Ch1. Ü Ì É · 3 4 1Ñ, P˘ Ch1. ܘô’Ì—É 2019 ... 3 {e t}haveconstantvariance. 4 {e...

152

Ch1. ˜— 1, P Y Q'˜Yü 2019-09-06 1, P Ch1. ˜— 2019-09-06 1 / 48

Transcript of Ch1. Ü Ì É · 3 4 1Ñ, P˘ Ch1. ܘô’Ì—É 2019 ... 3 {e t}haveconstantvariance. 4 {e...

Ch1. 시계열자료탐색

성병찬 교수

중앙대 응용통계학과

2019-09-06

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 1 / 48

Outline1 What can we forecast?

2 Time series data

3 The statistical forecasting perspective

4 Time plots

5 Seasonal plots

6 Lag plots and autocorrelation

7 White noise

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 2 / 48

What can we forecast?

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 3 / 48

What can we forecast?

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 4 / 48

What can we forecast?

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 5 / 48

What can we forecast?

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 6 / 48

What can we forecast?

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 7 / 48

What can we forecast?

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 8 / 48

What can we forecast?

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 9 / 48

Which is easiest to forecast?1 daily electricity demand in 3 days time2 timing of next Halley’s comet appearance3 time of sunrise this day next year4 Google stock price tomorrow5 Google stock price in 6 months time6 maximum temperature tomorrow7 exchange rate of $US/AUS next week8 total sales of drugs in Australian pharmacies next

monthhow do we measure “easiest”?what makes something easy/difficult to forecast?

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 10 / 48

Factors affecting forecastability

Something is easier to forecast if:we have a good understanding of the factors thatcontribute to itthere is lots of data available;the forecasts cannot affect the thing we are trying toforecast.there is relatively low natural/unexplainable randomvariation.the future is somewhat similar to the past

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 11 / 48

Outline1 What can we forecast?

2 Time series data

3 The statistical forecasting perspective

4 Time plots

5 Seasonal plots

6 Lag plots and autocorrelation

7 White noise

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 12 / 48

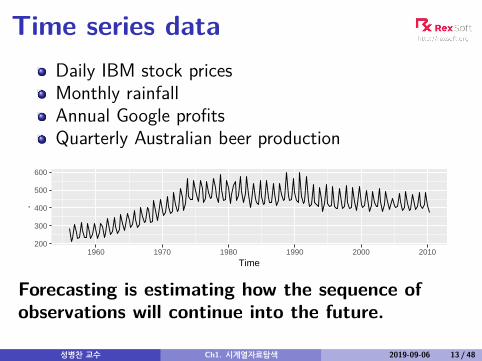

Time series dataDaily IBM stock pricesMonthly rainfallAnnual Google profitsQuarterly Australian beer production

200

300

400

500

600

1960 1970 1980 1990 2000 2010

Time

.

Forecasting is estimating how the sequence ofobservations will continue into the future.

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 13 / 48

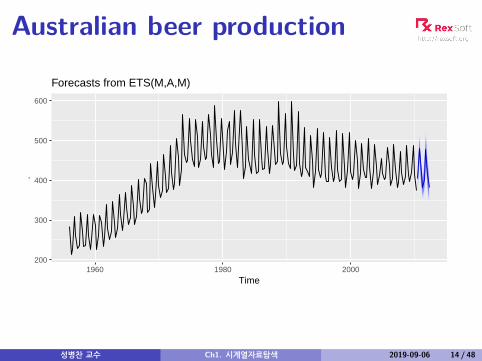

Australian beer production

200

300

400

500

600

1960 1980 2000

Time

.

Forecasts from ETS(M,A,M)

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 14 / 48

Australian beer production

350

400

450

500

1995 2000 2005 2010

Time

.

Forecasts from ETS(M,A,M)

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 15 / 48

Outline1 What can we forecast?

2 Time series data

3 The statistical forecasting perspective

4 Time plots

5 Seasonal plots

6 Lag plots and autocorrelation

7 White noise

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 16 / 48

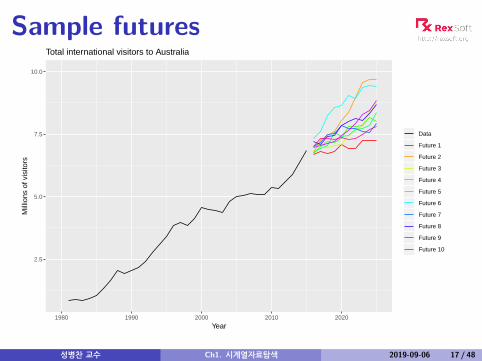

Sample futures

2.5

5.0

7.5

10.0

1980 1990 2000 2010 2020

Year

Mill

ions

of v

isito

rs

Data

Future 1

Future 2

Future 3

Future 4

Future 5

Future 6

Future 7

Future 8

Future 9

Future 10

Total international visitors to Australia

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 17 / 48

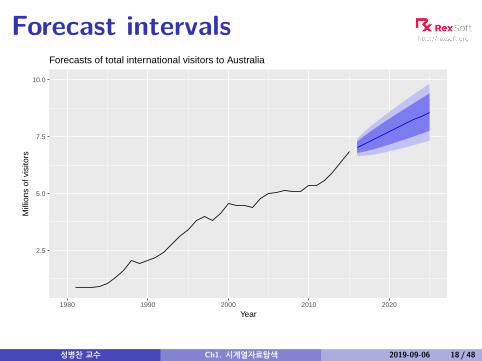

Forecast intervals

2.5

5.0

7.5

10.0

1980 1990 2000 2010 2020

Year

Mill

ions

of v

isito

rs

Forecasts of total international visitors to Australia

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 18 / 48

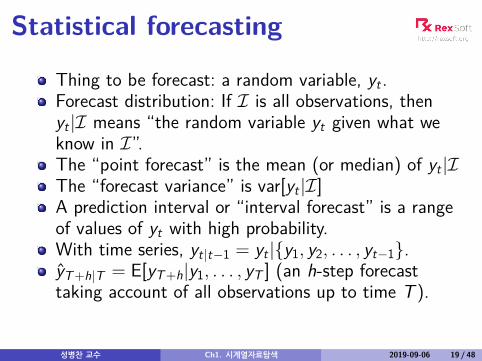

Statistical forecasting

Thing to be forecast: a random variable, yt .Forecast distribution: If I is all observations, thenyt |I means “the random variable yt given what weknow in I”.The “point forecast” is the mean (or median) of yt |IThe “forecast variance” is var[yt |I]A prediction interval or “interval forecast” is a rangeof values of yt with high probability.With time series, yt|t−1 = yt |{y1, y2, . . . , yt−1}.yT+h|T = E[yT+h|y1, . . . , yT ] (an h-step forecasttaking account of all observations up to time T ).

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 19 / 48

Outline1 What can we forecast?

2 Time series data

3 The statistical forecasting perspective

4 Time plots

5 Seasonal plots

6 Lag plots and autocorrelation

7 White noise

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 20 / 48

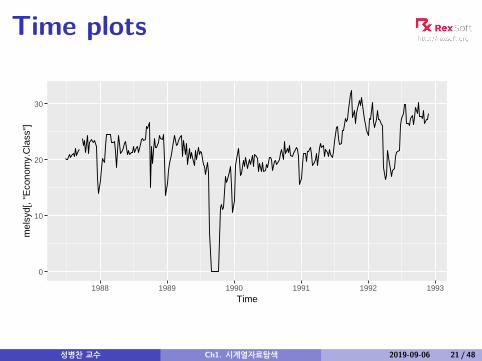

Time plots

0

10

20

30

1988 1989 1990 1991 1992 1993

Time

mel

syd[

, "E

cono

my.

Cla

ss"]

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 21 / 48

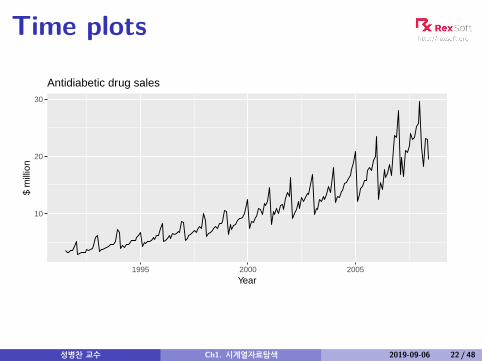

Time plots

10

20

30

1995 2000 2005

Year

$ m

illio

n

Antidiabetic drug sales

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 22 / 48

Outline1 What can we forecast?

2 Time series data

3 The statistical forecasting perspective

4 Time plots

5 Seasonal plots

6 Lag plots and autocorrelation

7 White noise

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 23 / 48

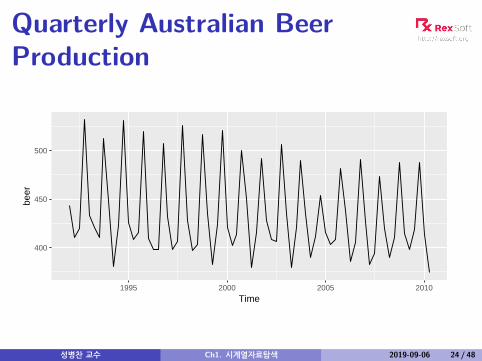

Quarterly Australian BeerProduction

400

450

500

1995 2000 2005 2010

Time

beer

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 24 / 48

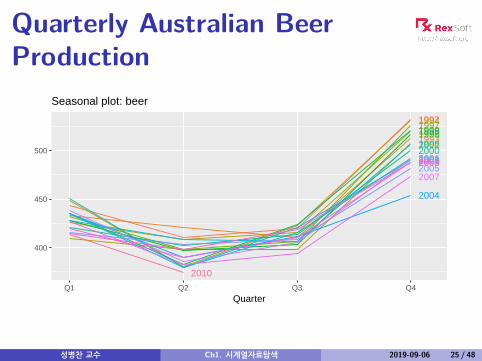

Quarterly Australian BeerProduction

1992

1993

199419951996

199719981999

200020012002

2003

2004

20052006

2007

20082009

2010

400

450

500

Q1 Q2 Q3 Q4

Quarter

Seasonal plot: beer

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 25 / 48

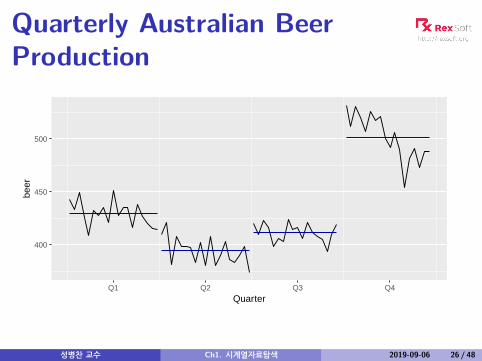

Quarterly Australian BeerProduction

400

450

500

Q1 Q2 Q3 Q4

Quarter

beer

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 26 / 48

Outline1 What can we forecast?

