Blog marki CROPP - prezentacja na Social Media Day, Wrocław 23.02.2012

Kiev Retail Market Overview

Q4 2016

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Kiev Retail Market Snapshot, Q4 2016

2

Supply

Quality shopping centre stock 957,800 sq m

Quality shopping centre stock per 1,000 inhabitants 330 sq m

Completions, Q4 2016 138,500 sq m

Completions, 2016 156,700 sq m

Announced completions, 2017 48,000 sq m

Vacancy rate 12.1%

Financial conditions

Prime shopping centre base rent* USD780 per sq m/ year

Operational expenses USD60 -110 per sq m/ year

*Rents are given for a single unit of 100 sq m GLA located on the ground floor of a retail gallery. Rents exclude VAT and OPEX.

Supply: Real Estate

Development

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Supply Dynamics, Kiev

4

0

40

80

120

160

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017F

Completions Forecast

'000 sq mCompletionsStock

In 2016, quality retail stock increased by 156,700 sq m. The new deliveries were Lavina Mall SEC (115,000 sq m GLA) and

TSUM (23,500 sq m), both in Q4 2016, and New Way SEC (16,000 sq m) and GorodOK SEC, Phase 3 (2,200 sq m) –

opened previously.

Announced completions for 2017 total 48,000 sq m in three shopping centres: Smart Plaza SEC (15,000 sq m); KIDEAL

SEC, Phase 1 (22,000 sq m), Retail Park Petrovka, Phase 1 (11,000 sq m). Two other shopping centres announced to be

commissioned in 2017 will likely be postponed until 2018.

0

200

400

600

800

1000

1200

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017F

Stock at the beginning of the year Completions

'000 sq m

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Kiev Existing Shopping Centres

Neighborhood

Community

Regional

Superregional

Specialty/ outlet

1

3

4

56

7

8 9

1112

13

14

15

16

17

18

1920

21

22

23

25

24

26

5

27

2829

2 10

3031

№ Name GLA Year

1 Globus 19 200 2002

2 GorodOk 29 2002003, 2015,

2016

3 Karavan 39 300 2003

4 Magelan 22 000 2003

5 Mandarin Plaza 9 400 2003

6 Ukraina 22 200 2003

7 Promenada Center 17 800 2004

8 Aladdin 10 200 2004

9 Piramida 12 600 2004

10 Plazma 16 400 2006

11 Kosmopolit, Phase I, II, III 43 0002006, 2007,

2009

12 Komod 7 600 2007

13 Arkadia 16 200 2007

14 Sky Mall, Phase I, II 65 600 2007, 2010

15Arkadia on Dneprovskaya

Emb.19 700 2008

16 Kvadrat Aurora 19 000 2008

17 Darnitsa 5 800 2008

18 Promenada Park, Phase I, II 30 000 2009, 2010

19 Dream Town, Phase I, II 90 000 2009, 2011

20 RayON 24 100 2012

21 Ocean Plaza 70 000 2012

22 Polyarny 8 600 2012

23 Silver Breeze 15 600 2013

24 Gulliver 45 500 2013

25Manufactura, outlet center,

Phase I, II21 600 2013, 2015

26 Art Mall 37 000 2013

27 Atmosfera 30 200 2014

28 Prospekt 41 400 2014

29 Doma Center 8 200 2015

30 Aprel 5 900 2015

31 New Way 16 000 2016

32 Lavina Mall 115 000 2016

33 TSUM 23 500 2016

32

33

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Kiev Future Shopping Centres

Retroville

83,000* sq m

SG (Stolitsa Group)

6

Lukyanovka

47,100 sq m

Arricano Real Estate

Blockbuster Mall

93,700 sq m

MEGALINE

KIDEAL, Phase 1

22,000 sq m

Immochan

Kyiv Mall

58,000 sq m

Dilays

River Mall

56,100 sq m

Vilna Ukraina

2018

Smart Plaza

15,000 sq m

UDP

2017

Retail Park

Petrovka, Phase 1

11,000 sq m

Immochan

2017

2018

2017

2018

2017/2018

2017/2018

*GLA is shown for all shopping centres.

