MINIT MESYUARAT WORKING GROUP LHDNM BERSAMA...

48

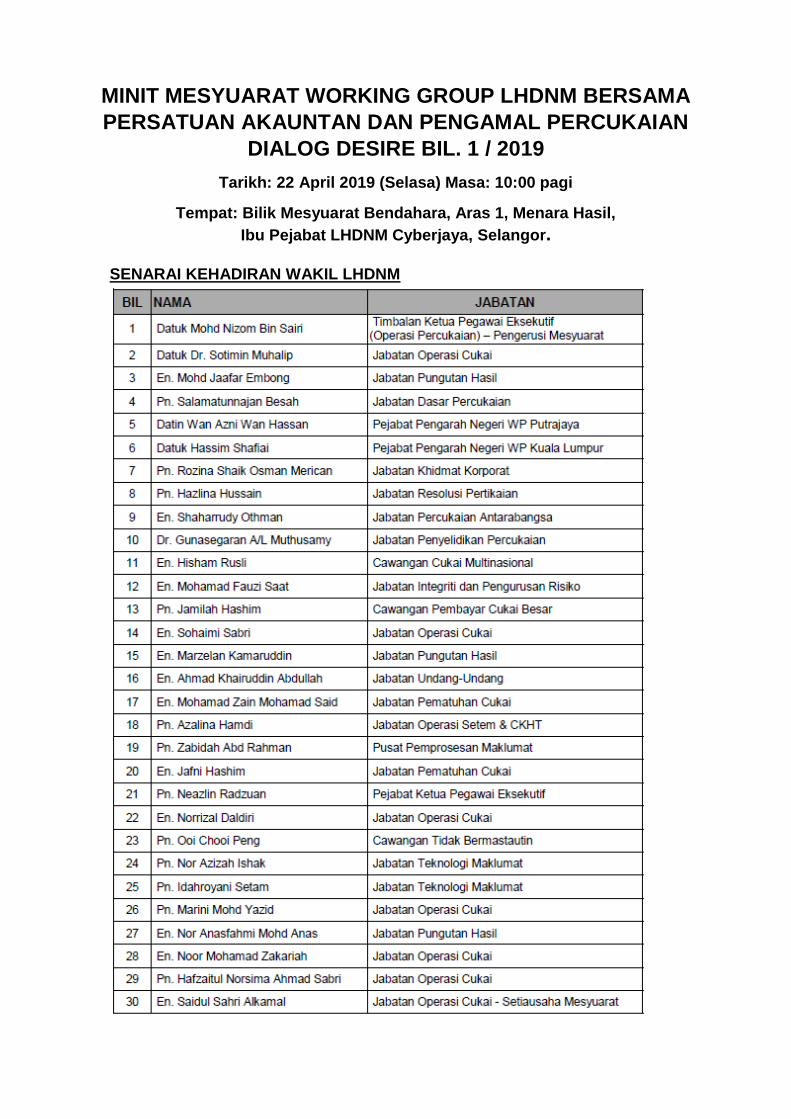

MINIT MESYUARAT WORKING GROUP LHDNM BERSAMA PERSATUAN AKAUNTAN DAN PENGAMAL PERCUKAIAN DIALOG DESIRE BIL. 1 / 2019 Tarikh: 22 April 2019 (Selasa) Masa: 10:00 pagi Tempat: Bilik Mesyuarat Bendahara, Aras 1, Menara Hasil, Ibu Pejabat LHDNM Cyberjaya, Selangor. SENARAI KEHADIRAN WAKIL LHDNM

Transcript of MINIT MESYUARAT WORKING GROUP LHDNM BERSAMA...

MINIT MESYUARAT WORKING GROUP LHDNM BERSAMA

PERSATUAN AKAUNTAN DAN PENGAMAL PERCUKAIAN

DIALOG DESIRE BIL. 1 / 2019

Tarikh: 22 April 2019 (Selasa) Masa: 10:00 pagi

Tempat: Bilik Mesyuarat Bendahara, Aras 1, Menara Hasil,

Ibu Pejabat LHDNM Cyberjaya, Selangor.

SENARAI KEHADIRAN WAKIL LHDNM

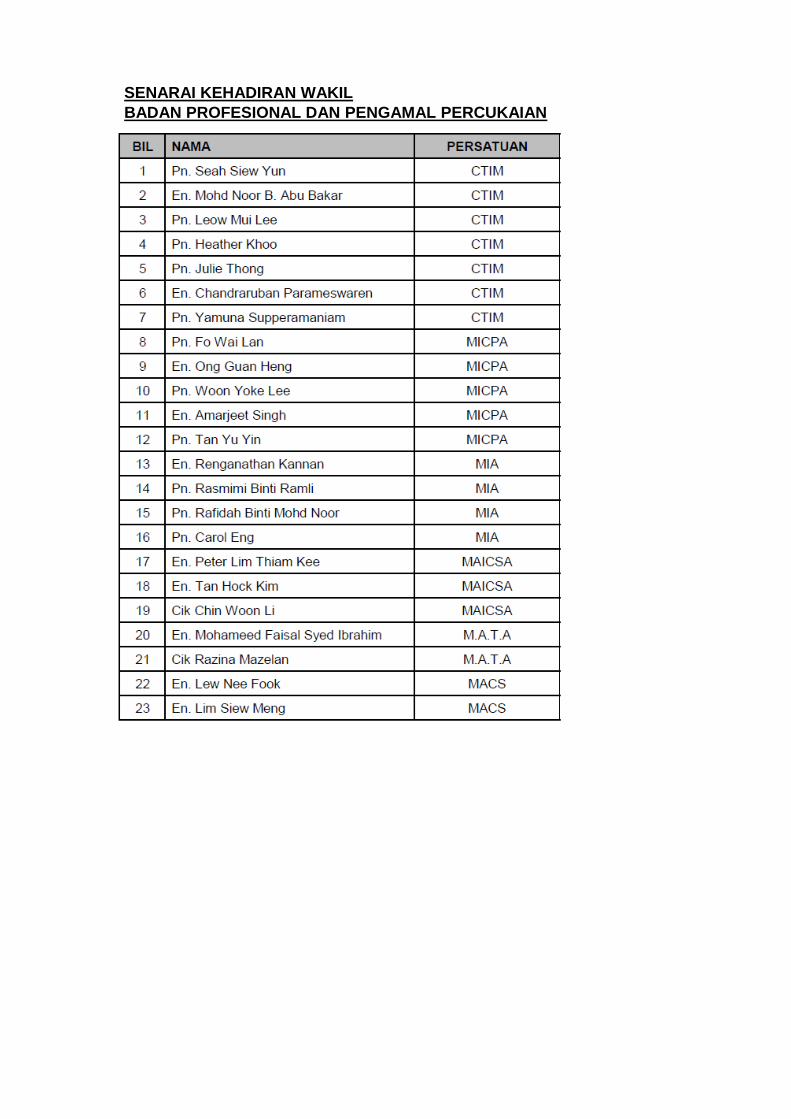

SENARAI KEHADIRAN WAKIL

BADAN PROFESIONAL DAN PENGAMAL PERCUKAIAN

1. UCAPAN PENDAHULUAN PENGERUSI

1.1 Pengerusi memulakan dengan ucapan salam, selamat pagi dan selamat

datang kepada ahli-ahli mesyuarat yang terdiri daripada wakil-wakil

badan profesional dan pengarah-pengarah Jabatan / Bahagian serta

wakil yang hadir ke mesyuarat DESIRE bagi tahun 2019.

1.2 Sesi dialog ini adalah bertujuan untuk menambahbaik sistem

penyampaian perkhidmatan LHDNM kepada pembayar cukai dan

mewujudkan tax eco-system yang sihat. Pengerusi mengalu-alukan

sebarang cadangan dan maklum balas dari badan-badan profesional

berkaitan penambahbaikan prosedur operasi untuk meningkatkan

perkhidmatan LHDNM termasuk e-Filing.

1.3 Badan profesional ini memainkan peranan yang penting kepada

kerajaan, khususnya LHDNM kerana sebagai pihak yang berhubung

rapat dengan pembayar cukai perlu bertanggungjawab membantu

kerajaan dan LHDNM dalam memberikan penerangan kepada

pembayar cukai berkaitan sistem percukaian dan perkhidmatan baharu

yang diperkenalkan sebagai kemudahan kepada pembayar cukai.

1.5 Dalam mesyuarat ini, isu-isu berkaitan operasi yang dikemukakan oleh

badan profesional dan badan pengamal percukaian ini telah di semak

dan di buat penambahbaikan bagi melancarkan lagi operasi percukaian

serta meningkatkan kecekapan sistem percukaian di samping

memudahkan urusan percukaian di pihak pembayar cukai dan ejen

cukai.

2. PERBINCANGAN ISU DAN MAKLUM BALAS LHDNM

2.1 Lampiran 1 – CTIM Memorandum On Compliance and Operational

2.2 Lampiran 2 – MICPA & CPA - Joint Operational Issues

2.3 Lampiran 3 – CTIM Memorandum On Compliance and Operational

(Additional Issues)

3. PERKARA BERBANGKIT

3.1 Lampiran 4 – Soalan dan Maklum balas Dibincangkan

4. PENUTUP

4.1 Pengerusi mengucapkan ribuan terima kasih kepada semua yang hadir

atas penglibatan dalam dialog ini yang memberikan manfaat kepada

kedua pihak iaitu LHDNM dan pengamal percukaian.

4.2 Pemakluman mengenai maklum balas Mesyuarat PEMUDAH – Doing

Business World Bank Ranking - Paying taxes

4.2.1 LHDNM akan mengeluarkan Garis Panduan Operasi Bil. 3 tahun

2019 untuk makluman dan rujukan pembayar cukai. Ianya

menjelaskan bahawa BNT yang diterima tidak akan di audit

kecuali memiliki kriteria berikut:

i. BNCP asal dikemukakan dalam tempoh yang ditetapkan

tetapi terdapat kesilapan pengiraan;

ii. BNCP diterima selepas tempoh yang ditetapkan;

iii. Terdapat kesilapan pengiraan cukai pada BNT; atau

iv. BNT diterima selepas tempoh 6 bulan yang dibenarkan

4.2.2 Secara dasarnya penjelasan dalam Garis Panduan Operasi

berkenaan akan membuat ranking LHDNM menjadi lebih baik

kerana salah faham di kalangan pembayar cukai bahawa

pengemukaan BNT akan menyebabkan mereka di audit.

4.2.3 Oleh kerana pengemukaan BNT adalah secara e-filing,

kesalahan pengiraan tidak akan berlaku dan LHDNM hanya

menyemak maklumat dan bukan mengaudit kes tersebut.

4.2.4 Diharap maklum balas kepada soal selidik boleh dibuat dengan

lebih telus dan adil serta ranking Malaysia akan menjadi lebih

baik.

4.2 Pengerusi menekankan supaya badan profesional mengemukakan isu

yang melibatkan prosedur operasi dan kelemahan sistem percukaian.

Manakala isu-isu kecil perlu diselesaikan di peringkat jabatan /

cawangan berkaitan. Langkah ini juga penting supaya permasalahan

yang berlaku boleh diselesaikan dengan kadar segera dan tidak perlu

menunggu mesyuarat ini yang hanya bersidang setahun sekali.

4.3 Beliau juga turut merakamkan penghargaan kepada pihak persatuan

yang telah memberikan input, cadangan dan maklum balas kepada

LHDNM melalui sesi ini. Mesyuarat ditamatkan pada jam 12.15 tengah

hari.

