CFO and Capital Market Financing - Stock Exchange of …€¦ · · 2016-09-16CFO and Capital...

60

Strictly Confidential CFO and Capital Market Financing

Transcript of CFO and Capital Market Financing - Stock Exchange of …€¦ · · 2016-09-16CFO and Capital...

Strictly Confidential

CFO and Capital Market Financing

Strictly Confidential

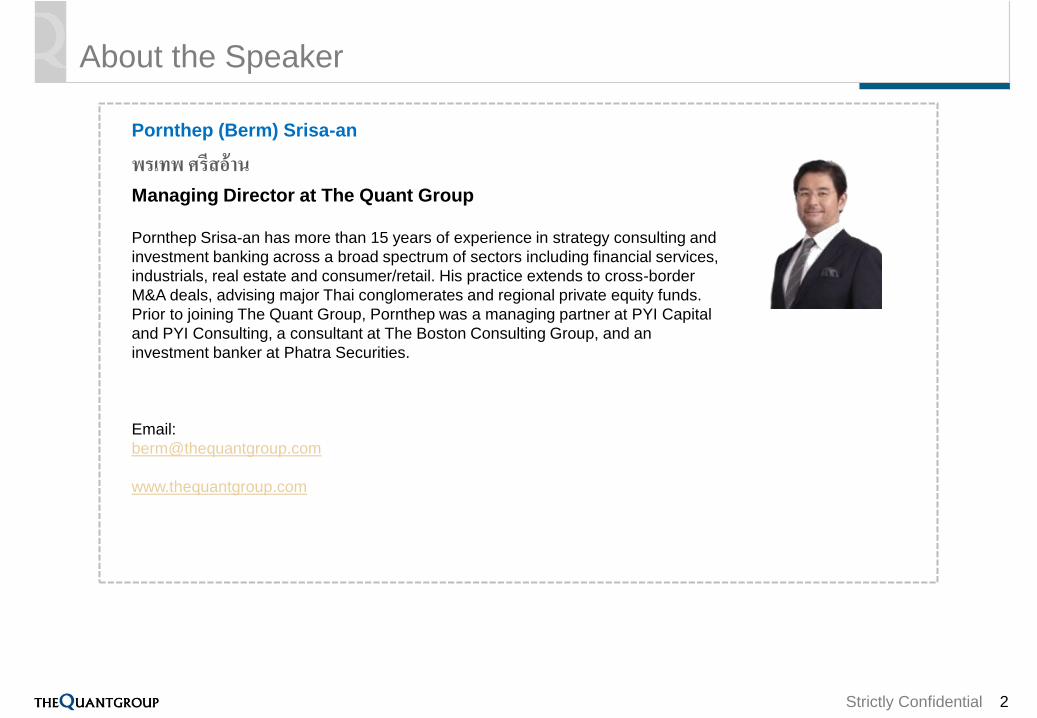

About the Speaker

2

Pornthep (Berm) Srisa-an

พรเทพ ศรีสอ้านManaging Director at The Quant Group

Pornthep Srisa-an has more than 15 years of experience in strategy consulting and

investment banking across a broad spectrum of sectors including financial services,

industrials, real estate and consumer/retail. His practice extends to cross-border

M&A deals, advising major Thai conglomerates and regional private equity funds.

Prior to joining The Quant Group, Pornthep was a managing partner at PYI Capital

and PYI Consulting, a consultant at The Boston Consulting Group, and an

investment banker at Phatra Securities.

Email:

www.thequantgroup.com

Strictly Confidential

Agenda

What is M&A?

M&A process and preparation

Roles of key parties

Key success factors

3

Strictly Confidential

What is M&A?

4

Strictly Confidential

What is M&A

5

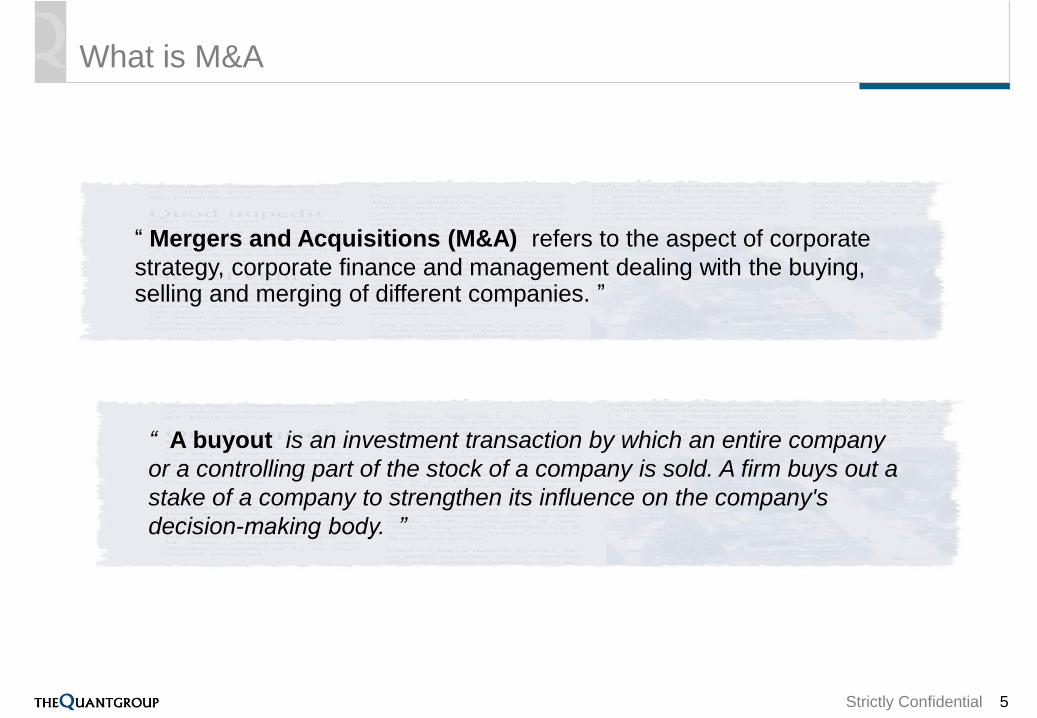

“ A buyout is an investment transaction by which an entire company

or a controlling part of the stock of a company is sold. A firm buys out a

stake of a company to strengthen its influence on the company's

decision-making body. ”

“ Mergers and Acquisitions (M&A) refers to the aspect of corporate

strategy, corporate finance and management dealing with the buying, selling and merging of different companies. ”

Strictly Confidential

Merger vs. Acquisition

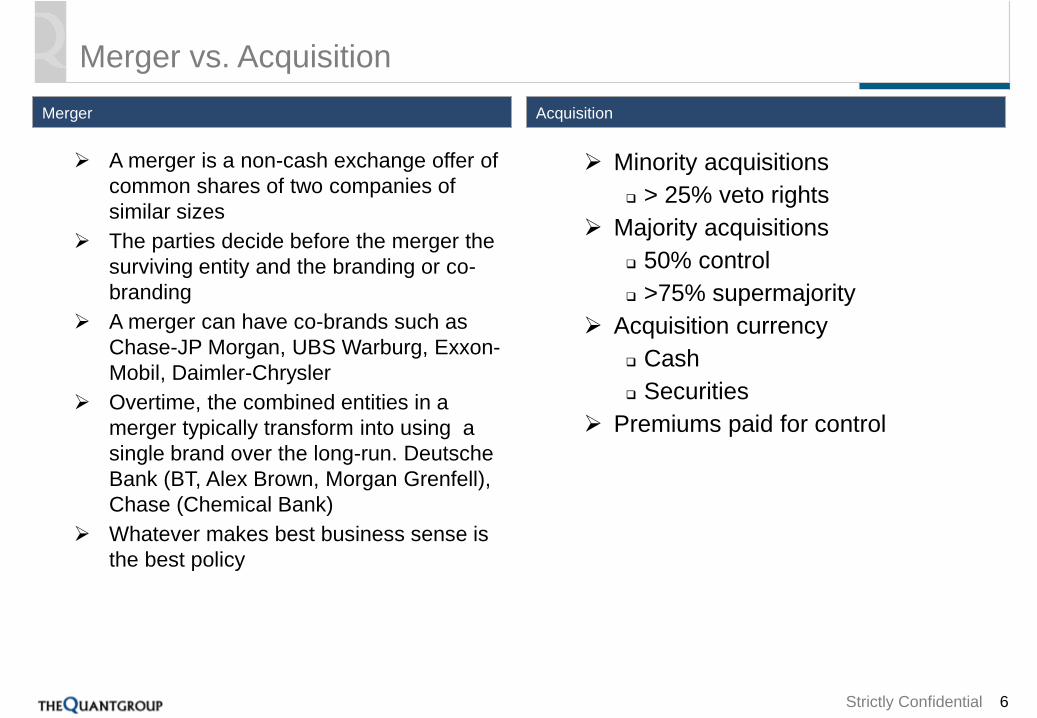

Merger

A merger is a non-cash exchange offer of

common shares of two companies of

similar sizes

The parties decide before the merger the

surviving entity and the branding or co-

branding

A merger can have co-brands such as

Chase-JP Morgan, UBS Warburg, Exxon-

Mobil, Daimler-Chrysler

Overtime, the combined entities in a

merger typically transform into using a

single brand over the long-run. Deutsche

Bank (BT, Alex Brown, Morgan Grenfell),

Chase (Chemical Bank)

Whatever makes best business sense is

the best policy

Acquisition

Minority acquisitions

> 25% veto rights

Majority acquisitions

50% control

>75% supermajority

Acquisition currency

Cash

Securities

Premiums paid for control

6

Strictly Confidential

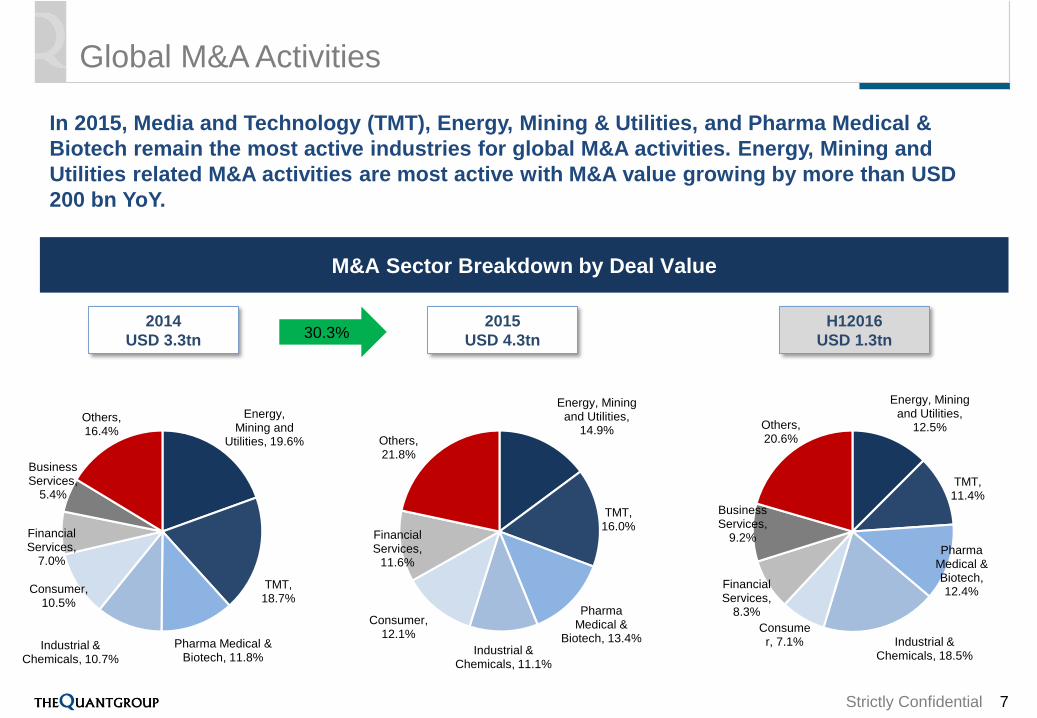

Global M&A Activities

In 2015, Media and Technology (TMT), Energy, Mining & Utilities, and Pharma Medical &

Biotech remain the most active industries for global M&A activities. Energy, Mining and

Utilities related M&A activities are most active with M&A value growing by more than USD

200 bn YoY.

7

M&A Sector Breakdown by Deal Value

2015

USD 4.3tn

2014

USD 3.3tn30.3%

H12016

USD 1.3tn

Energy, Mining and

Utilities, 19.6%

TMT, 18.7%

Pharma Medical & Biotech, 11.8%

Industrial & Chemicals, 10.7%

Consumer, 10.5%

Financial Services,

7.0%

Business Services,

5.4%

Others, 16.4%

Energy, Mining and Utilities,

12.5%

TMT, 11.4%

Pharma Medical & Biotech, 12.4%

Industrial & Chemicals, 18.5%

Consumer, 7.1%

Financial Services,

8.3%

Business Services,

9.2%

Others, 20.6%

Energy, Mining and Utilities,

14.9%

TMT, 16.0%

Pharma Medical &

Biotech, 13.4%Industrial &

Chemicals, 11.1%

Consumer, 12.1%

Financial Services,

11.6%

Others, 21.8%

Strictly Confidential

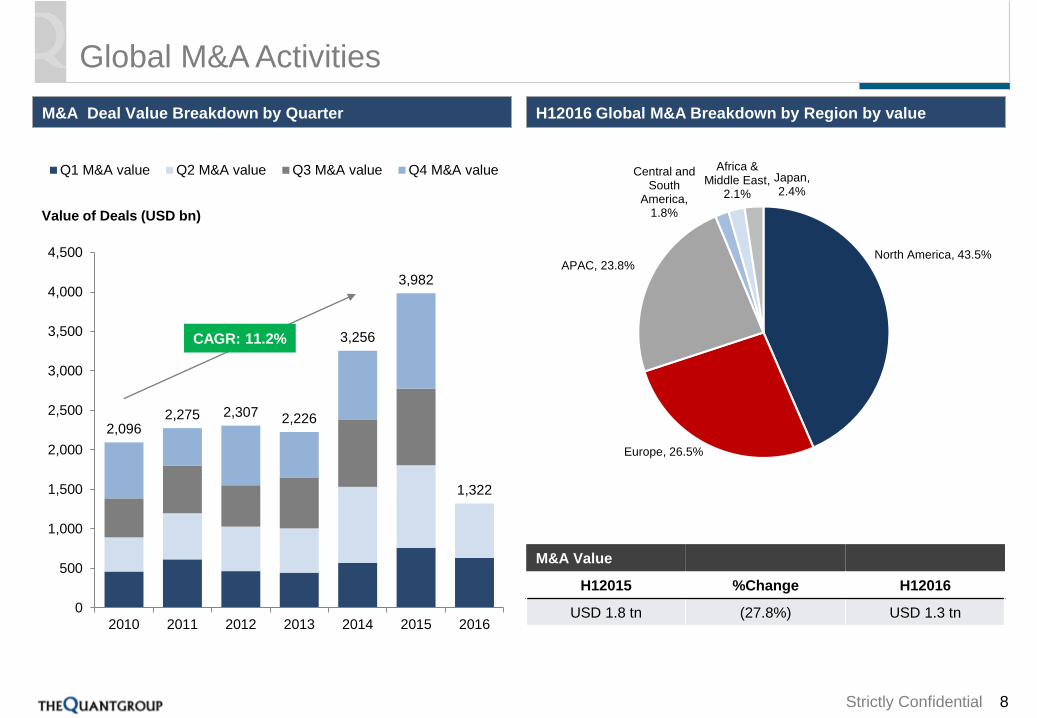

Global M&A Activities

M&A Deal Value Breakdown by Quarter H12016 Global M&A Breakdown by Region by value

8

2,0962,275 2,307 2,226

3,256

3,982

1,322

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2010 2011 2012 2013 2014 2015 2016

Q1 M&A value Q2 M&A value Q3 M&A value Q4 M&A value

Value of Deals (USD bn)

CAGR: 11.2%

North America, 43.5%

Europe, 26.5%

APAC, 23.8%

Central and South

America, 1.8%

Africa & Middle East,

2.1%

Japan, 2.4%

M&A Value

H12015 %Change H12016

USD 1.8 tn (27.8%) USD 1.3 tn

Strictly Confidential

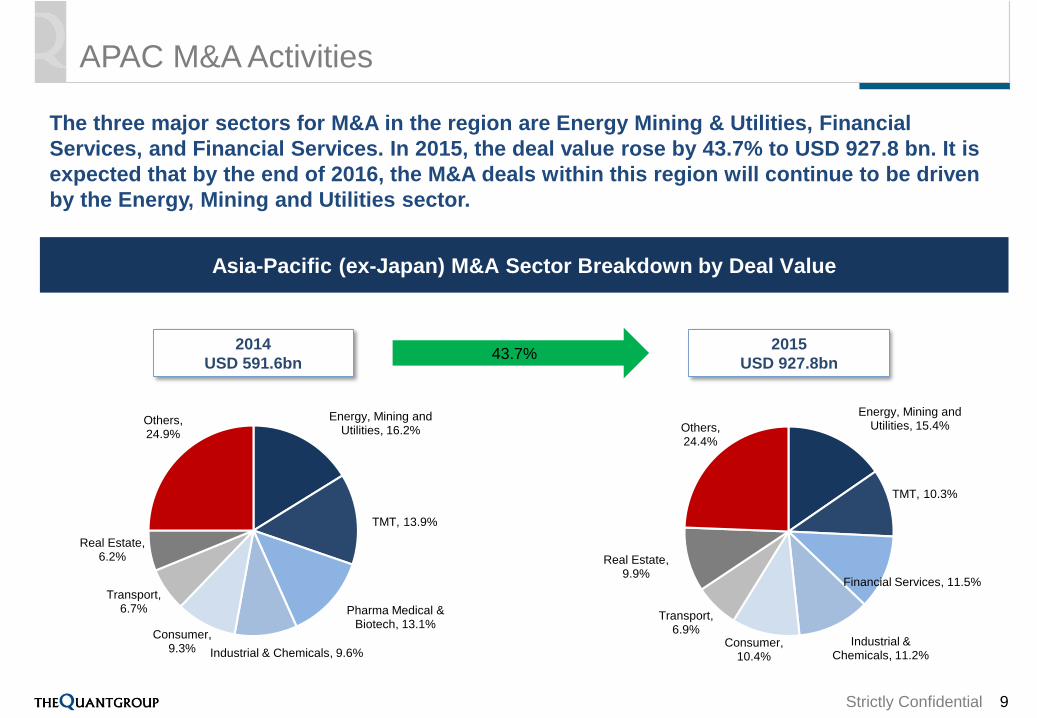

APAC M&A Activities

The three major sectors for M&A in the region are Energy Mining & Utilities, Financial

Services, and Financial Services. In 2015, the deal value rose by 43.7% to USD 927.8 bn. It is

expected that by the end of 2016, the M&A deals within this region will continue to be driven

by the Energy, Mining and Utilities sector.