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Retail Stock Breakdown by District

Goloseevskiy district remains the most saturated (737 sq m per 1,000 inhabitants). Solomenskiy district (163 sq m per 1,000

inhabitants) became the least saturated in Kiev in Q4 2016, replacing Sviatoshynskiy district (451 sq m per 1,000 inhabitants)

after the opening of Lavina Mall SEC.

In 2017, there will be no changes in the district ranking.

Shopping centres density by district*Quality retail breakdown by district*

*There are no quality shopping centres in Podol district.

7

0 200 400 600 800

Goloseevskiy

Obolonskiy

Sviatoshynskiy

Shevchenkovskiy

Pecherskiy

Dneprovskiy

Desnianskiy

Darnitskiy

Solomenskiy

sq m/'000 inh.

0

50

100

150

200

250

300

350

400

0

50

100

150

200

250

Stock Pipeline, 2017 Population (RHS)

'000 sq m '000 inh.

Demand: Consumer

Sector and Retailer

Activity

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Wages and Retail Turnover

In January-November 2016, retail turnover and wages in Ukraine grew by 3.7% YoY and 8.3% YoY respectively. The growth

was driven by lower inflation, increase in nominal wages and a low base of comparison.

Retail turnover and wages in Kiev in January-November 2016 also increased, by 5% and 13.9% YoY respectively.

Source: Ukrstat, Kievstat

Real wages and retail turnover, Ukraine, YoY

9

Real wages and retail turnover, Kiev, YoY

-25

-20

-15

-10

-5

0

5

10

15

20

2010 2011 2012 2013 2014 2015 2016

Retail turnover Wages

%

-30

-25

-20

-15

-10

-5

0

5

10

15

20

2010 2011 2012 2013 2014 2015 2016

Retail turnover Wages

%

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Retail Chains in the Market: Anchors

In Q4 2016, new shopping centre Lavina Mall SEC opened with such anchor tenants as Comfy and Eldorado, Ukraine’s largest Multiplex cinema, Silpo store with new design, amusement park "Galaxy". METRO opened a renewed hypermarket in Petrovka; Silpo and ATB Market opened their stores with new designs; Foxtrot and Eldorado opened stores with a new format.

Ukrainian brands and multibrand stores that were actively developing in 2016 include Must Have, Jasmine, VOVK, U Dress, Uamade. In 2016, the Epicenter network opened two new stores and carried out expansions of the two existing ones. InditexGroup opened the first Uterqüe store in Ukraine in the Gulliver shopping mall.

10

Type Key retailers Format

Food

ATB Market, Silpo, Velyka Kyshenya, VARUS, Fora, Cosmos, ECO-

Market, NOVUS, Billa, Furshet,TopmartSupermarket

METRO, Auchan, Fozzy, MegaMarket, Karavan, Tam-TamHypermarket

White and Brown Foxtrot, Eldorado, Comfy Multibrand

CinemaBatterfly, Liniya Kino, Multiplex, Odessa Kino, Oscar, Planeta Kino IMAX,

Cinema City, WizoriaMultiplex

DIY Epicentre, Novaya Liniya, Leroy Merlin, OLDI, Jysk DIY

Children's entertainment

centers (CEC)

Igroland, Fly Park, Happylon, Kids Will, Kidlandia, Sky Park, GalaxyCEC

Fashion Marka Ukraina, Inditex Group, LPP Group, Argo, LC Waikiki,

New Yorker, Mango, Domino Group, Arber Fashion Group, MTI Group

Multibrand/

Monobrand

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Retail Chains in the Market: Retail Gallery

11

Type Key retailers Format

Fashion

Benetton, Bershka, Cacharel, Calvin Klein, Colin's, Cropp Town, Diesel, Gant, Gloria

Jeans, Guess, House, Lacoste, Lerros, Mango, Massimo Dutti, Mohito, OGGI, O’stin,

Oysho, Promod, Pull&Bear, Stradivarius, Tommy Hilfiger, Topshop/Topman, US Polo

Assn.

