eáëÅçñ=póåÇáÅ~íÉ=PP oÉéçêí=~åÇ=^ÅÅçìåíë=OMMV...

36

eáëÅçñ=póåÇáÅ~íÉ=PP oÉéçêí=~åÇ=^ÅÅçìåíë=OMMV MV

-

Upload

truongdieu -

Category

Documents

-

view

223 -

download

1

Transcript of eáëÅçñ=póåÇáÅ~íÉ=PP oÉéçêí=~åÇ=^ÅÅçìåíë=OMMV...

eáëÅçñ=póåÇáÅ~íÉ=PPoÉéçêí=~åÇ=̂ ÅÅçìåíë=OMMV MV

`çåíÉåíë`Ü~áêã~åÛë=ëí~íÉãÉåí NaáêÉÅíçêë=~åÇ=~Çãáåáëíê~íáçå OoÉéçêí=çÑ=íÜÉ=aáêÉÅíçêë=çÑ=íÜÉ=ã~å~ÖáåÖ=~ÖÉåí Ppí~íÉãÉåí=çÑ=ã~å~ÖáåÖ=~ÖÉåíÛë=êÉëéçåëáÄáäáíáÉë TkçíáÅÉ=êÉÖ~êÇáåÖ=íÜÉ=^ååì~ä=dÉåÉê~ä=jÉÉíáåÖ UfåÇÉéÉåÇÉåí=^ìÇáíçêëÛ=êÉéçêí VmêçÑáí=~åÇ=äçëë=~ÅÅçìåíW=íÉÅÜåáÅ~ä=~ÅÅçìåí NMmêçÑáí=~åÇ=äçëë=~ÅÅçìåíW=åçåJíÉÅÜåáÅ~ä=~ÅÅçìåí NN_~ä~åÅÉ=ëÜÉÉí=J=~ëëÉíë NO_~ä~åÅÉ=ëÜÉÉí=J=äá~ÄáäáíáÉë NPpí~íÉãÉåí=çÑ=Å~ëÜ=Ñäçïë NQkçíÉë=íç=íÜÉ=Ñáå~åÅá~ä=ëí~íÉãÉåíë NR

Hiscox Syndicates Limited (HSL)

Hiscox Syndicates Ltd (HSL) is a subsidiary of Hiscox Ltd (Hiscox). HSL managed threeSyndicates in 2009; Syndicate 33 with a capacity of £750m, 73% of which was supplied by Hiscox; Syndicate 6104 with a capacity of £43m, 100% of which was supplied by third-party Members of Lloyd’s, and Syndicate 3624, with a capacity of £80m, which was 100% supplied by Hiscox. There is no conflict between the Syndicates as theyunderwrite clearly defined and separate business. Details of the performance of eachSyndicate can be found in the Directors’ report that follows.

Mother Nature decided to give us a particularly benign year for major losses andcatastrophes. Some would say we were lucky, but my definition of luck is when preparation meets opportunity, and our underwriters did an immense amount ofpreparation and research to underwrite a carefully controlled exposure which could benefit from a benign loss period, but not hurt us if nature turned vicious.

The investments, which were valued at deep discounts at the end of 2008 due to the banking and mortgage crises, recovered to more sensible levels giving a strongperformance for the Syndicates in 2009. Again not luck, as holding our nerve and believing that the downward valuation of our investments was exaggerated was alsorewarded.

I can only repeat and confirm what I said last year, that the general insurance industry and Lloyd’s in particular have performed excellently through the financial chaos of the last few years. I just hope that the regulators and government will appreciate the industry’sconservatism and value, and not wound it with some collateral damage from its currentbank bashing.

Robert Hiscox2 February 2010

CHAIRMAN’S STATEMENT 1HISCOX SYNDICATE 33

Managing agent:

Managing agentHiscox Syndicates Limited (HSL) is the managing agent of composite Syndicate 33, Special Purpose Syndicate 6104 and aligned Syndicate3624. HSL is an indirectly wholly owned subsidiary of Hiscox Ltd.

DirectorsR R S Hiscox (Chairman)S J BridgesD J W BruceR S ChildsA G C Howland Jackson (Non Executive)J S JonesI J MartinB E MasojadaR MerrettJ PinchinI N Thomson (Non Executive)N B TylerR C WatsonI T Webb-Wilson (Non Executive)

Company secretaryK Silverwood

Managing agent’s registered office1 Great St Helen’sLondon EC3A 6HX

Managing agent’s registered number02590623

Syndicate:

Active underwriterR Merrett

BankersBarclays Bank plcCrédit Agricole CIBLloyds TSB Bank plc

Investment managersAllianceBernstein LimitedWellington Management Company, LLPUBS Global Asset Management (Canada) Co.

Registered auditorsKPMG Audit Plc

DIRECTORS AND ADMINISTRATION 2HISCOX SYNDICATE 33

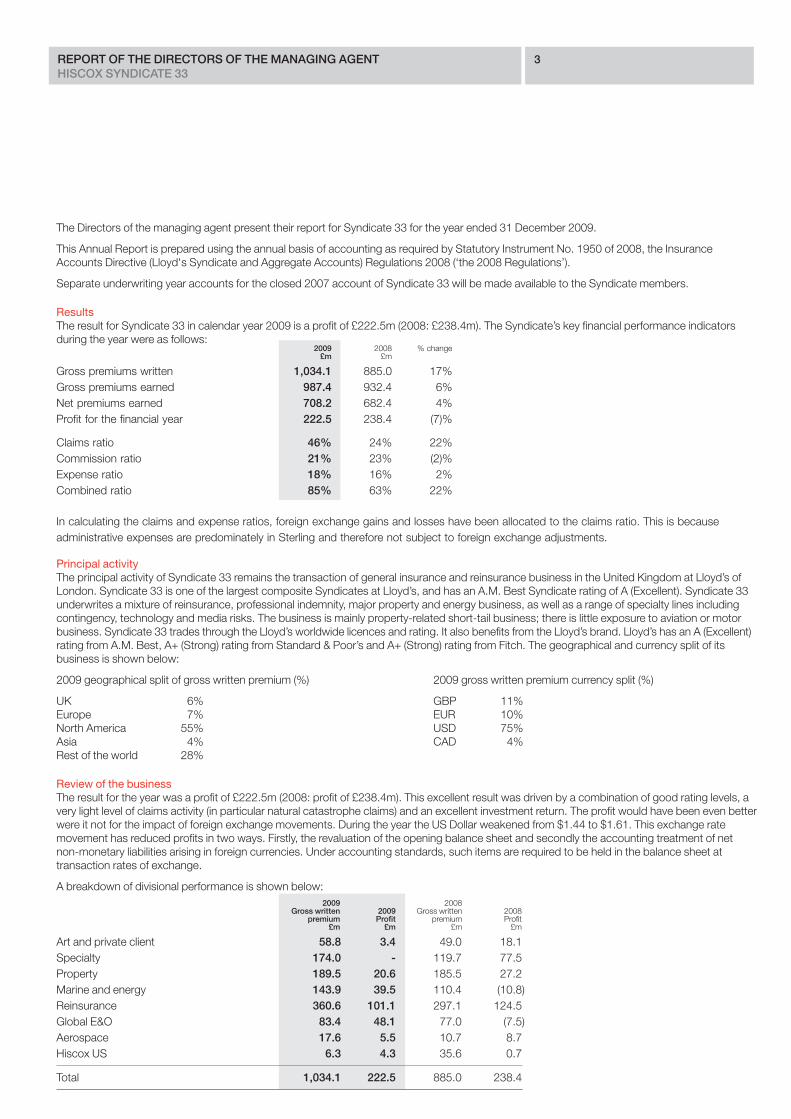

The Directors of the managing agent present their report for Syndicate 33 for the year ended 31 December 2009.

This Annual Report is prepared using the annual basis of accounting as required by Statutory Instrument No. 1950 of 2008, the Insurance Accounts Directive (Lloyd's Syndicate and Aggregate Accounts) Regulations 2008 (‘the 2008 Regulations’).

Separate underwriting year accounts for the closed 2007 account of Syndicate 33 will be made available to the Syndicate members.

ResultsThe result for Syndicate 33 in calendar year 2009 is a profit of £222.5m (2008: £238.4m). The Syndicate’s key financial performance indicatorsduring the year were as follows:

2009 2008 % change£m £m

Gross premiums written 1,034.1 885.0 17%Gross premiums earned 987.4 932.4 6%Net premiums earned 708.2 682.4 4%Profit for the financial year 222.5 238.4 (7)%

Claims ratio 46% 24% 22%Commission ratio 21% 23% (2)%Expense ratio 18% 16% 2%Combined ratio 85% 63% 22%

In calculating the claims and expense ratios, foreign exchange gains and losses have been allocated to the claims ratio. This is because administrative expenses are predominately in Sterling and therefore not subject to foreign exchange adjustments.

Principal activity The principal activity of Syndicate 33 remains the transaction of general insurance and reinsurance business in the United Kingdom at Lloyd’s ofLondon. Syndicate 33 is one of the largest composite Syndicates at Lloyd’s, and has an A.M. Best Syndicate rating of A (Excellent). Syndicate 33underwrites a mixture of reinsurance, professional indemnity, major property and energy business, as well as a range of specialty lines includingcontingency, technology and media risks. The business is mainly property-related short-tail business; there is little exposure to aviation or motorbusiness. Syndicate 33 trades through the Lloyd’s worldwide licences and rating. It also benefits from the Lloyd’s brand. Lloyd’s has an A (Excellent)rating from A.M. Best, A+ (Strong) rating from Standard & Poor’s and A+ (Strong) rating from Fitch. The geographical and currency split of itsbusiness is shown below:

2009 geographical split of gross written premium (%) 2009 gross written premium currency split (%)

UK 6% GBP 11%Europe 7% EUR 10%North America 55% USD 75%Asia 4% CAD 4%Rest of the world 28%

Review of the businessThe result for the year was a profit of £222.5m (2008: profit of £238.4m). This excellent result was driven by a combination of good rating levels, avery light level of claims activity (in particular natural catastrophe claims) and an excellent investment return. The profit would have been even better were it not for the impact of foreign exchange movements. During the year the US Dollar weakened from $1.44 to $1.61. This exchange ratemovement has reduced profits in two ways. Firstly, the revaluation of the opening balance sheet and secondly the accounting treatment of net non-monetary liabilities arising in foreign currencies. Under accounting standards, such items are required to be held in the balance sheet attransaction rates of exchange.

A breakdown of divisional performance is shown below:2009 2008

Gross written 2009 Gross written 2008premium Profit premium Profit

£m £m £m £m

Art and private client 58.8 3.4 49.0 18.1Specialty 174.0 - 119.7 77.5Property 189.5 20.6 185.5 27.2Marine and energy 143.9 39.5 110.4 (10.8)Reinsurance 360.6 101.1 297.1 124.5Global E&O 83.4 48.1 77.0 (7.5)Aerospace 17.6 5.5 10.7 8.7Hiscox US 6.3 4.3 35.6 0.7

Total 1,034.1 222.5 885.0 238.4

REPORT OF THE DIRECTORS OF THE MANAGING AGENT 3HISCOX SYNDICATE 33

REPORT OF THE DIRECTORS OF THE MANAGING AGENT CONTINUED 4HISCOX SYNDICATE 33

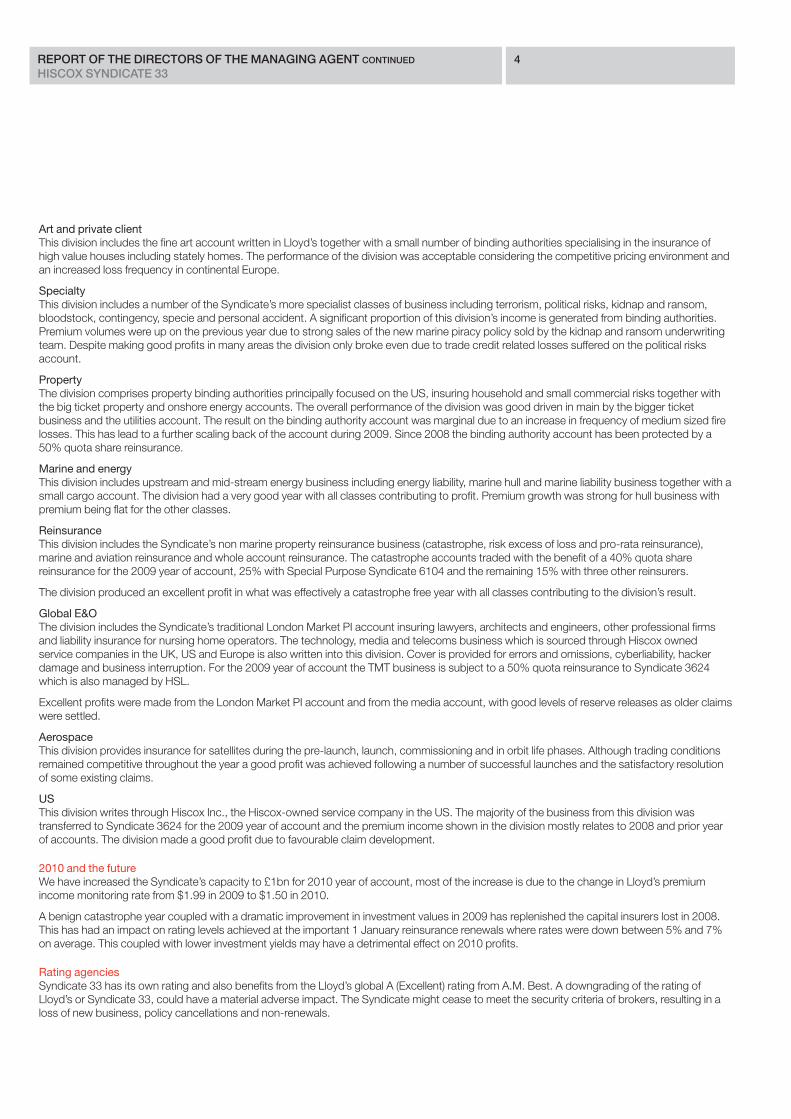

Art and private clientThis division includes the fine art account written in Lloyd’s together with a small number of binding authorities specialising in the insurance ofhigh value houses including stately homes. The performance of the division was acceptable considering the competitive pricing environment andan increased loss frequency in continental Europe.

SpecialtyThis division includes a number of the Syndicate’s more specialist classes of business including terrorism, political risks, kidnap and ransom,bloodstock, contingency, specie and personal accident. A significant proportion of this division’s income is generated from binding authorities.Premium volumes were up on the previous year due to strong sales of the new marine piracy policy sold by the kidnap and ransom underwritingteam. Despite making good profits in many areas the division only broke even due to trade credit related losses suffered on the political risksaccount.