9

Asia-Pacific (ex-Japan) M&A Sector Breakdown by Deal Value

2015

USD 927.8bn43.7%

Energy, Mining and Utilities, 15.4%

TMT, 10.3%

Financial Services, 11.5%

Industrial & Chemicals, 11.2%

Consumer, 10.4%

Transport, 6.9%

Real Estate, 9.9%

Others, 24.4%

Energy, Mining and Utilities, 16.2%

TMT, 13.9%

Pharma Medical & Biotech, 13.1%

Industrial & Chemicals, 9.6%

Consumer, 9.3%

Transport, 6.7%

Real Estate, 6.2%

Others, 24.9%

2014

USD 591.6bn

Strictly Confidential

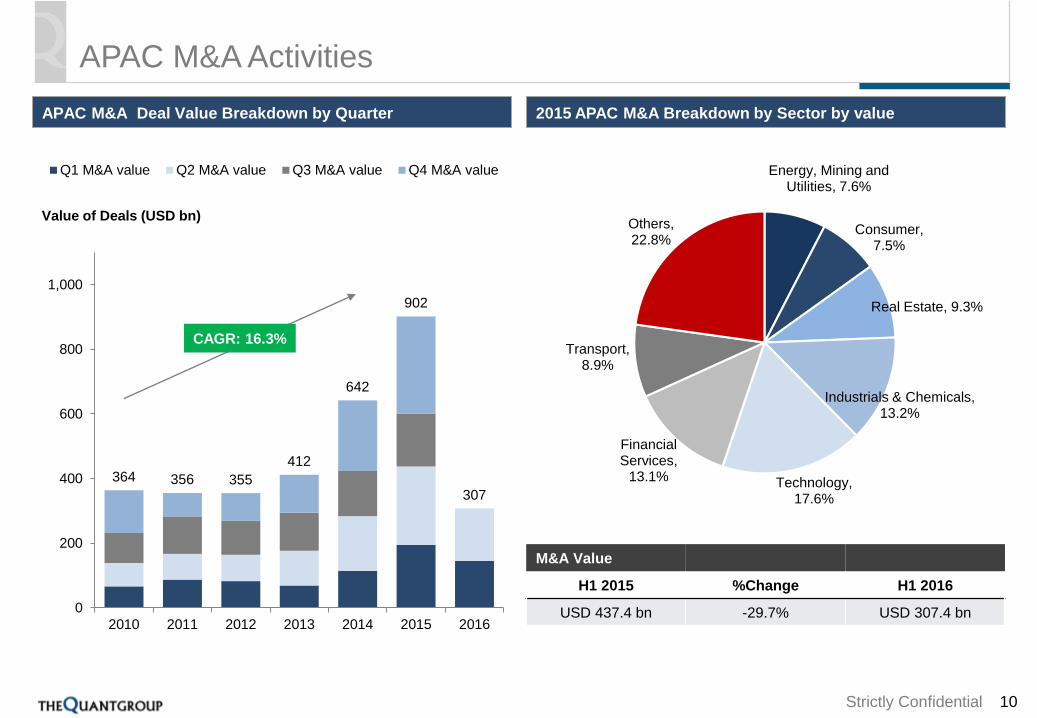

APAC M&A Activities

APAC M&A Deal Value Breakdown by Quarter 2015 APAC M&A Breakdown by Sector by value

10

364 356 355

412

642

902

307

0

200

400

600

800

1,000

2010 2011 2012 2013 2014 2015 2016

Q1 M&A value Q2 M&A value Q3 M&A value Q4 M&A value

Value of Deals (USD bn)

CAGR: 16.3%

Energy, Mining and Utilities, 7.6%

Consumer, 7.5%

Real Estate, 9.3%

Industrials & Chemicals, 13.2%

Technology, 17.6%

Financial Services,

13.1%

Transport, 8.9%

Others, 22.8%

M&A Value

H1 2015 %Change H1 2016

USD 437.4 bn -29.7% USD 307.4 bn

Strictly Confidential

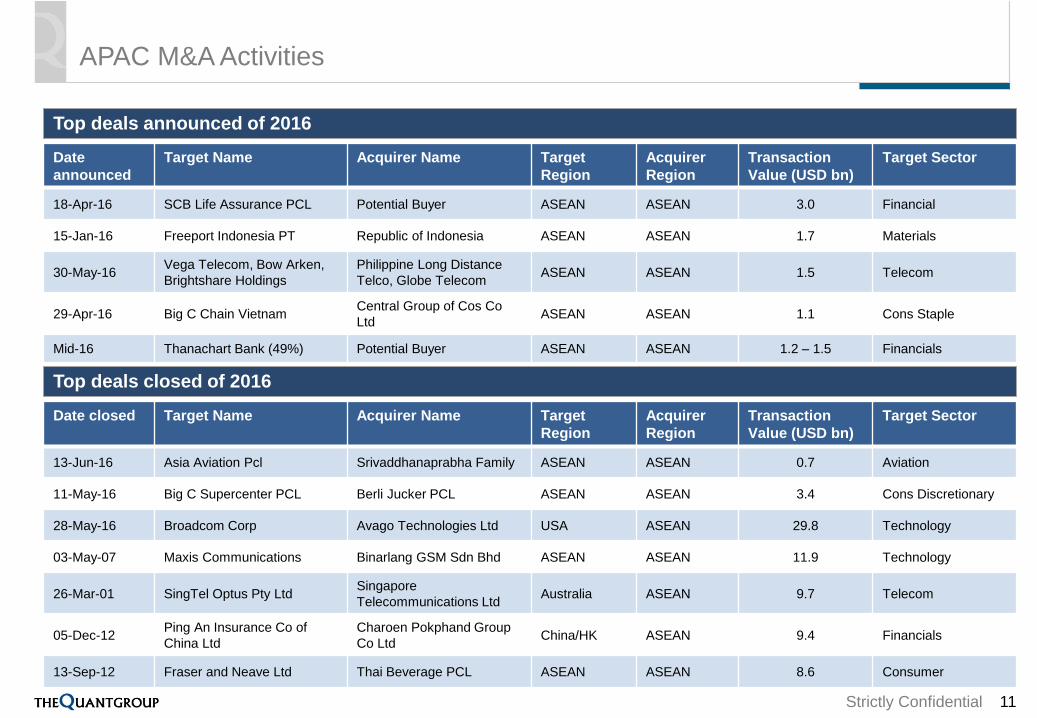

APAC M&A Activities

11

Date

announced

Target Name Acquirer Name Target

Region

Acquirer

Region

Transaction

Value (USD bn)

Target Sector

18-Apr-16 SCB Life Assurance PCL Potential Buyer ASEAN ASEAN 3.0 Financial

15-Jan-16 Freeport Indonesia PT Republic of Indonesia ASEAN ASEAN 1.7 Materials

30-May-16Vega Telecom, Bow Arken,

Brightshare Holdings

Philippine Long Distance

Telco, Globe TelecomASEAN ASEAN 1.5 Telecom

29-Apr-16 Big C Chain VietnamCentral Group of Cos Co

LtdASEAN ASEAN 1.1 Cons Staple

Mid-16 Thanachart Bank (49%) Potential Buyer ASEAN ASEAN 1.2 – 1.5 Financials

Date closed Target Name Acquirer Name Target

Region

Acquirer

Region

Transaction

Value (USD bn)

Target Sector

13-Jun-16 Asia Aviation Pcl Srivaddhanaprabha Family ASEAN ASEAN 0.7 Aviation

11-May-16 Big C Supercenter PCL Berli Jucker PCL ASEAN ASEAN 3.4 Cons Discretionary

28-May-16 Broadcom Corp Avago Technologies Ltd USA ASEAN 29.8 Technology

03-May-07 Maxis Communications Binarlang GSM Sdn Bhd ASEAN ASEAN 11.9 Technology

26-Mar-01 SingTel Optus Pty LtdSingapore

Telecommunications LtdAustralia ASEAN 9.7 Telecom

05-Dec-12Ping An Insurance Co of

China Ltd

Charoen Pokphand Group

Co LtdChina/HK ASEAN 9.4 Financials

13-Sep-12 Fraser and Neave Ltd Thai Beverage PCL ASEAN ASEAN 8.6 Consumer

Top deals announced of 2016

Top deals closed of 2016

Strictly Confidential

M&A Process and Preparation

12

Strictly Confidential

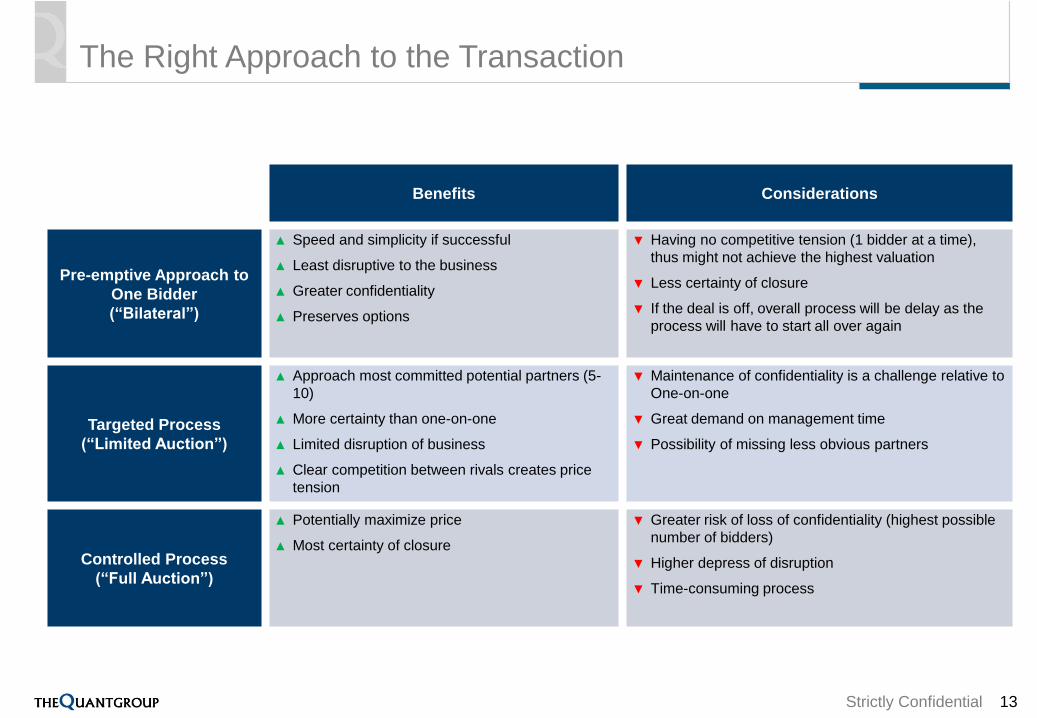

The Right Approach to the Transaction

13

Benefits Considerations

Pre-emptive Approach to

One Bidder

(“Bilateral”)

▲ Speed and simplicity if successful

▲ Least disruptive to the business

▲ Greater confidentiality

▲ Preserves options

▼ Having no competitive tension (1 bidder at a time),

thus might not achieve the highest valuation

▼ Less certainty of closure

▼ If the deal is off, overall process will be delay as the

process will have to start all over again

Targeted Process

(“Limited Auction”)

▲ Approach most committed potential partners (5-

10)

▲ More certainty than one-on-one

▲ Limited disruption of business

▲ Clear competition between rivals creates price

tension

▼ Maintenance of confidentiality is a challenge relative to

One-on-one

▼ Great demand on management time

▼ Possibility of missing less obvious partners

Controlled Process

(“Full Auction”)

▲ Potentially maximize price

▲ Most certainty of closure

▼ Greater risk of loss of confidentiality (highest possible

number of bidders)

▼ Higher depress of disruption

▼ Time-consuming process

Strictly Confidential

Transaction Process Timeline

14

Negotiations Closing

Perform Vender Due Diligence

Data collection and perform the

valuation exercise

Identify transaction rationales

Identify suitable structure

Conduct internal reorganization (if required)

Prepare Definitive

Agreements

Review and negotiate

terms and conditions on

DA

Fulfilling Conditions

Precedent

Sign DA

Tender offer (if required)

Transaction Completion

Approximately 8 weeks Approximately 4 Weeks

Finalize all

agreements

(i.e. SPA,

SHA)

Engage

advisors;

Prepare IM

Completion

Due Diligence by Investor

Non-binding

offer

Provide necessary document in

the dataroom

Q&As from investor, management

interview and / or site visit

Finalize pricing terms and

conditions

Binding offer

Approximately 8 weeks Approximately 4 weeks

ValuationIM

Preparation

Release

IM

Sell Side

Buy Side

Preliminary valuation, strategic

rationale and business due

diligence

Negotiation and preliminary

agree on valuation, major

terms and conditions

Review and negotiate

terms and conditions on

DA

Finalize acquisition

package

Fulfilling Conditions

Precedent

Sign DA

Tender offer (if required)

Transaction Completion

Thorough due diligence

Q&As from investor, management

interview and / or site visit

Finalize pricing

Arrange financing and post-

acquisition plan

Strictly Confidential

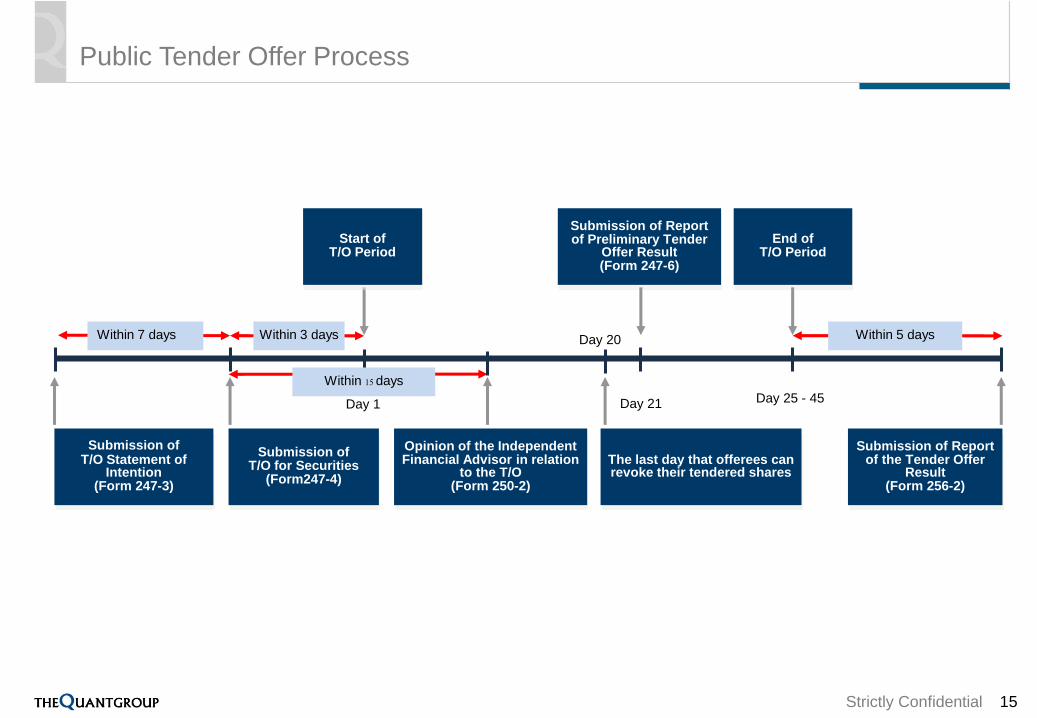

Public Tender Offer Process

15

Within 15 days

Submission of T/O for Securities

(Form247-4)

Within 3 days

Opinion of the Independent Financial Advisor in relation

to the T/O(Form 250-2)

Day 20

Day 21

Submission of Report of Preliminary Tender

Offer Result (Form 247-6)

Day 25 - 45

End of T/O Period

Within 5 days

Submission of Report of the Tender Offer

Result(Form 256-2)

Day 1

Start of T/O Period

Within 7 days

Submission of T/O Statement of

Intention(Form 247-3)

The last day that offerees can revoke their tendered shares

Strictly Confidential

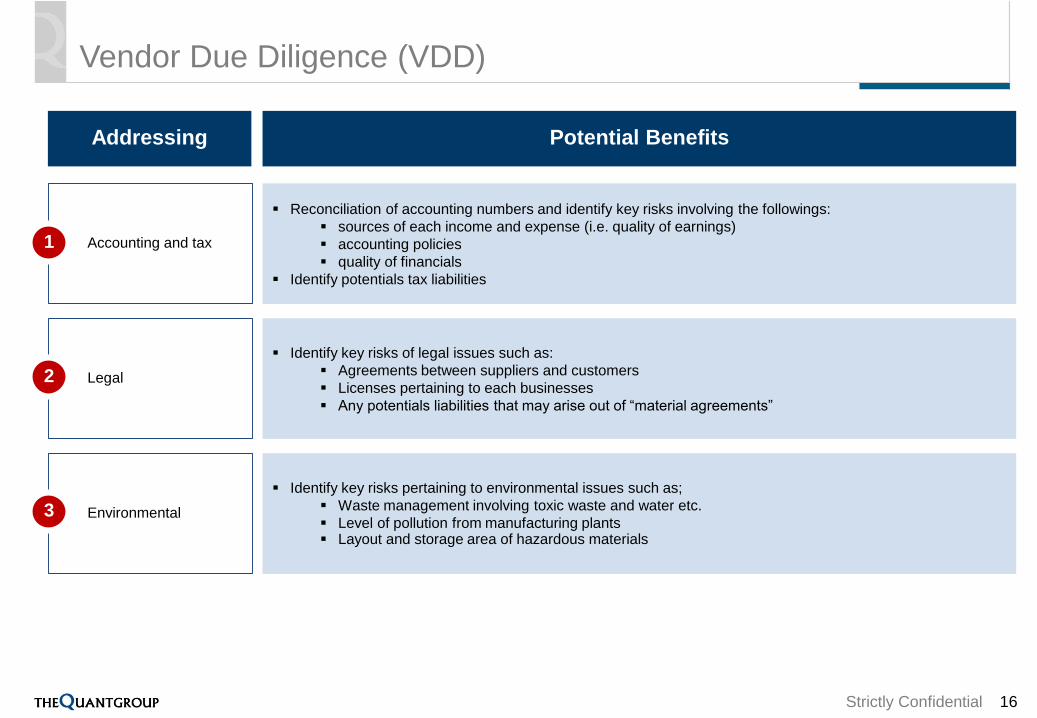

Vendor Due Diligence (VDD)

16

Addressing Potential Benefits

Accounting and tax

Legal

Environmental

Reconciliation of accounting numbers and identify key risks involving the followings:

sources of each income and expense (i.e. quality of earnings)

accounting policies

quality of financials

Identify potentials tax liabilities

Identify key risks of legal issues such as:

Agreements between suppliers and customers

Licenses pertaining to each businesses

Any potentials liabilities that may arise out of “material agreements”

Identify key risks pertaining to environmental issues such as;

Waste management involving toxic waste and water etc.

