Facing the challenge of a new age - 独立行政法人...

43

Logo Gobierno: 160x162px. Ministerio, Subsecretaría, Organismo, etc.:160x145px Facing the challenge of a new age: Chile and mining in the 21st century COCHILCO – Chilean Copper Commission Jorge Cantallopts Research Department Juanuary 20th, 2015

Transcript of Facing the challenge of a new age - 独立行政法人...

Logo Gobierno: 160x162px. Ministerio, Subsecretaría, Organismo, etc.:160x145px

Facing the challenge of a new age:

Chile and mining in the 21st century

COCHILCO – Chilean Copper Commission

Jorge Cantallopts Research Department

Juanuary 20th, 2015

1. Mining in Chile, a brief summary.

2. Enviromental and social licenses.

3. Costs and productivity challenges.

4. Final comments

Content

Ministry of Mines| COCHILCO

Imagen Referencial

1. Mining in Chile, a brief

summary

Ministry of Mines| COCHILCO

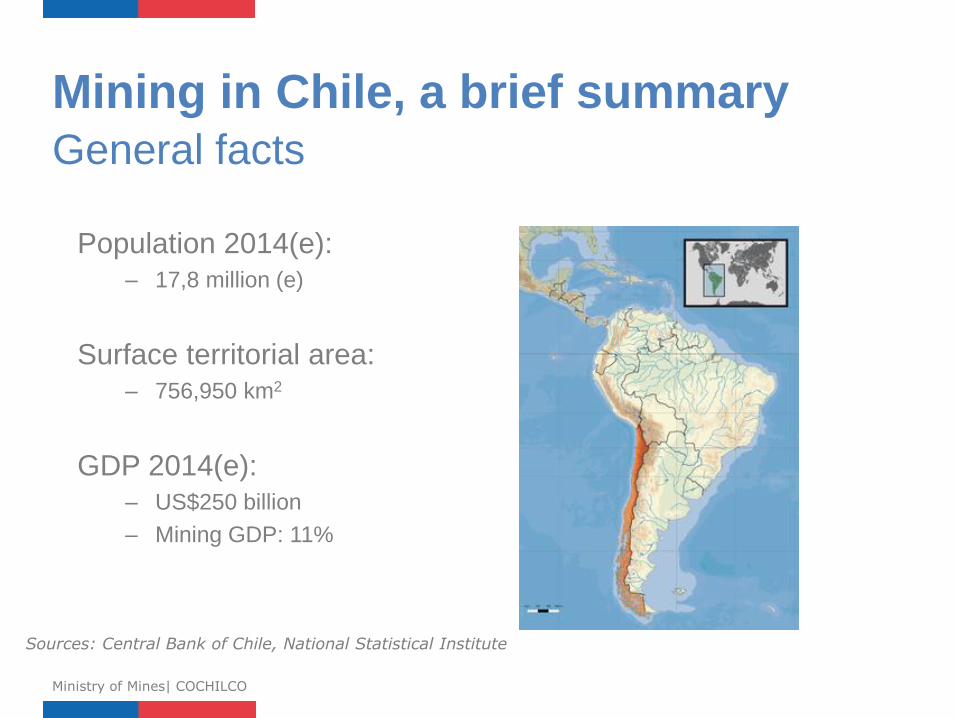

Population 2014(e): – 17,8 million (e)

Surface territorial area: – 756,950 km2

GDP 2014(e): – US$250 billion

– Mining GDP: 11%

Mining in Chile, a brief summary General facts

Ministry of Mines| COCHILCO

Sources: Central Bank of Chile, National Statistical Institute

Mining in Chile, a brief summary Mineral endowment

Ministry of Mines| COCHILCO

Sources: USGS Mineral Commodity Summaries, COCHILCO

Mo

42

95,9

21%

14%

3°

Cu

29

63,5

28% 32%

1°

Au

79

197,0

8% 2%

15°

Ag

47

107,9

14%

5%

7°

Re

75

186,2

52% 52%

1°

Li

3

6,9

58%

35%

1°

Y

53

126,9

24%

61%

1°

Share of world reserves

Share of world production

World production ranking

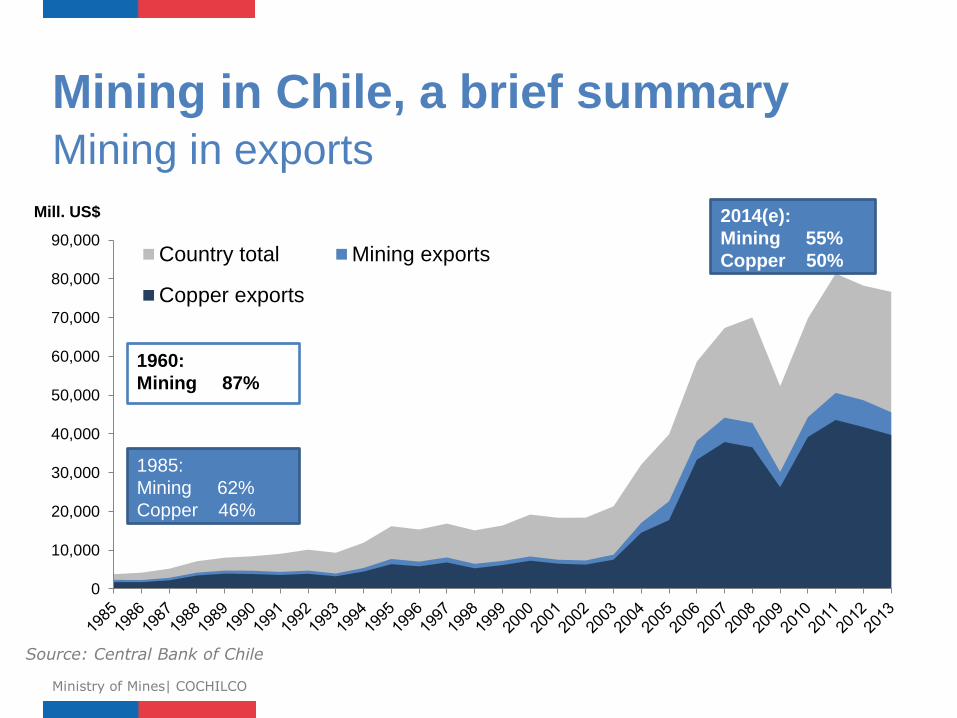

Mining in Chile, a brief summary Mining in exports

Ministry of Mines| COCHILCO

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Mill. US$

Country total Mining exports

Copper exports

2014(e):

Mining 55%

Copper 50%

1985:

Mining 62%

Copper 46%

1960:

