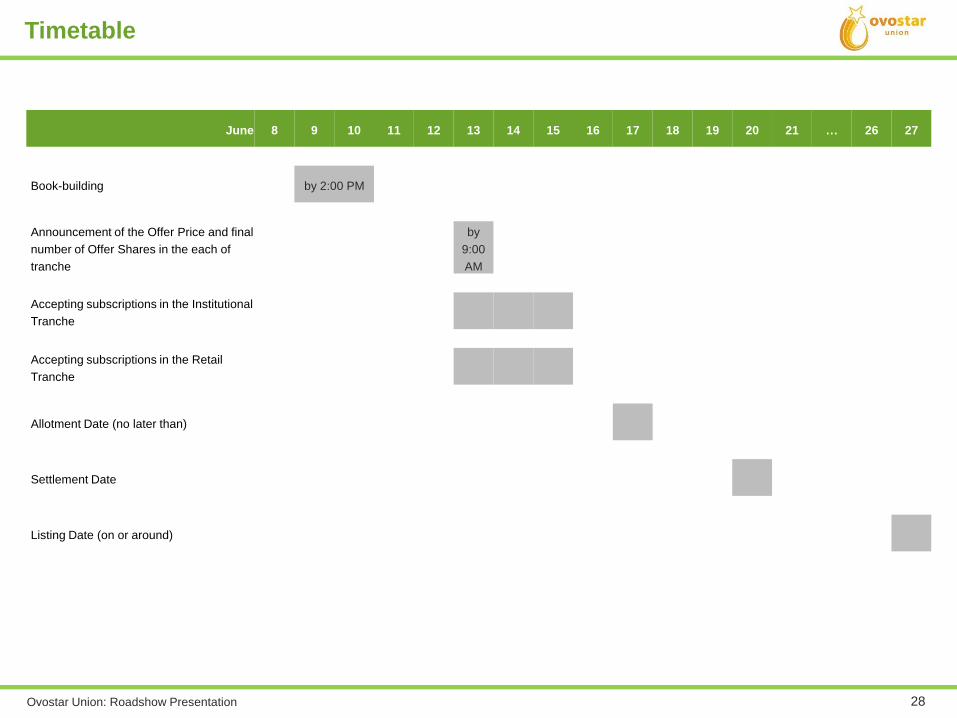

Timetable

June 8 9 10 11 12 13 14 15 16 17 18 19 20 21 … 26 27

Book-building by 2:00 PM

Announcement of the Offer Price and final

number of Offer Shares in the each of

tranche

by

9:00

AM

Accepting subscriptions in the Institutional

Tranche

Accepting subscriptions in the Retail

Tranche

Allotment Date (no later than)

Settlement Date

Listing Date (on or around)

