Natural gas pricing in India - EY · PDF fileNatural gas pricing in India Current policy and...

12

Natural gas pricing in India Current policy and potential impact

-

Upload

hoangkhuong -

Category

Documents

-

view

226 -

download

3

Transcript of Natural gas pricing in India - EY · PDF fileNatural gas pricing in India Current policy and...

Natural gas pricing in IndiaCurrent policy and potential impact

2 Natural gas pricing in India Current policy and potential impact

Current scenario in India’s natural gas market

Intricacies of natural gas pricing in India

Potential impact of new pricing on energy industry Co

nten

ts

3Natural gas pricing in India Current policy and potential impact

Current scenario in India’s natural gas marketChapter 1

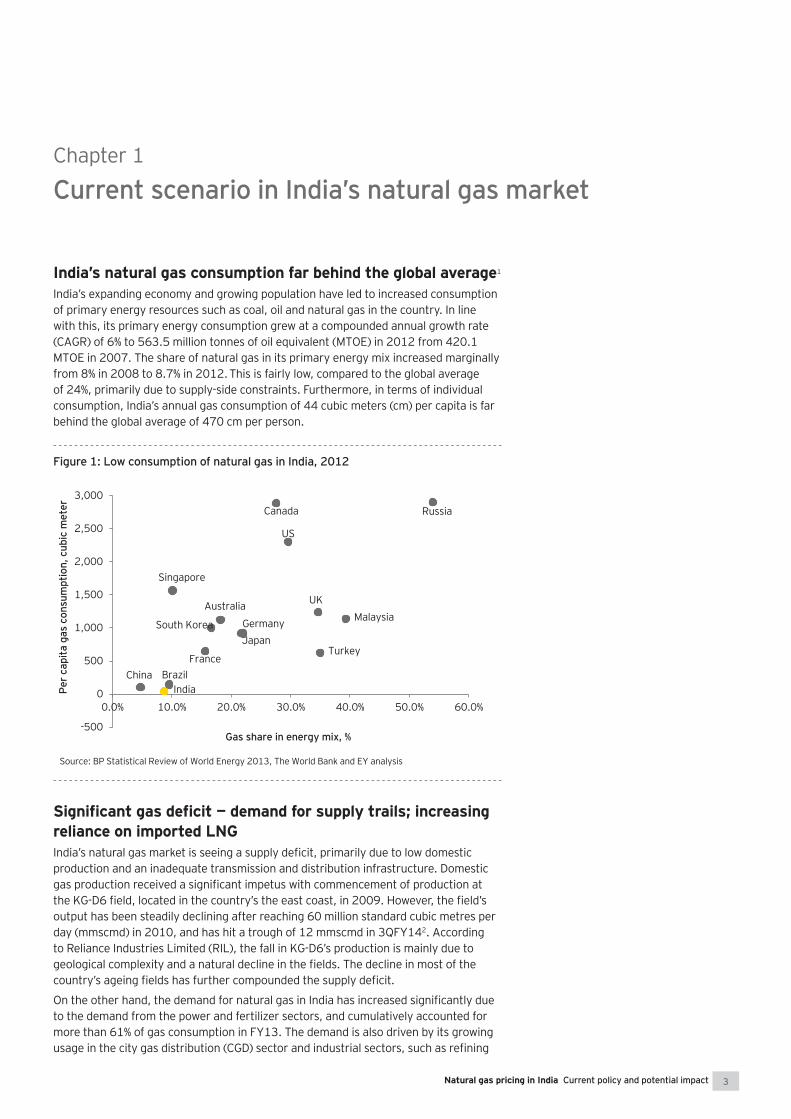

India’s natural gas consumption far behind the global average1

India’s expanding economy and growing population have led to increased consumption of primary energy resources such as coal, oil and natural gas in the country. In line with this, its primary energy consumption grew at a compounded annual growth rate (CAGR) of 6% to 563.5 million tonnes of oil equivalent (MTOE) in 2012 from 420.1 MTOE in 2007. The share of natural gas in its primary energy mix increased marginally from 8% in 2008 to 8.7% in 2012. This is fairly low, compared to the global average of 24%, primarily due to supply-side constraints. Furthermore, in terms of individual consumption, India’s annual gas consumption of 44 cubic meters (cm) per capita is far behind the global average of 470 cm per person.

