Emergence of Unconventional LNG and its Implications for LNG … · 2020-04-04 · Nihon...

27

Emergence of Unconventional LNG and its Implications for LNG Buyers in Asia-Pacific * All rights reserved. Northeast Asia Petroleum Forum 2011 October 19th, 2011 Kunio Nohata Senior General Manager Gas Resources Dept. Tokyo Gas Co., Ltd.

Transcript of Emergence of Unconventional LNG and its Implications for LNG … · 2020-04-04 · Nihon...

Emergence of Unconventional LNG

and

its Implications for LNG Buyers in

Asia-Pacific

* All rights reserved.

Northeast Asia Petroleum Forum 2011

October 19th, 2011

Kunio Nohata Senior General Manager

Gas Resources Dept. Tokyo Gas Co., Ltd.

2

Presentation Contents The LNG Market in Japan

Latest trends of Unconventional Gas

Impact of Unconventional Gas on the Asia-

Pacific Market

3

LNG Imports to Japan by Company (FY2010)

TEPCO (20.8)

Tokyo Gas (11.3)

Chubu

(10.4) Osaka

(8.2) Kansai

(4.8)

Tohoku (3.0)

Toho (3.0)

Gas companies

Electric power companies

Kyushu

(2.7)

Chugoku

(1.8)

Unit: Million tons Japan total (70.6)

Saibu Hiroshima

Shizuoka

Sendai

Nihon

電力/ガスの受入比率(10年度)

Source: Trade statistics, FEPC, Sekitsu, etc.

Tokyo Gas & TEPCO first imported LNG to Japan

in 1969

電力会社

ガス会社

62.3%

37.7%

Import shares of electric/ gas companies (FY2010)

Gas companies

Electric power companies

4

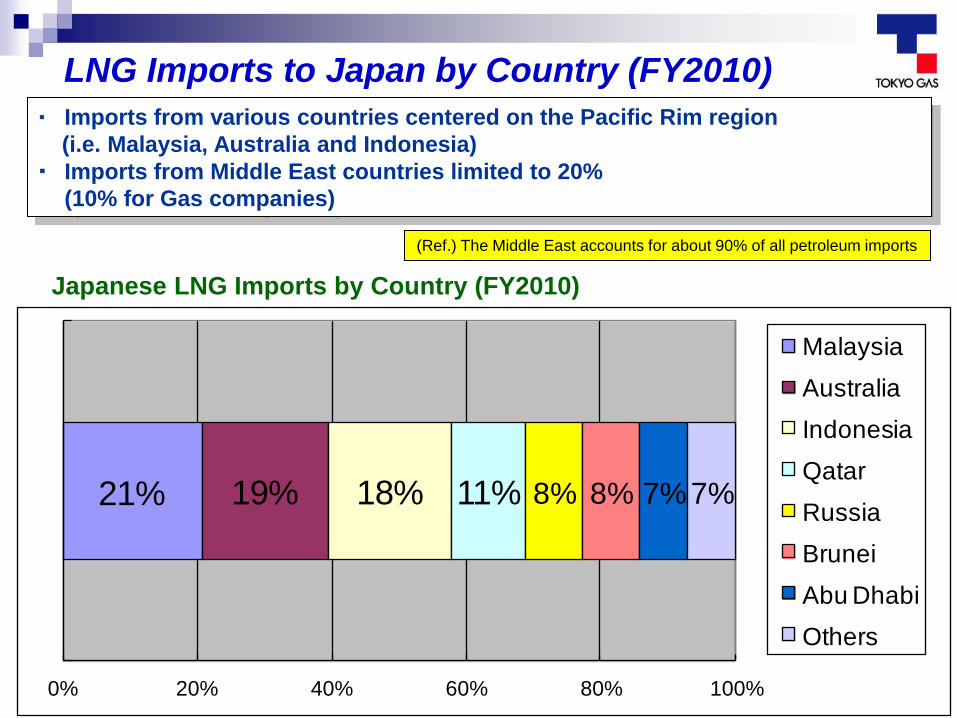

・ Imports from various countries centered on the Pacific Rim region

(i.e. Malaysia, Australia and Indonesia)

・ Imports from Middle East countries limited to 20%

(10% for Gas companies)

出典:貿易統計

Japanese LNG Imports by Country (FY2010)

21% 19% 18% 11% 8% 8% 7%7%

0% 20% 40% 60% 80% 100%

1

Malaysia

Australia

Indonesia

Qatar

Russia

Brunei

Abu Dhabi

Others

LNG Imports to Japan by Country (FY2010)

