Competitiveness Promotion and Clusters In … Porter of Harvard, author of numerous books on...

102

Competitiveness Promotion and Clusters In Colombia and El Salvador FINAL REPORT James W. Fox Louis Berger Group, Inc. November 2003

Transcript of Competitiveness Promotion and Clusters In … Porter of Harvard, author of numerous books on...

Competitiveness Promotion and Clusters

In Colombia and El Salvador

FINAL REPORT

James W. Fox

Louis Berger Group, Inc.

November 2003

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. i

Table of Contents

Chapter 1. What is “Competitiveness” All About? .............................................1

1.1 Introduction..............................................................................................1 1.2 Clustering, Value Chains, and Productivity.............................................5 1.3 Empirical Research on Cluster Issues......................................................9 1.4 Designs for Competitiveness Promotion .................................................12

Chapter 2. Colombian Experience with Promotion of Competitiveness ...........16 2.1 The Country Economic Context ..............................................................16 2.1.1 Background............................................................................16 2.1.2 Economic Policies..................................................................16 2.1.3 Trade Policy ...........................................................................17 2.1.4 Trade Institutions ...................................................................17 2.2 Colombian Trade Performance ..........................................................18 2.3 The Colombian Competitiveness Effort ............................................21

2.3.1 Initial Efforts to Promote Competitiveness............................21 2.3.2 Current Programs ...................................................................23

2.3.2.1 Encuentros Nacionales...............................................23 2.3.2.2 Specialized Networks.................................................25 2.3.2.3 Convenios de Competitividad Exportadora ...............25 2.3.2.4 CARCEs and Regional Development Efforts............31

2.4 Indicators of Changes in Colombian Export Competitiveness ..........32

2.4.1 Export Statistics .....................................................................32 2.4.2 Other Indicators of Change....................................................34

2.5 Conclusions ....................................................................................35 2.5.1 The Competitiveness Program...............................................35 2.5.2 The Policy Context ................................................................36 2.5.3 Country Environment.............................................................37

Chapter 3. Promotion of Competitiveness in El Salvador ..................................38 3.1 The Country Economic Context .............................................................38 3.1.1 Background............................................................................38 3.1.2 Economic Policies..................................................................39 3.1.3 Trade Policy ...........................................................................41 3.1.4 Trade Institutions ...................................................................42

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. ii

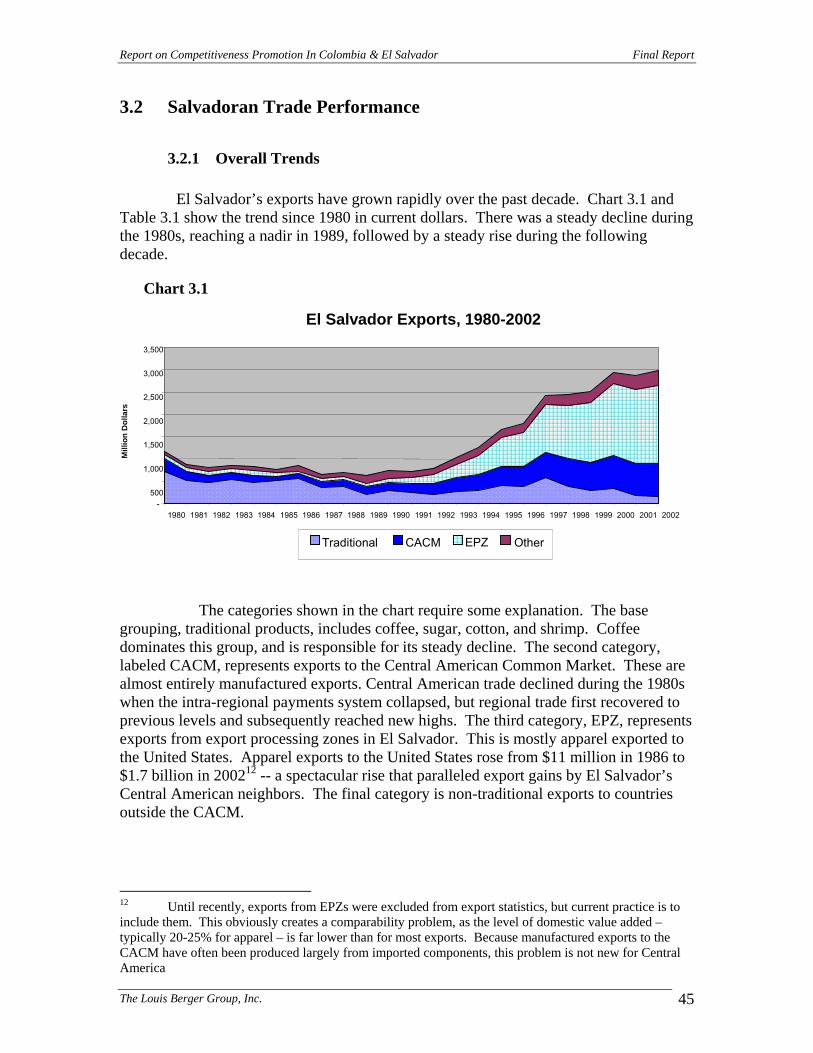

3.2 Salvadoran Trade Performance..........................................................45 3.2.1 Overall Trends .......................................................................45 3.2.2 Trends in Specific Sectors .....................................................46 3.3 The Salvadoran Competitiveness Effort ............................................49

3.3.1 Cluster Promotion ..................................................................50 3.3.2 Results from the Cluster Experiment.....................................52 3.3.3 Conclusions about Clusters………………………………....57

3.3.4 Other Competitiveness Promotion Activities ........................58

3.4 Indicators of Changes in Salvadoran Competitiveness......................58 3.4.1 Export Statistics .....................................................................58 3.4.2 Other Indicators of Progress ..................................................60

3.5 Conclusions… ....................................................................................61

Chapter 4. Measuring National Performance in Competitiveness.....................62

4.1 Introduction ....................................................................................62 4.2 The Global Competitiveness Report (GCR) ............................................62 4.2.1 The Methodology of of the GCR...........................................62

4.2.2 Evaluation of the Methodology ............................................64 4.2.3 Performance of El Salvador and Colombia in the GCR .......65 4.2.4 Using the GCR in Assessing Competitiveness Programs.....67 4.3 The World Bank’s Doing Business Database ..........................................68 4.4 Other Measures of Country Competitiveness ..........................................71 4.5 Comparing the Three Indices...................................................................72

Chapter 5. Summary Comments and Conclusions ...............................................73 5.1 Monitoring and Evaluation………………………………………….. .... 73 5.1.1 Tracking Performance During Implementation………….…. 73 5.1.2 Longer – Term Impact Measurement ……………………....75 5.2 Comparing the Two Cases………….…………………………………....76 5.3 Conclusions: What Can Donors Do? .........................................................77 5.3.1 Competitiveness- Specific Recommendations……………….. .77 5.3.2 Broader Recommendations……………………….…………....79 Appendix 1 Bibliography ....................................................................................80 Appendix 2 Specific Components of the Global Competitiveness Report............85 Appendix 3 Persons Interviewed...........................................................................87 Appendix 4 Sectoral Agreements in Colombia .....................................................89 Appendix 5 Scope of Work ...................................................................................90

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 1

Those who say the future is coming rapidly toward us are wrong. The future is really rushing away from us, and we have to hurry after it, or be left behind.

