Nigeria Pub

6

SOVEREIGN AND SUPRANATIONAL ISSUER COMMENT 3 February 2016 Contacts Aurelien Mali +971 4 237 9537 VP-Senior Analyst [email protected] Jeffrey Christiansen 971-4-237-9574 Associate Analyst [email protected] Matt Robinson 44-20-7772-5635 VP-Sr Credit Officer [email protected] Alastair Wilson 44-20-7772-1372 MD-Global Sovereign Risk [email protected] Government of Nigeria New Concessional Borrowing Will Provide Support Amid Intensifying Challenges On 31 January, the Government of Nigeria’s (Ba3 stable) finance minister, Mrs. Kemi Adeosun, issued a statement refuting press reports over the weekend indicating that the country has sought $3.5 billion in “emergency loans” from international institutions such as the World Bank and the African Development Bank (Aaa stable). The minister did confirm, however, that the government is discussing options for concessional financing, and reiterated the intention to borrow NGN1.8 trillion (around $9 billion) to fund the 2016 budget deficit and capital projects. Securing new concessional borrowing will help the country finance a third of its 2016 deficit (NGN2.2 trillion, or $11.2 billion at the official exchange rate of NGN197/USD, equivalent to 2.1% of GDP) and support foreign exchange reserves (which stood at $28.4 billion or roughly 5% of GDP at the end of 2015) in an environment where the country faces intensifying challenges as oil prices plumb to new lows in the mid-$20s/barrel, further pressuring Nigeria’s public finances and its slowing economy. Oil output accounts for only 10% of GDP but two-thirds of government revenues and 90% of export earnings. The sovereign already faces a widening general government deficit (forecasted by Moody’s at 3.05 trillion naira and 2.9% of GDP for 2016) and widening current account deficit. Meanwhile, an accumulation of arrears at the state and municipal level act as a drag on the economy, and a widening parallel market for US dollars illustrates naira’s vulnerability to adverse macroeconomic movements and investor sentiment. The decision to seek funding from International Financial Institutions does not signify a significant change in policy. According to previous government statements, Nigeria’s 2016 deficit funding need is likely to be met by a rough split borrowing between local and foreign currency. Raising about NGN1.2 trillion (roughly $6.1 billion) from the domestic capital market should not be too difficult. As shown in Exhibit 1, the domestic capital market (including pension funds, commercial banks, non-bank financial institutions, and other financial agents) has absorbed slightly more than NGN1 trillion of federal government debt on average each year since 2010. Having developed substantially over the past five years, Nigeria’s domestic capital market is increasingly able to absorb more government debt, especially as commercial banks are relatively liquid (with a loan to deposit ratio of around 55%) and a pension fund pool that is quickly growing (the largest fund in Nigeria reached its current size of $25 billion in only the last ten years).

-

Upload

jeff-christiansen -

Category

Documents

-

view

96 -

download

0

Transcript of Nigeria Pub

SOVEREIGN AND SUPRANATIONAL

ISSUER COMMENT3 February 2016

Contacts

Aurelien Mali +971 4 237 9537VP-Senior [email protected]

Jeffrey Christiansen 971-4-237-9574Associate [email protected]

Matt Robinson 44-20-7772-5635VP-Sr Credit [email protected]

Alastair Wilson 44-20-7772-1372MD-Global [email protected]

Government of NigeriaNew Concessional Borrowing Will Provide Support AmidIntensifying Challenges

On 31 January, the Government of Nigeria’s (Ba3 stable) finance minister, Mrs. KemiAdeosun, issued a statement refuting press reports over the weekend indicating that thecountry has sought $3.5 billion in “emergency loans” from international institutions such asthe World Bank and the African Development Bank (Aaa stable). The minister did confirm,however, that the government is discussing options for concessional financing, and reiteratedthe intention to borrow NGN1.8 trillion (around $9 billion) to fund the 2016 budget deficitand capital projects.

Securing new concessional borrowing will help the country finance a third of its 2016 deficit(NGN2.2 trillion, or $11.2 billion at the official exchange rate of NGN197/USD, equivalent to2.1% of GDP) and support foreign exchange reserves (which stood at $28.4 billion or roughly5% of GDP at the end of 2015) in an environment where the country faces intensifyingchallenges as oil prices plumb to new lows in the mid-$20s/barrel, further pressuringNigeria’s public finances and its slowing economy. Oil output accounts for only 10% of GDPbut two-thirds of government revenues and 90% of export earnings. The sovereign alreadyfaces a widening general government deficit (forecasted by Moody’s at 3.05 trillion naira and2.9% of GDP for 2016) and widening current account deficit. Meanwhile, an accumulation ofarrears at the state and municipal level act as a drag on the economy, and a widening parallelmarket for US dollars illustrates naira’s vulnerability to adverse macroeconomic movementsand investor sentiment.