Disediakan oleh;

Sekretariat DESIRE, LHDNM

22 April 2019

+

MEMORANDUM ON COMPLIANCE AND OPERATIONAL ISSUES

15 February 2019

Prepared by: Compliance & Operations Working Group (COWG) Chartered Tax Institute of Malaysia

Memorandum on Compliance and Operational Issues

Page 2 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

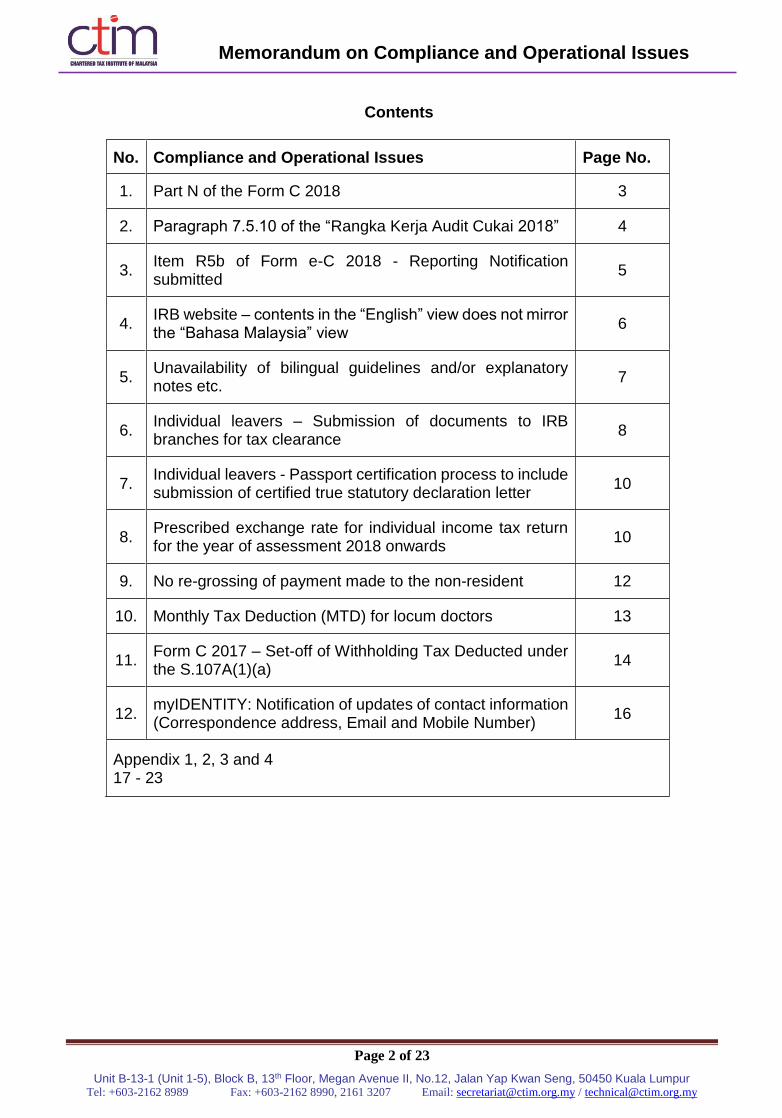

Contents

No. Compliance and Operational Issues Page No.

1. Part N of the Form C 2018 3

2. Paragraph 7.5.10 of the “Rangka Kerja Audit Cukai 2018” 4

3. Item R5b of Form e-C 2018 - Reporting Notification submitted

5

4. IRB website – contents in the “English” view does not mirror the “Bahasa Malaysia” view

6

5. Unavailability of bilingual guidelines and/or explanatory notes etc.

7

6. Individual leavers – Submission of documents to IRB branches for tax clearance

8

7. Individual leavers - Passport certification process to include submission of certified true statutory declaration letter

10

8. Prescribed exchange rate for individual income tax return for the year of assessment 2018 onwards

10

9. No re-grossing of payment made to the non-resident 12

10. Monthly Tax Deduction (MTD) for locum doctors 13

11. Form C 2017 – Set-off of Withholding Tax Deducted under the S.107A(1)(a)

14

12. myIDENTITY: Notification of updates of contact information (Correspondence address, Email and Mobile Number)

16

Appendix 1, 2, 3 and 4 17 - 23

Memorandum on Compliance and Operational Issues

Page 3 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

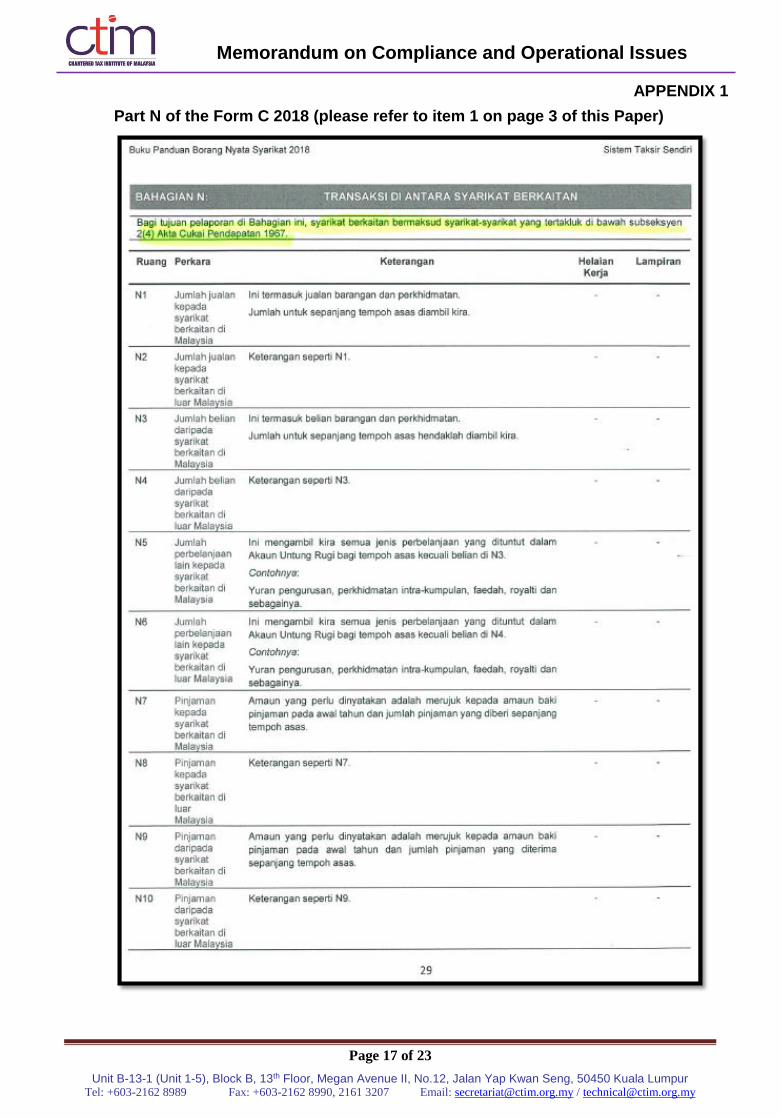

1. Part N of the Form C 2018

With reference to the attached IRB’s guidebook on Form C 2018, we noted that the

meaning of “related company for the purpose of reporting” (Part N of the Form C 2018)

is pursuant to Section 2(4) of the Income Tax Act 1967. [Please refer to Appendix 1]

S. 2(4) [Where companies in the same group]

Where—

(a) two or more companies are related within the meaning of section 6 of the

Companies Act, 1965;

(b) a company is so related to another company which is itself so related to a

third company;

(c) the same persons hold more than fifty per cent of the shares in each of two or

more companies; or

(d) each of two or more companies is so related to at least one of two or more

companies to which paragraph (c) applies,

all the companies in question are in the same group for the purposes of this Act.

S. 6 of the Company Act 1965 or S. 7 of the Company Act 2016

CTIM comments: We wish to get clarification on the meaning of “a company is so related to another

company which is itself so related to a third company” as per subparagraph (b) of Section

2(4). Please see the extract above.

Memorandum on Compliance and Operational Issues

Page 4 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

Maklumbalas LHDNM For clarification of “a company is so related to another company which is itself so related to a third company” is as per subparagraph (b) of Section 2(4). Please refer to Examples 1 and 2 of paragraph 1.5 of Chapter 1, Malaysian Transfer Pricing Guidelines. Thus, all these companies in the examples will be considered to be in the same group in accordance with subsection 2(4) of the ITA. Further examples and explanation on this matter and other issues pertaining to the controls will be provided on the IRB website.

2. Paragraph 7.5.10 of the “Rangka Kerja Audit Cukai 2018”

With reference to the attached IRB’s “Rangka Kerja Audit Cukai 2018”, we noted that

paragraph 7.5.10 has stated as follows: [Please refer to Appendix 2]

Kes audit perlu diselesaikan dalam tempoh tiga (3) bulan (90 hari kalendar) dari

permulaan tarikh lawatan audit. Sekiranya kes tidak dapat diselesaikan dalam tempoh

tiga (3) bulan, pembayar cukai akan dimaklumkan oleh LHDNM.

CTIM comments:

We would like to seek clarification on whether to apply the three (3) months or 90 days

for audit case completion.

Maklumbalas LHDNM

Kes perlu diselesaikan dalam tempoh 3 bulan terhad kepada 90 hari kalendar. Pindaan

dalam Rangka Kerja Audit akan dibuat.

Memorandum on Compliance and Operational Issues

Page 5 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

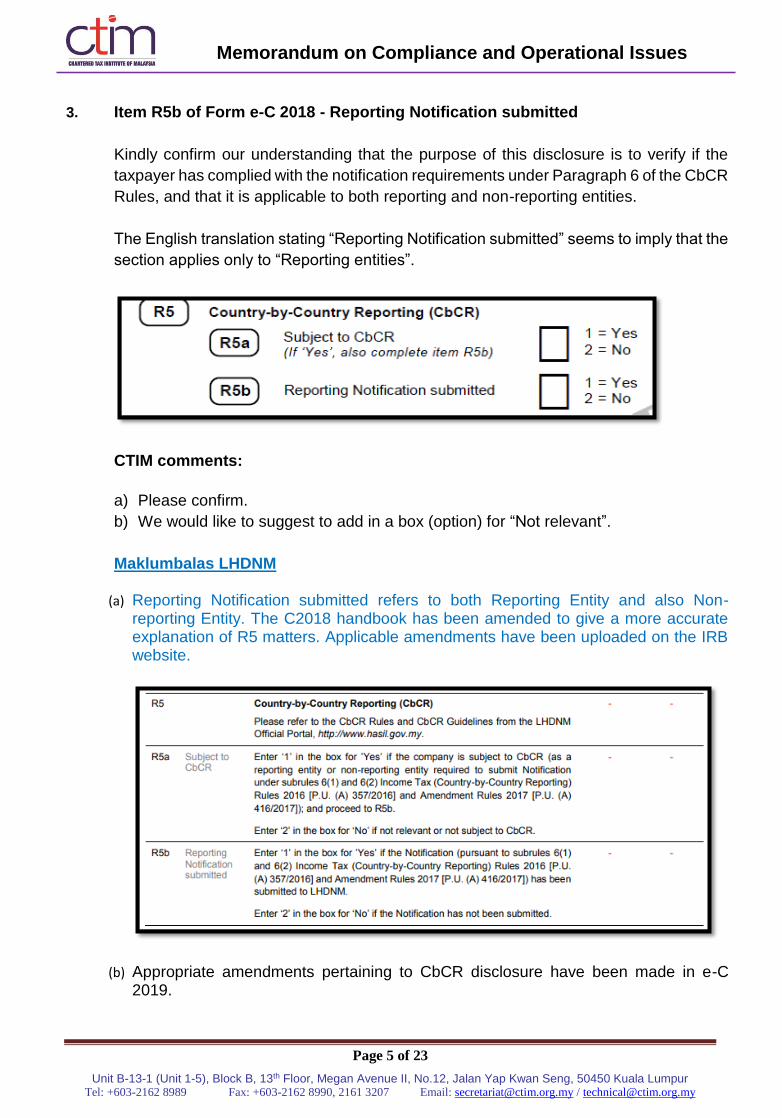

3. Item R5b of Form e-C 2018 - Reporting Notification submitted

Kindly confirm our understanding that the purpose of this disclosure is to verify if the

taxpayer has complied with the notification requirements under Paragraph 6 of the CbCR

Rules, and that it is applicable to both reporting and non-reporting entities.

