Managerial Finance FINA 6335 The CAPM and Cost of Capital Lecture 9.

32

Managerial Finance FINA 6335 The CAPM and Cost of Capital Lecture 9

-

date post

22-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of Managerial Finance FINA 6335 The CAPM and Cost of Capital Lecture 9.

Managerial Finance

FINA 6335

The CAPM and Cost of Capital

Lecture 9

Simplifying Assumptions

• Individuals can trade securities without regard to fees, taxes, and other frictions.

• Individuals get any relevant information about the firms they are interested in costlessly.

• Individual investors can borrow or save at the same riskless rate equal the the “riskfree rate”

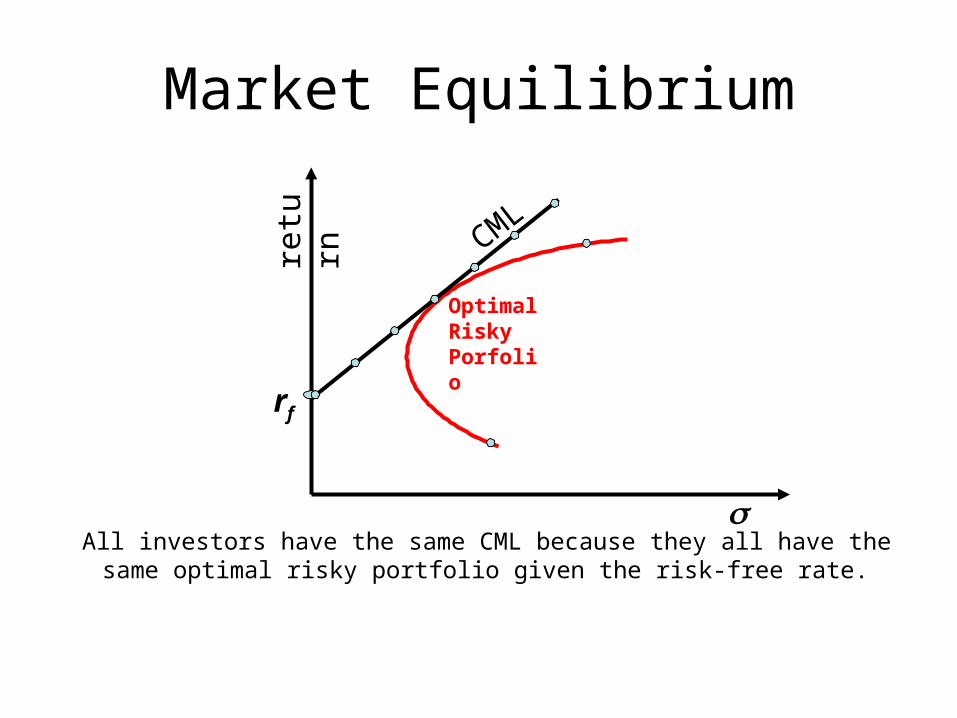

Market Equilibrium

All investors have the same CML because they all have the same optimal risky portfolio given the risk-free rate.

rf

retu

rn

Optimal Risky Porfolio

CML

Market Equilibrium

The CML:

Rp = Rf + (pMRM- Rf )

rf

retu

rn

Optimal Risky Porfolio

CML

Definition of Risk When Investors Hold the Market Portfolio

• Researchers have shown that the best measure of the risk of a security in a large portfolio is the beta ()of the security.

• Beta measures the responsiveness of a security to movements in the market portfolio.

)(

)(2

,

M

Mii R

RRCov

Estimates of for Selected Stocks

Stock BetaBank of America 1.55

Borland International 2.35

Travelers, Inc. 1.65

Du Pont 1.00

Kimberly-Clark Corp. 0.90

Microsoft 1.05

The Formula for Beta

)(

)(2

,

M

Mii R

RRCov

)(

)()( ,

M

iMii R

RRR

Relationship between Risk and Expected Return (CAPM)

• Expected Return on the Market:

• Expected return on an individual security:

PremiumRisk Market FM RR

)(β FMiFi RRRR

Market Risk Premium

This applies to individual securities held within well-diversified portfolios.