2 Time series data

3 The statistical forecasting perspective

4 Time plots

5 Seasonal plots

6 Lag plots and autocorrelation

7 White noise

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 27 / 48

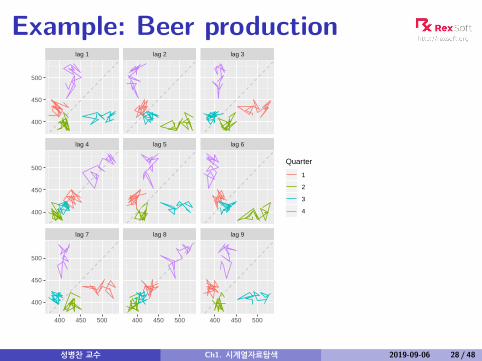

Example: Beer production

lag 7 lag 8 lag 9

lag 4 lag 5 lag 6

lag 1 lag 2 lag 3

400 450 500 400 450 500 400 450 500

400

450

500

400

450

500

400

450

500

Quarter

1

2

3

4

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 28 / 48

Lagged scatterplots

Each graph shows yt plotted against yt−k fordifferent values of k .The autocorrelations are the correlations associatedwith these scatterplots.

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 29 / 48

Autocorrelation

Covariance and correlation: measure extent of linearrelationship between two variables (y and X ).Autocovariance and autocorrelation: measure linearrelationship between lagged values of a time series y .

We measure the relationship between:yt and yt−1, yt and yt−2, yt and yt−3, etc.

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 30 / 48

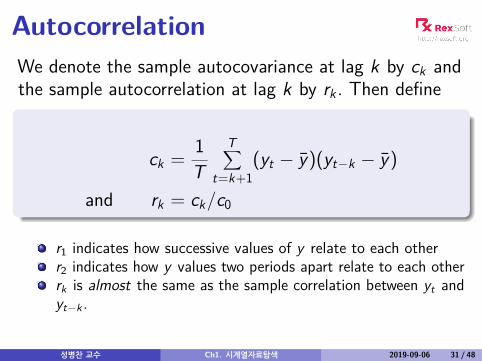

AutocorrelationWe denote the sample autocovariance at lag k by ck andthe sample autocorrelation at lag k by rk . Then define

ck = 1T

T∑t=k+1

(yt − y)(yt−k − y)

and rk = ck/c0

r1 indicates how successive values of y relate to each otherr2 indicates how y values two periods apart relate to each otherrk is almost the same as the sample correlation between yt andyt−k .

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 31 / 48

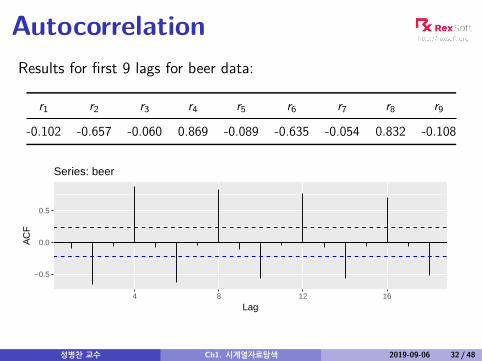

AutocorrelationResults for first 9 lags for beer data:

r1 r2 r3 r4 r5 r6 r7 r8 r9

-0.102 -0.657 -0.060 0.869 -0.089 -0.635 -0.054 0.832 -0.108

−0.5

0.0

0.5

4 8 12 16

Lag

AC

F

Series: beer

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 32 / 48

Autocorrelation

r4 higher than for the other lags. This is due to theseasonal pattern in the data: the peaks tend tobe 4 quarters apart and the troughs tend to be 2quarters apart.r2 is more negative than for the other lags becausetroughs tend to be 2 quarters behind peaks.Together, the autocorrelations at lags 1, 2, . . . , makeup the autocorrelation or ACF.The plot is known as a correlogram

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 33 / 48

ACF

−0.5

0.0

0.5

4 8 12 16

Lag

AC

F

Series: beer

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 34 / 48

Trend and seasonality in ACF plots

When data have a trend, the autocorrelations forsmall lags tend to be large and positive and slowlydecrease as the lags increase.When data are seasonal, the autocorrelations will belarger at the seasonal lags (i.e., at multiples of theseasonal frequency)When data are trended and seasonal, you see acombination of these effects.

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 35 / 48

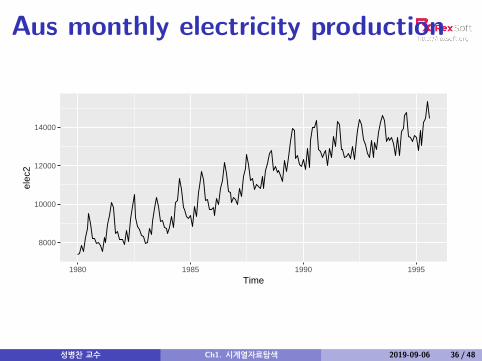

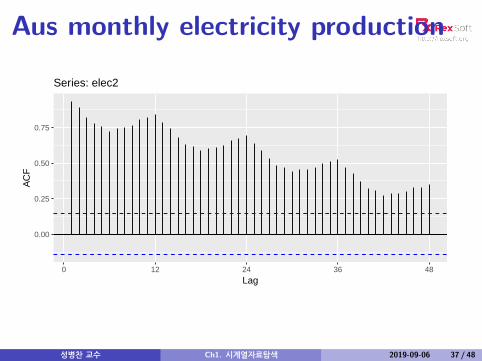

Aus monthly electricity production

8000

10000

12000

14000

1980 1985 1990 1995

Time

elec

2

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 36 / 48

Aus monthly electricity production

0.00

0.25

0.50

0.75

0 12 24 36 48

Lag

AC

F

Series: elec2

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 37 / 48

Aus monthly electricity production

Time plot shows clear trend and seasonality.The same features are reflected in the ACF.

The slowly decaying ACF indicates trend.The ACF peaks at lags 12, 24, 36, . . . , indicateseasonality of length 12.

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 38 / 48

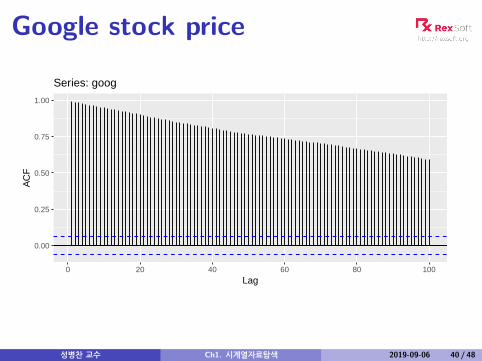

Google stock price

400

500

600

700

800

0 200 400 600 800 1000

Time

goog

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 39 / 48

Google stock price

0.00

0.25

0.50

0.75

1.00

0 20 40 60 80 100

Lag

AC

F

Series: goog

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 40 / 48

Outline1 What can we forecast?

2 Time series data

3 The statistical forecasting perspective

4 Time plots

5 Seasonal plots

6 Lag plots and autocorrelation

7 White noise

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 41 / 48

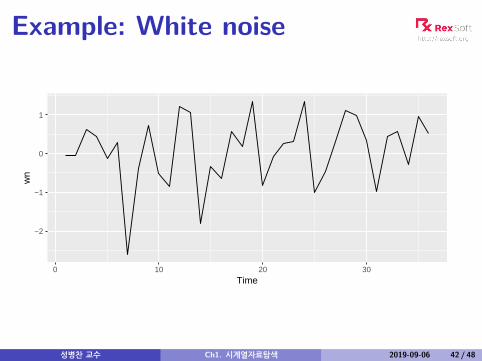

Example: White noise

−2

−1

0

1

0 10 20 30

Time

wn

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 42 / 48

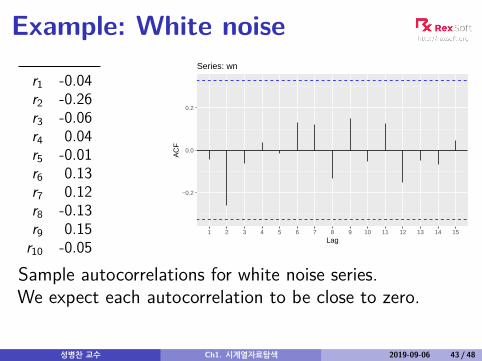

Example: White noise

r1 -0.04r2 -0.26r3 -0.06r4 0.04r5 -0.01r6 0.13r7 0.12r8 -0.13r9 0.15

r10 -0.05

Sample autocorrelations for white noise series.We expect each autocorrelation to be close to zero.

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 43 / 48

−0.2

0.0

0.2

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15Lag

AC

F

Series: wn

Sampling distribution of autocorrelations

Sampling distribution of rk for white noise data isasymptotically N(0,1/T ).

95% of all rk for white noise must lie within±1.96/

√T .

If this is not the case, the series is probably not WN.Common to plot lines at ±1.96/

√T when plotting

ACF. These are the {critical values}.

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 44 / 48

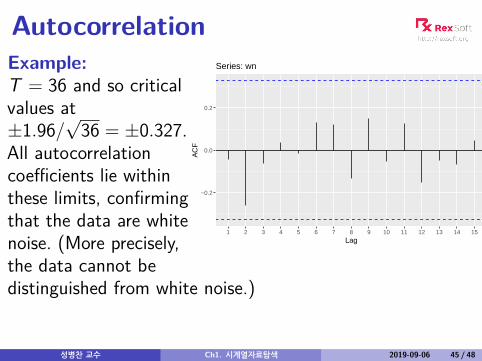

Autocorrelation

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 45 / 48

−0.2

0.0

0.2

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15Lag

AC

F

Series: wnExample:T = 36 and so criticalvalues at±1.96/

√36 = ±0.327.

All autocorrelationcoefficients lie withinthese limits, confirmingthat the data are whitenoise. (More precisely,the data cannot bedistinguished from white noise.)

