Inside Debt and Bank Performance During the Financial Crisis DNB 2012 Sjoerd van Bekkum.

22

Inside Debt and Bank Performance During the Financial Crisis DNB 2012 Sjoerd van Bekkum

-

Upload

posy-flynn -

Category

Documents

-

view

216 -

download

2

Transcript of Inside Debt and Bank Performance During the Financial Crisis DNB 2012 Sjoerd van Bekkum.

Inside Debt and Bank Performance During the Financial Crisis

DNB 2012 Sjoerd van Bekkum

Initiatives to reduce excessive risk taking incentives after the crisis

Compensation Fairness Act 2009 Shareholders should approve pay Shareholders appoint compensation directors

Dodd-Frank Wall-Street Reform 2010 Shareholders should vote on pay Shareholders can design their own pay proposals

G20’s FSB Sound Compensation Practices 2009“Engage shareholders with compensation”50% of variable pay should be awarded in shares or share-linked instruments

All shareholder-based!2

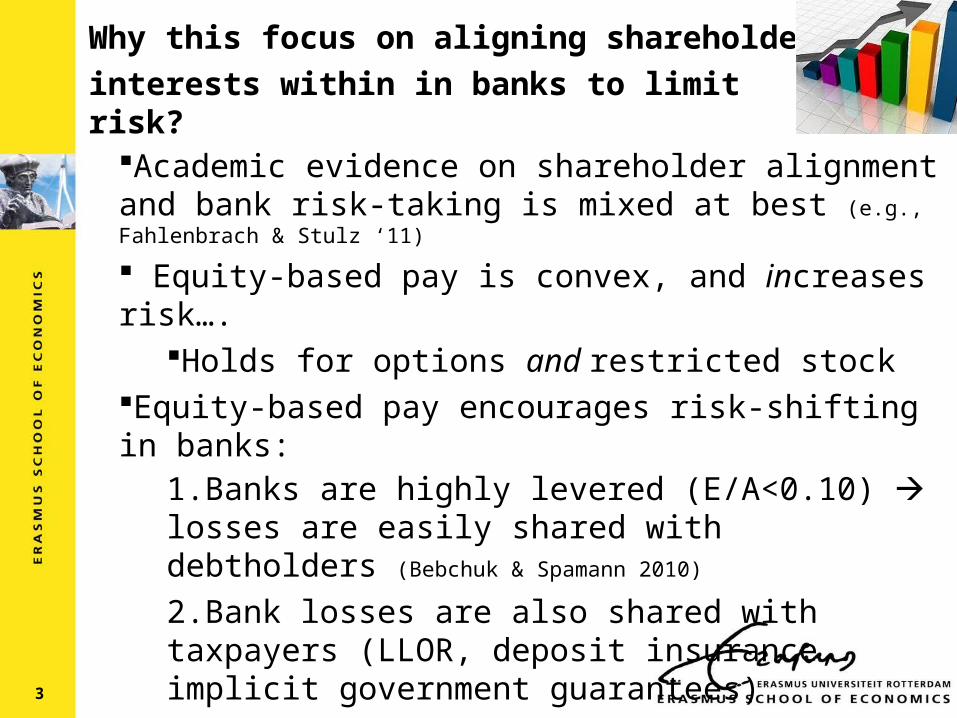

Why this focus on aligning shareholder

interests within in banks to limit risk?

Academic evidence on shareholder alignment and bank risk-taking is mixed at best (e.g., Fahlenbrach & Stulz ‘11)

Equity-based pay is convex, and increases risk…. Holds for options and restricted stock

Equity-based pay encourages risk-shifting in banks:1.Banks are highly levered (E/A<0.10) losses are easily shared with debtholders (Bebchuk & Spamann 2010)

2.Bank losses are also shared with taxpayers (LLOR, deposit insurance, implicit government guarantees)

if executive’s actions are unobserved, she will shift risk to taxpayers and other debtholders (Bolton et al. 2006)