Level of pollution from manufacturing plants Layout and storage area of hazardous materials

1

2

3

Strictly Confidential

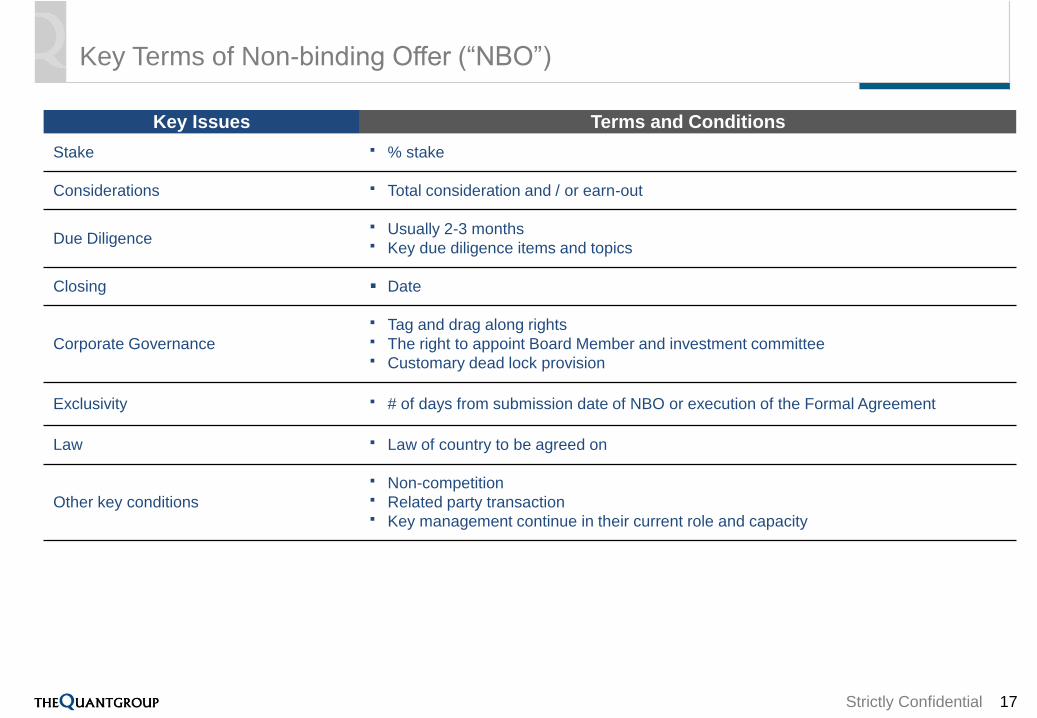

Key Terms of Non-binding Offer (“NBO”)

17

Key Issues Terms and Conditions

Stake % stake

Considerations Total consideration and / or earn-out

Due Diligence Usually 2-3 months Key due diligence items and topics

Closing Date

Corporate Governance

Tag and drag along rights The right to appoint Board Member and investment committee Customary dead lock provision

Exclusivity # of days from submission date of NBO or execution of the Formal Agreement

Law Law of country to be agreed on

Other key conditions

Non-competition Related party transaction Key management continue in their current role and capacity

Strictly Confidential

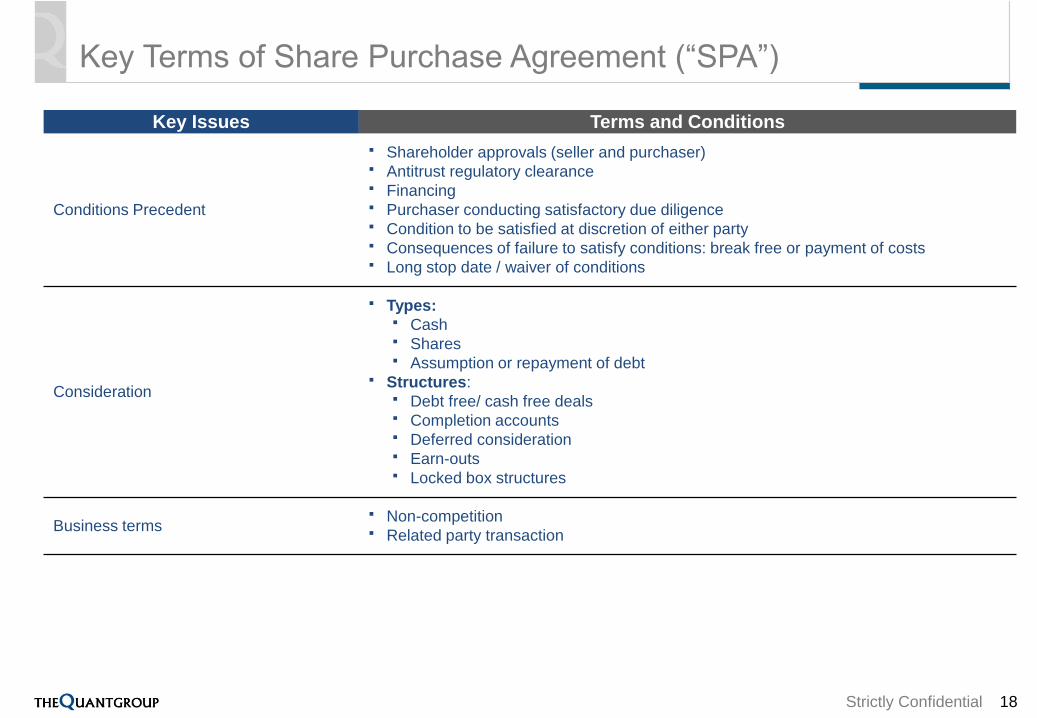

Key Terms of Share Purchase Agreement (“SPA”)

18

Key Issues Terms and Conditions

Conditions Precedent

Shareholder approvals (seller and purchaser) Antitrust regulatory clearance Financing Purchaser conducting satisfactory due diligence Condition to be satisfied at discretion of either party Consequences of failure to satisfy conditions: break free or payment of costs Long stop date / waiver of conditions

Consideration

Types: Cash Shares Assumption or repayment of debt

Structures: Debt free/ cash free deals Completion accounts Deferred consideration Earn-outs Locked box structures

Business terms Non-competition Related party transaction

Strictly Confidential

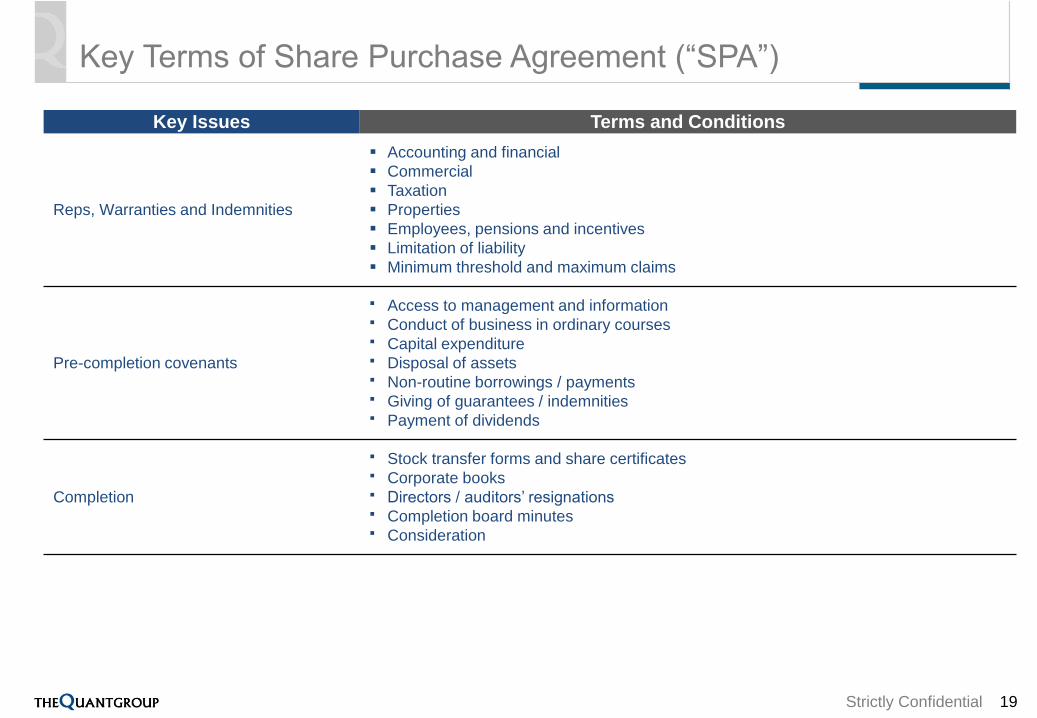

Key Terms of Share Purchase Agreement (“SPA”)

19

Key Issues Terms and Conditions

Reps, Warranties and Indemnities

Accounting and financial

Commercial

Taxation

Properties

Employees, pensions and incentives

Limitation of liability

Minimum threshold and maximum claims

Pre-completion covenants

Access to management and information Conduct of business in ordinary courses Capital expenditure Disposal of assets Non-routine borrowings / payments Giving of guarantees / indemnities Payment of dividends

Completion

Stock transfer forms and share certificates Corporate books Directors / auditors’ resignations Completion board minutes Consideration

Strictly Confidential

Roles of Key Parties

20

Strictly Confidential

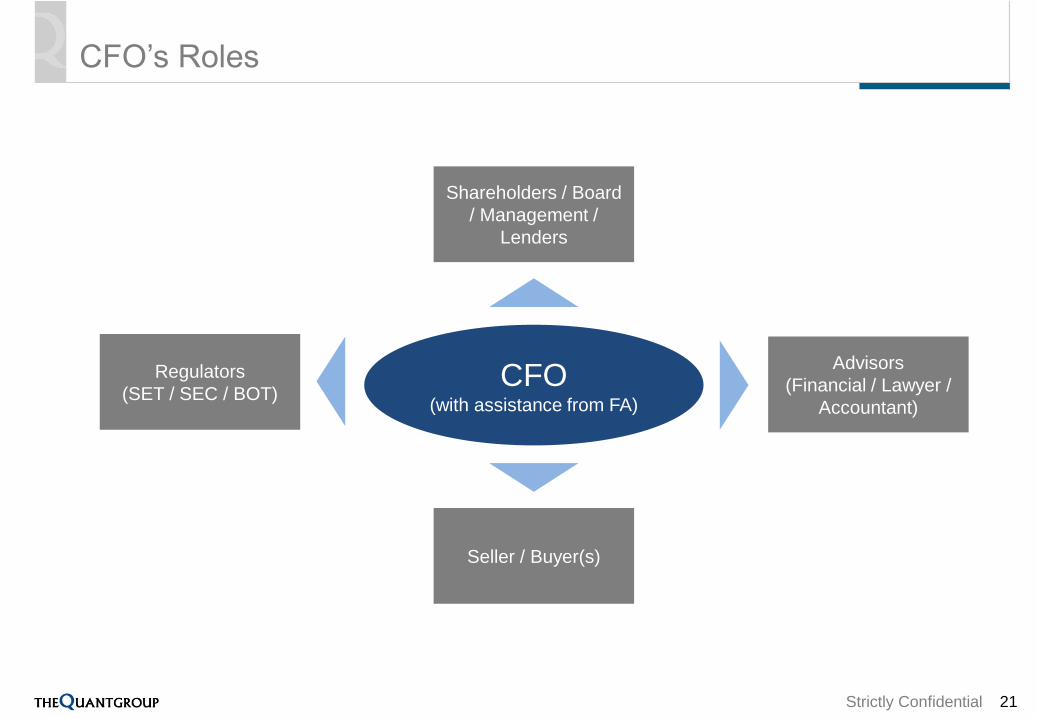

CFO’s Roles

21

CFO(with assistance from FA)

Shareholders / Board

/ Management /

Lenders

Advisors

(Financial / Lawyer /

Accountant)

Seller / Buyer(s)

Regulators

(SET / SEC / BOT)

Strictly Confidential

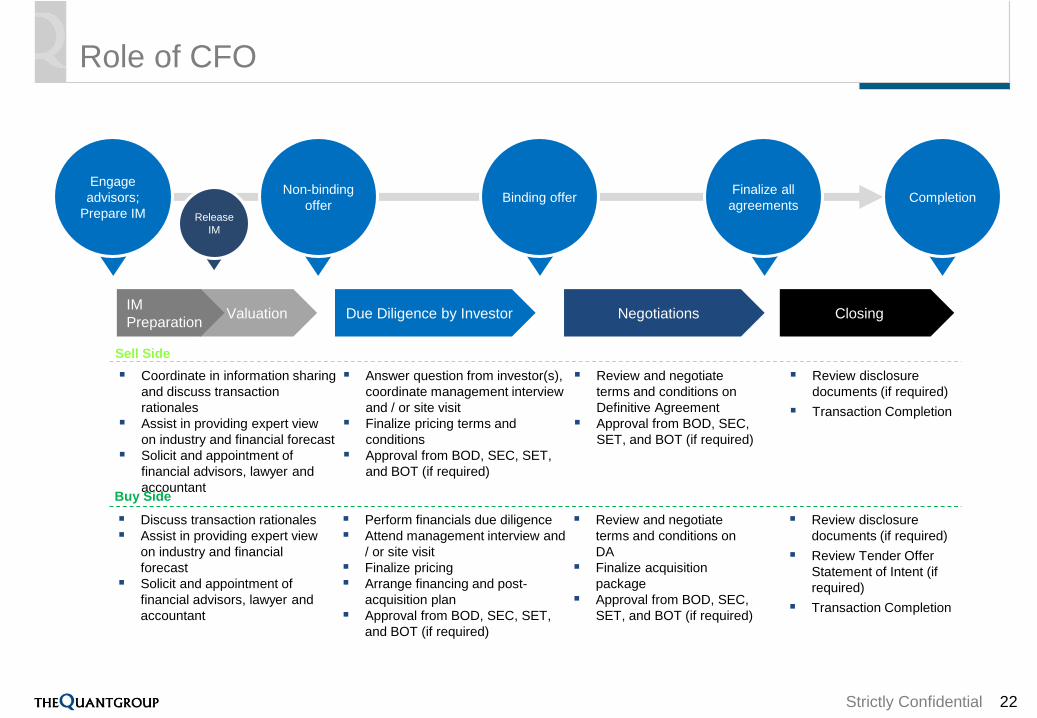

Role of CFO

22

Negotiations Closing

Finalize all

agreements

Engage

advisors;

Prepare IM

Completion

Due Diligence by Investor

Non-binding

offerBinding offer

ValuationIM

Preparation

Release

IM

Coordinate in information sharing

and discuss transaction

rationales

Assist in providing expert view

on industry and financial forecast

Solicit and appointment of

financial advisors, lawyer and

accountant

Review and negotiate

terms and conditions on

Definitive Agreement

Approval from BOD, SEC,

SET, and BOT (if required)

Review disclosure

documents (if required)

Transaction Completion

Answer question from investor(s),

coordinate management interview

and / or site visit

Finalize pricing terms and

conditions

Approval from BOD, SEC, SET,

and BOT (if required)

Sell Side

Buy Side

Discuss transaction rationales

Assist in providing expert view

on industry and financial

forecast

Solicit and appointment of

financial advisors, lawyer and

accountant

Review and negotiate

terms and conditions on

DA

Finalize acquisition

package

Approval from BOD, SEC,

SET, and BOT (if required)

Review disclosure

documents (if required)

Review Tender Offer

Statement of Intent (if

required)

Transaction Completion

Perform financials due diligence

Attend management interview and

/ or site visit

Finalize pricing

Arrange financing and post-

acquisition plan

Approval from BOD, SEC, SET,

and BOT (if required)