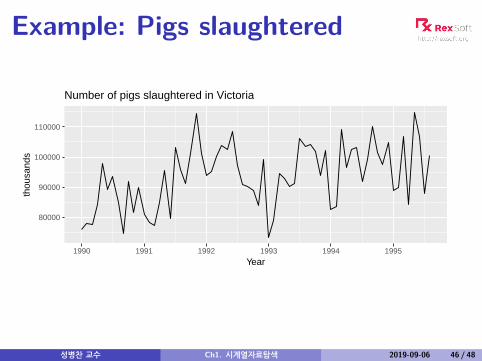

Example: Pigs slaughtered

80000

90000

100000

110000

1990 1991 1992 1993 1994 1995

Year

thou

sand

s

Number of pigs slaughtered in Victoria

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 46 / 48

Example: Pigs slaughtered

−0.2

0.0

0.2

12 246 18

Lag

AC

F

Series: pigs2

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 47 / 48

Example: Pigs slaughtered

Monthly total number of pigs slaughtered in the state ofVictoria, Australia, from January 1990 through August1995. (Source: Australian Bureau of Statistics.)

Difficult to detect pattern in time plot.ACF shows some significant autocorrelation at lags 1,2, and 3.r12 relatively large although not significant. This mayindicate some slight seasonality.

These show the series is not a white noise series.

성병찬 교수 Ch1. 시계열자료탐색 2019-09-06 48 / 48

Ch1-부록. 시계열자료탐색

성병찬 교수

중앙대 응용통계학과

2019-09-06

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 1 / 26

Outline

1 Box-Cox transformations

2 Residual diagnostics

3 Evaluating forecast accuracy

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 2 / 26

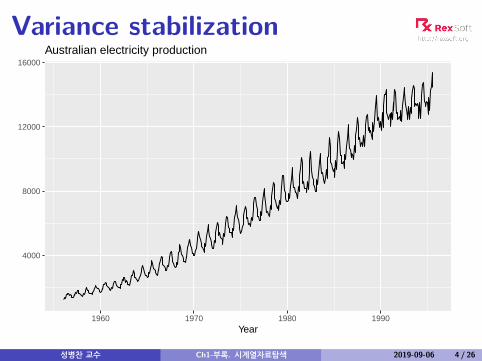

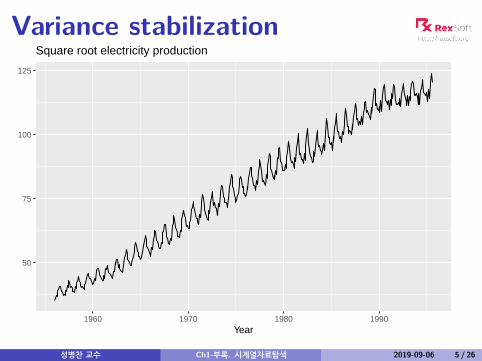

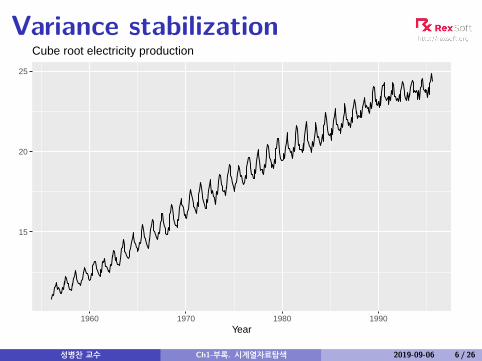

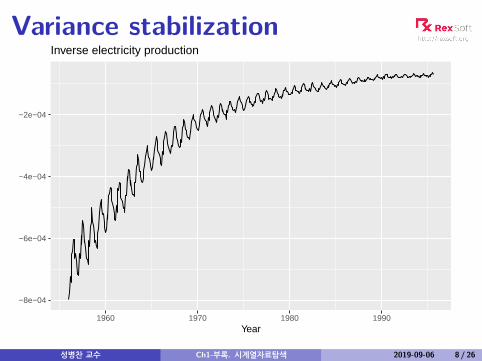

Variance stabilizationIf the data show different variation at different levels of theseries, then a transformation can be useful.Denote original observations as y1, . . . , yn and transformedobservations as w1, . . . ,wn.Mathematical transformations for stabilizing variation

Square root wt = √yt ↓Cube root wt = 3

√yt IncreasingLogarithm wt = log(yt) strength

Logarithms, in particular, are useful because they are moreinterpretable: changes in a log value are relative (percent)changes on the original scale.

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 3 / 26

Variance stabilization

4000

8000

12000

16000

1960 1970 1980 1990Year

Australian electricity production

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 4 / 26

Variance stabilization

50

75

100

125

1960 1970 1980 1990Year

Square root electricity production

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 5 / 26

Variance stabilization

15

20

25

1960 1970 1980 1990Year

Cube root electricity production

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 6 / 26

Variance stabilization

8

9

1960 1970 1980 1990Year

Log electricity production

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 7 / 26

Variance stabilization

−8e−04

−6e−04

−4e−04

−2e−04

1960 1970 1980 1990Year

Inverse electricity production

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 8 / 26

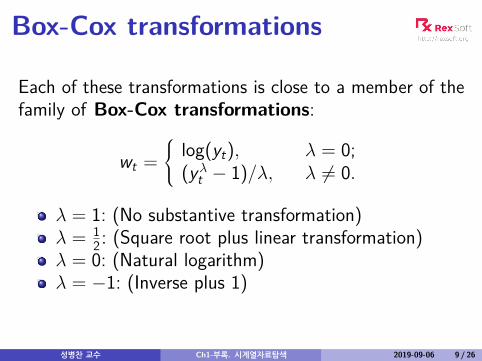

Box-Cox transformations

Each of these transformations is close to a member of thefamily of Box-Cox transformations:

wt = log(yt), λ = 0;

(yλt − 1)/λ, λ 6= 0.

λ = 1: (No substantive transformation)λ = 1

2 : (Square root plus linear transformation)λ = 0: (Natural logarithm)λ = −1: (Inverse plus 1)

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 9 / 26

Outline

1 Box-Cox transformations

2 Residual diagnostics

3 Evaluating forecast accuracy

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 10 / 26

Fitted values

yt|t−1 is the forecast of yt based on observationsy1, . . . , yt .We call these “fitted values”.Sometimes drop the subscript: yt ≡ yt|t−1.Often not true forecasts since parameters areestimated on all data.

For example:yt = y for average method.yt = yt−1 + (yT − y1)/(T − 1) for drift method.

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 11 / 26

Forecasting residuals

Residuals in forecasting: difference between observedvalue and its fitted value: et = yt − yt|t−1.

Assumptions1 {et} uncorrelated. If they aren’t, then information left in

residuals that should be used in computing forecasts.2 {et} have mean zero. If they don’t, then forecasts are

biased.Useful properties (for prediction intervals)

3 {et} have constant variance.4 {et} are normally distributed.

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 12 / 26

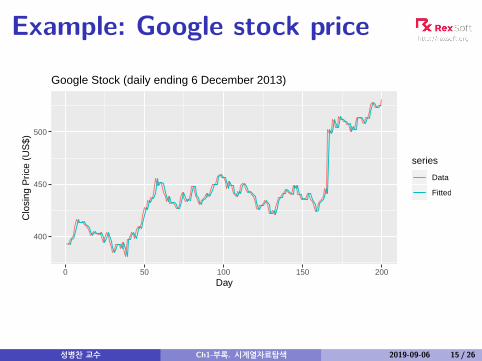

Example: Google stock price

400

450

500

0 50 100 150 200Day

Clo

sing

Pric

e (U

S$)

Google Stock (daily ending 6 December 2013)

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 13 / 26

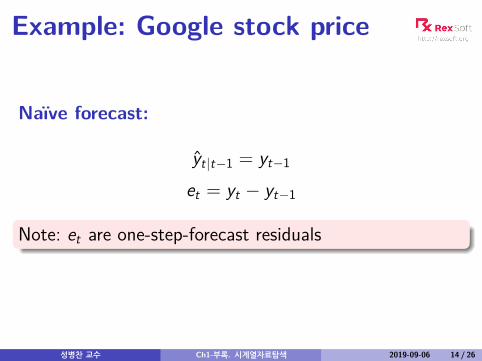

Example: Google stock price

Naïve forecast:

yt|t−1 = yt−1

et = yt − yt−1

Note: et are one-step-forecast residuals

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 14 / 26

Example: Google stock price

400

450

500

0 50 100 150 200Day

Clo

sing

Pric

e (U

S$)

series

Data

Fitted

Google Stock (daily ending 6 December 2013)

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 15 / 26

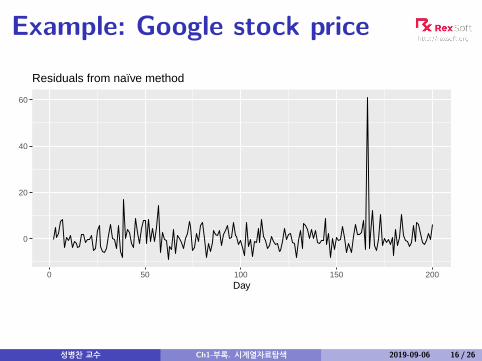

Example: Google stock price

0

20

40

60

0 50 100 150 200Day

Residuals from naïve method

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 16 / 26

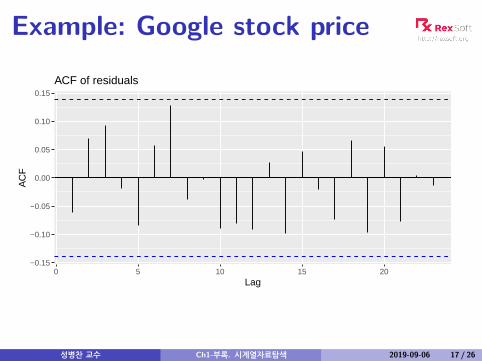

Example: Google stock price

−0.15

−0.10

−0.05

0.00

0.05

0.10

0.15

0 5 10 15 20Lag

AC

F

ACF of residuals

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 17 / 26

ACF of residuals

We assume that the residuals are white noise(uncorrelated, mean zero, constant variance). If theyaren’t, then there is information left in the residualsthat should be used in computing forecasts.So a standard residual diagnostic is to check the ACFof the residuals of a forecasting method.We expect these to look like white noise.

