H1 17 INTERIM RESULTS - Bourse PLC_Slide...reduced interest on external borrowings ... Enables...

34

H1 17 INTERIM RESULTS 28 SEPTEMBER 2016

Transcript of H1 17 INTERIM RESULTS - Bourse PLC_Slide...reduced interest on external borrowings ... Enables...

H1 17 INTERIM

RESULTS

28 SEPTEMBER 2016

DEFINITIONS

1

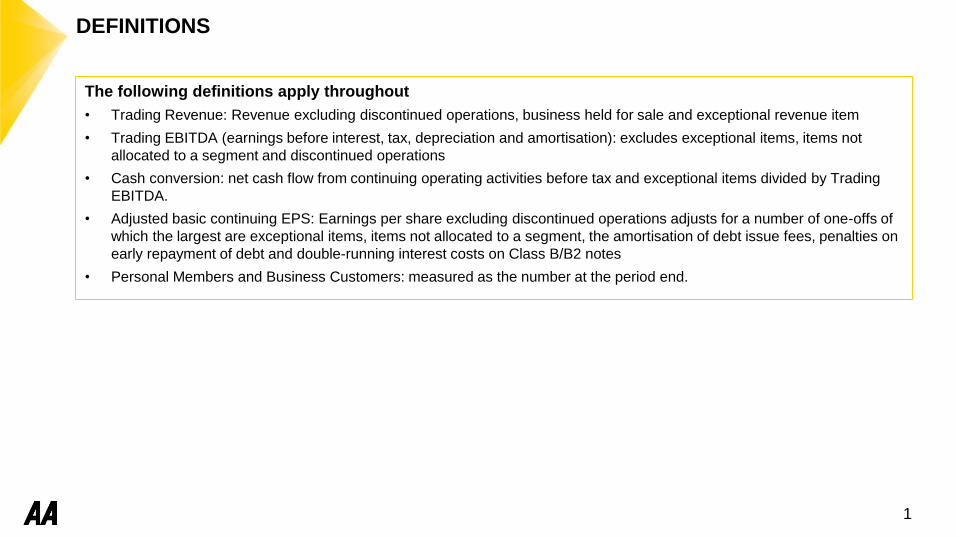

The following definitions apply throughout

• Trading Revenue: Revenue excluding discontinued operations, business held for sale and exceptional revenue item

• Trading EBITDA (earnings before interest, tax, depreciation and amortisation): excludes exceptional items, items not

allocated to a segment and discontinued operations

• Cash conversion: net cash flow from continuing operating activities before tax and exceptional items divided by Trading

EBITDA.

• Adjusted basic continuing EPS: Earnings per share excluding discontinued operations adjusts for a number of one-offs of

which the largest are exceptional items, items not allocated to a segment, the amortisation of debt issue fees, penalties on

early repayment of debt and double-running interest costs on Class B/B2 notes

• Personal Members and Business Customers: measured as the number at the period end.

Headlines Bob Mackenzie

Financials Martin Clarke

Strategy and outlook Bob Mackenzie

AGENDA

2

HIGHLIGHTS

GOOD PROGRESS TO DATE IN YEAR 2 OF THE TRANSFORMATION

Results in line with expectations

Transformation firmly on track

Ireland sold; £106m for debt pay down

Recommend interim dividend of 3.6p per share

TRANSFORMATION GAINING MOMENTUM

Growth in paid personal Members since April

Roadside retention up to 81%

App usage increased to 14% of personal

breakdowns

Productivity improved

Cost savings on target

IT investment on plan

Transformation capex – c. £10m saving

Normalised capex levels in sight

4

Transforming the AA into the UK’s pre-eminent Membership services organisation

FINANCIALS

In line with market expectations

FINANCIAL HEADLINES

6

Trading Revenue¹ up 2.2% at £467m despite IPT increase

• Roadside Trading revenue up 3.1% to £370m due to improved mix

Trading EBITDA¹ flat at £192m

• Roadside Trading EBITDA up 4.1% to £179m

Trading EBITDA margin¹ 41.1% (H1 16: 42.0%)

Adjusted EPS 10.3p (H1 16: 10.1p)

Cash conversion 99% (H1 16: 114%); Net debt of £2,677m³ (6.7x Trading EBITDA²)

post Ireland disposal in August

Interim dividend of 3.6p per share declared

¹ Excluding the Glass and Ireland businesses and exceptional revenue item ² Trading EBITDA for the last 12 months³ Net debt at 31 July 2016 plus the net proceeds from the sale of Ireland