Expected Return on an Individual Security

• This formula is called the Capital Asset Pricing Model (CAPM)

)(β FMiFi RRRR

• Assume i = 0, then the expected return is RF.• Assume i = 1, then Mi RR

Expected return on a security

=Risk-

free rate+

Beta of the security

×Market risk

premium

Relationship Between Risk & Expected Return

Exp

ecte

d re

turn

)(β FMiFi RRRR

FR

1.0

MR

)(β FMiFi RRRR

Relationship Between Risk & Expected Return

Exp

ecte

d re

turn

%3FR

%3

1.5

%5.13

5.1β i %10MR

%5.13%)3%10(5.1%3 iR

Summary and Conclusions

• This chapter sets forth the principles of modern portfolio theory.

• The expected return and variance on a portfolio of two securities A and B are given by

ABAABB2

BB2

AA2P )ρσ)(wσ2(w)σ(w)σ(wσ

)()()( BBAAP rEwrEwrE

Summary and Conclusions

• The efficient set of risky assets can be combined with riskless borrowing and lending. In this case, a rational investor will always choose to hold the portfolio of risky securities represented by the market portfolio.

P

Summary and Conclusions

• The contribution of a security to the risk of a well-diversified portfolio is proportional to the covariance of the security's return with the market’s return. This contribution is called the beta.

• The CAPM states that the expected return on a security is positively related to the security’s beta:

)(β FMiFi RRRR

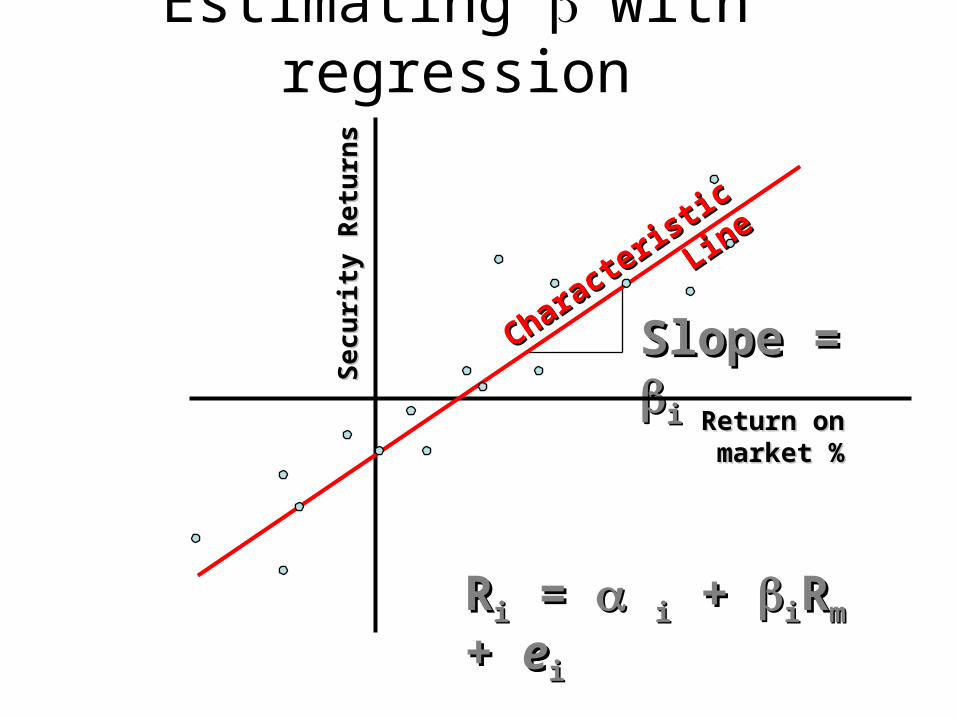

Estimating with regression

Sec

uri

ty R

etu

rns

Sec

uri

ty R

etu

rns

Return on Return on market %market %

RRii = = ii + + iiRRmm + + eeii

Slope = Slope = iiCharacte

ristic

Line

Characteris

tic Line

Security Market Line

Sec

uri

ty R

etu

rns

Sec

uri

ty R

etu

rns

BetaBeta

RRii = = RRff + + ii(R(Rmm – R – Rff ) )