PropertyThe division comprises property binding authorities principally focused on the US, insuring household and small commercial risks together withthe big ticket property and onshore energy accounts. The overall performance of the division was good driven in main by the bigger ticketbusiness and the utilities account. The result on the binding authority account was marginal due to an increase in frequency of medium sized firelosses. This has lead to a further scaling back of the account during 2009. Since 2008 the binding authority account has been protected by a50% quota share reinsurance.

Marine and energyThis division includes upstream and mid-stream energy business including energy liability, marine hull and marine liability business together with asmall cargo account. The division had a very good year with all classes contributing to profit. Premium growth was strong for hull business withpremium being flat for the other classes.

Reinsurance This division includes the Syndicate’s non marine property reinsurance business (catastrophe, risk excess of loss and pro-rata reinsurance),marine and aviation reinsurance and whole account reinsurance. The catastrophe accounts traded with the benefit of a 40% quota sharereinsurance for the 2009 year of account, 25% with Special Purpose Syndicate 6104 and the remaining 15% with three other reinsurers.

The division produced an excellent profit in what was effectively a catastrophe free year with all classes contributing to the division’s result.

Global E&OThe division includes the Syndicate’s traditional London Market PI account insuring lawyers, architects and engineers, other professional firmsand liability insurance for nursing home operators. The technology, media and telecoms business which is sourced through Hiscox ownedservice companies in the UK, US and Europe is also written into this division. Cover is provided for errors and omissions, cyberliability, hackerdamage and business interruption. For the 2009 year of account the TMT business is subject to a 50% quota reinsurance to Syndicate 3624which is also managed by HSL.

Excellent profits were made from the London Market PI account and from the media account, with good levels of reserve releases as older claimswere settled.

AerospaceThis division provides insurance for satellites during the pre-launch, launch, commissioning and in orbit life phases. Although trading conditionsremained competitive throughout the year a good profit was achieved following a number of successful launches and the satisfactory resolutionof some existing claims.

USThis division writes through Hiscox Inc., the Hiscox-owned service company in the US. The majority of the business from this division wastransferred to Syndicate 3624 for the 2009 year of account and the premium income shown in the division mostly relates to 2008 and prior yearof accounts. The division made a good profit due to favourable claim development.

2010 and the futureWe have increased the Syndicate’s capacity to £1bn for 2010 year of account, most of the increase is due to the change in Lloyd’s premiumincome monitoring rate from $1.99 in 2009 to $1.50 in 2010.

A benign catastrophe year coupled with a dramatic improvement in investment values in 2009 has replenished the capital insurers lost in 2008.This has had an impact on rating levels achieved at the important 1 January reinsurance renewals where rates were down between 5% and 7%on average. This coupled with lower investment yields may have a detrimental effect on 2010 profits.

Rating agenciesSyndicate 33 has its own rating and also benefits from the Lloyd’s global A (Excellent) rating from A.M. Best. A downgrading of the rating ofLloyd’s or Syndicate 33, could have a material adverse impact. The Syndicate might cease to meet the security criteria of brokers, resulting in aloss of new business, policy cancellations and non-renewals.

REPORT OF THE DIRECTORS OF THE MANAGING AGENT CONTINUED 5HISCOX SYNDICATE 33

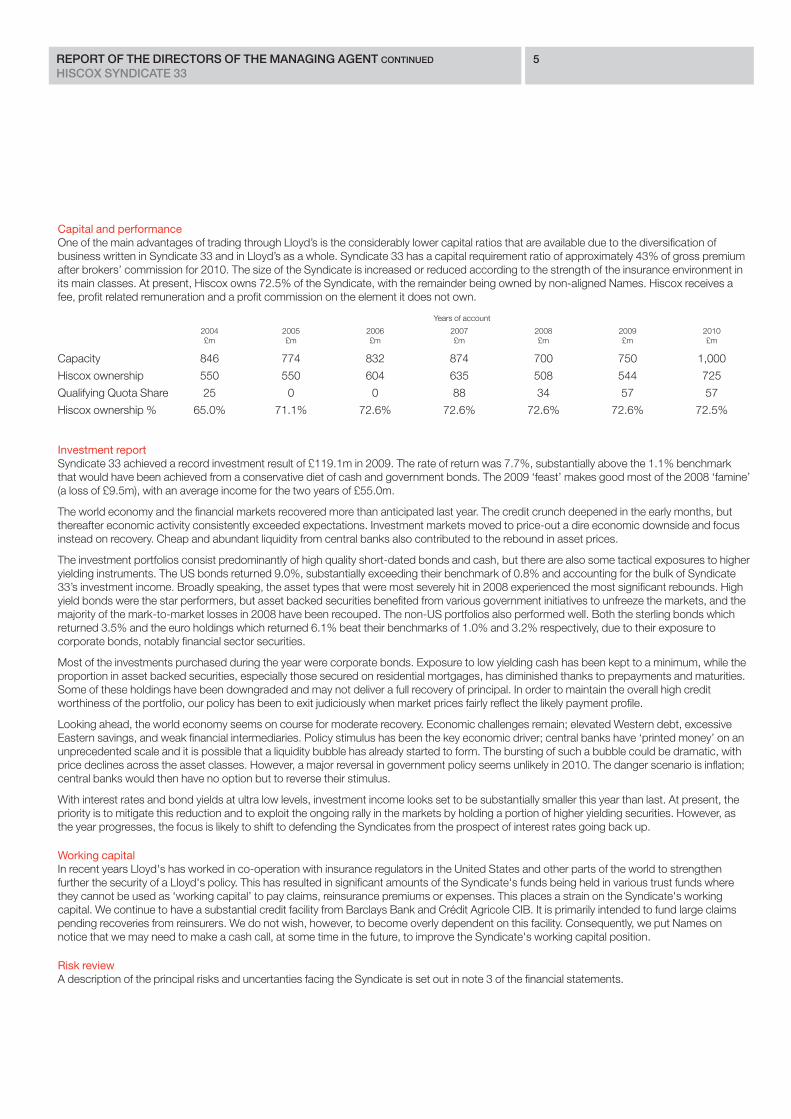

Capital and performanceOne of the main advantages of trading through Lloyd’s is the considerably lower capital ratios that are available due to the diversification ofbusiness written in Syndicate 33 and in Lloyd’s as a whole. Syndicate 33 has a capital requirement ratio of approximately 43% of gross premiumafter brokers’ commission for 2010. The size of the Syndicate is increased or reduced according to the strength of the insurance environment inits main classes. At present, Hiscox owns 72.5% of the Syndicate, with the remainder being owned by non-aligned Names. Hiscox receives afee, profit related remuneration and a profit commission on the element it does not own.

Investment reportSyndicate 33 achieved a record investment result of £119.1m in 2009. The rate of return was 7.7%, substantially above the 1.1% benchmarkthat would have been achieved from a conservative diet of cash and government bonds. The 2009 ‘feast’ makes good most of the 2008 ‘famine’(a loss of £9.5m), with an average income for the two years of £55.0m.

The world economy and the financial markets recovered more than anticipated last year. The credit crunch deepened in the early months, butthereafter economic activity consistently exceeded expectations. Investment markets moved to price-out a dire economic downside and focusinstead on recovery. Cheap and abundant liquidity from central banks also contributed to the rebound in asset prices.

The investment portfolios consist predominantly of high quality short-dated bonds and cash, but there are also some tactical exposures to higheryielding instruments. The US bonds returned 9.0%, substantially exceeding their benchmark of 0.8% and accounting for the bulk of Syndicate33’s investment income. Broadly speaking, the asset types that were most severely hit in 2008 experienced the most significant rebounds. Highyield bonds were the star performers, but asset backed securities benefited from various government initiatives to unfreeze the markets, and themajority of the mark-to-market losses in 2008 have been recouped. The non-US portfolios also performed well. Both the sterling bonds whichreturned 3.5% and the euro holdings which returned 6.1% beat their benchmarks of 1.0% and 3.2% respectively, due to their exposure tocorporate bonds, notably financial sector securities.

Most of the investments purchased during the year were corporate bonds. Exposure to low yielding cash has been kept to a minimum, while theproportion in asset backed securities, especially those secured on residential mortgages, has diminished thanks to prepayments and maturities.Some of these holdings have been downgraded and may not deliver a full recovery of principal. In order to maintain the overall high creditworthiness of the portfolio, our policy has been to exit judiciously when market prices fairly reflect the likely payment profile.

Looking ahead, the world economy seems on course for moderate recovery. Economic challenges remain; elevated Western debt, excessiveEastern savings, and weak financial intermediaries. Policy stimulus has been the key economic driver; central banks have ‘printed money’ on anunprecedented scale and it is possible that a liquidity bubble has already started to form. The bursting of such a bubble could be dramatic, withprice declines across the asset classes. However, a major reversal in government policy seems unlikely in 2010. The danger scenario is inflation;central banks would then have no option but to reverse their stimulus.

With interest rates and bond yields at ultra low levels, investment income looks set to be substantially smaller this year than last. At present, thepriority is to mitigate this reduction and to exploit the ongoing rally in the markets by holding a portion of higher yielding securities. However, asthe year progresses, the focus is likely to shift to defending the Syndicates from the prospect of interest rates going back up.

Working capitalIn recent years Lloyd's has worked in co-operation with insurance regulators in the United States and other parts of the world to strengthenfurther the security of a Lloyd's policy. This has resulted in significant amounts of the Syndicate's funds being held in various trust funds wherethey cannot be used as ‘working capital’ to pay claims, reinsurance premiums or expenses. This places a strain on the Syndicate's workingcapital. We continue to have a substantial credit facility from Barclays Bank and Crédit Agricole CIB. It is primarily intended to fund large claimspending recoveries from reinsurers. We do not wish, however, to become overly dependent on this facility. Consequently, we put Names onnotice that we may need to make a cash call, at some time in the future, to improve the Syndicate's working capital position.

Risk reviewA description of the principal risks and uncertanties facing the Syndicate is set out in note 3 of the financial statements.

Years of account

2004£m

2005 £m

2006£m

2007£m

2008£m

2009£m

2010£m

Capacity 846 774 832 874 700 750 1,000

Hiscox ownership 550 550 604 635 508 544 725

Qualifying Quota Share 25 0 0 88 34 57 57

Hiscox ownership % 65.0% 71.1% 72.6% 72.6% 72.6% 72.6% 72.5%

REPORT OF THE DIRECTORS OF THE MANAGING AGENT CONTINUED 6HISCOX SYNDICATE 33

Directors’ interestsNone of the Directors of the managing agent who served during the year ended 31 December 2009 were underwriting Names at Lloyd’s for the2007, 2008 or 2009 years of account.

R R S Hiscox (Chairman)S J BridgesD J W BruceR S Childs (appointed 21 September 2009)A G C Howland Jackson (Non Executive)J S Jones (appointed 21 September 2009)I J MartinB E MasojadaR Merrett (appointed 21 September 2009)J Pinchin (appointed 21 September 2009)S J Quick (resigned 21 August 2009)B C Ritchie (resigned 21 August 2009)I N Thomson (Non Executive)N B TylerR C WatsonI T Webb-Wilson (Non Executive)

K Silverwood became Company Secretary in place of J S Jones on 21 September 2009.

Statement of managing agent’s responsibilitiesThis statement is set out on page 7 of these accounts.

Disclosure of information to the auditorsThe Directors of the managing agent who held office at the date of approval of this managing agent’s report confirm that, so far as they areeach aware, there is no relevant audit information of which the Syndicate’s auditors are unaware; and each Director has taken all the stepsthat they ought to have taken as a Director to make themselves aware of any relevant audit information and to establish that the Syndicate’sauditors are aware of that information.

AuditorsThe managing agent proposes the re-appointment of KPMG Audit Plc as the Syndicate auditors.

By order of the Board

I J MartinDirector10 March 2010

STATEMENT OF MANAGING AGENT’S RESPONSIBILITIES 7HISCOX SYNDICATE 33

The managing agent is responsible for preparing the Syndicate Annual Report and Accounts in accordance with applicable law and regulations.

The Insurance Accounts Directive (Lloyd’s Syndicate and Aggregate Accounts) Regulations 2008 require the managing agent to prepare Syndicate annual accounts at 31 December each year in accordance with UK accounting standards and applicable law (UK GenerallyAccepted Accounting Practice). The annual accounts are required by law to give a true and fair view of the state of affairs of the Syndicate as at that date and of its profit or loss for that year.

In preparing those Syndicate annual accounts, the managing agent is required to:

1. select suitable accounting policies which are applied consistently, subject to changes arising on the adoption of new accounting standards in the year;

2. make judgements and estimates that are reasonable and prudent;

3. state whether applicable accounting standards have been followed, subject to any material departures disclosed and explained in the annual accounts; and

4. prepare the annual accounts on the basis that the Syndicate will continue to write future business unless it is inappropriate to presume the Syndicate will do so.

The managing agent is responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financialposition of the Syndicate and enable it to ensure that the Syndicate annual accounts comply with the 2008 Regulations. It is also responsiblefor safeguarding the assets of the Syndicate and hence for taking reasonable steps for prevention and detection of fraud and other irregularities.

The managing agent is responsible for the maintenance and integrity of the corporate and financial information included on the company’swebsite. Legislation in the UK governing the preparation and dissemination of financial statements may differ from legislation in otherjurisdictions.

Usually the only formal business conducted at the Syndicate Annual General Meeting (AGM) is the appointment of the Syndicate auditors forthe following year, and usually the attendance at the AGM, when it is held, is minimal.

In accordance with the Insurance Accounts Directive (Lloyd’s Syndicate and Aggregate Accounts) Regulations 2008 (‘the 2008 Regulations’) a Syndicate AGM was held in 2009 to appoint KPMG Audit Plc as the Syndicate’s registered auditor. The 2008 Regulations allow managingagents to dispense with the requirement to hold a Syndicate AGM and contain provisions for the reappointment of the auditor providing certain criteria are met.

This year, we therefore give notice that:

1. Hiscox Syndicates Limited does not propose to hold an AGM of the members of Syndicate 33 in 2010;

2. we propose that KPMG Audit Plc are re-appointed as the Syndicate’s registered auditor for the period of one year from the date of this Annual Report;

3. members may object to the matters set out above within 21 days of this notice.

If no objections to these proposals are received from any member within the specified period we shall notify Lloyd’s to that effect.

If any objections are received, depending on the level or nature of such objections, we shall then consider whether to:

1. apply for Lloyd’s consent not to hold an AGM, stating the reasons why not. Lloyd’s may give its consent subject to any such conditions and requirements as it may determine;

or

2. convene an AGM.

By order of the Board

J S JonesDirector10 March 2010

NOTICE REGARDING THE ANNUAL GENERAL MEETING 8HISCOX SYNDICATE 33

INDEPENDENT AUDITORS’ REPORT 9TO THE MEMBERS OF SYNDICATE 33

We have audited the annual accounts of Syndicate 33 for the year ended 31 December 2009 which comprise the profit and loss account, thebalance sheet, the statement of cash flow and the related notes 1 to 23. The Syndicate annual accounts have been prepared under theaccounting policies set out therein.

