London, 14 November 2017 · PDF file2016 Growth to 2040 Sources of global electricity demand...

16

© OECD/IEA 2017 London, 14 November 2017

Transcript of London, 14 November 2017 · PDF file2016 Growth to 2040 Sources of global electricity demand...

© OECD/IEA 2017

London, 14 November 2017

© OECD/IEA 2017

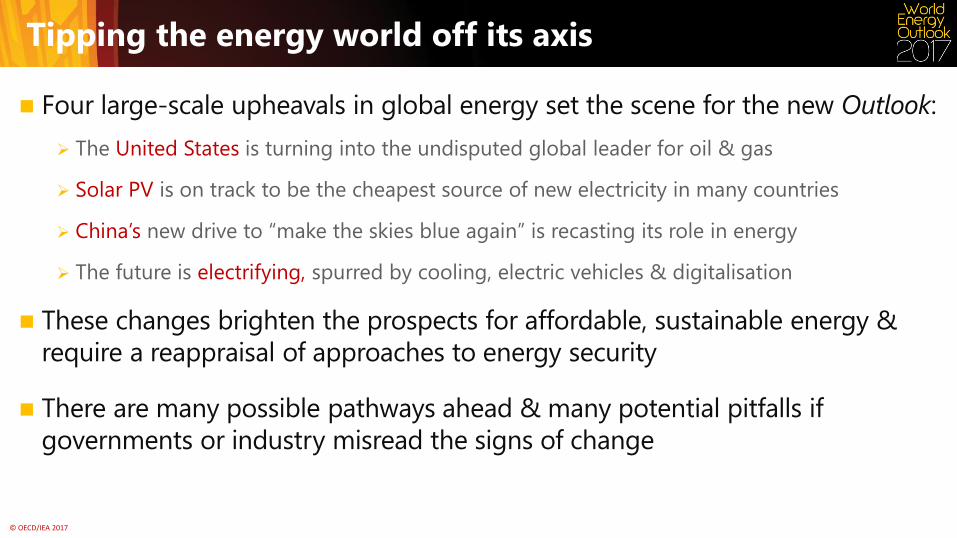

Tipping the energy world off its axis

Four large-scale upheavals in global energy set the scene for the new Outlook:

The United States is turning into the undisputed global leader for oil & gas

Solar PV is on track to be the cheapest source of new electricity in many countries

China’s new drive to “make the skies blue again” is recasting its role in energy

The future is electrifying, spurred by cooling, electric vehicles & digitalisation

These changes brighten the prospects for affordable, sustainable energy &

require a reappraisal of approaches to energy security

There are many possible pathways ahead & many potential pitfalls if

governments or industry misread the signs of change

© OECD/IEA 2017

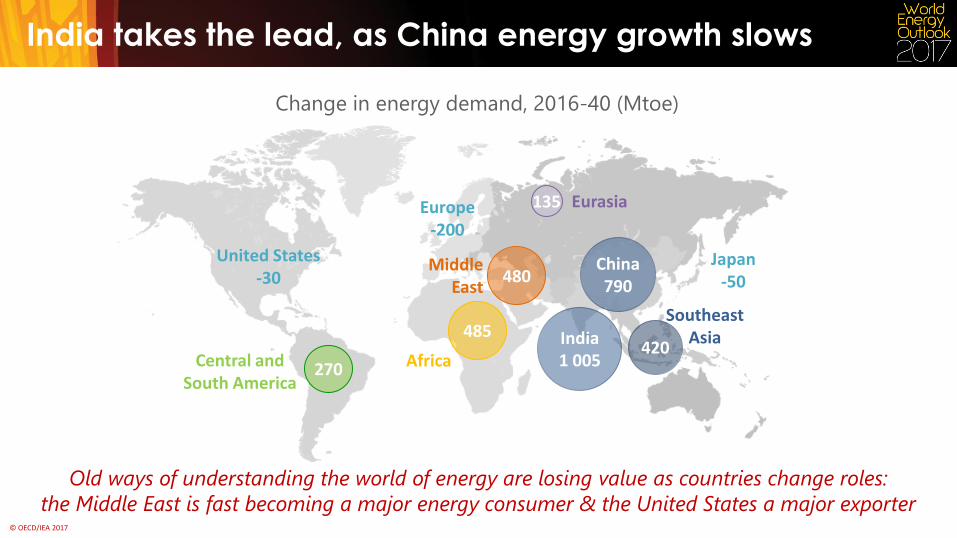

India takes the lead, as China energy growth slows

Change in energy demand, 2016-40 (Mtoe)