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 18 / 26

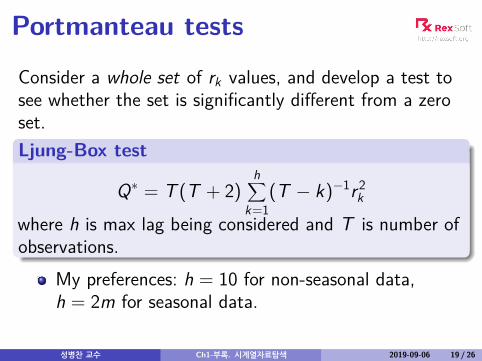

Portmanteau tests

Consider a whole set of rk values, and develop a test tosee whether the set is significantly different from a zeroset.Ljung-Box test

Q∗ = T (T + 2)h∑

k=1(T − k)−1r 2

k

where h is max lag being considered and T is number ofobservations.

My preferences: h = 10 for non-seasonal data,h = 2m for seasonal data.

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 19 / 26

Portmanteau tests

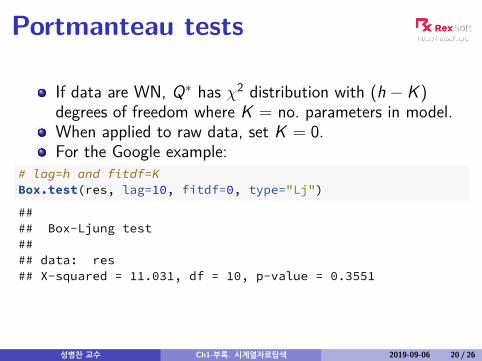

If data are WN, Q∗ has χ2 distribution with (h − K )degrees of freedom where K = no. parameters in model.When applied to raw data, set K = 0.For the Google example:

# lag=h and fitdf=KBox.test(res, lag=10, fitdf=0, type="Lj")

#### Box-Ljung test#### data: res## X-squared = 11.031, df = 10, p-value = 0.3551

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 20 / 26

Outline

1 Box-Cox transformations

2 Residual diagnostics

3 Evaluating forecast accuracy

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 21 / 26

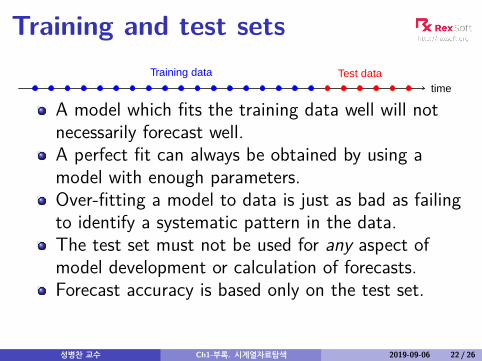

Training and test sets

time

Training data Test data

A model which fits the training data well will notnecessarily forecast well.A perfect fit can always be obtained by using amodel with enough parameters.Over-fitting a model to data is just as bad as failingto identify a systematic pattern in the data.The test set must not be used for any aspect ofmodel development or calculation of forecasts.Forecast accuracy is based only on the test set.

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 22 / 26

Forecast errors

Forecast “error”: the difference between an observed valueand its forecast.

eT+h = yT+h − yT+h|T ,

where the training data is given by {y1, . . . , yT}Unlike residuals, forecast errors on the test setinvolve multi-step forecasts.These are true forecast errors as the test data is notused in computing yT+h|T .

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 23 / 26

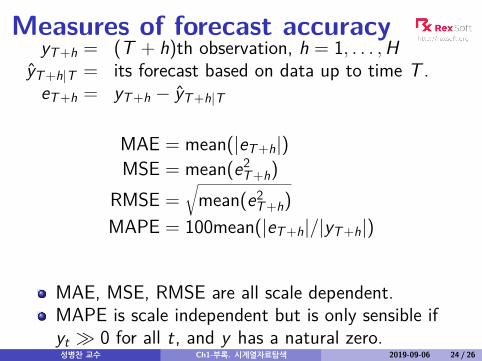

Measures of forecast accuracyyT+h = (T + h)th observation, h = 1, . . . ,H

yT+h|T = its forecast based on data up to time T .eT+h = yT+h − yT+h|T

MAE = mean(|eT+h|)MSE = mean(e2

T+h)RMSE =

√mean(e2

T+h)MAPE = 100mean(|eT+h|/|yT+h|)

MAE, MSE, RMSE are all scale dependent.MAPE is scale independent but is only sensible ifyt � 0 for all t, and y has a natural zero.성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 24 / 26

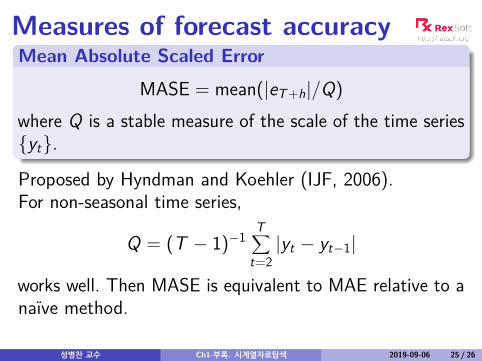

Measures of forecast accuracyMean Absolute Scaled Error

MASE = mean(|eT+h|/Q)where Q is a stable measure of the scale of the time series{yt}.

Proposed by Hyndman and Koehler (IJF, 2006).For non-seasonal time series,

Q = (T − 1)−1T∑

t=2|yt − yt−1|

works well. Then MASE is equivalent to MAE relative to anaïve method.

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 25 / 26

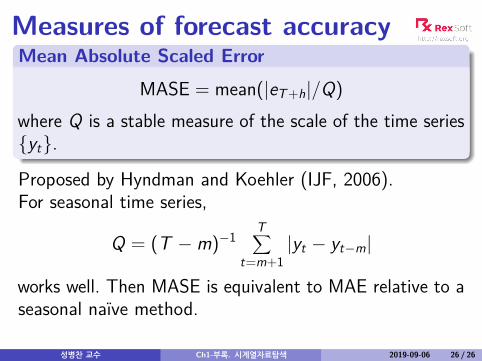

Measures of forecast accuracyMean Absolute Scaled Error

MASE = mean(|eT+h|/Q)where Q is a stable measure of the scale of the time series{yt}.

Proposed by Hyndman and Koehler (IJF, 2006).For seasonal time series,

Q = (T −m)−1T∑

t=m+1|yt − yt−m|

works well. Then MASE is equivalent to MAE relative to aseasonal naïve method.

성병찬 교수 Ch1-부록. 시계열자료탐색 2019-09-06 26 / 26

1장-실습

1) beer.xlsx 자료를 이용하여 엑셀로 시계열 그래프를 그리시오. 또한 REX의 [시계열자료 탐색] 메뉴

를 사용하여, 시계열 그래프와 ACF 그래프, 계절별 그래프, 지연 시차 그래프를 그리시오.

2) elec2.xlsx 자료를 이용하여 REX의 [시계열자료 탐색] 메뉴를 사용하여 분석하고 시계열 자료의 특

성을 파악하시오. 단, 계절=12로 설정하고 [출력옵션]을 사용하시오.

3) 엑셀의 =rand() 함수를 이용하여 100개의 시계열 자료(series1)를 생성하시오.

4) series1을 이용하여 임의보행(random walk) 시계열 자료(series2)를 생성하시오.

참고: 임의보행이란? 1t t ty y −= +

5) REX의 [시계열자료 탐색] 메뉴를 사용하여, series1과 series2의 시계열 그래프, ACF 그래프, 지연 시

차 그래프를 그리시오.

Ch2. ARIMA 분석

성병찬 교수

중앙대 응용통계학과

2019-09-06

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 1 / 54

Outline

1 Stationarity and differencing

2 Non-seasonal ARIMA models

3 Order selection

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 2 / 54

Stationarity

DefinitionIf {yt} is a stationary time series, then for all s, thedistribution of (yt , . . . , yt+s) does not depend on t.

A stationary series is:roughly horizontalconstant varianceno patterns predictable in the long-term

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 3 / 54

Stationary?

3600

3700

3800

3900

4000

0 50 100 150 200 250 300Day

Dow

Jon

es In

dex

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 4 / 54

Stationary?

−100

−50

0

50

0 50 100 150 200 250 300Day

Cha

nge

in D

ow J

ones

Inde

x

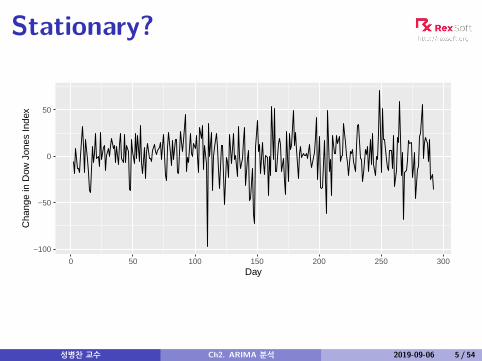

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 5 / 54

Stationary?

4000

5000

6000

1950 1955 1960 1965 1970 1975 1980Year

Num

ber

of s

trik

es

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 6 / 54

Stationary?

40

60

80

1975 1980 1985 1990 1995Year

Tota

l sal

es

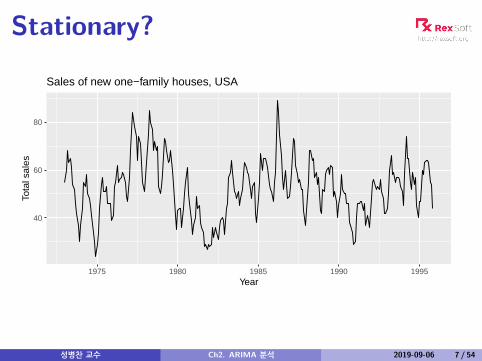

Sales of new one−family houses, USA

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 7 / 54

Stationary?

100

200

300

1900 1920 1940 1960 1980Year

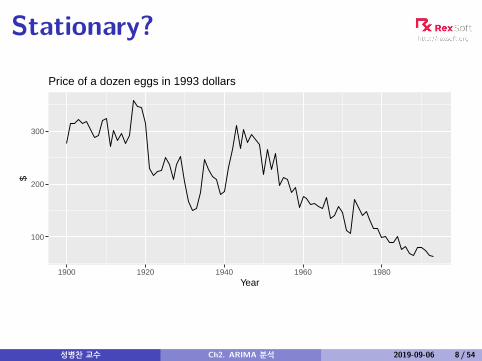

$

Price of a dozen eggs in 1993 dollars

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 8 / 54

Stationary?