The English translation stating “Reporting Notification submitted” seems to imply that the

section applies only to “Reporting entities”.

CTIM comments:

a) Please confirm.

b) We would like to suggest to add in a box (option) for “Not relevant”.

Maklumbalas LHDNM (a) Reporting Notification submitted refers to both Reporting Entity and also Non-

reporting Entity. The C2018 handbook has been amended to give a more accurate explanation of R5 matters. Applicable amendments have been uploaded on the IRB website.

(b) Appropriate amendments pertaining to CbCR disclosure have been made in e-C 2019.

Memorandum on Compliance and Operational Issues

Page 6 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

4. IRB website – contents in the “English” view does not mirror the “Bahasa

Malaysia” view.

Certain updates (for example, Nota Amalan 4/2018) appear only if viewed via the

Bahasa Malaysia language view as follows:

English version

Bahasa Malaysia version

CTIM comments:

a) With reference to the above, we would propose for the IRB to include a link in the

“English” view so that taxpayers are aware of the update.

b) We also noted that some of the updates were not flagged on the IRB’s homepage

but instead hidden in the pull-down tab menus or in the web page document itself.

We would like to suggest to the IRB to display the updates on the homepage itself

so that taxpayers can be made aware of new information or updates.

Memorandum on Compliance and Operational Issues

Page 7 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

Maklumbalas LHDNM

(a) Tindakan kemaskini halaman nota amalan telah dilaksanakan dan ambil maklum

akan perubahan-perubahan akan datang. LHDNM akan pastikan ianya selari

dengan perubahan bagi makluman Bahasa Malaysia dan Bahasa Inggeris.

LHDNM akan mengkaji sama ada cadangan CTIM boleh dilaksanakan sebagai

kaedah yang lebih mesra pengguna apabila mereka memilih untuk merujuk

dokumen dalam versi English yang dimuatnaik ke portal Hasil.

(b) Perkara baru akan dimasukkan dalam tab ‘Pengumuman’ / ‘Announcement’.

5. Unavailability of bilingual guidelines and/or explanatory notes etc. (Tindakan JOC)

The Form e-C explanatory notes (YA 2018) and many Guidelines issued are available

in Bahasa Malaysia only.

Given the number of multinational companies (MNC) operating in Malaysia, there are

many companies’ officers and/or directors required to sign off on documents, who are

foreigners and do not understand Bahasa Malaysia. Without the bilingual forms and/or

guidelines, the respective signatories would find it challenging as they would then be

required to sign off on documents which they do not comprehend.

CTIM comments:

We would like to request to provide the English translation for all Forms and Guidelines.

Maklumbalas LHDNM

Buku Panduan Borang C versi Bahasa Inggeris Tahun Taksiran 2018 telah dimuatnaik

ke Portal rasmi LHDNM untuk rujukan.

Memorandum on Compliance and Operational Issues

Page 8 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

6. Individual leavers – Submission of documents to IRB branches for tax clearance

There is no standard procedure across all IRB branches for submission of tax clearance

documents by either the tax agents or taxpayers.

Several IRB branches require taxpayers/tax agents to submit documents for tax

clearance at the general counter, whereas some require us to take queue numbers and

meet the assessment officer to submit the documents where the officer would review the

completeness of submission documents.

Additionally, we understand as part of the tax clearance process, the IRB officer may

require the taxpayer to furnish past year(s) records/documents for verification/audit.

Taxpayers and tax agents would be happy to cooperate to expedite the tax clearance

process. In relation to this, based on an encounter at the IRB Bangi branch recently, a

leaver taxpayer’s submission was rejected at the submission counter itself as all his prior

years’ Forms EA were not enclosed. Since the Garis Panduan Operasi Bil. 2 Tahun 2016

(GPHDN 2/2016) did not indicate that the individuals must furnish ALL prior years’ Forms

EA for tax clearance purposes, we would have expected the IRB officer to at least not

reject the submission and allow the taxpayer to separately submit the additional Forms

EA required.

CTIM comments:

We would like to request the IRB to clarify the standard procedure for submission of

documents for tax clearance by either the tax agents or taxpayers to minimise confusion

and allow tax agents to manage the resources required for submission of documents for

tax clearance.

Additionally, if the individual’s documents are complete per the SPC Guidelines No.

GPHDN2/2016 issued by the IRB, we would suggest the submission counter to accept

the submission document. Should the officer-in-charge require prior year documents,

they can contact the taxpayer/ tax agent representative for the documents.

Maklumbalas LHDNM

Mengikut subseksyen 83(3), ACP 1967 tanggungjawab majikan untuk memaklumkan

sekiranya pekerja berhenti kerja/bersara. Manakala subseksyen 83(4), ACP 1967

majikan hendaklah memaklumkan kepada KPHDN tidak kurang dari satu bulan sebelum

tarikh pekerja dijangka meninggalkan Malaysia.

Memorandum on Compliance and Operational Issues

Page 9 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

Kaedah permohonan hendaklah dibuat oleh majikan kepada KPHDN mengikut tempoh

yang ditetapkan bersama-sama dengan dokumen lengkap yang dikemukakan ke

cawangan LHDNM yang mengendalikan fail cukai pendapatan pekerja atau ke

cawangan LHDNM yang berhampiran.

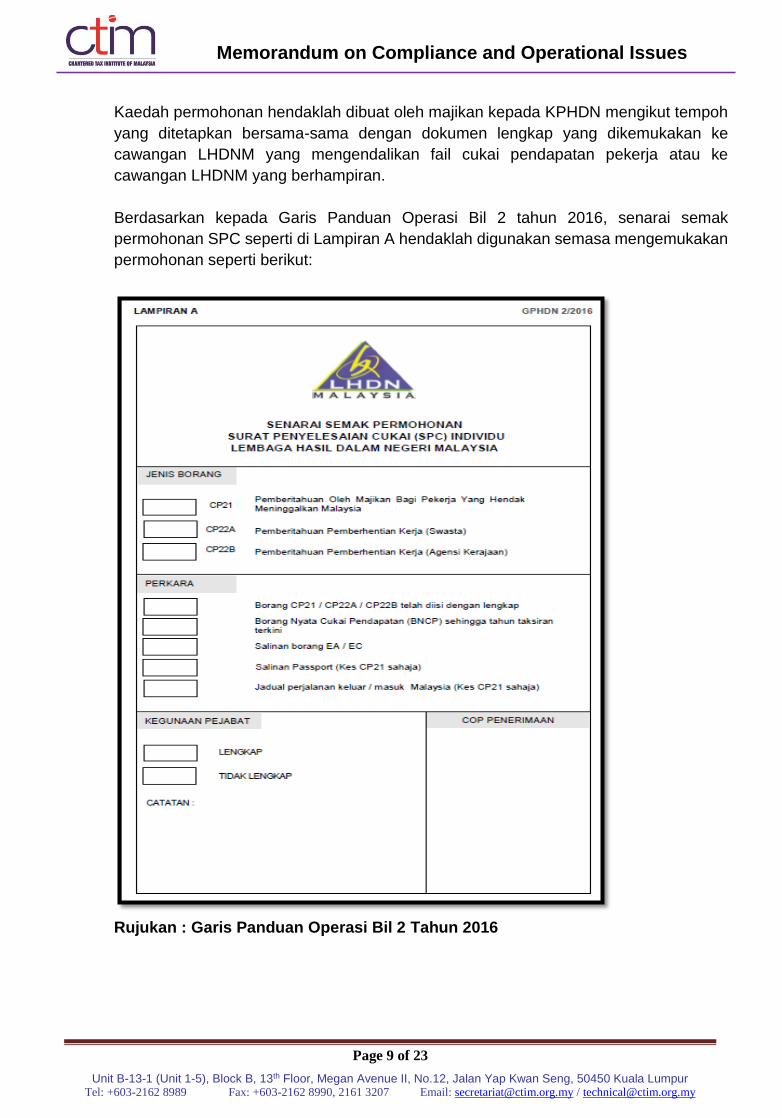

Berdasarkan kepada Garis Panduan Operasi Bil 2 tahun 2016, senarai semak

permohonan SPC seperti di Lampiran A hendaklah digunakan semasa mengemukakan

permohonan seperti berikut:

Rujukan : Garis Panduan Operasi Bil 2 Tahun 2016

Memorandum on Compliance and Operational Issues

Page 10 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

7. Individual leavers - Passport certification process to include submission of

certified true statutory declaration letter

Based on our previous liaison with the Jalan Tuanku Abdul Halim Branch (formerly Jalan

Duta branch), we understand that there is an internal circulation issued within the IRB

whereby with effect from 31 May 2018, it is mandatory for leavers whose passports are

certified by the Notary Public/ Commissioner of Oath to be enclosed with a copy of the

Statutory declaration letter duly signed by the individual and stamped by the respective

legal agency, failing which, the individual’s departure tax return will be assessed as a

non-resident although he is able to qualify as a resident. This practice is to be applied

across all IRB branches.

We have liaised with a few other IRB branches including Kuala Lumpur Bandar and

Petaling Jaya branches over the past 6 months and noted that each branch adopts a

different practice and some branches do not require the Statutory declaration letter.

CTIM comments:

We would suggest the standard process to be communicated to all taxpayers and

adopted across all branches to avoid confusion.

Maklumbalas LHDNM

Pengesahan yang dibuat ke atas dokumen perjalanan merupakan suatu medium untuk

membantu pembayar cukai yang tiada dokumen untuk pembuktian. Pengesahan

salinan pasport pembayar cukai oleh Notari Awam atau Pesuruhjaya Sumpah akan

dimasukkan ke dalam Garis Panduan Operasi yang baru dan boleh di dapati di Portal

Hasil untuk rujukan.

LHDNM akan mengeluarkan memo edaran ke semua cawangan untuk memaklumkan

kepada semua pegawai prosedur ini. Pegawai juga telah diingatkan semasa

Konvensyen Operasi Cukai baru-baru ini.

8. Prescribed exchange rate for individual income tax return for the year of

assessment 2018 onwards

We note from the IRB’s website that the IRB’s prescribed exchange rate for the year is

no longer available from 2018 <IRB Official Website> Home Page > Internal Link >

Foreign Exchange Rate>. Instead, only the monthly prescribed rates are available via a

link at the IRB’s website to the Jabatan Akauntan Negara Malaysia (JANM) website.

We had sought clarification from IRB Cyberjaya Unit Dasar Percukaian, who suggested

us to request for the average annual rates for 2018 from Bank Negara Malaysia (BNM)

or Ministry of Finance (MOF) if the average exchange rates for year 2018 are readily

available at their end.

