Korea Energy Demand Outlook · ISSN 1599-9009 June 2011 7PMVNF /P KEEI Korea Energy Demand Outlook...

151

KEEI Korea Energy Demand Outlook ISSN 1599-9009 June 2011 Volume 13, No. 2

Transcript of Korea Energy Demand Outlook · ISSN 1599-9009 June 2011 7PMVNF /P KEEI Korea Energy Demand Outlook...

KEEI

KEEI

KE

EI

Korea Energy Demand Outlook

ISSN 1599-9009

KoreaEnergy

Dem

andO

utlook June 2011

June2011

Volume 13, No. 2QUARTERLY ENERGY OUTLOOK

Korea Energy Economic Institute132 Naesonsunhwan-ro, Uiwang-si, Gyeonggi-do

Phone: (031)420-2114

Fax: (031)422-4958

E-mail : [email protected]

Hompage : http://www.keei.re.kr

Korea

Energy

Econom

icInstitute

에너지수요전망 문13-2 2011.9.16 2:11 PM 페이지1 매일3 MAC2PDF_IN 600DPI 175LPI T

수요전망 내지13-2 문 2011.9.16 2:11 PM 페이지148 매일3 MAC2PDF_IN 600DPI 125LPI T

ISSN 1599-9009

June 2011

Volume 13, No. 2

KEEIKorea Energy Demand Outlook

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지1 매일3 MAC2PDF_IN 600DPI 125LPI T

·In charge of overall research Choi, Do-young ([email protected])

·Oil/International oil market Kim, Soo-il ([email protected])

·Electricity/Transformation Choi, Do-young ([email protected])

·Town gas/Coal Lee, Sang-youl ([email protected])

·International LNG market Lee, Bo-hye ([email protected])

·Material/Research support Hwang, In-wook ([email protected])

·Statistical support Chung, Chang-bong ([email protected])

Phone: +82-31-420-2148, +82-31-420-2234

Fax: +82-31-420-2164

KEEI Korea Energy Demand Outlook

The 「KEEI Korea Energy Demand Outlook」is a report that analyzes trends in theinternational energy market and energy supply/demand trends in Korea, and makesshort-term forecasts on energy demand.

This report quickly identifies recent changes in energy supply and demand, thusproviding various energy supply/demand forecast indexes and information forgovernment policies. It is intended to contribute to government efforts in setting andadjusting an overall policy direction regarding energy supply and demand.

This report was written and edited by the Energy Demand and Supply ForecastTeam under the Center for Energy Information and Statistics of KEEI.

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지2 매일3 MAC2PDF_IN 600DPI 125LPI T

Summary ………………………………………………………………………………………… 7

Ⅰ. International Energy Market Trends…………………………………………………… 35

1. Trends in the international oil market and oil exports/imports ……………………… 37

2. Trends in the international natural gas market ……………………………………… 40

3. Trends in the international coal market ……………………………………………… 42

Ⅱ. Economic and Energy Consumption Trends in Korea …………………………… 45

1. Economic trends in Korea ……………………………………………………………… 47

2. Trends in primary energy consumption ……………………………………………… 51

3. Trends in final energy consumption …………………………………………………… 66

4. Trends in petroleum product consumption…………………………………………… 73

5. Trends in electricity consumption ……………………………………………………… 79

6. Trends in LNG and town gas consumption ………………………………………… 85

7. Trends in coal and other energy consumption ……………………………………… 89

Ⅲ. Energy Demand Outlook for 2011 …………………………………………………… 95

1. Outlook on the international energy market ………………………………………… 97

2. Domestic economic outlook and outlook assumptions…………………………… 103

3. Outlook on primary energy demand ………………………………………………… 108

4. Outlook on final energy demand……………………………………………………… 116

5. Outlook on petroleum product demand …………………………………………… 122

6. Outlook on electricity demand………………………………………………………… 124

7. Outlook on LNG and town gas demand …………………………………………… 129

8. Outlook on coal and other energy demand ………………………………………… 131

9. Characteristics and implications……………………………………………………… 136

Contents

3http://www.keei.re.kr

Summary

Table of Contents for Titles

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지3 매일3 MAC2PDF_IN 600DPI 125LPI T

KEEI Korea Energy Demand Outlook

4 KOREA ENERGY ECONOMICS INSTITUTE

<TableⅠ-1> Changes in international crude oil prices ……………………………………………… 37<TableⅠ-2> Changes in consumer prices of petroleum products in Korea ……………………… 38<TableⅠ-3> Trends in international natural gas supply and demand ……………………………… 40<TableⅠ-4> Trends in international natural gas prices ……………………………………………… 41<TableⅠ-5> Trends in global coal production ………………………………………………………… 44

<TableⅡ-1> Recent economic trends ………………………………………………………………… 48<TableⅡ-2> Composite index…………………………………………………………………………… 50<TableⅡ-3> Primary energy consumption trends …………………………………………………… 53<TableⅡ-4> Level of contribution of each factor that led to a rise in primary energy consumption in 2010 ………… 58<TableⅡ-5> Level of contribution of each factor that led to a rise in primary energy consumption in the first quarter of 2011… 60<TableⅡ-6> Temperature effect on increase in primary energy consumption …………………… 62<TableⅡ-7> Trends in final energy consumption……………………………………………………… 66<TableⅡ-8> Trends in petroleum product consumption by sector ………………………………… 74<TableⅡ-9> Trends in key petroleum product consumption ……………………………………… 75<TableⅡ-10> Trends in electricity consumption ……………………………………………………… 80<TableⅡ-11> Expansion of plant capacity by source in 2010 ……………………………………… 84<TableⅡ-12> Trends in LNG consumption …………………………………………………………… 85<TableⅡ-13> Trends in town gas consumption ……………………………………………………… 87<TableⅡ-14> Pig iron production, shipment, and inventory, and bituminous coal consumption for steel making…… 91<TableⅡ-15> Trends in coal consumption …………………………………………………………… 92<TableⅡ-16> Trends in consumption of thermal energy, new & renewable energy, and other energy ……… 93

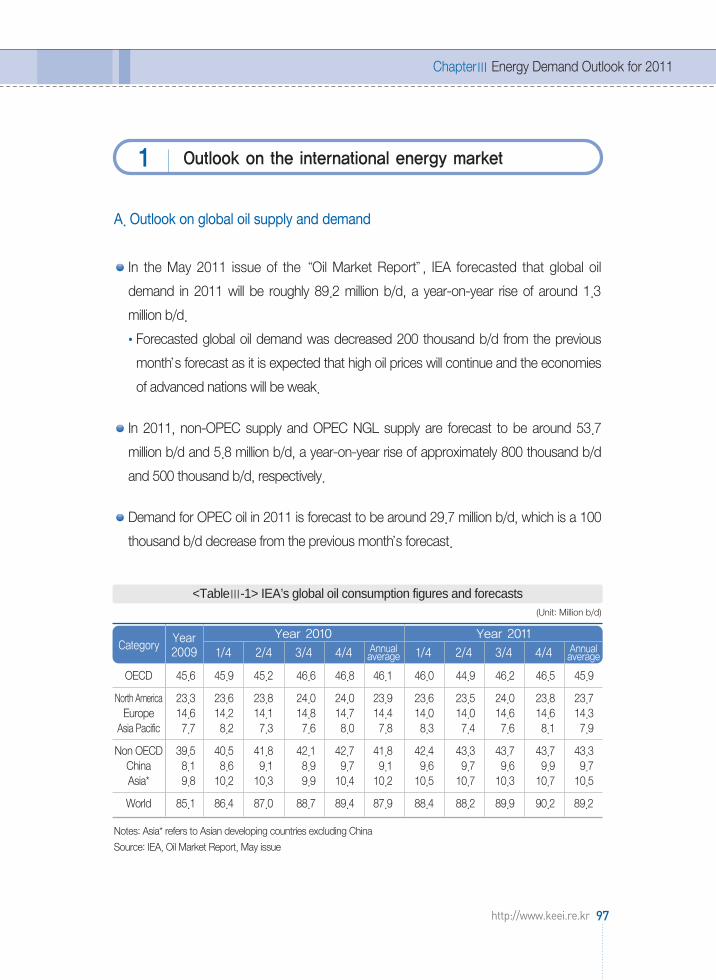

<TableⅢ-1> IEA’s global oil consumption figures and forecasts …………………………………… 97<TableⅢ-2> Oil price outlook for 2010 and 2011 (Dubai oil)………………………………………… 98<TableⅢ-3> Oil price outlook of major overseas organizations in March ………………………… 98<TableⅢ-4> International natural gas consumption and outlook …………………………………… 99<TableⅢ-5> International natural gas production and outlook …………………………………… 100<TableⅢ-6> Outlook on international natural gas prices …………………………………………… 101<TableⅢ-7> Outlook on international coal prices for 2011 ………………………………………… 103<TableⅢ-8> Economic outlook for 2011 …………………………………………………………… 105<TableⅢ-9> Economic outlook by major organizations in Korea ………………………………… 107<TableⅢ-10> Assumptions on temperature variables ……………………………………………… 107<TableⅢ-11> Outlook on primary energy demand ………………………………………………… 109

Table of Contents for Tables

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지4 매일3 MAC2PDF_IN 600DPI 125LPI T

SummaryContents

5http://www.keei.re.kr

<TableⅢ-12> Key indices related to energy consumption ………………………………………… 111<TableⅢ-13> Outlook on final energy demand……………………………………………………… 117<TableⅢ-14> Outlook on petroleum product demand by sector ………………………………… 122<TableⅢ-15> Outlook on demand for key petroleum products…………………………………… 123<TableⅢ-16> Outlook on electricity demand………………………………………………………… 124<TableⅢ-17> Trends in GDP elasticity of electricity demand ……………………………………… 125<TableⅢ-18> Outlook on LNG demand……………………………………………………………… 129<TableⅢ-19> Outlook on town gas demand………………………………………………………… 130<TableⅢ-20> Outlook on steel production…………………………………………………………… 132<TableⅢ-21> Outlook on coal demand ……………………………………………………………… 133<TableⅢ-22> Outlook on thermal energy, new & renewable energy, and other energy demand…… 135<TableⅢ-23> Outlook on energy intensity …………………………………………………………… 139<TableⅢ-24> Assumed changes in energy consumption caused by the temperature effect … 140<TableⅢ-25> Energy consumption and import and outlook ……………………………………… 144

[DiagramⅠ-1] Changes in petroleum product import prices and consumer prices ……………… 39[DiagramⅠ-2] Trends in international natural gas prices……………………………………………… 41[DiagramⅠ-3] International coal price trends…………………………………………………………… 42

[DiagramⅡ-1] Composite index ………………………………………………………………………… 50[DiagramⅡ-2] Recent economic and primary energy consumption trends ……………………… 52[DiagramⅡ-3] Trends in Dubai oil prices ……………………………………………………………… 54[DiagramⅡ-4] Trends in consumer prices of oil for transport………………………………………… 55[DiagramⅡ-5] Trends in primary energy consumption increase rate ……………………………… 56[DiagramⅡ-6] Level of contribution to increase in primary energy consumption by each factor in 2010 ………………… 59[DiagramⅡ-7] Level of contribution to increase in primary energy consumption by each factor in the first quarter of 2011 … 60[DiagramⅡ-8] Level of contribution of each factor towards annual primary energy increase since 2005 ………………… 61[DiagramⅡ-9] Assumed changes in primary energy consumption caused by the temperature effect …… 62[DiagramⅡ-10] Changes in HDD ……………………………………………………………………… 63[DiagramⅡ-11] Changes in CDD ……………………………………………………………………… 63[DiagramⅡ-12] Level of contribution of each energy source to primary energy increase in 2010 ………………… 64[DiagramⅡ-13] Level of contribution of each energy source to primary energy increase in the first quarter of 2011 … 65[DiagramⅡ-14] Final energy consumption by energy source and use……………………………… 67

Table of Contents for Diagrams

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지5 매일3 MAC2PDF_IN 600DPI 125LPI T