80

90

100

110

1990 1991 1992 1993 1994 1995Year

thou

sand

s

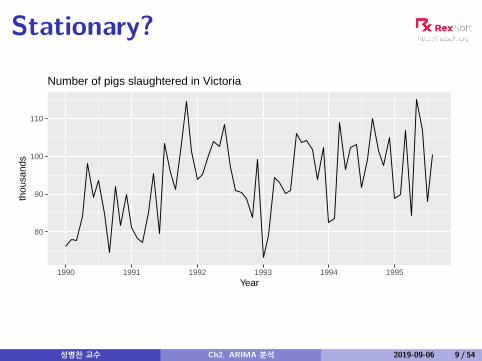

Number of pigs slaughtered in Victoria

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 9 / 54

Stationary?

0

2000

4000

6000

1820 1840 1860 1880 1900 1920Year

Num

ber

trap

ped

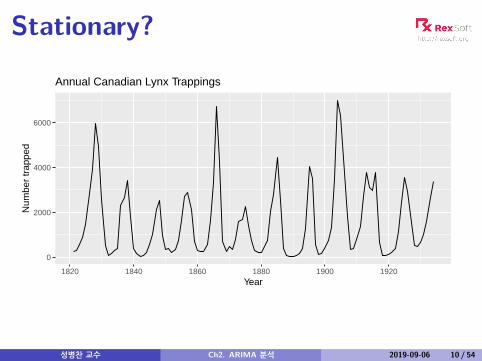

Annual Canadian Lynx Trappings

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 10 / 54

Stationary?

400

450

500

1995 2000 2005 2010Year

meg

alitr

es

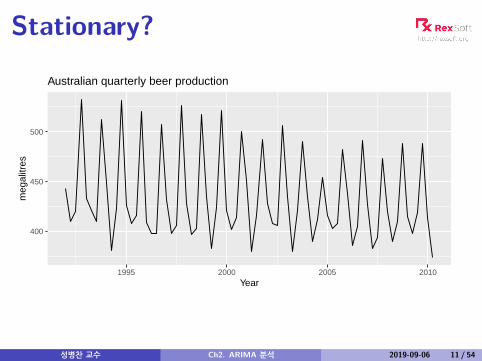

Australian quarterly beer production

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 11 / 54

Stationarity

DefinitionIf {yt} is a stationary time series, then for all s, thedistribution of (yt , . . . , yt+s) does not depend on t.

Transformations help to stabilize the variance.For ARIMA modelling, we also need to stabilize themean.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 12 / 54

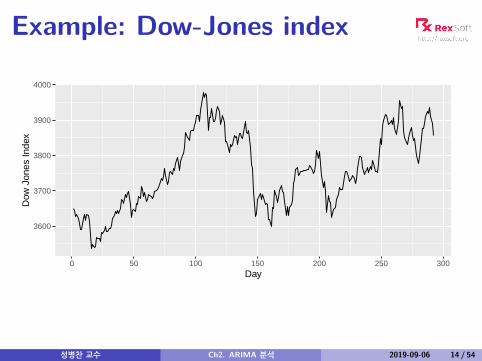

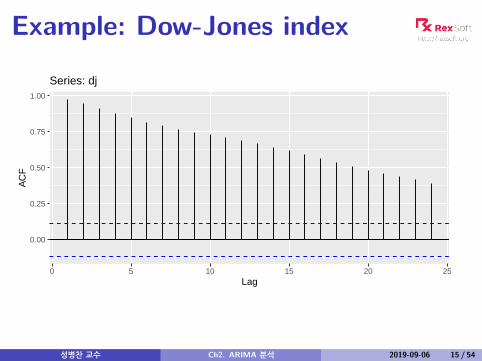

Non-stationarity in the mean

Identifying non-stationary seriestime plot.The ACF of stationary data drops to zero relativelyquicklyThe ACF of non-stationary data decreases slowly.For non-stationary data, the value of r1 is often largeand positive.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 13 / 54

Example: Dow-Jones index

3600

3700

3800

3900

4000

0 50 100 150 200 250 300Day

Dow

Jon

es In

dex

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 14 / 54

Example: Dow-Jones index

0.00

0.25

0.50

0.75

1.00

0 5 10 15 20 25Lag

AC

F

Series: dj

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 15 / 54

Example: Dow-Jones index

−100

−50

0

50

0 50 100 150 200 250 300Day

Cha

nge

in D

ow J

ones

Inde

x

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 16 / 54

Example: Dow-Jones index

−0.10

−0.05

0.00

0.05

0.10

0 5 10 15 20 25Lag

AC

F

Series: diff(dj)

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 17 / 54

Differencing

Differencing helps to stabilize the mean.The differenced series is the change between eachobservation in the original series: y ′t = yt − yt−1.The differenced series will have only T − 1 valuessince it is not possible to calculate a difference y ′1 forthe first observation.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 18 / 54

Second-order differencing

Occasionally the differenced data will not appearstationary and it may be necessary to difference the dataa second time:

y ′′t = y ′t − y ′t−1= (yt − yt−1)− (yt−1 − yt−2)= yt − 2yt−1 + yt−2.

y ′′t will have T − 2 values.In practice, it is almost never necessary to go beyondsecond-order differences.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 19 / 54

Seasonal differencing

A seasonal difference is the difference between anobservation and the corresponding observation from theprevious year.

y ′t = yt − yt−m

where m = number of seasons.For monthly data m = 12.For quarterly data m = 4.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 20 / 54

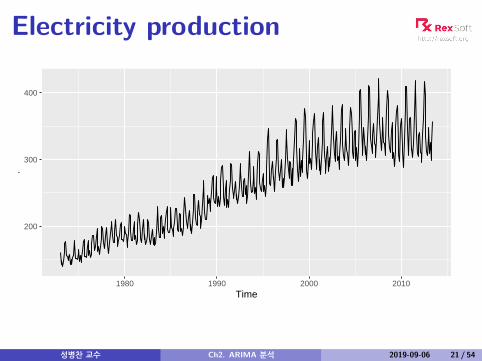

Electricity production

200

300

400

1980 1990 2000 2010Time

.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 21 / 54

Electricity production

5.1

5.4

5.7

6.0

1980 1990 2000 2010Time

.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 22 / 54

Electricity production

0.0

0.1

1980 1990 2000 2010Time

.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 23 / 54

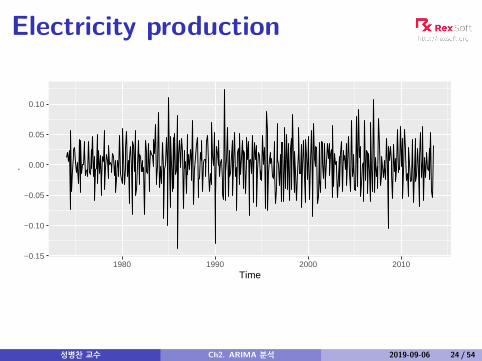

Electricity production

−0.15

−0.10

−0.05

0.00

0.05

0.10

1980 1990 2000 2010Time

.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 24 / 54

Electricity productionSeasonally differenced series is closer to beingstationary.Remaining non-stationarity can be removed withfurther first difference.

If y ′t = yt − yt−12 denotes seasonally differenced series,then twice-differenced series is

y ∗t = y ′t − y ′t−1= (yt − yt−12)− (yt−1 − yt−13)= yt − yt−1 − yt−12 + yt−13 .

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 25 / 54

Seasonal differencing

When both seasonal and first differences are applied. . .it makes no difference which is done first—the resultwill be the same.If seasonality is strong, we recommend that seasonaldifferencing be done first because sometimes theresulting series will be stationary and there will be noneed for further first difference.

It is important that if differencing is used, the differencesare interpretable.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 26 / 54

Interpretation of differencing

first differences are the change between oneobservation and the next;seasonal differences are the change between oneyear to the next.

But taking lag 3 differences for yearly data, for example,results in a model which cannot be sensibly interpreted.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 27 / 54

Backshift notationA very useful notational device is the backward shiftoperator, B, which is used as follows:

Byt = yt−1 .

In other words, B, operating on yt , has the effect ofshifting the data back one period. Two applicationsof B to yt shifts the data back two periods:

B(Byt) = B2yt = yt−2 .

For monthly data, if we wish to shift attention to “thesame month last year,” then B12 is used, and the notationis B12yt = yt−12.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 28 / 54

Backshift notationThe backward shift operator is convenient for describingthe process of differencing. A first difference can bewritten as

y ′t = yt − yt−1 = yt − Byt = (1− B)yt .

Note that a first difference is represented by (1− B).Similarly, if second-order differences (i.e., first differencesof first differences) have to be computed, then:

y ′′t = yt − 2yt−1 + yt−2 = (1− B)2yt .

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 29 / 54

Backshift notationSecond-order difference is denoted (1− B)2.Second-order difference is not the same as a seconddifference, which would be denoted 1− B2;In general, a dth-order difference can be written as

(1− B)dyt .

A seasonal difference followed by a first differencecan be written as

(1− B)(1− Bm)yt .

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 30 / 54

Backshift notation

The “backshift” notation is convenient because the termscan be multiplied together to see the combined effect.

(1− B)(1− Bm)yt = (1− B − Bm + Bm+1)yt

= yt − yt−1 − yt−m + yt−m−1.

For monthly data, m = 12 and we obtain the same resultas earlier.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 31 / 54

Outline

1 Stationarity and differencing

2 Non-seasonal ARIMA models

3 Order selection

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 32 / 54

Autoregressive modelsAutoregressive (AR) models:

yt = c + φ1yt−1 + φ2yt−2 + · · ·+ φpyt−p + εt ,

where εt is white noise. This is a multiple regression withlagged values of yt as predictors.

8

10

12

0 20 40 60 80 100Time

AR(1)

15.0

17.5

20.0

22.5

25.0

0 20 40 60 80 100Time

AR(2)

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 33 / 54

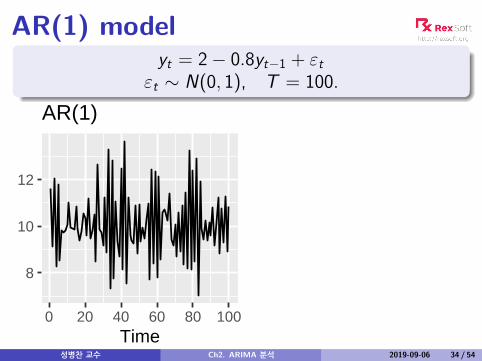

AR(1) modelyt = 2− 0.8yt−1 + εt

εt ∼ N(0, 1), T = 100.