Monobrand

Perfume and cosmeticsCosmo, Eva, Watsons, proStor, Bonjour, Brocard, L’Occitane, MAC, Bomond, Yves

Rocher, Glossary, NYX, LUSH

Monobrand,

Multibrand

Sport goods Arena, Adidas, Columbia, Nike, Puma, Reebok, Sportmaster, Megasport,

New Balance, Northland, Marathon, Svit Sportu, 2ХU, All Stars

Monobrand,

Multibrand

ShoesAldo, Antonio Biaggi, Carlo Pazolini, Rieker, Munchen, Vitto Rossi, Ecco, Geox, Luciano

Carvari, Respect, Welfare, Intertop, KARI, Loriblu

Monobrand,

Multibrand

Goods for children Antoshka, Budynok Igrashok, Planettoys, SMIK, Chicco, Mothercare,

Chudo-ostrov, Mikki

Монобрэнд,

Multibrand

Books and music КS, Bukva Multibrand

Accessories, jewelry, giftsAccessorize, Attribute, DEKA, Diva, LuxOptika, Pandora, Seta Décor, Swarovski,

Swatch, WOW shop, Secunda, Frey Wille

Monobrand,

Multibrand

Food courtMcDonald's, Pechena Kartoplya, SushiYa, Shokoladnitsa, Yapona Hata, L’kafa, Mafia,

Kredens, Salateira, Plushka, Kryla, France.ua, Souperia, Big BurgerMonobrand

Telecom & Electronics Ringoo, Allo, Citrus, Samsung, Lenovo, iStudioMonobrand,

Multibrand

Ukrainian fashion brandsKrisstel, Public&Private, U Dress, VOVK, Uamade, Natali Bolgar, Jasmine, Goldi, Arber,

A.Tan by Andre Tan, A TAN MANMonobrand

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Retail Chains: Franchising and Direct Market Entry

• In Q4 2016, almost 70% of the demand for quality retail spaces in Kiev was from fashion segment tenants.

• The demand from foreign retailers was comparable to the local brands’ demand.

12

Franchising Direct market entry

Retail gallery operators

Marks & Spencer GAP

Inditex

Zara

Nike Accessorize Oysho

Massimo DuttiGuess OGGI

Bershka

Promod Tommy Hilfiger Stradivaius

Uterqüe

Befree Orsay

LPP Group

Reserved

Cropp Town

United Colors of

BenettonKaren Millen

Mohito

Sinsay

Mothercare

DesigualHouse

Cacharel Baltika Group Monton

Mosaic

Love Republic Oasis New Yorker, Adidas, Mango

Luxury retailers

Dolce & Gabbana, Valentino, Saint Laurent,

Philipp Plein, Burberry, DiorLouis Vuitton, Chanel

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

International Newcomers to Kiev Retail Market

13

In Q4 2016, the following new brands entered the Kiev market: women's clothing and bags Uterqüe (Spain), menswear Eduard

Dressler (Germany), children's clothing Elsy (Italy), Calvin Klein Underwear (USA), women's clothing Liu Jo (Italy), men's

trousers Hiltl (Germany).

Overall in 2016, more than twenty international brands entered the Kiev retail market, representing Turkey, Germany, Italy,

Egypt, Spain, USA.