This report is made solely to the members of the Syndicate, as a body, in accordance with the Insurance Accounts Directive (Lloyd’s Syndicateand Aggregate Accounts) Regulations 2008. Our audit work has been undertaken so that we might state to the Syndicate’s members thosematters we are required to state in an auditors’ report and for no other purpose. To the fullest extent permitted by law, we do not accept orassume responsibility to anyone other than the Syndicate’s members as a body for our audit work, for this report, or for the opinions we haveformed.

Respective responsibilities of managing agent and auditors The managing agent’s responsibilities for preparing the Syndicate annual accounts in accordance with applicable law and UK AccountingStandards (UK Generally Accepted Accounting Practice) are set out in the statement of managing agent’s responsibilities on page 7.

Our responsibility is to audit the Syndicate annual accounts in accordance with relevant legal and regulatory requirements and InternationalStandards on Auditing (UK and Ireland).

We report to you our opinion as to whether the Syndicate annual accounts give a true and fair view and have been properly prepared in accordancewith the Insurance Accounts Directive (Lloyd’s Syndicate and Aggregate Accounts) Regulations 2008. We also report to you whether in ouropinion the managing agent’s report is consistent with the Syndicate annual accounts.

In addition we report to you if, in our opinion, the managing agent has not kept proper accounting records in respect of that Syndicate, if theSyndicate annual accounts are not in agreement with the accounting records, if we have not received all the information and explanations werequire for our audit, or if information specified by law regarding remuneration of the Directors of the managing agent and other transactions is not disclosed.

We read the other information attached to the Syndicate annual accounts and consider the implications for our report if we become aware of any apparent misstatements or material inconsistencies with the Syndicate annual accounts. Our responsibilities do not extend to any otherinformation.

Basis of audit opinion We conducted our audit in accordance with International Standards on Auditing (UK and Ireland) issued by the Auditing Practices Board. An auditincludes examination, on a test basis, of evidence relevant to the amounts and disclosures in the Syndicate annual accounts. It also includes anassessment of the significant estimates and judgments made by the managing agent in the preparation of the Syndicate annual accounts, and of whether the accounting policies are appropriate to the Syndicate's circumstances, consistently applied and adequately disclosed.

We planned and performed our audit so as to obtain all the information and explanations which we considered necessary in order to provide uswith sufficient evidence to give reasonable assurance that the Syndicate annual accounts are free from material misstatement, whether causedby fraud or other irregularity or error. In forming our opinion we also evaluated the overall adequacy of the presentation of information in theSyndicate annual accounts.

Opinion In our opinion:

• the Syndicate annual accounts give a true and fair view in accordance with UK Generally Accepted Accounting Practice of the state of Syndicate 33’s affairs as at 31 December 2009 and of its profit for the year then ended;

• the Syndicate annual accounts have been properly prepared in accordance with the Insurance Accounts Directive (Lloyd’s Syndicate and Aggregate Accounts) Regulations 2008; and

• the information given in the managing agent’s report is consistent with the Syndicate annual accounts.

S Tharani (Senior Statutory Auditor) For and on behalf of KPMG Audit Plc, Statutory Auditor Chartered Accountants Registered Auditor 8 Salisbury SquareLondon, EC4Y 8BB10 March 2010

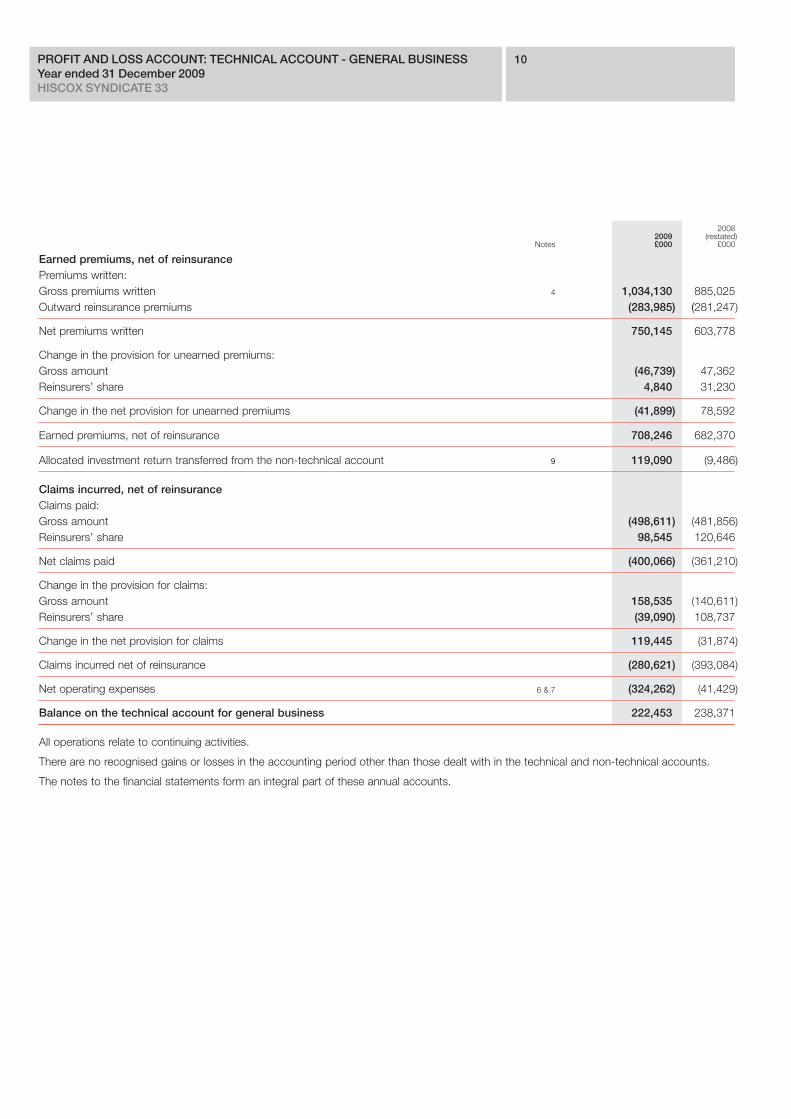

PROFIT AND LOSS ACCOUNT: TECHNICAL ACCOUNT - GENERAL BUSINESS 10Year ended 31 December 2009HISCOX SYNDICATE 33

20082009 (restated)

Notes £000 £000

Earned premiums, net of reinsurancePremiums written:Gross premiums written 4 1,034,130 885,025Outward reinsurance premiums (283,985) (281,247)

Net premiums written 750,145 603,778

Change in the provision for unearned premiums:Gross amount (46,739) 47,362Reinsurers’ share 4,840 31,230

Change in the net provision for unearned premiums (41,899) 78,592

Earned premiums, net of reinsurance 708,246 682,370

Allocated investment return transferred from the non-technical account 9 119,090 (9,486)

Claims incurred, net of reinsuranceClaims paid:Gross amount (498,611) (481,856)Reinsurers’ share 98,545 120,646

Net claims paid (400,066) (361,210)

Change in the provision for claims:Gross amount 158,535 (140,611)Reinsurers’ share (39,090) 108,737

Change in the net provision for claims 119,445 (31,874)

Claims incurred net of reinsurance (280,621) (393,084)

Net operating expenses 6 & 7 (324,262) (41,429)

Balance on the technical account for general business 222,453 238,371

All operations relate to continuing activities.

There are no recognised gains or losses in the accounting period other than those dealt with in the technical and non-technical accounts.

The notes to the financial statements form an integral part of these annual accounts.

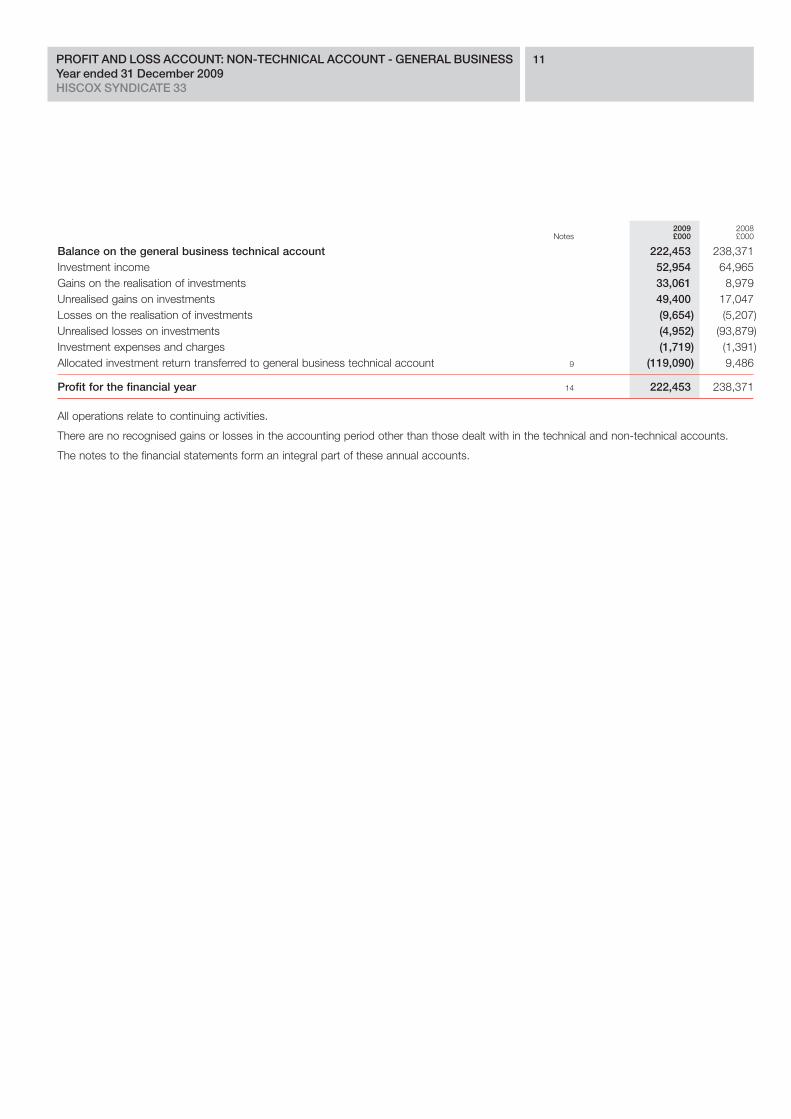

PROFIT AND LOSS ACCOUNT: NON-TECHNICAL ACCOUNT - GENERAL BUSINESS 11Year ended 31 December 2009HISCOX SYNDICATE 33

2009 2008Notes £000 £000

Balance on the general business technical account 222,453 238,371Investment income 52,954 64,965Gains on the realisation of investments 33,061 8,979Unrealised gains on investments 49,400 17,047Losses on the realisation of investments (9,654) (5,207)Unrealised losses on investments (4,952) (93,879)Investment expenses and charges (1,719) (1,391)Allocated investment return transferred to general business technical account 9 (119,090) 9,486

Profit for the financial year 14 222,453 238,371

All operations relate to continuing activities.

There are no recognised gains or losses in the accounting period other than those dealt with in the technical and non-technical accounts.

The notes to the financial statements form an integral part of these annual accounts.

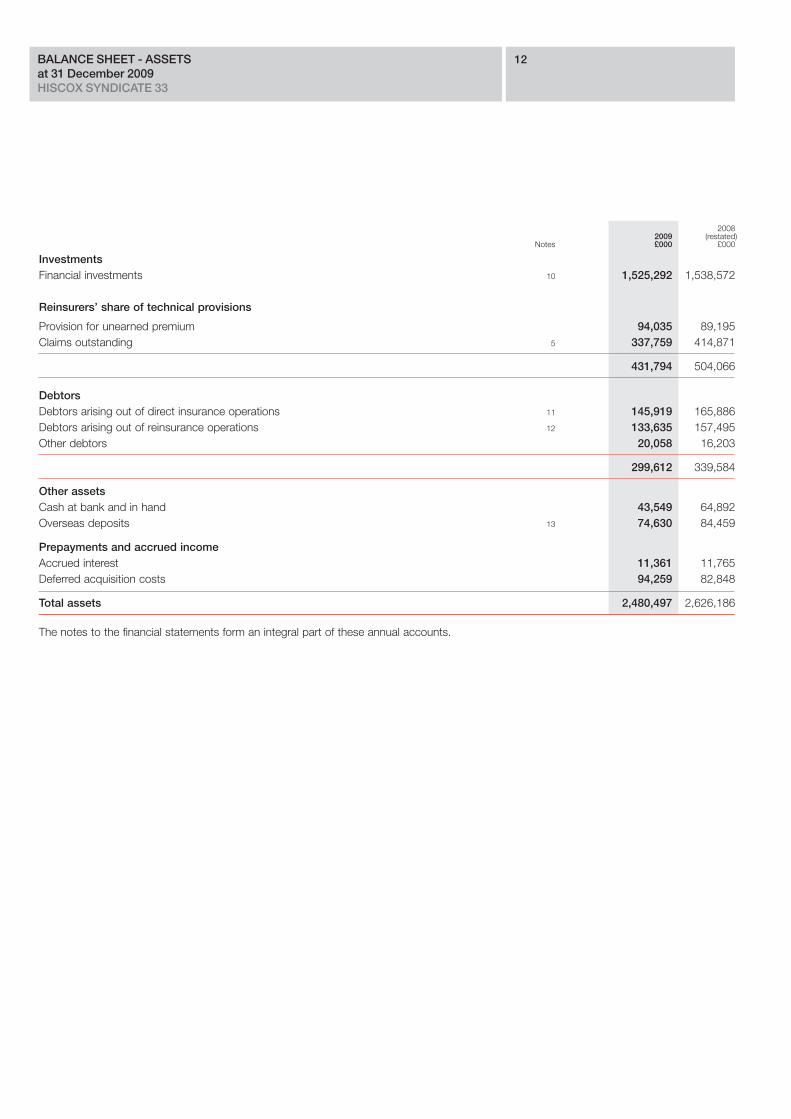

BALANCE SHEET - ASSETS 12at 31 December 2009HISCOX SYNDICATE 33

20082009 (restated)

Notes £000 £000

InvestmentsFinancial investments 10 1,525,292 1,538,572

Reinsurers’ share of technical provisions

Provision for unearned premium 94,035 89,195Claims outstanding 5 337,759 414,871

431,794 504,066

DebtorsDebtors arising out of direct insurance operations 11 145,919 165,886Debtors arising out of reinsurance operations 12 133,635 157,495Other debtors 20,058 16,203

299,612 339,584

Other assetsCash at bank and in hand 43,549 64,892Overseas deposits 13 74,630 84,459

Prepayments and accrued incomeAccrued interest 11,361 11,765Deferred acquisition costs 94,259 82,848

Total assets 2,480,497 2,626,186

The notes to the financial statements form an integral part of these annual accounts.