--Author Unknown

1. What is “Competitiveness” All About?1 1.1 Introduction

The proper meaning of the word competitiveness has been debated in recent years, usually with economists on one side, and others, including business theorists, on the other. To most economists, competitiveness means that suppliers of products or of factors of production are able to meet a market test. That is, others will purchase their good or service at a market price that covers the marginal costs of production. By definition, non-competitive firms will eventually disappear, for their operation is unsustainable since the sales price does not cover expenses.

There is general agreement on the economic interpretation of competitiveness.

The problem comes when the same term is used to refer to countries. Countries are not business units that will disappear if their products cannot find favor abroad. Instead, exchange rates and terms of trade will adjust so that the country finds itself in an economic position consistent with the capabilities of its economic units, its factor endowments of land, labor and capital, and the quality of its economic, political and social institutions. Countries with low capacity to produce goods and services will sell little to others, and consequently be able to buy little, and are likely to be poor. But they are not “uncompetitive,” just unproductive. 2

From the business school approach, competitiveness is related to choices about

technology, management, and markets. This approach is not viewed as fixed in proportion based on natural conditions, but rather as the result of choices made by firms. In its more nuanced form, analysts reviewing a country’s potential competitiveness use the term to encapsulate efforts to promote increased productivity and productive capability in developing countries. The basic concepts draw heavily on the ideas of

1 This report is an analysis of the existing information base on the concept of competitiveness, as a microeconomic tool for promotion of productivity growth. It draws upon the available literature and field visits to Colombia and El Salvador to explore the experience in this emerging area. The fieldwork in each country took place over 2-3 weeks, and included interviews with 35-40 leaders from business, government, and academia. The study was commissioned by the Inter-American Development Bank. The scope of work for the study is at Appendix 5. 2 Paul Krugman has been the most articulate opponent of the idea of competitiveness. He writes “competitiveness is a meaningless word when applied to national economies. And the obsession with competitiveness is both wrong and dangerous” (Krugman, 1994, p. 44). He goes on to argue that advocates of measures to improve national competitiveness are either nationalistic or ideological, and that they misunderstand (or refuse to consider) simple economic theory.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 2

Michael Porter of Harvard, author of numerous books on competitiveness strategies for business, including the massive study, The Competitive Advantage of Nations (1990). Porter notes that "the only meaningful concept of competitiveness at the national level is national productivity" (Porter, 1990, p. 6). 3

Much of the difference between economists and business theorists thus simply

reflect different definitions of the meaning of the term “competitiveness.” Both agree that it relates to productivity, but economists tend to focus on economy-wide factors that affect productivity, such as inflation, interest and exchange rates, and other economy-wide variables. Business theorists concentrate instead on what might be termed the microeconomics of competitiveness – those factors at the firm, industry, and institutional level that can make differences in productivity with a given set of macro-level indicators. Business theorists do not argue that macroeconomic issues are irrelevant, but only that they are not the part of the ‘productivity puzzle” that they are subjecting to analysis. This study focuses on the conceptual approach used by the business theorists, while recognizing that an appropriate macroeconomic and trade environment is critical to the general capacity of firms to operate successfully in any sector.

In The Competitive Advantage of Nations, Porter develops the concept of a cluster

of firms to explain the greater productivity of world class firms. A cluster is identified as “a geographically proximate group of interconnected companies and associated industries in a particular field, linked by commonalities and complexities.” Porter’s study shows competitive firms are more likely to arise where there are clusters of related or competing firms, and where several additional conditions are present. These conditions, popularized in the “Porter diamond,” include:

• Factor conditions, such as skilled labor and infrastructure; • Demand conditions, particularly in the home market; • Related and support industries, including universities and research

institutions; and • Firm strategy and structure.

In Porter’s model, it is the interaction of these four conditions that determines the competitiveness of a particular industry in any country. Where firms are fiercely competitive and where there is close interaction with the other elements of the diamond, there will be constant pressures for improvements in capabilities. Such improvements in each element of the diamond then feed back synergistically to increase the competitiveness of the entire cluster of firms, support industries and factors of production. An essential feature of the model is that individual firms cannot alone become competitive and stay competitive in world markets. There must be a nexus of competitors and of supporting industries that are also capable of delivering inputs and

3 "Seeking to explain ‘competitiveness’ at the national level, then, is to answer the wrong question. What we must understand instead is the determinants of productivity and the rate of productivity growth. To find answers, we must focus not on the economy as a whole but on specific industries and industry segments” (Porter, 1990, p. 9).

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 3

services to the firm that are also continually upgrading their capabilities. Achieving competitiveness thus involves all parts of the “value chain,” and not just the individual firm. Figure 1 provides the Porter diamond in graphic form. Porter’s theory of the key role of clusters was developed by studying successful firms in developed countries. Clusters have been observed as an outcome in a number of geographical locations, such as Hollywood and Silicon Valley. Nevertheless, the competitiveness theory embodies a number of ideas that have some power for explaining the relative success and failure of different developing countries in gaining markets for their exports. And this power has led researchers to seek ways in which clustering, or other aspects of competitiveness, might be used to promote faster productivity growth.

Figure 1: The Porter Diamond

Source: Michael Porter Two aspects of Porter’s model should be particularly noted in applying it to developing countries. His model assumes – based on his research during the 1980s – that sophisticated domestic demand for the products of an industry are an essential characteristic of competitive clusters. This is essential, he has argued, because only when the producer is very close to the market can innovation move quickly to meet changing consumer preferences. Second, Porter takes for granted that foreign-investment based clusters will not be competitive in his terms. This is because key decisions will be made in the foreign investor’s home country, rather than in the country where the investment is located. Consequently, activities of the firm in the recipient country will be subsidiary, and tend to lag trends in world markets.

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

ConditionsDemand

ConditionsDemand

Conditions

• The microeconomic business environment is comprised of the array of skills, knowledge, rules, policies, supporting industries, and institutions surrounding competition

A core of sophisticated and demanding local customer(s)Local customer needs that anticipate those elsewhereUnusual local demand in specialized segments that can be served nationally and globally

Presence of high quality, specialized inputs available to firms

–Human resources–Capital resources–Physical infrastructure–Administrative infrastructure– Information infrastructure–Scientific and technological

infrastructure–Natural resources

Access to capable, locally based suppliers and firms in related fieldsPresence of clusters instead of isolated industries

A local context and rules that encourage investment and sustained upgrading

–e.g., Intellectual property protection

Open and vigorous competition among locally based rivals

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 4

Based partly on Porter’s work, some development theorists believe that these ideas are important in developing countries, and that the development of competitive clusters can be catalyzed by “change agents” – governments or donors – working with the private sector. Among others, the actions change agents might pursue include:

• Fostering, through technical or financial support, the development of “clusters” around which common objectives can be sought by competing firms.

