participate in it” Warren Buffett someone who repeatedly ... Partners Letter... · Attached is...

8

"Look at market fluctuations as your friend rather than your enemy; profit from folly rather than participate in it” Warren Buffett "We believe that according the name 'investors' to institutions that trade actively is like calling someone who repeatedly engages in one-night stands a 'romantic" Warren Buffet The fund has been up and running for four months now and we certainly picked a very volatile time to launch. Pair wise correlation in June reached levels last seen in 1987 (see graph below) as volatility caused by macro uncertainty caused investors to sell stocks indiscriminately. We further more believe High Frequency Trading (HFT) which are run by computer programs employed by hedge funds, which currently accounts for between 50%- 70% of volume, has further increased this volatility and was the reason for the flash crash of May 6 where the Dow dropped 998 points in 10 min before rising 600 points before finally closing down 350. As mentioned in previous mails this recovery has been led by lower quality companies that are both operationally and financially geared with poor prospects. Many of these were of the verge of bankruptcy a year ago yet have outperformed quality for 14 months, the 3rd longest cycle since 1987. How long it will persist we cannot forecast but I think its safe to assume the trend is long in the tooth. The trifecta of volatility, high correlation and low quality outperforming is not a great environment for bottom up stock picking to outperform in the short term but does provide us with some wonderful opportunities to set the stage for significant outperformance over the next few years as we are able to buy quality companies with bright prospects at the same or even cheaper valuations than the market which in itself is cheap (see table below). When rationality returns and the market once again shows a preference for stable earnings with good prospects we should be duly rewarded even if multiples do not expand. With our bias for quality and concentration we should benefit disproportionately when this happens.

-

Upload

trinhkhanh -

Category

Documents

-

view

221 -

download

0

Transcript of participate in it” Warren Buffett someone who repeatedly ... Partners Letter... · Attached is...

"Look at market fluctuations as your friend rather than your enemy; profit from folly rather than participate in it” Warren Buffett "We believe that according the name 'investors' to institutions that trade actively is like calling someone who repeatedly engages in one-night stands a 'romantic" Warren Buffet The fund has been up and running for four months now and we certainly picked a very volatile time to launch. Pair wise correlation in June reached levels last seen in 1987 (see graph below) as volatility caused by macro uncertainty caused investors to sell stocks indiscriminately. We further more believe High Frequency Trading (HFT) which are run by computer programs employed by hedge funds, which currently accounts for between 50%-70% of volume, has further increased this volatility and was the reason for the flash crash of May 6 where the Dow dropped 998 points in 10 min before rising 600 points before finally closing down 350. As mentioned in previous mails this recovery has been led by lower quality companies that are both operationally and financially geared with poor prospects. Many of these were of the verge of bankruptcy a year ago yet have outperformed quality for 14 months, the 3rd longest cycle since 1987. How long it will persist we cannot forecast but I think its safe to assume the trend is long in the tooth. The trifecta of volatility, high correlation and low quality outperforming is not a great environment for bottom up stock picking to outperform in the short term but does provide us with some wonderful opportunities to set the stage for significant outperformance over the next few years as we are able to buy quality companies with bright prospects at the same or even cheaper valuations than the market which in itself is cheap (see table below). When rationality returns and the market once again shows a preference for stable earnings with good prospects we should be duly rewarded even if multiples do not expand. With our bias for quality and concentration we should benefit disproportionately when this happens.

Below is a table that illustrates the difference in yield between the earnings yield on the Dow and high grade corporate bond yields at every market bottom since 1932. The average difference at market bottoms since 1932 is -2.8%, we are currently sitting at approximately -4.3%. The earnings yield of the market as a whole is 9.6% when adjusted for the $100 of cash embedded in the SP500 its over 10%. If companies can grow at 5%, which they will be able to do without having to reinvest earnings since there is so much spare capacity, investors will receive mid double digit returns p.a. even if multiples did not expand. Our portfolio of assets are far cheaper than the market overall with better growth prospects and I expect our returns to be 20%+ p.a next couple of years. It amazes me that one can obtain such a large spread by owning a growing coupon relative to lending a fixed one. How long the anomaly will persist is beyond our ability to forecast but that it will eventually normalise is a certainty, as it always has in the past. Attached is our latest letter for your perusal where we speak in greater detail as to why we have such a constructive view currently.