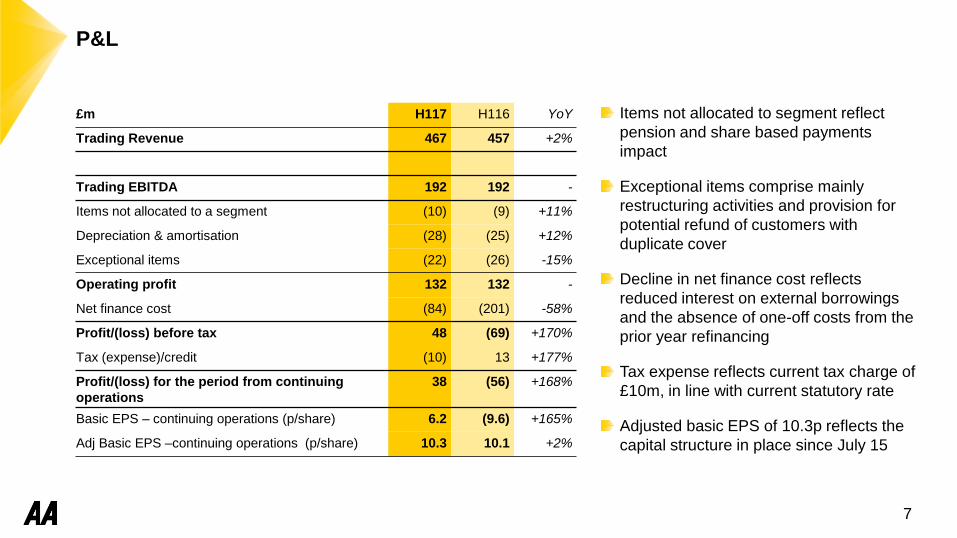

P&L

Items not allocated to segment reflect

pension and share based payments

impact

Exceptional items comprise mainly

restructuring activities and provision for

potential refund of customers with

duplicate cover

Decline in net finance cost reflects

reduced interest on external borrowings

and the absence of one-off costs from the

prior year refinancing

Tax expense reflects current tax charge of

£10m, in line with current statutory rate

Adjusted basic EPS of 10.3p reflects the

capital structure in place since July 15

7

£m H117 H116 YoY

Trading Revenue 467 457 +2%

Trading EBITDA 192 192 -

Items not allocated to a segment (10) (9) +11%

Depreciation & amortisation (28) (25) +12%

Exceptional items (22) (26) -15%

Operating profit 132 132 -

Net finance cost (84) (201) -58%

Profit/(loss) before tax 48 (69) +170%

Tax (expense)/credit (10) 13 +177%

Profit/(loss) for the period from continuing

operations

38 (56) +168%

Basic EPS – continuing operations (p/share) 6.2 (9.6) +165%

Adj Basic EPS –continuing operations (p/share) 10.3 10.1 +2%

ROADSIDE ASSISTANCE

8

H117 H116 YoY FY16 H1 on

FY

Personal Members (‘000s) 3,599 3,726 -3% 3,673 -2%

Average income per Member (£) 145 138 +5% 141 +3%

Personal paid² Members (‘000s) 3,321 3,340 -1% 3,331 flat

Average income per paid² Member (£) 157 154 +2% 156 +1%

Business customers (‘000s) 10,179 9,981 +2% 10,216 flat

Average income per business customer (£) 19 18 +6% 18 +6%

Breakdowns attended (‘000s)³ 1,759 1,662 +6% 3,459 n/a

Trading Revenue¹ up 3.1% to £370m

• Retention 81% (H1 16: 80%)

• Paid personal Members -0.6% YoY;

-0.3% on FY 16

• Average income per personal paid

Member +1.9% to £157 (net of 3.5%

uplift in IPT)

• Ancillary revenue up 14%

Trading EBITDA¹ up 4.1% to £179m

• Growth in income per personal Member

and B2B revenue; lower H1 advertising

spend (£5m vs £7.5m in H1 16)

• Partially offset by increased workload

from higher level of breakdowns attended

¹ Excluding items held for sale and exceptional revenue item

² Paid Members: Personal Members excluding free Memberships

³ Relevant period basis

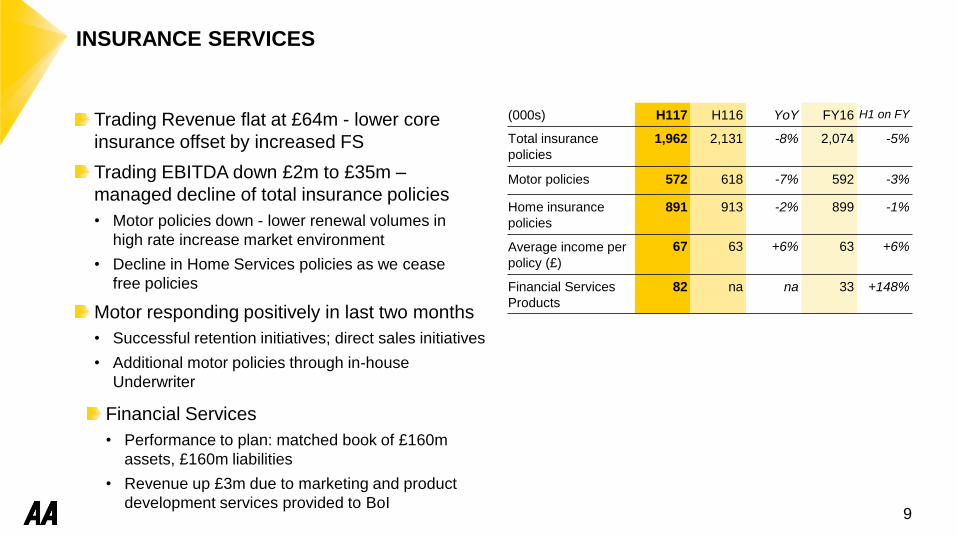

INSURANCE SERVICES

9

(000s) H117 H116 YoY FY16 H1 on FY

Total insurance

policies

1,962 2,131 -8% 2,074 -5%

Motor policies 572 618 -7% 592 -3%

Home insurance

policies

891 913 -2% 899 -1%

Average income per

policy (£)

67 63 +6% 63 +6%

Financial Services

Products

82 na na 33 +148%

Trading Revenue flat at £64m - lower core

insurance offset by increased FS

Trading EBITDA down £2m to £35m –

managed decline of total insurance policies

• Motor policies down - lower renewal volumes in

high rate increase market environment

• Decline in Home Services policies as we cease

free policies

Motor responding positively in last two months

• Successful retention initiatives; direct sales initiatives

• Additional motor policies through in-house

Underwriter

Financial Services

• Performance to plan: matched book of £160m

assets, £160m liabilities

• Revenue up £3m due to marketing and product

development services provided to BoI

IN-HOUSE UNDERWRITER

DRIVING SERVICES

10

Underwriter

• Progressing well

• Motor launched 30 January – 54k policies to date

• Home insurance underwriting launched in August

Driving Services

• Trading Revenue down 3% but EBITDA flat at £9m

– Fewer driving school franchisees reflecting

market conditions

– DriveTech police speed awareness courses

stable

– Cost savings support EBITDA

– Short term initiatives to improve driving school

performance

H117 H116 YoY FY16 H1 on FY

Policies

underwritten

(‘000s)