Memorandum on Compliance and Operational Issues

Page 11 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

Meanwhile, the abovementioned IRB officer has indicated that we should make do with

the exchange rates at the JANM’s website and suggested the following options when

preparing individuals’ annual income tax returns:

1. Use the monthly prescribed exchange rate for the month we prepare the tax return;

or

2. Use the monthly prescribed exchange rate for the month we submit the tax return;

or

3. Self-compute the average exchange rate for the year using the monthly rates

available; or

4. Convert the monthly foreign remuneration and each foreign expenses for tax relief

claims using the respective months’ prescribed exchange rates based on the month

payment received or made. [Note: Although this option is relatively most accurate,

this would be cumbersome for expatriates who receive monthly remuneration from

various countries and incur multiple expenses overseas over the year for tax relief

claims.]

As it turns out, we have faced pushbacks from IRB officers for tax returns prepared using

Option 1 and 2 above, while several other IRB officers have accepted it.

CTIM comments:

We would like to request the IRB to issue a guideline on the exchange rate to be used

by individual taxpayers to ensure consistency of the reporting from the taxpayer’s end

and the audit/verification at the IRB’s end.

Maklumbalas LHDNM

Kadar pertukaran matawang asing yang perlu digunakan pembayar cukai individu bagi

tujuan pelaporan borang nyata cukai pendapatan adalah kadar pertukaran matawang

asing monthly average basis bagi bulan Disember bagi tahun taksiran tersebut.

Kadar pertukaran matawang asing monthly average basis yang digunakan adalah

merujuk kepada Jadual Kadar Pertukaran Wang Asing yang dikeluarkan oleh Jabatan

Akauntan Negara Malaysia yang disediakan berasaskan kadar tukaran matawang oleh

Bank Negara Malaysia dan telah dimuatnaik ke Portal Rasmi LHDNM.

Memorandum on Compliance and Operational Issues

Page 12 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

9. No re-grossing of payment made to the non-resident

We refer to the Note to Example 15 under paragraph 12.1(b) of the Public Ruling (“PR”)

11/2018 on Withholding Tax on Special Classes of Income as follows: –

Note

Effective from the date of publication of this PR, where withholding tax under section

109B of the ITA is borne by a payer, the withholding tax is to be computed on the

gross amount paid to a non-resident. This means that the payment made to the non-

resident need not be re-grossed to determine the amount of withholding tax

CTIM Comments:

a) We would like to get the IRB’s written confirmation that the above Note also

applies to other WHT provisions in the ITA 1967.

b) Form e-C 2018 – Part M: Particulars of Withholding Taxes:

Where a payer is contracted to pay the full amount of the technical service fees

of RM150,000 to a non-resident in the 2018 basis period, and the payer also

undertakes to bear and pay the withholding tax to the DGIR within the stipulated

period, the amount to be disclosed in Part M of the Form e-C for the year of

assessment 2018 should be as follows:

Gross Fee = RM150,000

WHT remitted to the IRB = RM15,000

Net amount = RM150,000

However, when completing the above in Part M of the Form e-C 2018, the net

amount is automatically calculated as RM135,000.00 instead of RM150,000.00.

We would suggest to the IRB to remove the auto-formula in the system, so that

the taxpayer may key in the amount manually.

Maklumbalas LHDNM

(a) Ya, layanan ini terpakai kepada mana-mana bayaran yang tertakluk kepada cukai

pegangan di bawah peruntukan seksyen 109, 109A dan 109F.

(b) Cawangan Tidak Bermastautin bersetuju dengan cadangan CTIM.

Pindaan sistem e-Filing e-C 2018 telah dilakukan pada 15 April 2019. Pengguna

perlu input manual amaun Jumlah Bersih Dibayar.

Memorandum on Compliance and Operational Issues

Page 13 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

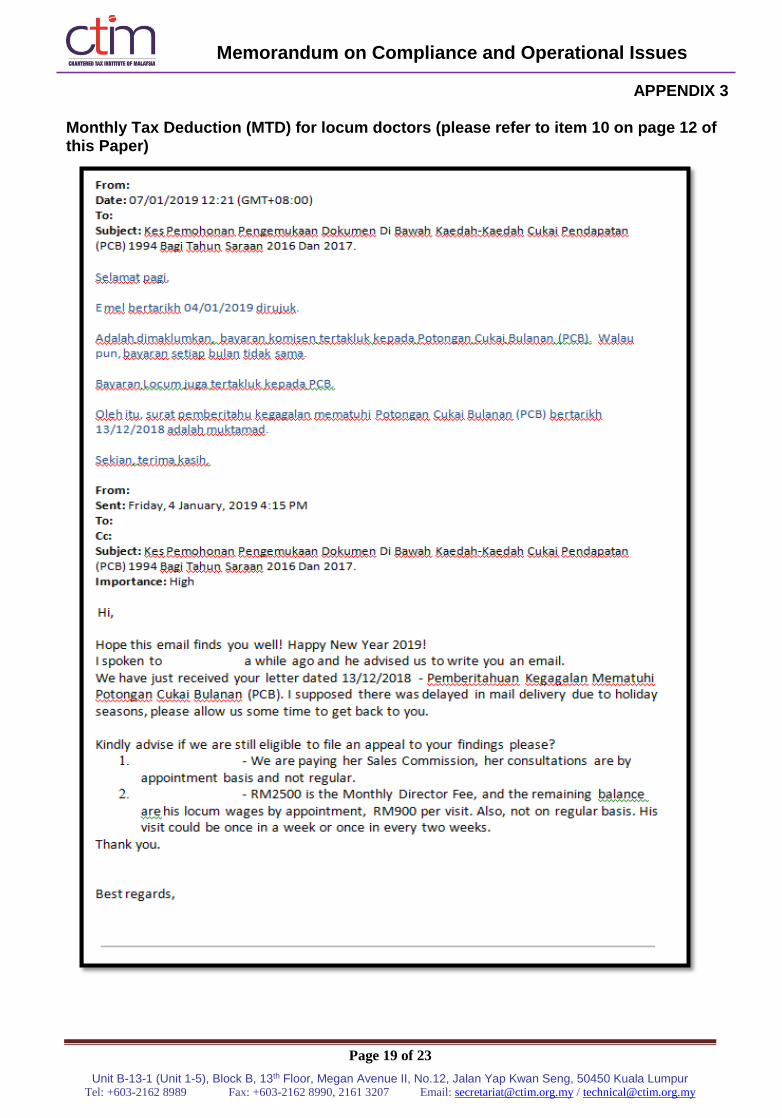

10. Monthly Tax Deduction (MTD) for locum doctors

During MTD audit, some IRB officers instructed employers to pay MTD for locum doctors

whom are not employees, even though these locum doctors have fixed working hours.

[Please refer to Appendix 3]

CTIM Comments:

In our view, locum fee paid to the doctors should not be subject to MTD as these doctors

are self-employed (contract for service) and not an employee (contract of service).

Please confirm.

Maklumbalas LHDNM

Persoalan sama ada bayaran kepada ‘locum doctors’ tertakluk kepada Potongan Cukai Berjadual (PCB) adalah bergantung kepada ‘nature of relationship’ antara ‘locum doctors’ dengan klinik/hospital. ‘Nature of relationship’ ini bermaksud sama ada khidmat ‘locum doctor’ ini berdasarkan kepada ‘contract of service’ atau ‘contract for service’. Sekiranya wujud ‘contract of service’ antara ‘locum doctor’ dengan klinik/hospital, maka bayaran kepada ‘locum doctors’ adalah tertakluk kepada PCB.

Kajian dijalankan ke atas praktis di Malaysia apabila sesebuah klinik / hospital

memerlukan khidmat locum doctor. LHDNM akan memberikan maklum balas kepada

kajian dan amalan praktikal oleh klinik dan hospital dan memastikan layanan cukai

sewajarnya di ambil kira dalam pengiraan PCB.

Mesyuarat bersetuju dengan cadangan CTIM dan proses kerja dalaman perlu

dikemaskini serta perlu dimaklumkan kepada semua pegawai audit PCB. Secara

umumnya, layanan cukai adalah bergantung kepada nature of relationship sama ada

berdasarkan lantikan atau kontrak perkhidmatan.