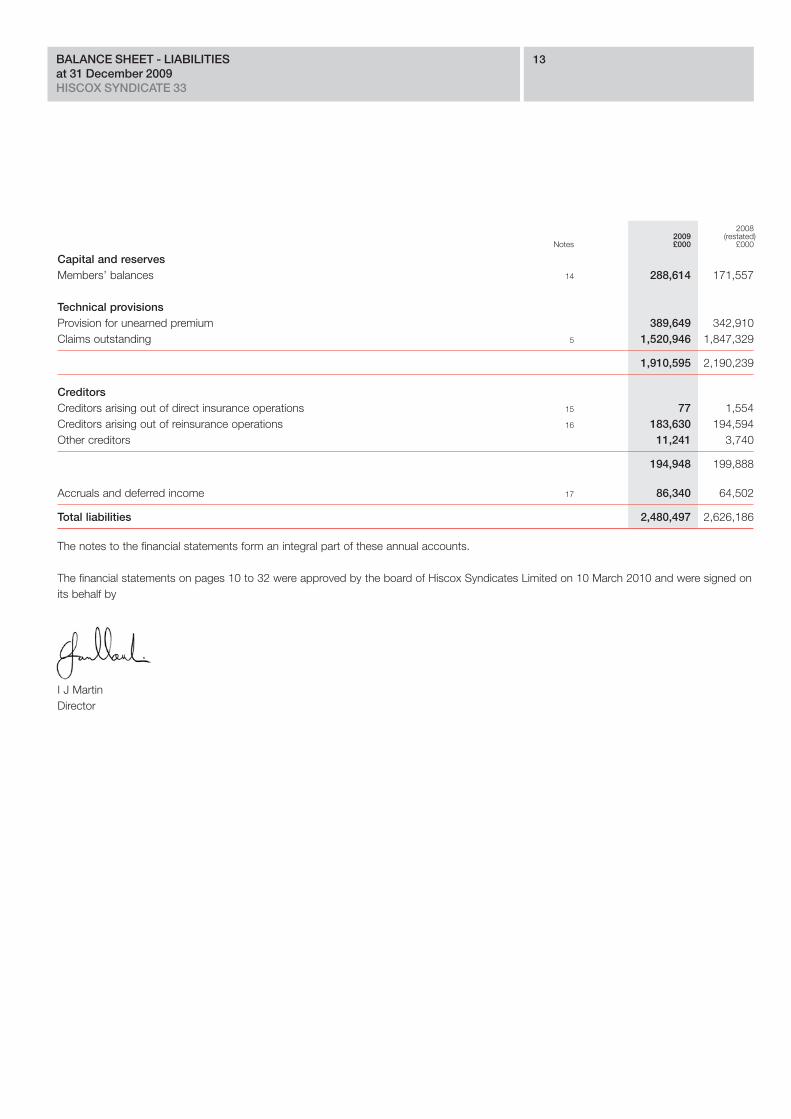

BALANCE SHEET - LIABILITIES 13at 31 December 2009HISCOX SYNDICATE 33

20082009 (restated)

Notes £000 £000

Capital and reservesMembers’ balances 14 288,614 171,557

Technical provisionsProvision for unearned premium 389,649 342,910Claims outstanding 5 1,520,946 1,847,329

1,910,595 2,190,239

CreditorsCreditors arising out of direct insurance operations 15 77 1,554Creditors arising out of reinsurance operations 16 183,630 194,594Other creditors 11,241 3,740

194,948 199,888

Accruals and deferred income 17 86,340 64,502

Total liabilities 2,480,497 2,626,186

The notes to the financial statements form an integral part of these annual accounts.

The financial statements on pages 10 to 32 were approved by the board of Hiscox Syndicates Limited on 10 March 2010 and were signed onits behalf by

I J MartinDirector

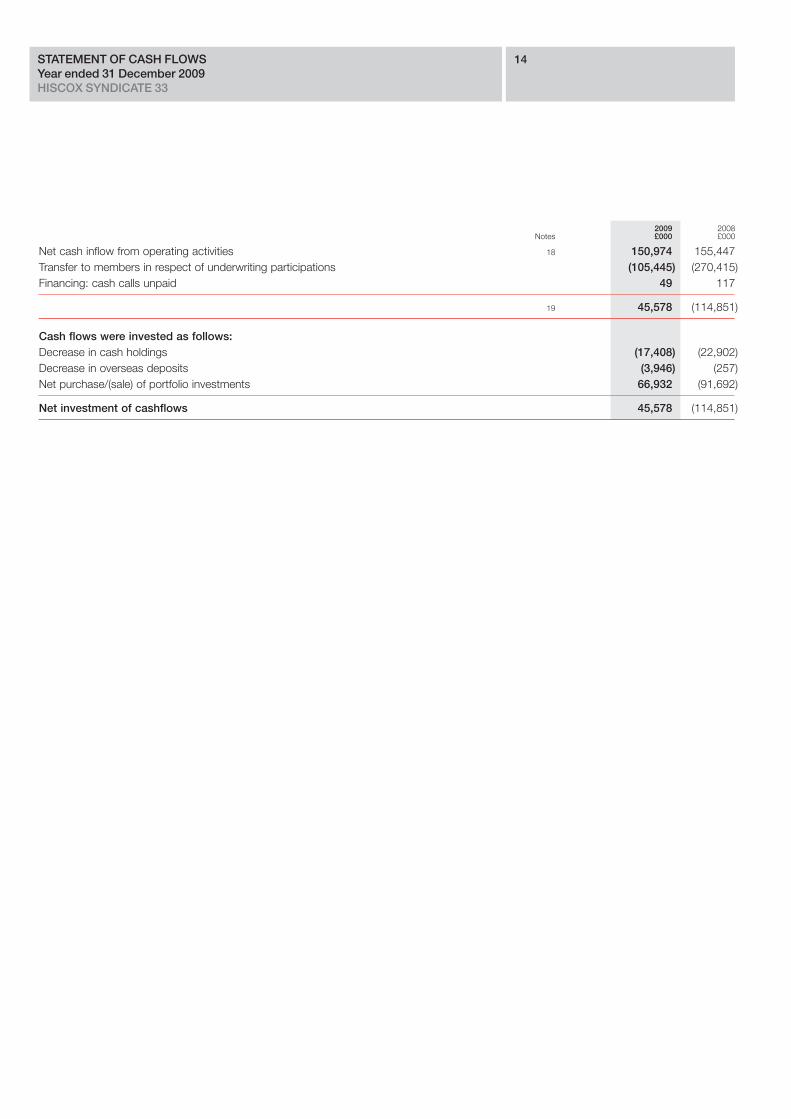

STATEMENT OF CASH FLOWS 14Year ended 31 December 2009HISCOX SYNDICATE 33

2009 2008Notes £000 £000

Net cash inflow from operating activities 18 150,974 155,447Transfer to members in respect of underwriting participations (105,445) (270,415)Financing: cash calls unpaid 49 117

19 45,578 (114,851)

Cash flows were invested as follows:Decrease in cash holdings (17,408) (22,902)Decrease in overseas deposits (3,946) (257)Net purchase/(sale) of portfolio investments 66,932 (91,692)

Net investment of cashflows 45,578 (114,851)

NOTES TO THE FINANCIAL STATEMENTS 15at 31 December 2009HISCOX SYNDICATE 33

1 Basis of preparationThese financial statements have been prepared in accordance with the Insurance Accounts Directive (Lloyd’s Syndicate and AggregateAccounts) Regulations 2008 and applicable Accounting Standards in the United Kingdom, and comply with the Statement of RecommendedPractice on Accounting for Insurance Business issued by the Association of British Insurers in December 2006.

2 Accounting policiesThe principal accounting policies have been applied consistently in dealing with items which are considered material in relation to theSyndicate’s financial statements, with the exception of reinsurers’ commissions and profit participations for which the accounting policy hasbeen amended in 2009 to better reflect the underlying transaction. This adjustment has no impact on profit for the financial year or capital andreserves. The 2008 comparative figures have been restated to reflect this new policy.

2(a) PremiumsWritten gross and outwards reinsurance premiums comprise premiums on contracts incepting during the financial year. Written premiums aredisclosed gross of commission payable to intermediaries and exclude taxes and duties levied on premiums.

Outwards reinsurance premiums are also disclosed gross of commissions and profit participations recoverable from reinsurers.

Premiums written include estimates for ‘pipeline’ premiums and adjustments to premiums written in prior accounting periods.

2(b) Unearned premiumsThe provision for unearned premium comprises the proportion of gross and outwards reinsurance premiums written, which is estimated to beearned in the following or subsequent financial years, computed separately for each insurance contract using the daily pro-rata method.

2(c) Acquisition costsAcquisition costs comprise all direct and indirect costs arising from the acquisition of insurance contracts. Deferred acquisition costs represent the proportion of acquisition costs incurred which corresponds to the proportion of gross premiums written which is unearned atthe balance sheet date.

2(d) ClaimsClaims incurred in respect of general business consist of claims and claims handling expenses paid during the financial year, together with themovement in the provision for outstanding claims and future claims handling expenses.

Outstanding claims comprise provisions for the estimated cost of settling all claims incurred but unpaid up to the balance sheet date whetherreported or not, together with related claims handling expenses. Anticipated reinsurance recoveries, and estimates of salvage and subrogationrecoveries, are disclosed separately as assets.

Whilst the Directors consider that the gross provisions for claims and the related reinsurance recoveries are fairly stated on the basis of theinformation currently available to them, the ultimate liability will vary as a result of subsequent information and events and may result in significant adjustments to the amounts provided. Adjustments to the amounts of claims provisions established in prior years are reflected inthe financial statements for the period in which the adjustments are made. The methods used and estimates made are reviewed regularly.

The provision for outstanding claims for the Syndicate is actuarially calculated using both the Chain Ladder and Bornhuetter-Ferguson methods. There is close communication between the actuaries and underwriters and allowance is made for the rating environment.

The Chain Ladder method is adopted where sufficient development data is available in order to produce estimates of the ultimate claims andpremiums by actuarial reserving group and year of account for the managed Syndicate. This methodology produces optimal estimates when alarge claims development history is available and the claims development patterns throughout the earliest years are stable.

Where losses in the earlier underwriting years have yet to fully develop, a 'tail' arises on the reserving data i.e. a gap between the current stage ofdevelopment and the fully developed amount. The Chain Ladder methodology is used to calculate average development factors which, by fittingthese development factors to a curve, allows an estimate to be made of the potential claims development expected between the current and thefully developed amount, known as a 'tail reserve'. This tail reserve is added to the current reserve position to calculate the total reserve required.

The Bornhuetter-Ferguson method is predominantly employed to produce ultimate loss estimates when there is little development data available e.g. in relation to more recent underwriting years. The Bornhuetter-Ferguson method is based on the Chain Ladder approach bututilises estimated ultimate loss ratios. In exceptional cases the required provision is calculated with reference to the actual exposures.

Ultimate premium and claims amounts are projected both gross and net of reinsurance using reinsurance recovery rates based on historicalexperience, adjusted for the current reinsurance programme.

Reinsurance security is monitored continuously throughout the year involving both external sources, such as Standard & Poor's and A.M.Best's rating information on reinsurers, and internal sources. Reinsurer default rates are applied to the expected future reinsurance recoveriesto determine a suitable level of bad debt provision.

Adjustments are made within the reserving methodology to remove distortions in the historical claims development patterns from large claimsnot expected to reoccur in the future.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 16at 31 December 2009HISCOX SYNDICATE 33

2 Accounting policies (continued)2(e) Unexpired riskProvision is made for unexpired risks arising from general business where the expected value of the claims and expenses attributable to theunexpired periods of policies in force at the balance sheet date exceeds the unearned premiums provision in relation to such policies after thededuction of any acquisition costs deferred. The provision for unexpired risks is calculated separately by classes of business which are managed together, after taking into account the relevant investment return.

2(f) InvestmentsThe Syndicate has classified its investments as financial assets at fair value through profit or loss. Management determines the classification of its investments at initial recognition. The decision by the Syndicate to designate its investments at fair value through profit or loss reflectsthe fact that the investment portfolios are managed, and their performance evaluated, on a fair value basis. Regular purchases and sales ofinvestments are accounted for at the date of trade.

A financial asset is classified into this category at inception if acquired principally for the purpose of selling in the short-term, if it forms part ofa portfolio of financial assets in which there is evidence of short-term profit taking. Listed investments comprise those quoted on the Londonand other International Stock Exchanges. Investments are stated at closing bid-market prices at the balance sheet date, or on the last stockexchange trading day before the balance sheet date.

In the case of financial instruments for which the market is no longer active or indicators of forced transactions exist, the fair value is determinedusing selected valuation techniques (including net present value techniques, the discounted cash flow method, comparison to similar instrumentsand valuation models). The valuation techniques use market observable inputs, where available, derived from similar assets in similar andactive markets, from recent transaction prices for comparable items and from other observable market data. The models are calibrated toestimate the price at which an orderly transaction would take place between market participants on the reporting date, taking into accountcurrent market conditions and applying appropriate risk adjustments. As a result the valuation techniques involve a considerable amount ofmanagement judgement. This is addressed by controls over the valuation process, including a review of the valuation results by senior management, verification of assumptions made and scrutinising the adjustments to fair values resulting from considerations of additional riskfactors.

2(g) Investment returnAll investment return is initially recognised in the non-technical account. It is then transferred to the technical account as it all relates to fundssupporting underwriting business.

Dividends on ordinary shares are recognised as income on the date the ordinary shares are marked ex-dividend. Other investment incomeand interest receivable are included in income on an accruals basis.

Realised gains or losses on investments represent the difference between net sales proceeds and their purchase price or their valuation at thecommencement of the year.

Unrealised gains and losses on investments represent the difference between the fair value of investments at the balance sheet date and their purchase price or their valuation at the commencement of the year. The movement in unrealised investment gains/losses includes an adjustment for previously recognised unrealised gains/losses on investments disposed of in the accounting period.

2(h) Rates of exchangeThe functional currency of the Syndicate is Pound Sterling. Assets, liabilities, revenues and costs denominated in foreign currencies arerecorded at the rates of exchange ruling at the dates of the transactions. At the balance sheet date, monetary assets and liabilities are translated at the year end rates of exchange. Unearned premiums and deferred acquisition costs are non monetary assets and liabilities andaccordingly are not retranslated from the historic rates. Exchange profits or losses arising on the translation of foreign currency amounts relating to the Syndicate insurance operations are included within net operating expenses in the technical account.