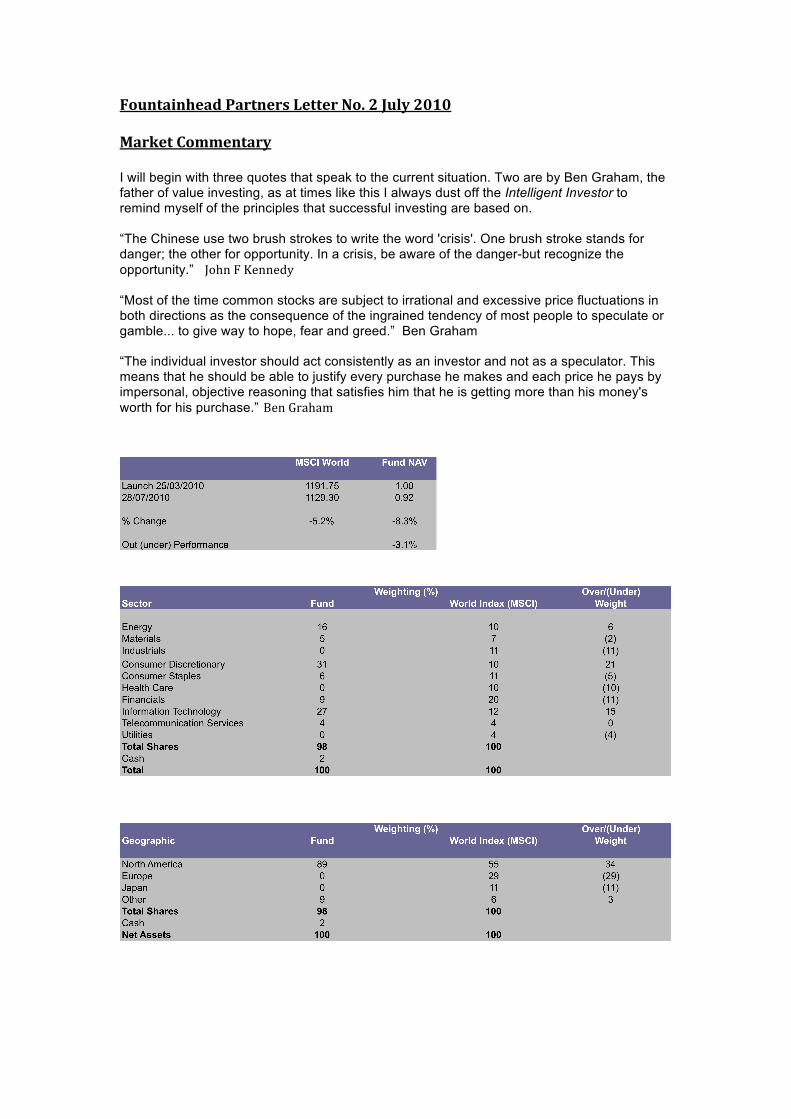

Fountainhead Partners Letter No. 2 July 2010 Market Commentary I will begin with three quotes that speak to the current situation. Two are by Ben Graham, the father of value investing, as at times like this I always dust off the Intelligent Investor to remind myself of the principles that successful investing are based on. “The Chinese use two brush strokes to write the word 'crisis'. One brush stroke stands for danger; the other for opportunity. In a crisis, be aware of the danger-but recognize the opportunity.” John F Kennedy “Most of the time common stocks are subject to irrational and excessive price fluctuations in both directions as the consequence of the ingrained tendency of most people to speculate or gamble... to give way to hope, fear and greed.” Ben Graham “The individual investor should act consistently as an investor and not as a speculator. This means that he should be able to justify every purchase he makes and each price he pays by impersonal, objective reasoning that satisfies him that he is getting more than his money's worth for his purchase.” Ben Graham

