J.P. Morgan 研究報告-Nothing but net 2014 global internet

325

www.jpmorganmarkets.com Global Equity Research 09 January 2014 Nothing But Net 2014 Global Internet Investment Guide US Internet Doug Anmuth AC (1-212) 622-6571 [email protected] Bloomberg JPMA ANMUTH <GO> J.P. Morgan Securities LLC Kaizad Gotla, CFA AC (1-212) 622-6436 [email protected] J.P. Morgan Securities LLC Bo Nam (1-212) 622-5032 [email protected] J.P. Morgan Securities LLC Diana R Kluger, CFA (1-212) 622-4539 [email protected] J.P. Morgan Securities LLC China Internet Alex Yao AC (852) 2800 8535 [email protected] J.P. Morgan Securities (Asia Pacific) Limited Korea Internet and Telco Stanley Yang AC (82-2) 758-5712 [email protected] J.P. Morgan Securities (Far East) Ltd, Seoul Branch Japan Games, Internet, Leisure Haruka Mori AC (81-3) 6736-8632 [email protected] JPMorgan Securities Japan Co., Ltd. Europe Media & Internet Nicolas J Dubourg AC (44-20) 7134-5226 [email protected] J.P. Morgan Securities plc CEEMEA Media & Telecoms Alexei Gogolev AC (7-495) 967-1029 [email protected] J.P. Morgan Bank International LLC Latin American Telecommunications / Media / Technology Andre Baggio, CFA AC * (55-11) 4950-3427 [email protected] Banco J.P. Morgan S.A. * Registered/qualified as a research analyst under NYSE/FINRA rules. See page 321 for analyst certification and important disclosures, including non-US analyst disclosures. J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

-

Upload

chen-terry -

Category

Internet

-

view

602 -

download

35

Transcript of J.P. Morgan 研究報告-Nothing but net 2014 global internet

www.jpmorganmarkets.com

Global Equity Research09 January 2014

Nothing But Net2014 Global Internet Investment Guide

US Internet

Doug Anmuth AC

(1-212) 622-6571

[email protected] JPMA ANMUTH <GO>J.P. Morgan Securities LLC

Kaizad Gotla, CFA AC

(1-212) [email protected]. Morgan Securities LLC

Bo Nam

(1-212) [email protected]. Morgan Securities LLC

Diana R Kluger, CFA

(1-212) [email protected]. Morgan Securities LLC

China Internet

Alex YaoAC

(852) 2800 [email protected]. Morgan Securities (Asia Pacific) Limited

Korea Internet and Telco

Stanley Yang AC

(82-2) [email protected]. Morgan Securities (Far East) Ltd, Seoul Branch

Japan Games, Internet, Leisure

Haruka MoriAC

(81-3) [email protected] Securities Japan Co., Ltd.

Europe Media & Internet

Nicolas J DubourgAC

(44-20) [email protected]. Morgan Securities plc

CEEMEA Media & Telecoms

Alexei GogolevAC

(7-495) [email protected]. Morgan Bank International LLC

Latin American Telecommunications / Media / Technology

Andre Baggio, CFA AC *

(55-11) [email protected] J.P. Morgan S.A.

* Registered/qualified as a research analyst under NYSE/FINRA rules.See page 321 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware thatthe firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

2

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

January 9, 2014

Dear Investors and Internet Followers,

2013 was a strong year for equity markets overall, and an even better year for Internet stocks. U.S. Internet stocks in our coverage universe appreciated by a market cap-weighted average of 78% vs. the S&P 500 up 30%, while global Internet names covered by J.P. Morgan increased 84% during the year. Broad-based strength was evident across online subscription, advertising, and commerce models given the backdrop of powerful secular trends and an improving macro environment.

We believe those underlying dynamics should continue in 2014, and mobile will become an even bigger driver of Internet models. As we think back through some of the major shifts in the consumer Internet era, including the move from dial-up to broadband and changes in how people consume content, none is more significant than the adoption of mobile devices. comScore data suggests that U.S. mobile usage time initially surpassed that of the desktop in mid-2013, and that directional trend should continue globally going forward. We think 2014 is a year in which the gap tightens between mobile usage and mobile conversions and revenue, turning mobile into a greater tailwind across our global Internet coverage universe.

The Internet sector is extremely dynamic and we believe innovation is stronger than ever driven by the combined viral effects of social and mobile, along with the broad access to computing infrastructure in the cloud as exemplified by Amazon’s AWS. Leading Internet platforms such as Google, Amazon, Facebook, Tencent, and Apple continue to thrive, but we are also seeing powerful ecosystems created by LinkedIn and Twitter, along with other social, commerce, and communications platforms. We are focused on a number of key trends in the U.S. in 2014 including: 1) Mobile conversions and revenue tightening the gap with mobile usage; 2) Native and News Feed advertising becoming the dominant format for mobile ad monetization; 3) Cross-device tracking and attribution becoming critical for marketers and publishers alike; 4) Traditional media measurement tools to help accelerate the shift of traditional media dollars online; 5) Advances in Last Mile eCommerce to drive online penetration in key retail categories; 6) Cloud-based services gaining significant scale; and 7) Continued blurring of the lines among online travel participants. On a global basis, many of the key themes outlined by our Internet team in other geographies relate to mobile and how it is driving gaming, commerce, and advertising.

From an investment perspective, we recognize that most of our companies trade at materially higher levels than they did a year ago, and we remain selective based on asset quality, growth, valuation, and other factors. But we also believe it is still early in the mobile Internet—considerable share gain opportunities remain across our global coverage universe and innovation will continue to drive disruptive technologies.

We hope our global outlook report is helpful in your investment process in 2014 and we look forward to working with you in the year ahead.

Sincerely,

Doug Anmuth (U.S.) Alex Yao (China)

Stanley Yang (Korea) Haruka Mori (Japan)

Nicolas Dubourg (Europe) Alexei Gogolev (Russia) Andre Baggio (Latin America)

3

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Table of ContentsGlobal Comp Sheet............................................................................ 6

Global Internet Top Picks................................................................... 8

U.S. Sector Outlook ....................................................................... 12

U.S. Internet Themes for 2014 ......................................................... 12

Revenue and Conversions to Tighten the Gap with Strong Mobile Usage .............................................................................................. 12

Native Ads to Drive Mobile Ad Monetization..................................... 20

Cross-Device Advertising and Attribution Becoming Critical............. 22

Traditional Media Measurement Tools to Drive Traditional Media Dollars Online .................................................................................. 25

Last Mile Drives Further Online/Offline Retail Convergence............. 28

Cloud-Based Services Gaining Scale............................................... 34

Blurring of the Lines in Online Travel ............................................... 37

U.S. Company Outlooks ................................................................ 39

Google ............................................................................................. 39

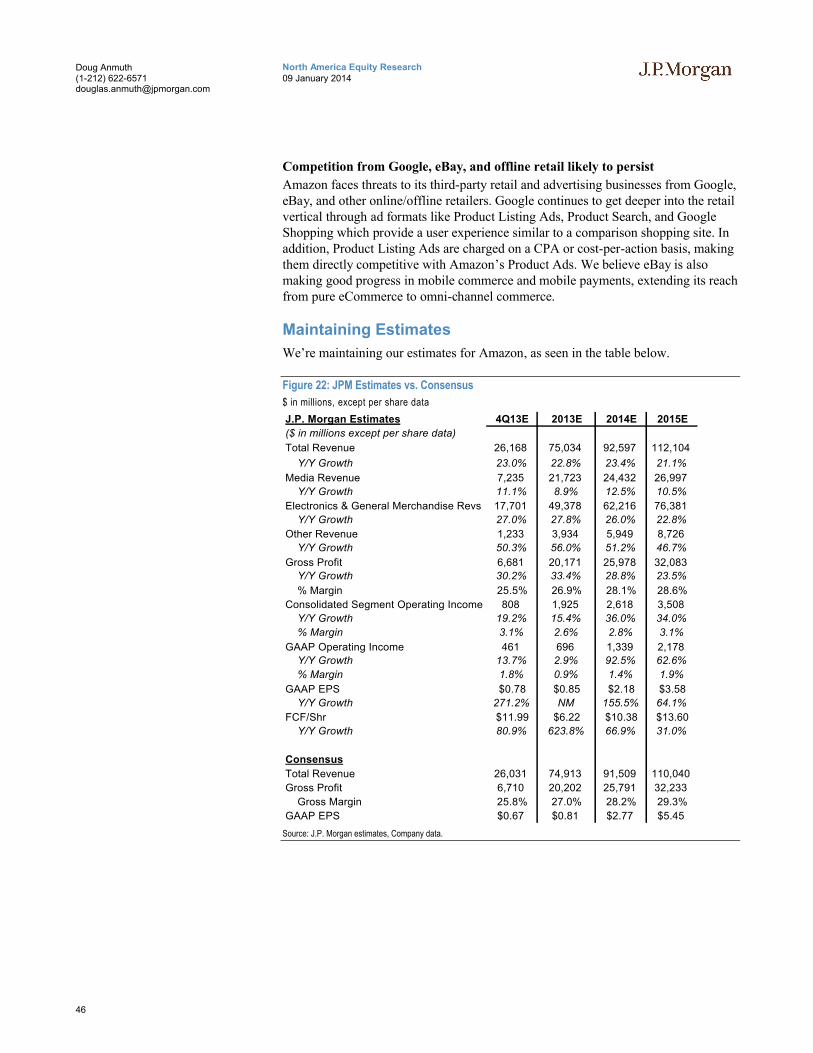

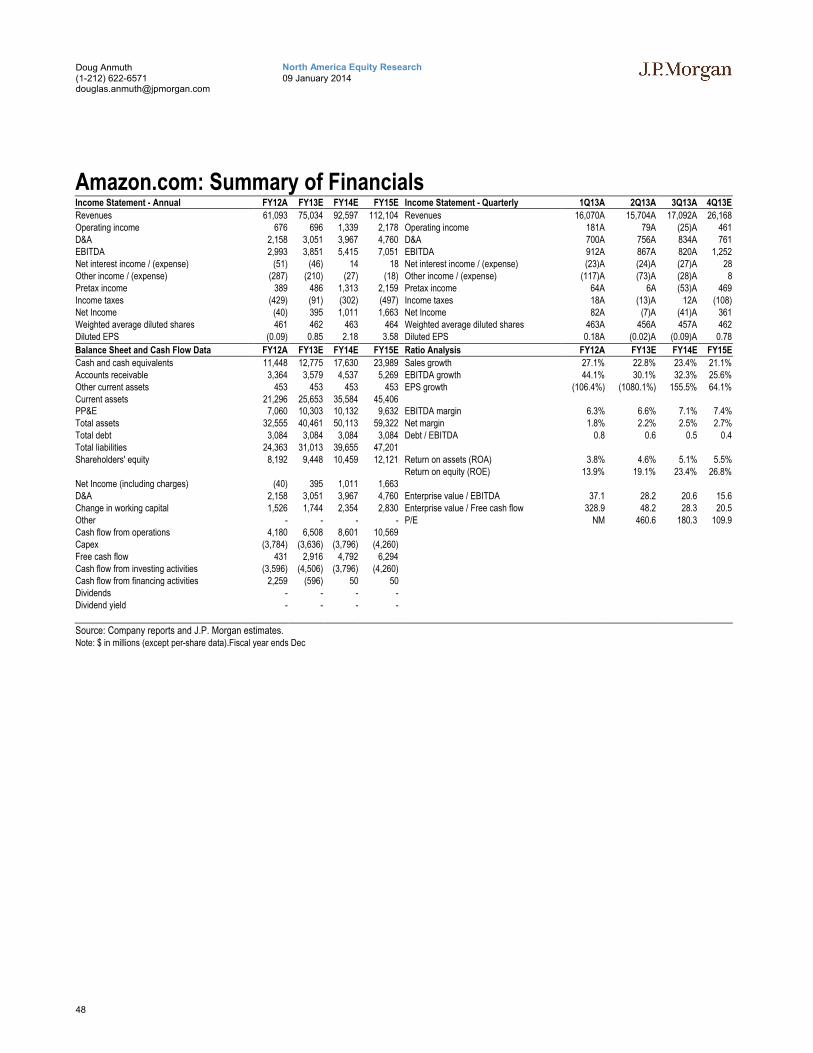

Amazon.com.................................................................................... 44

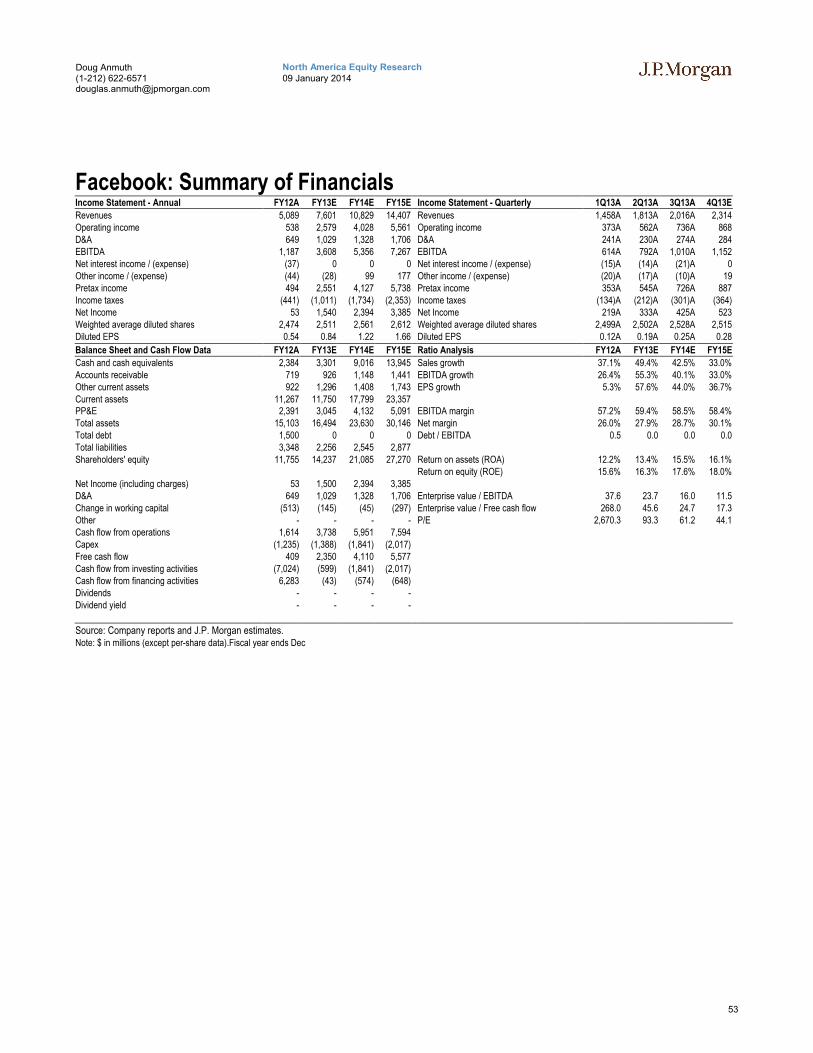

Facebook......................................................................................... 49

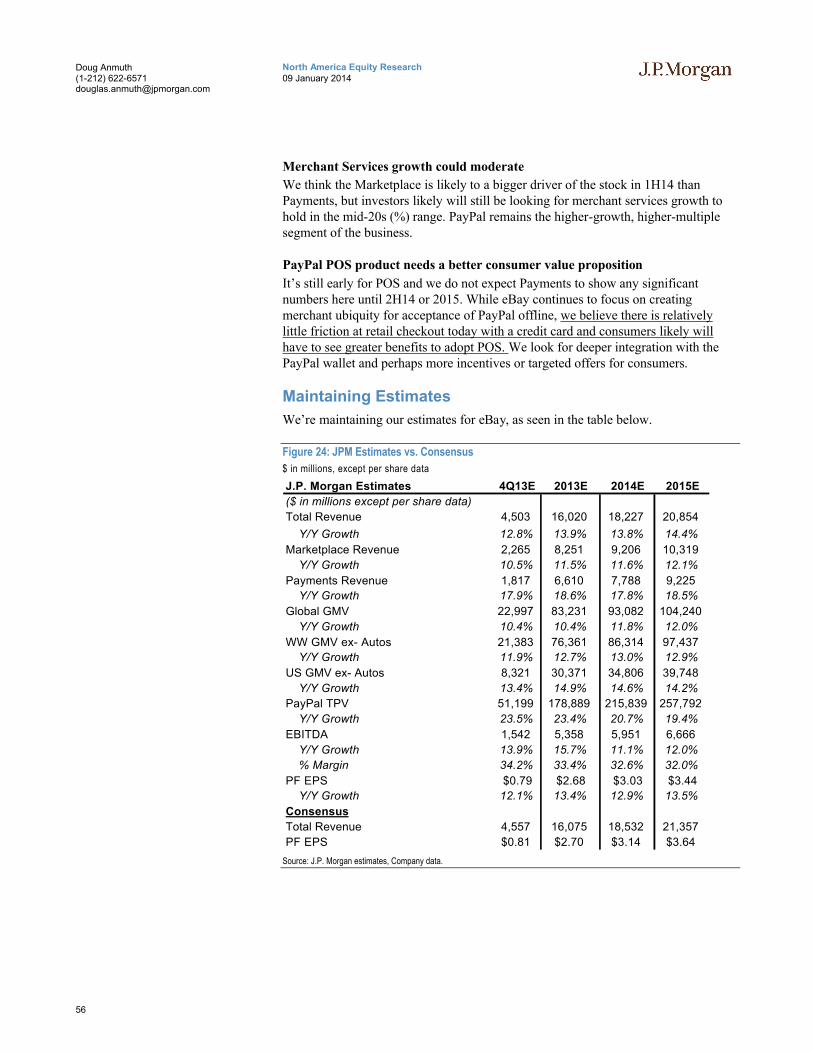

eBay, Inc.......................................................................................... 54

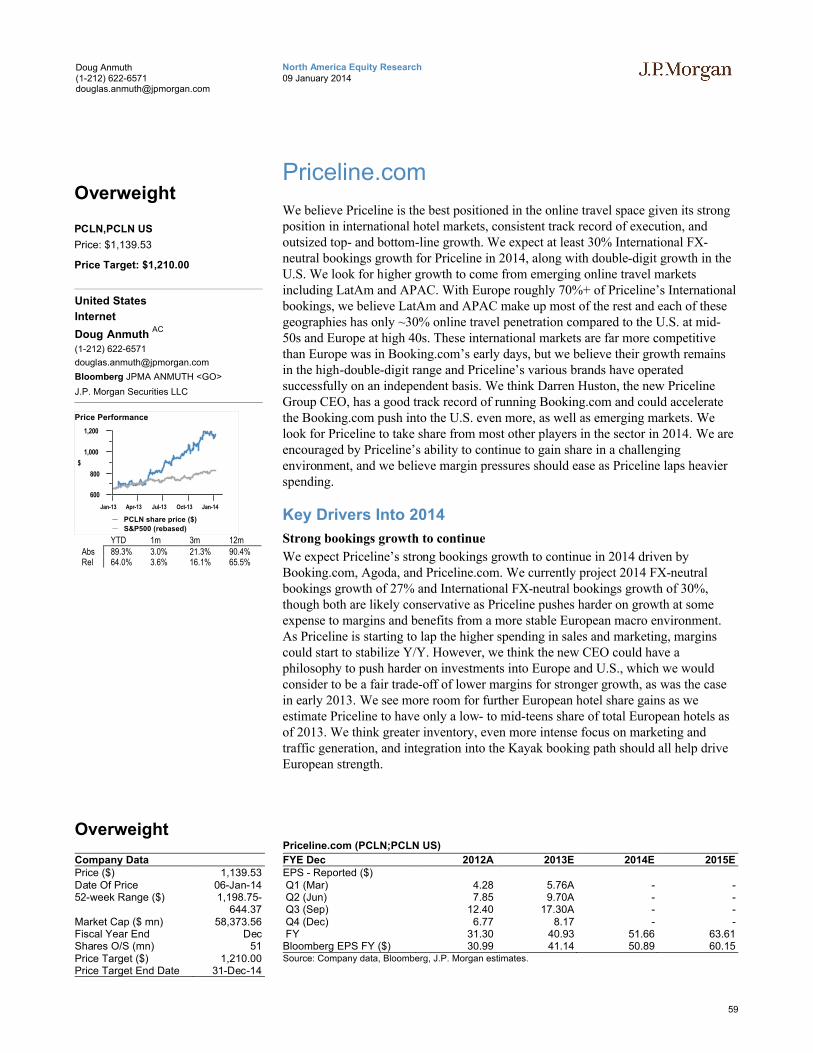

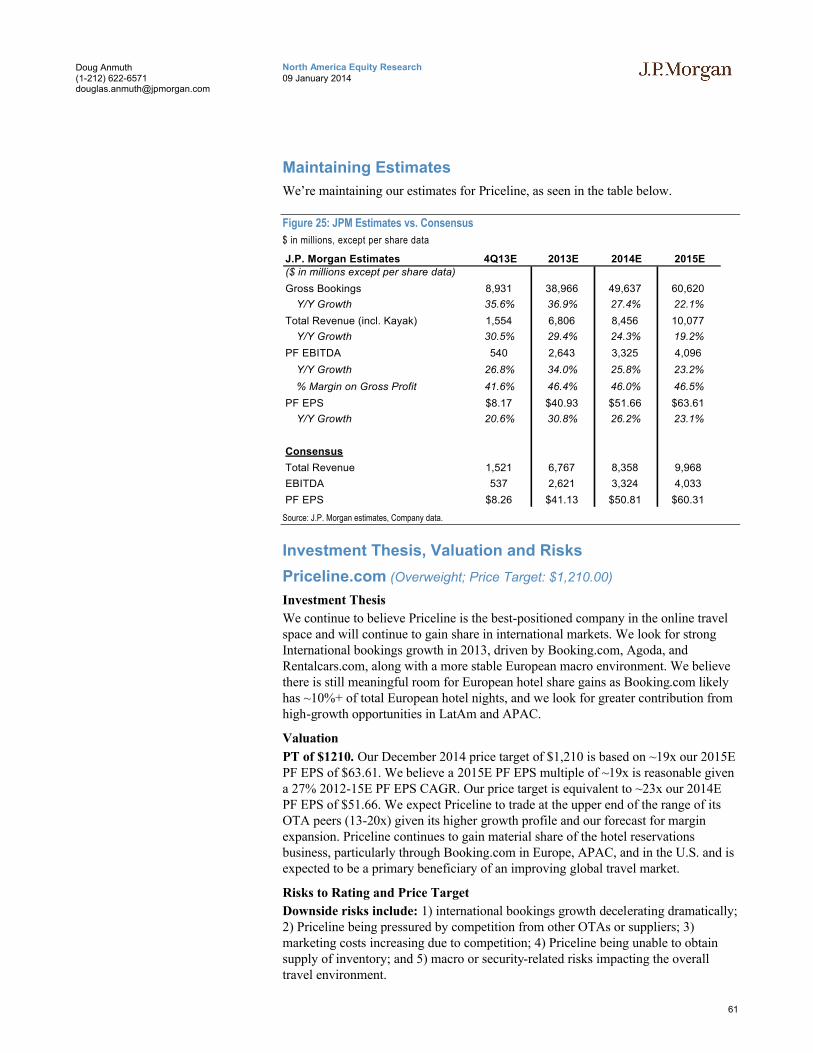

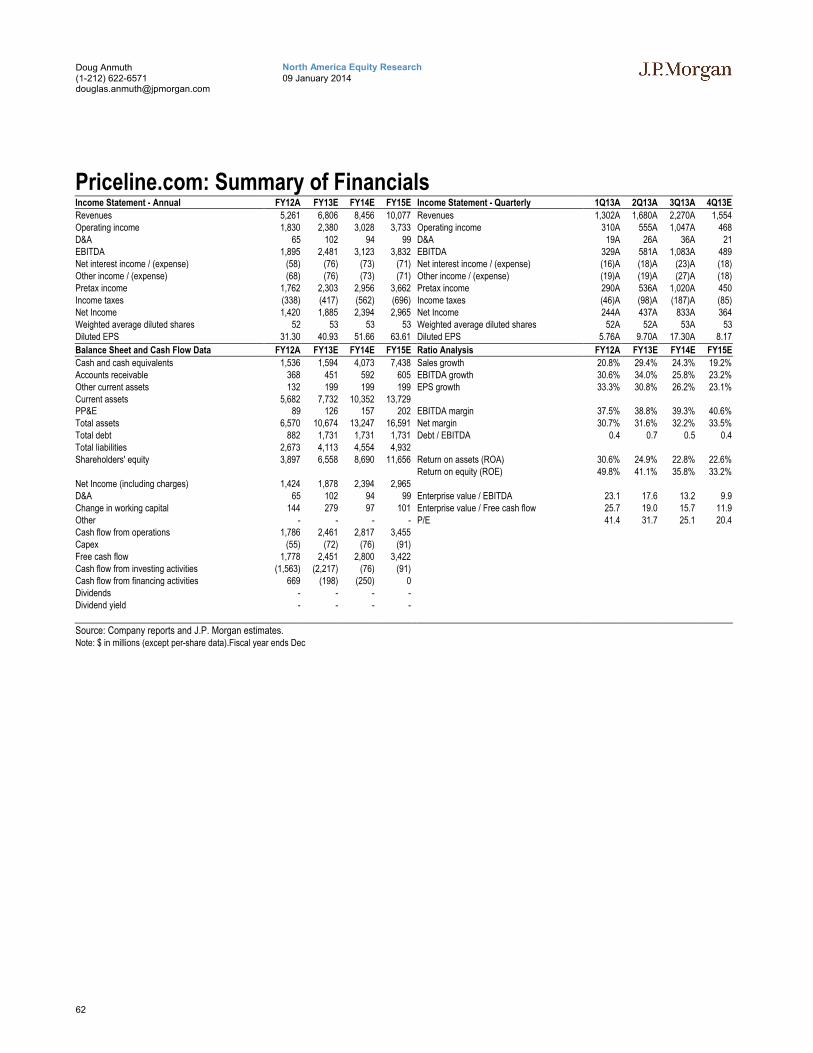

Priceline.com ................................................................................... 59

Yahoo Inc......................................................................................... 63

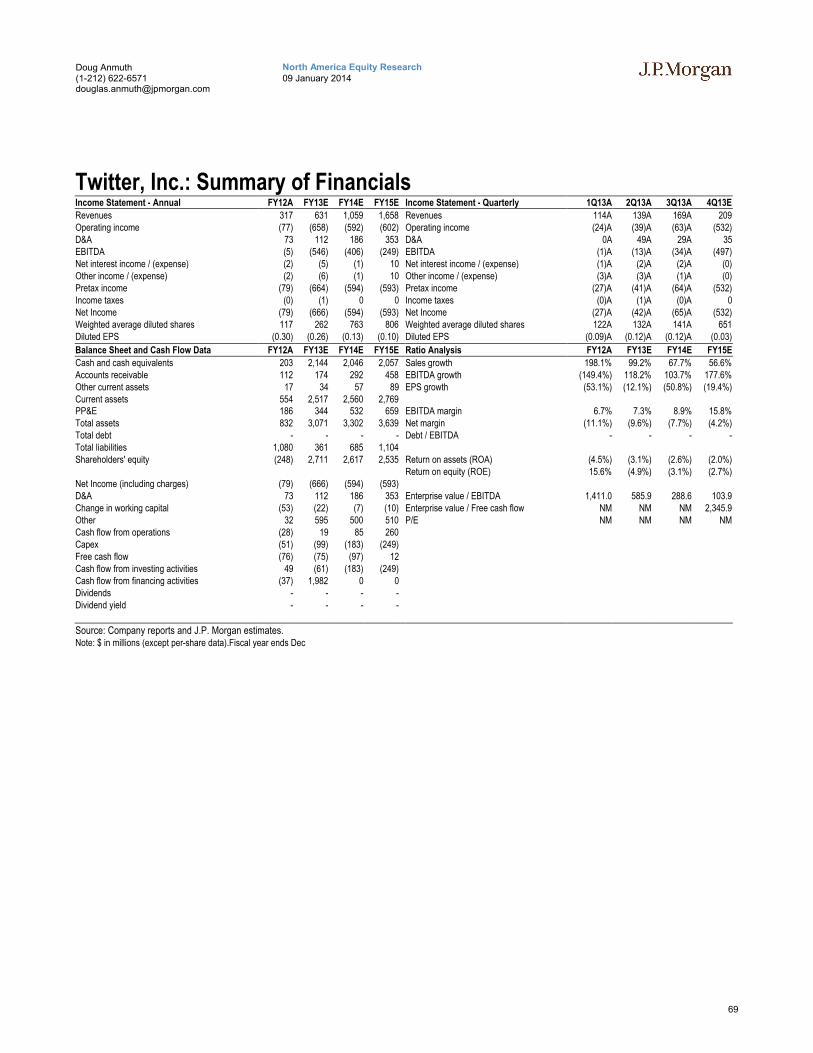

Twitter, Inc. ...................................................................................... 65

LinkedIn Corp................................................................................... 70

Netflix Inc......................................................................................... 75

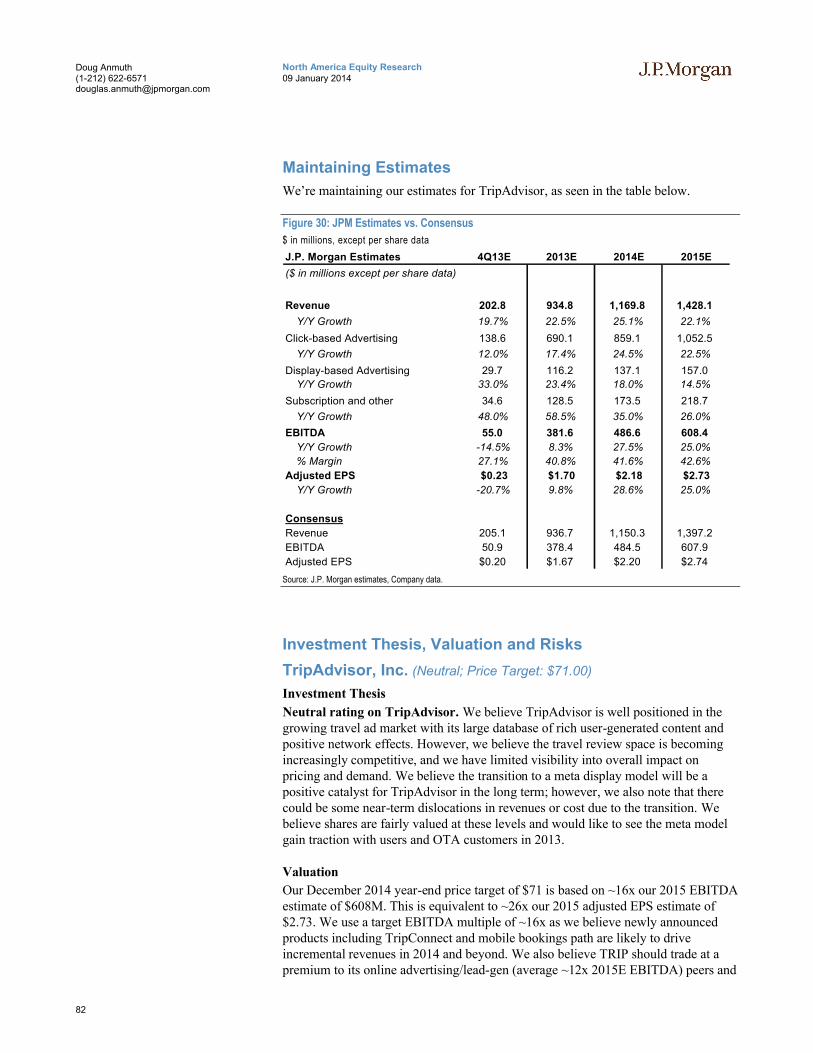

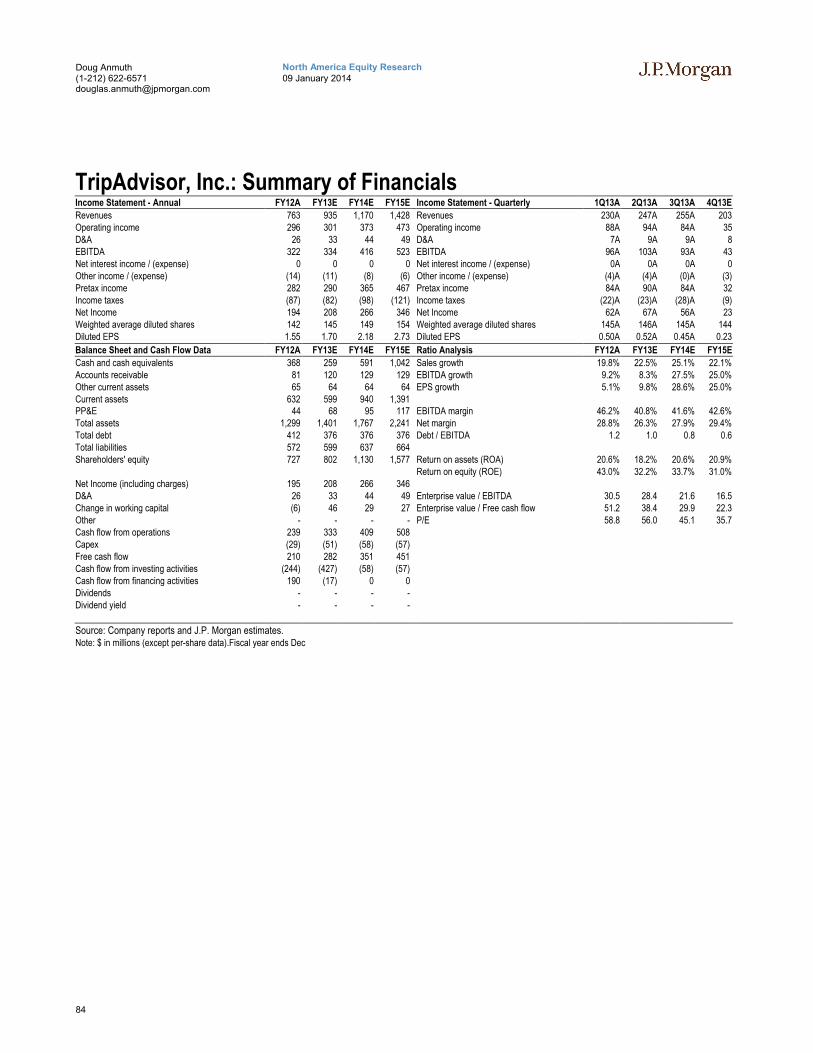

TripAdvisor, Inc. ............................................................................... 80

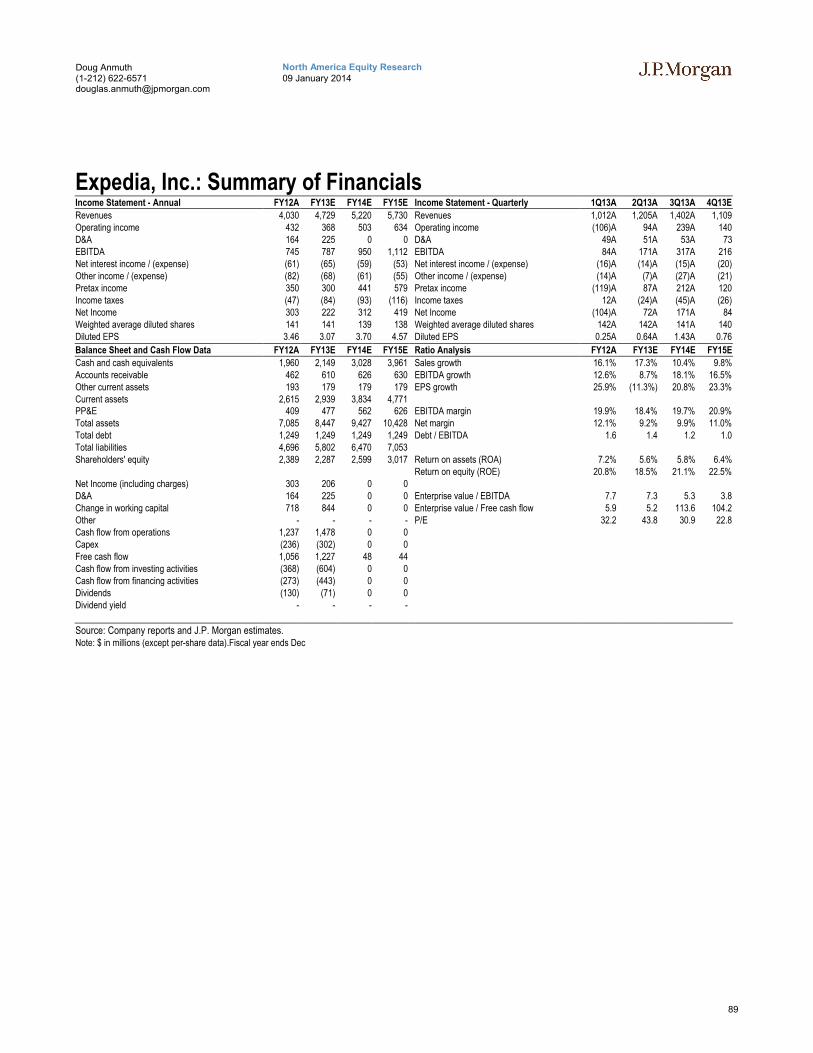

Expedia, Inc. .................................................................................... 85

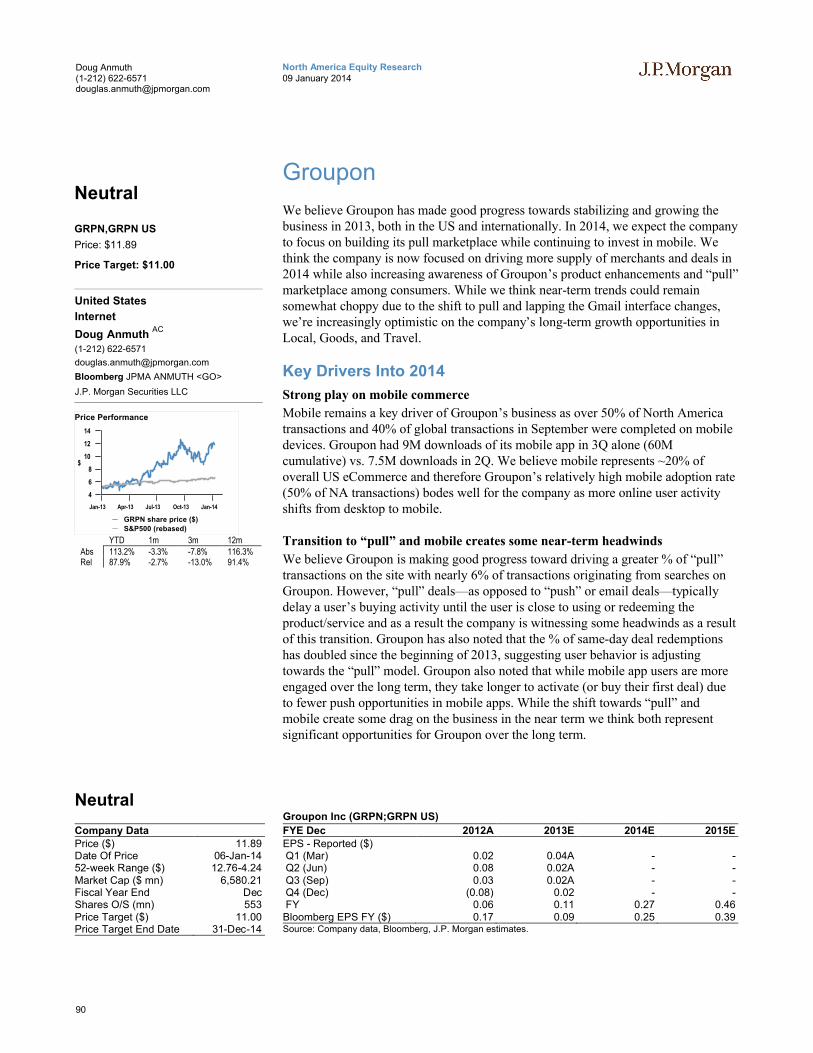

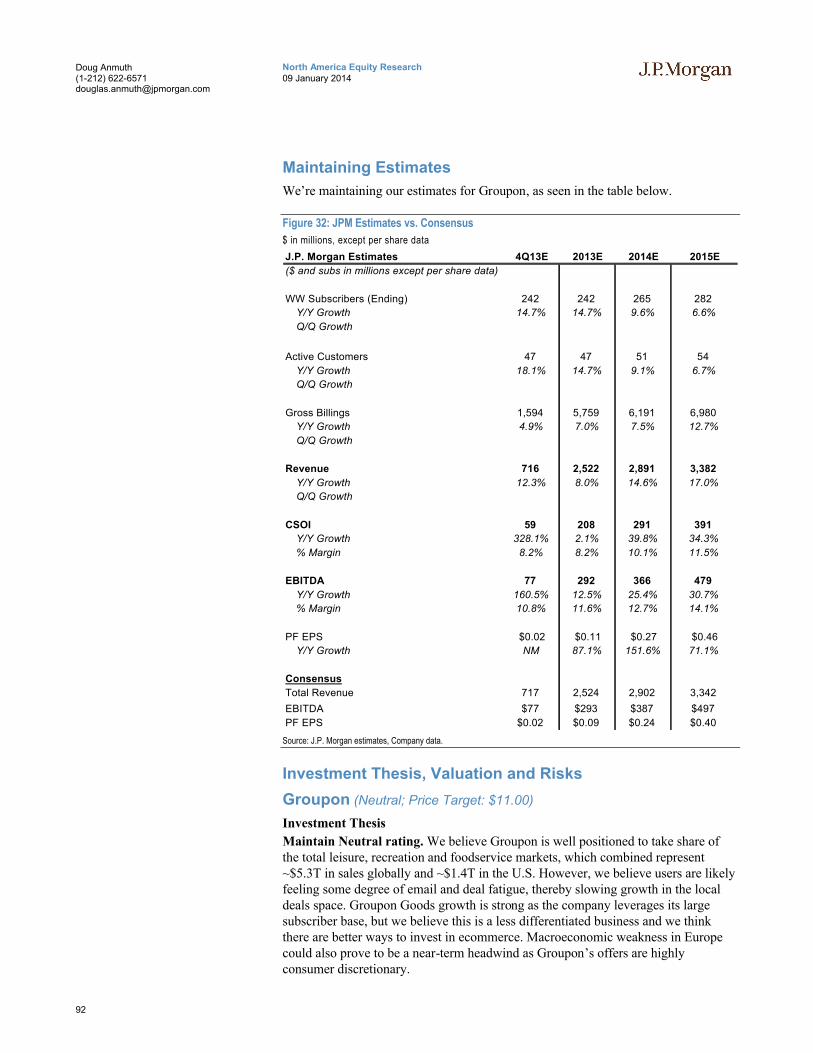

Groupon........................................................................................... 90

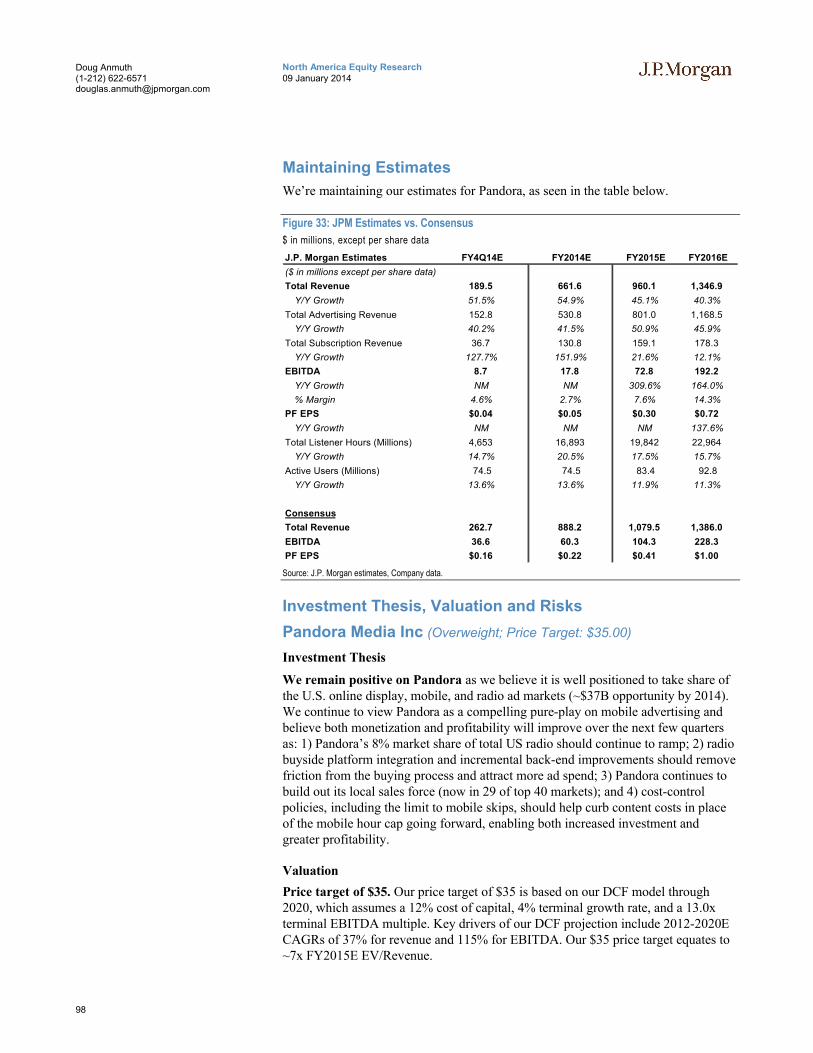

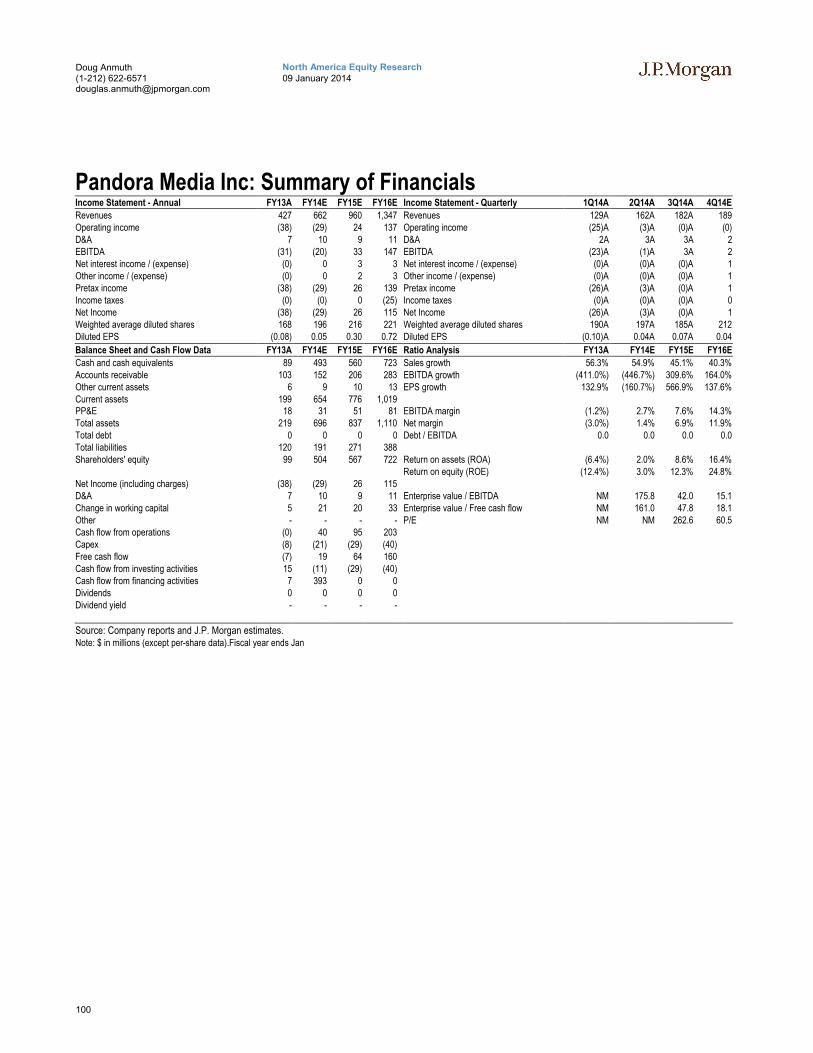

Pandora Media Inc........................................................................... 95