Old ways of understanding the world of energy are losing value as countries change roles:

India 1 005

420

Southeast Asia

China 790

United States -30

Japan -50

Europe -200

270 Central and South America

485

Africa

135 Eurasia

480 Middle

East

the Middle East is fast becoming a major energy consumer & the United States a major exporter

© OECD/IEA 2017

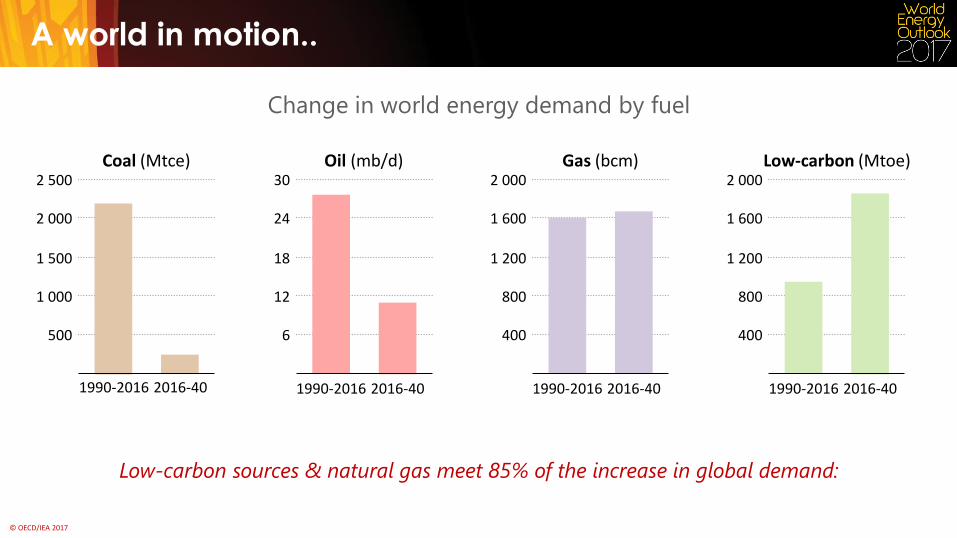

Low-carbon sources & natural gas meet 85% of the increase in global demand:

Change in world energy demand by fuel

Coal (Mtce)

500

1 000

1 500

2 000

2 500 Oil (mb/d)

6

12

18

24

30

1990-2016 2016-40

Gas (bcm)

400

800

1 200

1 600

2 000

1990-2016 2016-40

Low-carbon (Mtoe)

400

800

1 200

1 600

2 000

1990-2016 2016-40 1990-2016 2016-40

A world in motion..

© OECD/IEA 2017

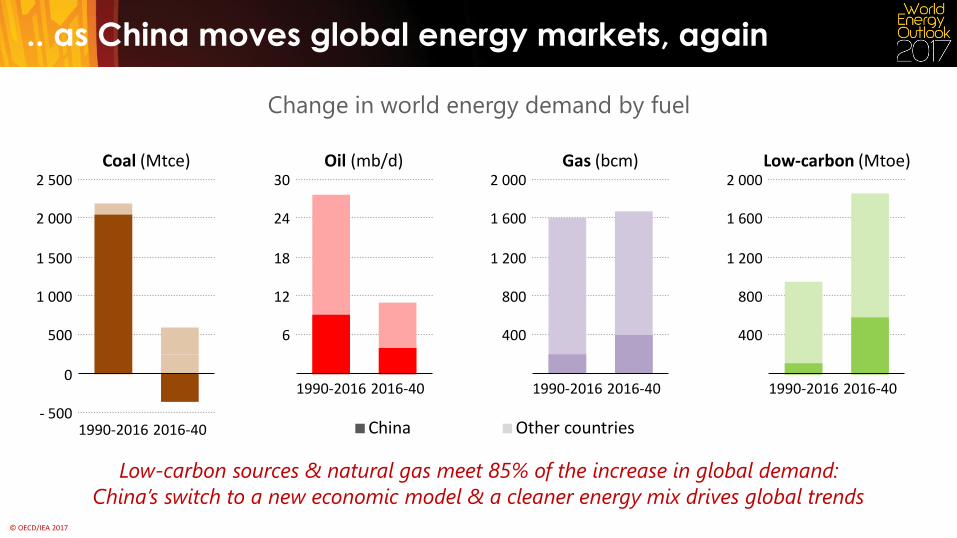

Change in world energy demand by fuel

Low-carbon sources & natural gas meet 85% of the increase in global demand:

Coal (Mtce)

0

500

1 000

1 500

2 000

2 500

- 500 1990-2016 2016-40

Oil (mb/d)

6

12

18

24

30

1990-2016 2016-40

Gas (bcm)

400

800

1 200

1 600

2 000

1990-2016 2016-40

Low-carbon (Mtoe)

400

800

1 200

1 600

2 000

1990-2016 2016-40

China’s switch to a new economic model & a cleaner energy mix drives global trends

Other countries China

.. as China moves global energy markets, again

© OECD/IEA 2017

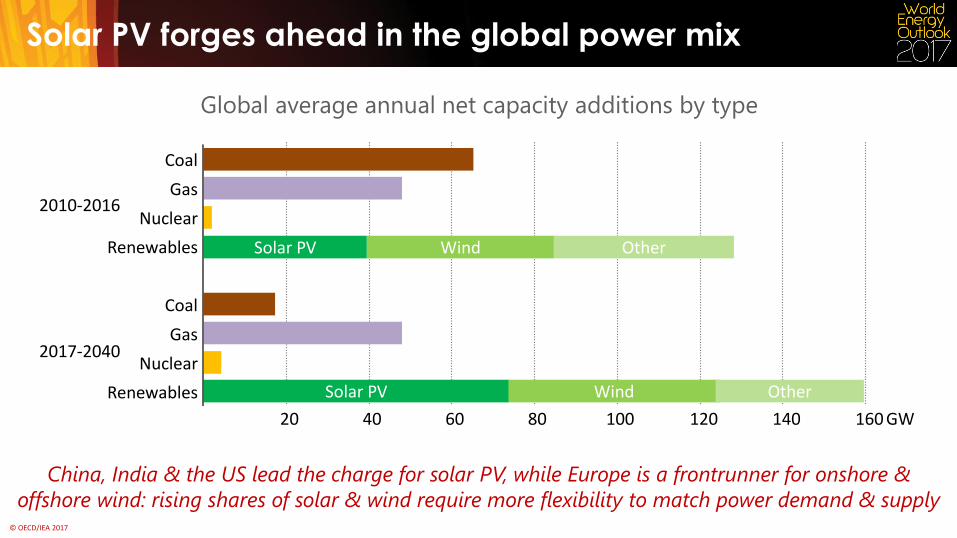

Solar PV forges ahead in the global power mix

Global average annual net capacity additions by type

China, India & the US lead the charge for solar PV, while Europe is a frontrunner for onshore &

offshore wind: rising shares of solar & wind require more flexibility to match power demand & supply