KEEI Korea Energy Demand Outlook

6 KOREA ENERGY ECONOMICS INSTITUTE

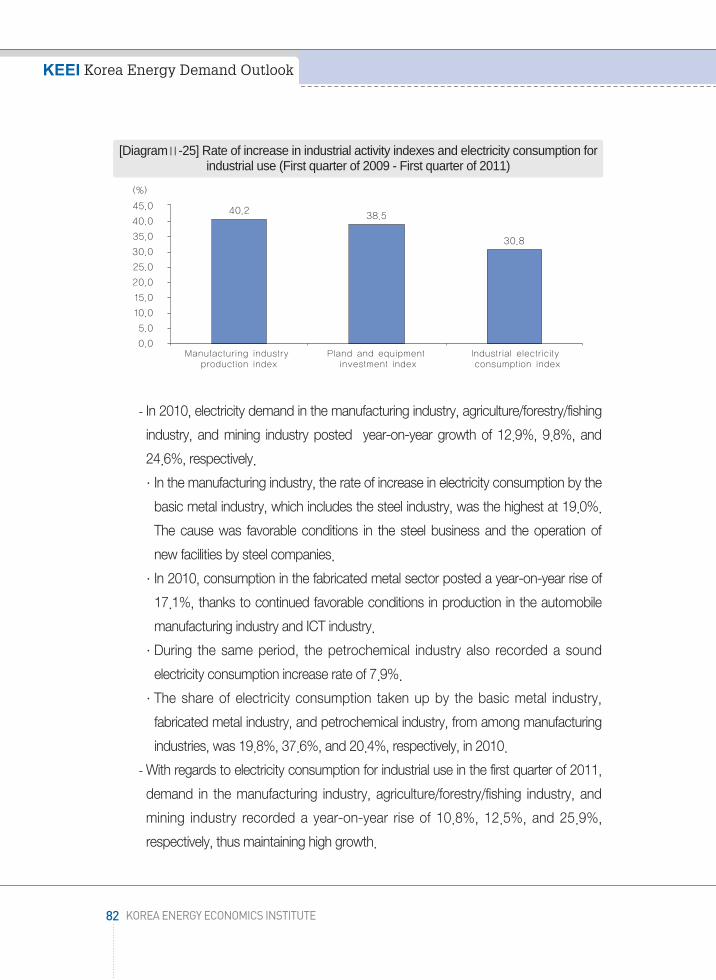

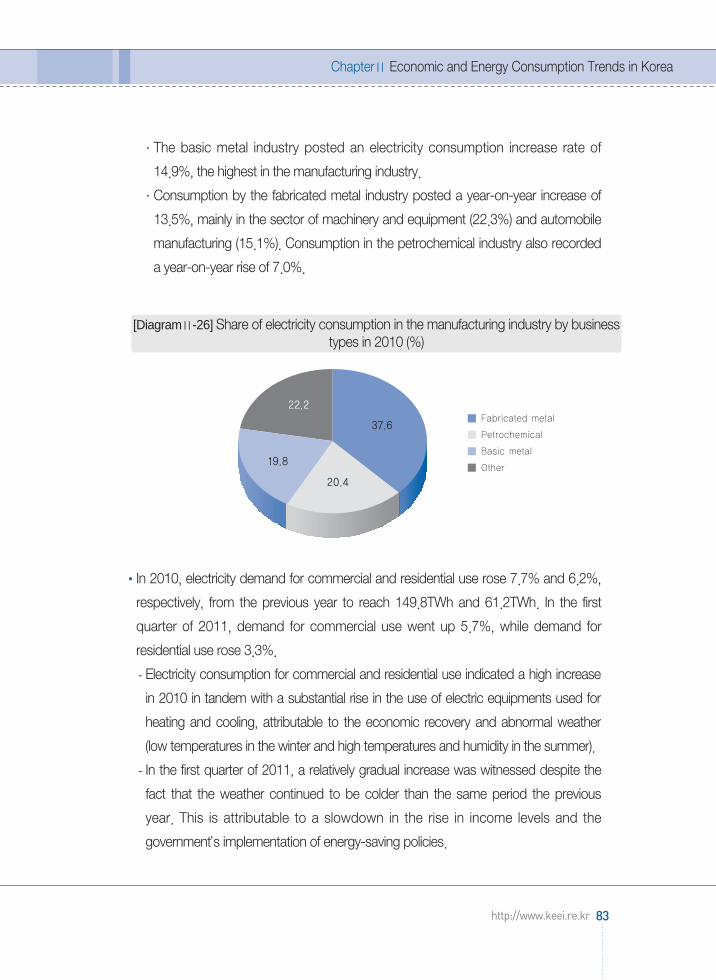

[DiagramⅡ-15] Business trends in the manufacturing industry and changes in electricity consumption for industrial use … 68[DiagramⅡ-16] Trends in the rate of final energy consumption increase by sector ……………… 70[DiagramⅡ-17] Changes in petroleum product consumption increase rate by sector ………… 74[DiagramⅡ-18] Changes in gasoline consumption and increase rate ……………………………… 76[DiagramⅡ-19] Changes in consumption of diesel for transport and increase rate ……………… 76[DiagramⅡ-20] Changes in consumption of kerosene and diesel, and increase rate …………… 77[DiagramⅡ-21] Changes in consumption of heavy oil and increase rate ………………………… 77[DiagramⅡ-22] Changes in consumption of naphtha and increase rate…………………………… 78[DiagramⅡ-23] Changes in LPG consumption and increase rate ………………………………… 78[DiagramⅡ-24] Recent manufacturing business trends and electricity consumption for industrial use…… 81[DiagramⅡ-25] Rate of increase in industrial activity indexes and electricity consumption for

industrial use (First quarter of 2009 - First quarter of 2011) ……………………… 82[DiagramⅡ-26] Share of electricity consumption in the manufacturing industry by

business types in 2010 (%) …………………………………………………………… 83[DiagramⅡ-27] Changes in the electricity consumption increase rate……………………………… 84[DiagramⅡ-28] Trends in LNG consumption increase rate per use………………………………… 86[DiagramⅡ-29] Trends in town gas consumption by month………………………………………… 88[DiagramⅡ-30] Trends in number of customers of town gas for industrial use …………………… 89[DiagramⅡ-31] Changes in the rate of increase in pig iron and bituminous coal for steel making…… 90

[DiagramⅢ-1] Outlook on international natural gas prices ………………………………………… 101[DiagramⅢ-2] Changes in CDD and HDD and assumptions for outlook ………………………… 108[DiagramⅢ-3] Forecasts on the economic growth rate and primary energy increase rate …… 110[DiagramⅢ-4] Forecasts on energy intensity and per capita consumption ……………………… 112[DiagramⅢ-5] Share of primary energy demand taken up by each energy source …………… 114[DiagramⅢ-6] Forecasts on level of contribution of each energy source to increase in primary energy … 115[DiagramⅢ-7] Share of final energy demand occupied by each sector ………………………… 120[DiagramⅢ-8] Share of final energy demand taken up by each energy source ………………… 121[DiagramⅢ-9] Outlook on economic growth rate and electricity demand increase rate ……… 126[DiagramⅢ-10] Outlook on electricity demand by sector…………………………………………… 126[DiagramⅢ-11] Trends in electricity consumption share of each sector and forecasts ………… 127[DiagramⅢ-12] Town gas trends and outlook by use ……………………………………………… 131[DiagramⅢ-13] Coal trends and forecasts per use ………………………………………………… 134[DiagramⅢ-14] Thermal energy trends and outlook ………………………………………………… 135[DiagramⅢ-15] Trends and outlook on new & renewable energy and other energy …………… 136[DiagramⅢ-16] Level of contribution of each factor towards a rise in primary energy consumption in the first quarter … 138[DiagramⅢ-17] Changes in share of winter peak demand taken up by heating load…………… 141[DiagramⅢ-18] Trends in oil dependence and forecasts…………………………………………… 143

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지6 매일3 MAC2PDF_IN 600DPI 125LPI T

Summary

7http://www.keei.re.kr

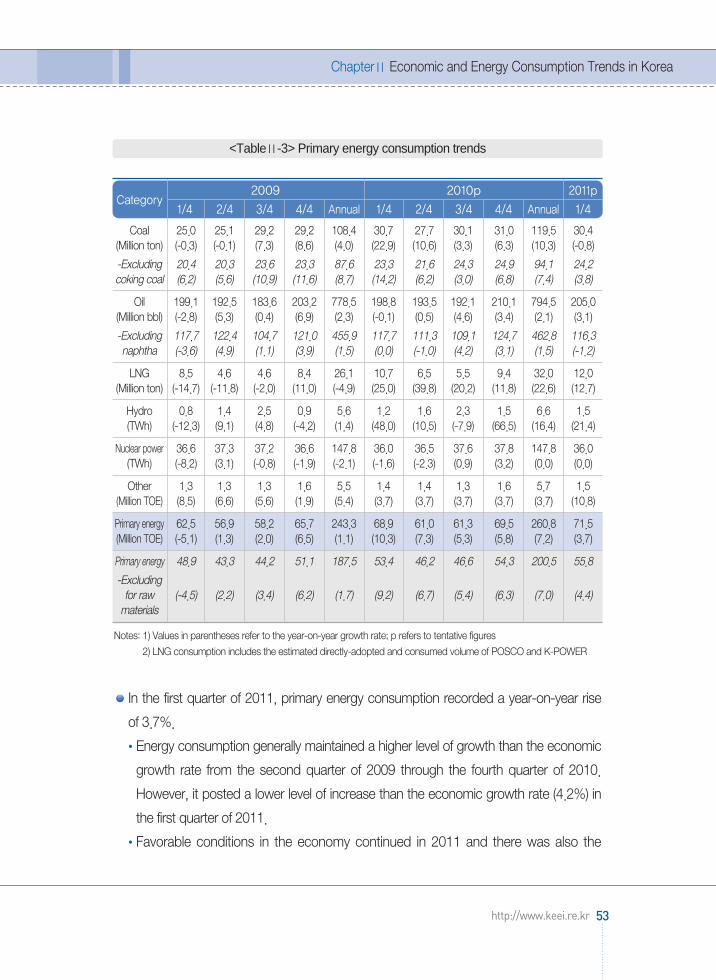

Primary energy consumption for the first quarter of 2011 tentatively reached 71.5

million TOE, a year-on-year rise of 3.7%.

Quarterly energy consumption generally maintained a higher level of growth than the

economic growth rate from the second quarter of 2009 through the fourth quarter of

2010. However, it posted a lower level of increase than the economic growth rate

(4.2%) in the first quarter of 2011.

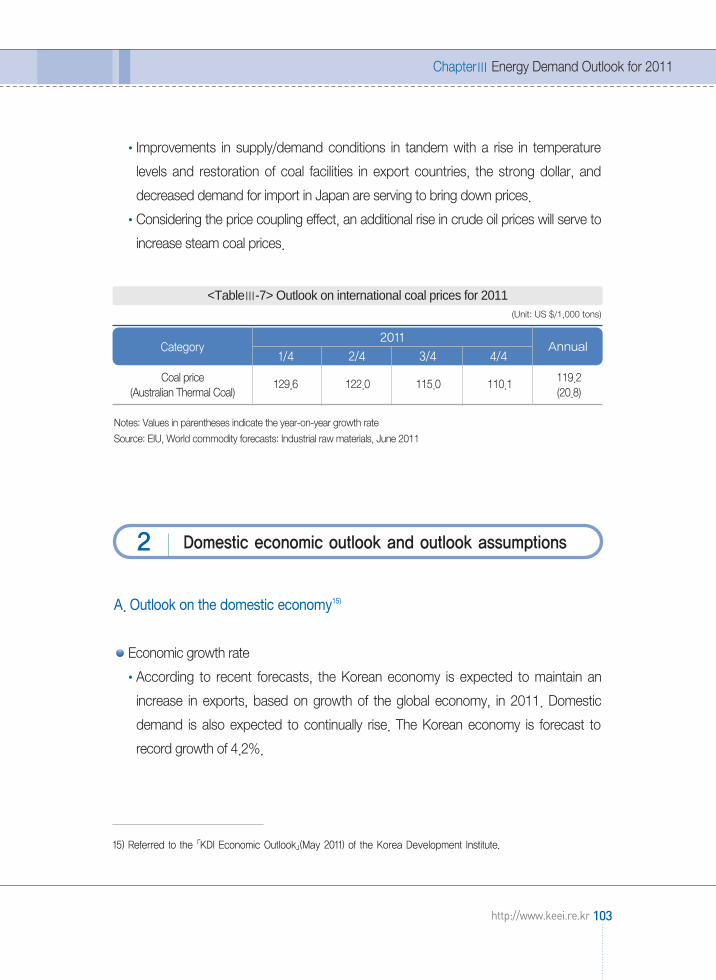

Favorable conditions in the economy continued in 2011 and there was also the

record-breaking cold wave in January in 48 years (5.4℃ drop from average month

temperature), triggering factors that would increase energy consumption. However,

primary energy consumption recorded a relatively low level of increase in the first

quarter.