Slope = Slope = R(m)-R(f)R(m)-R(f)

Securit

y Mark

et

Securit

y Mark

et

LineLine

Practical Issues in CAPM

• Forecasting Beta– The problem is that you assume your estimate

of Beta is the true value of Beta– “regression toward one”– Allow for extremes– What Time Horizon

• 2 years of weekly, or 5 years of monthly

The Security Market Line

• Risk free interest rate?

• The Market Risk Premium 5.7%

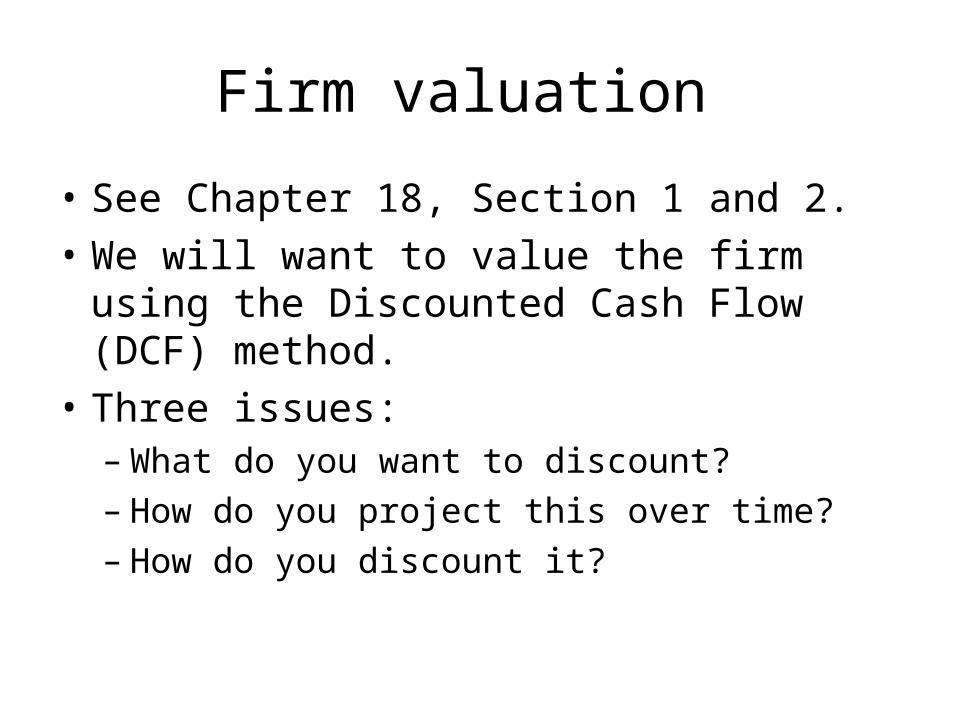

Firm valuation

• See Chapter 18, Section 1 and 2.

• We will want to value the firm using the Discounted Cash Flow (DCF) method.

• Three issues:– What do you want to discount?– How do you project this over time?– How do you discount it?

Be Heroic!!!

