Complete Vig

128

OFFICIAL VOTER INFORMATION GUIDE I, Debra Bowen, Secretary of State of the State of California, hereby certify that the measures included herein will be submitted to the electors at the General Election to be held on November 2, 2010, and that this guide has been prepared in accordance with the law. Witness my hand and the Great Seal of the State in Sacramento, California, this 10th day of August, 2010. Debra Bowen Secretary of State ELECTION TUESD A Y , NOVEMBER 2, 2010 C A L I F O R N I A

Transcript of Complete Vig

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 1/128

OFFICIAL VOTER INFORMATION GUIDE

I, Debra Bowen, Secretary of State of the State of California, hereby certify that the

measures included herein will be submitted to the electors at the General Election to be

held on November 2, 2010, and that this guide has been prepared in accordance with the law.

Witness my hand and the Great Seal of the State in Sacramento, California, this 10th day of August, 2010.

Debra BowenSecretary of State

ELECTIONTUESDAY, NOVEMBER 2, 2010

C A L I F O R N I A

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 2/128

Dear Fellow Voter:By registering to vote, you have taken the rst step in playing an active role in decidingCalifornia’s future. Now, to help you make your decisions, my ofce has created this OfcialVoter Information Guide that contains titles and summaries prepared by Attorney GeneralEdmund G. Brown Jr.; impartial analyses of the law and potential costs to taxpayers preparedby Legislative Analyst Mac Taylor; arguments in favor of and against ballot measures preparedby proponents and opponents; text of the proposed laws prepared/proofed by LegislativeCounsel Diane F. Boyer-Vine; and other useful information. The printing of the guide wasdone under the supervision of Acting State Printer Kevin P. Hannah.

This guide to statewide candidates and measures is just one of the useful tools for learningmore about what will be on your specic ballot. Information about non-statewide candidatesand measures is available in your county sample ballot booklet. (See page 89 of this guide formore details.)

Voting is easy, and any registered voter may vote by mail, or in his or her local polling place.The last day to request a vote-by-mail ballot from your county elections ofce is October 26.

There are more ways to participate in the electoral process. You can:

• Be a poll worker on Election Day, helping to make voting easier for all eligible votersand protecting ballots until they are counted by elections ofcials;

• Spread the word about voter registration deadlines and voting rights through emails,phone calls, brochures, and posters; and

• Help educate other voters about the candidates and issues by organizing discussiongroups or participating in debates with friends, family, and community leaders.

For more information about how and where to vote, as well as other ways you can participatein the electoral process, call (800) 345-VOTE or visit www.sos.ca.gov.

It is a wonderful privilege in a democracy to have a choice and the right to voice youropinion. As you know, some contests really do come down to a narrow margin of just a few votes. Whether you cast your ballot at a polling place or by mail, I encourage you to take thetime to carefully read about each candidate and ballot measure—and to know your votingrights.

Thank you for taking your civic responsibility seriously and making your voice heard!

VISIT THE SECRETARY OF STATE’S WEBSITE TO:

• View information on statewide ballot measures www.voterguide.sos.ca.gov

• Research campaign contributions and lobbying activity http://cal-access.sos.ca.gov/campaign

• Find your polling place on Election Day www.sos.ca.gov/elections/elections_ppl.htm

• Obtain vote-by-mail ballot information www.sos.ca.gov/elections/elections_m.htm

• Watch live election results after polls close on Election Day http://vote.sos.ca.gov

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 3/128

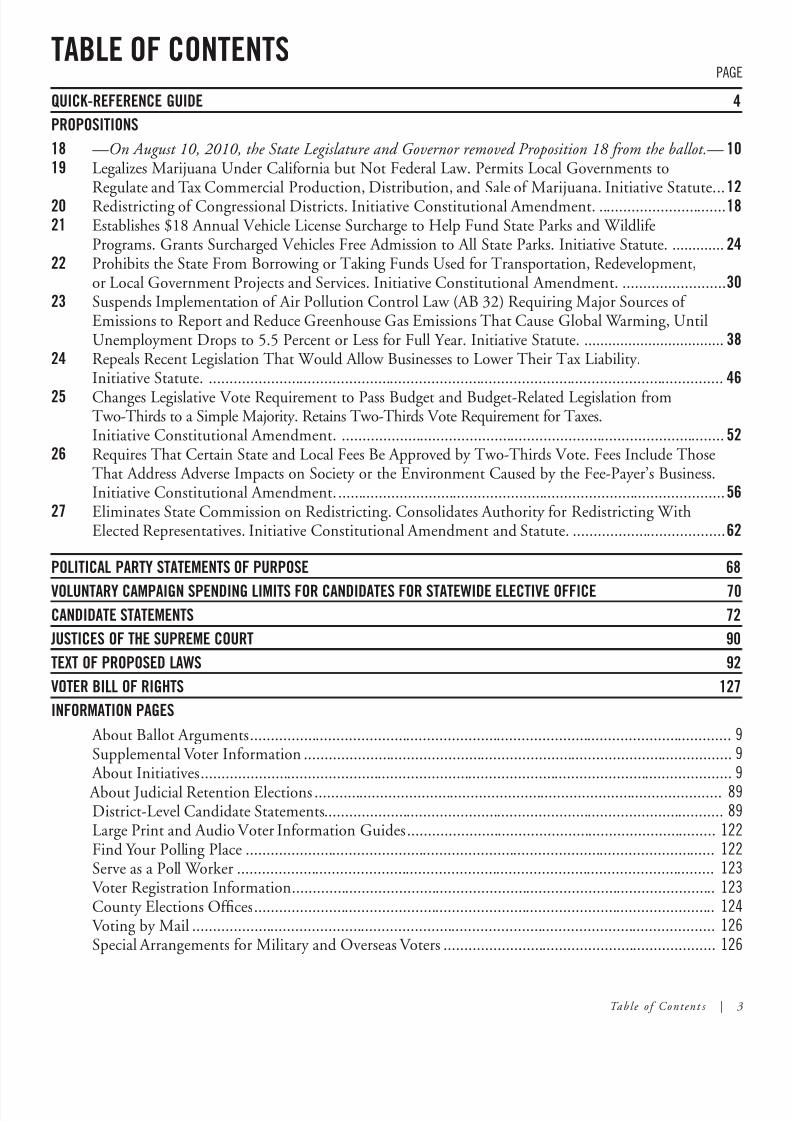

Table of Content s | 3

TABLE OF CONTENTS

QUICK-REFERENCE GUIDE 4

PROPOSITIONS

18 —On August 10, 2010, the State Legislature and Governor removed Proposition 18 from the ballot.— 10

19 Legalizes Marijuana Under California but Not Federal Law. Permits Local Governments to

Regulate and Tax Commercial Production, Distribution, and Sale of Marijuana. Initiative Statute. ..12

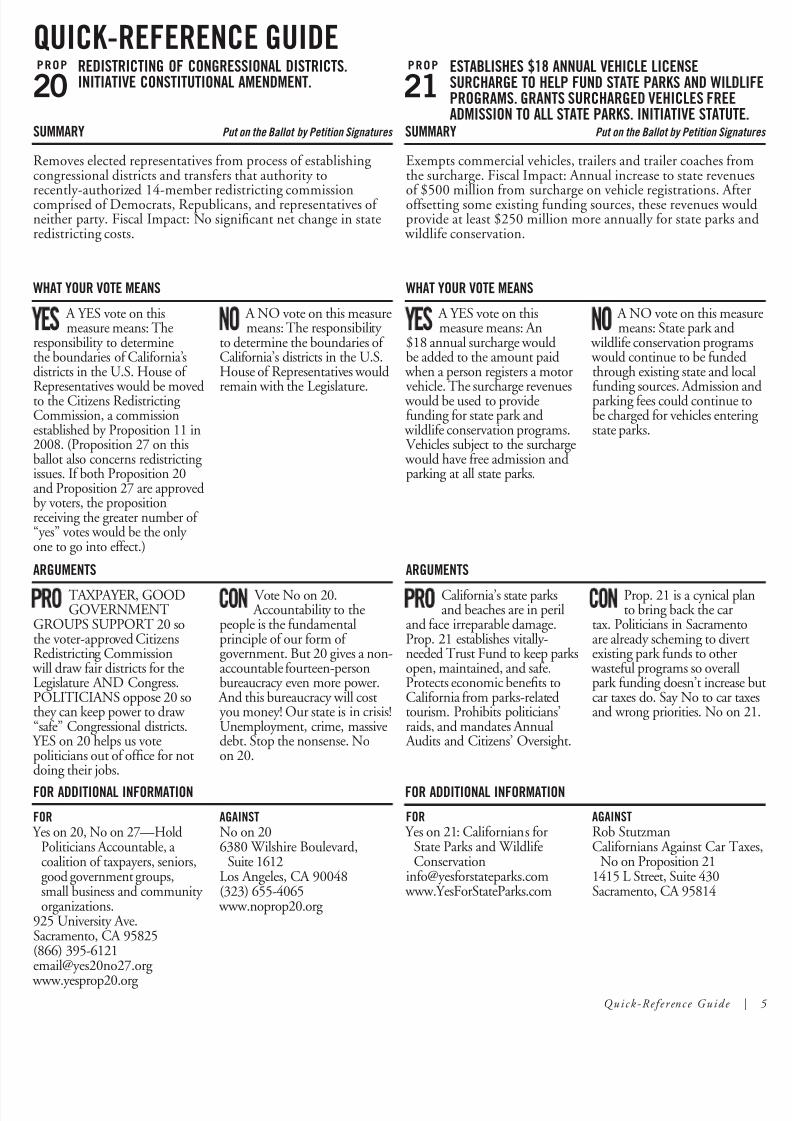

20 Redistricting of Congressional Districts. Initiative Constitutional Amendment. ...............................18

21 Establishes $18 Annual Vehicle License Surcharge to Help Fund State Parks and WildlifePrograms. Grants Surcharged Vehicles Free Admission to All State Parks. Initiative Statute. .............24

22 Prohibits the State From Borrowing or Taking Funds Used for Transportation, Redevelopment,or Local Government Projects and Services. Initiative Constitutional Amendment. .........................30

23 Suspends Implementation of Air Pollution Control Law (AB 32) Requiring Major Sources of Emissions to Report and Reduce Greenhouse Gas Emissions That Cause Global Warming, UntilUnemployment Drops to 5.5 Percent or Less for Full Year. Initiative Statute. ...................................38

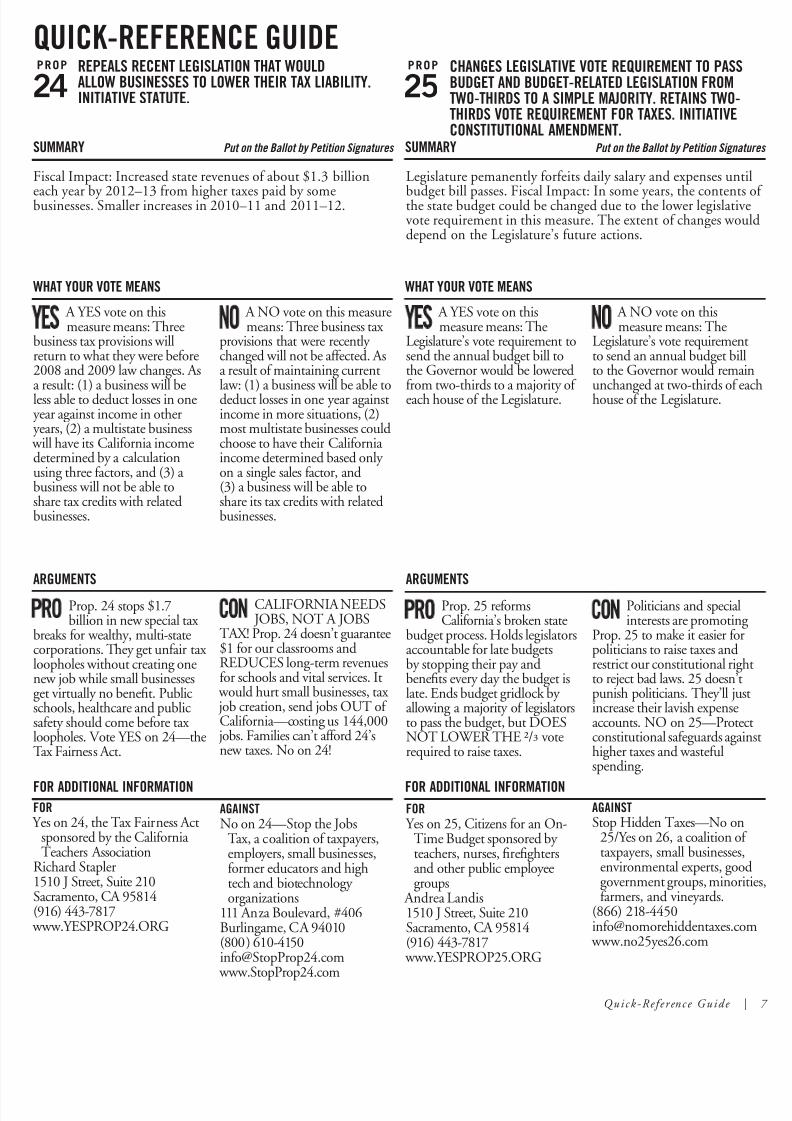

24 Repeals Recent Legislation That Would Allow Businesses to Lower Their Tax Liability.Initiative Statute. .............................................................................................................................46

25 Changes Legislative Vote Requirement to Pass Budget and Budget-Related Legislation fromTwo-Thirds to a Simple Majority. Retains Two-Thirds Vote Requirement for Taxes.Initiative Constitutional Amendment. .............................................................................................52