Yelp Inc.......................................................................................... 101

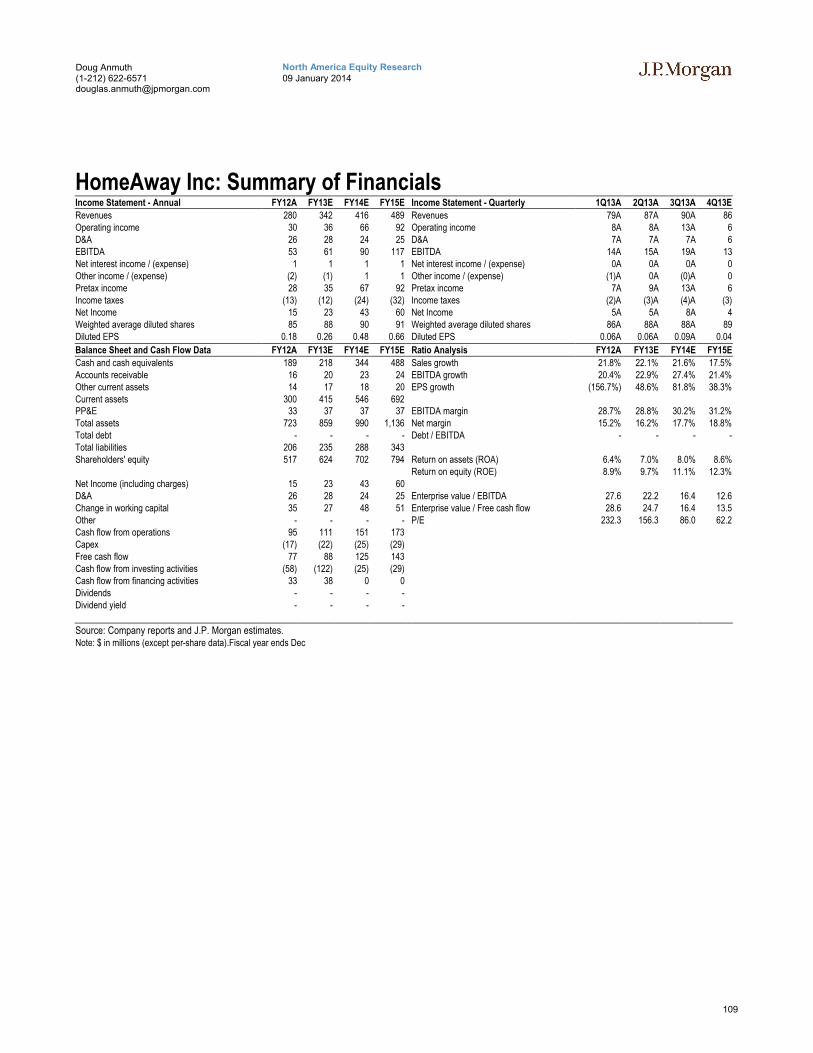

HomeAway Inc............................................................................... 105

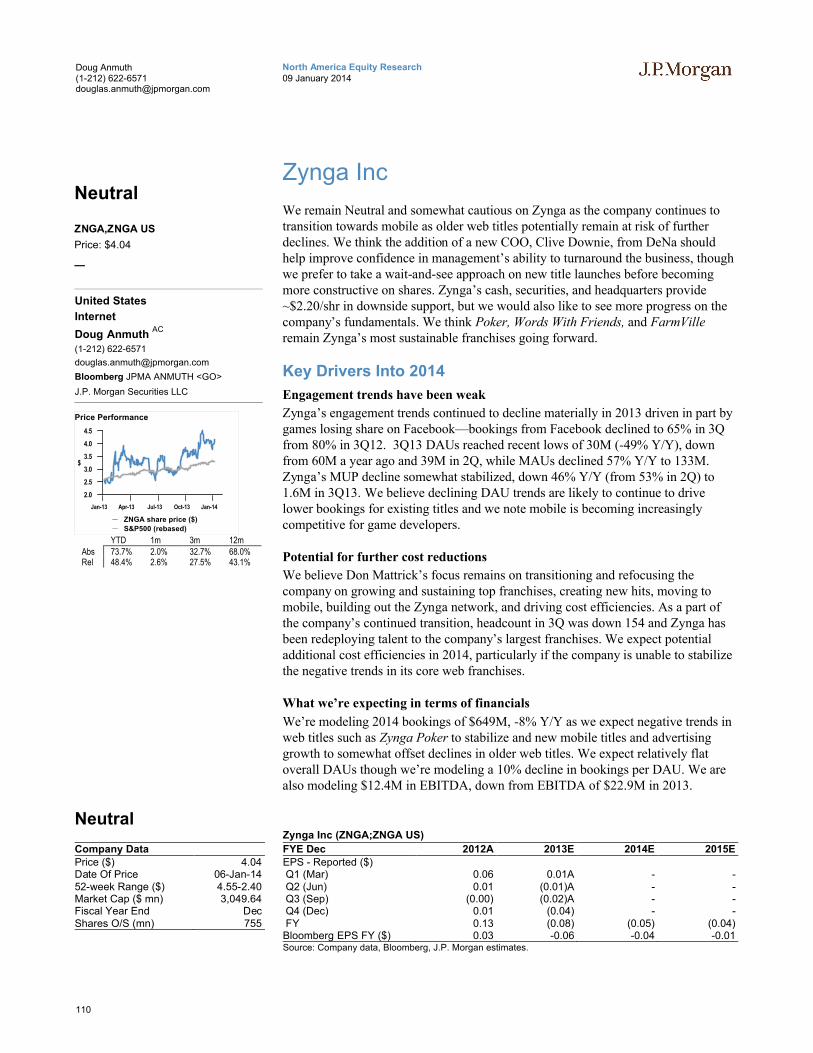

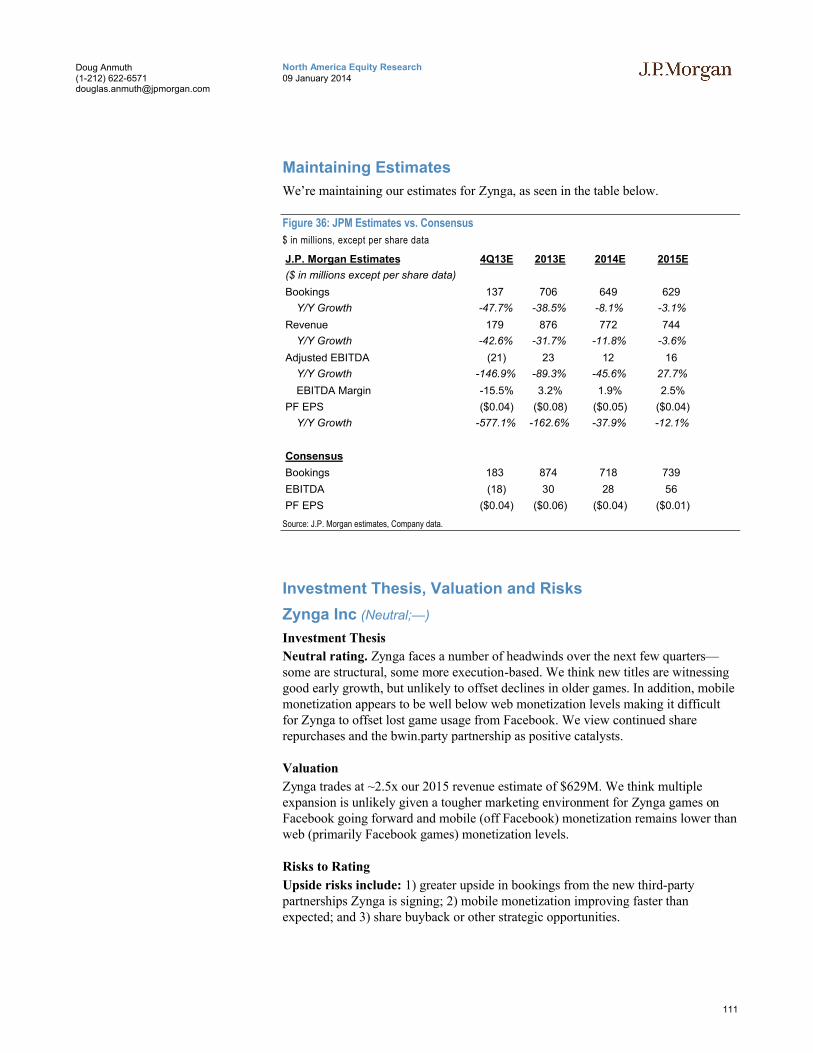

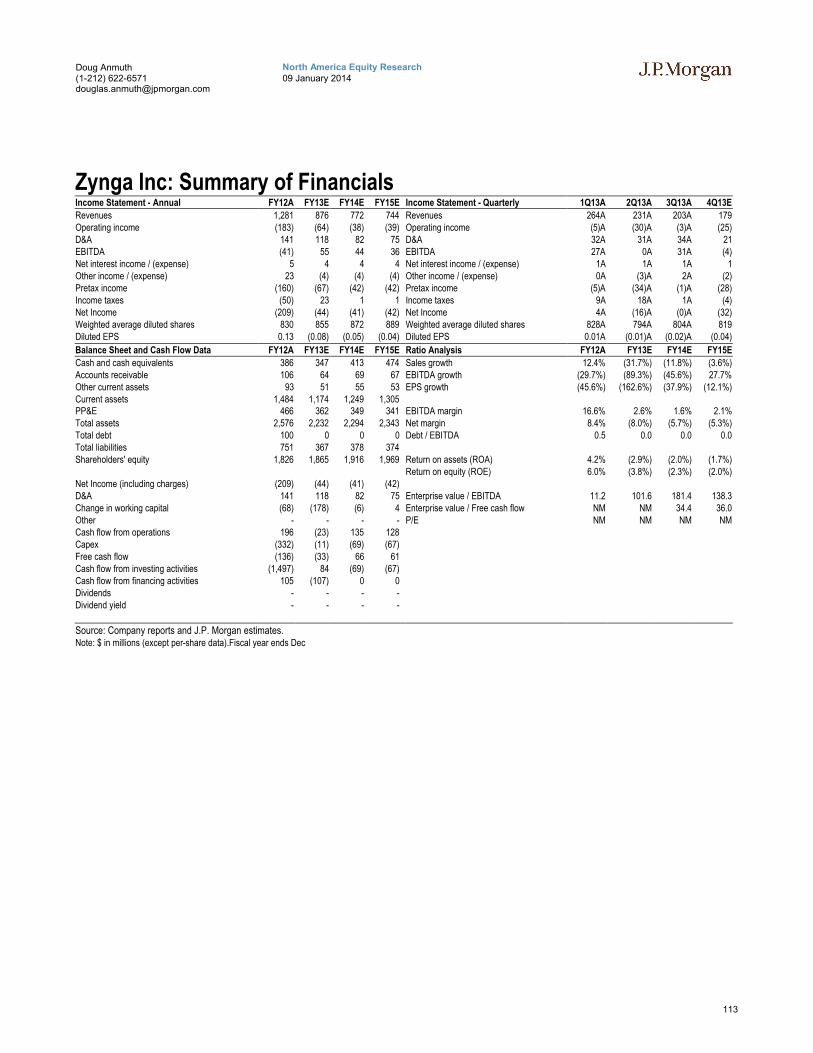

Zynga Inc....................................................................................... 110

Criteo ............................................................................................. 114

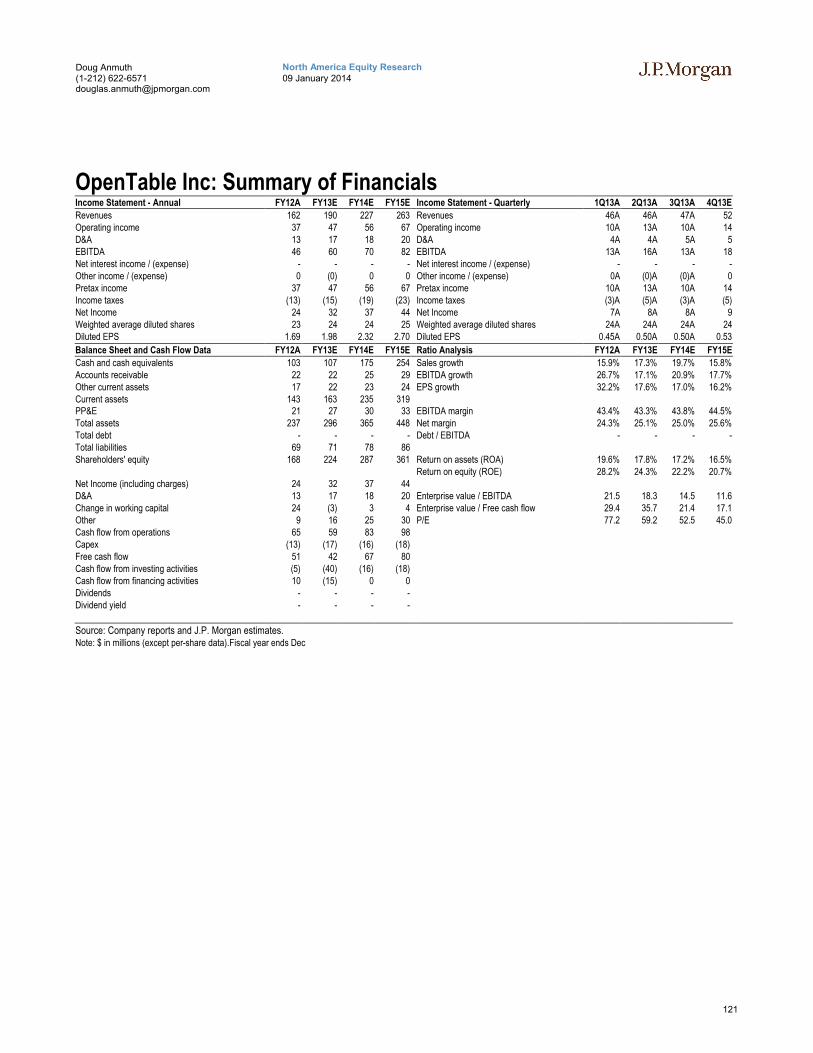

OpenTable Inc ............................................................................... 118

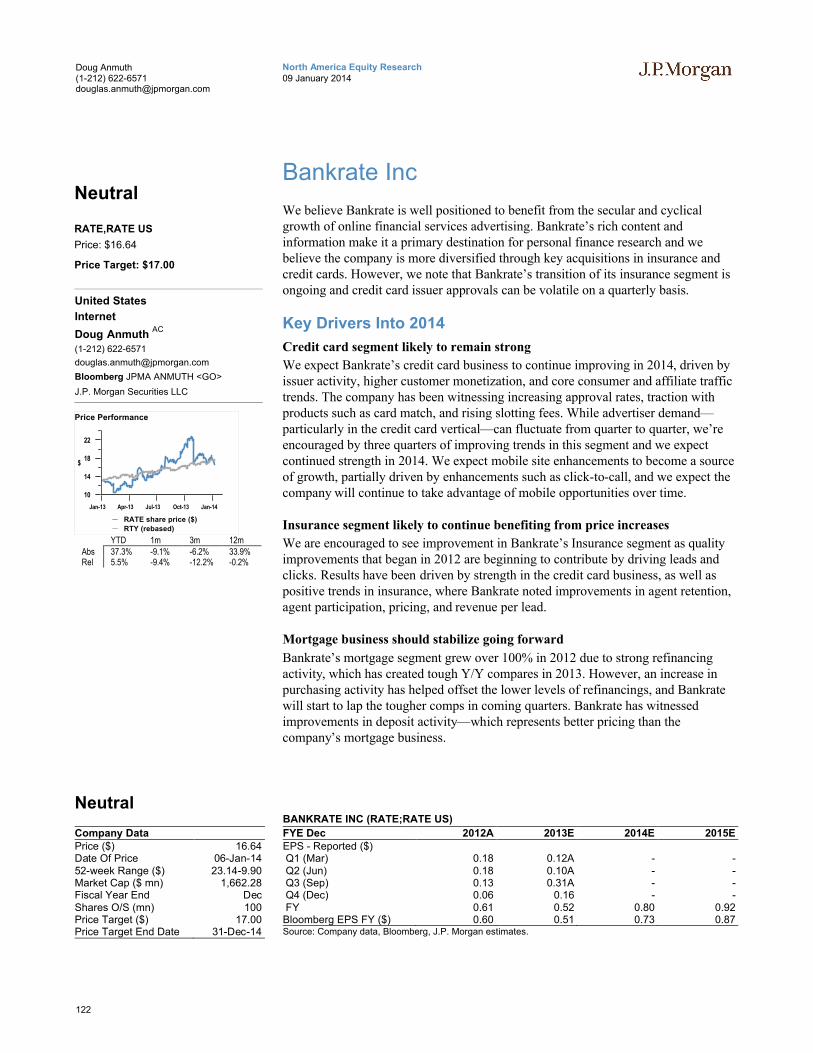

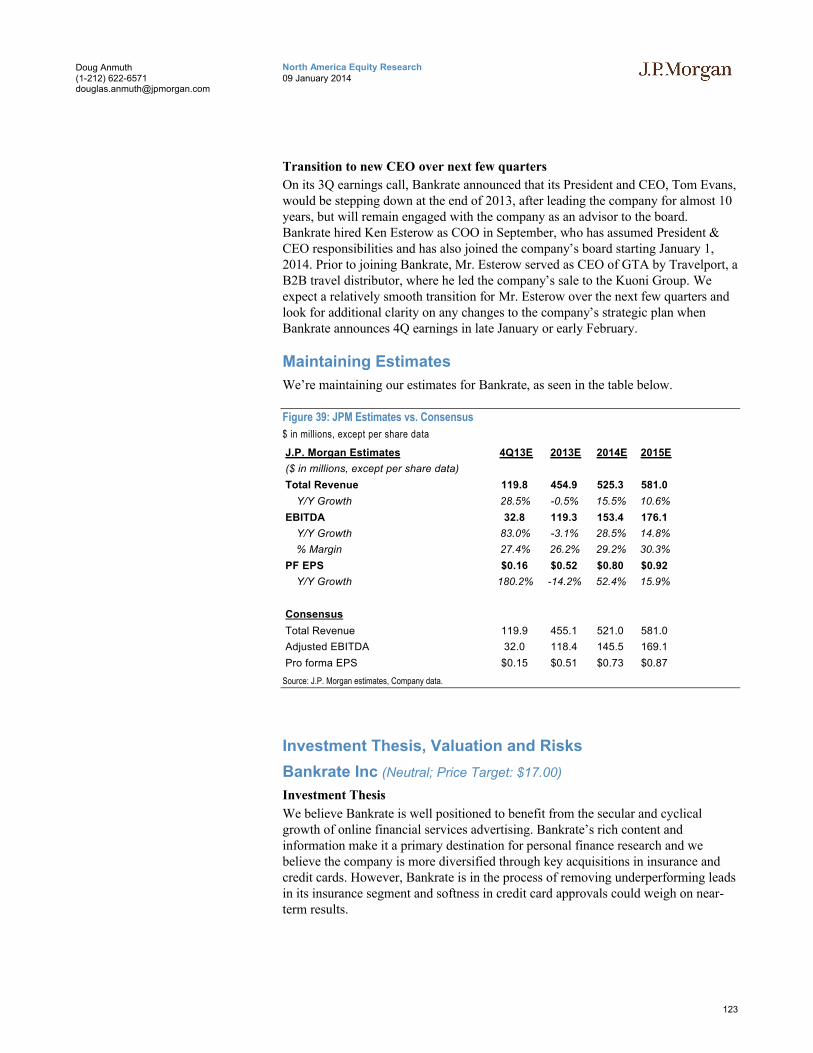

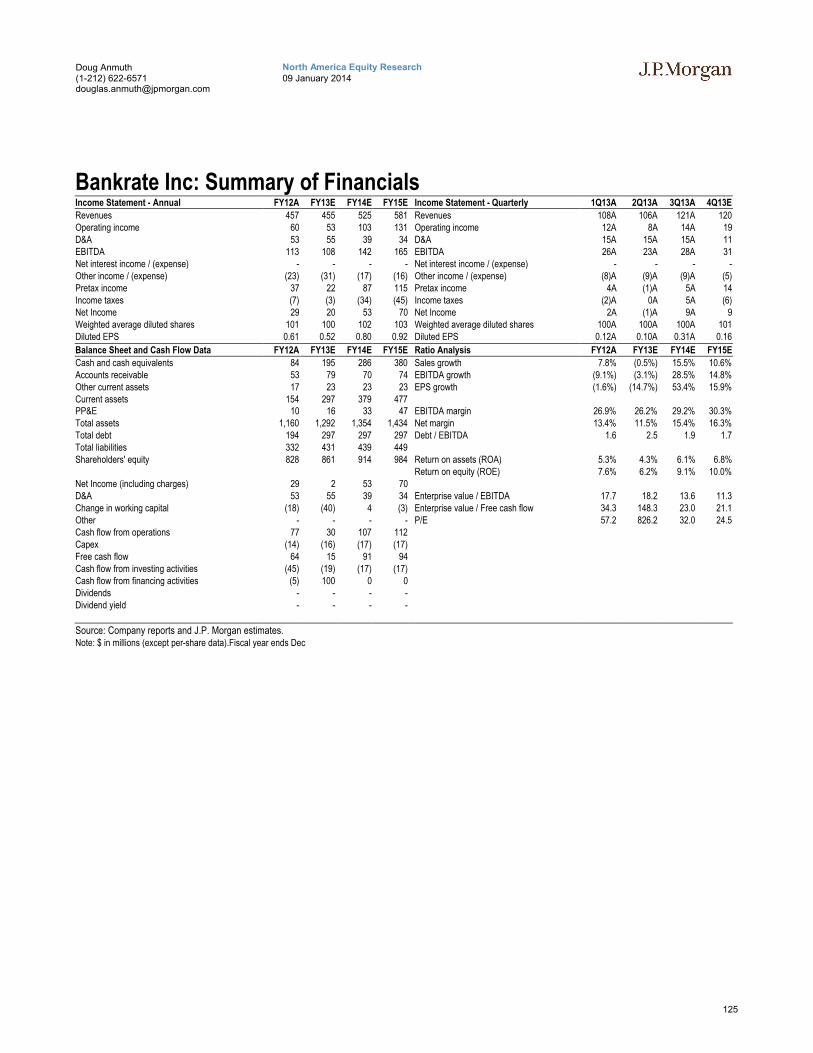

Bankrate Inc................................................................................... 122

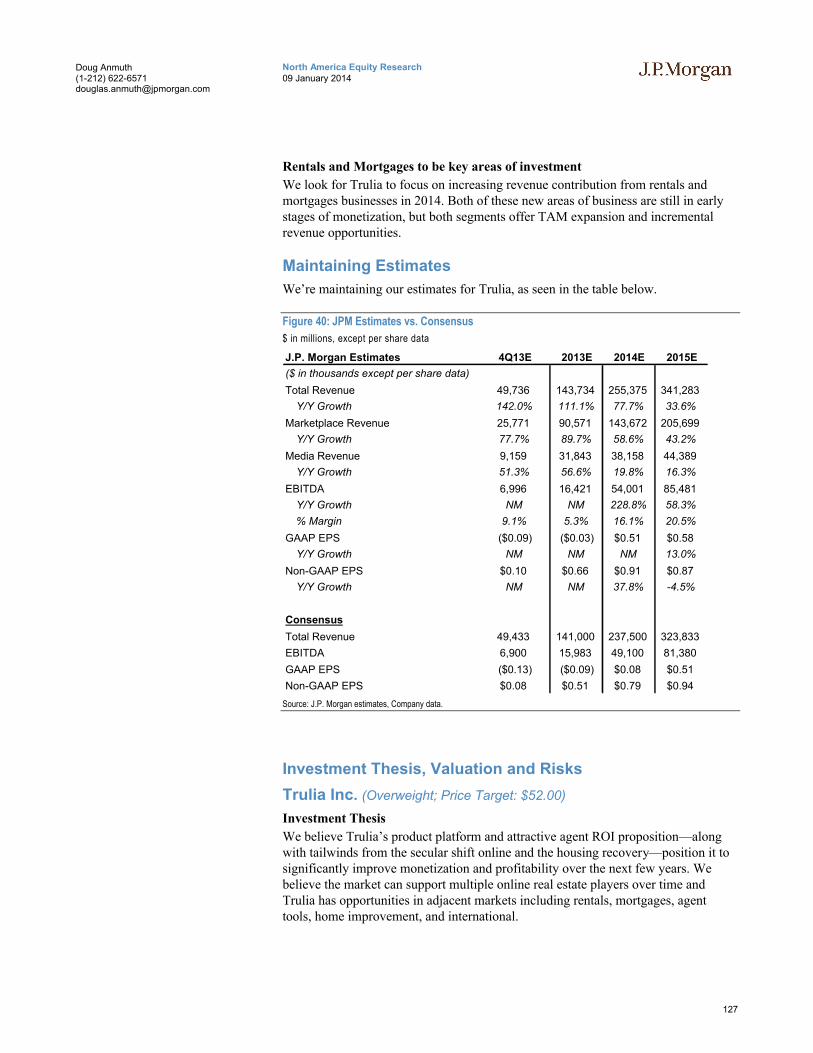

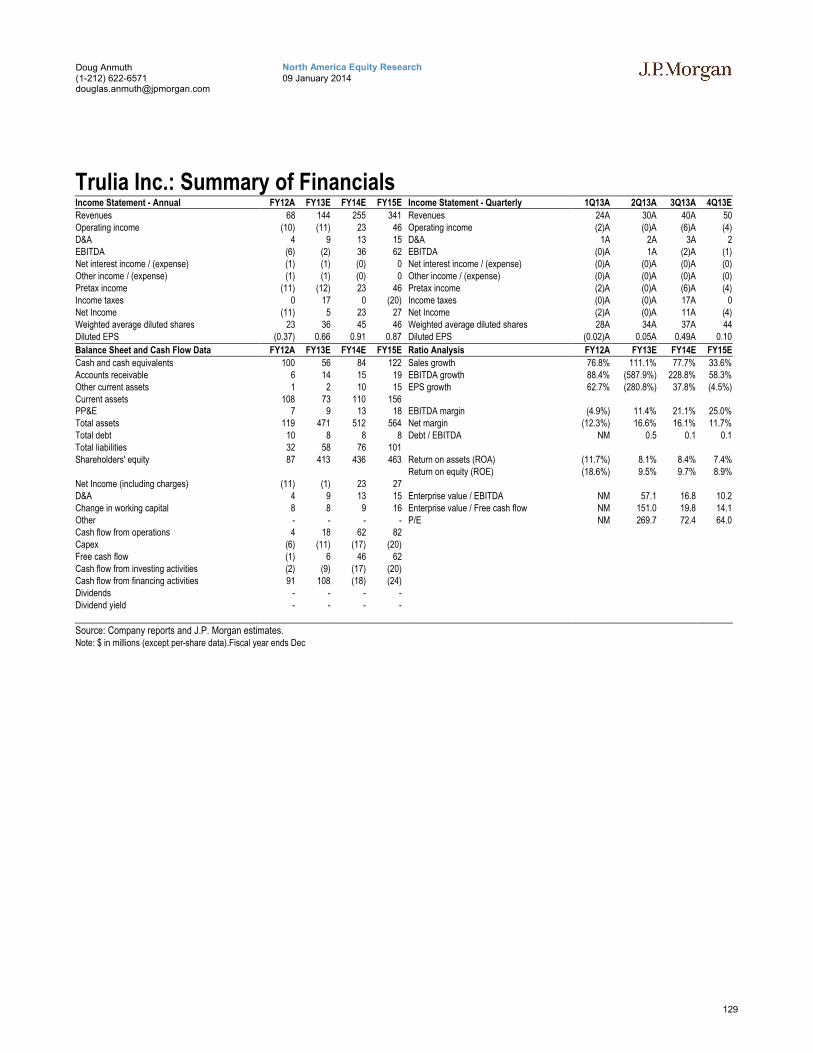

Trulia Inc. ....................................................................................... 126

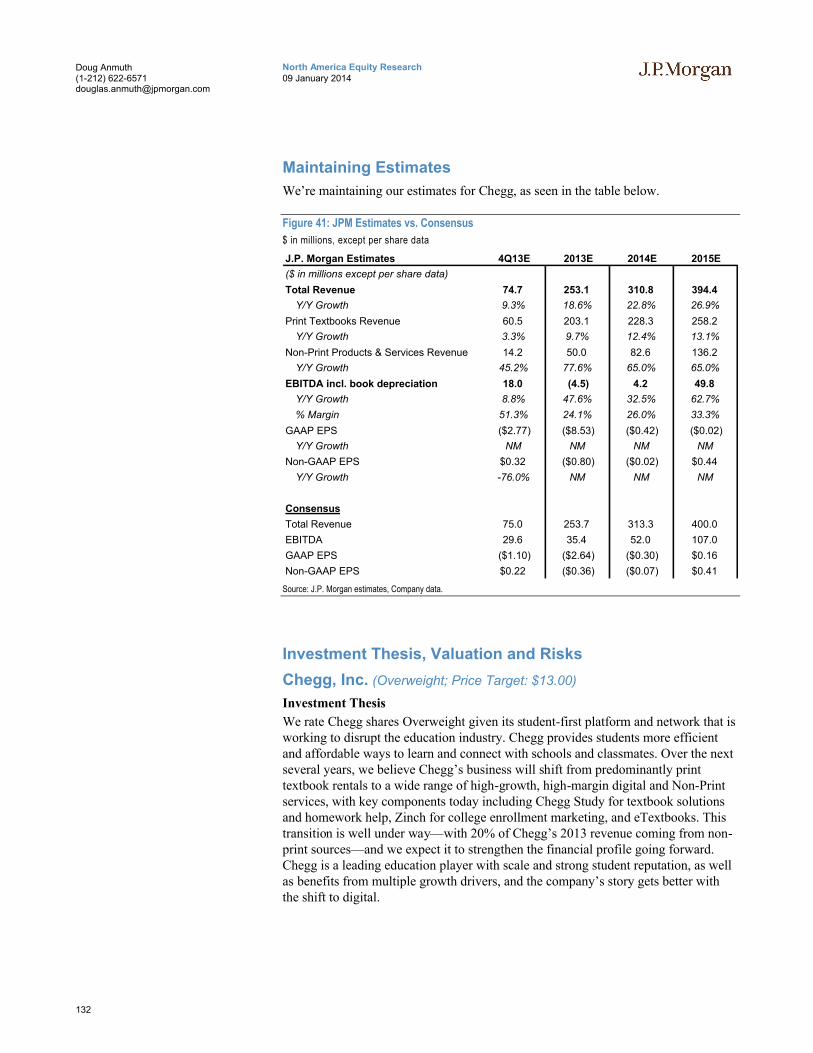

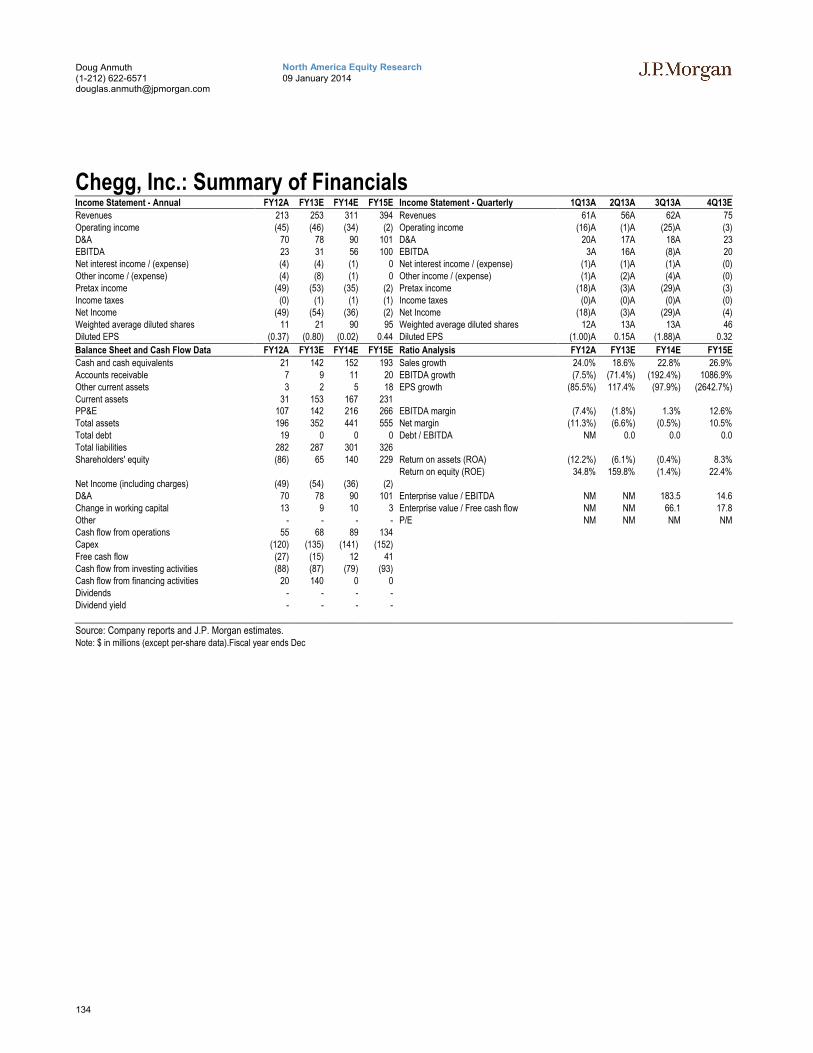

Chegg, Inc. .................................................................................... 130

4

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

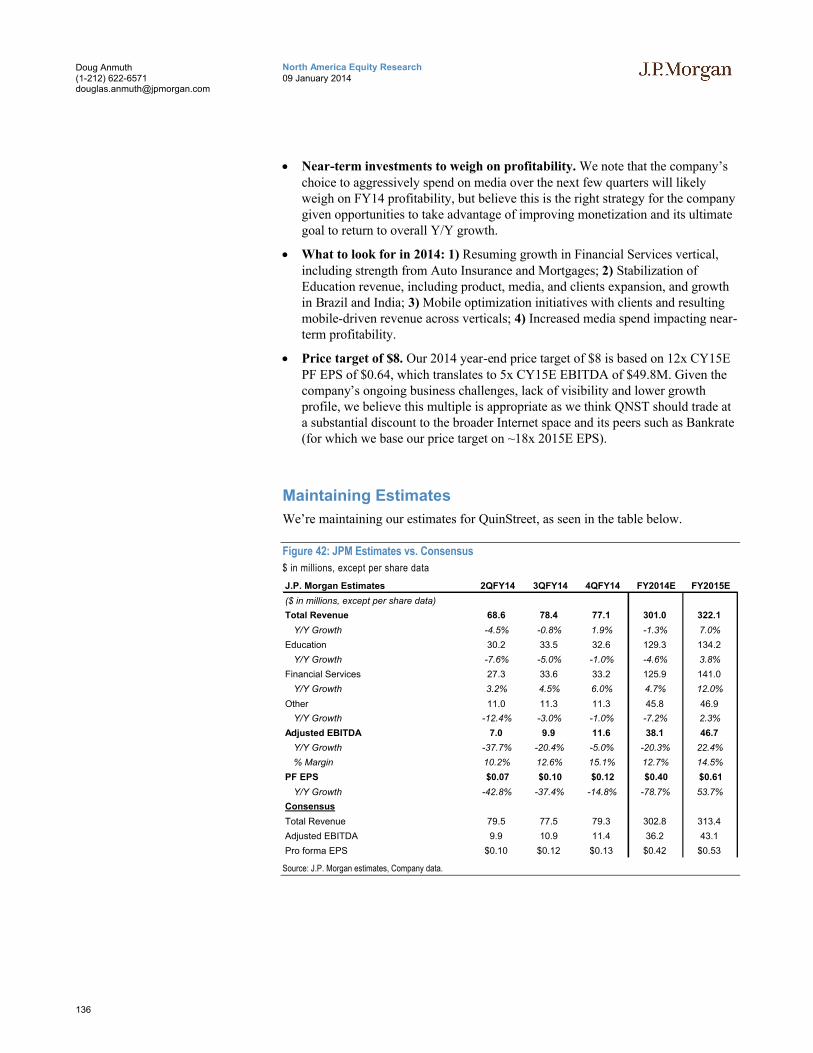

QuinStreet, Inc. .............................................................................. 135

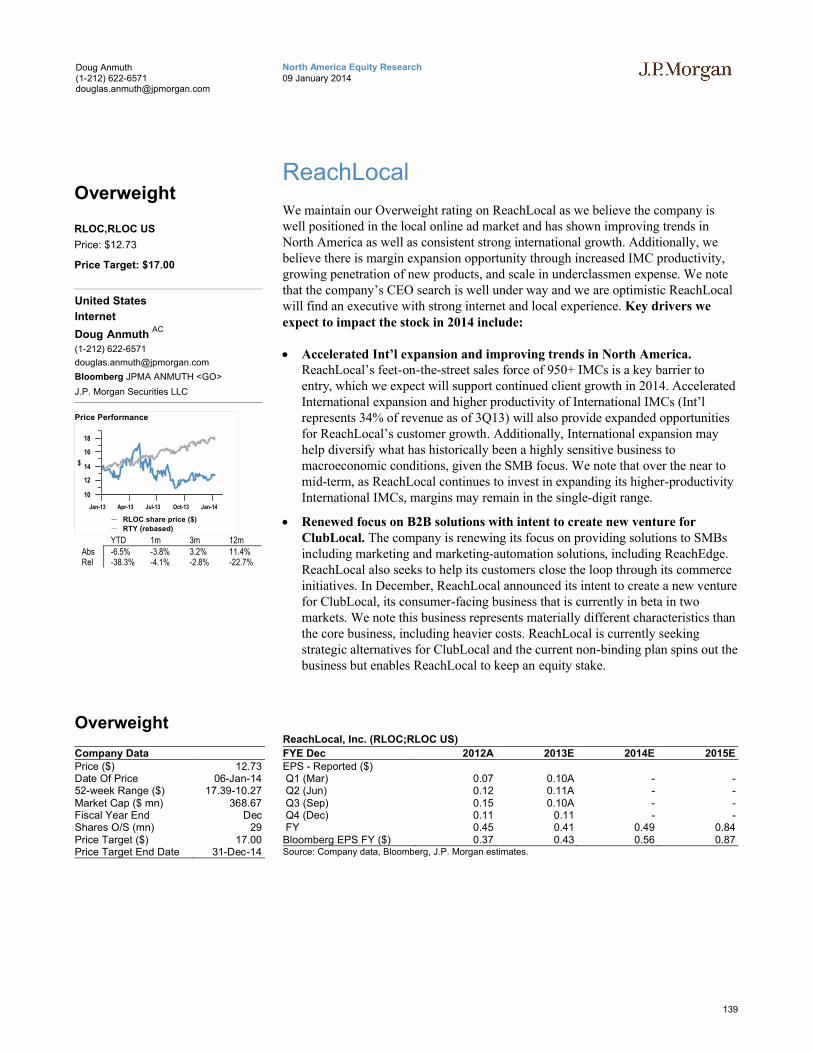

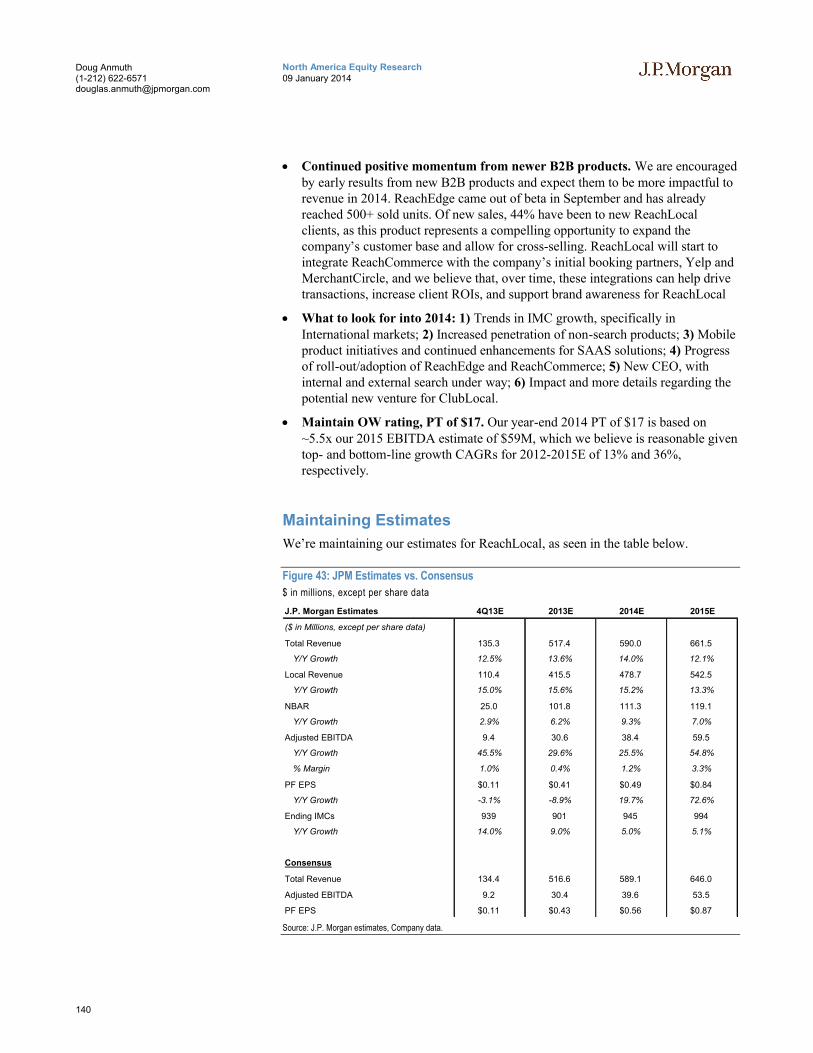

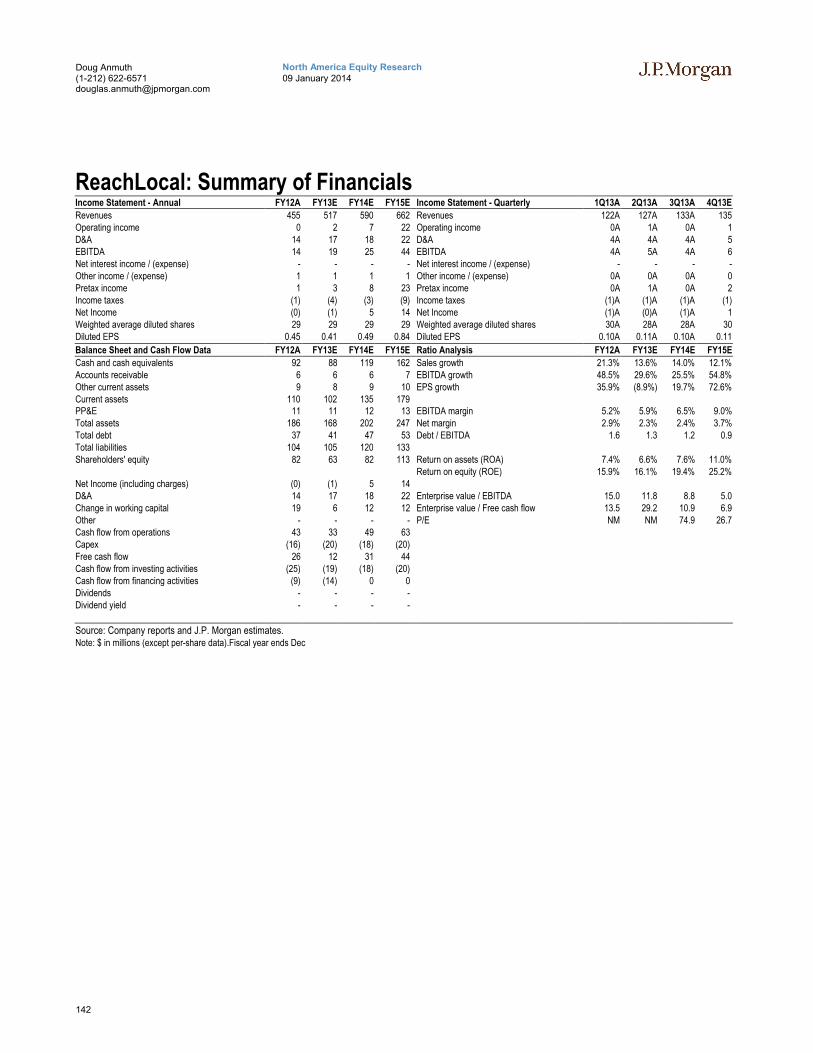

ReachLocal.................................................................................... 139

CafePress, Inc. .............................................................................. 143

LatAm Company Outlooks .......................................................... 147

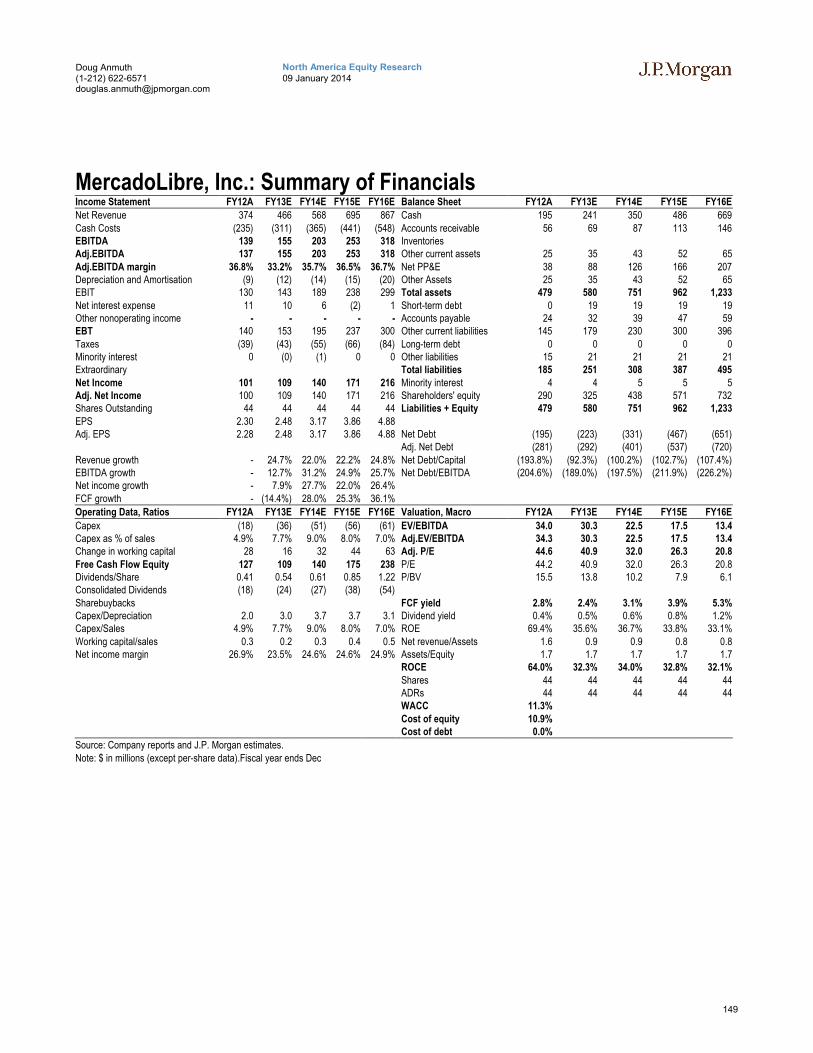

MercadoLibre, Inc. ......................................................................... 147

