DAS INVESTITIONS-POTENTIAL VON ASTANA Investors Service Center.

Our business is developing.

DEG – Deutsche Investitions- und Entwicklungsgesellschaft mbH

The role of DFI’s for providing sustainable long-term funding solutions October, 2012

Agenda

DFI’s Mandate

View on Africa

Risk Capital Approach

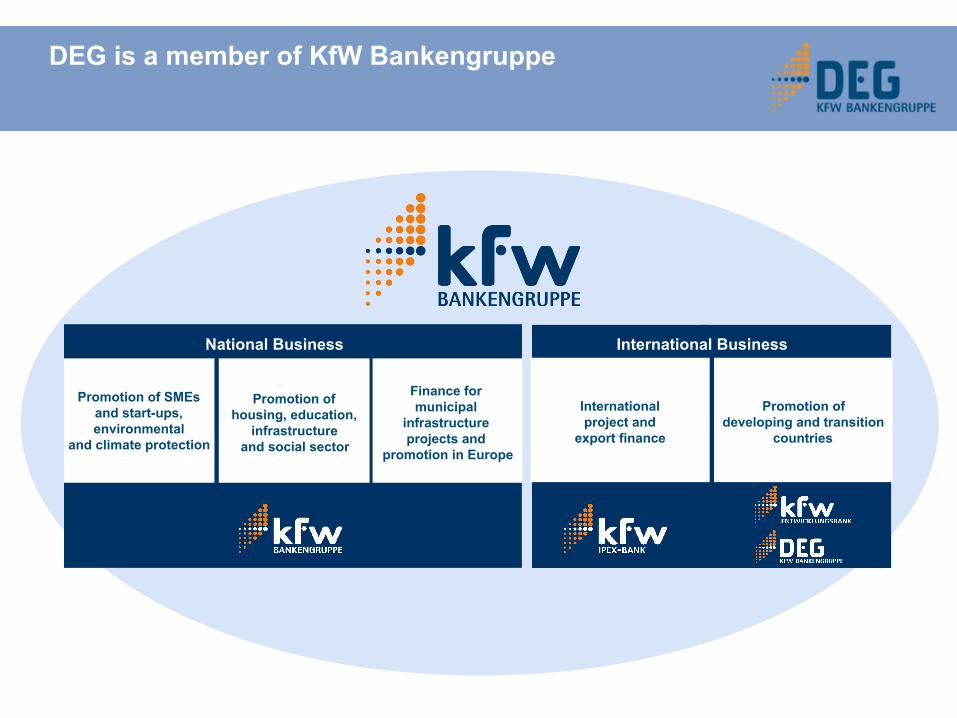

DEG is a member of KfW Bankengruppe

Promotion of developing and transition

countries

International project and

export finance

Promotion of housing, education,

infrastructure and social sector

Promotion of SMEs and start-ups, environmental

and climate protection

Finance for municipal

infrastructure projects and

promotion in Europe

National Business International Business

4

DEG Key Figures

Founded: 1962 Employees: 457 Seat: Köln Shareholder: KfW, Frankfurt Equity 2011: EUR 1.7 billion Total assets 2011: EUR 3.9 billion New commitments in 2011: EUR 1.2 billion (supporting investments worth EUR 6.8 billion)

Portfolio 2011: EUR 5.6 billion (supporting investments worth EUR 39.0 billion)

5

DFI’s Mandate

● Contribution to sustainable economic growth and poverty reduction through Promotion of private sector development in emerging markets

● Providers of long-term capital for private enterprises

● Usually > 4 years up to 15 years

● „Additionality“ by definition; complementary financing to commercial banks / PE funds ● Financing of financially sustainable projects / companies

● Market-oriented terms & conditions

● Environmental and social standards according to Worldbank /IFC guidelines ● Good Corporate Governance