The decision to seek funding from International Financial Institutions does not signify asignificant change in policy. According to previous government statements, Nigeria’s 2016deficit funding need is likely to be met by a rough split borrowing between local and foreigncurrency.

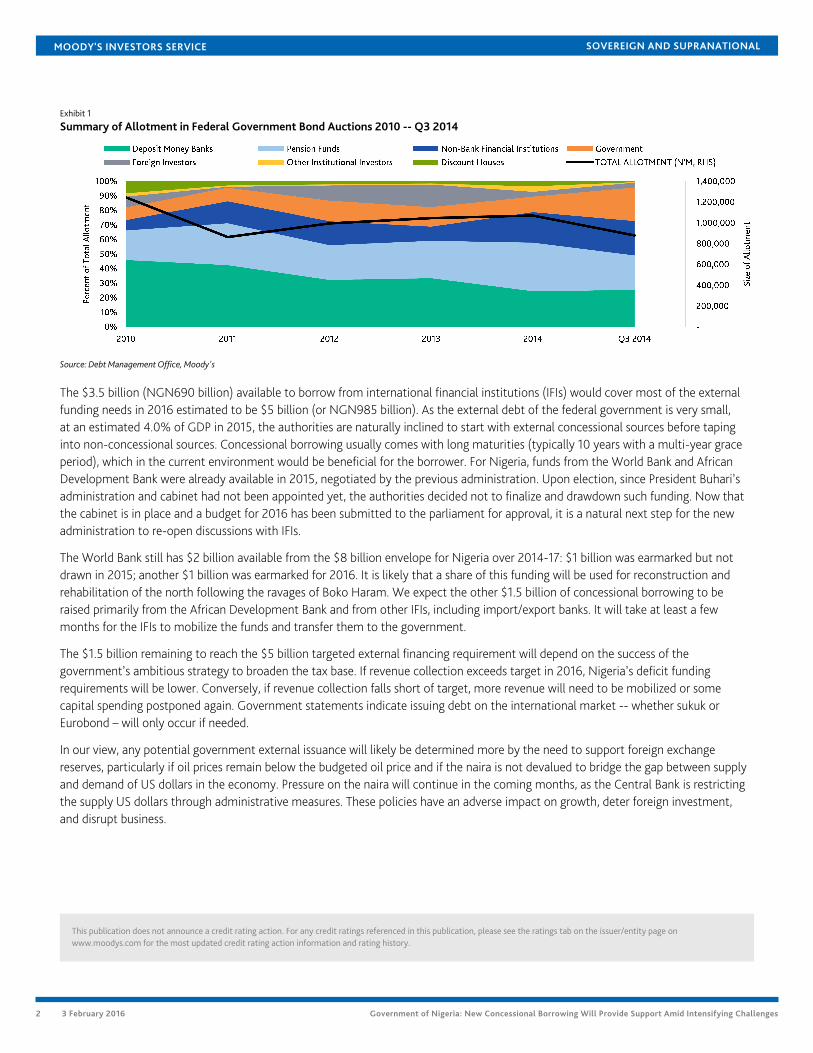

Raising about NGN1.2 trillion (roughly $6.1 billion) from the domestic capital market shouldnot be too difficult. As shown in Exhibit 1, the domestic capital market (including pensionfunds, commercial banks, non-bank financial institutions, and other financial agents) hasabsorbed slightly more than NGN1 trillion of federal government debt on average eachyear since 2010. Having developed substantially over the past five years, Nigeria’s domesticcapital market is increasingly able to absorb more government debt, especially as commercialbanks are relatively liquid (with a loan to deposit ratio of around 55%) and a pension fundpool that is quickly growing (the largest fund in Nigeria reached its current size of $25 billionin only the last ten years).

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 3 February 2016 Government of Nigeria: New Concessional Borrowing Will Provide Support Amid Intensifying Challenges

Exhibit 1

Summary of Allotment in Federal Government Bond Auctions 2010 -- Q3 2014

Source: Debt Management Office, Moody's

The $3.5 billion (NGN690 billion) available to borrow from international financial institutions (IFIs) would cover most of the externalfunding needs in 2016 estimated to be $5 billion (or NGN985 billion). As the external debt of the federal government is very small,at an estimated 4.0% of GDP in 2015, the authorities are naturally inclined to start with external concessional sources before tapinginto non-concessional sources. Concessional borrowing usually comes with long maturities (typically 10 years with a multi-year graceperiod), which in the current environment would be beneficial for the borrower. For Nigeria, funds from the World Bank and AfricanDevelopment Bank were already available in 2015, negotiated by the previous administration. Upon election, since President Buhari’sadministration and cabinet had not been appointed yet, the authorities decided not to finalize and drawdown such funding. Now thatthe cabinet is in place and a budget for 2016 has been submitted to the parliament for approval, it is a natural next step for the newadministration to re-open discussions with IFIs.