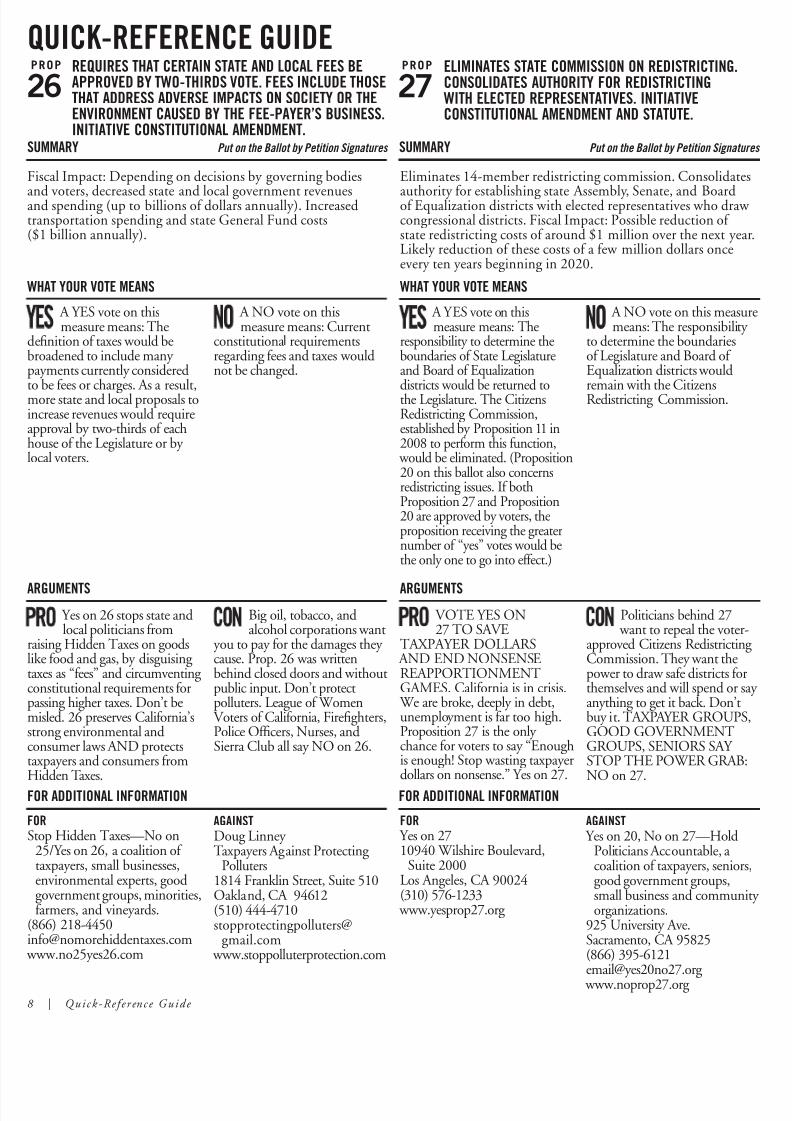

26 Requires That Certain State and Local Fees Be Approved by Two-Thirds Vote. Fees Include ThoseThat Address Adverse Impacts on Society or the Environment Caused by the Fee-Payer’s Business.Initiative Constitutional Amendment. ..............................................................................................56

27 Eliminates State Commission on Redistricting. Consolidates Authority for Redistricting WithElected Representatives. Initiative Constitutional Amendment and Statute. .....................................62

POLITICAL PARTY STATEMENTS OF PURPOSE 68

VOLUNTARY CAMPAIGN SPENDING LIMITS FOR CANDIDATES FOR STATEWIDE ELECTIVE OFFICE 70

CANDIDATE STATEMENTS 72

JUSTICES OF THE SUPREME COURT 90

TEXT OF PROPOSED LAWS 92

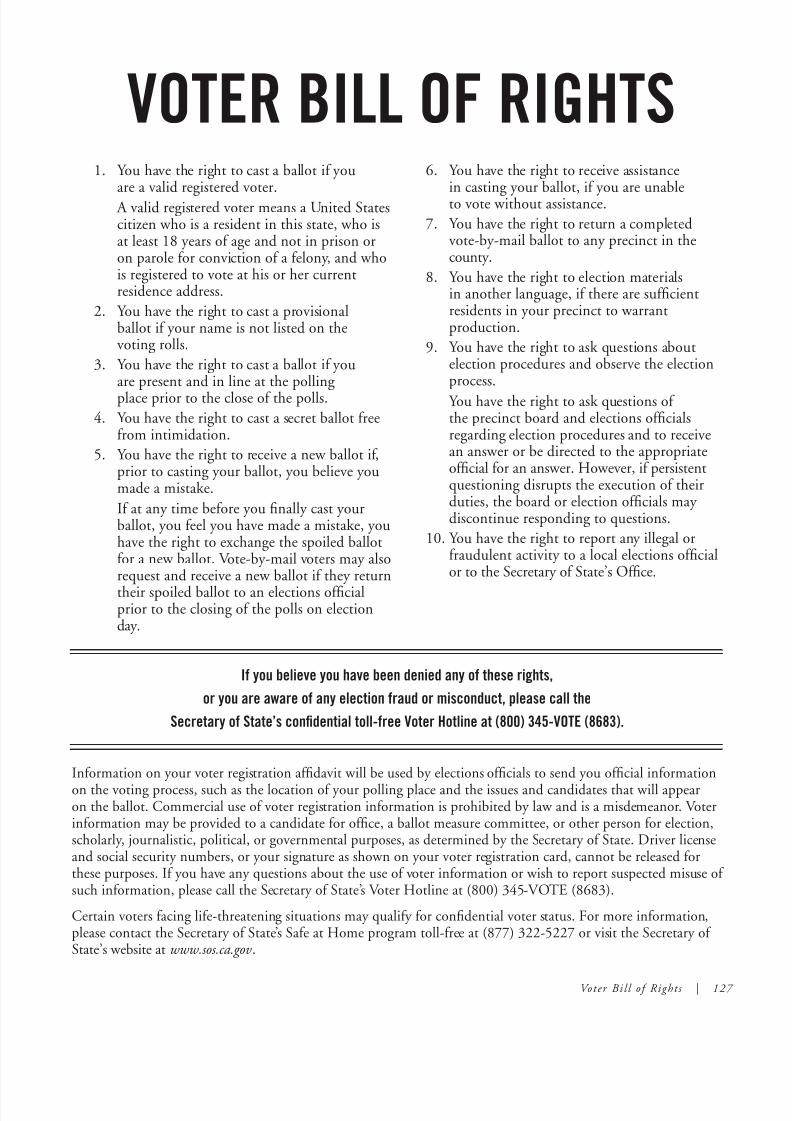

VOTER BILL OF RIGHTS 127

INFORMATION PAGES

PAGE

About Ballot Arguments .....................................................................................................................9 Supplemental Voter Information ........................................................................................................9About Initiatives .................................................................................................................................9

About Judicial Retention Elections ................................................................................................... 89District-Level Candidate Statements .................................................................................................89

Large Print and Audio Voter Information Guides ...........................................................................122Find Your Polling Place .................................................................................................................. 122

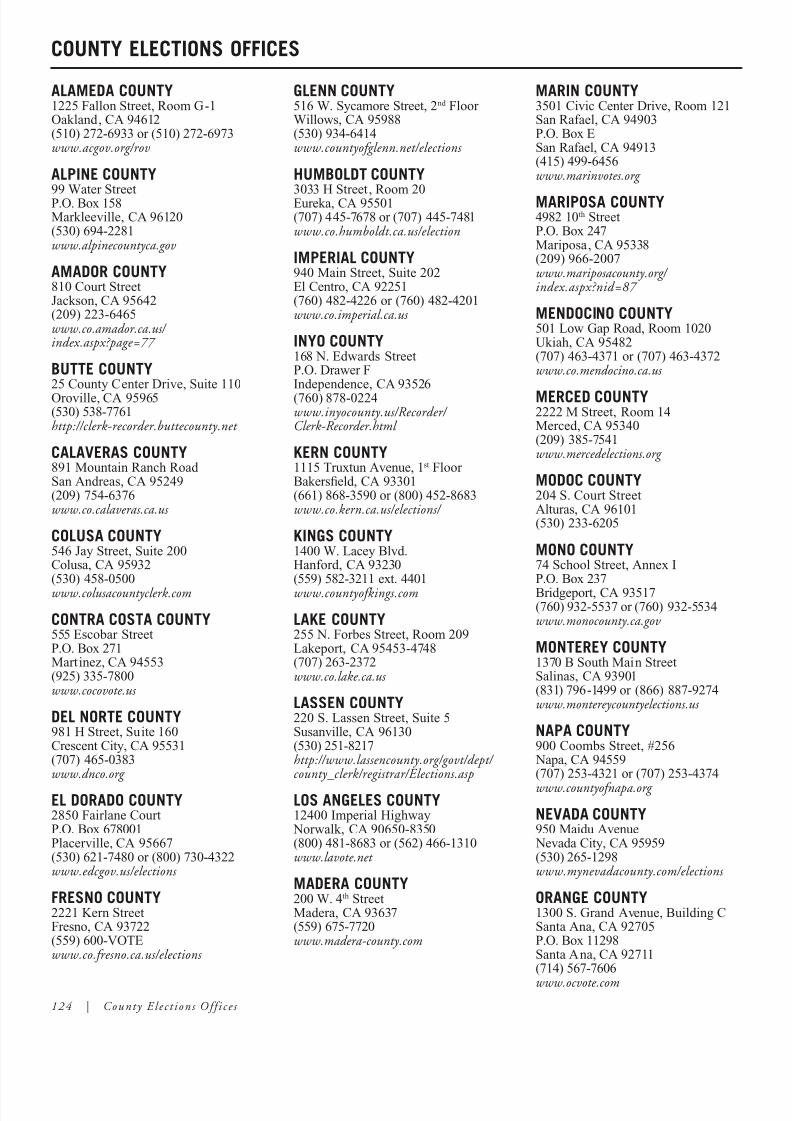

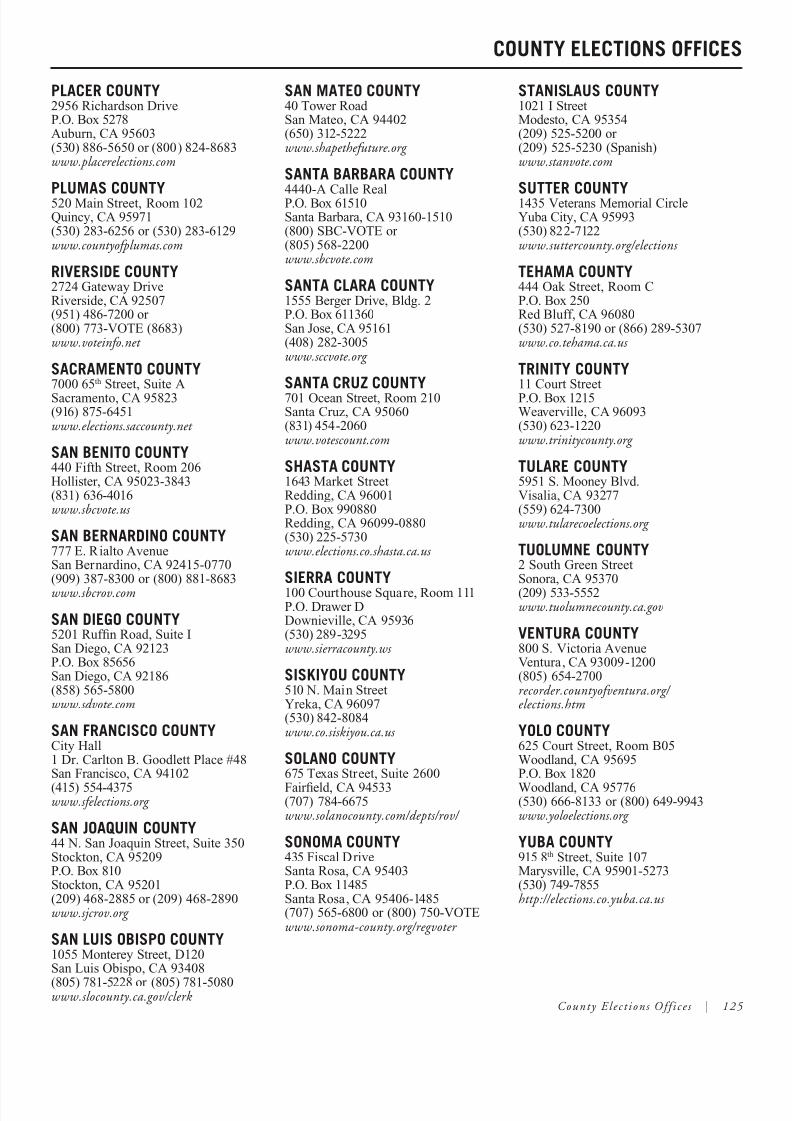

Serve as a Poll Worker .................................................................................................................... 123 Voter Registration Information ....................................................................................................... 123 County Elections Ofces................................................................................................................ 124

Voting by Mail ...............................................................................................................................126Special Arrangements for Military and Overseas Voters ..................................................................126

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 4/128

QUICK-REFERENCE GUIDEPROP

FOR ADDITIONAL INFORMATION

ARGUMENTS

Opposed by Mothers Against Drunk Driving

(MADD) because allows driversto smoke marijuana until themoment they climb behind the wheel. Endangers public safety. Jeopardizes $9,400,000,000.00in school funding, billions infederal contracts, thousands of jobs. Opposed by California’sSheriffs, Police Chiefs,Firefghters and District Attorneys. Vote “No” on 19.

COMMON SENSECONTROL OF

MARIJUANA. Stops wastingtaxpayer dollars on failedmarijuana prohibition. Controlsand taxes marijuana like alcohol.Makes marijuana availableonly to adults. Adds criminalpenalties for giving it to anyoneunder 21. Weakens drug cartels.Enforces road and workplacesafety. Generates billions inrevenue. Saves taxpayers money.

FOR James Rigdon Yes on Proposition 191776 Broadway Oakland, CA 94612(510) [email protected] www.yeson19.com

AGAINSTNo On Proposition 19—

Public Safety [email protected] www.NoOnProposition19.com

WHAT YOUR VOTE MEANS

Allows people 21 years old or older to possess, cultivate, ortransport marijuana for personal use. Fiscal Impact: Depending

on federal, state, and local government actions, potentialincreased tax and fee revenues in the hundreds of millions of dollars annually and potential correctional savings of severaltens of millions of dollars annually.

SUMMARY Put on the Ballot by Petition Signature

A NO vote on this measurmeans: The possession and

cultivation of marijuana forpersonal use and commercialmarijuana-related activities

would remain illegal understate law, unless allowed underthe state’s existing medicalmarijuana law.

A YES vote on thismeasure means:

Individuals age 21 or oldercould, under state law, possessand cultivate limited amounts

of marijuana for personal use.In addition, the state and localgovernments could authorize,regulate, and tax commercialmarijuana-related activitiesunder certain conditions. Theseactivities would remain illegalunder federal law.

LEGALIZES MARIJUANA UNDER CALIFORNIA BUT NOT FEDERALAW. PERMITS LOCAL GOVERNMENTS TO REGULATE AND TAXCOMMERCIAL PRODUCTION, DISTRIBUTION, AND SALE OFMARIJUANA. INITIATIVE STATUTE.