• The development of a national competitiveness strategy that brings together

government, business, labor and other interested organizations and seeks to eliminate obstacles to productivity and exporting.

• Promotion of cooperation of firms in different parts of the “value chain” for

specific products or sectors, with a view to reducing transactions costs between different parts of the chain, and improving the quality of products of one part of the chain that are inputs to other firms in the chain.

• Encouraging firms to “move up the value chain” by moving away from

commodity production for world markets to branding, or quality differentiation (e.g., promoting “Colombian coffee”) that will allow higher profit margins and provide some protection against competition from lower-wage countries.

• Dissemination of competitiveness concept through conferences, seminars, and

written material. As these suggestions indicate, and as subsequent sections of this report will document, the way that competitiveness has been used in El Salvador and Colombia, or more broadly by Michael Porter and the Global Competitiveness Report, has little in common with the view that countries can be competitive. Aided by the Global Competitiveness Report, both countries have used the concept to address characteristics of their national economic environment that limit their capacity to produce at higher levels of productivity. These include such things as poor government policies, poor road and port infrastructure, inadequate telecommunications, and inexistent links between academia and business. To the extent that “competitiveness” has become a term that focuses attention on the internal obstacles to higher productivity, it is neither wrong nor dangerous. Rather, it becomes a tool for a national focus on factors responsible for a country’s poverty and its inability to organize its national potential in a productive way.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 5

1.2 Clustering, Value Chains, and Productivity Below the very general issues surrounding the term “competitiveness,” there has been considerable theorizing by economists about the real-world issues that Michael Porter and other business theorists have proposed. In particular, there are four or five strands of economic thought that bear importantly on the importance of clustering for economic efficiency and productivity. The general topic for economists is the existence and significance of two terms that are opaque to outsiders: “externalities,” or “external economies.” The two terms are synonymous. They represent the net benefits to the economy, but not to the individual firm, of the combined activities of groups of firms or economic operators. Wall Street, or Hollywood, or Silicon Valley are all places where an industry benefits from an intense network of related firms, providing mutually-supporting benefits to others. Externalities can be negative as well as positive. The “tragedy of the commons,” where the over-fishing or over-grazing by each individual, in search of increased production, causes disastrous losses for all provides a good example of a negative externality. Each fisherman works harder to preserve his income as fish stocks are depleted, but the effort of all to do the same ultimately destroys the resource on which each depended. But while negative externalities end with a collapse in production, positive ones can produce virtuous circles of increasing productivity and prosperity. Alfred Marshall (1892) recognized the importance of geographical clustering of firms for economic efficiency. Marshall noted that firms in the same industry tended to cluster in the same geographic area, and that these industrial districts, or clusters, provided benefits (i.e., economists “externalities”) to the individual firms in comparison to firms located elsewhere. Any individual firm could more easily find a supply of workers with the appropriate skills than elsewhere. Indeed, workers hired from another firm might bring better technologies with them, so that all firms were able to gain in productivity from the circulation of workers among the different firms. Specialized service providers, knowledgeable about technical, design or marketing aspects of the product were likely to be more abundant than elsewhere, and materials relevant to the sector were likely to be cheaper and more easily obtained than elsewhere. Joseph Schumpeter’s conceptualization of entrepreneurship and innovation is a second key strand (Schumpeter, 1942). Schumpeter emphasized innovation as a central feature of the economic growth process, and the entrepreneur as the motive force. Schumpeter believed monopoly was an unimportant problem in the long run in a free-market economy, for innovations by one firm would later be imitated by others, eroding, and eventually eliminating, all monopolies, and therewith the profits of the original monopolist. Thus, economic growth was a treadmill, where constant innovation was the means to guarantee that any existing product or technology would gradually become obsolescent. The dynamic entrepreneurial processes of capitalism would assure this through new ideas, new firms, and new products. 4 4 This is also the theme of a new book by William Baumol, The Free-Market Innovation Machine, where the author argues that large companies have come to see constant innovation as essential to survival.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 6

Another feature of Schumpeter’s analysis is also important. He recognized that any innovation created negative externalities for others. The innovator’s profits will be larger than the economy’s benefits from his innovation. Henry Ford’s innovation created many jobs in the automobile industry, but also produced unemployment, bankruptcies and other dislocations in the carriage and other horse-related industries, as well as in less-efficient automobile producers. This process of “creative destruction” is beneficial in the longer term in freeing people and capital from low productivity areas, and redirecting their use for higher-productivity ones. China’s new efficiency in shoe production is creating massive employment there, but producing bankruptcies and unemployment in the shoe industry throughout the developing world, particularly for firms that failed to adapt to changing technological possibilities. Ronald Coase (1998) provides another important perspective with implications for competitiveness. He concluded that some types of externalities could be internalized by the firm. In particular, he concluded that the level of vertical integration of the business firm depended upon the level of transactions costs along the value chain from basic raw materials to final consumer. In parts of the chain where transactions costs were high, the firm would integrate backward into raw material production and/or forward into distribution of the product. Thus, a firm in an environment where contract enforcement was difficult, or where the quality or timeliness of raw material inputs was variable or uncertain, would be more vertically integrated than a firm in an environment where reliable relationships with suppliers were the norm. As suggested by Coase, it is not necessary for all firms to buy into the value chain for it to work since downstream firms unsatisfied with their inputs can integrate backward or individual downstream firms can contract with upstream firms to obtain products of the specified quality. Evidence suggests, however, that firms in developing countries confront numerous financial, economic, policy, technology, and even cultural barriers that can impede the adoption of appropriately integrated production chains. This will limit the productivity of the firm and, ultimately, the potential for exports of goods and services. The identification and removal of these barriers is one of the great challenges facing policymakers in the developing world and one that can best be addressed on a sector-by-sector basis. Mancur Olson, in The Logic of Collective Action (1962), provides the final strand of thinking relevant to the topic. Olson analyzed cooperation by business firms for collective purposes outside the confines of the individual enterprise. The logic of the individual enterprise is clear and unambiguous. The owners set the goals, and a hierarchical structure implements them. For collective activities of groups of individual enterprises there is no such clarity. In the absence of a “bottom line,” to identify success or failure, associations among businesses are typically voluntary. Individual members can leave whenever they see the costs of the grouping exceeding the benefits. This limits the capacity of the association to allocate the costs of the collectivity among the members. It also limits the capacity of the association to take positions that conflict with the views of important members. Either difficulty – high costs to individual members, or low (or negative) perceived benefits – tends to make such collective efforts weak. Sectors where there is a single dominant firm will tend to be better supplied with

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 7

collective goods than those where many smaller firms share the market, for the dominant firm will tend to be willing to underwrite a disproportionate share of the joint costs. In most cases, it is the firm at the top of the production chain, the one closest to the final consumer, who provides the needed leadership and absorbs the additional costs of promoting the benefits of collective action among firms. The smaller firms will pay less than their “fair share” of the collective enterprise, free-riding on the dominant firm’s self interest in funding the bulk of the collective effort. Olson draws three conclusions from these characteristics and from his analysis of existing collective efforts.

