Regulation of Financial Institutions Eric S. Rosengren President & CEO Federal Reserve Bank of...

22

Regulation of Financial Institutions Eric S. Rosengren President & CEO Federal Reserve Bank of Boston Open Classroom Northeastern University Boston, MA November 30, 2011 www.bostonfed.or g

-

Upload

cecil-bradford -

Category

Documents

-

view

215 -

download

0

Transcript of Regulation of Financial Institutions Eric S. Rosengren President & CEO Federal Reserve Bank of...

Regulation of Financial Institutions

Eric S. RosengrenPresident & CEO

Federal Reserve Bank of Boston

Open ClassroomNortheastern University

Boston, MA

November 30, 2011

www.bostonfed.org

Why Do We Regulate Financial Institutions?

If everyone wants funds at the same time cannot liquidate loans Depositors want immediate access to funds Borrowers want longer-term financing

Financial intermediaries borrow short and lend long – assume diversification reduces risk from maturity mismatch

Depression – bank runs – widespread bank closures

2

Depression Era Solution

Deposit Insurance – FDIC Banks have special role – depositors get

limited government guarantee Taxpayers at risk during failure

Banks limited in what risk they take Banks have capital requirements – CAMELS Regular bank exams

3

Problems Emerge

Interest on deposits does not rise at weaker banks Weak banks have incentive to take more risk Gains go to shareholders, losses go to

taxpayers Use financial institutions for other goals

Savings and Loans GSEs

Banks become larger and more complicated

4

Too Big to Fail

International loans – assumption that governments would not default

Real estate loans – assumption real estate values would not fall

Real estate securities – assumption securities with national pools of mortgages would be protected since national housing prices had not fallen

5

2007-2008

Runs are not unique to banks Investment banks – Bear Stearns, Lehman Insurance – AIG Money market funds – Reserve Primary Fund Exotic structures – SIV

International transmission of shocks – global banks are global problems

6

Money Market Mutual Funds (MMMFs)

Regulated by the SEC Must maintain significant liquidity ratios Limited in the duration and credit ratings of

instruments they can hold Not required to alter net value (NAV) to reflect

small movements in underlying asset values Like other mutual funds, not required to hold

any capital as protection This structure can generate shareholder “runs”

during times of financial stress7

Importance ofMoney Market Mutual Funds

Critical players in short-term credit markets Significant buyers of CP, ABCP and CDs Important source of financing for organizations