8

10

12

0 20 40 60 80 100Time

AR(1)

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 34 / 54

AR(1) model

yt = c + φ1yt−1 + εt

When φ1 = 0, yt is equivalent to WNWhen φ1 = 1 and c = 0, yt is equivalent to a RWWhen φ1 = 1 and c 6= 0, yt is equivalent to a RWwith driftWhen φ1 < 0, yt tends to oscillate betweenpositive and negative values.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 35 / 54

AR(2) modelyt = 8 + 1.3yt−1 − 0.7yt−2 + εtεt ∼ N(0, 1), T = 100.

15.0

17.5

20.0

22.5

25.0

0 20 40 60 80 100Time

AR(2)

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 36 / 54

Moving Average (MA) modelsMoving Average (MA) models:

yt = c + εt + θ1εt−1 + θ2εt−2 + · · ·+ θqεt−q,

where εt is white noise. This is a multiple regression with pasterrors as predictors. Don’t confuse this with moving averagesmoothing!

18

20

22

0 20 40 60 80 100Time

MA(1)

−5.0

−2.5

0.0

2.5

0 20 40 60 80 100Time

MA(2)

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 37 / 54

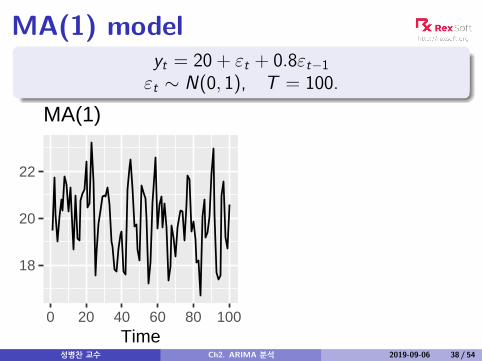

MA(1) modelyt = 20 + εt + 0.8εt−1εt ∼ N(0, 1), T = 100.

18

20

22

0 20 40 60 80 100Time

MA(1)

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 38 / 54

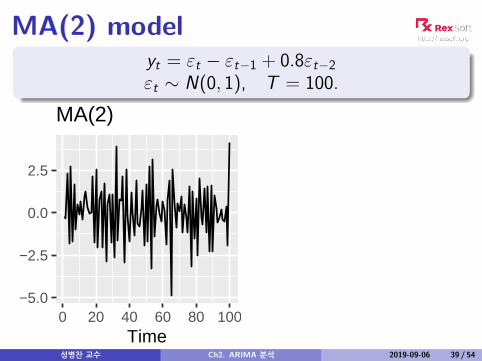

MA(2) modelyt = εt − εt−1 + 0.8εt−2εt ∼ N(0, 1), T = 100.

−5.0

−2.5

0.0

2.5

0 20 40 60 80 100Time

MA(2)

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 39 / 54

MA(∞) modelsIt is possible to write any stationary AR(p) process as anMA(∞) process.Example: AR(1)yt = φ1yt−1 + εt

= φ1(φ1yt−2 + εt−1) + εt

= φ21yt−2 + φ1εt−1 + εt

= φ31yt−3 + φ2

1εt−2 + φ1εt−1 + εt

. . .

Provided −1 < φ1 < 1:

yt = εt + φ1εt−1 + φ21εt−2 + φ3

1εt−3 + · · ·

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 40 / 54

ARIMA modelsAutoregressive Moving Average models:

yt = c + φ1yt−1 + · · ·+ φpyt−p

+ θ1εt−1 + · · ·+ θqεt−q + εt .

Predictors include both lagged values of yt andlagged errors.Conditions on coefficients ensure stationarity.Conditions on coefficients ensure invertibility.

Autoregressive Integrated Moving Average modelsCombine ARMA model with differencing.(1− B)dyt follows an ARMA model.성병찬 교수 Ch2. ARIMA 분석 2019-09-06 41 / 54

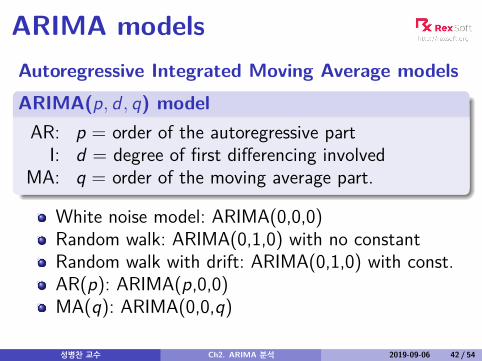

ARIMA modelsAutoregressive Integrated Moving Average modelsARIMA(p, d , q) modelAR: p = order of the autoregressive part

I: d = degree of first differencing involvedMA: q = order of the moving average part.

White noise model: ARIMA(0,0,0)Random walk: ARIMA(0,1,0) with no constantRandom walk with drift: ARIMA(0,1,0) with const.AR(p): ARIMA(p,0,0)MA(q): ARIMA(0,0,q)

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 42 / 54

Backshift notation for ARIMAARMA model:

yt = c + φ1Byt + · · ·+ φpBpyt + εt + θ1Bεt + · · ·+ θqBqεt

or (1− φ1B − · · · − φpBp)yt = c + (1 + θ1B + · · ·+ θqBq)εt

ARIMA(1,1,1) model:

(1− φ1B) (1− B)yt = c + (1 + θ1B)εt↑ ↑ ↑

AR(1) First MA(1)difference

Written out:

yt = c + yt−1 + φ1yt−1 − φ1yt−2 + θ1εt−1 + εt

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 43 / 54

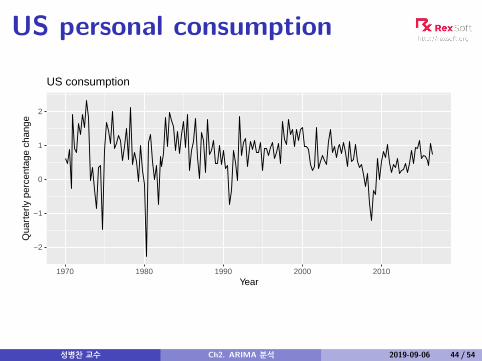

US personal consumption

−2

−1

0

1

2

1970 1980 1990 2000 2010Year

Qua

rter

ly p

erce

ntag

e ch

ange

US consumption

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 44 / 54

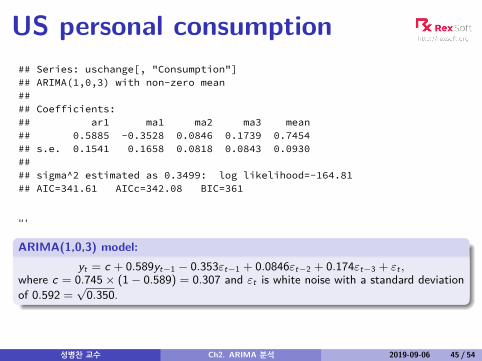

US personal consumption## Series: uschange[, "Consumption"]## ARIMA(1,0,3) with non-zero mean#### Coefficients:## ar1 ma1 ma2 ma3 mean## 0.5885 -0.3528 0.0846 0.1739 0.7454## s.e. 0.1541 0.1658 0.0818 0.0843 0.0930#### sigma^2 estimated as 0.3499: log likelihood=-164.81## AIC=341.61 AICc=342.08 BIC=361

“‘

ARIMA(1,0,3) model:yt = c + 0.589yt−1 − 0.353εt−1 + 0.0846εt−2 + 0.174εt−3 + εt ,

where c = 0.745× (1− 0.589) = 0.307 and εt is white noise with a standard deviationof 0.592 =

√0.350.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 45 / 54

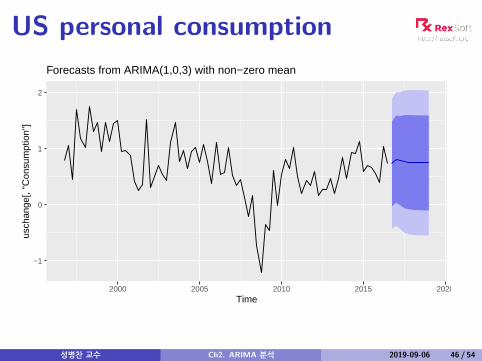

US personal consumption

−1

0

1

2

2000 2005 2010 2015 2020Time

usch

ange

[, "C

onsu

mpt

ion"

]

Forecasts from ARIMA(1,0,3) with non−zero mean

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 46 / 54

Outline

1 Stationarity and differencing

2 Non-seasonal ARIMA models

3 Order selection

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 47 / 54

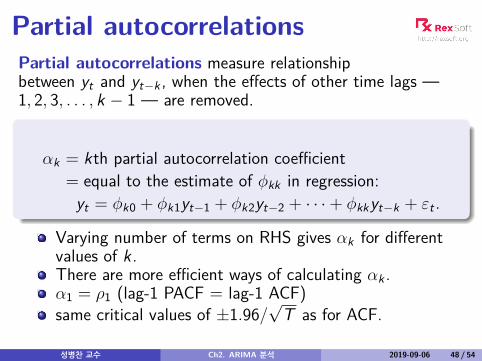

Partial autocorrelationsPartial autocorrelations measure relationshipbetween yt and yt−k , when the effects of other time lags —1, 2, 3, . . . , k − 1 — are removed.

αk = kth partial autocorrelation coefficient= equal to the estimate of φkk in regression:yt = φk0 + φk1yt−1 + φk2yt−2 + · · ·+ φkkyt−k + εt .

Varying number of terms on RHS gives αk for differentvalues of k .There are more efficient ways of calculating αk .α1 = ρ1 (lag-1 PACF = lag-1 ACF)same critical values of ±1.96/

√T as for ACF.

