Lecture 1-Financial Markets and Institutions Updated 11-23-13

26

Financial Markets and Institutions Case study: Financial Crisis - 2008

-

Upload

lingaraj-subudhi -

Category

Documents

-

view

15 -

download

2

description

brife about financial market

Transcript of Lecture 1-Financial Markets and Institutions Updated 11-23-13

Financial Markets and Institutions

Case study: Financial Crisis - 2008

Attendance and self‐study

It is for your benefit to attend all the classes. Minimum 80% attendance is expected. Lecture may not be repeated if it has been voluntarily missed by a candidate without any unavoidable reason.

Minimum 3 hours of self study is encouraged for every lecture. Your motivation and self study is the key to your learning experience.

Suggestions Everyone attending the lecture has to do it: a) Watch the video: http://vimeo.com/3261363 b) Read all the topics under "USA financial crisis" from: http://2008financialcrisis.umwblogs.org/analysis/.

Videos to watch: Relationship between bond prices and interest rates Trading Basics How the Markets Work Please read the web chapter on Financial markets and institutions.. Please study continuous compounding and materials regarding the present value of money.

Hari

Typewritten Text

http://wps.aw.com/wps/media/objects/5448/5579249/FinancialMarketsandInstitutions.pdf

What is a Market Definition: Congregation of buyers and sellers

Physical - Bazaar Electronic trading

Real assets vs. financial assets. Main street vs. wall street

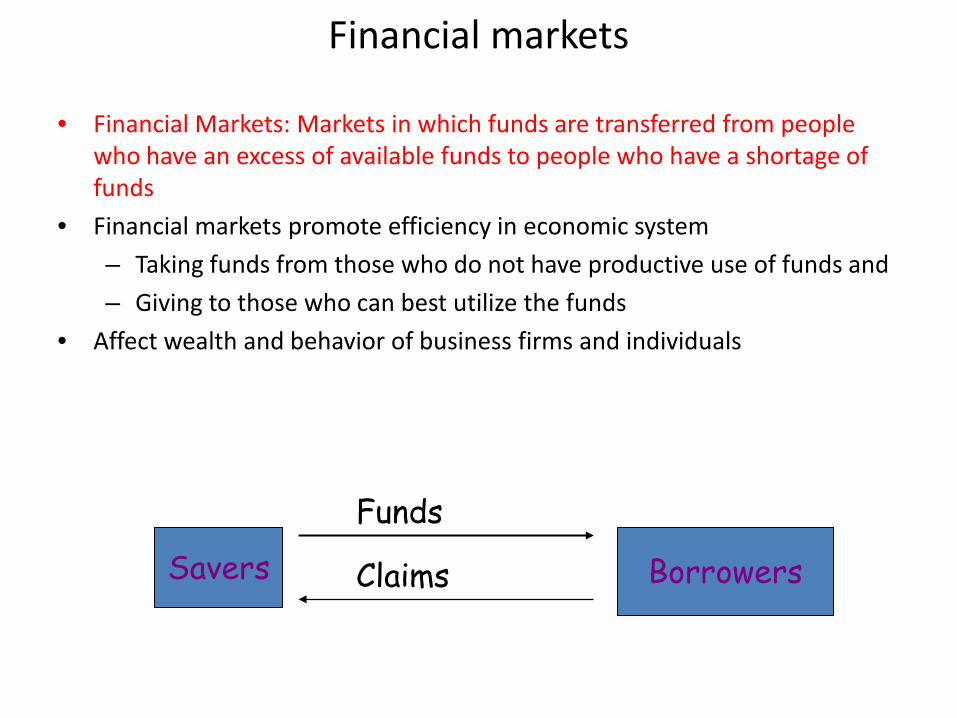

• Financial Markets: Markets in which funds are transferred from people who have an excess of available funds to people who have a shortage of funds

• Financial markets promote efficiency in economic system – Taking funds from those who do not have productive use of funds and – Giving to those who can best utilize the funds

• Affect wealth and behavior of business firms and individuals

Financial markets

Savers Borrowers Savers Borrowers

Funds

Claims

• Interest rates: An interest rate is the cost of borrowing or the price paid for the rental of funds (usually expressed as a percentage of the rental of 100 per year) – Interest rates affect both individuals’ and corporations’ decisions to

spend or save • A stock: A share of ownership in a corporation. It is a security, that is a claim

on the earnings and assets of the corporation. The stock market is where stocks are traded. – A stock index is a measure of performance of well-defined collection of

stocks. • Commodity markets are markets where raw or primary products are

exchanged. E.g., crude oil, gold markets

Important definitions

Hari

Typewritten Text

Below are some of the good proxies for risk free interest rate(it's subjective) a) Return on federal government securities b) Interbank exchange loan rates c) Interest rates charged by banks.

Hari

Typewritten Text

How would you study relationships between commodity markets and equity markets? Or relationship between risk free interest rates and equity markets.

Hari

Typewritten Text

Introduce Time Series modeling here.

Hari

Stamp

Hari

Stamp

Bond: A debt security that promises to make payments periodically for a specified period of time. The bond market is where bonds are traded.

– It enables corporations or governments to borrow to finance activities – It is where interest rates are determined

Important definitions

Derivatives: A financial asset whose value is derived from the value of an underlying asset.

– E.g. Option to buy a stock or a security. – Used to hedge risks and speculate.