dependent on wholesale financing Largest investor focused on high-quality, very

short-term paper

8

9

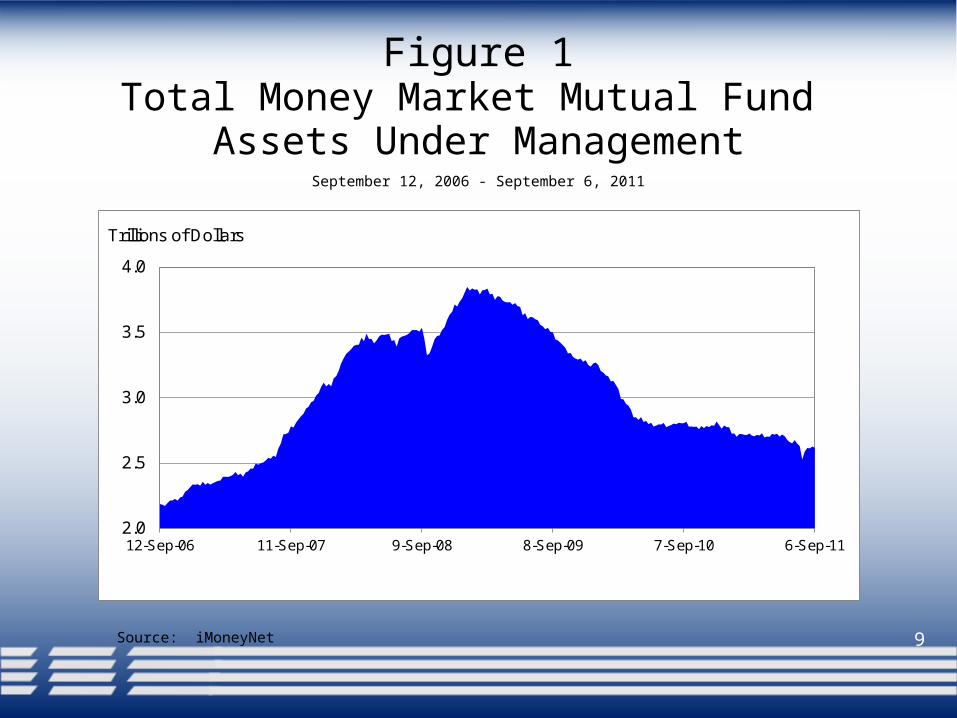

Figure 1Total Money Market Mutual Fund

Assets Under Management

Source: iMoneyNet

September 12, 2006 - September 6, 2011

2.0

2.5

3.0

3.5

4.0

12-Sep-06 11-Sep-07 9-Sep-08 8-Sep-09 7-Sep-10 6-Sep-11

Trillions of Dollars

10

Figure 2Total Money Market Mutual Fund

Assets Under Management by Type of Fund

Source: iMoneyNet

September 12, 2006 - September 6, 2011

0.0

0.5

1.0

1.5

2.0

2.5

12-Sep-06 11-Sep-07 9-Sep-08 8-Sep-09 7-Sep-10 6-Sep-11

Trillions of Dollars

Prime

Government

Tax-Free

LehmanFails (Sep 15)

11

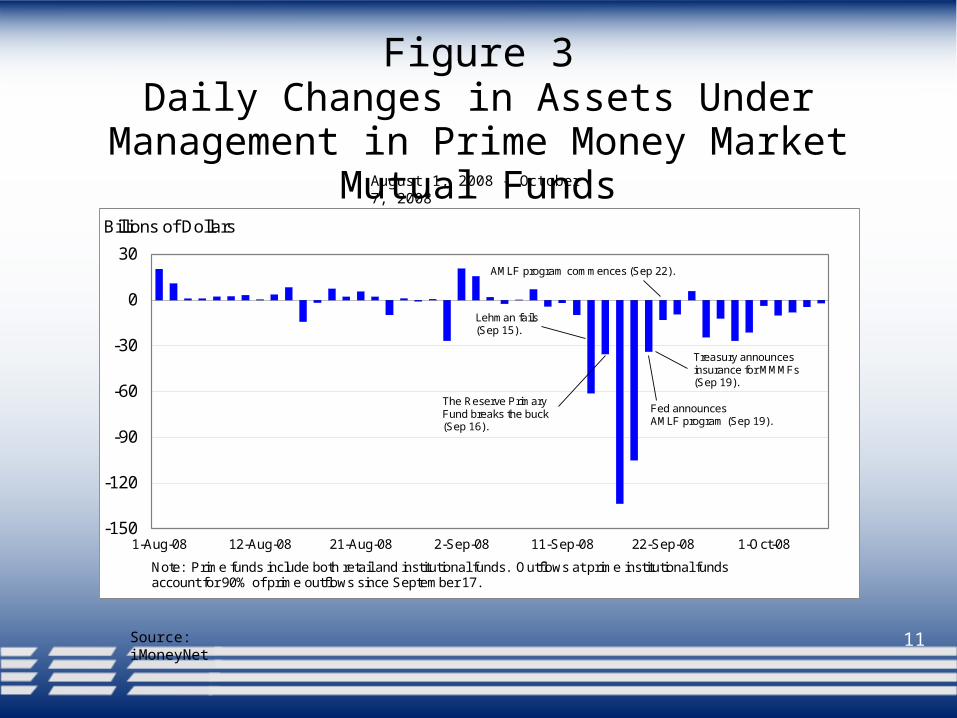

Figure 3Daily Changes in Assets Under Management

in Prime Money Market Mutual FundsAugust 1, 2008 - October 7, 2008

Source: iMoneyNet

-150

-120

-90

-60

-30

0

30

1-Aug-08 12-Aug-08 21-Aug-08 2-Sep-08 11-Sep-08 22-Sep-08 1-Oct-08

Note: Prime funds include both retail and institutional funds. Outflows at prime institutional funds account for 90% of prime outflows since September 17.

Billions of Dollars

Lehman fails(Sep 15).

The Reserve Primary Fund breaks the buck (Sep 16).

Fed announcesAMLF program (Sep 19).

AMLF program commences (Sep 22).

Treasury announces insurance for MMMFs (Sep 19).

