Presenting the FHA's HECM

27

FHA’s Home Equity Conversion Mortgage (HECM) UNDERSTANDING IT AS A CASH-FLOW MANAGEMENT TOOL FOR MATURE HOMEOWNERS

-

Upload

mary-jo-lafaye-reverse-mortgage -

Category

Economy & Finance

-

view

23 -

download

1

Transcript of Presenting the FHA's HECM

FHA’sHome Equity Conversion

Mortgage (HECM)

UNDERSTANDING IT AS A CASH-FLOW MANAGEMENT TOOL FOR MATURE

HOMEOWNERS

Your Presenters: Mary Jo and Amanda

HECM DefinedA federally-guaranteed home loan with deferred repayment:

◦primary residence◦single-family residence◦HUD-approved condos◦1-4 unit buildings◦Co-ops, not yet….

HECM Defined

Insured by HUD◦ non-recourse◦ no personal liability

(only subject property is liable for accrued debt)

HECM Defined Primary residence Borrower must be

62+ Loan amount is lower

if NBS is younger

HECM Defined Repayment deferred until Triggering Event:Death of last remaining borrower or

eligible non-borrowing spouse (NBS)12 consecutive months of all residents

being out of the home Choose to sell, re-fi or transfer title Convert to rental property

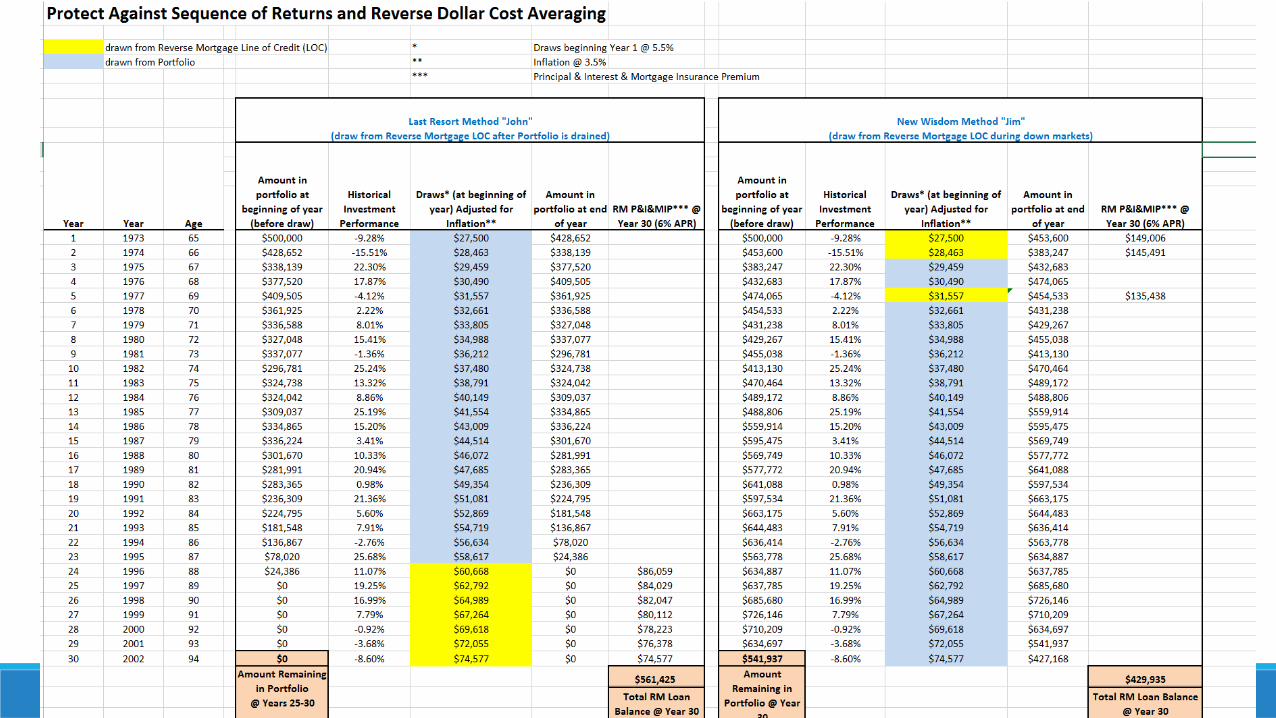

Sequence of Returns &Reverse Dollar Cost Averaging

A Different Kind of Cash Flow Management Tool: Variable interest rate (lender’s margin + Annual