A foreign exchange market is a market where funds are converted from one currency to another •To transfer funds from one country to another for trade

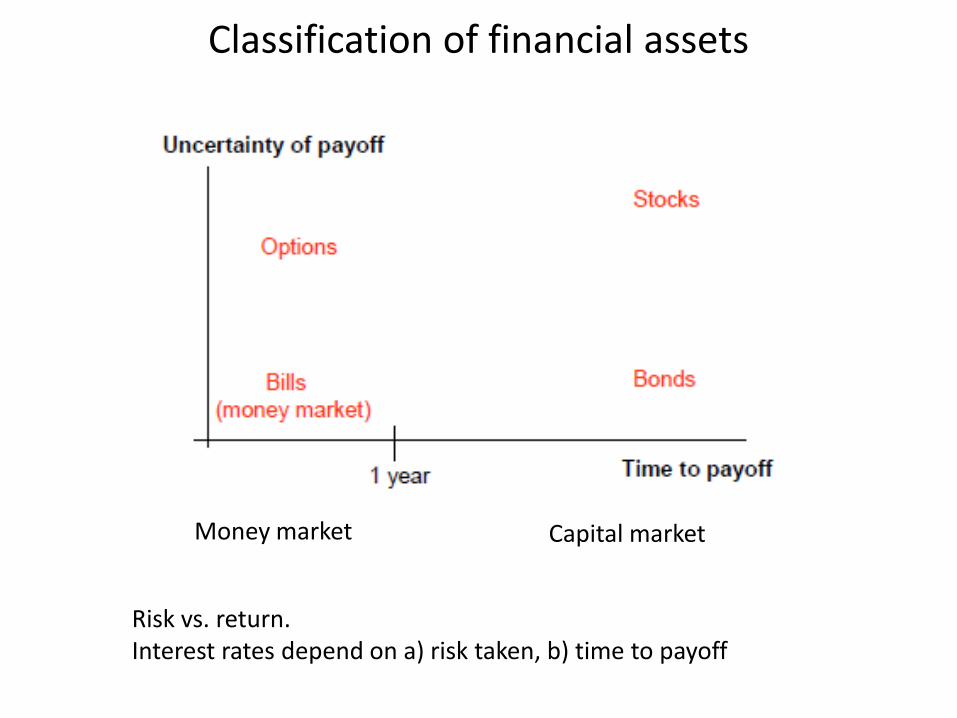

Classification of financial assets

Money market Capital market

Risk vs. return. Interest rates depend on a) risk taken, b) time to payoff

Hari

Stamp

Hari

Typewritten Text

Orders: 1) Long (Buy) 2) Short (Sell)

Hari

Typewritten Text

Hari

Typewritten Text

3) Sell short 4) Buy-to-cover

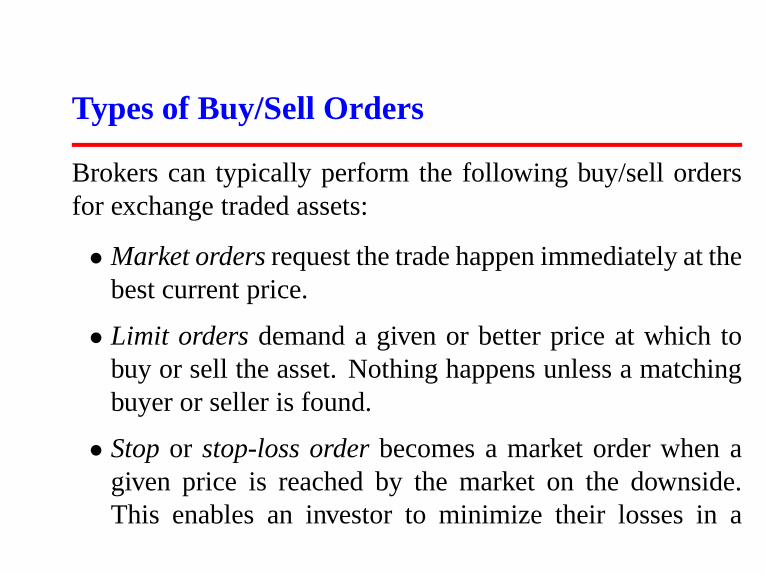

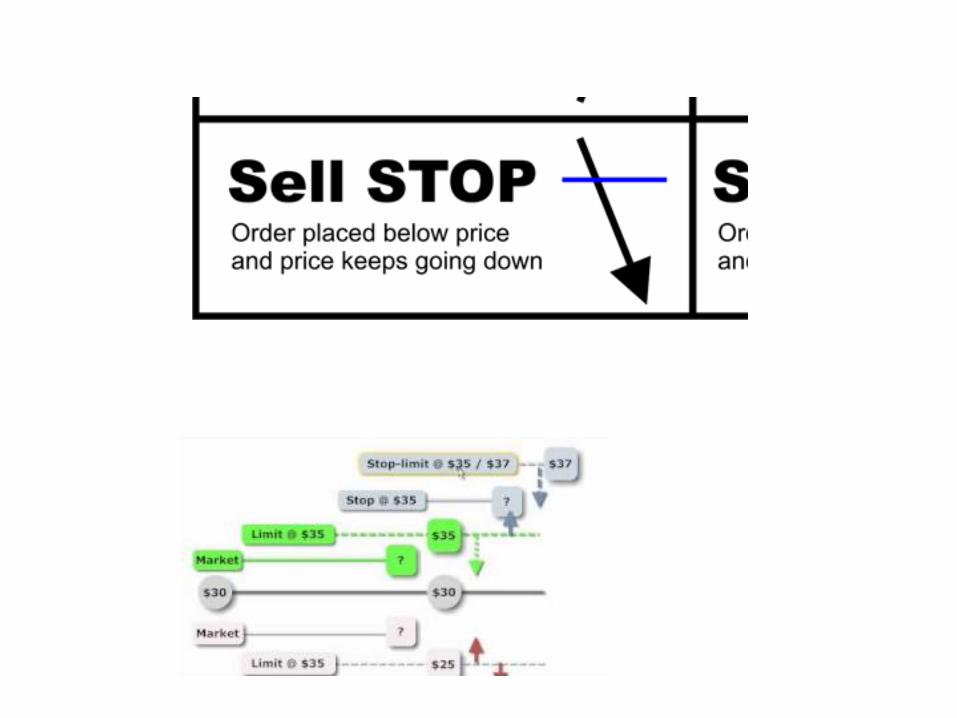

Types of Buy/Sell Orders

Brokers can typically perform the following buy/sell ordersfor exchange traded assets:

• Market orders request the trade happen immediately at thebest current price.

• Limit orders demand a given or better price at which tobuy or sell the asset. Nothing happens unless a matchingbuyer or seller is found.