Renewables

Nuclear

Gas

Coal

Renewables

Nuclear

Gas

Coal

20 40 60 80 100 120 140 160 GW

2010-2016

2017-2040

Solar PV Wind

Solar PV Wind Other

Other

© OECD/IEA 2017

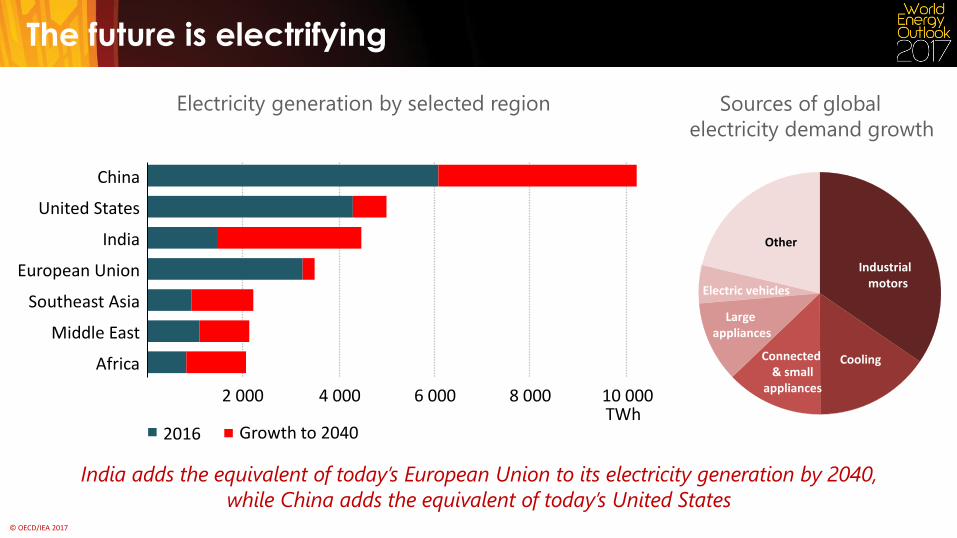

The future is electrifying

Electricity generation by selected region

India adds the equivalent of today’s European Union to its electricity generation by 2040,

Middle East

2 000 4 000 6 000 8 000 10 000

Africa

Southeast Asia

European Union

India

United States

China

TWh 2016 Growth to 2040

Sources of global

electricity demand growth

Industrial motors

Cooling

Large appliances

Connected & small

appliances

Electric vehicles

Other

while China adds the equivalent of today’s United States

© OECD/IEA 2017

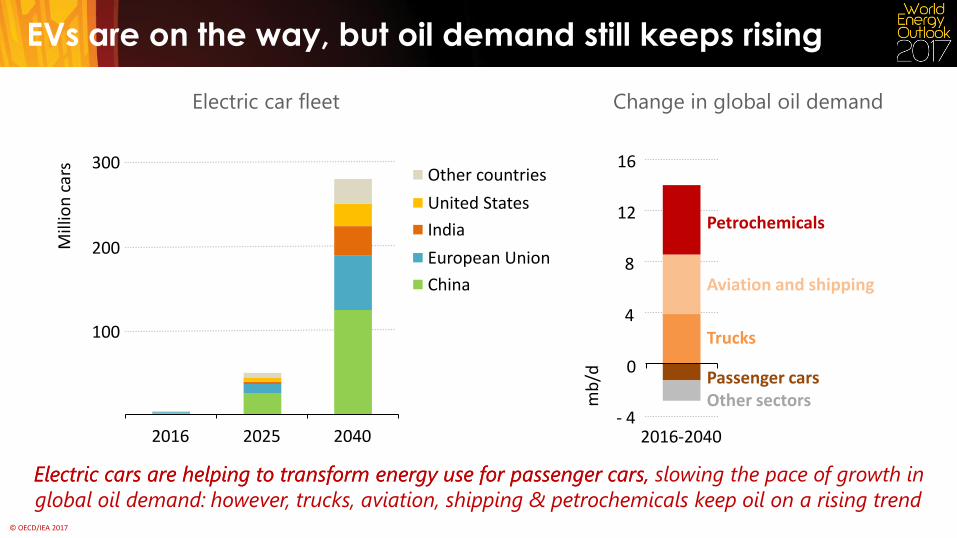

Electric cars are helping to transform energy use for passenger cars, slowing the pace of growth in

global oil demand: however, trucks, aviation, shipping & petrochemicals keep oil on a rising trend

Electric cars are helping to transform energy use for passenger cars, slowing the pace of growth in

global oil demand: however, trucks, aviation, shipping & petrochemicals keep oil on a rising trend