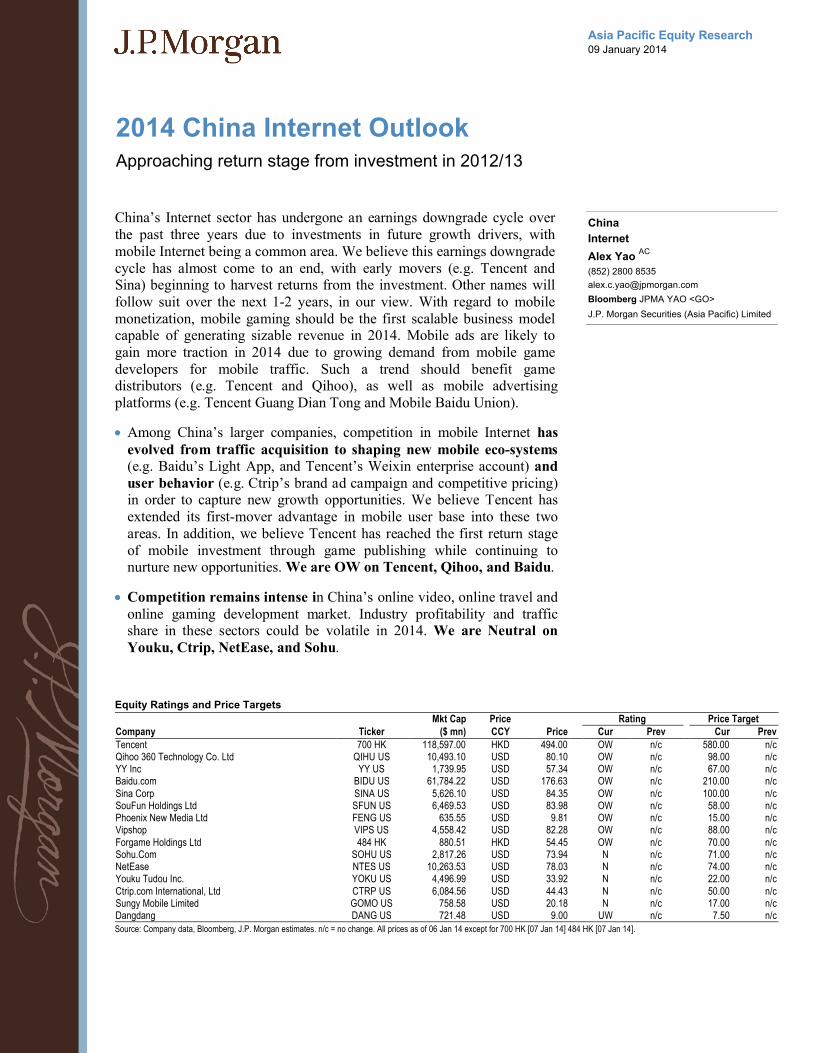

China Sector Outlook .................................................................. 150

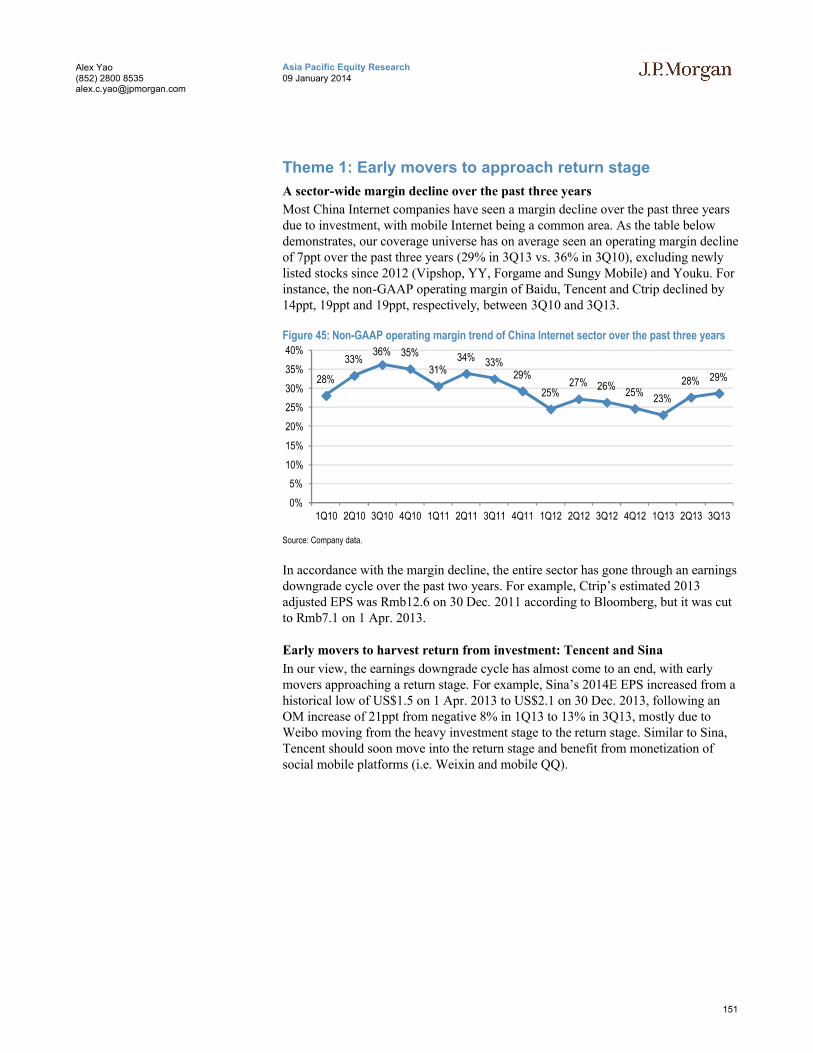

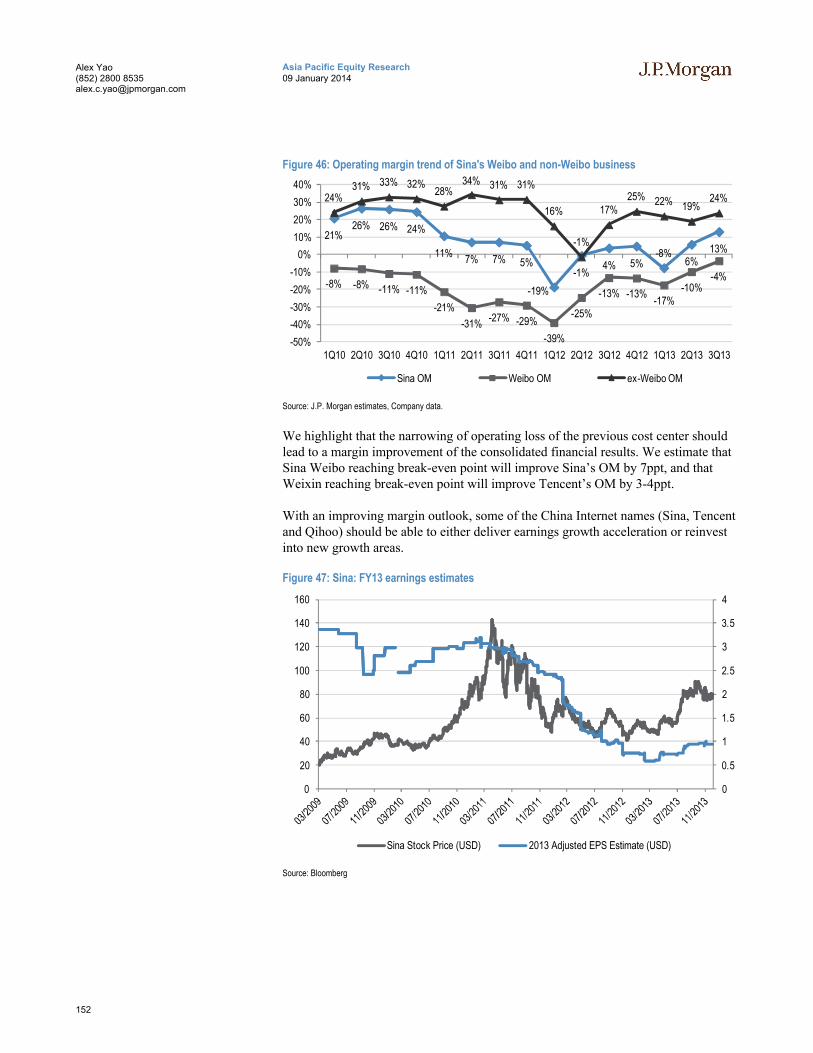

Early movers to approach return stage........................................... 151

Mobile game monetization to drive mobile traffic platforms’ earnings growth in 2014 ............................................................................... 154

Large mobile platforms attempting to shape new eco-system and user behavior......................................................................................... 158

Uncertainty in 2014 video outlook .................................................. 160

Continued growth of online-to-offline business; room for cooperation with big mobile platforms................................................................ 163

Online travel remains highly competitive ........................................ 165

China Company Outlooks ........................................................... 167

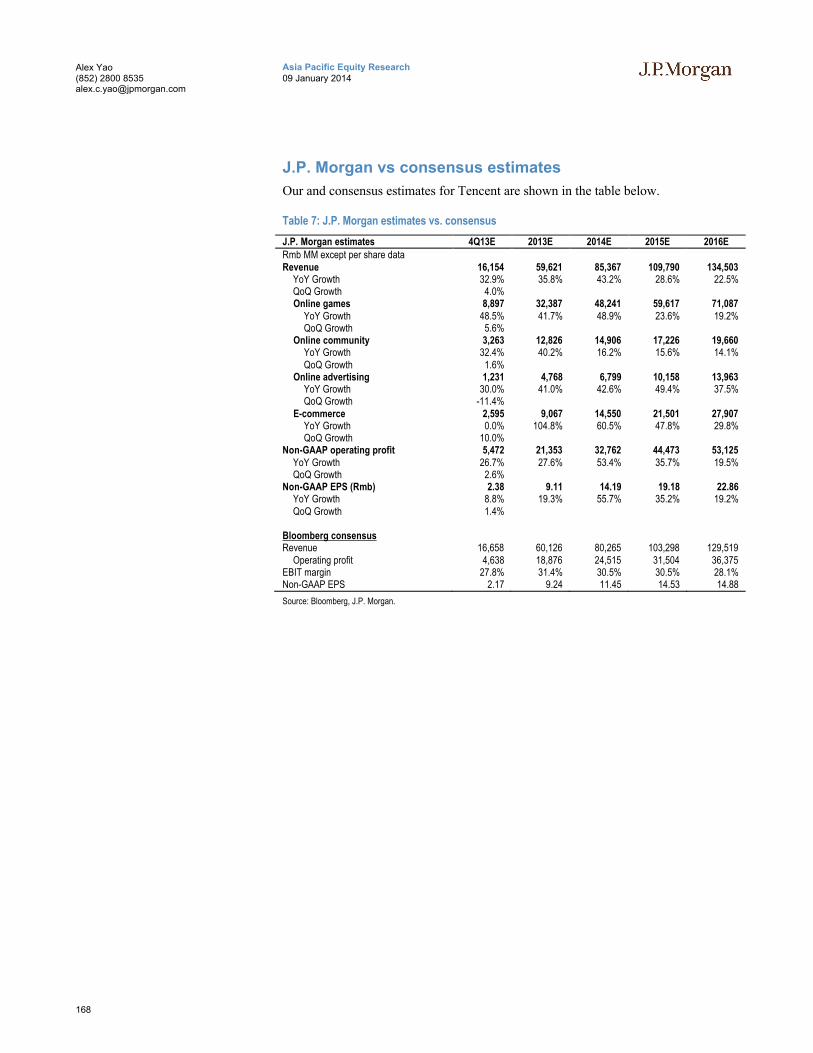

Tencent.......................................................................................... 167

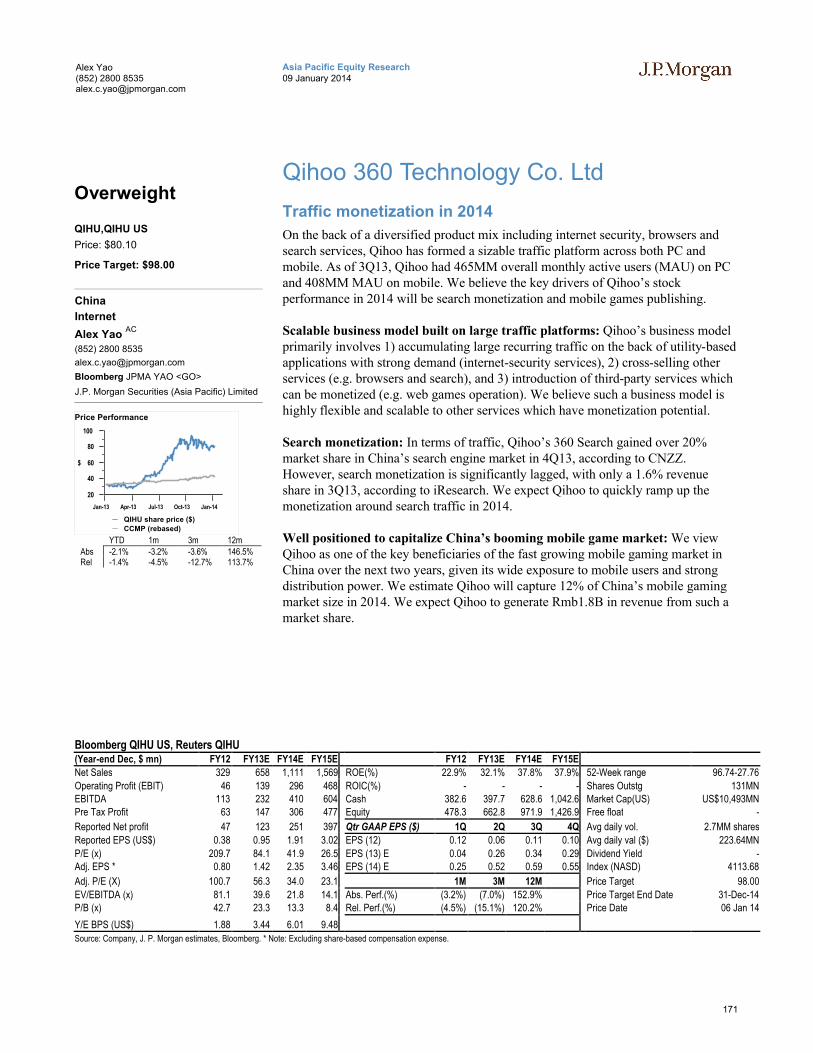

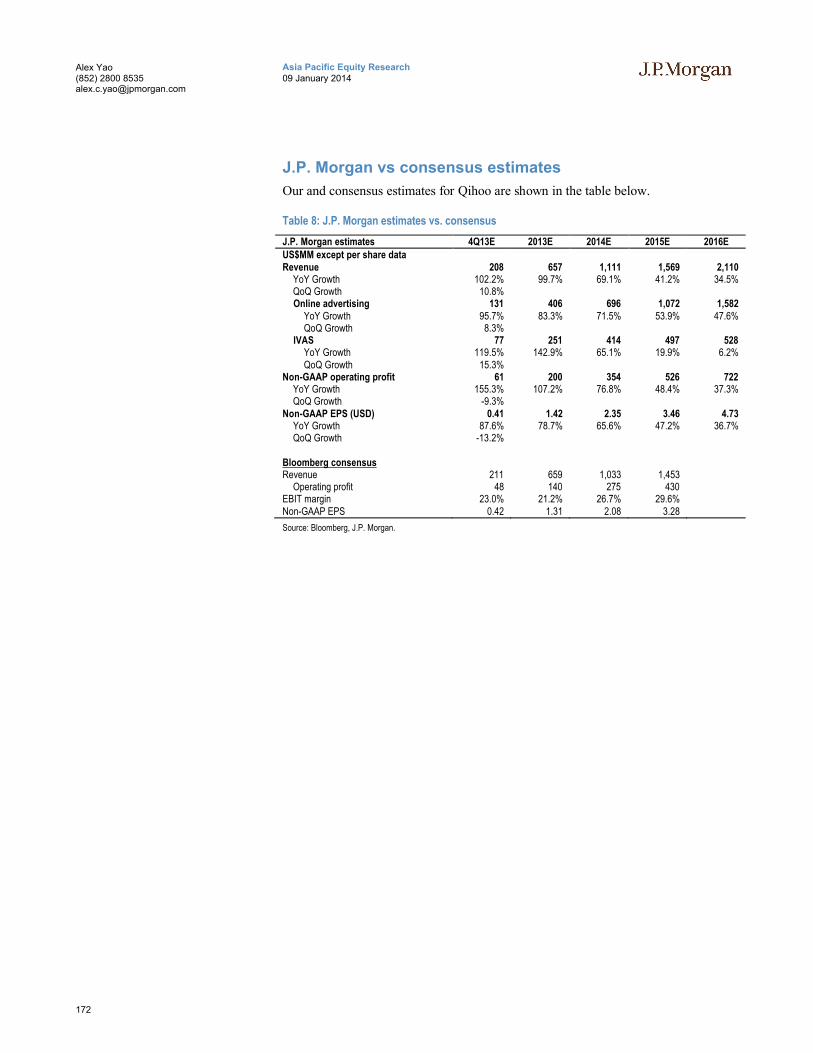

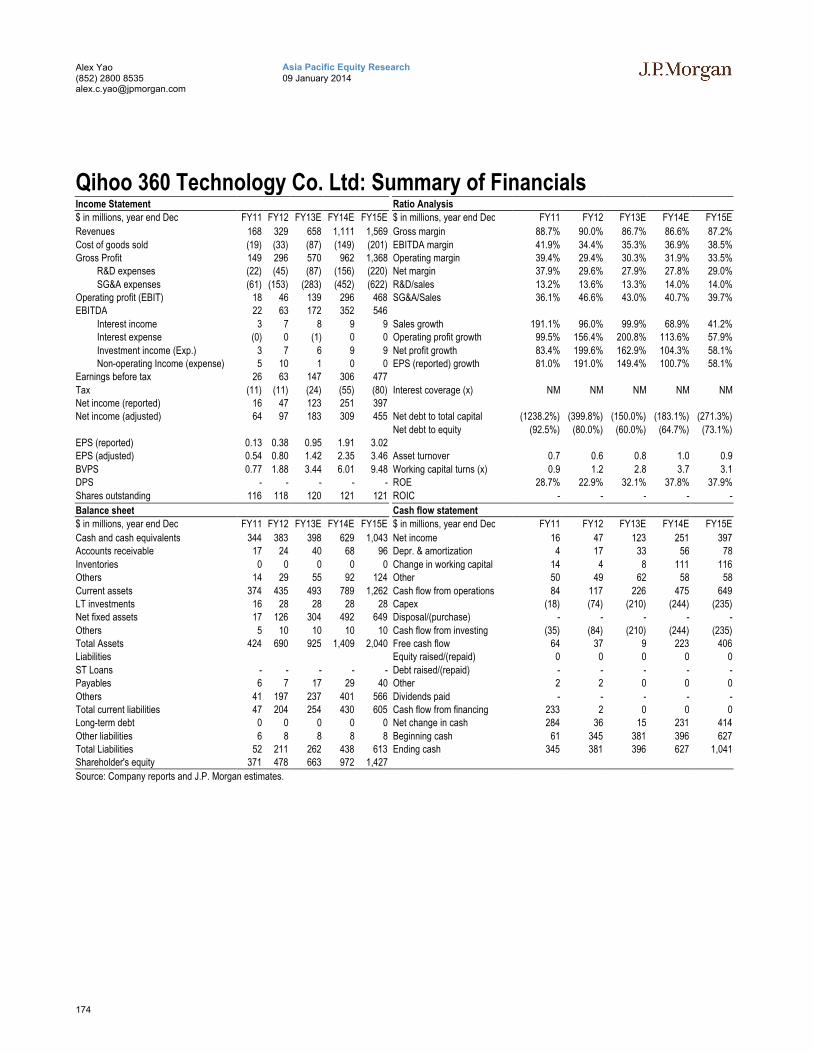

Qihoo 360 Technology Co. Ltd....................................................... 171

YY Inc ............................................................................................ 175

Baidu.com...................................................................................... 179

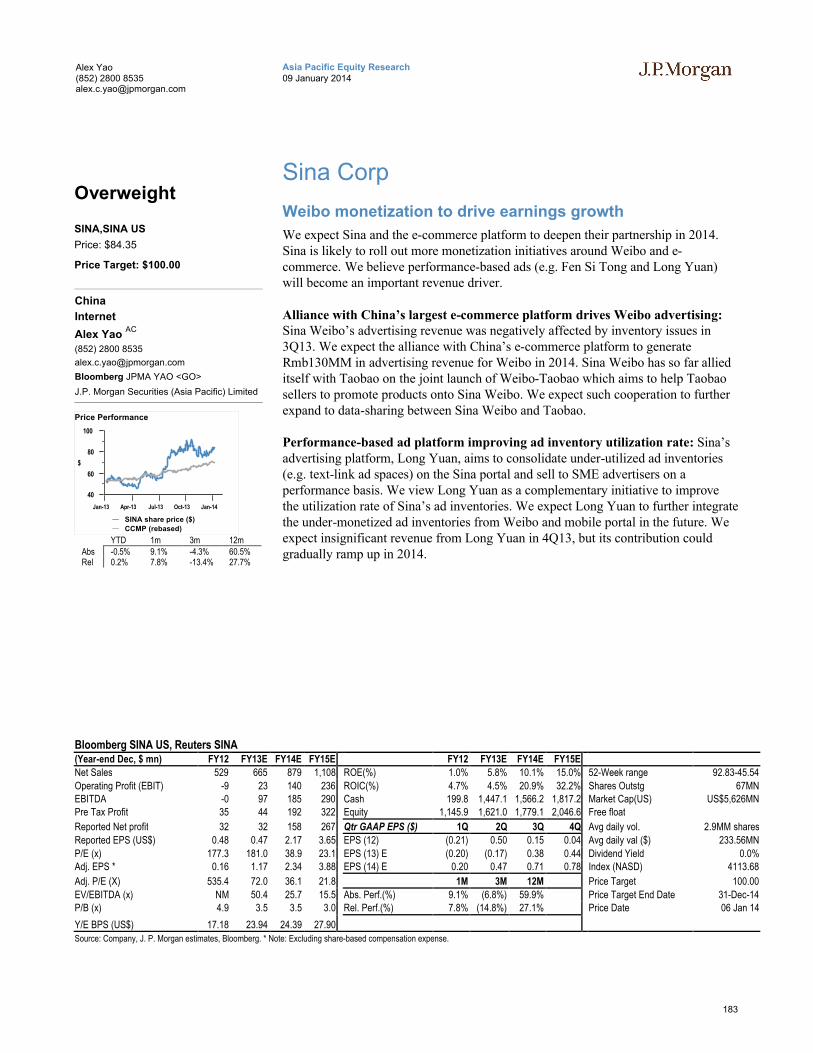

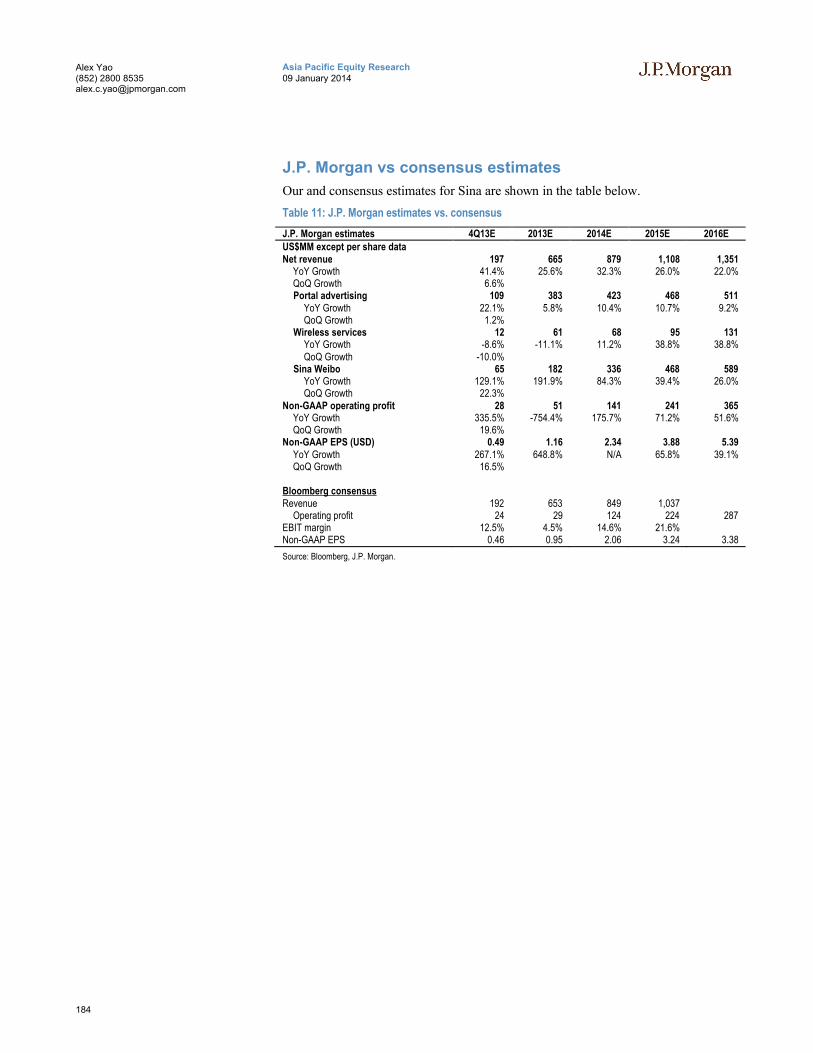

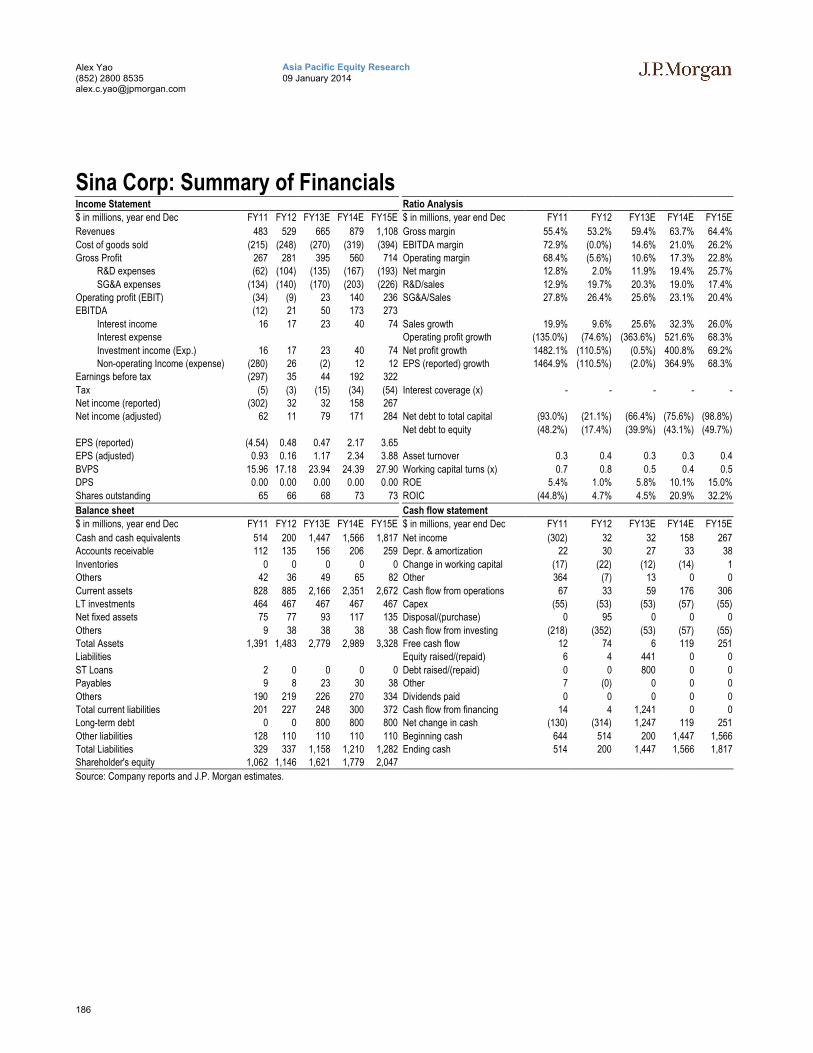

Sina Corp....................................................................................... 183

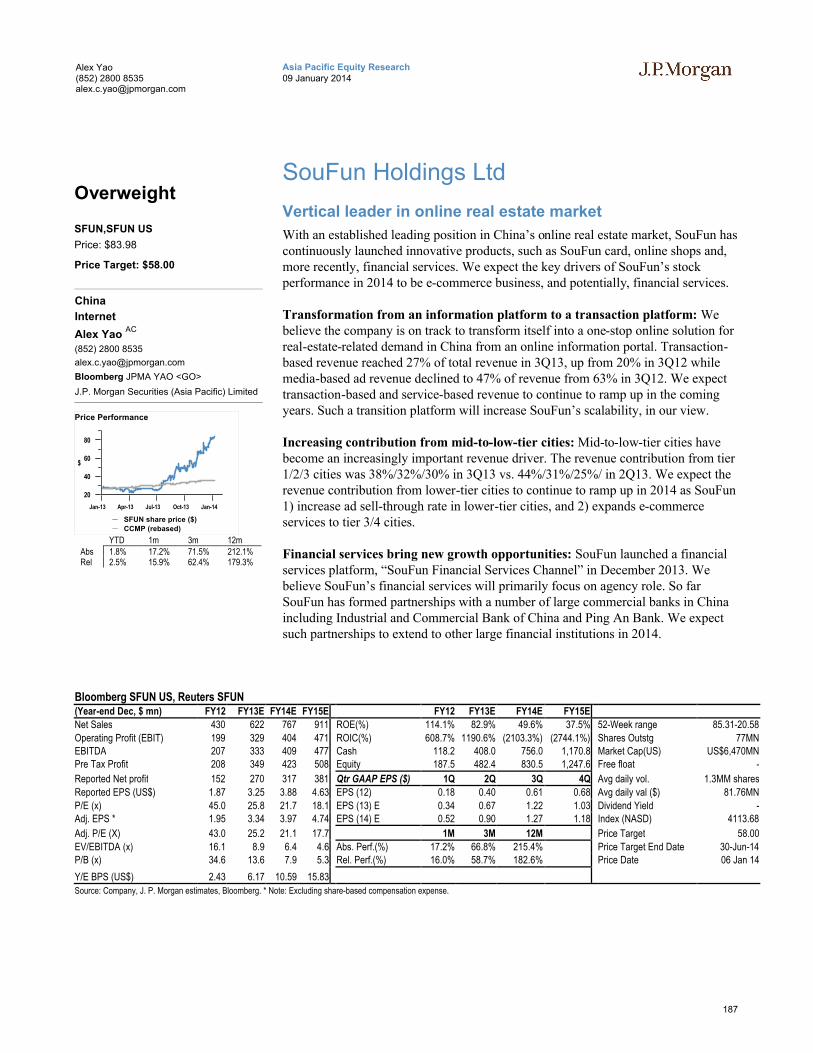

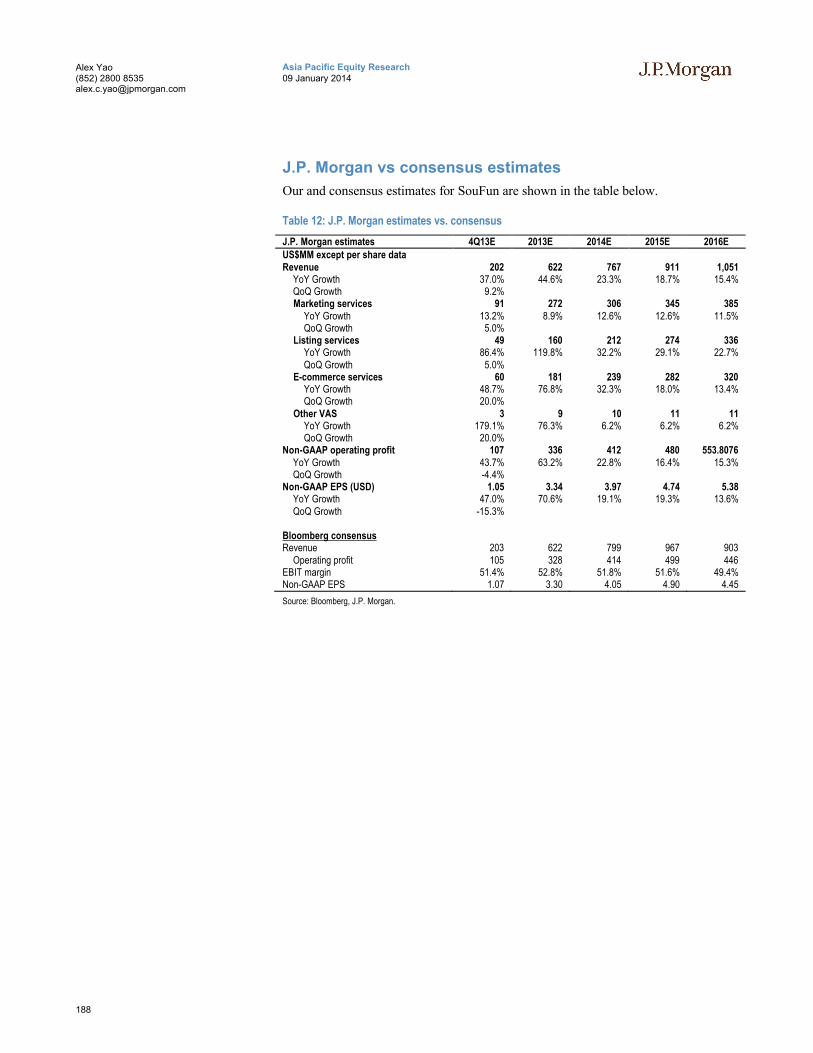

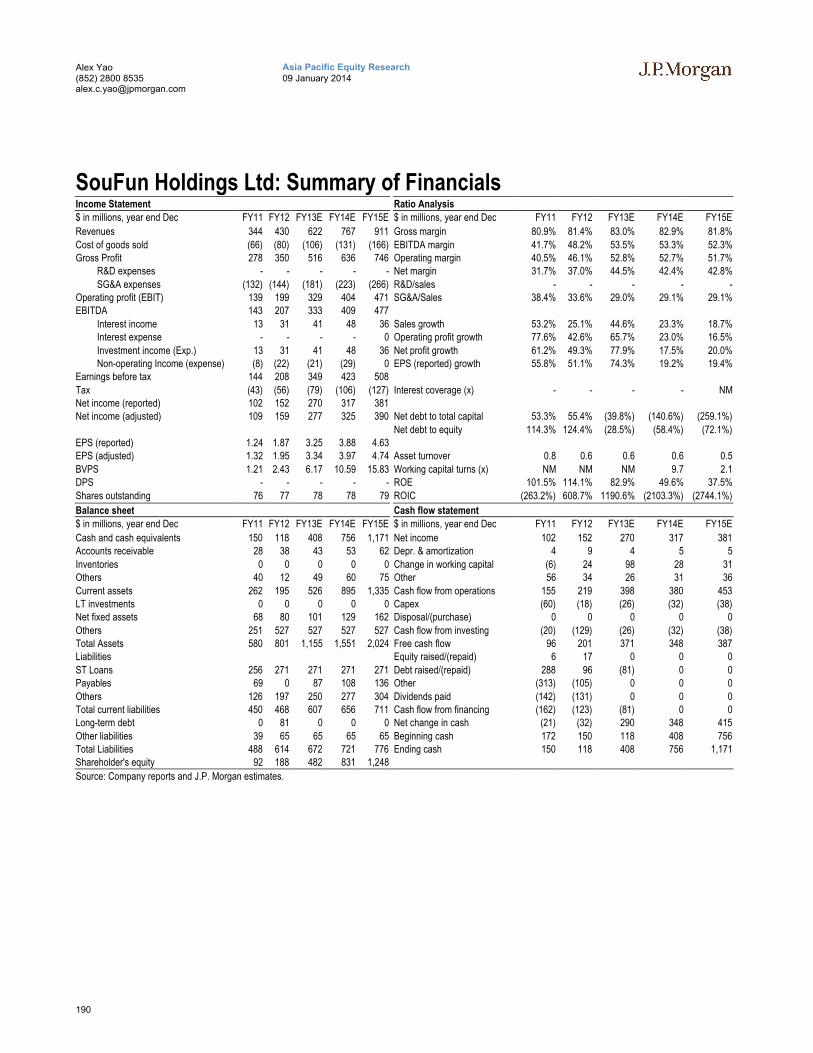

SouFun Holdings Ltd...................................................................... 187

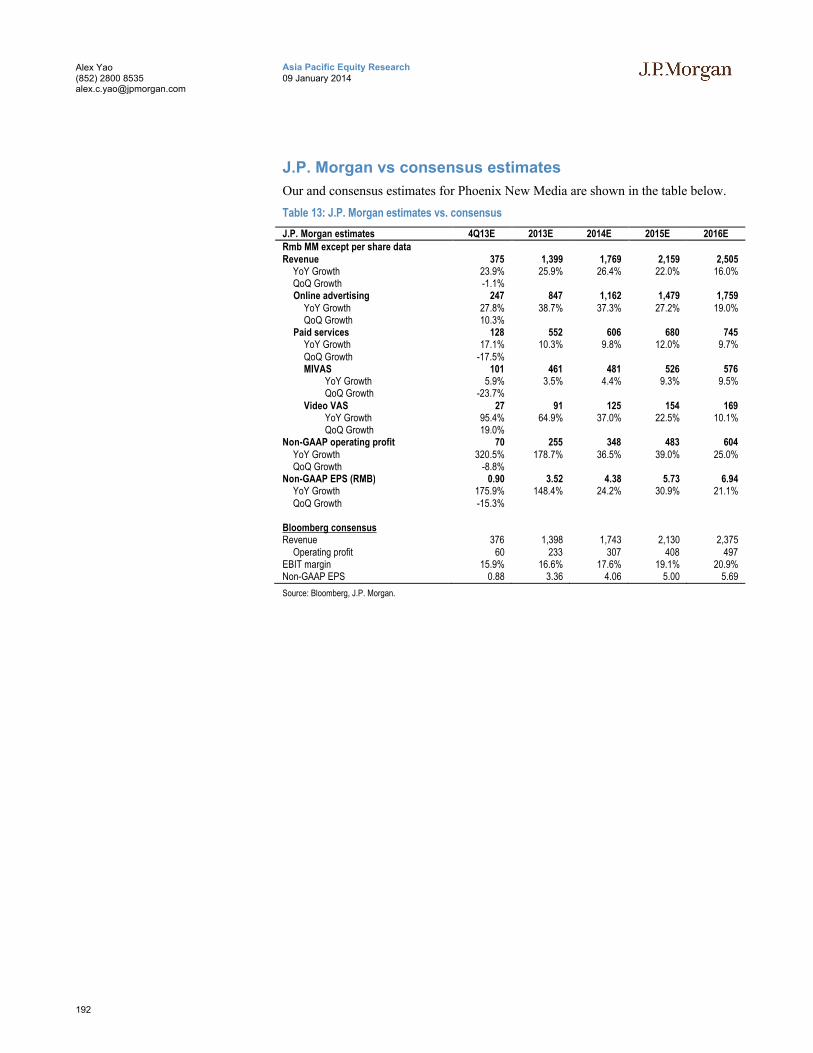

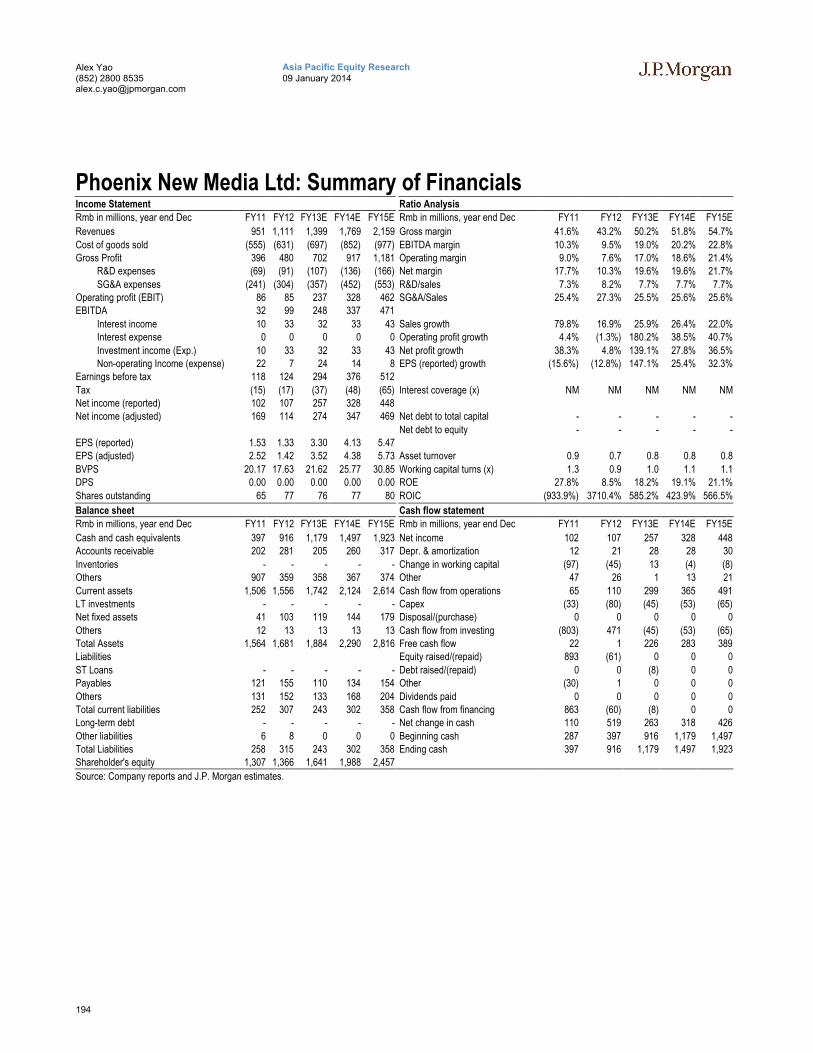

Phoenix New Media Ltd ................................................................. 191

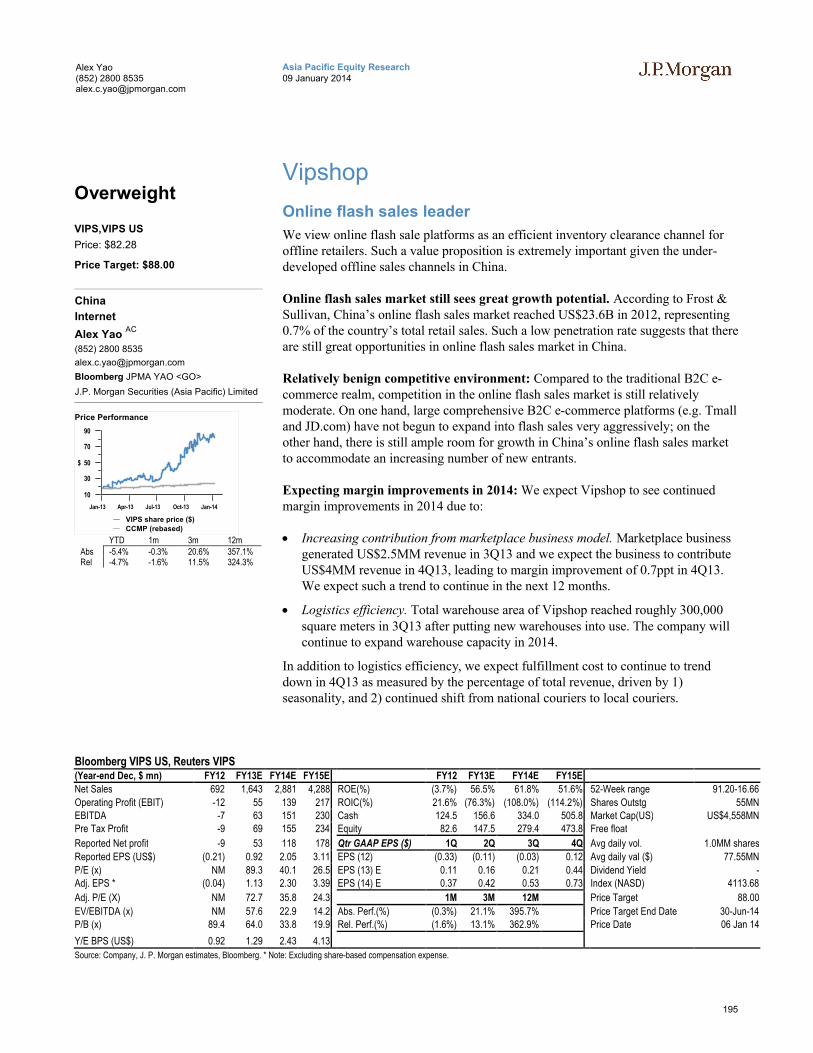

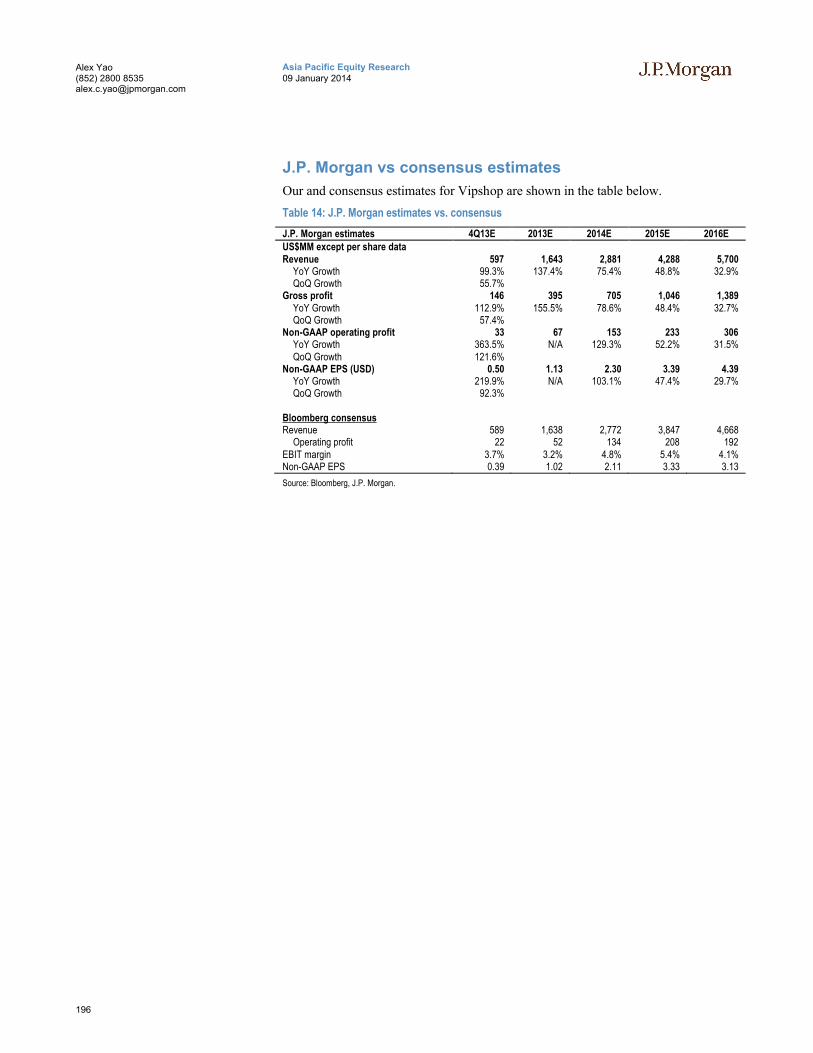

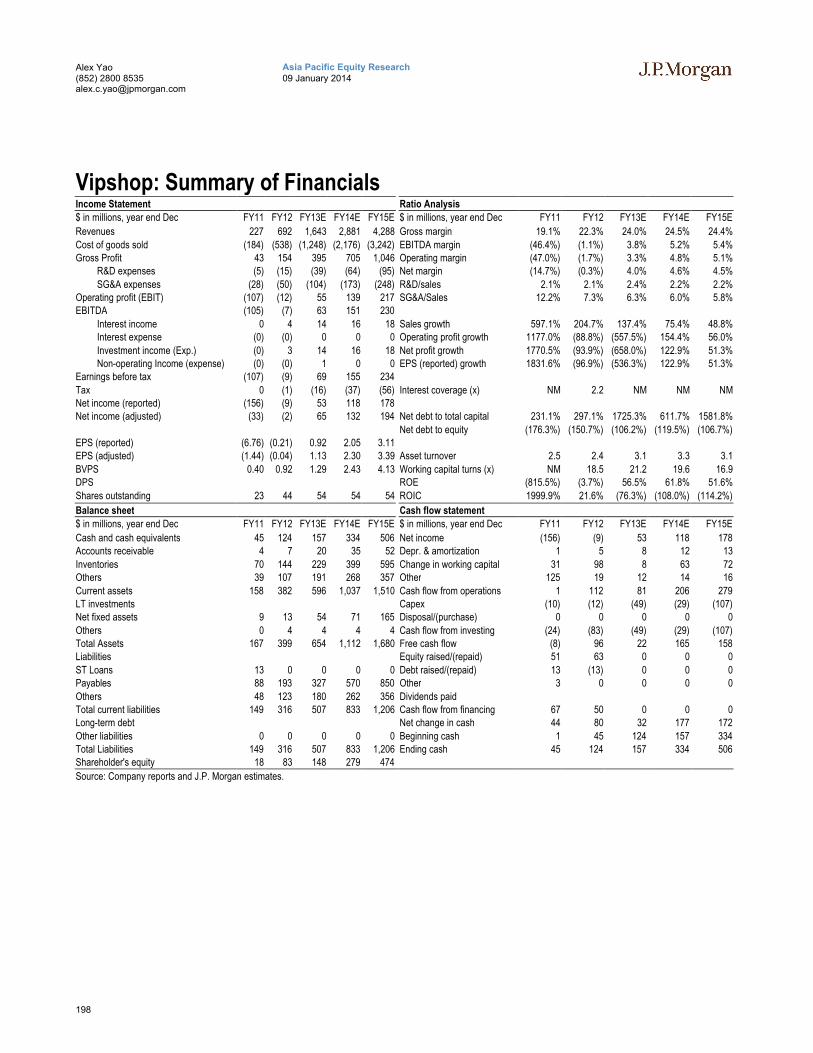

Vipshop.......................................................................................... 195