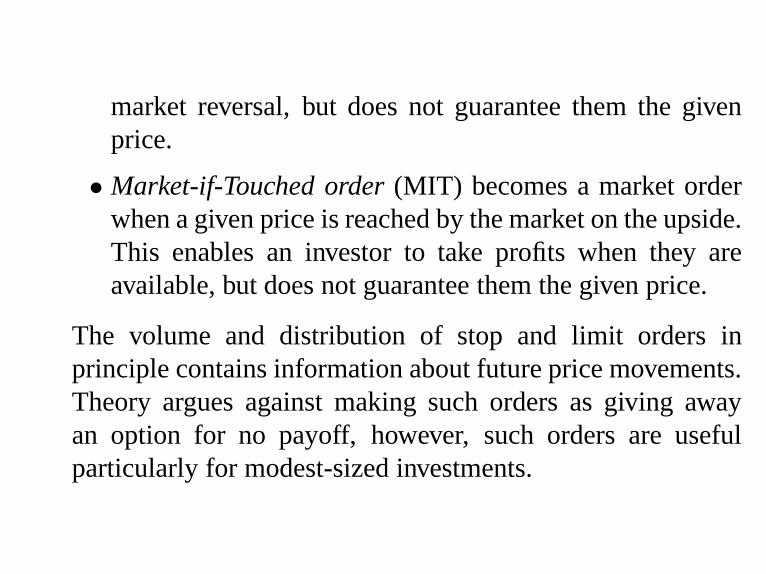

• Stop or stop-loss order becomes a market order when agiven price is reached by the market on the downside.This enables an investor to minimize their losses in a

market reversal, but does not guarantee them the givenprice.

• Market-if-Touched order (MIT) becomes a market orderwhen a given price is reached by the market on the upside.This enables an investor to take profits when they areavailable, but does not guarantee them the given price.

The volume and distribution of stop and limit orders inprinciple contains information about future price movements.Theory argues against making such orders as giving awayan option for no payoff, however, such orders are usefulparticularly for modest-sized investments.

Hari

Stamp

Hari

Stamp

Hari

Typewritten Text

Types of BUY/SELL orders

Hari

Stamp

Hari

Stamp

Hari

Typewritten Text

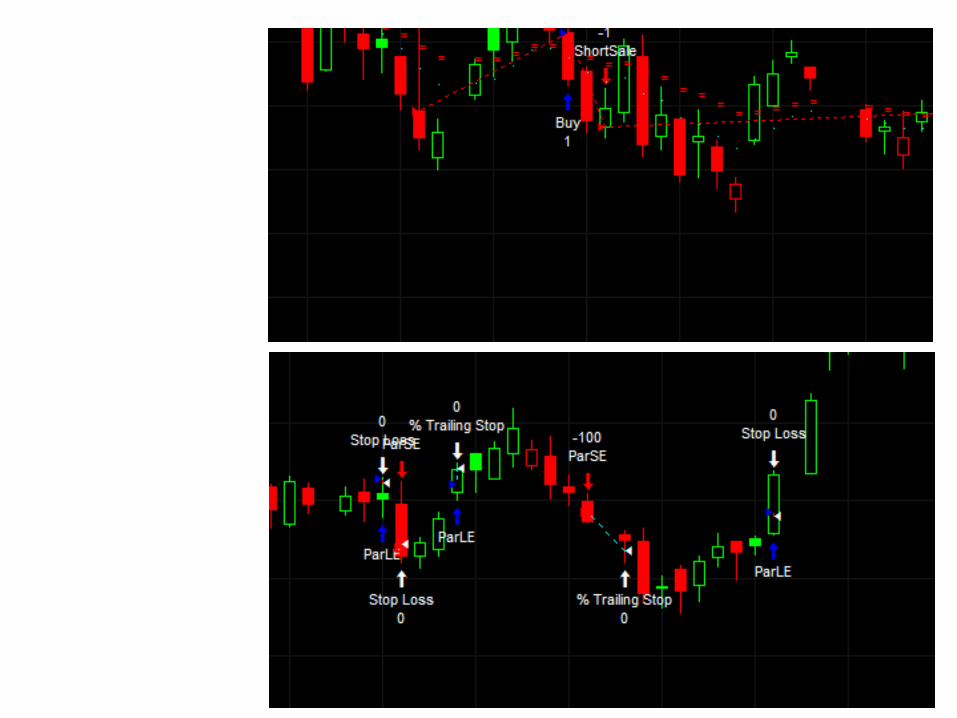

Tradestation BUY/SELL orders

Hari

Typewritten Text

Stop-loss Trailing stop Profit target

Hari

Stamp

Hari

Typewritten Text

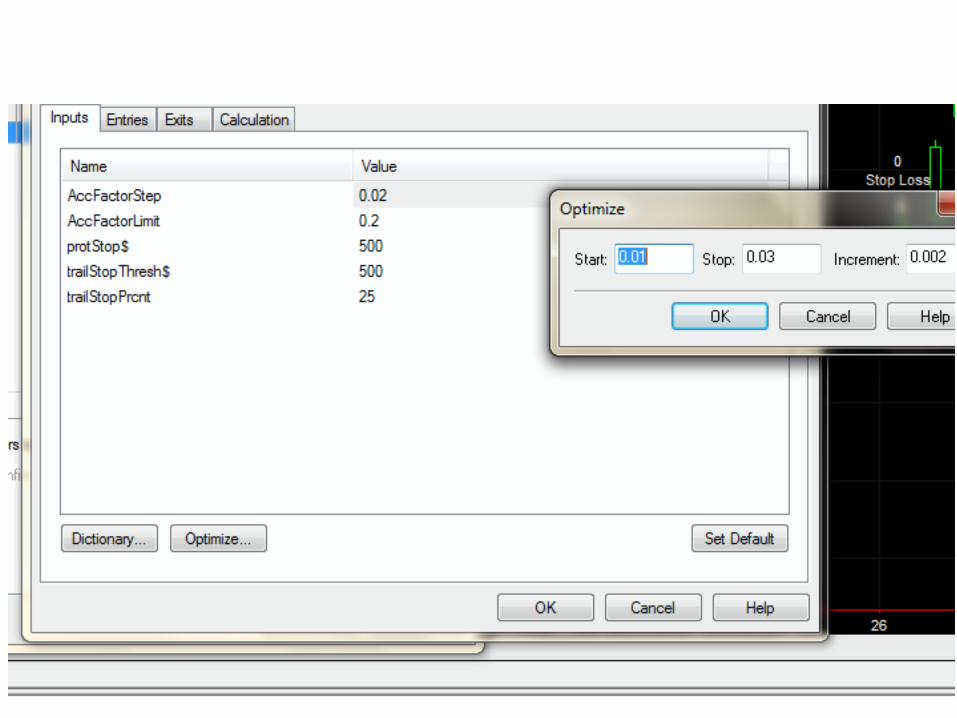

Strategy optimisation tool in TradeStation.