First, such collective efforts suffer from a severe free-rider problem, especially

when the action is likely to benefit both those who contributed to the effort and those who did not. The net result is an under-investment in these types of efforts. For that reason, a combination of public and private sector support is often needed to encourage the appropriate investments in policy reforms that benefit many actors.

Second, collective groups that succeed do so in part because they have developed

indirect mechanisms, or forms of moral suasion, to address the free rider problem. Third, because of the difficulty of creating and sustaining collective action, the

effective organizations in this area are likely to be those with long traditions and records of effective results. In many contexts, effective lobbying of the government is the most tangible evidence of success. As a result, the effective collective action organizations are likely to be those that represent vested interests of the past, rather than those representing emerging opportunities. Often these are the types of groups that benefit from the existing status quo and are reluctant to promote changes that alter factor prices (trade reform and tax reform) or encourage new entrants that may compete with existing quasi-monopolies (investment promotion). For these reasons, effective change requires not only committed private sector participation from leadership in new emerging sectors, but also an enlightened public sector role. In particular, the political leadership must actively support policy change.

Five general conclusions might be drawn from these strands of analysis: 1. There are definite economic benefits of clustering of firms in similar activities

that cannot be captured by individual firms. Geographical places that make it easy for such clustering to occur are likely to have more economic activity and income than those that do not.

2. Collective action “along the value chain” requires a strong economic

motivation. When transactions costs are high (e.g., quality uncertain, delivery schedules not meeting commitments, or prices too high) firms have an incentive to integrate vertically to overcome such problems. This case is the most common one in developing countries. Alternatively, specialized suppliers who focus on meeting the requirements of onward users have an economic incentive to offer the product in the way that meets the needs of these users.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 8

3. Developing and maintaining a collective association of firms, in the absence strong private sector leadership is difficult to sustain over a long period of time. Individual members will contribute less than would be optimal for the collectivity, and such efforts will tend to be under-funded. Collective efforts will also be timid, for fear of losing members opposed to assertive actions.

4. The main exception to the previous point is long-existing associations that

have found ways to address the free-rider problem, and that have shown proven capacity to influence government. As a consequence, the past will be over-represented in existing business associations because long-established associations have most effectively overcome collective-action problems. Firms in new sectors will typically be less well organized, and have little capacity to provide services to their members or to lobby government for more favorable policies. Consequently, public policy is likely to be backward-looking.

5. Productivity is the engine of economic progress. Firms must steadily improve

their manner of operation in order to survive, lest entrepreneurs elsewhere put them out of business. Appropriate government policies for infrastructure, market regulation, trade, and investment promotion can encourage an economic environment that supports new entrants and the dynamic innovation needed to boost productivity. In the absence of such measures, the gap between domestic and foreign productivity will only widen until the political and economic schema employed to protect domestic markets eventually collapses, at a high social and economic cost.

These observations suggest a useful role for governments and donor agencies in provisioning of public goods and helping to surmount coordination failures that often inhibit useful collective action. Productivity improvement is the key. Some productivity improvement can be obtained by collective action by firms in each sector. But such collective action is a public good that will be under-funded if left to the actions of the private sector. Government or donors can correct the imbalance between private and social benefit by partial funding of such activities. The outside funding changes the calculus of costs and benefits to the sector’s firms, and donor requirements for substantial contributions to the effort by the firms can help create the moral pressure for contributions by firms. They will also shift the calculus of net benefits toward stronger, more assertive actions, as long as the external funding source demands them as the price of the external assistance. 5 In sum, economic theory offers a clear basis for donor support for cluster development, contingent on substantial contributions to the effort by the firms in the

5 According to Porter "National governments, for their part, must set the appropriate goal, productivity, which underpins economic prosperity. They must strive for its true determinants, such as incentive, effort, and competition, not the tempting but usually counterproductive choices such as subsidy, extensive collaboration, and ‘temporary’ protection that are often proposed. Government's proper role is to push and challenge its industry to advance, not provide ‘help’ so industry can avoid it" (Porter, 1990, p. 30).

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 9

sector, and to the potential for this to yield sustained productivity increases by the firms in these clusters. 1.3 Empirical Research on Cluster Issues The above suggests that productivity growth is the primary goal, and some kinds of support for clusters or clustering, or value chains, may be warranted. The next question for purposes of analysis is, “what is a cluster?” Or more specifically, what kinds of groupings of businesses are desirable objects for government or donor support? Successful clusters of small enterprises in developed countries, with Italy (ceramics and shoes being two frequently-cited cases) the prime example, have excited much attention. Such clusters have conformed closely with the Porter model, building heavily on sophisticated domestic demand for their products, and developing a series of cooperative approaches among small firms, in the midst of intense competition among them. Two features of the Italian model are particularly attractive to development promoters. First, the firms have been able to capture international markets by providing designs that allow them to demand premium prices for their products. Second, this has been achieved in industries with many small firms. These two characteristics offer the best case from a development promoter’s perspective: indigenous-based development that draws its energy from small firms. And some have seen promotion of clustering among small and medium indigenous firms as the way forward in private-sector promotion. A priori reasoning suggests that the substantial fixed costs involved in identifying and developing export markets and continuing costs of innovating to stay abreast of markets are beyond the reach of small, individual firms. For that reason, there has been a strong interest among policymakers and academics to applying the lessons of successful clusters to overcome this barrier. 6 It is evident that in developing countries the base of technology, management skills and policy environment is not equivalent, making a direct application of developed-country experience less straightforward. O’Malley and Van Egeraat (2000) test Porter’s methodology for identifying successful industry clusters by applying it to Ireland. Their analysis identifies two problems in applying Porter’s theory to small, or to developing, countries. First, the predominance of foreign investment in leading export sectors and the relative lack of

6 It should be recognized, however, that once-successful clusters in developed countries can eventually lose their competitive edge. Cooke (2002) analyzes several European cases of successful clusters that failed to maintain their competitive position, and fell into decay. He studies several cases, including automotive parts, ceramics and silk manufacturing. Cooke concludes (p. 184) that “failing clusters have in common a characteristic of stubborn resistance to change, a cavalier collective attitude towards the value of knowledge other than that traditionally available, and a culture promoting the withholding of information of central importance to normal, day-to-day business functions.” In sum, Cooke’s analysis of the European experience emphasizes the need for: 1) business leadership oriented toward the future rather than the past; 2) close links between business and scientific research; and 3) rapid dissemination, rather than hoarding, of knowledge.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 10

domestic firms is a notable characteristic of such countries. Porter generally excludes foreign investors from a major role in clustering, believing that such firms mainly respond to decisions and priorities in their headquarters country. Consequently, they lack the independent decision-making and creativity that would make them candidates for industrial clustering in the investment-receiving country (Porter, 1990, p. 566-67 and 678-79). Second, they apply a specific Porter observation for identifying successful export sectors – that the sector’s exports as a share of world exports of their production exceed the country’s total share of world exports. In the case of Ireland, overall exports accounted in 1993 for 0.79% of world exports. Sectors where Ireland exports a larger share of world exports than 0.79% would be candidates for high competitiveness. Few indigenous sectors would qualify by this criterion, for foreign investors are the leading exporters from Ireland. If foreign firms are excluded from the export base, Ireland only accounts for about 0.4% of world exports. By this lower standard, a much larger number of sectors would qualify. Nevertheless, even this standard may be too crude. About half of Irish exports by domestic firms come from the meat and dairy sectors, which have little industrial value added from their raw material base, and represent a far lower share of employment and value added per dollar of exports than other export sectors. The successful industries by the Porter standard are then related to the industries where there is rapid growth in exports and employment. The fit is very poor, and the mostly “high-tech” industries that have been the source of growth have heavy foreign investment. Irish export success is compared to the EU, and deemed to be notable in those industries with large foreign investment. Clearly, for Ireland, competitive success has not been driven by strong domestic clusters.