Strictly Confidential

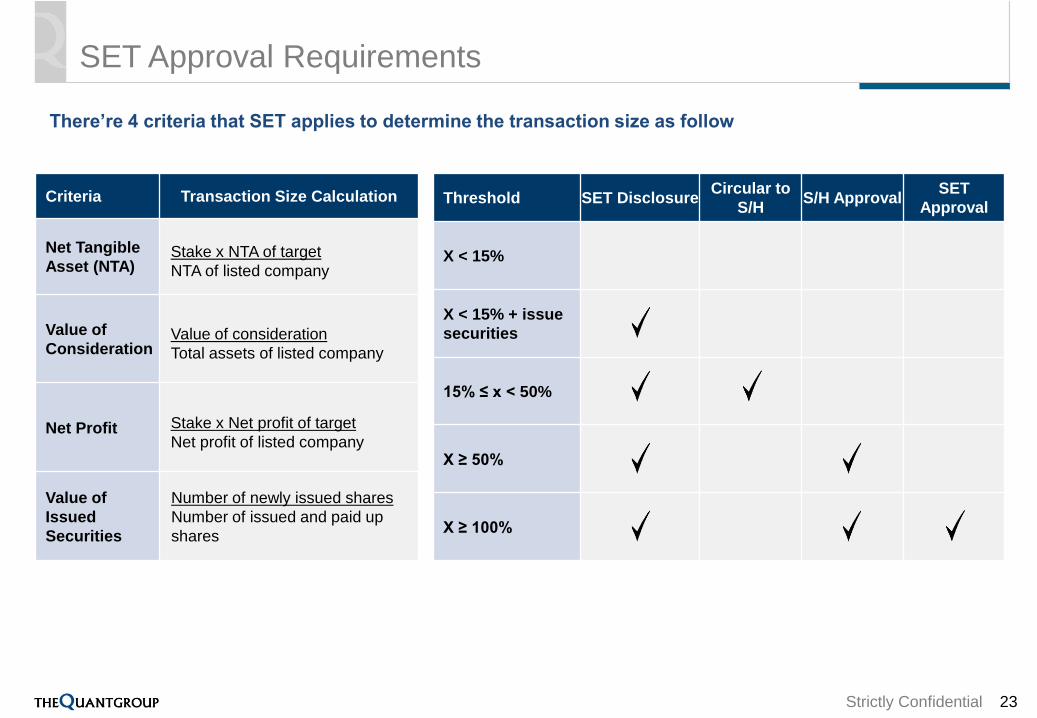

SET Approval Requirements

There’re 4 criteria that SET applies to determine the transaction size as follow

23

Criteria Transaction Size Calculation

Net Tangible

Asset (NTA)Stake x NTA of target

NTA of listed company

Value of

ConsiderationValue of consideration

Total assets of listed company

Net Profit Stake x Net profit of target

Net profit of listed company

Value of

Issued

Securities

Number of newly issued shares

Number of issued and paid up

shares

Threshold SET DisclosureCircular to

S/HS/H Approval

SET

Approval

X < 15%

X < 15% + issue

securities

15% ≤ x < 50%

X ≥ 50%

X ≥ 100%

Strictly Confidential

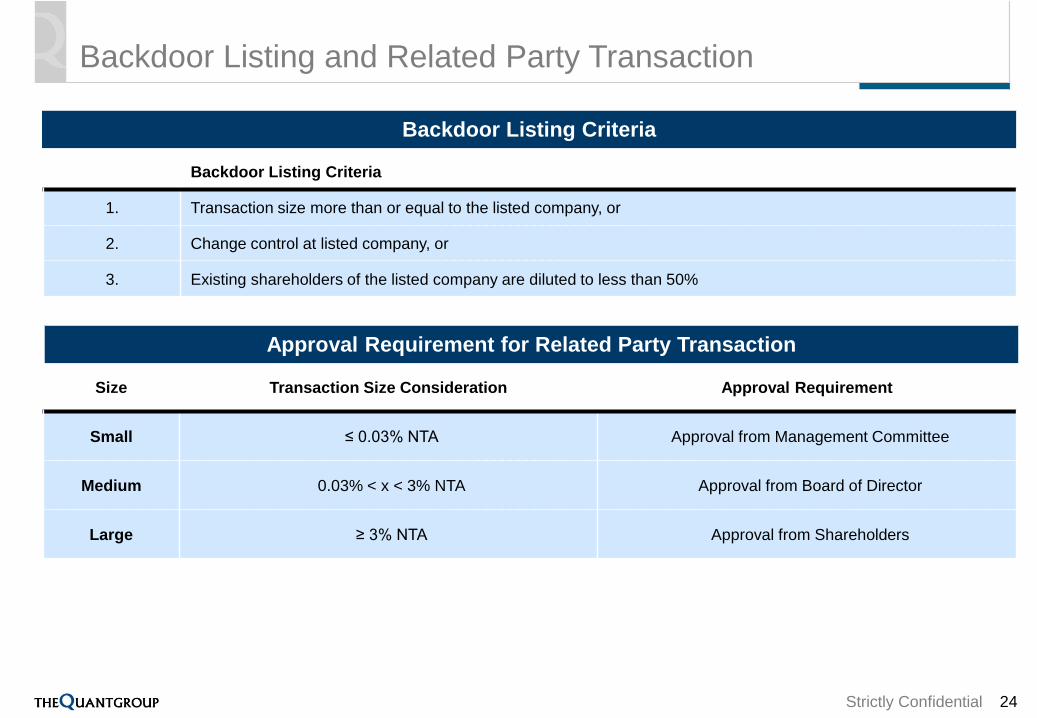

Backdoor Listing and Related Party Transaction

24

Backdoor Listing Criteria

1. Transaction size more than or equal to the listed company, or

2. Change control at listed company, or

3. Existing shareholders of the listed company are diluted to less than 50%

Size Transaction Size Consideration Approval Requirement

Small ≤ 0.03% NTA Approval from Management Committee

Medium 0.03% < x < 3% NTA Approval from Board of Director

Large ≥ 3% NTA Approval from Shareholders

Backdoor Listing Criteria

Approval Requirement for Related Party Transaction

Strictly Confidential

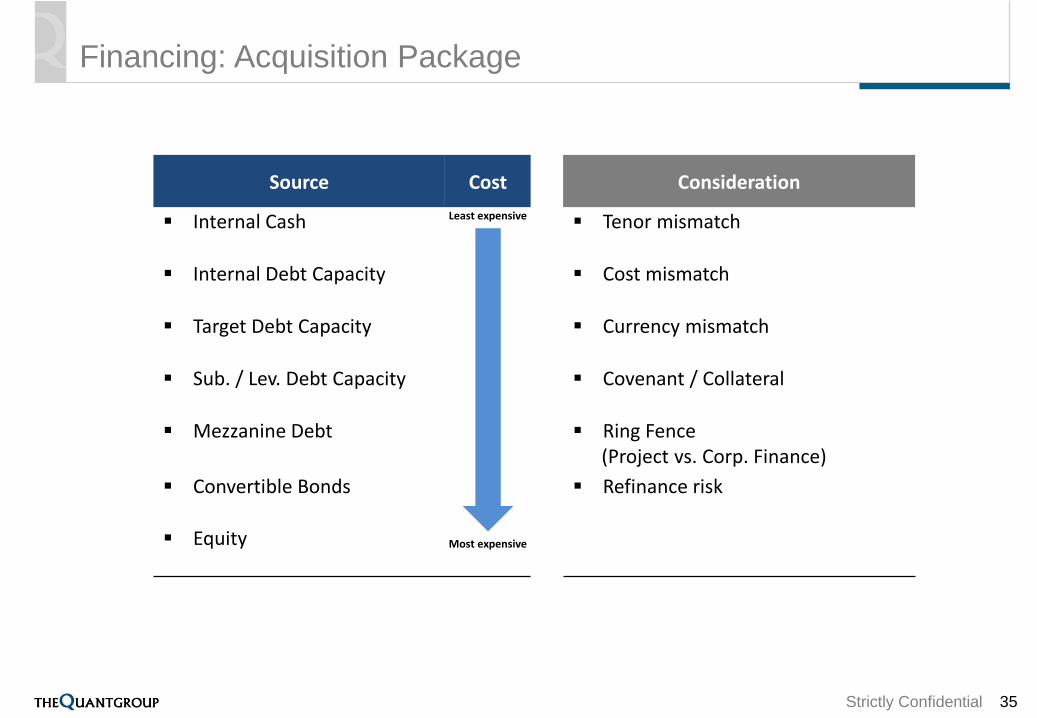

Financing Considerations

Company’s repayment capability

Company’s current restricted covenants

Security offered

Long-term capital structure

Future financing requirements

Degree of flexibility Matching principle

Principal repayment options

25

Strictly Confidential

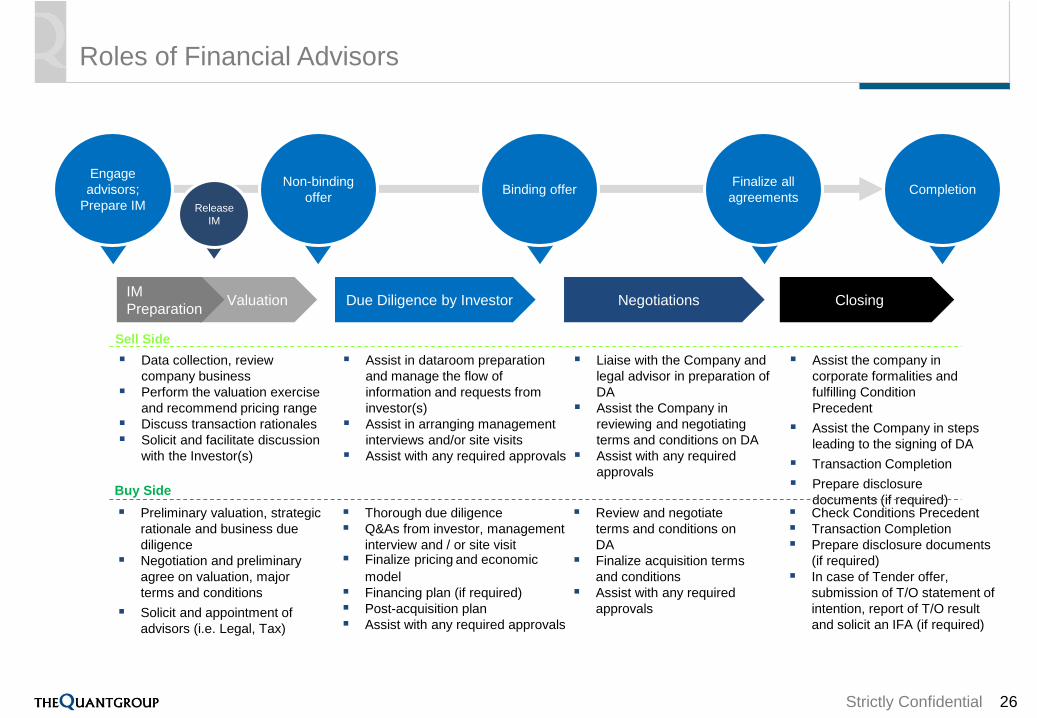

Roles of Financial Advisors

26

Negotiations Closing

Finalize all

agreements

Engage

advisors;

Prepare IM

Completion

Due Diligence by Investor

Non-binding

offerBinding offer

ValuationIM

Preparation

Release

IM

Data collection, review

company business

Perform the valuation exercise

and recommend pricing range

Discuss transaction rationales

Solicit and facilitate discussion

with the Investor(s)

Liaise with the Company and

legal advisor in preparation of

DA

Assist the Company in

reviewing and negotiating

terms and conditions on DA

Assist with any required

approvals

Assist the company in

corporate formalities and

fulfilling Condition

Precedent

Assist the Company in steps

leading to the signing of DA

Transaction Completion

Prepare disclosure

documents (if required)

Assist in dataroom preparation

and manage the flow of

information and requests from

investor(s)

Assist in arranging management

interviews and/or site visits

Assist with any required approvals

Sell Side

Buy Side

Preliminary valuation, strategic

rationale and business due

diligence

Negotiation and preliminary

agree on valuation, major

terms and conditions

Solicit and appointment of

advisors (i.e. Legal, Tax)

Review and negotiate

terms and conditions on

DA

Finalize acquisition terms

and conditions

Assist with any required

approvals

Check Conditions Precedent

Transaction Completion

Prepare disclosure documents

(if required)

In case of Tender offer,

submission of T/O statement of

intention, report of T/O result

and solicit an IFA (if required)

Thorough due diligence

Q&As from investor, management

interview and / or site visit Finalize pricing and economic

model

Financing plan (if required)

Post-acquisition plan

Assist with any required approvals

Strictly Confidential

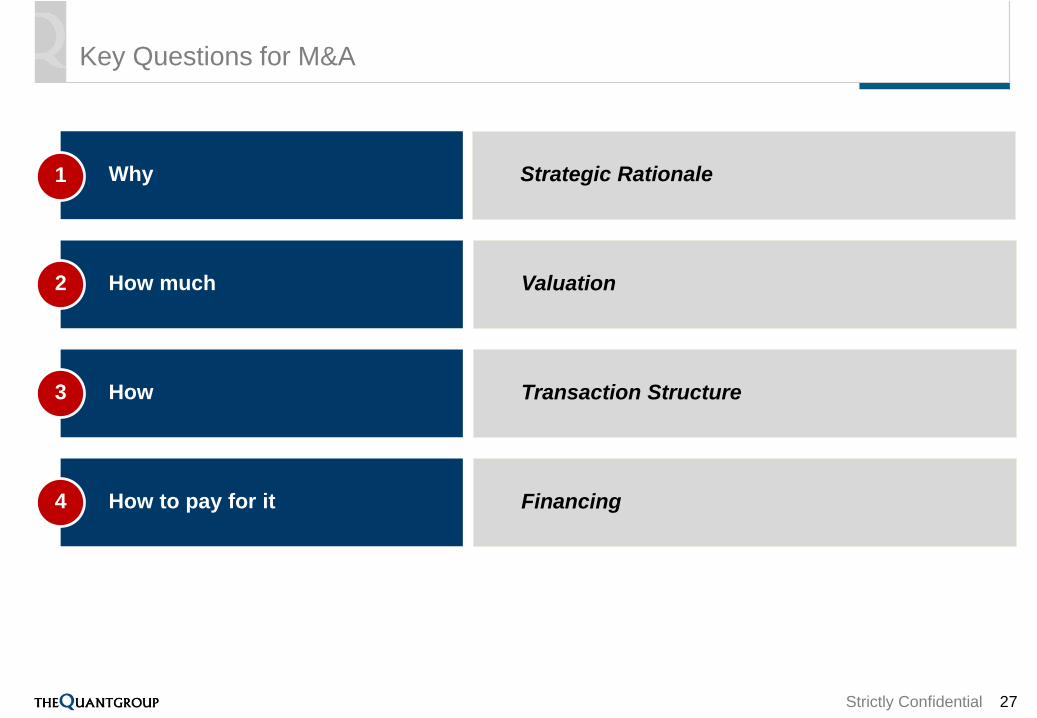

Key Questions for M&A

27

Strategic Rationale

Valuation

Transaction Structure

Financing

Why

How much

How

How to pay for it

1

2

3

4

Strictly Confidential

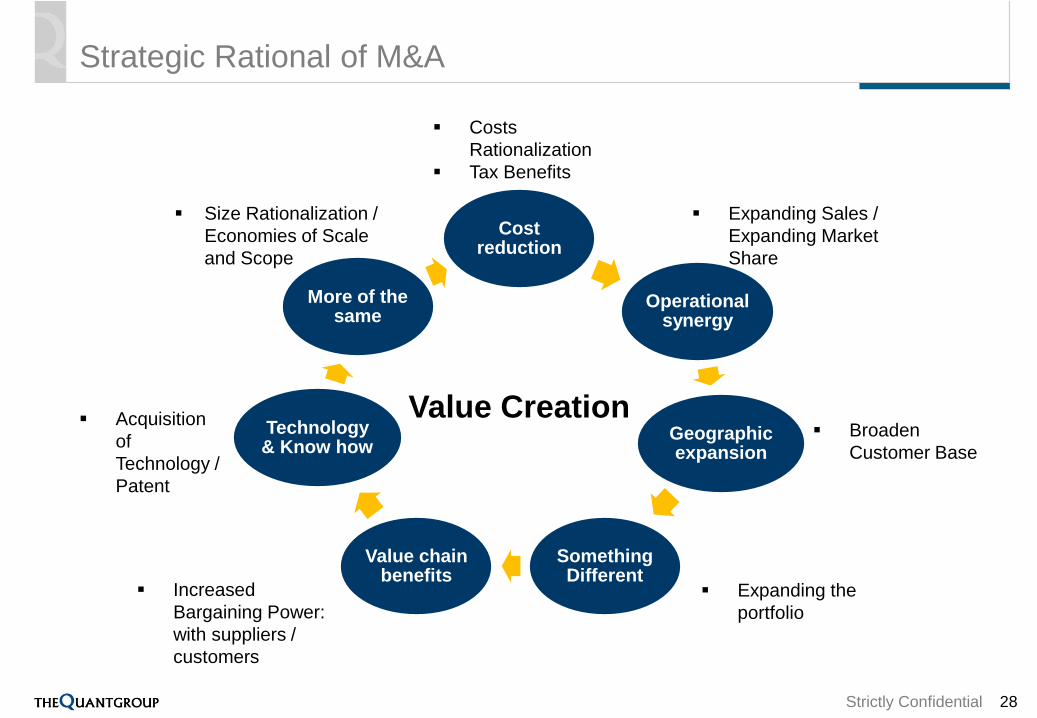

Strategic Rational of M&A

28

Cost reduction

Operational synergy

Geographic expansion

Something Different

Value chain benefits

Technology & Know how

More of the same

Value Creation Acquisition

of

Technology /

Patent

Increased

Bargaining Power:

with suppliers /

customers

Expanding Sales /

Expanding Market

Share

Broaden

Customer Base

Size Rationalization /

Economies of Scale

and Scope

Costs

Rationalization

Tax Benefits

Expanding the

portfolio

Strictly Confidential

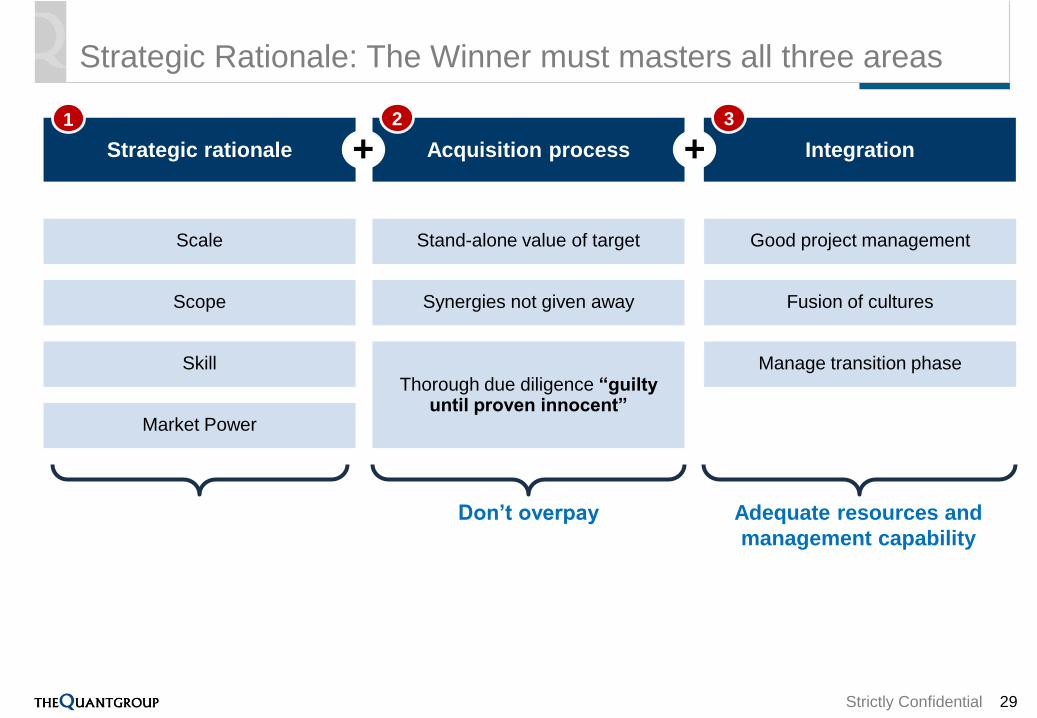

Strategic Rationale: The Winner must masters all three areas

29

Strategic rationale Acquisition process+ Integration+

Don’t overpay Adequate resources and

management capability

Scale

Scope

Market Power

Skill

Stand-alone value of target

Synergies not given away

Thorough due diligence “guilty until proven innocent”

Good project management

Fusion of cultures

Manage transition phase

1 2 3

Strictly Confidential

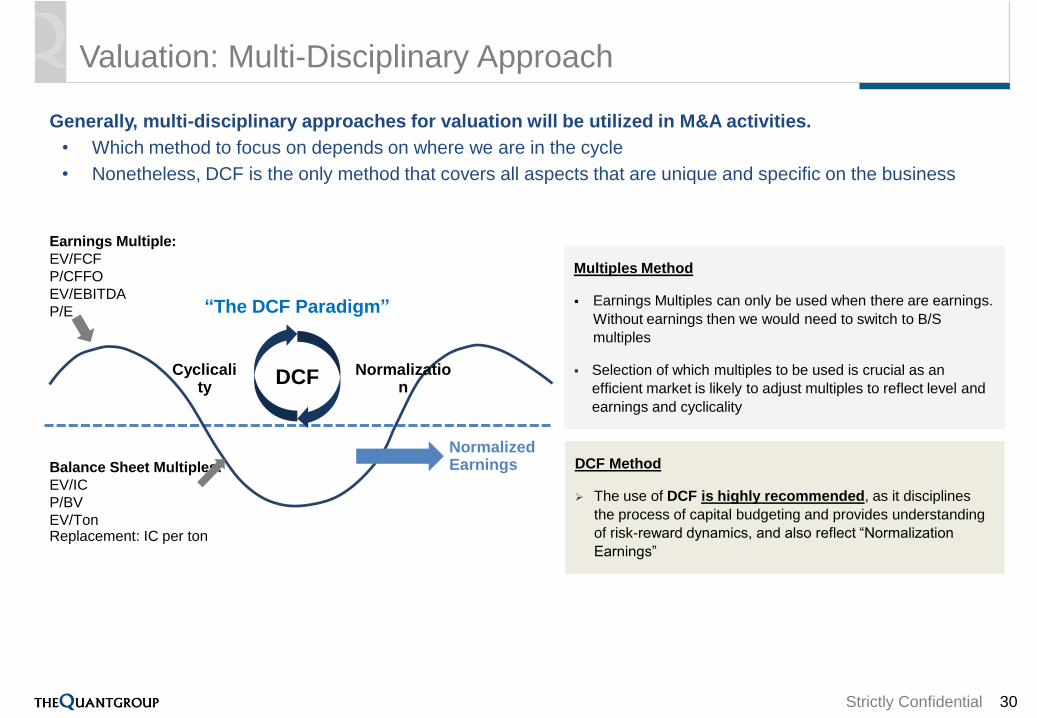

Valuation: Multi-Disciplinary Approach

Generally, multi-disciplinary approaches for valuation will be utilized in M&A activities.

• Which method to focus on depends on where we are in the cycle

• Nonetheless, DCF is the only method that covers all aspects that are unique and specific on the business

30

Multiples Method

Earnings Multiples can only be used when there are earnings.

Without earnings then we would need to switch to B/S

multiples

Selection of which multiples to be used is crucial as an

efficient market is likely to adjust multiples to reflect level and

earnings and cyclicality

DCF Method

The use of DCF is highly recommended, as it disciplines

the process of capital budgeting and provides understanding

of risk-reward dynamics, and also reflect “Normalization

Earnings”

Balance Sheet Multiples:

EV/IC

P/BV

EV/TonReplacement: IC per ton

Earnings Multiple:

EV/FCF

P/CFFO

EV/EBITDA

P/E

Normalized Earnings

DCFCyclicality

Normalization

“The DCF Paradigm”

Strictly Confidential

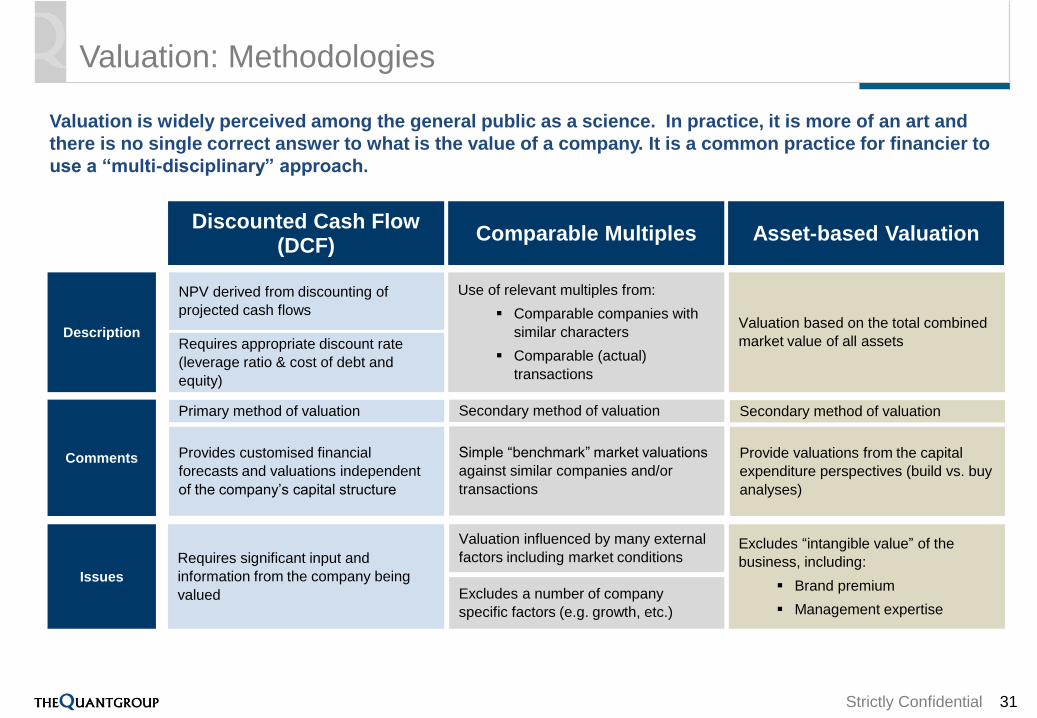

Valuation: Methodologies

Valuation is widely perceived among the general public as a science. In practice, it is more of an art and

there is no single correct answer to what is the value of a company. It is a common practice for financier to

use a “multi-disciplinary” approach.