Mining 87%

Source: Central Bank of Chile

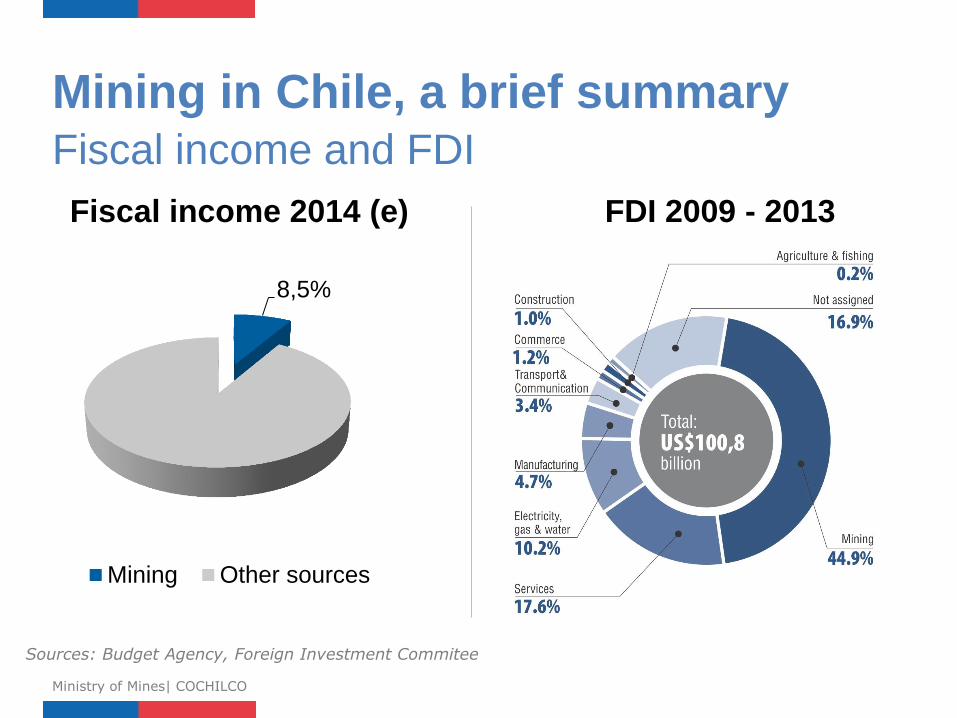

Mining in Chile, a brief summary Fiscal income and FDI

Ministry of Mines| COCHILCO

8,5%

Mining Other sources

Fiscal income 2014 (e)

Sources: Budget Agency, Foreign Investment Commitee

FDI 2009 - 2013

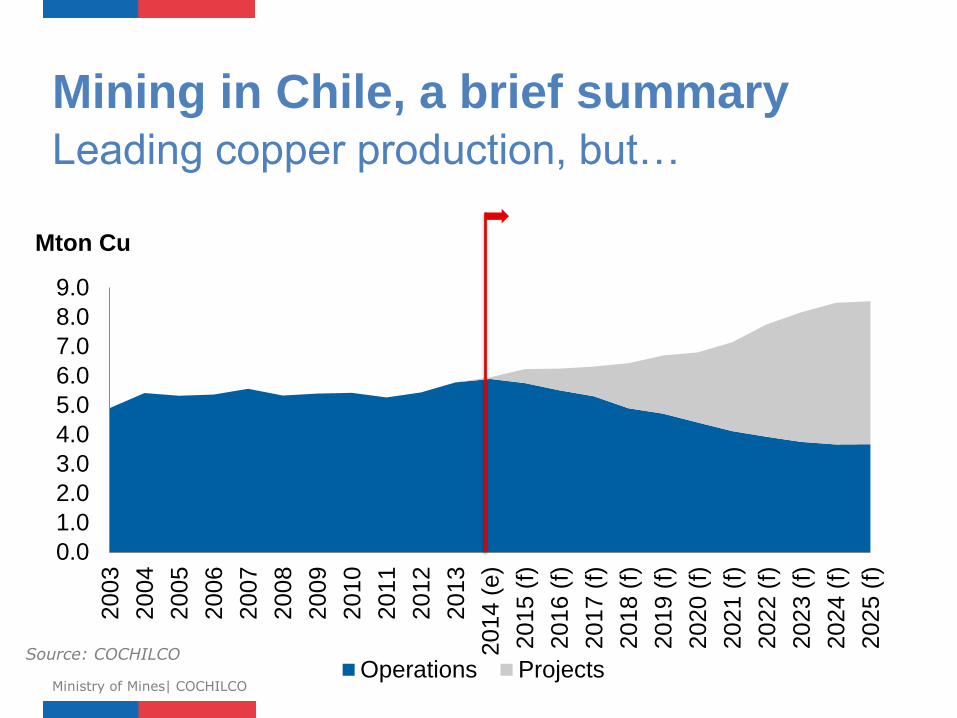

Mining in Chile, a brief summary Leading copper production, but…

Ministry of Mines| COCHILCO

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014 (

e)

2015 (

f)

2016 (

f)

2017 (

f)

2018 (

f)

2019 (

f)

2020 (

f)

2021 (

f)

20

22

(f)

2023 (

f)

2024 (

f)

2025 (

f)

Mton Cu

Operations ProjectsSource: COCHILCO

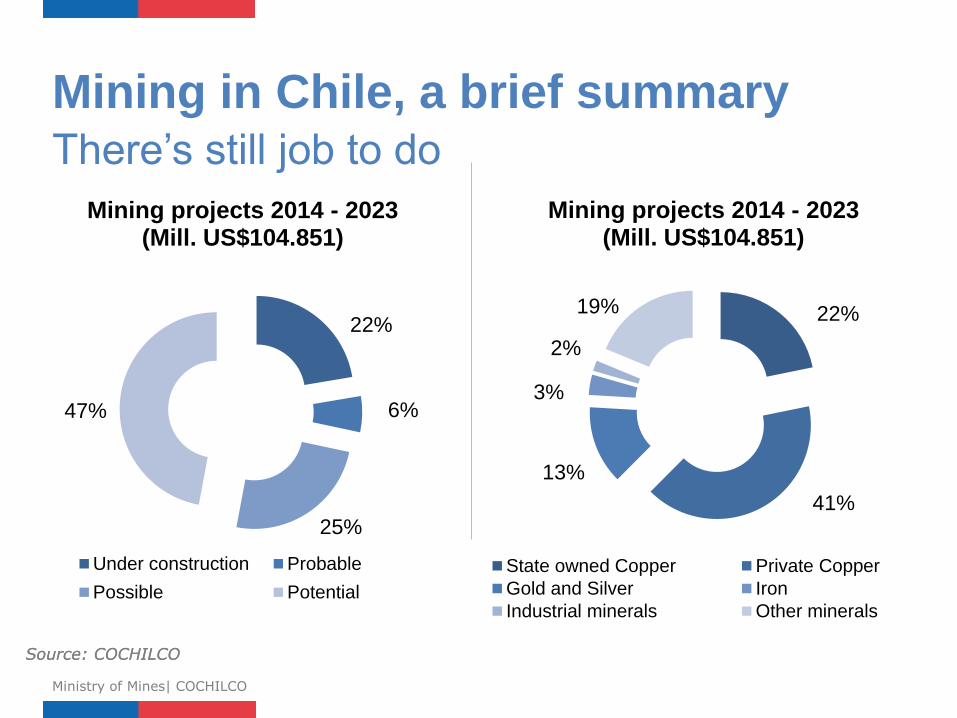

Mining in Chile, a brief summary There’s still job to do

Ministry of Mines| COCHILCO

Source: COCHILCO

22%

6%

25%

47%

Mining projects 2014 - 2023 (Mill. US$104.851)

Under construction Probable

Possible Potential

22%

41%

13%

3%

2%

19%

Mining projects 2014 - 2023 (Mill. US$104.851)