Memorandum on Compliance and Operational Issues

Page 14 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

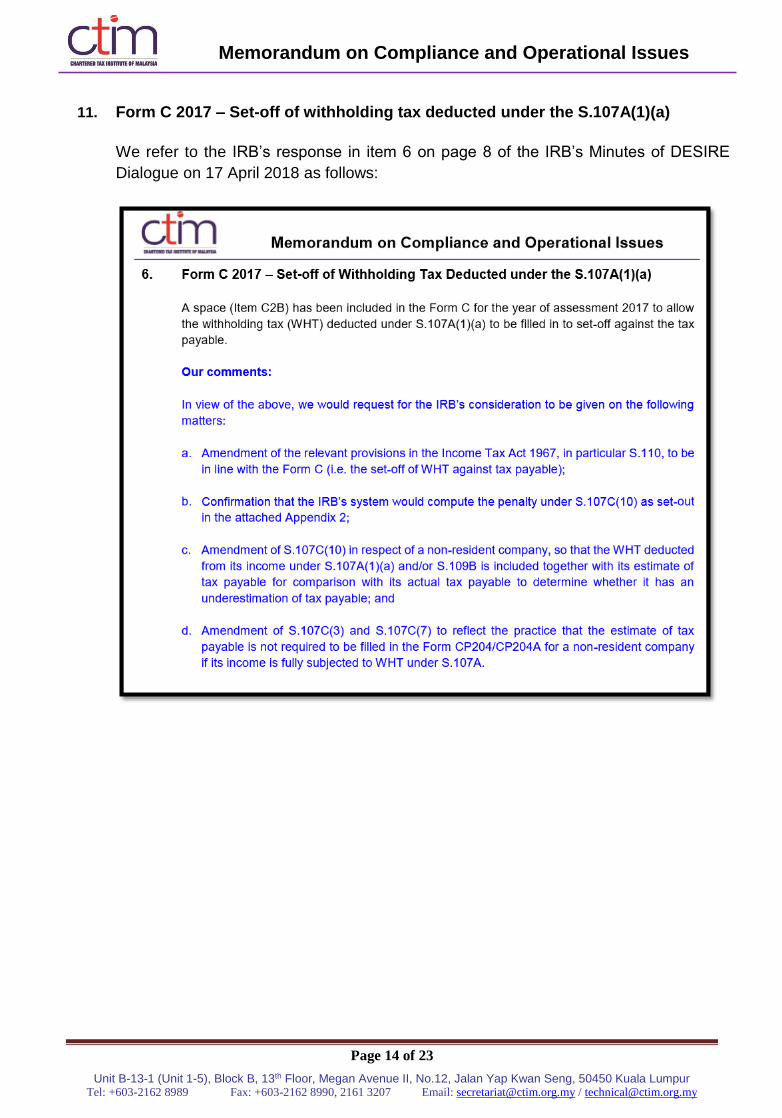

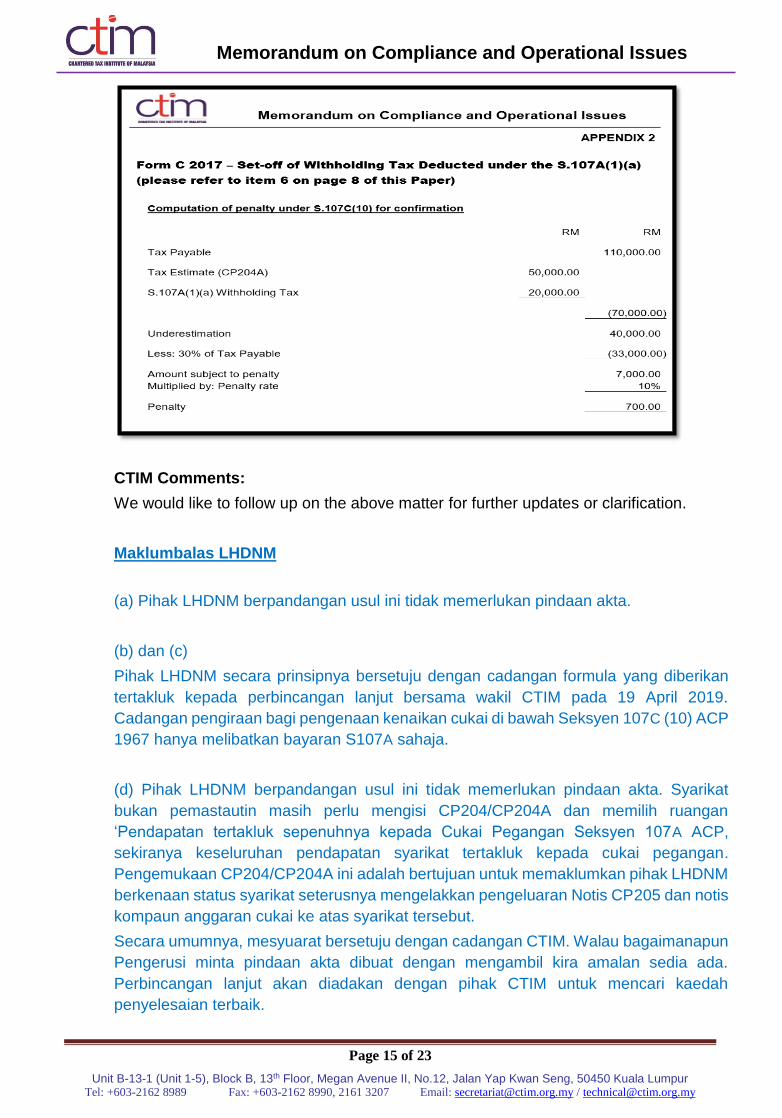

11. Form C 2017 – Set-off of withholding tax deducted under the S.107A(1)(a)

We refer to the IRB’s response in item 6 on page 8 of the IRB’s Minutes of DESIRE

Dialogue on 17 April 2018 as follows:

Memorandum on Compliance and Operational Issues

Page 15 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

CTIM Comments:

We would like to follow up on the above matter for further updates or clarification.

Maklumbalas LHDNM

(a) Pihak LHDNM berpandangan usul ini tidak memerlukan pindaan akta.

(b) dan (c)

Pihak LHDNM secara prinsipnya bersetuju dengan cadangan formula yang diberikan

tertakluk kepada perbincangan lanjut bersama wakil CTIM pada 19 April 2019.

Cadangan pengiraan bagi pengenaan kenaikan cukai di bawah Seksyen 107C (10) ACP

1967 hanya melibatkan bayaran S107A sahaja.

(d) Pihak LHDNM berpandangan usul ini tidak memerlukan pindaan akta. Syarikat

bukan pemastautin masih perlu mengisi CP204/CP204A dan memilih ruangan

‘Pendapatan tertakluk sepenuhnya kepada Cukai Pegangan Seksyen 107A ACP,

sekiranya keseluruhan pendapatan syarikat tertakluk kepada cukai pegangan.

Pengemukaan CP204/CP204A ini adalah bertujuan untuk memaklumkan pihak LHDNM

berkenaan status syarikat seterusnya mengelakkan pengeluaran Notis CP205 dan notis

kompaun anggaran cukai ke atas syarikat tersebut.

Secara umumnya, mesyuarat bersetuju dengan cadangan CTIM. Walau bagaimanapun

Pengerusi minta pindaan akta dibuat dengan mengambil kira amalan sedia ada.

Perbincangan lanjut akan diadakan dengan pihak CTIM untuk mencari kaedah

penyelesaian terbaik.

Memorandum on Compliance and Operational Issues

Page 16 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

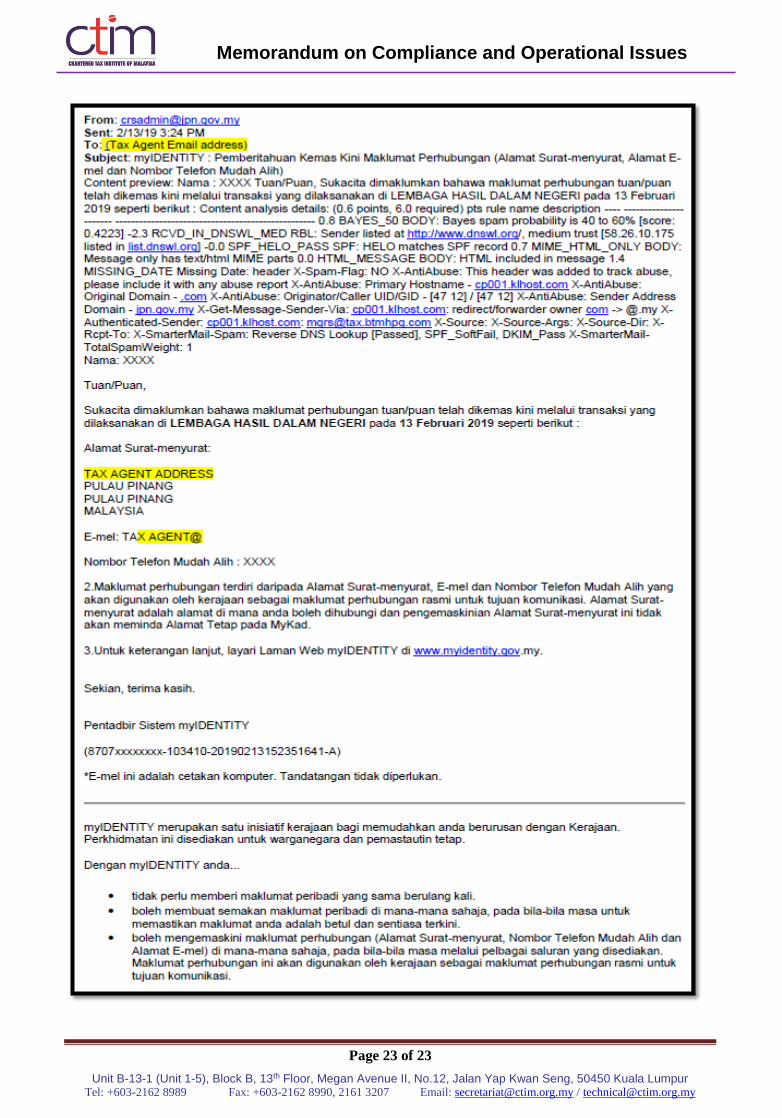

12. myIDENTITY: Notification of updates of contact information (correspondence

address, email and mobile phone number)

Our members raised concerns that they received emails from Jabatan Pengangkutan

Jalan (JPJ) and Jabatan Pendaftaran Negara (JPN) on notification of updates of contact

information via myIDENTITY’s initiative where the JPJ and JPN will use the contact

information updated through transactions with the IRB which consist of details like

addresses, email and mobile phone numbers for communication purposes.

Will notifications like JPJ summons which are not related to tax be also directed to the

tax agent’s address which is used as taxpayer’s correspondence address. [Please refer

to Appendix 4]

CTIM Comments:

The Institute is in opinion that tax correspondence address should only be meant for tax

related matters.

Maklumbalas LHDNM

myIDENTITY adalah satu inisiatif kerajaan untuk perkongsian maklumat dari agensi di

mana LHDNM adalah salah satu agensi yang terlibat. Walau bagaimanapun, maklumat

ejen cukai, seperti surat-menyurat, tidak akan dikemaskini sebagai maklumat terkini

pembayar cukai.

Pegawai LHDNM akan diingatkan agar menandakan alamat ejen cukai (tick box) agar

maklumat berkenaan tidak dihantar ke myIDENTITY untuk dikemaskini kerana

maklumat ejen cukai bukanlah maklumat peribadi pembayar cukai.

Memorandum on Compliance and Operational Issues

Page 17 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

APPENDIX 1

Part N of the Form C 2018 (please refer to item 1 on page 3 of this Paper)

Memorandum on Compliance and Operational Issues

Page 18 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

APPENDIX 2

Paragraph 7.5.10 of the “Rangka Kerja Audit Cukai 2018” (please refer to item 2 on

page 4 of this Paper)

Memorandum on Compliance and Operational Issues

Page 19 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

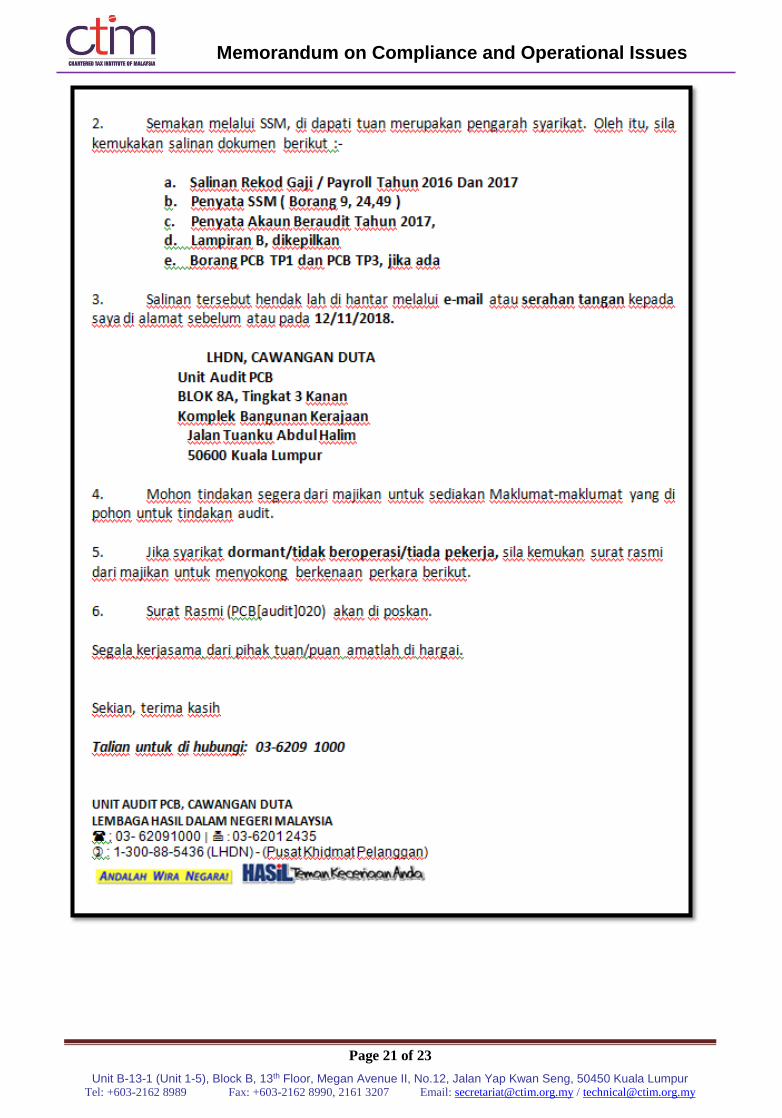

APPENDIX 3

Monthly Tax Deduction (MTD) for locum doctors (please refer to item 10 on page 12 of this Paper)