3

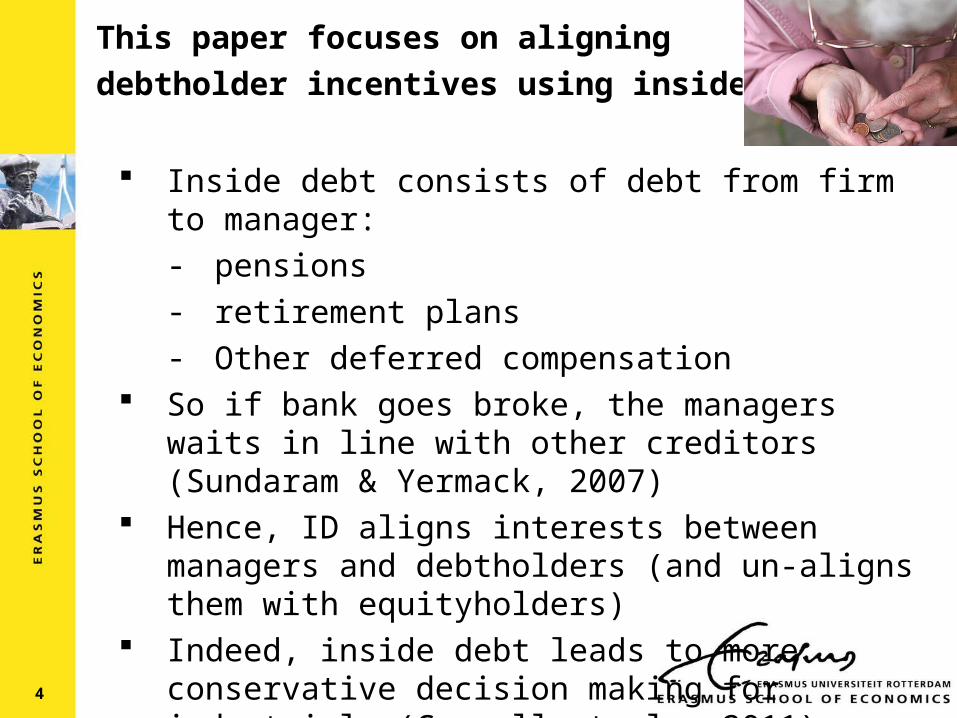

This paper focuses on aligning

debtholder incentives using inside debt

Inside debt consists of debt from firm to manager:- pensions - retirement plans - Other deferred compensation

So if bank goes broke, the managers waits in line with other creditors (Sundaram & Yermack, 2007)

Hence, ID aligns interests between managers and debtholders (and un-aligns them with equityholders)

Indeed, inside debt leads to more conservative decision making for industrials (Cassell et al., 2011)

4

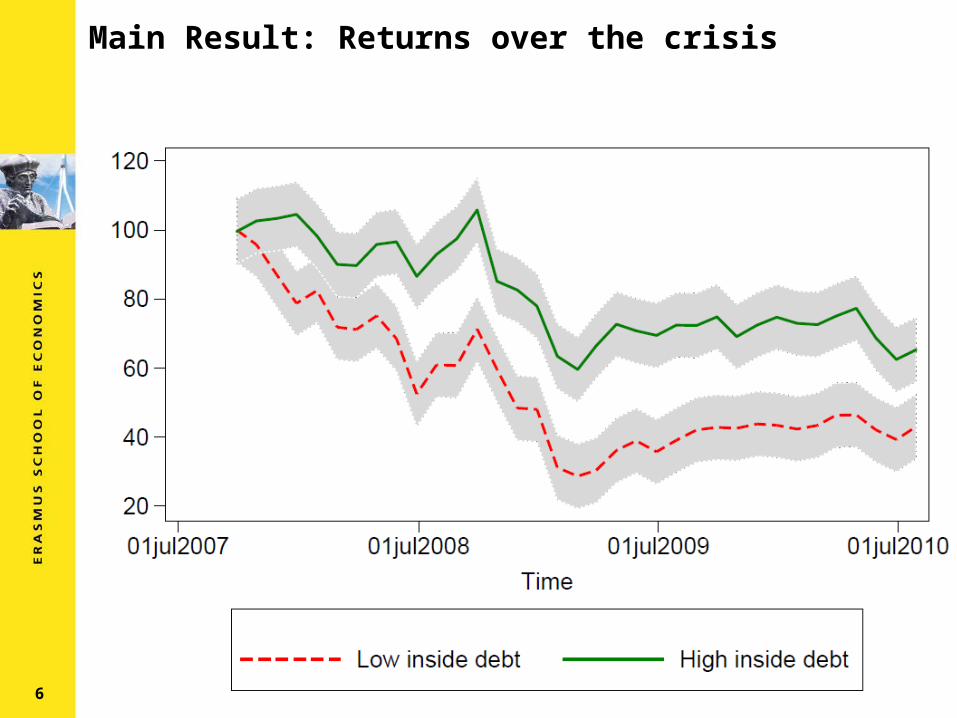

Inside debt encourages conservatismwhich pays off during bad times:

1.Shareholder implications:More inside debt better returns during crisis

2.Debtholder implications:More inside debt less downside risk during crisis

3.Investment policy:More inside debt better quality asset portfolio

4.Financing policy:More inside debt less “outside” debt

5

Main Result: Returns over the crisis

6

Data

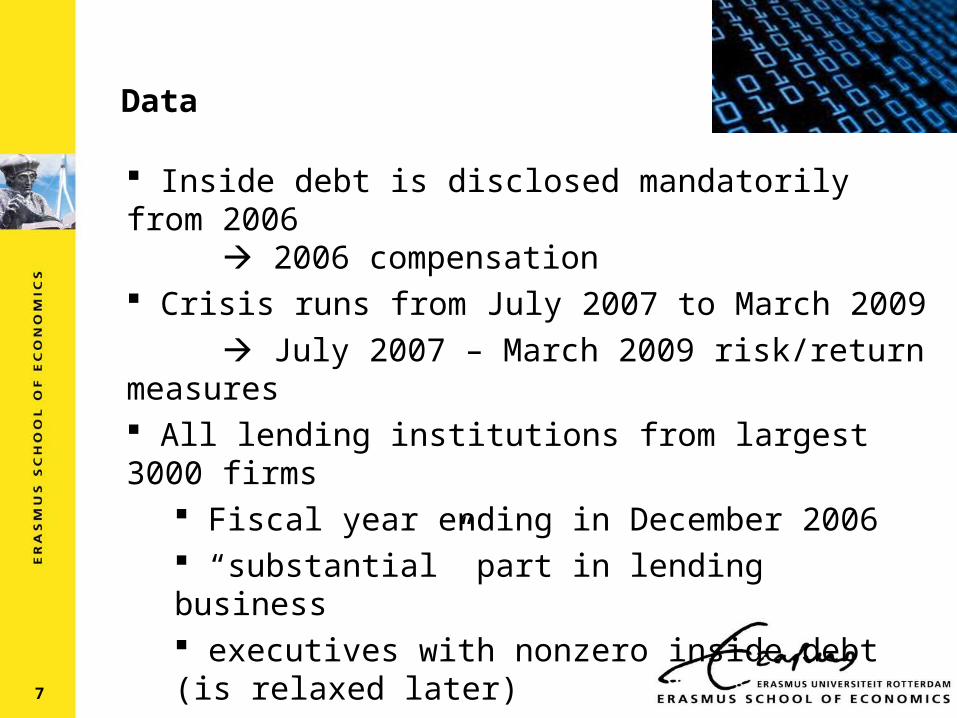

Inside debt is disclosed mandatorily from 2006 2006 compensation

Crisis runs from July 2007 to March 2009

July 2007 – March 2009 risk/return measures All lending institutions from largest 3000 firms

Fiscal year ending in December 2006 “substantial” part in lending business executives with nonzero inside debt (is relaxed later)

319 banks

7

Measuring enterprise-wide bank risk

Enterprise-wide bank risk: shareholders + debtholders No bonds/CDS data for most banks

Risk measures based on equity returns distribution

8 VaR

ESCoVaR

Volatility (T/S/I)

Measuring realized enterprise-wide bank risk

Enterprise-wide bank risk: shareholders + debtholders No bonds/CDS data for most banks

Risk measures based on equity returns distribution VaR Expected shortfall CoVaR Total / Systematic / Idiosyncratic volatility Prob(equity loss > 80%)

Risk-taking: Asset quality: % nonperforming assets ‘08Jan07-Jun07 repo growth

9

Measuring inside debt

Main idea (Jensen & Mecklin 1976): Optimally, manager’s D/E = firm’s D/E.