2(i) TaxationUnder Schedule 19 of the Finance Act 1993 managing agents are not required to deduct basic rate income tax from trading income. In addition, all UK basic rate income tax deducted from Syndicate investment income is recoverable by managing agents and consequently thedistribution made to members or their members’ agents is gross of tax. Capital appreciation falls within trading income and is also distributedgross of tax.

No provision has been made for any United States Federal Income Tax payable on underwriting results or investment earnings. Any paymentson account made by the Syndicate during the year are included in the balance sheet under the heading ‘other debtors’.

No provision has been made for any overseas tax payable by members on underwriting results.

2(j) Pension costsThe Hiscox Group operates a defined benefit pension scheme and a defined contribution pension scheme. The accrual of benefits for activemembers of the defined benefit scheme ceased on 31 December 2006. Pension contributions relating to Syndicate staff are charged to theSyndicate and included within net operating expenses. Movements in surpluses or deficits on the defined benefit pension scheme, on anFRS17 basis, that relate to the managed Syndicate are allocated equally between all open and constituted years of account.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 17at 31 December 2009HISCOX SYNDICATE 33

2(k) Profit commissionProfit commission is charged by the managing agent at a standard rate of 12.5%. This calculation is subject to the operation of a two-yeardeficit clause. An additional 2.5% profit commission is charged on the 2008 and subsequent years of account if target levels of profit areachieved.

2(l) Impairment of assetsAssets that have an indefinite useful life are not subject to amortisation and are tested annually or whenever there is an indication of impairment.Assets that are subject to amortisation are reviewed for impairment whenever events or changes in circumstances indicate that the carryingamount may not be recoverable.

(a) Non-financial assetsObjective factors that are considered when determining whether a non-financial asset may be impaired include, but are not limited to, the following:

• adverse economic, regulatory or environmental conditions that may restrict future cash flows and asset usage and/or recoverability;

• the likelihood of accelerated obsolescence arising from the development of new technologies and products; and

• the disintegration of the active market(s) to which the asset is related.

(b) Financial assetsObjective factors that are considered when determining whether a financial asset or group of financial assets may be impaired include, but are not limited to, the following:

• negative rating agency announcements in respect of investment issuers, reinsurers and debtors;

• significant reported financial difficulties of investment issuers, reinsurers and debtors;

• actual breaches of credit terms such as persistent late payments or actual default;

• the disintegration of the active market(s) in which a particular asset is traded or deployed;

• adverse economic or regulatory conditions that may restrict future cash flows and asset recoverability; and

• the withdrawal of any guarantee from statutory funds or sovereign agencies implicitly supporting the asset.

(c) Impairment lossAn impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. For the purpose of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows.

Where an impairment loss subsequently reverses, the carrying amount of the asset is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset in prior periods. A reversal of an impairment loss is recognised as income immediately.

2(m) Bad debtsBad debts are provided for only where specific information is available to suggest a debtor may be unable or unwilling to settle its debt to theSyndicate. The provision is calculated on a case-by-case basis.

2(n) Reinsurers' commissions and profit participationsReinsurers' commissions and profit participations, which include reinsurance profit commission and overriders, have been treated as a contribution to expenses, rather than as a premium adjustment as was the case in prior years.

3. Risk reviewThe major risks and uncertainties that the Syndicate faces are presented below. A number of these factors are common to all insurancebusinesses, while others are relevant to the Syndicate specifically.

Catastrophe and systemic insurance lossesIn common with other insurers, the Syndicate’s earnings can be affected by unpredictable events and circumstances. These may include, butare not limited to, conditions such as natural and other catastrophes, legal developments, social change and the emergence of latent risks.Such events could create significant levels of losses if the Syndicate’s underwriting models, aggregation tools and policy wordings do notprevent unplanned concentrations of risk, both in geographical regions and types of policy. Robust risk management and loss mitigationtechniques are employed to minimise this risk, including underwriting models, aggregation tools and policy wordings to prevent unplannedconcentrations of risk.

Competition and the insurance cycleThe Syndicate competes against major international groups with similar offerings. At times, a minority of these groups may choose to underwritefor cash flow or market share purposes and at prices that sometimes fall short of the suggested breakeven technical price. In common with allinsurers, the Syndicate is exposed to this price volatility. Accordingly, prolonged periods of low premium rating levels or high levels of competitionin the insurance markets are likely to have a negative impact on the Syndicate’s financial performance. The Syndicate monitors price levels on acontinuous basis and is firm in its resolve to reject business that is unlikely to generate underwriting profits.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 18at 31 December 2009HISCOX SYNDICATE 33

Binding authorities and other outsourcingThe Syndicate writes a considerable amount of premium income through agents to whom binding authority is given to accept risks on behalf of the Syndicate. All delegations are strictly controlled through tight underwriting guidelines and limits and extensive monitoring, review andauditing of the agencies. However, as there is no absolute guarantee that an agent will comply with the terms of its authority, the Syndicate couldbe exposed to unanticipated losses. Other business areas where the Syndicate is to some extent reliant on the timely and effective supply ofservices from third parties include back office policy processing, data entry and cash collection.

Credit risk with reinsurance counterpartiesThe Syndicate has exposure to credit risk, which is the risk that a counterparty will suffer a deterioration in solvency or be unable to pay amountsin full when due.

Key areas of exposure to credit risk include:– reinsurers’ share of insurance liabilities;– amounts due from reinsurers in respect of claims already paid;– amounts due from insurance contract holders;– amounts due from insurance intermediaries; and– counterparty risk with respect to investments and other deposits.

The Syndicate’s maximum exposure to credit risk is represented by the carrying values of monetary assets and reinsurance assets included in the balance sheet. The Syndicate structures the levels of credit risk accepted by placing limits on their exposure to a single counterparty, orgroups of counterparties, and to geographical and industry segments. Such risks are subject to an annual or more frequent review. There is nosignificant concentration of credit risk with respect to loans and receivables, as the Syndicate has a large number of internationally disperseddebtors with unrelated operations.

The Syndicate purchases reinsurance protection to contain exposure from single claims and the aggregation of claims from catastrophic events. If a reinsurer fails to pay a claim for any reason, the Syndicate remains liable for the payment to the policyholder. The creditworthiness of reinsurersis therefore continually reviewed throughout the year. The Syndicate’s experience of bad debt losses arising from its reinsurance arrangementscompares favourably with industry averages. The agency has established a reinsurance security committee which assesses and is required toapprove all new reinsurers before business is placed with them.

The Syndicate also mitigates credit counterparty risk by concentrating debt and fixed income investments in high quality instruments, including aparticular emphasis on government bonds and municipal agency instruments issued mainly by European Union and North American countries.

Exposure to credit riskThe carrying amount of financial assets and reinsurance assets represents the maximum credit risk exposed.

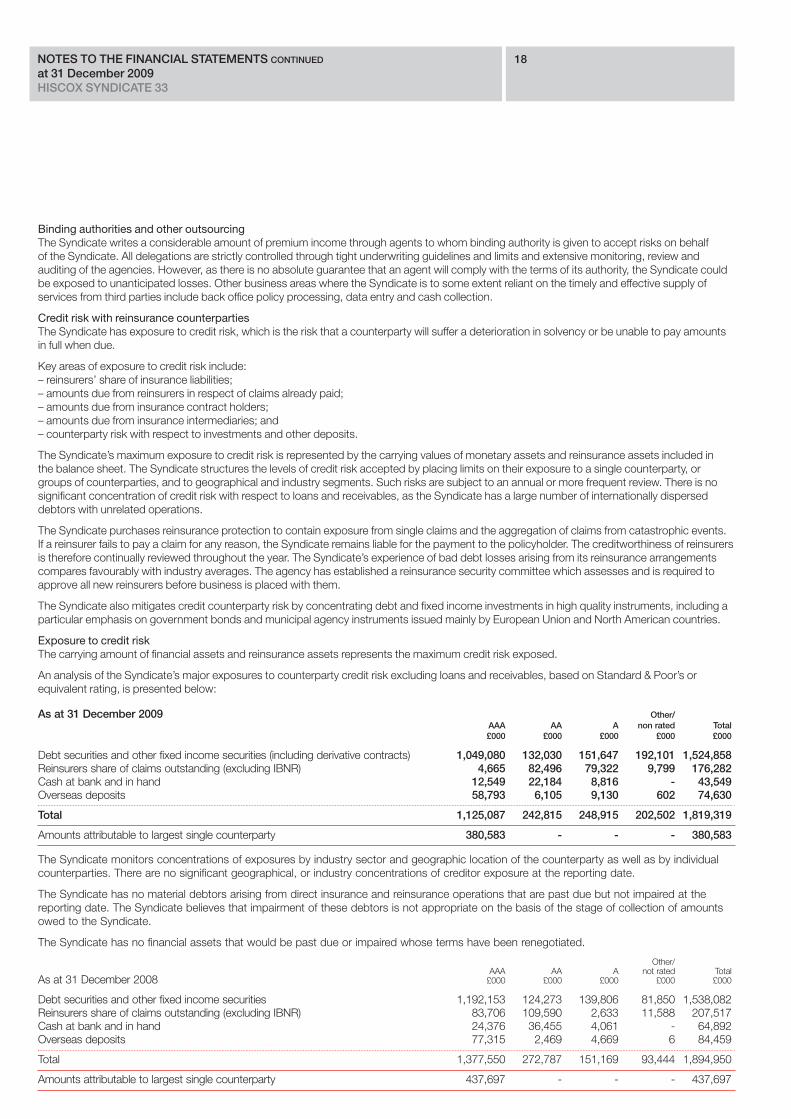

An analysis of the Syndicate’s major exposures to counterparty credit risk excluding loans and receivables, based on Standard & Poor’s orequivalent rating, is presented below:

As at 31 December 2009 Other/AAA AA A non rated Total£000 £000 £000 £000 £000

Debt securities and other fixed income securities (including derivative contracts) 1,049,080 132,030 151,647 192,101 1,524,858Reinsurers share of claims outstanding (excluding IBNR) 4,665 82,496 79,322 9,799 176,282Cash at bank and in hand 12,549 22,184 8,816 - 43,549Overseas deposits 58,793 6,105 9,130 602 74,630

Total 1,125,087 242,815 248,915 202,502 1,819,319

Amounts attributable to largest single counterparty 380,583 - - - 380,583

The Syndicate monitors concentrations of exposures by industry sector and geographic location of the counterparty as well as by individual counterparties. There are no significant geographical, or industry concentrations of creditor exposure at the reporting date.

The Syndicate has no material debtors arising from direct insurance and reinsurance operations that are past due but not impaired at the reporting date. The Syndicate believes that impairment of these debtors is not appropriate on the basis of the stage of collection of amounts owed to the Syndicate.

The Syndicate has no financial assets that would be past due or impaired whose terms have been renegotiated.

Other/AAA AA A not rated Total

As at 31 December 2008 £000 £000 £000 £000 £000

Debt securities and other fixed income securities 1,192,153 124,273 139,806 81,850 1,538,082Reinsurers share of claims outstanding (excluding IBNR) 83,706 109,590 2,633 11,588 207,517Cash at bank and in hand 24,376 36,455 4,061 - 64,892Overseas deposits 77,315 2,469 4,669 6 84,459

Total 1,377,550 272,787 151,169 93,444 1,894,950

Amounts attributable to largest single counterparty 437,697 - - - 437,697

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 19at 31 December 2009HISCOX SYNDICATE 33

At 31 December 2009 the Syndicate held no material financial assets that were past due or impaired, either for the current period under review or on a cumulative basis (2008: £nil). For the current and prior periods under review, all of the maturing financial assets settled on their original contractual terms and payment dates, and the Syndicate therefore experienced no losses of, or delays in recovering, principal amounts invested.

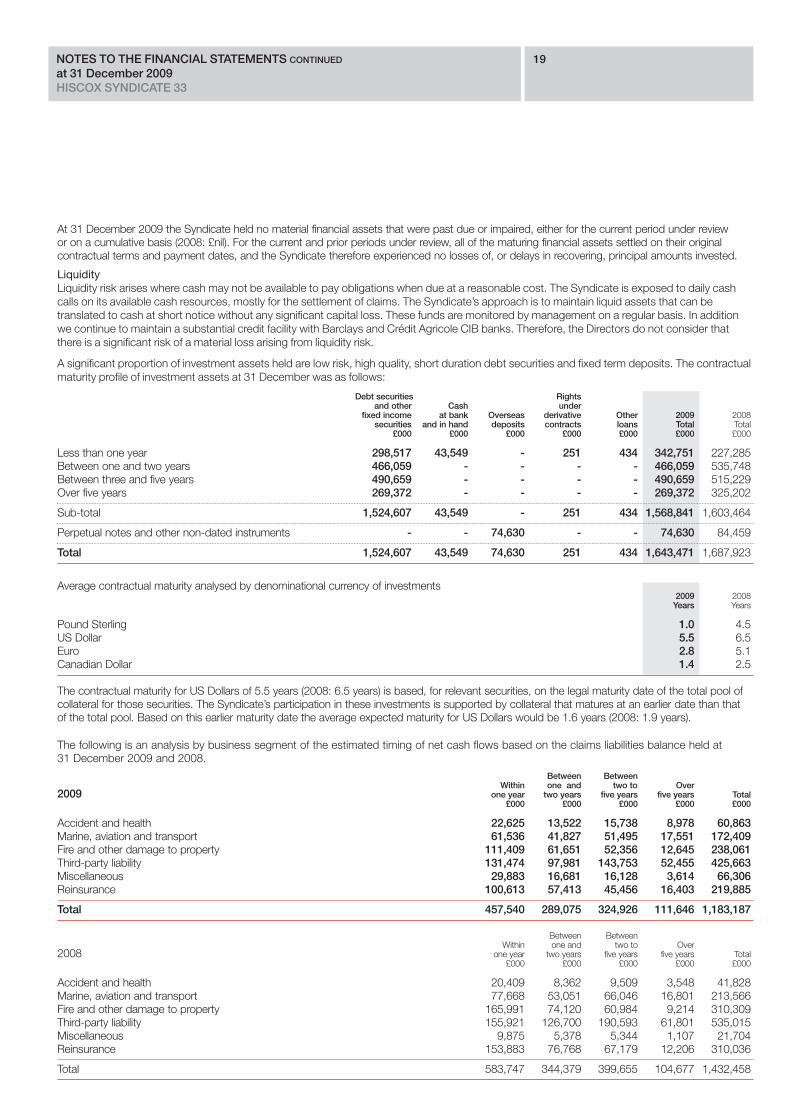

LiquidityLiquidity risk arises where cash may not be available to pay obligations when due at a reasonable cost. The Syndicate is exposed to daily cashcalls on its available cash resources, mostly for the settlement of claims. The Syndicate’s approach is to maintain liquid assets that can betranslated to cash at short notice without any significant capital loss. These funds are monitored by management on a regular basis. In additionwe continue to maintain a substantial credit facility with Barclays and Crédit Agricole CIB banks. Therefore, the Directors do not consider thatthere is a significant risk of a material loss arising from liquidity risk.