Memorandum on Compliance and Operational Issues

Page 20 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

Memorandum on Compliance and Operational Issues

Page 21 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

Memorandum on Compliance and Operational Issues

Page 22 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

APPENDIX 4 myIDENTITY: Notification of updates of contact information (correspondence address, email and mobile phone number) (please refer to item 12 on page 15 of this Paper)

Memorandum on Compliance and Operational Issues

Page 23 of 23

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected] / [email protected]

Malaysian Institute of Accountants

JOINT OPERATIONAL ISSUES

Jointly submitted by:

Malaysian Institute of Accountants (MIA) Dewan Akauntan Unit 33-01, Level 33, Tower A The Vertical, Avenue 3 Bangsar South City No. 8, Jalan Kerinchi 59200 Kuala Lumpur [Web] http://www.mia.org.my [Phone] + 60 3 2722 9200 [Fax] + 60 3 2722 9100

The Malaysian Institute of Certified Public Accountants (MICPA) No.15, Jalan Medan Tuanku

50300 Kuala Lumpur

[Web] http://www.micpa.com.my [Phone] + 60 3 2698 9622

[Fax] + 60 3 2698 9403

JOINT OPERATIONAL ISSUES

Contents Page 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12.

e-Filing of Form e-TC Late receipt of correspondences

1. Formula for Determination of MTD Based on the MTD Scheduler Table Unavailability of bilingual guidelines and / or explanatory notes, etc. Utilisation of tax credits against future tax instalment payments / tax payable to be automated Per diem allowances Section 91 of the ITA in relation to assessments and additional assessments in certain cases Section 103(1A) – Tax payable notwithstanding any appeal Section 112 of the ITA in relation to penalty imposed on late filing of return Appeals External body to handle complaints Use of Big Data technology for information gathering

1

1

2

2

2

2

3

3

3

3-4

4

4

1

1. e-Filing of Form e-TC

Issue:

The Form e-TC has been released for the unit trust / property trust to file their tax return electronically from Year of Assessment 2018. The following issues faced by tax agents when filing the Form e-TC for Year of Assessment 2018 on behalf of its clients have been escalated to the IRBM’s officers through phone calls and emails have yet to be resolved.

i. Unable to insert a negative sign under “Pendapatan bersih tahunan

semasa” column

Previously, the system allowed the user to key in a negative figure

under the “Pendapatan bersih tahun semasa” column. Although the

negative sign “i.e., -” is not shown in the Form e-TC, the total is summed

up correctly.

The system no longer allows the user to key in a negative figure under

the above said column.

ii. Incorrect balance carried forward

The “baki hantar hadapan” of the Form e-TC will automatically become

zero if the amount of loss is greater than the amount of balance brought

forward under the “Pendapatan tidak diagihkan” column (see cells circled

in black in Appendix 1).

iii. Blank page

Sometimes, the first page of the Form e-TC will appear blank (please refer

to the 2 different Forms e-TC attached in Appendix 2).

Comment: As the issues cannot be resolved before the filing deadline, the tax agents have submitted the manual Form TC instead. It is hoped that the issues can be resolved quickly to encourage more taxpayers to file return forms electronically.

2

Maklumbalas LHDNM i. & ii. Penambahan petak untuk tandakan nilai negatif hanya dapat dibuat

mulai Tahun Taksiran 2019.

Bagi Tahun Taksiran 2018, Jabatan Operasi Cukai mencadangkan

pengisian seperti berikut sebagai penyelesaian:-

Jika ada pendapatan – Masukkan amaun pendapatan

Jika kerugian – Isikan ‘0’.

iii. Masalah telah di kenal pasti dan tindakan pembetulan sistem telah dilakukan pada 2 April 2019. Pihak MIA & MICPA boleh memberi maklum balas semula jika masalah masih berlaku.

Semakan ke atas borang C, PT dan TA membenarkan ruangan untung rugi tahun semasa diletakkan amaun negatif. Oleh itu cadangan pindaan di atas boleh dilakukan seperti cadangan untuk penyeragaman dengan borang lain.

2. Late Receipt of Correspondences Fact of the case:

Despite the IRB’s notification that correspondences (except for service of notice under Section 145) to taxpayers will be sent via e-mail or fax if email is not available, late receipt of correspondences from the IRB via post is still happening. Details of the cases are appended in the table below and Appendix 3:

Maklumbalas LHDNM

Surat pertama: i. Ini merupakan kes pengeluaran surat tawaran PKPS bagi semua

kategori kod CMS PAM. ii. Kes diagihkan dalam CMS pada 18/12/2018 atas kod 0F,6 (Ada CP204

tetapi tidak dikenakan cukai). iii. Surat Tawaran PKPS bertarikh 19/12/2018 telah disediakan secara

manual mengikut format Memo JPC 27/11/2018. iv. Surat ini dihantar secara pos oleh Unit Pentadbiran. v. Penerimaan Surat mengikut rekod pembayar cukai adalah 14 Januari

2019.

Type of

Correspondences

IRB Branch Date of

Correspondence

Date of Receipt

Tax audit letters Cheras 29 November 2018 14 January

2019

SVDP letters Petaling Jaya 19 December 2018 14 January

2019

3

Isu kelewatan penerimaan surat di pihak pembayar cukai adalah di luar kawalan kerana melibatkan pihak ketiga. Walau bagaimanapun, cadangan MIA untuk mengemukakan surat kepada pembayar cukai melalui emel/faks boleh dipertimbangkan jika maklumat terkini pembayar cukai sentiasa dikemaskini sistem. Maklumbalas LHDNM Surat kedua:

i. Surat CP800 telah dikeluarkan pada 29/11/2018. ii. Surat telah dikemukakan ke Unit Mel/Pentadbiran cawangan pada

30/11/2018 untuk dihantar ke Pos Malaysia. iii. Pihak Unit Mel cawangan menghantar surat berkenaan pada hari

berikutnya. iv. Proses kerja Unit Mel cawangan, surat-surat akan dihantar setiap hari

ke Pos Malaysia. v. Tiada rekod atau senarai dibuat bagi penghantaran surat biasa kerana

bilangannya yang tinggi.

Cadangan untuk mengelakkan kelewatan penerimaan surat di masa hadapan oleh pembayar cukai, surat akan dikeluarkan melalui emel oleh pihak pegawai cawangan. Pengenalan MyTax dan semua urusan akan dihantar melalui emel kepada inbox pembayar cukai. Pembayar cukai wajib mengisi maklumat alamat e-mel di e-Filing.

3. Formula for Determination of MTD Based on the MTD Scheduler Table Presently the formula for determination of MTD based on the MTD Scheduler Table allows for the deduction of contributions to approved provident subject to the maximum combined life insurance and EPF relief allowed. With the segregation of the income tax relief on contributions to approved funds up to RM4,000 and income tax relief on takaful contributions or payment for life insurance premiums up to RM3,000 with effect from Year of Assessment 2019 onwards, the Institutes would like to propose for the IRBM’s consideration to include the deduction for takaful contributions or payments for life insurance premiums into the formula to minimise tax refund cases for individual taxpayers. Maklumbalas LHDNM Disarankan supaya menggunakan Kalkulator PCB yang terdapat di Portal Rasmi LHDNM bagi menggantikan penggunaan Jadual PCB. Kalkulator PCB boleh mengambil kira potongan sumbangan takaful atau bayaran premium insurans nyawa.

4

4. Unavailability of bilingual guidelines and / or explanatory notes etc. The Form e-C explanatory notes (YA 2017) and many Guidelines (e.g. RPGT Guidelines) issued are available in Bahasa Malaysia only. Given the number of multinational companies (MNC) operating in Malaysia, there are many companies’ officers and/or directors required to sign off on documents, who are foreigners and do not understand Bahasa Malaysia. Without the bilingual forms and/or guidelines, the respective signatories would find it challenging as they would then be required to sign off on documents which they do not comprehend. We would like to propose for the Inland Revenue Board of Malaysia (IRBM) to consider issuing all the forms and/or guidelines in English as well to attract foreign investments. Maklumbalas LHDNM Nota Penerangan Borang C versi Bahasa Inggeris Tahun Taksiran 2017 tidak dikeluarkan. Walau bagaimanapun, Buku Panduan Borang C versi Bahasa Inggeris Tahun Taksiran 2018 telah di muat naik ke Portal Rasmi LHDNM untuk rujukan. 5. Utilisation of tax credits against future tax instalment payments / tax payable to be automated Currently, applications for the utilization of tax credits against future tax installment payments / tax payable are done manually, by sending in letters (via post and e-mails) to the IRBM, and/or lodging in the applications at the IRBM’s counter. This is a time consuming process as taxpayers would be required to follow up with the IRBM officers on the approvals, or travel to the IRBM’s office to lodge in the application. We would propose for the IRBM to consider automating this process. For example, taxpayers can be provided an option to automatically utilize the tax credits against future tax installment payments / tax payable, by indicating their intent to do so via an online portal (e.g. Form e-C etc.). Maklumbalas LHDNM Pihak LHDNM tidak bersetuju dengan cadangan ini dan tidak akan melaksanakan secara automatik kes penggunaan kredit cukai bagi menyelesaikan ansuran berikutnya. Pihak kami akan membuat bayaran balik atas amaun kredit yang wujud.

5

6. Per diem allowances

The Institutes propose that the IRBM publish the per diem allowance rate (by countries) on its website after consultation with employers. With this, only the per diem allowance paid in excess of the published rate is reportable as income in the Form EA. This will create more certainty and simplicity in tax compliance under the SAS. This new tax treatment on per diem allowance has been adopted in Singapore with effect from YA 2005. Maklumbalas LHDNM Perkara ini memerlukan pindaan kepada peruntukan Akta dan ianya memerlukan kajian lanjut untuk pembuat polisi iaitu Kementerian Kewangan membuat keputusan. LHDNM akan membuat kajian lanjut mengenai perkara ini.

7. Section 91 of the ITA in relation to assessments and additional

assessments in certain cases The Director General (DG) can issue an assessment based on the ‘best of DG’s judgement’ without providing any grounds for the assessment. The Institutes are of the view that to enable taxpayers to submit a detailed appeal, a provision should be incorporated to require the DG to provide the computation and grounds for its adjustments giving rise to the additional tax. It is also proposed that this be extended to Real Property Gains Tax cases. Maklumbalas LHDNM Taksiran yang dibangkitkan berdasarkan best of DG’s judgement oleh LHDNM adalah berdasarkan justifikasi atau asas-asas tertentu. Pembayar cukai boleh mendapatkan justifikasi atau asas tersebut dari LHDNM dan diberi ruang untuk membuat bantahan/rayuan berhubung taksiran yang dibangkitkan ini. Oleh itu, LHDNM berpandangan tiada isu berbangkit berhubung perkara ini.

Jika terdapat kes-kes berbangkit, mohon pihak insitusi memberikan maklumat tersebut kepada LHDNM untuk disemak Perenggan 7.5 Rangka Kerja Audit Cukai 2018 telah menyatakan dengan jelas bahawa surat pelarasan cukai dan notis taksiran akan dikeluarkan untuk kes audit yang melibatkan pelarasan cukai. Ini termasuklah kes audit yang melibatkan taksiran anggaran / best of DG’s judgement’. Sekiranya tiada pelarasan cukai, surat memaklumkan tentang penyelesaian audit tanpa pelarasan akan dikeluarkan.