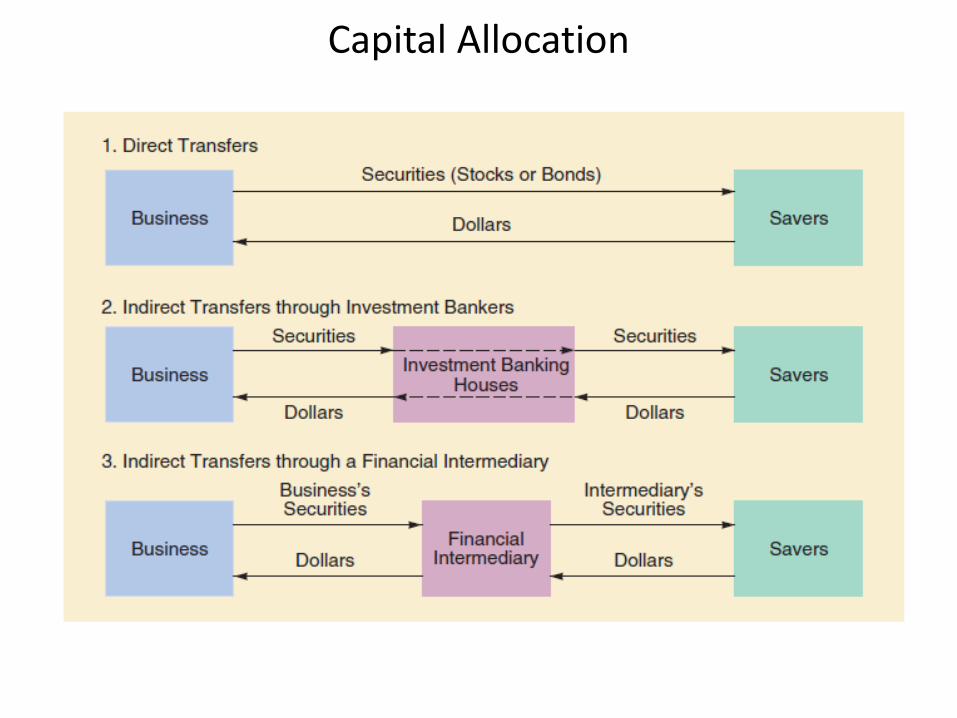

Capital Allocation

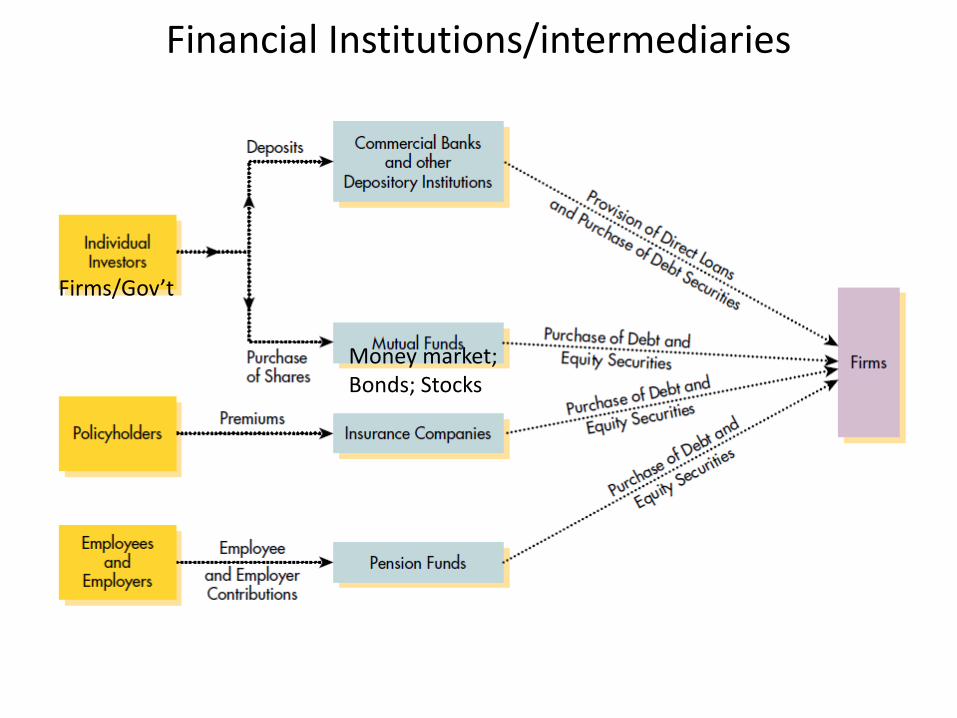

Financial Institutions/intermediaries

Firms/Gov’t

Money market; Bonds; Stocks

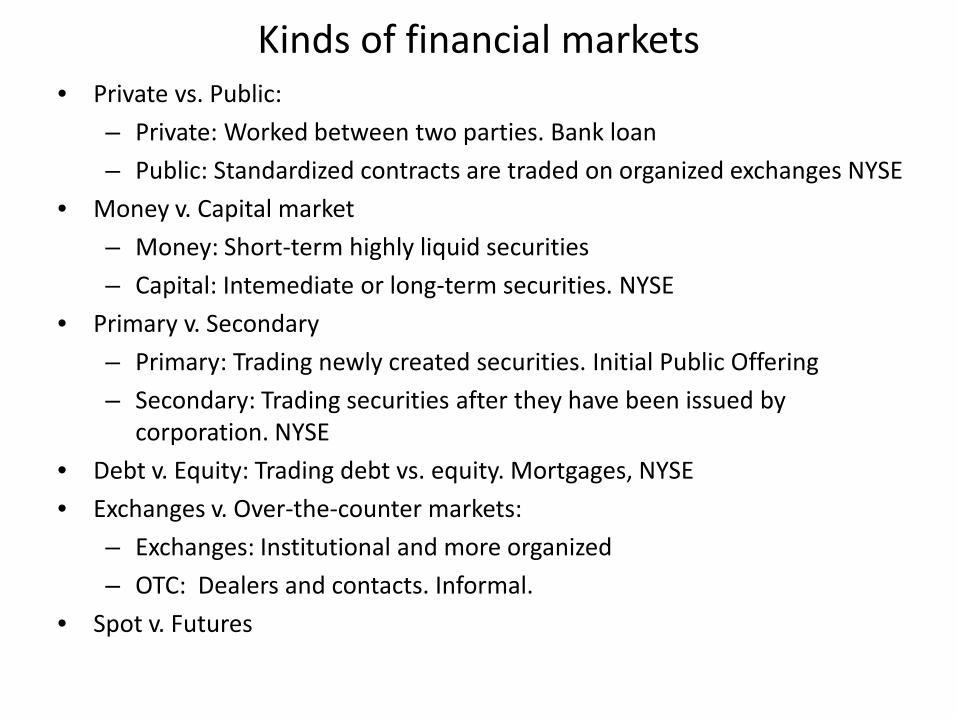

Kinds of financial markets • Private vs. Public:

– Private: Worked between two parties. Bank loan – Public: Standardized contracts are traded on organized exchanges NYSE

• Money v. Capital market – Money: Short-term highly liquid securities – Capital: Intemediate or long-term securities. NYSE

• Primary v. Secondary – Primary: Trading newly created securities. Initial Public Offering – Secondary: Trading securities after they have been issued by

corporation. NYSE • Debt v. Equity: Trading debt vs. equity. Mortgages, NYSE • Exchanges v. Over-the-counter markets:

– Exchanges: Institutional and more organized – OTC: Dealers and contacts. Informal.