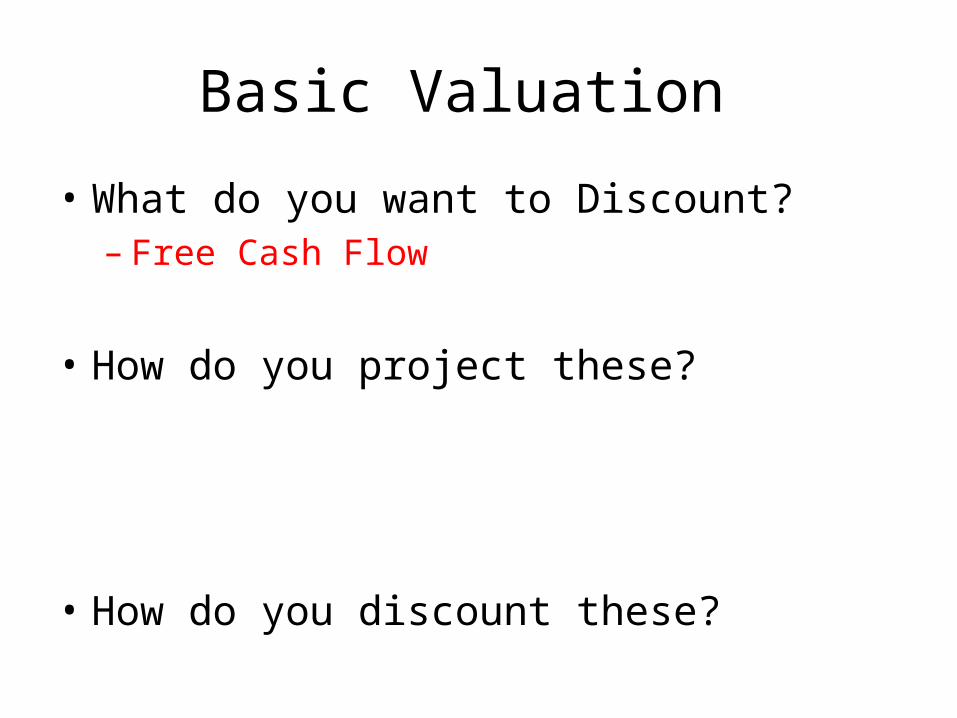

Basic Valuation

• What do you want to Discount?

• How do you project these?

• How do you discount these?

Basic Valuation

• What do you want to Discount?– Free Cash Flow

• How do you project these?

• How do you discount these?

Basic Valuation

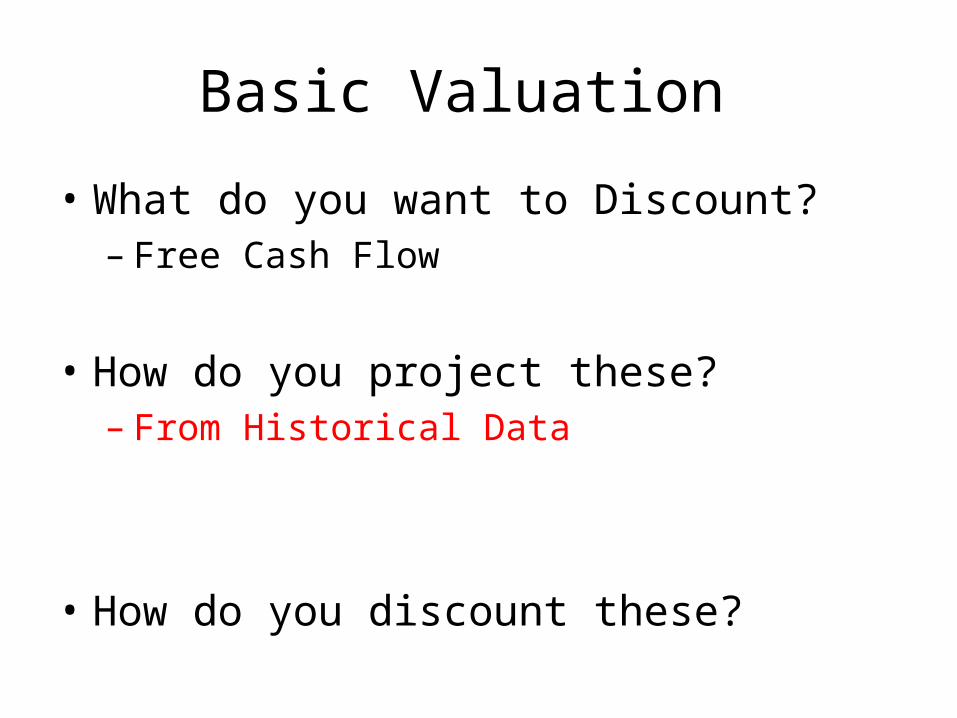

• What do you want to Discount?– Free Cash Flow

• How do you project these?– From Historical Data

• How do you discount these?