The World Bank still has $2 billion available from the $8 billion envelope for Nigeria over 2014-17: $1 billion was earmarked but notdrawn in 2015; another $1 billion was earmarked for 2016. It is likely that a share of this funding will be used for reconstruction andrehabilitation of the north following the ravages of Boko Haram. We expect the other $1.5 billion of concessional borrowing to beraised primarily from the African Development Bank and from other IFIs, including import/export banks. It will take at least a fewmonths for the IFIs to mobilize the funds and transfer them to the government.

The $1.5 billion remaining to reach the $5 billion targeted external financing requirement will depend on the success of thegovernment’s ambitious strategy to broaden the tax base. If revenue collection exceeds target in 2016, Nigeria’s deficit fundingrequirements will be lower. Conversely, if revenue collection falls short of target, more revenue will need to be mobilized or somecapital spending postponed again. Government statements indicate issuing debt on the international market -- whether sukuk orEurobond – will only occur if needed.

In our view, any potential government external issuance will likely be determined more by the need to support foreign exchangereserves, particularly if oil prices remain below the budgeted oil price and if the naira is not devalued to bridge the gap between supplyand demand of US dollars in the economy. Pressure on the naira will continue in the coming months, as the Central Bank is restrictingthe supply US dollars through administrative measures. These policies have an adverse impact on growth, deter foreign investment,and disrupt business.

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

3 3 February 2016 Government of Nigeria: New Concessional Borrowing Will Provide Support Amid Intensifying Challenges

We estimate the general government debt of Nigeria at approximately 15% of GDP, which compares favorably with Ba3 rated peers,whose average debt-to-GDP ratio is 44%. In case of a further shock to Nigeria’s public finances, we expect the federal government tomobilize more resources on its domestic capital markets and to resort to a mix of monetary and fiscal adjustment that would keep thedeficit below 3% of GDP for the federal government, consistent with the Fiscal Responsibility Act. For example, the government couldpass a supplementary budget to lower the budgeted oil price below its current $38/barrel, and/or a devaluation of the currency.

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

4 3 February 2016 Government of Nigeria: New Concessional Borrowing Will Provide Support Amid Intensifying Challenges

Moody's Related Research

Credit Analysis:

» Government of Nigeria, December 2015

Credit Opinion:

» Government of Nigeria, December 2015

Country Statistics:

» Government of Nigeria, November 2015

Sector In-Depth:

» Sovereigns - Sub-Saharan Africa: Most commodity exporters still vulnerable to price shock, scope for counter-cyclical policy islimited, December 2015

» Sovereigns - Sub-Saharan Africa: Twin Deficits, External Debt and Narrow Policy Space Increase Exposure to Fed Rate Hike,September 2015

Outlooks:

» Sovereign Outlook – Global: Stable Outlook Despite Low Growth, Jittery Markets and Uneven Reforms, November 2015

» Global Macro Outlook 2015-17: Lacklustre Global Economic Recovery Through 2017 Diminishes Resilience to Shocks, November2015

Methodology:

» Sovereign Bond Ratings, December 2015

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of thisreport and that more recent reports may be available. All research may not be available to all clients.

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

5 3 February 2016 Government of Nigeria: New Concessional Borrowing Will Provide Support Amid Intensifying Challenges

© 2016 Moody's Corporation, Moody's Investors Service, Inc., Moody's Analytics, Inc. and/or their licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES ("MIS") ARE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY'S ("MOODY'SPUBLICATIONS") MAY INCLUDE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKESECURITIES. MOODY'S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANYESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKETVALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY'S OPINIONS INCLUDED IN MOODY'S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICALFACT. MOODY'S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHEDBY MOODY'S ANALYTICS, INC. CREDIT RATINGS AND MOODY'S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDITRATINGS AND MOODY'S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDITRATINGS NOR MOODY'S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY'S ISSUES ITS CREDIT RATINGSAND PUBLISHES MOODY'S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY ANDEVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY'S CREDIT RATINGS AND MOODY'S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY'S CREDIT RATINGS OR MOODY'S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody's Publications.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY'S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY'S.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY'S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

Moody's Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody's Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody's Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading "Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY'S affiliate, Moody's InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody's Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001. MOODY'S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY'S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. ("MJKK") is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody'sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody's SF Japan K.K. ("MSFJ") is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization ("NRSRO"). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1015761

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

6 3 February 2016 Government of Nigeria: New Concessional Borrowing Will Provide Support Amid Intensifying Challenges

Contacts

Matt Robinson 44-20-7772-5635VP-Sr Credit [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454