Energy consumption trends

Summary▶

[Recent economic and primary energy consumption trends]

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지7 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: 1) Values in parentheses refer to the year-on-year growth rate; p refers to tentative figures2) LNG consumption includes the estimated directly-adopted and consumed volume of POSCO and K-POWER

Consumption trends by energy source

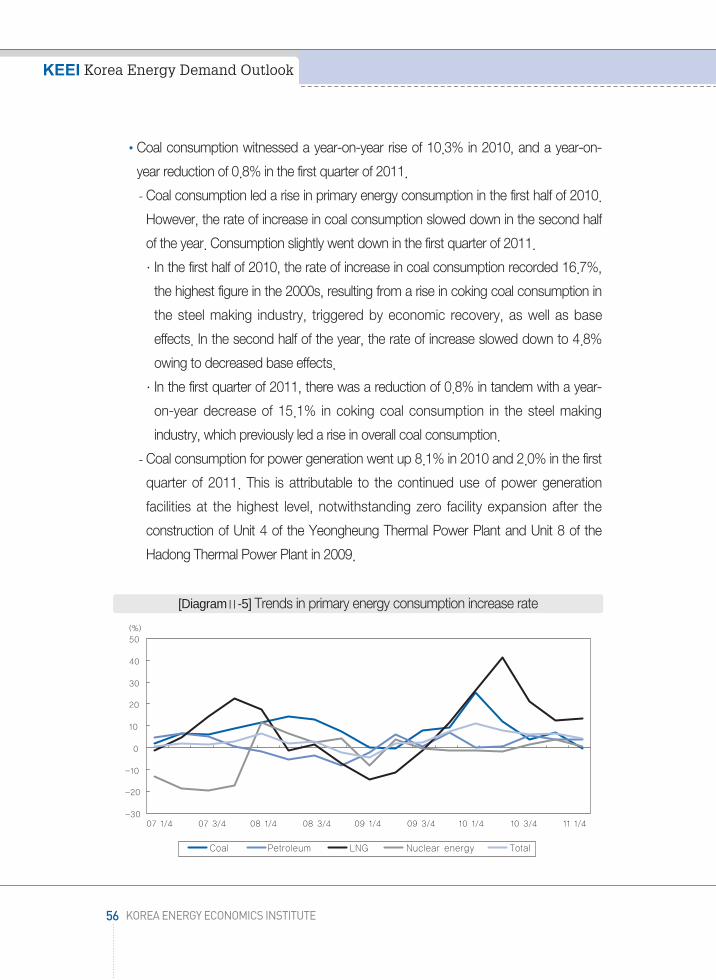

Coal consumption recorded a year-on-year rise of 10.3% in 2010, and a year-on-

year reduction of 0.8% in the first quarter of 2011.

- Coal consumption led a rise in primary energy consumption in the first half of 2010.

However, the rate of increase in coal consumption slowed down in the second half

of the year. Consumption slightly went down in the first quarter of 2011.

Oil consumption recorded sound growth of 2.1% in 2010 and 3.1% in the first

8 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Category2009 2010p 2011p

1/4 2/4 3/4 4/4 Annual 1/4 2/4 3/4 4/4 Annual 1/4

Coal 25.0 25.1 29.2 29.2 108.4 30.7 27.7 30.1 31.0 119.5 30.4 (Million ton) (-0.3) (-0.1) (7.3) (8.6) (4.0) (22.9) (10.6) (3.3) (6.3) (10.3) (-0.8)

-Excluding 20.4 20.3 23.6 23.3 87.6 23.3 21.6 24.3 24.9 94.1 24.2coking coal (6.2) (5.6) (10.9) (11.6) (8.7) (14.2) (6.2) (3.0) (6.8) (7.4) (3.8)

Oil 199.1 192.5 183.6 203.2 778.5 198.8 193.5 192.1 210.1 794.5 205.0(Million bbl) (-2.8) (5.3) (0.4) (6.9) (2.3) (-0.1) (0.5) (4.6) (3.4) (2.1) (3.1)

-Excluding 117.7 122.4 104.7 121.0 455.9 117.7 111.3 109.1 124.7 462.8 116.3naphtha (-3.6) (4.9) (1.1) (3.9) (1.5) (0.0) (-1.0) (4.2) (3.1) (1.5) (-1.2)

LNG 8.5 4.6 4.6 8.4 26.1 10.7 6.5 5.5 9.4 32.0 12.0 (Million ton) (-14.7) (-11.8) (-2.0) (11.0) (-4.9) (25.0) (39.8) (20.2) (11.8) (22.6) (12.7)

Hydro 0.8 1.4 2.5 0.9 5.6 1.2 1.6 2.3 1.5 6.6 1.5(TWh) (-12.3) (9.1) (4.8) (-4.2) (1.4) (48.0) (10.5) (-7.9) (66.5) (16.4) (21.4)

Nuclear power 36.6 37.3 37.2 36.6 147.8 36.0 36.5 37.6 37.8 147.8 36.0 (TWh) (-8.2) (3.1) (-0.8) (-1.9) (-2.1) (-1.6) (-2.3) (0.9) (3.2) (0.0) (0.0)

Other 1.3 1.3 1.3 1.6 5.5 1.4 1.4 1.3 1.6 5.7 1.5(Million TOE) (8.5) (6.6) (5.6) (1.9) (5.4) (3.7) (3.7) (3.7) (3.7) (3.7) (10.8)

Primary energy 62.5 56.9 58.2 65.7 243.3 68.9 61.0 61.3 69.5 260.8 71.5(Million TOE) (-5.1) (1.3) (2.0) (6.5) (1.1) (10.3) (7.3) (5.3) (5.8) (7.2) (3.7)

Primary energy 48.9 43.3 44.2 51.1 187.5 53.4 46.2 46.6 54.3 200.5 55.8

-Excluding for raw (-4.5) (2.2) (3.4) (6.2) (1.7) (9.2) (6.7) (5.4) (6.3) (7.0) (4.4)materials

<Primary energy consumption trends>

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지8 매일3 MAC2PDF_IN 600DPI 125LPI T

quarter of 2011.

- Oil consumption maintained a level similar to that reached in the previous year in the

first half of 2010. However, oil consumption indicated relatively high growth since

the second half of the year, owing to a substantial increase in consumption of oil for

industrial raw materials and transport fuel, in addition to a sharp rise in consumption

in the transformation (power generation) sector.

In 2010, natural gas (LNG) consumption witnessed a year-on-year rise of 22.6%,

followed by two-digit growth (12.7%) in the first quarter of 2011.

- Favorable conditions in the economy continued in the first quarter of 2011. This,

and the record-breaking cold wave led to a substantial rise in natural gas

consumption mainly for power generation.

The level of nuclear power generation in 2010 was similar to that recorded in 2009. In

the first quarter of 2011, the same level as the same period the previous year was

maintained.

- The level of power generation went down compared to the same period the

previous year owing to planned inspection of major facilities in January and

February 2011. However, it went up 8.6% in March, a result of operation of Singori

Nuclear Power Plant Unit 11).

Level of contribution of each factor that led to a year-on-year rise in primary energy

consumption in the first quarter of 2011

The economic growth effect contributed 107.9% (2.8 million TOE) to a rise in primary

energy consumption.

- This means that primary energy consumption would have increased by 2.8 million

TOE in the first quarter of 2011 as a result of the economic growth (4.2%) effect, if

there were no changes in other factors that trigger a change in consumption such

as temperature and energy efficiency.

9http://www.keei.re.kr

Summary

1) Korea’s 21st nuclear power plant; Commercial operation commenced on February 28, 2011

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지9 매일3 MAC2PDF_IN 600DPI 125LPI T

The temperature effect contributed 74.8% (1.9 million TOE) to a rise in primary energy

consumption.

- The average temperature in the first quarter dropped 1.2℃ compared to the same

period the previous year, including the record-breaking cold wave in 48 years that took

place in January 2011. Energy demand for heating increased because of the weather.

It is presumed that consumption went down 2.1 million TOE as a result of changes in

other factors such as energy efficiency improvements, a rise in oil prices, and

changes in industrial structure.

Notes: The energy efficiency effect includes all factors that trigger a change in energy consumption excluding thetemperature effect and economic growth effect such as changes in the industrial structure and energy prices andtechnical energy efficiency improvements.

Level of contribution of each final energy source to a rise in primary energy

consumption in the first quarter of 2011

The level of contribution of electricity (triggering energy consumption for power generation)

and energy for industrial raw materials (naphtha and coking coal) stood at 55.6% and

6.8%, respectively. The level of contribution of energy for industrial raw materials sharply

dropped compared to 2010 as a result of decreased consumption of coking coal (-15.1%).

The level of contribution of town gas, a key source of energy for heating, reached

20.6% in the first quarter owing to influence from the cold weather. In contrast, the level

of contribution of petroleum for fuel stood at -7.0% owing to decreased consumption.

10 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Category

Level of contribution toincrease in primaryenergy consumption

(%)

Contribution to a rise in consumption byeach factor in the first quarter of 2011

Contribution to change inconsumption (1,000 TOE)

Level of contribution (%)

Energy efficiency effect -2,121 -82.7 -3.1

Growth effect 2,768 107.9 4.0

Temperature effect 1,918 74.8 2.8

Change in primary energy 2,565 100.0 3.7

<Level of contribution of each factor that led to a rise in primary energy consumption in the first quarter of 2011>

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지10 매일3 MAC2PDF_IN 600DPI 125LPI T

Final energy consumption in the first quarter of 2011 recorded 53.8 million TOE, a

year-on-year increase of 2.8%.

In the first quarter of 2011, there was an even level of increase in energy

consumption of around 3% among different sectors. The transport sector and

industrial sector recorded a year-on-year increase of 3.2% and 2.8%, respectively,

thus posting a relatively high consumption increase rate.

The rate of increase in energy consumption in the residential/commercial sector and

public/other sector both posted a year-on-year rise of 2.7%. Consumption in the

residential/commercial and public/other sectors, in which energy consumption for

heating purposes takes up a high proportion, indicated a low increase rate. This

seems to be partly a result of influence of energy-saving policies such as the

‘measure on placing restrictions on heating temperatures in buildings’that was

implemented in response to a soar in oil prices.

- Consumption in the industrial sector indicated high growth of 7.9% from the

previous year in 2010. In the first quarter of 2011, however, the level of increase

slowed down to a year-on-year increase of 2.8%, attributable to base effects and

sluggish coking coal consumption.

11http://www.keei.re.kr

Summary

[Level of contribution of each energy source to primary energy increase in the first quarter of 2011]

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지11 매일3 MAC2PDF_IN 600DPI 125LPI T

The slowdown in consumption for industrial use resulted from a considerable drop in

coal (-6.2%) consumption, despite a soar in electricity (11.0%) and town gas (9.1%)

consumption.