● Positive development impact

6

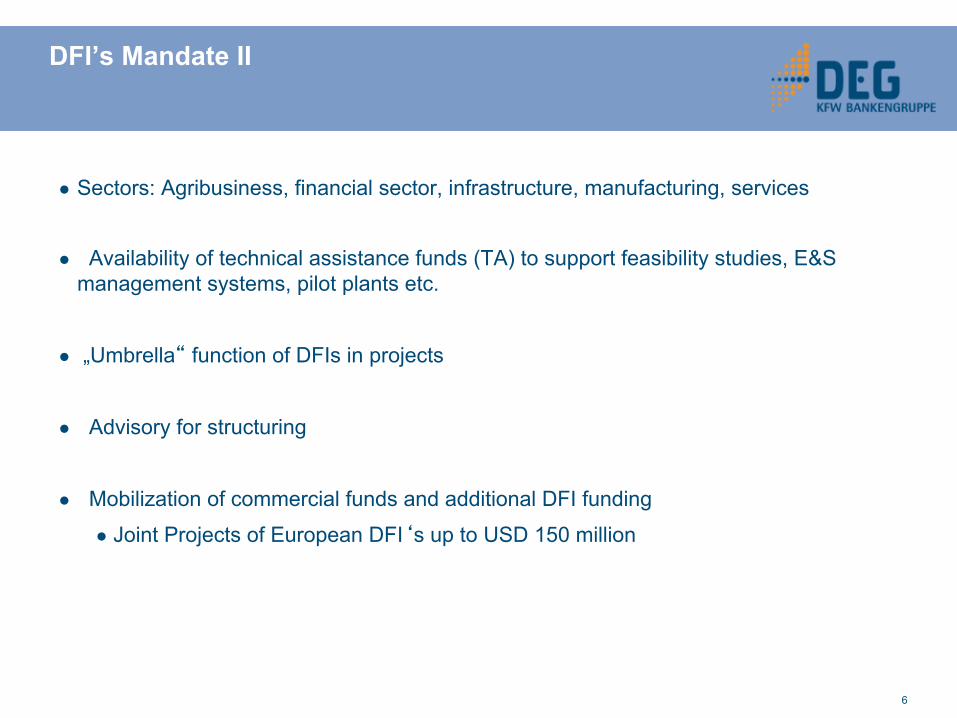

DFI’s Mandate II

● Sectors: Agribusiness, financial sector, infrastructure, manufacturing, services

● Availability of technical assistance funds (TA) to support feasibility studies, E&S management systems, pilot plants etc.