Ovostar Union: Roadshow Presentation 29

Appendix

Section 7

Ovostar Union: Roadshow Presentation 30

Management team

Name: Borys Bielikov

Age: 42 years

Position: CEO

Industry experience: 18 years

Name: Natalia Malyovana

Age: 31 years

Position: Commercial Director

Industry experience: 12 years

Name: Vitaliy Voron

Age: 43 years

Position: Production Director

Industry experience: 25 years

Name: Viacheslav Protsyshyn

Age: 36 years

Position: Logistics Director

Industry experience: 14 years

Name: Yuriy Doroshev

Age: 33 years

Position: CFO

Industry experience: 13 years

Name: Natalia Vlasniuk

Age: 40 years

Position: Marketing Director

Industry experience: 15 years

Name: Vitalii Veresenko

Age: 42 years

Position: Chairman of the Board

Industry experience: 20 years

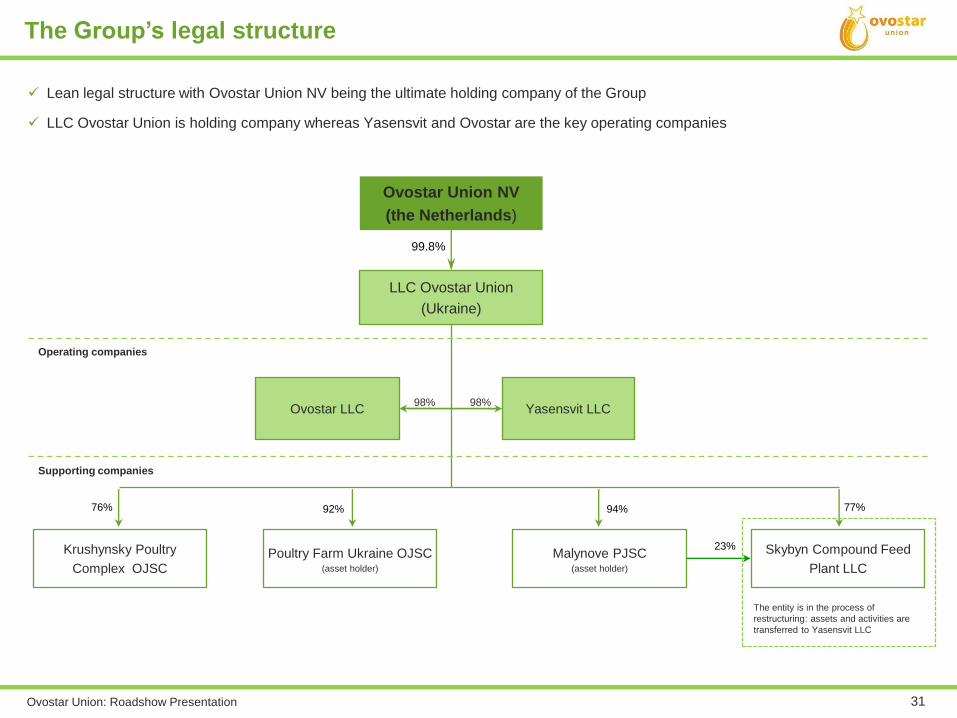

Ovostar Union: Roadshow Presentation 31

Poultry Farm Ukraine OJSC(asset holder)

LLC Ovostar Union

(Ukraine)

Malynove PJSC(asset holder)

Ovostar LLC Yasensvit LLC98%

76%

98%

92%

99.8%

94%

Ovostar Union NV

(the Netherlands)

Operating companies

Supporting companies

77%

Krushynsky Poultry

Complex OJSC

23% Skybyn Compound Feed

Plant LLC

The entity is in the process of

restructuring: assets and activities are

transferred to Yasensvit LLC

The Group’s legal structure

Lean legal structure with Ovostar Union NV being the ultimate holding company of the Group

LLC Ovostar Union is holding company whereas Yasensvit and Ovostar are the key operating companies

Ovostar Union: Roadshow Presentation 32

The Group primarily exports its shell eggs and egg

products to African countries (Liberia, Sierra Leone,

Congo, Angola, etc.), as well as CIS and

neighboring countries (Azerbaijan, Georgia,

Kazakhstan, Moldova, etc.), Sudan, China, Japan,

Iran, etc.