Notes: Values in parentheses are the year-on-year growth rate (%); p refers to tentative figures

12 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Category2009 2010p 2011p

1/4 2/4 3/4 4/4 Annual 1/4 2/4 3/4 4/4 Annual 1/4

Industry 25.4 26.1 26.6 28.0 106.1 28.9 28.3 27.6 29.7 114.5 29.7(Million TOE) (-6.1) (-1.3) (0.2) (6.1) (-0.3) (13.8) (8.5) (3.8) (5.9) (7.9) (2.8)-Excluding for 11.8 12.5 12.6 13.4 50.3 13.4 13.5 12.9 14.5 54.3 14.0raw materials (-4.9) (-1.1) (2.8) (4.8) (0.4) (13.3) (7.8) (2.6) (8.0) (7.9) (4.6)

Transport 8.5 9.1 9.1 9.3 35.9 8.5 9.2 9.5 9.6 36.8 8.8(Million TOE) (-2.9) (0.8) (2.3) (1.3) (0.4) (0.8) (1.9) (4.2) (2.8) (2.4) (3.2)

Residential 12.7 7.0 5.8 10.3 35.7 13.6 7.8 6.2 10.6 38.3 14.0/commercial(Million TOE) (-8.2) (0.9) (1.2) (5.1) (-1.4) (7.7) (12.3) (6.0) (3.4) (7.1) (2.7)

Public/other 1.1 1.0 1.0 1.2 4.3 1.2 1.0 1.1 1.2 4.6 1.2(Million TOE) (-0.5) (11.9) (5.9) (3.6) (4.8) (5.4) (1.8) (11.0) (3.3) (5.2) (2.7)

Total 47.7 43.1 42.5 48.7 182.1 52.3 46.4 44.3 51.1 194.1 53.8(Million TOE) (-6.0) (-0.3) (0.9) (4.9) (-0.3) (9.7) (7.6) (4.4) (4.7) (6.6) (2.8)

Total 34.1 29.5 28.5 34.1 126.3 36.8 31.5 29.6 35.9 133.9 38.1-Excluding for (-5.5) (0.3) (2.4) (3.8) (0.0) (7.8) (6.8) (4.1) (5.0) (6.0) (3.5)raw materials

Town gas 6.9 3.6 2.7 5.3 18.4 7.9 4.3 2.8 5.7 20.8 8.1(Billion m3) (-6.1) (-1.1) (-2.5) (5.4) (-1.5) (14.5) (20.9) (6.1) (7.8) (12.6) (2.8)

Oil 187.2 186.1 181.0 197.9 752.2 189.0 187.8 187.0 204.2 768.0 194.7(Million bbl) (-4.9) (3.6) (1.0) (6.8) (1.5) (1.0) (0.9) (3.3) (3.2) (2.1) (3.0)-Excluding 105.8 106.0 102.1 115.7 429.6 107.9 105.7 104.0 118.7 436.3 106.0naphtha (-7.2) (2.1) (2.2) (3.5) (0.0) (1.9) (-0.3) (1.9) (2.6) (1.6) (-1.8)

Electricity 100.3 94.0 99.0 101.2 394.5 112.5 103.6 109.1 109.0 434.2 121.4(TWh) (-2.3) (2.0) (2.7) (7.7) (2.4) (12.2) (10.3) (10.2) (7.7) (10.1) (7.9)

Coal 8.2 8.2 9.5 10.0 35.9 11.3 10.2 9.4 10.4 41.2 10.6(Million ton) (-15.4) (-16.4) (-0.5) (-3.3) (-8.9) (37.0) (24.1) (-1.2) (3.9) (14.7) (-5.5)-Excluding 3.7 3.4 3.9 4.2 15.2 3.9 4.0 3.5 4.3 15.8 4.4coking coal (-7.5) (-11.5) (8.6) (-5.6) (-4.3) (6.5) (17.1) (-9.1) (3.3) (4.0) (12.6)

Thermal and 1,870 1,391 1,223 1,933 6,418 2,001 1,486 1,269 2,009 6,765 2,173other (1.5) (1.7) (1.9) (4.6) (2.5) (7.0) (6.8) (3.7) (3.9) (5.4) (8.6)(Thousand TOE)

<Trends in final energy consumption>

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지12 매일3 MAC2PDF_IN 600DPI 125LPI T

In the 2000s, the transport sector indicated a stable increase in consumption. It

indicated a year-on-year rise of 2.4% in 2010, attributable to an upswing in gasoline

and jet oil consumption, and maintained sound growth of 3.2% in the first quarter of

2011.

In the first quarter of 2011, consumption in the residential/commercial sector

recorded a relatively gradual increase rate of 2.7% despite the emergence of factors

that would have triggered a rise in energy consumption as a result of abnormally low

temperatures (average temperature indicated a year-on-year drop of -1.2℃ and HDD

recorded a year-on-year rise of 6.9%).

Trends in final energy consumption by energy source in the first quarter of 2011

Electricity consumption sharply rose from a continued upswing in industrial activities

and the cold wave.

- Electricity, town gas, and oil consumption went up 7.9%, 2.8%, and 3.0%,

respectively, but coal consumption indicated a year-on-year drop of 5.5% owing to

decreased consumption of bituminous coal for steel making.

- In terms of oil, naphtha consumption rose 9.3% as a result of favorable conditions

in production in the petrochemical industry. On the other hand, consumption of

other products indicated relatively low growth such as gasoline (2.7%), kerosene

(5.3%), and diesel (1.7%).

- Consumption of town gas for industrial use rose 9.1%, thus leading a rise in overall

town gas consumption. Consumption for residential/commercial use recorded a

gradual increase of 1.1%.

- Despite the fact that bituminous coal consumption for steel making posted a year-

on-year rise of 5.6% and 10.9%, respectively, in February and March, coal

consumption recorded a year-on-year drop of 5.5% owing to a sharp decrease

(-40.5%) in January.

- Electricity consumption indicated a year-on-year rise of 7.9% because consumption

for industrial use remained to be strong (year-on-year rise of 11.0%).

- Electricity consumption for industrial use continued two-digit growth for four

13http://www.keei.re.kr

Summary

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지13 매일3 MAC2PDF_IN 600DPI 125LPI T

consecutive months from October 2010 through February 2011, attributable to an

upswing in production activities in industries that consume a great amount of

electricity (machinery and equipment, chemical products, automobiles, steel

making, etc.). It also recorded relatively high growth of 8.1% in March.

Primary energy demand in 2011 is expected to reach 269.9 million TOE, a year-on-

year rise of 3.5%.

The level of increase in primary energy demand is forecast to slow down this year

due to several factors: a decrease in the economic growth rate (6.2% in 2010 →

4.2% in 2011), removal of temperature effects resulting from an assumption that

average year temperatures will be recovered from the second through the fourth

quarter, and base effects from high growth in consumption in 2010.

Primary energy demand in 2011, excluding energy for raw material use (naphtha,

coking coal), is expected to go up a mere 3.4% from the previous year.

- In 2011, energy demand for raw material use will likely go up 3.9%, indicating

relatively quick growth.

- Favorable conditions in the oil and chemical industries are expected to continue,

resulting in forecasts that naphtha consumption for raw material use will rise by

5.7%. Consumption of coking coal is expected to become stagnant with the

reflection of base effects from a high rise in consumption recorded in the previous

year.

14 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Outlook on primary energy demand

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지14 매일3 MAC2PDF_IN 600DPI 125LPI T

15http://www.keei.re.kr

Summary

[Forecasts on the economic growth rate and primary energy increase rate]

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지15 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: 1) Values in parentheses refer to the year-on-year growth rate (%); p refers to tentative figures; e refers to estimates2) LNG consumption includes the estimated directly-adopted volume of POSCO and K-POWER

Forecasts on key energy indicators

The energy intensity (TOE/million won) deteriorated from 0.246 in 2008 to 0.248 in

2009 and 0.250 in 2010. However, it will likely improve to 0.248 in 2011.

16 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Category2010p 2011e

1/4 2/4 3/4 4/4 Annual 1/4 2/4 3/4 4/4 Annual

Coal 30.7 27.7 30.1 31.0 119.5 30.4 28.1 30.6 31.7 120.9(Million ton) (22.9) (10.6) (3.3) (6.3) (10.3) (-0.8) (1.5) (1.6) (2.3) (1.1)

-Excluding 23.3 21.6 24.3 24.9 94.1 24.2 21.8 24.4 25.1 95.6coking coal (14.2) (6.2) (3.0) (6.8) (7.4) (3.8) (1.3) (0.3) (0.9) (1.6)

Oil 198.8 193.5 192.1 210.1 794.5 205.0 196.2 193.7 212.0 806.8(Million bbl) (-0.1) (0.5) (4.6) (3.4) (2.1) (3.1) (1.4) (0.8) (0.9) (1.5)

-Excluding 117.7 111.3 109.1 124.7 462.8 116.3 109.6 107.1 123.6 456.6naphtha (0.0) (-1.0) (4.2) (3.1) (1.5) (-1.2) (-1.6) (-1.8) (-0.9) (-1.4)

LNG 10.7 6.5 5.5 9.4 32.0 12.0 7.1 6.0 10.1 35.3(Million ton) (25.0) (39.8) (20.2) (11.8) (22.6) (12.7) (10.1) (10.2) (7.7) (10.3)

Hydro 1.2 1.6 2.3 1.5 6.6 1.5 1.6 2.5 1.5 7.1(TWh) (48.0) (10.5) (-7.9) (66.5) (16.4) (21.4) (1.2) (8.4) (5.2) (8.4)

Nuclear power 36.0 36.5 37.6 37.8 147.8 36.0 38.1 40.7 40.7 155.5(TWh) (-1.6) (-2.3) (0.9) (3.2) (0.0) (0.0) (4.4) (8.5) (7.8) (5.2)

Other 1.4 1.4 1.3 1.6 5.7 1.5 1.5 1.4 1.8 6.1(Million TOE) (3.7) (3.7) (3.7) (3.7) (3.7) (10.8) (6.1) (6.1) (8.0) (7.8)

Primary energy 68.9 61.0 61.3 69.5 260.8 71.5 63.0 63.4 71.9 269.9(Million TOE) (10.3) (7.3) (5.3) (5.8) (7.2) (3.7) (3.2) (3.4) (3.5) (3.5)

Primary energy 53.4 46.2 46.6 54.3 200.5 55.8 47.5 48.0 56.0 207.3-Excludingfor raw (9.2) (6.7) (5.4) (6.3) (7.0) (4.4) (2.7) (2.9) (3.2) (3.4)materials

<Outlook on primary energy demand>

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지16 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: p refers to tentative figures; e refers to forecasts

Forecasts on primary energy demand by energy source

In 2011, coal demand is expected to show gradual growth of 1.1%, attributable to a

slowdown in coal consumption for power generation (no new facilities), sluggishness

in the cement industry, and base effects from a high increase in coking coal

consumption in the previous year.

In 2011, oil demand is expected to reach 806.8 million barrels, a year-on-year rise of

1.5%, owing to a rise in oil demand for industrial use as a result of the economic

recovery, despite continued high oil prices.

17http://www.keei.re.kr

Summary

Category 2005 2006 2007 2008 2009 2010p 2011e

Economic growth rate (%) 4.0 5.2 5.1 2.3 0.3 6.2 4.2

Primary energy consumption 3.8 2.1 1.3 1.8 1.1 7.2 3.5increase rate (%)

Energy intensity (TOE/Million won) 0.264 0.256 0.247 0.246 0.248 0.250 0.248

Per capita consumption (TOE) 4.75 4.83 4.88 4.95 4.99 5.34 5.51

<Key indices related to energy consumption>

[Forecasts on energy intensity and per capita consumption]

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지17 매일3 MAC2PDF_IN 600DPI 125LPI T

- Oil demand for industrial use is expected to indicate relatively high growth (2.1%) as

a result of increased consumption for raw material use, but the level of increase is

expected to decrease in comparison to 2010 owing to a decrease in demand for

heating purposes2).

- An increase in demand (5.7%) for naphtha, which accounts for 41.7% of total oil

consumption (as of 2010), is expected to lead an increase in total oil consumption

in 2011.

In 2011, LNG demand will likely record high growth of 10.3% compared to the

previous year. LNG demand for power generation, which accounted for 44% of

overall consumption in 2010, is expected to rise 16.0%, thus leading an overall

increase in LNG demand.

- Demand for LNG for power generation, which is used to handle peak load, is

forecast to record relatively high growth as it is expected that there will be

restrictions on the expansion of capacity of base-load power generation facilities

such as those for nuclear energy and bituminous coal and a high rise in electricity

demand.

The amount of nuclear power generation is forecast to record a year-on-year rise of

5.2% as new facilities are planned for operation in 2011, the first after 2005.

- There will likely be a rate of increase in the low 5% range as a result of effects of

facility expansion (approximately 5.5% increase is assumed)3) from the operation of

Singori Units 1 and 2.