● „Umbrella“ function of DFIs in projects

● Advisory for structuring

● Mobilization of commercial funds and additional DFI funding

● Joint Projects of European DFI‘s up to USD 150 million

7

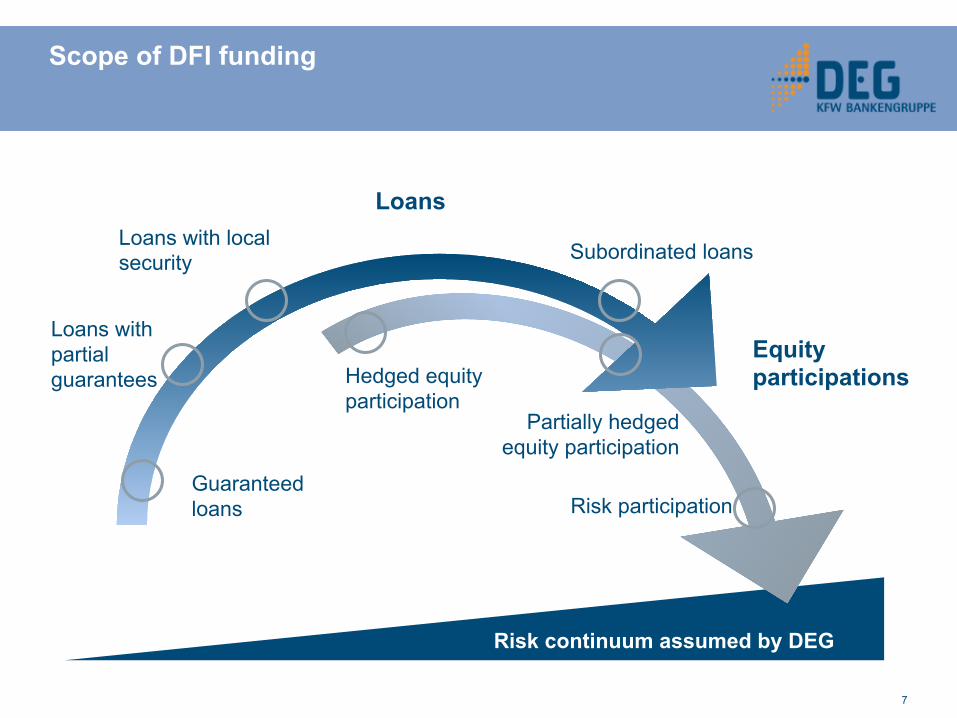

Scope of DFI funding

Risk continuum assumed by DEG

Loans

Guaranteed loans

Loans with partial guarantees Hedged equity

participation

Subordinated loans

Partially hedged equity participation

Risk participation

Loans with local security

Equity participations

8

European Initiatives

European Development Finance Institutions

European Financing Partners S.A.