The authors reject the idea, put forward by some Canadian researchers, of a “double diamond” model involving two countries. The United States is the largest foreign investor in Ireland, but Ireland’s markets are mostly in Europe and the UK. Thus, the learning relating to firm strategy is drawn from the USA, but the learning relating to customers comes from the UK and Europe. This kind of multiple diamond does not conform well with the Porter model, and suggests that the model may be less applicable to developing countries than to world leaders. While these critiques may have some merit, Porter’s view may rule over the longer term. Over time, the predominance of foreign investors may erode. The initial key driver to Ireland’s success in the Information, Communications and Technology (ICT) sector was FDI in assembly and manufacturing. Green (2000) documents a shift from electronics (the domain of foreign firms) to software development where small, indigenous firms are major players. 7 Similar effects are being observed in countries like

7 According to Green, “during the 1990s, indigenous firms achieved growth rates of 11 per cent a year for employment, 25 per cent a year for the value of sales and almost 40 per cent a year for the value of exports. While the electronics sector continues to be dominated by large multinational companies, employment in software products and services is more evenly divided between overseas and indigenous companies, mainly SMEs.” (Green, 2000, p. 2)

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 11

Costa Rica, where FDI has provided the impetus for the development of local suppliers in packaging and print and the development of an incipient software sector. Attenburg and Meyer-Stamer (1998) provide a useful perspective on the conditions under which clusters prosper in developing countries, addressing particularly the matter of technology transfer to firms in the cluster. Based on their review of the experience in developing countries, they propose a three-class typology for clusters:

• Clusters of small firms that are “surviving,” • Clusters of large-scale production, that include both small and large producers,

and • Clusters based on transnational corporations.

They provide diagnostics and recommendations for each type. They consider the first group to be hopeless in the longer term. They have little access to technological upgrading, and their sectors of concentration, such as shoes and clothing are daily exposed to greater competition from abroad. Some things can be done with such groups, though only with projects demanding strong actions on the part of the entrepreneurs. Government agencies and organizational forms like cooperatives cannot solve their problems. For many, the best solution is that they leave the sector for another, such as much of the service sector, which is less vulnerable to foreign competition. Attenburg and Meyer-Stamer consider the second group much more promising, due to the potential for technology transfer from large to smaller firms, and the possibility of strengthening linkages within the sector that will increase competitiveness throughout the value chain. They consider this group to be the most promising for development agencies to support. Opportunities for national development can also come from the third group, transnational corporations. This largely involves developing supplier relationships with transnational firms – though this is initially likely to be difficult because of the high quality standards of the multinationals, but public policy can push them to increase the capacity of local suppliers. This analysis by Attenberg and Meyer-Stamer is carried out under the assumption that firms located in the country are the source of technology upgrading. But this ignores the structure of much of today’s world trade. An understanding of the conditions of marketing in developed countries is key to understanding the driving force behind much of what is produced in developing countries. Humphrey and Schmitz (2002) address the capacity of industrial clusters to compete on international markets by examining relationships with global buyers. They argue that buyers are the critical link for moving beyond production of commodities. Commodities can be sold in arms-length transactions, but they offer little opportunity for upgrading quality to produce more sophisticated or more narrowly-tailored products that would command premium prices. While much of the literature in this area focuses on the cluster, the outcomes of cluster operations depend on the capabilities of individual firms in the cluster. Humphrey

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 12

and Schmitz (2002, p. 1024) argue that an emphasis on inter-firm relationships in clusters “crowds out the concern with what goes on inside the firm.” They argue that only individual firms that have strategic intent, and are willing to make substantial investments, will be able to successfully upgrade technologically. The explanation of the success of many East Asian firms, they argue, is that they exhibited these characteristics more clearly than firms in other regions. Sonobe, et al., (2002) offer some corroboration of this perspective, showing that the characteristics of individual entrepreneurs are key to long-term success. They examine the experience over a decade of the process of upgrading of children’s apparel production in firms in a single geographic cluster in China. Their longitudinal analysis came to two interesting conclusions. First, government action in establishing a specific marketplace was “particularly important in stimulating the entry of new enterprises in the early stage of cluster development, when the major products were simple and standard.” This led to an expansion of the number of firms and in employment, but the increased competition drove down earnings. In subsequent years, the enterprise success depended mainly on characteristics of the individual firm. Only those firms that were able to upgrade their product were able to prosper. The most successful in upgrading tended to be better-educated businessmen with marketing experience, and good business skills. For the purposes of this paper, the term “cluster” is defined as the organization and interaction among firms with government, academic institutions, research organizations and others in the formulation of business strategies and policy reform. It describes a strategic approach for organizing firms in order to achieve improvements in business practices as well as reforms in government policies. In this sense, it is more than just a value chain in which firms interact in order to achieve specific business targets. It is also more than just a sector, although the term cluster is sometimes intermixed with sectoral definitions. As will be shown later on, the measurement of impact data at the cluster level is fraught with challenges and sector data are sometimes used as proxies for measuring the impact of cluster initiatives. This is often the case since impact data is typically only available at the sector level or broad export classifications. 1.4 Designs for Competitiveness Promotion Both the term “clusters” (as described above) and the term “competitiveness” can be subject to overuse and overly broad definitions. For example, many would argue that the most effective “competitiveness“ program is to establish a favorable exchange rate policy and a stable macroeconomic environment. Others would complement these initiatives with programs focusing on improved labor supply, infrastructure, export and investment promotion, technology transfer, etc. While all of these initiatives are important, they are not directly addressed in this paper. Rather, they are indirectly presented as they relate to topics presented by the clusters themselves as part of the national dialogue. Specifically, this paper focuses on the design of competitiveness programs as they relate to the interaction between clusters (as defined above) and national dialogues that focus on cluster issues.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 13

Considerable theoretical and empirical work has been done on competitiveness. Most of this work, as discussed above, looks at clustering and related processes as the natural evolution of business capability in favorable environments. Some theorists have gone further, making recommendations for national programs to promote competitiveness. Michael Porter (2002) recommends the creation of such programs, involving several elements.

• First, industry associations and chambers of commerce focus their effort and attention on promotion of productivity-enhancing actions by their members and by governments, rather than seeking to lobby government for special privileges.

• Second, universities and research institutions establish linkages with the business

community to support research and technology dissemination relevant to productivity growth.