25 na na na na

H117 H116 YoY FY16 H1 on FY

Driving

instructors

2,516 2,602 -3% 2,574 -2%

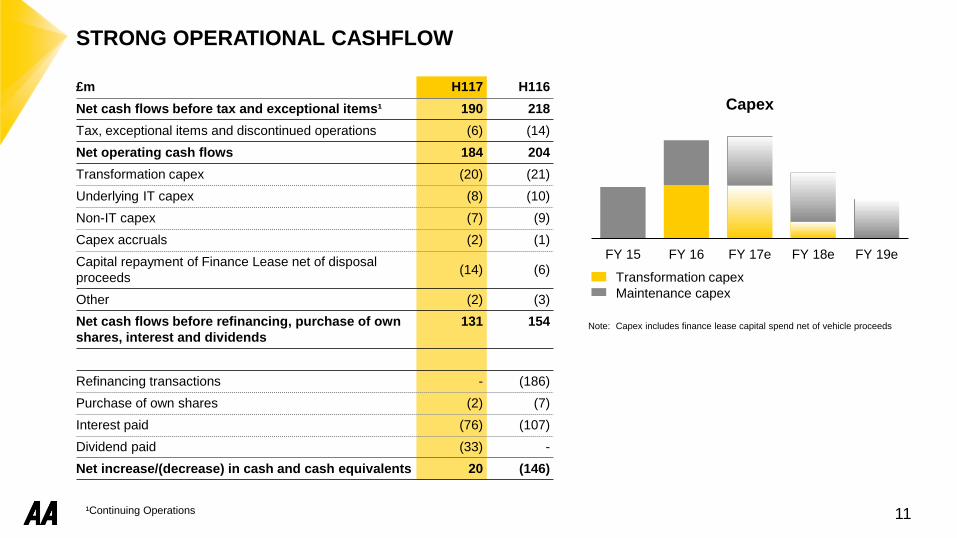

STRONG OPERATIONAL CASHFLOW

£m H117 H116

Net cash flows before tax and exceptional items¹ 190 218

Tax, exceptional items and discontinued operations (6) (14)

Net operating cash flows 184 204

Transformation capex (20) (21)

Underlying IT capex (8) (10)

Non-IT capex (7) (9)

Capex accruals (2) (1)

Capital repayment of Finance Lease net of disposal

proceeds(14) (6)

Other (2) (3)

Net cash flows before refinancing, purchase of own

shares, interest and dividends

131 154

Refinancing transactions - (186)

Purchase of own shares (2) (7)

Interest paid (76) (107)

Dividend paid (33) -

Net increase/(decrease) in cash and cash equivalents 20 (146)

11

Note: Capex includes finance lease capital spend net of vehicle proceeds

FY 15 FY 16 FY 17e FY 18e FY 19e

Capex

Transformation capex

Maintenance capex

¹Continuing Operations

£454m £475m £500m £500m

£250m

£735m

£158m

Senior TermFacility

Class A1notes

Class A2notes

Class A3notes

Class A4notes

NewClass B2

notes

Cash

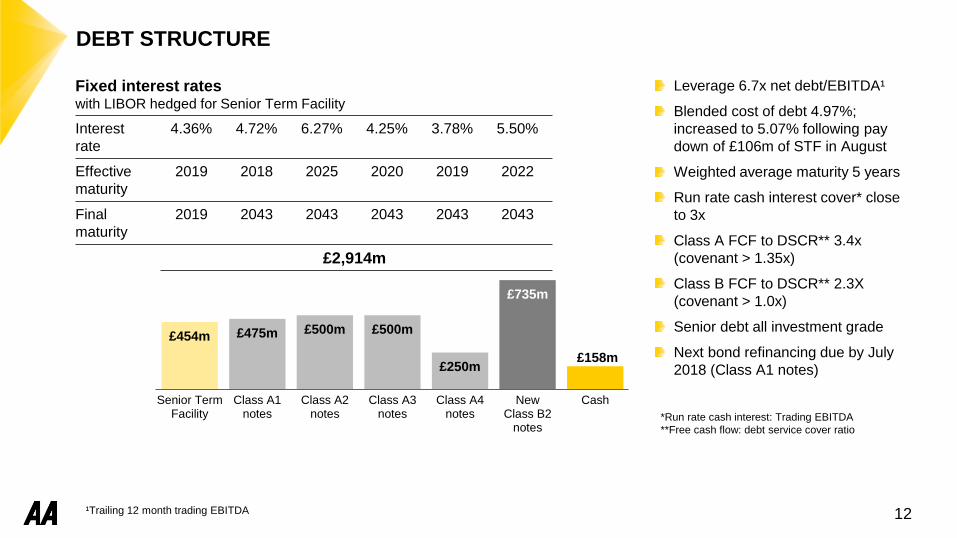

DEBT STRUCTURE

Leverage 6.7x net debt/EBITDA¹

Blended cost of debt 4.97%;

increased to 5.07% following pay

down of £106m of STF in August

Weighted average maturity 5 years

Run rate cash interest cover* close

to 3x

Class A FCF to DSCR** 3.4x

(covenant > 1.35x)

Class B FCF to DSCR** 2.3X

(covenant > 1.0x)

Senior debt all investment grade

Next bond refinancing due by July

2018 (Class A1 notes)

Fixed interest rates with LIBOR hedged for Senior Term Facility

Interest

rate

4.36% 4.72% 6.27% 4.25% 3.78% 5.50%

Effective

maturity

2019 2018 2025 2020 2019 2022

Final

maturity

2019 2043 2043 2043 2043 2043

£2,914m

12

*Run rate cash interest: Trading EBITDA

**Free cash flow: debt service cover ratio

¹Trailing 12 month trading EBITDA

PENSIONS

13

IAS 19 pension deficit of £622m (31 July 15: £329m)