2015 Future2014

Entered the market Plan to enter

Pedro del Hierro, Star Burger,

Intimissimi, Keddo, Calzedonia,

Lamoda

(e-commerce), Bottega Verde,

Glossip, Paul, Alberta Ferretti,

H.E. by Mango,

Prenatal Milano, Peacocks,

Egersund Seafood, Vapiano,

SAL Y LIMON

2016

Betty Barclay, ERES, Chloé,

Mango Megastore (Violeta), adL,

Silenza, Bosco Sport , Marella,

Idexe, Stefanel, Super Step,

Naturel by Silenza, Naf Naf, Yves

Saint Lauren, Dior, Suiteblanco,

Coqui, Maestrami, Stefanel,

Hunkemöller,

Menya Musashi Ramen Shop,

Galvanni, Eterna, Sanetta

Maje, Ravin Jeans, Reima,

Isabel Garcia, Rodenstock,

Armani Exchange, Silvian Heach,

KIWE, Sandro, Atos Lombardini,

Steiff, Falke, Falke Kid’s, Tezenis,

Converse, ROECKL, Uterqüe,

Eduard Dressler, Michael Kors,

Elsy, Calvin Klein Underwear, Liu

Jo, Hiltl, Imperial, Replay, N.UNO

Porter

Cortefiel, CCC, Falconeri,

Mavi, Defacto, Decathlon,

Koton, Intersport, FLO,

Cafe Barbera, Papa

John’s, VAISMANN,

BALDESSARINI

Market Balance

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Vacancy Rate Dynamics, Kiev

15

In Q4 2016, the vacancy rate in Kiev reached 12.1%, 7.5 ppt higher than in Q3 2016. The vacancy increase was due to the market

entering of two new quality facilities with GLA of 138,500 sq m.

There is a strong demand for retail space in quality shopping centres from local retailers, activity of foreign operators is picking up.

When excluding the new completions in Q4 2016, the vacancy rate would have been 4.1%.

Vacancy rate dynamics

*The map shows the average vacancy rate in districts, as well as the dynamics of change in the last quarter. There are no quality shopping centres in Podol district.

Vacancy rate by district*

11.5%

0.1%

1.3%

2.1%

3.0%6.5%

50.0%

1.1%

9.6%

12.1%

4.6%4.1%

0%

2%

4%

6%

8%

10%

12%

14%

The average market vacancy rate

Vacancy rate without shopping centres completed in Q4

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Prime Base Rent: European Benchmarks*

16

In 2016, prime base rent grew by 8% and reached 780 USD/ sq m/ year (65 USD/ sq m/ month). The increase was due to the

recovery of retail turnover, steady demand for premium locations, and seasonal factors.

In Q4 2016, there were no significant changes in rental rates.

*Excluding VAT and OPEX.

780

0 500 1 000 1 500 2 000 2 500 3 000 3 500

Zagreb

Amsterdam

Belgrade

Kiev

Milan

Budapest

Bucharest

Rome

Athens

Madrid

St. Petersburg

Lisbon

Prague

Oslo

Berlin

Warsaw

Brussels

Paris

London

Moscow

USD/ sq

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

Base Rents by Tenant Format, Q4 2016

• The practice of renegotiation of rental agreements between landlords and tenants still exists in the market but has become less common.

• Individual arrangements for fixing the exchange rate at a level below the rate of the NBU were almost completely replaced by the new lease agreements based on the market rental rate in foreign currency. Fixing rental rates according to NBU rate for the first 3-6 months is less used.

• For the shopping gallery, new contracts usually include step-rent for the first 2-3 years.

• Landlords became more attentive to retailer turnover data control.

17

*Excluding VAT and OPEX.