31

Description

Comments

Requires significant input and

information from the company being

valued

Issues

Discounted Cash Flow (DCF)

Comparable Multiples Asset-based Valuation

NPV derived from discounting of

projected cash flows

Requires appropriate discount rate

(leverage ratio & cost of debt and

equity)

Primary method of valuation

Provides customised financial

forecasts and valuations independent

of the company’s capital structure

Use of relevant multiples from:

Comparable companies with

similar characters

Comparable (actual)

transactions

Secondary method of valuation

Simple “benchmark” market valuations

against similar companies and/or

transactions

Valuation influenced by many external

factors including market conditions

Excludes a number of company

specific factors (e.g. growth, etc.)

Valuation based on the total combined

market value of all assets

Secondary method of valuation

Provide valuations from the capital

expenditure perspectives (build vs. buy

analyses)

Excludes “intangible value” of the

business, including:

Brand premium

Management expertise

Strictly Confidential

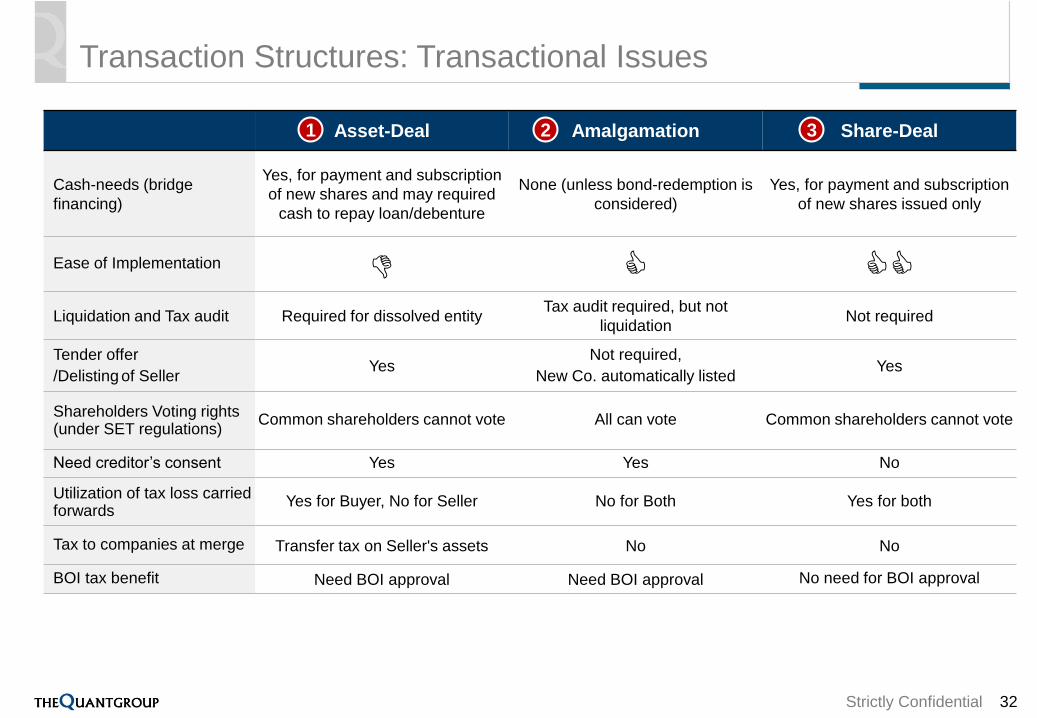

Transaction Structures: Transactional Issues

32

Asset-Deal Amalgamation Share-Deal

Cash-needs (bridge

financing)

Yes, for payment and subscription

of new shares and may required

cash to repay loan/debenture

None (unless bond-redemption is

considered)

Yes, for payment and subscription

of new shares issued only

Ease of Implementation

Liquidation and Tax audit Required for dissolved entityTax audit required, but not

liquidationNot required

Tender offer

/Delisting of SellerYes

Not required,

New Co. automatically listedYes

Shareholders Voting rights (under SET regulations)

Common shareholders cannot vote All can vote Common shareholders cannot vote

Need creditor’s consent Yes Yes No

Utilization of tax loss carried forwards

Yes for Buyer, No for Seller No for Both Yes for both

Tax to companies at merge Transfer tax on Seller's assets No No

BOI tax benefit Need BOI approval Need BOI approval No need for BOI approval

1 2 3

Strictly Confidential

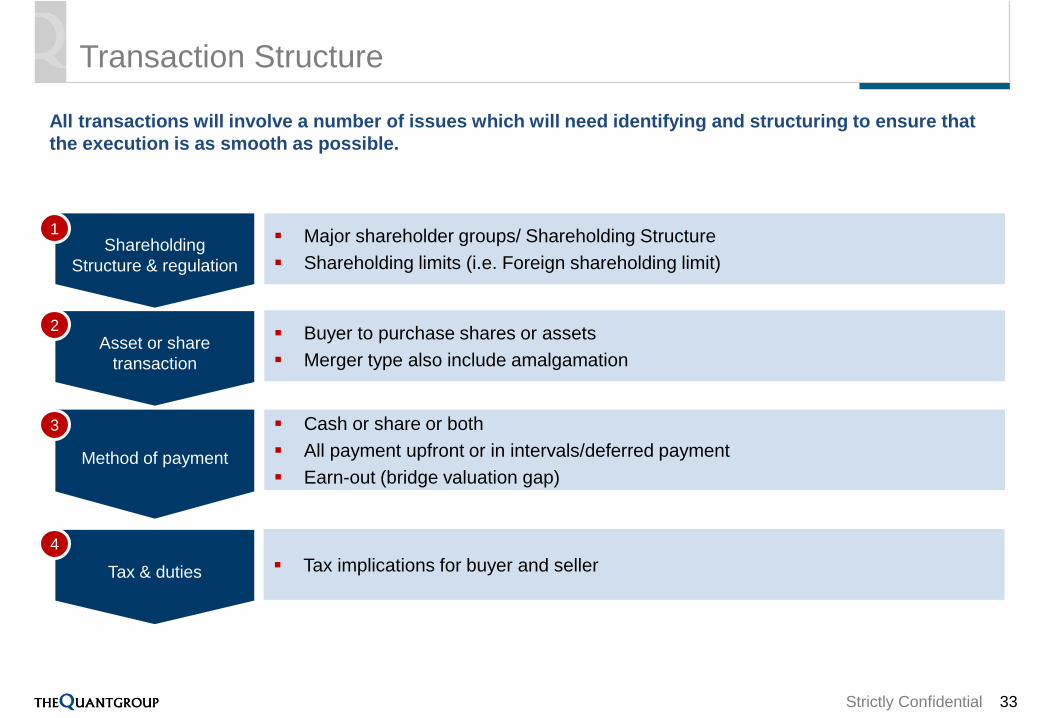

Transaction Structure

All transactions will involve a number of issues which will need identifying and structuring to ensure that

the execution is as smooth as possible.

33

Shareholding

Structure & regulation

Asset or share

transaction

Method of payment

Tax & duties

1

2

3

4

Major shareholder groups/ Shareholding Structure

Shareholding limits (i.e. Foreign shareholding limit)

Buyer to purchase shares or assets

Merger type also include amalgamation

Cash or share or both

All payment upfront or in intervals/deferred payment

Earn-out (bridge valuation gap)

Tax implications for buyer and seller

Strictly Confidential

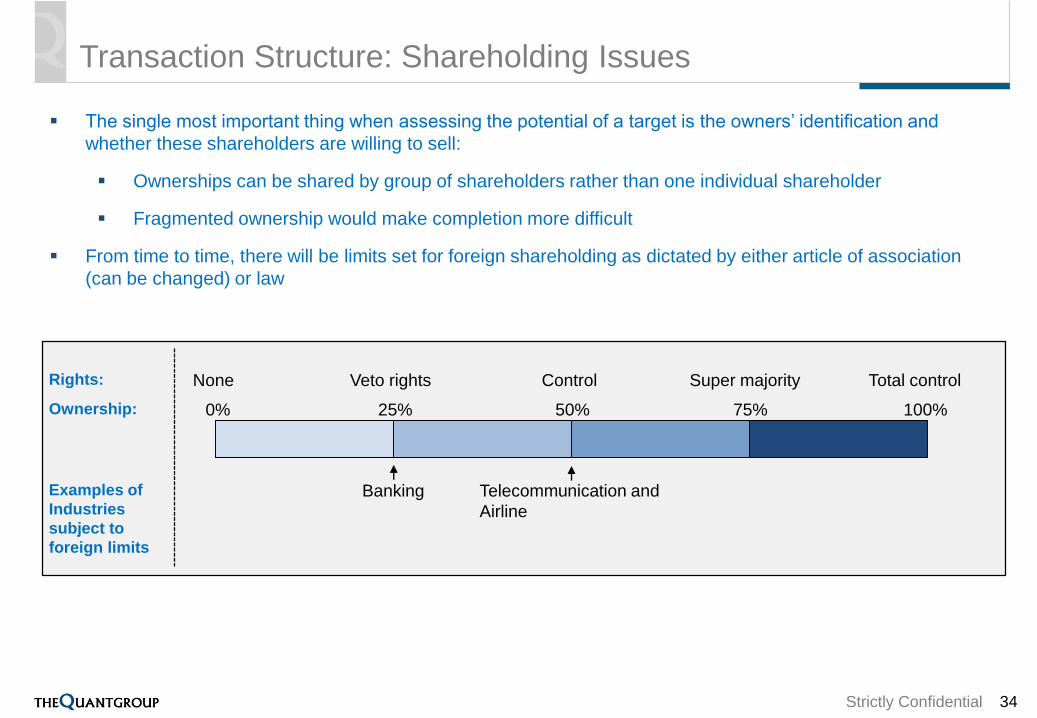

Transaction Structure: Shareholding Issues

The single most important thing when assessing the potential of a target is the owners’ identification and

whether these shareholders are willing to sell:

Ownerships can be shared by group of shareholders rather than one individual shareholder

Fragmented ownership would make completion more difficult

From time to time, there will be limits set for foreign shareholding as dictated by either article of association

(can be changed) or law

34

0% 25% 50% 75% 100%

Veto rights Control Super majority Total controlRights:

Ownership:

None

Examples of

Industries

subject to

foreign limits

Banking Telecommunication and

Airline

Strictly Confidential

Financing: Acquisition Package

35

Source Cost Consideration

Internal Cash Least expensive Tenor mismatch

Internal Debt Capacity Cost mismatch

Target Debt Capacity Currency mismatch

Sub. / Lev. Debt Capacity Covenant / Collateral

Mezzanine Debt Ring Fence (Project vs. Corp. Finance)

Convertible Bonds Refinance risk

Equity Most expensive

Strictly Confidential

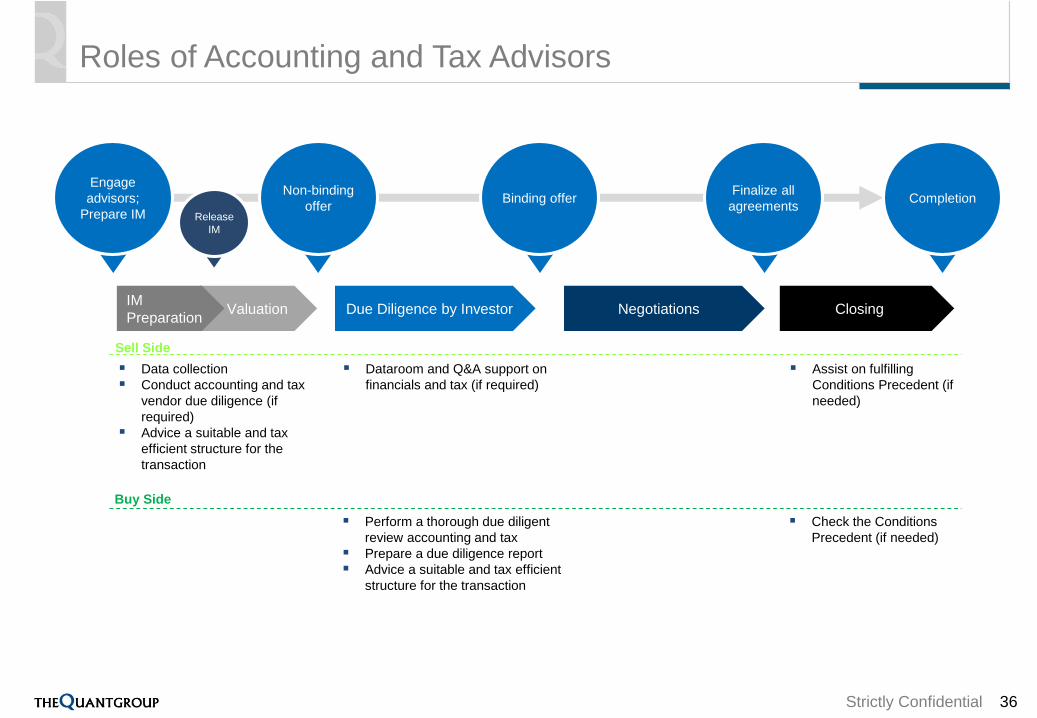

Roles of Accounting and Tax Advisors

36

Negotiations Closing

Finalize all

agreements

Engage

advisors;

Prepare IM

Completion

Due Diligence by Investor

Non-binding

offerBinding offer

ValuationIM

Preparation

Release

IM

Data collection

Conduct accounting and tax

vendor due diligence (if

required)

Advice a suitable and tax

efficient structure for the

transaction

Assist on fulfilling

Conditions Precedent (if

needed)

Dataroom and Q&A support on

financials and tax (if required)

Sell Side

Buy Side

Perform a thorough due diligent

review accounting and tax

Prepare a due diligence report

Advice a suitable and tax efficient

structure for the transaction

Check the Conditions

Precedent (if needed)

Strictly Confidential

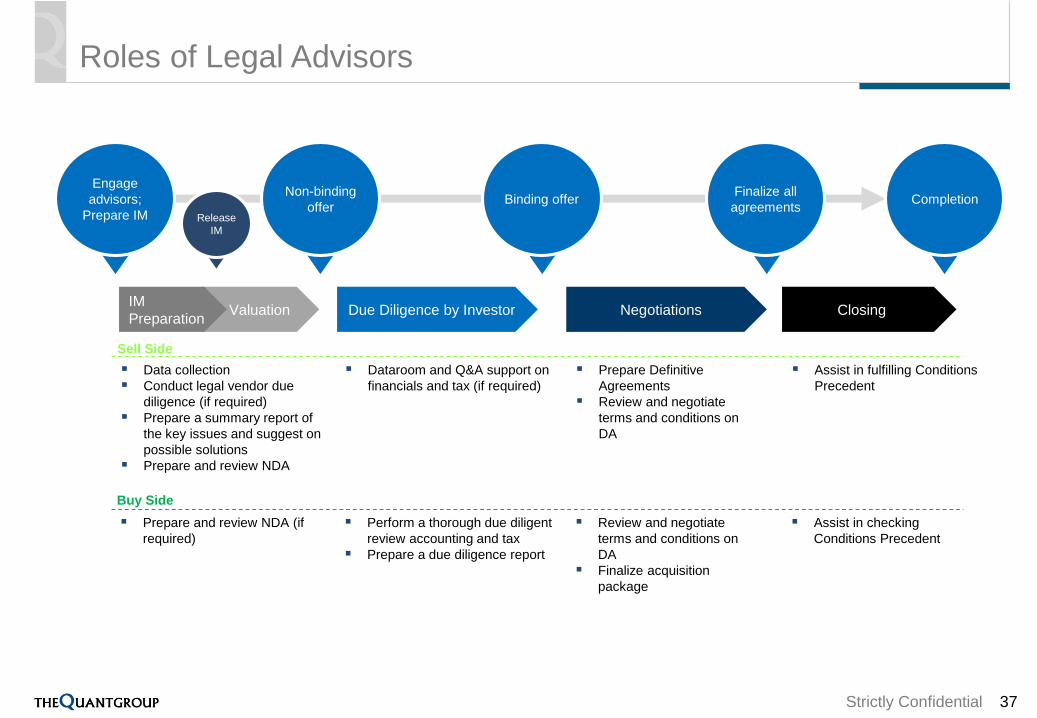

Roles of Legal Advisors

37

Negotiations Closing

Finalize all

agreements

Engage

advisors;

Prepare IM

Completion

Due Diligence by Investor

Non-binding

offerBinding offer

ValuationIM

Preparation

Release

IM

Data collection

Conduct legal vendor due

diligence (if required)

Prepare a summary report of

the key issues and suggest on

possible solutions

Prepare and review NDA

Prepare Definitive

Agreements

Review and negotiate

terms and conditions on

DA

Assist in fulfilling Conditions

Precedent

Dataroom and Q&A support on

financials and tax (if required)

Sell Side

Buy Side

Prepare and review NDA (if

required)