Forecasts on level of contribution made by each final energy source to primary energy

demand

The level of contribution made by electricity, which triggers energy consumption for

18 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

2) This results from assuming average year temperatures.3) The total facility capacity of Singori Units 1 and 2 is 2,000MW, which accounts for 11.3% of the nuclear power

plant capacity (17,716MW) recorded at the end of 2010. However, completion of construction of Singori Unit 2is scheduled for the end of December 2011. Production of electricity through actual pilot operations will likelybe possible in the second half of the year.

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지18 매일3 MAC2PDF_IN 600DPI 125LPI T

power generation, is forecast to rise from 46.3% in 2010 to around 54.6% in 2011.

The level of contribution of demand for industrial raw material use is expected to

slightly drop from 26.0% in 2010 to 25.5% in 2011 as a result of a slowdown in

coking coal consumption.

It is forecast that town gas demand for industrial use and heating will slow down

based on the assumption that there will be a slowdown in economic growth and

average year temperatures will be recovered. The level of contribution of town gas to

an increase in primary energy demand is forecast to decrease from 15.7% in 2010 to

14.3% in 2011.

Petroleum products for fuel, excluding naphtha, are expected to record a decrease in

consumption (-1.3%) in 2011, thus contributing to reducing primary energy demand

by 8.4%.

19http://www.keei.re.kr

Summary

[Forecasts on level of contribution of each energy source to increase in primary energy]

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지19 매일3 MAC2PDF_IN 600DPI 125LPI T

Final energy demand is forecast to record a year-on-year increase of 3.1% in 2011 to

reach 200.2 million TOE.

Consumption soared in the industrial sector and residential/commercial/public sector

in 2010, but the level of consumption increase is expected to substantially slow down

in 2011 due to base effects. The transport sector will likely indicate an increase rate

similar to the previous year.

In 2011, demand in the industrial sector is expected to record sound growth of 3.9%

despite base effects from a substantial rise in consumption in 2010.

Energy demand in the transport sector is expected to mark an increase rate of 2.3%,

which is similar to the previous year, attributable to a rise in new car sales and

overseas traveling, a result of continued economic recovery, and an increase in

demand for international freight transport, despite high oil prices.

The residential/commercial/public sector will likely indicate a substantial slowdown in

the demand increase rate at 1.8% in 2011. This is because of base effects as it is

assumed that average year temperatures will be recovered as well as a slowdown in

the level of increase in income levels.

20 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Outlook on final energy demand

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지20 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: Values in parentheses are the year-on-year growth rate (%); p refers to tentative figures; e refers to forecasts

21http://www.keei.re.kr

Summary

Category2010p 2011e

1/4 2/4 3/4 4/4 Annual 1/4 2/4 3/4 4/4 Annual

Industry 28.9 28.3 27.6 29.7 114.5 29.7 29.5 28.7 31.0 119.0(Million TOE) (13.8) (8.5) (3.8) (5.9) (7.9) (2.8) (4.2) (4.0) (4.6) (3.9)

-Excluding for 13.4 13.5 12.9 14.5 54.3 14.0 14.0 13.3 15.1 56.4raw materials (13.3) (7.8) (2.6) (8.0) (7.9) (4.6) (3.7) (2.8) (4.6) (4.0)

Transport 8.5 9.2 9.5 9.6 36.8 8.8 9.4 9.7 9.8 37.6(Million TOE) (0.8) (1.9) (4.2) (2.8) (2.4) (3.2) (1.9) (2.0) (2.1) (2.3)

Residential/commercial 14.9 8.8 7.3 11.8 42.8 15.3 8.9 7.4 11.9 43.5/public

(Million TOE) (7.5) (11.0) (6.7) (3.4) (6.9) (2.7) (0.9) (2.6) (0.7) (1.8)

Total 52.3 46.4 44.3 51.1 194.1 53.8 47.8 45.8 52.7 200.2Million TOE (9.7) (7.6) (4.4) (4.7) (6.6) (2.8) (3.1) (3.3) (3.2) (3.1)

Total 36.8 31.5 29.6 35.9 133.9 38.1 32.3 30.4 36.8 137.6-Excluding for (7.8) (6.8) (4.1) (5.0) (6.0) (3.5) (2.4) (2.5) (2.6) (2.8)raw materials

Town gas 7.9 4.3 2.8 5.7 20.8 8.1 4.5 3.1 5.9 21.7(Billion m3) (14.5) (20.9) (6.1) (7.8) (12.6) (2.8) (4.6) (9.5) (4.4) (4.5)

Oil 189.0 187.8 187.0 204.2 768.0 194.7 190.4 188.6 206.0 779.6(Million bbl) (1.0) (0.9) (3.3) (3.2) (2.1) (3.0) (1.3) (0.9) (0.9) (1.5)

-Excluding 107.9 105.7 104.0 118.7 436.3 106.0 103.7 102.0 117.6 429.2naphtha (1.9) (-0.3) (1.9) (2.6) (1.6) (-1.8) (-1.9) (-1.9) (-1.0) (-1.6)

Electricity 112.5 103.6 109.1 109.0 434.2 121.4 110.6 114.8 115.4 462.2(TWh) (12.2) (10.3) (10.2) (7.7) (10.1) (7.9) (6.7) (5.3) (5.9) (6.5)

Coal 11.3 10.2 9.4 10.4 41.2 10.6 10.4 9.8 11.0 41.9(Million ton) (37.0) (24.1) (-1.2) (3.9) (14.7) (-5.5) (2.1) (5.1) (5.7) (1.6)

--Excluding 3.9 4.0 3.5 4.3 15.8 4.4 4.1 3.6 4.4 16.6coking coal (6.5) (17.1) (-9.1) (3.3) (4.0) (12.6) (1.7) (2.1) (2.7) (4.8)

Thermal and 2,001 1,486 1,269 2,009 6,765 2,173 1,609 1,390 2,192 7,364other

(Thousand TOE) (7.0) (6.8) (3.7) (3.9) (5.4) (8.6) (8.3) (9.5) (9.1) (8.9)

<Outlook on final energy demand>

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지21 매일3 MAC2PDF_IN 600DPI 125LPI T

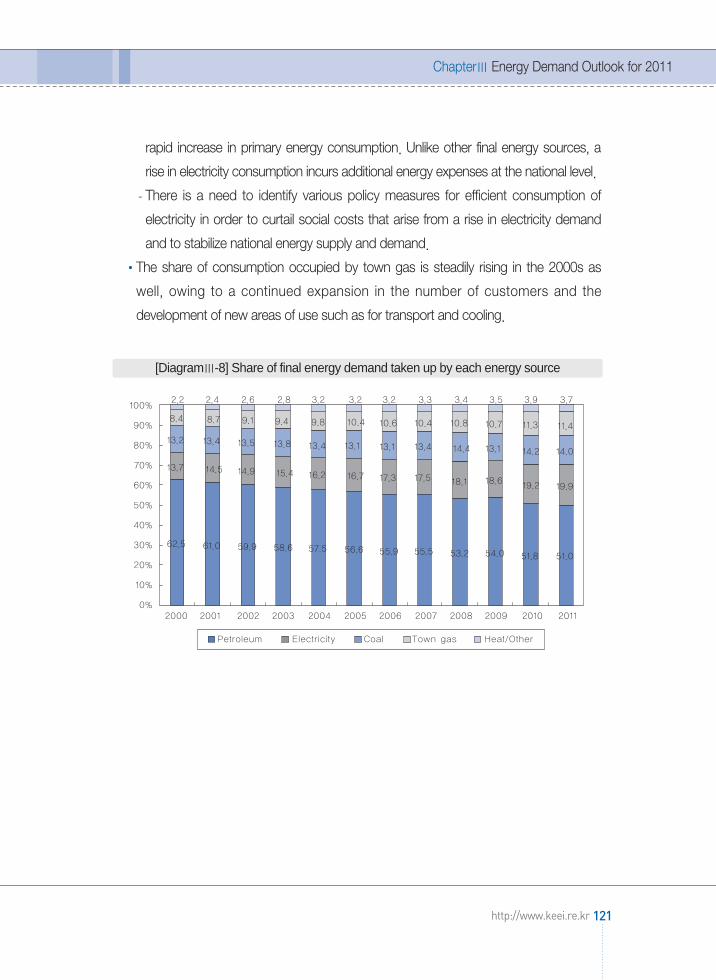

In terms of each energy source, most energy sources will likely post a lower

consumption increase rate in 2011 compared to the previous year due to a slowdown

in economic growth and base effects from the assumption that average year climate

conditions will be recovered.

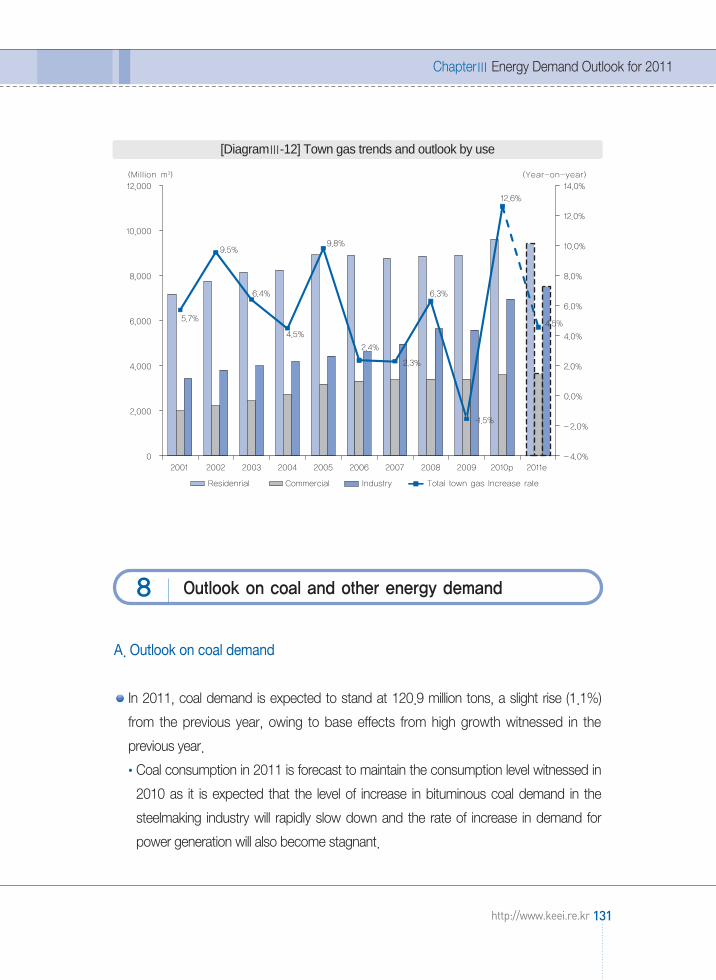

Town gas consumption went up 12.6% in 2010, owing to a surge in demand for

industrial use resulting from economic recovery and abnormally low temperatures.

However, the level of increase is expected to slow down to 4.5% in 2011.

In 2011, oil consumption for industrial raw material use is expected to lead a rise in oil

demand.

- Oil demand for raw material use, including naphtha, solvent, and asphalt, is

expected to indicate a year-on-year rise of 2.1% owing to continued favorable

conditions in the economy and a rise in domestic ethylene production as a result of

influence from the Japanese earthquake.

Electricity will likely indicate relatively high growth of 6.5% in 2011 resulting from

several factors: continued, sound economic growth, relatively low charge, continued

dissemination of equipment that use electricity, and convenience in use.

In 2011, coal consumption in the final sector is forecast to see an increase of 1.6%

owing to forecasts of decreased demand for cement production as well as a

slowdown in bituminous coal demand for steel making as a result of base effects.