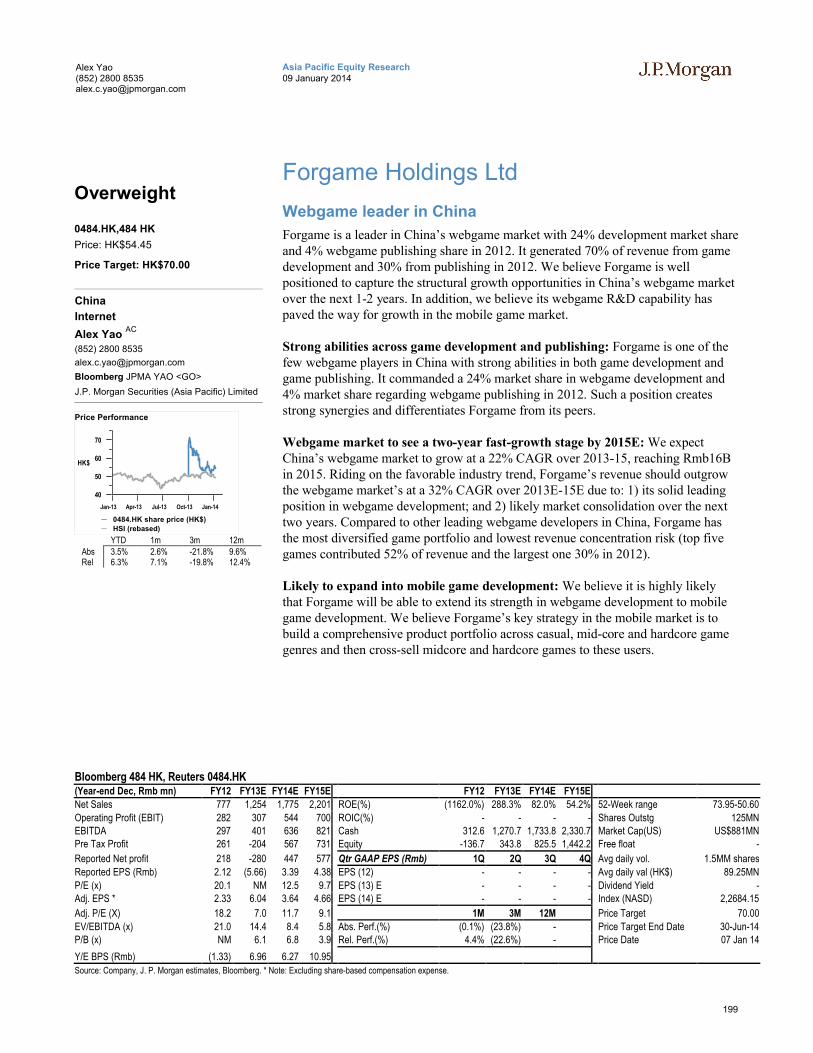

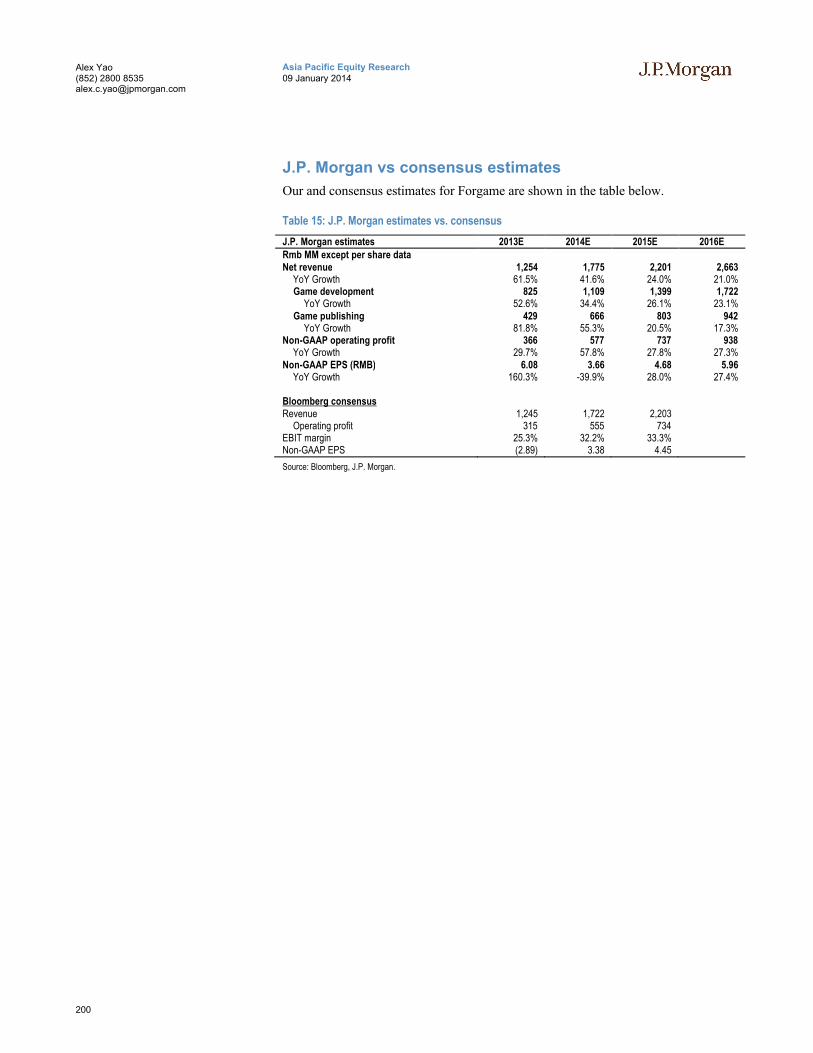

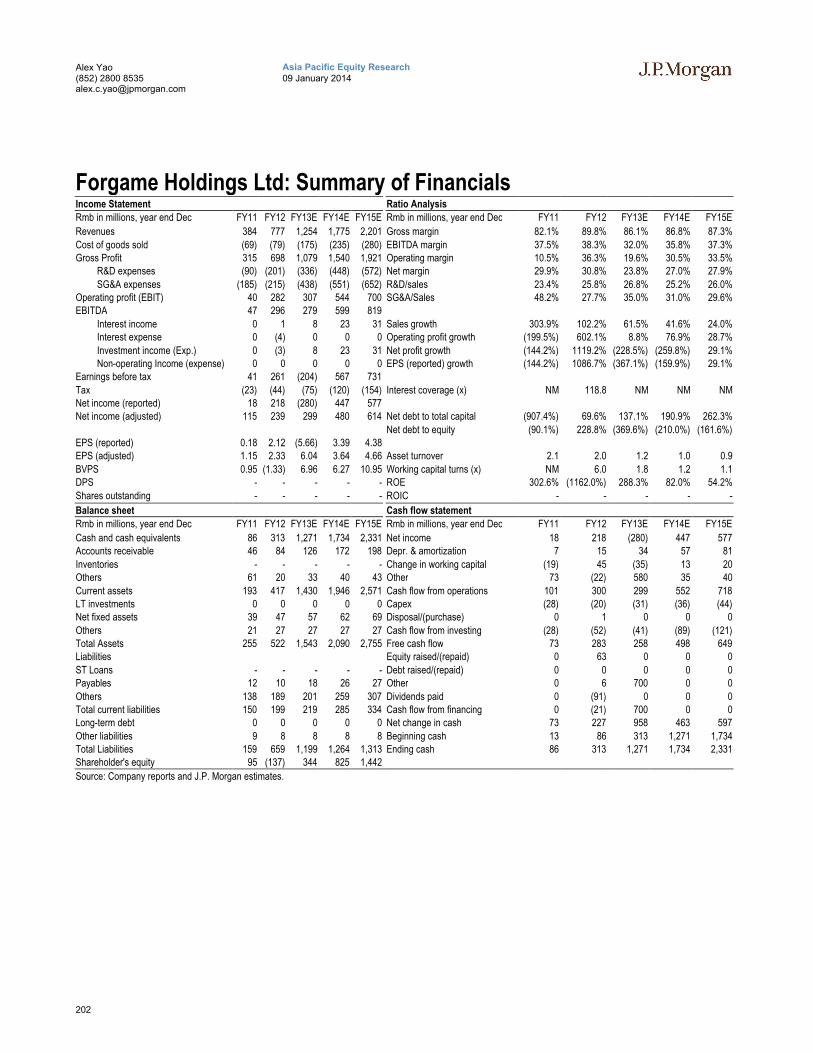

Forgame Holdings Ltd.................................................................... 199

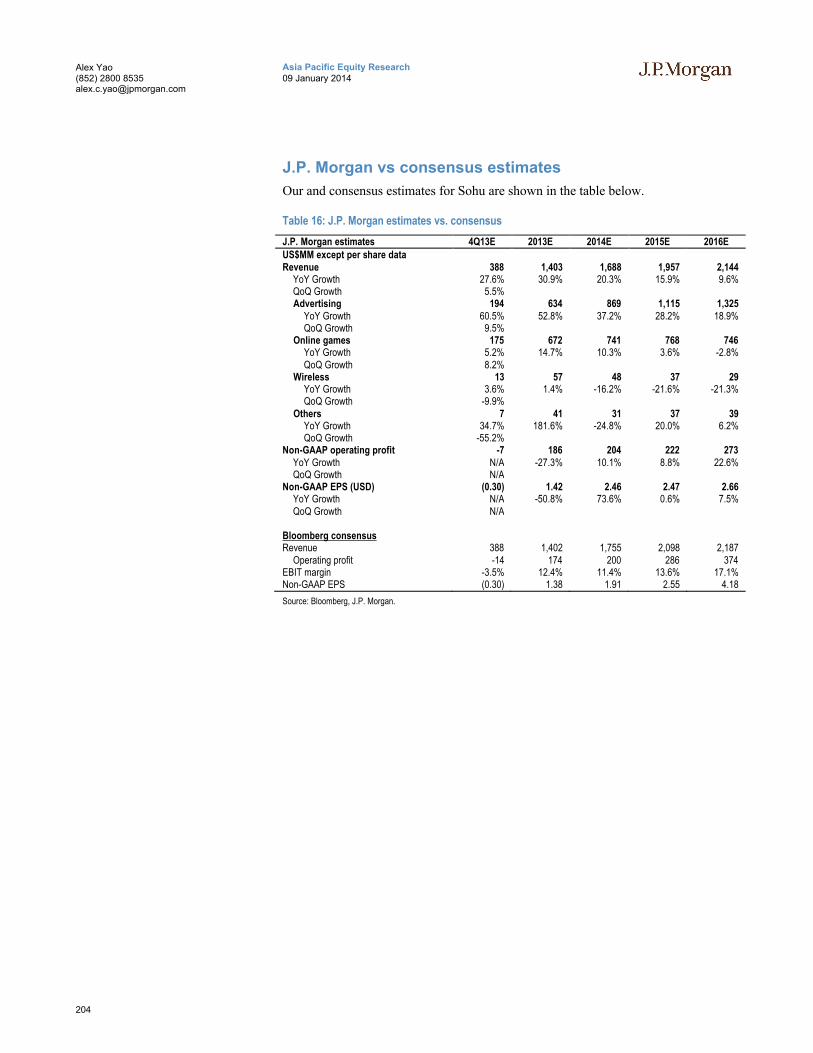

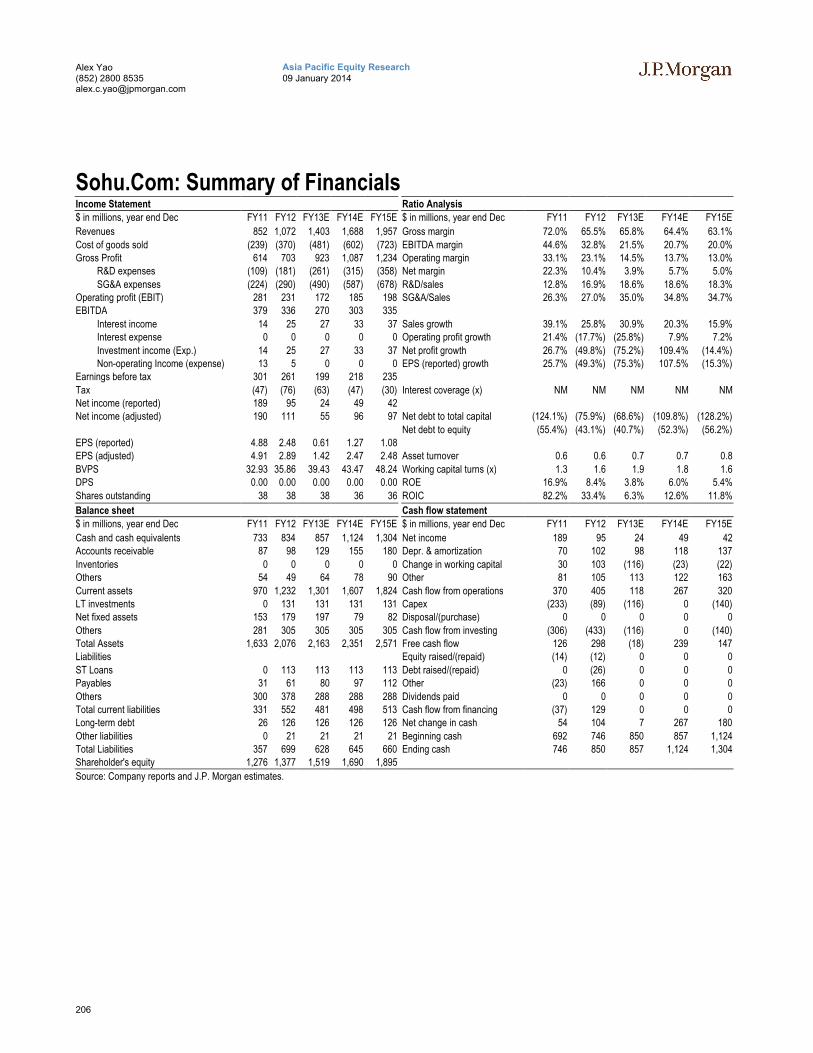

Sohu.Com...................................................................................... 203

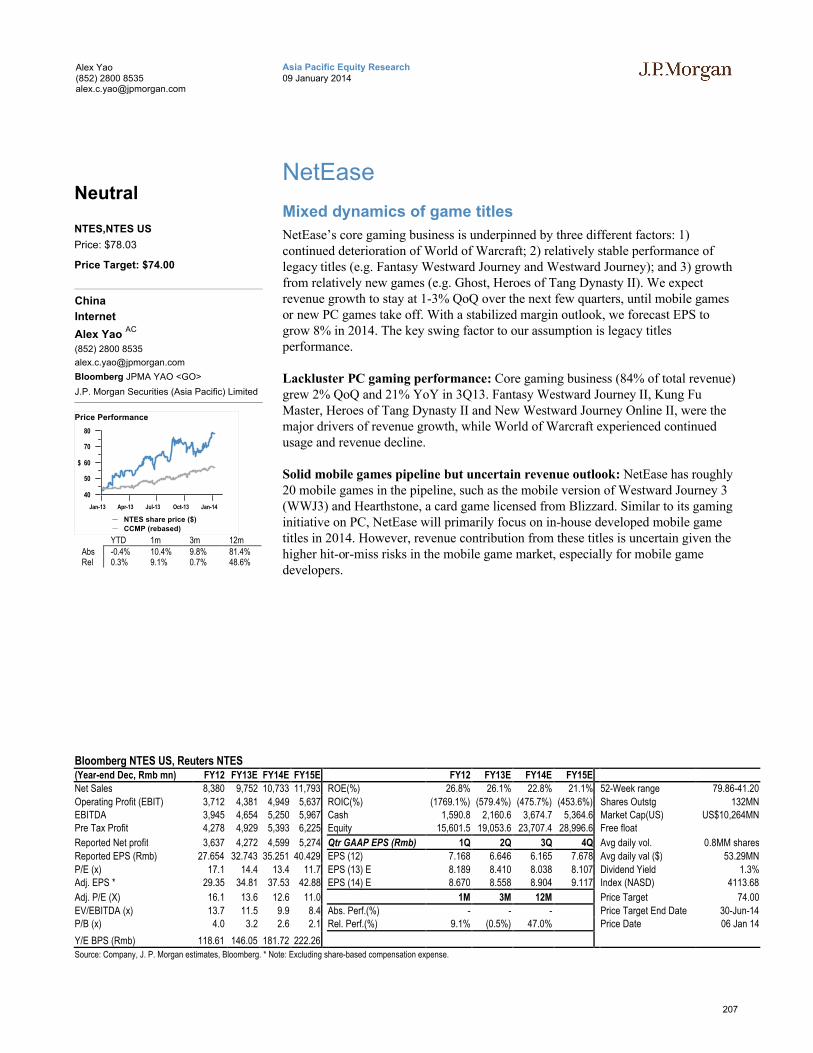

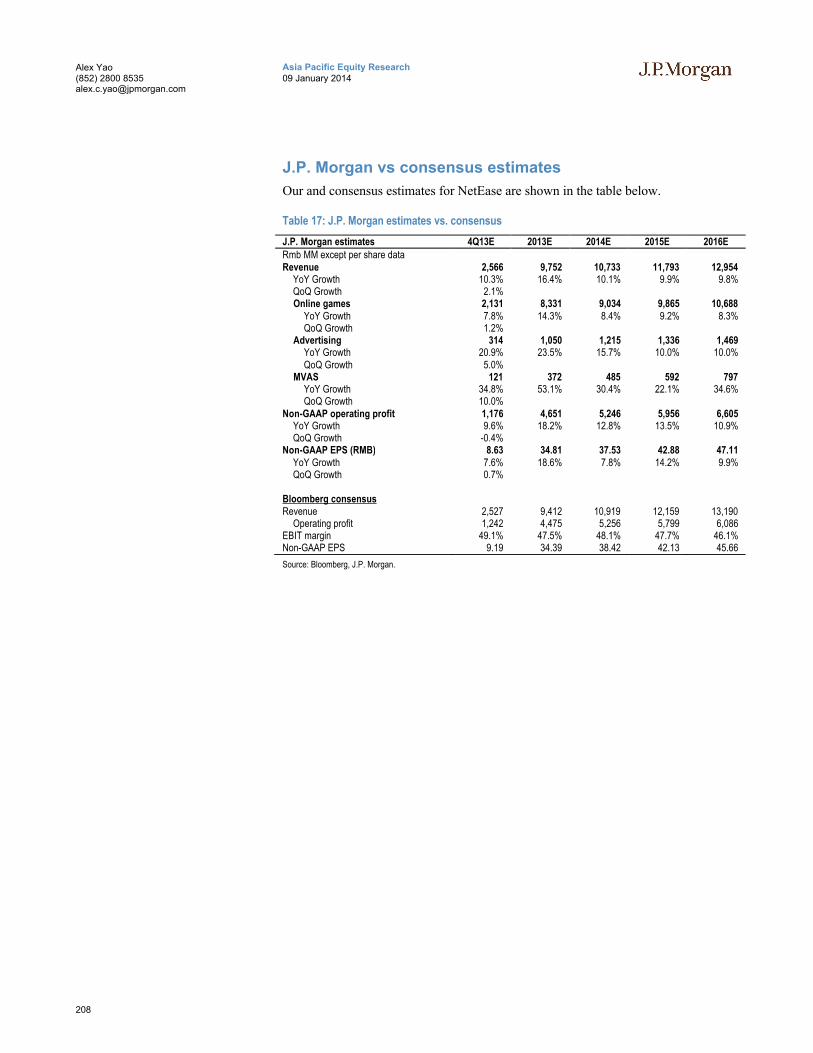

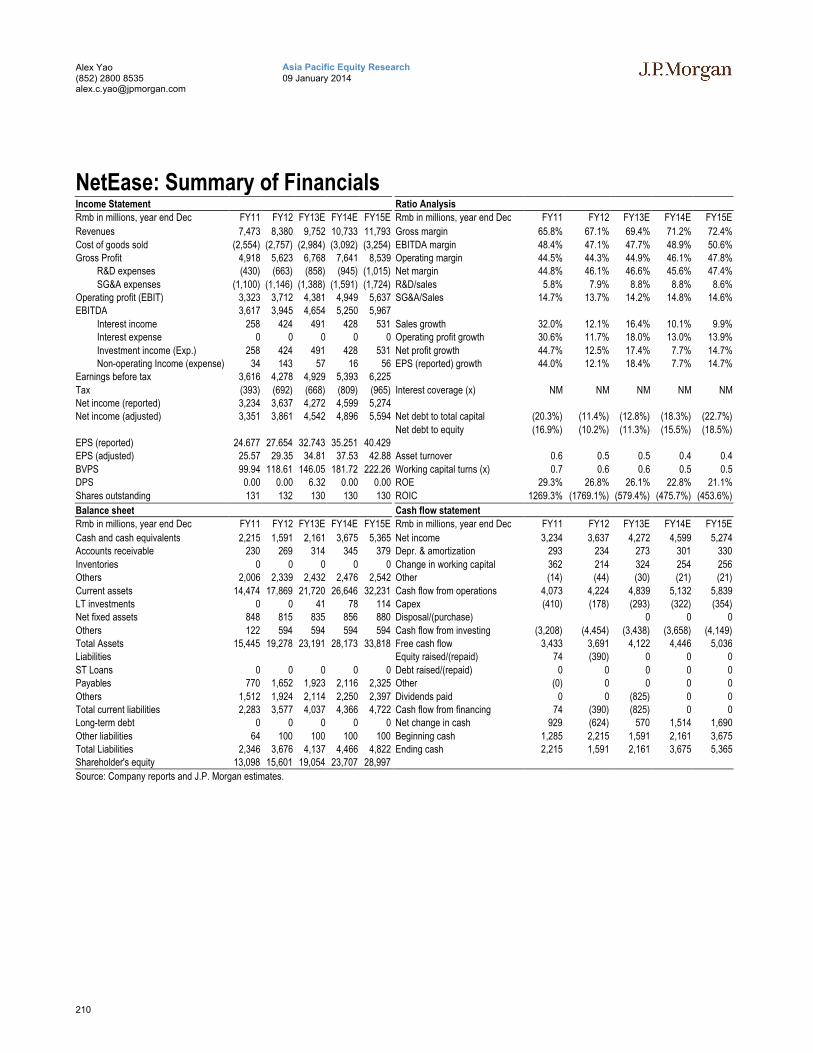

NetEase......................................................................................... 207

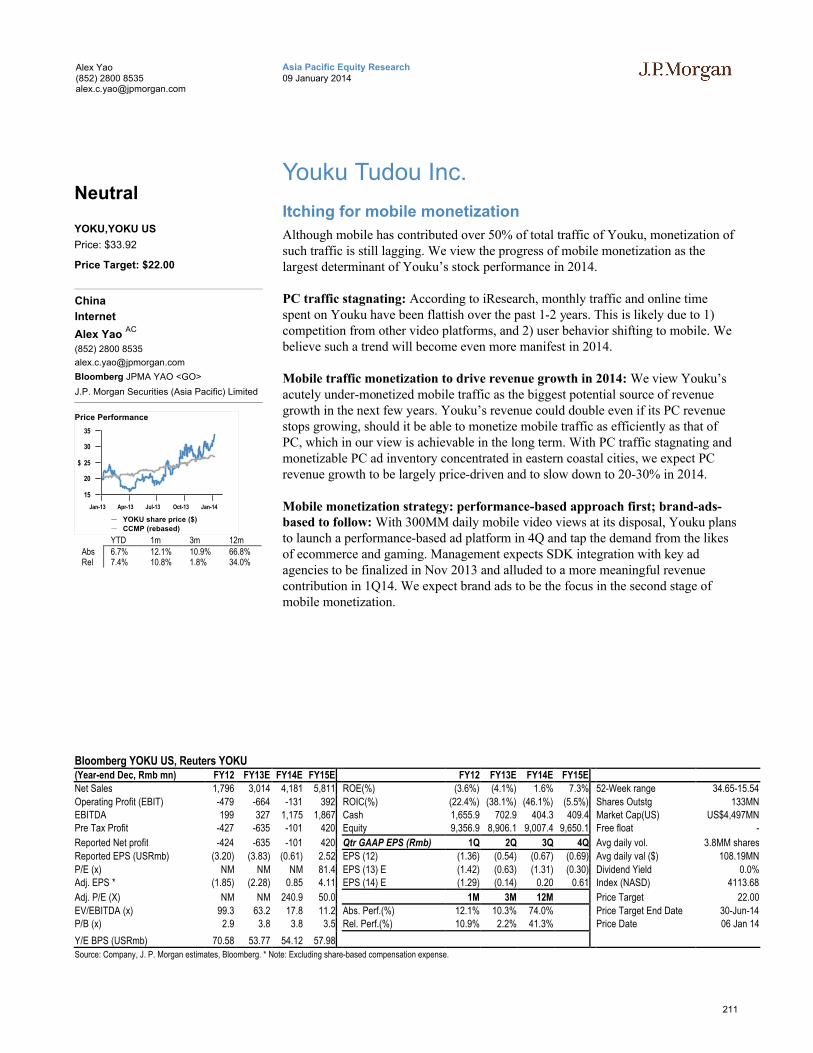

Youku Tudou Inc............................................................................ 211

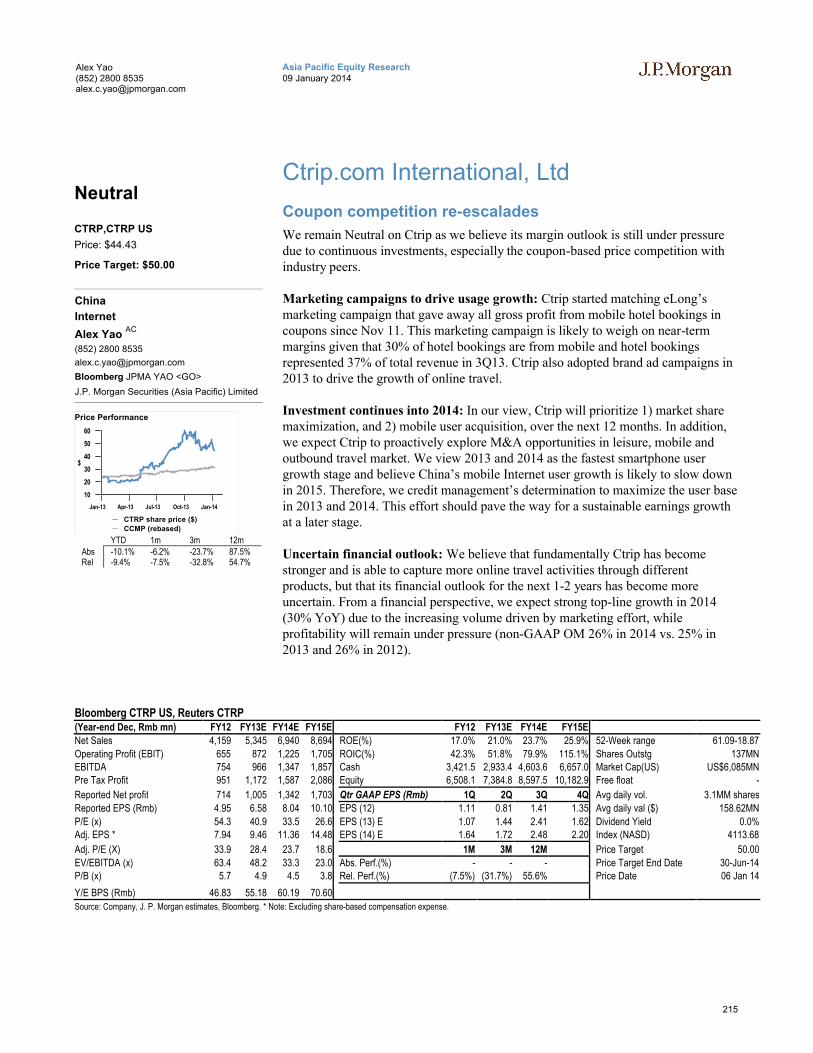

Ctrip.com International, Ltd ............................................................ 215

Sungy Mobile Limited..................................................................... 219

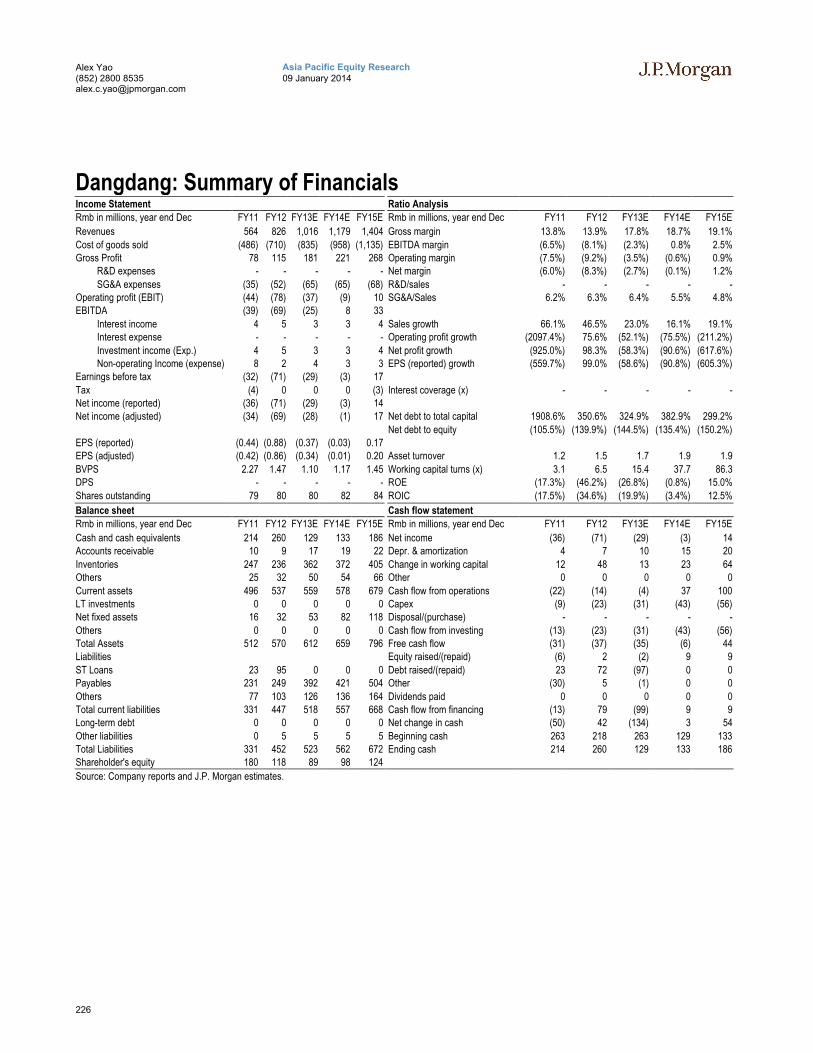

Dangdang ...................................................................................... 223

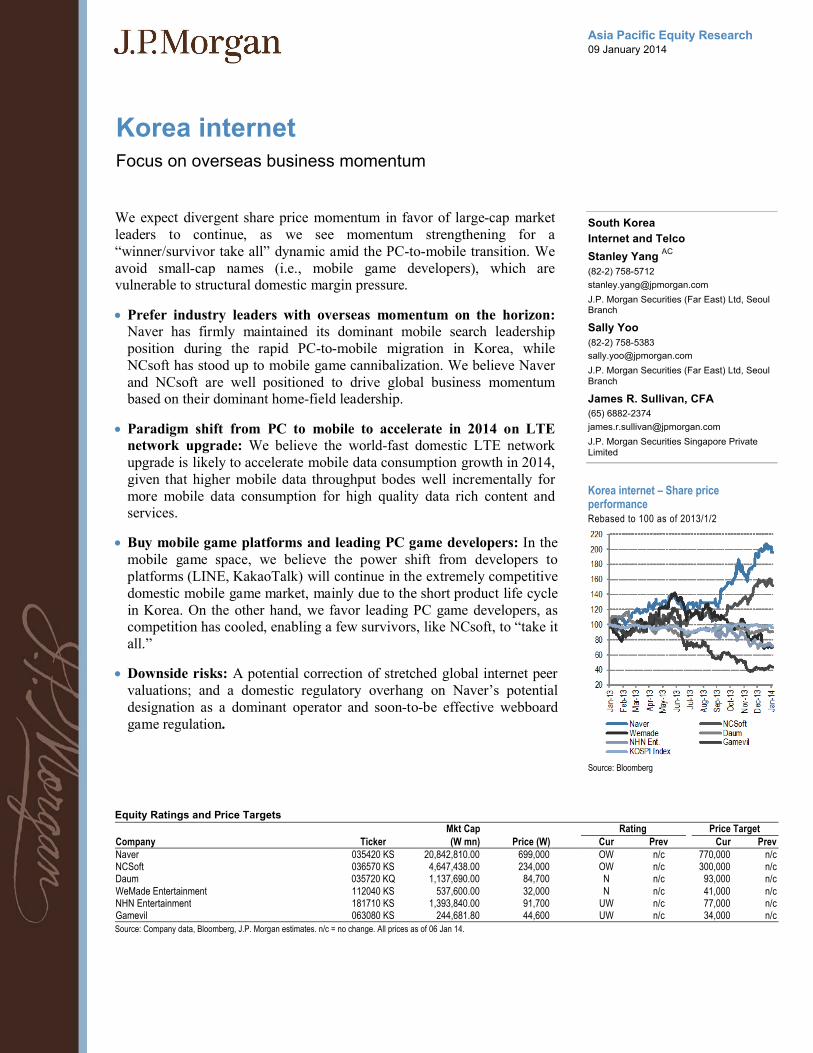

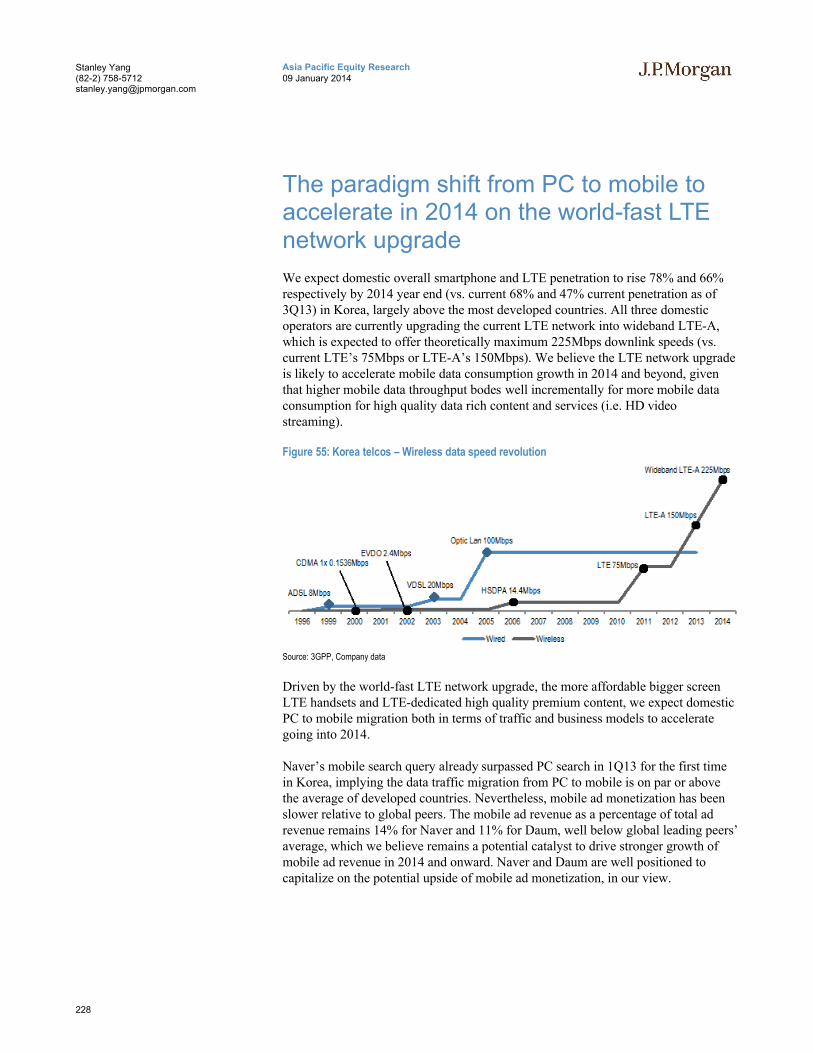

Korea Sector Outlook .................................................................. 227

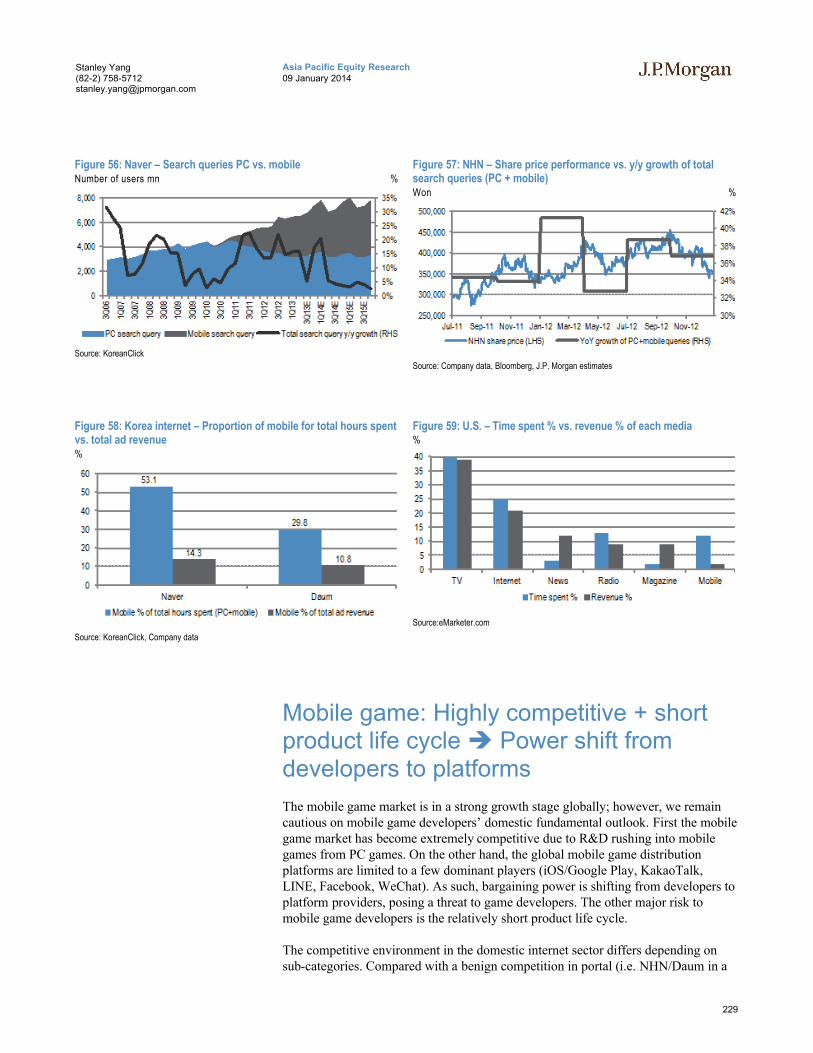

The paradigm shift from PC to mobile to accelerate in 2014 on the world-fast LTE network upgrade .................................................... 228

Mobile game: Highly competitive + short product life cycle Power shift from developers to platforms .................................................. 229

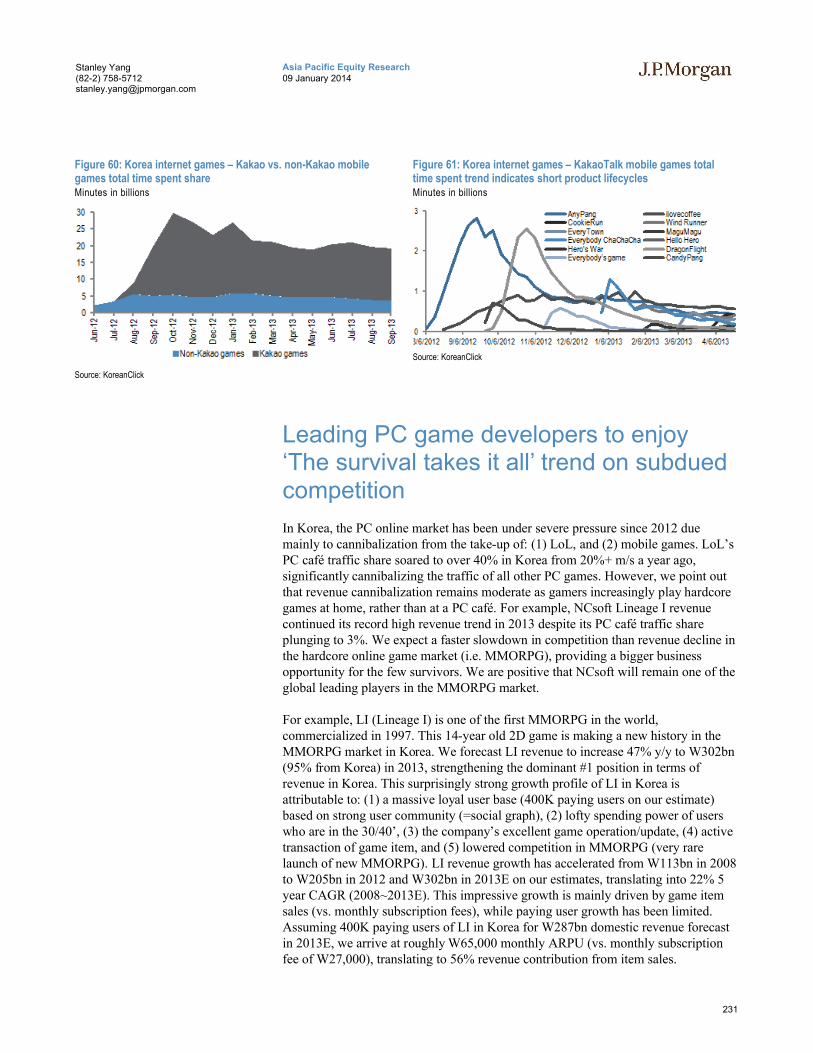

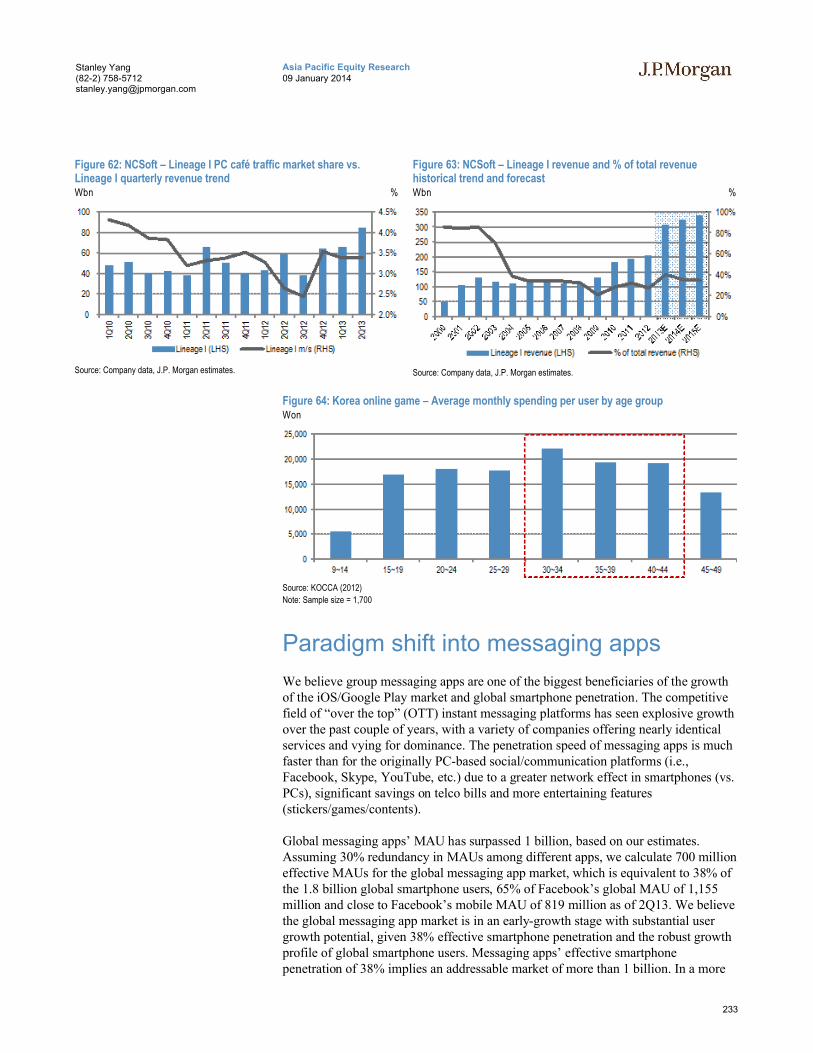

Leading PC game developers to enjoy ‘The survival takes it all’ trend on subdued competition ................................................................. 231

5

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Paradigm shift into messaging apps............................................... 233