(Ref.) The Middle East accounts for about 90% of all petroleum imports

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

CY2010

CY2011

5

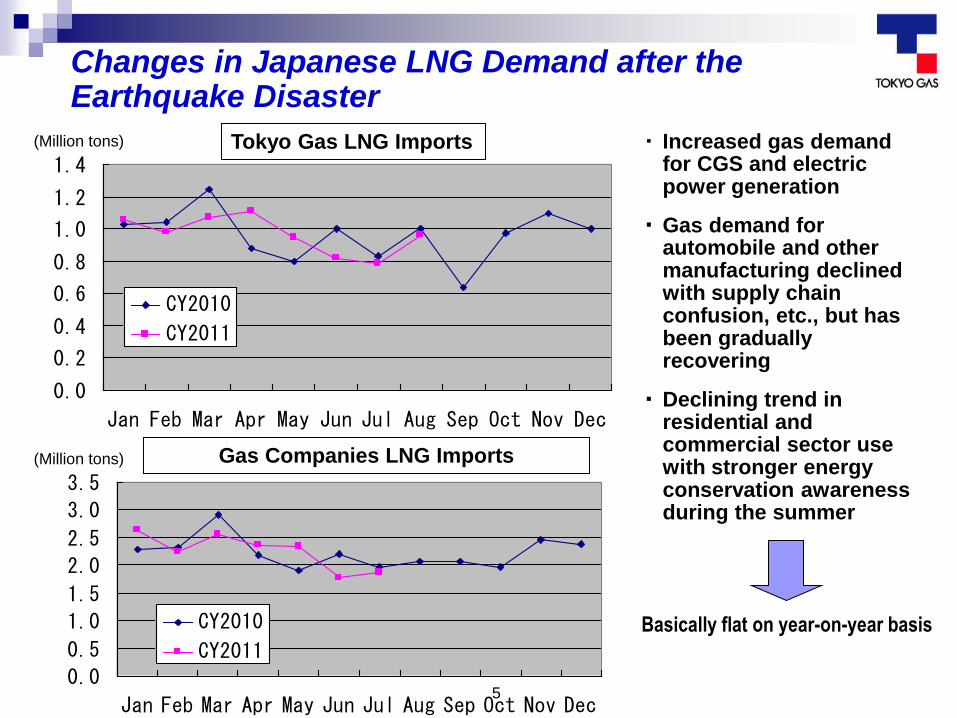

Changes in Japanese LNG Demand after the Earthquake Disaster

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

CY2010

CY2011

(Million tons)

(Million tons)

Tokyo Gas LNG Imports

Gas Companies LNG Imports

・ Increased gas demand for CGS and electric power generation

・ Gas demand for automobile and other manufacturing declined with supply chain confusion, etc., but has been gradually recovering

・ Declining trend in residential and commercial sector use with stronger energy conservation awareness during the summer

Basically flat on year-on-year basis

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

CY2010

CY2011

6

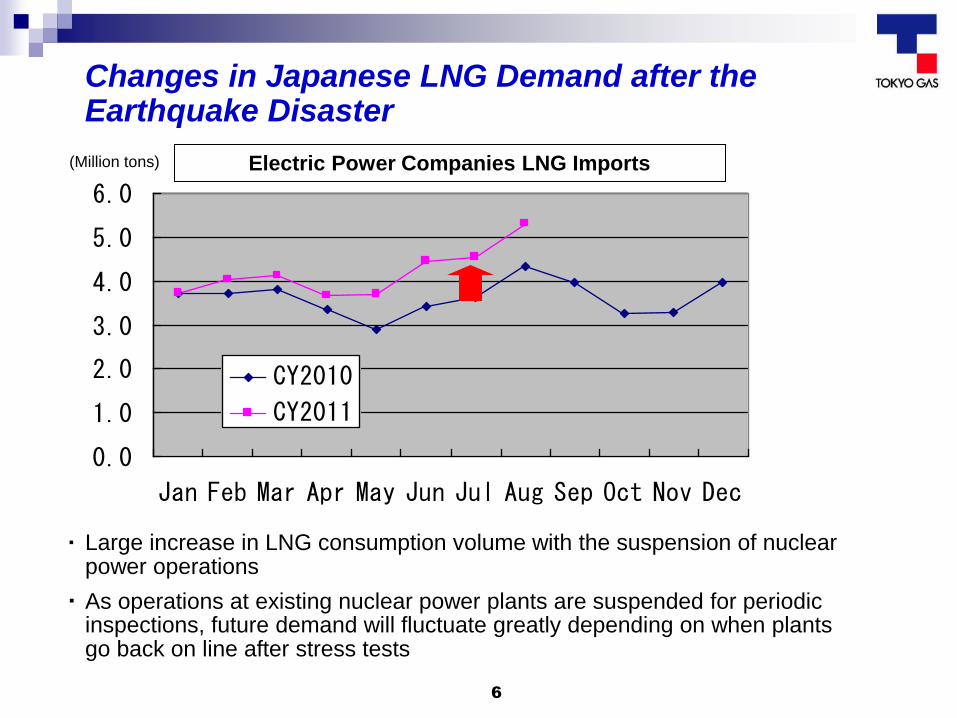

Changes in Japanese LNG Demand after the Earthquake Disaster

(Million tons) Electric Power Companies LNG Imports

・ Large increase in LNG consumption volume with the suspension of nuclear power operations

・ As operations at existing nuclear power plants are suspended for periodic inspections, future demand will fluctuate greatly depending on when plants go back on line after stress tests

7 7

Negishi LNG Terminal

Ohgishima LNG Terminal

Sodegaura LNG TerminalNegishi LNG Terminal

Ohgishima LNG Terminal

Sodegaura LNG Terminal

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

2010 2011 2012 2013 2014 2015

bcm

* All rights reserved.

LNG Demand Outlook for Tokyo Gas

Kashima PL

2012~ Hitachi LNG Terminal

2015~

Reinforcement of infrastructure

to expand LNG demand

<Tokyo Gas supply plan (prior to the disaster) >

Annual growth rate of approx. 3%

between FY2010 and FY2015

Hitachi LNG Terminal

(planned) 2015~

Kashima PL

(under construction)

2012~

(Actual) (FY)

Potential increase in

demand

8

LNG Demand Outlook for Japan

Source: The IEEJ (Prior to the disaster)

0.0

20.0

40.0

60.0

80.0

100.0

2010 2015 2020 2030

ハイケース

ローケース

?

・ While gas companies had assumed an increase in LNG demand prior to the earthquake disaster, the outlook is for an even larger increase from expansion in demand for CGS and gas air conditioning.