• Spot v. Futures

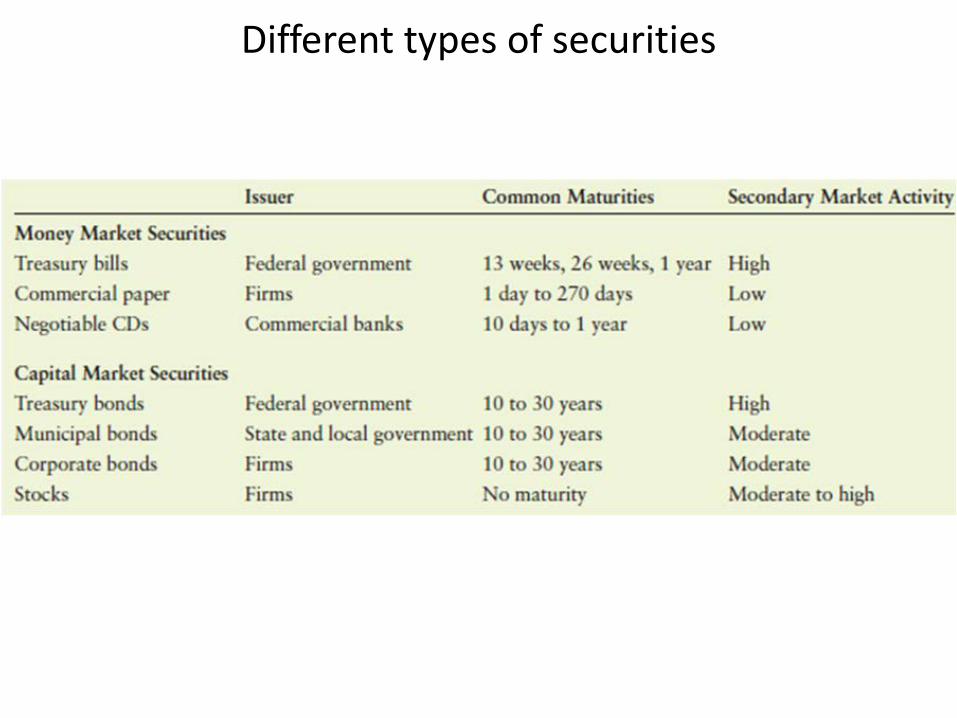

Different types of securities

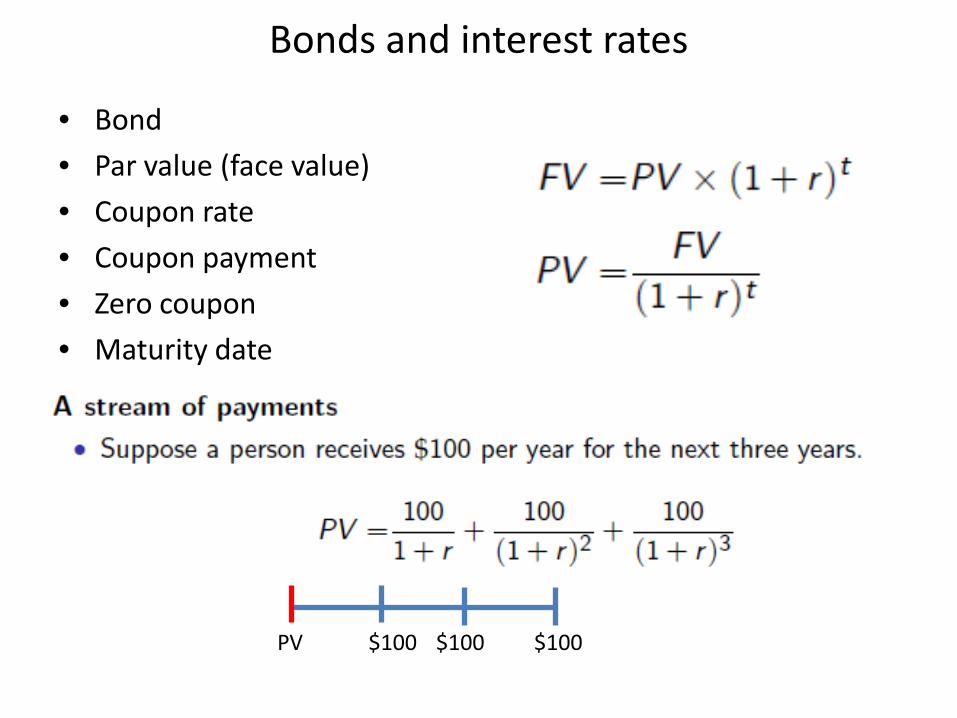

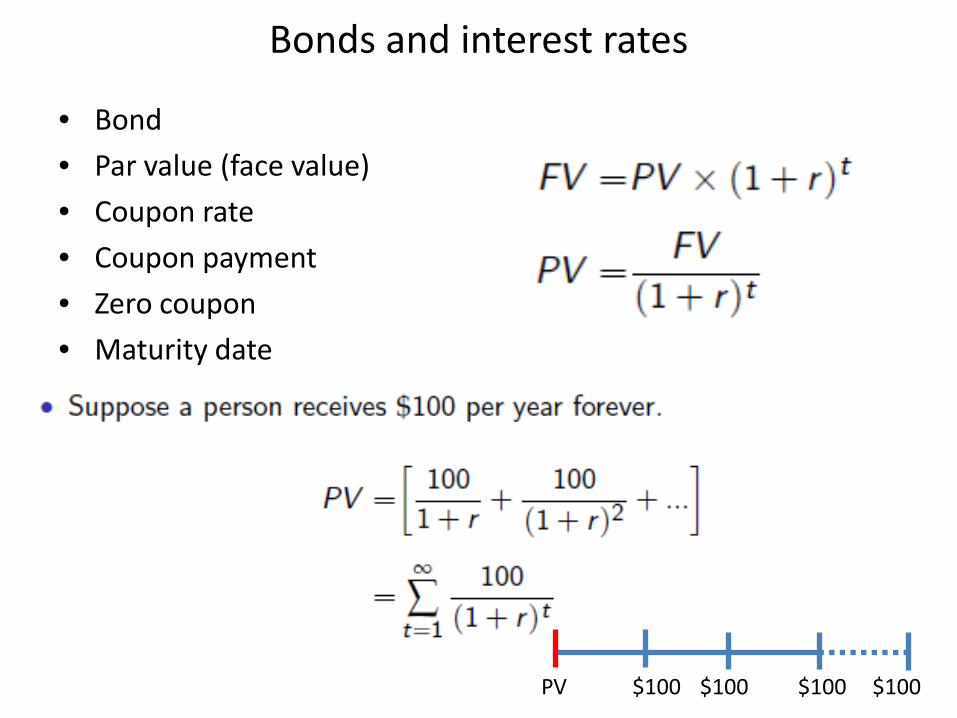

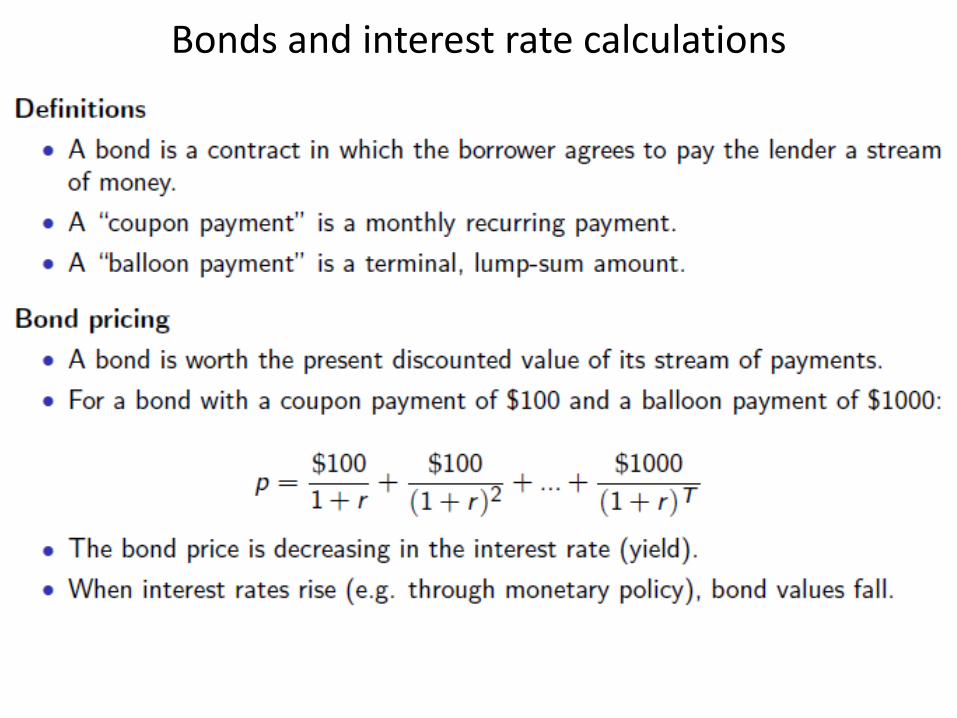

Bonds and interest rates

• Bond • Par value (face value) • Coupon rate • Coupon payment • Zero coupon • Maturity date

PV $100 $100 $100

Bonds and interest rates

• Bond • Par value (face value) • Coupon rate • Coupon payment • Zero coupon • Maturity date