Basic Valuation

• What do you want to Discount?– Free Cash Flow

• How do you project these?– From Historical Data

• How do you discount these?– The Cost of Capital or (Weighted Average)

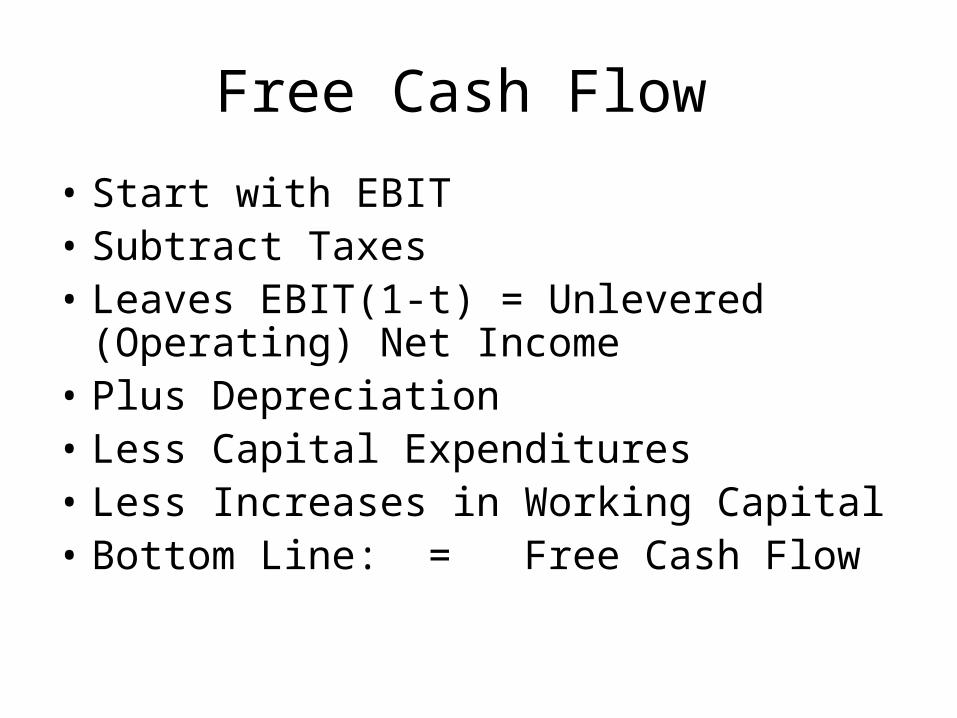

Free Cash Flow

• Start with EBIT • Subtract Taxes • Leaves EBIT(1-t) = Unlevered (Operating)

Net Income• Plus Depreciation • Less Capital Expenditures • Less Increases in Working Capital • Bottom Line: = Free Cash Flow

Example:Current Sales = $60 Cost of Goods Sold 25

Gross Profit 35Less Operating Expenses 9Less Depreciation 6

EBIT 20Less Income Tax Rate (@ 35%) 7

Operating (Unlevered) NI 13Plus Depreciation 6Less Capital Expenditures 2Less Increases in Working Capital 1Free Cash Flow 16