19

On August 10, 2010, the State Legislature and

Governor removed Proposition 18 from the ballot.

4 | Quick-Re f e rence Guide

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 5/128

QUICK-REFERENCE GUIDEPROP PROP

FOR ADDITIONAL INFORMATIONFOR ADDITIONAL INFORMATION

FORYes on 20, No on 27—Hold

Politicians Accountable, acoalition of taxpayers, seniors,good government groups,small business and community organizations.

925 University Ave.Sacramento, CA 95825(866) [email protected]

www.yesprop20.org

AGAINSTNo on 206380 Wilshire Boulevard,

Suite 1612Los Angeles, CA 90048(323) 655-4065 www.noprop20.org

FOR Yes on 21: Californians for

State Parks and WildlifeConservation

[email protected] www.YesForStateParks.com

AGAINSTRob StutzmanCalifornians Against Car Taxe

No on Proposition 211415 L Street, Suite 430Sacramento, CA 95814

ARGUMENTS ARGUMENTS

Prop. 21 is a cynical planto bring back the car

tax. Politicians in Sacramentoare already scheming to divertexisting park funds to other wasteful programs so overallpark funding doesn’t increase bcar taxes do. Say No to car taxeand wrong priorities. No on 21

California’s state parksand beaches are in peril

and face irreparable damage.Prop. 21 establishes vitally-needed Trust Fund to keep parksopen, maintained, and safe.Protects economic benefts toCalifornia from parks-relatedtourism. Prohibits politicians’raids, and mandates Annual Audits and Citizens’ Oversight.

Vote No on 20. Accountability to the

people is the fundamentalprinciple of our form of government. But 20 gives a non-accountable fourteen-personbureaucracy even more power. And this bureaucracy will costyou money! Our state is in crisis!Unemployment, crime, massivedebt. Stop the nonsense. Noon 20.

TAXPAYER, GOODGOVERNMENT

GROUPS SUPPORT 20 sothe voter-approved CitizensRedistricting Commissionwill draw fair districts for theLegislature AND Congress.POLITICIANS oppose 20 sothey can keep power to draw “safe” Congressional districts.YES on 20 helps us votepoliticians out of of fce for notdoing their jobs.

WHAT YOUR VOTE MEANSWHAT YOUR VOTE MEANS

Removes elected representatives from process of establishingcongressional districts and transfers that authority to

recently-authorized 14-member redistricting commissioncomprised of Democrats, Republicans, and representatives of neither party. Fiscal Impact: No signifcant net change in stateredistricting costs.

Exempts commercial vehicles, trailers and trailer coaches fromthe surcharge. Fiscal Impact: Annual increase to state revenues

of $500 million from surcharge on vehicle registrations. Afteroffsetting some existing funding sources, these revenues wouldprovide at least $250 million more annually for state parks and wildlife conservation.

SUMMARY Put on the Ballot by Petition Signatur

A NO vote on this measurmeans: State park and

wildlife conservation programs would continue to be fundedthrough existing state and local

funding sources. Admission anparking fees could continue tobe charged for vehicles enteringstate parks.

A YES vote on thismeasure means: An

$18 annual surcharge wouldbe added to the amount paid when a person registers a motor

vehicle. The surcharge revenues would be used to providefunding for state park and wildlife conservation programs.Vehicles subject to the surcharge would have free admission andparking at all state parks.

ESTABLISHES $18 ANNUAL VEHICLE LICENSESURCHARGE TO HELP FUND STATE PARKS AND WILDLIFPROGRAMS. GRANTS SURCHARGED VEHICLES FREEADMISSION TO ALL STATE PARKS. INITIATIVE STATUTE.

21

A NO vote on this measuremeans: The responsibility

to determine the boundaries of California’s districts in the U.S.House of Representatives would

remain with the Legislature.

A YES vote on thismeasure means: The

responsibility to determinethe boundaries of California’sdistricts in the U.S. House of

Representatives would be movedto the Citizens RedistrictingCommission, a commissionestablished by Proposition 11 in2008. (Proposition 27 on thisballot also concerns redistrictingissues. If both Proposition 20and Proposition 27 are approvedby voters, the propositionreceiving the greater number of “yes” votes would be the only one to go into effect.)

SUMMARY Put on the Ballot by Petition Signatures

20REDISTRICTING OF CONGRESSIONAL DISTRICTS.INITIATIVE CONSTITUTIONAL AMENDMENT.

Quick-Re f e rence Guide |

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 6/128

QUICK-REFERENCE GUIDEPROP PROP

ARGUMENTSRGUMENTS

FOR ADDITIONAL INFORMATIONOR ADDITIONAL INFORMATION

YES on 22 stops statepoliticians from taking

ocal government funds. 22tops the State from takingas taxes voters have dedicatedo transportation. 22 protectsocal services: 9-1-1 emergency esponse, police, fre, libraries,ransit, road repairs. Supportedy California Fire Chiefs

Association, California PoliceChiefs Association, CaliforniaLibrary Association.

California’s teachers,frefghters, nurses, and

taxpayer advocates say NO on22. If 22 passes, public schoolsstand to lose billions of dollars.22 takes money frefghters useto fght fres and natural disasters while protecting redevelopmentagencies and their developerfriends. Another propositionthat sounds good, but makesthings worse.

Texas oil companiesdesigned 23 to kill

clean energy and air pollutionstandards in California. 23threatens public health withmore air pollution, increasesdependence on costly oil, andkills competition from job-creating California wind andsolar companies. AmericanLung Association in California,California ProfessionalFirefghters: NO on 23.

ORYes on 22, Californians to

Protect Local Taxpayers &Vital Services121 L Street #803acramento, CA 95814888) [email protected]

www.SaveLocalServices.com

AGAINSTNo on 22—Citizens Against

Taxpayer Giveaways,sponsored by CaliforniaProfessional Firefghters.

Joshua Heller1510 J Street, Suite 210Sacramento, CA 95814(916) 443-7817 www.votenoprop22.com

FOR Yes on 23—A coalition of

taxpayers, small business,frefghters, labor, agriculture,transportation, food producers,energy and forestry companiesand air quality of fcials.

1215 K Street, Suite 2260Sacramento, CA 95814(866) [email protected]

www.yeson23.com

AGAINSTNo on 23: Californians to Stop

the Dirty Energy Proposition(888) [email protected]

Yes on 23 saves jobs,prevents energy tax

increases, and helps families, while preserving California’sclean air and water laws.California can’t afford self-imposed energy costs thatdon’t reduce global warming.2.3 million Californians areunemployed; Proposition 23 will save over a million jobs that would otherwise be destroyed. www.yeson23.com

WHAT YOUR VOTE MEANSWHAT YOUR VOTE MEANS

Prohibits State, even during severe fscal hardship, from delaying

distribution of tax revenues for these purposes. Fiscal Impact:Decreased state General Fund spending and/or increased stateevenues, probably in the range of $1 billion to several billionsf dollars annually. Comparable increases in funding for statend local transportation programs and local redevelopment.

Fiscal Impact: Likely modest net increase in overall economic

activity in the state from suspension of greenhouse gasesregulatory activity, resulting in a potentially signifcant netincrease in state and local revenues.

A NO vote on this measuremeans: The state could

continue to implement themeasures authorized under Assembly Bill 32 to address

global warming.

A YES vote on thismeasure means:

Certain existing and proposedregulations authorized understate law (“Assembly Bill 32”) to

address global warming wouldbe suspended. These regulations would remain suspended untilthe state unemployment ratedrops to 5.5 percent or lower forone year.

SUMMARY Put on the Ballot by Petition Signature

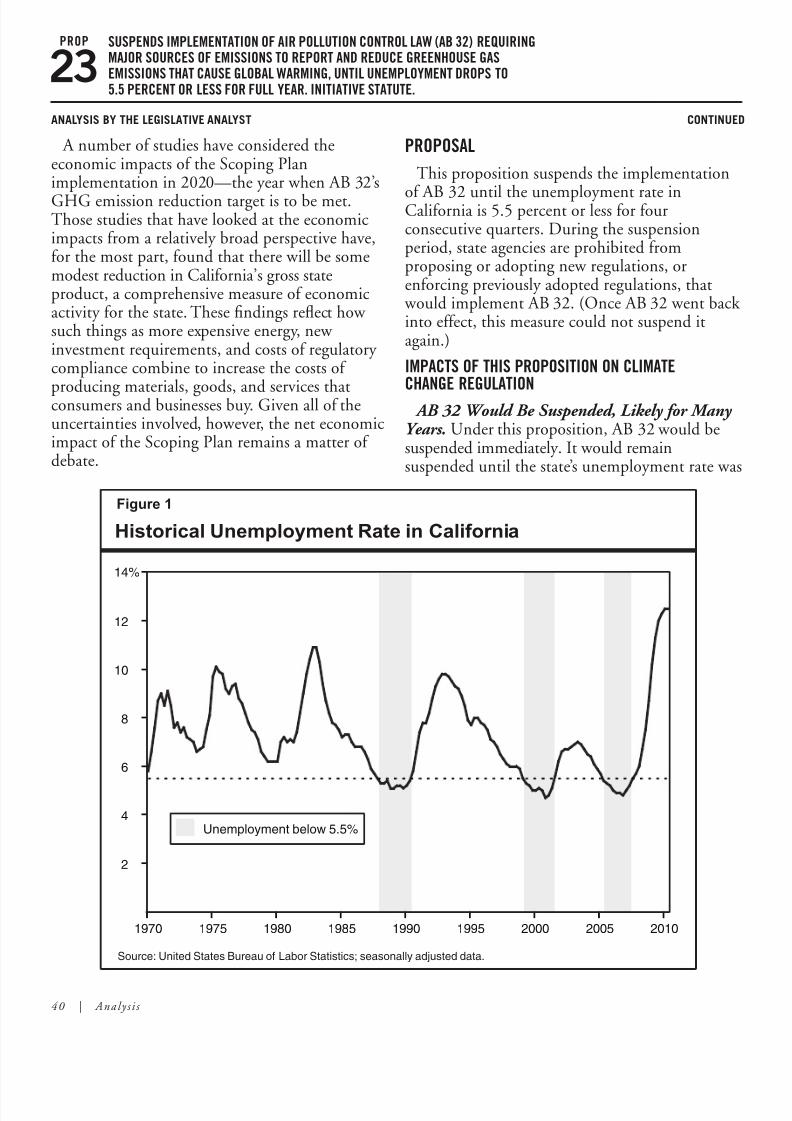

SUSPENDS IMPLEMENTATION OF AIR POLLUTION CONTROLLAW (AB 32) REQUIRING MAJOR SOURCES OF EMISSIONS TOREPORT AND REDUCE GREENHOUSE GAS EMISSIONS THATCAUSE GLOBAL WARMING, UNTIL UNEMPLOYMENT DROPS TO5.5 PERCENT OR LESS FOR FULL YEAR. INITIATIVE STATUTE.

23

A NO vote on this measuremeans: The state’s current

authority over state fuel taxand local property tax revenues would not be affected.

A YES vote on thismeasure means: The

tate’s authority to use oredirect state fuel tax and local

property tax revenues would be

ignifcantly restricted.

PROHIBITS THE STATE FROM BORROWING OR TAKINGFUNDS USED FOR TRANSPORTATION, REDEVELOPMENT,OR LOCAL GOVERNMENT PROJECTS AND SERVICES.INITIATIVE CONSTITUTIONAL AMENDMENT.

22

UMMARY Put on the Ballot by Petition Signatures

6 | Quick-Re f e rence Guide

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 7/128

QUICK-REFERENCE GUIDEPROP PROP

ARGUMENTS ARGUMENTS

FOR ADDITIONAL INFORMATIONFOR ADDITIONAL INFORMATION

Prop. 24 stops $1.7billion in new special tax

breaks for wealthy, multi-statecorporations. They get unfair taxloopholes without creating onenew job while small businessesget virtually no beneft. Publicschools, healthcare and publicsafety should come before taxloopholes. Vote YES on 24—theTax Fairness Act.

CALIFORNIA NEEDS JOBS, NOT A JOBS

TAX! Prop. 24 doesn’t guarantee$1 for our classrooms andREDUCES long-term revenuesfor schools and vital services. It would hurt small businesses, tax job creation, send jobs OUT of California—costing us 144,000 jobs. Families can’t afford 24’snew taxes. No on 24!

Prop. 25 reformsCalifornia’s broken state

budget process. Holds legislatorsaccountable for late budgetsby stopping their pay andbenefts every day the budget islate. Ends budget gridlock by allowing a majority of legislatorsto pass the budget, but DOESNOT LOWER THE ²/³ voterequired to raise taxes.

Politicians and specialinterests are promoting

Prop. 25 to make it easier forpoliticians to raise taxes andrestrict our constitutional rightto reject bad laws. 25 doesn’tpunish politicians. They’ll justincrease their lavish expenseaccounts. NO on 25—Protectconstitutional safeguards againshigher taxes and wastefulspending.

FORYes on 24, the Tax Fairness Act

sponsored by the CaliforniaTeachers Association

Richard Stapler1510 J Street, Suite 210Sacramento, CA 95814(916) 443-7817www.YESPROP24.ORG

AGAINSTNo on 24—Stop the Jobs

Tax, a coalition of taxpayers,employers, small businesses,former educators and hightech and biotechnology organizations

111 Anza Boulevard, #406Burlingame, CA 94010(800) [email protected] www.StopProp24.com

AGAINSTStop Hidden Taxes—No on

25/Yes on 26, a coalition of taxpayers, small businesses,environmental experts, goodgovernment groups, minoritiefarmers, and vineyards.

(866) [email protected] www.no25yes26.com

FOR Yes on 25, Citizens for an On-

Time Budget sponsored by teachers, nurses, frefghtersand other public employeegroups

Andrea Landis1510 J Street, Suite 210Sacramento, CA 95814(916) 443-7817 www.YESPROP25.ORG

WHAT YOUR VOTE MEANSWHAT YOUR VOTE MEANS

Legislature pemanently forfeits daily salary and expenses until

budget bill passes. Fiscal Impact: In some years, the contents othe state budget could be changed due to the lower legislativevote requirement in this measure. The extent of changes woulddepend on the Legislature’s future actions.

Fiscal Impact: Increased state revenues of about $1.3 billion

each year by 2012–13 from higher taxes paid by somebusinesses. Smaller increases in 2010–11 and 2011–12.