• Third, one or more independent institutions provide leadership in promoting the

national agenda. Several features of the third element need elaboration. Porter argues that such institutions need broad involvement of the private sector, academia and government. Nevertheless, they need to be independent of government, in order to assure that they support long-term efforts, which will be beyond the life-span of any individual administration. Consequently, they need strong cross-party backing with governmental support regardless of the party in power.

There has been no empirical evaluative work that would confirm or reject Porter’s proposed approach. Indeed, the broadness of the concept, the long time horizon and the variety of other factors likely to be at work strongly suggest that evaluation is not a feasible tool. Long time horizons and long chains of connection between actions and outcomes are both factors that tend to reduce evaluation to speculation. As an action program, moreover, Porter’s approach leaves a very limited role for government or for donors. Both are likely to seek results within a limited (3-4 year) time horizon, and to seek to use direct control and action by timetable, rather than the more limited role of encouraging action by others. A somewhat different model has been developed by a number of countries, often in collaboration with donor agencies. This typically involves thee major elements:

• A national competitiveness council, which brings the political leadership together with all other interested parties;

• A secretariat, that supports both the competitiveness council, if it exists, and

cluster groupings; and

• “Clusters” of firms and other institutions along the value chain of a particular product, or of organizations involved in a particular sector.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 14

The IDB has been active at the cluster level through projects in a number of countries. USAID has been particularly active at the competitiveness council level, setting up programs in Sri Lanka, Mongolia, Croatia, Macedonia, and the Dominican Republic, among other countries. INCAE, the Central American business school, has worked at the regional level in Central America, while the Corporación Andino de Fomento (CAF) has done so for the Andean region. CAF has also promoted academic analysis of competitiveness issues. Australia created a national competitiveness council in 1995, and Ireland did so in 1997, both without donor support. The programs in the other countries are even more recent. Broadly speaking, the institutional design of such programs has tended to involve government directly as the promoter and manager of the effort. The institutional analysis of this approach presents a number of different questions. A National Competitiveness Council (NCC). All governments establish myriad councils and advisory bodies. Many are purely decorative or ceremonial, while others provide forums for important discussions on national priorities, important initiatives and information exchange. In addition to the problem of differentiating a competitiveness council from these other types of advisory body, three questions will immediately arise:

• Is a national competitiveness council needed? • If the answer to the previous question is yes, how can councils established by a

particular government administration to further its policy and political goals become a vehicle for achieving national long-term goals for competitiveness?

• How big should such a council be, and what type of people should be members?

• How frequent should the meetings of the council be, and what types of policy

issues should it address? The first issue – whether to have a national competitiveness council, and, if so, how to structure its operation seems to have no clear answer in the literature. In part, the reason surely lies in the importance of the “software” of personalities and staffing relative to the “hardware” of formal organizational arrangements. A second problem is that a national competitiveness council will not operate in virgin territory. Most countries have already established a variety of councils for national economic purposes (national export councils, national productivity councils, national investment promotion councils, national manufacturing councils, among others) that have functioned well or badly, but whose formal existence continues to include some of the terrain that a national competitiveness council might cover. Or, the failure of so many previous initiatives makes the new proposal for a national competitiveness council likely to be viewed as just another fad, destined to suffer the same fate as previous efforts. Unfortunately, this study cannot shed light on some of these issues. As discussed below in the relevant sections, neither country studied here has a national competitiveness council in operation. Colombia had such a council during a previous

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 15

administration, and the issues relating to its performance are discussed in the context of the Colombian experience. Given the lack of a council, the primary role in promoting competitiveness has fallen in each of the two countries studied on a unit within a governmental ministry – the Ministry of Economy in the case of El Salvador, and the Ministry of Foreign Trade in the Colombian case. The relation between such governmental promotion units and cluster development is an issue for which the experience of both countries offers useful lessons, to be discussed in the appropriate section of the report. The Secretariat. A typical competitiveness project will have a special office to promote the creation of clusters and to support those in existence, and to provide staff support to the national competitiveness council if it exists. Typically, the secretariat is a special office in a government ministry, usually the ministry of economy. In some cases, the location is outside the government, funded by a donor. Experience suggests that cluster secretariats inside the government will have less capacity to interact with the private sector members effectively than a secretariat outside the government. This is because, as shown in previous studies of government export promotion (e.g., McKean and Fox, 1994) that government institutions intended to support the private sector tend to be too mired in internal governmental politics to be able to understand and respond to the real concerns of the private sector. Yet, a location within government assures adequate resources for funding the secretariat, and provides a much stronger connection to the political leadership. This connection may be key to achieving results on policy issues. The Clusters. Several design issues relate to the clusters.

• Where should the leadership of the cluster lie? Should it be with the private-sector firms that are the membership, or should the government representative set the agenda and meeting schedules?

• If donor resources are being provided to the clusters, what mechanisms

need to be in place to assure efficient use of the resources?

• How are clusters to be conceptualized? Are they temporary groups that meet to achieve specific goals and then disband, or are they the beginning of more permanent institutions. If the latter, how are they to be funded in the longer term? In most countries there are already-existing private sector associations and chambers that cluster together the firms in a particular industry. How should the competitiveness clusters relate to such associations?

The chapters on the experiences of Colombia and El Salvador offer answers to some, but not all, of these questions. Leadership by the private sector does seem to be essential for long-run success of clusters. The questions of the best mechanisms for efficiency and the best institutional structure for cluster groupings defy easy answers, though the two country experiences provide some insights into the issues.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 16

2. Colombian Experience with Promotion of Competitiveness

This chapter discusses the experience of Colombia in the promotion of competitiveness. Section 2.1 provides an overview of the country’s overall economic policy. Section 2.2 reviews Colombia’s competitiveness over time, as evidenced by its exports. Section 2.3 discusses the competitiveness promotion effort of the government and the experience of seven of the clusters promoted or supported by the government. Section 2.4 looks for evidence of changes in Colombian competitiveness during the period (1992-2002) during which these efforts have been underway. Section 2.5 offers some conclusions and observations on the Colombian experience. 2.1 The Country Economic Context

2.1.1 Background

In a broad sense, Colombian concern about competitiveness goes back to the mid-1960s. At that time, concern about declining terms of trade for the country’s major export – coffee – led to a variety of governmental efforts to develop a more diversified export base. In Latin America, Colombia pioneered three tools to promote increased exports of non-traditional products. The first was a crawling-peg exchange rate, intended to assure exporters that they would receive a constant price, in real terms for their exports. At the time, most Latin American countries maintained fixed exchange rates, punctuated by periodic crises, ending in devaluation when the country’s imbalance of payments left no alternative. Second, Colombia implemented the Plan Vallejo, a scheme to rebate import duties on imported raw materials, capital goods or intermediate goods incorporated into exported products. Its intent was to assure that exports were not disadvantaged by the country’s highly protectionist trade regime. Third, the country pioneered export subsidies, called CATS (for Certificados de Abono Tributario), that gave tax exoneration equal to 9-15% of the value of exports, maturing in a few months. These instruments were negotiable, so they functioned as a direct export subsidy. A fourth instrument, the Colombian Institute for Foreign Trade, INCOMEX, provided assistance to exporters. The first three instruments were indeed pioneering ones in Latin America, later copied by other countries. INCOMEX was not an innovation in an institutional sense, as most Latin American countries also had an export promotion agency, but INCOMEX proved more capable than most.