PV $100 $100 $100 $100

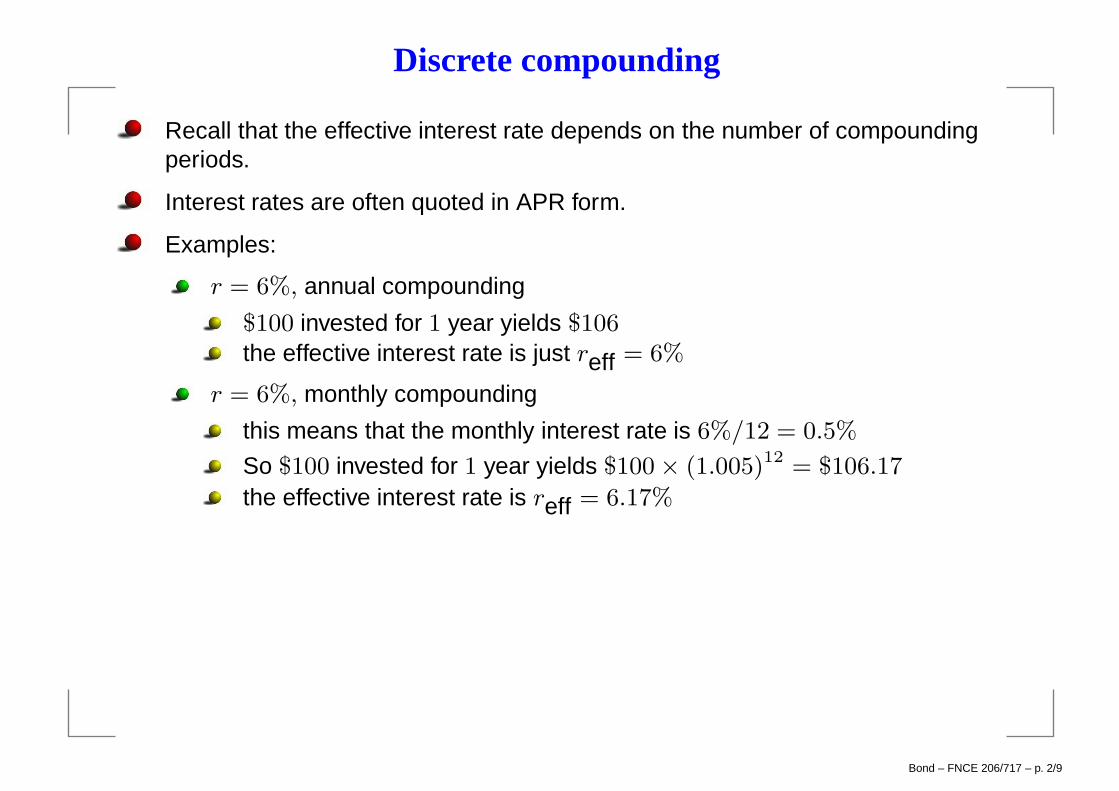

Discrete compounding

Recall that the effective interest rate depends on the number of compoundingperiods.

Interest rates are often quoted in APR form.

Examples:

r = 6%, annual compounding

$100 invested for 1 year yields $106the effective interest rate is just reff = 6%