9

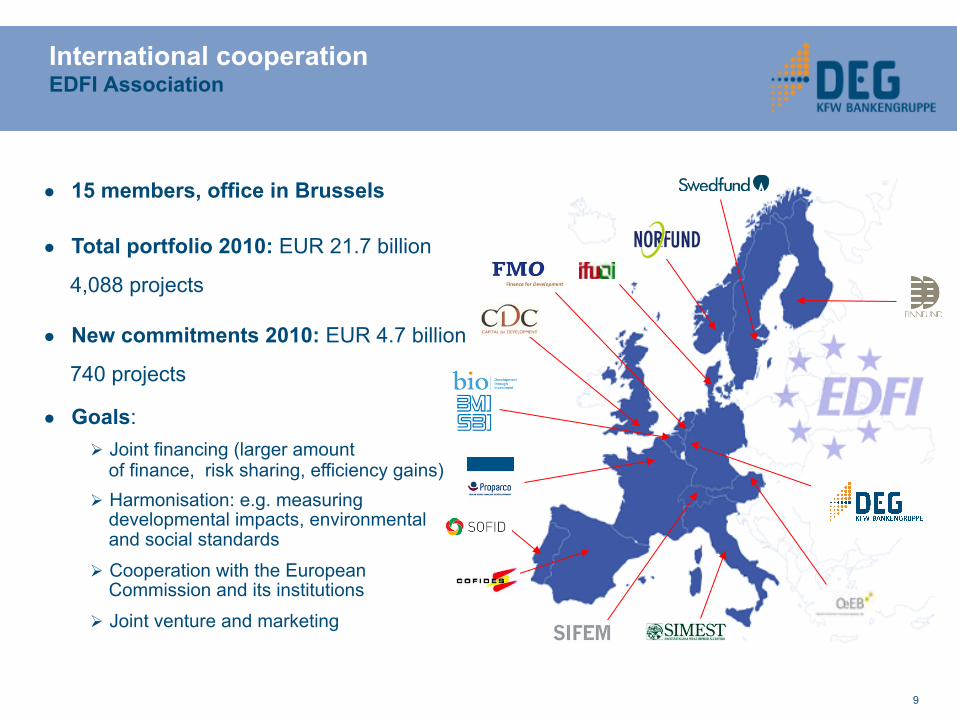

● 15 members, office in Brussels

● Total portfolio 2010: EUR 21.7 billion

4,088 projects

● New commitments 2010: EUR 4.7 billion

740 projects

● Goals: Ø Joint financing (larger amount

of finance, risk sharing, efficiency gains) Ø Harmonisation: e.g. measuring

developmental impacts, environmental and social standards

Ø Cooperation with the European Commission and its institutions

Ø Joint venture and marketing

International cooperation EDFI Association

10

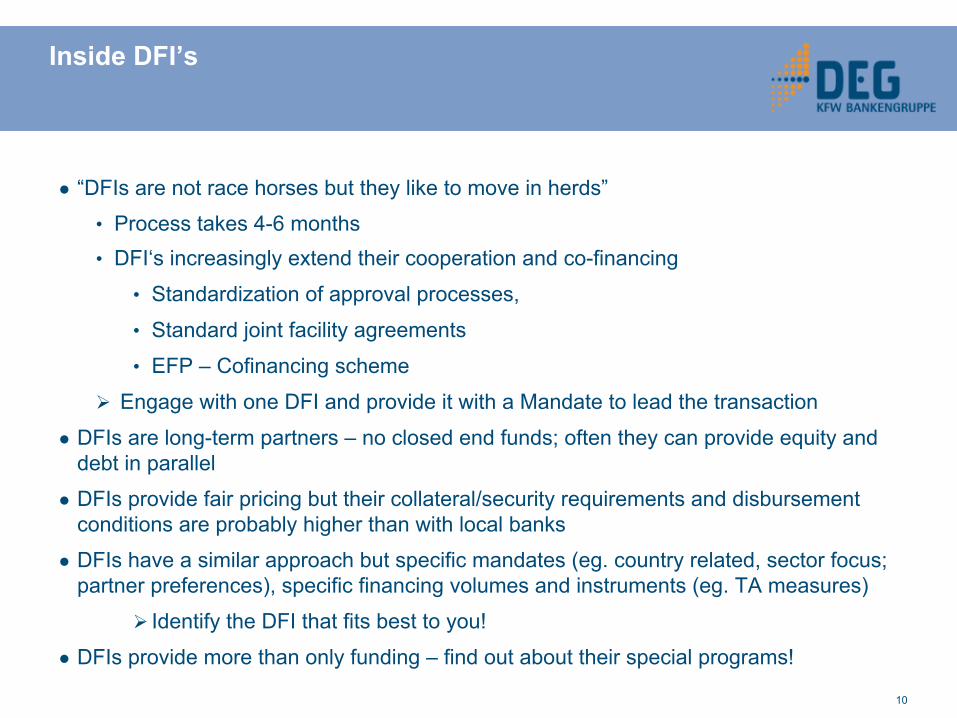

Inside DFI’s

● “DFIs are not race horses but they like to move in herds”

• Process takes 4-6 months • DFI‘s increasingly extend their cooperation and co-financing

• Standardization of approval processes,

• Standard joint facility agreements

• EFP – Cofinancing scheme

Ø Engage with one DFI and provide it with a Mandate to lead the transaction

● DFIs are long-term partners – no closed end funds; often they can provide equity and debt in parallel

● DFIs provide fair pricing but their collateral/security requirements and disbursement conditions are probably higher than with local banks

● DFIs have a similar approach but specific mandates (eg. country related, sector focus; partner preferences), specific financing volumes and instruments (eg. TA measures)

Ø Identify the DFI that fits best to you!

● DFIs provide more than only funding – find out about their special programs!

11

DEG’s strategic focus

Africa and Future Markets

Risk Capital

SME (through SME-funds and local banks)

Climate Protection (renewable energy, energy efficiency, biomass)