・ Electric power companies had projected declining LNG demand from a shift to nuclear power prior to the earthquake disaster, but LNG demand will greatly increase in the short term. Long-term demand will fluctuate widely depending on Japan’s nuclear power and energy policies.

High Demand Case

Low Demand Case

(MTPA)

9

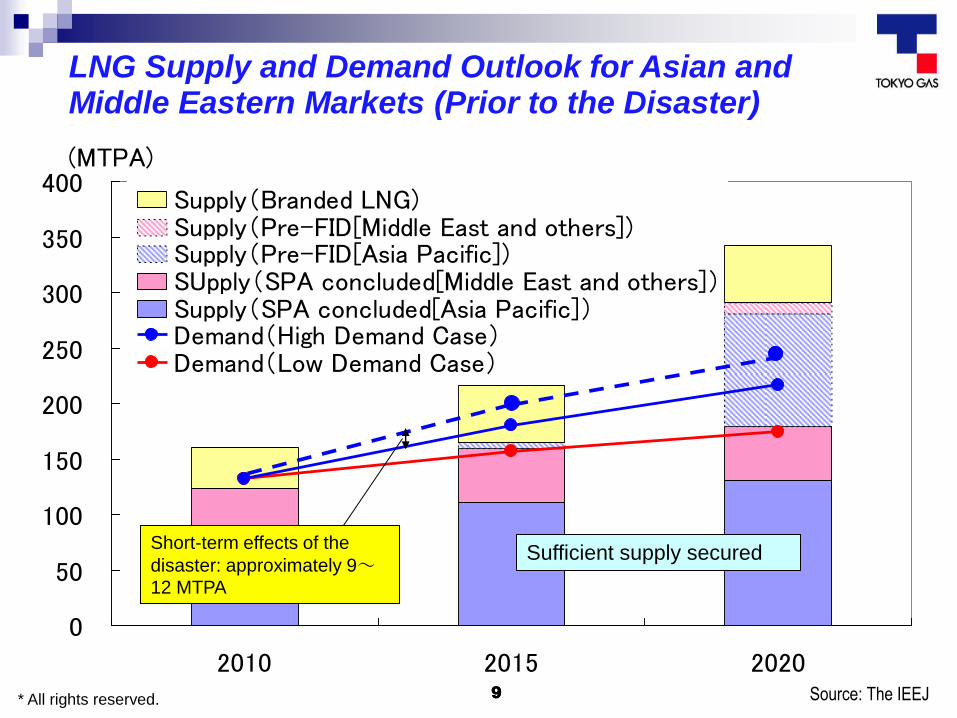

0

50

100

150

200

250

300

350

400

2010 2015 2020

Supply(Branded LNG)Supply(Pre-FID[Middle East and others])Supply(Pre-FID[Asia Pacific])SUpply(SPA concluded[Middle East and others])Supply(SPA concluded[Asia Pacific])Demand(High Demand Case)Demand(Low Demand Case)

(MTPA)

9 * All rights reserved. 9 Source: The IEEJ

LNG Supply and Demand Outlook for Asian and Middle Eastern Markets (Prior to the Disaster)

Short-term effects of the

disaster: approximately 9~12 MTPA

Sufficient supply secured

10

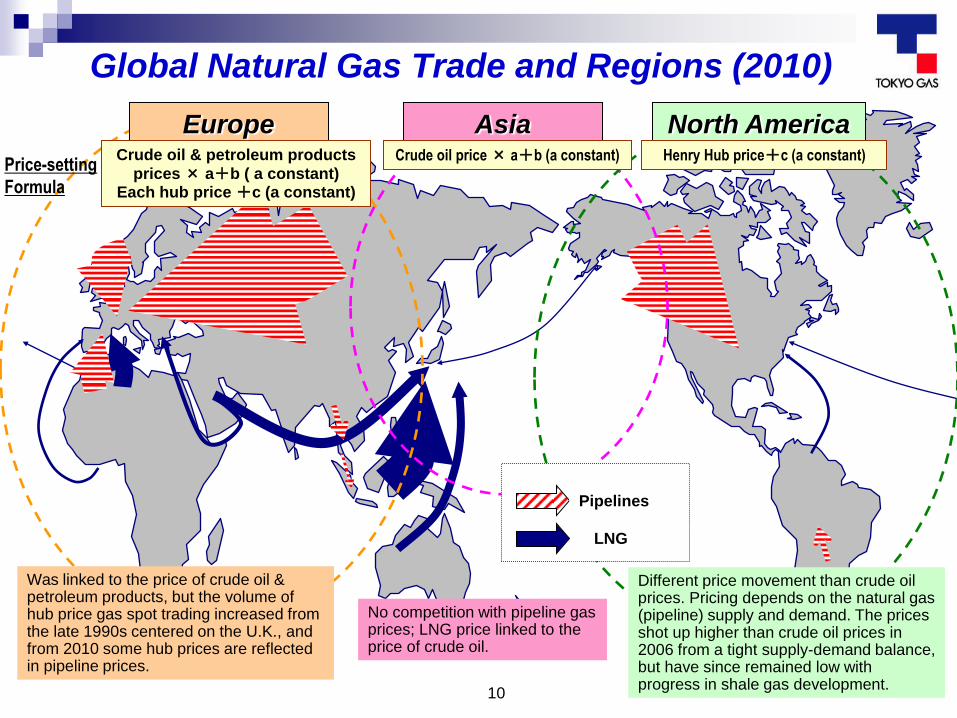

Global Natural Gas Trade and Regions (2010)

Europe Asia North America Crude oil & petroleum products

prices × a+b ( a constant) Each hub price +c (a constant)

Crude oil price × a+b (a constant) Henry Hub price+c (a constant) Price-setting

Formula

LNG

Pipelines

Different price movement than crude oil prices. Pricing depends on the natural gas (pipeline) supply and demand. The prices shot up higher than crude oil prices in 2006 from a tight supply-demand balance, but have since remained low with progress in shale gas development.