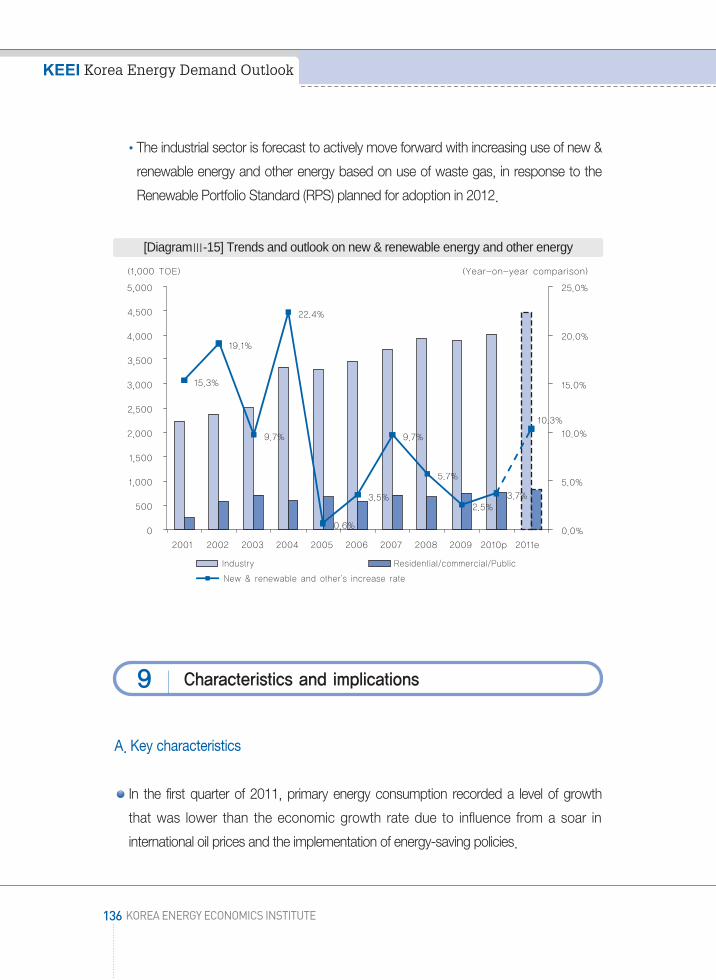

Thermal energy is forecast to witness a slowdown in the consumption increase rate

at 4.5% in 2011. New & renewable energy is expected to post an increase rate of

approximately 10%, thanks to the government’s active implementation of

propagation policies.

22 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지22 매일3 MAC2PDF_IN 600DPI 125LPI T

In the first quarter of 2011, primary energy consumption recorded a level of growth

that was lower than the economic growth rate due to influence from a soar in

international oil prices and the implementation of energy-saving policies.

From the second quarter of 2009 through the fourth quarter of 2010, quarterly

primary energy consumption continued a level of growth that was higher than the

economic growth rate. In the first quarter of 2011, however, it recorded a level of

increase that was lower than the economic growth rate (4.2%) at 3.7%.

Primary energy consumption indicated a relatively low increase rate in the first quarter

of 2011 despite continued favorable conditions in the economy as well as a cold

wave. The average temperature in January (-7.2℃) was as much as 5.4℃ lower than

average month temperatures.

* A 10.5% increase in industrial activity (mining/manufacturing industry production

index) in the first quarter: (Year 2010) 129.8 → (Year 2011) 143.3

* A 6.9% increase in HDD in the first quarter: (Year 2010) 1,588 → (Year 2011) 1,696

This seems to be partly attributable to a sudden rise in international oil prices and the

resulting execution of energy-saving policies such as the ‘measure on placing

restrictions on heating temperatures in buildings’.

* Dubai oil price: (December 2010) $88.95/bbl → (March 2011) $108.53/bbl (22.0%↑)

- The ‘measure on placing restrictions on heating temperatures in buildings’was

carried out for four weeks (January 24-February 18, 2011), targeting 441 large

buildings, in response to high oil prices as well as record-breaking peak demand.

All target buildings maintained appropriate heating temperature levels.

- Results of an analysis on the level of contribution made by each factor towards a

rise in primary energy consumption in the first quarter of 2011 lead to the

assumption that the government’s implementation of energy-saving policies and a

rise in oil prices, excluding economic growth and temperature effects, resulted in

energy consumption-reducing effects of 2.1 million TOE.

23http://www.keei.re.kr

Summary

Key characteristics

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지23 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: The energy efficiency effect includes all factors that trigger a change in energy consumption excluding thetemperature effect and economic growth effect such as changes in the industrial structure and energy pricesas well as technical energy efficiency improvements.

Forecasts on energy intensity improvements in 2011

Energy intensity (TOE/million won) deteriorated in 2009 and 2010, but is expected to

improve to 0.248 in 2011.

- The worsened energy intensity of 2009 resulted from a 1.1% rise in primary energy

consumption, triggered by favorable conditions in production activities in industries

that consume great amounts of energy, against the backdrop of a substantial

slowdown in the economic growth rate (0.3%) due to the financial crisis.

- The worsened energy intensity of 2010 resulted from a soar in energy demand for

heating and cooling purposes, a result of abnormal climate conditions (abnormally

low temperatures in the winter and high temperature and humidity levels in the

summer), an increase in the number of steel facilities (Hyundai Steel and Dongkuk

Steel), and an increase in industrial activities owing to the economic recovery.

The worsened energy intensity in 2009 and 2010 seems to be temporary amid mid-

to long-term energy efficiency improvements.

24 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

[Level of contribution of each factor towards a rise in primary energy consumption in the first quarter of 2011]

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지24 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: p refers to tentative figures, e refers to forecasts

Continued rapid increase in electricity consumption

Electricity maintained a rapid increase in consumption due to several factors: low

charge; continued favorable conditions in industries that consume a great amount of

electricity; and diversification, increased size, and propagation of electric equipments.

- Electricity consumption indicated annual average growth of 9.8% in the 1990s, and

continued an annual average increase of 6.1% in the 2000s, the highest among key

final energy sources.

- Even in 2008 and 2009, when the final energy consumption increase rate stood at

a mere 0.6% and -0.3%, respectively, electricity consumption recorded relatively

high growth of 4.5% and 2.4%, respectively.

- Electricity consumption indicated two-digit growth (10.1%) in 2010, attributable to

the economic recovery and temperature effects. It is forecast to record high growth

of 6.5% in 2011 as well.

The rapid increase in consumption of electricity has expanded the level of

contribution made by electricity (triggering input of energy for power generation)

towards a rise in primary energy consumption.

- The level of contribution of electricity towards a rise in primary energy is forecast to

go up from 46.3% in 2010 to around 54.6% in 2011.

Electricity is expected to continue to perform leading roles in Korea’s energy demand

for the time being as a result of increased value added of core manufacturing industry

products, which consume great amounts of electricity, and changes in lifestyles

triggered by technological development.

25http://www.keei.re.kr

Summary

Category 2005 2006 2007 2008 2009 2010p 2011e

Primary energy consumption 3.8 2.1 1.3 1.8 1.1 7.2 3.5increase rate (%)

Energy intensity (TOE/Million won) 0.264 0.256 0.247 0.246 0.248 0.250 0.248

<Outlook on energy intensity>

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지25 매일3 MAC2PDF_IN 600DPI 125LPI T

Energy demand increasingly sensitive to temperature changes

It has been assessed that temperature changes had a substantial influence on

primary energy consumption in the 2000s. In particular, the climate factor served to

substantially raise energy consumption in 2005 and 2010.

- This is because energy consumption now flexibly responds to temperature changes

in tandem with increased dissemination and use of cooling and heating equipment,

a result of economic growth and abnormal climate conditions that have frequently

occurred in the 2000s.

Of peak demand in the summer and winter, demand for cooling and heating

purposes is taking up a higher percentage, according to analysis results (Korea

Power Exchange). This supports the fact that energy demand is becoming sensitive

to temperature changes.

- The share of peak load taken up by electricity used for heating purposes is

assumed at more than 25% at peak demand last winter (December 2010-February

2011).

Source: Press release by the Korea Power Exchange (Results of analysis of winter peak demand from 2010 to 2011),March 7, 2011

26 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

[Changes in share of winter peak demand taken up by heating load]

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지26 매일3 MAC2PDF_IN 600DPI 125LPI T

It is forecast that peak demand (74,770MW) this summer (June-August 2011) will

record a year-on-year rise of 7.0%4), of which demand for cooling will likely reach

17,290MW, accounting for 23.1% of total electricity demand.

- Electricity demand for cooling is expected to indicate a year-on-year increase of

12.3% at peak load in the summer of 2011. It is thus forecast to increase much

rapidly than the average rate of increase in electricity demand.

As such, it is becoming increasingly important to come up with policies on stabilizing

energy supply and demand, such as measures on electricity demand side

management in preparation for peak demand in the summer and winter.

It is forecast that oil dependence regarding primary energy consumption will decrease.

The share of oil reached its peak at 63% in 1994 and continued to decrease

afterwards. It stood at 40.0% in 2010 and is expected to further drop to 39.3% in

2011.

- The primary energy share taken up by naphtha, which is mainly used for industrial

raw materials, reached 16.3% in 2010, higher than LNG (15.9%) and nuclear

energy (12.9%). It is forecast to go up to 16.6% in 2011 as a result of an upswing in

the petrochemical industry.

- When excluding naphtha, the share of primary energy taken up by oil is expected to

decrease from 23.7% in 2010 to 22.7% in 2011. The share of primary energy

occupied by oil, excluding naphtha, is lower than that of coal (28.6%) and is almost

at the LNG (17.0%) level.

Considering Korea’s industrial structure, where the level of contribution of the

petrochemical industrial to the economy is high, the nation’s oil dependence target

should be set targeting petroleum products for fuel, excluding for industrial raw

material use (naphtha, asphalt, etc.).

27http://www.keei.re.kr

Summary

4) Refer to press release of the Ministry of Knowledge Economy (“Full launch of an emergency measure teamon electricity supply/demand this summer”, June 20, 2011)

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지27 매일3 MAC2PDF_IN 600DPI 125LPI T

In 2011, the value of energy imports is expected to reach a record-breaking 164.1

billion dollars, a year-on-year rise of 34.9%.

In 2010, the value of imported energy (oil, natural gas, coal, uranium) stood at 121.7

billion dollars, a year-on-year increase of 33.4%.

- The amount of energy imports (oil, natural gas, coal) indicated a year-on-year

increase of 8.8%, but the value of imports rose substantially owing to a surge in

energy prices such as international oil prices.

The value of energy imports in 2011 is estimated to reach a record-breaking 164.1

billion dollars.

- The level of increase in energy demand (imports) is expected to slow down this

year, but the value of energy imports is expected to indicate a year-on-year rise of

34.9%, owing to continued increase in international energy prices.

28 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

[Trends in oil dependence and forecasts]

Policy implications

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지28 매일3 MAC2PDF_IN 600DPI 125LPI T

* Oil: (’09) $66.6 billion → (’10) $90.9 billion → (’11) $126.3 billion

* LNG: (’09) $13.9 billion → (’10) $17 billion → (’11) $22.8 billion

* Bituminous coal: (’09) $9 billion → (’10) $11.4 billion → (’11) $13.4 billion

Notes: 1. Values in parentheses are the year-on-year growth rate (%); p refers to tentative figures; e refers to forecasts

There is a need to strengthen measures on stabilizing LNG supply and demand in

2011.

LNG consumption rose 22.6% in 2010 as a result of an increase in demand for

power generation. It is expected to mark high growth of 10.3% in 2011 as well.

* Rate of increase in consumption for power generation: (’09) -13.2% → (’10) 38.3%

→ (’11) 16.0%

* Rate of increase in consumption for town gas: (’09) 0.9% → (’10) 12.6% → (’11)

5.6%

- The increase in LNG demand for power generation, which is used to handle peak

load, is a result of a rise in electricity demand and limited construction of base-load

29http://www.keei.re.kr

Summary

Category 2006 2007 2008 2009 2010p 2011e

Primary energy 233.4 236.5 240.8 243.3 260.8 269.9consumption

(Million TOE) (2.1) (1.3) (1.8) (1.1) (7.2) (3.5)

Amount of imports 238.7 246.8 255.5 257.1 279.6 285.2(Million TOE) (4.5) (3.4) (3.5) (0.6) (8.8) (2.0)

Unit cost (CIF)

- Oil ($/barrel) 62.8 69.3 98.3 60.8 78.7 103.4(24.4) (10.4) (41.7) (-38.2) (29.6) (31.3)

- LNG ($/ton) 472.2 494.9 726.6 537.3 521.6 640.0(21.9) (4.8) (46.8) (-26.1) (-2.9) (22.7)

- Bituminous 69.3 75.6 130.6 100.3 107.7 125.0coal ($/ton) (-4.2) (9.1) (72.8) (-23.2) (7.4) (16.1)

Value of imports 856 950 1,415 912 1,217 1,641(100 million dollars) (28.3) (11.0) (49.0) (-35.6) (33.4) (34.9)

<Energy consumption and import and outlook>

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지29 매일3 MAC2PDF_IN 600DPI 125LPI T

power generation facilities (nuclear power, bituminous coal).