2.1.2 Economic Policies

Colombia’s economic policies in recent decades have maintained a consistency unusual in Latin America. Management of external debt and monetary policy has been conservative, and has helped Colombia avoid severe economic crises. During the 1980s, the country consistently maintained a positive GDP growth rate, and, at 3.5%, grew faster than any other Latin American country for the decade. In only one year (1999) during

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 17

the last four decades, was GDP growth negative. High inflation has been a consistent feature of economic management through the end of the century, but it has been held in a relatively narrow range of 15-25% per year. (Even so, this meant that prices increased more than one thousand-fold between 1963 and 2000.) This consistency was maintained in part by a large governmental role in the economy. Government ownership of infrastructure and of the country’s considerable oil production, along with government controls over foreign exchange and imports – where nearly all imports required official approval – imposed challenges to efficiency and posed a major burden on the private sector. It was due only to the relatively high quality of the government economic management bureaucracy and the relative absence of corruption that the system was able to sustain itself. The strains from the heavy hand of government gradually became evident from the mid-1970s onward, when the country’s linkages to the world economy (at least for legal exports) seemed gradually to diminish in various sectors.

2.1.3 Trade Policy Colombia’s trade policy has fluctuated over the years between protectionist and very protectionist. Export promotion has operated alongside high import tariff barriers and a system of administrative approvals. Administrative approval was finally eliminated in 1990-91, when there was also a major reduction in import tariffs. Concern about exporting has varied over time, as governments alternated between a primary concern about domestic issues and fears of isolation from the world economy. The real exchange rate has been an indicator of these concerns. Where exports were a major preoccupation, government tried to maintain a stable, competitive, real exchange rate. Where domestic concerns took precedence, as in the 1975-85 decade, or in the mid-1990s, the real rate appreciated.

2.1.4 Trade Institutions Colombia has the full range of institutions intended to promote the country’s competitiveness in world markets. Until recently, a separate ministry, the Ministry of Foreign Trade, Mincomex, was responsible for promotion of Colombia’s insertion into the world economy. Recently, that ministry was merged with the Ministry of Development, to form the Ministry of Trade, Industry and Tourism. Three other institutions are related to the ministry. Proexport, the export promotion agency, offers assistance to exporters in the forms of information, and grants for travel to trade fairs and other export development activities. Bancoldex, the export financing institution, offers credit to exporters. And Coinvertir, the mixed public-private investment promotion agency, helps companies find foreign partners.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 18

2.2 Colombian Trade Performance Between 1960 and 1985, Colombia’s exports gradually, and steadily, declined as a share of total production (see Chart 2.1). This was a time when trade was rising as a share of total production for the world as a whole, and for many developing countries. At a time when world markets offered growing opportunities for producers wanting to export to industrial country markets, Colombia was only a modest participant. Exports fell from 13.2% of GDP in 1960 to a nadir of 9% in 1983 – a figure very low for a country with Colombia’s population. It was a very closed economy. Chart 2.1

Colombian Exports of Goods and ServicesAs a Percentage of GDP

-

5

10

15

20

25

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Colombian exports have gradually diversified from the heavy dependence on coffee in the 1950s and 1960s. Chart 2.2 shows the trend in total exports (in current dollars) for four categories of product: coffee, minerals (which include petroleum, coal, ferronickel, emeralds and gold), non-coffee agriculture, and industrial products. Table 2.2 provides greater disaggregated categories. Minerals began to play an important role from 1985 on, and are partly responsible for the rise in Colombia’s export/GDP ratio. In the 1990s, other non-coffee sectors became more important. Non-coffee agriculture includes cut flowers, which have grown steadily and consistently since the 1970s; bananas, which stagnated after 1990, following two decades of rapid growth; and other products, which have shown little trend. Industrial products have had widely varying trends. Textiles and clothing exports have shown several periods of sharply rising exports, followed by periods of steady decline. Exports in 2002 were lower than in 1993. Leather and leather products rose steadily, also until 1993, and

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 19

then fell steadily. Chemicals, and other manufactures (which includes a variety of smaller export categories) have grown more rapidly and consistently. Considering the 1980-2002 period, only two categories from Table 2.1 grew at double-digit rates in current dollars: minerals and chemicals. Both of these sectors use very capital-intensive technologies, and the former is very dependent on natural resources. Neither sector generates very much employment. (Over the 1991-2000 period, employment in mining, chemicals, and petroleum refining rose by 188,000, while the number of people in the 15-60 age group rose by 4.2 million.) Chart 2.2

Of the other non-traditional, non-mineral categories shown in Table 2.1, only flowers have shown a consistent growth performance. Textiles and clothing show cyclical tendencies probably related to changes in the real exchange rate. Leather and leather products show a consistent rise until 1991, when a gradual and steady decline began.

Colombian Exports, 1970-2002

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002Year

Coffee Minerals Other Agriculture Industrial

Million Dollars

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 20

Table 2.1 Colombian Exports, 1970-2002

Million US Dollars

Year Total Coffee Minerals Bananas Flowers

Other Agri-

culture

Textiles and

Clothing Chemicals

Leather and

Leather Products

Other Manu-

factures1970 736 467 93 - - 51 51 8 7 58 1971 690 395 85 - - 57 54 14 9 76 1972 866 430 123 - - 75 91 21 21 105 1973 1,177 597 162 - - 96 115 37 30 141 1974 1,417 622 151 - 16 146 145 76 23 237 1975 1,469 672 121 - 19 233 94 60 21 248 1976 1,745 967 87 - 22 236 129 53 25 225 1977 2,434 1,498 117 - 33 297 126 55 35 275 1978 3,018 1,979 143 - 48 278 144 60 38 328 1979 3,234 2,005 141 - 68 272 208 73 43 424 1980 3,917 2,361 184 94 97 237 236 98 36 573 1981 2,925 1,423 118 122 109 256 205 95 47 551 1982 3,067 1,562 276 151 111 158 197 97 60 456 1983 3,033 1,506 537 148 121 114 111 106 35 354 1984 3,404 1,765 617 198 130 136 100 108 31 320 1985 3,496 1,746 673 156 132 147 108 130 55 350 1986 5,060 2,988 767 200 149 139 150 142 77 448 1987 4,915 1,651 1,784 210 145 164 196 191 98 476 1988 4,965 1,641 1,563 252 190 184 287 214 116 517 1989 5,711 1,524 2,155 260 221 200 425 201 134 590 1990 6,721 1,415 2,774 318 229 271 572 235 171 736 1991 7,114 1,336 2,403 405 280 419 762 345 243 921 1992 6,900 1,259 2,274 407 340 349 633 390 208 1,040 1993 7,116 1,140 2,421 425 379 258 732 441 242 1,077 1994 8,816 1,990 2,776 490 426 323 731 549 224 1,307 1995 10,298 1,832 3,732 429 476 322 845 829 203 1,630 1996 10,672 1,578 4,429 459 510 264 761 895 136 1,640 1997 11,555 2,261 4,023 503 545 260 729 1,093 129 2,013 1998 10,890 1,893 3,546 483 556 310 676 1,117 135 2,174 1999 11,576 1,324 4,998 560 550 269 642 1,196 125 1,912 2000 13,121 1,069 5,980 481 581 288 769 1,360 173 2,419 2001 12,309 764 4,841 408 610 348 825 1,399 181 2,934 2002 11,908 772 4,799 441 673 270 736 1,361 153 2,704