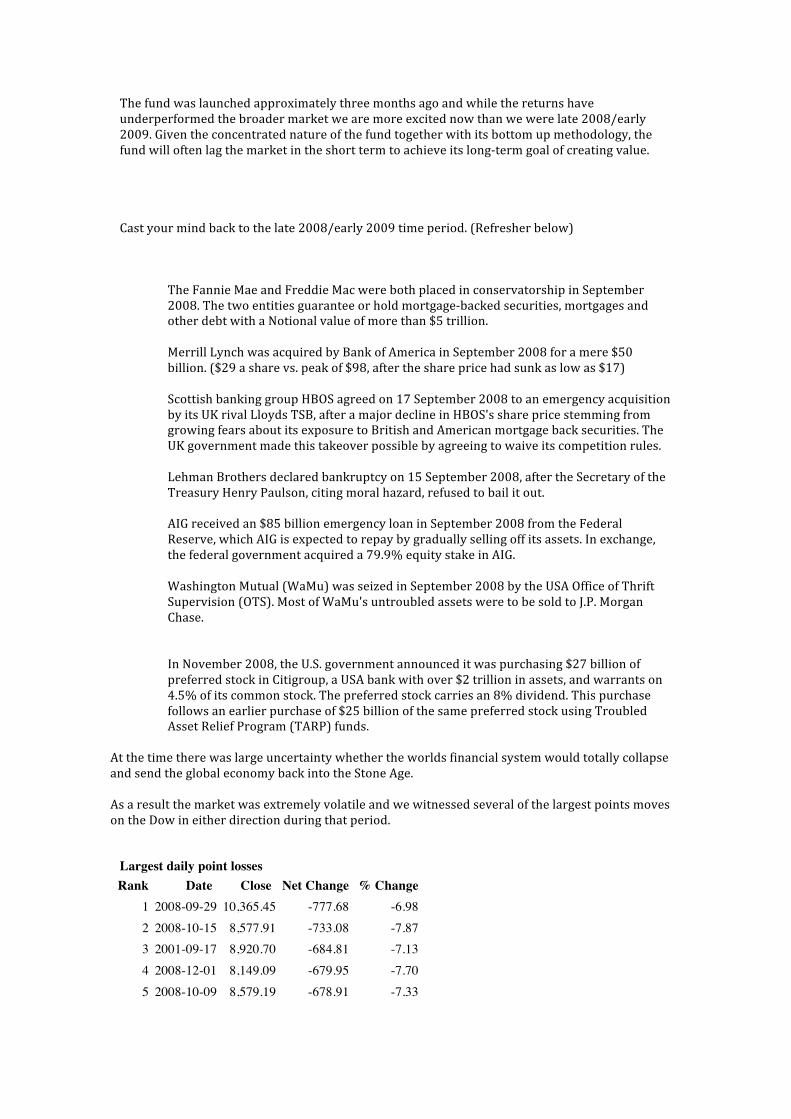

The fund was launched approximately three months ago and while the returns have underperformed the broader market we are more excited now than we were late 2008/early 2009. Given the concentrated nature of the fund together with its bottom up methodology, the fund will often lag the market in the short term to achieve its long-‐term goal of creating value. Cast your mind back to the late 2008/early 2009 time period. (Refresher below)

The Fannie Mae and Freddie Mac were both placed in conservatorship in September 2008. The two entities guarantee or hold mortgage-‐backed securities, mortgages and other debt with a Notional value of more than $5 trillion.

Merrill Lynch was acquired by Bank of America in September 2008 for a mere $50 billion. ($29 a share vs. peak of $98, after the share price had sunk as low as $17)

Scottish banking group HBOS agreed on 17 September 2008 to an emergency acquisition by its UK rival Lloyds TSB, after a major decline in HBOS's share price stemming from growing fears about its exposure to British and American mortgage back securities. The UK government made this takeover possible by agreeing to waive its competition rules.

Lehman Brothers declared bankruptcy on 15 September 2008, after the Secretary of the Treasury Henry Paulson, citing moral hazard, refused to bail it out.