Was linked to the price of crude oil & petroleum products, but the volume of hub price gas spot trading increased from the late 1990s centered on the U.K., and from 2010 some hub prices are reflected in pipeline prices.

No competition with pipeline gas prices; LNG price linked to the price of crude oil.

0

6

12

18

24

CL01

CL02

CL03

CL04

CL05

CL06

CL07

CL08

CL09

CL10

CL11

㌦/m

mbt

u

0

18

36

54

72

90

108

126

144

㌦/

バレ

ル

米国(ヘンリーハブ)

原油 (JCC)

日本・アジア (LNG)ロシア→欧州 (PL)

英国 (NBP)

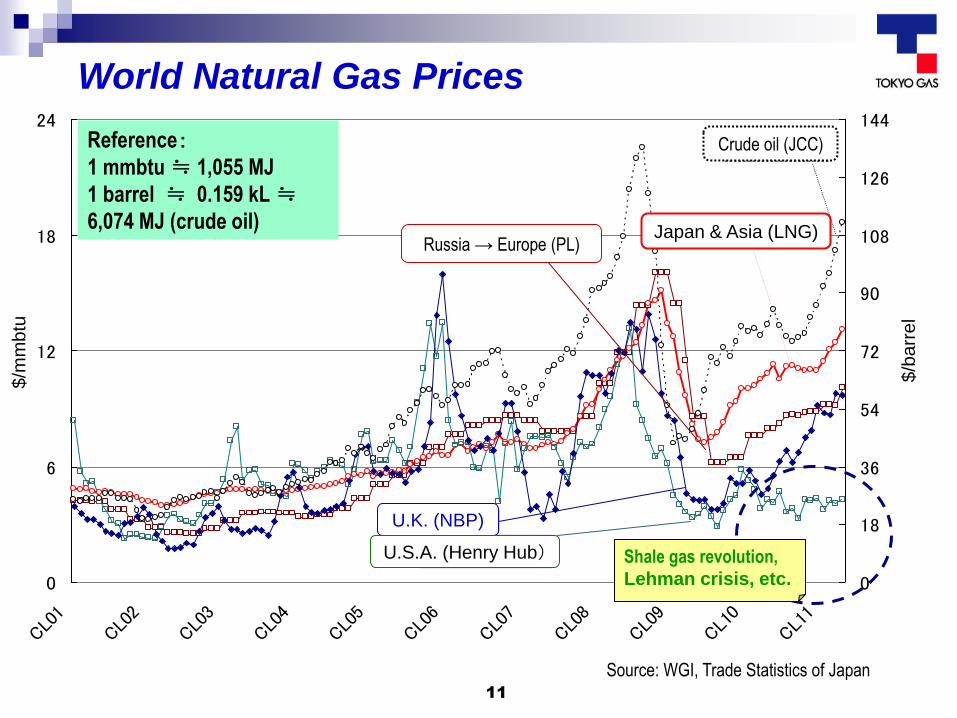

11

Reference:

1 mmbtu ≒ 1,055 MJ

1 barrel ≒ 0.159 kL ≒

6,074 MJ (crude oil)

Source: WGI, Trade Statistics of Japan

World Natural Gas Prices

Shale gas revolution,

Lehman crisis, etc.

Russia → Europe (PL) Japan & Asia (LNG)

Crude oil (JCC)

U.K. (NBP)

U.S.A. (Henry Hub)