Response to the Rapid Withdrawals

Treasury temporary insurance program Federal Reserve Bank of Boston administered

Fed lending facility Addressed short-term liquidity needs of MMMFs Helped stabilize short-term credit markets

disrupted by rapid liquidations Efforts proved successful at restoring stability,

avoiding further harm Balances have gradually declined (low rate

environment and corresponding returns)12

13

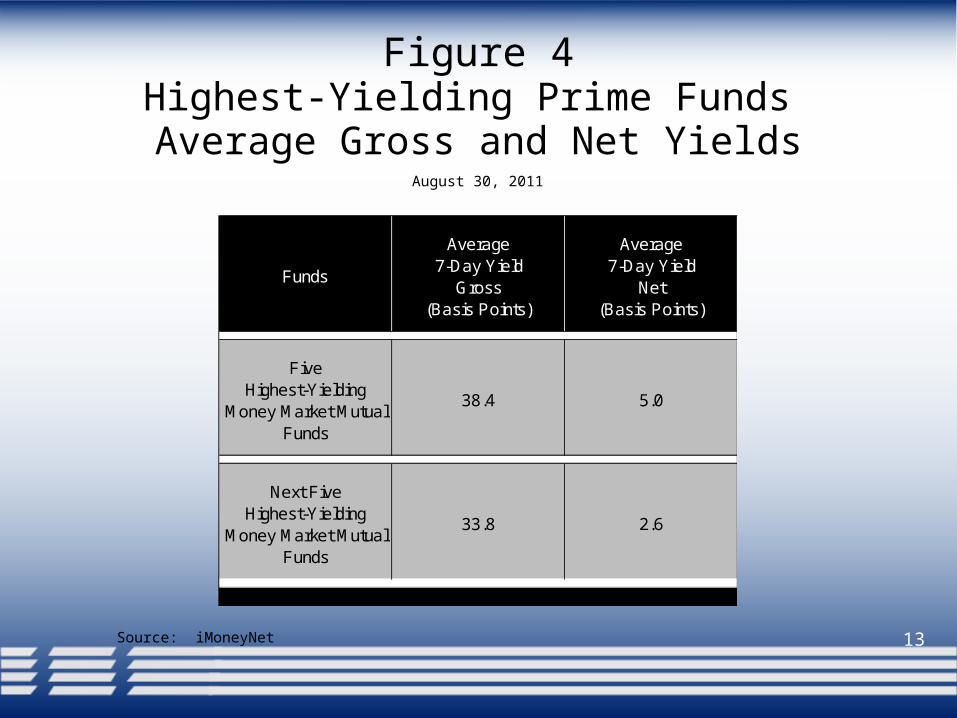

Figure 4Highest-Yielding Prime Funds Average Gross and Net Yields

Source: iMoneyNet

August 30, 2011

Funds

Average 7-Day Yield

Gross (Basis Points)

Average 7-Day Yield

Net (Basis Points)

Five Highest-Yielding

Money Market Mutual Funds

38.4 5.0

Next Five Highest-Yielding

Money Market Mutual Funds

33.8 2.6

14

Figure 5Foreign Exposure of Five Largest Prime

Money Market Mutual Funds

Source: Crane Data, Mutual Fund Company Websites

As of February 28, 2011 and August 31, 2011

-20

0

20

40

60

80

TotalForeign

Europe France UK Germany Italy

as of February 28, 2011

as of August 31, 2011

Change (Percentage Point Difference)

Percent

Financial Stability and MMMFs

Actions have been taken recently – improved liquidity and monthly reporting of holdings

Credit risk and MMMFs holdings Is the current structure appropriate given the

critical role of MMMFs to short-term credit markets?