• Increase in deficit driven by decline in corporate bond yields, particularly since UK referendum

vote to leave the EU

Triennial review of AA UK pension scheme commenced

• Anticipate a significant increase from previous valuation of £202m (31 March 2013) due to

reduction in long term gilt yields

• Deficit likely to be materially below IAS 19 valuation

• Review completion due by June 2017

Review of options to mitigate current and future liabilities

Decline in bond yields provides refinancing opportunity

FINANCIAL IMPLICATIONS OF THE TRANSFORMATION

14

Transformation capex: c.£10m saving allowing investment in other areas

Investment in marketing and brand: £10m plus additional spend on the product

proposition

IT opex: c£8m pa

Post-transformation capex run rate: IT c£10m; property & equipment c£10m; net

vehicle costs c£20m

Restructuring costs: £45m over three years

Cost savings: at least £40m in respect of the FY15 cost base in FY19

• Cost savings on target; phase 2 to commence once IT is in place

Driving revenue and earnings growth

STRATEGY

THE STRATEGIC PRIORITIES

BUILDING MOMENTUM IN YEAR 2 OF TRANSFORMATION

1. Strengthen the AA to become the pre-

eminent membership services

organisation in the UK

2. Revolutionise customer experience

through investing in the brand and

embracing new technologies

3. Reduce Group borrowings and the

associated interest costs

THE TIME LINE

Year 1 FY16 Stronger foundations delivered

Year 2 FY17 Building momentum for change

Year 3 FY18 Realise the transformation

Year 4 FY19 Delivering growth

16

Transforming the AA into the UK’s pre-eminent Membership organisation

ROADSIDE PERSONAL MEMBERSHIP – REVERSING THE DECLINE

Growth in paid personal membership numbers

since April and continuing since July

Retention improved to 81% (80% last year)

Stay AA since inception

• Calls to Stay AA down 9%

• Save rate up 7 percentage points

• Discount rate down 7 percentage points

Double-digit growth in new business volumes

• Re-invigorated marketing approach

• Improved digital capabilities

• Lower price increases to drive retention

• Advertising gaining traction

17

MONTHLY PAID NEW BUSINESS VOLUMES

YoY growth (%)

Jul-1

4

Aug-14

Sep-14

Oct-1

4

Nov-14

Dec-14

Jan-15

Feb-15

Mar-15

Apr-1

5

May-15

Jun-15

Jul-1

5

Aug-15

Sep-15

Oct-1

5

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-1

6

May-16

Jun-16

Jul-1

6

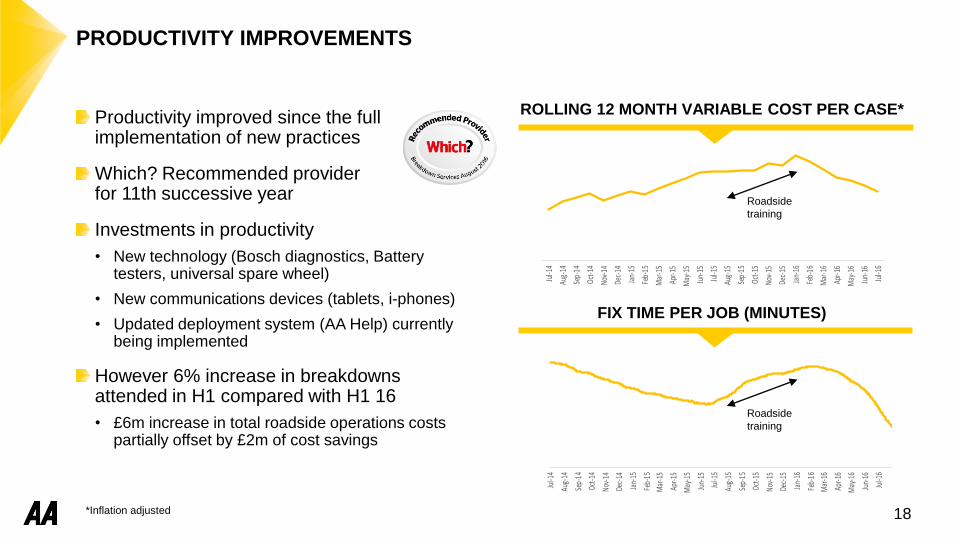

PRODUCTIVITY IMPROVEMENTS

18

Productivity improved since the full implementation of new practices

Which? Recommended provider for 11th successive year

Investments in productivity

• New technology (Bosch diagnostics, Battery testers, universal spare wheel)

• New communications devices (tablets, i-phones)

• Updated deployment system (AA Help) currently being implemented

However 6% increase in breakdowns attended in H1 compared with H1 16

• £6m increase in total roadside operations costs partially offset by £2m of cost savings

ROLLING 12 MONTH VARIABLE COST PER CASE*

Roadside

training

Jul-1

4

Aug-14

Sep-14

Oct-1

4

Nov-14

Dec-14

Jan-15

Feb-15

Mar-15

Apr-1

5

May-15

Jun-15

Jul-1

5

Aug-15

Sep-15

Oct-1

5

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-1

6

May-16

Jun-16

Jul-1

6

Roadside

training

FIX TIME PER JOB (MINUTES)