Review and negotiate

terms and conditions on

DA

Finalize acquisition

package

Assist in checking

Conditions Precedent

Perform a thorough due diligent

review accounting and tax

Prepare a due diligence report

Strictly Confidential

Key Success Factors

38

Strictly Confidential

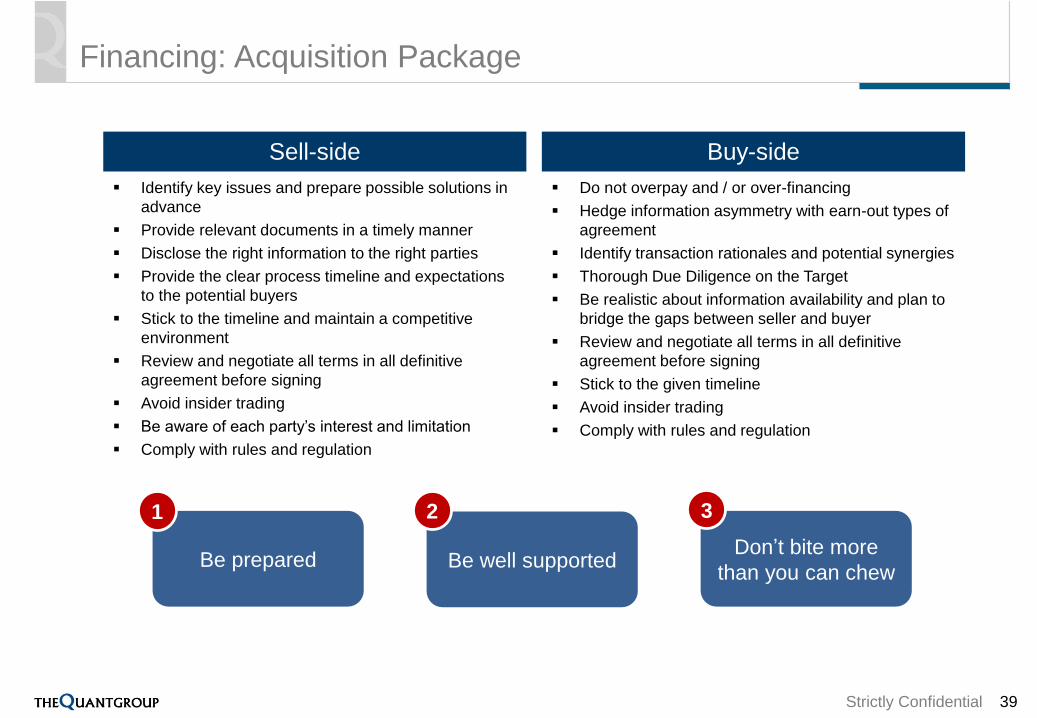

Financing: Acquisition Package

39

Sell-side

Identify key issues and prepare possible solutions in

advance

Provide relevant documents in a timely manner

Disclose the right information to the right parties

Provide the clear process timeline and expectations

to the potential buyers

Stick to the timeline and maintain a competitive

environment

Review and negotiate all terms in all definitive

agreement before signing

Avoid insider trading

Be aware of each party’s interest and limitation

Comply with rules and regulation

Buy-side

Do not overpay and / or over-financing

Hedge information asymmetry with earn-out types of

agreement

Identify transaction rationales and potential synergies

Thorough Due Diligence on the Target

Be realistic about information availability and plan to

bridge the gaps between seller and buyer

Review and negotiate all terms in all definitive

agreement before signing

Stick to the given timeline

Avoid insider trading

Comply with rules and regulation

Be prepared Be well supportedDon’t bite more

than you can chew

1 2 3

Strictly Confidential

Case Study: Asia Aviation

Strictly Confidential

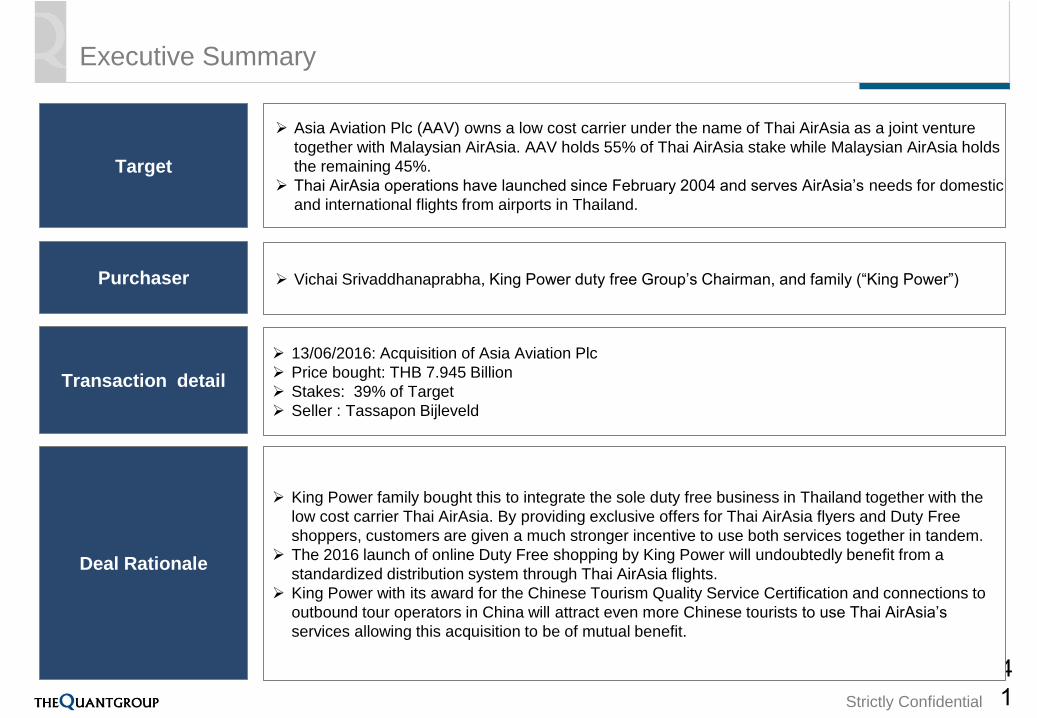

Executive Summary

4

1

Target

Purchaser

Transaction detail

Asia Aviation Plc (AAV) owns a low cost carrier under the name of Thai AirAsia as a joint venture

together with Malaysian AirAsia. AAV holds 55% of Thai AirAsia stake while Malaysian AirAsia holds

the remaining 45%.

Thai AirAsia operations have launched since February 2004 and serves AirAsia’s needs for domestic

and international flights from airports in Thailand.

Vichai Srivaddhanaprabha, King Power duty free Group’s Chairman, and family (“King Power”)

13/06/2016: Acquisition of Asia Aviation Plc

Price bought: THB 7.945 Billion

Stakes: 39% of Target

Seller : Tassapon Bijleveld

Deal Rationale

King Power family bought this to integrate the sole duty free business in Thailand together with the

low cost carrier Thai AirAsia. By providing exclusive offers for Thai AirAsia flyers and Duty Free

shoppers, customers are given a much stronger incentive to use both services together in tandem.

The 2016 launch of online Duty Free shopping by King Power will undoubtedly benefit from a

standardized distribution system through Thai AirAsia flights.

King Power with its award for the Chinese Tourism Quality Service Certification and connections to

outbound tour operators in China will attract even more Chinese tourists to use Thai AirAsia’s

services allowing this acquisition to be of mutual benefit.

Strictly Confidential

Company Overview: Asia Aviation Public Company Limited

Company Overview

Asia Aviation Public Company Limited (“AAV”) provides airline

services primarily in Thailand

AAV operates through traditional Scheduled Flight Operations and

Charter Flight Operations

Shareholding Structure

4

2Source: Company Information, Bloomberg 16 September 2016

THB bn FY2013 FY2014 FY2015 LTM

Revenue 23.5 25.4 29.5 31.6

EBITDA 2.2 0.5 4.3 5.8

Margin 9.4% 2.2% 14.6% 18.3%

Net Income 1.0 0.2 1.1 1.8

Margin 4.4% 0.7% 3.7% 5.7%

Global Presence – Flight Routes

Key Financials

Market Statistics FY2015 LTM

Market Capitalization 25.5 34.0

Enterprise Value 40.2 48.5

Implied multiples

P / E 23.6 x 19.0 x

EV / EBITDA 9.3 x 8.4 x

Pre-Acquisition

Headquartered in

Bangkok, Thailand

Post-Acquisition

AirAsia Investment

Foreign Investors

Asia Aviation Plc

Thai AirAsia

Thai AirAsia Flights

• 364 International Flights

to 21 Destinations

• 665 Domestic Flights to

20 Destinations

Fleet Size

• Total of 45 Airbus A320

Thai ManagementAirAsia Berhad

100%

45%

45% 55%

55%

AirAsia Investment

Foreign Investors

Asia Aviation Plc

Thai AirAsia

Thai ManagementAirAsia Berhad

100%

45%

6% 55%

55%

King Power Family

39%

Strictly Confidential

Big C’s acquisition of Carrefour Thailand

Strictly Confidential

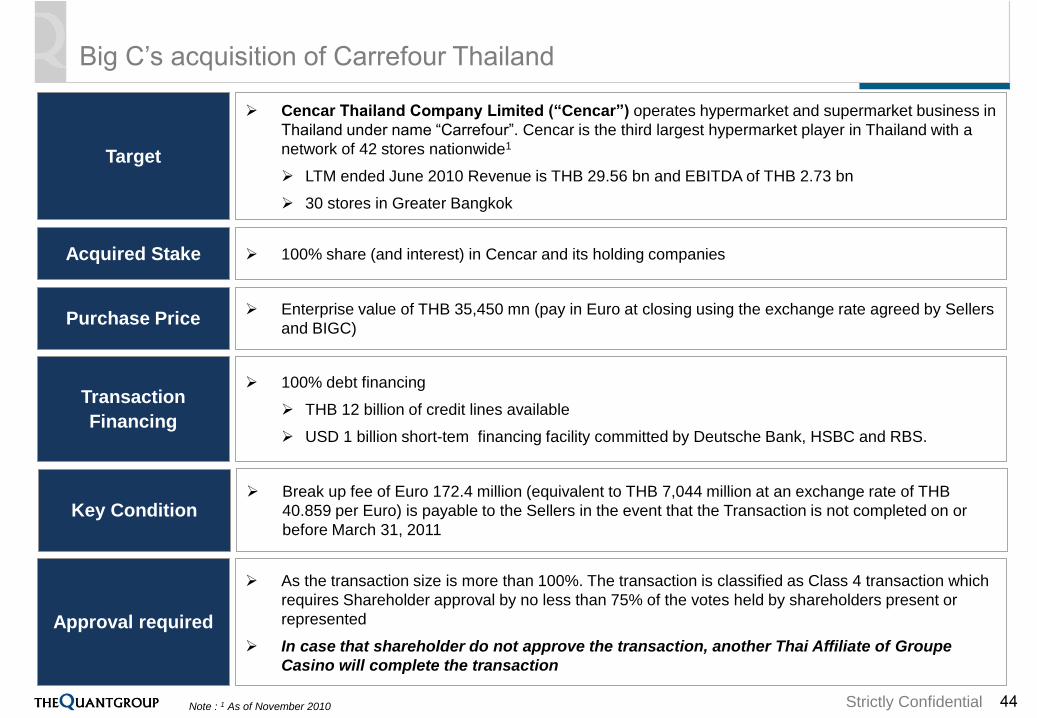

Big C’s acquisition of Carrefour Thailand

Cencar Thailand Company Limited (“Cencar”) operates hypermarket and supermarket business in

Thailand under name “Carrefour”. Cencar is the third largest hypermarket player in Thailand with a

network of 42 stores nationwide1

LTM ended June 2010 Revenue is THB 29.56 bn and EBITDA of THB 2.73 bn

30 stores in Greater Bangkok

Target

Enterprise value of THB 35,450 mn (pay in Euro at closing using the exchange rate agreed by Sellers

and BIGC) Purchase Price

As the transaction size is more than 100%. The transaction is classified as Class 4 transaction which

requires Shareholder approval by no less than 75% of the votes held by shareholders present or

represented

In case that shareholder do not approve the transaction, another Thai Affiliate of Groupe

Casino will complete the transaction

Approval required

44Note : 1 As of November 2010

100% share (and interest) in Cencar and its holding companies Acquired Stake

100% debt financing

THB 12 billion of credit lines available

USD 1 billion short-tem financing facility committed by Deutsche Bank, HSBC and RBS.

Transaction

Financing

Break up fee of Euro 172.4 million (equivalent to THB 7,044 million at an exchange rate of THB

40.859 per Euro) is payable to the Sellers in the event that the Transaction is not completed on or

before March 31, 2011 Key Condition

Strictly Confidential

Benefits of the Transaction

Acquisition of 42 stores will bring the number of Big C stores to 113

Market share will increase from 13% to 19%

Net sales will increase by 42%

Improved bargaining power with suppliers through increased scale and network

Increase Big C’s

bargaining power

with suppliers

Acquisition of 37 new shopping centers increase Big C’s shopping center to over 106 in total

Increased scale to add more value creative opportunities

Accelerate the dual

retail-property

model

Store conversion and centralized planning will result in revenue increase

Improved purchasing conditions with a significant increase in buying volume

Shared service and infrastructure will lead to SG&A reduction

Implement

significant

synergies

Bangkok is highly competitive market for Retailers

Suitable locations for expansion are limited

The acquisition of 30 Carrefour stores in Bangkok will double Big C’s presence in Bangkok

Enhance network in

Greater Bangkok

Carrefour targets mid-to-high income vs Big C’s mid-to-low income

Big C will be able to penetrate into new customer segment

Capture new

customer segment

1

2

3

4

5

45

Strictly Confidential

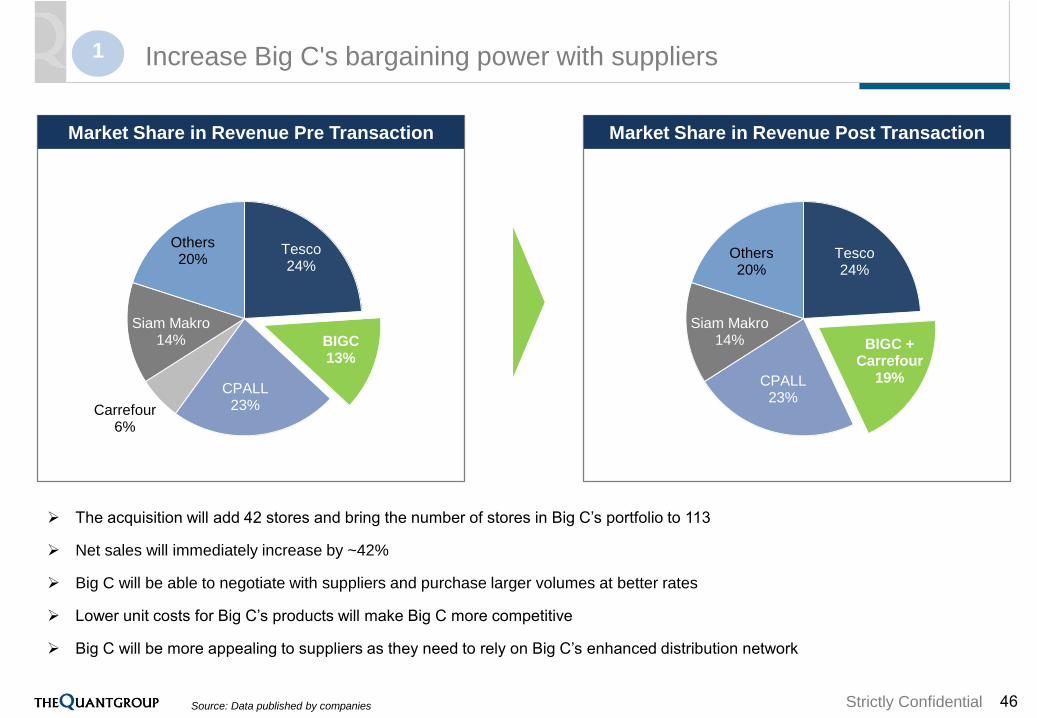

The acquisition will add 42 stores and bring the number of stores in Big C’s portfolio to 113

Net sales will immediately increase by ~42%

Big C will be able to negotiate with suppliers and purchase larger volumes at better rates

Lower unit costs for Big C’s products will make Big C more competitive

Big C will be more appealing to suppliers as they need to rely on Big C’s enhanced distribution network

Tesco 24%

BIGC13%

CPALL23%Carrefour

6%

Siam Makro14%

Others20% Tesco

24%

BIGC + Carrefour

19%CPALL23%

Siam Makro14%

Others20%

Source: Data published by companies

Market Share in Revenue Pre Transaction Market Share in Revenue Post Transaction

46

Increase Big C's bargaining power with suppliers1

Strictly Confidential

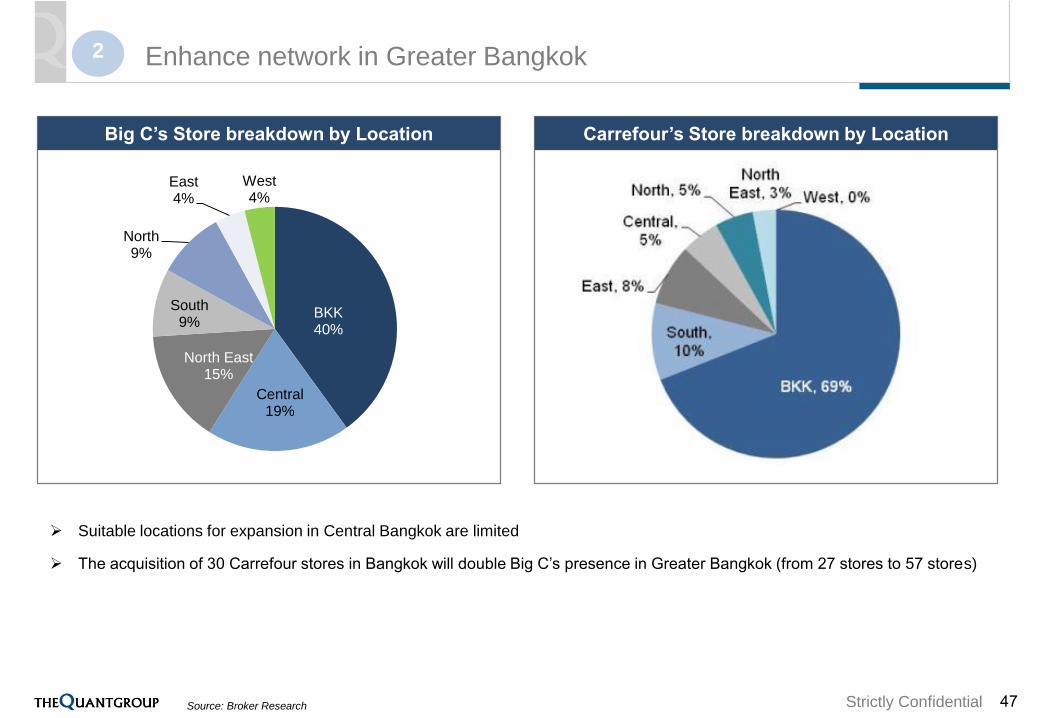

Suitable locations for expansion in Central Bangkok are limited

The acquisition of 30 Carrefour stores in Bangkok will double Big C’s presence in Greater Bangkok (from 27 stores to 57 stores)

Source: Broker Research

Big C’s Store breakdown by Location Carrefour’s Store breakdown by Location

BKK40%

Central19%

North East15%

South9%

North9%

East4%

West4%

47

Enhance network in Greater Bangkok2

Strictly Confidential

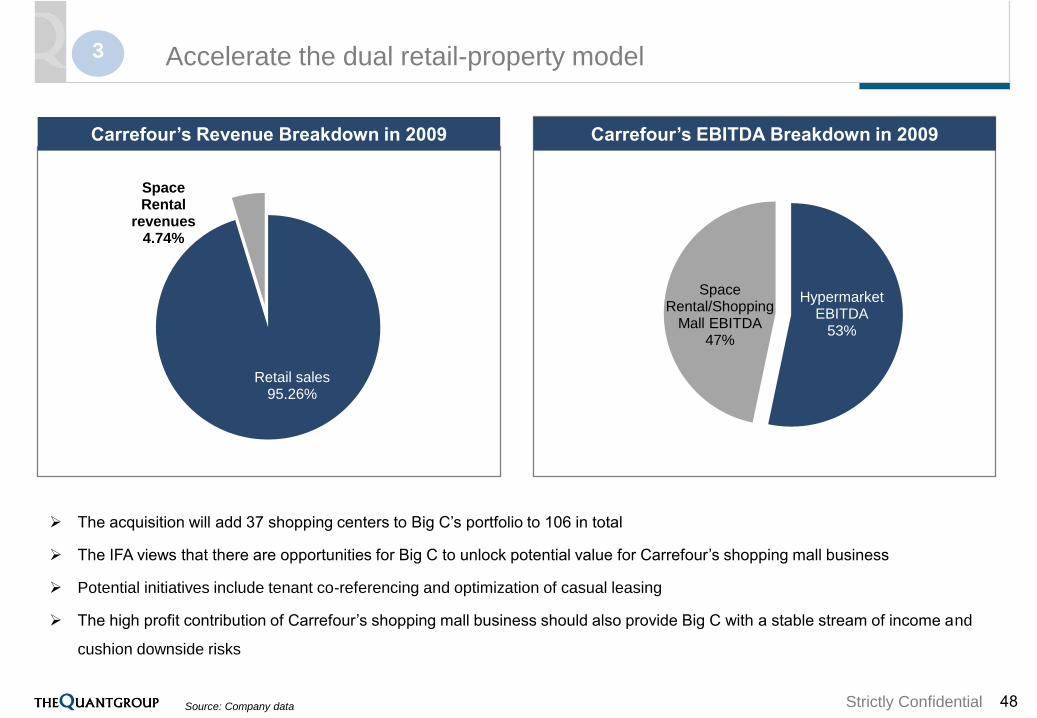

The acquisition will add 37 shopping centers to Big C’s portfolio to 106 in total

The IFA views that there are opportunities for Big C to unlock potential value for Carrefour’s shopping mall business

Potential initiatives include tenant co-referencing and optimization of casual leasing

The high profit contribution of Carrefour’s shopping mall business should also provide Big C with a stable stream of income and

cushion downside risks

Source: Company data

Retail sales95.26%

Space Rental

revenues4.74%

Hypermarket EBITDA

53%

Space Rental/Shopping

Mall EBITDA47%

Carrefour’s EBITDA Breakdown in 2009Carrefour’s Revenue Breakdown in 2009

48

Accelerate the dual retail-property model3

Strictly Confidential

Store conversion from Carrefour to Big C is expected to increase sales density to be in line with higher