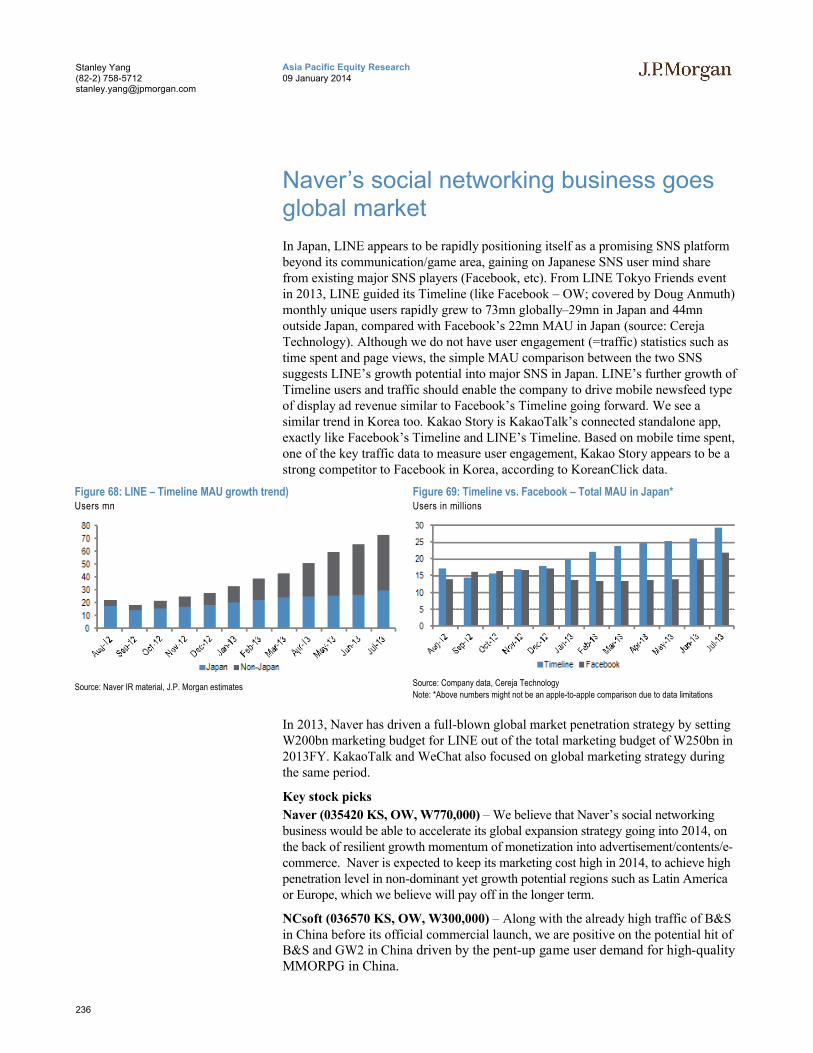

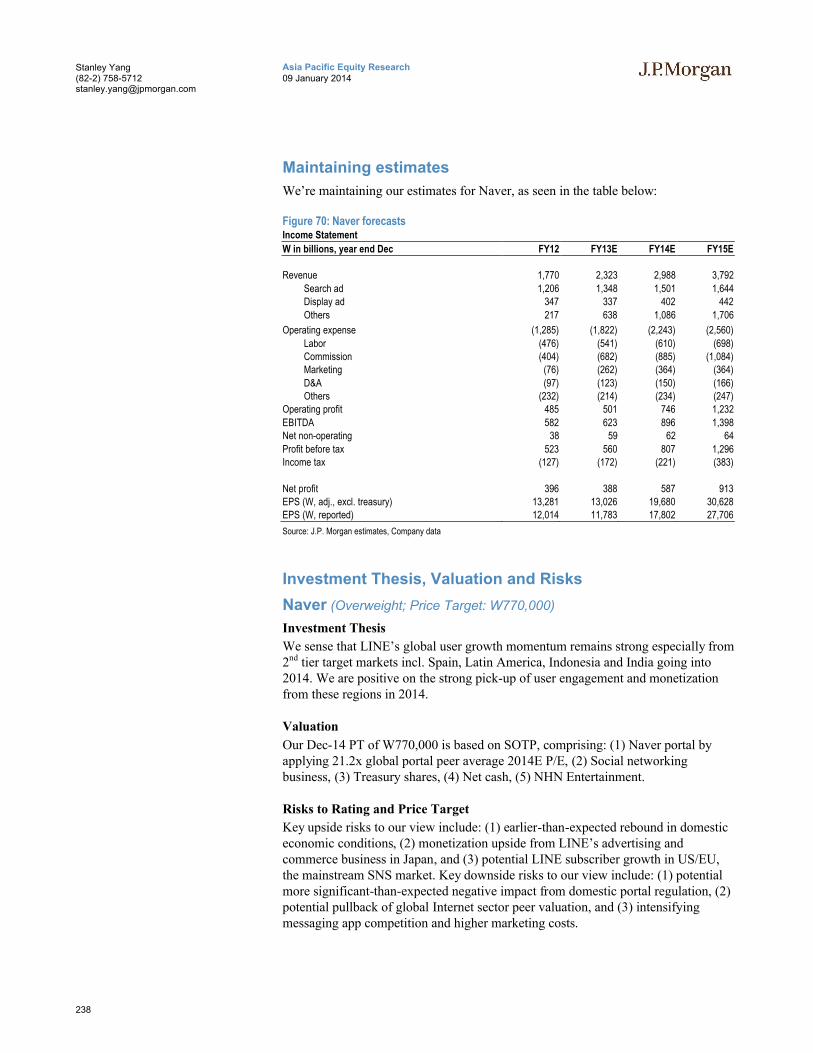

Naver’s social networking business goes global market................. 236

Korea Company Outlooks ........................................................... 237

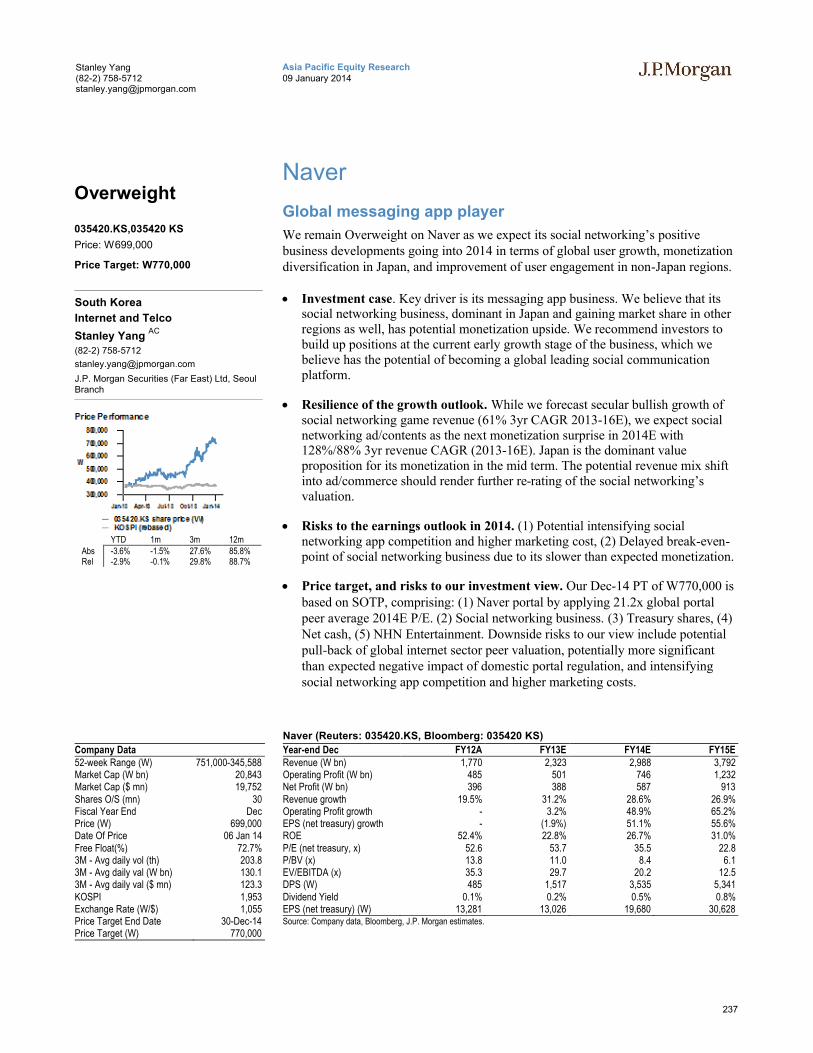

Naver ............................................................................................. 237

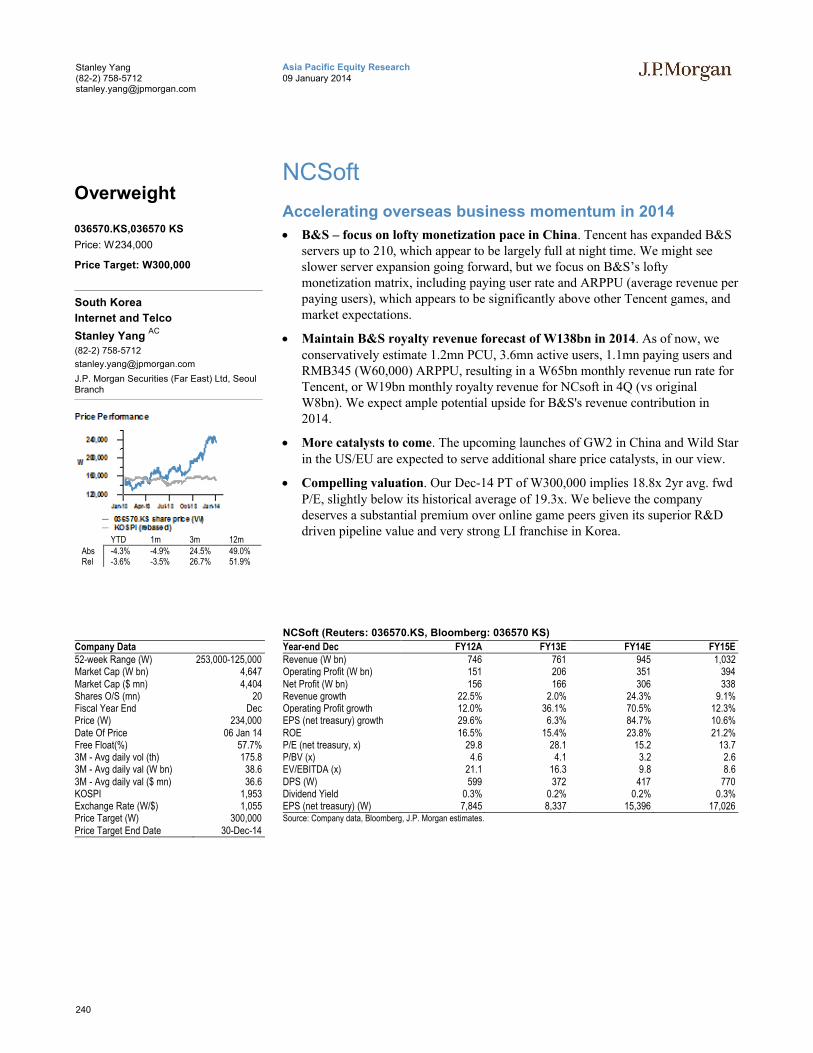

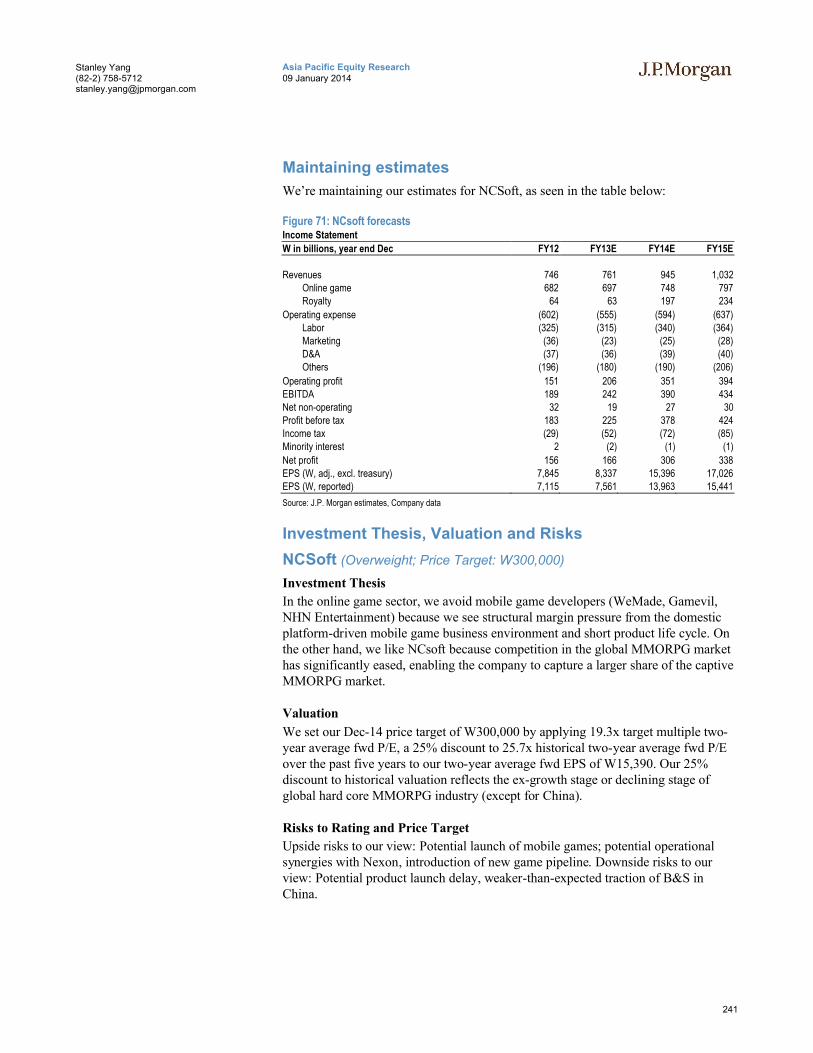

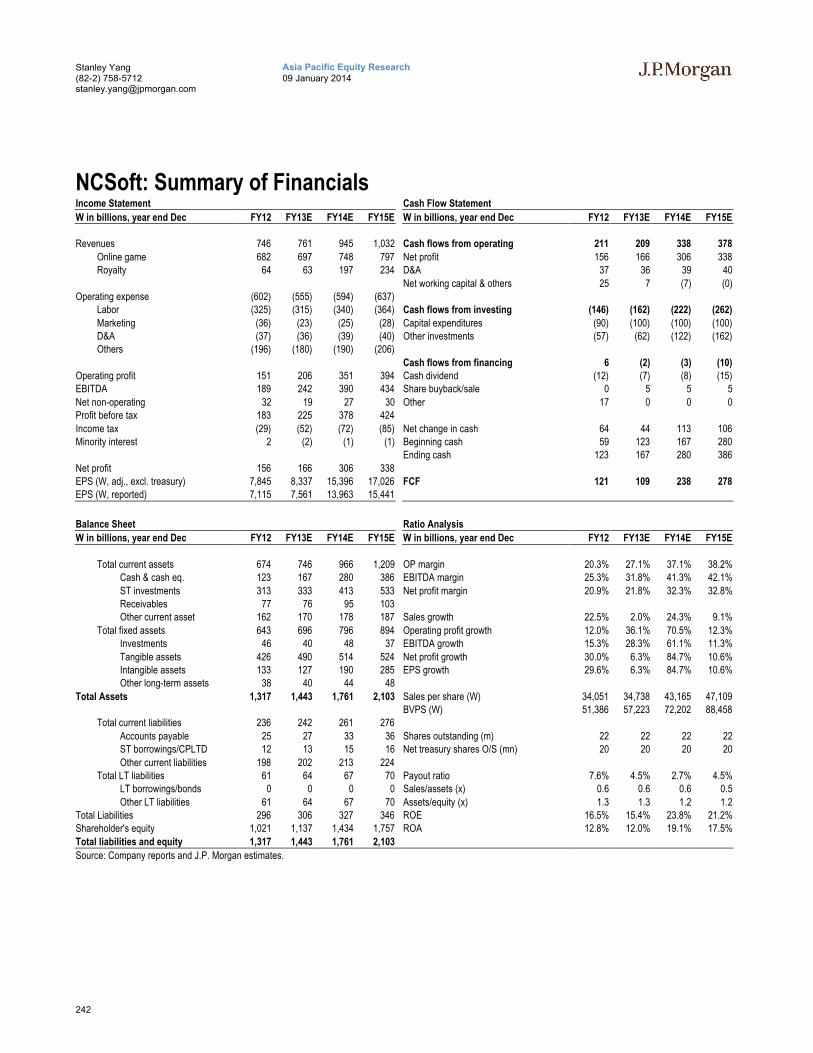

NCSoft ........................................................................................... 240

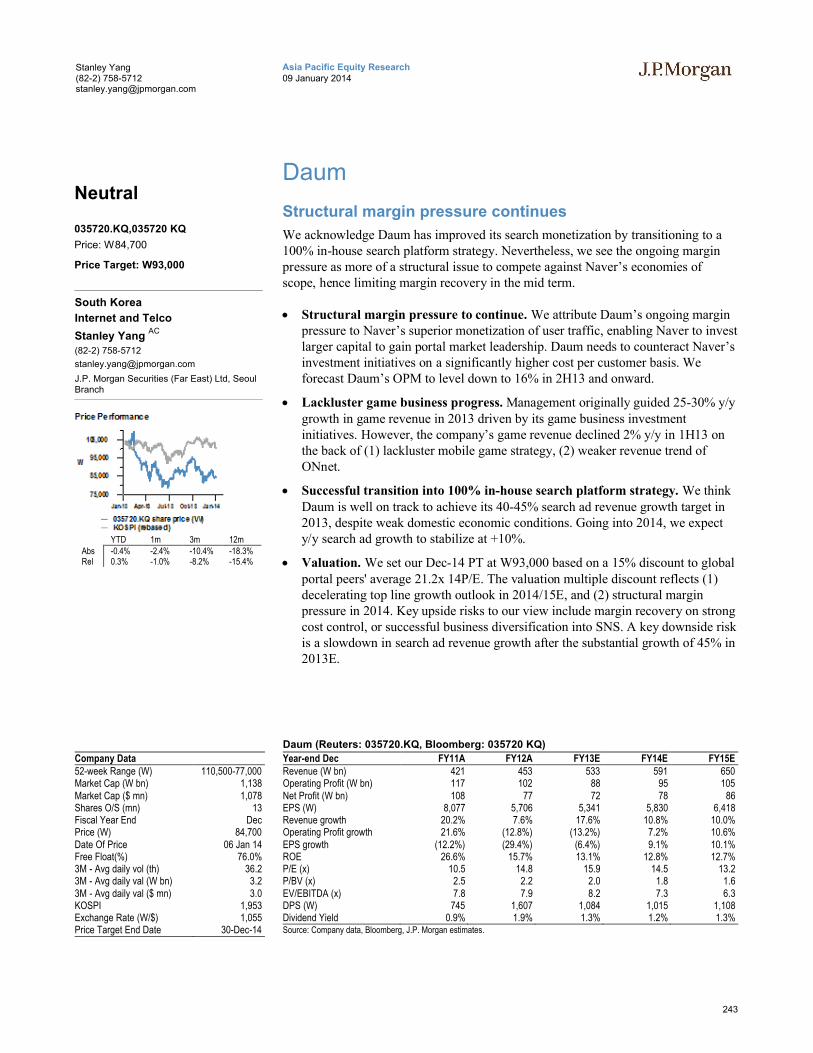

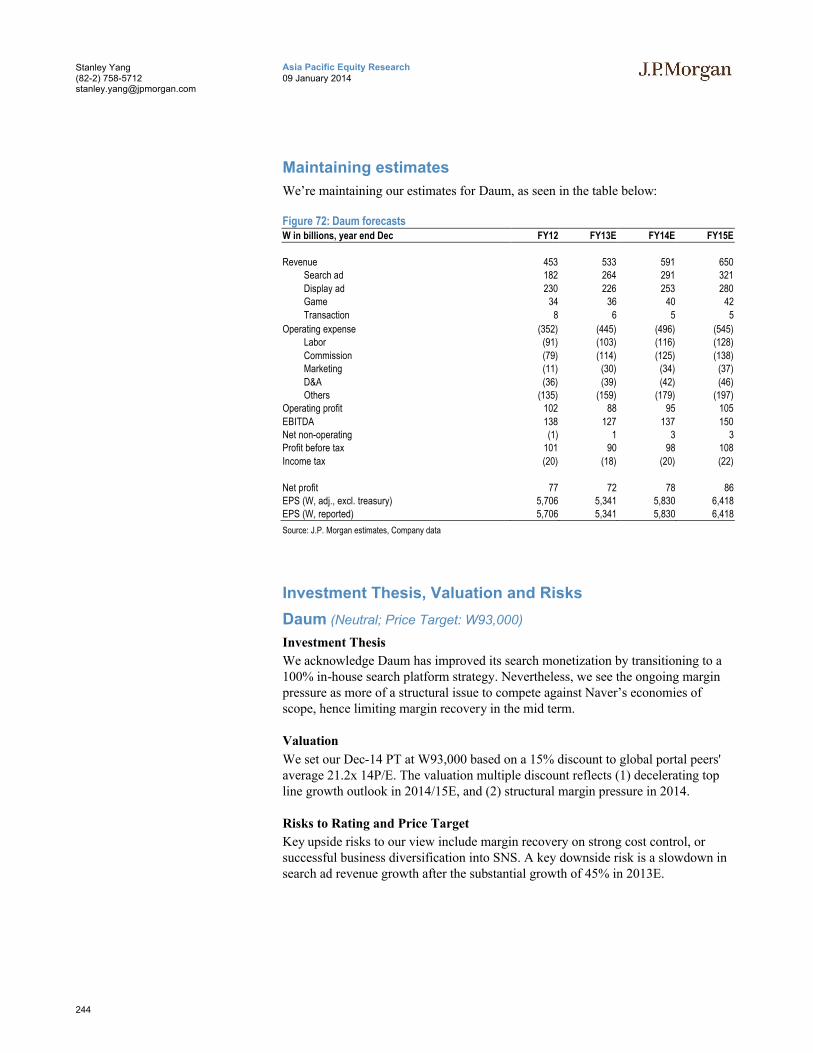

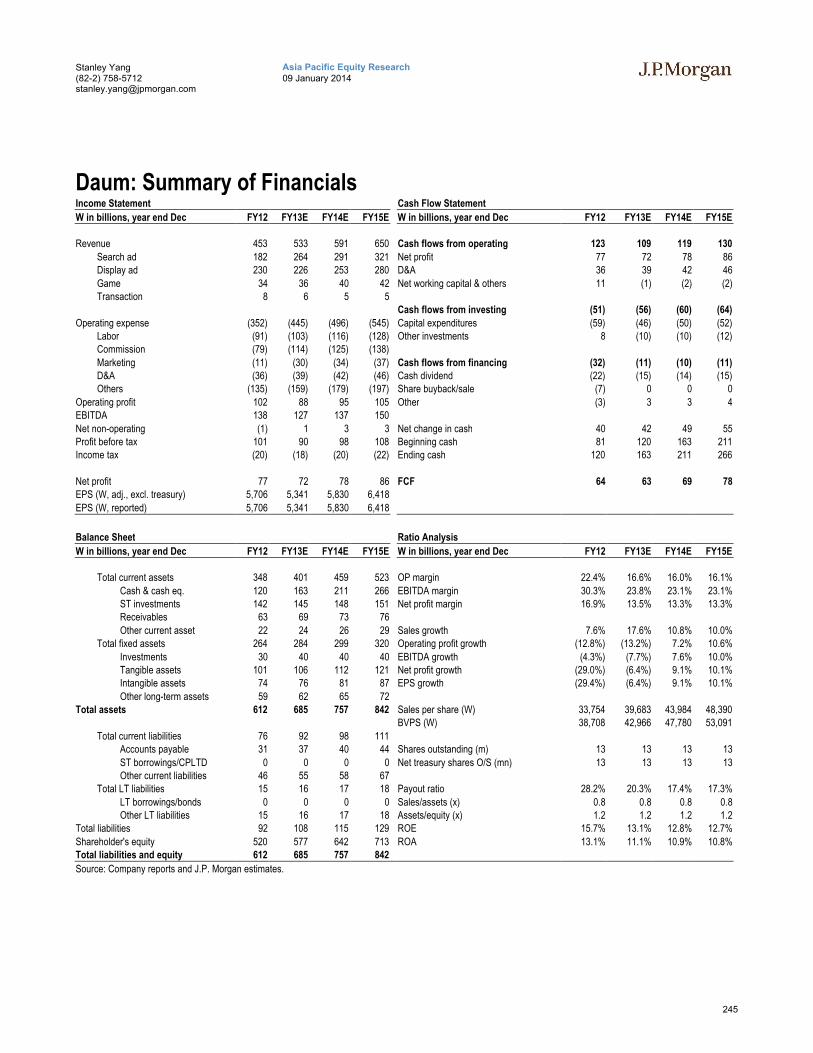

Daum............................................................................................. 243

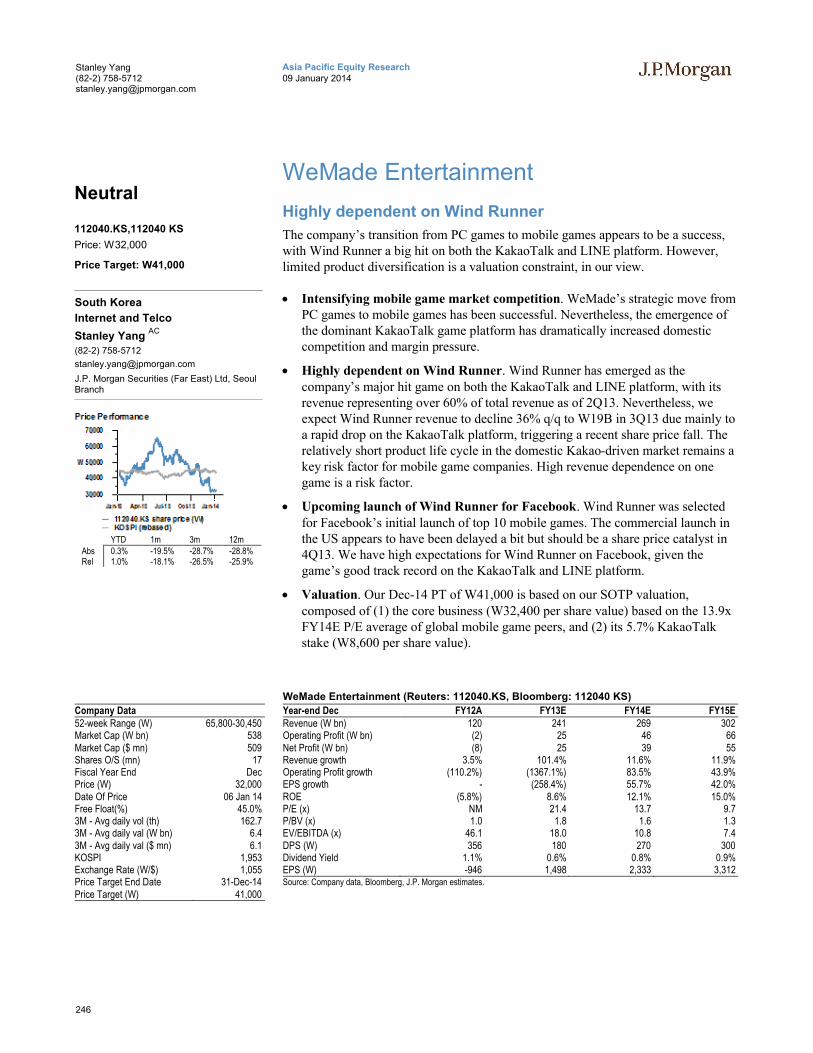

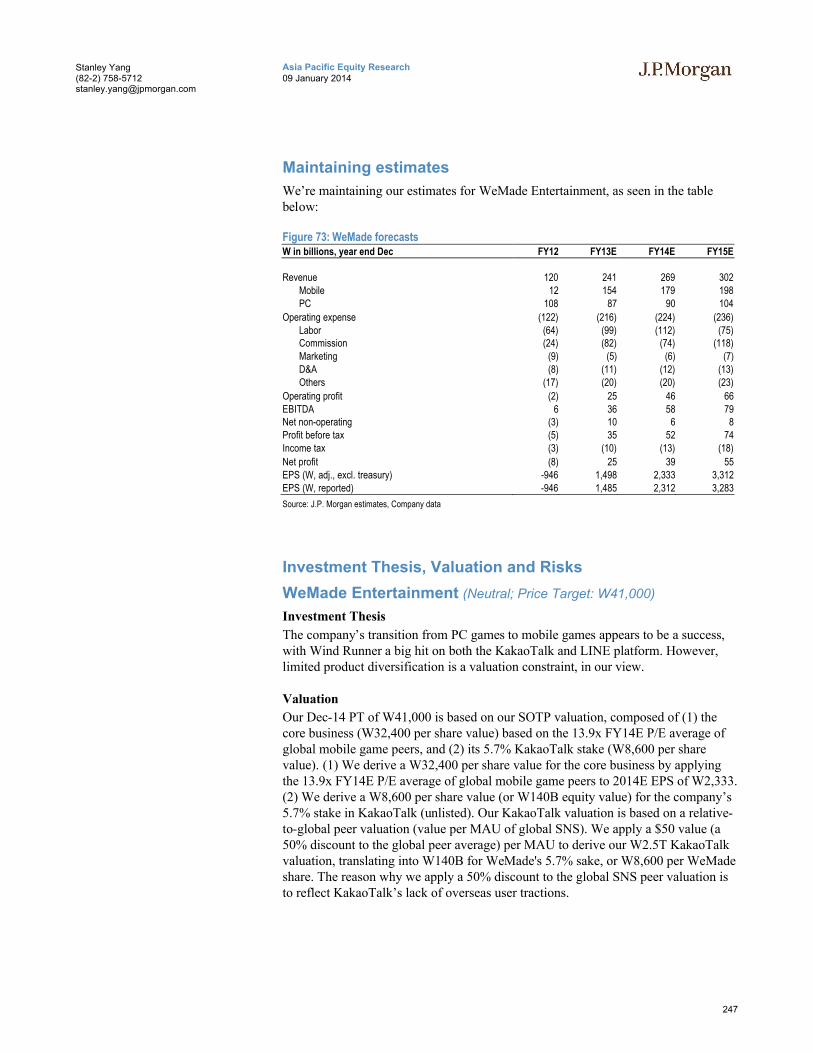

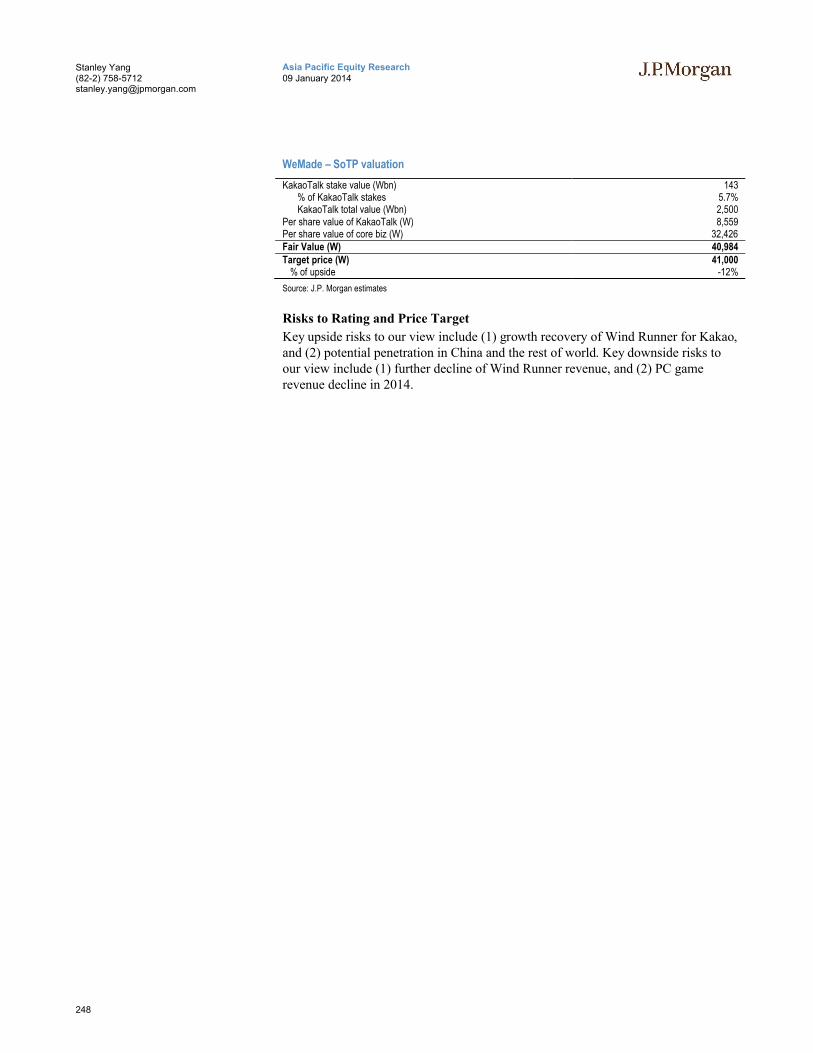

WeMade Entertainment ................................................................. 246

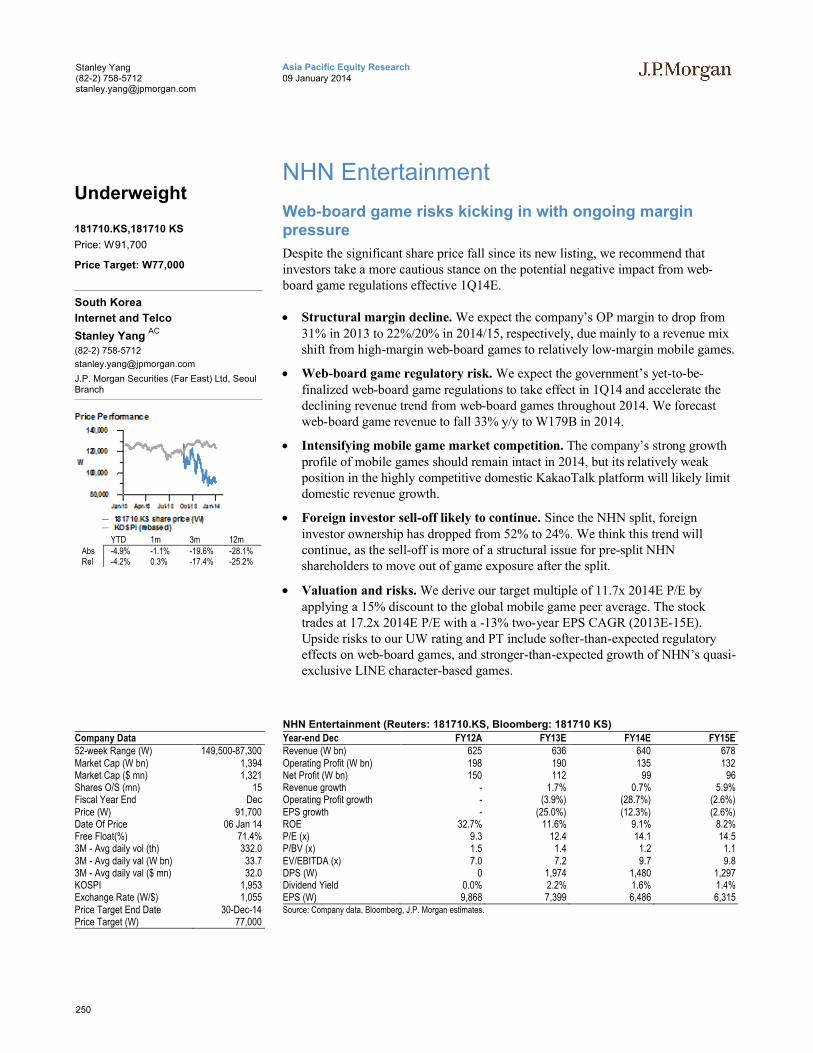

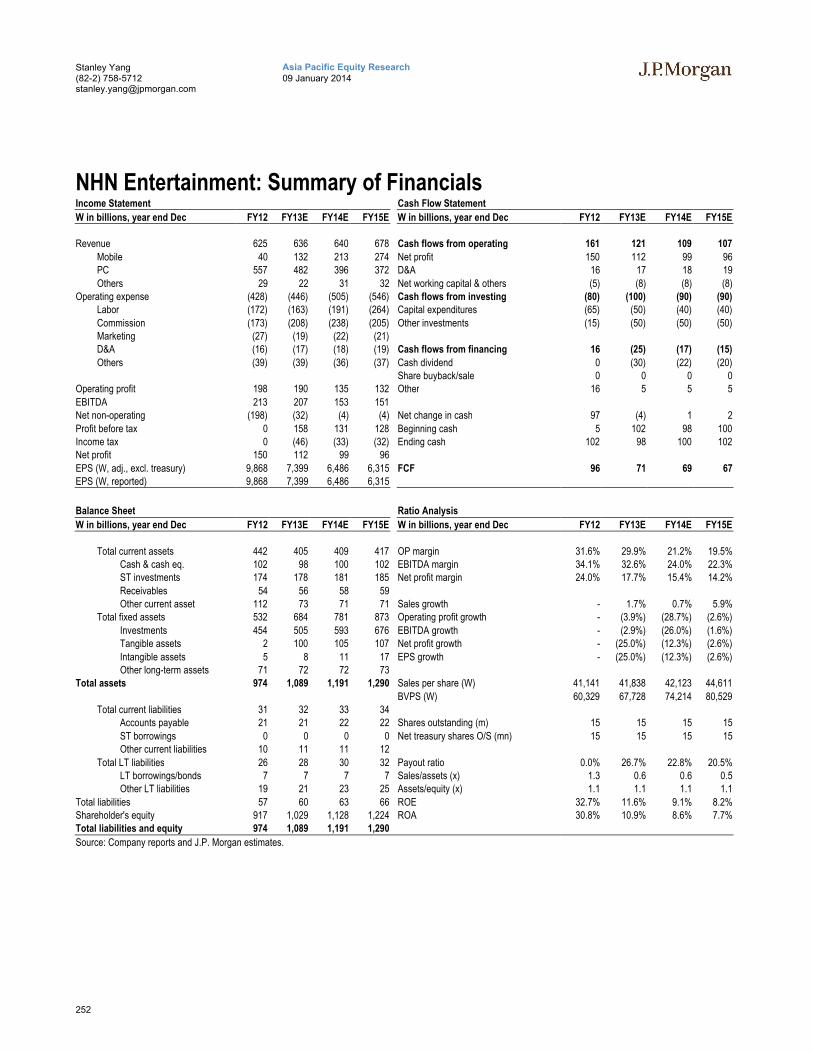

NHN Entertainment........................................................................ 250

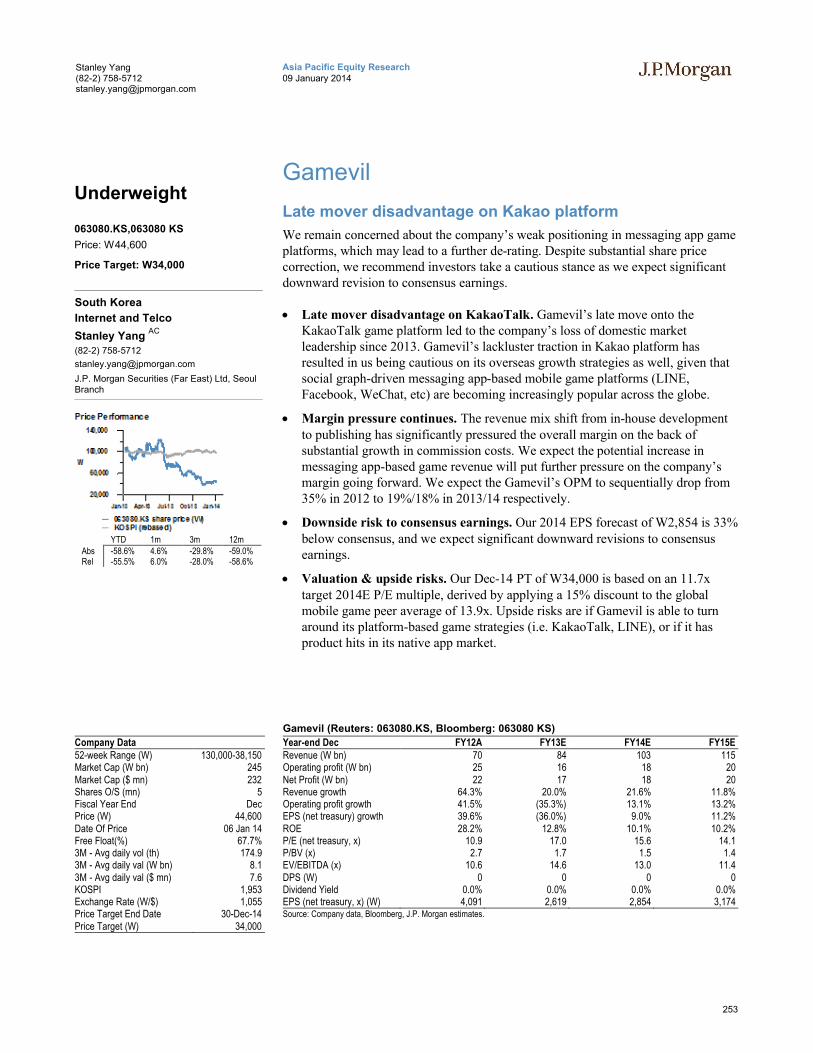

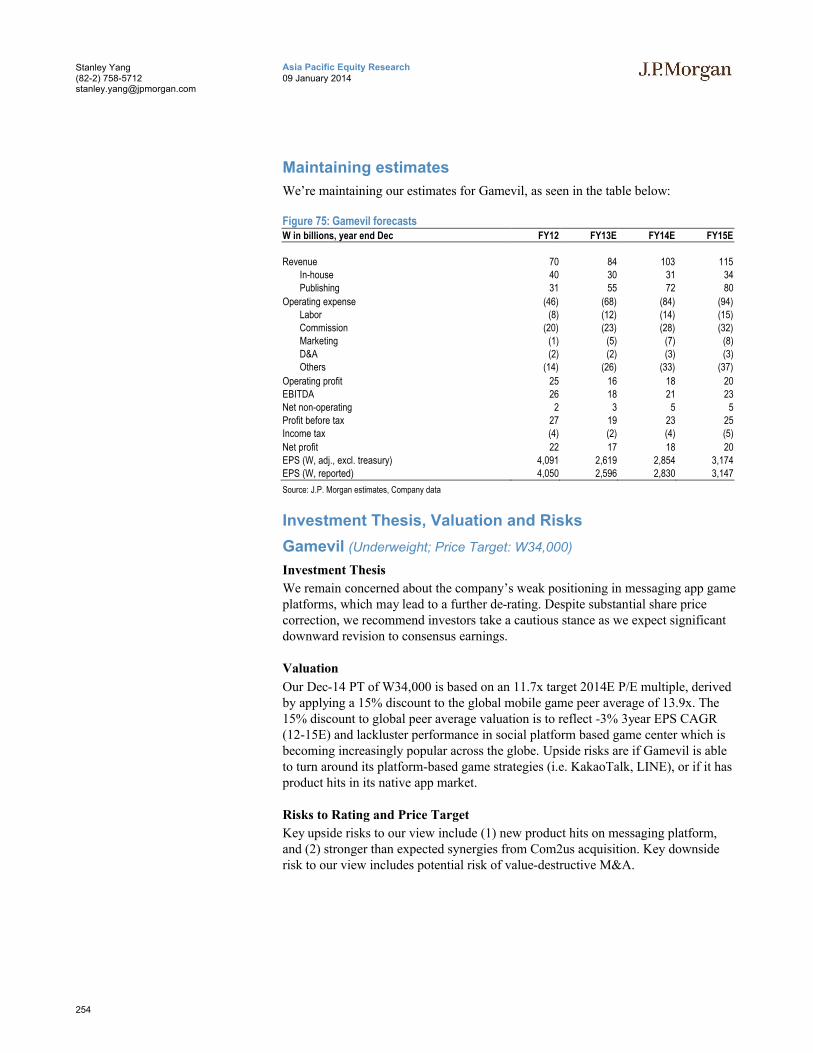

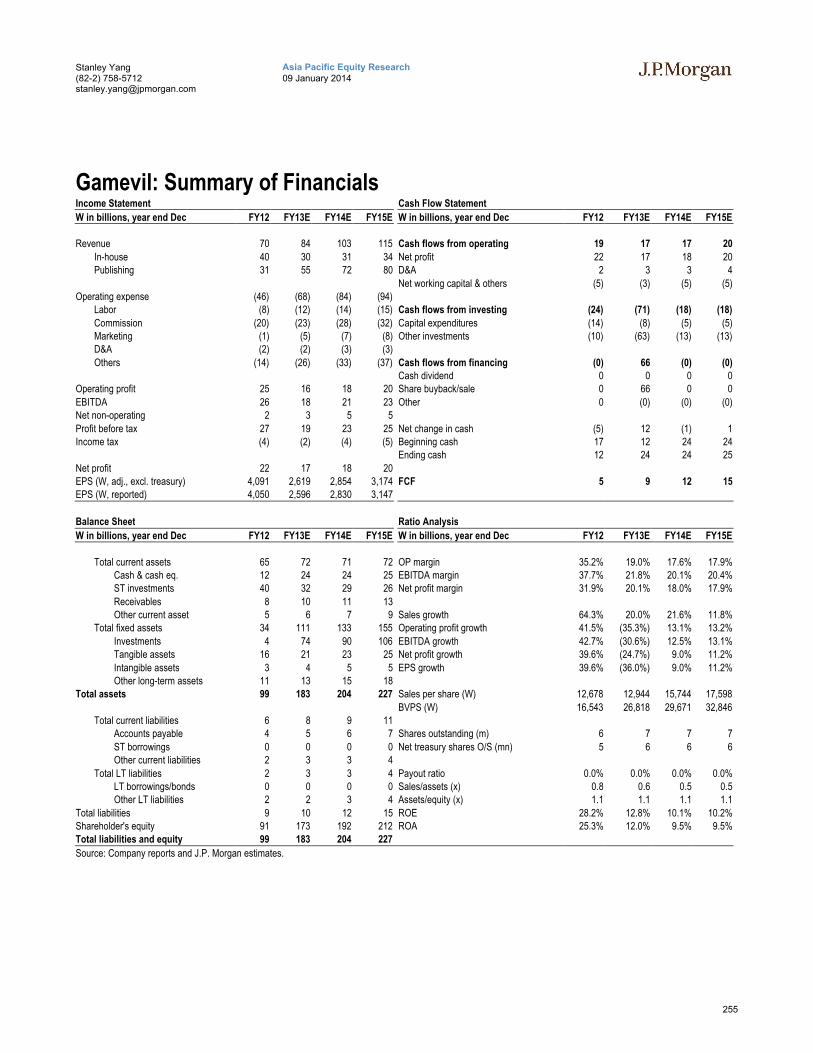

Gamevil.......................................................................................... 253

Japan Sector Outlook .................................................................. 257

Smartphones Are Changing the World........................................... 258

E-commerce: Five factors likely to accelerate shift toward e-commerce...................................................................................................... 262

Smartphone-driven growth creating good conditions for online advertising ..................................................................................... 264

Japan Company Outlooks........................................................... 266

Yahoo Japan (4689)....................................................................... 266