however, trucks, aviation, shipping & petrochemicals keep oil on a rising trend

EVs are on the way, but oil demand still keeps rising

Electric car fleet

100

200

300

2016 2025 2040

Mill

ion

car

s

Other countries

United States

India

European Union

China

Passenger cars Other sectors

Change in global oil demand

4

8

12

16

Petrochemicals

Aviation and shipping

Trucks

mb

/d

- 4 2016-2040

0

© OECD/IEA 2017

25

30

35

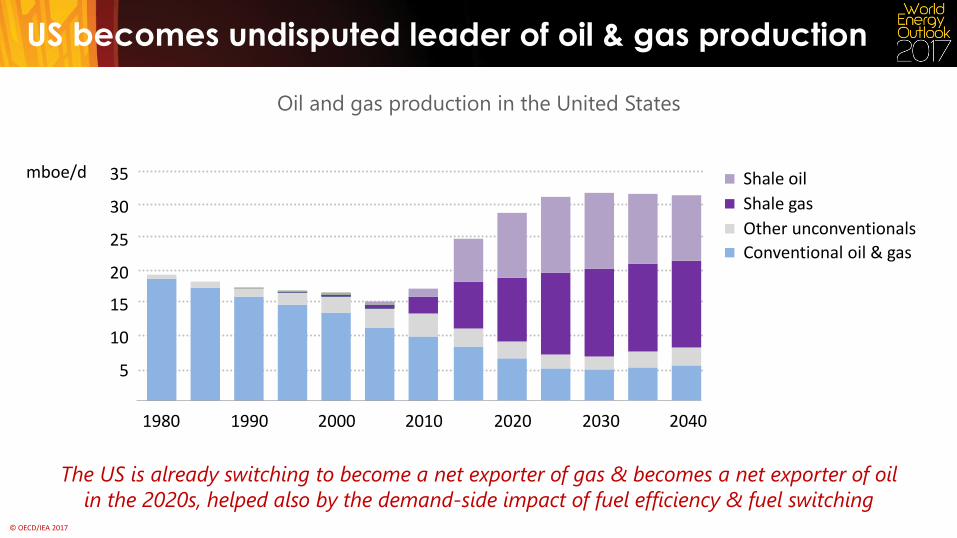

US becomes undisputed leader of oil & gas production

Oil and gas production in the United States

The US is already switching to become a net exporter of gas & becomes a net exporter of oil

in the 2020s, helped also by the demand-side impact of fuel efficiency & fuel switching