State owned Copper Private Copper

Gold and Silver Iron

Industrial minerals Other minerals

Source: COCHILCO

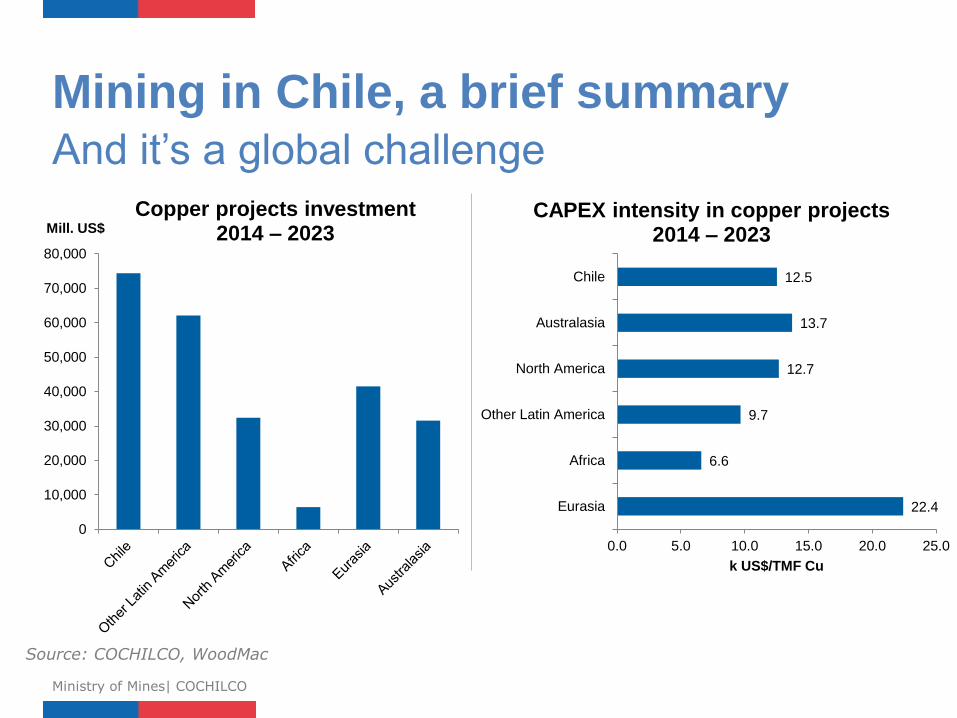

Mining in Chile, a brief summary And it’s a global challenge

Ministry of Mines| COCHILCO

Source: COCHILCO, WoodMac

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Mill. US$

Copper projects investment 2014 – 2023

22.4

6.6

9.7

12.7

13.7

12.5

0.0 5.0 10.0 15.0 20.0 25.0

Eurasia

Africa

Other Latin America

North America

Australasia

Chile

k US$/TMF Cu

CAPEX intensity in copper projects 2014 – 2023

Imagen Referencial

2. Enviromental and social

licenses

Ministry of Mines| COCHILCO

Enviromental and social licenses

Ministry of Mines| COCHILCO

Mine

closure

Smelters

emissions

Local

communities Human

resources Water

availability

Enviromental and social licenses

Ministry of Mines| COCHILCO

Mine

closure

Smelters

emissions

Local

communities Human

resources Water

availability

• Improvement in legal framework in 2011lead to

new obligations to mining operation related to

mining closure.

• In 2014 more than 100 mining operations

submit their closure plan.

• Expected value of first approach reach Mill. US$

12.238.

Enviromental and social licenses Mine closure

Ministry of Mines| COCHILCO

Source: National Service of Geology and Mines

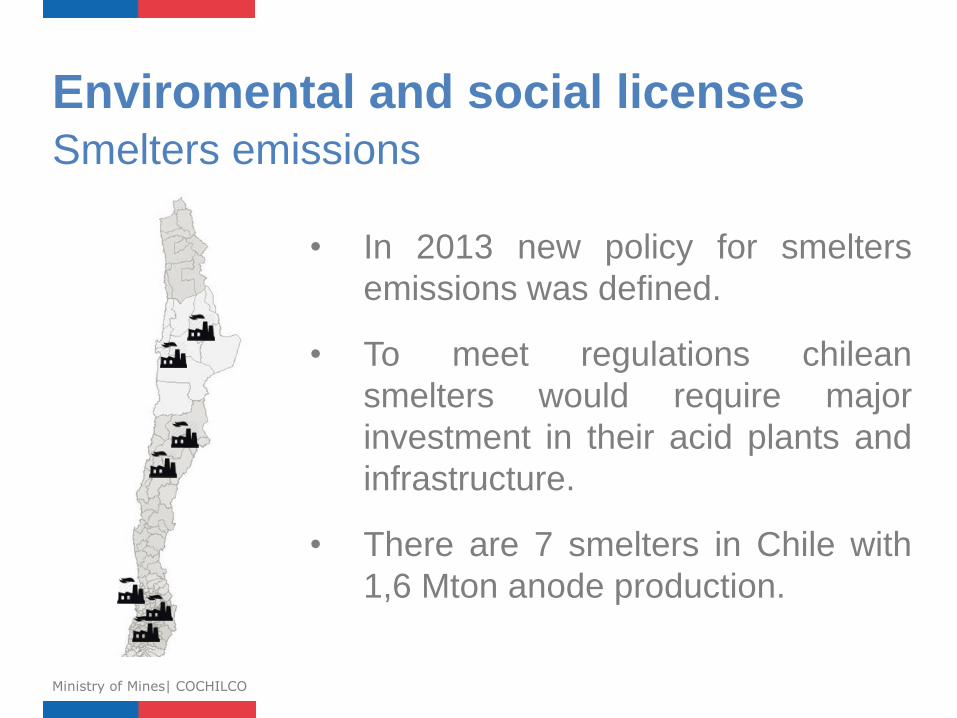

• In 2013 new policy for smelters

emissions was defined.

• To meet regulations chilean

smelters would require major

investment in their acid plants and

infrastructure.

• There are 7 smelters in Chile with

1,6 Mton anode production.

Enviromental and social licenses Smelters emissions

Ministry of Mines| COCHILCO

Enviromental and social licenses

Ministry of Mines| COCHILCO

Mine

closure

Smelters

emissions

Local

communities Human

resources Water

availability

• Several projects have to deal in a new way with

society.

• Empowered citizens, social awareness, search

for mutual benefit and legal framework (C169).