A NO vote on thismeasure means: The

Legislature’s vote requirementto send an annual budget billto the Governor would remain

unchanged at two-thirds of eachouse of the Legislature.

A YES vote on thismeasure means: The

Legislature’s vote requirement tosend the annual budget bill tothe Governor would be lowered

from two-thirds to a majority of each house of the Legislature.

SUMMARY Put on the Ballot by Petition SignaturSUMMARY Put on the Ballot by Petition Signatures

CHANGES LEGISLATIVE VOTE REQUIREMENT TO PASSBUDGET AND BUDGET-RELATED LEGISLATION FROMTWO-THIRDS TO A SIMPLE MAJORITY. RETAINS TWO-THIRDS VOTE REQUIREMENT FOR TAXES. INITIATIVECONSTITUTIONAL AMENDMENT.

25

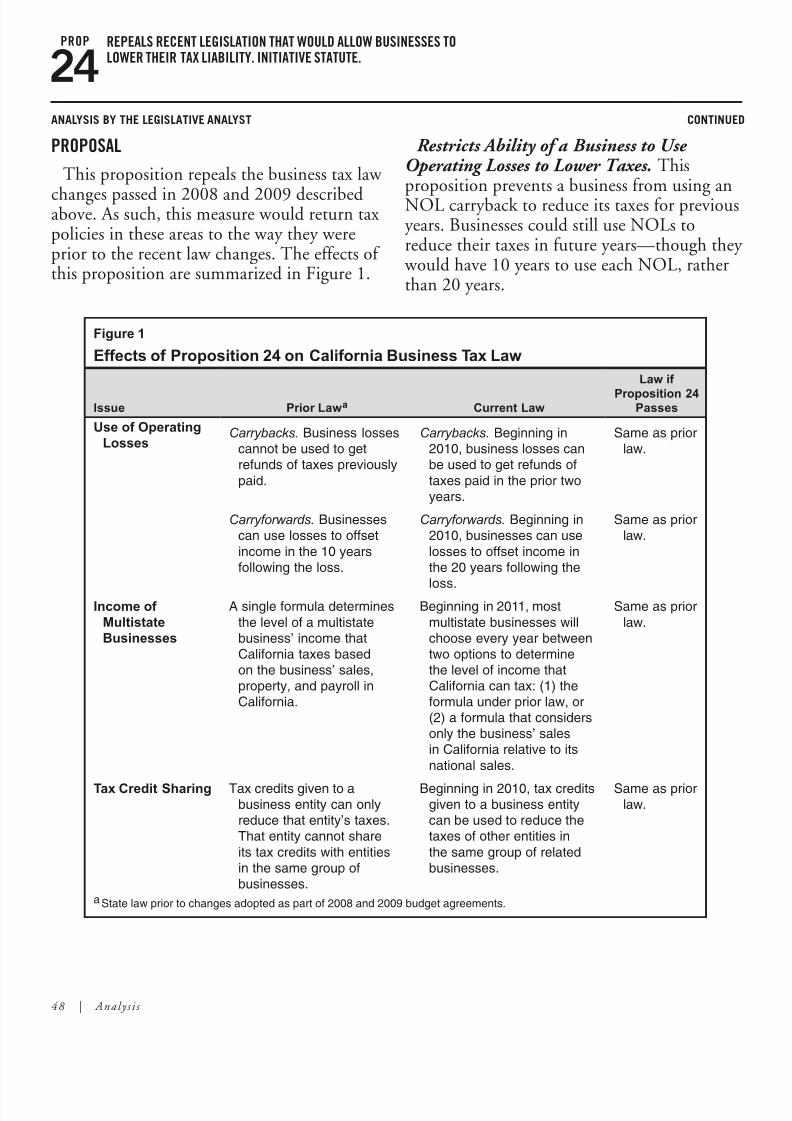

A NO vote on this measuremeans: Three business tax

provisions that were recently changed will not be affected. Asa result of maintaining current

law: (1) a business will be able todeduct losses in one year againstincome in more situations, (2)most multistate businesses couldchoose to have their Californiaincome determined based only on a single sales factor, and(3) a business will be able toshare its tax credits with relatedbusinesses.

A YES vote on thismeasure means: Three

business tax provisions willreturn to what they were before2008 and 2009 law changes. As

a result: (1) a business will beless able to deduct losses in oneyear against income in otheryears, (2) a multistate businesswill have its California incomedetermined by a calculationusing three factors, and (3) abusiness will not be able toshare tax credits with relatedbusinesses.

REPEALS RECENT LEGISLATION THAT WOULDALLOW BUSINESSES TO LOWER THEIR TAX LIABILITY.INITIATIVE STATUTE.

24

Quick-Re f e rence Guide |

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 8/128

QUICK-REFERENCE GUIDEPROP PROP

OR ADDITIONAL INFORMATION FOR ADDITIONAL INFORMATION

ORtop Hidden Taxes—No on25/Yes on 26, a coalition of taxpayers, small businesses,environmental experts, goodgovernment groups, minorities,farmers, and vineyards.

866) [email protected]

www.no25yes26.com

AGAINST Yes on 20, No on 27—Hold

Politicians Accountable, acoalition of taxpayers, seniors,good government groups,small business and communityorganizations.

925 University Ave.Sacramento, CA 95825(866) [email protected]

www.noprop27.org

AGAINSTDoug Linney Taxpayers Against Protecting

Polluters1814 Franklin Street, Suite 510Oakland, CA 94612(510) 444-4710stopprotectingpolluters@

gmail.com www.stoppolluterprotection.com

FOR Yes on 2710940 Wilshire Boulevard,

Suite 2000Los Angeles, CA 90024(310) 576-1233 www.yesprop27.org

Politicians behind 27 want to repeal the voter-

approved Citizens RedistrictingCommission. They want thepower to draw safe districts forthemselves and will spend or sayanything to get it back. Don’tbuy it. TAXPAYER GROUPS,GOOD GOVERNMENTGROUPS, SENIORS SAY STOP THE POWER GRAB:NO on 27.

VOTE YES ON27 TO SAVE

TAXPAYER DOLLARS AND END NONSENSEREAPPORTIONMENTGAMES. California is in crisis. We are broke, deeply in debt,unemployment is far too high.Proposition 27 is the only chance for voters to say “Enoughis enough! Stop wasting taxpayerdollars on nonsense.” Yes on 27.

Big oil, tobacco, andalcohol corporations want

you to pay for the damages they cause. Prop. 26 was writtenbehind closed doors and withoutpublic input. Don’t protectpolluters. League of WomenVoters of California, Firefghters,Police Of fcers, Nurses, andSierra Club all say NO on 26.

Yes on 26 stops state andlocal politicians from

aising Hidden Taxes on goodske food and gas, by disguisingaxes as “fees” and circumventingonstitutional requirements for

passing higher taxes. Don’t bemisled. 26 preserves California’strong environmental andonsumer laws AND protectsaxpayers and consumers from

Hidden Taxes.

RGUMENTS ARGUMENTS

WHAT YOUR VOTE MEANSWHAT YOUR VOTE MEANS

A NO vote on this measuremeans: The responsibility

to determine the boundariesof Legislature and Board of Equalization districts would

remain with the CitizensRedistricting Commission.

A YES vote on thismeasure means: The

responsibility to determine theboundaries of State Legislatureand Board of Equalization

districts would be returned tothe Legislature. The CitizensRedistricting Commission,established by Proposition 11 in2008 to perform this function,

would be eliminated. (Proposition20 on this ballot also concernsredistricting issues. If bothProposition 27 and Proposition20 are approved by voters, theproposition receiving the greaternumber of “yes” votes would bethe only one to go into effect.)

ELIMINATES STATE COMMISSION ON REDISTRICTING.CONSOLIDATES AUTHORITY FOR REDISTRICTINGWITH ELECTED REPRESENTATIVES. INITIATIVECONSTITUTIONAL AMENDMENT AND STATUTE.

27

A NO vote on thismeasure means: Current

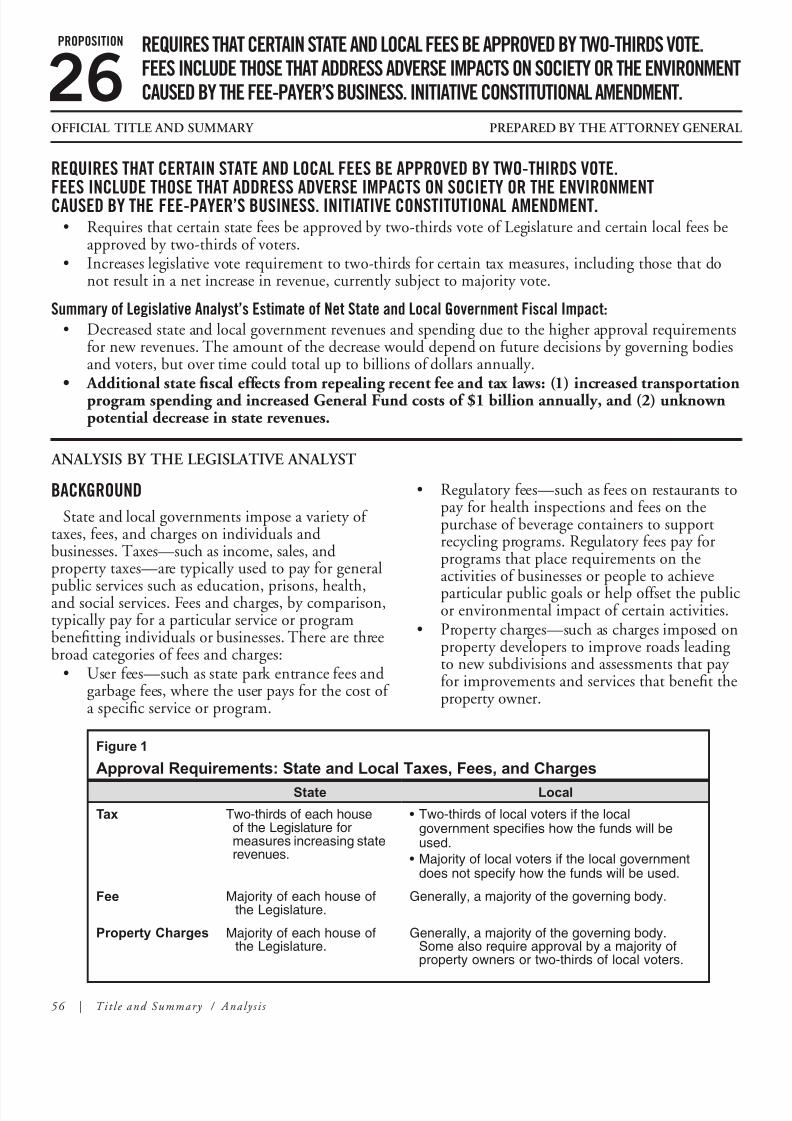

constitutional requirementsregarding fees and taxes wouldnot be changed.

A YES vote on thismeasure means: The

defnition of taxes would beroadened to include many

payments currently considered

o be fees or charges. As a result,more state and local proposals toncrease revenues would requirepproval by two-thirds of each

house of the Legislature or by ocal voters.

REQUIRES THAT CERTAIN STATE AND LOCAL FEES BEAPPROVED BY TWO-THIRDS VOTE. FEES INCLUDE THOSETHAT ADDRESS ADVERSE IMPACTS ON SOCIETY OR THEENVIRONMENT CAUSED BY THE FEE-PAYER’S BUSINESS.INITIATIVE CONSTITUTIONAL AMENDMENT.

26

Eliminates 14-member redistricting commission. Consolidates

authority for establishing state Assembly, Senate, and Boardof Equalization districts with elected representatives who draw congressional districts. Fiscal Impact: Possible reduction of state redistricting costs of around $1 million over the next year.Likely reduction of these costs of a few million dollars onceevery ten years beginning in 2020.

Fiscal Impact: Depending on decisions by governing bodies

nd voters, decreased state and local government revenuesnd spending (up to billions of dollars annually). Increasedransportation spending and state General Fund costs$1 billion annually).

SUMMARY Put on the Ballot by Petition SignatureUMMARY Put on the Ballot by Petition Signatures

| Quick-Re f e rence Guide

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 9/128

| 9

The Secretary o State’s Ofce does not write ballot arguments. Arguments in avor o and against ballot measures are provided by the proponents and opponents o the ballotmeasures.

I multiple arguments are submitted or or against a measure, the law requires that frstpriority be given to arguments written by legislators in the case o legislative measures,and arguments written by the proponents o an initiative or reerendum in the case o aninitiative or reerendum measure.

Subsequent priority or all measures goes to bona fde associations o citizens and then toindividual voters. The submitted argument language cannot be verifed or accuracy orchanged in any way unless a court orders it to be changed.

About Ballot Arguments

This Voter Inormation Guide is current as o the August date o printing. I any additionalstatewide measures qualiy or the ballot, a supplemental Voter Inormation Guide will beprepared and mailed to you.

I you or someone you know does not receive a guide, you may view the inormation atwww.voterguide.sos.ca.gov or request an additional copy by calling the Secretary o State’stoll-ree Voter Hotline at (800) 345-VOTE (8683). Copies are also available at your locallibrary and county elections ofce. Copies o the state Voter Inormation Guide and yourcounty sample ballot booklet also will be available at your polling place on Election Day.

Supplemental Voter Information

Oten reerred to as “direct democracy,” the initiative process is the power o the peopleto place measures on a statewide ballot. These measures can either create or change lawsand amend the constitution. I the initiative proposes to create or change Caliornia laws,proponents must gather petition signatures o registered voters equal in number to fvepercent o the votes cast or all candidates or Governor in the most recent gubernatorial

election. I the initiative proposes to amend the Caliornia Constitution, proponents mustgather petition signatures o registered voters equal in number to eight percent o the votescast or all candidates or Governor in the most recent gubernatorial election. To be enacted,an initiative requires a simple majority o the total votes cast.

About Initiatives

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 10/128

10 |

On August 10, 2010, the State Legislature and Governor removed Proposition 18 from the ballot.

PROPOSITION

18

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 11/128

| 11

On August 10, 2010, the State Legislature and Governor removed Proposition 18 from the ballot.