German Clients

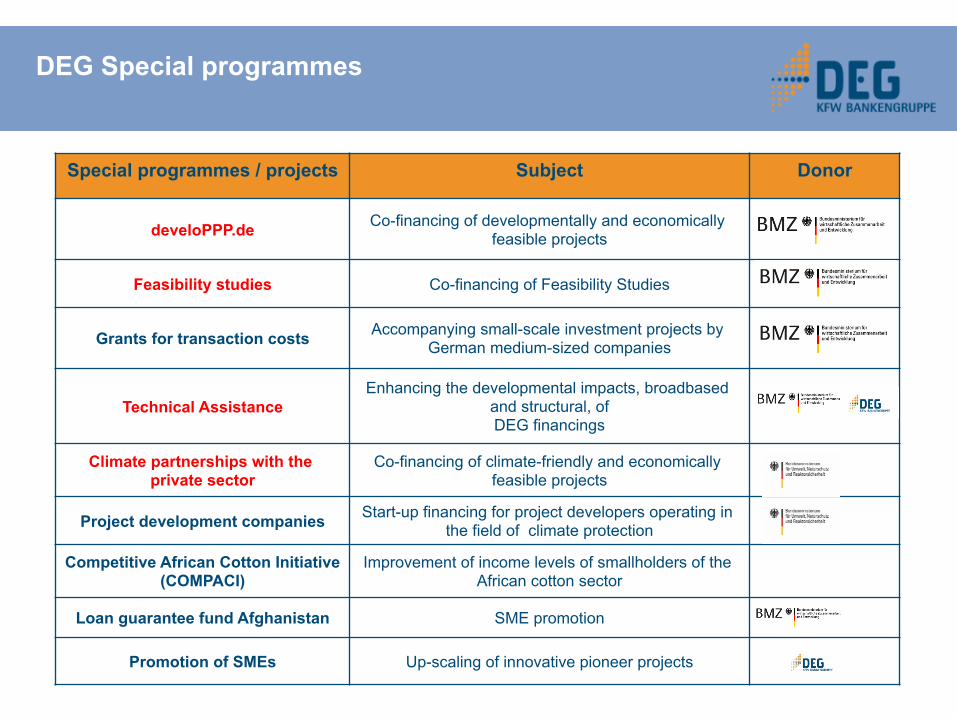

Special programmes / projects Subject Donor

develoPPP.de Co-financing of developmentally and economically feasible projects BMZ

Feasibility studies Co-financing of Feasibility Studies

Grants for transaction costs Accompanying small-scale investment projects by German medium-sized companies

Technical Assistance Enhancing the developmental impacts, broadbased

and structural, of DEG financings

Climate partnerships with the private sector

Co-financing of climate-friendly and economically feasible projects

Project development companies Start-up financing for project developers operating in the field of climate protection

Competitive African Cotton Initiative (COMPACI)