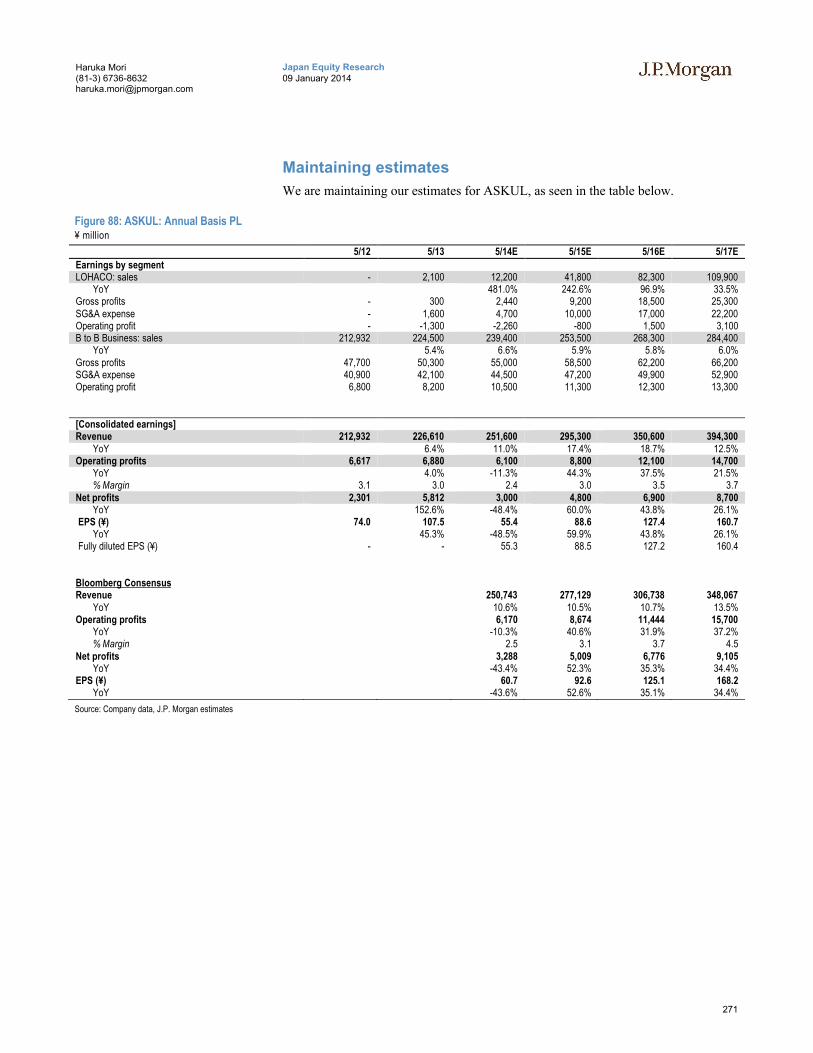

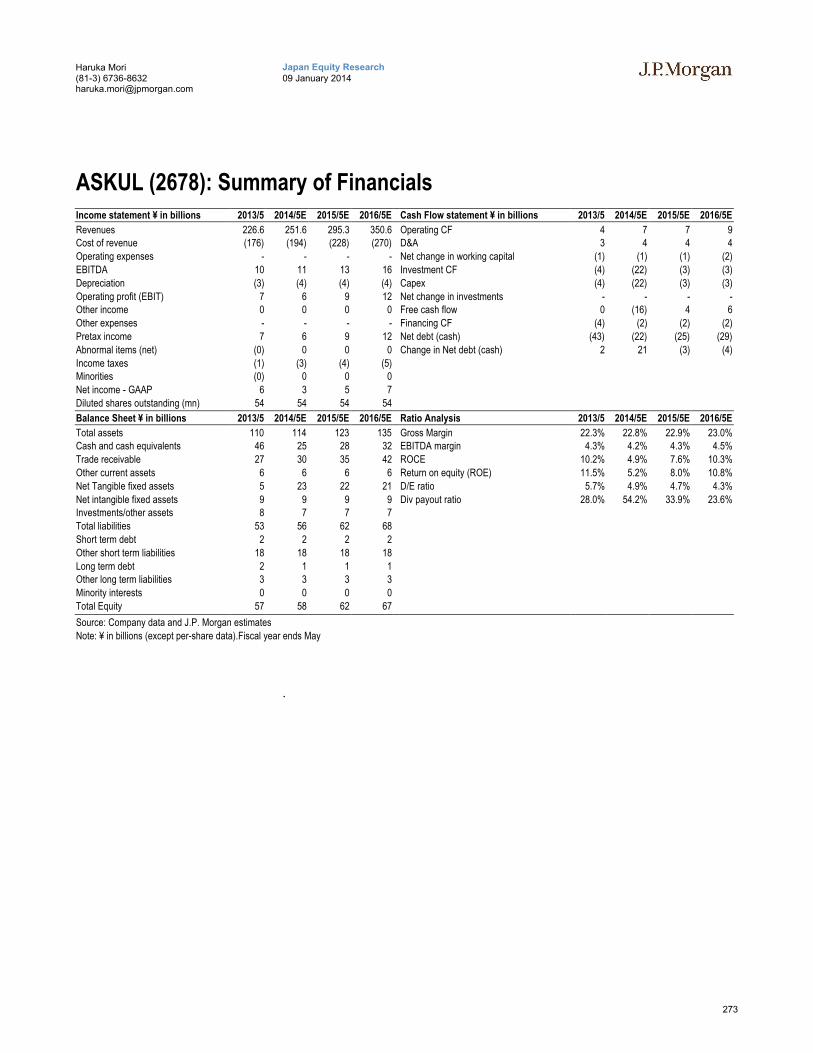

ASKUL (2678)................................................................................ 270

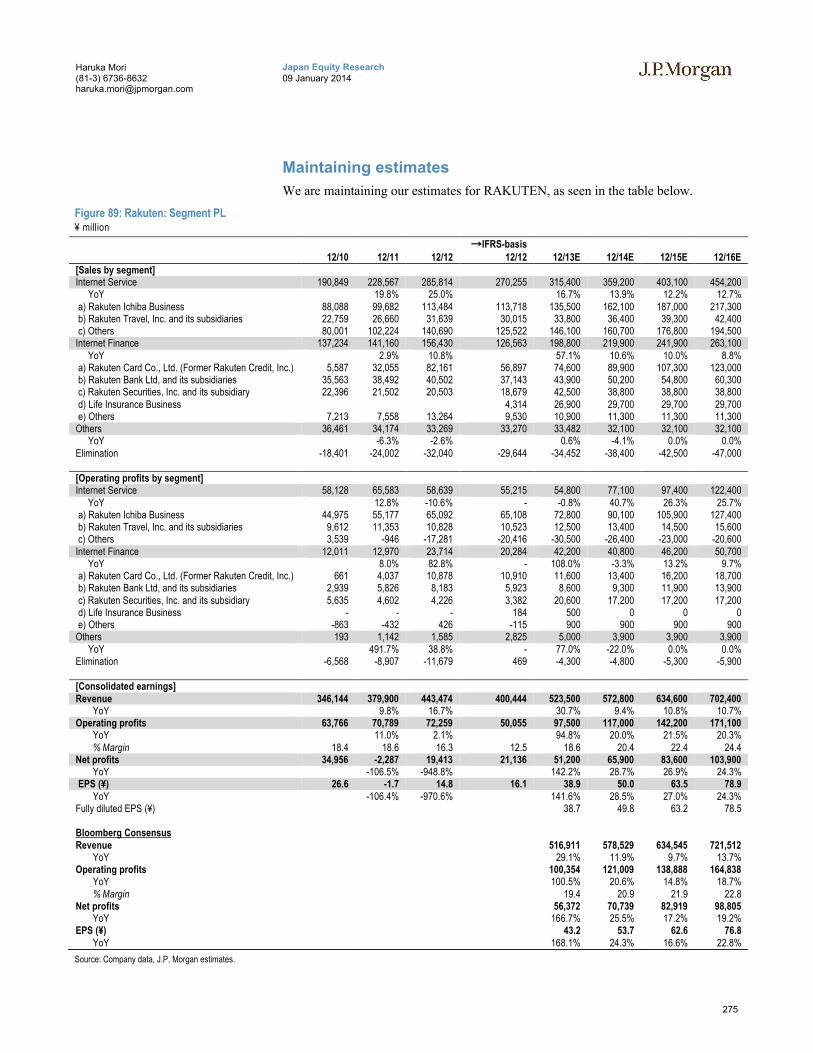

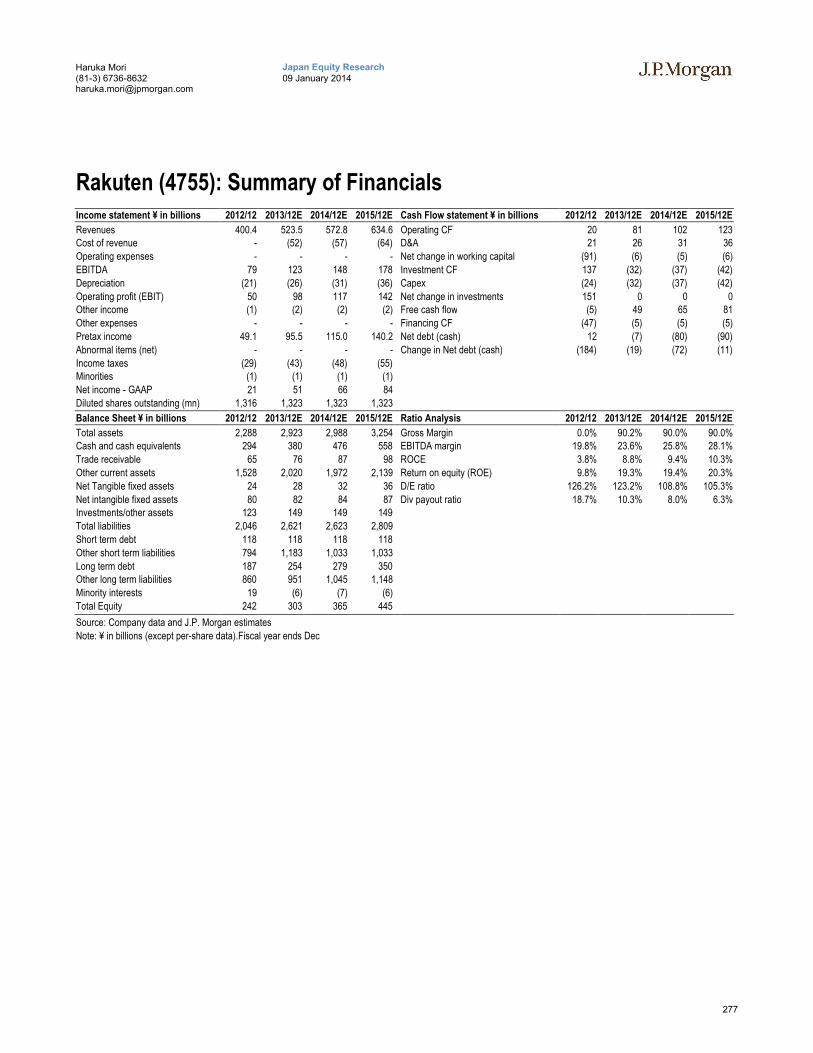

Rakuten (4755) .............................................................................. 274

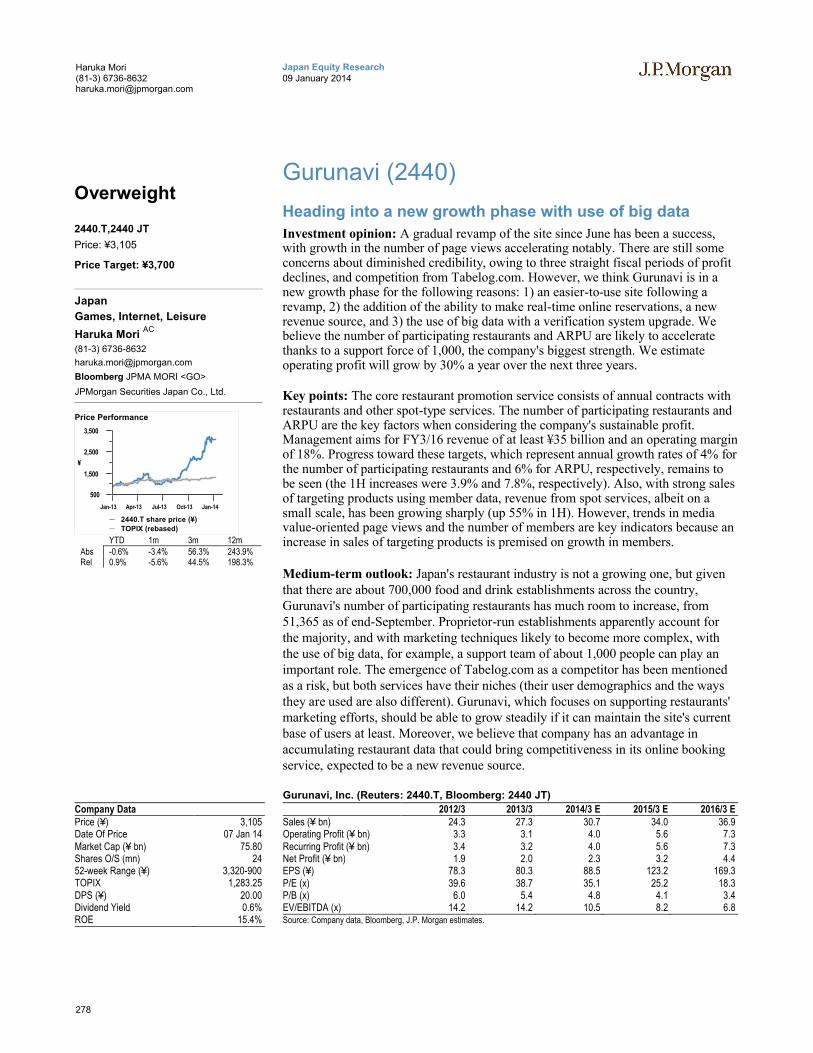

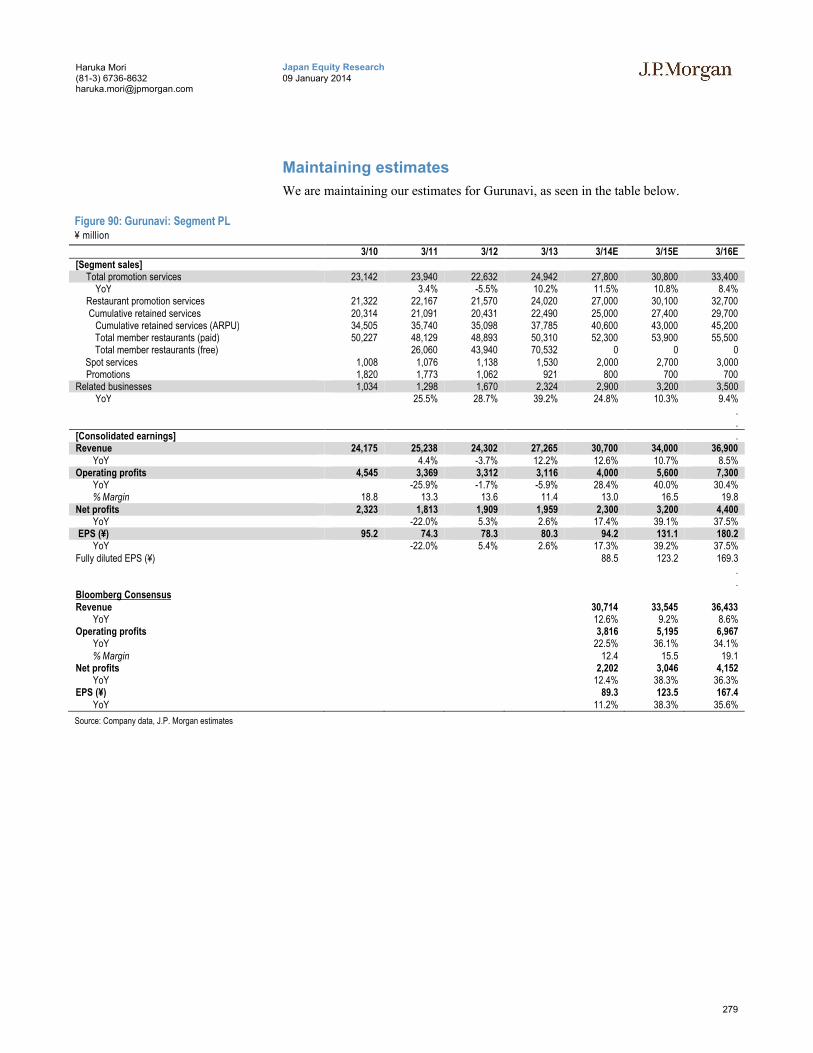

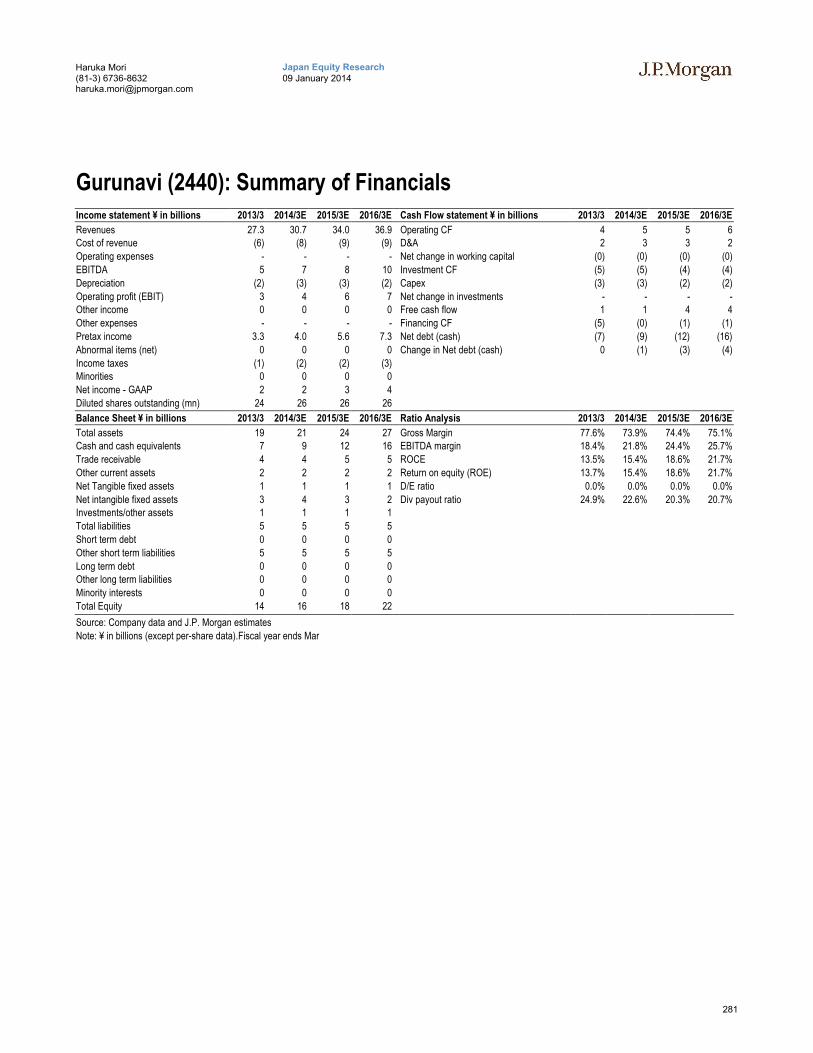

Gurunavi (2440)............................................................................. 278

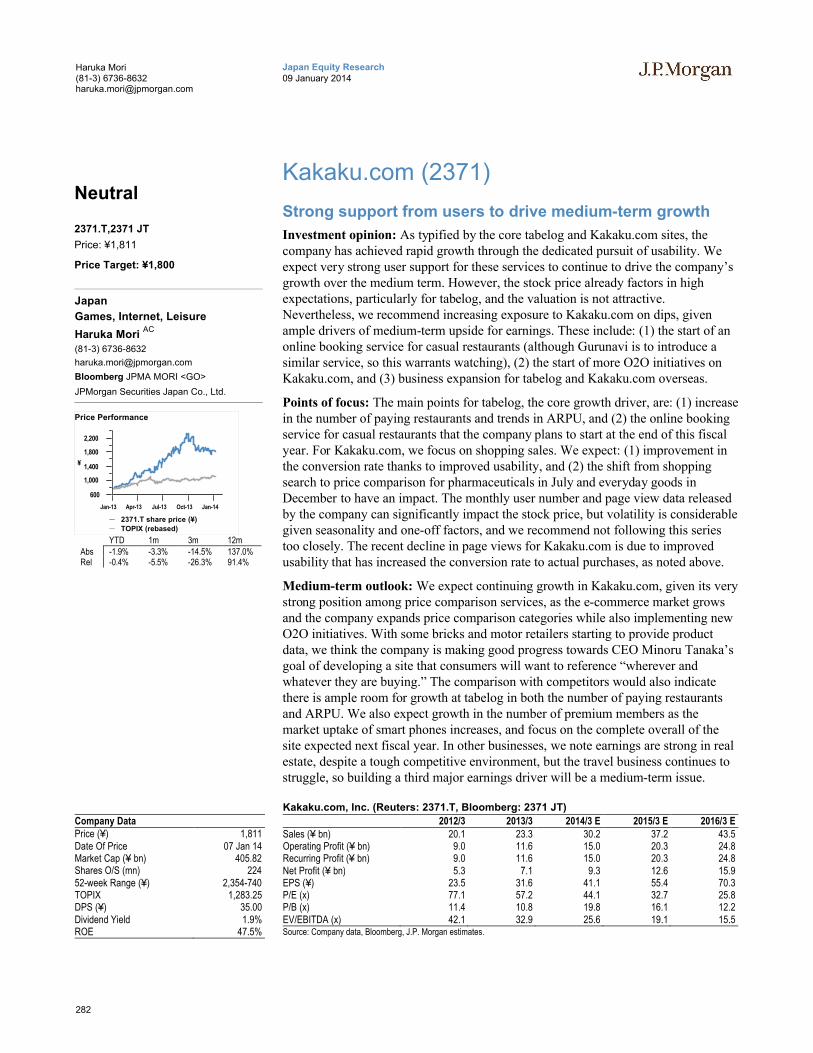

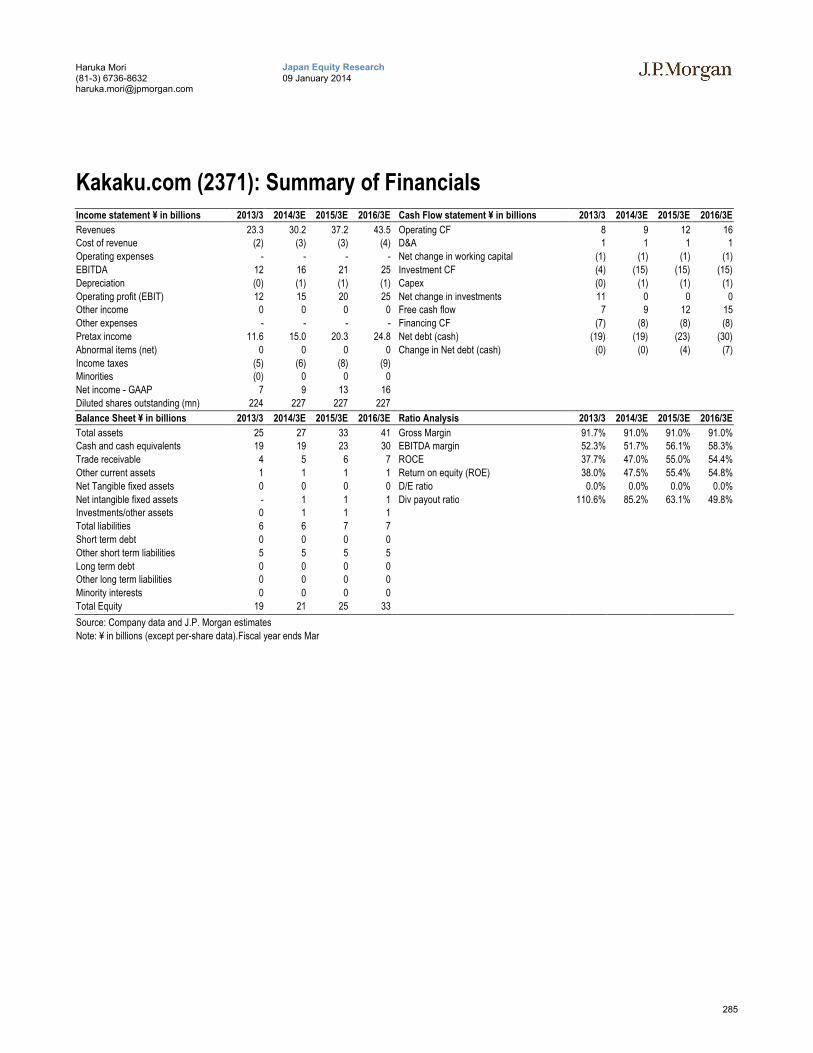

Kakaku.com (2371)........................................................................ 282

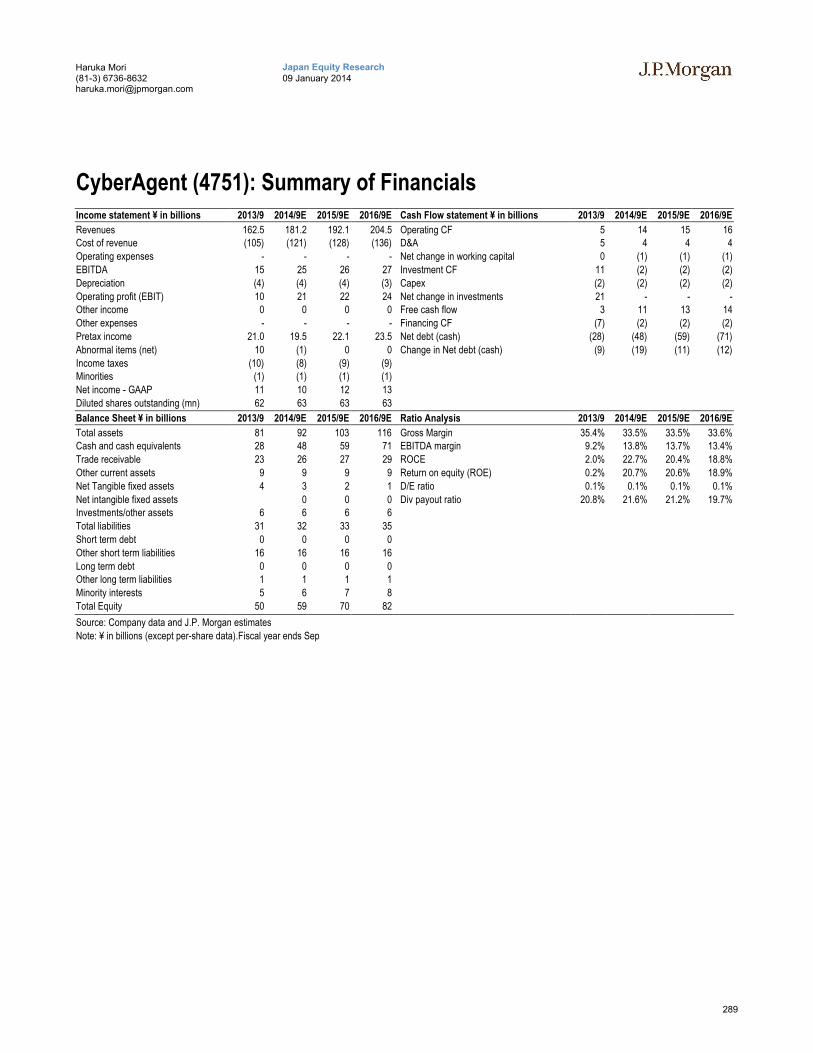

CyberAgent (4751)......................................................................... 286

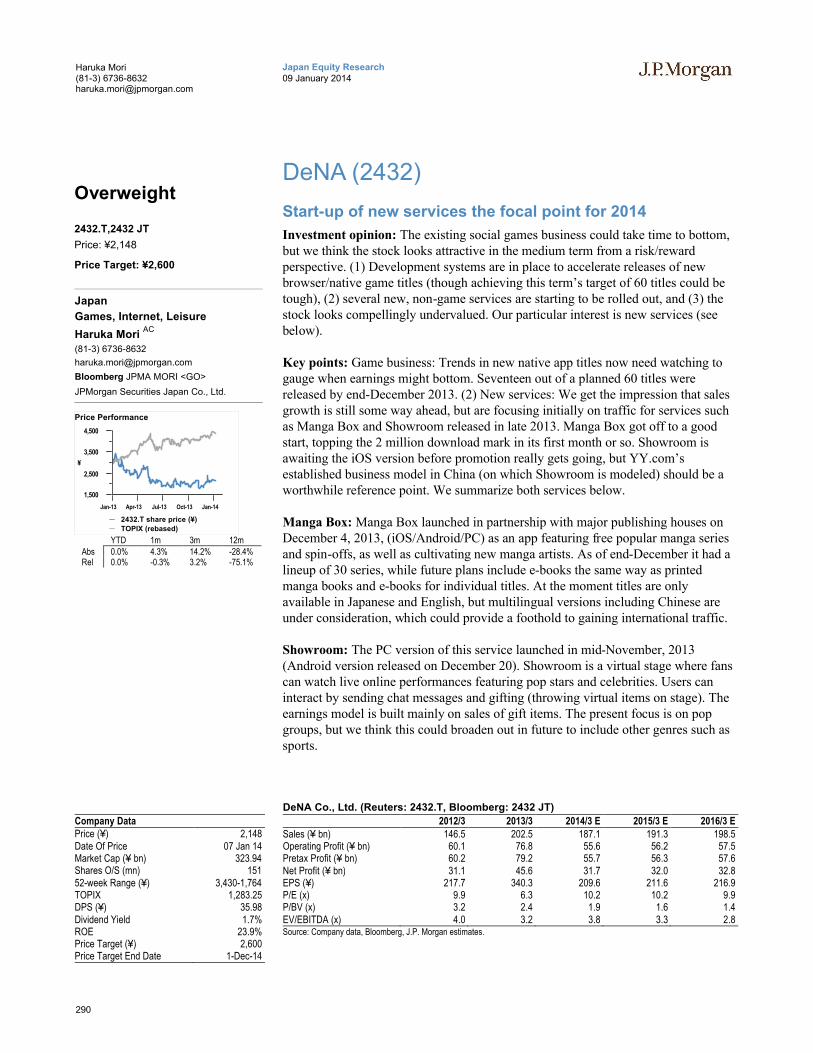

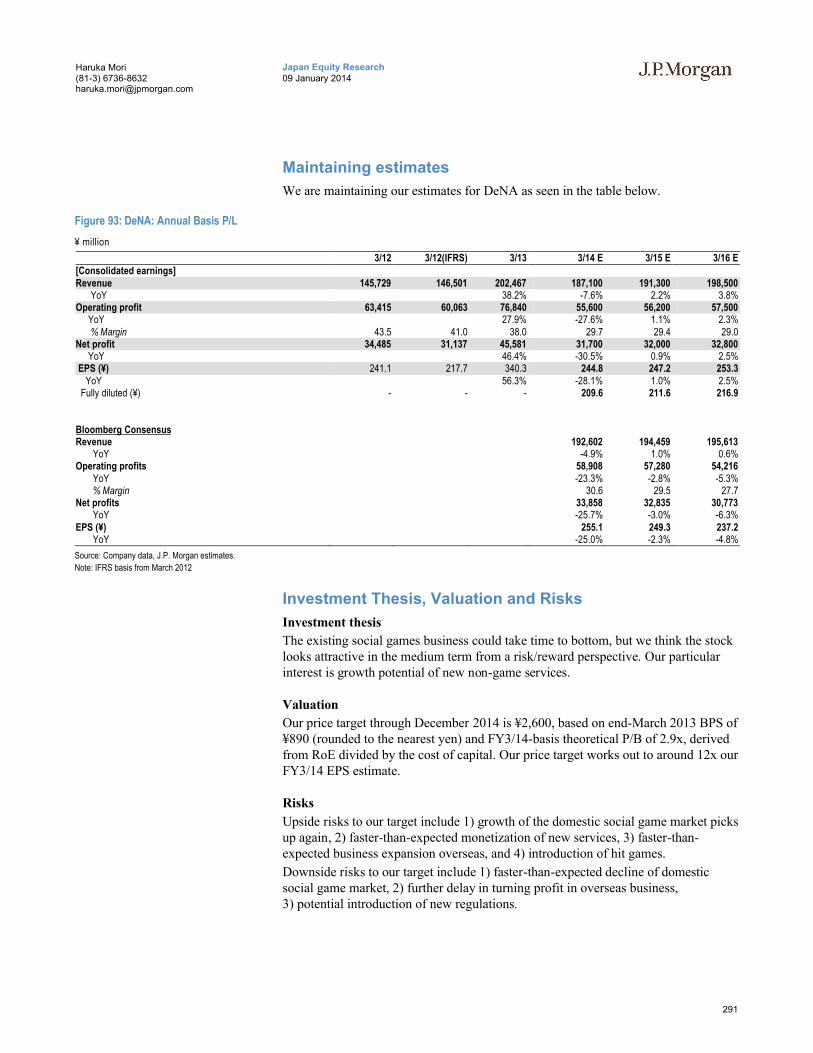

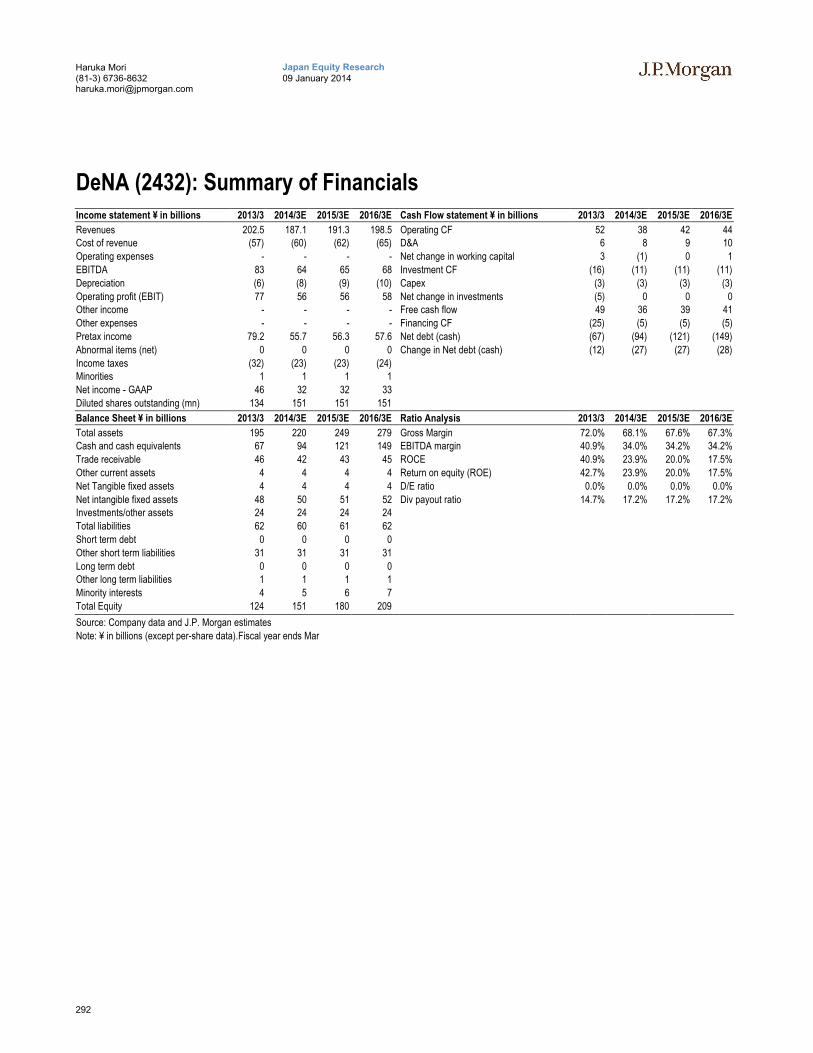

DeNA (2432).................................................................................. 290

Gree (3632) ................................................................................... 293

Europe Sector Outlook ................................................................ 296

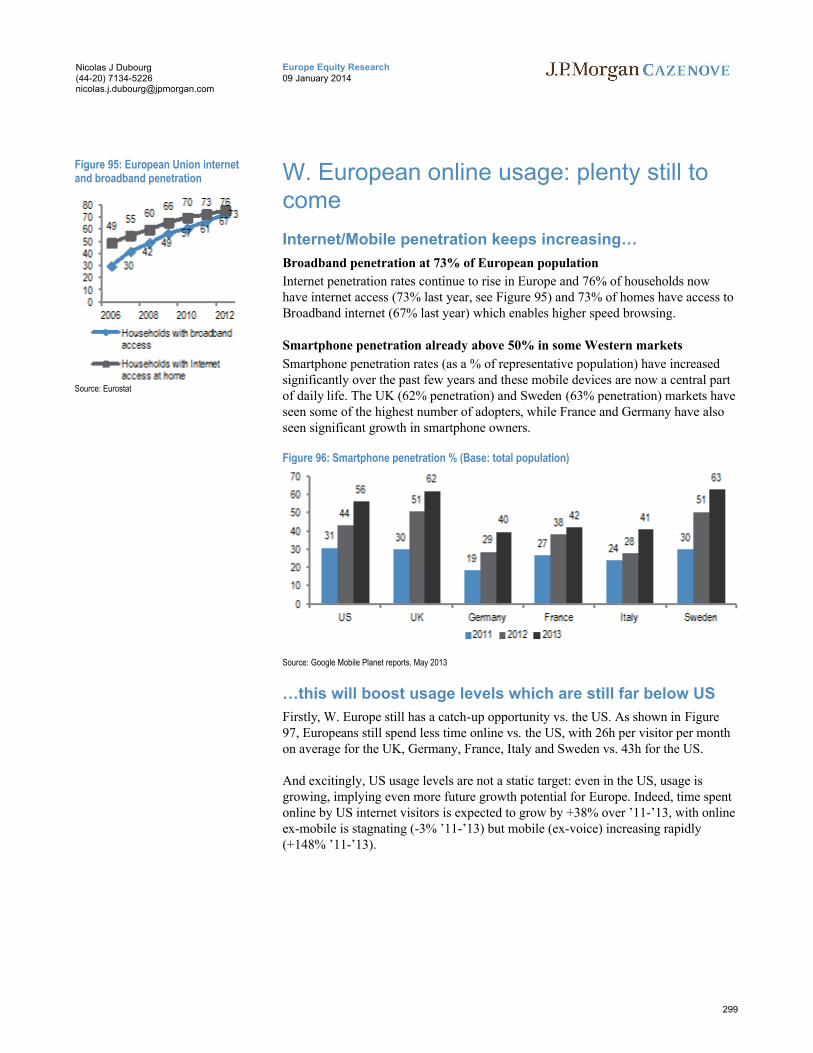

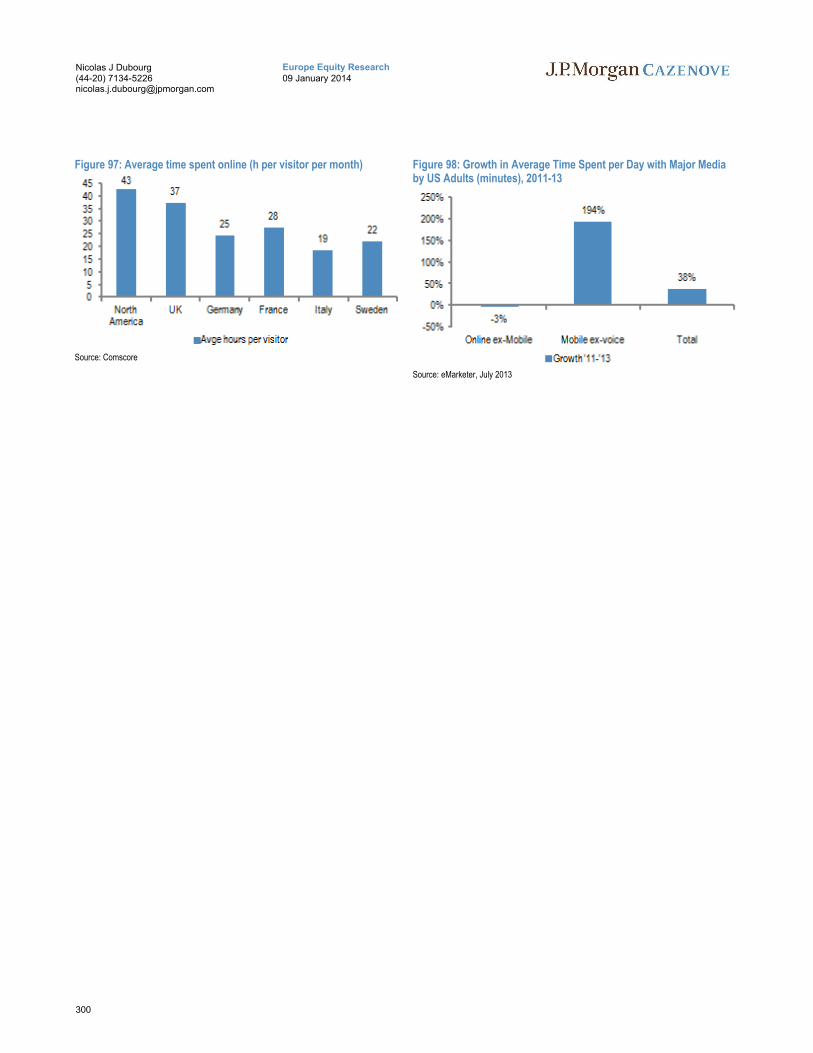

W. European online usage: plenty still to come.............................. 299

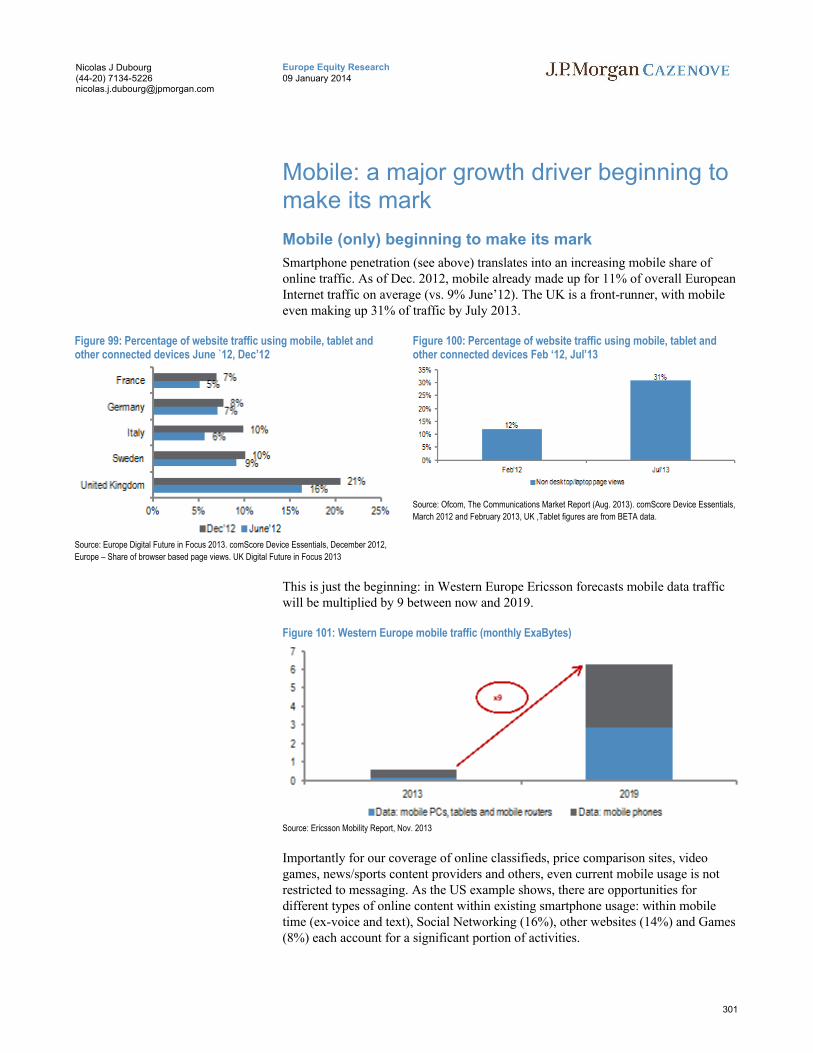

Mobile: a major growth driver beginning to make its mark.............. 301

Online Advertising: structural shift to online still gaining speed....... 305

Russia Sector Outlook................................................................. 307

Russian Internet Themes ............................................................... 308

Russia Company Outlooks.......................................................... 313

Mail.ru Group ................................................................................. 313

Yandex........................................................................................... 317

The authors acknowledge the contribution to this report of Pranav Goel of J.P. Morgan India Private Limited and Binbin Ding of J.P. Morgan Securities Asia Pacific Limited.