6

Rujukan terperinci kepada:

7.5.4 Pembayar cukai akan dimaklumkan mengenai penemuan audit yang meliputi perkara-perkara berikut:

a) isu-isu audit yang dibangkitkan;

b) sebab dan rasional isu-isu yang dibangkitkan; dan

c) jumlah cadangan pelarasan cukai dan penalti (jika ada) dan tahun-tahun taksiran yang terlibat.

7.5.5 Sekiranya terdapat pelarasan cukai, surat pemberitahuan cadangan pelarasan cukai yang terperinci dan sebab-sebab pelarasan dibuat akan dikeluarkan. Pembayar cukai akan diberi peluang untuk memberi maklum balas dan penjelasan berkenaan dengan penemuan audit dan cadangan pelarasan cukai yang dikemukakan. 7.5.6 Jika pembayar cukai tidak berpuashati dengan cadangan pelarasan cukai yang dibangkitkan, pembayar cukai boleh membuat bantahan secara rasmi dalam tempoh lapan belas (18) hari dari tarikh surat pemberitahuan pelarasan dengan mengemukakan maklumat tambahan dan bukti-bukti untuk menyokong bantahannya. 7.5.9. Seterusnya notis taksiran cukai atau pemberitahuan tidak kena cukai akan dikeluarkan. Sekiranya tiada pelarasan dibuat, surat memaklumkan tentang penyelesaian audit tanpa pelarasan akan dikeluarkan.

8. Section 103(1A) – Tax payable notwithstanding any appeal Presently, under section 103(2), the tax payable under an assessment or

increased assessment, shall on the service of the notice of assessment or

composite assessment or increased assessment, as the case may be, be due

and payable notwithstanding any appeal.

There are instances where the raising of the abovementioned assessments a

long time after the time bar period has caused undue financial burden to

taxpayers. Moreover, the appeal process frequently takes several years to

complete giving rise to extreme financial hardship to taxpayers who finally won

the appeal.

For equity and fairness, the Institutes would like to propose that a mechanism be introduced in the ITA to allow the Courts to review the payment of such taxes based on the merits for raising such assessments.

7

Maklumbalas LHDNM Pihak LHDNM tidak bersetuju dengan cadangan tersebut. Pembayar cukai telah diberikan ruang untuk membuat rayuan jika tidak berpuas hati dengan taksiran yang dibangkitkan sehingga kepada peringkat Pesuruhjaya Khas Cukai Pendapatan (PKCP). Setiap taksiran yang dibangkitkan oleh LHDNM adalah berdasarkan merit masing-masing. Oleh itu, tidak timbul isu berkaitan taksiran dibangkitkan tanpa merit.

9. Section 112 of the ITA in relation to penalty imposed on late filing of return Based on the Guideline on Imposition of Penalties under Section 112(3) of the ITA issued by the IRBM on 5 March 2015 (GPHDN 1/2015), the penalty rates for late filing ranging from 20% to 35% will be imposed on tax payable depending on the delay in filing. The penalty rates would appear to be inequitable and unfair in cases where taxes have already been paid (i.e. monthly tax instalments), given that in such instances, there is no economic loss to the Government. Due regard should be given to the tax instalments which have already been paid, and as such, the penalties should be imposed only on the amount of tax that is outstanding. The penalties should also reflect the taxpayer’s record of default and not just the delay in submission – e.g. penalties could be increased in line with the number of occasions that a taxpayer has defaulted in lodging its returns. Note: We understand that the IRBM is currently looking into this. Maklumbalas LHDNM Kaedah pengiraan penalti di bawah subseksyen 112(3) ACP 1967 mengambil kira bayaran pendahuluan bagi tahun berkenaan mulai 1 Januari 2019. Kadar penalti yang dikenakan ke atas kategori pembayar cukai di bawah seksyen 77 dan 77A ACP 1967 adalah berdasarkan tempoh masa yang diambil untuk mengemukakan BNCP selepas tarikh akhir pengemukaan. Tempoh kelewatan akan diambil kira dari tarikh akhir pengemukaan jika BNCP gagal dikemukakan dalam tempoh tambahan/lanjutan masa yang dibenarkan.

8

10. Appeals (a) The Institutes strongly urge the Authorities to review the composition of

the Special Commissioner of Tax (SCIT), a tribunal which handles tax

appeals. We are of the view that the tribunal must have more than one

panel in order for justice to be served.

In addition, for the timely disposal of appeals, the Institutes would like to

propose for a review of the timeframe for disposal of appeals (made via a

Form Q) by the DGIR to be reduced to a period of 6 months.

(b) The Dispute Resolution Department of the IRBM is responsible for hearing

and considering appeals by taxpayers before their cases are presented to

the Special Commissioner of Income Tax. The dispute resolution process

could be enhanced to allow more appeals to be covered with a view of

resolving the cases before the case is heard by the SCIT. This would give

space for the parties involved to achieve the best solution and save time

and cost.

To expedite the dispute resolution process, the Institutes would like to propose that the Authorities consider appointing a representative from the private sector to share his/her practical experience so that more cases can be resolved efficiently.

Maklumbalas LHDNM

(a) Under the Act, SCIT is allowed to have more than one panel. But the challenge is on the insufficient number of commissioners appointed. However, this issue is best addressed by MOF as the IRBM is not involved in the appointment of commissioners. Alternatively, the MOF should consider appointing commissioners other than officers from AG Chambers.

In order for both parties (IRBM and taxpayers) to come to an out of court settlement, a reasonable time period is needed. Based on the Dispute Resolution Department’s record, taxpayers will normally optimize the full 12-month period before agreeing to settle their appeal with an out of court settlement. Therefore it is of the view of this department that the 12-month period is necessary to encourage taxpayers to agree with IRBM.

9

(b) Based on the Dispute Resolution Department’s record, all requests for dispute resolution proceeding by taxpayers have been entertained by the Department. In fact there have also been cases where the Department had initiated dispute resolution process to effectively resolve disputed matters in a timely manner though there was no request made by taxpayer.

Record shows that the department had disposed of appeals effectively and efficiently. Therefore it is not necessary to appoint a representative from the private sector as part of the dispute resolution panel.

11. External body to handle complaints

In Australia, all complaints are made to the Inspector General of Taxation (Previously handled by the Commonwealth Ombudsman), a body that is separate from the Tax Authority who would conduct an independent investigation. Refer to https://igt.gov.au/making-a-complaint/ for more information.

The IGT covers a broad range of complaint areas including mishandling of queries, mistreatment by officers etc., The IGT prepares a report each year and this is published and made available to the Parliament and the General Public.

Malaysia may implement the same to encourage transparency and

improving the service standard of the IRBM.

Maklumbalas LHDNM 1. Pengurusan Aduan Integriti berhubung salah laku Pegawai LHDNM

dikendalikan sepenuhnya oleh Bahagian Integriti, Jabatan Integriti & Pengurusan Risiko (JIPR) sepertimana yang diarahkan di dalam pekeliling dan garis panduan berikut :

a) Pekeliling Perkhidmatan Bilangan 6 Tahun 2013 : Penubuhan Unit Integriti Di Semua Agensi Awam yang dikeluarkan oleh Jabatan Perkhidmatan Awam (JPA)

b) Garis Panduan Pengurusan Unit Integriti Agensi Awam Tahun 2019 yang dikeluarkan oleh Suruhanjaya Pencegahan Rasuah Malaysia (SPRM).

2. Aduan Integriti berhubung salah laku Pegawai LHDNM boleh disalurkan melalui kaedah-kaedah berikut:

10

a) Tab khas di Portal Rasmi LHDNM Web www.hasil.gov.my >Hubungi Kami > Maklum Balas > Laporkan Salah Laku Pegawai

b) Emel atau Surat aduan terus kepada Ketua Pegawai Integriti (CIO) LHDNM.

c) Talian terus kepada CIO LHDNM. d) Temujanji dengan Pengarah Bahagian Integriti di JIPR.

Bagi tujuan pemantauan aduan, langkah-langkah yang diambil oleh LHDNM adalah seperti berikut :

1. Menyediakan tab khas untuk saluran aduan di Portal Rasmi LHDNM

2. Pemantauan Aduan berhubung dengan operasi percukaian adalah melalui :

a. LHDNM : i. Jawatankuasa Tetap Pengurusan Aduan peringkat Ibu

Pejabat ii. Jawatankuasa Aduan peringkat cawangan

b. Agensi luar :

i. Kementerian Kewangan - Mesyuarat pengurusan aduan peringkat Kementerian Kewangan

ii. Biro Pengaduan Awam – pantau segala jenis perkhidmatan kerajaan dan swasta

11

12. Use of Big Data technology for information gathering Based on public announcements, the IRBM is currently embarking on a Big

Data initiative named ‘Hasil Power Data’ that envisages the application of Big

Data in taxation in line with the development of technology and digitalisation.

Hence, it is suggested that IRBM be granted access (albeit in a limited manner)

to relevant data from other agencies, bodies and financial institutions such as

from the Royal Malaysian Customs Department and the Companies

Commission of Malaysia to gain, verify and ascertain relevant information and

thereby reduce the need for site visits that may cause discomfort and deter

business operations.

It is suggested that the application of XBRL be done extensively throughout the industry including for filing purpose (similar to the system used in the Inland Revenue Authority of Singapore) that had proven to provide seamless tax filing and exchange of information between authorities and increasing the level of transparency. Maklumbalas LHDNM LHDNM sememangnya telah menggunakan data dari pelbagai agensi untuk meningkatkan kecekapan perkhidmatan dan mengintegrasi perkongsian maklumat. LHDNM akan memperkenalkan penghantaran Helaian Kerja Pengiraan Cukai dan penyata kewangan dengan menggunakan sistem pengemukaan XBRL yang dinamakan Malaysia Income Tax Reporting System (MITRS). Pelaksanaan XBRL dilaksanakan secara berperingkat mengikut entiti pelapor. Peringkat awal perlaksanaan akan melibatkan kes-kes syarikat yang terpilih untuk audit bagi mengemukakan Helaian Kerja Pengiraan Cukai dan penyata kewangan secara pilihan menggunakan MITRS. Pelan pelaksanaan MITRS telah dimuat naik di portal rasmi LHDNM untuk rujukan. Sistem MITRS telah dibuka untuk pengujian dan maklumbalas oleh orang awam bermula 15 April 2019.

MEMORANDUM ON COMPLIANCE AND OPERATIONAL ISSUES

(ADDITIONAL ISSUES)

29 March 2019

Prepared by: Compliance & Operations Working Group (COWG)

Memorandum on Compliance and Operational Issues (Additional Issues)

Page 2 of 5

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

Contents

Page No.

COMPLIANCE AND OPERATIONAL ISSUES

1 Appeal for lower tax estimate of less than the minimum 85% amount not allowed with effect from YA 2019

3

2 Foreign Exchange (“Fx”) Rates 5

Memorandum on Compliance and Operational Issues (Additional Issues)

Page 3 of 5

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

1. Appeal for lower tax estimate of less than the minimum 85% amount not allowed with effect from YA 2019

Issues raised by member which is reproduced below:

We have received an email reply from one of the officers from Pusat Pemprosesan (Unit

Anggaran Cukai) with regards to one of our appeal for lower tax estimate cases for the year

of assessment (“YA”) 2019 whereby we were informed that Pusat Pemprosesan will not allow

any appeals for lower tax estimate of less than the minimum 85% amount with effect from YA

2019.