Improvement of income levels of smallholders of the African cotton sector

Loan guarantee fund Afghanistan SME promotion /

Promotion of SMEs Up-scaling of innovative pioneer projects

DEG Special programmes

13

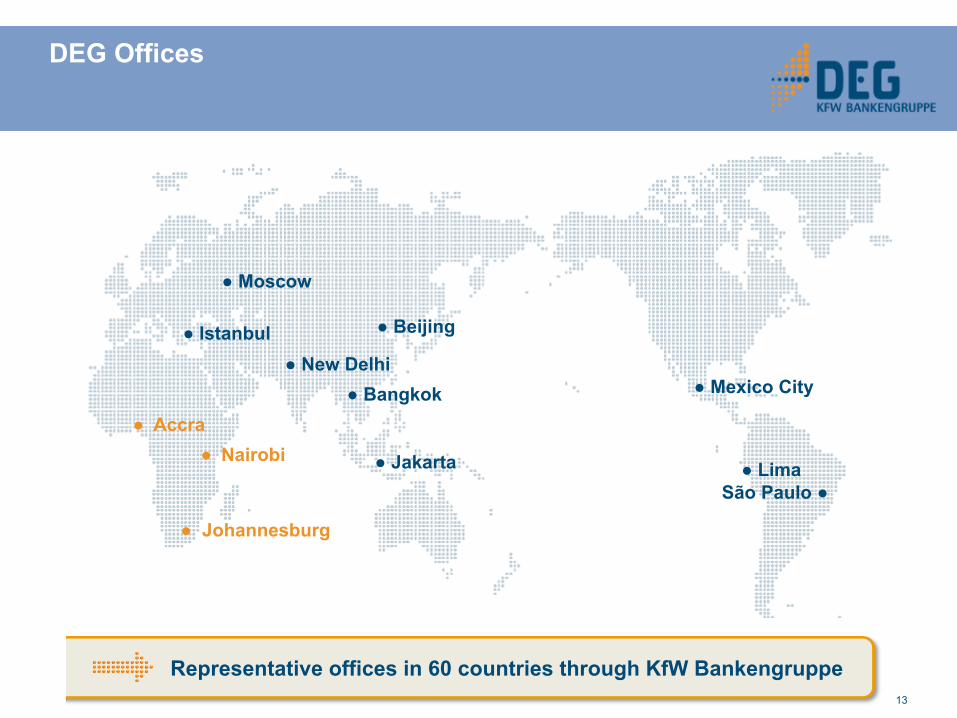

DEG Offices

● Jakarta

● New Delhi

● Johannesburg

● Accra

● Beijing

● Bangkok

São Paulo ● ● Lima

● Mexico City

● Moscow

● Nairobi

● Istanbul

Representative offices in 60 countries through KfW Bankengruppe

Agenda

DFI’s mandate

View on Africa

Risk Capital Approach

15

Outlook for Africa I

● Political stability and governance in Africa have improved: Meanwhile we’ve seen more than 30 times peaceful transitions of that governments or presidents – this trend is expected to continue.

● In recent year a number of African countries have introduced liberal policies (eg. liberalization of telecoms sector) and privatized large state-owned companies

● Africa is the fastest growing region the world after Asia. 7 out of the 10 fastest growing economies in the world until 2015 will be from Sub Saharan Africa. Africa’s economy is expected to grow 7% p.a. over the next 20 years.

● By the year 2050 the population in Africa will double from todays 1 billion to 2 billion and the population is young (median of 18 years) leading to a demographic dividend.

● This will lift long term growth by creating new labor force, urbanization and the related rise of new middle class. By 2020 more than half of African households will have an income exceeding 5,000 USD/Year.

● In 2010 total foreign direct investment was more than $55 billion—five times what it was a decade earlier, and much more than Africa receives in aid. Especially in connection with mining and exploration of natural resources an increase of FDI in medium term can be expected.

16

Outlook for Africa

● Debt levels of African countries are on average much lower than for OECD countries (eg. Kenya 50%; Nigeria 20% Debt/GDP); countries can further leverage the economies and can sustain higher nominal debt levels due to high economic growth

● Prices of natural resources likely to remain high. The USA intends to import from Africa as much oil as from Saudi Arabia by the year 2015. More than 60% of the worlds reserves of – for example – Coltan, Chrome or Cobalt lie under African soil. Substantial new discoveries of oil and gas in East Africa and Mozambique.

● Africa holds 60% of the world’s uncultivated arable land, which will play a key role to ensure global food security.

ð African is becoming one of the most attractive places to invest in the world !

17

Lessons Learnt in Africa

● Building (or expanding) a company in Africa tends to require more time and resources compared to other emerging markets.

● Infrastructure bottlenecks often have an impact on inputs (energy, goods, services) and the distribution of finished goods.

● While top management can mostly be recruited through attractive compensation, experienced middle management and skilled workers are not readily available and need to be trained over time in order to achieve efficiency.

● Once a facility is fully operational, margins are usually much higher than in developed markets, due to low input cost and weak competition combined with high growth.

● As penetration rates (eg. in financial sector) are still low, growth rates can be very high; income elasticity to demand for FMCG, financial services is high

ð Projects need to be developed carefully taking; importance of local partner with good track record

ð Leverage should be conservative and contingencies must be sufficient to meet unexpected cost over-runs

ð Implementation of governance structure is important to avoid mismanagement and fraud