PROP

18

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 12/128

12 | Ti t l e and Summary / Analy s i s

PROPOSITION

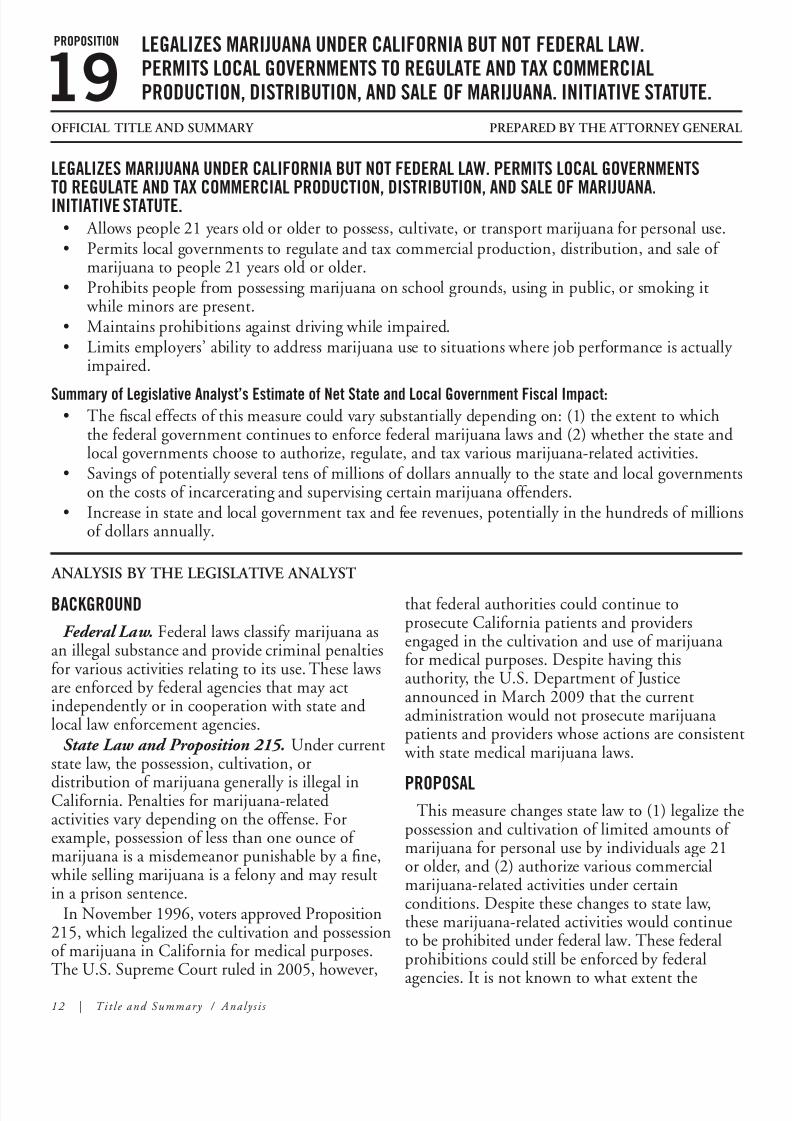

OFFICIAL TITLE AND SUMMARY PREPARED BY THE ATTORNEY GENERAL

LEGALIZES MARIJUANA UNDER CALIFORNIA BUT NOT FEDERAL LAW. PERMITS LOCAL GOVERNMENTS

TO REGULATE AND TAX COMMERCIAL PRODUCTION, DISTRIBUTION, AND SALE OF MARIJUANA.INITIATIVE STATUTE.

• Allowspeople21yearsoldoroldertopossess,cultivate,ortransportmarijuanaforpersonaluse.• Permitslocalgovernmentstoregulateandtaxcommercialproduction,distribution,andsaleofmarijuanatopeople21yearsoldorolder.

• Prohibitspeoplefrompossessingmarijuanaonschoolgrounds,usinginpublic,orsmokingit whileminorsarepresent.

• Maintainsprohibitionsagainstdrivingwhileimpaired.• Limitsemployers’abilitytoaddressmarijuanausetosituationswherejobperformanceisactuallyimpaired.

Summary of Legislative Analyst’s Estimate of Net State and Local Government Fiscal Impact:• Thescaleffectsofthismeasurecouldvarysubstantiallydependingon:(1)theextenttowhichthefederalgovernmentcontinuestoenforcefederalmarijuanalawsand(2)whetherthestateandlocalgovernmentschoosetoauthorize,regulate,andtaxvariousmarijuana-relatedactivities.

• Savingsofpotentiallyseveraltensofmillionsofdollarsannuallytothestateandlocalgovernmentsonthecostsofincarceratingandsupervisingcertainmarijuanaoffenders.

• Increaseinstateandlocalgovernmenttaxandfeerevenues,potentiallyinthehundredsofmillionsofdollarsannually.

LEGALIZES MARIJUANA UNDER CALIFORNIA BUT NOT FEDERAL LAW.PERMITS LOCAL GOVERNMENTS TO REGULATE AND TAX COMMERCIALPRODUCTION, DISTRIBUTION, AND SALE OF MARIJUANA. INITIATIVE STATUTE.19

thatfederalauthoritiescouldcontinuetoprosecuteCaliforniapatientsandprovidersengagedinthecultivationanduseofmarijuanaformedicalpurposes.Despitehavingthisauthority,theU.S.DepartmentofJusticeannouncedinMarch2009thatthecurrentadministrationwouldnotprosecutemarijuanapatientsandproviderswhoseactionsareconsistent withstatemedicalmarijuanalaws.

PROPOSALThismeasurechangesstatelawto(1)legalizethepossessionandcultivationoflimitedamountsofmarijuanaforpersonalusebyindividualsage21orolder,and(2)authorizevariouscommercialmarijuana-relatedactivitiesundercertainconditions.Despitethesechangestostatelaw,thesemarijuana-relatedactivitieswouldcontinuetobeprohibitedunderfederallaw.Thesefederalprohibitionscouldstillbeenforcedbyfederal

agencies.Itisnotknowntowhatextentthe

BACKGROUND

Federal Law. Federallawsclassifymarijuanaasanillegalsubstanceandprovidecriminalpenaltiesforvariousactivitiesrelatingtoitsuse.Theselawsareenforcedbyfederalagenciesthatmayactindependentlyorincooperationwithstateandlocallawenforcementagencies.

State Law and Proposition 215. Undercurrentstatelaw,thepossession,cultivation,or

distributionofmarijuanagenerallyisillegalinCalifornia.Penaltiesformarijuana-relatedactivitiesvarydependingontheoffense.Forexample,possessionoflessthanoneounceofmarijuanaisamisdemeanorpunishablebyane, whilesellingmarijuanaisafelonyandmayresultinaprisonsentence.InNovember1996,votersapprovedProposition215,whichlegalizedthecultivationandpossessionofmarijuanainCaliforniaformedicalpurposes.TheU.S.SupremeCourtruledin2005,however,

ANALYSIS BY THE LEGISLATIVE ANALYST

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 13/128

For text of Proposition 19, see page 92. Analy s i s | 13

federalgovernmentwouldcontinuetoenforcethem.Currently,nootherstatepermitscommercialmarijuana-relatedactivitiesfornon-medicalpurposes.

State Legalization of Marijuana Possession andCultivation for Personal Use

Underthemeasure,personsage21oroldergenerallymay(1)possess,process,shareortransportuptooneounceofmarijuana;(2)cultivatemarijuanaonprivatepropertyinanareaupto25squarefeetperprivateresidenceorparcel;(3)possessharvestedandlivingmarijuanaplantscultivatedinsuchanarea;and(4)possessanyitemsorequipmentassociatedwiththeaboveactivities.Thepossessionandcultivationofmarijuanamustbesolelyforanindividual’spersonalconsumptionandnotforsaletoothers,andconsumptionofmarijuanawouldonlybepermittedinaresidenceorother“non-publicplace.”(Oneexceptionisthatmarijuanacouldbesoldandconsumedinlicensedestablishments,asdiscussedbelow.)Thestateandlocalgovernmentscouldalsoauthorizethepossessionandcultivation

oflargeramountsofmarijuana.Stateandlocallawenforcementagenciescouldnotseizeordestroymarijuanafrompersonsincompliancewiththemeasure.Inaddition,themeasurestatesthatnoindividualcouldbepunished,ned,ordiscriminatedagainstforengaginginanyconductpermittedbythemeasure.However,itdoesspecifythatemployers wouldretainexistingrightstoaddressconsumptionofmarijuanathatimpairsanemployee’sjobperformance.Thismeasuresetsforthsomelimitsonmarijuanapossessionandcultivationforpersonaluse.Forexample,thesmokingofmarijuanainthepresenceofminorsisnotpermitted.Inaddition,themeasurewouldnotchangeexistinglawsthatprohibitdrivingundertheinuenceofdrugsorthatprohibitpossessingmarijuanaonthegroundsofelementary,middle,andhighschools.Moreover,apersonage21orolderwhoknowinglygavemarijuanatoapersonage18through20

couldbesenttocountyjailforuptosixmonths

andnedupto$1,000peroffense.(Themeasuredoesnotchangeexistingcriminallawswhichimposepenaltiesforadultswhofurnishmarijuanatominorsundertheageof18.)

Authorization of Commercial Marijuana Activities

Themeasureallowslocalgovernmentstoauthorize,regulate,andtaxvariouscommercialmarijuana-relatedactivities.Asdiscussedbelow,thestatealsocouldauthorize,regulate,andtaxsuchactivities.

Regulation.Themeasureallowslocalgovernmentstoadoptordinancesandregulations

regardingcommercialmarijuana-relatedactivities—includingmarijuanacultivation,processing,distribution,transportation,andretailsales.Forexample,localgovernmentscouldlicenseestablishmentsthatcouldsellmarijuanatopersons21andolder.Localgovernmentscouldregulatethelocation,size,hoursofoperation,andsignsanddisplaysofsuchestablishments.Individualscouldtransportmarijuanafromalicensedmarijuanaestablishmentinonelocalitytoalicensedestablishmentinanotherlocality,

regardlessofwhetheranylocalitiesinbetweenpermittedthecommercialproductionandsaleofmarijuana.However,themeasuredoesnotpermitthetransportationofmarijuanabetweenCaliforniaandanotherstateorcountry.Anindividualwhowaslicensedtosellmarijuanatoothersinacommercialestablishmentandwhonegligentlyprovidedmarijuanatoapersonunder21wouldbebannedfromowning,operating,beingemployedby,assisting,orenteringalicensedmarijuanaestablishmentforoneyear.Localgovernmentscouldalsoimposeadditionalpenaltiesorcivilnesoncertainmarijuana-relatedactivities,suchasforviolationofalocalordinancelimitingthehoursofoperationofalicensedmarijuanaestablishment. Whetherornotlocalgovernmentsengagedinthisregulation,thestatecould,onastatewidebasis,regulatethecommercialproductionofmarijuana.Thestatecouldalsoauthorizetheproductionofhemp,atypeofmarijuanaplant

LEGALIZES MARIJUANA UNDER CALIFORNIA BUT NOT FEDERAL LAW.PERMITS LOCAL GOVERNMENTS TO REGULATE AND TAX COMMERCIALPRODUCTION, DISTRIBUTION, AND SALE OF MARIJUANA. INITIATIVE STATUTE.

PROP

19

ANALYSIS BY THE LEGISLATIVE ANALYST CONTINUED

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 14/128

ANALYSIS BY THE LEGISLATIVE ANALYST CONTINUED

14 | Analy s i s

PROP

19

thatcanbeusedtomakeproductssuchasfabricandpaper.

Taxation. Themeasurerequiresthatlicensedmarijuanaestablishmentspayallapplicablefederal,state,andlocaltaxesandfeescurrentlyimposedonothersimilarbusinesses.Inaddition,themeasurepermitslocalgovernmentstoimposenewgeneral,excise,ortransfertaxes,aswellasbenetassessmentsandfees,onauthorizedmarijuana-relatedactivities.Thepurposeofsuchchargeswouldbetoraiserevenueforlocalgovernmentsand/ortooffsetanycostsassociated withmarijuanaregulation.Inaddition,thestate

couldimposesimilarcharges.FISCAL EFFECTS

Manyoftheprovisionsinthismeasurepermit,butdonotrequire,thestateandlocalgovernmentstotakecertainactionsrelatedtotheregulationandtaxationofmarijuana.Thus,itisuncertaintowhatextentthestateandlocalgovernmentswouldinfactundertakesuchactions.Forexample,itisunknownhowmanylocalgovernmentswouldchoosetolicenseestablishmentsthatwouldgroworsellmarijuanaorimposeanexcisetaxonsuchsales.Inaddition,althoughthefederalgovernmentannouncedinMarch2009thatitwouldnolongerprosecutemedicalmarijuanapatientsandproviderswhoseactionsareconsistentwithProposition215,ithascontinuedtoenforceitsprohibitionsonnon-medicalmarijuana-relatedactivities.Thismeansthatthefederalgovernmentcouldprosecuteindividualsforactivitiesthat

wouldbepermittedunderthismeasure.Totheextentthatthefederalgovernmentcontinuedtoenforceitsprohibitionsonmarijuana,itwouldhavetheeffectofimpedingtheactivitiespermittedbythismeasureunderstatelaw.Thus,therevenueandexpenditureimpactsofthismeasurearesubjecttosignicantuncertainty.

Impacts on State and Local Expenditures

Reduction in State and Local Correctional Costs. Themeasurecouldresultinsavingstothe

stateandlocalgovernmentsbyreducingthenumberofmarijuanaoffendersincarceratedinstateprisonsandcountyjails,aswellasthenumberplacedundercountyprobationorstateparolesupervision.Thesesavingscouldreachseveraltensofmillionsofdollarsannually.Thecountyjailsavingswouldbeoffsettotheextentthatjailbedsnolongerneededformarijuanaoffenderswereusedforothercriminalswhoarenowbeingreleasedearlybecauseofalackofjailspace.

Reduction in Court and Law Enforcement Costs.Themeasurewouldresultinareductionin

stateandlocalcostsforenforcementofmarijuana-relatedoffensesandthehandlingofrelatedcriminalcasesinthecourtsystem.However,itislikelythatthestateandlocalgovernmentswouldredirecttheirresourcestootherlawenforcementandcourtactivities.

Other Fiscal Effects on State and Local Programs.Themeasurecouldalsohavescaleffectsonvariousotherstateandlocalprograms.Forexample,themeasurecouldresultinanincreaseintheconsumptionofmarijuana,potentiallyresultinginanunknownincreaseinthenumberofindividualsseekingpubliclyfundedsubstanceabusetreatmentandothermedicalservices.Thismeasurecouldalsohavescaleffectsonstate-andlocallyfundeddrugtreatmentprogramsforcriminaloffenders,suchasdrugcourts.Moreover,themeasurecouldpotentiallyreduceboththecostsandoffsettingrevenuesofthestate’sMedicalMarijuanaProgram,apatientregistrythatidentiesthoseindividualseligible

understatelawtolegallypurchaseandconsumemarijuanaformedicalpurposes.