Measured in levels (Edmans & Liu 2011) and 1st differences (Wei & Yermack 2011)

10

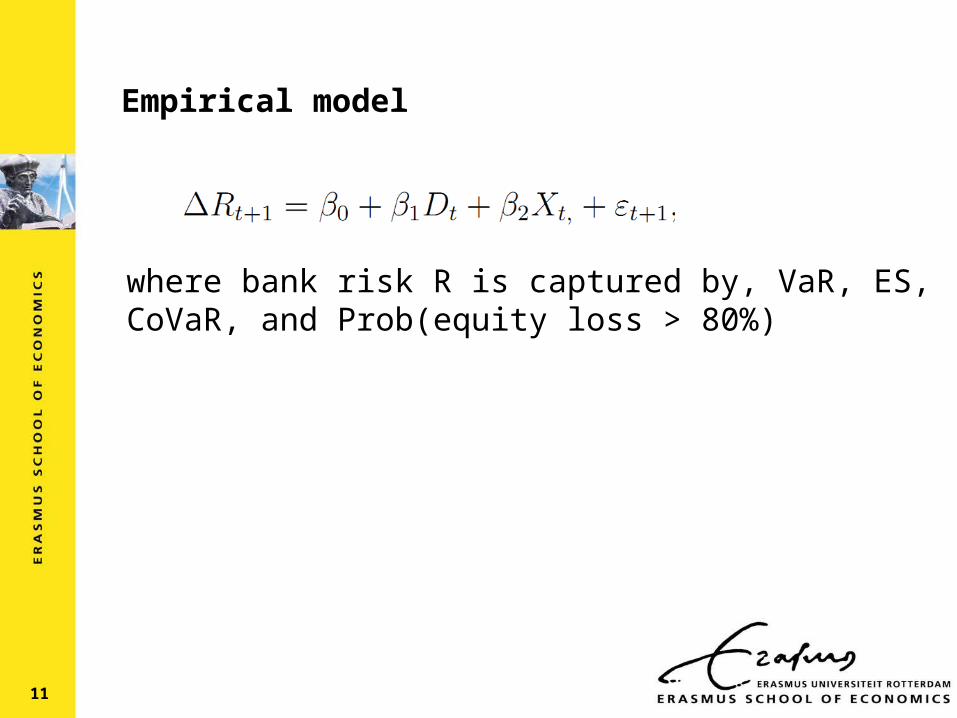

Empirical model

where bank risk R is captured by, VaR, ES, CoVaR, and Prob(equity loss > 80%)

11

Results:BHRs

12

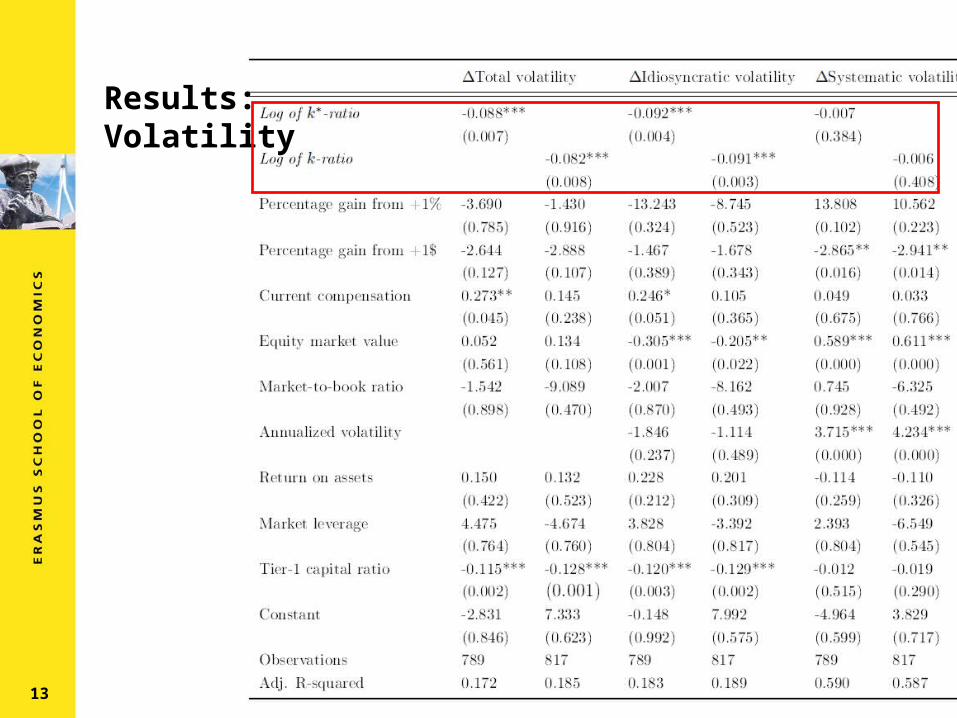

Results:Volatility

13

Results:

Enterprise-

Wide risk

14

Results:

Risk-taking

15

Endogeneity concerns

These findings are also consistent with:Inside debt being only awarded when expected future risk is low!