Figure 1: Low consumption of natural gas in India, 2012

-500

0

500

1,000

1,500

2,000

2,500

3,000

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

Per c

apita

gas

con

sum

ptio

n, c

ubic

met

er

Gas share in energy mix, %

Source: BP Statistical Review of World Energy 2013, The World Bank and EY analysis

ChinaIndia

BrazilFrance

Singapore

South Korea

Australia

GermanyJapan

Canada

US

UK

Turkey

Malaysia

Russia

reliance on imported LNG

production and an inadequate transmission and distribution infrastructure. Domestic

output has been steadily declining after reaching 60 million standard cubic metres per day (mmscmd) in 2010, and has hit a trough of 12 mmscmd in 3QFY142. According to Reliance Industries Limited (RIL), the fall in KG-D6’s production is mainly due to

to the demand from the power and fertilizer sectors, and cumulatively accounted for more than 61% of gas consumption in FY13. The demand is also driven by its growing

4 Natural gas pricing in India Current policy and potential impact

and petrochemicals. Rising concerns on carbon emission have also contributed to the demand for natural gas in the country.3

4 According to the BP Statistical Review of World Energy 2013, India is the world’s fourth-largest

despite rising production and import of gasOver the next few years, the shortfall in natural gas production in the country is expected to continue with its supply trailing demand. Shortage of gas is likely to reach its peak in FY15, with around 37% of the demand being unmet.5

expected to remain the anchor segments that consume natural gas and are likely to account for around 68% of the total demand for it in FY17. Furthermore, deregulated pricing of petroleum products and an increasing focus on addressing environmental concerns are expected to drive the demand for natural gas from industrial users,

price-sensitive and will depend on the price affordability of end users, especially in the power and fertilizer sectors.6

Figure 2: Future natural gas demand-supply scenario (mmscmd)

Source: Ministry of Petroleum and Natural Gas

87 87 129 150149 170 177 209371 405 446 473

135148 140

114

FY14 FY15 FY16 FY17

LNG imports

Domestic production

Natural gas demandDe cit

of 15% from FY14 in India. Most of this incremental supply is expected to be met

increase to 150 mmscmd in FY17, contributing around 42% of the total supply.

Domestic production is expected to increase at a CAGR of around 12%.7 This is likely to come from new discoveries which are currently under development, expectation of partial recovery in the output from KG-D6 and increased production from unconventional sources, particularly coal bed methane.

5Natural gas pricing in India Current policy and potential impact

Intricacies of natural gas pricing in IndiaChapter 2

complex and heterogeneousThere are multiple natural gas pricing regimes in India. These can be divided into the following:

Administered Pricing Mechanism (APM)

APM gas pricing:

fertilizer and power plants, court-mandated customers and those requiring less than 50 thousand standard cubic metres per day (mscmpd) at APM rates. The price of APM gas has been set by the Government on a cost-plus basis and is US$4.2 per mmbtu in

APM price elsewhere in the country (the balance 40% is paid by the Government to 8

India’s move toward a market-based pricing regime: In June 2013, the Cabinet Committee on Economic Affairs (CCEA) approved a market-based pricing formula for produced natural gas produced in India. The revised prices are based on recommendations made by the Rangarajan Committee. The pricing formula, valid for

up from US$4.2 per mmbtu currently. The upward revision in prices is based on the

are calculated on a trailing 12-month basis. Prices will be revised every quarter.