LIBOR) Revolving Line of Credit (LOC)

◦ LOC restores if borrower ever chooses to make a payment (always optional)

◦ Growth Rate of credit line is automatic and federally-guaranteed

◦ regardless of home value or outside factors available proceeds uncapped over life of loan

Draws are tax-free

HECM Defined Lump Sum◦ Fixed-interest rate◦ NOT a revolving LOC◦ Extinguish existing mortgage

and consumer debt to reduce draw rate from investment portfolio

Availability of funds Variable interest rate (lender’s margin + Annual LIBOR)

◦Revolving Line of Credit◦Tenure – lifetime payment to borrower based on age

◦Term – choose number of months or monthly amount

Flexibility of variable rate loan

Borrower can choose combo of any/all options at closing◦ LOC + lump sum + tenure

or term paymentBorrower can restructure at

any time and as needed

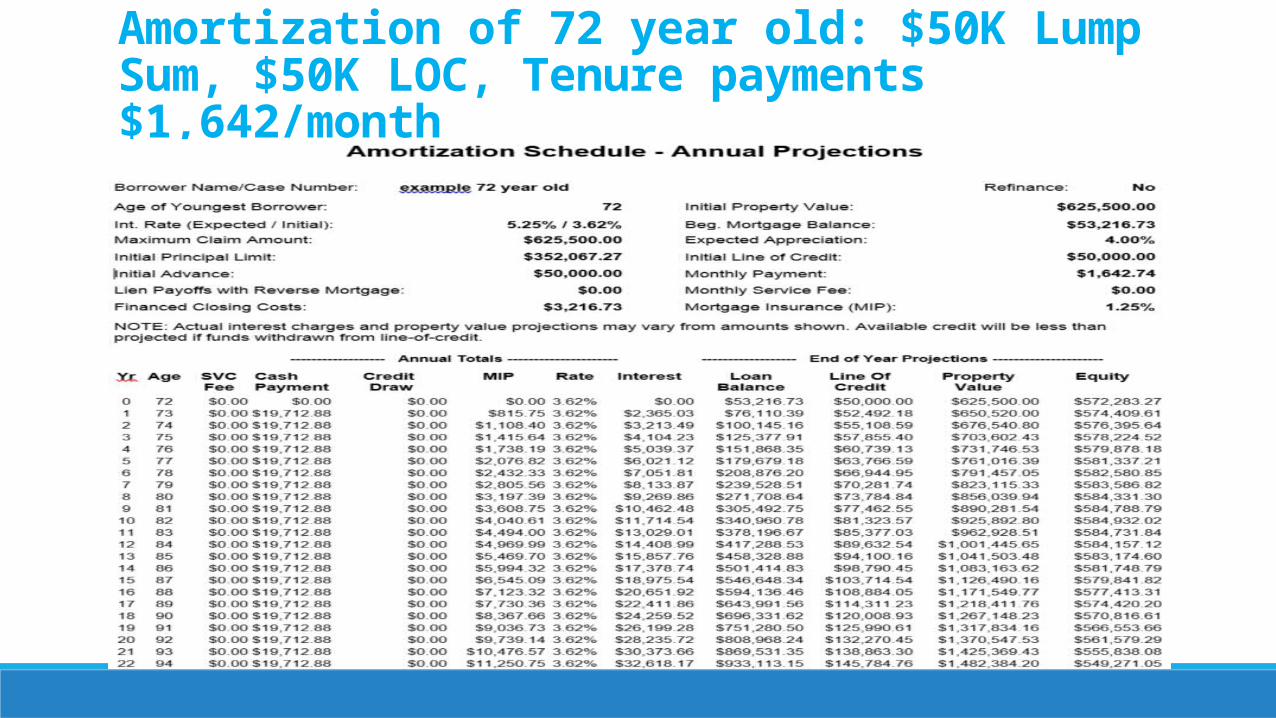

Amortization of 72 year old: $50K Lump Sum, $50K LOC, Tenure payments $1,642/month

HECM vs. HELOC The HECM loan is vastly more flexible and offers protections not available in other types of lines of credit

◦ LOC cannot be arbitrarily frozen or reduced◦ Non-recourse◦ Never re-casts into a P&I payment◦ Zero monthly repayment ◦ Open ended term (lifetime residency)◦ Unlimited Draw period◦ Federally-regulated

What’s new?Lower IMIP for borrowers accessing <60% year one.Eligible non-borrowing spouse now protected for lifeDefault reduction plan instituted by HUD •Minimal financial and credit assessment done at

application• LESA (set-aside) created for borrowers with prop

tax / home owner’s insurance delinquency

What’s new?