ð Properly managed projects/companies in Africa are highly attractive

18

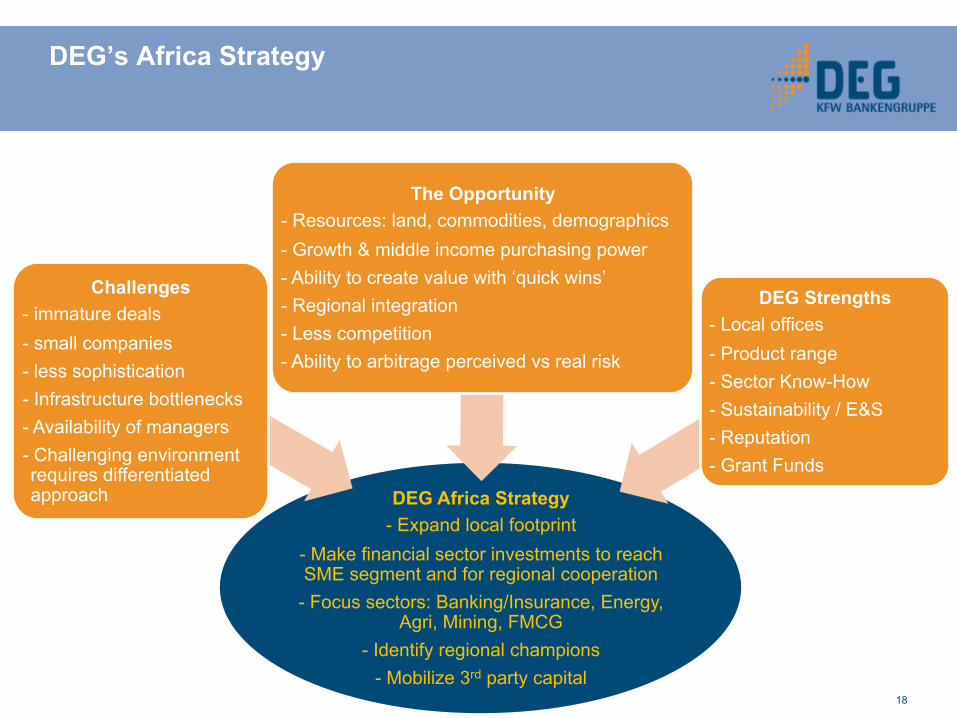

DEG’s Africa Strategy

DEG Africa Strategy - Expand local footprint

- Make financial sector investments to reach SME segment and for regional cooperation

- Focus sectors: Banking/Insurance, Energy, Agri, Mining, FMCG

- Identify regional champions - Mobilize 3rd party capital

Challenges - immature deals - small companies - less sophistication - Infrastructure bottlenecks - Availability of managers - Challenging environment requires differentiated approach

The Opportunity - Resources: land, commodities, demographics - Growth & middle income purchasing power - Ability to create value with ‘quick wins’ - Regional integration - Less competition - Ability to arbitrage perceived vs real risk

DEG Strengths - Local offices - Product range - Sector Know-How - Sustainability / E&S - Reputation - Grant Funds