Non-APM gas pricing: for which prices are determined by the market, and (ii) domestically produced gas from

Pre-NELP PSC pricing: This is applicable for gas produced from in Panna-Mukta,

NELP gas pricing:price of gas is determined on the basis of arm’s length prices (market prices), subject to the Government’s approval, and is controlled by PSC terms. This pricing regime was valid until March 2014. After this, a new pricing mechanism has come into force, based on the Ranagrajan Committee’s recommendations. Currently,

Price of imported gas (LNG): been linked to Japanese Custom Cleared (JCC) prices and varies on a monthly basis for

its demand sees limited growth from this source. According to industry estimates, the

spot price was at around US$18 per mmbtu in January 2014 .

6 Natural gas pricing in India Current policy and potential impact

Potential impact of new pricing on energy industry

Chapter 3

Overall, the new gas pricing policy augurs well for India’s natural gas market. It is expected to increase domestic production by encouraging upstream investment. This will improve India’s energy security and increase availability of gas for its key gas-consuming industries.

So far, the gas market has been adversely affected by the Government’s current gas-pricing policy and investment in the upstream sector declined to US$1.8 billion

to the on-going General Elections in the country, is expected to increase certainty and transparency in pricing of natural gas in India.

Upstream sector

The increase in natural gas prices is expected to encourage investment in the upstream segment and boost production. It will also improve the commercial viability of

US$12 per mmbtu due to the factors mentioned above.10

11 According to Morgan Stanley, gas prices of more than

12

The proposed hike in gas prices will help to boost the revenues of indigenous gas

domestic gas. According to Moody’s estimates, the proposed increase in gas prices

US$500 million in FY15.13 Furthermore, the rise in gas prices will augment the

Increased production of gas will help to alleviate the existing supply crunch, and reduce the country’s reliance on high-priced LNG. However, price-sensitive sectors

there is a need for the Government’s policy to effectively address the concerns of the consuming sector.

7Natural gas pricing in India Current policy and potential impact

Power sector

The power sector is the largest consumer of natural gas in India. Gas-powered power plants are plagued by high generation costs and a low average plant load factor (PLF).Currently, around 6,000 MW of commissioned and 1,000 MW of un-commissioned

non-functional due to unavailability of gas. While the new pricing regime is expected to increase domestic gas supply, which can be used to bring these power plants on stream, the demand for natural gas for gas-based power generation remains highly price-sensitive. Power plants are currently being supplied APM gas at US$4.2 per

players. The increase in gas prices to US$8.4 per mmbtu is expected to result in a rise

the companies to switch from natural gas to coal due to high conversion costs, a longer gestation period, their reliance on imported coal and environmental constraints14.

Fertilizer sectorIn the case of the fertilizer sector, another major consumer of gas, increased gas prices would result in a rise in feedstock costs and working capital requirements.

8 Natural gas pricing in India Current policy and potential impact

the fertilizer industry, since it enjoys a top priority position for allocation of gas.15 In .

According to a report submitted by the Government’s Parliamentary Standing

every rise of US$1 per mmbtu in gas prices. Consequently, this would lead to an increase in the Government’s subsidy burden. An increase in gas prices to around 8.4

billion). This subsidy burden can be offset by additional revenues received by the

operations expected in development of new gas resources.

The CGD sector is another key consumer and has witnessed rapid growth in recent years. The sector will continue to create a demand due to the addition of gas networks

will increase sourcing costs for CGD companies with a high APM gas allocation. CGD companies are expected to witness a decline in their earnings due to an increase in their input costs. These companies are unlikely to pass on the increase in gas prices to industrial and domestic consumers due to their limited headroom with alternative fuels

since the cost of sourcing is dollar-dominated16. Overall, increased availability of

Petrochemicals and other consuming sectorsThe petrochemicals sector uses natural gas to extract ethane and produce polyethylene, propane and butane for production of LPG. Input costs account for around 80% of manufacturing costs. Increased gas prices would mean reduced

such as ceramics and glass, since their input costs are also likely to go up with the price revision. On the other hand, companies that have replaced expensive fuels such as

gas prices, since the sector meets most of its demand from imported gas or naphtha.