Lifetime interest rate cap lowered from 10 to 5. Borrower has option for no set up fee loan Higher rate = faster increase in LOC funds

HUD’s formula 10-year LIBOR swap (used in Expected Rate)

and

Age of youngest borrower determines

Principal Limit Factor (Percentage of 625,500 or home value,

whichever is less)

No Longer a Last ResortMichael Kitces, recently spoke at NAPFA May 2015, “Taking a Fresh Look at Reverse Mortgages”Barry Sacks, “Reversing Conventional Wisdom”Salter and Evensky, “Standby Reverse Mortgages: A Risk Management Tool for Retirement Distrbutions”Boston College Center for Retirement Research, “Using Your House for Income in Retirement”

Application Timing? When LIBOR increases, $$ available to Borrower decreases. Example: 73 year old5% Exp Rate = 58% Principal Limit Factor6% Exp Rate = 49% Principal Limit Factor8% Exp Rate = 37% Principal Limit Factor10% Exp Rate = 28% Principal Limit Factor

Case StudiesSequence of Returns in Draw Period – Line of CreditDrawing more than recommended – TenureHealth care – TermCombo (LOC/Term/Tenure)Extinguish mortgageDownsizeDivorce/inheritance – Settle the estateAvoid Capital Gains - Stay in home

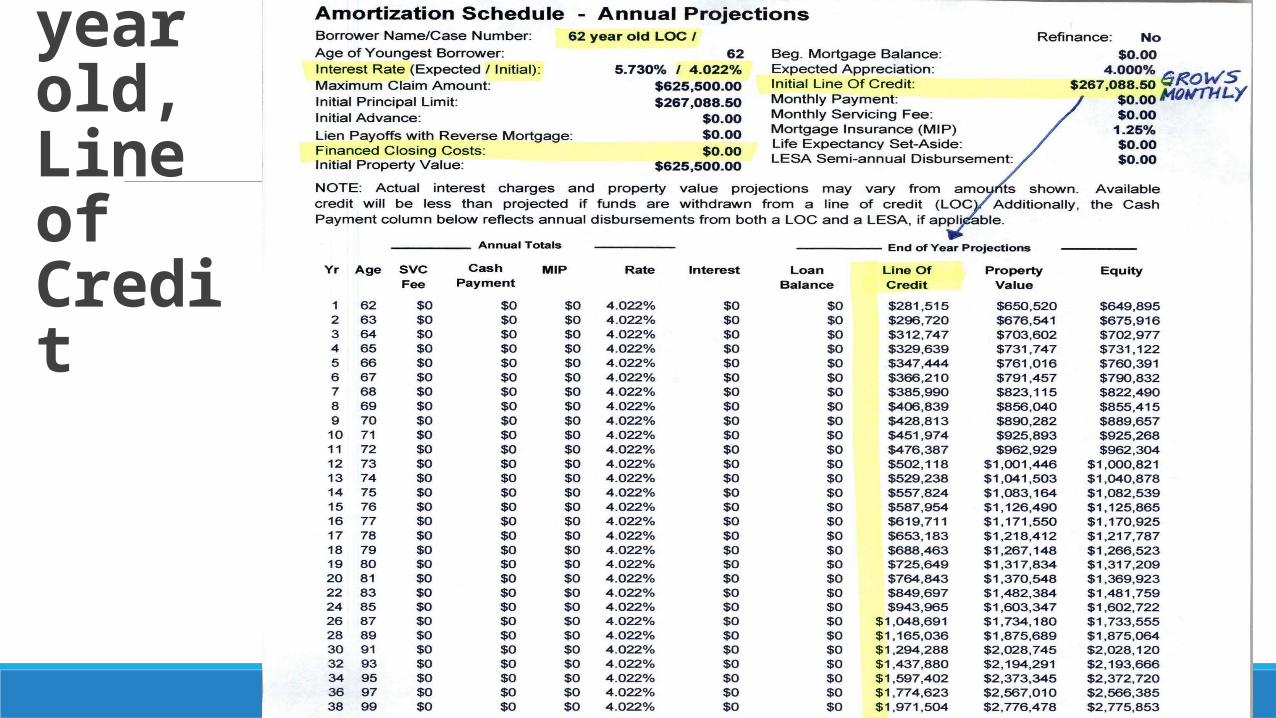

62 year old, Line of Credit

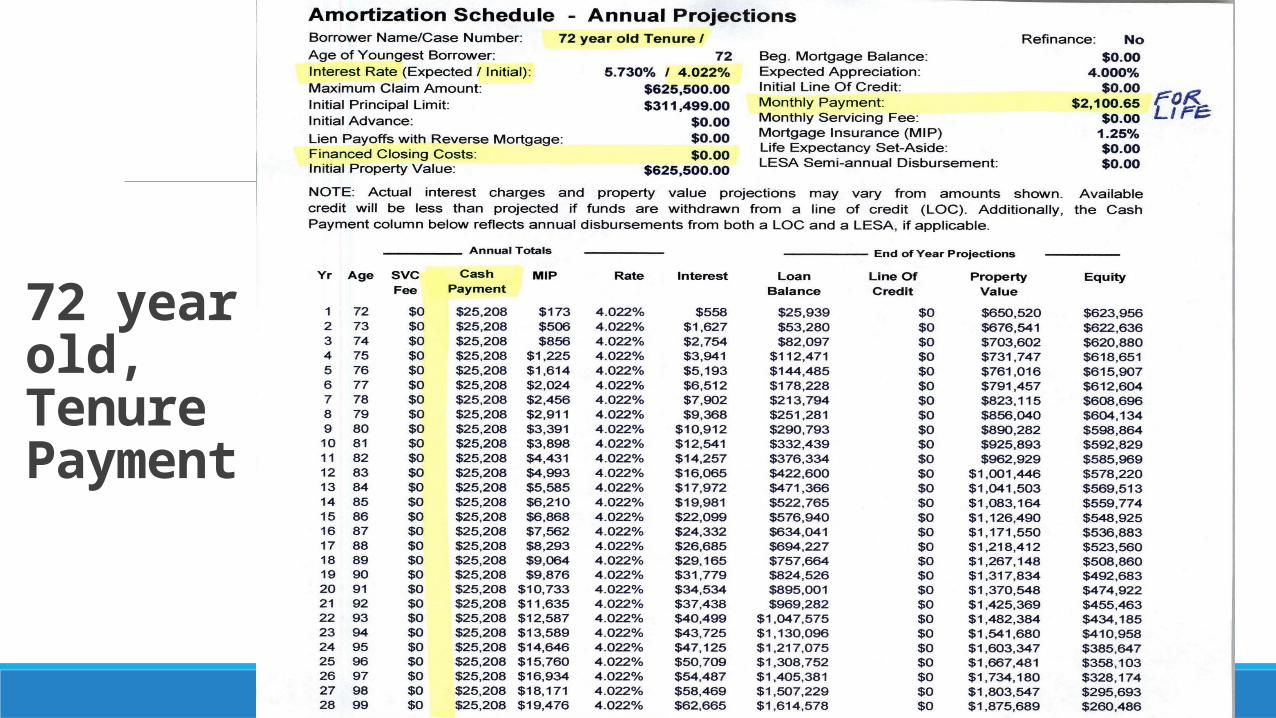

72 year old, Tenure Payment

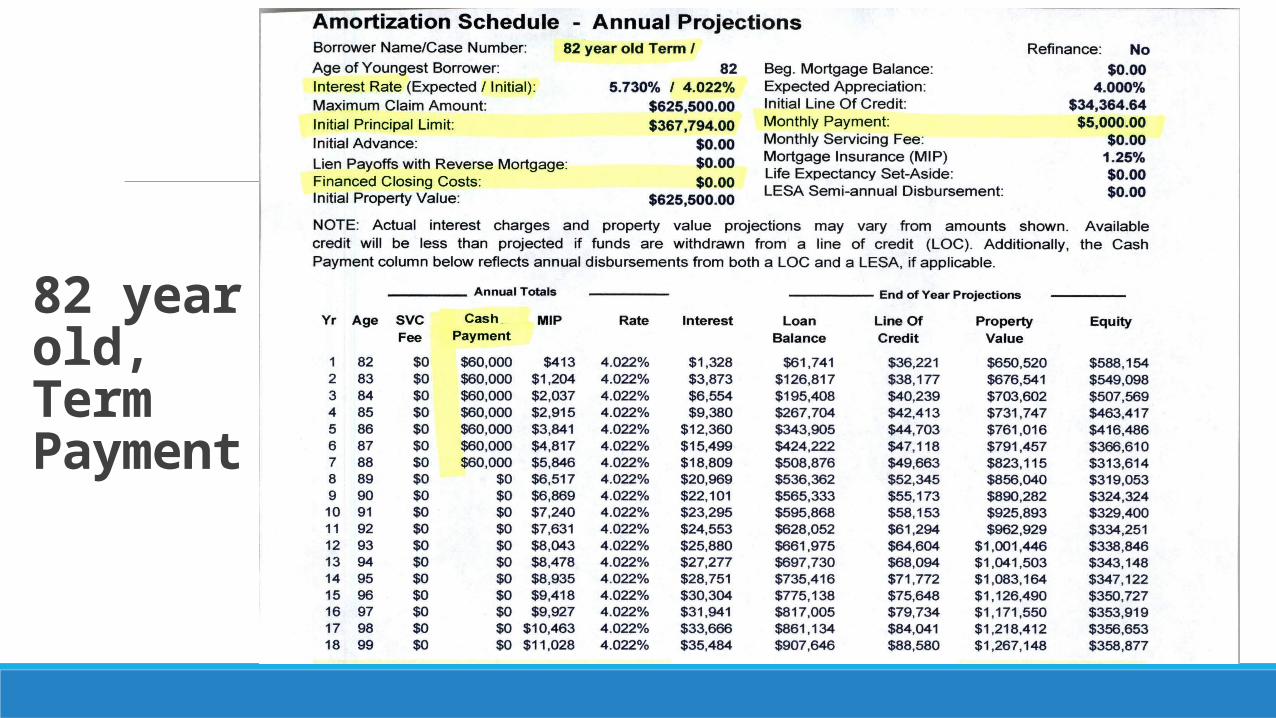

82 year old, Term Payment

What else? Downsizing:

◦Eliminate existing mortgage payments

and◦Beef up Investment Portfolio

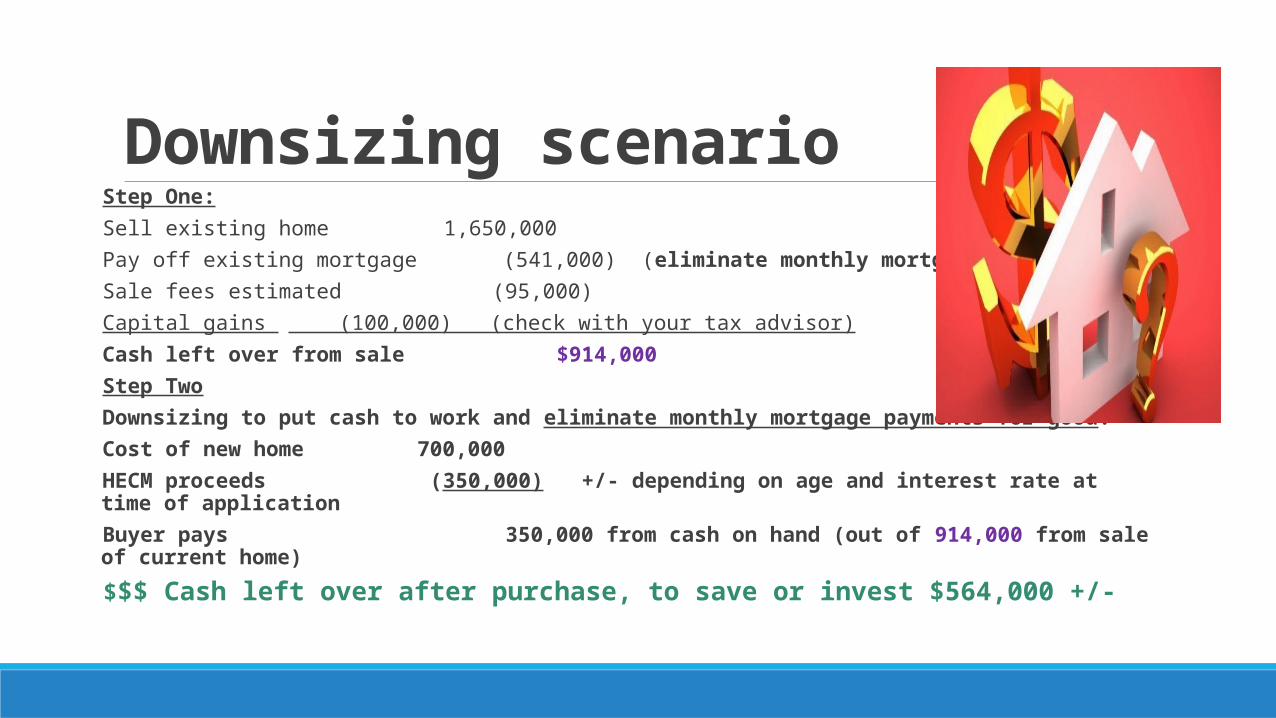

Downsizing scenario Step One: Sell existing home 1,650,000 Pay off existing mortgage (541,000) (eliminate monthly mortgage payments) Sale fees estimated (95,000) Capital gains (100,000) (check with your tax advisor) Cash left over from sale $914,000 Step Two Downsizing to put cash to work and eliminate monthly mortgage payments for good: Cost of new home 700,000 HECM proceeds (350,000) +/- depending on age and interest rate at time of application Buyer pays 350,000 from cash on hand (out of 914,000 from sale of current home)