Impacts on State and Local Revenues

Thestateandlocalgovernmentscouldreceiveadditionalrevenuesfromtaxes,assessments,andfeesfrommarijuana-relatedactivitiesallowedunderthismeasure.IfthecommercialproductionandsaleofmarijuanaoccurredinCalifornia,thestateandlocalgovernmentscouldreceiverevenuesfromavarietyofsourcesinthewaysdescribed

below.

LEGALIZES MARIJUANA UNDER CALIFORNIA BUT NOT FEDERAL LAW.PERMITS LOCAL GOVERNMENTS TO REGULATE AND TAX COMMERCIALPRODUCTION, DISTRIBUTION, AND SALE OF MARIJUANA. INITIATIVE STATUTE.

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 15/128

ANALYSIS BY THE LEGISLATIVE ANALYST CONTINUED

For text of Proposition 19, see page 92. Analy s i s | 15

PROP

19

• Existing Taxes. Businessesproducingandsellingmarijuanawouldbesubjecttothesametaxesasotherbusinesses.Forinstance,

thestateandlocalgovernmentswouldreceivesalestaxrevenuesfromthesaleofmarijuana.Similarly,marijuana-relatedbusinesseswithnetincomewouldpayincometaxestothestate.Totheextentthatthisbusinessactivitypulledinspendingfrompersonsinotherstates,themeasurewouldresultinanetincreaseintaxableeconomicactivityinthestate.

• New Taxes and Fees on Marijuana. As

describedabove,localgovernmentsareallowedtoimposetaxes,fees,andassessmentsonmarijuana-relatedactivities.Similarly,thestatecouldimposetaxesandfeesonthesetypesofactivities.(Aportionofanynewrevenuesfromthesesourceswould

beoffsetbyincreasedregulatoryandenforcementcostsrelatedtothelicensingandtaxationofmarijuana-relatedactivities.)

Asdescribedearlier,boththeenforcementdecisionsofthefederalgovernmentandwhetherthestateandlocalgovernmentschoosetoregulateandtaxmarijuanawouldaffecttheimpactofthismeasure.Itisalsounclearhowthelegalizationofsomemarijuana-relatedactivitieswouldaffectitsoveralllevelofusageandprice,whichinturncouldaffectthelevelofstateorlocalrevenuesfromtheseactivities.Consequently,themagnitudeofadditionalrevenuesisdifculttoestimate.To

theextentthatacommercialmarijuanaindustrydevelopedinthestate,however,weestimatethatthestateandlocalgovernmentscouldeventuallycollecthundredsofmillionsofdollarsannuallyinadditionalrevenues.

LEGALIZES MARIJUANA UNDER CALIFORNIA BUT NOT FEDERAL LAW.PERMITS LOCAL GOVERNMENTS TO REGULATE AND TAX COMMERCIALPRODUCTION, DISTRIBUTION, AND SALE OF MARIJUANA. INITIATIVE STATUTE.

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 16/128

16 | Arguments Arguments printed on this page are the opinions of the authors and have not been checked for accur acy by any ofcial agency .

LEGALIZES MARIJUANA UNDER CALIFORNIA BUT NOT FEDERAL LAW.PERMITS LOCAL GOVERNMENTS TO REGULATE AND TAX COMMERCIALPRODUCTION, DISTRIBUTION, AND SALE OF MARIJUANA. INITIATIVE STATUTE.

PROP

19ARGUMENT IN FAVOR OF PROPOSITION 19

REBUTTAL TO ARGUMENT IN FAVOR OF PROPOSITION 19

As California public safety leaders, we agree that Proposition19 is aw ed public policy and would compromise the safety of our roadways, workplaces, and communities. Before voting onthis proposition, please take a few minutes to read it.

Proponents claim, “Proposition 19 maintains strict criminalpenalties or driving under the inuence.” That statement isfalse. In fact, Proposition 19 gives drivers the “right” to usemarijuana right up to the point when they climb behind the

wheel, but unlike as with drunk driving, Proposition 19 fails toprovide the Highway Patrol with any tests or objective standardsfor determining what constitutes “driving under the inuence.’’That’s why Mothers Against Drunk Driving (MADD) strongly opposes Proposition 19.

Proponents claim Proposition 19 is “preserving the right of employers to maintain a drug-free workplace.” This is also false.

According to the California Chamber of Commerce, the factsare that Proposition 19 creates special rights for employees topossess marijuana on the job, and that means no company in

California can meet federal drug-free workplace standards, orqualify for federal contracts. The California State Firefghters

Association warns this one drafting mistake alone could costthousands of Californians to lose their jobs.

Again, contrary to what proponents say, the statewideorganizations representing police, sheriffs and drug court judgesare all urging you to vote “No” on Proposition 19. Passageof Proposition 19 seriously compromises the safety of ourcommunities, roadways, and workplaces.

STEVE COOLEY, District Attorney Los Angeles County KAMALA HARRIS, District Attorney San Francisco County KEVIN NIDA, PresidentCalifornia State Firefghters Association

PROPOSITION 19: COMMON SENSE CONTROL OFMARIJUANA

Today, hundreds of millions of taxpayer dollars are spentenforcing the failed prohibition of marijuana (also known as“cannabis”).

Currently, marijuana is easier for kids to get than alcohol,because dealers don’t require ID.

Prohibition has created a violent criminal market run by international drug cartels.

Police waste millions of taxpayer dollars targeting non-violentmarijuana consumers, while thousands of violent crimes gounsolved.

And there is $14 billion in marijuana sales every year inCalifornia, but our debt-ridden state gets nothing from it.

Marijuana prohibition has failed. WE NEED A COMMON SENSE APPROACH TO

CONTROL AND TAX MARIJUANA LIKE ALCOHOL.Proposition 19 was carefully written to get marijuana under

control.Under Proposition 19, only adults 21 and over can possess up

to one ounce of marijuana, to be consumed at home or licensedestablishments. Medical marijuana patients’ rights are preserved.

If we can control and tax alcohol, we can control and taxmarijuana.

PUT STRICT SAFETY CONTROLS ON MARIJUANA Proposition 19 maintains strict criminal penalties for driving

under the inuence, increases penalties for providing marijuanato minors, and bans smoking it in public, on school grounds,and around minors.

Proposition 19 keeps workplaces safe, by preserving the rightof employers to maintain a drug-free workplace.

PUT POLICE PRIORITIES WHERE THEY BELONG

According to the FBI, in 2008 over 61,000 Californians werearrested for misdemeanor marijuana possession, while 60,000violent crimes went unsolved. By ending arrests of non-violentmarijuana consumers, police will save hundreds of millions of taxpayer dollars a year, and be able to focus on the real threat:violent crime.

Police, Sheriffs, and Judges support Proposition 19.HELP FIGHT THE DRUG CARTELSMarijuana prohibition has created vicious drug cartels across

our border. In 2008 alone, cartels murdered 6,290 civiliansin Mexico—more than all U.S. troops killed in Iraq and

Afghanistan combined.60 percent of drug cartel revenue comes from the illegal U.S.

marijuana market.By controlling marijuana, Proposition 19 will help cut off

funding to the cartels.GENERATE BILLIONS IN REVENUE TO FUND WHAT

MATTERSCaliornia aces historic defcits, which, i state government

doesn’t balance the budget, could lead to higher taxes and feesfor the public, and more cuts to vital services. Meanwhile, thereis $14 billion in marijuana transactions every year in California,but we see none of the revenue that would come from taxing it.

Proposition 19 enables state and local governments to taxmarijuana, so we can preserve vital services.

The State’s tax collector, the Board of Equalization, saystaxing marijuana would generate $1.4 billion in annual revenue,

which could fund jobs, healthcare, public safety, parks, roads,transportation, and more.

LET’S REFORM CALIFORNIA’S MARIJUANA LAWSOutlawing marijuana hasn’t stopped 100 million Americans

from trying it. But we can control it, make it harder for kids toget, weaken the cartels, focus police resources on violent crime,and generate billions in revenue and savings.

We need a common sense approach to control marijuana. YES on 19.www.taxcannabis.org

JOSEPH D. McNAMARA, San Jose Police Chief (Ret.)JAMES P. GRAY, Orange County Superior Court Judge (Ret.)STEPHEN DOWNING, Deputy Chief (Ret.)Los Angeles Police Department

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 17/128

Arguments printed on this page are the opinions of the authors and have not been checked for accur acy by any ofcial agency . Arguments | 17

ARGUMENT AGAINST PROPOSITION 19

REBUTTAL TO ARGUMENT AGAINST PROPOSITION 19

LEGALIZES MARIJUANA UNDER CALIFORNIA BUT NOT FEDERAL LAW.PERMITS LOCAL GOVERNMENTS TO REGULATE AND TAX COMMERCIALPRODUCTION, DISTRIBUTION, AND SALE OF MARIJUANA. INITIATIVE STATUTE.

PROP

19

Even if you support legalization of recreational marijuana, youshould vote “No” on Proposition 19.

Why? Because the authors made several huge mistakes in writing this initiative which will have severe, unintendedconsequences.

For example, Mothers Against Drunk Driving (MADD)strongly opposes Proposition 19 because it will prevent bus andtrucking companies from requiring their drivers to be drug-free.Companies won’t be able to take action against a “stoned” driveruntil after he or she has a wreck, not before.

School districts may currently require school bus drivers tobe drug-free, but if Proposition 19 passes, their hands will betied—until after tragedy strikes. A school bus driver would beforbidden to smoke marijuana on schools grounds or whileactually behind the wheel, but could arrive for work withmarijuana in his or her system.

Public school superintendent John Snavely, Ed.D. warns thatProposition 19 could cost our K–12 schools as much as $9.4billion in lost federal funding. Another error could potentially cost schools hundreds of millions of dollars in federal grantsfor our colleges and universities. Our schools have already experienced severe budget cuts due to the state budget crisis.

The California Chamber of Commerce found that “if passed,this initiative could result in employers losing public contractsand grants because they could no longer effectively enforcethe drug-free workplace requirements outlined by the federalgovernment.”

Employers who permit employees to sell cosmetics or schoolcandy bars to co-workers in the ofce, may no w also be requiredto allow any employee with a “license” to sell marijuana in theofce.

Under current law, if a worker shows up smelling of alcoholor marijuana, an employer may remove the employee from adangerous or sensitive job, such as running medical lab tests ina hospital, or operating heavy equipment. But if Proposition 19passes, the worker with marijuana in his or her system may notbe removed from the job until after an accident occurs.

The California Police Chiefs Association opposes Proposition19 because proponents “forgot” to include a standard for whatconstitutes “driving under the inuence.” Under Proposition 19,a driver may legally drive even if a blood test shows they havemarijuana in their system.

Gubernatorial candidates Republican Meg Whitman andDemocrat Jerry Brown have both studied Proposition 19 andare urging all Californians to vote “No,” as are Democratic andRepublican candidates for Attorney General, Kamala Harris andSteve Cooley.

Don’t be fooled. The proponents are hoping you willthink Proposition 19 is about “medical” marijuana. It is not.Proposition 19 makes no changes either way in the medicalmarijuana laws.

Proposition 19 is simply a jumbled legal nightmare that willmake our highways, our workplaces and our communities lesssafe. We strongly urge you to vote “No” on Prop. 19.

DIANNE FEINSTEIN, United States SenatorLAURA DEAN-MOONEY, National PresidentMothers Against Drunk Driving

THE CHOICE IS CLEAR: REAL CONTROL OFMARIJUANA, OR MORE OF THE SAME

Let’s be honest. Our marijuana laws have failed. Rather thanaccepting things as they are, we can control marijuana.

Like the prohibition of alcohol in the past, outlawingmarijuana hasn’t worked. It’s created a criminal market run by violent drug cartels, wasted police resources, and drained ourstate and local budgets. Proposition 19 is a more honest policy,and a common sense solution to these problems. Proposition19 will control marijuana like alcohol, making it available only to adults, enforce strong driving and workplace safety laws, putpolice priorities where they belong, and generate billions inneeded revenue.

THE CHOICE IS CLEAR: REAL CONTROL OFMARIJUANA, OR MORE OF THE SAME

We can make it harder for kids to get marijuana, or we canaccept the status quo, where marijuana is easier for kids to getthan alcohol.

We can let police prevent violent crime, or we can accept

the status quo, and keep wasting resources sending tensof thousands of non-violent marijuana consumers—adisproportionate number who are minorities—to jail.

We can control marijuana to weaken the drug cartels, or we

can accept the status quo, and continue to fund violent gangs with illegal marijuana sales in California.

We can tax marijuana to generate billions for vital services, or we can accept the status quo, and turn our backs on this neededrevenue.

THE CHOICE IS CLEAR Vote Yes on 19.

JOYCELYN ELDERS, United States Surgeon General (Ret.)ALICE A. HUFFMAN, PresidentCalifornia NAACPDAVID DODDRIDGE, Narcotics Detective (Ret.)Los Angeles Police Department

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 18/128

18 | Ti t l e and Summary / Analy s i s

PROPOSITION

OFFICIAL TITLE AND SUMMARY PREPARED BY THE ATTORNEY GENERAL

REDISTRICTING OF CONGRESSIONAL DISTRICTS. INITIATIVE CONSTITUTIONAL AMENDMENT.

• Removeselectedrepresentativesfromtheprocessofestablishingcongressionaldistrictsandtransfersthatauthoritytotherecently-authorized14-memberredistrictingcommission.• RedistrictingcommissioniscomprisedofveDemocrats,veRepublicans,andfourvotersregisteredwithneitherparty.

• Requiresthatanynewly-proposeddistrictlinesbeapprovedbyninecommissionersincludingthreeDemocrats,threeRepublicans,andthreefromneitherparty.

Summary of Legislative Analyst’s Estimate of Net State and Local Government Fiscal Impact:

• Nosignicantnetchangeinstateredistrictingcosts.

REDISTRICTING OF CONGRESSIONAL DISTRICTS.INITIATIVE CONSTITUTIONAL AMENDMENT.