Agenda

DFI‘s Mandate

View on Africa

Risk Capital Approach

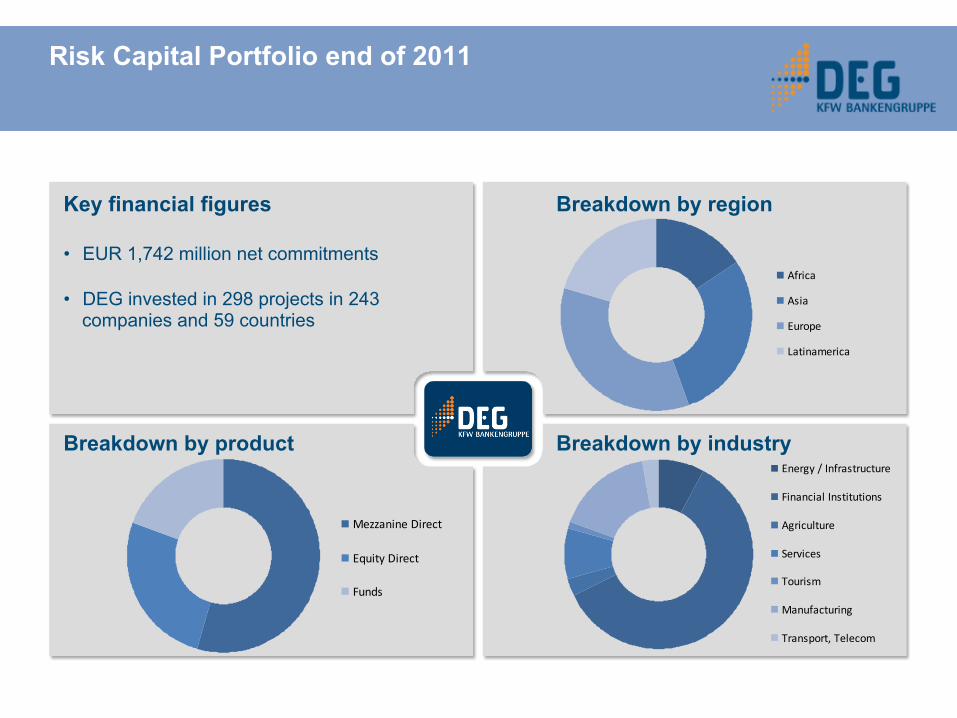

Risk Capital Portfolio end of 2011

Breakdown by region

Breakdown by product Breakdown by industry

Key financial figures • EUR 1,742 million net commitments

• DEG invested in 298 projects in 243

companies and 59 countries

Mezzanine Direct

Equity Direct

Funds

Africa

Asia

Europe

Latinamerica

Energy / Infrastructure

Financial Institutions

Agriculture

Services

Tourism

Manufacturing

Transport, Telecom

Risk Capital Direct Investments

● Size: € 5 – 25 mln

● Risk: moderate, later stage, no rescues, focus on current yield

● Instruments: equity, risk mitigated equity, equity mezz, debt mezz

● DEG Role: significant minority (10-30%), joint control, active shareholder

● Sectors: „old-economy“ sectors, significant sector, partner with sector know-how

● Transactions: prefer growth over buyout, alignment of interest, 5–7 year exit horizon, multiple & reasonable exit options, minority protection rights, risk/return balance

● Countries:

● DEG office countries: all products, comfortable with lead role

● Other Countries: co-invest with aligned local partners, different products

● Exceptions: Financial institutions with comfortable regulatory environment

22

Fund Investments

● Focus on mid-market PE & Mezzanine Funds (USD 100-400 million) targeting Control Transactions or Structured Equity Investments in traditional industries with potential for strong growth and/or consolidation.

● Limited number of sector funds: infrastructure, clean energy/ cleantech, forestry

● No investments in Technology, Real Estate, Early Stage, Distressed Asset Funds

● Experienced Fund Management Team with credible Track Record (but first time funds)

● Buy-and-build Strategies usually create long-term value for Investors and positive development effects such as employment, tax income etc.

� Potential for Co-Investments (Equity and/or Debt at market conditions) free of carry and management fee

● Risk-adequate return expectation (usually 20-30% gross)

23

SME Frontier Initiative

DEG will invest EUR 100m in 10-15 SME-funds within 3 years

DEG expects a relatively lower return for the facility compared to its regular / mid market fund business. In exchange the development impact should be considerably higher.

All potential SME funds need to fulfill the following SME initiative criteria:

● The fund needs to invest in SME; whereas SME should fulfill IFC’s criteria

● In addition to SME-investments the funds need to fulfill one of the following criteria:

- specialized financing instruments (mezzanine or income participating loans)

- focus on particular business segments (e.g. bottom-of-the pyramid, social entrepreneurs, climate change)

- fund invests in low income and/or high risk countries

24

Representative offices of DEG in Africa

Ghana: Andreas Voss

Volta Street No. 7

Airport Residential Area

P.O. Box 9698 K.I.A.

ACCRA

Tel.: + 233 21 7639-42

Fax: + 233 21 7639-41

eMail: [email protected]

Kenya:

Eric Kaleja

Riverside Drive

P.O.Box 52074 – 00200

NAIROBI

Tel. : + 254 20 4228-202

Fax: + 254 20 4228-222

eMail: [email protected]

South Africa:

Michael Fischer

Regent Place, 2nd Floor

Cradock Ave, Rosebank 2196

P.O. Box 2402, Saxonwold 2132

JOHANNESBURG

Tel.: + 27 11 5072-500

Fax: + 27 11 5072-508

eMail: [email protected]