Enviromental and social licenses Local communities

Ministry of Mines| COCHILCO

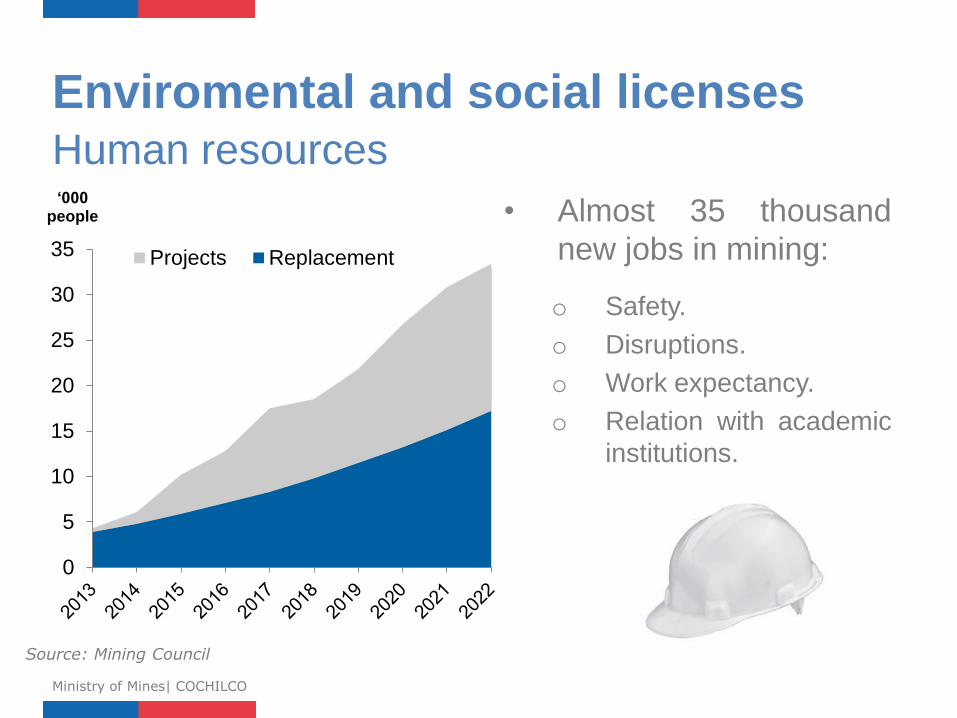

Enviromental and social licenses Human resources

Ministry of Mines| COCHILCO

0

5

10

15

20

25

30

35

‘000 people

Projects Replacement

Source: Mining Council

• Almost 35 thousand

new jobs in mining:

o Safety.

o Disruptions.

o Work expectancy.

o Relation with academic

institutions.

Enviromental and social licenses

Ministry of Mines| COCHILCO

Mine

closure

Smelters

emissions

Local

communities Human

resources Water

availability

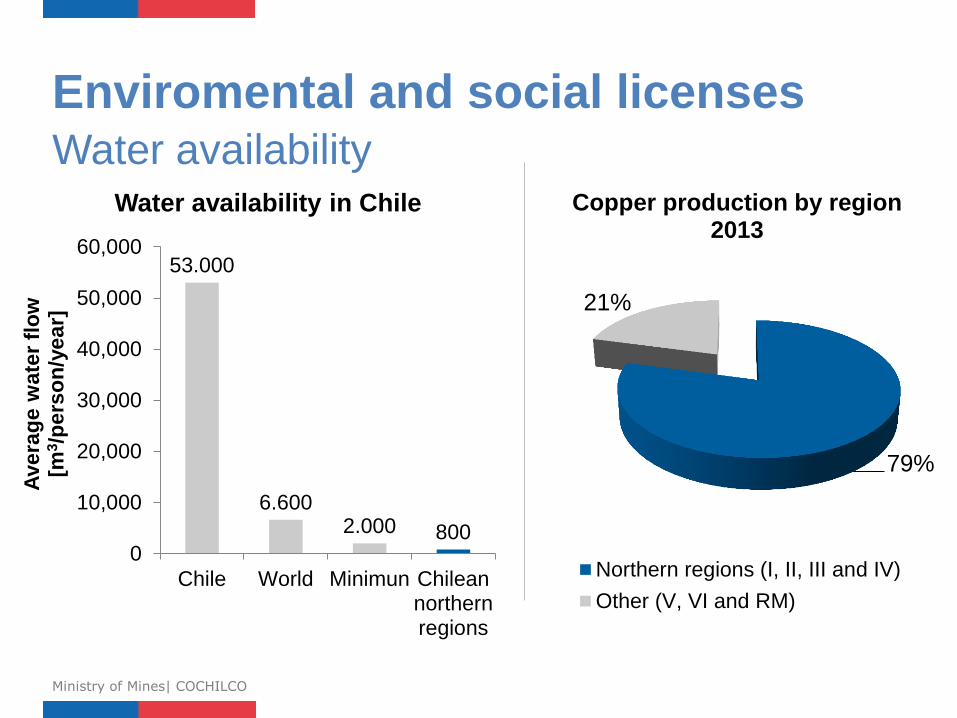

Enviromental and social licenses Water availability

Ministry of Mines| COCHILCO

53.000

6.600 2.000 800

0

10,000

20,000

30,000

40,000

50,000

60,000

Chile World Minimun Chileannorthernregions

Avera

ge

wate

r fl

ow

[m

3/p

ers

on

/ye

ar]

Water availability in Chile

79%

21%

Copper production by region 2013

Northern regions (I, II, III and IV)

Other (V, VI and RM)