$/b

arr

el

$/m

mb

tu

The LNG Market in Japan

Latest trends of Unconventional Gas

Impact of Unconventional Gas on the Asia-

Pacific Market

12

Presentation Contents

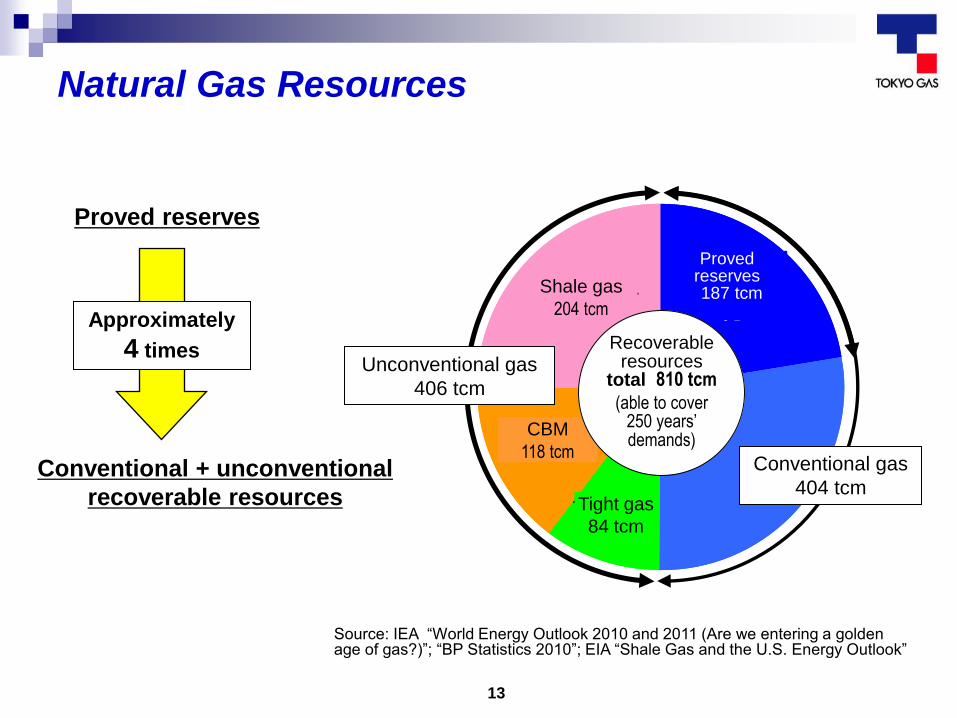

非在来型ガス406兆m3

シェールガス204兆m3

CBM118兆m3

タイトガス84兆m3

在来型ガス404兆m3

従来の確認埋蔵量187兆m3

回収可能な埋蔵量計810兆m3(250年分に相当)

13

Natural Gas Resources

Proved reserves

Conventional + unconventional

recoverable resources

Approximately

4 times

Source: IEA “World Energy Outlook 2010 and 2011 (Are we entering a golden age of gas?)”; “BP Statistics 2010”; EIA “Shale Gas and the U.S. Energy Outlook”

Unconventional gas

406 tcm

Conventional gas

404 tcm

Shale gas

204 tcm

CBM

118 tcm

Tight gas

84 tcm

Proved reserves 187 tcm

Recoverable resources

total 810 tcm

(able to cover 250 years’ demands)

14

Global Unconventional Gas Distribution

Australia

Source: NPC 2007

China

North America

Europe

Argentina South Africa

Presence of major oil companies (“Majors”)

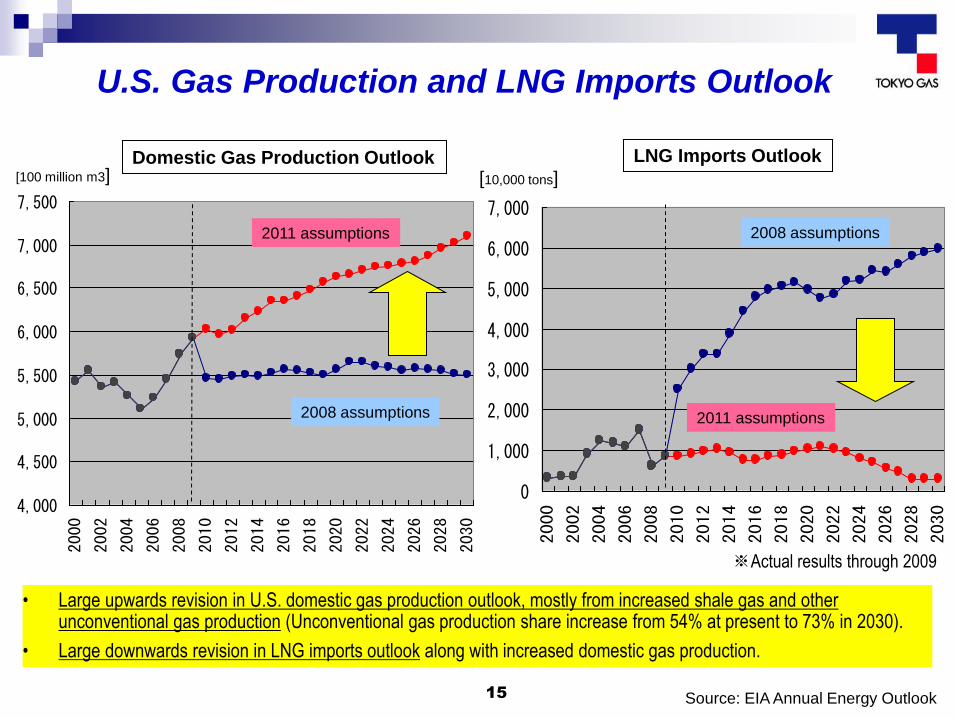

15 Source: EIA Annual Energy Outlook

U.S. Gas Production and LNG Imports Outlook

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

• Large upwards revision in U.S. domestic gas production outlook, mostly from increased shale gas and other unconventional gas production (Unconventional gas production share increase from 54% at present to 73% in 2030).

• Large downwards revision in LNG imports outlook along with increased domestic gas production.

Domestic Gas Production Outlook LNG Imports Outlook

※Actual results through 2009

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2011 assumptions

2008 assumptions

2008 assumptions

2011 assumptions

[100 million m3] [10,000 tons]

16 16 * All rights reserved.