5

10

15

20

1980 1990 2000 2010 2020 2030 2040

mboe/d Shale oil

Shale gas

Other unconventionals

Conventional oil & gas

© OECD/IEA 2017

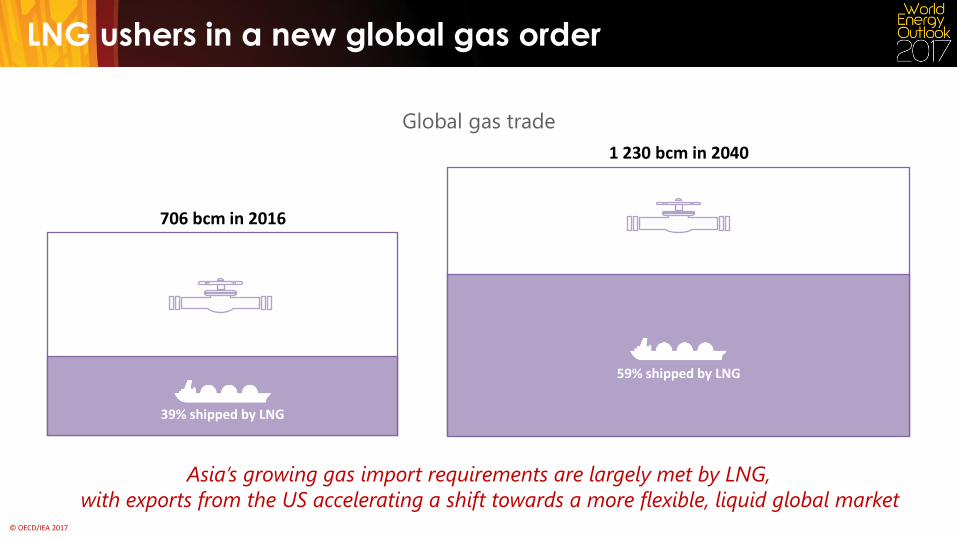

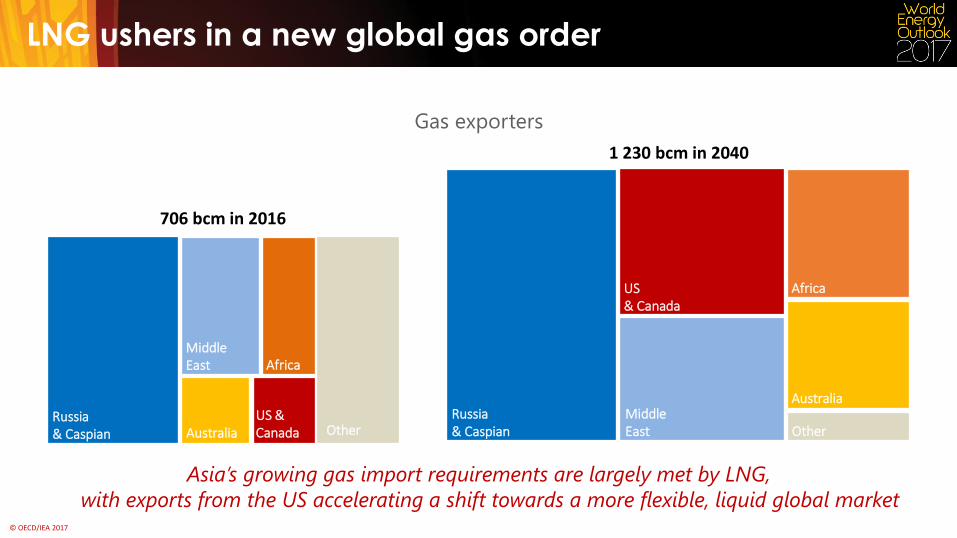

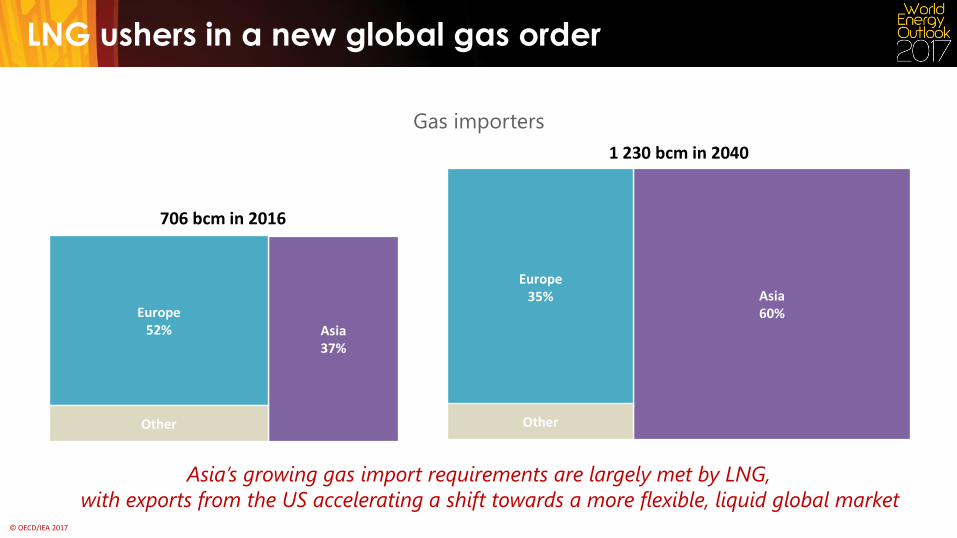

706 bcm in 2016

Asia’s growing gas import requirements are largely met by LNG,

with exports from the US accelerating a shift towards a more flexible, liquid global market

LNG ushers in a new global gas order

Global gas trade

39% shipped by LNG

1 230 bcm in 2040

59% shipped by LNG

© OECD/IEA 2017

706 bcm in 2016

Asia’s growing gas import requirements are largely met by LNG,

with exports from the US accelerating a shift towards a more flexible, liquid global market

LNG ushers in a new global gas order

1 230 bcm in 2040

Australia Russia & Caspian

Middle East

Other

Africa

US & Canada

Australia Russia & Caspian

Middle East Other

Africa US & Canada

Gas exporters

© OECD/IEA 2017

706 bcm in 2016

Global gas trade

Asia’s growing gas import requirements are largely met by LNG,

with exports from the US accelerating a shift towards a more flexible, liquid global market