Carrefour’s sales following store optimization program

Centralized planning opportunities to generate income from tenant co-referencing, product promotions

and new product launches

Commercial

synergy

Opportunities to implement cost optimization programs including logistics and administrative expenses:

Shared distribution centers and supporting infrastructure

Consolidate headcounts at head office

Pooling of advertising

The IFA is of the view that Carrefour’s SG&A (distribution) costs as % of sales will decline by additional

0.5% each year during 2011-2012

Cost synergy

The pooling of purchases will provide benefits in terms of stronger bargaining power and better

purchasing terms with suppliers

The IFA forecasts that the combined purchasing volume of Big C and Carrefour will increase Carrefour’s

commercial margin by 1.0% during 2011-2012

Purchasing

synergy

These synergies do not include additional synergies of THB 4,600 million on Big C’s side

49

Implement significant synergies4

Strictly Confidential

Shareholding Structure Pre and Post Transaction

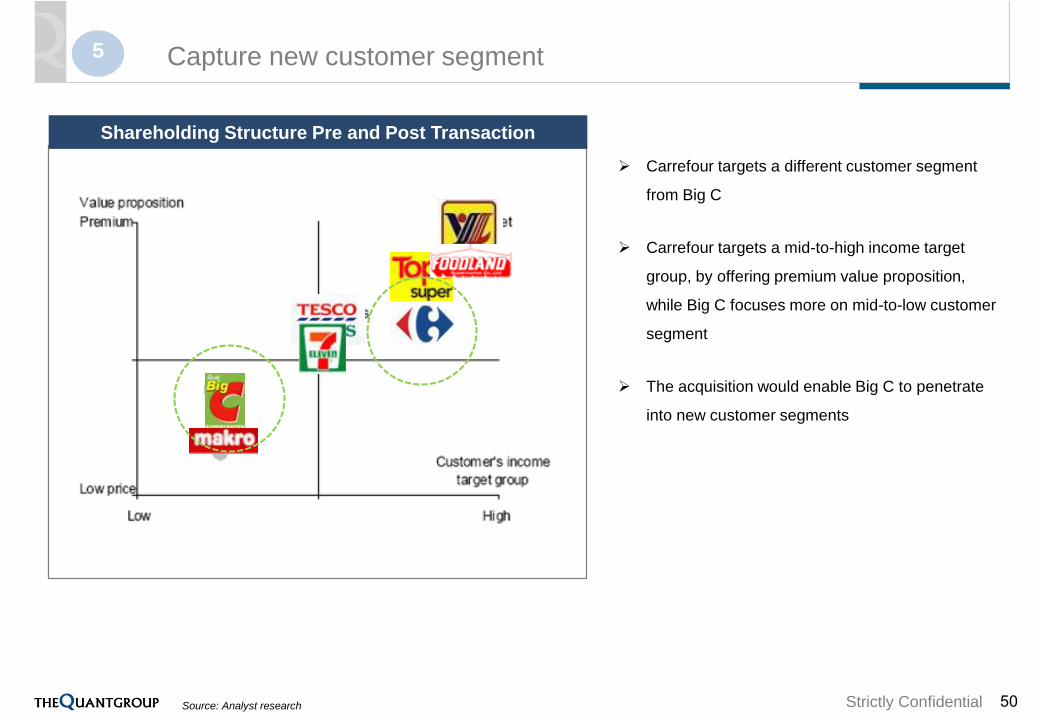

Carrefour targets a different customer segment

from Big C

Carrefour targets a mid-to-high income target

group, by offering premium value proposition,

while Big C focuses more on mid-to-low customer

segment

The acquisition would enable Big C to penetrate

into new customer segments

Source: Analyst research 50

Capture new customer segment5

Strictly Confidential

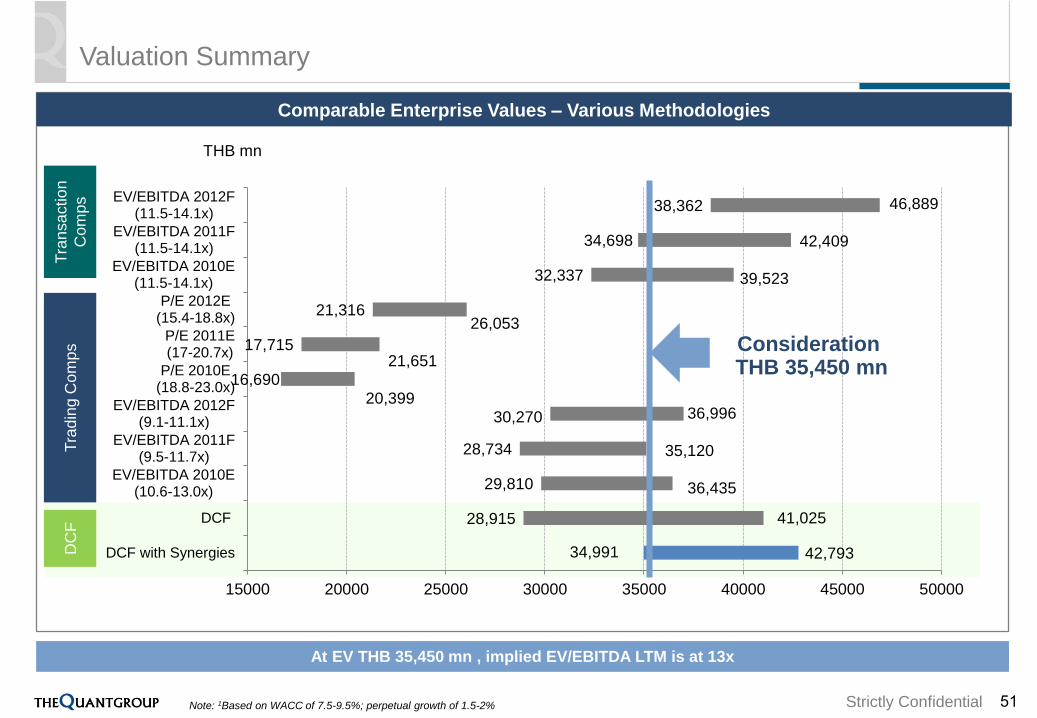

34,991

28,915

29,810

28,734

30,270

16,690

17,715

21,316

32,337

34,698

38,362

15000 20000 25000 30000 35000 40000 45000 50000

DCF with Synergies

DCF

EV/EBITDA 2010E(10.6-13.0x)

EV/EBITDA 2011F(9.5-11.7x)

EV/EBITDA 2012F(9.1-11.1x)

P/E 2010E(18.8-23.0x)

P/E 2011E(17-20.7x)

P/E 2012E(15.4-18.8x)

EV/EBITDA 2010E(11.5-14.1x)

EV/EBITDA 2011F(11.5-14.1x)

EV/EBITDA 2012F(11.5-14.1x)

Valuation Summary

THB mn

Note: 1Based on WACC of 7.5-9.5%; perpetual growth of 1.5-2%

Tra

nsa

ctio

n

Com

ps

Tra

din

g C

om

ps

46,889

42,409

39,523

36,996

35,120

36,435

41,025

20,399

21,651

26,053

At EV THB 35,450 mn , implied EV/EBITDA LTM is at 13x

Consideration THB 35,450 mn

Comparable Enterprise Values – Various Methodologies

42,793DC

F

51

Strictly Confidential

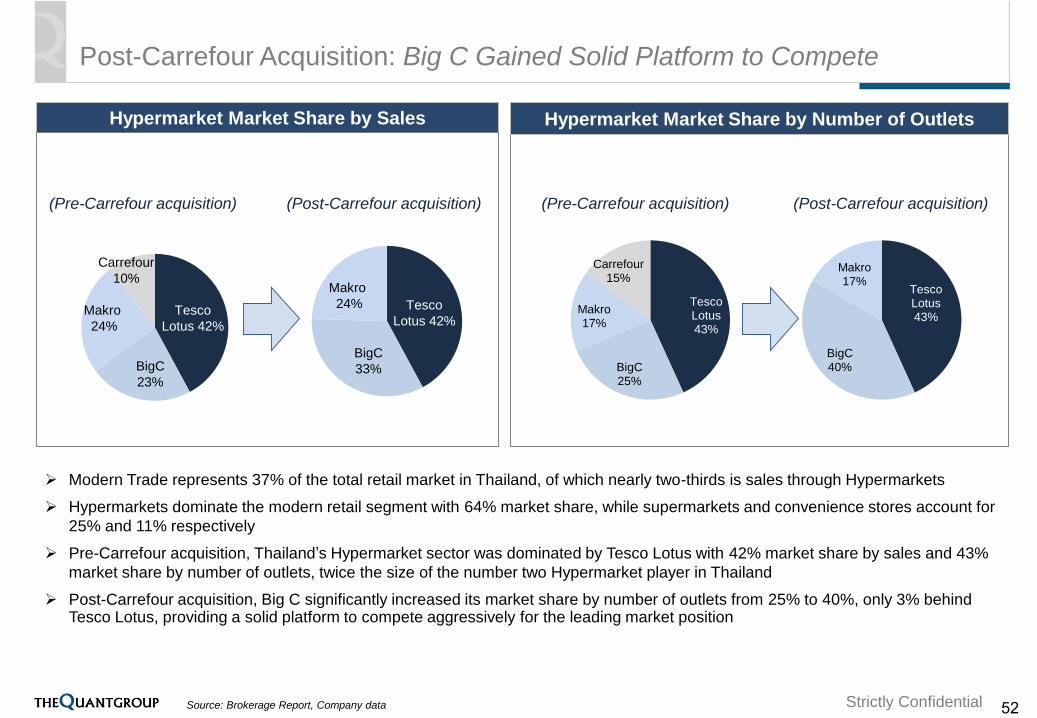

Tesco Lotus43%

BigC40%

Makro17%

Modern Trade represents 37% of the total retail market in Thailand, of which nearly two-thirds is sales through Hypermarkets

Hypermarkets dominate the modern retail segment with 64% market share, while supermarkets and convenience stores account for

25% and 11% respectively

Pre-Carrefour acquisition, Thailand’s Hypermarket sector was dominated by Tesco Lotus with 42% market share by sales and 43%

market share by number of outlets, twice the size of the number two Hypermarket player in Thailand

Post-Carrefour acquisition, Big C significantly increased its market share by number of outlets from 25% to 40%, only 3% behind Tesco Lotus, providing a solid platform to compete aggressively for the leading market position

Tesco

Lotus 42%

BigC

23%

Makro

24%

Source: Brokerage Report, Company data

(Post-Carrefour acquisition)

Carrefour

10%

Tesco

Lotus 42%

BigC

33%

Makro

24%

(Pre-Carrefour acquisition)

Hypermarket Market Share by Sales

Tesco Lotus43%

BigC25%

Makro17%

Carrefour15%

(Post-Carrefour acquisition)(Pre-Carrefour acquisition)

Hypermarket Market Share by Number of Outlets

52

Post-Carrefour Acquisition: Big C Gained Solid Platform to Compete

Strictly Confidential

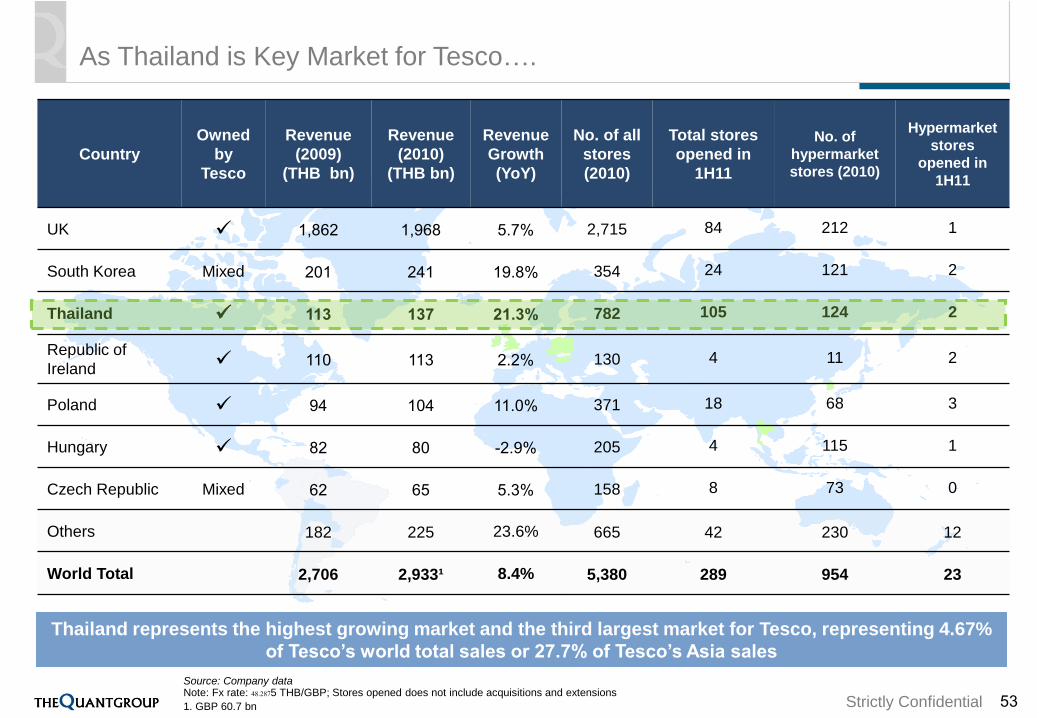

Country

Owned

by

Tesco

Revenue

(2009)

(THB bn)

Revenue

(2010)

(THB bn)

Revenue

Growth

(YoY)

No. of all

stores

(2010)

Total stores

opened in

1H11

No. of

hypermarket

stores (2010)

Hypermarket

stores

opened in

1H11

UK 1,862 1,968 5.7% 2,715 84 212 1

South Korea Mixed 201 241 19.8% 354 24 121 2

Thailand 113 137 21.3% 782 105 124 2

Republic of

Ireland 110 113 2.2% 130 4 11 2

Poland 94 104 11.0% 371 18 68 3

Hungary 82 80 -2.9% 205 4 115 1

Czech Republic Mixed 62 65 5.3% 158 8 73 0

Others 182 225 23.6% 665 42 230 12

World Total 2,706 2,933¹ 8.4% 5,380 289 954 23

As Thailand is Key Market for Tesco….

Thailand represents the highest growing market and the third largest market for Tesco, representing 4.67%

of Tesco’s world total sales or 27.7% of Tesco’s Asia sales

Source: Company dataNote: Fx rate: 48.2875 THB/GBP; Stores opened does not include acquisitions and extensions

1. GBP 60.7 bn 53

Strictly Confidential

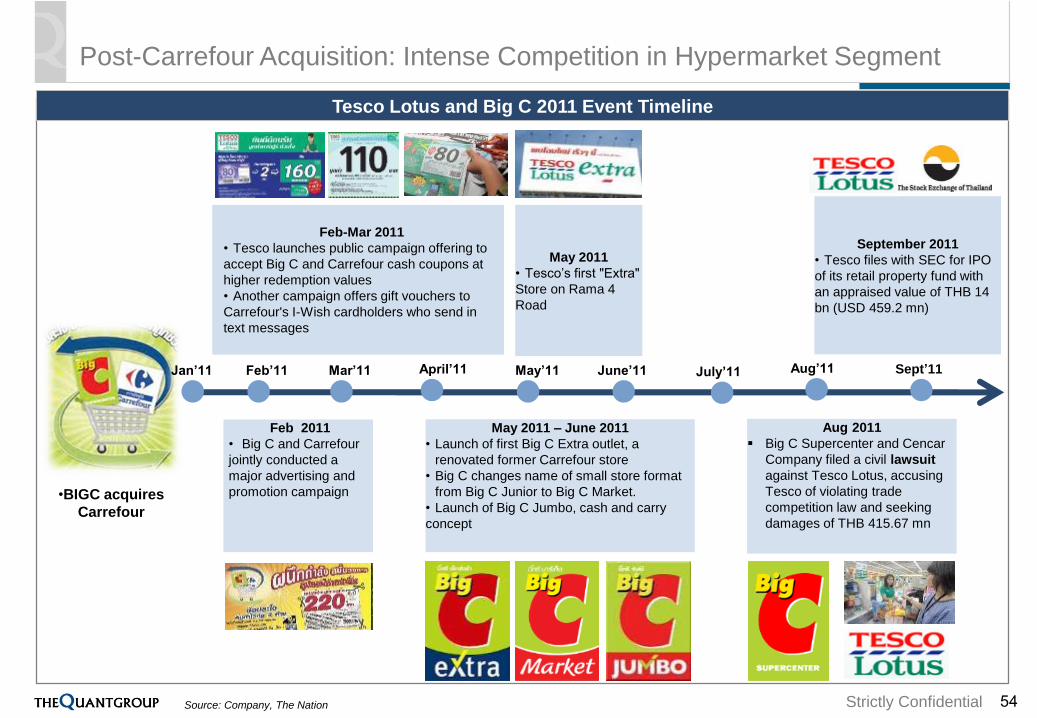

May 2011

• Tesco’s first "Extra"

Store on Rama 4

Road

May 2011 – June 2011

• Launch of first Big C Extra outlet, a

renovated former Carrefour store

• Big C changes name of small store format

from Big C Junior to Big C Market.

• Launch of Big C Jumbo, cash and carry

concept

•BIGC acquires

Carrefour

Aug 2011

Big C Supercenter and Cencar

Company filed a civil lawsuit

against Tesco Lotus, accusing

Tesco of violating trade

competition law and seeking

damages of THB 415.67 mn

September 2011

• Tesco files with SEC for IPO

of its retail property fund with

an appraised value of THB 14

bn (USD 459.2 mn)

Feb 2011

• Big C and Carrefour

jointly conducted a

major advertising and

promotion campaign

Feb-Mar 2011

• Tesco launches public campaign offering to

accept Big C and Carrefour cash coupons at

higher redemption values

• Another campaign offers gift vouchers to

Carrefour's I-Wish cardholders who send in

text messages

Feb’11 Mar’11 April’11 May’11 June’11 July’11 Aug’11 Sept’11Jan’11

Source: Company, The Nation

Tesco Lotus and Big C 2011 Event Timeline

54

Post-Carrefour Acquisition: Intense Competition in Hypermarket Segment

Strictly Confidential

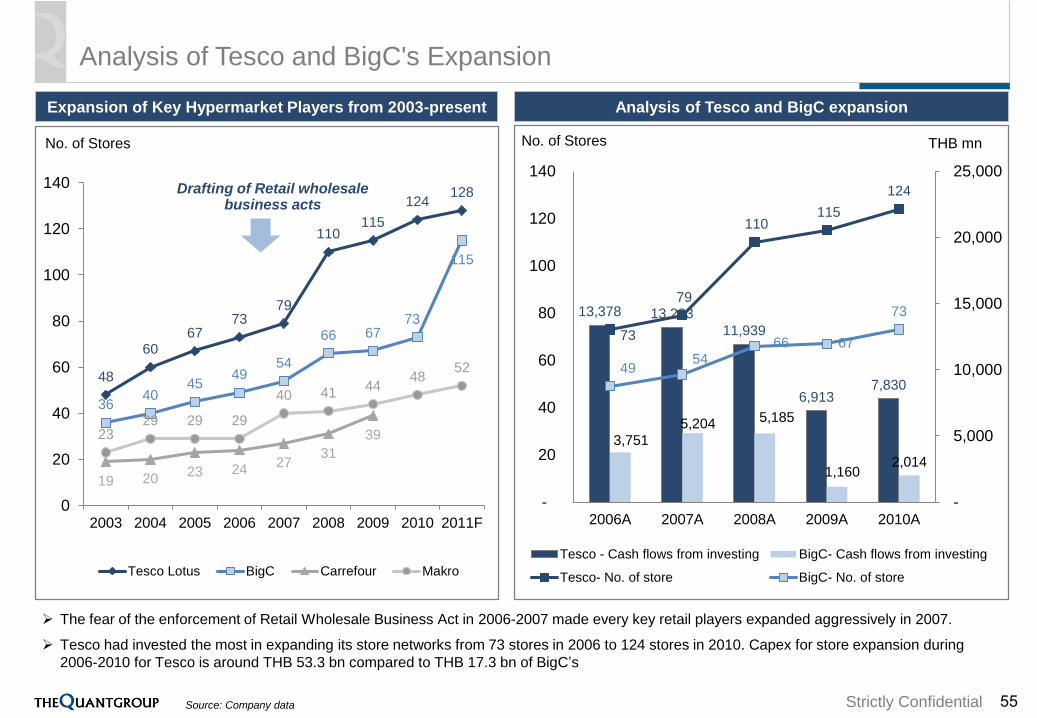

48

6067

7379

110115

124128

3640

4549

54

66 6773

115

19 2023 24

2731

392329 29 29

40 4144

4852

0

20

40

60

80

100

120

140

2003 2004 2005 2006 2007 2008 2009 2010 2011F

Tesco Lotus BigC Carrefour Makro

13,378 13,223

11,939

6,9137,830

3,751

5,204 5,185

1,1602,014

73

79

110 115

124

49 54

66 67

73

-

5,000

10,000

15,000

20,000

25,000

-

20

40

60

80

100

120

140

2006A 2007A 2008A 2009A 2010A

Tesco - Cash flows from investing BigC- Cash flows from investing

Tesco- No. of store BigC- No. of store

Analysis of Tesco and BigC's Expansion

No. of Stores

The fear of the enforcement of Retail Wholesale Business Act in 2006-2007 made every key retail players expanded aggressively in 2007.