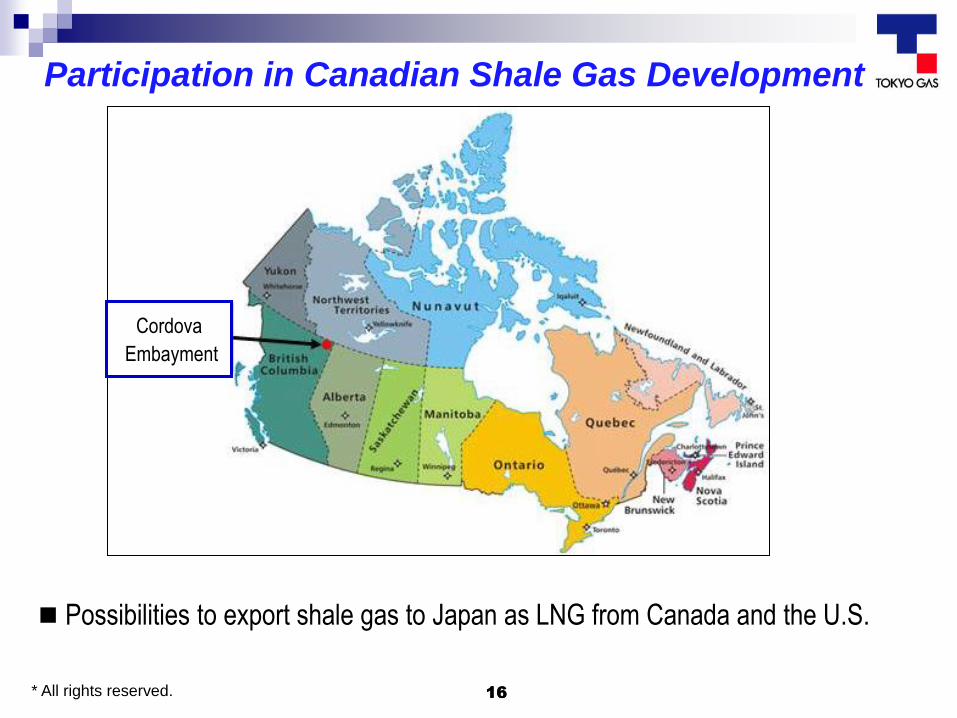

Participation in Canadian Shale Gas Development

Possibilities to export shale gas to Japan as LNG from Canada and the U.S.

Cordova

Embayment

17

North America LNG Export Plan

Kitimat (Canada)

Apache (GN, KOGAS, MC) 10 MTPA; to begin supply in 2015

Shell (Canada)

Partner (CNPC, KOGAS, MC)

Sabin Pass (Louisiana, U.S.; in operation as an LNG receiving terminal)

Free Port (Texas, U.S.; in operation as an LNG receiving terminal)

Sabin PassFree Port

Kitmat

Multiple projects are being advanced to liquefy North American natural gas and export it to Asia and Europe.

* The U.S. was only allowing gas exports to countries that have an FTA with the U.S., but Sabin Pass received permission for exports on May 20.

18

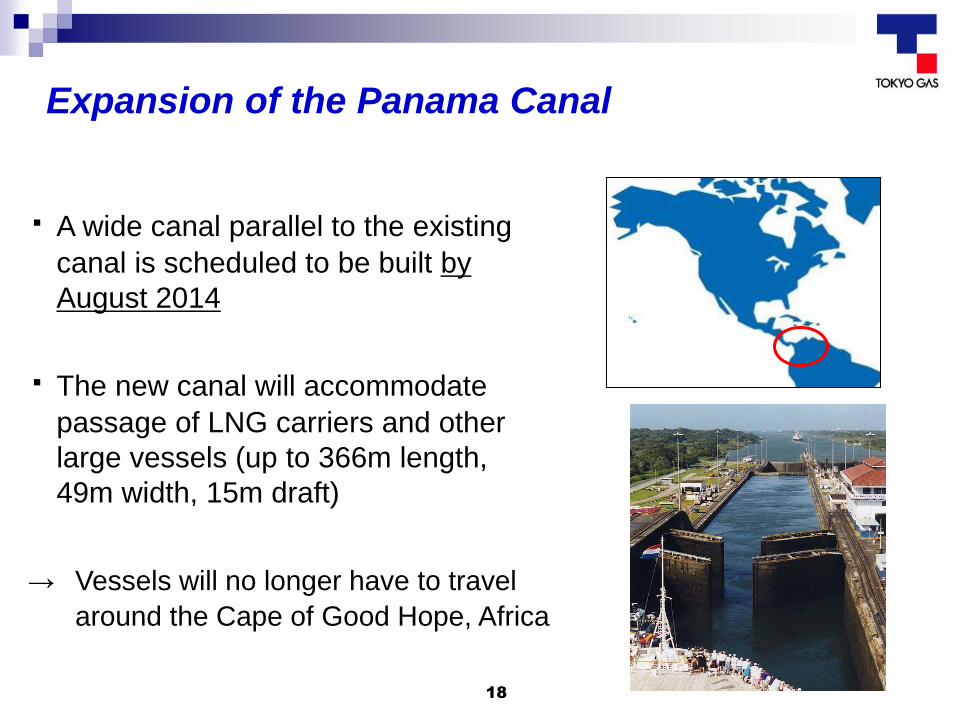

Expansion of the Panama Canal

・ A wide canal parallel to the existing

canal is scheduled to be built by

August 2014

・ The new canal will accommodate

passage of LNG carriers and other

large vessels (up to 366m length,

49m width, 15m draft)

→ Vessels will no longer have to travel

around the Cape of Good Hope, Africa

19 19 * All rights reserved.