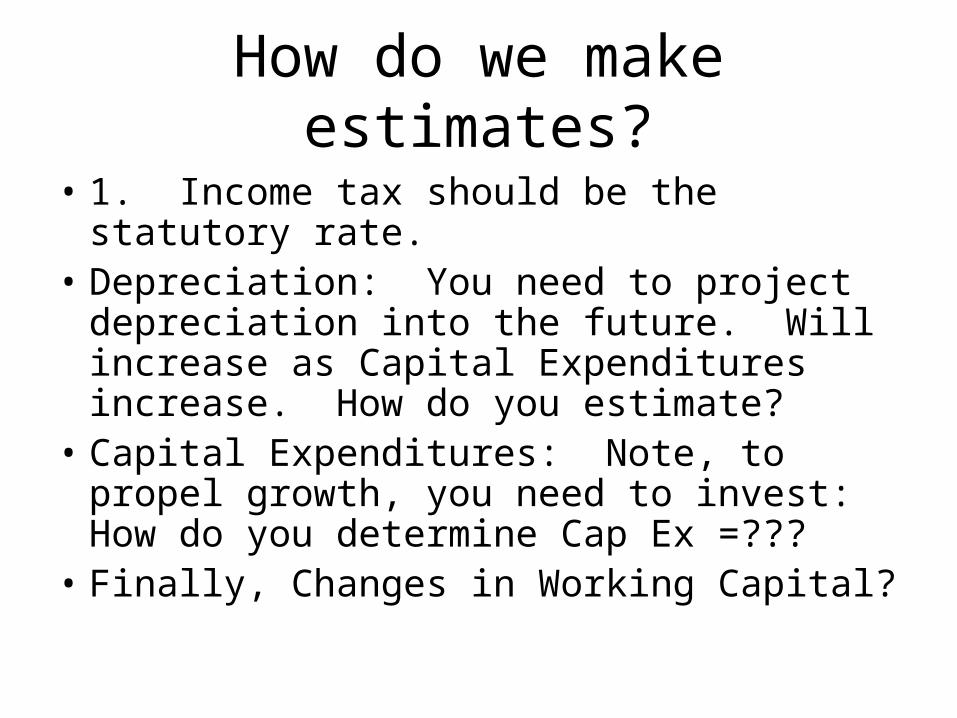

How do we make estimates?

• 1. Income tax should be the statutory rate. • Depreciation: You need to project

depreciation into the future. Will increase as Capital Expenditures increase. How do you estimate?

• Capital Expenditures: Note, to propel growth, you need to invest: How do you determine Cap Ex =???

• Finally, Changes in Working Capital?

Projections of Growth:

• Recall: growth depends on 2 variables:Retention rate = (1 – Payout ratio)

Return on Investments = Operating Income as a percentage of Book Value of Assets

• Consider Historical Rates as well:

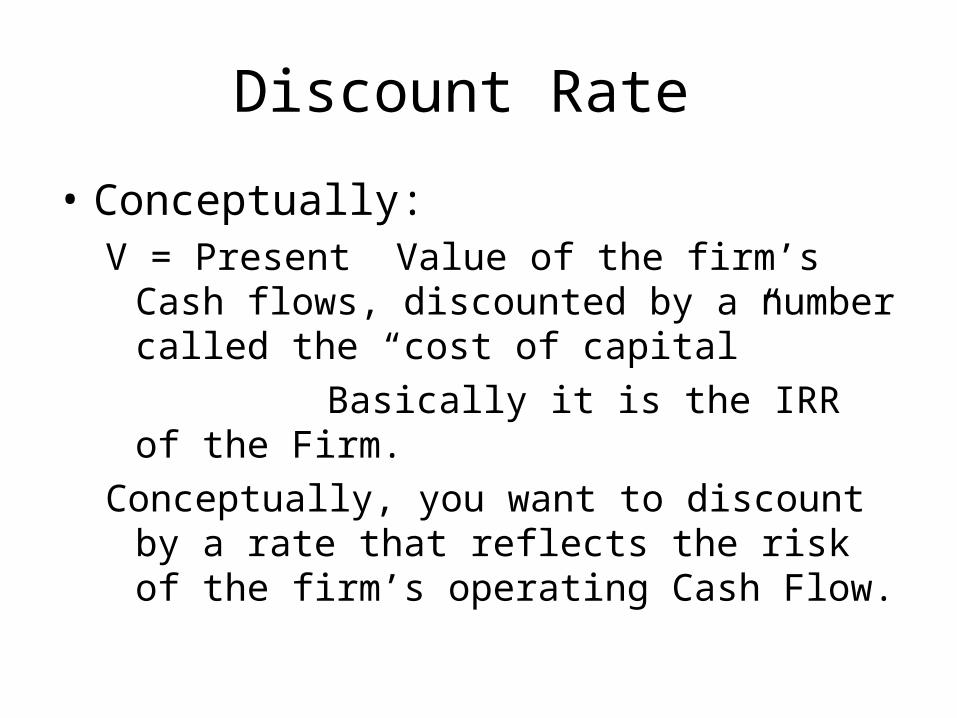

Discount Rate

• Conceptually:V = Present Value of the firm’s Cash flows,

discounted by a number called the “cost of capital”