A significant proportion of investment assets held are low risk, high quality, short duration debt securities and fixed term deposits. The contractualmaturity profile of investment assets at 31 December was as follows:

Debt securities Rightsand other Cash under

fixed income at bank Overseas derivative Other 2009 2008securities and in hand deposits contracts loans Total Total

£000 £000 £000 £000 £000 £000 £000

Less than one year 298,517 43,549 - 251 434 342,751 227,285Between one and two years 466,059 - - - - 466,059 535,748Between three and five years 490,659 - - - - 490,659 515,229Over five years 269,372 - - - - 269,372 325,202

Sub-total 1,524,607 43,549 - 251 434 1,568,841 1,603,464

Perpetual notes and other non-dated instruments - - 74,630 - - 74,630 84,459

Total 1,524,607 43,549 74,630 251 434 1,643,471 1,687,923

Average contractual maturity analysed by denominational currency of investments2009 2008

Years Years

Pound Sterling 1.0 4.5US Dollar 5.5 6.5Euro 2.8 5.1Canadian Dollar 1.4 2.5

The contractual maturity for US Dollars of 5.5 years (2008: 6.5 years) is based, for relevant securities, on the legal maturity date of the total pool ofcollateral for those securities. The Syndicate’s participation in these investments is supported by collateral that matures at an earlier date than that of the total pool. Based on this earlier maturity date the average expected maturity for US Dollars would be 1.6 years (2008: 1.9 years).

The following is an analysis by business segment of the estimated timing of net cash flows based on the claims liabilities balance held at 31 December 2009 and 2008.

Between BetweenWithin one and two to Over

2009 one year two years five years five years Total£000 £000 £000 £000 £000

Accident and health 22,625 13,522 15,738 8,978 60,863Marine, aviation and transport 61,536 41,827 51,495 17,551 172,409Fire and other damage to property 111,409 61,651 52,356 12,645 238,061Third-party liability 131,474 97,981 143,753 52,455 425,663Miscellaneous 29,883 16,681 16,128 3,614 66,306Reinsurance 100,613 57,413 45,456 16,403 219,885

Total 457,540 289,075 324,926 111,646 1,183,187

Between BetweenWithin one and two to Over

2008 one year two years five years five years Total£000 £000 £000 £000 £000

Accident and health 20,409 8,362 9,509 3,548 41,828Marine, aviation and transport 77,668 53,051 66,046 16,801 213,566Fire and other damage to property 165,991 74,120 60,984 9,214 310,309Third-party liability 155,921 126,700 190,593 61,801 535,015Miscellaneous 9,875 5,378 5,344 1,107 21,704Reinsurance 153,883 76,768 67,179 12,206 310,036

Total 583,747 344,379 399,655 104,677 1,432,458

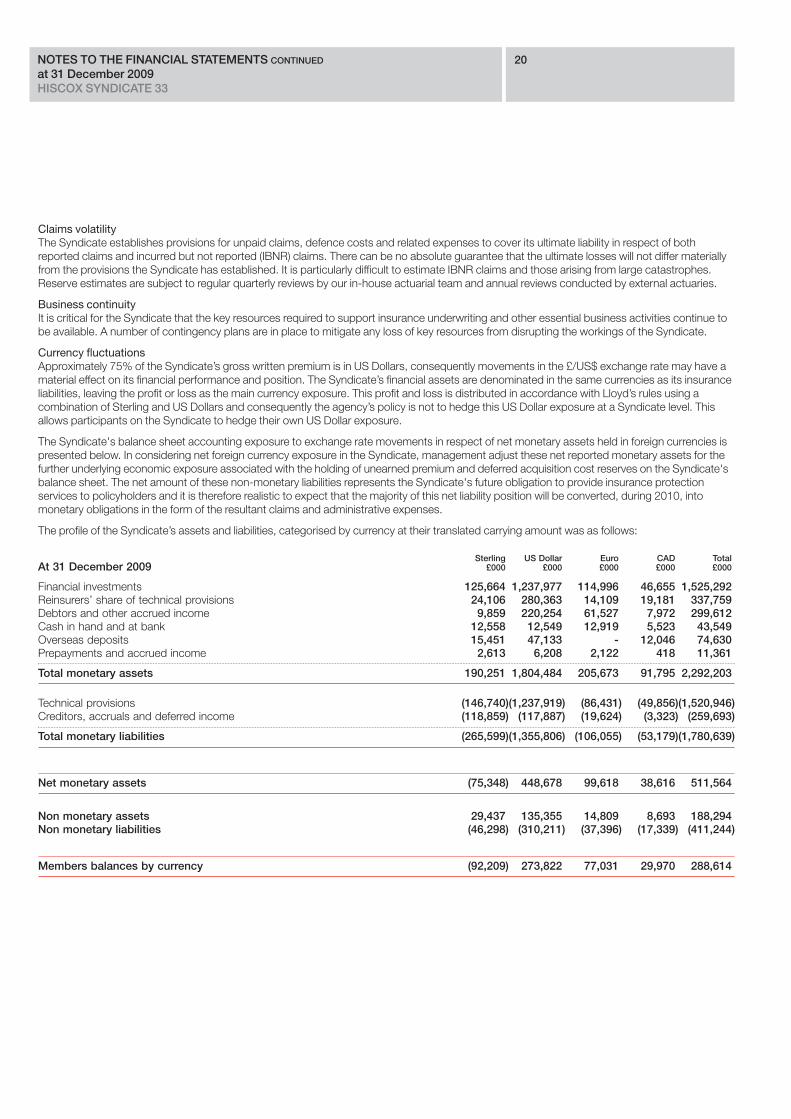

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 20at 31 December 2009HISCOX SYNDICATE 33

Claims volatilityThe Syndicate establishes provisions for unpaid claims, defence costs and related expenses to cover its ultimate liability in respect of bothreported claims and incurred but not reported (IBNR) claims. There can be no absolute guarantee that the ultimate losses will not differ materiallyfrom the provisions the Syndicate has established. It is particularly difficult to estimate IBNR claims and those arising from large catastrophes.Reserve estimates are subject to regular quarterly reviews by our in-house actuarial team and annual reviews conducted by external actuaries.

Business continuityIt is critical for the Syndicate that the key resources required to support insurance underwriting and other essential business activities continue tobe available. A number of contingency plans are in place to mitigate any loss of key resources from disrupting the workings of the Syndicate.

Currency fluctuationsApproximately 75% of the Syndicate’s gross written premium is in US Dollars, consequently movements in the £/US$ exchange rate may have amaterial effect on its financial performance and position. The Syndicate’s financial assets are denominated in the same currencies as its insuranceliabilities, leaving the profit or loss as the main currency exposure. This profit and loss is distributed in accordance with Lloyd’s rules using acombination of Sterling and US Dollars and consequently the agency’s policy is not to hedge this US Dollar exposure at a Syndicate level. Thisallows participants on the Syndicate to hedge their own US Dollar exposure.

The Syndicate's balance sheet accounting exposure to exchange rate movements in respect of net monetary assets held in foreign currencies ispresented below. In considering net foreign currency exposure in the Syndicate, management adjust these net reported monetary assets for thefurther underlying economic exposure associated with the holding of unearned premium and deferred acquisition cost reserves on the Syndicate'sbalance sheet. The net amount of these non-monetary liabilities represents the Syndicate's future obligation to provide insurance protectionservices to policyholders and it is therefore realistic to expect that the majority of this net liability position will be converted, during 2010, intomonetary obligations in the form of the resultant claims and administrative expenses.

The profile of the Syndicate’s assets and liabilities, categorised by currency at their translated carrying amount was as follows:

Sterling US Dollar Euro CAD TotalAt 31 December 2009 £000 £000 £000 £000 £000

Financial investments 125,664 1,237,977 114,996 46,655 1,525,292Reinsurers’ share of technical provisions 24,106 280,363 14,109 19,181 337,759Debtors and other accrued income 9,859 220,254 61,527 7,972 299,612Cash in hand and at bank 12,558 12,549 12,919 5,523 43,549Overseas deposits 15,451 47,133 - 12,046 74,630Prepayments and accrued income 2,613 6,208 2,122 418 11,361

Total monetary assets 190,251 1,804,484 205,673 91,795 2,292,203

Technical provisions (146,740)(1,237,919) (86,431) (49,856)(1,520,946)Creditors, accruals and deferred income (118,859) (117,887) (19,624) (3,323) (259,693)

Total monetary liabilities (265,599)(1,355,806) (106,055) (53,179)(1,780,639)

Net monetary assets (75,348) 448,678 99,618 38,616 511,564

Non monetary assets 29,437 135,355 14,809 8,693 188,294Non monetary liabilities (46,298) (310,211) (37,396) (17,339) (411,244)

Members balances by currency (92,209) 273,822 77,031 29,970 288,614

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 21at 31 December 2009HISCOX SYNDICATE 33

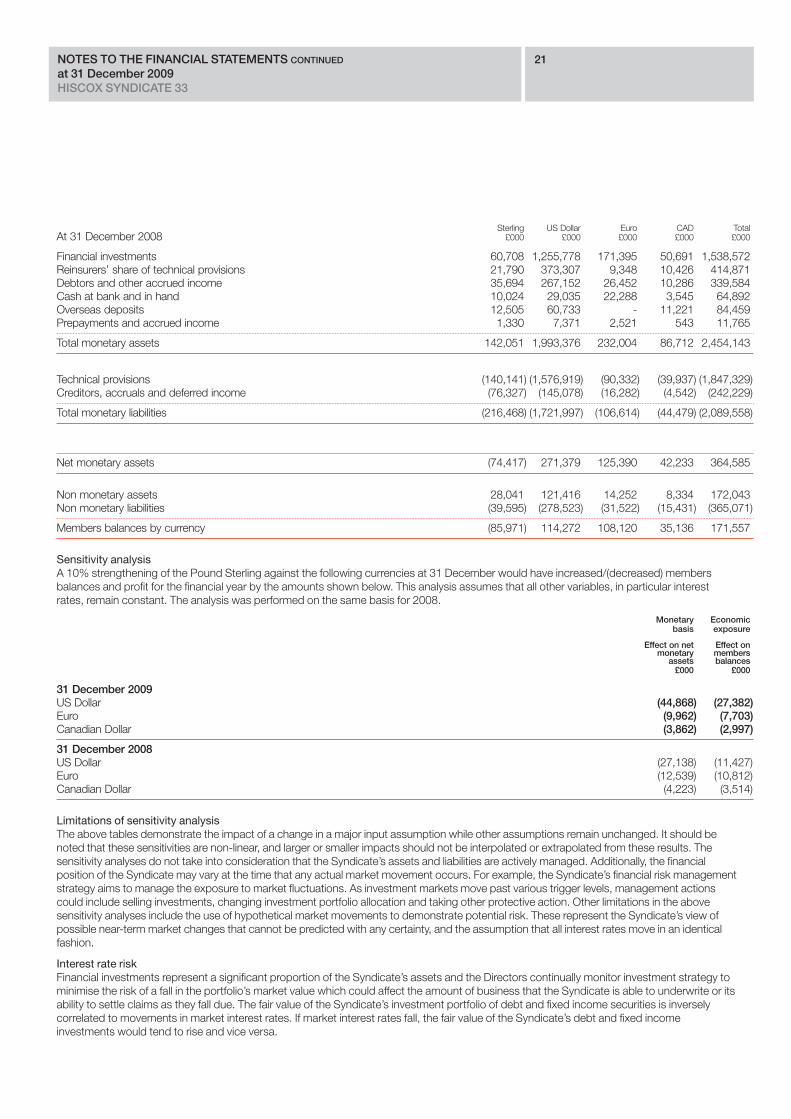

Sterling US Dollar Euro CAD TotalAt 31 December 2008 £000 £000 £000 £000 £000

Financial investments 60,708 1,255,778 171,395 50,691 1,538,572Reinsurers’ share of technical provisions 21,790 373,307 9,348 10,426 414,871Debtors and other accrued income 35,694 267,152 26,452 10,286 339,584Cash at bank and in hand 10,024 29,035 22,288 3,545 64,892Overseas deposits 12,505 60,733 - 11,221 84,459Prepayments and accrued income 1,330 7,371 2,521 543 11,765

Total monetary assets 142,051 1,993,376 232,004 86,712 2,454,143

Technical provisions (140,141) (1,576,919) (90,332) (39,937) (1,847,329)Creditors, accruals and deferred income (76,327) (145,078) (16,282) (4,542) (242,229)

Total monetary liabilities (216,468) (1,721,997) (106,614) (44,479) (2,089,558)

Net monetary assets (74,417) 271,379 125,390 42,233 364,585

Non monetary assets 28,041 121,416 14,252 8,334 172,043Non monetary liabilities (39,595) (278,523) (31,522) (15,431) (365,071)

Members balances by currency (85,971) 114,272 108,120 35,136 171,557

Sensitivity analysisA 10% strengthening of the Pound Sterling against the following currencies at 31 December would have increased/(decreased) membersbalances and profit for the financial year by the amounts shown below. This analysis assumes that all other variables, in particular interestrates, remain constant. The analysis was performed on the same basis for 2008.

Monetary Economicbasis exposure

Effect on net Effect onmonetary members

assets balances£000 £000

31 December 2009US Dollar (44,868) (27,382)Euro (9,962) (7,703)Canadian Dollar (3,862) (2,997)

31 December 2008US Dollar (27,138) (11,427)Euro (12,539) (10,812)Canadian Dollar (4,223) (3,514)

Limitations of sensitivity analysisThe above tables demonstrate the impact of a change in a major input assumption while other assumptions remain unchanged. It should benoted that these sensitivities are non-linear, and larger or smaller impacts should not be interpolated or extrapolated from these results. Thesensitivity analyses do not take into consideration that the Syndicate’s assets and liabilities are actively managed. Additionally, the financialposition of the Syndicate may vary at the time that any actual market movement occurs. For example, the Syndicate’s financial risk managementstrategy aims to manage the exposure to market fluctuations. As investment markets move past various trigger levels, management actionscould include selling investments, changing investment portfolio allocation and taking other protective action. Other limitations in the abovesensitivity analyses include the use of hypothetical market movements to demonstrate potential risk. These represent the Syndicate’s view ofpossible near-term market changes that cannot be predicted with any certainty, and the assumption that all interest rates move in an identicalfashion.

Interest rate riskFinancial investments represent a significant proportion of the Syndicate’s assets and the Directors continually monitor investment strategy tominimise the risk of a fall in the portfolio’s market value which could affect the amount of business that the Syndicate is able to underwrite or itsability to settle claims as they fall due. The fair value of the Syndicate’s investment portfolio of debt and fixed income securities is inverselycorrelated to movements in market interest rates. If market interest rates fall, the fair value of the Syndicate’s debt and fixed incomeinvestments would tend to rise and vice versa.