15

No One Proposal has beenSettled on – My Preferred Approach

A meaningful capital-like buffer – perhaps 3%

If violated, automatically leads to conversion to a floating NAV

If plan for a buffer isn’t produced and accepted, require MMMFs to float NAV

16

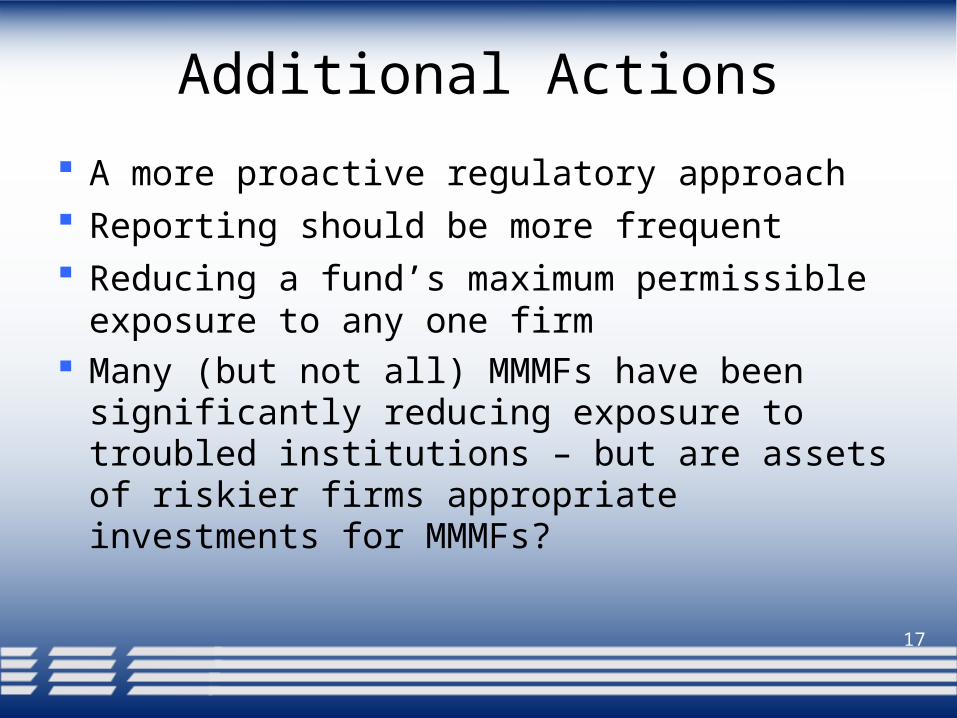

Additional Actions

A more proactive regulatory approach Reporting should be more frequent Reducing a fund’s maximum permissible

exposure to any one firm Many (but not all) MMMFs have been

significantly reducing exposure to troubled institutions – but are assets of riskier firms appropriate investments for MMMFs?

17

MMMFs are Intertwined with Another Systemic Risk Issue

Dependence of foreign branches and agencies in the U.S. on short-term wholesale funding

Not able to get deposit insurance or FHLB membership

Issuing jumbo CDs, CP, and repurchase agreements

During times of stress, less stable than retail deposits

18

Challenges from Europe

Banks are large relative to their economies Global banks have significant operations in

the United States Many global banks have large exposures to

European sovereign debt Wholesale credit markets showing significant

stress

19

20

Figure 6Bank Size Relative to Country Size:

Assets of Largest Bank as a Share of GDP

Source: Global Finance, IMF

as of Year End 2010

Note: Includes the U.S. and all European countries with a bank ranked in the top 50 worldwide as of year end 2010.