9Natural gas pricing in India Current policy and potential impact

1.

2.

3.

4.

5.

6.

7.

8. 16 April 2014.

Moneywise Media Pvt. Ltd.

10.

11. 2013 Reuters Limited.

12. �Research.

13.

14. �

15.

16.

References

10 Natural gas pricing in India Current policy and potential impact

For more information, visit www.ey.com/in

Connect with us

Assurance, Tax, Transactions, Advisory A comprehensive range of high-quality services to help you navigate your next phase of growth

Read more on www.ey.com/India/Services

Our services

Centers of excellence for key sectors Our sector practices ensure our work with you is tuned in to the realities of your industry

Read about our sector knowledge at ey.com/India/industries

Sector focus

Easy access to our knowledge publications. Any time.

http://webcast.ey.com/thoughtcenter/

Webcasts and podcasts

www.ey.com/subscription-form

Follow us @EY_India Join the Business network from Ernst & Young

Stay connected

11Natural gas pricing in India Current policy and potential impact

Ahmedabad

Ambawadi, Ahmedabad-380015

Bengaluru

“U B City” Canberra Block

Bengaluru-560 001

1st Floor, Prestige Emerald

Lavelle Road JunctionBengaluru-560 001

Chandigarh1st Floor, SCO: 166-167

ChennaiTidel Park6th & 7th Floor

Taramani, Chennai-600113

Hyderabad

Kochi

Kochi - 682 304

Kolkata22, Camac Street3rd Floor, Block C”Kolkata-700 016

Mumbai14th Floor, The Ruby

Dadar (west)Mumbai-400 028, India

5th Floor Block B-2

Goregaon (E)Mumbai-400 063, India

NCRGolf View Corporate

Sector 42

18-20 Kasturba Gandhi Marg

Tower 2, Sector 126

Pune

Panchshil Tech Park

Pune-411 006

PHD Chamber contacts:

Hydrocarbon Committee, PHD Chamber of Commerce & Industry

Rajeev Mathur Chairman

Dilip Khanna & S. K. Jain Co-Chairman

Dr. Ranjeet Mehta

Gurpreet Kaur Joint Secretary [email protected]

Mahima Tyagi Assistant Secretary [email protected]

Khushboo Khanna

Web: www.phdcci.in

EY contacts:

Dilip Khanna Partner, Transaction Advisory Services [email protected]

Raju Lal Partner, Risk Advisory Services [email protected]

Devinder Chawla Partner, Business Advisory Services [email protected]

Sanjay Grover Partner, Tax & Regulatory Services [email protected]

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK companylimited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our

Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016

All Rights Reserved.

ED 0115

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the

LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

RS

one or more of the independent member firms of Ernst & Young Global Limited

Ernst & Young LLPEY | Assurance | Tax | Transactions | Advisory

old proactive and dynamic multi-State apex organization working at the grass-root level and with strong national

and Central Indian States along with Bihar, Jharkhand in the Eastern region and UT of Chandigarh. It has direct

acts as a catalyst in the promotion of industry, trade and

based policy advocacy role, positively impacts the economic growth and development of the nation.

We are globally connected through institutional linkages with over 60 important foreign Chambers of Commerce. Government of India has authorised us to issue certificate of origin (non-preferential) to Indian exporters. We also attest commercial documents of various types. Recommendation letters for visas for business promotion to foreign diplomatic missions in India are also issued for representatives of Indian companies.

In its endeavour towards capacity building in the country,

development training programmes in cooperation with the Konrad Adenauer Foundation of Germany. Through the support of its members, the Chamber has been regularly contributing in cash and kind towards relief and rehabilitation of the victims of natural calamities and disasters. In keeping with the motto adopted 'Ethics

Excellence annually.

Delhi and Chandigarh provide modern conferencing and catering facilities for corporate events, board meetings, training programmes, etc. With a modern auditorium, several conference and meeting rooms to suit different requirements and also a business centre, while the ambience is international, the cost is economical.