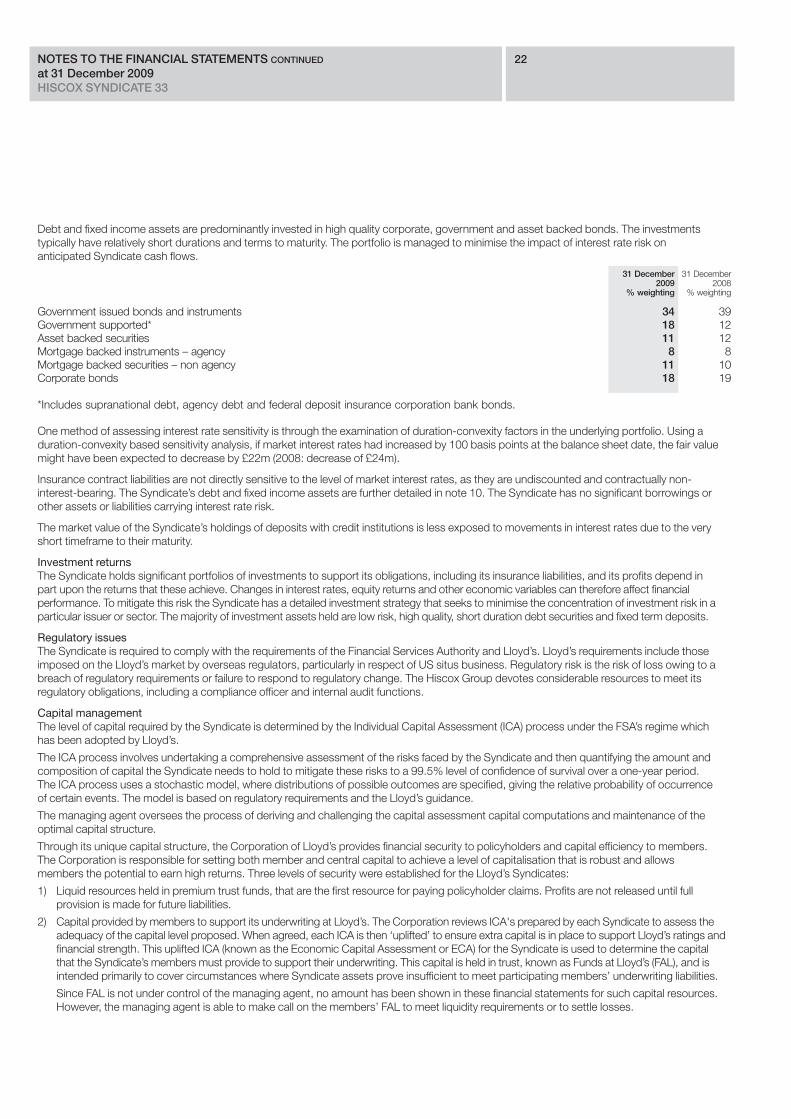

Debt and fixed income assets are predominantly invested in high quality corporate, government and asset backed bonds. The investmentstypically have relatively short durations and terms to maturity. The portfolio is managed to minimise the impact of interest rate risk onanticipated Syndicate cash flows.

31 December 31 December2009 2008

% weighting % weighting

Government issued bonds and instruments 34 39Government supported* 18 12Asset backed securities 11 12Mortgage backed instruments – agency 8 8Mortgage backed securities – non agency 11 10Corporate bonds 18 19

*Includes supranational debt, agency debt and federal deposit insurance corporation bank bonds.

One method of assessing interest rate sensitivity is through the examination of duration-convexity factors in the underlying portfolio. Using aduration-convexity based sensitivity analysis, if market interest rates had increased by 100 basis points at the balance sheet date, the fair valuemight have been expected to decrease by £22m (2008: decrease of £24m).

Insurance contract liabilities are not directly sensitive to the level of market interest rates, as they are undiscounted and contractually non-interest-bearing. The Syndicate’s debt and fixed income assets are further detailed in note 10. The Syndicate has no significant borrowings orother assets or liabilities carrying interest rate risk.

The market value of the Syndicate’s holdings of deposits with credit institutions is less exposed to movements in interest rates due to the veryshort timeframe to their maturity.

Investment returnsThe Syndicate holds significant portfolios of investments to support its obligations, including its insurance liabilities, and its profits depend in part upon the returns that these achieve. Changes in interest rates, equity returns and other economic variables can therefore affect financialperformance. To mitigate this risk the Syndicate has a detailed investment strategy that seeks to minimise the concentration of investment risk in aparticular issuer or sector. The majority of investment assets held are low risk, high quality, short duration debt securities and fixed term deposits.

Regulatory issuesThe Syndicate is required to comply with the requirements of the Financial Services Authority and Lloyd’s. Lloyd’s requirements include thoseimposed on the Lloyd’s market by overseas regulators, particularly in respect of US situs business. Regulatory risk is the risk of loss owing to abreach of regulatory requirements or failure to respond to regulatory change. The Hiscox Group devotes considerable resources to meet itsregulatory obligations, including a compliance officer and internal audit functions.

Capital management The level of capital required by the Syndicate is determined by the Individual Capital Assessment (ICA) process under the FSA’s regime whichhas been adopted by Lloyd’s.

The ICA process involves undertaking a comprehensive assessment of the risks faced by the Syndicate and then quantifying the amount andcomposition of capital the Syndicate needs to hold to mitigate these risks to a 99.5% level of confidence of survival over a one-year period.The ICA process uses a stochastic model, where distributions of possible outcomes are specified, giving the relative probability of occurrenceof certain events. The model is based on regulatory requirements and the Lloyd’s guidance.

The managing agent oversees the process of deriving and challenging the capital assessment capital computations and maintenance of theoptimal capital structure.

Through its unique capital structure, the Corporation of Lloyd’s provides financial security to policyholders and capital efficiency to members.The Corporation is responsible for setting both member and central capital to achieve a level of capitalisation that is robust and allowsmembers the potential to earn high returns. Three levels of security were established for the Lloyd’s Syndicates:

1) Liquid resources held in premium trust funds, that are the first resource for paying policyholder claims. Profits are not released until full provision is made for future liabilities.

2) Capital provided by members to support its underwriting at Lloyd’s. The Corporation reviews ICA's prepared by each Syndicate to assess theadequacy of the capital level proposed. When agreed, each ICA is then ‘uplifted’ to ensure extra capital is in place to support Lloyd’s ratings and financial strength. This uplifted ICA (known as the Economic Capital Assessment or ECA) for the Syndicate is used to determine the capital that the Syndicate’s members must provide to support their underwriting. This capital is held in trust, known as Funds at Lloyd’s (FAL), and is intended primarily to cover circumstances where Syndicate assets prove insufficient to meet participating members’ underwriting liabilities.

Since FAL is not under control of the managing agent, no amount has been shown in these financial statements for such capital resources. However, the managing agent is able to make call on the members’ FAL to meet liquidity requirements or to settle losses.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 22at 31 December 2009HISCOX SYNDICATE 33

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 23at 31 December 2009HISCOX SYNDICATE 33

3) The Central Fund which comprises central assets funded by members’ annual contributions and subordinated debt. The Corporation of Lloyd’s regularly reviews and determines the optimum level of central assets, seeking to balance the need for robust financial security against the members’ desire for cost-effective mutuality of capital. In particular, the Corporation’s modelling stress tests each member’s underwriting portfolio against a number of scenarios and a range of forecasts of market conditions. Members’ contributions to the Central Fund for 2009 were set at 0.5% of gross written premiums.

4 Segmental analysisAn analysis of the underwriting result before investment return is set out below:

2009 Gross Gross Gross Netpremiums premiums claims operating Reinsurance

written earned incurred expenses balance Total£000 £000 £000 £000 £000 £000

Direct insurance:Accident and health 87,559 73,420 (44,443) (27,713) (5,141) (3,877)Marine aviation and transport 125,000 115,516 (42,642) (31,478) (15,087) 26,309Fire and other damage to property 341,942 326,669 (148,711) (98,869) (70,464) 8,625Third-party liability 99,546 106,031 (26,201) (31,053) (17,450) 31,327Miscellaneous 19,510 19,632 (44,695) (3,131) 2,042 (26,152)

673,557 641,268 (306,692) (192,244) (106,100) 36,232Reinsurance 360,573 346,123 (33,384) (132,018) (113,590) 67,131

Total 1,034,130 987,391 (340,076) (324,262) (219,690) 103,363

2008Net

Gross Gross Gross operating Reinsurancepremiums premiums claims expenses balance

written earned incurred restated restated Total£000 £000 £000 £000 £000 £000

Direct insurance:Accident and health 41,806 42,764 (7,515) (11,447) (3,023) 20,779Marine aviation and transport 91,421 97,210 (98,531) (7,943) 13,249 3,985Fire and other damage to property 312,137 335,549 (214,404) (15,499) (17,450) 88,196Third-party liability 121,499 122,430 (111,276) (32,022) 17,156 (3,712)Miscellaneous 21,055 21,196 (3,839) (3,325) (2,443) 11,589

587,918 619,149 (435,565) (70,236) 7,489 120,837Reinsurance 297,107 313,238 (186,902) 28,807 (28,123) 127,020

Total 885,025 932,387 (622,467) (41,429) (20,634) 247,857

All premiums were concluded in the UK.

The geographical analysis of gross premiums earned by destination is as follows:2009 2008£000 £000

United Kingdom 55,230 44,866European Union member states (excluding UK) 75,210 76,863United States 508,797 459,046Other 348,153 351,612

Total 987,390 932,387

5 Claims outstandingA release of £141.7m from the net reserve for claims outstanding, set at 31 December 2008, has been made in calendar year 2009. Netreserves for claims outstanding at 31 December 2007 were reduced by £112.8m in calendar year 2008.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 24at 31 December 2009HISCOX SYNDICATE 33

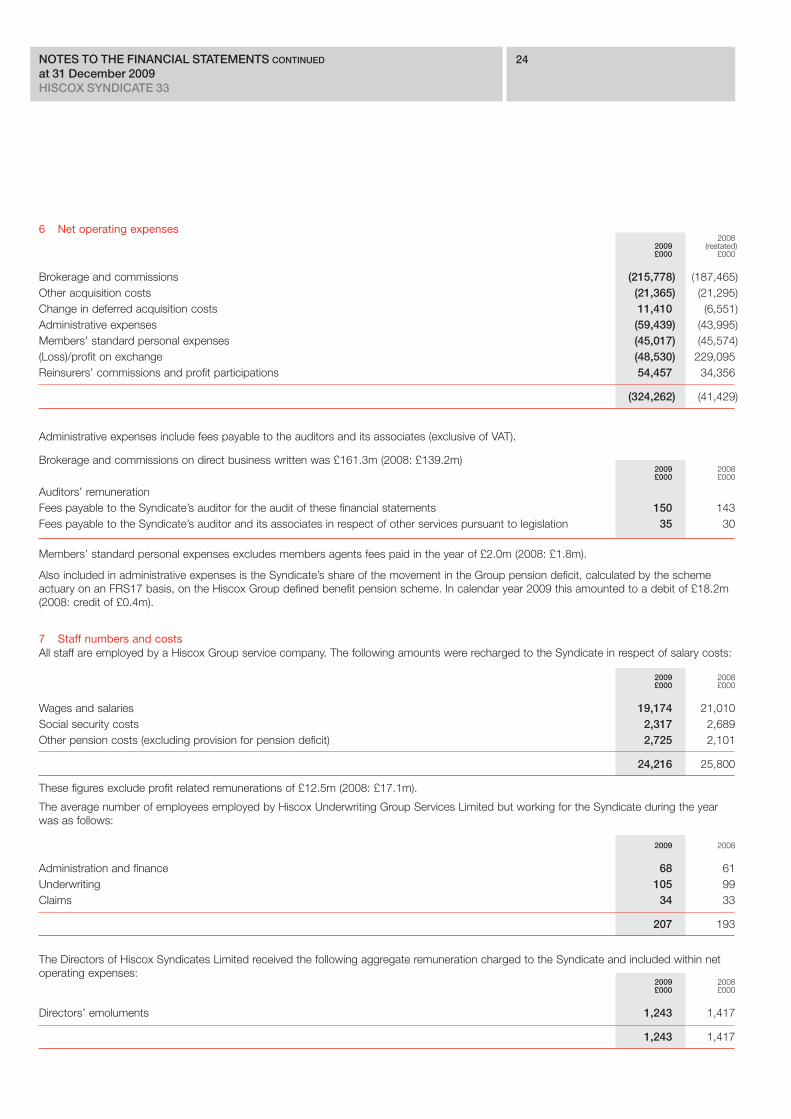

6 Net operating expenses2008

2009 (restated)£000 £000

Brokerage and commissions (215,778) (187,465)Other acquisition costs (21,365) (21,295)Change in deferred acquisition costs 11,410 (6,551)Administrative expenses (59,439) (43,995)Members’ standard personal expenses (45,017) (45,574)(Loss)/profit on exchange (48,530) 229,095Reinsurers’ commissions and profit participations 54,457 34,356

(324,262) (41,429)

Administrative expenses include fees payable to the auditors and its associates (exclusive of VAT).

Brokerage and commissions on direct business written was £161.3m (2008: £139.2m)2009 2008£000 £000

Auditors’ remunerationFees payable to the Syndicate’s auditor for the audit of these financial statements 150 143Fees payable to the Syndicate’s auditor and its associates in respect of other services pursuant to legislation 35 30

Members’ standard personal expenses excludes members agents fees paid in the year of £2.0m (2008: £1.8m).

Also included in administrative expenses is the Syndicate’s share of the movement in the Group pension deficit, calculated by the scheme actuary on an FRS17 basis, on the Hiscox Group defined benefit pension scheme. In calendar year 2009 this amounted to a debit of £18.2m(2008: credit of £0.4m).

7 Staff numbers and costsAll staff are employed by a Hiscox Group service company. The following amounts were recharged to the Syndicate in respect of salary costs:

2009 2008£000 £000

Wages and salaries 19,174 21,010Social security costs 2,317 2,689Other pension costs (excluding provision for pension deficit) 2,725 2,101

24,216 25,800

These figures exclude profit related remunerations of £12.5m (2008: £17.1m).