6

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

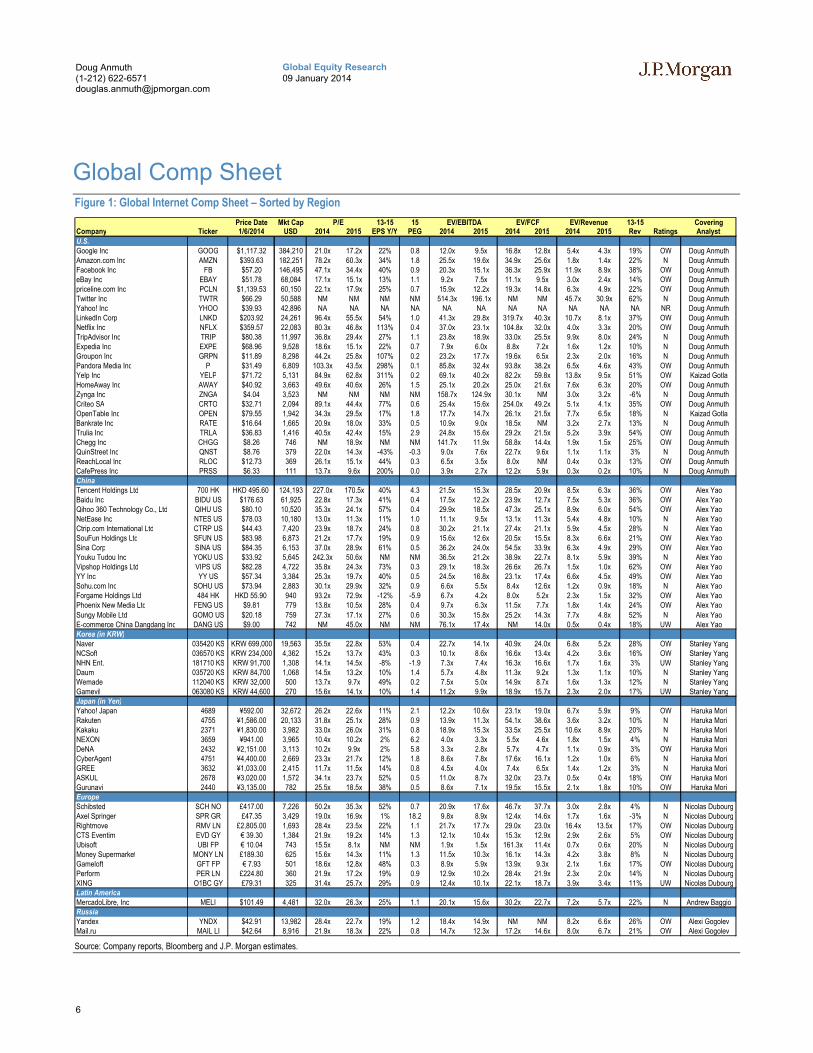

Global Comp SheetFigure 1: Global Internet Comp Sheet – Sorted by Region

Price Date Mkt Cap 13-15 15 13-15 CoveringCompany Ticker 1/6/2014 USD 2014 2015 EPS Y/Y PEG 2014 2015 2014 2015 2014 2015 Rev Ratings Analyst

U.S.Google Inc GOOG $1,117.32 384,210 21.0x 17.2x 22% 0.8 12.0x 9.5x 16.8x 12.8x 5.4x 4.3x 19% OW Doug AnmuthAmazon.com Inc AMZN $393.63 182,251 78.2x 60.3x 34% 1.8 25.5x 19.6x 34.9x 25.6x 1.8x 1.4x 22% N Doug AnmuthFacebook Inc FB $57.20 146,495 47.1x 34.4x 40% 0.9 20.3x 15.1x 36.3x 25.9x 11.9x 8.9x 38% OW Doug AnmutheBay Inc EBAY $51.78 68,084 17.1x 15.1x 13% 1.1 9.2x 7.5x 11.1x 9.5x 3.0x 2.4x 14% OW Doug Anmuthpriceline.com Inc PCLN $1,139.53 60,150 22.1x 17.9x 25% 0.7 15.9x 12.2x 19.3x 14.8x 6.3x 4.9x 22% OW Doug AnmuthTwitter Inc TWTR $66.29 50,588 NM NM NM NM 514.3x 196.1x NM NM 45.7x 30.9x 62% N Doug AnmuthYahoo! Inc YHOO $39.93 42,896 NA NA NA NA NA NA NA NA NA NA NA NR Doug AnmuthLinkedIn Corp LNKD $203.92 24,261 96.4x 55.5x 54% 1.0 41.3x 29.8x 319.7x 40.3x 10.7x 8.1x 37% OW Doug AnmuthNetflix Inc NFLX $359.57 22,083 80.3x 46.8x 113% 0.4 37.0x 23.1x 104.8x 32.0x 4.0x 3.3x 20% OW Doug AnmuthTripAdvisor Inc TRIP $80.38 11,997 36.8x 29.4x 27% 1.1 23.8x 18.9x 33.0x 25.5x 9.9x 8.0x 24% N Doug AnmuthExpedia Inc EXPE $68.96 9,528 18.6x 15.1x 22% 0.7 7.9x 6.0x 8.8x 7.2x 1.6x 1.2x 10% N Doug AnmuthGroupon Inc GRPN $11.89 8,298 44.2x 25.8x 107% 0.2 23.2x 17.7x 19.6x 6.5x 2.3x 2.0x 16% N Doug AnmuthPandora Media Inc P $31.49 6,809 103.3x 43.5x 298% 0.1 85.8x 32.4x 93.8x 38.2x 6.5x 4.6x 43% OW Doug AnmuthYelp Inc YELP $71.72 5,131 84.9x 62.8x 311% 0.2 69.1x 40.2x 82.2x 59.8x 13.8x 9.5x 51% OW Kaizad GotlaHomeAway Inc AWAY $40.92 3,663 49.6x 40.6x 26% 1.5 25.1x 20.2x 25.0x 21.6x 7.6x 6.3x 20% OW Doug AnmuthZynga Inc ZNGA $4.04 3,523 NM NM NM NM 158.7x 124.9x 30.1x NM 3.0x 3.2x -6% N Doug AnmuthCriteo SA CRTO $32.71 2,094 89.1x 44.4x 77% 0.6 25.4x 15.6x 254.0x 49.2x 5.1x 4.1x 35% OW Doug AnmuthOpenTable Inc OPEN $79.55 1,942 34.3x 29.5x 17% 1.8 17.7x 14.7x 26.1x 21.5x 7.7x 6.5x 18% N Kaizad GotlaBankrate Inc RATE $16.64 1,665 20.9x 18.0x 33% 0.5 10.9x 9.0x 18.5x NM 3.2x 2.7x 13% N Doug AnmuthTrulia Inc TRLA $36.83 1,416 40.5x 42.4x 15% 2.9 24.8x 15.6x 29.2x 21.5x 5.2x 3.9x 54% OW Doug AnmuthChegg Inc CHGG $8.26 746 NM 18.9x NM NM 141.7x 11.9x 58.8x 14.4x 1.9x 1.5x 25% OW Doug AnmuthQuinStreet Inc QNST $8.76 379 22.0x 14.3x -43% -0.3 9.0x 7.6x 22.7x 9.6x 1.1x 1.1x 3% N Doug AnmuthReachLocal Inc RLOC $12.73 369 26.1x 15.1x 44% 0.3 6.5x 3.5x 8.0x NM 0.4x 0.3x 13% OW Doug AnmuthCafePress Inc PRSS $6.33 111 13.7x 9.6x 200% 0.0 3.9x 2.7x 12.2x 5.9x 0.3x 0.2x 10% N Doug AnmuthChinaTencent Holdings Ltd 700 HK HKD 495.60 124,193 227.0x 170.5x 40% 4.3 21.5x 15.3x 28.5x 20.9x 8.5x 6.3x 36% OW Alex YaoBaidu Inc BIDU US $176.63 61,925 22.8x 17.3x 41% 0.4 17.5x 12.2x 23.9x 12.7x 7.5x 5.3x 36% OW Alex YaoQihoo 360 Technology Co., Ltd QIHU US $80.10 10,520 35.3x 24.1x 57% 0.4 29.9x 18.5x 47.3x 25.1x 8.9x 6.0x 54% OW Alex YaoNetEase Inc NTES US $78.03 10,180 13.0x 11.3x 11% 1.0 11.1x 9.5x 13.1x 11.3x 5.4x 4.8x 10% N Alex YaoCtrip.com International Ltd CTRP US $44.43 7,420 23.9x 18.7x 24% 0.8 30.2x 21.1x 27.4x 21.1x 5.9x 4.5x 28% N Alex YaoSouFun Holdings Ltd SFUN US $83.98 6,873 21.2x 17.7x 19% 0.9 15.6x 12.6x 20.5x 15.5x 8.3x 6.6x 21% OW Alex YaoSina Corp SINA US $84.35 6,153 37.0x 28.9x 61% 0.5 36.2x 24.0x 54.5x 33.9x 6.3x 4.9x 29% OW Alex YaoYouku Tudou Inc YOKU US $33.92 5,645 242.3x 50.6x NM NM 36.5x 21.2x 38.9x 22.7x 8.1x 5.9x 39% N Alex YaoVipshop Holdings Ltd VIPS US $82.28 4,722 35.8x 24.3x 73% 0.3 29.1x 18.3x 26.6x 26.7x 1.5x 1.0x 62% OW Alex YaoYY Inc YY US $57.34 3,384 25.3x 19.7x 40% 0.5 24.5x 16.8x 23.1x 17.4x 6.6x 4.5x 49% OW Alex YaoSohu.com Inc SOHU US $73.94 2,883 30.1x 29.9x 32% 0.9 6.6x 5.5x 8.4x 12.6x 1.2x 0.9x 18% N Alex YaoForgame Holdings Ltd 484 HK HKD 55.90 940 93.2x 72.9x -12% -5.9 6.7x 4.2x 8.0x 5.2x 2.3x 1.5x 32% OW Alex YaoPhoenix New Media Ltd FENG US $9.81 779 13.8x 10.5x 28% 0.4 9.7x 6.3x 11.5x 7.7x 1.8x 1.4x 24% OW Alex Yao

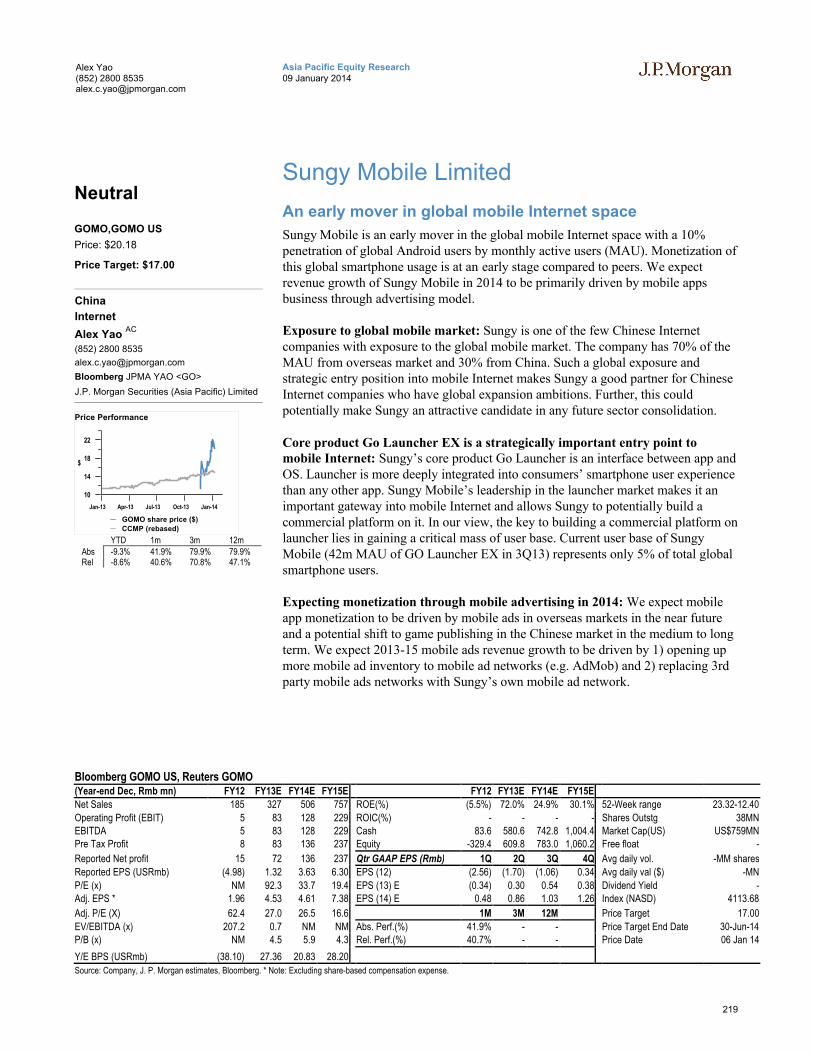

Sungy Mobile Ltd GOMO US $20.18 759 27.3x 17.1x 27% 0.6 30.3x 15.8x 25.2x 14.3x 7.7x 4.8x 52% N Alex YaoE-commerce China Dangdang Inc DANG US $9.00 742 NM 45.0x NM NM 76.1x 17.4x NM 14.0x 0.5x 0.4x 18% UW Alex YaoKorea (in KRW)Naver 035420 KS KRW 699,000 19,563 35.5x 22.8x 53% 0.4 22.7x 14.1x 40.9x 24.0x 6.8x 5.2x 28% OW Stanley YangNCSoft 036570 KS KRW 234,000 4,362 15.2x 13.7x 43% 0.3 10.1x 8.6x 16.6x 13.4x 4.2x 3.6x 16% OW Stanley YangNHN Ent. 181710 KS KRW 91,700 1,308 14.1x 14.5x -8% -1.9 7.3x 7.4x 16.3x 16.6x 1.7x 1.6x 3% UW Stanley YangDaum 035720 KS KRW 84,700 1,068 14.5x 13.2x 10% 1.4 5.7x 4.8x 11.3x 9.2x 1.3x 1.1x 10% N Stanley YangWemade 112040 KS KRW 32,000 500 13.7x 9.7x 49% 0.2 7.5x 5.0x 14.9x 8.7x 1.6x 1.3x 12% N Stanley YangGamevil 063080 KS KRW 44,600 270 15.6x 14.1x 10% 1.4 11.2x 9.9x 18.9x 15.7x 2.3x 2.0x 17% UW Stanley YangJapan (in Yen)Yahoo! Japan 4689 ¥592.00 32,672 26.2x 22.6x 11% 2.1 12.2x 10.6x 23.1x 19.0x 6.7x 5.9x 9% OW Haruka MoriRakuten 4755 ¥1,586.00 20,133 31.8x 25.1x 28% 0.9 13.9x 11.3x 54.1x 38.6x 3.6x 3.2x 10% N Haruka MoriKakaku 2371 ¥1,830.00 3,982 33.0x 26.0x 31% 0.8 18.9x 15.3x 33.5x 25.5x 10.6x 8.9x 20% N Haruka MoriNEXON 3659 ¥941.00 3,965 10.4x 10.2x 2% 6.2 4.0x 3.3x 5.5x 4.6x 1.8x 1.5x 4% N Haruka MoriDeNA 2432 ¥2,151.00 3,113 10.2x 9.9x 2% 5.8 3.3x 2.8x 5.7x 4.7x 1.1x 0.9x 3% OW Haruka MoriCyberAgent 4751 ¥4,400.00 2,669 23.3x 21.7x 12% 1.8 8.6x 7.8x 17.6x 16.1x 1.2x 1.0x 6% N Haruka MoriGREE 3632 ¥1,033.00 2,415 11.7x 11.5x 14% 0.8 4.5x 4.0x 7.4x 6.5x 1.4x 1.2x 3% N Haruka MoriASKUL 2678 ¥3,020.00 1,572 34.1x 23.7x 52% 0.5 11.0x 8.7x 32.0x 23.7x 0.5x 0.4x 18% OW Haruka MoriGurunavi 2440 ¥3,135.00 782 25.5x 18.5x 38% 0.5 8.6x 7.1x 19.5x 15.5x 2.1x 1.8x 10% OW Haruka MoriEuropeSchibsted SCH NO £417.00 7,226 50.2x 35.3x 52% 0.7 20.9x 17.6x 46.7x 37.7x 3.0x 2.8x 4% N Nicolas DubourgAxel Springer SPR GR £47.35 3,429 19.0x 16.9x 1% 18.2 9.8x 8.9x 12.4x 14.6x 1.7x 1.6x -3% N Nicolas DubourgRightmove RMV LN £2,805.00 1,693 28.4x 23.5x 22% 1.1 21.7x 17.7x 29.0x 23.0x 16.4x 13.5x 17% OW Nicolas DubourgCTS Eventim EVD GY € 39.30 1,384 21.9x 19.2x 14% 1.3 12.1x 10.4x 15.3x 12.9x 2.9x 2.6x 5% OW Nicolas DubourgUbisoft UBI FP € 10.04 743 15.5x 8.1x NM NM 1.9x 1.5x 161.3x 11.4x 0.7x 0.6x 20% N Nicolas DubourgMoney Supermarket MONY LN £189.30 625 15.6x 14.3x 11% 1.3 11.5x 10.3x 16.1x 14.3x 4.2x 3.8x 8% N Nicolas DubourgGameloft GFT FP € 7.93 501 18.6x 12.8x 48% 0.3 8.9x 5.9x 13.9x 9.3x 2.1x 1.6x 17% OW Nicolas DubourgPerform PER LN £224.80 360 21.9x 17.2x 19% 0.9 12.9x 10.2x 28.4x 21.9x 2.3x 2.0x 14% N Nicolas DubourgXING O1BC GY £79.31 325 31.4x 25.7x 29% 0.9 12.4x 10.1x 22.1x 18.7x 3.9x 3.4x 11% UW Nicolas DubourgLatin AmericaMercadoLibre, Inc MELI $101.49 4,481 32.0x 26.3x 25% 1.1 20.1x 15.6x 30.2x 22.7x 7.2x 5.7x 22% N Andrew BaggioRussiaYandex YNDX $42.91 13,982 28.4x 22.7x 19% 1.2 18.4x 14.9x NM NM 8.2x 6.6x 26% OW Alexi GogolevMail.ru MAIL LI $42.64 8,916 21.9x 18.3x 22% 0.8 14.7x 12.3x 17.2x 14.6x 8.0x 6.7x 21% OW Alexi Gogolev

EV/RevenueEV/EBITDAP/E EV/FCF

Source: Company reports, Bloomberg and J.P. Morgan estimates.

7

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

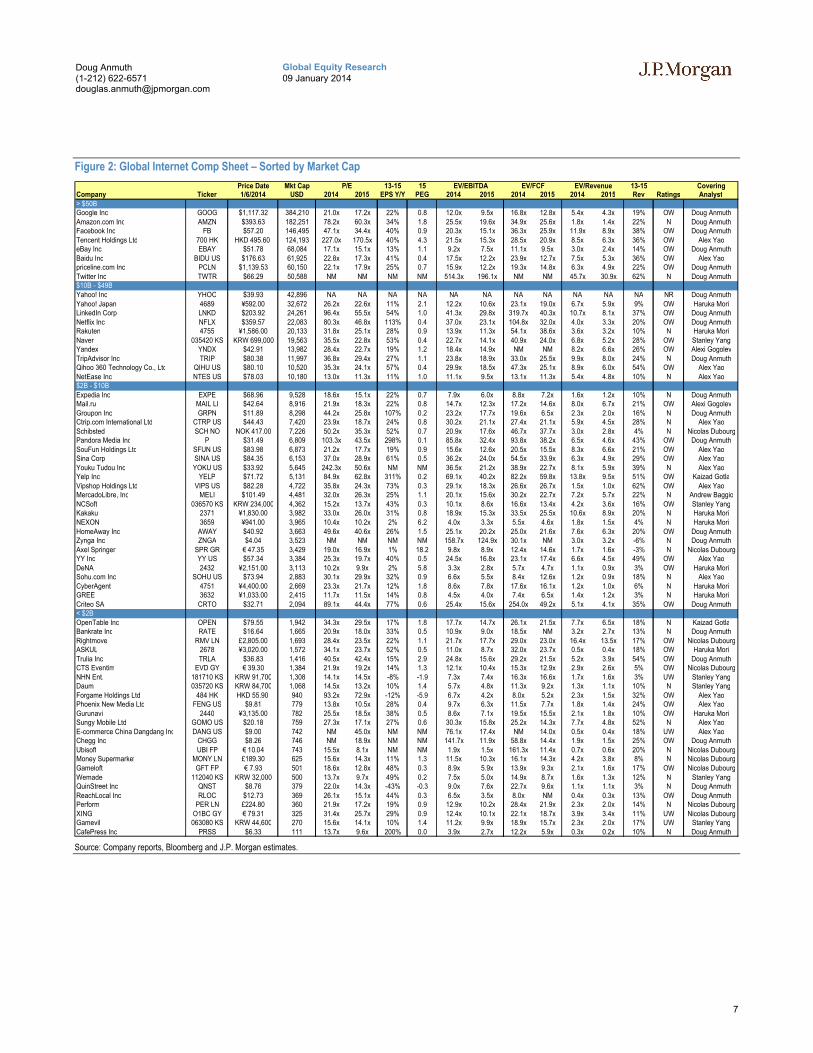

Figure 2: Global Internet Comp Sheet – Sorted by Market Cap

Price Date Mkt Cap 13-15 15 13-15 CoveringCompany Ticker 1/6/2014 USD 2014 2015 EPS Y/Y PEG 2014 2015 2014 2015 2014 2015 Rev Ratings Analyst> $50BGoogle Inc GOOG $1,117.32 384,210 21.0x 17.2x 22% 0.8 12.0x 9.5x 16.8x 12.8x 5.4x 4.3x 19% OW Doug AnmuthAmazon.com Inc AMZN $393.63 182,251 78.2x 60.3x 34% 1.8 25.5x 19.6x 34.9x 25.6x 1.8x 1.4x 22% N Doug AnmuthFacebook Inc FB $57.20 146,495 47.1x 34.4x 40% 0.9 20.3x 15.1x 36.3x 25.9x 11.9x 8.9x 38% OW Doug AnmuthTencent Holdings Ltd 700 HK HKD 495.60 124,193 227.0x 170.5x 40% 4.3 21.5x 15.3x 28.5x 20.9x 8.5x 6.3x 36% OW Alex YaoeBay Inc EBAY $51.78 68,084 17.1x 15.1x 13% 1.1 9.2x 7.5x 11.1x 9.5x 3.0x 2.4x 14% OW Doug AnmuthBaidu Inc BIDU US $176.63 61,925 22.8x 17.3x 41% 0.4 17.5x 12.2x 23.9x 12.7x 7.5x 5.3x 36% OW Alex Yaopriceline.com Inc PCLN $1,139.53 60,150 22.1x 17.9x 25% 0.7 15.9x 12.2x 19.3x 14.8x 6.3x 4.9x 22% OW Doug AnmuthTwitter Inc TWTR $66.29 50,588 NM NM NM NM 514.3x 196.1x NM NM 45.7x 30.9x 62% N Doug Anmuth$10B - $49BYahoo! Inc YHOO $39.93 42,896 NA NA NA NA NA NA NA NA NA NA NA NR Doug AnmuthYahoo! Japan 4689 ¥592.00 32,672 26.2x 22.6x 11% 2.1 12.2x 10.6x 23.1x 19.0x 6.7x 5.9x 9% OW Haruka MoriLinkedIn Corp LNKD $203.92 24,261 96.4x 55.5x 54% 1.0 41.3x 29.8x 319.7x 40.3x 10.7x 8.1x 37% OW Doug AnmuthNetflix Inc NFLX $359.57 22,083 80.3x 46.8x 113% 0.4 37.0x 23.1x 104.8x 32.0x 4.0x 3.3x 20% OW Doug AnmuthRakuten 4755 ¥1,586.00 20,133 31.8x 25.1x 28% 0.9 13.9x 11.3x 54.1x 38.6x 3.6x 3.2x 10% N Haruka MoriNaver 035420 KS KRW 699,000 19,563 35.5x 22.8x 53% 0.4 22.7x 14.1x 40.9x 24.0x 6.8x 5.2x 28% OW Stanley YangYandex YNDX $42.91 13,982 28.4x 22.7x 19% 1.2 18.4x 14.9x NM NM 8.2x 6.6x 26% OW Alexi GogolevTripAdvisor Inc TRIP $80.38 11,997 36.8x 29.4x 27% 1.1 23.8x 18.9x 33.0x 25.5x 9.9x 8.0x 24% N Doug AnmuthQihoo 360 Technology Co., Ltd QIHU US $80.10 10,520 35.3x 24.1x 57% 0.4 29.9x 18.5x 47.3x 25.1x 8.9x 6.0x 54% OW Alex YaoNetEase Inc NTES US $78.03 10,180 13.0x 11.3x 11% 1.0 11.1x 9.5x 13.1x 11.3x 5.4x 4.8x 10% N Alex Yao$2B - $10BExpedia Inc EXPE $68.96 9,528 18.6x 15.1x 22% 0.7 7.9x 6.0x 8.8x 7.2x 1.6x 1.2x 10% N Doug AnmuthMail.ru MAIL LI $42.64 8,916 21.9x 18.3x 22% 0.8 14.7x 12.3x 17.2x 14.6x 8.0x 6.7x 21% OW Alexi GogolevGroupon Inc GRPN $11.89 8,298 44.2x 25.8x 107% 0.2 23.2x 17.7x 19.6x 6.5x 2.3x 2.0x 16% N Doug AnmuthCtrip.com International Ltd CTRP US $44.43 7,420 23.9x 18.7x 24% 0.8 30.2x 21.1x 27.4x 21.1x 5.9x 4.5x 28% N Alex YaoSchibsted SCH NO NOK 417.00 7,226 50.2x 35.3x 52% 0.7 20.9x 17.6x 46.7x 37.7x 3.0x 2.8x 4% N Nicolas DubourgPandora Media Inc P $31.49 6,809 103.3x 43.5x 298% 0.1 85.8x 32.4x 93.8x 38.2x 6.5x 4.6x 43% OW Doug AnmuthSouFun Holdings Ltd SFUN US $83.98 6,873 21.2x 17.7x 19% 0.9 15.6x 12.6x 20.5x 15.5x 8.3x 6.6x 21% OW Alex YaoSina Corp SINA US $84.35 6,153 37.0x 28.9x 61% 0.5 36.2x 24.0x 54.5x 33.9x 6.3x 4.9x 29% OW Alex YaoYouku Tudou Inc YOKU US $33.92 5,645 242.3x 50.6x NM NM 36.5x 21.2x 38.9x 22.7x 8.1x 5.9x 39% N Alex YaoYelp Inc YELP $71.72 5,131 84.9x 62.8x 311% 0.2 69.1x 40.2x 82.2x 59.8x 13.8x 9.5x 51% OW Kaizad GotlaVipshop Holdings Ltd VIPS US $82.28 4,722 35.8x 24.3x 73% 0.3 29.1x 18.3x 26.6x 26.7x 1.5x 1.0x 62% OW Alex YaoMercadoLibre, Inc MELI $101.49 4,481 32.0x 26.3x 25% 1.1 20.1x 15.6x 30.2x 22.7x 7.2x 5.7x 22% N Andrew BaggioNCSoft 036570 KS KRW 234,000 4,362 15.2x 13.7x 43% 0.3 10.1x 8.6x 16.6x 13.4x 4.2x 3.6x 16% OW Stanley YangKakaku 2371 ¥1,830.00 3,982 33.0x 26.0x 31% 0.8 18.9x 15.3x 33.5x 25.5x 10.6x 8.9x 20% N Haruka MoriNEXON 3659 ¥941.00 3,965 10.4x 10.2x 2% 6.2 4.0x 3.3x 5.5x 4.6x 1.8x 1.5x 4% N Haruka MoriHomeAway Inc AWAY $40.92 3,663 49.6x 40.6x 26% 1.5 25.1x 20.2x 25.0x 21.6x 7.6x 6.3x 20% OW Doug AnmuthZynga Inc ZNGA $4.04 3,523 NM NM NM NM 158.7x 124.9x 30.1x NM 3.0x 3.2x -6% N Doug AnmuthAxel Springer SPR GR € 47.35 3,429 19.0x 16.9x 1% 18.2 9.8x 8.9x 12.4x 14.6x 1.7x 1.6x -3% N Nicolas DubourgYY Inc YY US $57.34 3,384 25.3x 19.7x 40% 0.5 24.5x 16.8x 23.1x 17.4x 6.6x 4.5x 49% OW Alex YaoDeNA 2432 ¥2,151.00 3,113 10.2x 9.9x 2% 5.8 3.3x 2.8x 5.7x 4.7x 1.1x 0.9x 3% OW Haruka MoriSohu.com Inc SOHU US $73.94 2,883 30.1x 29.9x 32% 0.9 6.6x 5.5x 8.4x 12.6x 1.2x 0.9x 18% N Alex YaoCyberAgent 4751 ¥4,400.00 2,669 23.3x 21.7x 12% 1.8 8.6x 7.8x 17.6x 16.1x 1.2x 1.0x 6% N Haruka MoriGREE 3632 ¥1,033.00 2,415 11.7x 11.5x 14% 0.8 4.5x 4.0x 7.4x 6.5x 1.4x 1.2x 3% N Haruka MoriCriteo SA CRTO $32.71 2,094 89.1x 44.4x 77% 0.6 25.4x 15.6x 254.0x 49.2x 5.1x 4.1x 35% OW Doug Anmuth< $2BOpenTable Inc OPEN $79.55 1,942 34.3x 29.5x 17% 1.8 17.7x 14.7x 26.1x 21.5x 7.7x 6.5x 18% N Kaizad GotlaBankrate Inc RATE $16.64 1,665 20.9x 18.0x 33% 0.5 10.9x 9.0x 18.5x NM 3.2x 2.7x 13% N Doug AnmuthRightmove RMV LN £2,805.00 1,693 28.4x 23.5x 22% 1.1 21.7x 17.7x 29.0x 23.0x 16.4x 13.5x 17% OW Nicolas DubourgASKUL 2678 ¥3,020.00 1,572 34.1x 23.7x 52% 0.5 11.0x 8.7x 32.0x 23.7x 0.5x 0.4x 18% OW Haruka MoriTrulia Inc TRLA $36.83 1,416 40.5x 42.4x 15% 2.9 24.8x 15.6x 29.2x 21.5x 5.2x 3.9x 54% OW Doug AnmuthCTS Eventim EVD GY € 39.30 1,384 21.9x 19.2x 14% 1.3 12.1x 10.4x 15.3x 12.9x 2.9x 2.6x 5% OW Nicolas DubourgNHN Ent. 181710 KS KRW 91,700 1,308 14.1x 14.5x -8% -1.9 7.3x 7.4x 16.3x 16.6x 1.7x 1.6x 3% UW Stanley YangDaum 035720 KS KRW 84,700 1,068 14.5x 13.2x 10% 1.4 5.7x 4.8x 11.3x 9.2x 1.3x 1.1x 10% N Stanley YangForgame Holdings Ltd 484 HK HKD 55.90 940 93.2x 72.9x -12% -5.9 6.7x 4.2x 8.0x 5.2x 2.3x 1.5x 32% OW Alex YaoPhoenix New Media Ltd FENG US $9.81 779 13.8x 10.5x 28% 0.4 9.7x 6.3x 11.5x 7.7x 1.8x 1.4x 24% OW Alex YaoGurunavi 2440 ¥3,135.00 782 25.5x 18.5x 38% 0.5 8.6x 7.1x 19.5x 15.5x 2.1x 1.8x 10% OW Haruka MoriSungy Mobile Ltd GOMO US $20.18 759 27.3x 17.1x 27% 0.6 30.3x 15.8x 25.2x 14.3x 7.7x 4.8x 52% N Alex YaoE-commerce China Dangdang Inc DANG US $9.00 742 NM 45.0x NM NM 76.1x 17.4x NM 14.0x 0.5x 0.4x 18% UW Alex YaoChegg Inc CHGG $8.26 746 NM 18.9x NM NM 141.7x 11.9x 58.8x 14.4x 1.9x 1.5x 25% OW Doug AnmuthUbisoft UBI FP € 10.04 743 15.5x 8.1x NM NM 1.9x 1.5x 161.3x 11.4x 0.7x 0.6x 20% N Nicolas DubourgMoney Supermarket MONY LN £189.30 625 15.6x 14.3x 11% 1.3 11.5x 10.3x 16.1x 14.3x 4.2x 3.8x 8% N Nicolas DubourgGameloft GFT FP € 7.93 501 18.6x 12.8x 48% 0.3 8.9x 5.9x 13.9x 9.3x 2.1x 1.6x 17% OW Nicolas DubourgWemade 112040 KS KRW 32,000 500 13.7x 9.7x 49% 0.2 7.5x 5.0x 14.9x 8.7x 1.6x 1.3x 12% N Stanley YangQuinStreet Inc QNST $8.76 379 22.0x 14.3x -43% -0.3 9.0x 7.6x 22.7x 9.6x 1.1x 1.1x 3% N Doug AnmuthReachLocal Inc RLOC $12.73 369 26.1x 15.1x 44% 0.3 6.5x 3.5x 8.0x NM 0.4x 0.3x 13% OW Doug AnmuthPerform PER LN £224.80 360 21.9x 17.2x 19% 0.9 12.9x 10.2x 28.4x 21.9x 2.3x 2.0x 14% N Nicolas DubourgXING O1BC GY € 79.31 325 31.4x 25.7x 29% 0.9 12.4x 10.1x 22.1x 18.7x 3.9x 3.4x 11% UW Nicolas DubourgGamevil 063080 KS KRW 44,600 270 15.6x 14.1x 10% 1.4 11.2x 9.9x 18.9x 15.7x 2.3x 2.0x 17% UW Stanley YangCafePress Inc PRSS $6.33 111 13.7x 9.6x 200% 0.0 3.9x 2.7x 12.2x 5.9x 0.3x 0.2x 10% N Doug Anmuth

EV/FCF EV/RevenueEV/EBITDAP/E

Source: Company reports, Bloomberg and J.P. Morgan estimates.

8

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Global Internet Top Picks

U.S.

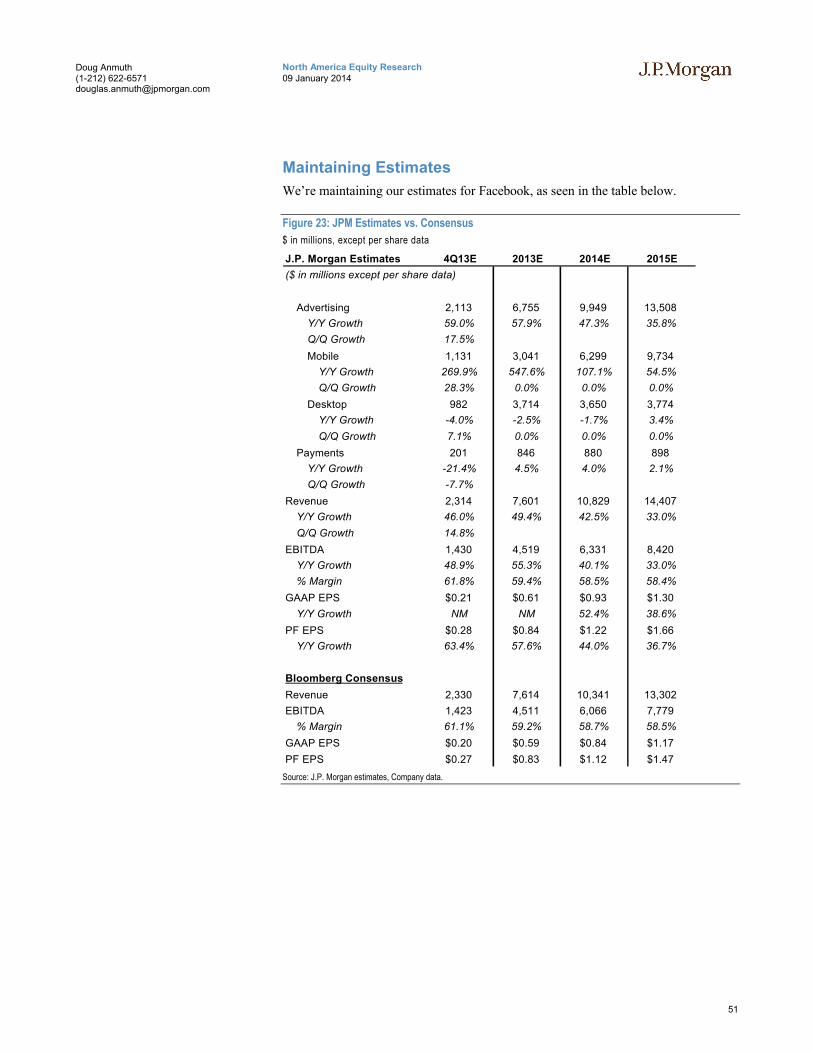

Facebook: Overweight, $62 PT. Facebook remains a top pick into 2014 as we believe it is still early in monetizing the company’s base of 1.2B users globally. Facebook’s mobile advertising should surpass desktop in 4Q13 and we expect mobile to account for 63% of total ad revenue in 2014. We believe advertiser demand and ads quality should more than offset slower increases in ad load, thereby driving higher relevancy and click-through rates and ultimately greater quality over time. We think Instagram and auto-play video ads could also drive upside to our and Street estimates. We note that our 2014 PF EPS estimate for Facebook is currently 7% above consensus and our 2015 estimate is 12% ahead.

Google: Overweight, $1,305 PT. We believe Google’s strong position in both mobile and video should drive continued share gains in online advertising, and Google remains focused on product innovation and disruptive technologies. As users become more comfortable and savvy transacting through mobile devices and Google delivers more efficient and better-targeted ads through initiatives such as Estimated Total Conversions and Enhanced Campaigns, we expect mobile to become a bigger tailwind for the company in upcoming quarters. We are also increasingly optimistic on YouTube now that the company is utilizing Nielsen’s Online Campaign Ratings (OCR) tags. Our ad industry discussions suggest that TV ad buyers would like to spend more money online and we believe familiar measurement methodology through OCR will help to accelerate this shift. We remain optimistic on Google growing traction with PLAs into 2014 and the potential for Network Sites to rebound from a heavily self-inflicted slowdown in 2013. We expect Google to continue to deliver strong growth off a large base and we believe the combination of growth and stability in the business model, still-reasonable valuation (17.2x 2015E PF EPS), and significant cash on the balance sheet (~15% of the market cap) help make Google a strong play in 2014.

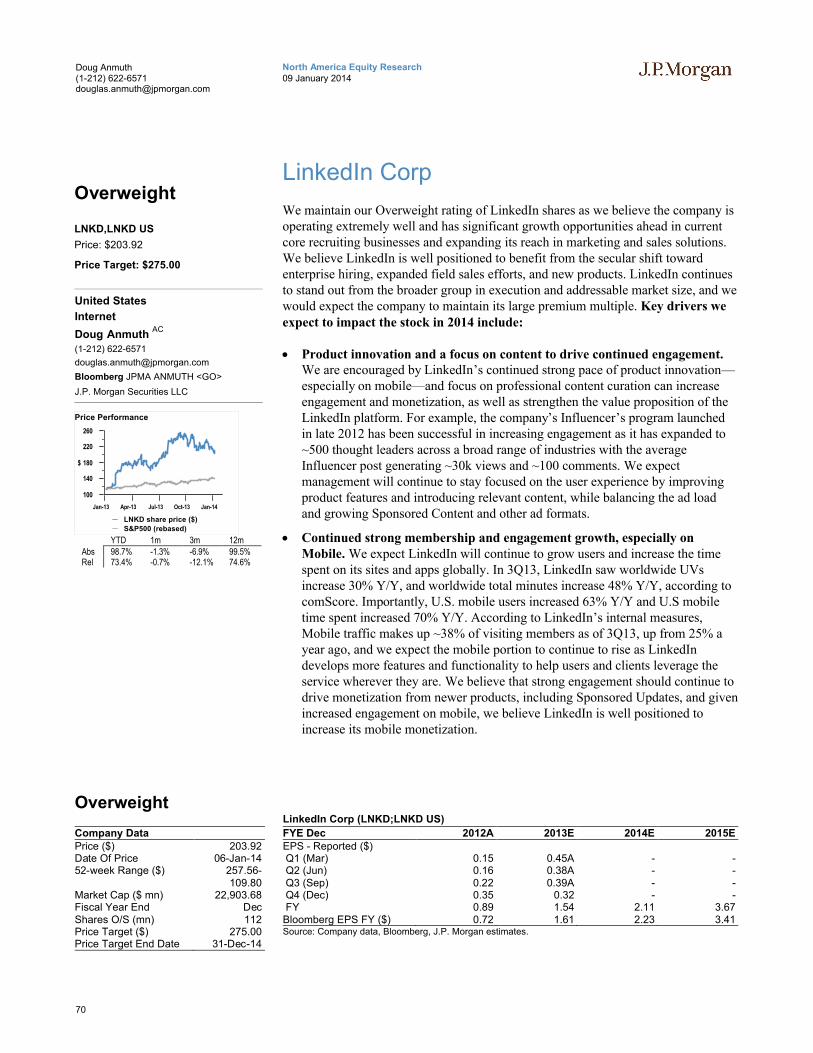

LinkedIn: Overweight, $275 PT. We believe LinkedIn is well positioned to benefit from the secular shift toward enterprise hiring, expanded field sales efforts, and new products. We would be buyers of the recent weakness in LinkedIn as we remain optimistic on Talent Solutions growth driven by deeper enterprise penetration, a pricing increase impacting half of all subscribers in 2014, and potential for stabilization in international markets. We also expect accelerating Marketing Solutions growth in 2014 as LinkedIn laps tougher comps after 1Q and Sponsored Updates should benefit from significant dollars moving toward Newsfeed and Native ads. It remains early for Sales Navigator, but we believe the product will be extended more towards corporates this year. We believe LinkedIn remains focused on product innovation and engagement and we would take advantage of recent weakness in the shares.

Pandora: Overweight, $35 PT. Pandora is our top SMid-cap pick as we continue to view the stock as a compelling pure play on mobile and believe the company is at an inflection point on monetization. We highlight recent listener metrics and app download trends, which represent solid continued growth in hours, users, and market share despite a heightened competitive environment. We also highlight recent updates to Pandora’s auto strategy, including achieving 4M unique native auto

9

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

activations and introducing in-car targeted advertising. We believe Pandora’s monetization and profitability will improve going forward as: 1) Pandora’s 8.6% market share of total US radio should continue to ramp; 2) radio buy-side platform integration should remove friction from the buying process and attract more ad spend; 3) increased audience segmentation and auto-focused campaigns should help support increasing CPMs; 4) Pandora continues to build out its local sales force (now in 29 of top 40 markets); and 5) cost-control policies including the limit to mobileskips should help curb content costs in place of the 40-hour mobile cap, enabling greater leverage in content acquisition.

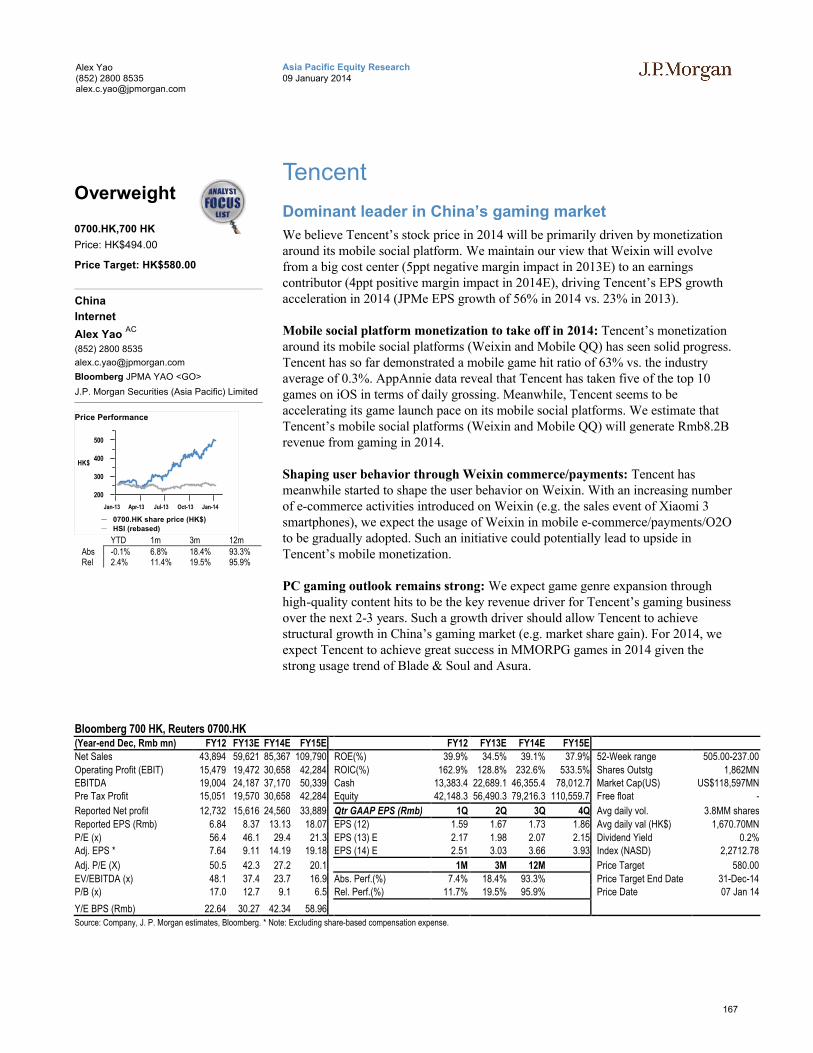

China

Tencent: Overweight, HK$580 PT. We maintain our Overweight rating on Tencent with a Dec-14 PT of HK$580. We believe Tencent is a dominant leader in China’s gaming market and it is expected to capture a 48% market share in China’s total gaming market in 2014. On PC side, we expect Tencent’s revenue growth to be driven by continued high-quality hit content (e.g., Blade & Soul and Asura) over the next 2-3 years. On mobile side, Tencent is well positioned across the entire mobile games value chain including development, publishing and distribution. Such positioning allows Tencent to capture a significant portion of value created in China’s mobile gaming market. We estimate Tencent will generate RMB8.2bn mobile gaming revenue in 2014. In the long run, we expect Tencent will obtain more market share in mobile gaming market than in PC gaming market, given its stronger mobile distribution power, Weixin’s high-end user base and fast game genre expansion on mobile.

Qihoo: Overweight, US$98 PT. We maintain our Overweight rting on Qihoo with a Dec-14 PT of US$98. We view Qihoo as one of the key beneficiaries in the fast-growing mobile gaming market in China over the next two years, due to its wide exposure to mobile users (over 400m monthly active users on mobile) and strong distribution power on mobile (over 45m daily average distribution volume from 360 Mobile Assistant). We estimate Qihoo will capture 12% of China’s mobile gaming market in 2014. Qihoo should generate RMB1.8bn revenue from such a market share. Meanwhile, we expect Qihoo to quickly ramp up monetization of its search traffic in 2014, which is currently significantly under-monetized (1.6% revenue share vs. over 20% traffic share).

YY: Overweight, US$67 PT. We maintain our Overweight rating on YY with a Dec-14 PT of US$67. YY has established a large social-oriented user base on the back of its technology strengths in rich-media-based group communications on a real-time basis. Such an advantage is highly scalable to other internet activities which require online group voice/video communications, e.g., online recruiting and online education. Meanwhile, with sizable organic traffic, YY is able to cross-sell other internet content/services (e.g., online gaming) to users. We expect YY’s growth in 2014 to be primarily driven by 1) continued strong growth of YY Music, 2) PC game licensing, and 3) mobile games development and publishing.

10

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Korea

Naver: Overweight, W770,000 PT. Internet traffic is highly concentrated in the dominant portal, Naver, in Korea. We are positive on the potential monetization upside of Naver’s mobile ad business. We also believe the potential monetization upside of Naver’s global social networking business has yet to be fully captured by the market due to the time lag between subscriber growth and monetization.

NCsoft: Overweight, W300,000 PT. We like the company’s leading global position in the captive hardcore MMORPG market on significantly subdued competition (a few survivors take all). The upcoming launches of GW2 in China and Wild Star in the US/EU are expected to serve as additional share price catalysts, in addition to B&S’s current strong traction in China.

Japan

Yahoo Japan: Overweight, ¥600 PT. Following the shift to an advertising income model, we expect the stock to gradually start pricing in the medium-term potential for e-commerce as investors confirm that growth in the number of store openings boosts product numbers, increases customer pulling power, and expands sales value. However, we expect smartphone advertising and YDN to drive stable growth for core advertising sales for the foreseeable future, and think the stock is very attractive from a risk/reward perspective.

Askul: Overweight, ¥3,700 PT. While valuations look demanding and the share price appears to have risen on investor expectations, we think LOHACO will gradually start to benefit from Yahoo Japan’s initiatives (which will step up from early 2014) as faster growth in e-commerce provides a tailwind. Specifically, we note 1) benefits in terms of attracting customers, 2) the use of big data, and 3) growth in logistics volumes. We focus on this stock because we think it could be major beneficiary of Yahoo Japan’s new e-commerce strategy.

Europe

Gameloft: Overweight, €9.50 PT. We are Overweight on Gameloft with target price of €9.50. Gameloft is one of the leading developers of games for digital platforms such as mobile phones, smartphones and tablets and, in our view, an ideal play on soaring mobile device sales along with freemium games across the globe. The future for the online game industry looks bright: the number of smartphone subscriptions is set to triple to 5.6bn by 2019, with APAC reaching 4.7bn. Within mobile use, gaming is the 3rd most popular activity (6h per month, source: Ericsson mobility report, November). And Gameloft is likely to be a key beneficiary due to 1) unparalleled mobile exposure: games on smartphones and tablets made up 69% of Gameloft’s revenues in Q313 (mobile 98% of Q2 in total), 2) great geographical exposure: LatAm and APAC already made up 36% of revenues in Q3, 3) focus on freemium: sales of virtual goods and advertising within games accounted for 80% of Gameloft’s Q3 smartphone revenues, offering access to gamers at lower price points and recurring revenues from a given game, 4) limited single-game risk: no game contributes over 10% of revenues, so Gameloft is not dependent on one hit. On our estimates, +17% revenues CAGR’13-’15 translates into +37% EBITDA CAGR even as, we assume c.60% of adj. operating costs are fixed (i.e. growing at c.7% p.a. to FY15), with the remainder growing in line with sales. Gameloft stopped hiring in August 2012 (having significantly built up its game developing capacity) and signaled that up to 80% of costs are fixed. H113 results/FY13 guidance then

11

Global Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

confirmed operating leverage is kicking in. Gameloft may further boost profitability as it reduces its annual slate to 15-20 games by 2014 (vs. FY13’s 22) and focuses on evolving successful games. Gameloft shares are trading on 12.8x 2013EEV/EBITDA which we see as attractive given Gameloft’s 13E-15E EBITDA CAGR of +37%. We leave our estimates unchanged and our EBIT estimate is +10% ahead of BBG consensus in ‘14.

Moneysupermarket: Overweight, 211p PT. We are OW the leader in UK online price comparison (from N) as i) ST uncertainty is reduced (Q3 results and FY13 guidance have shown some stabilization/recovery since the flat y/y revenues of July),ii) the Money vertical (c.30% of revs revs’12) will no longer suffer from tough comparables from Q413/Q114 and iii) the structural growth opportunity remains: more customers could switch providers and do so online: switches/new purchases still make up only 26%/13%/16% of yearly market volumes in the key home insurance, cards and energy verticals and only 55%/56%/32% of those purchases occur online, vs. 44%/81% for motor insurance. The next catalyst will be the Q4 post close update on January 14. Energy is providing a case study to support the structural growth view: prospects for Energy price comparison websites have boomed with i) recent increases in UK Energy prices, which have prompted 900k households to switch providers in Oct/Nov’13 and ii) the end of doorstep-selling in 2012, which leaves more space for online sales. We now see Energy contributing £20m to MONY revenues in FY13 (c.9% of group revenues, vs. £8-9m in FY12), rising progressively thereafter. Our MONY Energy revenue estimate for 2016 is consistent with i) 5.6m Energy customers switching providers overall in the UK (no change vs. 2012), ii) 50% doing so online (vs. 32% for Energy in 2012 and 55% for Home Insurance), iii) MONY taking a 16% market share of online switches (more than the c.9% we estimate for 2012 but less than MONY’s apparent share in October’13), at JPMe c.£60 fee per switch. We also see increasing mobile adoption favouring MONY. MONY is the market leader in the financial price comparison market (>40% share of visits) and we expect their app to be the leader. Mobile users have only a few apps they use on a regular base: this creates significant barriers to entry and increases market share. Our EPS estimates are in line/+5% ahead of BBG. Our Dec-14E PT is DCF-based (WACC of 9%, g 2%) and is 211p. MONY trades at 12.9x EV/EBITDA’13 for 9% EBITDA CAGR’13-’15 but also a highly competitive 6.3% Equity FCF yield ’14 & 4.1% dividend yield ’14. Our Bull case offers a DCF value of 236p and 28% upside.

Russia

Yandex: Overweight, $50 PT. Yandex is the leading advertising platform in Russiawith over 300K+ advertisers in 1H13, accounting for c57% of the Russia online ad market. Yandex is also #1 internet destination, with c55 mn unique monthly visitors. Yandex is leveraging its platform and has become #1 comparison shopping destination, used by 40% of Russian online shoppers (Source: AKAR). Yandex in Turkey: while its search market share remains in the low-single digits, the company plans to start to monetize its product. We continue to prefer Yandex among the Russian TMT space and see the stock as an attractive long-term play on Russian consumption and internet roll-out. We believe the name deserves a premium valuation due to strong fundamentals, well-regarded corporate governance and high share liquidity. Any announcement on dividend could well extend the share price rally.

12

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

U.S. Internet Themes for 2014

Revenue and Conversions to Tighten the Gap with Strong Mobile Usage

“The trend has been that mobile was winning…it’s now won.”– Eric Schmidt, Google Chairman

In 2014, global mobile usage should continue to take share from desktop—havingalready crossed 50% of total online usage in the U.S. in 2013—and given continuing growth in smartphone and tablet subscribers worldwide. However, the monetization and commerce associated with that usage has lagged, and we think that 2014 can be a year of catch-up as users become savvier and more comfortable with devices, apps continue to improve in functionality and UI, and more sites become mobile-optimized. Importantly, advertising spend on mobile devices is expected to continue growing as a portion of internet spend, which is, of course, also growing. MagnaGlobal expects global mobile advertising revenue will reach $15.9B in 2014, up 31% Y/Y, representing 12.4% of total online ad spend, relative to 10.7% of estimated total spend for 2013. We expect to see key stakeholders’ success increasingly impacted by their ability to take advantage of the mobile shift, including companies with an online advertising-driven business model, and retailers and eCommerce operators. The discussion below includes: 1) how far along we are in the mobile usage transition; 2) how users engage differently with mobile sites and apps relative to engagement and conversion patterns on desktop; and 3) which companies are best positioned to benefit most or are already closing the gap between mobile usage and mobile revenue.