* Base-load power facility increase rate (as of the end of the year): (’09) 1.2% →

(’10) 2.5% → (’11) 2.4%

* Electricity demand increase rate: (’09) 2.4% → (’10) 10.1% → (’11) 6.5%

- In addition to LNG demand for power generation, LNG demand for town gas also

soars in case of a cold wave. As such, there is a need for thorough reviews and

measures to achieve stability in LNG supply and demand in the winter.

- There is also a possibility of a sharp rise in LNG demand to replace nuclear power

generation in Japan from the second half of the year, making it increasingly

important to draw up measures on stabilizing supply and demand in the winter.

There is a need to strengthen electricity demand management and boost efficiency in

use of electricity.

There are various restraints on the expansion of power generation facilities needed to

satisfy electricity demand. As such, there is a need to concentrate on electricity

demand management policies at the national level.

What is important is the smooth implementation of the load management system that

was adopted at the end of 2010.

- There is a need to take timely measures against mid-week changes in

supply/demand conditions that result from abnormal weather through flexible

operation5) of the ‘weekly forecast demand adjustment’system, which is a load

management charge system.

- To enhance effectiveness of load management, there is a need to expand the

target of load management from the previous industrial sector (steel making,

cement, etc.) to the service industry. There is also a need to extend the load

management period and expand targets, leading to the need for additional

30 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

5) Previously, a notice on one-time execution was made on the Friday the week earlier. By makingimprovements to the system, the first notice is now made on the Friday the week before, followed by asecond notice during the week in consideration of changes in conditions.

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지30 매일3 MAC2PDF_IN 600DPI 125LPI T

budgetary support.

- There is also a need to encourage the maintenance of appropriate cooling and

heating temperatures in large buildings, where energy is excessively consumed, by

spreading information on how to use energy efficiently.

There is a need to adjust the electricity charge to a realistic level so as to reduce

excessive consumption (especially for heating purposes) of electricity.

- Large shopping malls, financial institutes, and other organizations in the service

industry tend to provide excessive heating and cooling in Korea.

- To remove such practices that lead to the waste of resources, there is an urgent

need to strengthen the market functions of energy prices.

31http://www.keei.re.kr

Summary

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지31 매일3 MAC2PDF_IN 600DPI 125LPI T

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지32 매일3 MAC2PDF_IN 600DPI 125LPI T

Energy Demand Outlook for 2011

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지33 매일3 MAC2PDF_IN 600DPI 125LPI T

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지34 매일3 MAC2PDF_IN 600DPI 125LPI T

ChapterⅠInternational Energy

Market Trends

1. Trends in the international oil market and oil exports/imports

2. Trends in the international natural gas market

3. Trends in the international coal market

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지35 매일3 MAC2PDF_IN 600DPI 125LPI T

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지36 매일3 MAC2PDF_IN 600DPI 125LPI T

A. Trends in international oil prices and domestic petroleum product prices

International oil prices sharply rose after the second half of 2010 and reached the

highest level since 2008 in April 2011. However, the death of Osama bin Laden,

concerns of decreased oil demand as a result of concerns over a global economic

downturn, and the strong dollar led to international oil prices recording a 6.7% drop

from the previous month to stand at $108.4/barrel (Dubai oil).

International petroleum product prices slightly went down in tandem with a decrease

in international crude oil prices. The price of gasoline stood at (92RON) $109.6/barrel,

while that of diesel recorded $117.5/barrel and naphtha $97.9/barrel.

Notes: Values in parentheses indicate the year-on-year increase rate (%)

ChapterⅠ International Energy Market Trends

37http://www.keei.re.kr

Trends in the international oil market and oil exports/imports1

(Unit: $/Bbl, %)

Category WTI Brent Dubai

Year 2008 99.92 (27.21) 97.47 (24.85) 94.29 (25.86)

Year 2009 61.94 (-37.98) 61.73 (-35.74) 61.92 (-32.37)

Year 2010 79.49 (17.55) 79.66 (17.93) 78.13 (16.21)

January 2011 89.54 (14.30) 96.78 (26.69) 92.55 (20.59)

February 2011 89.66 (17.28) 103.90 (40.75) 100.24 (36.20)

March 2011 102.97 (26.73) 114.64 (45.21) 108.53 (40.33)

April 2011 109.96 (30.13) 123.26 (45.17) 115.76 (38.40)

May 2011 101.29 (37.42) 114.27 (51.91) 108.04 (40.60)

<TableⅠ-1> Changes in international crude oil prices

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지37 매일3 MAC2PDF_IN 600DPI 125LPI T

B. Trends in petroleum product prices in Korea

In May 2011, consumer prices of gasoline and diesel in Korea recorded a year-on-year

increase of 11.9% and 16.5%, respectively. Consumer prices of butane for vehicles

went up 12.0%.

The prices of diesel and butane recorded relatively rapid growth. The relative price of

diesel and butane for vehicles against gasoline was around 91.5% and 55.1%,

respectively.

Notes: Values in parentheses indicate the relative price against gasoline prices (%)

Consumer prices of petroleum products in Korea are roughly 2.4 times (gasoline) and

2.0 times (diesel) higher than prices in the Singapore spot market around two weeks

earlier.

38 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

(Unit: Won/liter, Won/kg, %)

Category Gasoline Diesel Butane for transport

Year 2008 1,692.14 1,614.44 (95.4) 1,009.04 (59.6)

Year 2009 1,600.72 1,397.47 (87.3) 828.70 (51.8)

Year 2010 1,710.41 1,502.80 (87.9) 952.16 (55.7)

January 2011 1,825.40 1,621.70 (88.8) 1,183.80 (58.5)

February 2011 1,850.00 1,651.70 (89.3) 1,214.10 (57.8)

March 2011 1,939.00 1,755.90 (90.6) 1,296.20 (55.1)

April 2011 1,951.20 1,792.80 (91.9) 1,357.50 (54.8)

May 2011 1,938.50 1,772.90 (91.5) 1,369.60 (55.1)

<TableⅠ-2> Changes in consumer prices of petroleum products in Korea

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지38 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: Gasoline (92RON) and diesel (0.05%) prices were calculated by using the weekly average price of the Singaporespot market and the weekly average exchange rate

C. Trends in crude oil and petroleum product exports/imports

In March 2011, the crude oil import volume stood at 80.1 million barrels, recording a

year-on-year rise of 19.8%. The import value (based on CIF) rose 62.5% to reach 8.41

billion dollars.

The import volume for the first quarter of 2011 posted 235.1 million barrels, a year-on-year

rise of 13.3%, while the value posted a rise of 43.4% to stand at 22.96 billion dollars.

Crude oil imports maintained a high level of increase compared to the same period

the previous year, attributable to a soar in petroleum product exports and a rise in

production activities resulting from a favorable turn in the economy.

From January through March 2011, petroleum product imports recorded a year-on-

year increase of 0.1% to post 73.6 million barrels. In contrast, petroleum product

exports witnessed a year-on-year rise of 25.9% to reach 90.0 million barrels.

Imports of naphtha and heavy oil went down, triggered by a rise in domestic

production. In contrast, LPG imports went up. Overall, petroleum product imports

ChapterⅠ International Energy Market Trends

39http://www.keei.re.kr

[DiagramⅠ-1] Changes in petroleum product import prices and consumer prices

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지39 매일3 MAC2PDF_IN 600DPI 125LPI T

remained at a level similar to that recorded in the same period the previous year.

Exports substantially rose as a result of improvements in the refining margin and

petroleum product support for the Japanese earthquake.

A. Trends in supply and demand

International natural gas demand, which went down in 2009 due to the economic

downturn, turned into an upward trend in 2010 to record 3,170.6 billion ㎥, a 4.9% rise

from the previous year.

The relatively low price and increased industrial demand in OECD countries and

emerging countries have led a rise in natural gas consumption.

International natural gas production, which went down 3.1% in 2009, rose 4.8% in

2010 from the previous year to post 3,159.6 billion m3.

Various factors have led to an increase in the international natural gas production

volume: Russia’s recovery of production power, a rise in unconventional gas

production in the US, and increased LNG production in Qatar.

Notes: Values in parentheses indicate the year-on-year growth rate (%)Source: EIU, World commodity forecasts: Industrial raw materials, June 2011

40 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Trends in the international natural gas market2

(Unit: Billion m3)

Category Consumption Production

Year 2008 3,140.8 (3.1) 3,112.6 (4.1)

Year 2009 3,023.2 (-3.7) 3,014.9 (-3.1)

Year 2010 3,170.6 (4.9) 3,159.6 (4.8)

<TableⅠ-3> Trends in international natural gas supply and demand

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지40 매일3 MAC2PDF_IN 600DPI 125LPI T

B. Price trends

In 2010, international natural gas prices (prices at which natural gas was imported by

Japan) reached US$ 10.85/mBtu, a year-on-year rise of 21.4%. It went up to US$

12.05/mBtu in the first quarter of 2011.

The worsened nuclear power plant incident in Japan contributed to a rise in

international LNG prices, including LNG prices in Europe. However, it did not

influence the US to a great extent as the US is able to internally obtain natural gas

thanks to shale gas development.

Notes: Natural gas prices for the US are based on Henry Hub, while prices for Europe (excluding the UK) are based onimport border prices. Prices for Japan are LNG import prices.

Source: EIU, World commodity forecasts: Industrial raw materials, June 2011

Notes: Natural gas prices for the US are based on Henry Hub, while prices for Europe (excluding the UK) are basedon import border prices.

Source: EIU, World commodity forecasts: Industrial raw materials, May 2010-June 2011

ChapterⅠ International Energy Market Trends

41http://www.keei.re.kr

(Unit: US$/mBtu)

CategoryYear 2010 Year 2011

1/4 2/4 3/4 4/4 Annual 1/4

US 5.15 4.32 4.28 3.80 4.39 4.18

Europe 8.84 7.51 8.26 8.54 8.29 9.45

Japan 10.32 10.95 11.22 10.91 10.85 12.05

<TableⅠ-4> Trends in international natural gas prices

[DiagramⅠ-2] Trends in international natural gas prices

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지41 매일3 MAC2PDF_IN 600DPI 125LPI T

International coal prices have been continuing an upward trend since March 2009,

owing to a rise in demand resulting from the global economic recovery. Last winter,

international coal prices remained strong, resulting from localized heavy rain in coal

exporting countries and an abnormal cold wave in the northern hemisphere.

What mainly led the rise in prices is demand in emerging countries in Asia such as

China and India.

- China shifted into a pure importer of steam coal in 2009, and imported 82 million

tons (net import of 65.6 million tons) in 2010. The country has become the world’s

No. 2 steam coal importer, following Japan (Platts, May 2011).

- India is also recording a continuous rise in imports, although the rise is not as sharp

as China. The country imported 45 million tons in 2010 (World’s No. 5 importer).

Total imports in Asia (1 million tons): (’08) 392.3 ⇒ (’09) 428.0 ⇒ (’10) 451.5

Source: Datastream (IMF Primary Commodity Price)

42 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

Trends in the international coal market6)3

6) For this chapter, information provided in the ‘International Steam Coal Price Trends and Outlook’section ofthe 「Global Energy Market Insight (Volume 11-12)」was extracted and organized.

[DiagramⅠ-3] International coal price trends

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지42 매일3 MAC2PDF_IN 600DPI 125LPI T

The rise in prices at the end of 2010 and in January 2011 is mainly attributable to

heavy rainfall in exporting countries.

- La Nina caused localized heavy rain in major coal exporting countries - Australia,

Indonesia, Republic of South Africa, and Venezuela. This led to issues in production

and shipment.