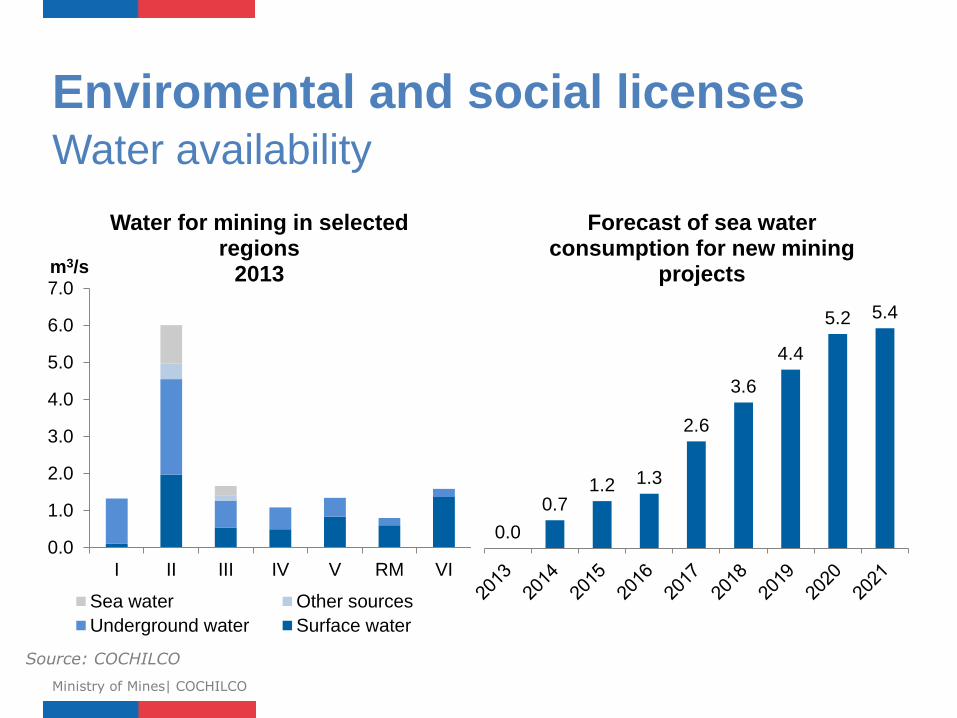

Enviromental and social licenses Water availability

Ministry of Mines| COCHILCO

0.0

0.7 1.2 1.3

2.6

3.6

4.4

5.2 5.4

Forecast of sea water consumption for new mining

projects

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

I II III IV V RM VI

m3/s

千

Water for mining in selected regions

2013

Sea water Other sources

Underground water Surface water

Source: COCHILCO

Imagen Referencial

3. Costs and productivity

challenges

Ministry of Mines| COCHILCO

Costs and productivity challenges

Ministry of Mines| COCHILCO

Geology

Mining costs

Energy costs

and

consumption Productivity Strategic

inputs

Costs and productivity challenges

Ministry of Mines| COCHILCO

Geology

Mining costs

Energy costs

and

consumption Productivity Strategic

inputs

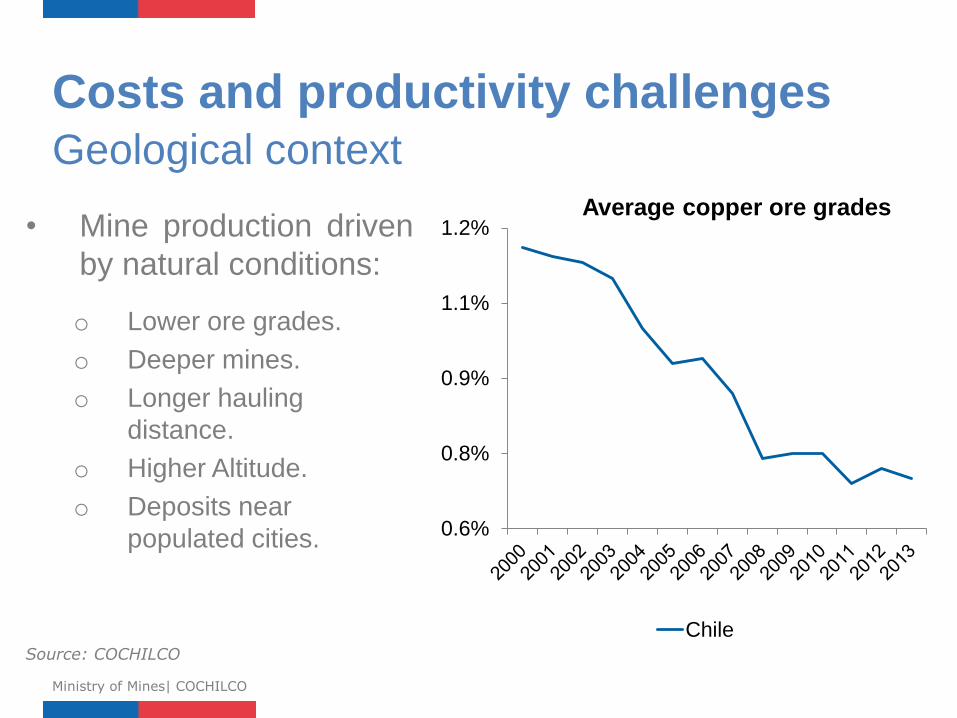

Costs and productivity challenges Geological context

Ministry of Mines| COCHILCO

• Mine production driven

by natural conditions:

o Lower ore grades.

o Deeper mines.

o Longer hauling

distance.

o Higher Altitude.

o Deposits near

populated cities.

Source: COCHILCO

0.6%

0.8%

0.9%

1.1%

1.2%Average copper ore grades

Chile

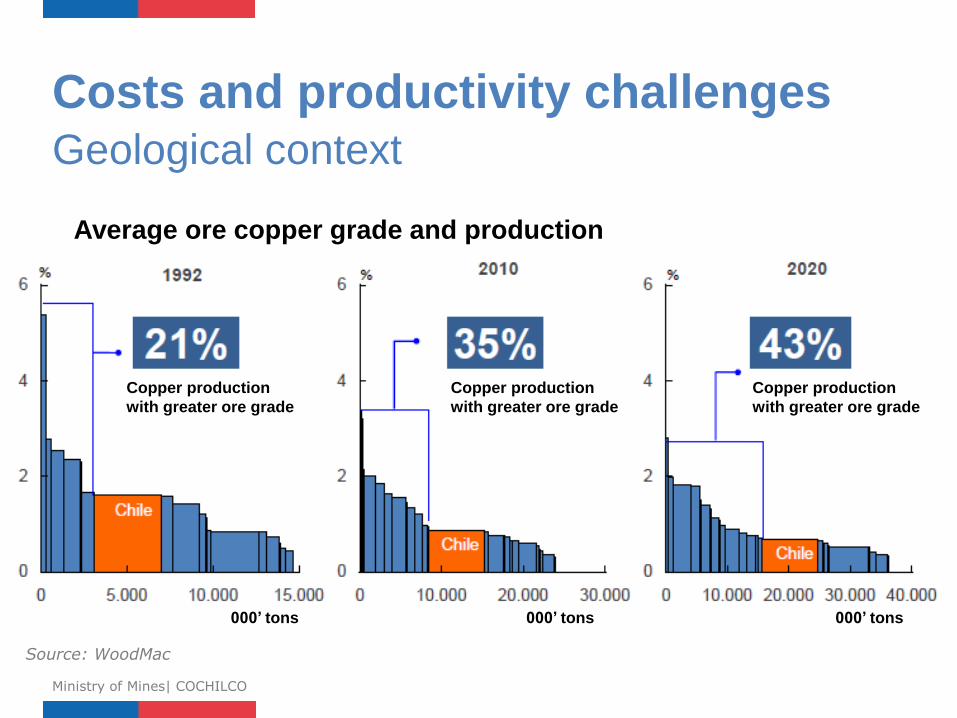

Costs and productivity challenges Geological context

Ministry of Mines| COCHILCO

Source: WoodMac

Average ore copper grade and production

000’ tons 000’ tons 000’ tons

Copper production

with greater ore grade

Copper production

with greater ore grade

Copper production

with greater ore grade

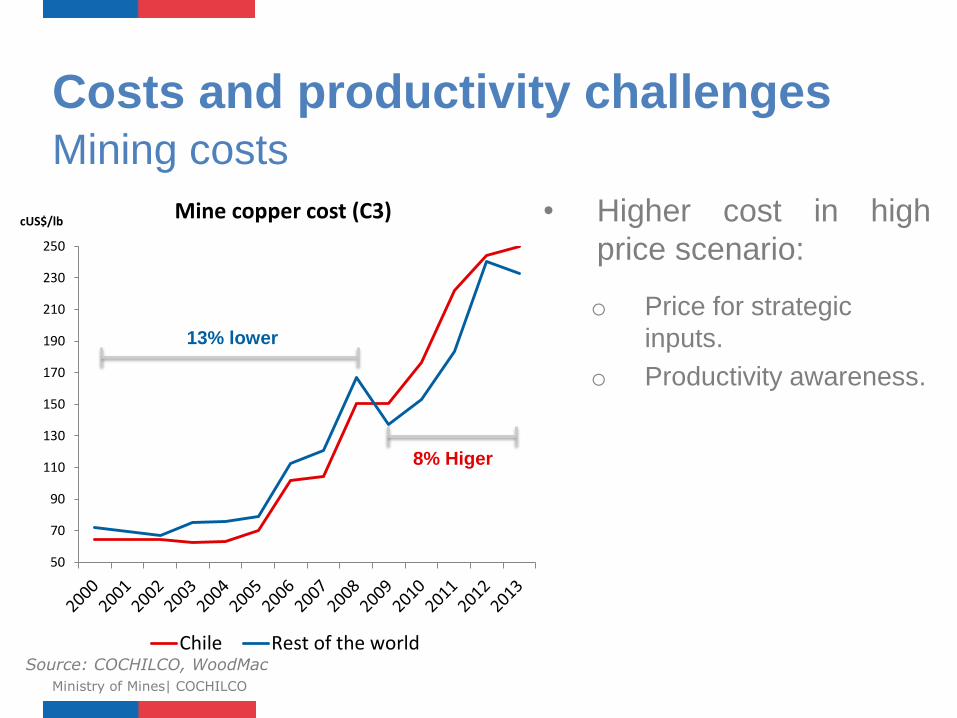

Costs and productivity challenges Mining costs

Ministry of Mines| COCHILCO

• Higher cost in high

price scenario:

o Price for strategic

inputs.

o Productivity awareness.