Basically it is the IRR of the Firm.

Conceptually, you want to discount by a rate that reflects the risk of the firm’s operating Cash Flow.

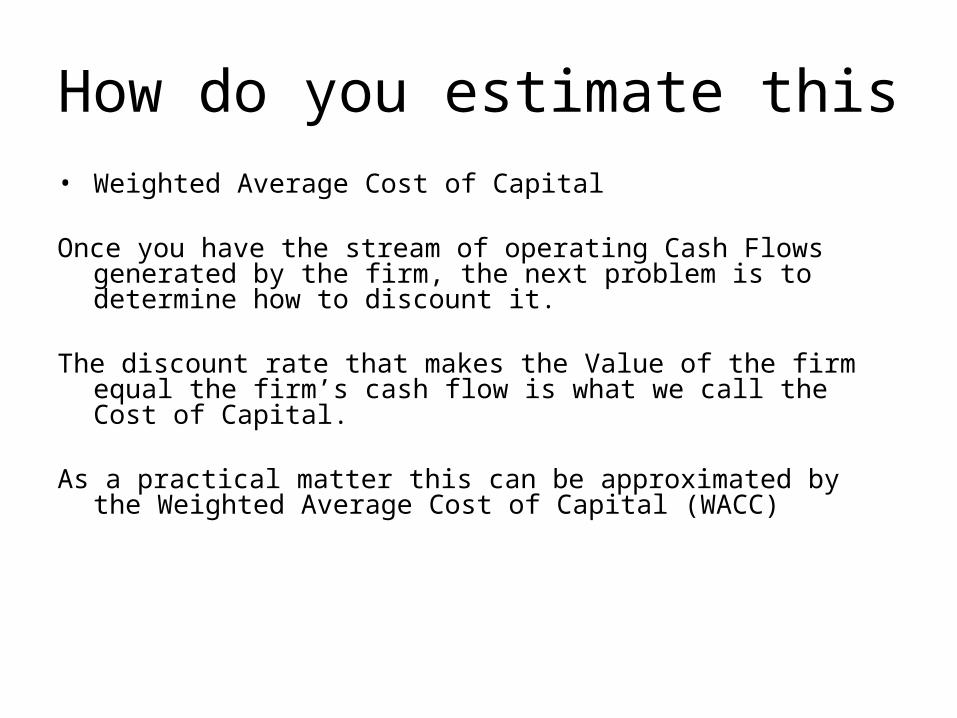

How do you estimate this• Weighted Average Cost of Capital

Once you have the stream of operating Cash Flows generated by the firm, the next problem is to determine how to discount it.

The discount rate that makes the Value of the firm equal the firm’s cash flow is what we call the Cost of Capital.

As a practical matter this can be approximated by the Weighted Average Cost of Capital (WACC)

WACC• The WACC is defined as:

rWACC = rE X (E/(E+D)) + rD(1-t) X (D/(E+D))

The weighted average of the (after tax) cost of the component securities issued by the firm, weighted by the proportion of those securities issued by the firm.

rE is the required return to the equity of the firm rD is the required return to the debt of the firm D is the (market value) of the debt issued by the firm E is the market value of the equity.t is the firms tax rate.

WACC Estimation

• Some of these variables are not easily estimated so we make some assumptions:

To estimate D use the Book value of the debt.

To estimate rD use the ratio of Total Interest payments to the total book value of the debt

To estimate rE use the Capital Asset Pricing Model