AIG received an $85 billion emergency loan in September 2008 from the Federal Reserve, which AIG is expected to repay by gradually selling off its assets. In exchange, the federal government acquired a 79.9% equity stake in AIG. Washington Mutual (WaMu) was seized in September 2008 by the USA Office of Thrift Supervision (OTS). Most of WaMu's untroubled assets were to be sold to J.P. Morgan Chase.

In November 2008, the U.S. government announced it was purchasing $27 billion of preferred stock in Citigroup, a USA bank with over $2 trillion in assets, and warrants on 4.5% of its common stock. The preferred stock carries an 8% dividend. This purchase follows an earlier purchase of $25 billion of the same preferred stock using Troubled Asset Relief Program (TARP) funds.

At the time there was large uncertainty whether the worlds financial system would totally collapse and send the global economy back into the Stone Age. As a result the market was extremely volatile and we witnessed several of the largest points moves on the Dow in either direction during that period.

Largest daily point losses Rank Date Close Net Change % Change

1 2008-09-29 10,365.45 -777.68 -6.98 2 2008-10-15 8,577.91 -733.08 -7.87 3 2001-09-17 8,920.70 -684.81 -7.13 4 2008-12-01 8,149.09 -679.95 -7.70 5 2008-10-09 8,579.19 -678.91 -7.33

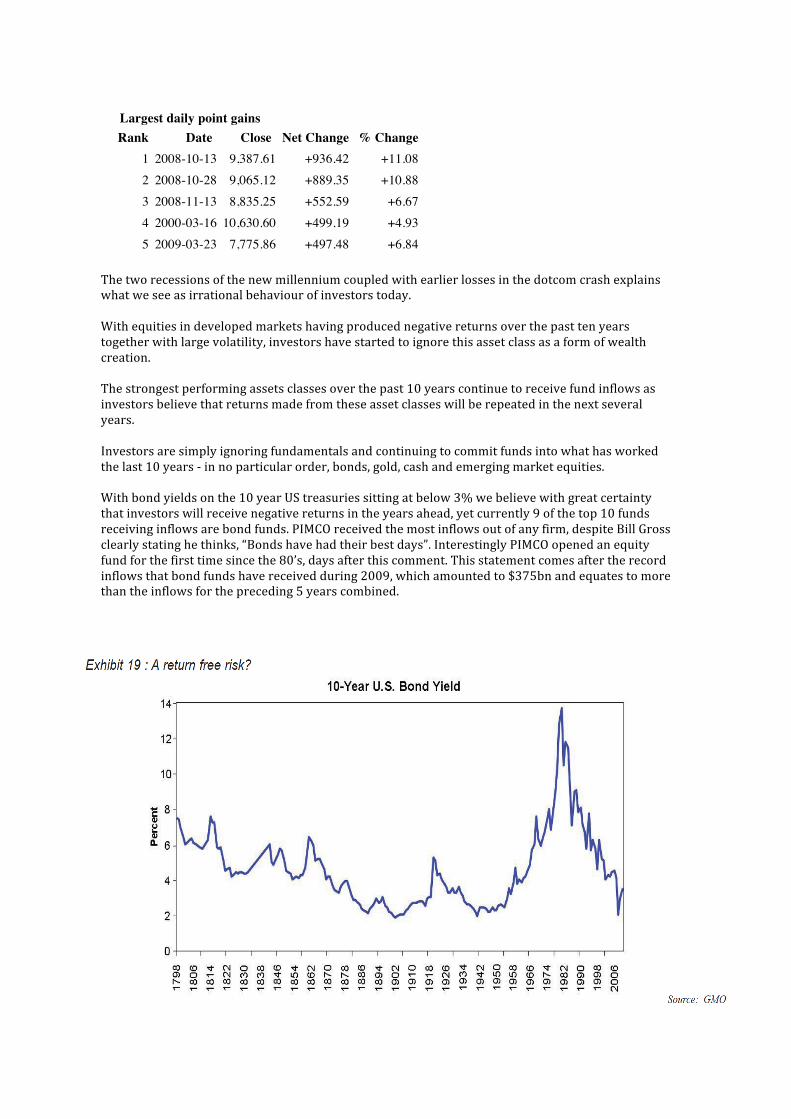

Largest daily point gains Rank Date Close Net Change % Change

1 2008-10-13 9,387.61 +936.42 +11.08 2 2008-10-28 9,065.12 +889.35 +10.88 3 2008-11-13 8,835.25 +552.59 +6.67 4 2000-03-16 10,630.60 +499.19 +4.93 5 2009-03-23 7,775.86 +497.48 +6.84