50

70

90

110

130

150

170

190

210

230

250

cUS$/lb Mine copper cost (C3)

Chile Rest of the world

13% lower

8% Higer

Source: COCHILCO, WoodMac

Costs and productivity challenges

Ministry of Mines| COCHILCO

Geology

Mining costs

Energy costs

and

consumption Productivity Strategic

inputs

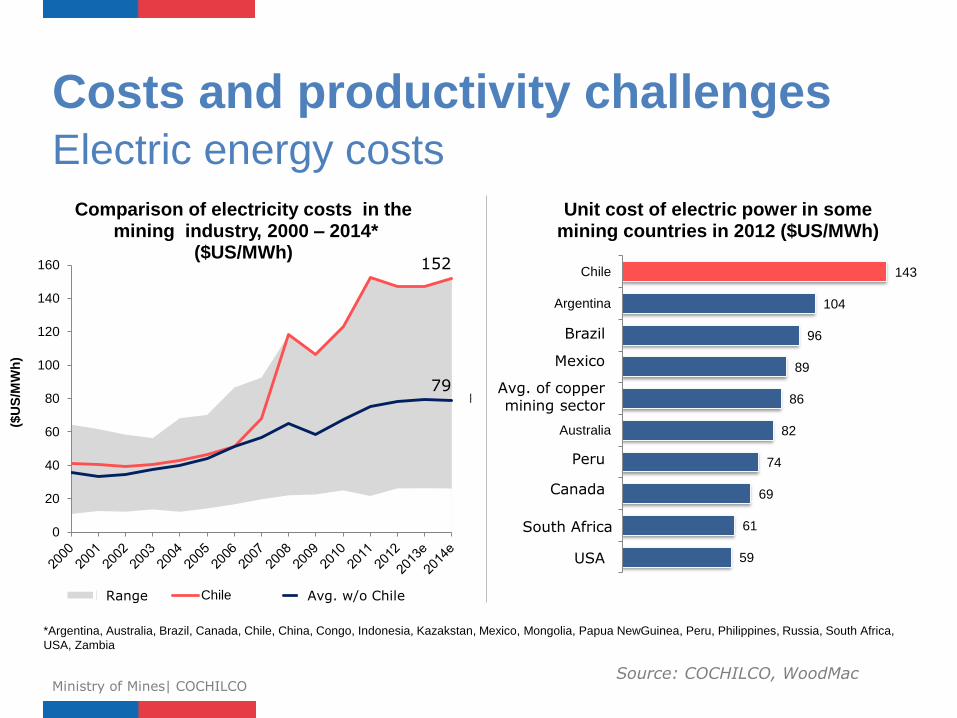

Costs and productivity challenges Electric energy costs

Ministry of Mines| COCHILCO

*Argentina, Australia, Brazil, Canada, Chile, China, Congo, Indonesia, Kazakstan, Mexico, Mongolia, Papua NewGuinea, Peru, Philippines, Russia, South Africa,

USA, Zambia

0

20

40

60

80

100

120

140

160

($U

S/M

Wh

)

Comparison of electricity costs in the mining industry, 2000 – 2014*

($US/MWh)

Max Chile Promedio sin Chile

59

61

69

74

82

86

89

96

104

143

EE.UU.

Sudáfrica

Canadá

Perú

Australia

Prom. Minería de Cobre

México

Brazil

Argentina

Chile

Unit cost of electric power in some mining countries in 2012 ($US/MWh)

Brasil

Avg. w/o Chile

Brazil

Mexico

Avg. of copper mining sector

Peru

Canada

South Africa

USA

Range

79

152

Source: COCHILCO, WoodMac

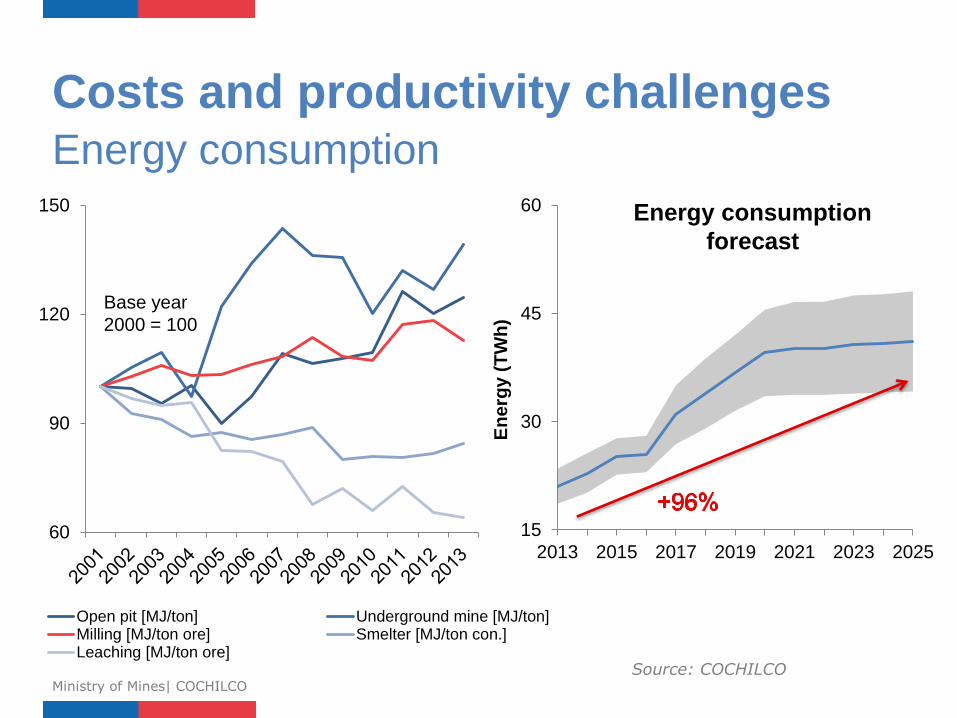

Costs and productivity challenges Energy consumption

Ministry of Mines| COCHILCO

60

90

120

150

Open pit [MJ/ton] Underground mine [MJ/ton]Milling [MJ/ton ore] Smelter [MJ/ton con.]Leaching [MJ/ton ore]

15

30

45

60

2013 2015 2017 2019 2021 2023 2025

En

erg

y (

TW

h)