Nearing Mobile Usage Inflection Point

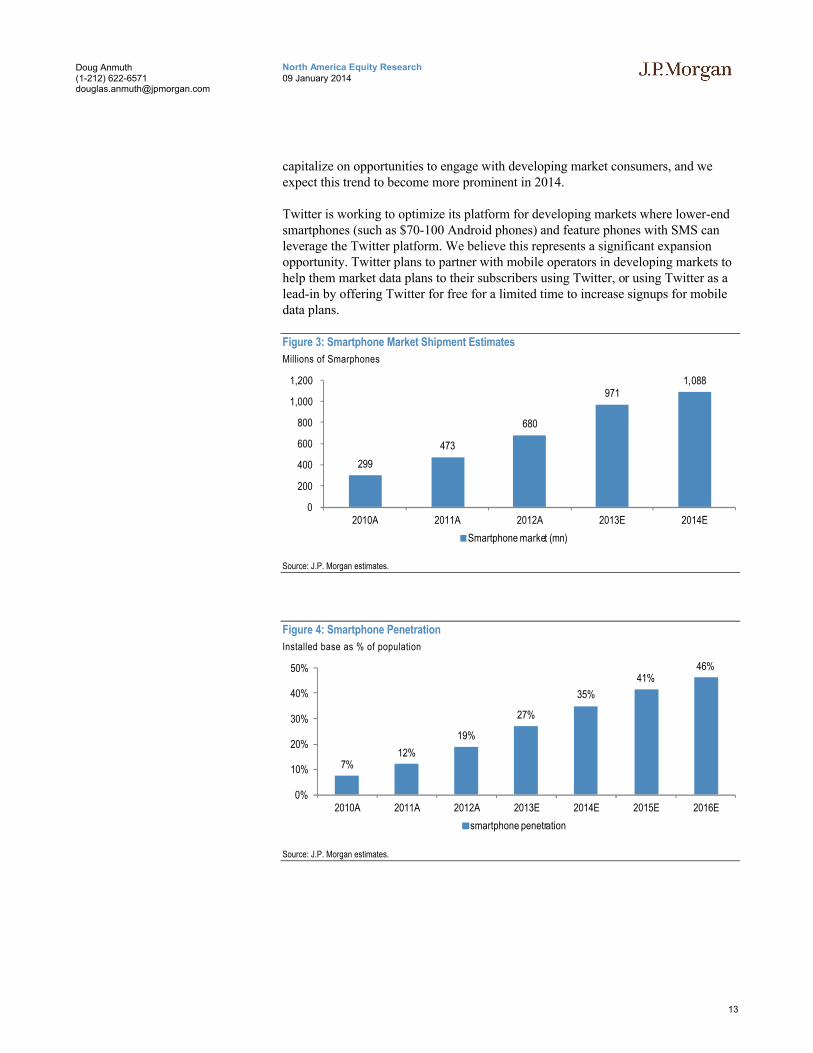

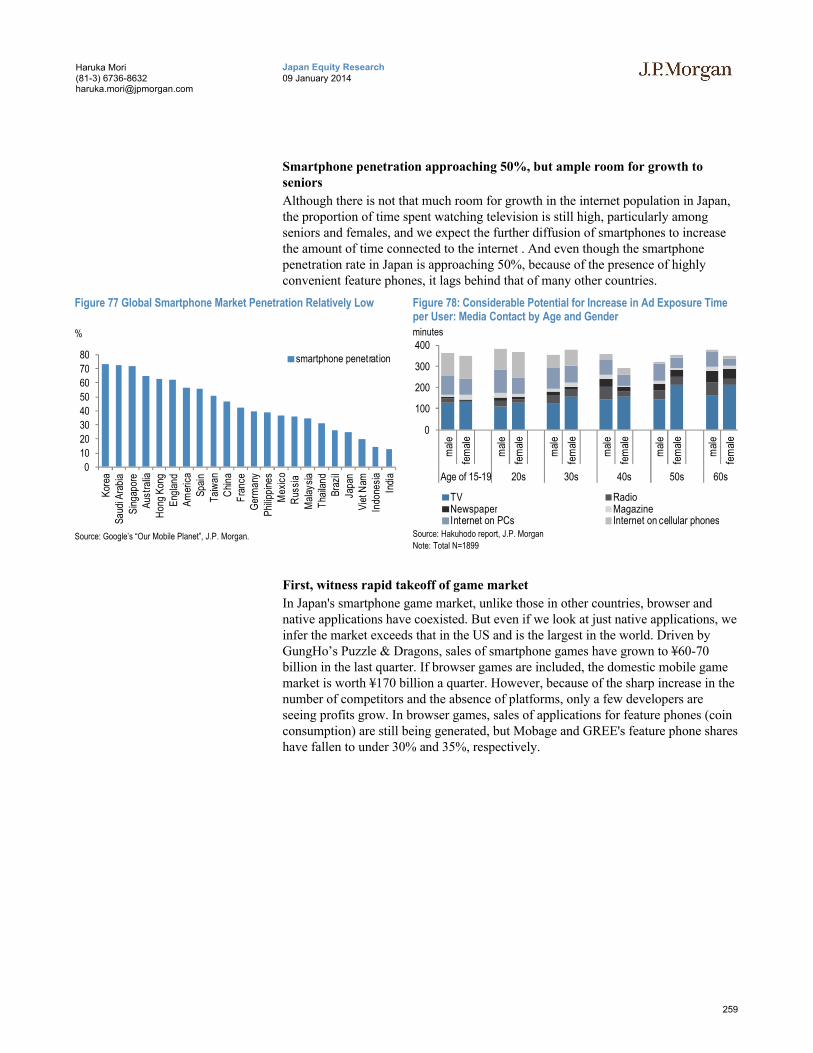

Mobile usage accelerating while penetration continues to grow, but given saturation levels in certain markets, growth may decelerate

Current J.P. Morgan estimates put global smartphone shipments at 971M for 2014, and while growth continues, it may decelerate given increasing global penetration as high as 60s-70s (%) in countries including UAE, South Korea, Saudi Arabia, Singapore, and Norway. While smartphone penetration is above 50% in most developed countries, according to Google’s Our Mobile Planet research, developing countries still have significant room to grow smartphone users with India’s penetration at only 13%. Additionally, J.P. Morgan estimates put global tablet shipments at 221M in 2013 and are expected to reach 277M in 2014, and 318M in 2015. Despite smartphone and tablet growth reaching more mature levels over the coming years, we believe the monetization associated with those users will grow much faster, as mobile revenue still pales in comparison to mobile usage.

We believe that global mobile internet usage is still at a very early growth stage and as traffic per user increases, the way in which users engage with mobile applications and sites will evolve and impact the companies most levered to mobile engagement, including Facebook, Twitter, Pandora, Google, and others. In 2013 we saw many companies—notably Twitter—increase focus on adapting their local services to

13

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

capitalize on opportunities to engage with developing market consumers, and we expect this trend to become more prominent in 2014.

Twitter is working to optimize its platform for developing markets where lower-end smartphones (such as $70-100 Android phones) and feature phones with SMS can leverage the Twitter platform. We believe this represents a significant expansion opportunity. Twitter plans to partner with mobile operators in developing markets to help them market data plans to their subscribers using Twitter, or using Twitter as a lead-in by offering Twitter for free for a limited time to increase signups for mobile data plans.

Figure 3: Smartphone Market Shipment Estimates

Millions of Smarphones

299

473

680

9711,088

0

200

400

600

800

1,000

1,200

2010A 2011A 2012A 2013E 2014E

Smartphone market (mn)

Source: J.P. Morgan estimates.

Figure 4: Smartphone Penetration

Installed base as % of population

7%12%

19%

27%

35%

41%46%

0%

10%

20%

30%

40%

50%

2010A 2011A 2012A 2013E 2014E 2015E 2016E

smartphone penetration

Source: J.P. Morgan estimates.

14

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

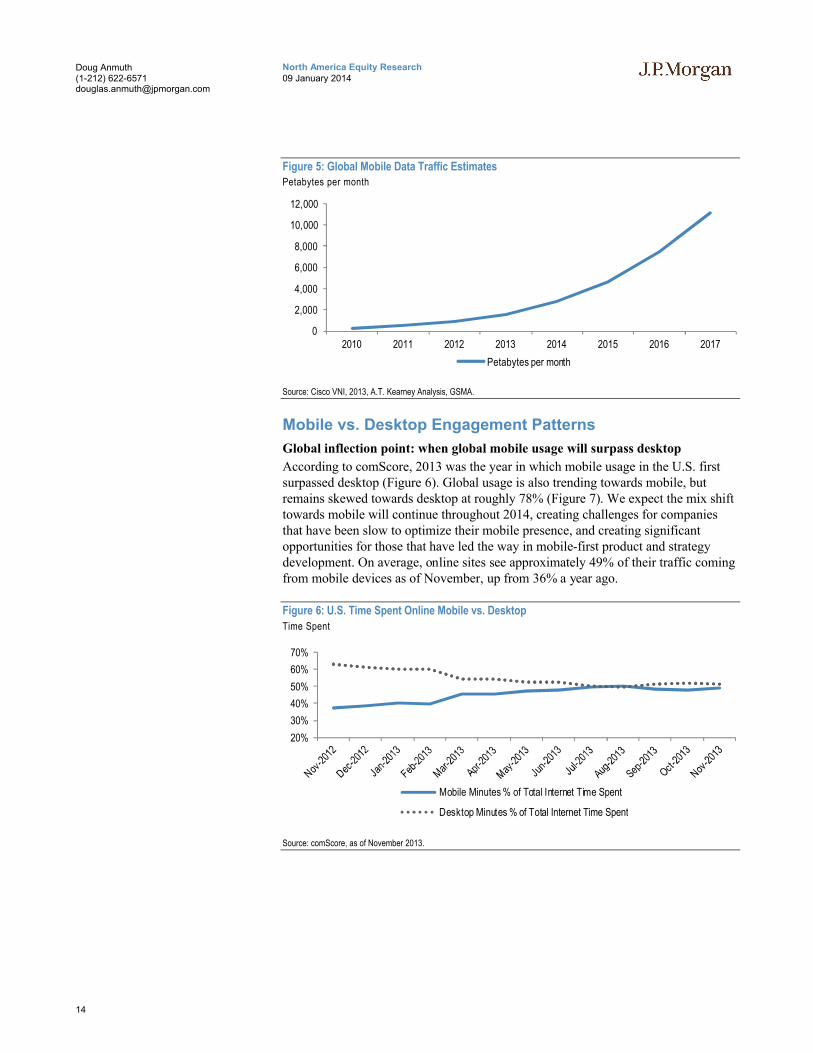

Figure 5: Global Mobile Data Traffic EstimatesPetabytes per month

0

2,000

4,000

6,000

8,000

10,000

12,000

2010 2011 2012 2013 2014 2015 2016 2017

Petabytes per month

Source: Cisco VNI, 2013, A.T. Kearney Analysis, GSMA.

Mobile vs. Desktop Engagement Patterns

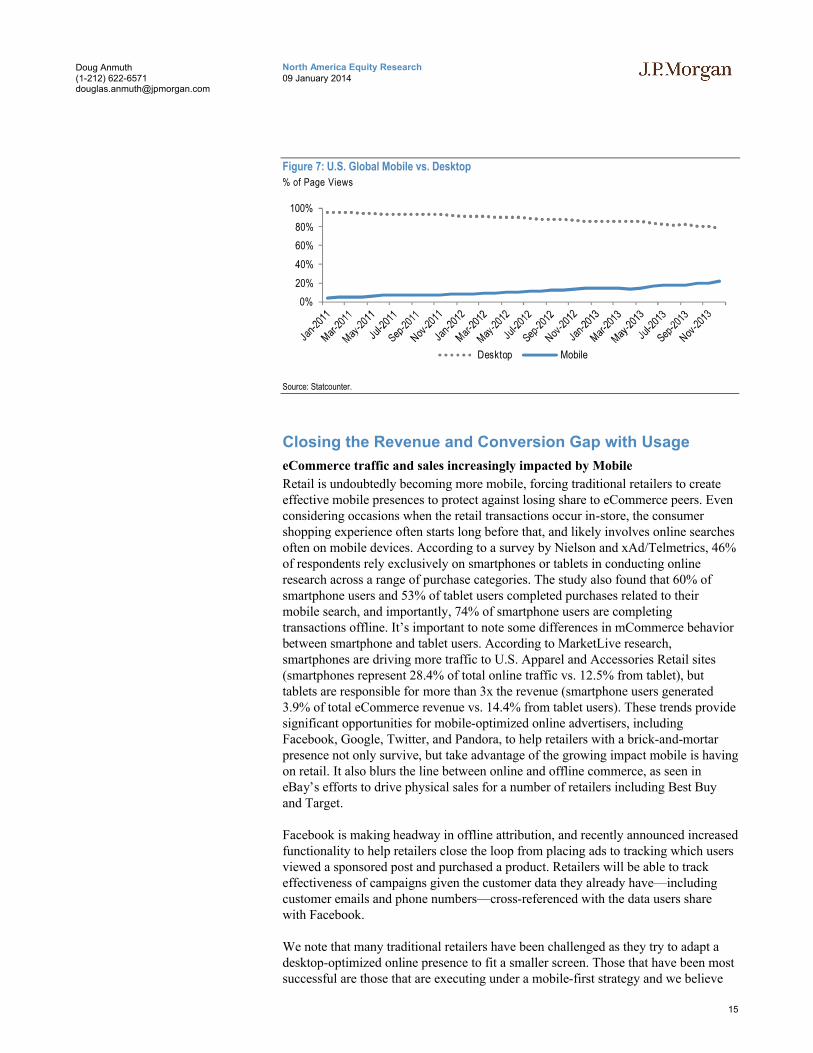

Global inflection point: when global mobile usage will surpass desktop

According to comScore, 2013 was the year in which mobile usage in the U.S. first surpassed desktop (Figure 6). Global usage is also trending towards mobile, but remains skewed towards desktop at roughly 78% (Figure 7). We expect the mix shift towards mobile will continue throughout 2014, creating challenges for companies that have been slow to optimize their mobile presence, and creating significant opportunities for those that have led the way in mobile-first product and strategy development. On average, online sites see approximately 49% of their traffic coming from mobile devices as of November, up from 36% a year ago.

Figure 6: U.S. Time Spent Online Mobile vs. Desktop

Time Spent

20%

30%

40%

50%

60%

70%

Mobile Minutes % of Total Internet Time Spent

Desktop Minutes % of Total Internet Time Spent

Source: comScore, as of November 2013.

15

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Figure 7: U.S. Global Mobile vs. Desktop

% of Page Views

0%

20%

40%

60%

80%

100%

Desktop Mobile

Source: Statcounter.

Closing the Revenue and Conversion Gap with Usage

eCommerce traffic and sales increasingly impacted by Mobile

Retail is undoubtedly becoming more mobile, forcing traditional retailers to create effective mobile presences to protect against losing share to eCommerce peers. Even considering occasions when the retail transactions occur in-store, the consumer shopping experience often starts long before that, and likely involves online searches often on mobile devices. According to a survey by Nielson and xAd/Telmetrics, 46% of respondents rely exclusively on smartphones or tablets in conducting online research across a range of purchase categories. The study also found that 60% of smartphone users and 53% of tablet users completed purchases related to their mobile search, and importantly, 74% of smartphone users are completing transactions offline. It’s important to note some differences in mCommerce behavior between smartphone and tablet users. According to MarketLive research,smartphones are driving more traffic to U.S. Apparel and Accessories Retail sites (smartphones represent 28.4% of total online traffic vs. 12.5% from tablet), but tablets are responsible for more than 3x the revenue (smartphone users generated 3.9% of total eCommerce revenue vs. 14.4% from tablet users). These trends provide significant opportunities for mobile-optimized online advertisers, including Facebook, Google, Twitter, and Pandora, to help retailers with a brick-and-mortar presence not only survive, but take advantage of the growing impact mobile is having on retail. It also blurs the line between online and offline commerce, as seen in eBay’s efforts to drive physical sales for a number of retailers including Best Buy and Target.

Facebook is making headway in offline attribution, and recently announced increased functionality to help retailers close the loop from placing ads to tracking which users viewed a sponsored post and purchased a product. Retailers will be able to track effectiveness of campaigns given the customer data they already have—including customer emails and phone numbers—cross-referenced with the data users share with Facebook.

We note that many traditional retailers have been challenged as they try to adapt a desktop-optimized online presence to fit a smaller screen. Those that have been most successful are those that are executing under a mobile-first strategy and we believe

16

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

2014 will be another year of mobile-first product roll-outs and mobile-optimized online presence. We highlight Groupon as an eCommerce company driven by mobilegiven 60M+ cumulative app downloads and 50%+ of North American transactions occurring on mobile.

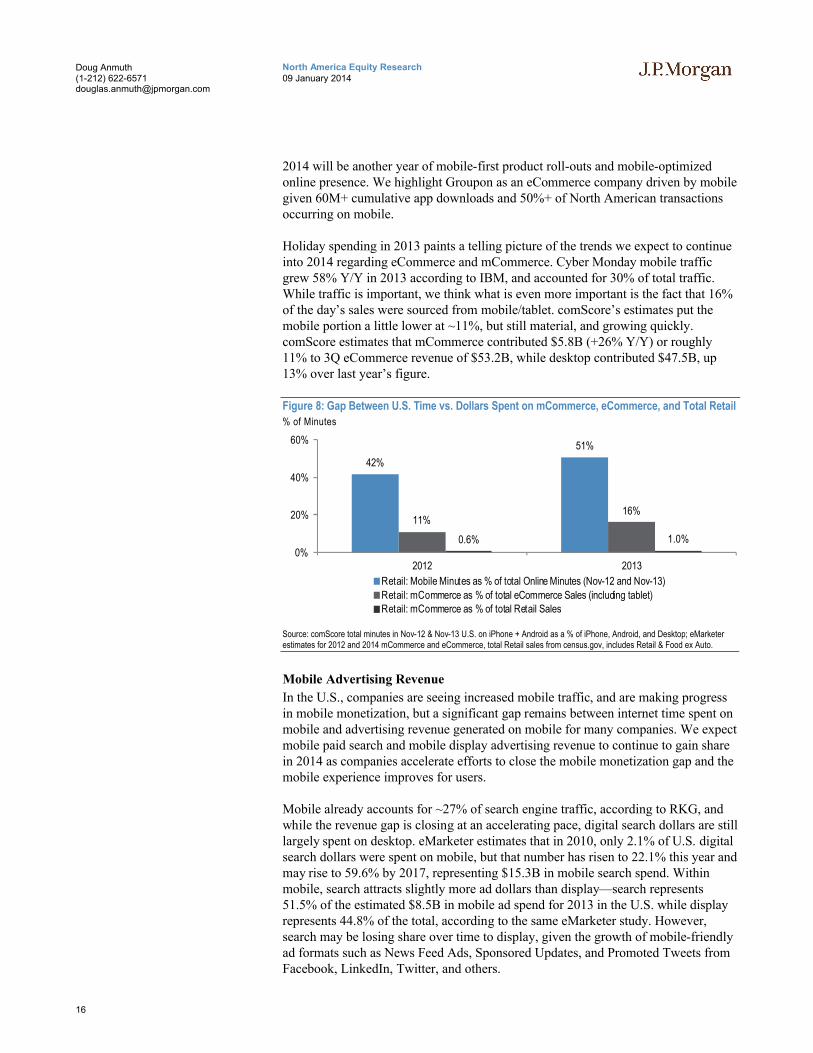

Holiday spending in 2013 paints a telling picture of the trends we expect to continue into 2014 regarding eCommerce and mCommerce. Cyber Monday mobile traffic grew 58% Y/Y in 2013 according to IBM, and accounted for 30% of total traffic. While traffic is important, we think what is even more important is the fact that 16% of the day’s sales were sourced from mobile/tablet. comScore’s estimates put the mobile portion a little lower at ~11%, but still material, and growing quickly. comScore estimates that mCommerce contributed $5.8B (+26% Y/Y) or roughly 11% to 3Q eCommerce revenue of $53.2B, while desktop contributed $47.5B, up 13% over last year’s figure.

Figure 8: Gap Between U.S. Time vs. Dollars Spent on mCommerce, eCommerce, and Total Retail

% of Minutes

42%

51%

11%16%

0.6% 1.0%0%

20%

40%

60%

2012 2013

Retail: Mobile Minutes as % of total Online Minutes (Nov-12 and Nov-13)

Retail: mCommerce as % of total eCommerce Sales (including tablet)Retail: mCommerce as % of total Retail Sales

Source: comScore total minutes in Nov-12 & Nov-13 U.S. on iPhone + Android as a % of iPhone, Android, and Desktop; eMarketer estimates for 2012 and 2014 mCommerce and eCommerce, total Retail sales from census.gov, includes Retail & Food ex Auto.

Mobile Advertising Revenue

In the U.S., companies are seeing increased mobile traffic, and are making progress in mobile monetization, but a significant gap remains between internet time spent on mobile and advertising revenue generated on mobile for many companies. We expect mobile paid search and mobile display advertising revenue to continue to gain share in 2014 as companies accelerate efforts to close the mobile monetization gap and the mobile experience improves for users.

Mobile already accounts for ~27% of search engine traffic, according to RKG, and while the revenue gap is closing at an accelerating pace, digital search dollars are still largely spent on desktop. eMarketer estimates that in 2010, only 2.1% of U.S. digital search dollars were spent on mobile, but that number has risen to 22.1% this year and may rise to 59.6% by 2017, representing $15.3B in mobile search spend. Within mobile, search attracts slightly more ad dollars than display—search represents 51.5% of the estimated $8.5B in mobile ad spend for 2013 in the U.S. while display represents 44.8% of the total, according to the same eMarketer study. However, search may be losing share over time to display, given the growth of mobile-friendly ad formats such as News Feed Ads, Sponsored Updates, and Promoted Tweets from Facebook, LinkedIn, Twitter, and others.

17

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

We believe Pandora is a compelling pure-play mobile advertising company for which usage is ~80% mobile. In 3QFY14, 73% of the company’s advertising revenue came from mobile. Given that the company’s product is an audio experience, the business model lends itself well to mobile advertising, where the user interaction with an ad is no different on desktop and mobile. Audio ads are interruptive and Pandora’s targetability is high given user-reported information. We believe that Pandora is at an inflection point on monetization driven by its market share gains, buy-side platform integration, and expanding sales efforts.

Facebook has also emerged as a leader in monetizing mobile usage; increasing the ad load in the News Feed has been an important driver of the company’s ad revenue growth in 2013, but we believe that users, engagement, and ad quality/pricing have also been significant monetization drivers and will be more important drivers of mobile advertising growth in 2014. Facebook indicated that it expects slowing growth in ad load (i.e., % of News Feed stories that are ads) going forward and that future monetization gains are likely to be driven by ad-quality improvements. The company also indicated that mobile ad load increased modestly from 2Q to 3Q while desktop News Feed ad load increased to a somewhat greater extent. We note that Facebook’s 3Q Mobile revenue grew 34% Q/Q despite relatively modest ad load increases, suggesting users, usage, and ad-quality improvements can continue to drive strong revenue growth going forward. We believe managing ad load is important to maintaining the user experience for the long term and we think higher ad prices can be driven by continued increases in News Feed ad demand and quality, along with FBX in the Mobile News Feed and auto-play video ads.

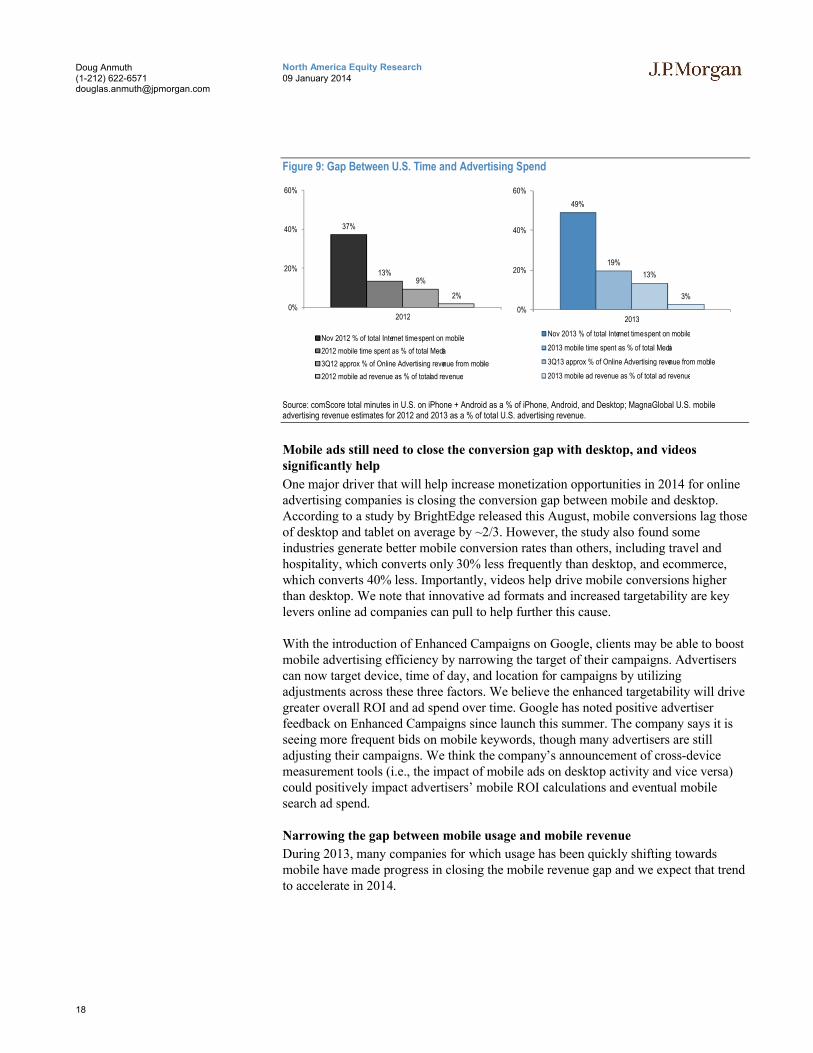

The figure below demonstrates the gap between total online time spent in the U.S. on mobile devices (excluding tablet) relative to the approximate portion of online and total advertising revenue allocated to mobile advertising in 2012 and 2013. Importantly, while monetization improved this year, the gap between mobile time spent and mobile advertising spend has widened as mobile usage growth has been relatively faster. We expect companies to make more progress on closing the gap in 2014, aided by increased targetability, including further adoption of Google’s Enhanced Campaigns device bid adjuster, and expanded and enhanced ad formats focused on increasing mobile advertising ROI.

18

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Figure 9: Gap Between U.S. Time and Advertising Spend

49%

19%

13%

3%

0%

20%

40%

60%

2013

Nov 2013 % of total Internet time spent on mobile

2013 mobile time spent as % of total Media

3Q13 approx % of Online Advertising revenue from mobile

2013 mobile ad revenue as % of total ad revenue

37%

13%9%

2%

0%

20%

40%

60%

2012

Nov 2012 % of total Internet time spent on mobile

2012 mobile time spent as % of total Media

3Q12 approx % of Online Advertising revenue from mobile

2012 mobile ad revenue as % of total ad revenue

Source: comScore total minutes in U.S. on iPhone + Android as a % of iPhone, Android, and Desktop; MagnaGlobal U.S. mobile advertising revenue estimates for 2012 and 2013 as a % of total U.S. advertising revenue.

Mobile ads still need to close the conversion gap with desktop, and videos significantly help

One major driver that will help increase monetization opportunities in 2014 for online advertising companies is closing the conversion gap between mobile and desktop. According to a study by BrightEdge released this August, mobile conversions lag those of desktop and tablet on average by ~2/3. However, the study also found some industries generate better mobile conversion rates than others, including travel and hospitality, which converts only 30% less frequently than desktop, and ecommerce, which converts 40% less. Importantly, videos help drive mobile conversions higher than desktop. We note that innovative ad formats and increased targetability are key levers online ad companies can pull to help further this cause.

With the introduction of Enhanced Campaigns on Google, clients may be able to boost mobile advertising efficiency by narrowing the target of their campaigns. Advertisers can now target device, time of day, and location for campaigns by utilizing adjustments across these three factors. We believe the enhanced targetability will drive greater overall ROI and ad spend over time. Google has noted positive advertiser feedback on Enhanced Campaigns since launch this summer. The company says it is seeing more frequent bids on mobile keywords, though many advertisers are still adjusting their campaigns. We think the company’s announcement of cross-device measurement tools (i.e., the impact of mobile ads on desktop activity and vice versa) could positively impact advertisers’ mobile ROI calculations and eventual mobilesearch ad spend.

Narrowing the gap between mobile usage and mobile revenue

During 2013, many companies for which usage has been quickly shifting towards mobile have made progress in closing the mobile revenue gap and we expect that trend to accelerate in 2014.

19

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

We note that Pandora and Facebook are companies that stand out in achieving superior mobile monetization, making significant progress in closing the gap. These companies have been able to generate increased mobile advertising demand from higher-quality advertisers. Given the data these companies possess and innovation in mobile ad formats, they have benefited from a mix of pricing and volume increases. For example, Pandora’s video and audio ads command premium pricing to mobile display ads with CPMs in the $15-$25, $8-$12, and $5-$7 range, respectively. We expect these companies to continue to make progress towards mobile monetization and usage equality in 2014. We also highlight companies with significant potential to close larger monetization gaps, including Google. We believe Google has the targetability data, engagement, and ad tech innovation including Enhanced Campaigns to make material progress in closing its monetization gap in 2014.

20

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

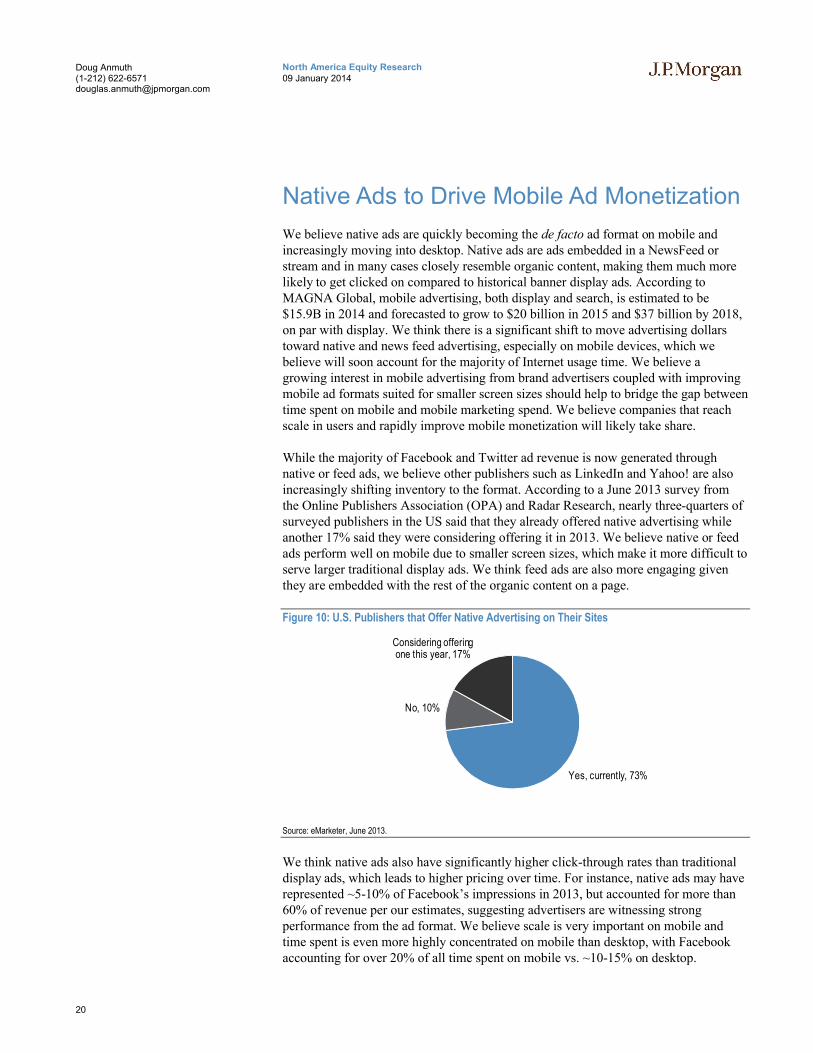

Native Ads to Drive Mobile Ad Monetization

We believe native ads are quickly becoming the de facto ad format on mobile and increasingly moving into desktop. Native ads are ads embedded in a NewsFeed or stream and in many cases closely resemble organic content, making them much more likely to get clicked on compared to historical banner display ads. According to MAGNA Global, mobile advertising, both display and search, is estimated to be $15.9B in 2014 and forecasted to grow to $20 billion in 2015 and $37 billion by 2018, on par with display. We think there is a significant shift to move advertising dollars toward native and news feed advertising, especially on mobile devices, which we believe will soon account for the majority of Internet usage time. We believe a growing interest in mobile advertising from brand advertisers coupled with improving mobile ad formats suited for smaller screen sizes should help to bridge the gap between time spent on mobile and mobile marketing spend. We believe companies that reach scale in users and rapidly improve mobile monetization will likely take share.

While the majority of Facebook and Twitter ad revenue is now generated through native or feed ads, we believe other publishers such as LinkedIn and Yahoo! are also increasingly shifting inventory to the format. According to a June 2013 survey from the Online Publishers Association (OPA) and Radar Research, nearly three-quarters of surveyed publishers in the US said that they already offered native advertising while another 17% said they were considering offering it in 2013. We believe native or feedads perform well on mobile due to smaller screen sizes, which make it more difficult to serve larger traditional display ads. We think feed ads are also more engaging given they are embedded with the rest of the organic content on a page.

Figure 10: U.S. Publishers that Offer Native Advertising on Their Sites

Yes, currently, 73%

No, 10%

Considering offering one this year, 17%

Source: eMarketer, June 2013.

We think native ads also have significantly higher click-through rates than traditional display ads, which leads to higher pricing over time. For instance, native ads may have represented ~5-10% of Facebook’s impressions in 2013, but accounted for more than 60% of revenue per our estimates, suggesting advertisers are witnessing strong performance from the ad format. We believe scale is very important on mobile and time spent is even more highly concentrated on mobile than desktop, with Facebook accounting for over 20% of all time spent on mobile vs. ~10-15% on desktop.

21

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Overall, we believe Twitter is in a similar position in monetization as Facebook was a bit more than a year ago when it had just turned on news feed ads across both desktop and mobile. That is to say the basic products are there and still being developed, and we believe it is early in building advertiser demand in the platform. However, we are clearly bullish on the shift of dollars toward news feed ads, particularly on mobile devices, and we expect Twitter to realize significant ARPU gains over time.

Twitter offers advertisers some basic re-targeting and programmatic capabilities today, though the company does not offer advertisers the ability to bid on individual impressions in real-time. We believe the addition of Twitter ad inventory on the MoPub Marketplace (i.e., MoPub’s ad exchange) should significantly accelerate Twitter’s efforts in RTB and drive higher monetization and ad pricing over time. We expect strong demand for Twitter’s RTB products from direct response advertisers but also from brand advertisers over time, and we note Facebook continues to witness strong demand for FBX (Facebook Exchange) ads both in the Desktop News Feed aswell as its Desktop Right Rail, and we expect FBX to soon move to mobile.

Twitter launched Promoted Tweets in the Timeline in April 2010. This was an early form of news feed advertising that was soon adopted by other companies. Facebook launched Sponsored Stories in the News Feed in January 2012 for the desktop and in March 2012 for mobile devices.

We believe LinkedIn is also making good progress with its Sponsored Content native ads. More than 1,000 advertisers are running Sponsored Updates, a single-digit percentage of LinkedIn advertisers on any given day. We believe the Sponsored Update ad load is running at around a mid-single-digit percentage of total pieces of content in the newsfeed. Also, similar to what can been seen at Facebook, Sponsored Updates have higher click-through rates, particularly on mobile, which currently accounts for 2/3 of LinkedIn’s Sponsored Updates revenue. LinkedIn noted that sponsored jobs in the feed have performed particularly well. We believe Sponsored Updates eCPMs are already higher than for LinkedIn’s traditional display ads and pricing should increase more as advertiser demand in the platform begins to build.

22

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Cross-Device Advertising and Attribution Becoming Critical

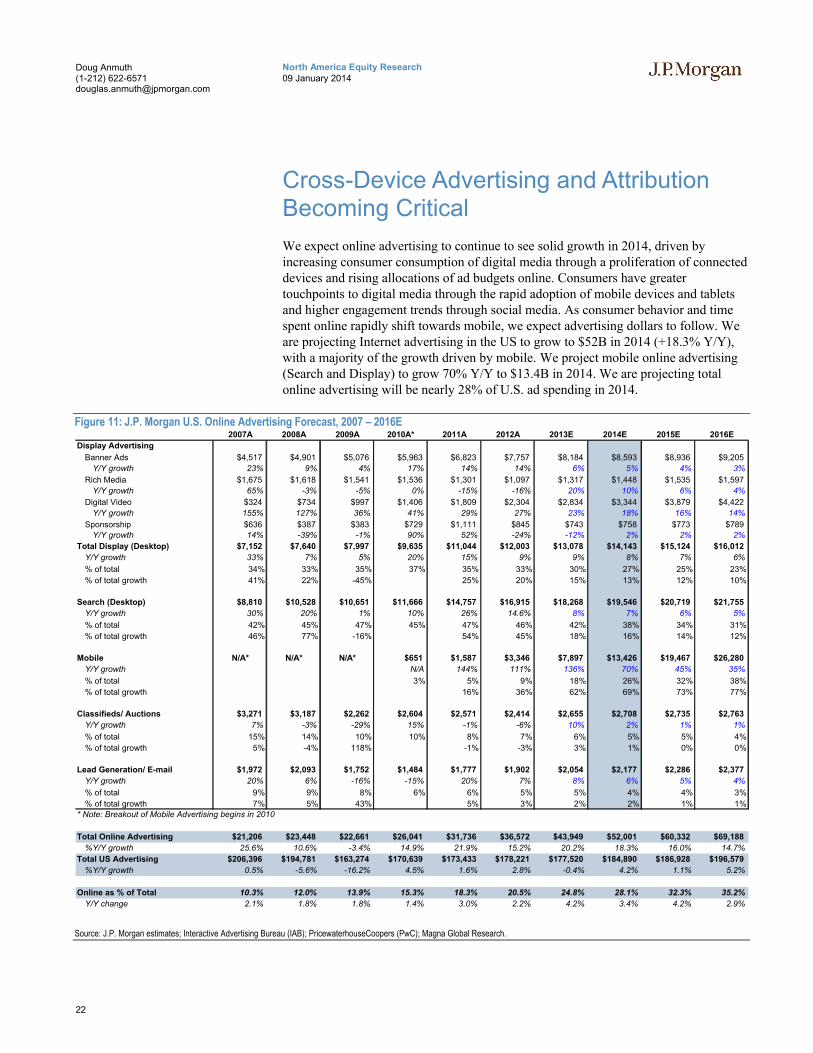

We expect online advertising to continue to see solid growth in 2014, driven by increasing consumer consumption of digital media through a proliferation of connected devices and rising allocations of ad budgets online. Consumers have greater touchpoints to digital media through the rapid adoption of mobile devices and tablets and higher engagement trends through social media. As consumer behavior and time spent online rapidly shift towards mobile, we expect advertising dollars to follow. We are projecting Internet advertising in the US to grow to $52B in 2014 (+18.3% Y/Y), with a majority of the growth driven by mobile. We project mobile online advertising (Search and Display) to grow 70% Y/Y to $13.4B in 2014. We are projecting total online advertising will be nearly 28% of U.S. ad spending in 2014.

Figure 11: J.P. Morgan U.S. Online Advertising Forecast, 2007 – 2016E2007A 2008A 2009A 2010A* 2011A 2012A 2013E 2014E 2015E 2016E

Display Advertising

Banner Ads $4,517 $4,901 $5,076 $5,963 $6,823 $7,757 $8,184 $8,593 $8,936 $9,205

Y/Y growth 23% 9% 4% 17% 14% 14% 6% 5% 4% 3%

Rich Media $1,675 $1,618 $1,541 $1,536 $1,301 $1,097 $1,317 $1,448 $1,535 $1,597

Y/Y growth 65% -3% -5% 0% -15% -16% 20% 10% 6% 4%

Digital Video $324 $734 $997 $1,406 $1,809 $2,304 $2,834 $3,344 $3,879 $4,422

Y/Y growth 155% 127% 36% 41% 29% 27% 23% 18% 16% 14%

Sponsorship $636 $387 $383 $729 $1,111 $845 $743 $758 $773 $789

Y/Y growth 14% -39% -1% 90% 52% -24% -12% 2% 2% 2%

Total Display (Desktop) $7,152 $7,640 $7,997 $9,635 $11,044 $12,003 $13,078 $14,143 $15,124 $16,012

Y/Y growth 33% 7% 5% 20% 15% 9% 9% 8% 7% 6%

% of total 34% 33% 35% 37% 35% 33% 30% 27% 25% 23%

% of total growth 41% 22% -45% 25% 20% 15% 13% 12% 10%

Search (Desktop) $8,810 $10,528 $10,651 $11,666 $14,757 $16,915 $18,268 $19,546 $20,719 $21,755

Y/Y growth 30% 20% 1% 10% 26% 14.6% 8% 7% 6% 5%

% of total 42% 45% 47% 45% 47% 46% 42% 38% 34% 31%

% of total growth 46% 77% -16% 54% 45% 18% 16% 14% 12%

Mobile N/A* N/A* N/A* $651 $1,587 $3,346 $7,897 $13,426 $19,467 $26,280

Y/Y growth N/A 144% 111% 136% 70% 45% 35%

% of total 3% 5% 9% 18% 26% 32% 38%

% of total growth 16% 36% 62% 69% 73% 77%

Classifieds/ Auctions $3,271 $3,187 $2,262 $2,604 $2,571 $2,414 $2,655 $2,708 $2,735 $2,763

Y/Y growth 7% -3% -29% 15% -1% -6% 10% 2% 1% 1%

% of total 15% 14% 10% 10% 8% 7% 6% 5% 5% 4%

% of total growth 5% -4% 118% -1% -3% 3% 1% 0% 0%

Lead Generation/ E-mail $1,972 $2,093 $1,752 $1,484 $1,777 $1,902 $2,054 $2,177 $2,286 $2,377

Y/Y growth 20% 6% -16% -15% 20% 7% 8% 6% 5% 4%

% of total 9% 9% 8% 6% 6% 5% 5% 4% 4% 3%

% of total growth 7% 5% 43% 5% 3% 2% 2% 1% 1%

* Note: Breakout of Mobile Advertising begins in 2010

Total Online Advertising $21,206 $23,448 $22,661 $26,041 $31,736 $36,572 $43,949 $52,001 $60,332 $69,188

%Y/Y growth 25.6% 10.6% -3.4% 14.9% 21.9% 15.2% 20.2% 18.3% 16.0% 14.7%

Total US Advertising $206,396 $194,781 $163,274 $170,639 $173,433 $178,221 $177,520 $184,890 $186,928 $196,579

%Y/Y growth 0.5% -5.6% -16.2% 4.5% 1.6% 2.8% -0.4% 4.2% 1.1% 5.2%

Online as % of Total 10.3% 12.0% 13.9% 15.3% 18.3% 20.5% 24.8% 28.1% 32.3% 35.2%

Y/Y change 2.1% 1.8% 1.8% 1.4% 3.0% 2.2% 4.2% 3.4% 4.2% 2.9%

Source: J.P. Morgan estimates; Interactive Advertising Bureau (IAB); PricewaterhouseCoopers (PwC); Magna Global Research.

23

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Advertising continues to shift online and, as people spend more time on various devices at different times of the day at different locations, advertisers are looking for ways to reach consumers at multiple touchpoints throughout the day. We believe there is less of an emphasis on desktop vs. mobile and a greater focus on the right context. There is less separation of usage times across various devices, as seen in the figure below. A typical Internet user is on several devices simultaneously throughout the day and now second or even third screen experiences are fairly constant. We believe it is critical for advertisers to use new tools to target their advertising effectively and they need to be able to track/measure behavior across devices as users are on multiple devices throughout the day. Several of the largest online advertisers have already begun shifting their products in this direction, particularly the companies for which users are and can be logged in across various devices and services. As shown in Figure 12 below, mobile phone and tablet activity spikes in the evening hours.

Figure 12: Share of Daily Traffic by Device

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

12:00 AM 4:00 AM 8:00 AM 12:00 PM 4:00 PM 8:00 PM

Sh

are

of

Dai

ly D

evic

e Tr

affic

Tablet Mobile Computer

Source: comScore.

Google launches Estimated Cross-Device Conversions

In November 2013, Google launched Estimated Cross-Device Conversions (ECDC) in AdWords as a part of the new Estimated Total Conversions (ETC) product. Other products to come in the ETC series will include phone calls and in-store visits. ECDC is aimed at providing advertisers with data to reflect the impact of an advertiser’s campaigns across various devices. This is a natural progression of Google’s holistic perspective of online advertising that is highlighted in Enhanced Campaigns. Enhanced Campaigns allow advertisers to reach users on all devices through a single AdWords campaign where the context of the user is of greater focus rather than just looking at which device they are using. Through ETC products, Google is creating analytics tools to measure conversions that start with an AdWords click that leads to a transaction completed on any device, on the phone, or in-store.

Google estimates ECDC based on aggregate data from users who are signed into the Google accounts across multiple devices, which is used to create an anonymous and aggregate estimate for the number of cross-device conversions attributed to AdWords.

24

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

ECDC uses last paid click attribution so that the conversions are attributed to the ad that was last clicked before the transaction, lead submission, or other call to action was placed. Google currently calculates ECDC for conversion paths that start from a Google search but the company is looking for ways to capture cross-device conversions from display and other search networks. In early tests, Google reported that the entertainment vertical saw the largest increase of conversions at 12%, travel and technology at 8%, retail at 7%, and local at 2%. Going forward, we expect Google to continue to add additional tools for other conversion types such as phone calls and in-store visits. Early checks with SEMs suggest some advertisers using ECDC are seeing an increase in conversions as high as 33%.

Facebook expected to further enable cross-device targeting

Facebook is another online platform where users are signed in across multiple devices. Though not yet available, Facebook Exchange (FBX) ads will soon become available in the mobile News Feed, we believe. As a reminder, FBX enables real-time bidding driven by advertisers’ cookie-based data rather than simply targeting through broad demographics or interests. We believe the incorporation of FBX ads into Facebook’s mobile News Feed will be material. For example, if a user visits an online travel site at work on a desktop but leaves before the check-out process, that OTA can re-target the same user on Facebook with additional messages or offers when they check their mobile app later at home.

Facebook also offers Custom Audiences, a product that allows advertisers to upload customer information gathered from their offline customers such as emails, user IDs, or phone numbers and target them on Facebook. We are encouraged that Facebook’s ability to leverage third-party data through the Facebook Exchange (FBX) and Custom Audiences can drive improvements in yield. Third-party data through FBX and Custom Audiences pushes Facebook further down the purchase funnel, driving higher ROI and ad spend. We look for further investments and advertiser tools to further enable these actions in 2014.

Twitter launches retargeting with Tailored Audiences

Twitter rolled out Tailored Audiences (TA) globally in November 2013. TA enables ad retargeting on Twitter’s platform using user behavior on other websites. Since the beta test began in July, Twitter has reported seeing strong results. HubSpot reported seeing a 45% lift in engagement rates, Krossover saw a 74% decrease in cost per customer acquisition (CPA), and New Relic saw 195% higher conversion rates. Ad partners that are helping Twitter with TA include Adara, AdRoll, BlueKai, Chango, DataXu, Dstillery, Lotame, Quantcast, ValueClick, and [x+1]. We believe retargeting will be an effective tool for Twitter’s advertisers given the platform’s advantage on mobile devices and we look for more dynamic cross-device ad targeting tools to come.

25

North America Equity Research09 January 2014

Doug Anmuth(1-212) [email protected]

Traditional Media Measurement Tools to Drive Traditional Media Dollars Online