The two recessions of the new millennium coupled with earlier losses in the dotcom crash explains what we see as irrational behaviour of investors today. With equities in developed markets having produced negative returns over the past ten years together with large volatility, investors have started to ignore this asset class as a form of wealth creation. The strongest performing assets classes over the past 10 years continue to receive fund inflows as investors believe that returns made from these asset classes will be repeated in the next several years. Investors are simply ignoring fundamentals and continuing to commit funds into what has worked the last 10 years -‐ in no particular order, bonds, gold, cash and emerging market equities. With bond yields on the 10 year US treasuries sitting at below 3% we believe with great certainty that investors will receive negative returns in the years ahead, yet currently 9 of the top 10 funds receiving inflows are bond funds. PIMCO received the most inflows out of any firm, despite Bill Gross clearly stating he thinks, “Bonds have had their best days”. Interestingly PIMCO opened an equity fund for the first time since the 80’s, days after this comment. This statement comes after the record inflows that bond funds have received during 2009, which amounted to $375bn and equates to more than the inflows for the preceding 5 years combined.

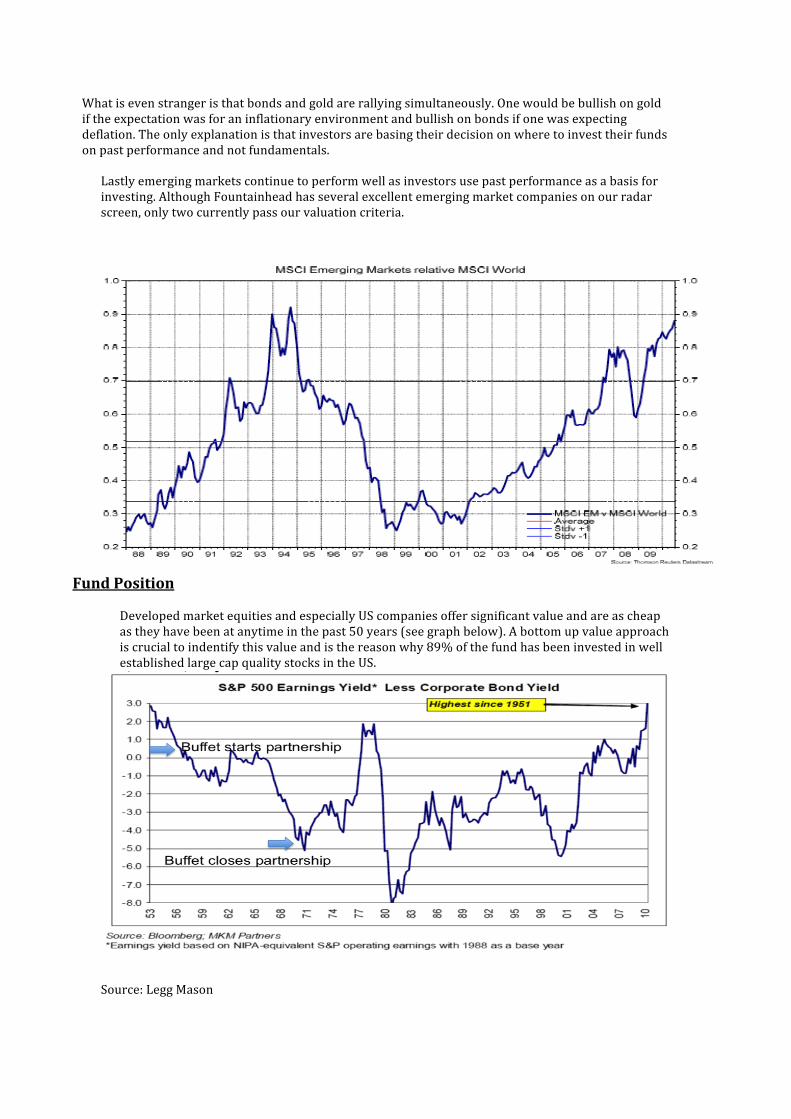

What is even stranger is that bonds and gold are rallying simultaneously. One would be bullish on gold if the expectation was for an inflationary environment and bullish on bonds if one was expecting deflation. The only explanation is that investors are basing their decision on where to invest their funds on past performance and not fundamentals.

Lastly emerging markets continue to perform well as investors use past performance as a basis for investing. Although Fountainhead has several excellent emerging market companies on our radar screen, only two currently pass our valuation criteria.

Fund Position Developed market equities and especially US companies offer significant value and are as cheap as they have been at anytime in the past 50 years (see graph below). A bottom up value approach is crucial to indentify this value and is the reason why 89% of the fund has been invested in well established large cap quality stocks in the US.

Source: Legg Mason

Once again I reiterate to partners that most of these companies are actually global companies with US listing, but due to the negativity surrounding equity investing in the US, one can buy these stocks at fantastic prices. One has far more visibility today than what one had in 2008/early 2009, yet many of these stocks trade at very similar prices to what we saw the during the worst part of the crisis. This increases our belief for the return potential of the portfolio. All the companies, whether from balance sheet perspective or from the large amount of costs that they have managed to save, are far superior to the position they were in during the crisis. All these companies are trading on high double digit free cash flow yields or owners earnings as Warren Buffet refers to it, based depressed earnings and are therefore likely to grow significantly the next few years with well capitalized balance sheets, Mr Market however is not paying any attention to fundamentals at the moment. Even if the global economy remains stagnant for the foreseeable future these stocks will still provide excellent returns, all that is required is patience. If the global economy surprises on the upside the returns will be even better