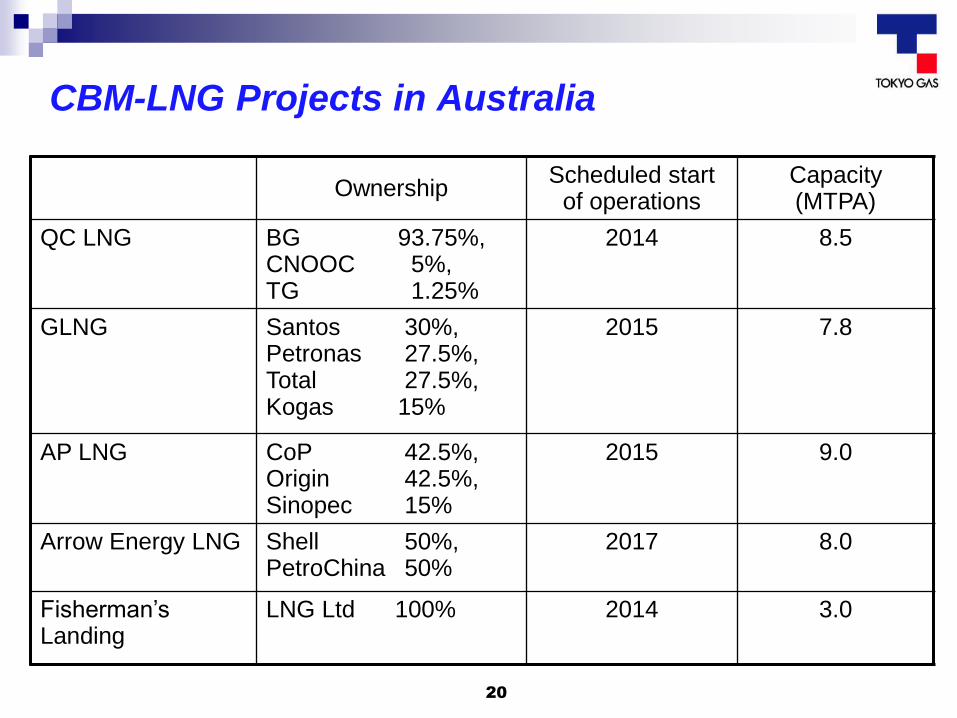

Participation in CBM-LNG Projects in Australia

Several CBM-LNG export projects are currently underway in Queensland.

Potential production volume of 50 MTPA after 2014.

SPA for Queensland Curtis LNG with

BG Group plc. (March 2011)

Tokyo Gas is the first Japanese CBM-LNG buyer.

Source: Wood Mackenzie, JOGMEC

20

CBM-LNG Projects in Australia

Ownership Scheduled start

of operations Capacity (MTPA)

QC LNG BG 93.75%, CNOOC 5%, TG 1.25%

2014 8.5

GLNG Santos 30%, Petronas 27.5%, Total 27.5%, Kogas 15%

2015 7.8

AP LNG CoP 42.5%, Origin 42.5%, Sinopec 15%

2015 9.0

Arrow Energy LNG Shell 50%, PetroChina 50%

2017 8.0

Fisherman’s Landing

LNG Ltd 100% 2014 3.0

21

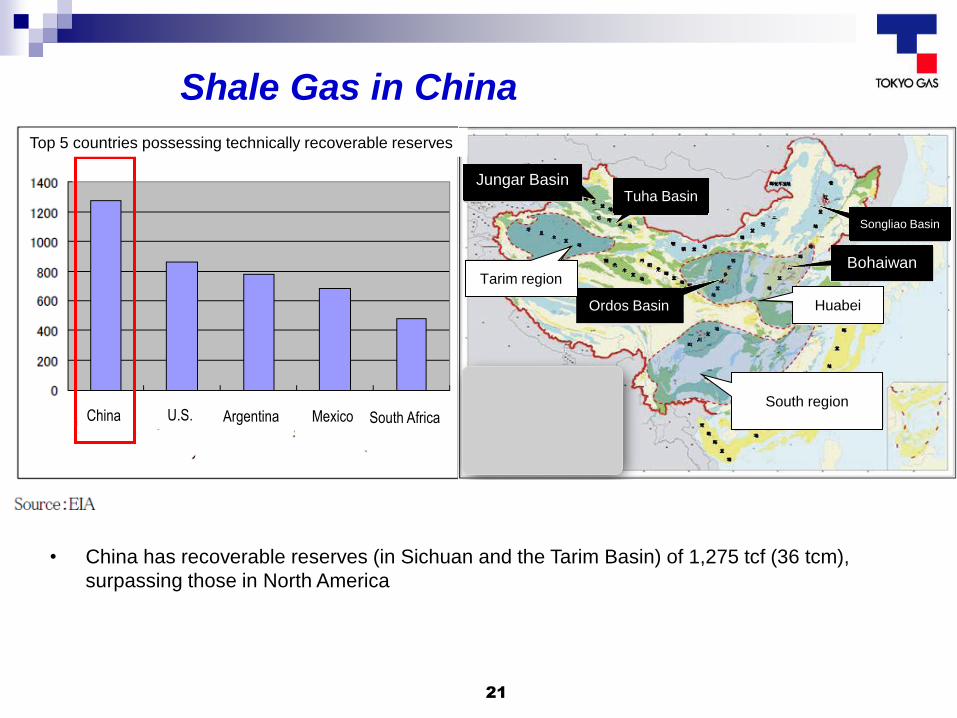

Shale Gas in China

• China has recoverable reserves (in Sichuan and the Tarim Basin) of 1,275 tcf (36 tcm),