Tesco had invested the most in expanding its store networks from 73 stores in 2006 to 124 stores in 2010. Capex for store expansion during

2006-2010 for Tesco is around THB 53.3 bn compared to THB 17.3 bn of BigC’s

Analysis of Tesco and BigC expansion

Source: Company data

THB mn

Drafting of Retail wholesalebusiness acts

Expansion of Key Hypermarket Players from 2003-present

No. of Stores

55

Strictly Confidential

Case Study: F&N

Strictly Confidential

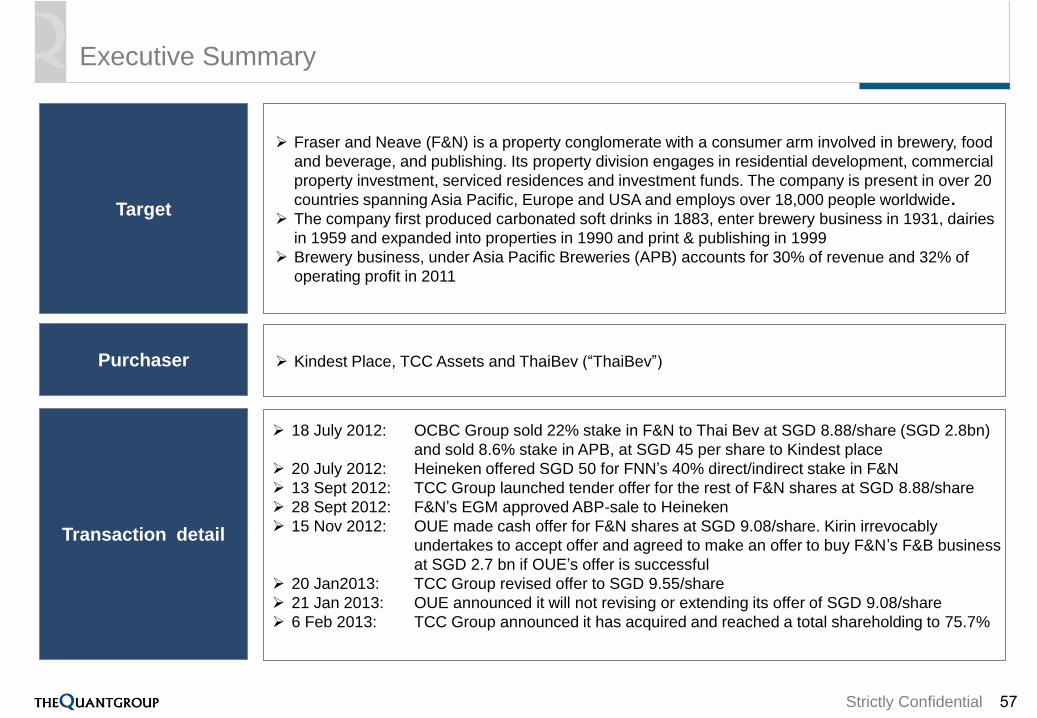

Executive Summary

57

Target

Purchaser

Transaction detail

Fraser and Neave (F&N) is a property conglomerate with a consumer arm involved in brewery, food

and beverage, and publishing. Its property division engages in residential development, commercial

property investment, serviced residences and investment funds. The company is present in over 20

countries spanning Asia Pacific, Europe and USA and employs over 18,000 people worldwide.

The company first produced carbonated soft drinks in 1883, enter brewery business in 1931, dairies

in 1959 and expanded into properties in 1990 and print & publishing in 1999

Brewery business, under Asia Pacific Breweries (APB) accounts for 30% of revenue and 32% of

operating profit in 2011

Kindest Place, TCC Assets and ThaiBev (“ThaiBev”)

18 July 2012: OCBC Group sold 22% stake in F&N to Thai Bev at SGD 8.88/share (SGD 2.8bn)

and sold 8.6% stake in APB, at SGD 45 per share to Kindest place

20 July 2012: Heineken offered SGD 50 for FNN’s 40% direct/indirect stake in F&N

13 Sept 2012: TCC Group launched tender offer for the rest of F&N shares at SGD 8.88/share

28 Sept 2012: F&N’s EGM approved ABP-sale to Heineken

15 Nov 2012: OUE made cash offer for F&N shares at SGD 9.08/share. Kirin irrevocably

undertakes to accept offer and agreed to make an offer to buy F&N’s F&B business

at SGD 2.7 bn if OUE’s offer is successful

20 Jan2013: TCC Group revised offer to SGD 9.55/share

21 Jan 2013: OUE announced it will not revising or extending its offer of SGD 9.08/share

6 Feb 2013: TCC Group announced it has acquired and reached a total shareholding to 75.7%

Strictly Confidential

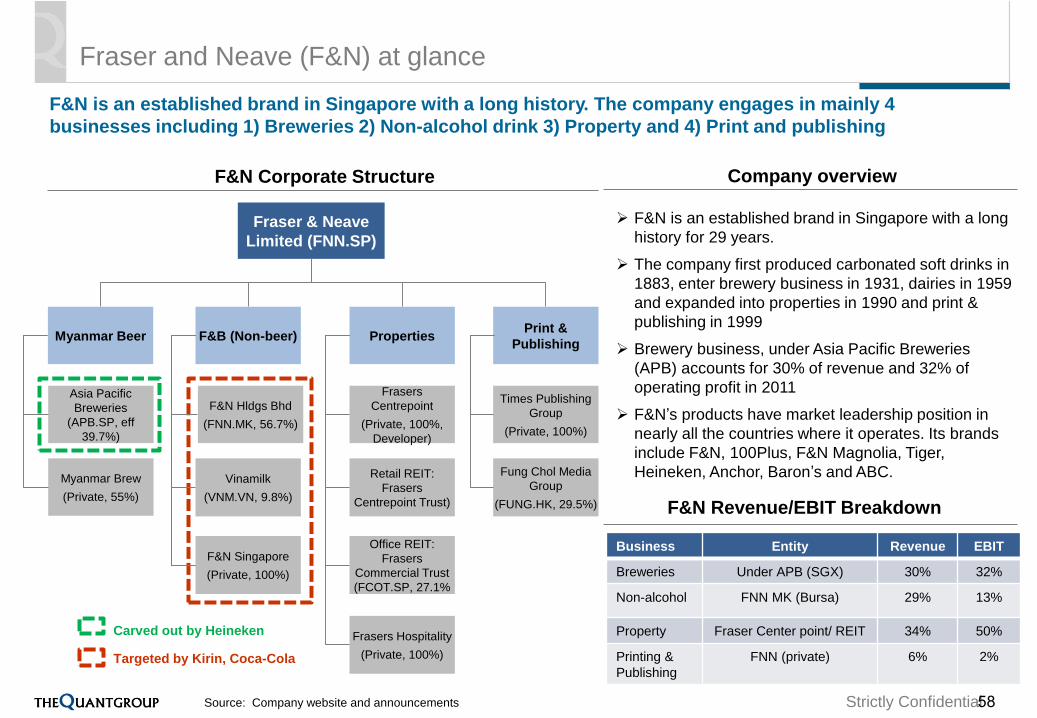

Fraser and Neave (F&N) at glance

F&N is an established brand in Singapore with a long history. The company engages in mainly 4

businesses including 1) Breweries 2) Non-alcohol drink 3) Property and 4) Print and publishing

58

F&N Corporate Structure

Carved out by Heineken

Targeted by Kirin, Coca-Cola

F&N is an established brand in Singapore with a long

history for 29 years.

The company first produced carbonated soft drinks in

1883, enter brewery business in 1931, dairies in 1959

and expanded into properties in 1990 and print &

publishing in 1999

Brewery business, under Asia Pacific Breweries

(APB) accounts for 30% of revenue and 32% of

operating profit in 2011

F&N’s products have market leadership position in

nearly all the countries where it operates. Its brands

include F&N, 100Plus, F&N Magnolia, Tiger,

Heineken, Anchor, Baron’s and ABC.

Business Entity Revenue EBIT

Breweries Under APB (SGX) 30% 32%

Non-alcohol FNN MK (Bursa) 29% 13%

Property Fraser Center point/ REIT 34% 50%

Printing &

Publishing

FNN (private) 6% 2%

F&N Revenue/EBIT Breakdown

Fraser & Neave

Limited (FNN.SP)

Myanmar Beer F&B (Non-beer) PropertiesPrint &

Publishing

Asia Pacific

Breweries

(APB.SP, eff

39.7%)

Myanmar Brew

(Private, 55%)

F&N Hldgs Bhd

(FNN.MK, 56.7%)

Vinamilk

(VNM.VN, 9.8%)

F&N Singapore

(Private, 100%)

Frasers

Centrepoint

(Private, 100%,

Developer)

Retail REIT:

Frasers

Centrepoint Trust)

Office REIT:

Frasers

Commercial Trust

(FCOT.SP, 27.1%

Frasers Hospitality

(Private, 100%)

Times Publishing

Group

(Private, 100%)

Fung Chol Media

Group

(FUNG.HK, 29.5%)

Source: Company website and announcements

Company overview

Strictly Confidential

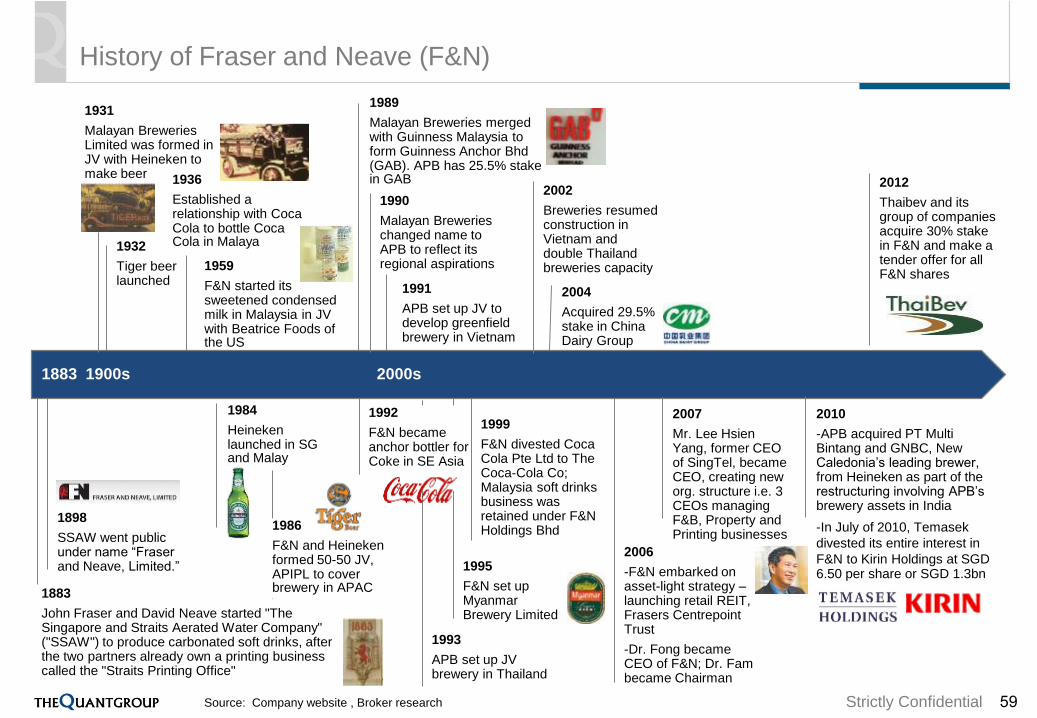

History of Fraser and Neave (F&N)

59

1883 1900s 2000s

1883

John Fraser and David Neave started "The Singapore and Straits Aerated Water Company" ("SSAW") to produce carbonated soft drinks, after the two partners already own a printing business called the "Straits Printing Office"

1898

SSAW went public under name “Fraser and Neave, Limited.”

1931

Malayan Breweries Limited was formed in JV with Heineken to make beer

1932

Tiger beer launched

1936

Established a relationship with Coca Cola to bottle Coca Cola in Malaya

1959

F&N started its sweetened condensed milk in Malaysia in JV with Beatrice Foods of the US

1984

Heineken launched in SG and Malay

1986

F&N and Heineken formed 50-50 JV, APIPL to cover brewery in APAC

1989

Malayan Breweries merged with Guinness Malaysia to form Guinness Anchor Bhd(GAB). APB has 25.5% stake in GAB

1990

Malayan Breweries changed name to APB to reflect its regional aspirations

1991

APB set up JV to develop greenfield brewery in Vietnam

1992

F&N became anchor bottler for Coke in SE Asia

1993

APB set up JV brewery in Thailand

1995

F&N set up Myanmar Brewery Limited

1999

F&N divested Coca Cola Pte Ltd to The Coca-Cola Co; Malaysia soft drinks business was retained under F&N Holdings Bhd

2002

Breweries resumed construction in Vietnam and double Thailand breweries capacity

2004

Acquired 29.5% stake in China Dairy Group

2006

-F&N embarked on asset-light strategy –launching retail REIT, Frasers CentrepointTrust

-Dr. Fong became CEO of F&N; Dr. Fambecame Chairman

2007

Mr. Lee HsienYang, former CEO of SingTel, became CEO, creating new org. structure i.e. 3 CEOs managing F&B, Property and Printing businesses

2010

-APB acquired PT Multi Bintang and GNBC, New Caledonia’s leading brewer, from Heineken as part of the restructuring involving APB’s brewery assets in India

-In July of 2010, Temasek

divested its entire interest in

F&N to Kirin Holdings at SGD 6.50 per share or SGD 1.3bn

Source: Company website , Broker research

2012

Thaibev and its group of companies acquire 30% stake in F&N and make a tender offer for all F&N shares

Strictly Confidential

Carlsberg31%

Tiger35%

Heineken8%

Others26%

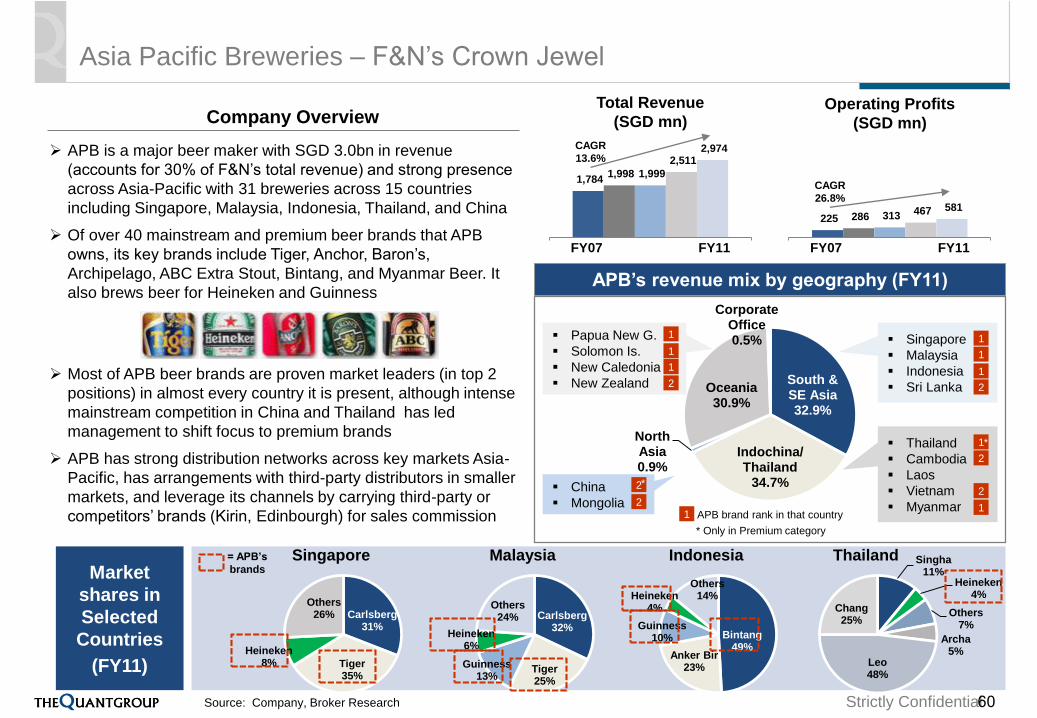

Asia Pacific Breweries – F&N’s Crown Jewel

Company Overview

APB is a major beer maker with SGD 3.0bn in revenue

(accounts for 30% of F&N’s total revenue) and strong presence

across Asia-Pacific with 31 breweries across 15 countries

including Singapore, Malaysia, Indonesia, Thailand, and China

Of over 40 mainstream and premium beer brands that APB

owns, its key brands include Tiger, Anchor, Baron’s,

Archipelago, ABC Extra Stout, Bintang, and Myanmar Beer. It

also brews beer for Heineken and Guinness

Most of APB beer brands are proven market leaders (in top 2

positions) in almost every country it is present, although intense

mainstream competition in China and Thailand has led

management to shift focus to premium brands

APB has strong distribution networks across key markets Asia-

Pacific, has arrangements with third-party distributors in smaller

markets, and leverage its channels by carrying third-party or

competitors’ brands (Kirin, Edinbourgh) for sales commission

South & SE Asia32.9%

Indochina/Thailand

34.7%

North Asia0.9%

Oceania30.9%

Corporate Office0.5%

APB’s revenue mix by geography (FY11)

Singapore

Malaysia

Indonesia

Sri Lanka

Thailand

Cambodia

Laos

Vietnam

Myanmar

Papua New G.

Solomon Is.

New Caledonia

New Zealand

China

Mongolia1 APB brand rank in that country

1

1

1

2

1*

* Only in Premium category

2

2

1

2

2

*

1

1

2

1

Market

shares in

Selected

Countries

(FY11)

Singapore

Carlsberg32%

Tiger25%

Guinness13%

Heineken6%

Others24%

Malaysia

Bintang49%

Anker Bir23%

Guinness10%

Heineken4%

Others14%

Indonesia Singha11%

Heineken4%

Others7%

Archa5%

Leo48%

Chang25%

Thailand

60

1,784 1,998 1,999

2,511 2,974

Total Revenue

(SGD mn)

FY07 FY11

Operating Profits

(SGD mn)

225 286 313 467 581

FY07 FY11

Source: Company, Broker Research

CAGR

13.6%

CAGR

26.8%

= APB’s

brands