Source: COCHILCO

Base year

2000 = 100

Energy consumption

forecast

Costs and productivity challenges

Ministry of Mines| COCHILCO

Geology

Mining costs

Energy costs

and

consumption Productivity Strategic

inputs

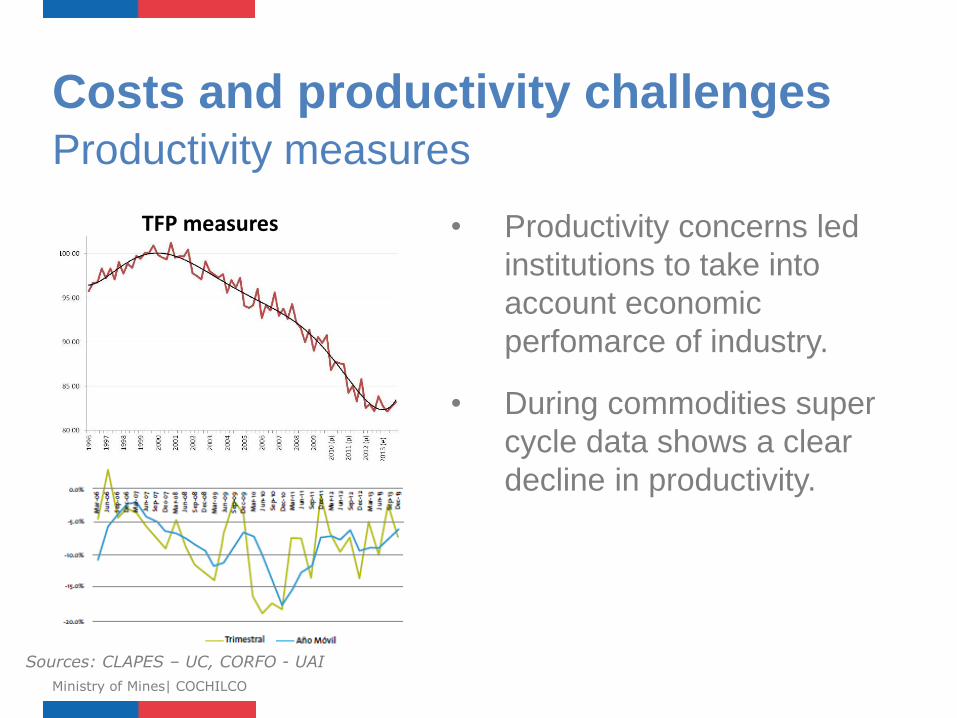

Costs and productivity challenges Productivity measures

Ministry of Mines| COCHILCO

Sources: CLAPES – UC, CORFO - UAI

• Productivity concerns led

institutions to take into

account economic

perfomarce of industry.

• During commodities super

cycle data shows a clear

decline in productivity.

TFP measures

Costs and productivity challenges Productivity measures

Ministry of Mines| COCHILCO

Source: COCHILCO

100%

80%

70%

80%

90%

100%

110%

To

tal F

ac

tor

Pro

du

cti

vit

y

Base year

2000 = 100%

0

50

100

150

200

250

300

Cu Production Labor

Energy consumption Capital stock

Cu Reserves Ore grade

Base year

2000 = 100

Chilean copper

mines TFP

Input index

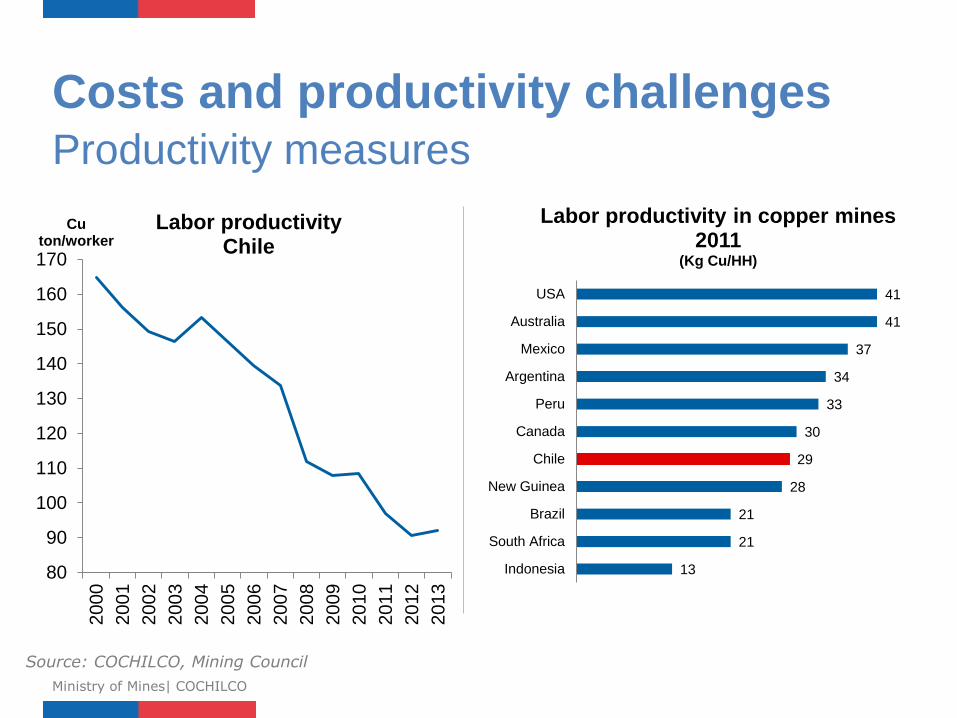

Costs and productivity challenges Productivity measures

Ministry of Mines| COCHILCO

Source: COCHILCO, Mining Council

80

90

100

110

120

130

140

150

160

170

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Cu ton/worker

Labor productivity Chile

13

21

21

28

29

30

33

34

37

41

41

Indonesia

South Africa

Brazil

New Guinea

Chile

Canada

Peru

Argentina

Mexico

Australia

USA

Labor productivity in copper mines 2011

(Kg Cu/HH)

Costs and productivity challenges

Ministry of Mines| COCHILCO

Geology

Mining costs

Energy costs

and

consumption Productivity Strategic

inputs

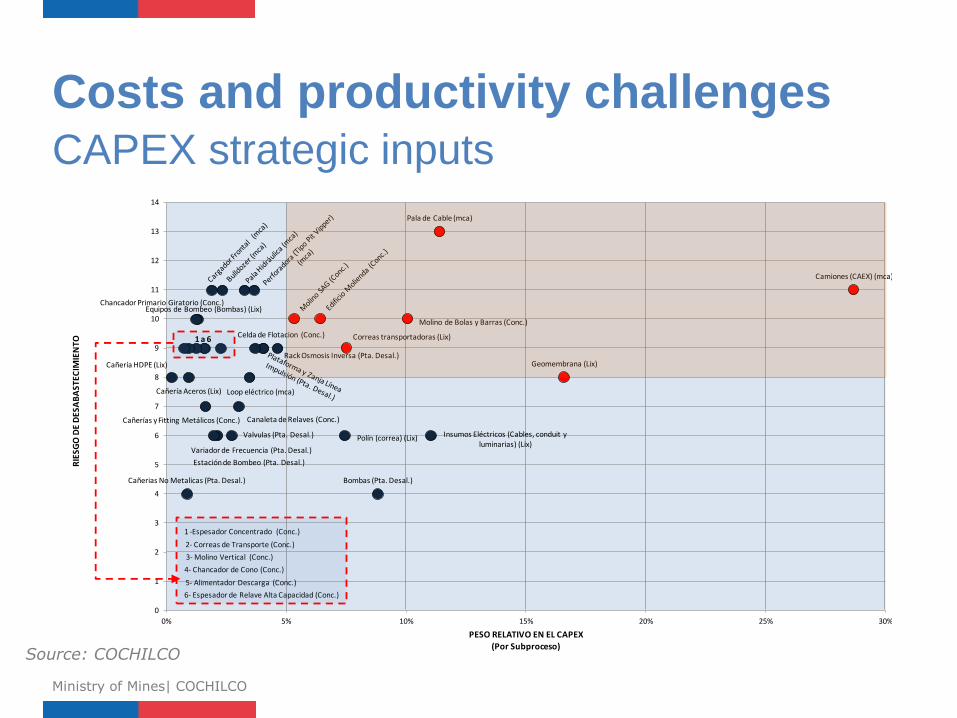

Costs and productivity challenges CAPEX strategic inputs

Ministry of Mines| COCHILCO

Pala de Cable (mca)

Camiones (CAEX) (mca)

Molino de Bolas y Barras (Conc.)