Export to Africa countries contributed for 50% of

total exports sales

Egg products exports structure, 2010

10%

4%50%

26%

7%

Iraq Kazakhstan African countries*

UAE Georgia Moldova

Source: Ovostar Union Source: Ovostar Union

6%

35%

29%

19%

12%

Iran Belarus Sudan China Azerbaijan

* Liberia, Angola, Congo, Sierra Leone

mUSD 2.2 mUSD 1.2

Eggs exports structure, 2010

Export – main directions

The Group intends to develop export sales channel

further and focus on other more prospective export

markets, including CIS and the Middle East

In 2009 Ovostar Union obtained Halal certificate

allowing to export to Muslim countries

In April 2011 Ovostar Union obtained Kosher

certification allowing export to Israel

Ovostar Union: Roadshow Presentation 33

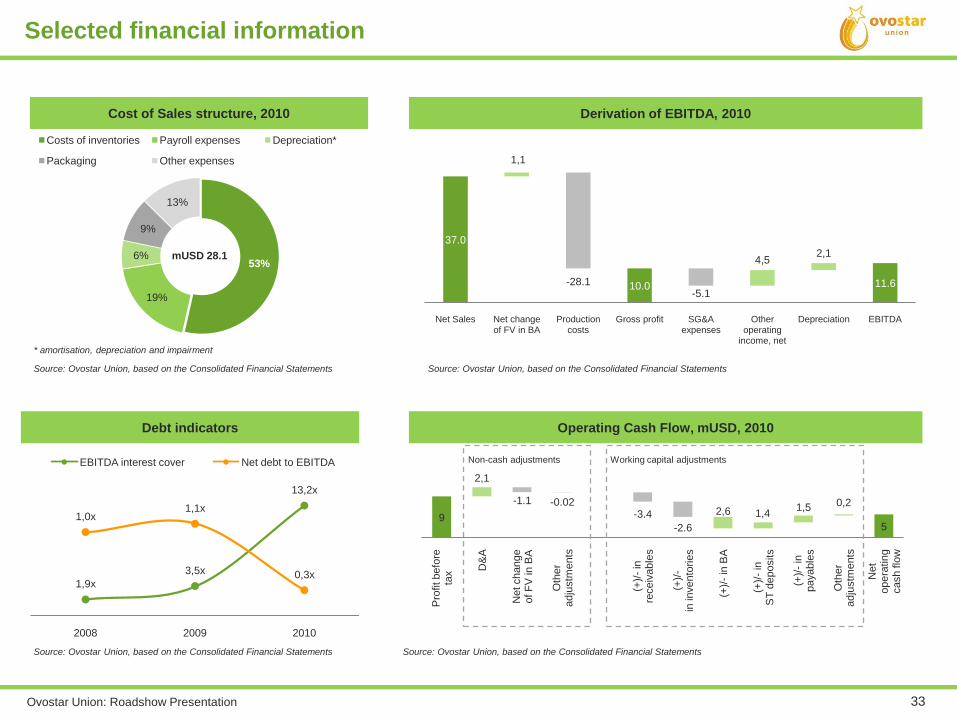

53%

19%

6%

9%

13%

Costs of inventories Payroll expenses Depreciation*

Packaging Other expenses

Operating Cash Flow, mUSD, 2010

Selected financial information

Debt indicators

1,9x

3,5x

13,2x

1,0x1,1x

0,3x

2008 2009 2010

EBITDA interest cover Net debt to EBITDA

Source: Ovostar Union, based on the Consolidated Financial Statements

95

2,1

-1.1 -0.02-3.4

-2.6

2,6 1,41,5 0,2

Pro

fit befo

reta

x

D&

A

Net change

of F

V in

BA

Oth

er

adju

stm

ents

(+)/

-in

re

ceiv

able

s

(+)/

-in

in

vento

rie

s

(+)/

-in

BA

(+)/

-in

ST

deposits

(+)/

-in

payable

s

Oth

er

adju

stm

ents

Net

opera

tin

gcash flo

w

Non-cash adjustments Working capital adjustments

Derivation of EBITDA, 2010

37.0

10.0 11.6

1,1

-28.1-5.1

4,52,1

Net Sales Net changeof FV in BA

Production costs

Gross profit SG&A expenses

Other operating

income, net

Depreciation EBITDA

Cost of Sales structure, 2010

Source: Ovostar Union, based on the Consolidated Financial Statements Source: Ovostar Union, based on the Consolidated Financial Statements

Source: Ovostar Union, based on the Consolidated Financial Statements

mUSD 28.1

* amortisation, depreciation and impairment

Ovostar Union: Roadshow Presentation 34

Note: Revaluation of biological assets methodology (IAS 41)

Biological assets (both current and non-current) are presented on the Balance Sheet at fair value (calculated using

DCF approach), as prescribed by IFRS

Revaluation procedure is performed at each reporting date

Main assumptions impacting the fair value in Balance Sheet are: flock number, hen age, expected cost per hen,

expected income per hen, hen productivity, production cycle and discount rate

Net change in fair value is calculated by adjusting the difference between opening and closing fair value of biological

assets on changes in value as a result of capitalization of costs and asset disposal during the period

Revaluation of biological assets

Ovostar Union: Roadshow Presentation 35

Borys Bielikov

CEO

Ovostar Union

Tel.: +380 44 354 29 60

Fax: +380 44 354 29 61

E-Mail: [email protected]

Vitalii Veresenko

Chairman of the Board

Ovostar Union

Tel.: +380 44 354 29 60

Fax: +380 44 354 29 61

E-Mail: [email protected]

Natalia Malyovana

Commercial Director

Ovostar Union

Tel.: +380 44 354 29 60

Fax: +380 44 354 29 61

E-Mail: [email protected]

Contact details

Ekaterina Pavlovskaya

IR manager

Ovostar Union

Tel.: +380 44 354 29 60

Fax: +380 44 354 29 61

E-Mail: [email protected]