When we sought clarification from the Inland Revenue Board (“IRB”) officer, we were verbally

informed that there was an internal instruction given to them on 15 February 2019 on this

matter. Furthermore, she informed that effective from 15 February 2019, Pusat Pemprosesan

(Unit Anggaran Cukai) will only consider special revision applications after the 9th month of

the basis period of a year of assessment together with valid reasons and supporting

documents.

Furthermore, the IRB has not notified taxpayers on any change to their operational guidelines

(Garis Panduan Operasi Bil.1 Tahun 2017) dated 23 February 2017 which mentioned that

Pusat Pemprosesan would consider appeals for lower tax estimate less than the minimum

85% amount specified in Section 107C(3) of the Income Tax Act (“ITA”) 1967.

Additional verbal clarification obtained from the IRB:

The IRB officer in charge of CP204 in the IRB Tax Operation Department has confirmed that

the Guidelines on the submission of the estimated tax payable under Section 107C, ITA 1967

(Garis Panduan Operasi Bil.1 Tahun 2017) have been withdrawn from the IRB website in

order to revise the Guidelines accordingly.

The officer also confirmed that appeals for lower tax estimate of less than the minimum 85%

amount will not be allowed with effect from YA 2019.

According to the officer, no announcement will be made publicly on this matter for the time

being but the IRB will inform the professional bodies on this matter during a dialogue.

CTIM comments:

i. We hope that the IRB could reconsider the above by allowing any appeals for lower tax estimate less than the minimum 85% amount on a case to case basis, especially if the case is genuine and can be substantiated with documented evidence such as the following: -

Taxpayers who have incurred / projected current year business losses (e.g. due to loss of a particular project resulting in huge drop in revenue);

Taxpayers with carry forward business losses, sufficient to set-off against the current year business profits; and

Taxpayers who are in the process of closing down business and under liquidation or strike-off.

ii. We would also like to request the IRB to make an announcement if there is any withdrawal of guidelines etc. from the IRB website.

Memorandum on Compliance and Operational Issues (Additional Issues)

Page 4 of 5

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

Maklumbalas LHDNM

Berkuatkuasa daripada tahun taksiran 2006, anggaran cukai yang kena dibayar bagi sesuatu

tahun taksiran hendaklah tidak kurang daripada 85% anggaran cukai dipinda bagi tahun taksiran

sebelumnya. Jika tiada pindaan anggaran cukai dikemukakan, anggaran cukai tahun semasa

hendaklah tidak kurang daripada 85% anggaran cukai pada tahun taksiran sebelum.

Bagi syarikat yang baru memulakan operasi, syarikat boleh menentukan anggaran cukai bagi

tahun taksiran pertama mengikut anggaran keuntungan syarikat. Anggaran cukai pada tahun

taksiran pertama tersebut akan menjadi asas untuk menentukan anggaran cukai tahun taksiran

berikutnya.

Secara dasarnya, pembayar cukai dibenarkan untuk membuat pindaan anggaran cukai tetapi

oleh kerana jumlah pindaan anggaran cukai yang terlalu tinggi dari tahun ke setahun, LHDNM

tidak dapat membenarkan amalan ini berterusan. Pusat Pemprosesan Maklumat dimohon untuk

menyemak dan mempertimbangkan kes-kes tertentu dengan syarat dan proses yang lebih ketat.

Makluman ini akan disampaikan kepada pegawai yang terlibat yang mana ianya hanya

melibatkan pegawai di Pusat Pemprosesan Maklumat.

Memorandum on Compliance and Operational Issues (Additional Issues)

Page 5 of 5

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

2. Foreign Exchange (“Fx”) Rates

The IRB used to provide the attached Fx Rates table on its website. The rates were provided for each YA, up to YA 2017. The IRB has ceased to provide the rates on a YA basis. In place of this, the IRB's website currently directs users to use rates from the Accountant General's (AG) website. The issue is that the rates from the AG's website are based on monthly rates.

CTIM comments:

Taxpayers should be entitled to adopt Fx rates from any credible sources such as Bank Negara, Accountant General and even the IRB. The law does not mandate taxpayers to adopt an IRB endorsed rate. However, as a practical matter, the IRB should clarify/state the specific purpose of the current monthly rates. The move from the former YA rates to the current monthly rates raises a practical confusion for those who have been and wish to continue to rely on rates given by the IRB.

Maklumbalas LHDNM

Kadar pertukaran matawang asing yang perlu digunakan pembayar cukai individu bagi tujuan

pelaporan borang nyata cukai pendapatan adalah kadar pertukaran matawang asing monthly

average basis bagi bulan Disember bagi tahun taksiran tersebut.

Kadar pertukaran matawang asing monthly average basis yang digunakan adalah merujuk

kepada Jadual Kadar Pertukaran Wang Asing yang dikeluarkan oleh Jabatan Akauntan Negara

Malaysia yang disediakan berasaskan kadar tukaran matawang oleh Bank Negara Malaysia dan

telah dimuat naik ke Portal Rasmi LHDNM.

DESIRE BIL. 1/2019 LAMPIRAN 4

ms. 1 / 3

SOALAN DAN MAKLUM BALAS TAMBAHAN – DESIRE BIL 1 TAHUN 2019

1. Refund of individual (expatriate) to be refunded to company or third party - MIA

Terdapat cawangan yang tidak membenarkan bayaran balik dibuat kepada pihak

ketiga dan perlu dibuat bayaran balik kepada akaun individu berkenaan sahaja.

Maklumbalas LHDNM

LHDNM tidak mengeluarkan sebarang arahan berkenaan dan akan menyemak

dengan Cawangan Kota Kinabalu seperti yang dimaklumkan. Tiada arahan tidak

membenarkan bayaran balik kepada pihak ketiga. LHDNM akan menyemak semula

prosedur dan memaklumkan cawangan yang terlibat.

Pihak MIA perlu memberikan maklumat terperinci untuk semakan lanjut.

2. Time bar to open file for audit that do not justify what item to open so that the tax

payer will not argue. Ejen cukai telah memberikan penerangan kepada pelanggan

tentang time barred, tetapi pelanggan mendapatkan nasihat pihak guaman bahawa

LHDNM perlu membuktikan terdahulu isu penemuan selepas 6 tahun. It is the

responsibility of IRB to prove fraud and negligence - CTIM

Maklumbalas LHDNM

Dalam proses taksiran dan rayuan taksiran, pembayar cukai telah dimaklumkan

penemuan audit dan perbincangan boleh dibuat bagi semakan sebarang maklumat

yang diperlukan oleh pembayar cukai. Pembayar cukai perlu membuktikan jika tiada

kesalahan fraud and negligence dalam penemuan audit berkenaan.

Walaupun dokumen tidak perlu di simpan bagi tempoh melebihi tujuh (7) tahun, jika

ada penemuan audit bagi kesalahan fraud and negligence, LHDNM boleh

membangkitkan taksiran berdasarkan bukti yang diperolehi. Pembayar cukai boleh

membuat bantahan atau rayuan bagi kes berkenaan.

3. IRB officers not following guideline of allowable expenses. Terdapat aduan daripada

ahli di mana allowable expenses ditolak tanpa alasan yang kukuh - MAICSA

Maklumbalas LHDNM

Sebarang aduan boleh dibuat dengan menyatakan secara jelas fakta kes untuk

semakan dan tindakan pihak pengurusan LHDNM. Pegawai LHDNM akan sentiasa

diingatkan dan diberikan latihan agar mengikut arahan, pekeliling dan prosedur

kerja yang telah ditetapkan.

DESIRE BIL. 1/2019 LAMPIRAN 4

ms. 2 / 3

4. Stamp duty on share transfer guideline (EPS) - MAICSA

Tiada garis panduan dan penjelasan berkenaan pindah milik saham. Pindaan Akta

Syarikat yang terdahulu memerlukan pindaan kepada garis panduan bagi pindah

milik saham.

Maklumbalas LHDNM

Garis panduan dan penerangan tentang pindah milik saham akan dikeluarkan

dalam masa terdekat. Pertimbangan perlu dibuat berkenaan isu kecekapan dan

beberapa isu yang berkaitan. Pindaan garis panduan akan mengambilkira

perubahan No PAR Value dalam Akta Syarikat yang terkini.

5. Voluntary Disclosure Issues / Program Khas Pengakuan Sukarela (PKPS)

– MIA / CTIM

Pembayar cukai menemui bukti dan bercadang untuk membuat pindaan pengakuan

yang kedua tetapi akan menyebabkan cukai lebih rendah daripada pengakuan

asal? Adakah ini dibenarkan?

Terdapat pembayar cukai yang membuat pelaporan bagi tahun kebelakangan

dalam tahun 2017, tetapi tidak memaklumkan bagi tahun taksiran yang mana,

adakah tahun selain 2017 itu akan tertakluk kepada audit?

Kaveat dalam surat - untuk kes pindahan harga (transfer pricing). Adakah pindahan

harga tidak termasuk dalam PKPS?

Ada yang meminta dokumen tambahan bagi PKPS dan amalan ini tidak selaras di

beberapa cawangan LHDNM.

MIA mencadangkan kepada LHDNM untuk membuat promosi agar pembayar cukai

melantik ejen cukai yang sah sahaja dan bukan bogus tax agent.

Maklumbalas LHDNM

Pengakuan adalah melibatkan kes cukai kena dibayar dan jika ada pengurangan

cukai adalah tertakluk kepada audit.

Pembayar cukai perlu memaklumkan LHDNM pengakuan sukarela dibuat untuk

tahun taksiran tertentu supaya direkodkan bahawa pengakuan tersebut merujuk

kepada tahun taksiran yang terlibat sahaja walaupun taksiran dilaporkan

keseluruhannya dalam tahun 2017. LHDNM akan menerima maklumat pengakuan

sukarela yang dibuat dalam tempoh Program Khas dengan suci hati.

Kaveat dalam surat bagi kes pindahan harga disebabkan oleh pelarasan oleh pihak

lain iaitu negara ketiga.

DESIRE BIL. 1/2019 LAMPIRAN 4

ms. 3 / 3

Permintaan dokumen tambahan diperlukan jika melibatkan kesalahan pengiraan

cukai oleh pembayar cukai dan mungkin akan menyebabkan terkurang amaun cukai

tambahan berkenaan. Sepatutnya tiada dokumen tambahan diperlukan dalam

pengakuan sukarela dan pihak cawangan akan dimaklumkan sewajarnya.

Makluman Tambahan Berkenaan Program Khas Pengakuan Sukarela

Kerajaan telah memutuskan untuk menyambung tempoh Program Khas

Pengakuan Sukarela seperti berikut:

Tempoh Kadar Penalti

3 Nov 2018 – 30 Jun 2019 10%

1 Julai 2019 – 30 Sept 2019 15%

LHDNM menyeru agar pihak persatuan dan badan profesional membantu

mempromosi Program Khas Pengakuan Sukarela kepada semua pembayar cukai

dan rakyat Malaysia untuk mengambil peluang pelanjutan tempoh masa ini

dengan segera dan tidak bertangguh lagi kerana tempoh ini tidak mungkin akan

dilanjutkan lagi oleh pihak Kerajaan.

LHDNM akan mengeluarkan Garis Panduan Operasi Bil. 1 Tahun 2019 dengan

sedikit penambahbaikan dan penjelasan tentang Program Khas Pengakuan

Sukarela.