Risk is measured around unanticipated shock Impact of 2006 debt on 2007-2008 realized risks Accumulated pensions are stock, not flow

Inside debt is only awarded by banks operating in a stable environment

2006 volatility does not explain realized risks

inside debt discourages pre-crisis repo growthRe-estimation using IV:

16

Endogeneity concerns

Re-estimation using IV: Executive age (Fahlenbrach & Stulz; Sundaram & Yermack 2007) Size (exluding TBTF)Tax status (Sundaram & Yermack 2007) Maximum state tax rate (Anantharaman et al. 2010) Newly hired executive (Sundaram & Yermack 2007) Industry median inside debt (Murphy 1999) previous controls

17

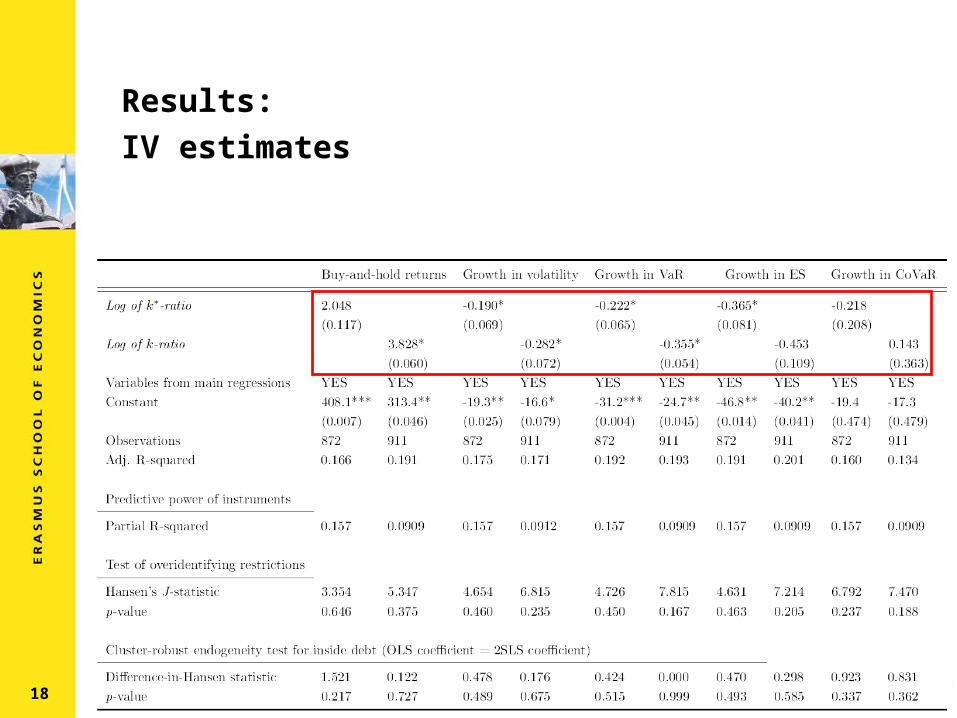

Results:

IV estimates

18

More alternative explanations:

I also do the following robustness checks: 10% of all banks disappear from sample

Adjust BHR for return after merger/delistingInclude executives without any inside debt

Create a 0/1 variable for whether sb has inside debt Re-estimate model on expanded sample

Presented estimates are at the executive level Results also hold at the CEO/CFO/bank level

Too-big-to-fail institutions might pay more inside debt

AND are less risky Results also hold without TBTF banks

19

Results: Robustness

20

Conclusion

Inside debt limits bank risk:• less negative returns• lower volatility and tail risk• discouragement of risk-taking

Power shift in governance from shareholders to debtholders limits risk

Inside debt less risk better performance during crises

Trade-off between upside potential and downside risk is beyond the scope of this paper But given that risk should be limited, inside debt might be a way to do it.

21

22