Source: Banco de la Republica

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 21

2.3 The Colombian Competitiveness Effort

2.3.1 Initial Efforts to Promote Competitiveness As stated earlier, Colombia had long had a set of government institutions aimed at promoting competitiveness in a broad sense, as export promotion and industrial development policy. The effort to promote clusters, or competitiveness in the Michael Porter sense, is more recent, beginning in about 1992. A competitiveness consulting firm, The Monitor Company8, was hired by the Colombian government’s industry-promotion agency, the Instituto de Fomento Industrial (IFI), to study Colombia’s competitive situation, and its major problems, and to make recommendations for government action. The initial Monitor findings were discussed at a well-attended conference in 1993. The Monitor work identified a number of specific ideas, based on the Porter diamond, to increase Colombian competitiveness, such as gaining greater knowledge of the needs of buyers, and seeking to move into more profitable market niches. The work also identified cultural attitudes – “mental models,” in Monitor’s terms – that were seen as limiting the ability of Colombian firms to become more productive. According to Monitor, some firms viewed the different actors in the production chain for their product as competitors in a zero-sum game rather than collaborators. Thus, leather tanners and leather manufacturers, or sugar cane growers and processors, would see themselves at war with the other party over prices, each trying to use any economic or political resources at its disposal to shift bargaining power to its side.9 Following the initial work, Monitor was hired by the petrochemical and plastics association, Acoplasticos, to do an analysis of the competitive situation of the firms in that association. Subsequently, Monitor assisted several other industry associations, including leather, and textiles and apparel to form cluster groupings. The Monitor work with sector clusters generated interest by municipal governments in several cities on applying these concepts, and Monitor subsequently helped the governments of the five major cities (or their departmental governments) to formulate strategies for regional competitiveness. This work was co-financed by the local or regional governments and the Corporación Andino de Fomento (CAF). At the national level, interest in clusters continued after a change in government in 1994. The government also implemented Monitor’s recommendation that the government establish a national competitiveness council to oversee the process of increasing the country’s competitiveness. The council, the Consejo Nacional de Competitividad, established in 1995, was chaired by the president, and included nineteen other people appointed by the president: six government representatives (mostly ministers

8 This is a Cambridge, Massachusetts firm associated with Michael Porter, and headed by Michael Fairbanks. 9 The Monitor experience in Colombia provided much of the material for the 1997 book, Plowing the Sea, by Fairbanks and Lindsay.

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 22

responsible for economic sectors), seven representatives from the business sector, and three each from labor unions and academic institutions. The government’s national planning department provided secretariat functions, though apparently without additional budgetary resources to fulfill this mandate. The council was mandated to oversee five programs (Martínez, 1997, p. 135): the national policy for science and technology, the strategic exporting plan, the policy for modernization of agriculture and the rural sector, the policy for modernization of industry, and the strategy for infrastructure for competitiveness. As these mandates indicate, the council was a vehicle for implementing the programs of one administration, rather than a non-political forum for trying to address national problems of inefficiency and low productivity. It died with the arrival of a new government, and promotion of competitiveness was transferred to the ministry of foreign trade. Three sectoral competitiveness agreements were signed between the government and the private sector (and with labor unions in two cases), during the 1994-1998 period. These were for textiles and clothing, metalworking and capital goods and pulp-paper-printing. The signers of the agreements for the business sector were business associations, not individual firms. The national competitiveness council seems to have viewed its function in promoting competitiveness more in line with traditional ideas from Latin America – sectoral planning, subsidies and bailouts – than in the Porterite view that competitiveness should depend on firm-level productivity, and not on government subsidies. For example, a 1998 assessment of the sectoral competitiveness agreement on textiles and clothing calls for joint planning by Colciencias, the government’s scientific institution, the national planning office and business firms to jointly coordinate plans to upgrade the technology of the sector (DNP 1988). The government investment promotion organization, IFI, was expected to provide financing to reduce the liabilities of firms in the sector, and the social security institute is directed to adjust the pension contributions of firms in the sector to their capacity to pay (see DNP 1987). In general, the approach was to back away from the “sudden and indiscriminate” economic liberalization of the previous administration, and undertake a “gradual and selective” move in the same direction (Martínez, 1997, p. 116). Thus, it was a partial return to the more traditional Latin American view that government policy as arbiter of the fortunes of individual economic sectors. This approach produced few concrete results in competitiveness, and, as discussed earlier, the appreciation of the exchange rate during the early 1990s reduced the profitability of exporting. The Samper government did, however, establish a network of centers for productivity and technology at the sectoral level. These centers have continued to work to support dissemination of new technologies. Overall, however, the national competitiveness council lacked consistent interest from the highest levels of government or strong support from the private sector, and had no lasting impact. In 1998, another change in government brought an increased attention to external competitiveness, and greater focus on clusters as a tool for productivity increases. As noted above, the functions of the national competitiveness council were transferred to the

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 23

Ministry of Foreign Trade (Mincomex), with created structures to promote export growth, cluster development, and regional export strategies.

2.3.2 Current Programs The overall competitiveness effort is managed by the Ministry of Commerce, Industry and Tourism. This ministry is a recent amalgamation of Mincomex, which previously managed the competitiveness effort, and the Ministry of Economic Development, which was concerned with domestic economic promotion. The competitiveness unit in the Ministry has a professional staff of 17 people to manage the various elements of the competitiveness strategy. The head of the competitiveness unit continued in the same position through a change in government, clearly signaling that the competitiveness effort transcended programs of individual administrations.

The program is called the Red Colombia Compite, or Colombian Competitiveness Network, and is organized into four main elements: national conferences, competitiveness agreements, regional competitiveness committees, and specialized networks. Each is described below.

2.3.2.1 Encuentros Nacionales de Productividad y Competitividad These national conferences on productivity and competitiveness have been held semi-annually for the past four years, and bring together the President, ministers and a large number of leaders from the private sector. About 1,000 people typically participate in the meetings. The structure and activities of the most recent meeting, in May 2003, are described in Box 1. In effect, the Encuentros have replaced a national competitiveness council as the principal forum for interaction between the government and the business sector. The broad-based character of the meetings and the fact that they have continued from one governmental administration to another suggest real value. Indeed, it could be viewed an important “democratization” of the effort from a council where all of the members are appointed by the president. Both government and private-sector leaders give considerable credit to the Encuentros as a tool for achieving better understanding between government and the private sector. Both regard the Encuentros as very important for promoting action on competitiveness. Many in the private sector see them as the most important vehicle for demonstrating government commitment to exports and competitiveness. There is no formal or unambiguous set of commitments against which progress can be measured

Report on Competitiveness Promotion In Colombia & El Salvador Final Report

The Louis Berger Group, Inc. 24