20

InNovember2008,voterspassedProposition11,whichcreatedtheCitizensRedistrictingCommissiontoestablishnewdistrictboundariesfortheStateAssembly,StateSenate,andBOEbeginningafterthe2010census.Tobeestablishedonceeverytenyears,thecommissionwillconsistof14registeredvoters—5Democrats,5Republicans,and4others—whoapplyforthepositionandarechosenaccordingtospeciedrules. Whenthecommissionsetsdistrictboundaries,itmustmeettherequirementsoffederallawandotherrequirements,suchasnotfavoringordiscriminatingagainstpoliticalparties,incumbents,orpoliticalcandidates.Inaddition,thecommissionisrequired,totheextentpossible,toadoptdistrictboundariesthat:• Maintainthegeographicintegrityofanycity,county,neighborhood,and“communityofinterest”inasingledistrict.(Thecommission

isresponsiblefordening“communitiesofinterest”foritsredistrictingactivities.)

• Developgeographicallycompactdistricts.• PlacetwoAssemblydistrictstogetherwithinoneSenatedistrictandplacetenSenatedistrictstogetherwithinoneBOEdistrict.

ThismeasuretakestheresponsibilitytodetermineboundariesforCalifornia’scongressionaldistrictsawayfromtheStateLegislature.Instead,thecommissionrecentlyestablishedbyvoterstodrawdistrictboundariesofstateofceswoulddeterminetheboundariesofcongressionaldistricts.

BACKGROUND

Inaprocessknownas“redistricting,”theStateConstitutionrequiresthatthestateadjusttheboundarylinesofdistrictsonceeverytenyearsfollowingthefederalcensusfortheState Assembly,StateSenate,StateBoardofEqualization(BOE),andCalifornia’scongressionaldistrictsfortheU.S.HouseofRepresentatives.Tocomplywithfederallaw,redistrictingmustestablishdistrictswhichareroughlyequalinpopulation.

Recent Changes to State Legislature and BOE

Redistricting.Inthepast,districtboundariesforalloftheofceslistedaboveweredeterminedinbillsthatbecamelawaftertheywereapprovedbytheLegislatureandsignedbytheGovernor.Onsomeoccasions,whentheLegislatureandtheGovernorwereunabletoagreeonredistrictingplans,theCaliforniaSupremeCourtperformedtheredistricting.

ANALYSIS BY THE LEGISLATIVE ANALYST

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 19/128

For text of Proposition 20, see page 95. Analy s i s | 19

Current Congressional Redistricting Process.Currently,Californiaisentitledto53ofthe435seatsintheU.S.HouseofRepresentatives.

Proposition11didnotchangetheredistrictingprocessforthese53congressionalseats.Currently,therefore,redistrictingplansforcongressionalseatsareincludedinbillsthatareapprovedbytheLegislature.Proposition11,however,didmakesomechangestotherequirementsthattheLegislaturemustmeetindrawingcongressionaldistricts.TheLegislature—likethecommission—nowmustattempttodrawgeographicallycompactdistricts

andmaintaingeographicintegrityoflocalities,neighborhoods,andcommunitiesofinterest,asdenedbytheLegislature.Proposition11,however,doesnotprohibittheLegislaturefromfavoringordiscriminatingagainstpoliticalparties,incumbents,orpoliticalcandidateswhendrawingcongressionaldistricts.

PROPOSAL

Proposed New Method for Congressional Redistricting.ThismeasureamendstheConstitutiontochangetheredistrictingprocessforCalifornia’sdistrictsintheU.S.HouseofRepresentatives.Specically,themeasureremovestheauthorityforcongressionalredistrictingfromtheLegislatureandinsteadgivesthisauthoritytotheCitizensRedistrictingCommission.The

commissionwoulddrawcongressionaldistrictsessentiallyasitdrawsotherdistrictlinesunderProposition11.Thecommission,forexample,couldnotdrawcongressionaldistrictsinordertofavorincumbents,politicalcandidates,orpoliticalparties.Thecommissionalsoistoconsiderthegeographicintegrityofcities,counties,neighborhoods,andcommunitiesofinterest.AsunderProposition11,compliancewithfederallaw wouldberequired.

“Community of Interest” D efned.InadditiontoaddingsimilarcriteriaforcongressionalredistrictingasthoseestablishedinProposition11,

themeasuredenesa“communityofinterest”forbothcongressionalredistrictingandredistrictingofStateAssembly,StateSenate,andBOEseats.Acommunityofinterestisdenedas“acontiguouspopulationwhichsharescommonsocialandeconomicintereststhatshouldbeincludedwithinasingledistrictforpurposesofitseffectiveandfairrepresentation.”

Two Redistricting-Related Measures on This Ballot.Inadditiontothismeasure,anothermeasureontheNovember2010ballot—Proposition27—concernsredistrictingissues.Keyprovisionsofthesetwopropositions,aswellascurrentlaw,aresummarizedinFigure1.Ifbothofthesemeasuresareapprovedbyvoters,thepropositionreceivingthegreaternumberof“yes”voteswouldbetheonlyonetogointoeffect.

REDISTRICTING OF CONGRESSIONAL DISTRICTS.INITIATIVE CONSTITUTIONAL AMENDMENT.

PROP

20

ANALYSIS BY THE LEGISLATIVE ANALYST CONTINUED

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 20/128

ANALYSIS BY THE LEGISLATIVE ANALYST CONTINUED

20 | Analysi s

FISCAL EFFECTS

Redistricting Costs Prior to Proposition 11and Under Current Law. TheLegislaturespentabout$3millionin2001fromitsownbudgetspecicallyforredistrictingactivities,suchasthepurchaseofspecializedredistrictingsoftwareandequipment.Inadditiontothesecosts,some

regularlegislativestaffmembers,facilities,andequipment(whichareusedtosupportotherday-to-dayactivitiesoftheLegislature)wereusedtemporarilyforredistrictingefforts.

In2009,undertheProposition11process,theLegislatureapproved$3millionfromthestate’sGeneralFundforredistrictingactivitiesrelatedtothe2010census.Inaddition,about$3millionhasbeenspentfromanotherstatefundtosupporttheapplicationandselectionprocessforcommissionmembers.Forfutureredistrictingefforts,

Proposition11requiresthecommissionprocesstobefundedatleastatthepriordecade’slevelgrownforination.TheLegislaturecurrentlyfundscongressionalredistrictingactivitieswithinitsbudget.

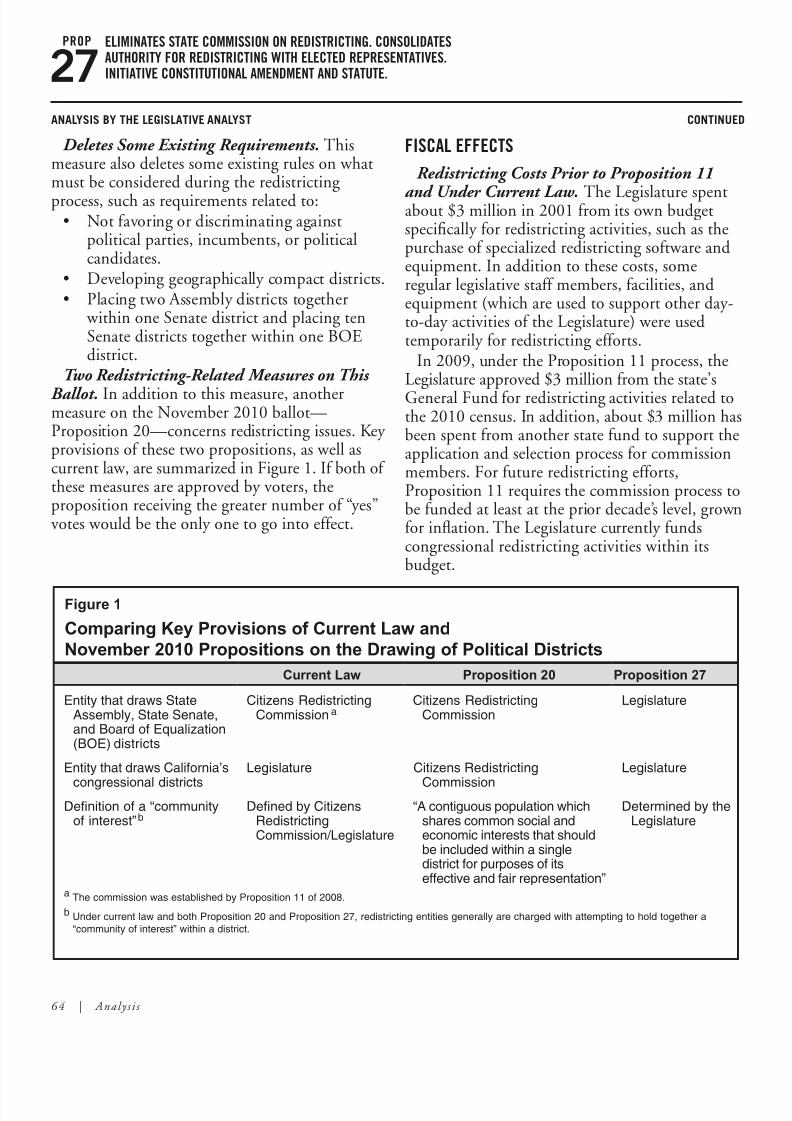

Figure 1

Comparing Key Provisions of Current Law and

November 2010 Propositions on the Drawing of Political Districts

Current Law Proposition 20 Proposition 27

Entity that draws StateAssembly, State Senate,and Board of Equalization(BOE) districts

Citizens RedistrictingCommission a

Citizens RedistrictingCommission

Legislature

Entity that draws California’scongressional districts

Legislature Citizens RedistrictingCommission

Legislature

Defnition of a “communityof interest” b

Defned by CitizensRedistrictingCommission/Legislature

“A contiguous population which

shares common social and

economic interests that should

be included within a single

district for purposes of its

effective and fair representation”

Determined by theLegislature

a The commission was established by Proposition 11 of 2008.

b Under current law and both Proposition 20 and Proposition 27, redistricting entities generally are charged with attempting to hold together a“community of interest” within a district.

REDISTRICTING OF CONGRESSIONAL DISTRICTS.INITIATIVE CONSTITUTIONAL AMENDMENT.

PROP

20

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 21/128

ANALYSIS BY THE LEGISLATIVE ANALYST CONTINUED

For text of Proposition 20, see page 95. Analy s i s | 21

Redistricting Costs Under This Proposal. ThismeasurewouldconsolidateallredistrictingactivityundertheCitizensRedistrictingCommission

processestablishedbyProposition11in2008.Thecommissionwouldexperienceincreasedcosts

fromhandlingcongressionalredistrictingactivities.Thesecosts,however,wouldbeoffsetbyareductionintheLegislature’sredistrictingcosts. Anynetchangeinfutureredistrictingcostsunderthismeasureprobablywouldnotbesignicant.

REDISTRICTING OF CONGRESSIONAL DISTRICTS.INITIATIVE CONSTITUTIONAL AMENDMENT.

PROP

20

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 22/128

REDISTRICTING OF CONGRESSIONAL DISTRICTS.INITIATIVE CONSTITUTIONAL AMENDMENT.

20PROP

22 | Arguments Arguments printed on this page are the opinions of the authors and have not been checked for accur acy by any ofcial agency .

ARGUMENT IN FAVOR OF PROPOSITION 20

REBUTTAL TO ARGUMENT IN FAVOR OF PROPOSITION 20

DON’T BE FOOLED—NO ON PROPOSITION 20—IT WASTES TAXPAYER DOLLARS

Perhaps Charles Munger, Junior, the sole bankroller o Prop. 20,has ooled well-meaning David Pacheco, Kathay Feng, and JohnKabateck. But don’t let him ool you.

Prop. 20 guarantees no level o airness, guarantees nocompetitive districts, guarantees nothing—except thatvoters cannot hold those who draw congressional districtlines accountable or what they do AND THAT YOU, THE TAXPAYER, WILL FOOT THE BILL FOR MUNGER’S SCHEME.

Accountability to the people is the undamental principle o our orm o government. But Prop. 20 gives a non-accountable14-person bureaucracy even more power over the people. And, o course, this bureaucracy will cost you money.

Proponents have stated (unknowingly) the most obvious reasonto vote No on 20: BELIEVE IT OR NOT, these people want toextend the travesty o the existing redistricting commission evenurther! Who, other than a handul o lobbyists, lawyers, and

politicians has been able to gure out the incredibly complicatedlabyrinth or choosing the commission?

And the bureaucrats who emerge rom this wasteul inscrutableprocess will have absolute power over our legislative districts.VOTERS WILL NEVER HAVE A CHANCE TO HOLD

THEM RESPONSIBLE FOR WHAT THEY DO.Our state is in crisis! Unemployment, crime, massive debt. It istime to stop nonsense political games o reapportionment.

Save taxpayer dollars, hold the power brokers accountable tothe people. Vote No on Proposition 20. Vote Yes on its rival,Proposition 27.

MARK MURRAY, Executive DirectorCaliornians Against Waste

HANK LACAYO, PresidentCongress o Caliornia Seniors

DANIEL H. LOWENSTEIN, Founding ChairmanCaliornia Fair Political Practices Commission

Proposition 20 will put an end to legislators drawing electiondistricts or their riends in Congress—districts that virtually guarantee Members o Congress get reelected even when they don’t listen to voters.

Proposition 20 will create air congressional districts that makeour congressional representatives more accountable to voters andmake it easier to vote them out o oce when they don’t do their jobs.

Proposition 20 simply extends the redistricting reorms voterspassed in 2008 (Prop. 11) so the voter-approved independentCitizens Redistricting Commission, instead o politicians, drawsCaliornia congressional districts in addition to drawing statelegislative districts.

The Commission is already being organized to draw airdistricts. Visit the ocial state site to see preparations or theCitizens Redistricting Commission’s redistricting in 2011(www.wedrawthelines.ca.gov ).

Proposition 20 will:•

Create air congressional districts.• Help make our congressional representatives more

accountable and responsive to voters.• Make it easier to vote Members o Congress out o oce i

they’re not doing their jobs. YES ON PROPOSITION 20: STOP THE BACKROOM

DEALSRight now, legislators and their paid consultants draw districts

behind closed doors to guarantee their riends in Congress arereelected. Sacramento politicians pick the voters or their riendsin Congress, rather than voters choosing who will represent them.

The Los Angeles Times and Orange County Register revealedthat in the last redistricting, 32 Members o Congress and otherpoliticians paid one political consultant over ONE MILLIONdollars to draw district boundaries to guarantee their reelection!