LNG ushers in a new global gas order

Gas exporters Gas importers

1 230 bcm in 2040

Asia 37%

Europe 52%

Other

Asia 60%

Europe 35%

Other

© OECD/IEA 2017

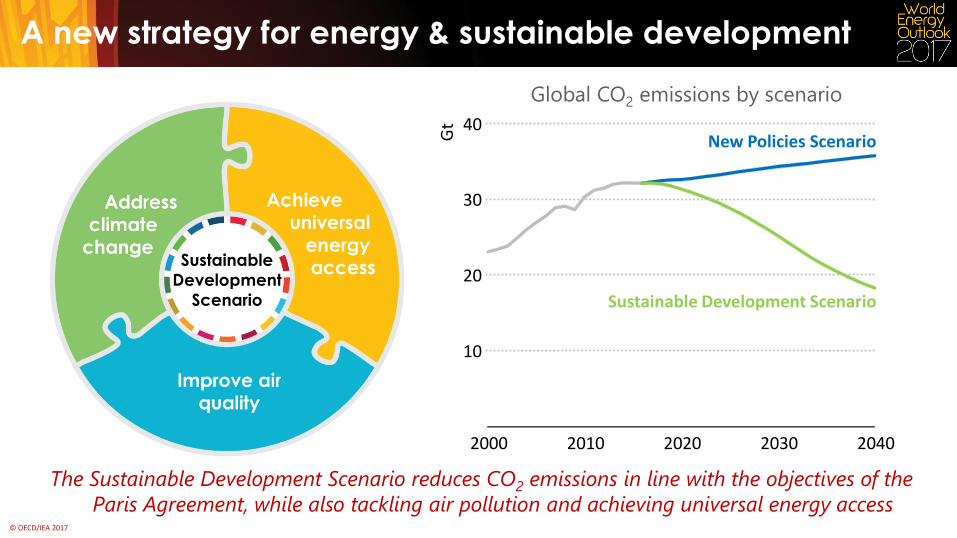

A new strategy for energy & sustainable development

Sustainable

Development

Scenario

The Sustainable Development Scenario reduces CO2 emissions in line with the objectives of the

Paris Agreement, while also tackling air pollution and achieving universal energy access

New Policies Scenario

Sustainable Development Scenario

Global CO2 emissions by scenario

10

20

30

40

2000 2010 2020 2030 2040 G

t

© OECD/IEA 2017

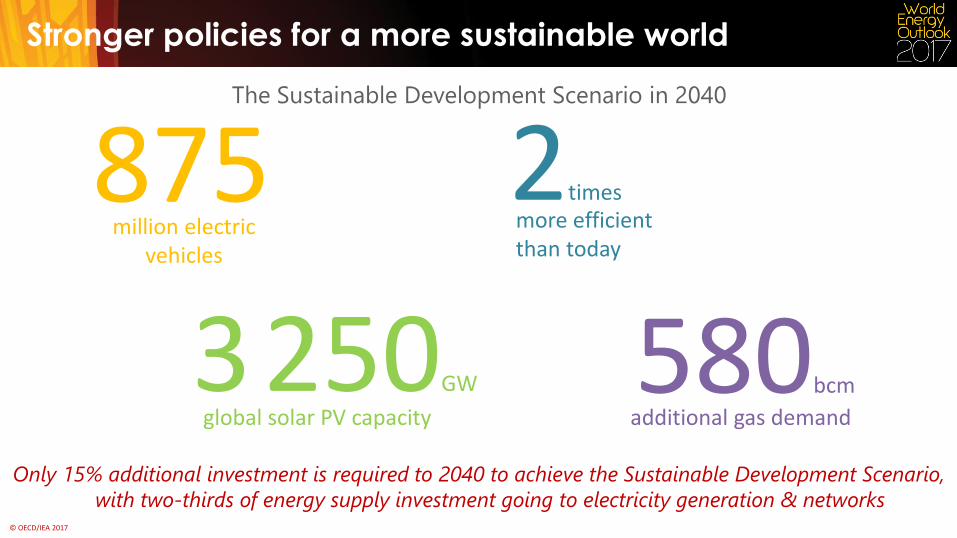

Stronger policies for a more sustainable world

580bcm additional gas demand

2times more efficient than today

3 250GW

global solar PV capacity

875 million electric

vehicles

Only 15% additional investment is required to 2040 to achieve the Sustainable Development Scenario,

with two-thirds of energy supply investment going to electricity generation & networks

The Sustainable Development Scenario in 2040

© OECD/IEA 2017

Conclusions

The oil & gas boom in the United States is shaking up the established order, with major

implications for markets, trade flows, investment & energy security

The versatility of natural gas means that it is well placed to grow, but it cannot afford

price spikes or uncertainty over methane leaks

China continues to shape global trends, but in new ways as its “energy revolution”

drives cost reductions for a wide range of clean energy technologies

Our strategy for sustainable energy shows that concerted action to address climate

change is fully compatible with global goals on universal access & air quality

Electrification & digitalisation are the future for many parts of the global energy system,

creating new opportunities but also risks that policy makers have to address

© OECD/IEA 2017

iea.org/weo