*Inflation adjusted

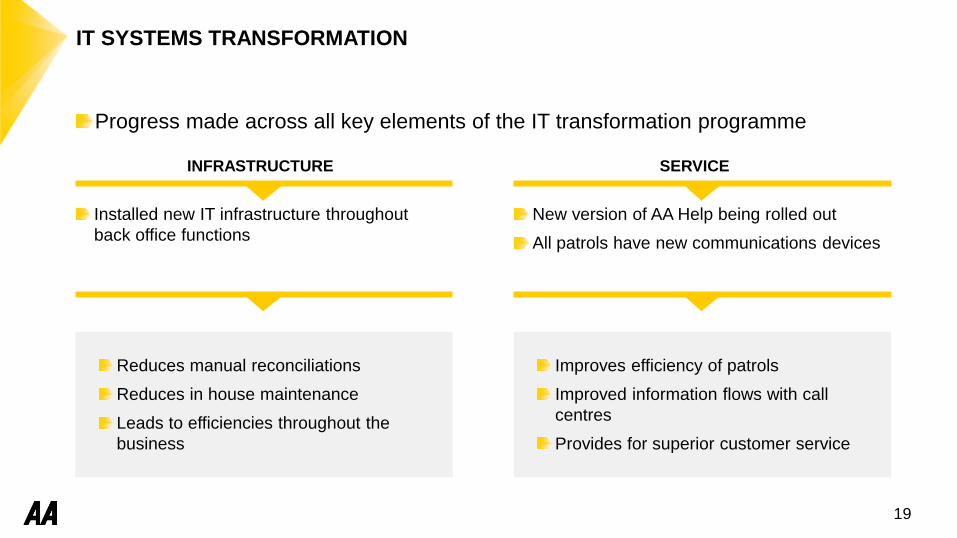

IT SYSTEMS TRANSFORMATION

19

Progress made across all key elements of the IT transformation programme

Installed new IT infrastructure throughout

back office functions

INFRASTRUCTURE

New version of AA Help being rolled out

All patrols have new communications devices

SERVICE

Reduces manual reconciliations

Reduces in house maintenance

Leads to efficiencies throughout the

business

Improves efficiency of patrols

Improved information flows with call

centres

Provides for superior customer service

IT SYSTEMS TRANSFORMATION

20

Marketing element live since March

Full CRM now being rolled out and uploaded

Expected be finalised in Autumn 2017

Improved on-boarding journey

CRM

Enables 360-degree view of customer,

integrating customer data

Real-time, automated reporting and

insight

Allows for relevant, personal and iterative

conversations with customers

Enables next best action to drive sales

Will facilitate easier cross sell

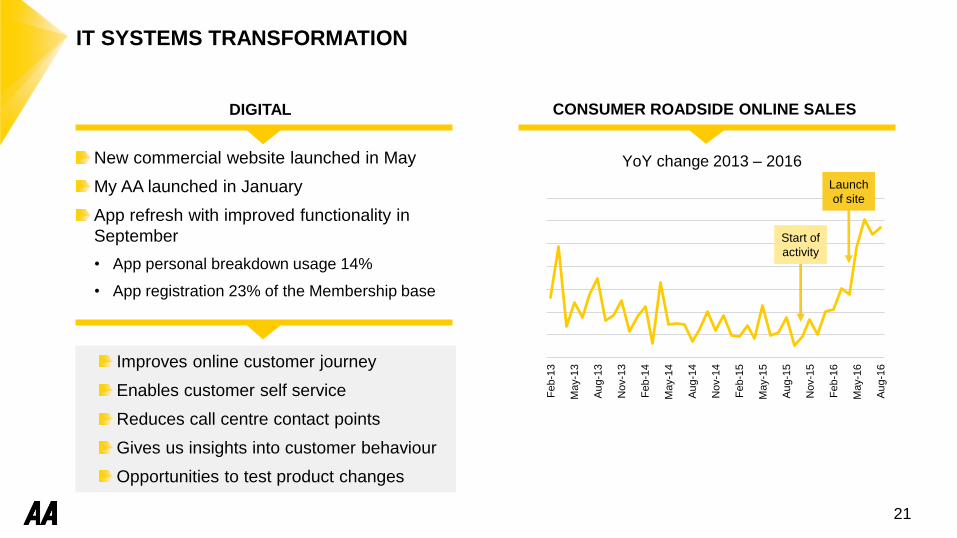

IT SYSTEMS TRANSFORMATION

21

New commercial website launched in May

My AA launched in January

App refresh with improved functionality in

September

• App personal breakdown usage 14%

• App registration 23% of the Membership base

DIGITAL

Improves online customer journey

Enables customer self service

Reduces call centre contact points

Gives us insights into customer behaviour

Opportunities to test product changes

CONSUMER ROADSIDE ONLINE SALES

Fe

b-1

3

May-1

3

Au

g-1

3

Nov-1

3

Fe

b-1

4

May-1

4

Au

g-1

4

Nov-1

4

Fe

b-1

5

May-1

5

Au

g-1

5

Nov-1

5

Fe

b-1

6

May-1

6

Au

g-1

6

Start of

activity

YoY change 2013 – 2016

Launch

of site

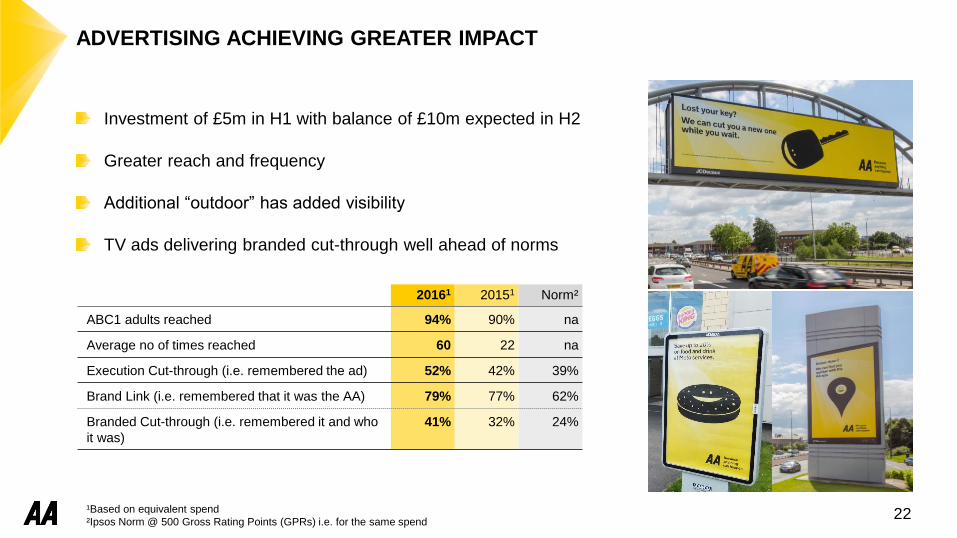

ADVERTISING ACHIEVING GREATER IMPACT

22

Investment of £5m in H1 with balance of £10m expected in H2

Greater reach and frequency

Additional “outdoor” has added visibility

TV ads delivering branded cut-through well ahead of norms

20161 20151 Norm²

ABC1 adults reached 94% 90% na

Average no of times reached 60 22 na

Execution Cut-through (i.e. remembered the ad) 52% 42% 39%

Brand Link (i.e. remembered that it was the AA) 79% 77% 62%

Branded Cut-through (i.e. remembered it and who

it was)

41% 32% 24%

¹Based on equivalent spend

²Ipsos Norm @ 500 Gross Rating Points (GPRs) i.e. for the same spend

FINANCIAL SERVICES AND IN HOUSE UNDERWRITER

23