The average number of employees employed by Hiscox Underwriting Group Services Limited but working for the Syndicate during the year was as follows:

2009 2008

Administration and finance 68 61Underwriting 105 99Claims 34 33

207 193

The Directors of Hiscox Syndicates Limited received the following aggregate remuneration charged to the Syndicate and included within net operating expenses:

2009 2008£000 £000

Directors’ emoluments 1,243 1,417

1,243 1,417

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 25at 31 December 2009HISCOX SYNDICATE 33

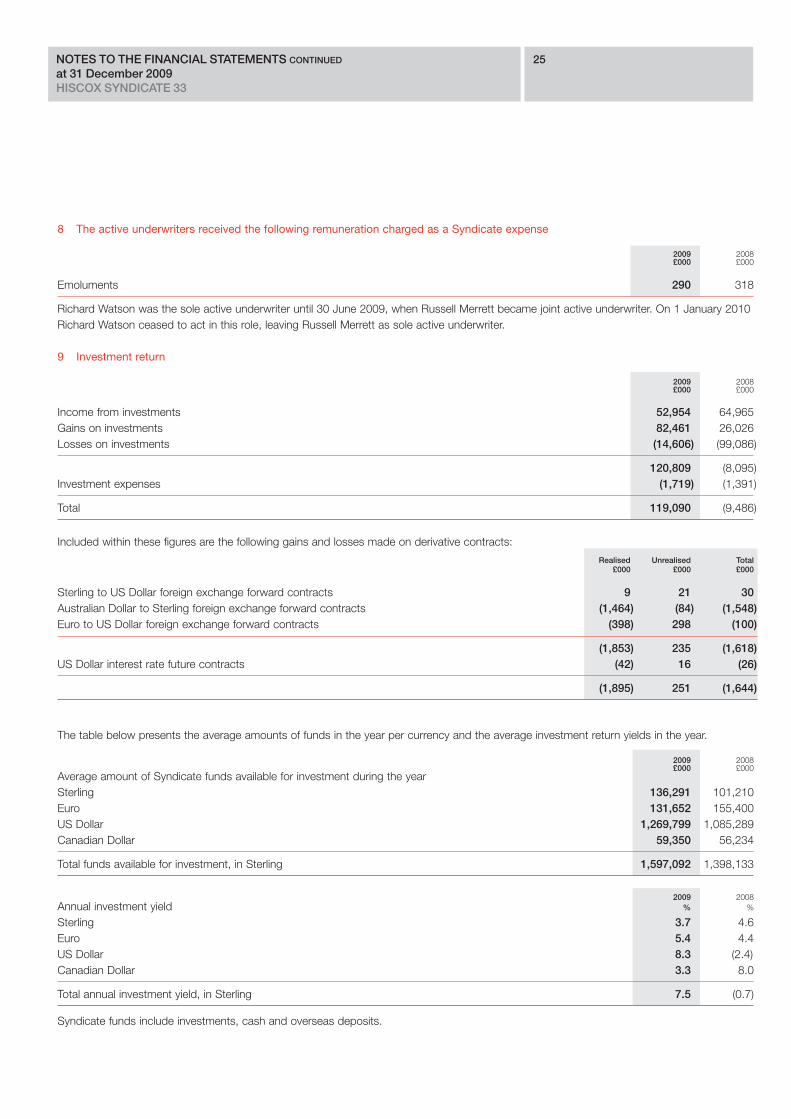

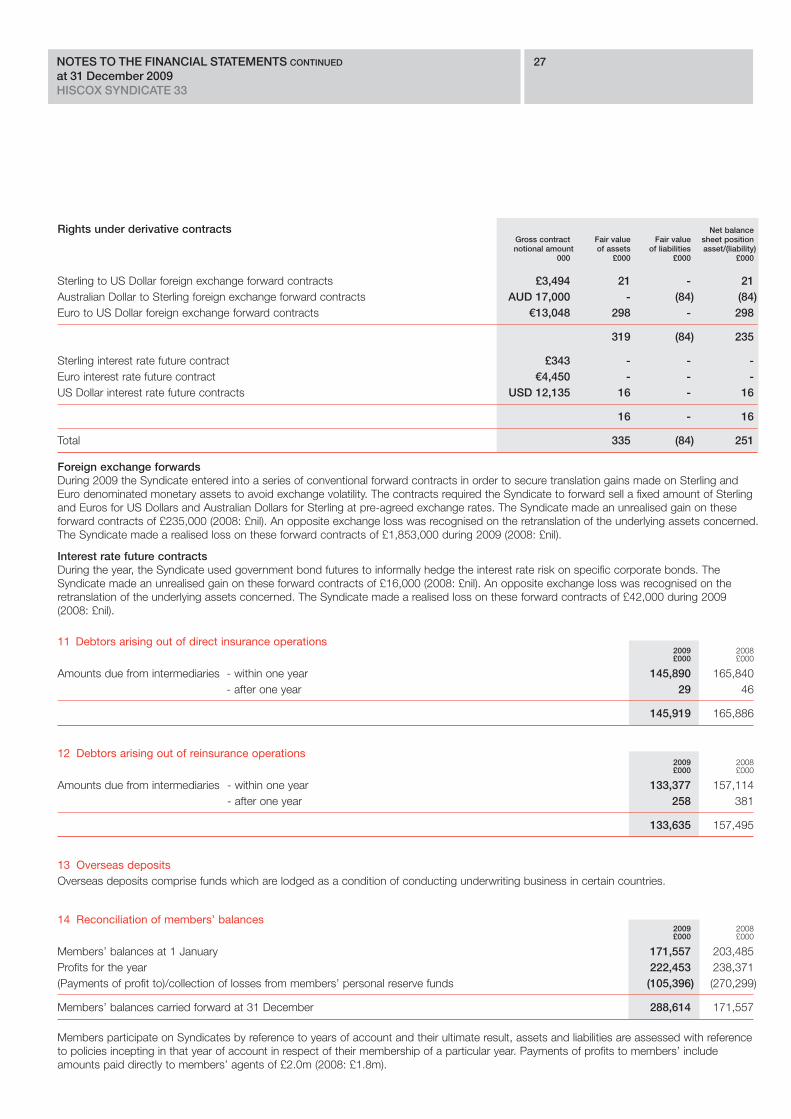

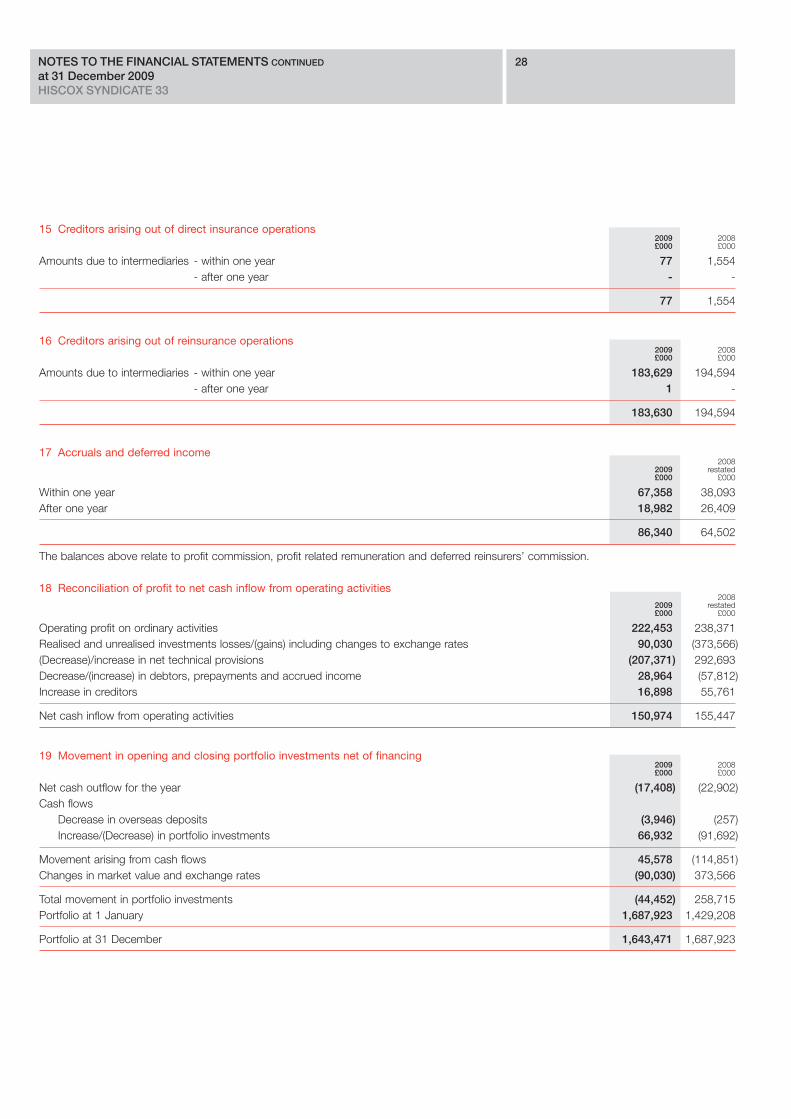

8 The active underwriters received the following remuneration charged as a Syndicate expense

2009 2008£000 £000

Emoluments 290 318

Richard Watson was the sole active underwriter until 30 June 2009, when Russell Merrett became joint active underwriter. On 1 January 2010Richard Watson ceased to act in this role, leaving Russell Merrett as sole active underwriter.

9 Investment return

2009 2008£000 £000

Income from investments 52,954 64,965Gains on investments 82,461 26,026Losses on investments (14,606) (99,086)

120,809 (8,095)Investment expenses (1,719) (1,391)

Total 119,090 (9,486)

Included within these figures are the following gains and losses made on derivative contracts:

Realised Unrealised Total£000 £000 £000

Sterling to US Dollar foreign exchange forward contracts 9 21 30Australian Dollar to Sterling foreign exchange forward contracts (1,464) (84) (1,548)Euro to US Dollar foreign exchange forward contracts (398) 298 (100)

(1,853) 235 (1,618)US Dollar interest rate future contracts (42) 16 (26)

(1,895) 251 (1,644)

The table below presents the average amounts of funds in the year per currency and the average investment return yields in the year.

2009 2008£000 £000

Average amount of Syndicate funds available for investment during the yearSterling 136,291 101,210Euro 131,652 155,400US Dollar 1,269,799 1,085,289Canadian Dollar 59,350 56,234

Total funds available for investment, in Sterling 1,597,092 1,398,133

2009 2008Annual investment yield % %

Sterling 3.7 4.6Euro 5.4 4.4US Dollar 8.3 (2.4)Canadian Dollar 3.3 8.0

Total annual investment yield, in Sterling 7.5 (0.7)

Syndicate funds include investments, cash and overseas deposits.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED 26at 31 December 2009HISCOX SYNDICATE 33

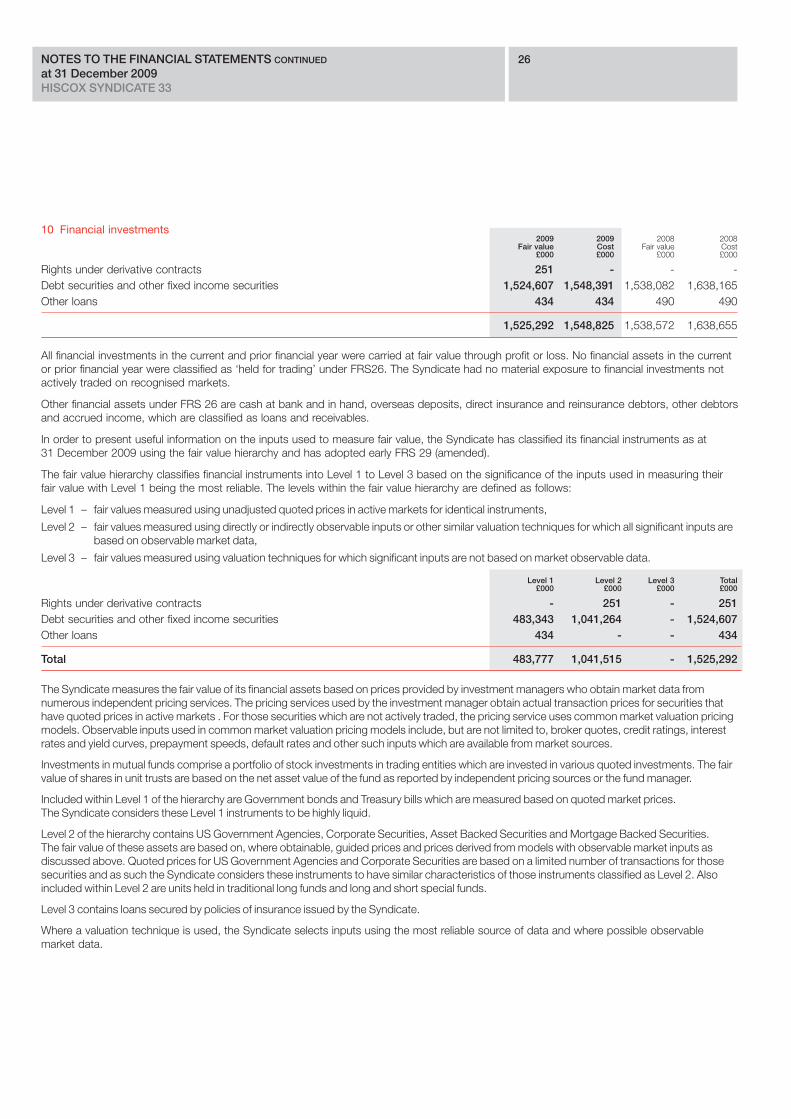

10 Financial investments2009 2009 2008 2008

Fair value Cost Fair value Cost£000 £000 £000 £000

Rights under derivative contracts 251 - - -Debt securities and other fixed income securities 1,524,607 1,548,391 1,538,082 1,638,165Other loans 434 434 490 490

1,525,292 1,548,825 1,538,572 1,638,655

All financial investments in the current and prior financial year were carried at fair value through profit or loss. No financial assets in the current or prior financial year were classified as ‘held for trading’ under FRS26. The Syndicate had no material exposure to financial investments notactively traded on recognised markets.

Other financial assets under FRS 26 are cash at bank and in hand, overseas deposits, direct insurance and reinsurance debtors, other debtorsand accrued income, which are classified as loans and receivables.

In order to present useful information on the inputs used to measure fair value, the Syndicate has classified its financial instruments as at 31 December 2009 using the fair value hierarchy and has adopted early FRS 29 (amended).

The fair value hierarchy classifies financial instruments into Level 1 to Level 3 based on the significance of the inputs used in measuring their fair value with Level 1 being the most reliable. The levels within the fair value hierarchy are defined as follows:

Level 1 – fair values measured using unadjusted quoted prices in active markets for identical instruments,

Level 2 – fair values measured using directly or indirectly observable inputs or other similar valuation techniques for which all significant inputs are based on observable market data,

Level 3 – fair values measured using valuation techniques for which significant inputs are not based on market observable data.

Level 1 Level 2 Level 3 Total£000 £000 £000 £000

Rights under derivative contracts - 251 - 251Debt securities and other fixed income securities 483,343 1,041,264 - 1,524,607Other loans 434 - - 434

Total 483,777 1,041,515 - 1,525,292