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 48 / 54

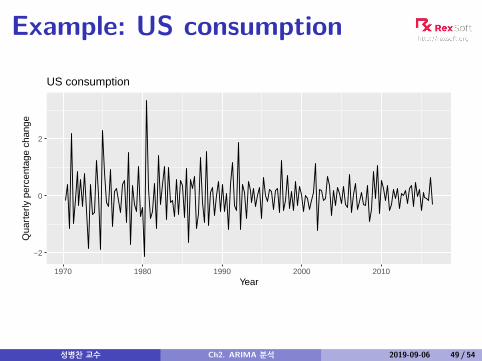

Example: US consumption

−2

0

2

1970 1980 1990 2000 2010Year

Qua

rter

ly p

erce

ntag

e ch

ange

US consumption

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 49 / 54

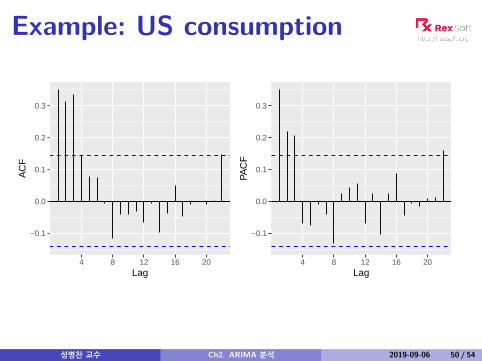

Example: US consumption

−0.1

0.0

0.1

0.2

0.3

4 8 12 16 20Lag

AC

F

−0.1

0.0

0.1

0.2

0.3

4 8 12 16 20Lag

PAC

F

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 50 / 54

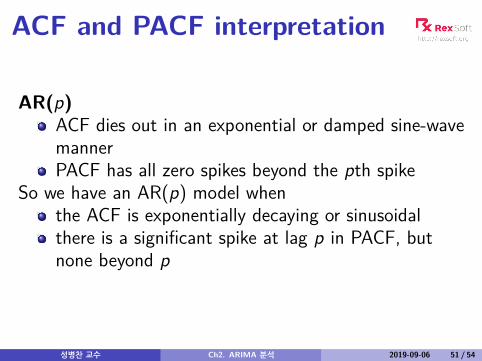

ACF and PACF interpretation

AR(p)ACF dies out in an exponential or damped sine-wavemannerPACF has all zero spikes beyond the pth spike

So we have an AR(p) model whenthe ACF is exponentially decaying or sinusoidalthere is a significant spike at lag p in PACF, butnone beyond p

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 51 / 54

ACF and PACF interpretation

MA(q)PACF dies out in an exponential or dampedsine-wave mannerACF has all zero spikes beyond the qth spike

So we have an MA(q) model whenthe PACF is exponentially decaying or sinusoidalthere is a significant spike at lag q in ACF, but nonebeyond q

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 52 / 54

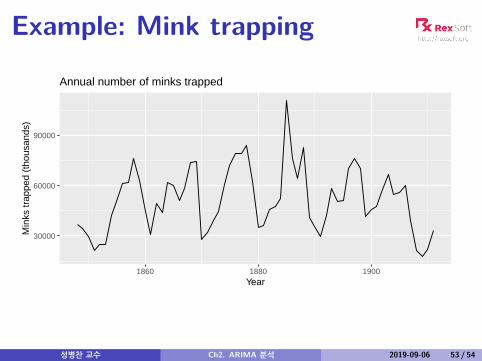

Example: Mink trapping

30000

60000

90000

1860 1880 1900Year

Min

ks tr

appe

d (t

hous

ands

)

Annual number of minks trapped

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 53 / 54

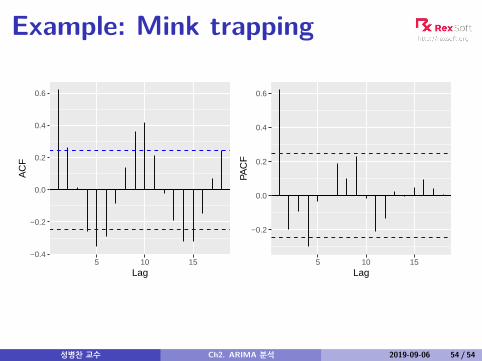

Example: Mink trapping

−0.4

−0.2

0.0

0.2

0.4

0.6

5 10 15Lag

AC

F

−0.2

0.0

0.2

0.4

0.6

5 10 15Lag

PAC

F

성병찬 교수 Ch2. ARIMA 분석 2019-09-06 54 / 54

2장-실습

1) dj.xlsx 파일의 시계열 자료를 [ARIMA 모형]으로 분석하시오.

([비계절 및 계절 차수 자동 선택] 옵션 및 [출력옵션] 탭을 이용)

A. 어떤 모형이 적합되었는가?

B. 잔차는 백색잡음의 가정을 만족하는가?

C. 예측치는 어떤 특징을 가지는가?

2) usmelec.xlsx 파일의 시계열 자료를 [ARIMA 모형]으로 분석하시오.

3) 엑셀 워크시트에 AR(1)과 MA(1)을 따르는 시계열을 각각 생성하시오.

4) ACF와 PACF의 특징을 관찰하고, 이론적 특성과 어떻게 다른지 설명하시오.

Ch3. 지수평활법 분석

성병찬 교수

중앙대 응용통계학과

2019-09-06

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 1 / 21

Outline

1 Simple exponential smoothing

2 Trend methods

3 Seasonal methods

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 2 / 21

Simple methodsTime series y1, y2, . . . , yT .Random walk forecasts

yT+h|T = yT

Average forecasts

yT+h|T = 1T

T∑t=1

yt

Want something in between that weights most recentdata more highly.Simple exponential smoothing uses a weighted movingaverage with weights that decrease exponentially.

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 3 / 21

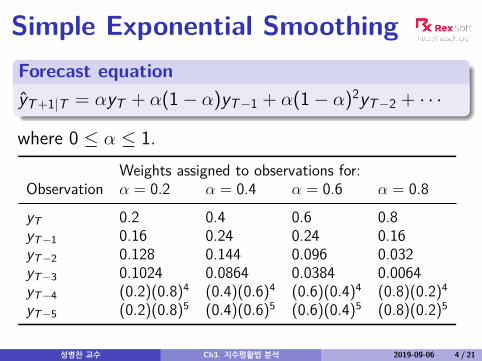

Simple Exponential SmoothingForecast equationyT+1|T = αyT + α(1− α)yT−1 + α(1− α)2yT−2 + · · ·

where 0 ≤ α ≤ 1.Weights assigned to observations for:

Observation α = 0.2 α = 0.4 α = 0.6 α = 0.8

yT 0.2 0.4 0.6 0.8yT−1 0.16 0.24 0.24 0.16yT−2 0.128 0.144 0.096 0.032yT−3 0.1024 0.0864 0.0384 0.0064yT−4 (0.2)(0.8)4 (0.4)(0.6)4 (0.6)(0.4)4 (0.8)(0.2)4

yT−5 (0.2)(0.8)5 (0.4)(0.6)5 (0.6)(0.4)5 (0.8)(0.2)5

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 4 / 21

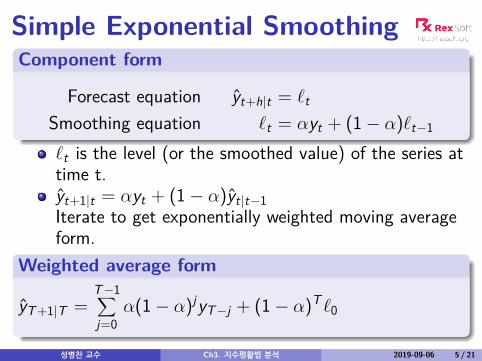

Simple Exponential SmoothingComponent form

Forecast equation yt+h|t = `t

Smoothing equation `t = αyt + (1− α)`t−1

`t is the level (or the smoothed value) of the series attime t.yt+1|t = αyt + (1− α)yt|t−1Iterate to get exponentially weighted moving averageform.

Weighted average form

yT+1|T =T−1∑j=0

α(1− α)jyT−j + (1− α)T `0

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 5 / 21

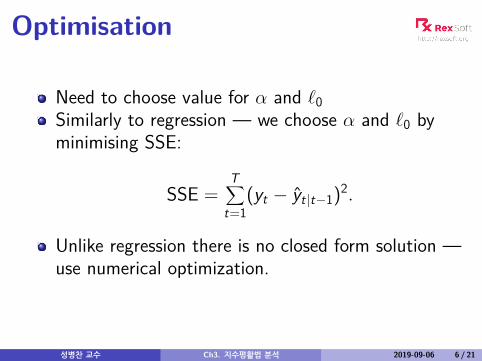

Optimisation

Need to choose value for α and `0Similarly to regression — we choose α and `0 byminimising SSE:

SSE =T∑

t=1(yt − yt|t−1)2.

Unlike regression there is no closed form solution —use numerical optimization.

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 6 / 21

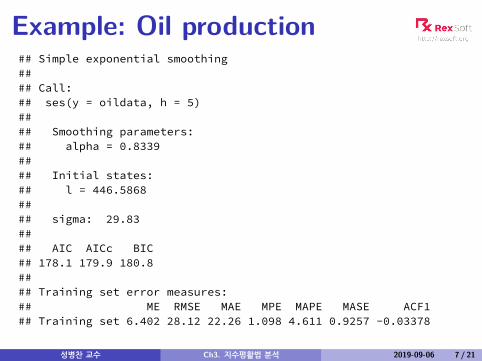

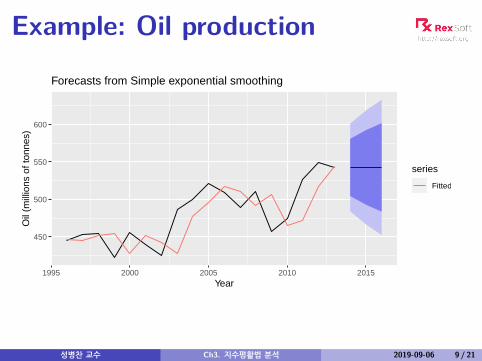

Example: Oil production## Simple exponential smoothing#### Call:## ses(y = oildata, h = 5)#### Smoothing parameters:## alpha = 0.8339#### Initial states:## l = 446.5868#### sigma: 29.83#### AIC AICc BIC## 178.1 179.9 180.8#### Training set error measures:## ME RMSE MAE MPE MAPE MASE ACF1## Training set 6.402 28.12 22.26 1.098 4.611 0.9257 -0.03378