Launched cards, loans, savings, and mortgages (in

August) in partnership with the Bank of Ireland

£160m matched book value

AA positioned in top 1-5 savings; top 10 for cards

and loans

FINANCIAL SERVICES INSURANCE UNDERWRITER

Insurance Underwriter launched in January to

participate on the AA’s motor insurance panel

25k policies written by end of July; 54k by end

of September

Home insurance launched in August

Too early for material financial contribution but

early signs are promising

*For cards, this analysis does not show the fee based long dated balance transfer (BT) card segment.

As at 12th September 2016

AA UNDERWRITER POLICIES BY ORIGIN

52%32%

16% Has never been an AA insurancecustomer

Was once previously an AAinsurance customer

An existing AA insurance customer

Strengthened foundations and revolutionising customer experience

SUMMARY

24

Transformation well on track

• Continue to invest in brand marketing and product proposition

• Targeting cost savings from FY19 of at least £40m pa off the FY15 base

• Saving of c.£10m transformation capex allowing investment in other areas

Growth in Membership numbers - continued improvement into August and September

Free cash flow generation to be enhanced following transformation

Trading in line with market expectations for FY17; building momentum for FY18

The UK’s pre-eminent Membership services organisation

APPENDIX

£m H117 H116 Change

% of

Group

Roadside Assistance 370 359 +3.1% 79% Increase in average revenue per customer and

B2B revenue

Insurance Services 64 64 - 14% Lower policy numbers offset by higher income

per policy

Driving Services 32 33 -3.0% 7% Lower driving school franchises

Insurance

Underwriting

1 1 - -

Trading revenue 467 457 +2.2%

Business held for

sales¹

- 9

Exceptional revenue

provision

(10) -

Total revenue 457 466 -1.9%

REVENUE

271 In September 2015, AA plc group completed the sale of its subsidiary Autowindshields (UK) Limited. As a result, this business was presented as held for sale in

the prior period.

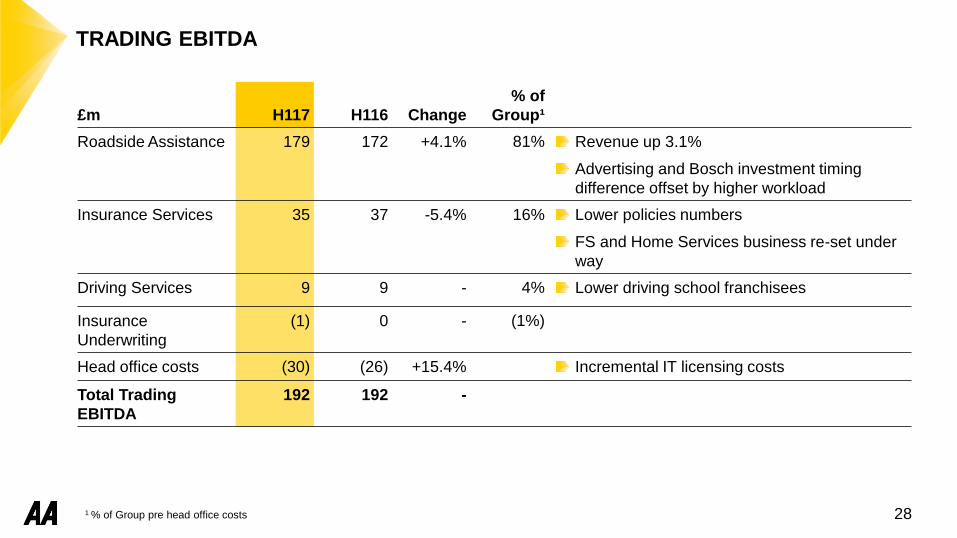

TRADING EBITDA

£m H117 H116 Change

% of

Group¹

Roadside Assistance 179 172 +4.1% 81% Revenue up 3.1%

Advertising and Bosch investment timing

difference offset by higher workload

Insurance Services 35 37 -5.4% 16% Lower policies numbers

FS and Home Services business re-set under

way

Driving Services 9 9 - 4% Lower driving school franchisees

Insurance

Underwriting

(1) 0 - (1%)