Proposition 20 puts an end to backroom deals by ensuringredistricting is completely open to the public and transparent.Proposition 20 means no secret meetings or payments are allowedand politicians can’t divide communities just to get the politicaloutcome they want.

YES ON PROPOSITION 20: HOLD POLITICIANS ACCOUNTABLE

When politicians are guaranteed reelection, they have littleincentive to work together to solve the serious problems we allace.

Proposition 20 will create air districts so politicians willactually have to work or our votes and respond to voter needs.

“When v oters can fnally hold politicians accountable, politicians will have to quit playing games and work to address the serious challenges Californians face.” —Ruben Guerra, Latin Business Association

The choice is simple:GOOD GOVERNMENT GROUPS ASK YOU TO VOTE

“YES” ON PROPOSITION 20 to orce politicians to competein air districts so we can hold them accountable.

POLITICIANS WANT YOU TO VOTE “NO” ONPROPOSITION 20 so they can stife voters’ voices so we can’thold them accountable.

It’s time we stand up to the politicians and special interests andextend voter-approved redistricting reorms to include Congress.Voters already created the Commission—it’s common sense

to have the Commission draw congressional as well as legislativedistricts.

“People from every walk of life support Proposition 20 to send amessage to politicians that it’s time to put voters in charge and get California back on track.” — Joni Low, Asian Business Association of San Diego

JOIN US IN VOTING YES ON PROPOSITION 20.YesProp20.org

DAVID PACHECO, Caliornia President AARP

KATHAY FENG, Executive DirectorCaliornia Common Cause

JOHN KABATECK, Executive DirectorNational Federation o Independent Business/Caliornia

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 23/128

20PROP

Arguments printed on this page are the opinions of the authors and have not been checked for accur acy by any ofcial agency . Arguments | 23

ARGUMENT AGAINST PROPOSITION 20

REBUTTAL TO ARGUMENT AGAINST PROPOSITION 20

REDISTRICTING OF CONGRESSIONAL DISTRICTS.INITIATIVE CONSTITUTIONAL AMENDMENT.

NO ON 20—it wastes taxpayer dollars and it turns back theclock on redistricting law. Proposition 20 is a disaster . . . itmust be deeated.

NO ON PROPOSITION 20—IT WASTES TAXPAYER DOLLARS:

20 is the brainchild o Charles Munger, Jr.—son o multi-billionaire Wall Street tycoon Charles Munger. MUNGER JUNIOR IS THE SOLE BANK-ROLLER OF 20. (Well,our other contributors have given all o $700.) But just or itsqualication, MUNGER GAVE $3.3 MILLION, a gure that will probably multiply many times by Election Day.

But i Proposition 20 passes, the taxpayers will start paying thebills instead o Munger Junior. Prop. 20 will cost us millions o dollars. Compare Prop. 20 with its rival, Prop. 27.

First, non-partisan experts have concluded that YES ONPROP. 27 saves taxpayer dollars:

“Summary o estimate by Legislative Analyst and Directoro Finance o scal impact on state and local government:

LIKELY DECREASE IN STATE REDISTRICTING COSTSTOTALING SEVERAL MILLION DOLLARS EVERY TEN YEARS.”

Second, Prop. 20 adds to the cascade o waste that Prop. 27 would avoid. Governor Schwarzenegger has already proposedgoing back to the well to double the redistricting budget, spendingMILLIONS MORE DOLLARS to draw lines or politicians while the state is acing a $19 billion decit.

AND NOW WITH PROP. 20, MUNGER JUNIOR WANTSTO MAKE THIS WASTEFUL BUREAUCRACY SPRAWLEVEN FURTHER AT THE EXTRA EXPENSE OF YOU, THETAXPAYER.

NO ON PROPOSITION 20—IT MANDATES JIM CROW ECONOMIC DISTRICTS:

Proposition 20 turns back the clock on redistricting law.Inexplicably, Proposition 20 mandates that all districts (including Assembly, Senate, and Congress) must be segregated by incomelevel. This pernicious Prop. 20 mandates that all districts besegregated according to “similar living standards” and thatdistricts include only people “with similar work opportunities.”

“Prop. 20 is insulting to all Caliornians. Jim Crow districts area thing o the past. 20 sets back the clock on redistricting law. Noon 20.”—Julian Bond, Chairman Emeritus, NAACP

Jim Crow districts are a throwback to an awul bygoneera. Districting by race, by class, by liestyle or by wealth isunacceptable. Munger Junior may not want to live in the samedistrict as his chaueur, but Caliornians understand these code words. The days o “country club members only’’ districts or o “poor people only” districts are over. NO ON PROP. 20—allCaliornians MUST be treated equally.

OUR DEMOCRATIC REPUBLIC IS NOT A TOY TO BEPLAYED WITH FOR THE SELF-AGGRANDIZEMENT OFTHE IDLE SECOND-GENERATION RICH.

NO ON 20, YES ON 27.

DANIEL H. LOWENSTEIN, Founding ChairmanCaliornia Fair Political Practices Commission

AUBRY L. STONE, PresidentCaliornia Black Chamber o Commerce

CARL POPE, ChairmanSierra Club

The argument against Proposition 20 is one o the most angry and over-the-top you’ll ever see in the Voter Guide.

THE POLITICIANS BEHIND IT SHOULD BE ASHAMED.

They’re desperate because voters can pass Proposition 20 and

stop Sacramento politicians rom drawing election districts toensure their riends in Congress are reelected, even when they don’t listen to voters.

That’s a threat to them. Politicians will say anything to protecttheir “sae” seats in Congress so they’re not accountable to voters.

DON’T BE MISLED BY THE POLITICIANS’ BOGUS“COST” ARGUMENT.

FACT: The non-partisan state Legislative Analyst ound Prop.20 will result in “probably no signicant change in redistrictingcosts.” Cal-Tax and other taxpayer groups support 20.

HERE’S WHY PASSING PROPOSITION 20 IS SOIMPORTANT:

FACT: In the last redistricting, Latino leaders sued ater aCaliornia Congressman had 170,000 Latinos carved out o hisdistrict just to ensure he’d get reelected. Now he’s leading thecharge against 20!

FACT: Politicians want to deeat 20 so they can keep drawingdistricts that divide communities, cities and counties and dilutevoters’ voices—just to get sae seats.

FACT: 20 will nally put an end to the politicians’ sel-serving,backroom deals.

FACT: With 20, the voter-approved Citizens RedistrictingCommission will draw air congressional districts in a completely transparent manner, giving voters power to hold politiciansaccountable.

The Caliornia Black Chamber o Commerce, Latin Business Association, Asian Pacic Islander American Public Aairs Association all say YES on 20!

Check it out or yoursel: www.YesProp20.org

ALICE HUFFMAN, PresidentCaliornia NAACP

JULIAN CANETE, Executive DirectorCaliornia Hispanic Chambers o Commerce

RICHARD RIDER, Chairman

San Diego Tax Fighters

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 24/128

24 | Title and Summary / Analysi s

ESTABLISHES $18 ANNUAL VEHICLE LICENSE SURCHARGE TO HELP FUND STATE PARKS AND

WILDLIFE PROGRAMS. GRANTS SURCHARGED VEHICLES FREE ADMISSION TO ALL STATE PARKS.INITIATIVE STATUTE.• Requiresdepositofsurchargerevenueinanewtrustfundandrequiresthattrustfundsbeused

solelytooperate,maintainandrepairstateparksandtoprotectwildlifeandnaturalresources.• Exemptscommercialvehicles,trailersandtrailercoachesfromthesurcharge.• RequiresannualauditbytheStateAuditorandreviewbyacitizensoversightcommittee.

Summary of Legislative Analyst’s Estimate of Net State and Local Government Fiscal Impact:

• Increasedstaterevenuesofabout$500millionannuallyfromanannualsurchargeonvehicleregistrations.

• Newrevenueswouldbeusedtooffsetabout$50millionlossofparkday-usefeerevenues,and

couldbeusedtoreplaceupto$200millionannuallyfromexistingstatefundscurrentlyspentonstateparksandwildlifeconservationprograms.

• Increasedfundingforstateparksandwildlifeconservationofatleast$250millionannually.

ESTABLISHES $18 ANNUAL VEHICLE LICENSE SURCHARGE TO HELP FUNDSTATE PARKS AND WILDLIFE PROGRAMS. GRANTS SURCHARGED VEHICLESFREE ADMISSION TO ALL STATE PARKS. INITIATIVE STATUTE.

usefees)andstategasolinetaxrevenues.Thedevelopmentofnewstateparksandcapitalimprovementstoexistingparksarelargelyfundedfrombondfundsthathavebeenapprovedinthe

pastbyvoters.Thereisasignicantbacklogofmaintenanceprojectsinstateparks,whichhavenodedicatedannualfundingsource.TheDPRalsoadministersgrantprogramsforlocalparks,fundedlargelythroughbondfunds. Wildlifeconservationprogramsinvariousotherstatedepartments,suchasDFG,arefundedthroughacombinationoftheGeneralFund,regulatoryfees,andbondfunds.Statefundingfor wildlifeconservationprogramoperationsisaround$100millionperyear.Bondfundsarethe

primaryfundingsourceforlandacquisitionsandothercapitalprojectsforwildlifeconservationpurposes. Annual Vehicle Registration Fees. Thestatecollectsanumberofchargesannuallywhenapersonregistersavehicle.TheDepartmentofMotorVehicles(DMV)collectstheserevenuesonbehalfofthestate.

BACKGROUND

The State Park System and State Wildlife Conservation Agencies. Californiahas278stateparks,ofwhich246areoperatedandmaintained

bytheCaliforniaDepartmentofParksandRecreation(DPR)and32bylocalentities.Otherstatedepartments,suchastheDepartmentofFishandGame(DFG)andvariousstateconservancies,ownandmaintainotherlandsforwildlifeconservationpurposes.TheStateWildlifeConservationBoardacquirespropertyandprovidesgrantsforpropertyacquisitiontostateandlocalentitiesforwildlifeconservationpurposes.TheOceanProtectionCouncilisastate

agencyresponsibleforcoordinatingstateactivitiestoprotectoceanresources.Funding for State Parks and Wildlife

Conservation. Overthelastveyears,statefundingfortheoperationofstateparkshasbeenaround$300millionannually.Ofthisamount,about$150millionhascomefromtheGeneralFund,withthebalancecominglargelyfromparkuserfees(suchasadmission,camping,andother

ANALYSIS BY THE LEGISLATIVE ANALYST

PROPOSITION

21OFFICIAL TITLE AND SUMMARY PREPARED BY THE ATTORNEY GENERAL

8/8/2019 Complete Vig

http://slidepdf.com/reader/full/complete-vig 25/128

21PROP

For text of Proposition 21, see page 97. Analy s i s | 25

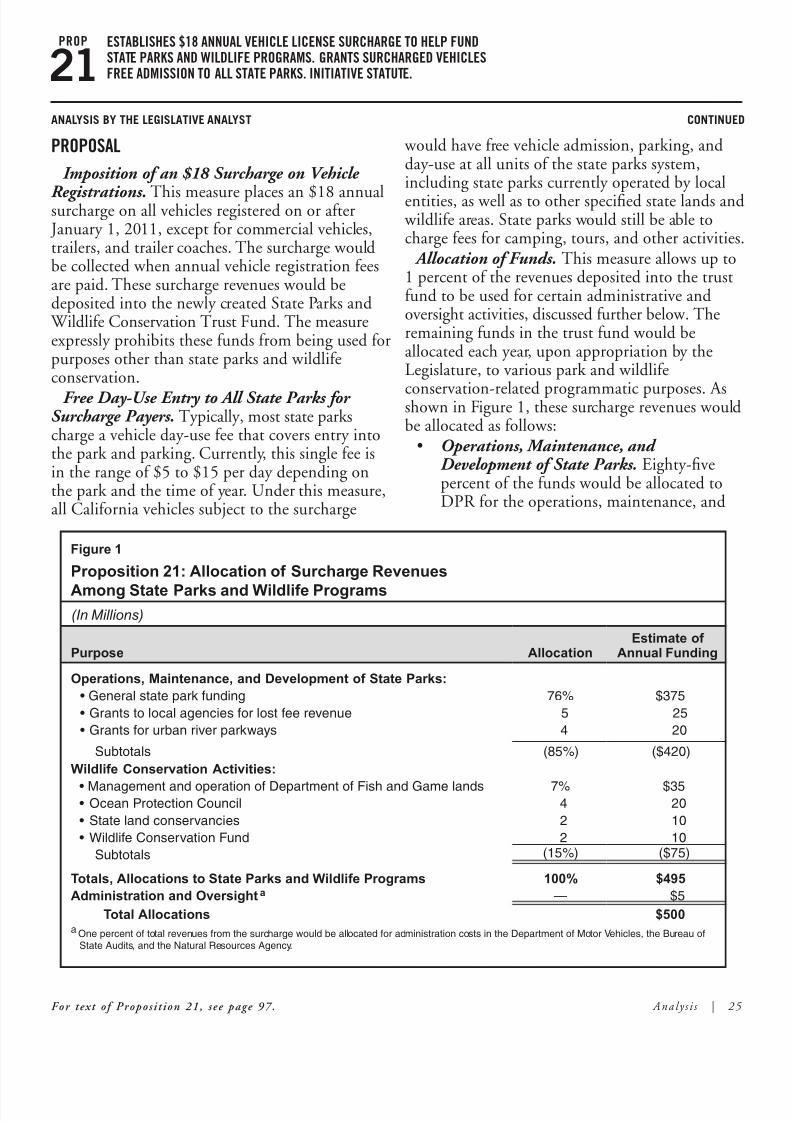

PROPOSAL

Imposition of an $18 Surcharge on Vehicle

Registrations. Thismeasureplacesan$18annualsurchargeonallvehiclesregisteredonorafter January1,2011,exceptforcommercialvehicles,trailers,andtrailercoaches.Thesurchargewouldbecollectedwhenannualvehicleregistrationfeesarepaid.ThesesurchargerevenueswouldbedepositedintothenewlycreatedStateParksand WildlifeConservationTrustFund.Themeasureexpresslyprohibitsthesefundsfrombeingusedforpurposesotherthanstateparksandwildlifeconservation.

Free Day-Use Entry to All State Parks for Surcharge Payers.Typically,moststateparkschargeavehicleday-usefeethatcoversentryintotheparkandparking.Currently,thissinglefeeisintherangeof$5to$15perdaydependingontheparkandthetimeofyear.Underthismeasure,allCaliforniavehiclessubjecttothesurcharge