0

50

100

150

200

250

300

Percent

Switzerland

Netherlands

DenmarkSweden

Belgium

SpainUnited

KingdomFrance

GermanyItaly

United States

21

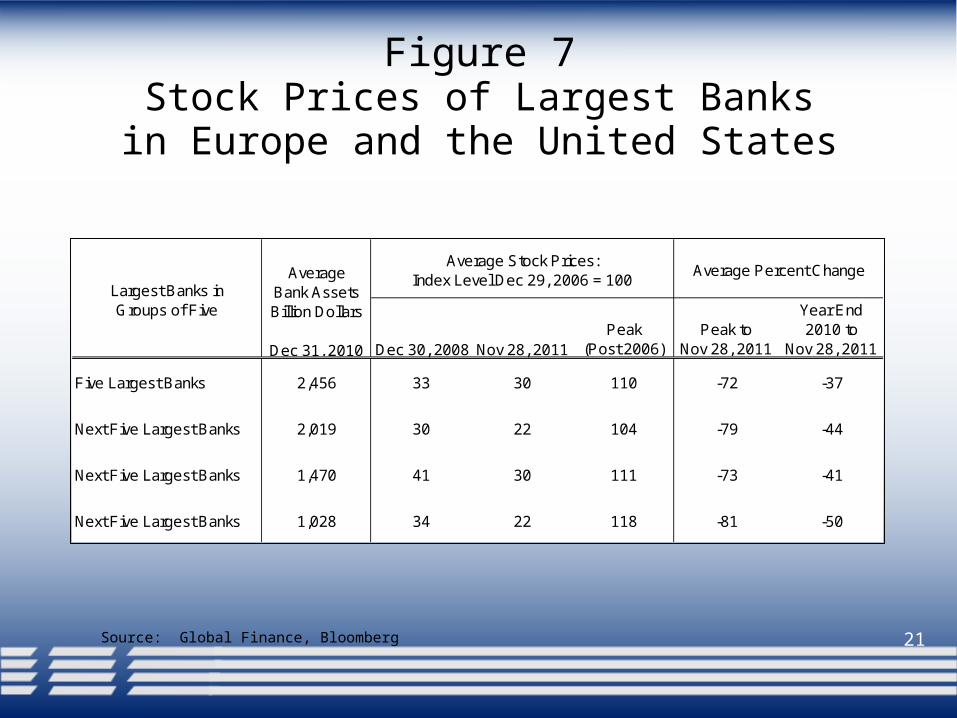

Figure 7Stock Prices of Largest Banks

in Europe and the United States

Source: Global Finance, Bloomberg

Dec 30, 2008 Nov 28, 2011Peak

(Post 2006)Peak to

Nov 28, 2011

Year End 2010 to

Nov 28, 2011

2,456 33 30 110 -72 -37

2,019 30 22 104 -79 -44

1,470 41 30 111 -73 -41

1,028 34 22 118 -81 -50

Largest Banks in Groups of Five

Next Five Largest Banks

Average Percent ChangeAverage Stock Prices:

Index Level Dec 29, 2006 = 100Average Bank Assets Billion Dollars sssssssssss Dec 31, 2010

Five Largest Banks

Next Five Largest Banks

Next Five Largest Banks

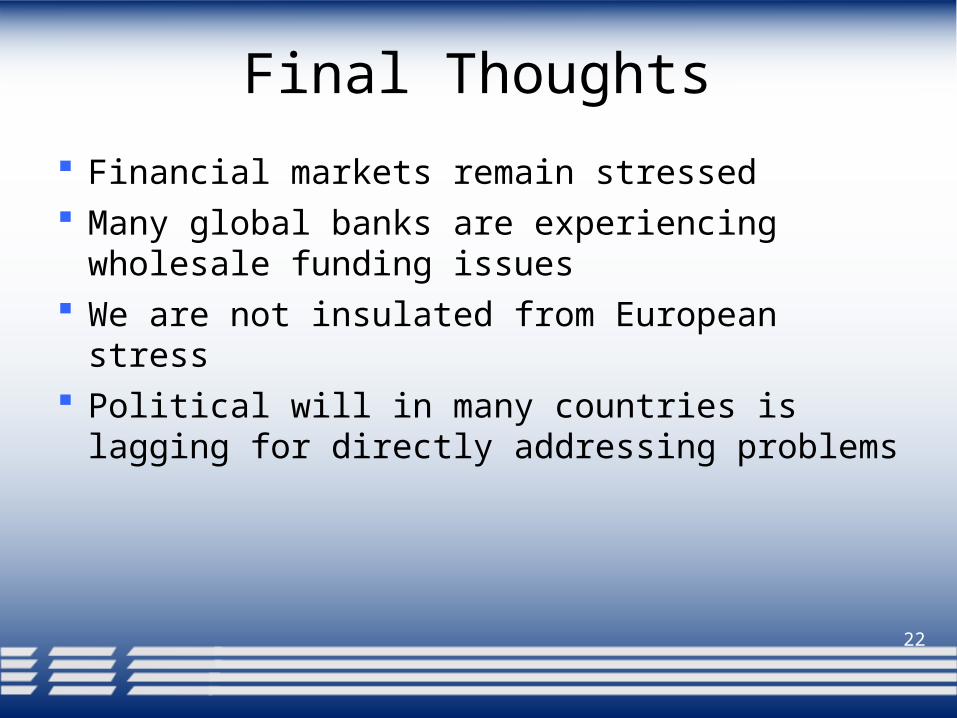

Final Thoughts

Financial markets remain stressed Many global banks are experiencing

wholesale funding issues We are not insulated from European stress Political will in many countries is lagging for

directly addressing problems

22

![[Kestävän aluesuunnittelun työkalut käyttöön 3.10.2013] Katriina Rosengren, SYKE: KEKO B-tutkimuskokonaisuus ja tulosodotukset](https://static.fdocument.pub/doc/165x107/547175b4b4af9fae0a8b4bb9/kestaevaen-aluesuunnittelun-tyoekalut-kaeyttoeoen-3102013-katriina-rosengren-syke-keko-b-tutkimuskokonaisuus-ja-tulosodotukset.jpg)