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 7 / 21

Example: Oil productionYear Time Observation Level Forecast

t yt `t yt+1|t1995 0 446.591996 1 445.36 445.57 446.591997 2 453.20 451.93 445.571998 3 454.41 454.00 451.931999 4 422.38 427.63 454.002000 5 456.04 451.32 427.632001 6 440.39 442.20 451.322002 7 425.19 428.02 442.202003 8 486.21 476.54 428.022004 9 500.43 496.46 476.542005 10 521.28 517.15 496.462006 11 508.95 510.31 517.152007 12 488.89 492.45 510.312008 13 509.87 506.98 492.452009 14 456.72 465.07 506.982010 15 473.82 472.36 465.072011 16 525.95 517.05 472.362012 17 549.83 544.39 517.052013 18 542.34 542.68 544.39

h yT+h|T2014 1 542.682015 2 542.682016 3 542.68

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 8 / 21

Example: Oil production

450

500

550

600

1995 2000 2005 2010 2015Year

Oil

(mill

ions

of t

onne

s)

series

Fitted

Forecasts from Simple exponential smoothing

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 9 / 21

Outline

1 Simple exponential smoothing

2 Trend methods

3 Seasonal methods

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 10 / 21

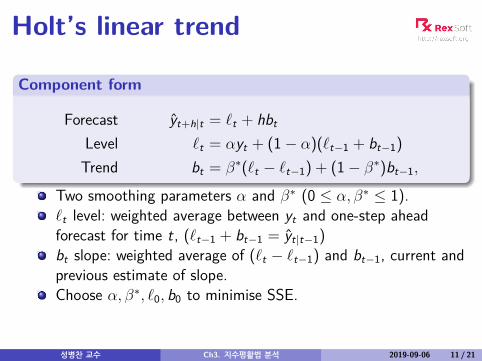

Holt’s linear trend

Component form

Forecast yt+h|t = `t + hbt

Level `t = αyt + (1− α)(`t−1 + bt−1)Trend bt = β∗(`t − `t−1) + (1− β∗)bt−1,

Two smoothing parameters α and β∗ (0 ≤ α, β∗ ≤ 1).`t level: weighted average between yt and one-step aheadforecast for time t, (`t−1 + bt−1 = yt|t−1)bt slope: weighted average of (`t − `t−1) and bt−1, current andprevious estimate of slope.Choose α, β∗, `0, b0 to minimise SSE.

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 11 / 21

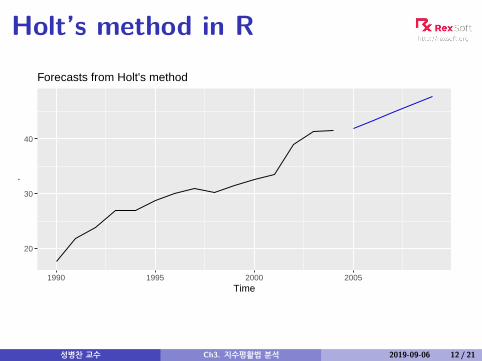

Holt’s method in R

20

30

40

1990 1995 2000 2005Time

.

Forecasts from Holt's method

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 12 / 21

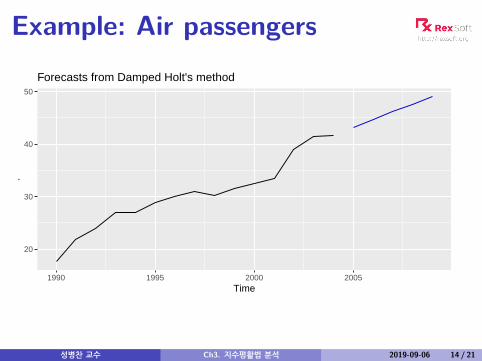

Damped trend method

Component form

yt+h|t = `t + (φ+ φ2 + · · ·+ φh)bt

`t = αyt + (1− α)(`t−1 + φbt−1)bt = β∗(`t − `t−1) + (1− β∗)φbt−1.

Damping parameter 0 < φ < 1.If φ = 1, identical to Holt’s linear trend.As h→∞, yT+h|T → `T + φbT/(1− φ).Short-run forecasts trended, long-run forecastsconstant.

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 13 / 21

Example: Air passengers

20

30

40

50

1990 1995 2000 2005Time

.

Forecasts from Damped Holt's method

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 14 / 21

Outline

1 Simple exponential smoothing

2 Trend methods

3 Seasonal methods

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 15 / 21

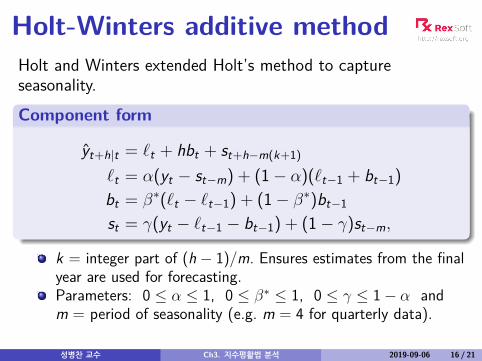

Holt-Winters additive methodHolt and Winters extended Holt’s method to captureseasonality.

Component form

yt+h|t = `t + hbt + st+h−m(k+1)

`t = α(yt − st−m) + (1− α)(`t−1 + bt−1)bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γ(yt − `t−1 − bt−1) + (1− γ)st−m,

k = integer part of (h − 1)/m. Ensures estimates from the finalyear are used for forecasting.Parameters: 0 ≤ α ≤ 1, 0 ≤ β∗ ≤ 1, 0 ≤ γ ≤ 1− α andm = period of seasonality (e.g. m = 4 for quarterly data).

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 16 / 21

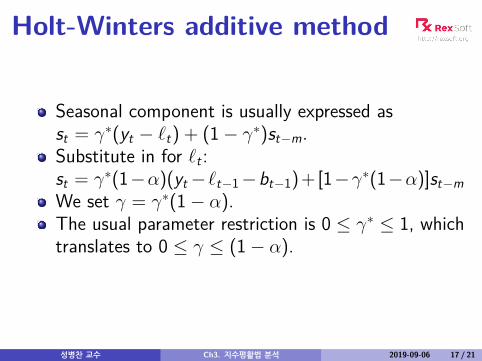

Holt-Winters additive method

Seasonal component is usually expressed asst = γ∗(yt − `t) + (1− γ∗)st−m.Substitute in for `t :st = γ∗(1−α)(yt−`t−1−bt−1)+[1−γ∗(1−α)]st−mWe set γ = γ∗(1− α).The usual parameter restriction is 0 ≤ γ∗ ≤ 1, whichtranslates to 0 ≤ γ ≤ (1− α).

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 17 / 21

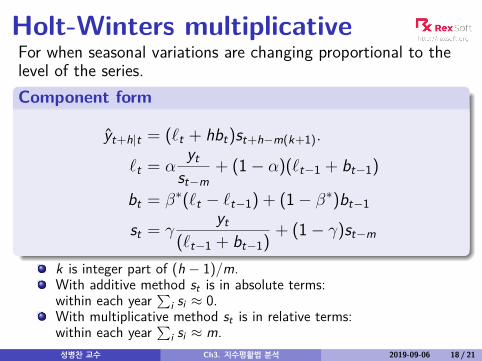

Holt-Winters multiplicativeFor when seasonal variations are changing proportional to thelevel of the series.Component form

yt+h|t = (`t + hbt)st+h−m(k+1).

`t = αyt

st−m+ (1− α)(`t−1 + bt−1)

bt = β∗(`t − `t−1) + (1− β∗)bt−1

st = γyt

(`t−1 + bt−1)+ (1− γ)st−m

k is integer part of (h − 1)/m.With additive method st is in absolute terms:within each year

∑i si ≈ 0.

With multiplicative method st is in relative terms:within each year

∑i si ≈ m.

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 18 / 21

Example: Visitor Nights

40

60

80

2008 2012 2016YearIn

tern

atio

nal v

isito

r ni

ght i

n A

ustr

alia

(m

illio

ns)

Data

HW additive forecasts

HW multiplicative forecasts

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 19 / 21

Estimated components

levelslope

season2007 2010 2013 2016

40

50

60

0.7008

0.7012

0.7016

−10−5

05

10

Year

Additive states

levelslope

season

2007 2010 2013 2016

40

50

60

0.65

0.70

0.75

0.80.91.01.11.2

Year

Multiplicative states

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 20 / 21

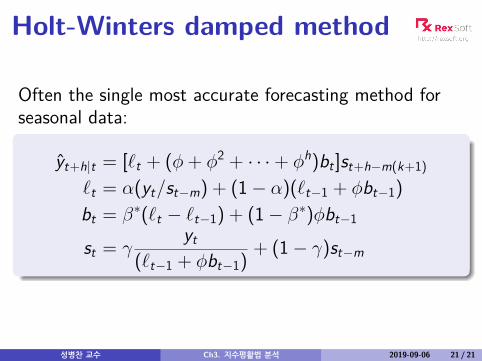

Holt-Winters damped method

Often the single most accurate forecasting method forseasonal data:

yt+h|t = [`t + (φ+ φ2 + · · ·+ φh)bt ]st+h−m(k+1)

`t = α(yt/st−m) + (1− α)(`t−1 + φbt−1)bt = β∗(`t − `t−1) + (1− β∗)φbt−1

st = γyt

(`t−1 + φbt−1)+ (1− γ)st−m

성병찬 교수 Ch3. 지수평활법 분석 2019-09-06 21 / 21

3장-실습

1) oildata.xlsx 자료를 이용하여 강의록 7~8페이지와 같은 계산을 시행하시오. 엑셀의 [해찾기] 기능을

사용하고 REX의 결과값과 비교하시오.

2) hw_models.xlsx 자료를 이용하여 다음 물음에 답하시오.

A. Holt-Winters의 가법 모형을 적합하고, 추정된 평활상수를 쓰시오.

B. [분해 도표]에서 각 시계열 구성성분들(수준, 추세, 계절)이 어떻게 분해되었는지 확인하시오.

C. ARIMA 모형, 지수평활법(HW 가법 및 승법 모형)을 각각 적용하고 모형의 적합도를 비교하고,

예측치와 함께 그림을 그리시오.

![Ó47 é4?4=-]'Î é { ã : ) f9 i1ú - n8^ ¹ ´ V / / + û é Ì Ç ü « £4È-ú ¤ / /1ñ æ ê / / Ç é t 1g %l æ Ê1ñ ½ æ%5 1ñ Ç" !¢ Ô Î é%51ñ é £! Ç ü « æ](https://static.fdocument.pub/doc/165x107/602daf6322287520c162e7e0/47-44-f-9-i1-n8-v-oe-4-.jpg)