- The abnormal cold wave in the northern hemisphere is further aggravating coal

supply/demand conditions. Strengthened export control by the Indonesian

government and a rise in freight rates in the Republic of South Africa also

contributed to the rise in prices.

Spot prices in Asia are becoming stabilized after reaching their peak in January 2011.

- This is a result of improvements in supply/demand conditions, attributable to the

recovery of coal production and transport facilities, a rise in temperatures, and

stoppage of a coal power plant because of the Great East Japan Earthquake.

The Great East Japan Earthquake in March led to the stoppage of a 7,650MW coal

power plant, triggering a drop in the spot prices of steam coal.

- Spot prices of steam coal in Australia went down around 10 dollars/ton in the week

following the earthquake, compared to the week of the earthquake.

- In the mid-term future, steam coal demand will likely go up as a result of

improvements in the level of use of existing power plants, but this will likely have a

limited influence on the international coal market.

ChapterⅠ International Energy Market Trends

43http://www.keei.re.kr

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지43 매일3 MAC2PDF_IN 600DPI 125LPI T

Notes: Values in parentheses indicate the year-on-year growth rateSource: EIU, World commodity forecast: Industrial raw materials, June 2011

44 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

(Unit: 1,000 tons)

Category 2008 2009 2010

China 2,800 3,050 3,575

US 1,063 973 983

India 516 555 560

Australia 398 399 415

Russia 325 298 314

Indonesia 274 302 324

Global total 6,808 6,967 7,612(5.9) (2.3) (9.3)

<TableⅠ-5> Trends in global coal production

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지44 매일3 MAC2PDF_IN 600DPI 125LPI T

ChapterⅡEconomic and Energy

Consumption Trends in Korea

1. Economic trends in Korea

2. Trends in primary energy consumption

3. Trends in final energy consumption

4. Trends in petroleum product consumption

5. Trends in electricity consumption

6. Trends in LNG and town gas consumption

7. Trends in coal and other energy consumption

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지45 매일3 MAC2PDF_IN 600DPI 125LPI T

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지46 매일3 MAC2PDF_IN 600DPI 125LPI T

Outline

According to Industrial Activity Trends announced by Statistics Korea in April 2011,

the mining/manufacturing industry, retail sales, facility investments, and completed

construction went down from the same month the previous year in April. Service

production indicated year-on-year growth. The cyclical component of coincident

index and composite leading index went down from the previous month in terms of a

comparison to the same month the previous year.

Production trends

Mining/manufacturing industry production went up 6.9% from the same month the

previous year, thanks to favorable conditions in semiconductors and parts (20.6%)

and in the automobile industry (8.5%), resulting in an upward trend for 22

consecutive months. This is despite a slump in image/sound/communication

equipment (-18.2%) and electric equipment (-5.7%).

The average operating rate in the manufacturing sector dropped 2.0%p from the

previous month to stand at 80.5%.

In terms of the service industry, there was a decrease in real estate/lease (-16.1%),

education (-0.1%), etc., but a rise in finance/insurance (9.1%), business facilities

management/business support (7.4%), health and social welfare (4.5%), etc. led to

an overall increase of 3.1% from the same month the previous year.

Consumption trends

Retail sales witnessed a year-on-year rise of 5.0% owing to a rise in sales of durables (15.7%)

including computers, telecommunication equipment, and passenger cars, and quasi-

durables (7.2%) such as clothes, despite a drop in nondurables (-1.7%) such as car fuel.

ChapterⅡ Economic and Energy Consumption Trends in Korea

47http://www.keei.re.kr

Economic trends in Korea7)1

7) Summary of Industry Activity Trends (April 2011) of Statistics Korea

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지47 매일3 MAC2PDF_IN 600DPI 125LPI T

Source: Statistics Korea, Industrial Activity Trends (April 2011), May 2011 The Bank of Korea, Economic Statistics System (Price index)

48 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

(Unit: Compared to the same period (month) last year, %)

CategoryYear 2010 Year 2011

Annual 1/4 4/4 April 1/4p February Marchp Aprilp

Production

Consumption

Investment

Prices

Sales of consumer goods(compared to the same

month (period))

Consumer prices

Producer prices

Mining/manu

facturingindustry

Production(Compared tosame month(period))

(Automobiles)

Shipment

·Exports

Inventory

Average operating rate

Productioncapacity

Facility investmentindex

Domestic ordersfor machinery

Constructioncompleted in Korea

Construction orders in Korea

·Domesticdemand

·Manufacturingsector( I C T )

Manufacturingindustry

Facility

Construction

16.2

16.7

25.2

23.1

14.4

11.5

18.2

17.4

81.2

7.2

6.6

25.1

11.2

-3.3

-18.7

2.9

3.8

25.4

26.6

45.9

48.8

20.9

19.5

22.7

7.5

80.4

6.2

9.7

30.0

10.3

3.4

-1.6

2.7

2.6

11.7

12.0

15.2

10.2

11.9

8.3

16.9

17.4

80.8

7.4

5.1

13.6

11.3

-4.3

-40.2

3.6

5.0

19.5

20.1

31.0

35.0

16.5

15.5

18.0

12.5

81.7

6.6

7.3

32.5

27.2

-5.7

-14.1

2.6

3.2

10.6

10.8

14.3

16.1

11.9

7.2

18.4

10.3

83.2

6.8

5.1

6.6

19.5

-12.7

-12.8

4.5

6.7

9.0

9.3

17.7

12.8

10.2

5.9

16.1

11.2

82.2

6.9

-0.8

1.0

26.1

-20.0

-16.7

4.5

6.6

9.0

9.2

9.1

11.8

10.6

5.5

17.8

10.3

82.5

6.5

5.2

0.3

14.4

-8.1

13.7

4.7

7.3

6.9

7.1

12.4

8.5

7.3

2.2

14.3

8.9

80.5

6.5

5.0

-1.1

9.7

-8.9

-2.7

4.2

6.8

<TableⅡ-1> Recent economic trends

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지48 매일3 MAC2PDF_IN 600DPI 125LPI T

- In terms of different retail business types, there was a rise in convenience stores

(15.7%), department stores (13.0%), nonstore retailing (9.3%), and large discount

stores (7.5%).

Investment trends

Facility investments saw a year-on-year drop of 1.1% due to a decrease in

investments in transportation equipment such as passenger cars and airplanes,

despite an increase in investments in machinery such as conveying machinery for

industrial use.

The number of domestic orders for machinery went down in the public sector.

However, the number of orders rose for other transportation equipment and

machinery and equipment, etc. in the private manufacturing sector, leading to an

overall year-on-year rise of 9.7%.

Completed construction witnessed a year-on-year drop of 8.9% owing to decreased

performance in construction and public works.

Construction orders (at current prices) posted a year-on-year decrease of 2.7%,

owing to decreased orders in the private sector for electricity generation, electric

power transmission, etc. and in the public sector for flood control afforestation,

housing, etc.

Business indices

The cyclical component of coincident index went down 0.7%p from the previous

month, attributable to a drop in the domestic shipment index, manufacturing

operation ratio index, wholesale and retail sales index, and completed construction

value, despite a rise in non-farm payrolls and import value.

The leading index’s year-on-year comparison recorded a 0.5%p decrease from the

previous month, owing to a drop in the consumer expectation index, the ratio of

those seeking to hire to those seeking jobs, capital good import value, inventory cycle

index, etc., despite an increase in the value of construction orders and KOSPI (Korea

Composite Stock Price Index).

ChapterⅡ Economic and Energy Consumption Trends in Korea

49http://www.keei.re.kr

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지49 매일3 MAC2PDF_IN 600DPI 125LPI T

Source: Statistics Korea, Industrial Activity Trends (April 2011), May 2011

Source: Statistics Korea, Korean Statistical Information Service (http://kosis.kr). As of April 2011.

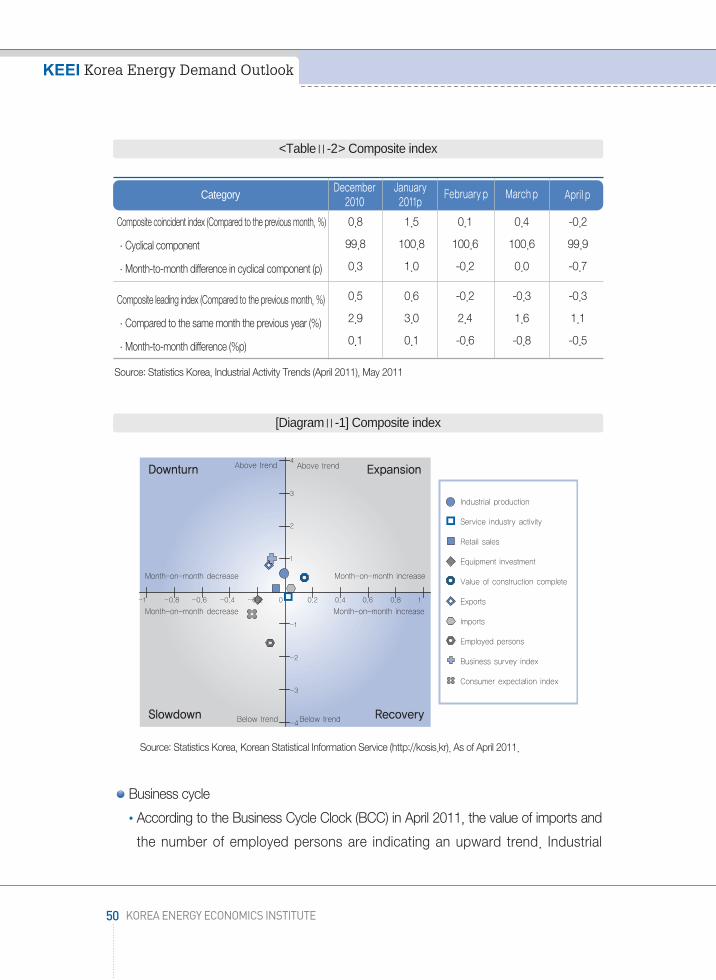

Business cycle

According to the Business Cycle Clock (BCC) in April 2011, the value of imports and

the number of employed persons are indicating an upward trend. Industrial

50 KOREA ENERGY ECONOMICS INSTITUTE

KEEI Korea Energy Demand Outlook

CategoryDecember

2010January2011p

Februaryp Marchp Aprilp

0.8 1.5 0.1 0.4 -0.2

99.8 100.8 100.6 100.6 99.9

0.3 1.0 -0.2 0.0 -0.7

0.5 0.6 -0.2 -0.3 -0.3

2.9 3.0 2.4 1.6 1.1

0.1 0.1 -0.6 -0.8 -0.5

<TableⅡ-2> Composite index

Composite coincident index (Compared to the previous month, %)

·Cyclical component

·Month-to-month difference in cyclical component (p)

Composite leading index (Compared to the previous month, %)

·Compared to the same month the previous year (%)

·Month-to-month difference (%p)

[DiagramⅡ-1] Composite index

수요전망 내지13-2 문 2011.9.16 2:10 PM 페이지50 매일3 MAC2PDF_IN 600DPI 125LPI T

production, retail sales, the value of exports, and business survey index are in the

slowdown phase.

The equipment investment index, value of construction complete, and consumer

expectation index are on a downward trend, while service industry activity is making

a recovery.

Compared to March, the value of imports, the number of employed persons, and

service industry activity went up.

In contrast, industrial production, retail sales, value of exports, business survey index,

equipment investment, value of construction complete, and consumer expectation

index went down.

Primary energy consumption for 2010 tentatively reached 260.8 million TOE, a year-

on-year rise of 7.2%.

Primary energy consumption went up by 10.3% in the first quarter and 7.3% in the

second quarter according to quarterly economic growth patterns. The rate of

increase stood at 5.3% in the third quarter and 5.8% in the fourth quarter, indicating

a slowdown in the level of increase in the second half of the year.

The rise in primary energy consumption in 2010 is attributable to the economy taking

a favorable turn (including base effects from the economic downturn of the previous

year) and temperature effect (abnormally low temperatures in the winter and high

temperatures and high humidity in the summer).

- An upswing in production in industries that consume a great amount of electricity

such as fabricated metal as well as an expansion of steel making facilities that

consume a great amount of electricity led the increase in energy consumption in