Profile Area, sq mRental rate, USD/sq

m/month*

Rental rate, USD/sq

m/year*

Hypermarkets >7 000 8-12 100-140

Supermarkets 2 000 – 5 000 9-13 110-160

Convenience store 600 –2 000 10-15 120-180

White and brown > 1 000 6-10 70-120

600 – 1 000 8-12 100-140

Cinema > 2 000 6-10 70-120

Entertainment 1 000 – 3 000 5-8 60-100

Food courts 40 -90 40-50 480-600

Restaurants 250 – 600 15-25 180-300

Perfume and cosmetics250 – 450 40-50 480-600

50 – 100 50-60 600-720

Sporting goods> 1 500 8-10 100-120

< 300 20-30 240-360

Goods for children

> 800 8-12 100-140

250 – 600 15-20 180-240

70 – 120 20-30 240-360

Household goods < 2 000 6-10 70-120

Fashion and apparel

1 000 – 2 000 8-12 100-140

300 – 600 15-25 180-300

150 – 300 25-35 300-420

100 – 150 35-45 420-540

JLL – Kiev Retail Market Overview, Q4 2016

Source: JLL

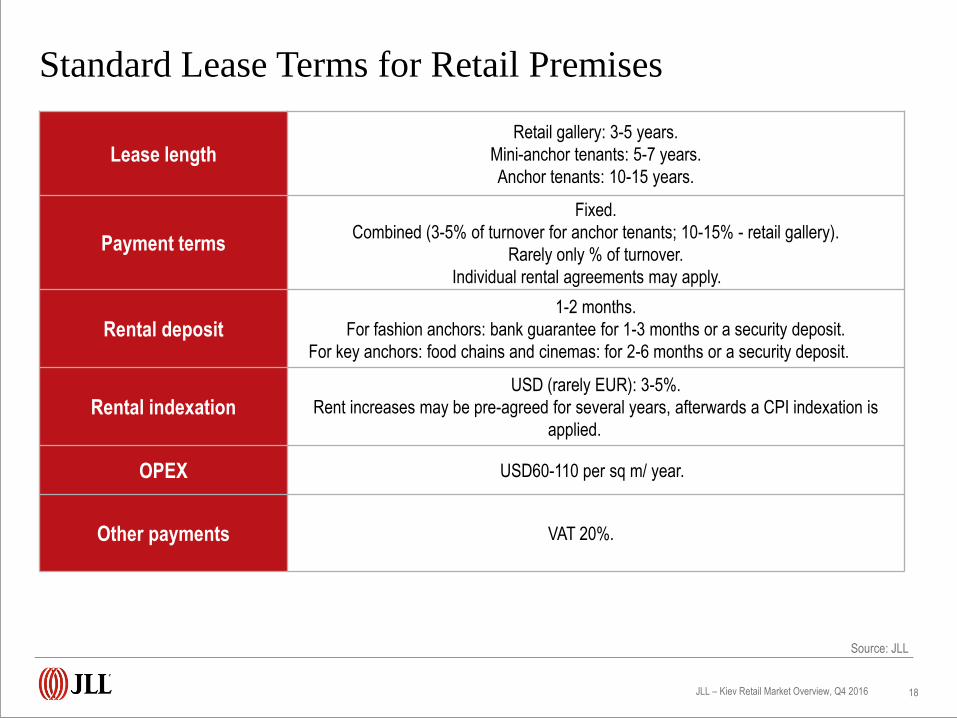

Standard Lease Terms for Retail Premises

18

Lease length Retail gallery: 3-5 years.

Mini-anchor tenants: 5-7 years.

Anchor tenants: 10-15 years.

Payment terms

Fixed.

Combined (3-5% of turnover for anchor tenants; 10-15% - retail gallery).

Rarely only % of turnover.

Individual rental agreements may apply.

Rental deposit 1-2 months.

For fashion anchors: bank guarantee for 1-3 months or a security deposit.

For key anchors: food chains and cinemas: for 2-6 months or a security deposit.

Rental indexation USD (rarely EUR): 3-5%.

Rent increases may be pre-agreed for several years, afterwards a СРI indexation is

applied.

OPEX USD60-110 per sq m/ year.

Other payments VAT 20%.

© Copyright 2017 Jones Lang LaSalle. All rights reserved. The information contained in this document is proprietary to Jones Lang LaSalle and shall be used solely for the purposes of

evaluating this proposal. All such documentation and information remains the property of Jones Lang LaSalle and shall be kept confidential. Reproduction of any part of this document is

authorised only to the extent necessary for its evaluation. It is not to be shown to any third party without the prior written authorisation of Jones Lang LaSalle. All information contained

herein is from sources deemed reliable; however, no representation or warranty is made as to the accuracy thereof

Thank You!