surpassing those in North America

Top 5 countries possessing technically recoverable reserves

China U.S. Argentina

Mexico

South Africa

Jungar Basin Tuha Basin

Ordos Basin

Songliao Basin

Bohaiwan Tarim region

Huabei

South region

The LNG Market in Japan

Latest Trends of Unconventional Gas

Impact of Unconventional Gas on the Asia-

Pacific Market

22

Presentation Contents

23

Impact of Unconventional Gas on the Asia-Pacific

Market

・ Progress of shale gas and CBM development in East Asia

・ Start-up of many CMB projects in Australia

Large role in easing the supply-demand balance in the

Asia-Pacific market

24

Impact of Unconventional Gas on the Asia-Pacific

Market

North American shale gas LNG export plan

・ Impact on traditional LNG price in the Asia-Pacific market

・ Enhancement of liquidity in the spot market

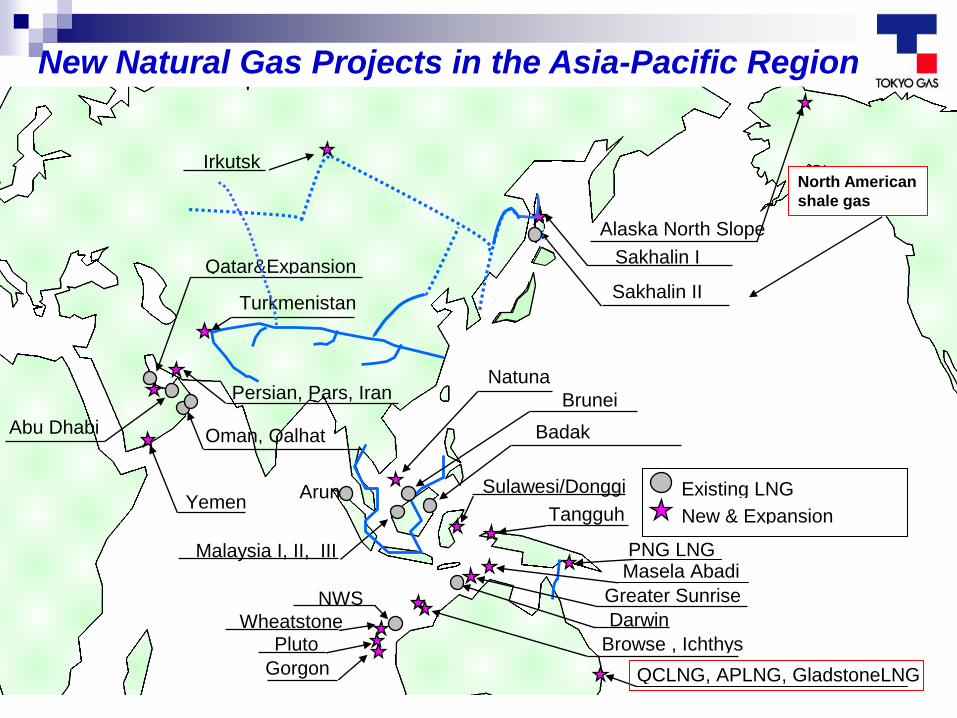

Sakhalin II

Irkutsk

Alaska North Slope

Tangguh

Badak

Qatar&Expansion

Oman, Qalhat

YemenNew & Expansion

Natuna

Turkmenistan

Persian, Pars, Iran

(Iran)

Sulawesi/Donggi Existing LNG Arun

Abu Dhabi

Alaska Kenai

Brunei

Malaysia I, II, III

Darwin

Greater Sunrise

Browse , Ichthys

NWS

Gorgon

PlutoWheatstone

Sakhalin I

QCLNG, APLNG, GladstoneLNG

Masela AbadiPNG LNG

New Natural Gas Projects in the Asia-Pacific Region

North American

shale gas

26

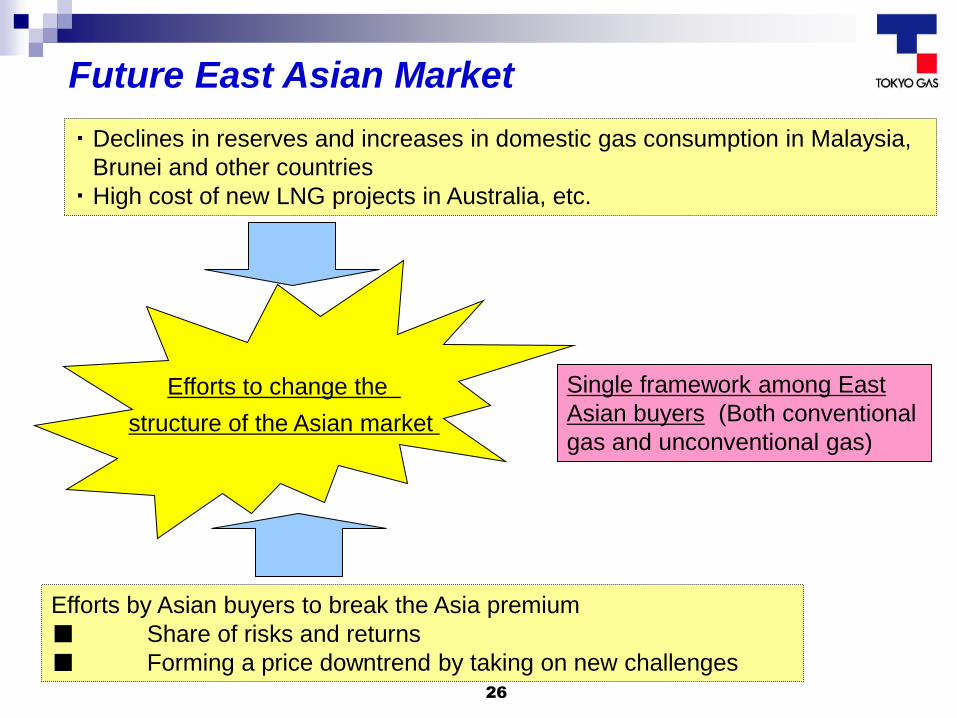

Future East Asian Market

Efforts to change the

structure of the Asian market

・ Declines in reserves and increases in domestic gas consumption in Malaysia,

Brunei and other countries

・ High cost of new LNG projects in Australia, etc.

Efforts by Asian buyers to break the Asia premium

■ Share of risks and returns

■ Forming a price downtrend by taking on new challenges

Single framework among East

Asian buyers (Both conventional

gas and unconventional gas)

27

The “Energy Horizon” (new LNG carrier christened July 6)

Thank you for your kind attention.