Head office costs (30) (26) +15.4% Incremental IT licensing costs

Total Trading

EBITDA

192 192 -

281 % of Group pre head office costs

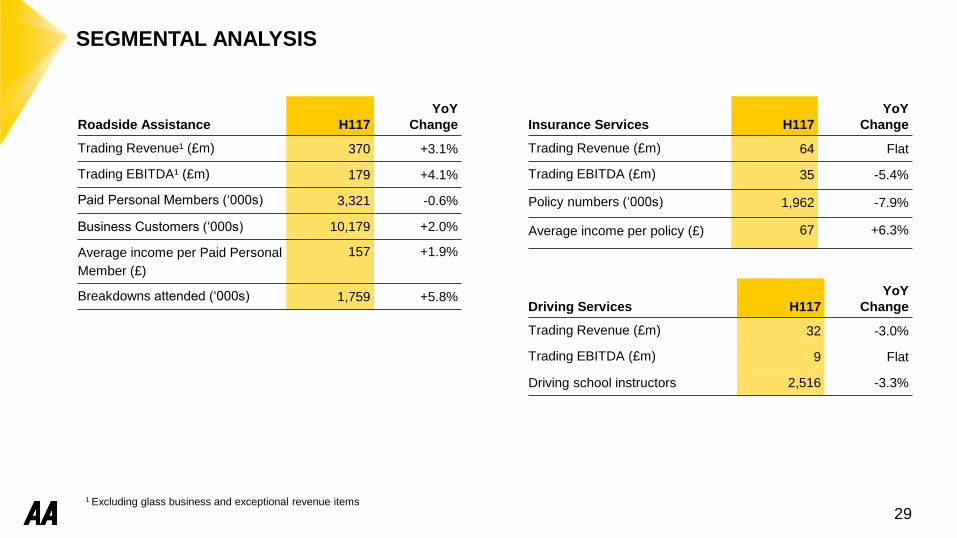

SEGMENTAL ANALYSIS

Insurance Services H117

YoY

Change

Trading Revenue (£m) 64 Flat

Trading EBITDA (£m) 35 -5.4%

Policy numbers (‘000s) 1,962 -7.9%

Average income per policy (£) 67 +6.3%

Driving Services H117

YoY

Change

Trading Revenue (£m) 32 -3.0%

Trading EBITDA (£m) 9 Flat

Driving school instructors 2,516 -3.3%

Roadside Assistance H117

YoY

Change

Trading Revenue¹ (£m) 370 +3.1%

Trading EBITDA¹ (£m) 179 +4.1%

Paid Personal Members (‘000s) 3,321 -0.6%

Business Customers (‘000s) 10,179 +2.0%

Average income per Paid Personal

Member (£)

157 +1.9%

Breakdowns attended (‘000s) 1,759 +5.8%

291 Excluding glass business and exceptional revenue items

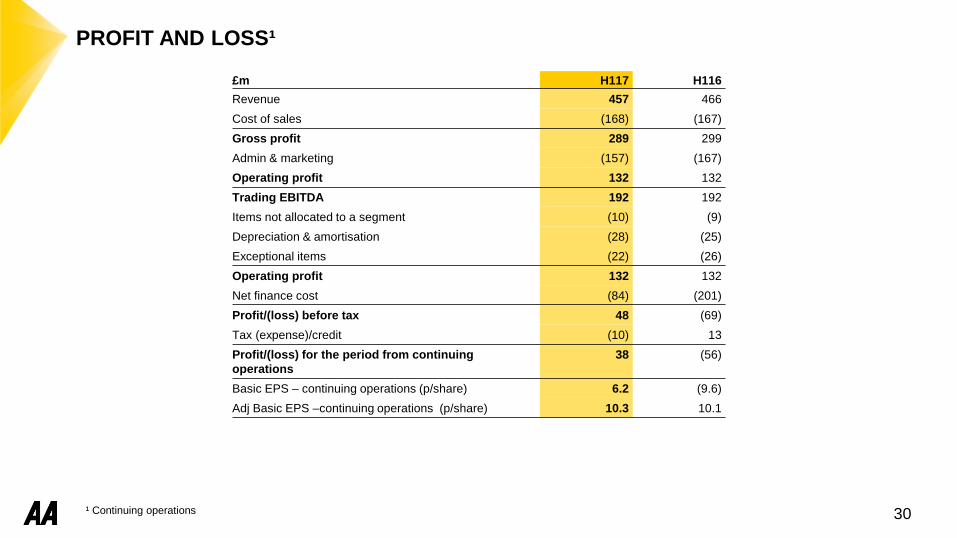

PROFIT AND LOSS¹

£m H117 H116

Revenue 457 466

Cost of sales (168) (167)

Gross profit 289 299

Admin & marketing (157) (167)

Operating profit 132 132

Trading EBITDA 192 192

Items not allocated to a segment (10) (9)

Depreciation & amortisation (28) (25)

Exceptional items (22) (26)

Operating profit 132 132

Net finance cost (84) (201)

Profit/(loss) before tax 48 (69)

Tax (expense)/credit (10) 13

Profit/(loss) for the period from continuing

operations

38 (56)

Basic EPS – continuing operations (p/share) 6.2 (9.6)

Adj Basic EPS –continuing operations (p/share) 10.3 10.1

30¹ Continuing operations

BALANCE SHEET

£m H117 H116

Goodwill and other intangible assets 1,276 1,271

Property, plant and equipment 117 106

Investments in joint ventures and associates 11 8

Deferred tax assets 107 57

Non-current assets 1,511 1,442

Inventories 6 5

Trade and other receivables 169 185

Cash and cash equivalents 158 155

Current assets 333 345

Assets held for sale 93 3

Total assets 1,937 1,790

Trade and other payables (502) (523)

Current tax payable (11) -

Provisions (21) (7)

Current liabilities (534) (530)

Borrowings and loans (2,922) (2,911)

Finance lease obligations (21) (20)

Defined benefit pension scheme liabilities (622) (329)

Provisions (7) (11)

Insurance technical provisions (4) (4)