Equipos de Bombeo (Bombas) (Lix)Chancador Primario Giratorio (Conc.)

Correas transportadoras (Lix)

Rack Osmosis Inversa (Pta. Desal.)

Celda de Flotacion (Conc.)

6- Espesador de Relave Alta Capacidad (Conc.)

5- Alimentador Descarga (Conc.)

4- Chancador de Cono (Conc.)

3- Molino Vertical (Conc.)

2- Correas de Transporte (Conc.)

1 -Espesador Concentrado (Conc.)

Geomembrana (Lix)

Loop eléctrico (mca)Cañería Aceros (Lix)

Cañería HDPE (Lix)

Canaleta de Relaves (Conc.)Cañerías y Fitting Metálicos (Conc.)

Insumos Eléctricos (Cables, conduit y luminarias) (Lix)

Polín (correa) (Lix)Valvulas (Pta. Desal.)

Estación de Bombeo (Pta. Desal.)

Variador de Frecuencia (Pta. Desal.)

Bombas (Pta. Desal.)Cañerias No Metalicas (Pta. Desal.)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

0% 5% 10% 15% 20% 25% 30%

RIE

SGO

DE

DES

AB

AST

ECIM

IEN

TO

PESO RELATIVO EN EL CAPEX

(Por Subproceso)

1 a 6

Source: COCHILCO

Costs and productivity challenges CAPEX strategic inputs

Ministry of Mines| COCHILCO

• Higher share in total cost and higher

availability risk:

o SAG, ball and bar mills (Mill).

o Milling infraestructure (Mill).

o Mineral conveyor (Leaching).

o Geomembrane (Leaching).

o Trucks and Electric Shovel (Open Pit).

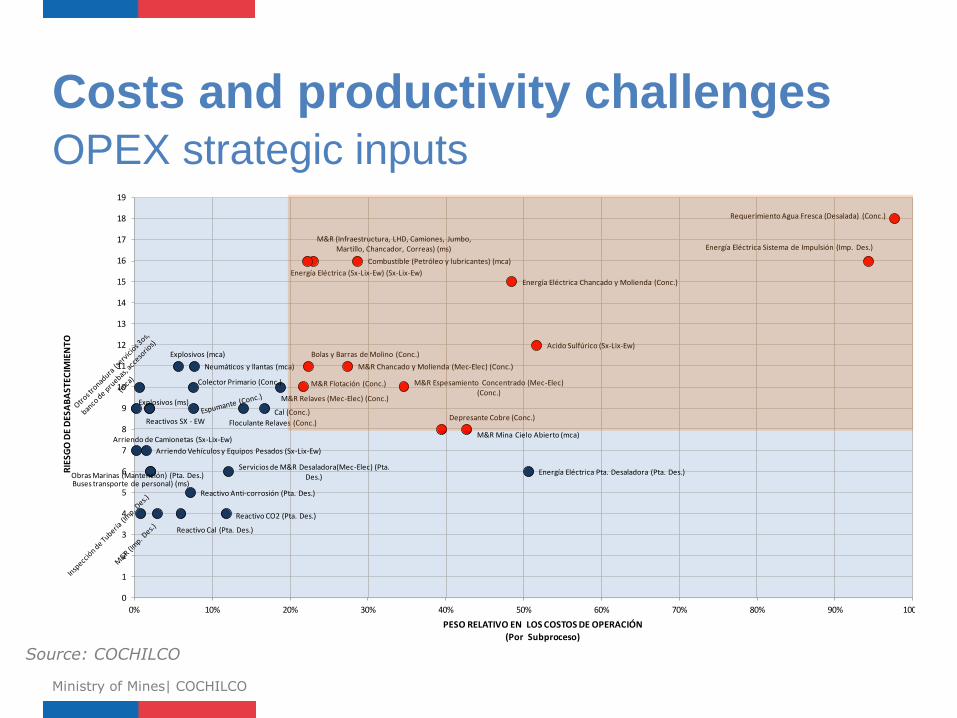

Costs and productivity challenges OPEX strategic inputs

Ministry of Mines| COCHILCO

Source: COCHILCO

Requerimiento Agua Fresca (Desalada) (Conc.)

Energía Eléctrica Sistema de Impulsión (Imp. Des.)

Combustible (Petróleo y lubricantes) (mca)

M&R (Infraestructura, LHD, Camiones, Jumbo, Martillo, Chancador, Correas) (ms)

Energía Eléctrica (Sx-Lix-Ew) (Sx-Lix-Ew)Energía Eléctrica Chancado y Molienda (Conc.)

Acido Sulfúrico (Sx-Lix-Ew)

M&R Chancado y Molienda (Mec-Elec) (Conc.)

Bolas y Barras de Molino (Conc.)

Neumáticos y llantas (mca)

Explosivos (mca)

M&R Espesamiento Concentrado (Mec-Elec) (Conc.)

M&R Flotación (Conc.)

M&R Relaves (Mec-Elec) (Conc.)

Colector Primario (Conc.)

Cal (Conc.)

Floculante Relaves (Conc.)Reactivos SX - EW

Explosivos (ms)

M&R Mina Cielo Abierto (mca)

Depresante Cobre (Conc.)

Arriendo Vehículos y Equipos Pesados (Sx-Lix-Ew)

Arriendo de Camionetas (Sx-Lix-Ew)

Energía Eléctrica Pta. Desaladora (Pta. Des.)Servicios de M&R Desaladora(Mec-Elec) (Pta.

Des.)Obras Marinas (Mantención) (Pta. Des.)Buses transporte de personal) (ms)

Reactivo Anti-corrosión (Pta. Des.)

Reactivo CO2 (Pta. Des.)

Reactivo Cal (Pta. Des.)

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

RIE

SGO

DE

DES

AB

AST

ECIM

IEN

TO

PESO RELATIVO EN LOS COSTOS DE OPERACIÓN(Por Subproceso)

Costs and productivity challenges OPEX strategic inputs

Ministry of Mines| COCHILCO

• Higher share in total cost and higher availability risk for every process:

o Electric energy (Leaching, Mill, Sea water pumping).

o Fuel (Open Pit).

o Fresh water (Mill).

o Materials and Replacement parts (Underground Mine, Open pit and Miill).

o Sulphuric Acid (Leaching).

o Flotation reagents (Mill).

o Steel balls and bars (Mill).

Imagen Referencial

4. Final comments

Ministry of Mines| COCHILCO

• Chile has been recognized as a major center for

mining investment.

• Mineral endowment and projects support mining

production forecasting.

• Challenges arise from several interacting factors:

o Enviromental.

o Local communities

o Productivity.

o Costs

Final comments

Ministry of Mines| COCHILCO

• Lower grades and other natural conditions of

deposits encourage the need to sustain mining

development.

• Technology, innovation, changes in processes,

community relation models and costs restraints

are leading efforts of mining activity in Chile.

Final comments

Ministry of Mines| COCHILCO

Logo Gobierno: 160x162px. Ministerio, Subsecretaría, Organismo, etc.:160x145px

Facing the challenge of a new age:

Chile and mining in the 21st century

COCHILCO – Chilean Copper Commission

Jorge Cantallopts Research Department

Juanuary 20th, 2015