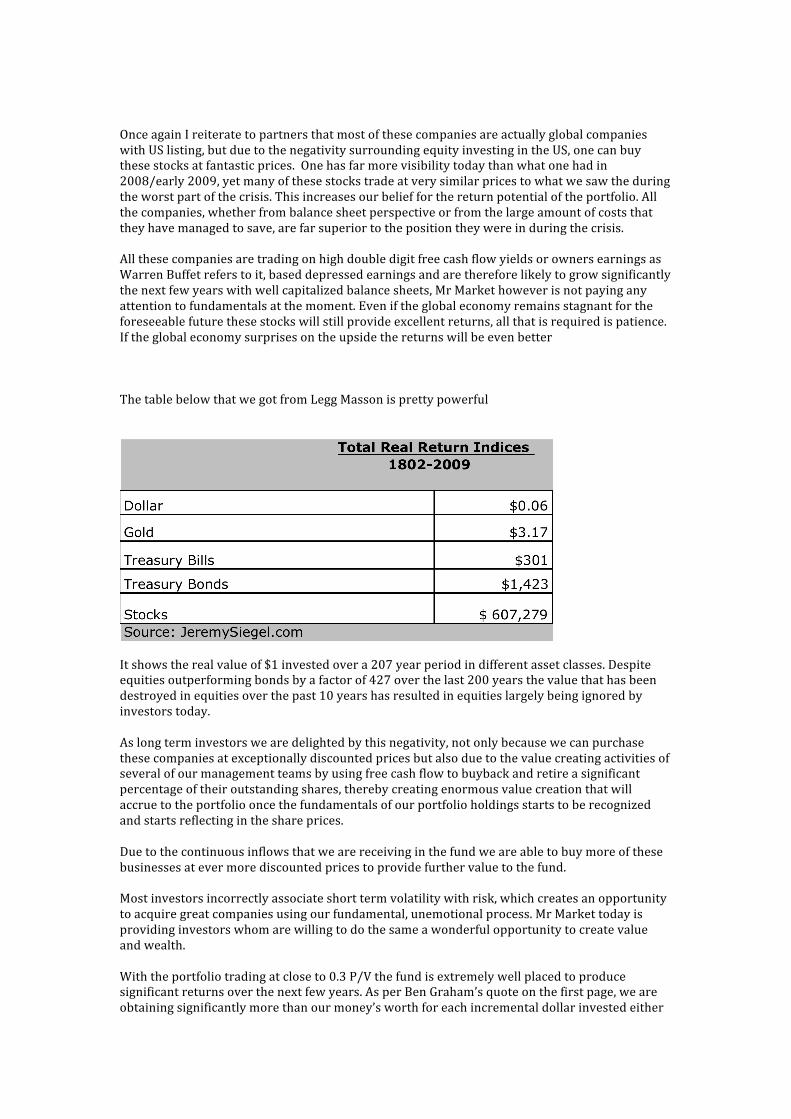

The table below that we got from Legg Masson is pretty powerful

It shows the real value of $1 invested over a 207 year period in different asset classes. Despite equities outperforming bonds by a factor of 427 over the last 200 years the value that has been destroyed in equities over the past 10 years has resulted in equities largely being ignored by investors today. As long term investors we are delighted by this negativity, not only because we can purchase these companies at exceptionally discounted prices but also due to the value creating activities of several of our management teams by using free cash flow to buyback and retire a significant percentage of their outstanding shares, thereby creating enormous value creation that will accrue to the portfolio once the fundamentals of our portfolio holdings starts to be recognized and starts reflecting in the share prices. Due to the continuous inflows that we are receiving in the fund we are able to buy more of these businesses at ever more discounted prices to provide further value to the fund. Most investors incorrectly associate short term volatility with risk, which creates an opportunity to acquire great companies using our fundamental, unemotional process. Mr Market today is providing investors whom are willing to do the same a wonderful opportunity to create value and wealth. With the portfolio trading at close to 0.3 P/V the fund is extremely well placed to produce significant returns over the next few years. As per Ben Graham’s quote on the first page, we are obtaining significantly more than our money’s worth for each incremental dollar invested either

via inflows invested by us or via the action of the management teams of our investee companies via buybacks. We have attached two reports for interested readers, the first by Legg Masson covering the topic of sideways markets that occur if macro data tends to be weak and non directional as we had in the mid 70’s till early