r = 6%, monthly compounding

this means that the monthly interest rate is 6%/12 = 0.5%

So $100 invested for 1 year yields $100 × (1.005)12 = $106.17

the effective interest rate is reff = 6.17%

Bond – FNCE 206/717 – p. 2/9

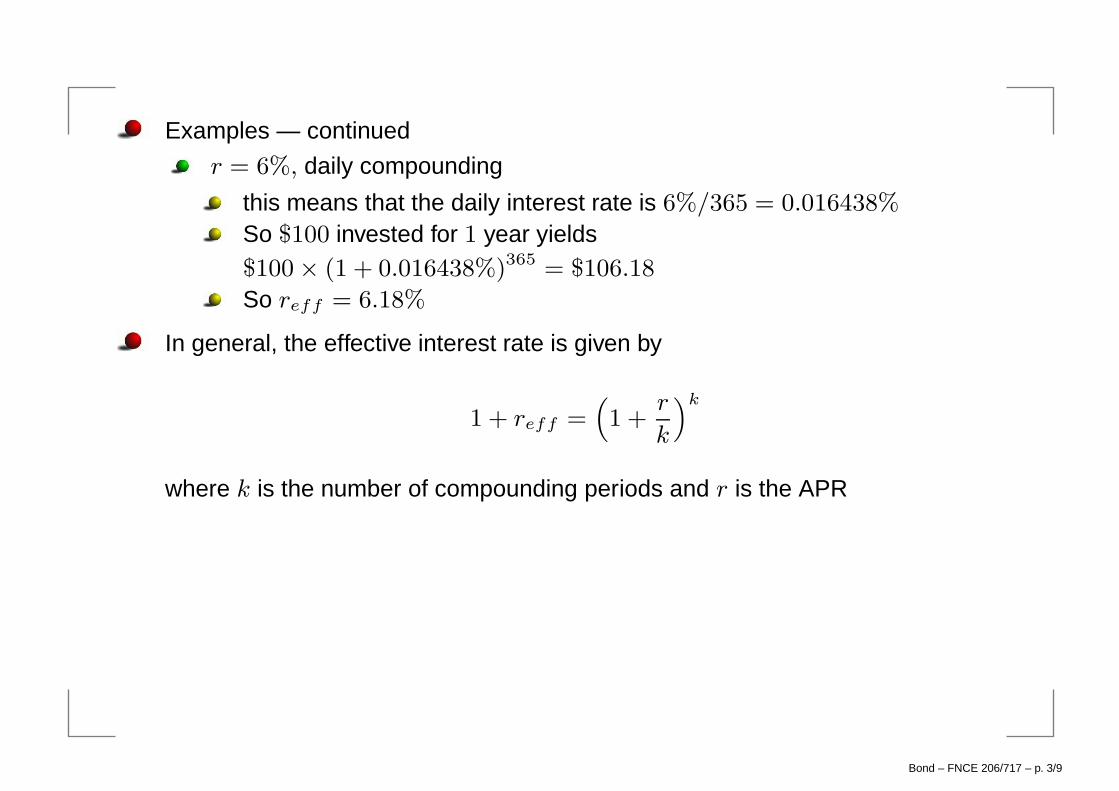

Examples — continued

r = 6%, daily compounding

this means that the daily interest rate is 6%/365 = 0.016438%

So $100 invested for 1 year yields$100 × (1 + 0.016438%)365 = $106.18

So reff = 6.18%

In general, the effective interest rate is given by

1 + reff =(

1 +r

k

)k

where k is the number of compounding periods and r is the APR

Bond – FNCE 206/717 – p. 3/9

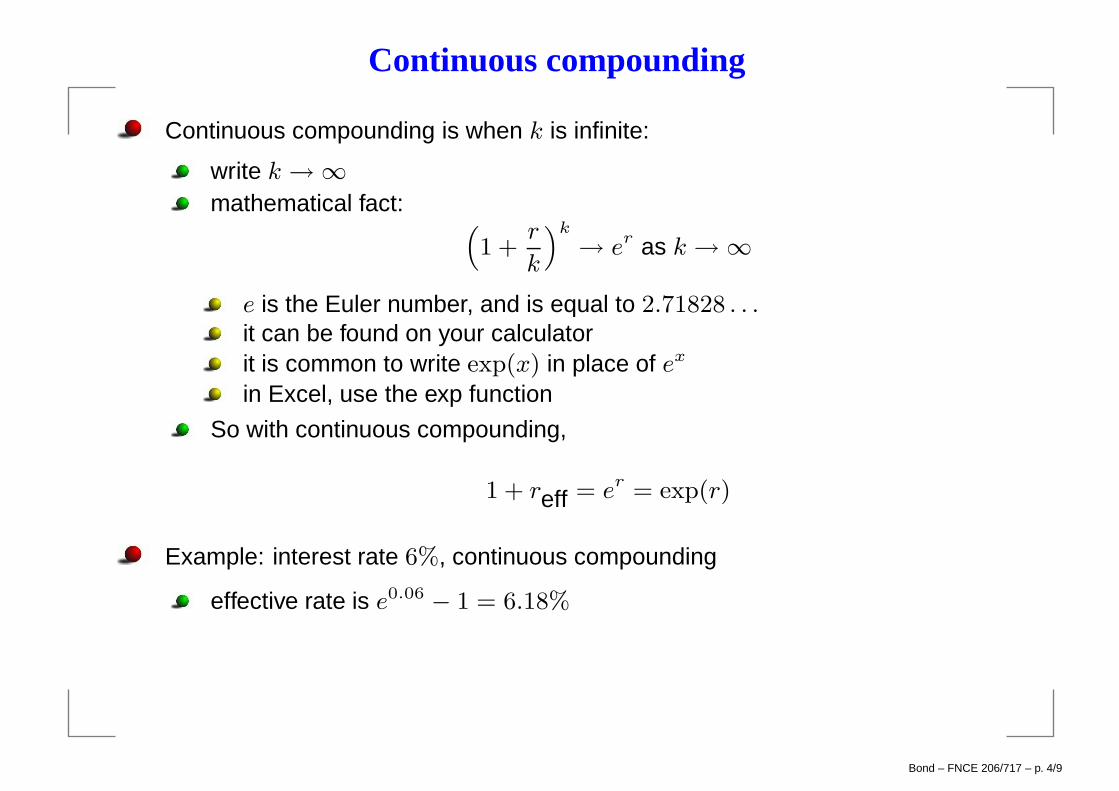

Continuous compounding

Continuous compounding is when k is infinite:

write k → ∞

mathematical fact:(

1 +r

k

)k

→ er as k → ∞

e is the Euler number, and is equal to 2.71828 . . .it can be found on your calculatorit is common to write exp(x) in place of ex

in Excel, use the exp function

So with continuous compounding,

1 + reff = er = exp(r)

Example: interest rate 6%, continuous compounding

effective rate is e0.06− 1 = 6.18%

Bond – FNCE 206/717 – p. 4/9

Bonds and interest rate calculations

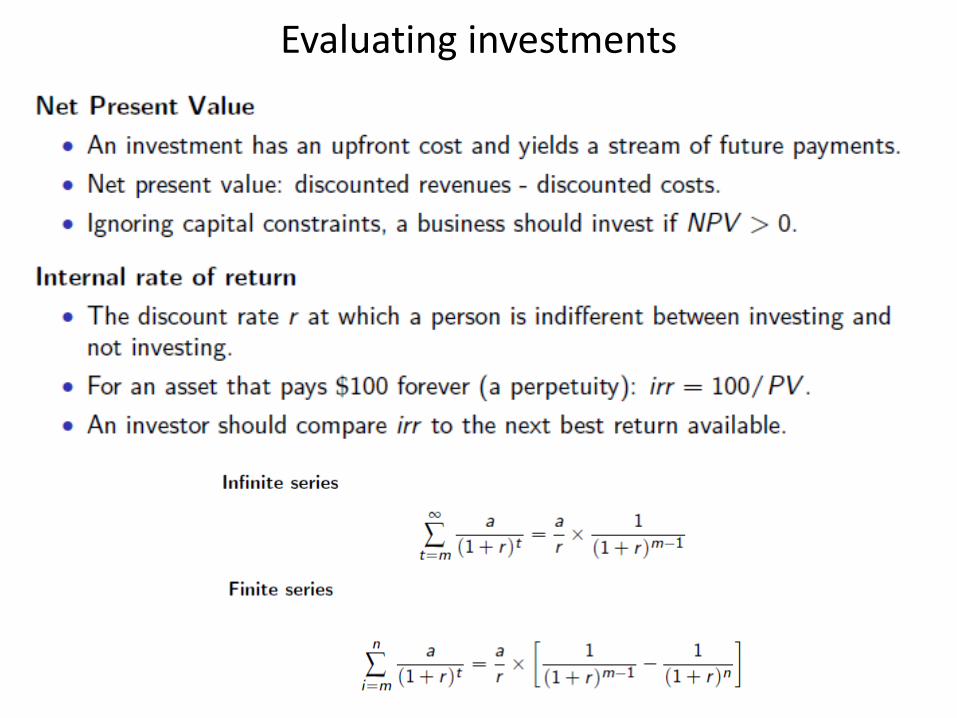

Evaluating investments