$$$ Cash left over after purchase, to save or invest $564,000 +/-

No Longer a Last Resort Based on current academic and scholarly research, advisors may have a fiduciary responsibility to evaluate -- for each client entering retirement -- the potential effectiveness of the FHA’s HECM to reduce the probability of untimely portfolio exhaustion.

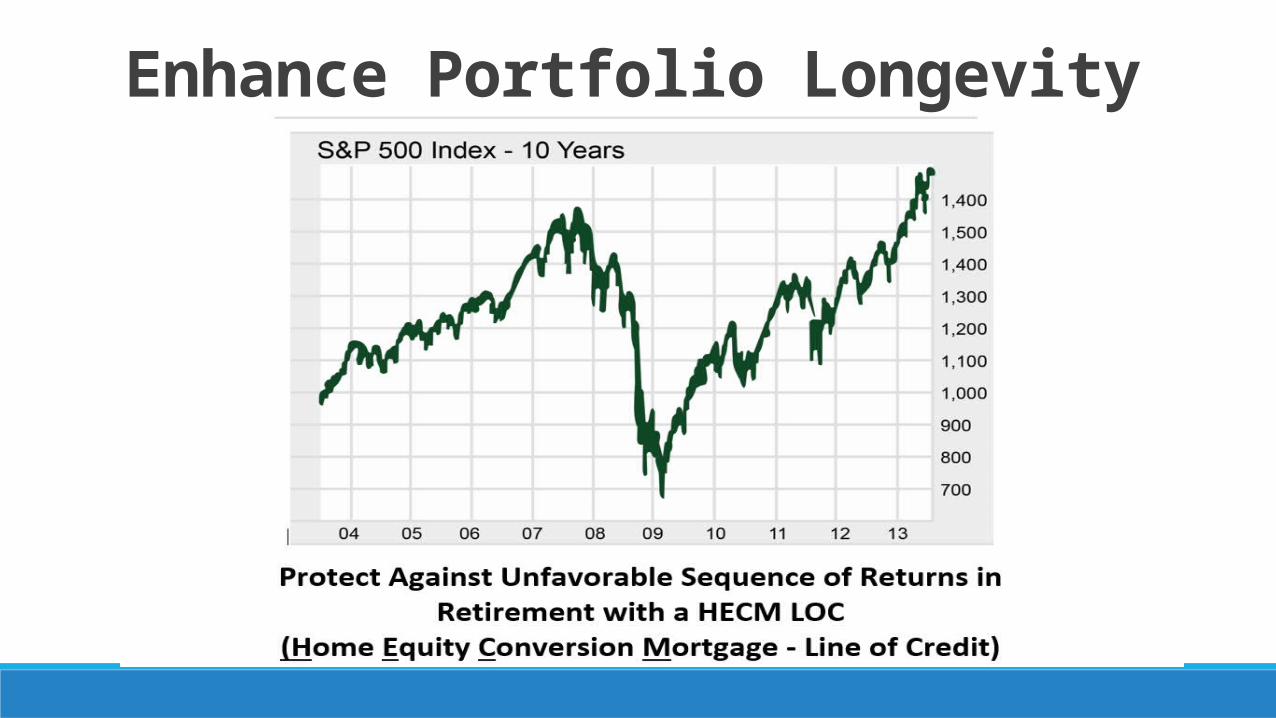

Enhance Portfolio LongevityEnhance Portfolio Longevity

All research posted on-line at:

www.FhaReverseBlog.com

Amanda Keith, CPA, nmls# 1247741 415.747.5668

900 Larkspur Landing Circle, Suite 240, Larkspur, CA 94939Fax 650.284.2599

Thank You!