Non-current liabilities (3,576) (3,275)

Liabilities held for sale (40) (4)

Total liabilities (4,150) (3,809)

Net liabilities (2,213) (2,019)31

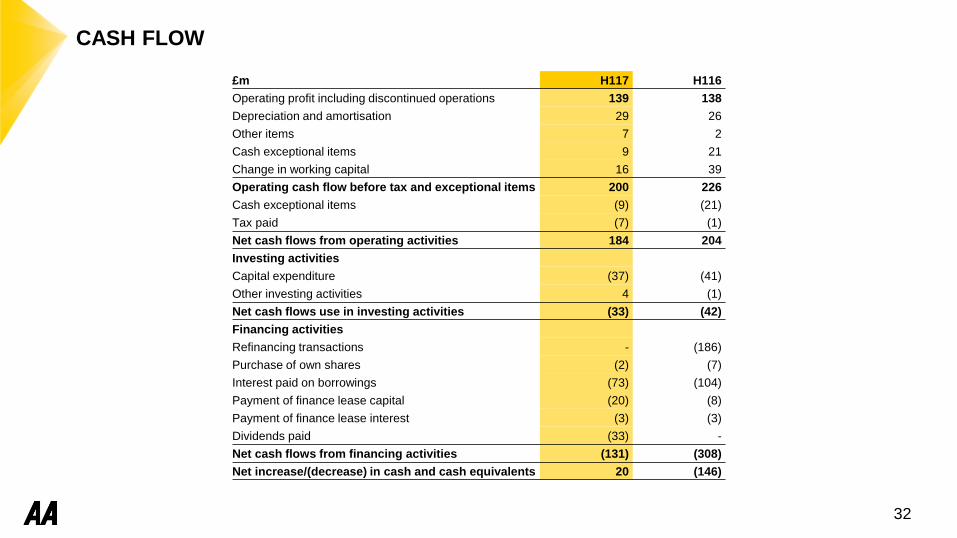

CASH FLOW

£m H117 H116

Operating profit including discontinued operations 139 138

Depreciation and amortisation 29 26

Other items 7 2

Cash exceptional items 9 21

Change in working capital 16 39

Operating cash flow before tax and exceptional items 200 226

Cash exceptional items (9) (21)

Tax paid (7) (1)

Net cash flows from operating activities 184 204

Investing activities

Capital expenditure (37) (41)

Other investing activities 4 (1)

Net cash flows use in investing activities (33) (42)

Financing activities

Refinancing transactions - (186)

Purchase of own shares (2) (7)

Interest paid on borrowings (73) (104)

Payment of finance lease capital (20) (8)

Payment of finance lease interest (3) (3)

Dividends paid (33) -

Net cash flows from financing activities (131) (308)

Net increase/(decrease) in cash and cash equivalents 20 (146)

32

¹Excludes available and restricted cash balances available for sale

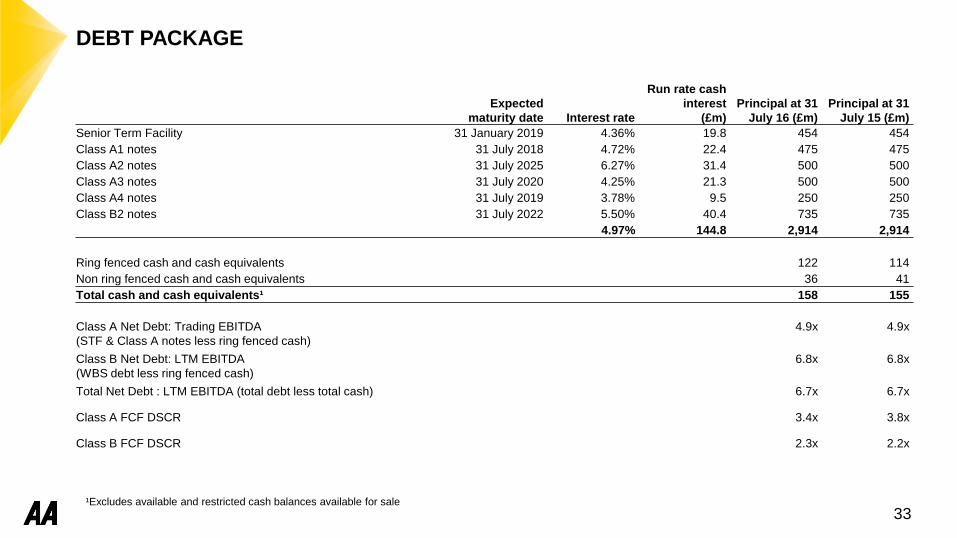

DEBT PACKAGE

Expected

maturity date Interest rate

Run rate cash

interest

(£m)

Principal at 31

July 16 (£m)

Principal at 31

July 15 (£m)

Senior Term Facility 31 January 2019 4.36% 19.8 454 454

Class A1 notes 31 July 2018 4.72% 22.4 475 475

Class A2 notes 31 July 2025 6.27% 31.4 500 500

Class A3 notes 31 July 2020 4.25% 21.3 500 500

Class A4 notes 31 July 2019 3.78% 9.5 250 250

Class B2 notes 31 July 2022 5.50% 40.4 735 735

4.97% 144.8 2,914 2,914

Ring fenced cash and cash equivalents 122 114

Non ring fenced cash and cash equivalents 36 41

Total cash and cash equivalents¹ 158 155

Class A Net Debt: Trading EBITDA

(STF & Class A notes less ring fenced cash)

4.9x 4.9x

Class B Net Debt: LTM EBITDA

(WBS debt less ring fenced cash)

6.8x 6.8x

Total Net Debt : LTM EBITDA (total debt less total cash) 6.7x 6.7x

Class A FCF DSCR 3.4x 3.8x

Class B FCF DSCR 2.3x 2.2x

33