eighties (SP500 was at the same level in 1982 as it was in 1975, a period when stock pickers such as Buffett and Ruane produced average annual returns of 31% and 28% respectively). You will find some of the material very interesting, especially in an environment where long term value investing is being ignored as an investment principle. Also included is Legg Masons Bill Miller, July 2010 comment I will end of with a excerpt from this report “It is almost tautology in capital markets that the best investments are those with the worst previous returns, where expectations are low, demand is down, and prospects appear at best highly uncertain. In 1980 bonds had been through a 30 year bear market relative to stocks, inflation was soaring, yields were at historic highs, yet expected to go higher, and a long bull market in bonds was at hand. The idea that US interest rates would be near all time lows 30 years later would have been dismissed as ludicrous. The situation is now reversed, with stocks having underperformed bonds for decades. The point here is simple: US large capitalization stocks present a once in a lifetime opportunity to buy the best quality companies in the world at bargain prices. The last time they were this cheap relative to bonds was 1951. I was 1 year old then, but did not have sufficient sentience or capital to invest”. BM I will conclude with a quote by Warren Buffet that sums up how we feel at present. He said this when he began actively buying stocks again in the mid 70’s. "Look At All Those Beautiful, Scantily Clad Girls Out There!" WB As always if you have any questions do not hesitate to contact me. Yours in Value Fountainhead Partners July 2010

![4.3 Oriya Code Chart - tdil.meity.gov.in file0b25 \ oriya letter tha 0b26] oriya letter da 0b27 ^ oriya letter dha 0b28 _ oriya letter na 0b29 0b2a ‘ oriya letter](https://static.fdocument.pub/doc/165x107/5cc209a788c993062d8d13a9/43-oriya-code-chart-tdilmeitygovin-oriya-letter-tha-0b26-oriya-letter-da.jpg)